Embed Size (px)

Citation preview

Slide Title

(2nd Line)

TRIYARDS HOLDINGS LIMITED

Investor Presentation

15 January 2014

Slide Title

(2nd Line)

DISCLAIMER

This presentation contains forward-looking statements concerning the financial condition, results of operations and businesses of Triyards Holdings Limited (“Triyards” or the “Company”). All statements other than statements of historical fact are, or may be deemed to be, forward-looking statements. Forward-looking statements are statements of future expectations that are based on management’s current expectations and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in these statements. Forward-looking statements include, among other things, statements concerning the potential exposure of Triyards to market risks and statements expressing management’s expectations, beliefs, estimates, forecasts, projections and assumptions. Although the Company believes that the expectations reflected in such forward-looking statements are reasonable, it can give no assurance that such expectations will prove to have been correct. All forward looking-statements contained in this presentation are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. Readers should not place undue reliance on forward-looking statements. Each forward looking statement speaks only as of the date of this presentation. Neither the Company nor any of its subsidiaries and associates undertake any obligation to publicly update or revise any forward-looking statement as a result of new information, future events or other information. In light of these risks, results could differ materially from those stated, implied or inferred from the forward-looking statements contained in this presentation.

Slide Title

(2nd Line) Introducing TRIYARDS

1 • On Vision and Mission

2 • Our Yards

3 • Scope of Services

4 • Our Competitive Strengths

5 • Our Track Record

6 • Strategies for Growth

7 • Outlook and Prospects

8 • Financial Highlights

Slide Title

(2nd Line) Our Vision and Mission

Our VISION is to be the preferred engineering, ship construction and fabrication solutions provider to the offshore oil and gas, and marine industries globally.

Our MISSION is to consistently create value for our clients by providing quality, cost-effective products on time and on budget.

Slide Title

(2nd Line)

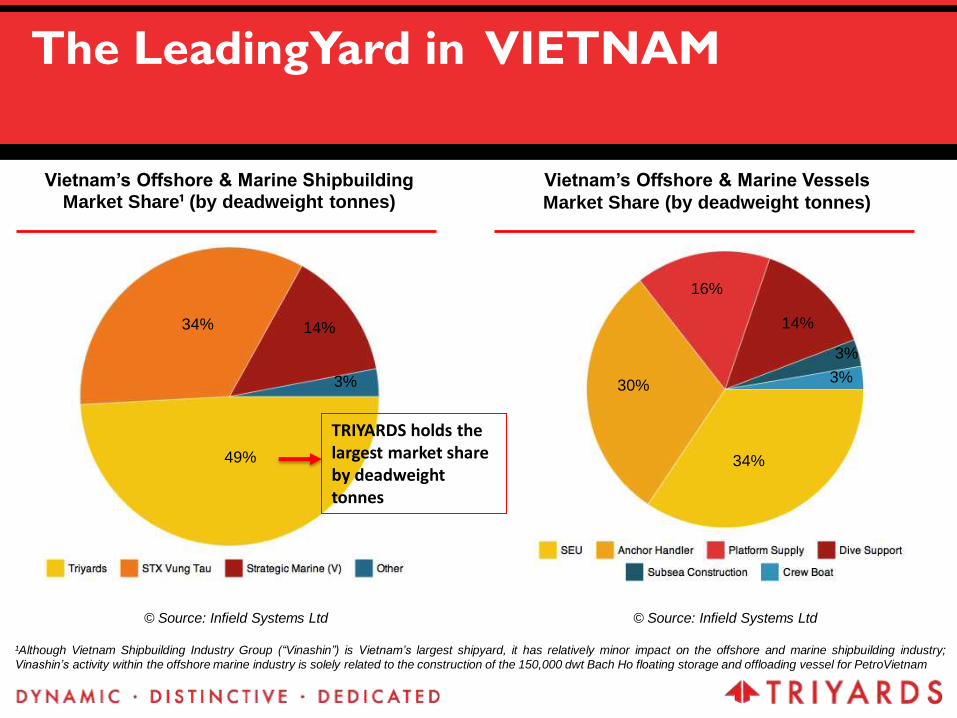

The LeadingYard in VIETNAM

Vietnam’s Offshore & Marine Shipbuilding Market Share¹ (by deadweight tonnes)

Vietnam’s Offshore & Marine Vessels

Market Share (by deadweight tonnes)

© Source: Infield Systems Ltd © Source: Infield Systems Ltd

¹Although Vietnam Shipbuilding Industry Group (“Vinashin”) is Vietnam’s largest shipyard, it has relatively minor impact on the offshore and marine shipbuilding industry;

Vinashin’s activity within the offshore marine industry is solely related to the construction of the 150,000 dwt Bach Ho floating storage and offloading vessel for PetroVietnam

14% 34%

49%

3%

TRIYARDS holds the largest market share by deadweight tonnes

3%

30%

34%

3%

16%

14%

Slide Title

(2nd Line)

OUR YARDS

TRIYARDS SSY (Ho Chi Minh, Vietnam)

• Size of facility: 100,000sqm

• Water Frontage: 340m

• Undercover workshop: 50,000sqm

- Includes block shops, erection shops,

outfitting shops, piping shops, machine

shop, electrical shop, blasting & painting

shops

• Industrial activities yard: 80,000sqm

- with 100T hydraulic transporter, 10 – 50T

gantry cranes & 250T crawler cranes, etc.

• Launching way: 61m x 141m

• Marine outfitting quay: max 10m draft

Slide Title

(2nd Line) OUR YARDS

TRIYARDS SOFEL (Vung Tau, Vietnam)

• Size of facility: 134,000sqm

• Water Frontage: 347m

• Undercover workshop: 20,858sqm

- Includes block shops, outfitting shops, piping

shops, machine shop, electrical shop, blasting &

painting shops

• Industrial activities yard: 96,000sqm

- with 100T hydraulic transporter, 120T A crane &

250T crawler crane

• Skid-way: 26m x 130m

• Launching way: 52m x 175m

• Marine outfitting quay: Max 10m draft

Slide Title

(2nd Line)

• Size of facility: More than 650,000 square feet of

fabrication facilities, including two steel burning machines,

fabrication area with overhead cranes, machine shop, and

hydraulics bay

• Undercover workshop: Fabrication facility exceeding

200,000 square feet

• Industrial activities Yard: Cranes, winches, A-frames

and other hydraulic and electric marine deck handling

equipment

OUR YARDS

TRIYARDS Houston

Slide Title

(2nd Line)

Our Scope of Products and Services

Offshore fabrication (FPSO Turret, CALM Buoy)

Offshore Heavy Lift Equipment (Knuckle Boom Crane, Leg Encircling Crane)

Ship repair & conversion

Industrial Fabrication (Diverters for refineries and power plants)

Offshore Support &

Construction Vessels

Offshore Service

Platform (SEU) &

Drilling Rig (TDU)

We perform work for turn-key projects

Slide Title

(2nd Line)

Slide Title

(2nd Line)

Our Competitive Strengths

Leading market position in

South East Asia for SEUs

Strong track record capability

for sophisticated vessels

Experienced

management team and

integrated project

management capability

Strategic locations in

Vietnam

Competitive position

Design and fabrication for

offshore equipment

Slide Title

(2nd Line)

Underpenetrated SEU market in Asia

Region No. of SEUs No. of platforms Ratio of platforms per SEUs

North America 240 3,257 14

Southeast Asia, Middle East and West Africa

54 3,266 60

Source: Macquarie Research, July 2013

Only 1 SEU per 60 platforms in Southeast Asia, Middle East and West Africa, as compared to 1

SEU per 14 platforms in North America

No. of SEUs

Slide Title

(2nd Line)

Why SEU? (replacing the tender barge)

Operationally superior to tender barge: Self-propelled, facilitating intra-field movement without AHTS Significant reduction in downtime, due to harsh weather condition Offer safer operating condition Competitive day-rate\

Slide Title

(2nd Line)

Value Proposition of SEUs

SEUs

Mobility Safety Cost-Efficiency Accommodation

• Self-propelled

• eliminates

need for third

party tugs

• adjustable

height provides

stable platform

• safer than a

barge

• reduce downtime of

production wells and

reliance on barges

• can accommodate as

many as 150-200

personnel on board

Source: Macquarie Research, July 2013

• Self-propelled, self elevating offshore working platforms, with large open deck space

• Performs range of services – repair & maintenance of platforms, well servicing, accommodation

• Ability to reposition at offshore site or move to new location without assistance

Slide Title

(2nd Line) End Users of SEUs – Global outreach

Brunei Offshore

Bintulu Offshore

Indonesia Nigeria

Slide Title

(2nd Line)

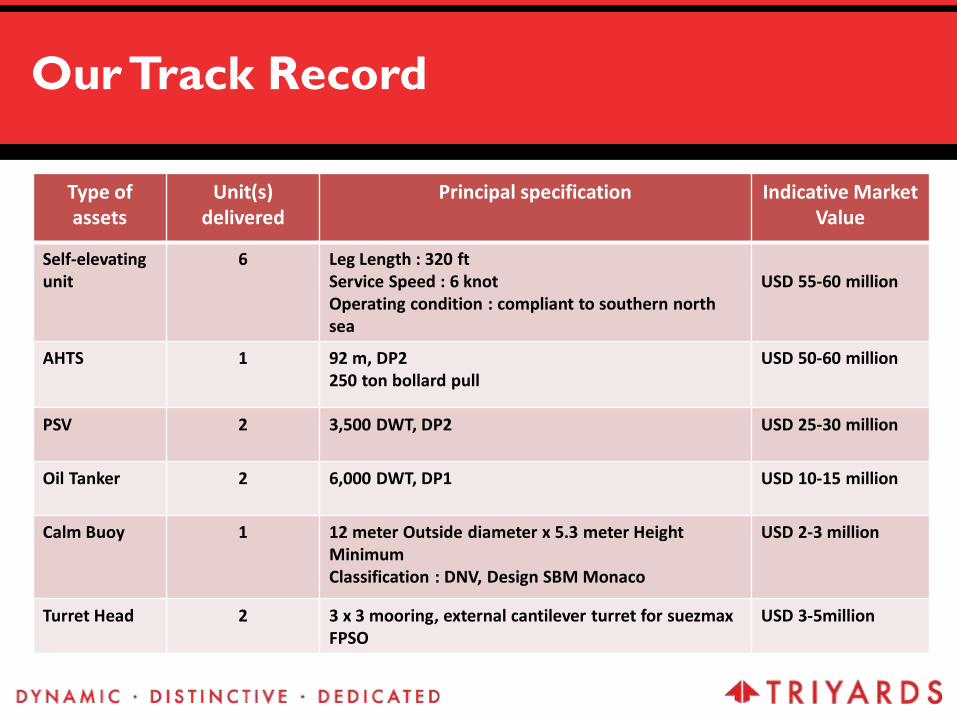

Type of assets

Unit(s) delivered

Principal specification Indicative Market Value

Self-elevating unit

6 Leg Length : 320 ft Service Speed : 6 knot Operating condition : compliant to southern north sea

USD 55-60 million

AHTS 1 92 m, DP2 250 ton bollard pull

USD 50-60 million

PSV 2 3,500 DWT, DP2 USD 25-30 million

Oil Tanker 2 6,000 DWT, DP1 USD 10-15 million

Calm Buoy 1 12 meter Outside diameter x 5.3 meter Height Minimum Classification : DNV, Design SBM Monaco

USD 2-3 million

Turret Head 2 3 x 3 mooring, external cantilever turret for suezmax FPSO

USD 3-5million

Our Track Record

Slide Title

(2nd Line) Our Track Record- other oil & gas

applications

TURRET HEAD

FPSO PERISAI KAMELIA CALM BUOY – SBM MONACO

Slide Title

(2nd Line) Constellation Facts

8.5 million man hours with zero fatal incident

Hull and structural outfitting - 26,900T of steel, from

grade A to EH69. - Capability of handling

exotic materials Electrical - 860km of cables

(from fiber optic to 6.6kV cables)

Piping - 180km of piping (PVC-GRE-SS-C/S-Copper)

Slide Title

(2nd Line) Integrated Capabilities

• Reels & Cradles fabricated by SOFEL

• 80 Ton Crane fabricated by Houston

Slide Title

(2nd Line) Our Strategies for Growth

Slide Title

(2nd Line)

PROGRESSION

OF PRODUCTS

2007: 1st Generation SEU

Leg Length: 320 feet

Water Depth: 70m

Accommodation: 160 personnel

2012: 2nd Generation SEU

Leg Length: 450 feet

Water Depth: 80m

Accommodation: 300 personnel

2013: 3rd Generation SEU

Leg Length: 530 Feet

Water Depth: 121m

Accommodation: 220 personnel

Premium Class, HPHT.

Slide Title

(2nd Line)

Introducing TDU-400

Lighter in overall weight, compared to other rigs of its

own class

Increased deck strength; enhancing storage for today’s

most advanced drilling tools

Exceed Class rules for 100 knots wind and wave criteria

Global operation in 400ft of working water depth

32,500ft drilling depth

1,500,000 hook load

80 ft cantilever reach

Maximize fluid volumes, dry bulk storage capacity

Innovative modular electrical outfitting approach to

maximize construction efficiency and minimize

commissioning time

Slide Title

(2nd Line)

Capabilities Comparisons of

TDU-400 Drilling Rig

Designer

Britain Singapore USA Europe

Triyards

(TDU 400)

Working Water Depth (ft)

400 400 400 350 400

Wave Criteria @ 100 kt wind (ft)

60 (info not available)

(info not available)

60 54

Wind Speed (kt)

100 (info not available)

(info not available)

100 100

Cantilever reach to well enter (ft)

75 70 80 70 80

Max hook load @ max Cantilever

reach (kips)

2000 1500 2000 1485 1500

Accommodations

140 150 150 120 220

Drill Depth (ft)

35000 30000 35000 30000 35000

Slide Title

(2nd Line)

We remain focused on our strategies

Focused on the design and construction of SEUs and sophisticated OSVs

Develop own offshore equipment product line and branding for offshore equipment (i.e. cranes, A-frames, winches)

Expand ship repair business

Expand into new product categories such as fabrication of aluminium-based vessels

Establish presence in new markets (i.e. Brazil, Australia)

Slide Title

(2nd Line) Milestones

Mainboard Listing:

Debut on SGX-ST

Contract Win: US$90m

contract for BH 450 SEU

Proprietary SEU Design:

Launched TDU-400

(400ft drilling jack-up)

15 Nov 2012

28 Oct 2013

01 Jul 2013

07 May 2013

17 Aug 2013

18 Oct 2012

New Revenue Stream:

Commissioned 10,000 tonne

floating dock and secured 1st third

party ship repair deal

Contract Win: US$60m

for BH 335 SEU

9 Jan 2013 Strong Financial Support:

Established US$250m

Multicurrency Debt

Issuance Programme

Contract Win: US$59m

contract for BH 335 SEU

and turret construction

Slide Title

(2nd Line) Outlook and Prospects

Slide Title

(2nd Line)

Outlook and Prospects

0

2,000

4,000

6,000

8,000

10,000

12,000

2007 2008 2009 2010 2011 2012 2013e 2014e 2015e 2016e

Africa Asia Australasia Europe Latin America Middle East North America

Capex for offshore oilfield infrastructure expected to grow from US$341 billion during 2007/2011

to more than US$589 billion during 2012/16. Largest share of this growth in capex is in shallow

waters in South East Asia and Middle East

Asia in growing trend of Offshore CAPEX

Source: Infield Systems Ltd

Slide Title

(2nd Line) Financial Highlights

Slide Title

(2nd Line)

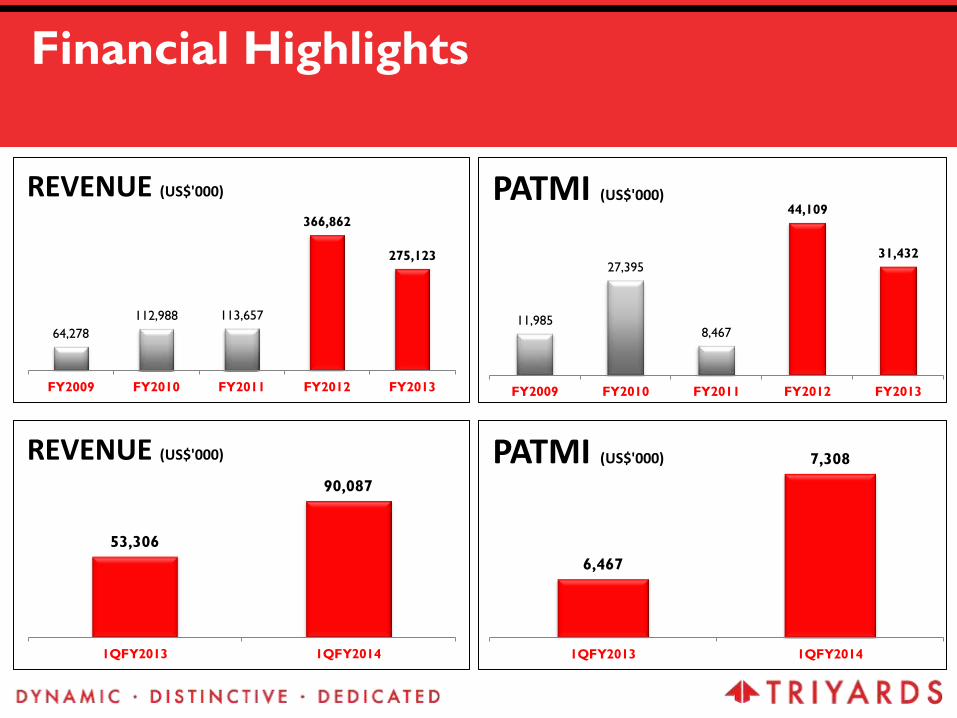

Financial Highlights

64,278

112,988 113,657

366,862

275,123

FY2009 FY2010 FY2011 FY2012 FY2013

REVENUE (US$'000)

11,985

27,395

8,467

44,109

31,432

FY2009 FY2010 FY2011 FY2012 FY2013

PATMI (US$'000)

53,306

90,087

1QFY2013 1QFY2014

REVENUE (US$'000)

6,467

7,308

1QFY2013 1QFY2014

PATMI (US$'000)

Slide Title

(2nd Line)

Financial Highlights

Generated a positive operating cashflow of US$15.8 million for FY13 compared to operating net outflow of

US$11.1 million in the previous corresponding year.

Largely boosted by the positive results as well as diligent working capital management.

FY2009 FY2010 FY2011 FY2012 FY2013

Operating 23,109 37,347 (16,881) (11,087) 15,752

Investing (33,249) (12,162) (30,188) (14,650) (33,019)

Financing 4,237 9,916 13,583 28,187 25,267

-40000

-30000

-20000

-10000

0

10000

20000

30000

40000

50000

FY09 FY10 FY11 FY12 FY13

US$ 000

Operating Cashflow Investing Cashflow Financing Cashflow

Slide Title

(2nd Line)

Financial Highlights

Development of SSY

Development of SOFEL Acquisition of Houston yard

Floating Dock TDU 400 Design

NTA increased mainly derived from increase in retained earning

25,026

52,541 60,889

104,998

147,210 154,518

FY2009 FY2010 FY2011 FY2012 FY2013 1QFY14

SHAREHOLDERS’ FUND(US$'000)

45,661

54,211

79,906

89,181

102,189 101,676

FY2009 FY2010 FY2011 FY2012 FY2013 1QFY14

FIXED ASSETS (US$'000)

Slide Title

(2nd Line)

Financial Highlights

US$’000 As at 31

Aug 2013

As at 30

Nov 2013

Current assets 210,091 242,461

Non-current assets 109,831 109,343

Current liabilities 172,645 197,219

Non-current

liabilities 67 67

Total Equity 147,210 154,518

Interest cover

(times) (2) 16.90 11.91

Current ratio 1.22 1.23

Return on equity 21% -

(*) Net cash position

(1) – Net Debt / Equity (2) - EBITDA/Interest Expense

0.44

0.55 0.56

0.52 0.54

0.25

0.36

0.19

0.09 0.09

FY2009 FY2010* FY2011 FY2012 FY2013 1QFY14

GEARING RATIO (1)

Overall CAPEX

Slide Title

(2nd Line) ORDERBOOK

Current Orderbook as at 31 August 2013

Net contract value amount to approximately US$217m

Vessel Type Specifications Type of

Customer

Year of

Contract

Year of

Expected

Delivery

Self-elevating unit 425 ft leg length Sale to third party 2012 2014

Self-elevating unit 425 ft leg length Sale to third party 2012 2014

Self-elevating unit 335 ft leg length Sale to third party 2013 2014

SCV (Lewek

Constellation)

DP3, 3,000 MT crane,

deepwater multi-lay

pipelay vessel

Sale to Ezra Group 2011 2014

US$59m contract wins announced in October 2013 comprising 10th SEU and

turret for an FSO unit

Slide Title

(2nd Line)

Q&A