Embed Size (px)

Citation preview

Service Tax & Service Tax & CENVAT Credit CENVAT Credit

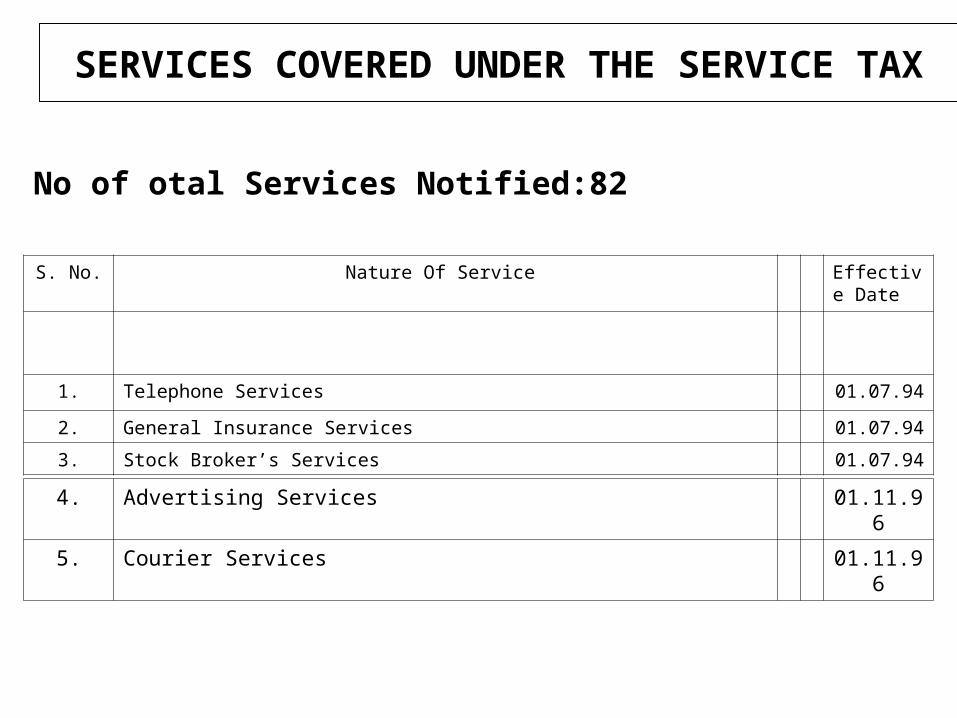

SERVICES COVERED UNDER THE SERVICE TAX

No of otal Services Notified:82

S. No. Nature Of Service Effective Date

1. Telephone Services 01.07.94

2. General Insurance Services 01.07.94

3. Stock Broker’s Services 01.07.94

4. Advertising Services 01.11.96

5. Courier Services 01.11.96

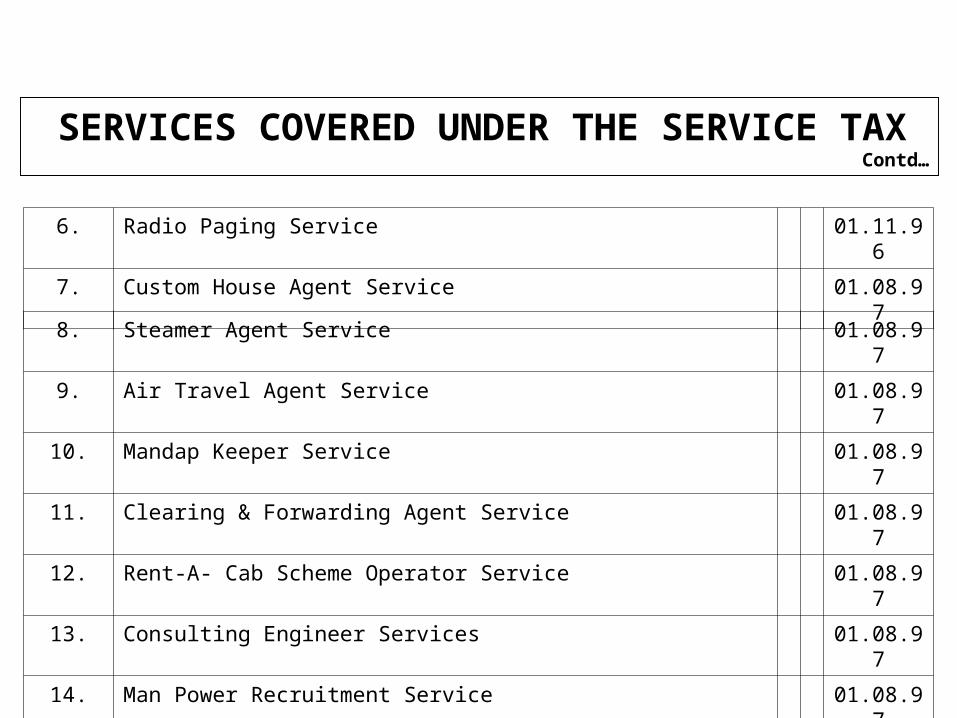

SERVICES COVERED UNDER THE SERVICE TAX Contd…

8. Steamer Agent Service 01.08.97

9. Air Travel Agent Service 01.08.97

10. Mandap Keeper Service 01.08.97

11. Clearing & Forwarding Agent Service 01.08.97

12. Rent-A- Cab Scheme Operator Service 01.08.97

13. Consulting Engineer Services 01.08.97

14. Man Power Recruitment Service 01.08.97

15. Tour Operator Services 01.08.97

6. Radio Paging Service 01.11.96

7. Custom House Agent Service 01.08.97

SERVICES COVERED UNDER THE SERVICE TAX Contd…

16. Architect Services 16.10.98

17. Interior Decorator/Designers Services 16.10.98

18. Under Writer Services 16.10.98

19. Credit Rating Agency Services 16.10.98

20. Chartered Accountants Services 16.10.98

21. Cost Accountants Services 16.10.98

22. Company Secretary Services 16.10.98

23. Real Estate Agent/Consultant Services 16.10.98

24. Security/Detective Agency Services 16.10.98

25. Market Research Agency Services 16.10.98

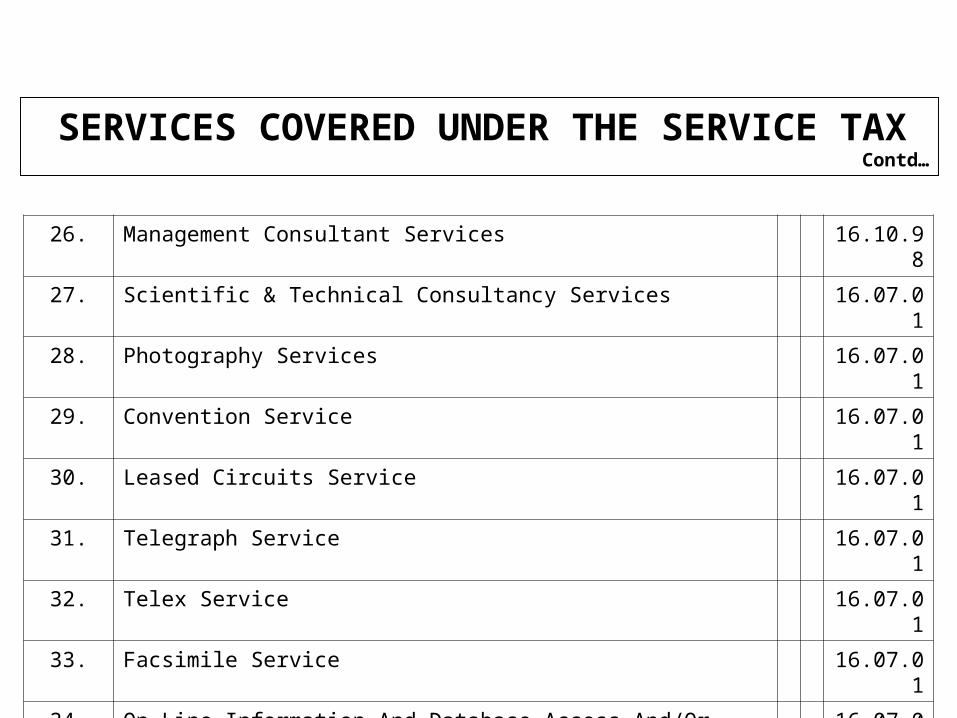

SERVICES COVERED UNDER THE SERVICE TAX Contd…

26. Management Consultant Services 16.10.98

27. Scientific & Technical Consultancy Services 16.07.01

28. Photography Services 16.07.01

29. Convention Service 16.07.01

30. Leased Circuits Service 16.07.01

31. Telegraph Service 16.07.01

32. Telex Service 16.07.01

33. Facsimile Service 16.07.01

34. On-Line Information And Database Access And/Or Retrieval Service 16.07.01

35. Video Tape Production Service 16.07.01

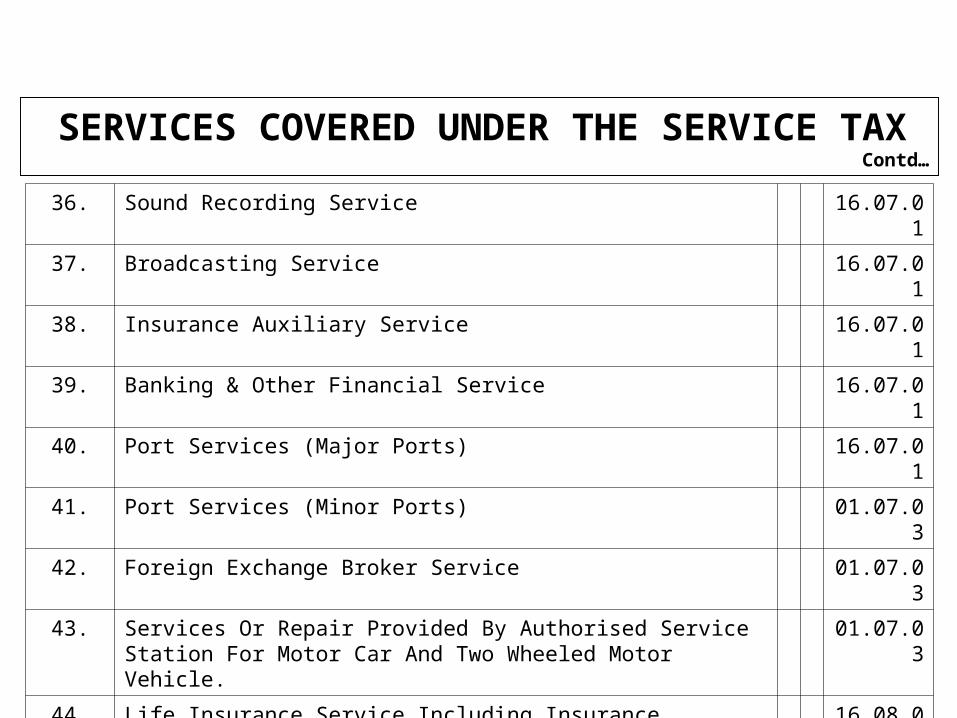

SERVICES COVERED UNDER THE SERVICE TAX Contd…

36. Sound Recording Service 16.07.01

37. Broadcasting Service 16.07.01

38. Insurance Auxiliary Service 16.07.01

39. Banking & Other Financial Service 16.07.01

40. Port Services (Major Ports) 16.07.01

41. Port Services (Minor Ports) 01.07.03

42. Foreign Exchange Broker Service 01.07.03

43. Services Or Repair Provided By Authorised Service Station For Motor Car And Two Wheeled Motor Vehicle.

01.07.03

44. Life Insurance Service Including Insurance Auxiliary Services Relating To Life Insurance

16.08.02

45. Cargo Handling Services 16.08.02

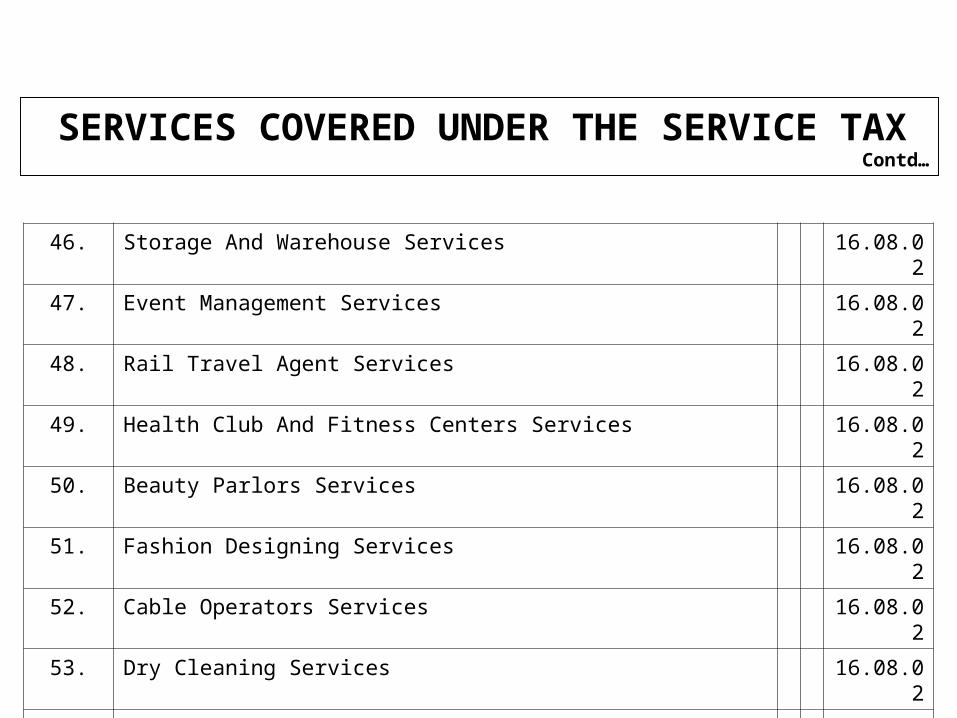

SERVICES COVERED UNDER THE SERVICE TAX Contd…

46. Storage And Warehouse Services 16.08.02

47. Event Management Services 16.08.02

48. Rail Travel Agent Services 16.08.02

49. Health Club And Fitness Centers Services 16.08.02

50. Beauty Parlors Services 16.08.02

51. Fashion Designing Services 16.08.02

52. Cable Operators Services 16.08.02

53. Dry Cleaning Services 16.08.02

54. Business Auxiliary Services 01.07.03

55. Commercial Training & Coaching Centre 01.07.03

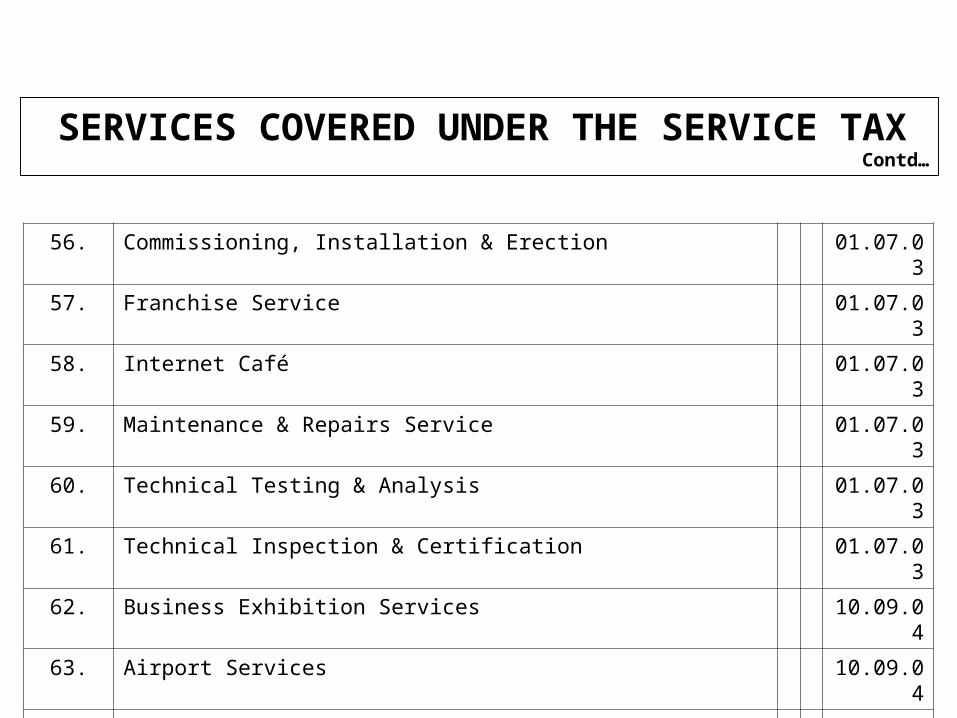

SERVICES COVERED UNDER THE SERVICE TAX Contd…

56. Commissioning, Installation & Erection 01.07.03

57. Franchise Service 01.07.03

58. Internet Café 01.07.03

59. Maintenance & Repairs Service 01.07.03

60. Technical Testing & Analysis 01.07.03

61. Technical Inspection & Certification 01.07.03

62. Business Exhibition Services 10.09.04

63. Airport Services 10.09.04

64. Transport Of Goods By Air 10.09.04

65. Survey And Exploration Of Minerals 10.09.04

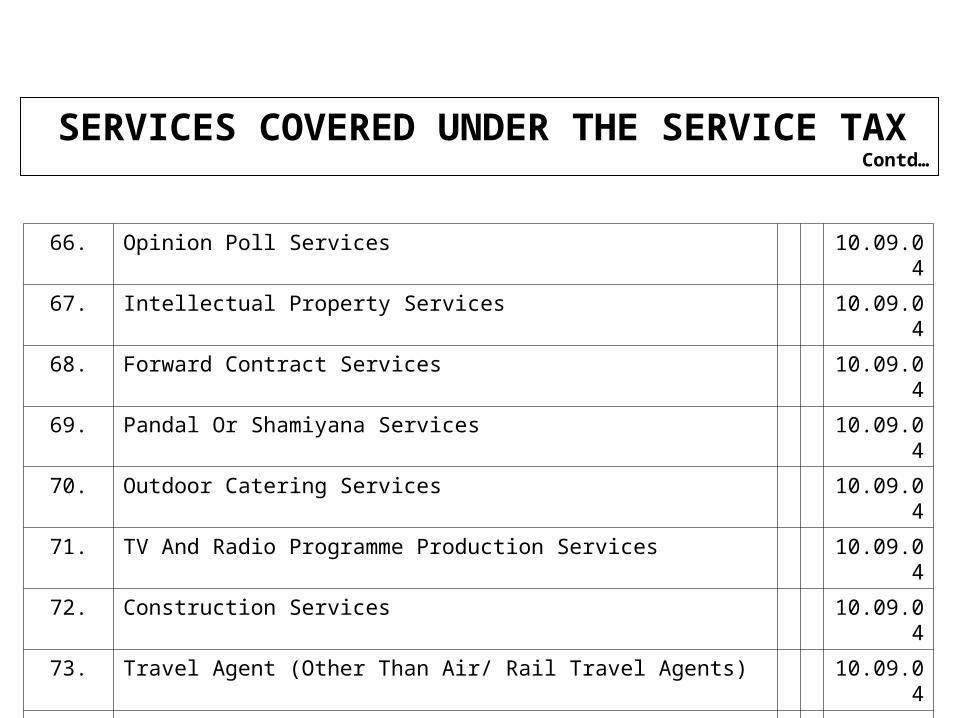

SERVICES COVERED UNDER THE SERVICE TAX Contd…

66. Opinion Poll Services 10.09.04

67. Intellectual Property Services 10.09.04

68. Forward Contract Services 10.09.04

69. Pandal Or Shamiyana Services 10.09.04

70. Outdoor Catering Services 10.09.04

71. TV And Radio Programme Production Services 10.09.04

72. Construction Services 10.09.04

73. Travel Agent (Other Than Air/ Rail Travel Agents) 10.09.04

74. Booking Of Goods For Transportation By Road 01.01.05

Extension of the Service Tax net – Budget 2005

74 Transport of goods through pipeline or other conduit.75 preparation and clearance, excavation, earth moving

and demolition services, other than those provided to agriculture, irrigation and watershed development.

76 Dredging services of rivers, ports, harbors, backwater and estuaries.

77 Survey and map making other than by Government Departments.

78 Cleaning services other than in relation to agriculture, horticulture, animal husbandry or dairying.

79 Membership of Clubs or Associations (religious forum, political organizations will be excluded).

80 Packaging services.81 Mailing list compilation and mailing; and82 Construction of residential complexes having more

than twelve residential houses or apartments together with common areas and other appurtenances.

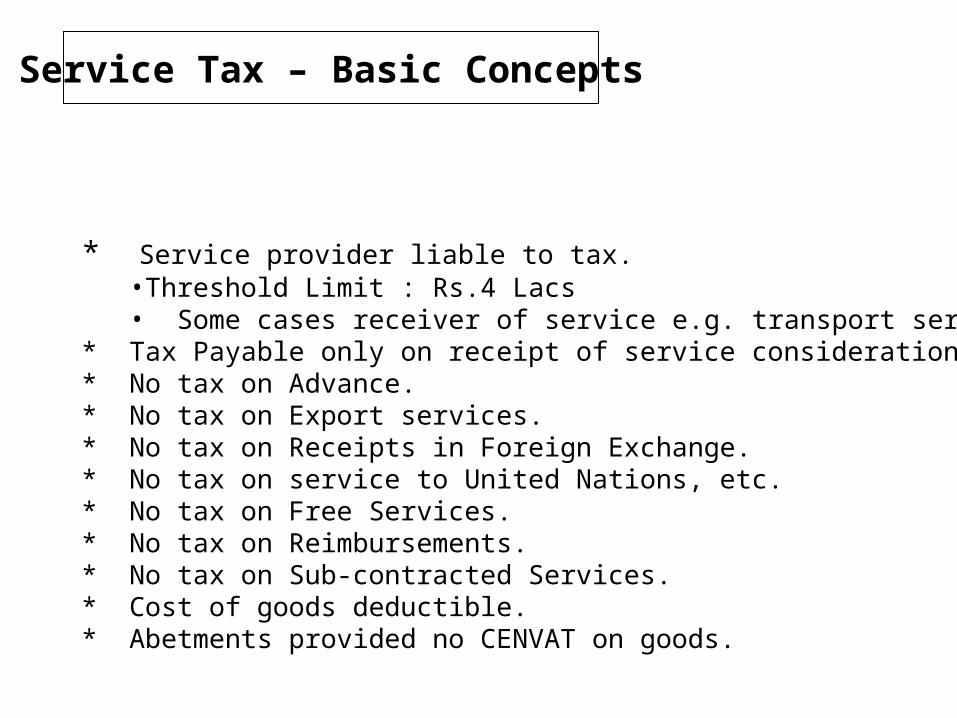

* Service provider liable to tax.•Threshold Limit : Rs.4 Lacs• Some cases receiver of service e.g. transport service.

* Tax Payable only on receipt of service consideration.* No tax on Advance.* No tax on Export services.* No tax on Receipts in Foreign Exchange.* No tax on service to United Nations, etc.* No tax on Free Services.* No tax on Reimbursements.* No tax on Sub-contracted Services.* Cost of goods deductible.* Abetments provided no CENVAT on goods.

Service Tax – Basic Concepts

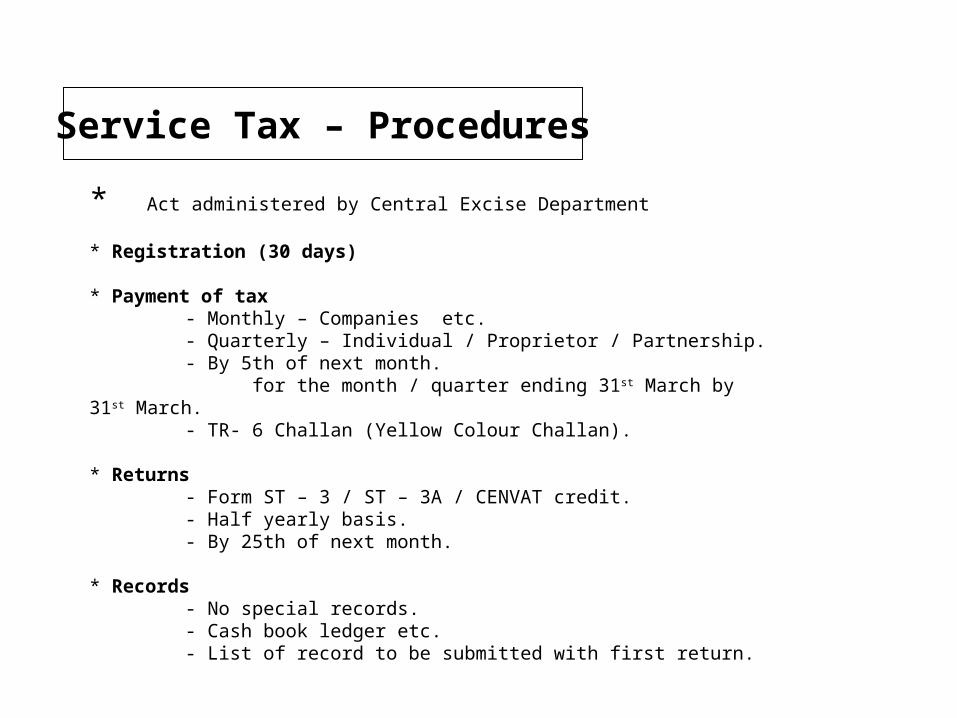

* Act administered by Central Excise Department

* Registration (30 days)

* Payment of tax- Monthly – Companies etc.- Quarterly – Individual / Proprietor / Partnership.- By 5th of next month. for the month / quarter ending 31st March by 31st March.- TR- 6 Challan (Yellow Colour Challan).

* Returns- Form ST – 3 / ST – 3A / CENVAT credit.- Half yearly basis.- By 25th of next month.

* Records- No special records.- Cash book ledger etc.- List of record to be submitted with first return.

Service Tax – Procedures

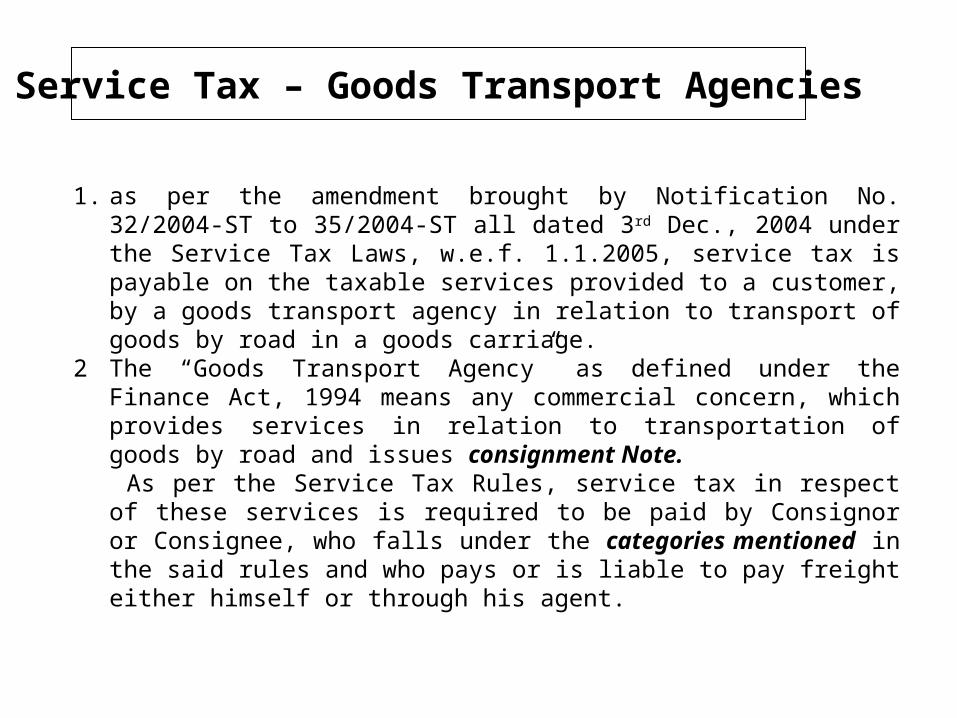

1. as per the amendment brought by Notification No. 32/2004-ST to 35/2004-ST all dated 3rd Dec., 2004 under the Service Tax Laws, w.e.f. 1.1.2005, service tax is payable on the taxable services provided to a customer, by a goods transport agency in relation to transport of goods by road in a goods carriage.

2 The “Goods Transport Agency” as defined under the Finance Act, 1994 means any commercial concern, which provides services in relation to transportation of goods by road and issues consignment Note. As per the Service Tax Rules, service tax in respect of these services is required to be paid by Consignor or Consignee, who falls under the categories mentioned in the said rules and who pays or is liable to pay freight either himself or through his agent.

Service Tax – Goods Transport Agencies

Registration Each office that is liable to make payment against freight and on whom the

GTA raises invoices, would be required to obtain registration under the Service Tax regulations, being the person liable to pay service tax on

In case the said office is already registered under the Service Tax regulations in any other taxable service category, the existing registration certificate may be suitably amended.

The location is paying transportation charges o behalf of other locations to obtain centralised registration by including such other locations as additional places in the centralised registration.

Service Tax – Goods Transport Agencies

Transport contractors to issue serially numbered“Consignment Note” giving Name of the consignor and consignee.

ii. Registration number of the goods carriage in which the goods are transported.

iii. Details of goods transported.iv. Details of the place of origin and destinationv. Person liable for paying service tax (viz. whether consignor, consignee

or goods transport agency)Transport Agency will raise Bill/Invoicefor each of the consignment Note, separately

which are serially numbered and shall contain the following details, (i) Name, address and the registration number of such person. Goods

transport Agencies may not be required to mention their Registration numbers in the bills/invoices raised on us.

(ii) Name and address of the person receiving taxable service(iii) Description, classification and value of taxable service provided or to

be provided(iv) The service tax payable thereon.(v) The Consignment Note Number and date.(vi) Gross weight of the consignment (vii) Other details mentioned in the said Rule viz. 7.2.3. Such Bill/Invoice will be raised by concerned Goods Transport

Agency

Service Tax – Goods Transport Agencies

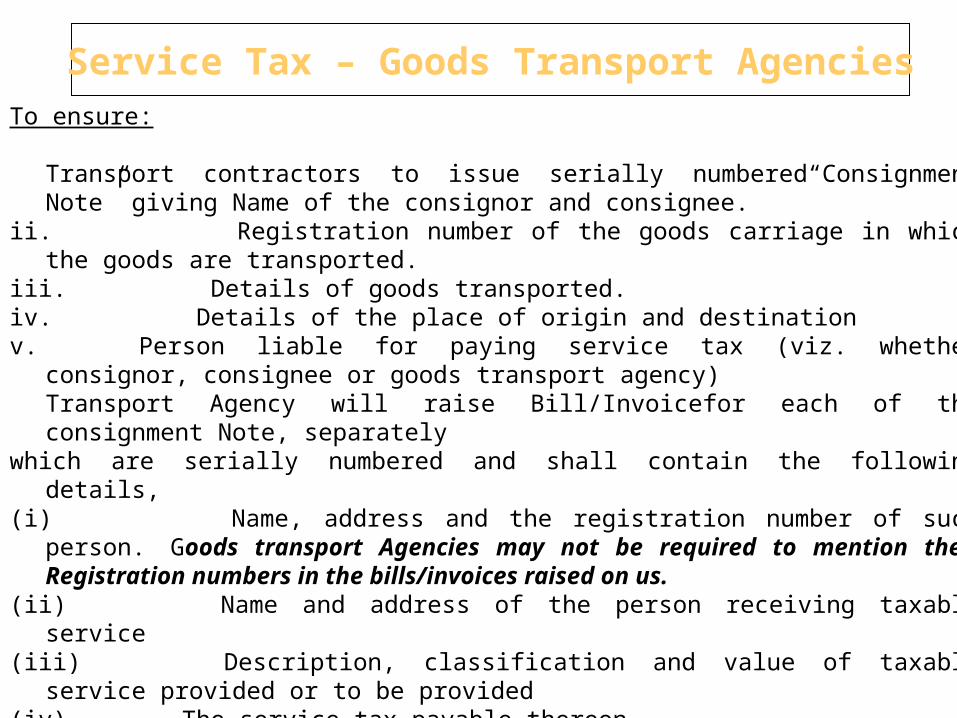

To ensure:

Transport contractors to issue serially numbered“Consignment Note” giving Name of the consignor and consignee.

ii. Registration number of the goods carriage in which the goods are transported.

iii. Details of goods transported.iv. Details of the place of origin and destinationv. Person liable for paying service tax (viz. whether consignor, consignee or

goods transport agency)Transport Agency will raise Bill/Invoicefor each of the consignment Note, separately

which are serially numbered and shall contain the following details, (i) Name, address and the registration number of such person. Goods

transport Agencies may not be required to mention their Registration numbers in the bills/invoices raised on us.

(ii) Name and address of the person receiving taxable service(iii) Description, classification and value of taxable service provided or to be

provided(iv) The service tax payable thereon.(v) The Consignment Note Number and date.(vi) Gross weight of the consignment (vii) Other details mentioned in the said Rule viz. 7.2.3. Such Bill/Invoice will be raised by concerned Goods Transport Agency

Service Tax – Goods Transport Agencies

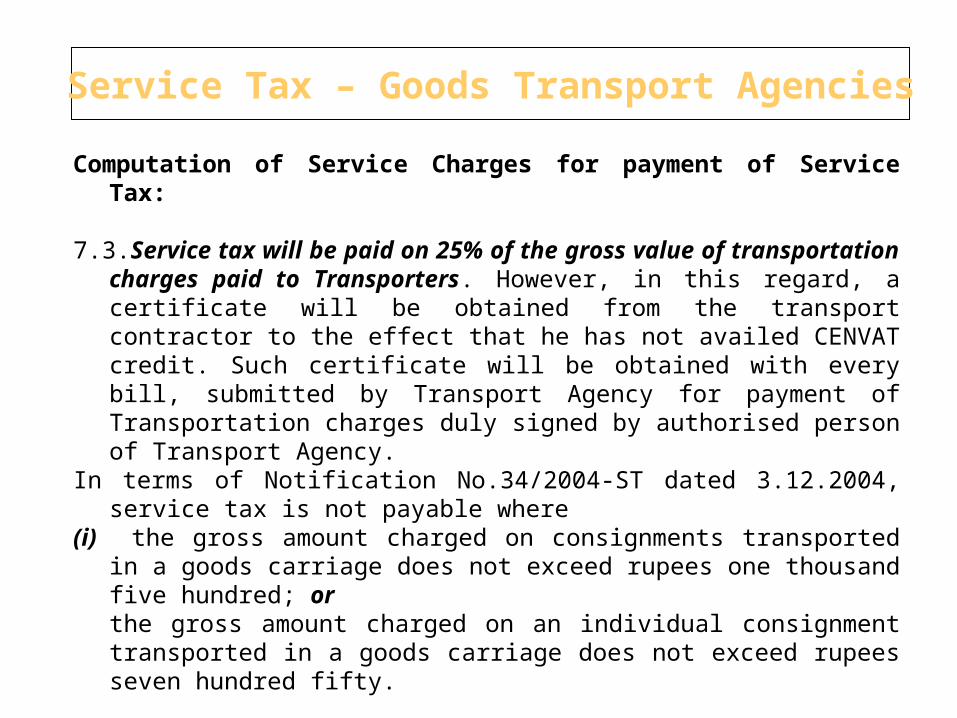

Computation of Service Charges for payment of Service Tax: 7.3.Service tax will be paid on 25% of the gross value of

transportation charges paid to Transporters. However, in this regard, a certificate will be obtained from the transport contractor to the effect that he has not availed CENVAT credit. Such certificate will be obtained with every bill, submitted by Transport Agency for payment of Transportation charges duly signed by authorised person of Transport Agency.

In terms of Notification No.34/2004-ST dated 3.12.2004, service tax is not payable where

(i) the gross amount charged on consignments transported in a goods carriage does not exceed rupees one thousand five hundred; orthe gross amount charged on an individual consignment transported in a goods carriage does not exceed rupees seven hundred fifty.

Therefore, service tax is exempt if either condition of clause (i) or condition of clause (ii) are satisfied.

Service Tax – Goods Transport Agencies

Payments: All the locations who have obtained registration , are required to

make payment of service tax in line with the above on due date viz. 25th of the following month of the payment made and not of the services availed or bill date, in respect of such services availed on or after 1.1.2005. However, in respect of payments for transportation charges made in the month of March, the service tax payment thereof is to be made on of before 31st March of the same year.

Recovery of service tax paid from the customersWherever actual transportation charges are recovered from the

customer separately as per contract for supply of products, then, in addition to such transportation charges, the service tax paid by us on such transportation charges may also be recovered from the customer by composite billing. However, service tax paid by IOC on on transportation charges in respect of supply of MS, HSD supplies to RO Dealers and SKO(PDS)/ LPG(Dom) to distributors may not be recovered from such RO dealers/Distributors, till further instructions from Pricing Group.

Service Tax – Goods Transport Agencies

7. Credit of Service Tax paid: As per CENVAT credit rules manufacturer of goods can take credit of

service tax on any input service. ‘Input Services’ defined in the rules mean any service used by the manufacturer of goods in relation to the clearance of the goods from the place of removal. Though the “place of removal” is not defined under Service Tax Laws, definition for the same could be taken from Sec.4(2)(c) of CE Act. Therefore, if service tax on inward transportation of our own Refinery manufactured goods up to the place of removal is paid by our terminals/depots viz. place of removal (where excise duty is paid on normal transaction value), receiving the goods, details of service tax paid on such inward transportation charges with required documents will have to be provided to the concerned refinery from where goods are moved for availing input service tax credit. Since we pay service tax on transportation charges, our service tax-paying document (prescribed challan) along with bill for transportation received from transporter will be the document for claiming input service tax credit.

Service Tax – Goods Transport Agencies

CENVAT Credit Rules

What is meant by an input service?

For a service provider:

Input service means any service used by a provider of taxable service for providing an output service.

For a manufacturer:

Input Service means any service used by a manufacturer, whether directly or indirectly, in relation to the manufacture of final products and clearance of final products from the place of removal.

CENVAT Credit Rules

What is meant by an input service?Includes services used in relation to

Setting up, modernization, renovation, repairs to a factory / premises of a service provider or his officeAdvertisement or sale promotionMarket researchProcurement of inputsActivity relating to business such as accounting, auditing, financing, recruitment, quality control, coaching, training, computer networking, credit rating, share registry, security, inwards / outward transportation of inputs / capital goods / finished goods

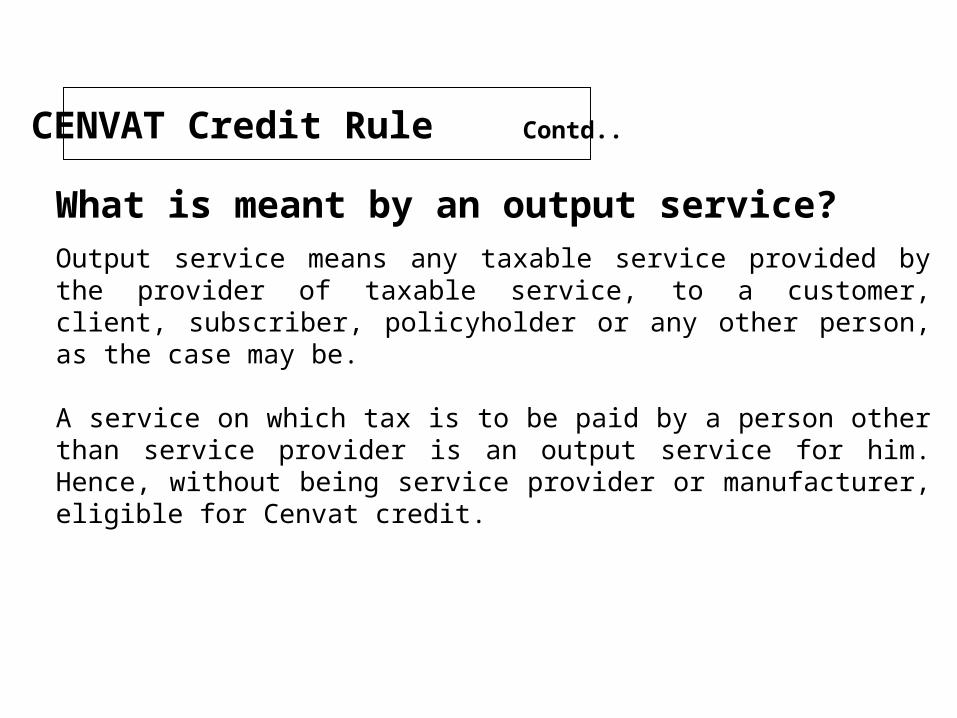

What is meant by an output service?Output service means any taxable service provided by the provider of taxable service, to a customer, client, subscriber, policyholder or any other person, as the case may be.

A service on which tax is to be paid by a person other than service provider is an output service for him. Hence, without being service provider or manufacturer, eligible for Cenvat credit.

CENVAT Credit Rule Contd..

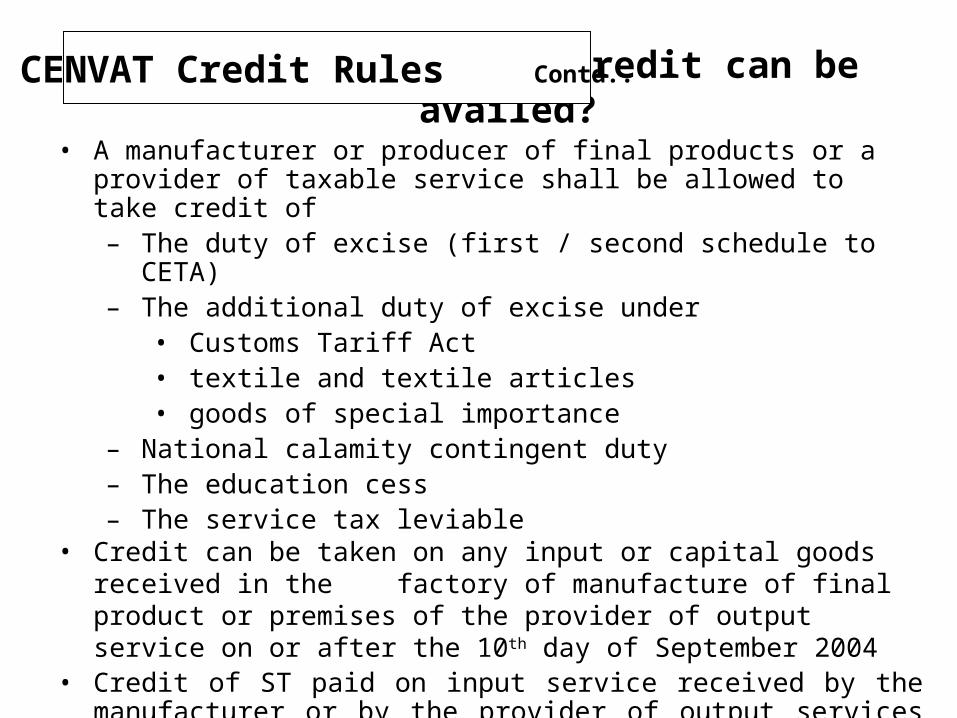

What kind of Cenvat credit can be availed?• A manufacturer or producer of final products or a provider of taxable

service shall be allowed to take credit of– The duty of excise (first / second schedule to CETA)– The additional duty of excise under

• Customs Tariff Act• textile and textile articles • goods of special importance

– National calamity contingent duty– The education cess– The service tax leviable

• Credit can be taken on any input or capital goods received in the factory of manufacture of final product or premises of the provider of output service on or after the 10th day of September 2004

• Credit of ST paid on input service received by the manufacturer or by the provider of output services on or after the 10th day of September 2004

CENVAT Credit Rules Contd..

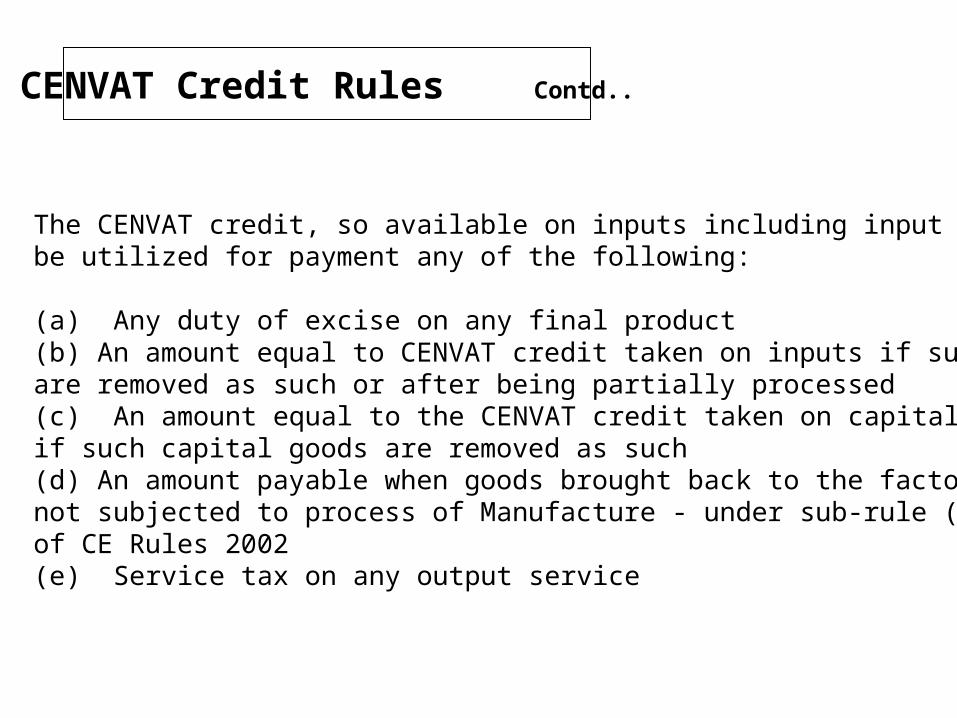

The CENVAT credit, so available on inputs including input services may be utilized for payment any of the following: (a) Any duty of excise on any final product(b) An amount equal to CENVAT credit taken on inputs if such inputs are removed as such or after being partially processed(c) An amount equal to the CENVAT credit taken on capital goods if such capital goods are removed as such(d) An amount payable when goods brought back to the factory are not subjected to process of Manufacture - under sub-rule (2) of Rule 16 of CE Rules 2002(e) Service tax on any output service

CENVAT Credit Rules Contd..

What is Input Service Distributor?

Input service distributor means an office of the manufacturer of final products or output service, which receives invoices issued under rule 4A of the Service Tax Rules, 1994 towards purchases of input services and issues invoice, bill or challan for the purposes of distributing the credit of service tax paid on such input services to such manufacturer or provider of output service.

Input Service Distributor need not be registered.Will have to file a return of input tax distributed.

CENVAT Credit Rules Contd..

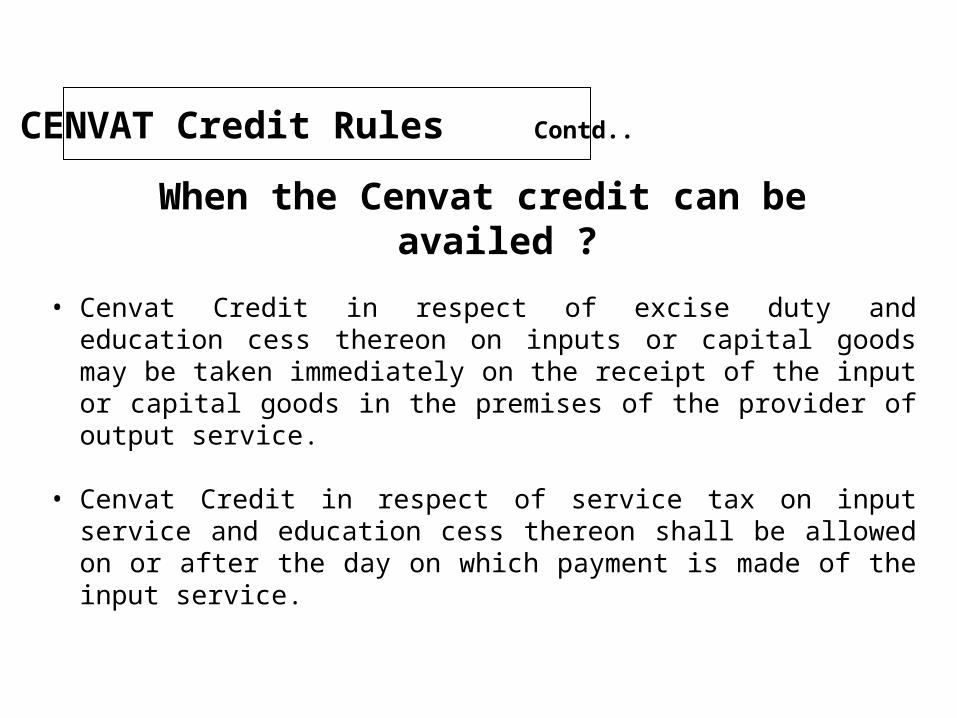

When the Cenvat credit can be availed ?

• Cenvat Credit in respect of excise duty and education cess thereon on inputs or capital goods may be taken immediately on the receipt of the input or capital goods in the premises of the provider of output service.

• Cenvat Credit in respect of service tax on input service and education cess thereon shall be allowed on or after the day on which payment is made of the input service.

CENVAT Credit Rules Contd..

Cenvat Admissibility:Manufacturing Units: Lube Plant / Small Can Filling Plant should avail the credit of the Service Tax

billed on them and paid by them on services used in or in relation to the Manufacture, in addition to the duties of excise paid on various inputs / Capital goods and the same can be used for payment of duty / service tax wherein taxable services are rendered as provider.

The Service Tax paid on Transportation relating to clearance of duty paid

products to the Depots is available for credit as it is attributable to clearance of product from the place of removal. If receiving location is paying the transportation for movement from the manufacturing plant then the same can be transferred to the plant for availing credit.

In addition the manufacturing units can also avail credit on services covered

by the second part of the definition of “Input Services” like ‘activities relating to business’ etc. The guidelines forwarded may be referred for details of activities relating to manufacturing and activities relating to business.

CENVAT Credit Rules Contd..

Cenvat Admissibility: Marketing terminals/Locations:

Many of the Marketing locations/Terminals may not be provider of output services. Therefore there may not be payment of service tax by such locations as “provider of output services”. However, these locations may be paying service tax to service provider or as service availer in respect of some of the services like transportation charges etc. to Excise Authorities for products transferred from our own Refineries under Normal Transaction Value.

Under such circumstances, these locations should take credit of

service tax paid to provider of services against the service tax payable to Excise authorities as output service provider , wherever applicable (like hospitality etc.refer Para 11). After such adjustments, if any input service tax credit, including service tax paid as availer of services eg. On Transportation charges etc., same may be transferred to respective refinery of IOC from where the product has been received, as ISD.

The feasibility of claiming/transferring the credit by the locations receiving the

product from OMC’s refineries is being examined and we will revert back shortly. In the mean while the details should be kept ready.

CENVAT Credit Rules Contd..

Cenvat Admissibility:

All administrative offices Viz. Regional , State, Area, Divisional Offices:

For service tax paid on other input services on activities relating to business and covered in the second part of the definition they may act as ISD and transfer the credit to Gujarat refinery.

CENVAT Credit Rules Contd..

On what basis Cenvat credit can be taken?

The Cenvat credit can be taken on the basis of following documents• an excise invoice issued by a manufacturer or importer of inputs or

capital goods.• a supplementary invoice issued by a manufacturer or importer of inputs

or capital goods.• a bill of entry.• an invoice or bill or challan issued by a provider of input service on or

after the 10th September, 2004.• An invoice issued by a input service distributor.

CENVAT Credit Rules Contd..

The above documents should contain at least

• Details of payment of duty or service tax • Description of goods or taxable service• Assessable value• Name and address of the factory or warehouse or provider of output

service• Registration number under central excise or service tax

Not required if invoice from input distributors.

CENVAT Credit Rules Contd..

separate record for taxable and non-taxable or exempted services?

A service provider should maintain separate record for taxable and non-taxable or exempted services in respect of receipt, consumption and inventory of inputs and input services meant for use in providing taxable output service and exempted output service. He can take Cenvat credit on only that quantity of inputs or input services which is intended for use in providing taxable output services.

However, he has an option not to maintain separate record as above but in such cases he shall be allowed to utilize the Cenvat credit only to the extent of 20% of the amount of service tax payable on taxable output service.

CENVAT Credit Rules Contd..

FAQs

Whether 100% Cenvat is available on capital goods?

The restriction of 50% on credit on capital goods would continue for manufactures as well as service providers. The credit of balance 50% can be availed in any subsequent financial year. However, on capital goods that are used exclusively in providing exempted services, Cenvat credit will not be allowed.

FAQs Contd..

How the Cenvat credit can be utilized by a service provider?

A service provider can utilize the Cenvat credit for payment of;Service Tax on any output service.a)An amount equal to Cenvat credit taken on inputs if such inputs are removed as such or after being partially processed; or b)An amount equal to the Cenvat credit taken on capital goods if such capital goods are removed as such;c)Education cess on excisable goods and on taxable services can be utilized only for payment of education cess on (a) Service Tax on output service and (b) excise duty on inputs or capital goods if these are removed from his premises.

FAQs Contd..

What if the output services are exported?

If the output services are exported, the Cenvat credit in respect of the inputs or input services used in providing such output services shall be allowed to be utilized by the provider of service towards payment of Service Tax on taxable output service. And where for any reason such adjustment is not possible, he shall be allowed refund of such amount subject to certain safeguards, conditions and limitations.

How the manufacturer can utilize such Cenvat credit?

The manufacturer can utilize the Cenvat credit of service tax for payment of any duty of excise on any final products. The Cenvat credit of education cess can be utilized only for payment of education cess on excise duty on any final products and also on inputs or capital goods if these are removed from his factory.

FAQs Contd..

What if the final products are exported?If the final products or intermediate products are exported, the CENVAT credit in respect of the input services used in manufacturing such products shall be allowed to be utilized by the manufacturers towards payment of duty of excise on any final products cleared for home consumption or for export on payment of duty. And where for any reason such adjustment is not possible, he shall be allowed refund of such amount subject to certain safeguards, conditions and limitations. Provided that no refund of credit shall be allowed if the manufacturer avails of drawback allowed under the Customs and central Excise Duties Drawback Rules, 1995, or claims a rebate of duty under the Central Excise Rules, 2002, in respect of such duty.

FAQs Contd..

What records should be maintained to avail the credit?

• To avail the Cenvat credit of service tax on input services proper records for the receipt and consumption of the input services are to be maintained.

• To avail the Cenvat credit of excise duty on inputs and capital goods, proper records for the receipt, disposal, consumption and inventory of the inputs and capital goods are to be maintained.

• The record should contain relevant information regarding the value, duty or tax paid, Cenvat credit taken or utilized, the person from whom the inputs or capital goods or input services have been procured.

• The burden of proof regarding the admissibility of the Cenvat credit shall lie upon the person taking such credit.

FAQs Contd..

Is there any separate return to be filed for Cenvat credit availed and utilized?

The provider of output service availing Cenvat credit shall submit a Half Yearly return to the superintendent of central excise, by the end of the month following the particular half-year (i.e. for half year ending 30.09.2004, the return is to be submitted before 31.10.2004)

The input service distributor is to submit a half yearly Statement, giving the details of credit received and distributed during the said half year to the Superintended of Central Excise, by the end of the month following the half year. No form is prescribed for the Statement.

FAQs Contd..

What are the consequences if Cenvat credit is taken wrongly?

Where the Cenvat credit has been wrongly taken or utilized or erroneously refunded, the same along with interest shall be recovered.

If any person takes Cenvat credit in respect of input services, wrongly or without taking reasonable steps to ensure that appropriate Service Tax on the said input services has been paid as indicated in the documents accompanying the input services or contravenes any of the provisions of these rules, then such person shall be liable to a penalty which may extend up to ten thousand rupees.

FAQs Contd..

If any person takes Cenvat credit in respect of inputs or capital goods, wrongly or without taking reasonable steps to ensure that appropriate duty on the said inputs or capital goods has been paid as indicated in the documents accompanying the inputs or capital goods or contravenes any of the provisions of these rules, then, all such goods shall be liable to confiscation. Also such person shall be liable to a penalty not exceeding the duty on the excisable goods in respect of which any contravention has been committed, or ten thousand rupees, whichever is greater.

FAQs Contd..

In a case, where the Cenvat credit has been taken or utilized wrongly on account of (i) fraud, (ii) willful mis-statement (iii) collusion or (iv) suppression of facts or (v) contravention of any of the provisions of the Finance Act or the rules made there under with intention to evade payment of service tax, then, the provider of output service shall also be liable to pay penalty, in addition to Service Tax and interest, if any, payable by him, a sum which shall not be less than, but which shall not exceed twice, the amount of Service Tax sought to be evaded.

The penalty may be reduced to 25% of Service Tax amount in certain circumstances.

FAQs Contd..

Issues Needing Discussions and Decisions

Procedure to be followed for transfer of credit from :(a) Locations(b) State Offices(c) Regional Offices

Suggested: - Credit at RO/SO to be transferred to Mfg. Unit within State/RO- Nodal Point for transfer of Credit at non-mfg locations

to be State Offices.- Data to be captured by State Offices thru system- Credit to be transferred through RO/HO to Refinery

Issues Contd..

Treatment of Credit at the locations rendering output Services

Suggested:Considering difficulties involved in separate accounting,Credit to be transferred to Mfg location/Refinery as ISD and not to be Claimed as Service Provider

Issues Contd..

Treatment of Credit at the RO making payment of Service Tax for other locations

Suggested:Considering difficulties involved in separate accounting,Credit to be transferred to Mfg location/Refinery as ISD and not to be Claimed as Service Provider

Issues Contd..

Treatment of Credit at the locations receiving products Partly from OMCs

Suggested:Credit to be transferred to Mfg location/Refinery as ISD

Issues Contd..

Treatment of Credit at the locations receiving products Exclusively from OMCs

Suggested:Credit cannot be availed

Issues Contd..

Accounting Treatment

Suggested:?

Issues Contd..

Can the service tax paid in respect of services of GTA by Road for clearance of product from the terminal to depot/customer be adjusted against the service tax payable as provider?

Ans: Yes. For inward Transportation only.

Issues Contd..

Whether service tax credit can be availed in respect of service tax paid on GTA by Road for clearance of product from the refinery/terminal/depot/IOBL to COCO/DOLD/COLD as they being the actual place of removal?

Yes.

Issues Contd..

Whether service tax paid on GTA by Road in respect of purchased product from OMCs or other private refineries or imported product for clearance from the place of removal i.e from terminal to depot can be availed as input credit?

Issues Contd..

CFA

Who is liable for Registration for GTA – IOC or CFA?

Liability of Service Tax for transportation payment made by CFA/DOLGfor sale to the Customers. CFA is raising Commission bill on IOC, which is inclusive of all Taxes on which CFA is paying Service Tax to the department.IOC is loosing Input Tax credit as Service Tax included in the commissionnot shown separately by CFA.

Issues Contd..

ACCOUNTING FOR SERVICE TAX

The Service Tax law recognised only cash system of accountancy. However the Companies Act requires accrual system of accountancy applying the accounting standards of ICAI.

ICAI provides that the cost of goods be taken net of CENVAT credit. The same treatment applies for the CENVAT credit available on the services.

Thus, how to keep a track in accounts for Service Tax payable and CENVAT credit.

Either create memoranda ledger accounts or make some additional entries in financial books. The following entries are suggested in financial books.

ACCOUNTING FOR SERVICE TAX Contd..

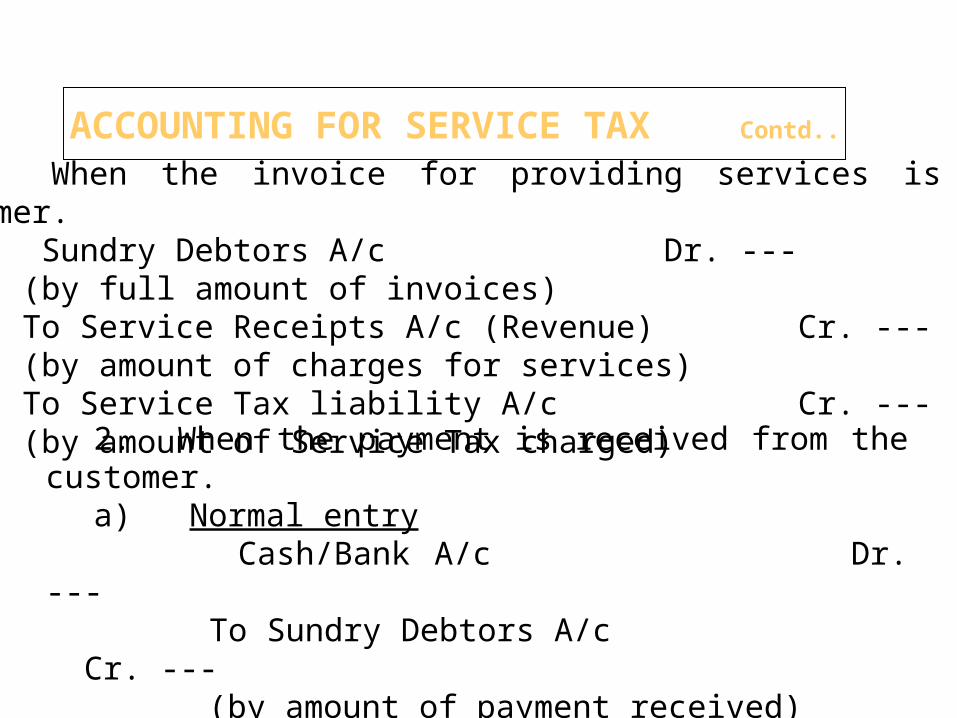

1. When the invoice for providing services is raised to customer.

Sundry Debtors A/c Dr. --- (by full amount of invoices) To Service Receipts A/c (Revenue) Cr. --- (by amount of charges for services) To Service Tax liability A/c Cr. --- (by amount of Service Tax charged)

2. When the payment is received from the customer.a) Normal entry Cash/Bank A/c Dr. --- To Sundry Debtors A/c Cr.

--- (by amount of payment received)

SHAH BAHETI CHANDAK & CO.,CHARTERED ACCOUNTANTS, NAGPUR

ACCOUNTING FOR SERVICE TAX Contd..

b) Additional Entry Service Tax liability a/c Dr. --- To Service Tax payable a/c Cr. ---By the amount of Service Tax component received. The total of all such credit in Service Tax payable a/c during the period will be actual amount payable for the period.3. When the goods (inputs) are purchased. Material A/c Dr. --- (net value of goods) CENVAT credit available Dr. --- (By the amount of CENVAT credit available) To Sundry Creditors A/c Cr. ---This is normal entry. No further entry is required as CENVAT credit is available on goods even if suppliers bill is not paid.

SHAH BAHETI CHANDAK & CO.,CHARTERED ACCOUNTANTS, NAGPUR

ACCOUNTING FOR SERVICE TAX Contd..

4. When the input service is received, : Service A/c (Primary head) Dr. --- (net value of services) CENVAT credit Receivable A/c Dr. --- (by amount of Service Tax charged in the bill) To Sundry Creditors A/c Cr.

---5. When the payment is made to the input service

provider.a) Normal entry Sundry Creditors A/c Dr. --- To Cash/Bank A/c Cr.

--- (By amount paid)

SHAH BAHETI CHANDAK & CO.,CHARTERED ACCOUNTANTS, NAGPUR

ACCOUNTING FOR SERVICE TAX Contd..

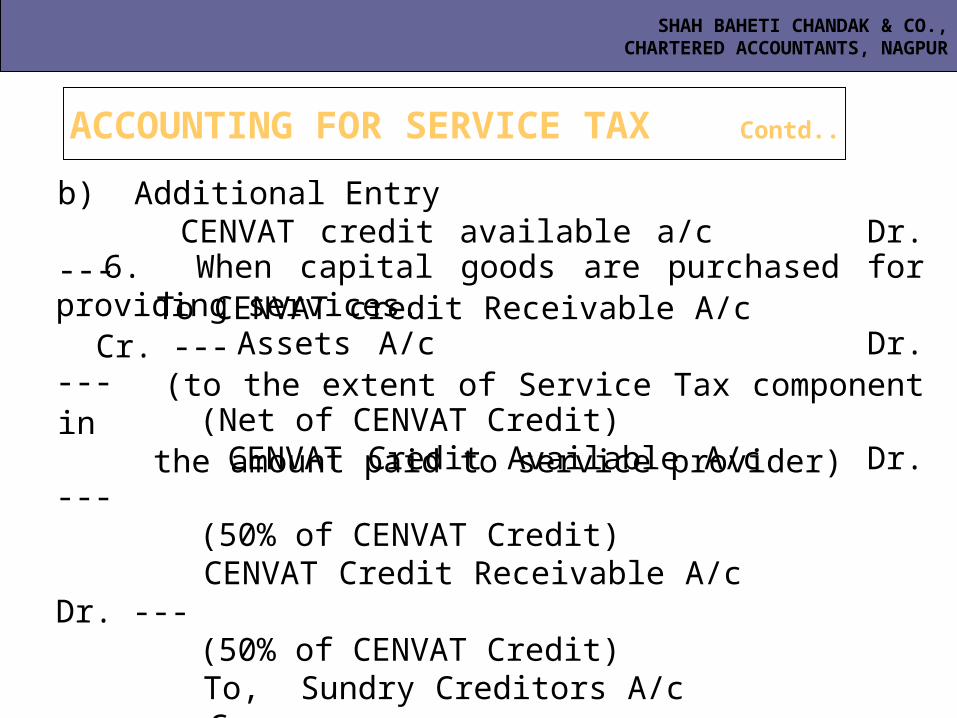

b) Additional Entry CENVAT credit available a/c Dr. --- To CENVAT credit Receivable A/c Cr. --- (to the extent of Service Tax component in the amount paid to service provider)6. When capital goods are purchased for providing services.

Assets A/c Dr. --- (Net of CENVAT Credit) CENVAT Credit Available A/c Dr. --- (50% of CENVAT Credit) CENVAT Credit Receivable A/c Dr. --- (50% of CENVAT Credit) To, Sundry Creditors A/c Cr.

---Since only 50% is available in the year of purchase.

SHAH BAHETI CHANDAK & CO.,CHARTERED ACCOUNTANTS, NAGPUR

ACCOUNTING FOR SERVICE TAX Contd..

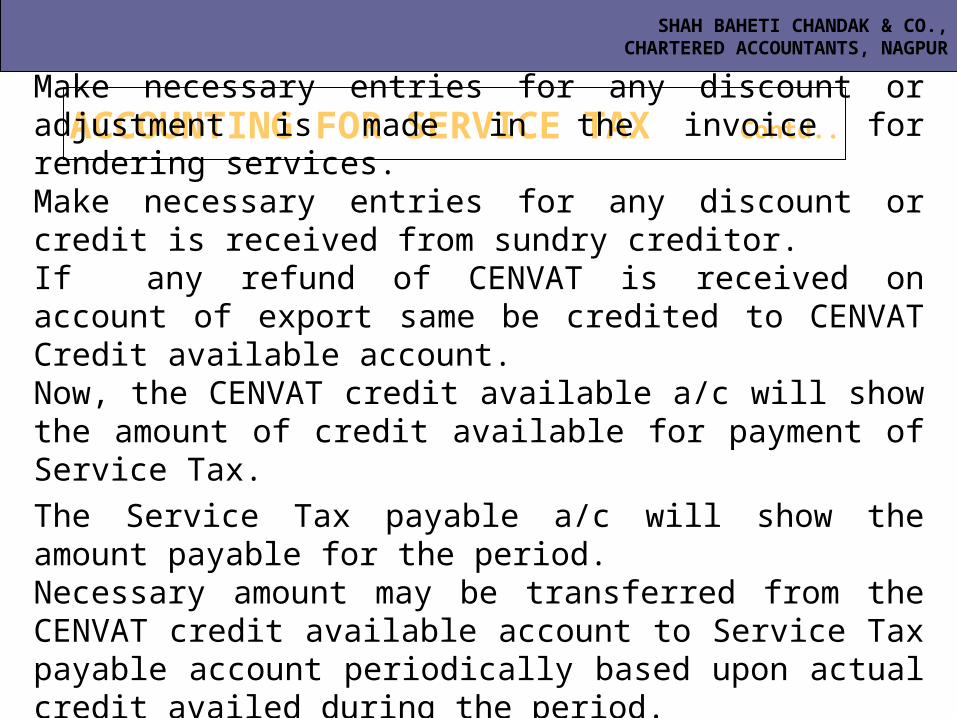

Make necessary entries for any discount or adjustment is made in the invoice for rendering services. Make necessary entries for any discount or credit is received from sundry creditor. If any refund of CENVAT is received on account of export same be credited to CENVAT Credit available account.Now, the CENVAT credit available a/c will show the amount of credit available for payment of Service Tax.

The Service Tax payable a/c will show the amount payable for the period.Necessary amount may be transferred from the CENVAT credit available account to Service Tax payable account periodically based upon actual credit availed during the period.

The actual amount of Tax paid be debited to Service Tax payable a/c.

SHAH BAHETI CHANDAK & CO.,CHARTERED ACCOUNTANTS, NAGPUR

ACCOUNTING FOR SERVICE TAX Contd..

At the end of a year : (a) Service Tax payable a/c will show a credit balance which

would be equal to Service Tax payable at the year end. (b) The Service Tax liability a/c will represents liability of the

Service Tax, which has not become due since the payment for rendering services is not received.

(c) CENVAT credit available a/c will show a debit balance which is available for discharging the liability

(d) The CENVAT Credit Receivable a/c will shows a debit balance which will be available in next year for availment subject to fulfillment of conditions i.e. (i) payment of consideration to the service provider or (ii) balance of credit available for capital goods to be used in any of the subsequent year.

Take the review and make necessary adjustments.

Any Questions ?

SHAH BAHETI CHANDAK & CO.,CHARTERED ACCOUNTANTS, NAGPUR

![Cenvat Accounting[1]](https://img.pdfslide.us/doc/110x75/54193e3a7bef0a05088b4642/cenvat-accounting1.jpg)