Embed Size (px)

Citation preview

SERVICE TAX AMENDMENTS FINANCE ACT 2016 & RECENT ISSUES

PRESENTATION FOR KORBA CPE CHAPTER OF CIRC OF ICAI

Compiled By : CA Ramandeep Singh Bhatia

RATES OF SERVICE TAXKrishi Kalyan Cess (KKC)In order to boost the agriculture sector, the Finance Minister has introduced a new Cess called as the Krishi Kalyan Cess. It shall to be levied @ 0.5% on value of all taxable services. Its proceeds will be exclusively used for financing initiatives relating to improvement of agriculture and welfare of farmers. The Cess has come into force with effect from 1st June, 2016. Summary Chart of Service tax Rates

Period Calculation Effective RateUp to 31/5/15 12% ST + 0.24 EC +0.12% SHEC 12.36%

1/6/15 to 14/11/15 14% ST 14.00%15/11/15 to 31/5/16 14% ST + 0.5% SBC 14.50%

1/6/16Onward

14%ST +0.5% KKC+SBC+0.5% 15.00%

FAQ’ ON KKCNow, the Central Government vide Circular No. 194/04/2016-ST, Dated: May 26, 2016

KKC (Minor Head)

Tax Collection Other Receipts (Interest)

Deduct Refunds

Penalties

0044-00-507 00441509 00441510 00441511 00441512

Further, the following have also been provided for w.e.f 1st June 2016:1) Is it applicable to Reverse Charge Also ?

2) Is it applicable to Exempt Services ?

3) Applicable on which Value ?

FAQ’ ON KKC•Value of taxable services for the purposes of the Krishi Kalyan Cess will be the value as determined in accordance with the Service Tax (Determination of Value) Rules, 2006.

•Thus, KKC would be levied in the following manner:In terms of Service Tax Valuation Rules, Service tax along with SB Cess and KKC needs to be applied on taxable value. Accordingly, effective rate of Service tax in following illustrative cases would be:

Particulars Effective Service Tax Rate including SBC & KKC

Works Contract: Original works 6% (15% x 40%)

Works Contract: Other than Original Work 10.50% (15% x 70%)

Restaurant and Outdoor catering: AC Restaurant services

6% (15% x 40%)

Restaurant and Outdoor catering: Outdoor catering services

9% (15% x 60%)

FAQ’ ON KKC5) Cenvat Credit Avilable ?

Central Government vide Notification No. 28/2016-Central Excise (N.T.), Dated: May 26, 2016 has amended CENVAT Credit Rules, 2004 to allow Cenvat credit of KKC to a service provider.

Definition of “service tax & cess” in the amended Notification No. 39/2012-ST dated June 20, 2012 (Rebate of the duty paid on excisable inputs or Service tax and cess paid on all input services used in providing service exported).

-CENVAT credit in respect of KKC shall be utilized only towards payment of KKC.

Comments: KKC would add to the cost for the manufacturers as they will not be able to avail the credit of KKC paid by them on input services utilised during manufacture. The prices will rise to that extent as cost would be recovered from ultimate consumers only.

FAQ’ ON KKC6) Point of Taxation of Levy of Krishi Kalyan Cess (KKC) ?Explanation 1 and 2 inserted with effect from March 1, 2016 to Rule 5 of the Point of Taxation Rules, 2011 directs that KKC will be applicable in the following cases:

Service provided and invoice issued before June 1, 2016 if but payment received after this date

• Service provided before June 1, 2016 but invoice issued (after 14 Days)and

payment received after this date

Rule -5(A) Invoice Issued & Payment Received before 1st June – NO STRule -5(B) Payment Received before 1st June + Invoice issued with 14 Days- NO STRule -3(A) Service Provided before 1st June + Invoice issued within 14 Days –No ST

Rule 4A of the Service Tax Rules, 2004 determines completion of service to be the date of invoice. Accordingly, if completion of service can be evidenced to be prior to imposition of KKC, it is doubtful if the rule can eclipse the levy under section 66B of Finance Act, 1994.

FAQ’ ON KKC7) Where the service tax is paid at an alternative rate in terms of sub-rules 7,7A,7B and 7C to Rule 6 ?

Total Service tax liability calculated under Rule 6(7)(7A), (7B) or (7C) * 0.5 (KKC)

__________________________________________________________14 (being the rate of service tax)

For example : for domestic bookings the rate of KKC would be: 0.7% * 0.5% / 14% = 0.025%

SEC.66D-NEGATIVE LIST

1) Educational services by way of

(a) pre-school education and education up to higher and secondary school or equivalent,

(b) education as a part of a curriculum for obtaining a qualification recognized by any law for the time being in force and

(c) education as a part of an approved vocational education course (This amendment would come into effect from the date of enactment of Finance Bill, 2016 -14/05/2016);

(d) Notification No.25/2012-ST as amended by Notification No.09/2016-ST dated 1st March, 2016 Included in Mega / General Exemption List.

BROADENING TAX BASE : ENTRIES REMOVED FROM LIST

SEC.66D-NEGATIVE LIST

2) Service of transportation of passengers, with or without accompanied belongings, by a stage carriage (w.e.f. 1st June 2016);

However, such services by a non-air-conditioned contract carriage will continue to be exempted by way of exemption Notification No. 25/2012-ST, as amended by notification No. 09/2016-ST, dated 1st March 2016

The service of transportation of passengers by air-conditioned stage carriage is being taxed at the same level of abatement (60%) as applicable to the transportation of passengers by a contract carriage, with same conditions of non-availment of Cenvat credit.

BROADENING TAX BASE : ENTRIES REMOVED FROM LIST

CHAPTER V-FINANCE ACT’94

Activity carried out by a lottery distributors or selling agents of the state government under the provision of the Lotteries (Regulation ) Act , 1998, Is Leviable to Service Tax

Explanation :2 , Section 65B(44)

A. Section 65(B) (44) – Definition of Service

B. Section 66(E) – Declared Service Assignment by the Government of the right to use the radio frequency spectrum is proposed to be declared service under section 66E and therefore it is made clear that it is not to be treated as sale of intangible goods.

CHAPTER V-FINANCE ACT’94

Section 67A has been amended and linked with the POT Rules and thus harmony has been created. Now, it is expected to settle the disputes regarding applicability of rate of service tax. The POT Rules shall remain relevant for determining rate of service tax as well as due date of payment of tax. (Enactment -14/05/2016)

C. Section 67A linked with Point of Taxation Rules (POT)

D. Period of limitation for bona-fide assesses extendedSection 73 has been amended to increase the limitation period from 18 months to 30 months for short levy/non-levy/short payment/non-payment/ erroneous refund of Service Tax.(Enactment -14/05/2016)

CHAPTER V-FINANCE ACT’94E. Section 75 - Interest on delayed payment of service tax

Scenario ProposedWillful default* and value of taxable service in

preceding year is less than Rs.60 lakh21%

Willful default and value of taxable service in preceding year is more than Rs.60 lakh

24%

Other cases where value of taxable service in preceding year is less than Rs.60 Lakh

12%

Other cases where value of taxable service in preceding year is more than Rs.60 Lakh

15%

*Willful default- Cases where Service Tax collected but not deposited to the credit of central government- Enactment – 14/05/2016

CHAPTER V-FINANCE ACT’94

wherein it is proposed to provide that prosecution proceedings under section 78A shall be deemed to be closed in cases where the main demand and penalty proceedings have been closed under section 76 or section 78, by making suitable changes to section 78A by addition of an explanation.(Enactment -14/05/2016)

F. Section 78A Prosecution proceedings-Explanation Inserted

G Section 89 - Offences and penaltiesThe power to arrest in Service Tax is being restricted only to situations, where the taxpayer has collected the tax but not deposited it to the credit of the central government, and that too the above a threshold of Rs.2 crore. The monetary limit for launching prosecution is being increased to Rs. 2 crore of Service Tax evasion. (Enactment -14/05/2016)

CHAPTER V-FINANCE ACT’94

In the provision of Section 90 as we have seen in above case and to wide powers of department, the Finance Minister proposed to omit sub-section 2 to Section 90. Existing sub-section to section 90 provides that an offence even if it is cognizable and bailable as per the provisions of the Code of Criminal Procedure, 1973 shall be non-cognizable and bailable if it was not cognizable as per provision of the Finance Act, 1994. (Enactment -14/05/2016)

H. Section 90 Cognizance of offences

I. Section 91 Power to ArrestNow, in cases where the assessee is collecting Service Tax above Rs. 2Cr. and not depositing it to the credit of the central government, the Pr. CCE or CCE may authorize the Central Excise Officer, not below the rank of Superintendent of Central Excise, to arrest such all person.

CHAPTER V-FINANCE ACT’94

Amendment so as to enable allowing of rebate by way of notification as well as rules.

J. Section 93 A – Power to Grant Rebate

K. Section 101New-Service Tax Exemption to Canal , Dam or Other Irrigation Work , Retrospective Amendment

-Definition of Government Authority Amended – With retrospective effect 30/01/2014

-Refund Available – Service Tax collected from 30/01/2014

-Claim – 6 Month from date of Enactment -14/05/2016

CHAPTER V-FINANCE ACT’94L. Section 102New-Restoration of Certain Exemption withdrawn last year for projects , Contracts in respect of Government Building.

Notification 06/2015 dated 1st March’ 2015 had withdrawn the exemption given to certain construction related services to Government, Local Authority or a governmental authority w.e.f. 01st April’ 2015.

The same is being restored for the services provided under a contract which had been entered into prior to 01.03.2015 and on which appropriate stamp duty, where applicable, had been paid prior to that date. The exemption is being restored till 31.03.2020. [Notification No. 25/2012-ST as amended by notification No 09/2016-ST, dated 1st March, 2016].

Refund Claim – 6 Month from date of Enactment -14/05/2016 Period 01/04/2015 to 29/02/2016

CHAPTER V-FINANCE ACT’94M. Section 103New-Restoration of Exemption from Service Tax on services by way of construction, erection, etc. of original works pertaining to an airport, port was withdrawn with effect from 1.4.2015.

Contract which had been entered into prior to 01.03.2015 and on which appropriate stamp duty, where applicable, had been paid prior to that date subject to production of certificate from the Ministry of Civil Aviation or Ministry of Shipping, as the case may be, that the contract had been entered into prior to 01.03.2015.

Refund Claim – 6 Month from date of Enactment -14/05/2016 Period 01/04/2015 to 29/02/2016

NOTIFICATION NO.25/2012-STA. Service provided by EPFO are exempt from service

tax – Sr. no 49 with effect from 01.04.2016

B. Service provided by SEBI are also exempt -Sr. no 51 with effect from 01.04.2016

C. Services of life insurance business provided by way of annuity under the National Pension System (NPS) regulated by Pension Fund Regulatory Sr. no 26 C with effect from 01.04.2016

D. Services provided by Biotechnology Industry Research Assistance Council (BIRAC) approved biotechnology incubators to the incubates are being exempted from service tax. (Amendment in Not. 32/2012 with effect from 01.04.2016)

NOTIFICATION NO.25/2012-STE. Services provided by National Centre for Cold Chain

Development under Department of Agriculture, Cooperation and Farmer‟s Welfare, Government of India, by way of knowledge dissemination are being exempted from service tax. Sr. no 52 with effect from 01.04.2016

F. Services provided by Insurance Regulatory and Development Authority (IRDA) of India are being exempted

from service tax. Sr. no 50 with effect from 01.04.2016

G. Services of general insurance business provided under „Niramaya‟ Health I nsurance scheme launched by National Trust for the Welfare of Persons with Autism, Cerebral Palsy, Mental Retardation and Multiple Disability in collaboration with private/public insurance companies are being exempted from service tax. Sr. no 26(Q )with effect

from 01.04.2016

NOTIFICATION NO.25/2012-STK. Services by way of construction, erection etc. of a civil structure

or any other original works pertaining to the “In-situ Rehabilitation of existing slum dwellers using land as a resource through private participation” component of Housing for All (HFA) (Urban) Mission / Pradhan Mantri Awas Yojana (PMAY), except in respect of such dwelling units of the projects which are not constructed for existing slum dwellers, is being exempted from service tax (Sr. no 13 (ba) w.e.f.1st March, 2016).

L. Services by way of construction, erection etc., of a civil structure or any other original works pertaining to the “Beneficiary-led individual house construction / enhancement” component of Housing for All (HFA) (Urban) Mission/ Pradhan Mantri Awas Yojana (PMAY) is being exempted from service tax (Sr. no 13 (bb) w.e.f.1st March, 2016).

NOTIFICATION NO.25/2012-STH. The threshold exemption limit of consideration charged

for services provided by a performing artist in folk or classical art forms of music, dance or theatre, is being increased from Rs 1 lakh to Rs 1.5 lakh per performance. Sr. no 16 with effect

from 01.04.2016 – (Brand Ambassador not Covered)

I. Services provided by way of skill/vocational training by Deen Dayal Upadhyay Grameen Kaushalya Yojana training partners are being exempted from service tax. Sr. no 9 (D) with effect from 01.04.2016

J. Services of assessing bodies empanelled centrally by Directorate General of Training, Ministry of Skill Development & Entrepreneurship are being exempted from service tax. . Sr. no 9 (C) with effect from 01.04.2016.

NOTIFICATION NO.25/2012-STK. Services by way of construction, erection, etc., of original works

pertaining to low cost houses up to a carpet area of 60 sq.m per house in a housing project approved by the competent authority under the “Affordable housing in partnership” component of PMAY or any housing scheme of a State Government are being exempted from service tax (Sr. no 14 (ca) w.e.f.1st March, 2016 ).

L. Services provided by the Indian Institutes of Management (IIM) by way of 2 year full time Post Graduate Programme in Management(PGPM) (other than executive development programme), admissions to which are made through Common Admission Test conducted by IIMs, 5 year Integrated Programme in Management and Fellowship Programme in Management are being exempted from service tax (Sr. no 9 (B) w.e.f. 1st March, 2016 ).

NOTIFICATION NO.25/2012-STM. Services by way of transportation of goods by an aircraft from

place outside India upto the customs station of clearance in India (Sr. no 53 (ca) w.e.f. 1st June, 2016 ). (Earlier was in Negative list)

O. Transport of Passenger ,with or without accompanied belonging by – Stage Carriage other than air conditioned stage carriage (Sr. no 23 (BB) w.e.f. 1st June, 2016 ). (Earlier was in Negative list)

P. Service Tax leviable on services of Senior Advocates Services provided by a senior advocate to an advocate or partnership firm of advocates or business entity having turnover up to Rs.10 Lakh in preceding financial year.

Services provided by a person represented on an arbitral tribunal to an arbitral tribunal;

Service Tax payable by the service provider Forward Charge (effective from 1st April 2016). (who is Senior Advocate)

ABATMENTS-NOTIFICATION NO.26/2012-STRationalization of various Abatements Effective From – 01/04/2016

SR.No

Rationalization of various Abatements

Existing Abatement-

Rate

Proposed Abatement-

Rate

1 Passenger/Goods Transportation by Rail – Abatement 70%

70% - 4.5%Without Credit

70% - 4.5%With Input Service Credit

2 Transportation of Goods in Containers by Rail

70% - 4.5%Without Credit

60% - 6.00%With Input Service Credit

3 Transportation of goods by Vessel

70% - 4.5%Without Credit

70% - 4.5%With Input Service Credit

ABATMENTS-NOTIFICATION NO.26/2012-STRationalization of various Abatements Effective From – 01/04/2016

SR.No

Rationalization of various Abatements

Existing Abatement-

Rate

Proposed Abatement-

Rate

4 Services of construction of complex, building, civil structure, or a part thereof , Intended for a sale to buyer , wholly or partly

Low EndedLess than 2000 Sqft + Amt less

than Rs.1 Crore

Low Ended –

75%- 3.5%

High Ended – 70% -/4.2%

Both Type –

70% - 4.2%

ABATMENTS-NOTIFICATION NO.26/2012-STRationalization of various Abatements Effective From – 01/04/2016

SR.No

Rationalization of various Abatements

Existing Abatement-

Rate

Proposed Abatement-

Rate

5 Abatement rate on tour operator services Package Tour (Inclusive all) & other than packaged tour

(tour operator is providing services solely of arranging or booking accommodation for any person in relation to a tour, abatement of 90% is available with specified conditions)

Package Tour(Inclusive all)- 75% - 3.75%

Other thanPackage Tour-60% - 6.00%

All Type : 70% - 4.5%

ABATMENTS-NOTIFICATION NO.26/2012-STRationalization of various Abatements Effective From – 01/04/2016

SR.No

Rationalization of various Abatements

Existing Abatement-

Rate

Proposed Abatement-

Rate

6 Abatement on transport of used household goods by a Goods Transport Agency (GTA) is being rationalized at the rate of 60% without availment of CENVAT credit on inputs, input services and capital goods by the service provider.

70%- 4.5% 60%-6.00%

7 Abatement for the service of transport of goods by vessel

70%-4.5%No Cenvat Credit

70%-4.5%Input Service is

allowed

ABATMENTS-NOTIFICATION NO.26/2012-STRationalization of various Abatements Effective From – 01/04/2016

SR.No

Rationalization of various Abatements

Existing Abatement-

Rate

Proposed Abatement-

Rate

8 Services provided by foreman to a chit fund under the Chit Funds Act, 1982 are proposed to be taxed at an abated value of 70% (with abatement of 30%) subject to the condition that CENVAT credit of inputs, input services and capital goods has not been availed.

0% - 15%

(CENVAT Credit on Input ,

Input Service &

Capital Goods)

30% - 10.50%

(No- CENVAT)

REVERSE CHARGE MECHANISMEffective From – 01/04/2016

A. No more reverse charge on services provided by Mutual fund agents

Services provided by mutual fund agents/distributor to a mutual fund or asset management company are being put under forward charge, i.e. the service provider is being made liable to pay service tax. The small sub-agents down the distribution chain will still be eligible for small service provider exemption [threshold turnover of Rs 10 lakh/year] and a very small number will be liable to pay service tax.

B. Any Service Provided by Government or Local Authority to business Entities – Liability on Recipient

REVERSE CHARGE MECHANISMEffective From – 01/04/2016

Notification No.30/2012-ST Amendment- Sr. No.6 ‘by way of supports service ‘ deleted.

B. Any Service Provided by Government or Local Authority to business Entities – Liability on Recipient

SERVICE TAX RULESEffective From – 01/04/2016

Individuals and partnership firms are given special treatment under Rule 6 of the ST Rules, who are allowed to pay tax on quarterly basis upon receipt of service proceeds (up to Rs.50 lacs turnover). This benefit has been extended to OPCs and HUFs.

A. Rule-6 One Person Company (OPC) and HUF treated on par with individuals and firms

B. Rule-7A ST on Single premium insurance policies is reduced from 3.5% to 1.4%The service tax liability on single premium annuity (insurance) policies is being rationalized and the effective alternate service tax rate (composition rate) is being prescribed at 1.4% of the total premium charged.

THE POINT OF TAXATION RULES (POTR)Effective From – 01/03/2016

Section 67A has been amended and linked with the POT Rules and thus harmony has been created. Now, it is expected to settle the disputes regarding applicability of rate of service tax. The POT Rules shall remain relevant for determining rate of service tax as well as due date of payment of tax.

A. Section 67 A Linked With POT

B. Rule-5 Invariably made applicable for New Levy & Collection of New Levy

Explanation – Inserted- K K C & S B C

ANNUAL RETURN

Effective From – 01/04/2016

A new concept of furnishing of Annual Return is proposed to be introduced in service tax. Such annual return shall be required to be filed in addition to the existing system of Half Yearly returns.

- Certain Threshold,

- Can be Revised with in One month

- Upto 30th November

Information Technology Software Effective From – 01/03/2016Chapter -85 Notified under Section 4A of the CEA

Where it is required to show RSP (retail Sale Price ) Fixed on the Package as per Legal Metrological act

Central Excise Duty / CVD –

Note Sale – Deemed Sale as per Service Tax , hence no Service tax

Where it is not required to show RSP (retail Sale Price ) Fixed on the Package as per Legal Metrological act

CVD or Central Excise exempted for the Value of Media & Information.

Service Tax will be Levied on that portion.

CVD or Central Excise will be levied on Value of medium on which it is recorded + Freight & Insurance.

Indirect Tax Dispute Resolution Scheme, 2016Effective From – 14/05/2016

The scheme is a step towards resolving litigations still pending at the initial level before the first appellate authorities.

Persons opting for the scheme will have to pay the tax along with interest and in case the matter in appeal is related to penalty imposed under the impugned order then 25% of such penal amount will have to be paid. The unique feature of the scheme is that opting under scheme and paying tax and penalty would not render the matter as being decided on merits and would not result in any binding precedent for other cases.

Detailed Scheme issued .Major Benefit- Prosecution can be avoided & Penalty can be Saved to some extent.

CENVAT CREDIT RULES , 2004Effective From – 01/04/2016A. AMENDMENTS RELATED TO CAPITAL GOODS

1) Wagons of sub heading 8606 92 included in the definition of capital goods

2) The Capital goods used in office located within factory is also eligible for CENVAT CREDIT.

3) CENVAT credit on inputs and capital goods used for pumping of water, for captive use in the factory, is being allowed even where such capital goods are installed outside the factory.

4) All capital goods having value upto Rs.10,000/- per piece are being included in the definition of inputs.

CENVAT CREDIT RULES , 2004Effective From – 01/04/2016

B. AMENDMENTS RELATED TO INPUTS SEND TO JOB WORKER

1) Manufacturer of final products is being allowed to take CENVAT credit on tools of Chapter 82 of the Central Excise Tariff in addition to credit on jigs, fixtures, moulds & dies, when intended to be used in the premises of job-worker or another manufacturer who manufactures the goods as per specification of manufacturer of final products.(Tools, implements, cutlery, spoons and forks, of base metal; parts thereof of base metal)

2) It is also being provided that a manufacturer can send jigs, fixtures, moulds & dies goods directly to such other manufacturer or job-worker without bringing the same to his premises.

3) The permission given by an Assistant Commissioner or Deputy Commissioner to a manufacturer of the final products for sending Inputs or partially processed inputs can be send outside factory to a job-worker and clearance there from on payment of duty is valid for 3 financial years.

CENVAT CREDIT RULES , 2004Effective From – 01/04/2016

C. CENVAT CREDIT ELIGIBILITY

1) Radio Frequency Spectrum, Mines etc.: CENVAT credit of Service Tax paid on amount charged for assignment by Government or any other person of a natural resource such as radio-frequency spectrum, mines etc. shall be spread over the period of time for which the rights have been assigned.

2) Where the manufacturer of goods or provider of output service further assigns such right to use assigned to him by the Government or any other person, in any financial year, to another person against a consideration, balance CENVAT credit not exceeding the service tax payable on the consideration charged by him for such further assignment, shall be allowed in the same financial year.

CENVAT CREDIT RULES , 2004Effective From – 01/04/2016

C. CENVAT CREDIT ELIGIBILITY

Infrastructure Cess: Cenvat credit cannot be utilised for payment of Infrastructure Cess. Further, no credit of this Cess would be available under the Credit Rules.

Infrastructure Cess is a levy/tax imposed by the Union Government on the production of vehicles, at the rate of 1% on small petrol, LPG, CNG (gas based) cars, 2.5% on Diesel Cars of certain capacity and 4% on other higher engine capacity vehicles and Sports Utility Vehicles (SUVs), for the purposes of financing infrastructure projects.

Infrastructure cess has come into effect from 1 March 2016.

Cess is exempted for certain motor vehicles such as three wheelers, electric vehicles, hydrogen /fuel cell based vehicles, vehicles certified to be used for physically challenged/ differently abled persons etc. Further, this is also exempted for other public utility transport vehicles like buses (which transport more than 10 persons) and cars /vehicles which are registered solely for serving as taxis or as ambulances.

CENVAT CREDIT RULES , 2004Effective From – 01/04/2016

D. AMENDMENT IN RULE – 6 (REVERSAL OF CREDIT)

Rule 6(1): The existing principle that CENVAT credit shall not be allowed on such quantity of input and input services as is used in or in relation to manufacture of exempted goods and exempted service. The procedure for calculation of credit not allowed is provided in sub-rules (2) and (3), for two different situations.

Rule 6(2): A manufacturer who exclusively manufactures exempted goods for their clearance up to the place of removal or a service provider who exclusively provides exempted services shall pay (i.e. reverse) the entire credit and effectively not be eligible for credit of any inputs and input services used.

CENVAT CREDIT RULES , 2004Effective From – 01/04/2016

D. AMENDMENT IN RULE – 6 (REVERSAL OF CREDIT)

Rule 6(3) exempted goods and final products excluding exempted goods or provides two classes of services, namely exempted services and output services excluding exempted services, then the manufacturer or the provider of the output service shall exercise One of the two options, namely,

(a) pay an amount equal to 6% of value of the exempted goods and 7% of value of the exempted services, subject to a maximum of the total credit taken or

(b) pay an amount as determined under sub-rule (3A).

CENVAT CREDIT RULES , 2004Effective From – 01/04/2016

Rule 6 (3A) : Provisionally for each month. Intimation in writing to the Superintendent of Central Excise is necessary. The four key steps for calculating the credit required to be paid are

– No credit of inputs or input services used exclusively in manufacture of exempted goods or for provision of exempted services shall be available

– Full credit of input or input services used exclusively in final products excluding exempted goods or output services excluding exempted services shall be available;– Credit left thereafter is common credit and shall be attributed towards exempted goods and exempted services by multiplying the common credit with the ratio of value of exempted goods manufactured or exempted services provided to the total turnover of exempted and non-exempted goods and exempted and non-exempted services in the previous financial year;

– Final reconciliation and adjustments are provided for after close of financial year by 30th June of the succeeding financial year, as provided in the existing rule.

CENVAT CREDIT RULES , 2004Effective From – 01/04/2016

D. AMENDMENT IN RULE – 6 (REVERSAL OF CREDIT)

New sub-rule (3AA): A manufacturer or a provider of output service who has failed to follow the procedure of giving prior intimation, may be allowed by a Central Excise officer, competent to adjudicate such case, to follow the procedure and pay the amount prescribed subject to payment of interest calculated at the rate of 15% p.a.

New sub-rule (3AB) (transitional provision) The existing rule 6 of CCR would continue to be in operation upto 30.06.2016, for the units who are required to discharge the obligation in respect of financial year 2015-16.

Rule 6(3B) Allow banks and other financial institutions to reverse credit in respect of exempted services on actual basis in addition to the option of 50% reversal.

CASE –LAWS No Service tax on sale of under construction flats

if contract price includes value of land

Suresh Kumar Bansal Vs. Union of India & Ors; Anuj Goyal & Ors Vs. Union of India & Ors [2016-TIOL-1077-HC-DEL-ST]-03/06/2016

Petitioners’ contentions:•The Agreement entered with the Builder are for purchase of immovable property and the Parliament does not have the legislative competence to levy Service tax on such transaction;

The entries relating to taxation in List I and List II of the Seventh Schedule to the Constitution of India were mutually exclusive and the Parliament did not have the power to levy tax on immovable property; thus, the levy of Service tax on agreements for purchase of flats was beyond the legislative competence of the Parliament;

CASE –LAWS No Service tax on sale of under construction flats

if contract price includes value of land

Suresh Kumar Bansal Vs. Union of India & Ors; Anuj Goyal & Ors Vs. Union of India & Ors [2016-TIOL-1077-HC-DEL-ST]-03/06/2016

Petitioners’ contentions:Their Agreement with the Builder is a composite contract for purchase of immovable property and in absence of specific provisions for ascertaining the service component of the said Agreement, the levy would be beyond the legislative competence of the Parliament;

There was no service element in preferential location charges which were levied by the Builder and the same related only to the location of the immovable property and, therefore, such charges were not exigible to Service tax.

CASE –LAWS Suresh Kumar Bansal Vs. Union of India & Ors; Anuj Goyal & Ors Vs. Union of India & Ors [2016-TIOL-1077-HC-DEL-ST]-03/06/2016

Revenue’s contention: The Revenue submitted that development of a project results in the substantial value addition on bare land and includes various services such as consulting services, engineering services, management services, architectural services etc.

These services are subsumed in the taxable service as contemplated under Section 65(105)(zzzh) of the Finance Act. The Revenue also submitted that as the gross charges include value of land and construction material, only 25% of the Base Selling Price (BSP) charged by a Builder from the ultimate consumer is subjected to levy of Service tax.However, in case of preferential location charges, the entire amount charged by a developer is for value addition and therefore, the gross amount charged for such services is chargeable to Service tax under Section 66 read with Section 65(105)(zzzzu) of the Finance Act.

CASE –LAWS Suresh Kumar Bansal Vs. Union of India & Ors; Anuj Goyal & Ors Vs. Union of India & Ors [2016-TIOL-1077-HC-DEL-ST]-03/06/2016

Held:

The Hon’ble High Court of Delhi after detailed deliberation held as under:

- No services are rendered in a contract to sell immovable property

- Imposition of Service tax in relation to a transaction between a developer of a complex and a prospective buyer does not impinges on the legislative field reserved for the States.

- No statutory machinery provision for determining the service element in Composite Contract

CASE –LAWS Held: The Hon’ble High Court of Delhi after detailed deliberation held as under:

Undisputedly, the contract between a buyer and a builder/ promoter/ developer in development and sale of a complex is a composite one. The arrangement between the buyer and the developer is not for procurement of services simplicitor;

While the legislative competence of the Parliament to tax the element of service involved cannot be disputed but the levy itself would fail, if it does not provide for a mechanism to ascertain the value of the services component which is the subject of the levy;

In the present case, there is no machinery provision for ascertaining the service element involved in the composite contract. In order to sustain the levy of Service tax on services, it is essential that the machinery provisions should provide for a mechanism for ascertaining the measure of tax, that is, the value of services which are charged to Service tax.

CASE –LAWS NO SERVICE TAX AUDIT BY THE

DEPARTMENTAL OFFICER

MEGA CABS PVT. LTD Vs. Union of India [2016-TIOL-1077-HC-DEL-ST]-03/06/2016

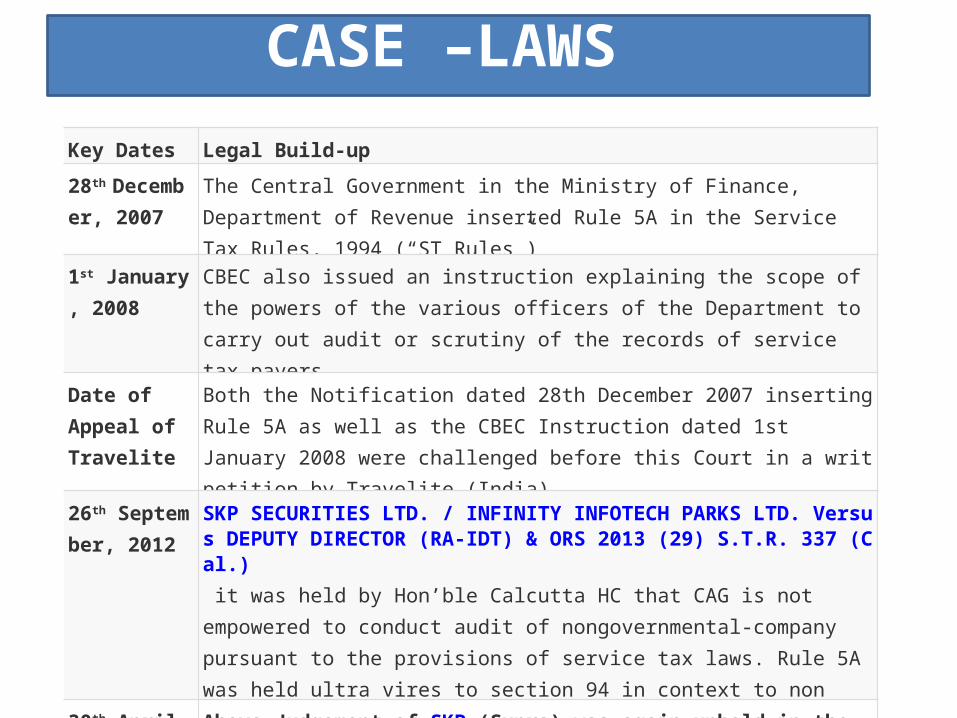

CASE –LAWS Key Dates Legal Build-up

28th December, 2007

The Central Government in the Ministry of Finance, Department of Revenue inserted Rule 5A in the Service Tax Rules, 1994 (“ST Rules”)

1st January, 2008

CBEC also issued an instruction explaining the scope of the powers of the various officers of the Department to carry out audit or scrutiny of the records of service tax payers.

Date of Appeal of Travelite

Both the Notification dated 28th December 2007 inserting Rule 5A as well as the CBEC Instruction dated 1st January 2008 were challenged before this Court in a writ petition by Travelite (India)

26th September, 2012

SKP SECURITIES LTD. / INFINITY INFOTECH PARKS LTD. Versus DEPUTY DIRECTOR (RA-IDT) & ORS 2013 (29) S.T.R. 337 (Cal.) it was held by Hon’ble Calcutta HC that CAG is not empowered to conduct audit of nongovernmental-company pursuant to the provisions of service tax laws. Rule 5A was held ultra vires to section 94 in context to non governmental company audit by CAG while referring the case to chief justice for divisional bench adjudication.

30th April, 2014

Above Judgement of SKP (Supra) was again upheld in the case of INFINITY INFOTECH PARKS LTD. Versus UNION OF INDIA 2014 (36) S.T.R. 37 (Cal.)

CASE –LAWS Key Dates Legal Build-up

4th August, 2014

Travelite (India) v. Union of India 2014 (35) STR 653 (Delhi), a Division Bench of this Court struck down Rule 5A(2) as being ultra vires Section 72A read with Section 94(2) of the FA. The consequent Circular of CBEC Instruction dated 1st January 2008 was also struck down. It was clarified that Service Tax Audit Manual, 2011 was merely an instrument of instructions for the Service Tax authorities and has no statutory force

6th August, 2014

94(2)(k) was inserted vide Finance Act, 2014

5th December, 2014

New Rule 5A(2) Substituted

10th December, 2014

Circular No. 181/7/2014-ST was issued by the CBEC clarifying that in view of the insertion of Section 94(2)(k), the officers of the Service Tax Departments could proceed with conducting audits as before. It was stated that that expression ‘verified’ used in Section 94(2)(k) of the FA was of wide import and would include within its scope audit by the departmental officers.

CASE –LAWS Key Dates Legal Build-up

18th December, 2014

Special Leave Petition No. 34872/2014 was filed in the Supreme Court by the Union of India vide order of the Supreme Court while directing notice in the said Special Leave Petition directed that there would be a stay of the operation of the decision of this Court in Travelite (India) v. Union of India (supra)

27th February, 2015

Circular No. 995/2/2015-CX was issued by the CBEC on the subject “Central Excise and Service Tax Audit norms to be followed by the Audit Commissionerates” and this too contemplated the Department’s officers themselves undertaking audits. A Central Excise and Service Tax Audit Manual, 2015 was also issued by the Directorate General of Audit of the CBEC in this regard.

3rd June, 2016

Delhi HC Again Strikes Down (In the Present Case) the Amended Rule 5A (2) to the extent of Department’s authority to Conduct ‘Audit’ of Assessees registered under Service Tax.

CASE –LAWS

Section 94(2)(k) of the FA,1994

“94. Power to make rules.-(1) The Central Government may, by notification in the Official Gazette, make rules for carrying out the provisions of this Chapter.

(2) In particular, and without prejudice to the generality of the foregoing power, such rules may provide for all or any of the following matters, namely (k) “imposition, on persons liable to pay service tax, for the proper levy and collection of tax, of duty of furnishing information, keeping records and the manner in which such records shall be verified”

CASE –LAWS

Rule 5A. (2) Every assessee, shall, on demand make available to the officer empowered under sub-rule (1) or the audit party deputed by the Commissioner or the Comptroller and Auditor General of India, or a cost accountant or chartered accountant nominated under section 72A of the Finance Act, 1994,–(i) the records maintained or prepared by him in terms of sub-rule (2) of rule 5;(ii) the cost audit reports, if any, under section 148 of the Companies Act, 2013 (18 of 2013); and(iii) the income-tax audit report, if any, under section 44AB of the Income-tax Act, 1961 (43 of 1961),

for the scrutiny of the officer or the audit party, or the cost accountant or chartered accountant, within the time limit specified by the said officer or the audit party or the cost accountant or chartered accountant, as the case may be

CASE –LAWS

Held by Hon’ble Delhi HC

Rule 5A(2) is ultra vires to the FA and, therefore, strikes it down to that extent;

Expression ‘verify’ in Section 94(2)(k) of the FA cannot be construed as audit of the accounts of an Assessee and, therefore, Rule 5A(2) cannot be sustained with reference to Section 94(2)(k) of the FA.

CA . RAMANDEEP SINGH BHATIA

Qualifications :

FCA, CS (EXE) , BCOM,CERT. IFRS, CERT. IDT, CERT. CBA, DISA

Associated to:

-Trainer ICAI Raipur- GMCS/OTC/ITT- Trainer MCA Investor Awareness Program- Editor Newsletter Income Tax Bar Association Raipur- Vice President (Training) – JCI Raipur Capital- Executive Member of Governing Board of CG IDT Association

+919827152729 [email protected]

facebook.com/caramandeep.bhatiaTwitter/caramandeep

![Cenvat Accounting[1]](https://img.pdfslide.us/doc/110x75/54193e3a7bef0a05088b4642/cenvat-accounting1.jpg)