Embed Size (px)

Citation preview

1

Recent Issues in Service Tax,

CENVAT & VAT

Jayraj S. Sheth

16 October 2014

3

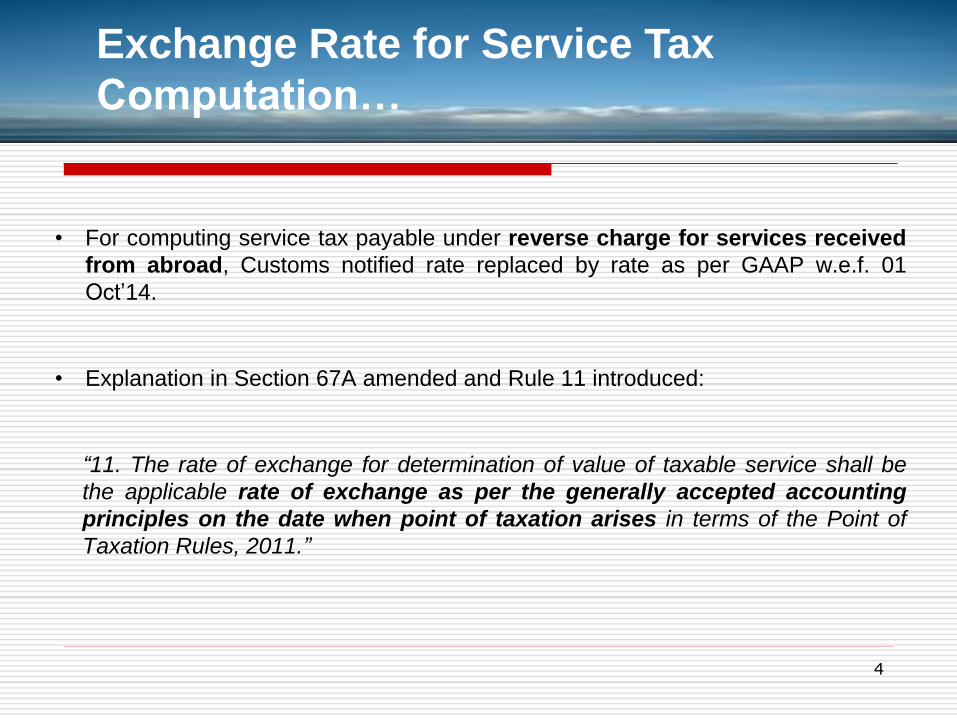

Exchange Rate for Service

Tax Computation

• For computing service tax payable under reverse charge for services received

from abroad, Customs notified rate replaced by rate as per GAAP w.e.f. 01

Oct‟14.

• Explanation in Section 67A amended and Rule 11 introduced:

“11. The rate of exchange for determination of value of taxable service shall be

the applicable rate of exchange as per the generally accepted accounting

principles on the date when point of taxation arises in terms of the Point of

Taxation Rules, 2011.”

4

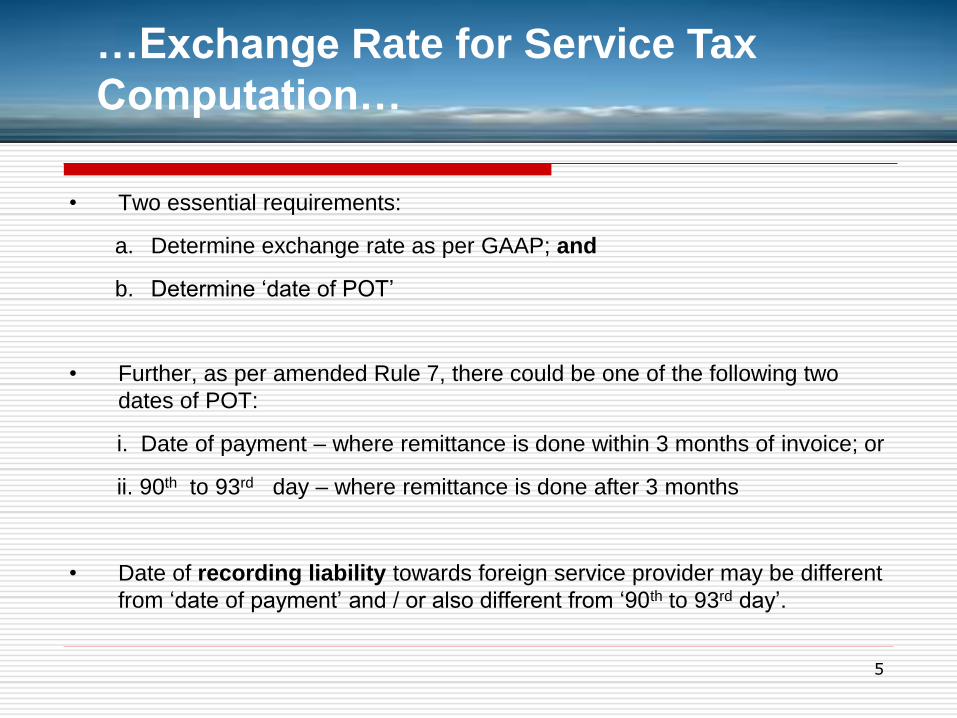

Exchange Rate for Service Tax

Computation…

• Two essential requirements:

a. Determine exchange rate as per GAAP; and

b. Determine „date of POT‟

• Further, as per amended Rule 7, there could be one of the following two

dates of POT:

i. Date of payment – where remittance is done within 3 months of invoice; or

ii. 90th to 93rd day – where remittance is done after 3 months

• Date of recording liability towards foreign service provider may be different

from „date of payment‟ and / or also different from „90th to 93rd day‟.

5

…Exchange Rate for Service Tax

Computation…

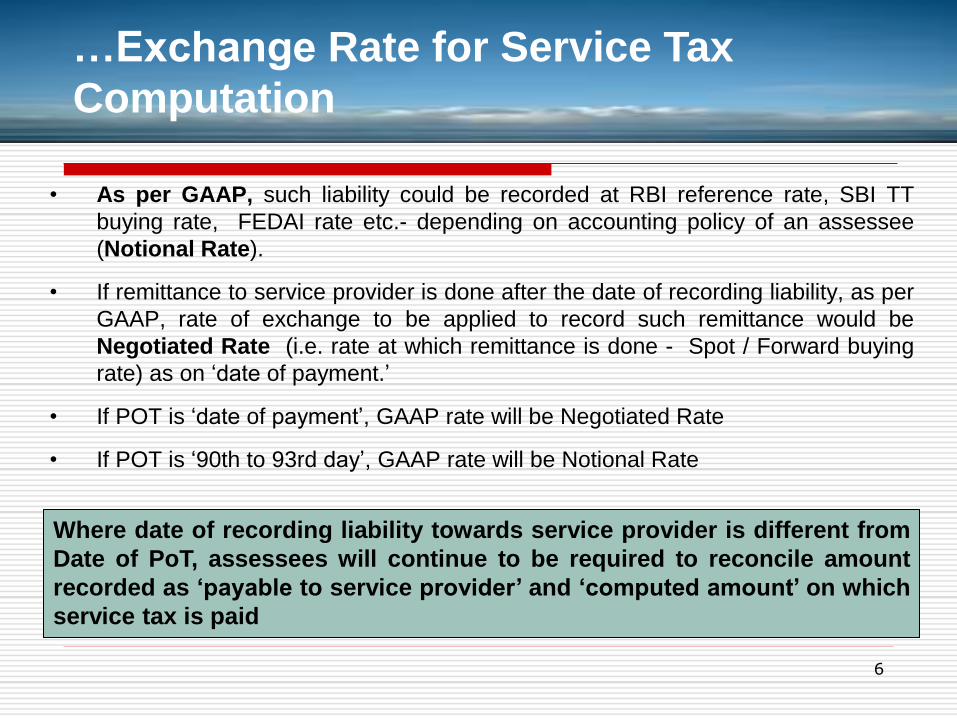

• As per GAAP, such liability could be recorded at RBI reference rate, SBI TT

buying rate, FEDAI rate etc.- depending on accounting policy of an assessee

(Notional Rate).

• If remittance to service provider is done after the date of recording liability, as per

GAAP, rate of exchange to be applied to record such remittance would be

Negotiated Rate (i.e. rate at which remittance is done - Spot / Forward buying

rate) as on „date of payment.‟

• If POT is „date of payment‟, GAAP rate will be Negotiated Rate

• If POT is „90th to 93rd day‟, GAAP rate will be Notional Rate

6

…Exchange Rate for Service Tax

Computation

Where date of recording liability towards service provider is different from

Date of PoT, assessees will continue to be required to reconcile amount

recorded as „payable to service provider‟ and „computed amount‟ on which

service tax is paid

7

Remittance from HO in India

to Overseas Branch

• Overseas Branch and HO in India are „deemed‟ to be „distinct persons‟ –

Explanation 3(b) read with Explanation 4 to Section 65B(44)

• Overseas Branch receives remittances from HO to meet local expenses for

goods and services consumed abroad

• Overseas Branch may be a mere „representative‟ or „liaison‟ office not

conducting any substantial business abroad

• „Service‟ is defined as “any activity carried out by a person for another for

consideration….”

• Valuation Section 67 refers to „gross amount charged by the service

provider‟ and defines „consideration‟ to include “any amount that is payable

for the taxable services provided….”

8

Remittance from HO in India to Overseas

Branch…

• Issue:

− Is deeming fiction of Section 65B(44) to be extended to further „deem‟

such remittances as „consideration‟ for representational / liaison activities

done by Overseas Branch for HO; and

− Therefore, attracting service tax under reverse charge for HO?

(Even if there is no formal arrangement between them, of Overseas

Branch being a „service provider‟ of the HO as a „service receiver‟?)

9

…Remittance from HO in India to Overseas

Branch…

Possible to argue that there is no „deemed service‟ by Branch to HO and

therefore, no service tax is applicable on remittances to Branch

• In Para 2.4.2 of Education Guide, while explaining the above deeming fiction,

CBEC has clarified that:

“…Implications of these deeming provisions are that inter-se provision of

services between such persons, deemed to be separate persons, would be

taxable.………”

Thus, there ought to be provision of „services‟ (as defined) by the Branch to HO:

- as is generally the case between a „service provider‟ and a „service receiver;

and

- which is ordinarily demonstrated through an oral / written arrangement

entered into for a „consideration‟.

10

…Remittance from HO in India to Overseas

Branch…

11

• In CIT v. Amarchand N. Shroff [(1963) 48 ITR 59 (SC)] and in CIT v. Vadilal

Lallubhai [(1972) 86 ITR 2 (SC)] Supreme Court has held that a deeming

fiction in a taxing law should be carried only up to the extent for which it is

created and that it cannot be extended beyond the purpose for which it is

created.

• Reliance can also be placed on Circular No. 163 (dated 10th July 2012) issued

by CBEC in the context of negative list covering “transactions in money”

arising from inward remittances to India from overseras, where it is clarified

that:

“…there is no service tax per se on the amount of foreign currency remitted to

India from overseas. In the negative list regime, „service‟ has been defined in

clause (44) of section 65B of the Finance Act 1994, as amended, which

excludes transaction in money. As the amount of remittance comprises

money, the activity does not comprise a „service‟ and thus not subjected to

service tax”.

…Remittance from HO in India to Overseas

Branch…

12

• This view is reiterated by CBEC in recent Circular No. 180 (dated 14

October 2014) – “money does not constitute a service”

• Also, recently, in Circular No. 179 (dated 24 Sept ‟14), in the context of Joint

Ventures, CBEC has clarified:

“… cash calls are capital contributions made by the members of JV to the

JV. If cash calls are merely a transaction in money, they are excluded from

the definition of service provided in section 65B(44) of the Finance Act,

1994. Whether a „cash call‟ is „merely… a transaction in money‟ [in terms of

section 65B(44) of the Finance Act, 1994] and hence not in the nature of

consideration for taxable service, would depend on the terms of the

Joint Venture Agreement, which may vary from case to case.”

…Remittance from HO in India to Overseas

Branch…

13

• Support can also be drawn from the following recent CESTAT rulings, though

they were stay matters relating to pre-negative list regime:

− Infosys BPO Ltd. v. CST [2014-TIOL-1847-CESTAT-BANG ]

− Hetero Drugs Ltd. v. CCE [2014-TIOL-1896-CESTAT-BANG]

…Remittance from HO in India to Overseas

Branch

Clarification from CBEC can help avoid possible disputes / hardships

14

Use of Digital Signature for

Excise and Service Tax

Invoices

15

• Manufacturers / service providers are reluctant to issue digitally signed invoices due

to risk of CENVAT credit not being allowed to buyer / service receiver – physical

signature is still resorted to by most of the assessees

• Section 5 of Information Technology Act, 2000 has a non obstante clause allowing

issuance of digitally signed documents overriding every other law so far as it relates

to authentication by affixing „signature‟ of any person:

“Where any law provides that information or any other matter shall be authenticated

by affixing the signature or any document shall be signed or bear the signature of any

person then, notwithstanding anything contained in such law, such requirement

shall be deemed to have been satisfied, if such information or matter is authenticated

by means of digital signature affixed in such manner as may be prescribed by the

Central Government.”

Use of Digital Signature for Excise and

Service Tax Invoices…

16

“Explanation.-For the purposes of this section, "signed", with its grammatical

variations and cognate expressions, shall, with reference to a person, mean

affixing of his hand written signature or any mark on any document and the

expression "signature" shall be construed accordingly.”

• CBDT has issued a Circular (No. 2/2007 dated 21 May 2007) allowing the tax

deductors to use their digital signatures for the purpose of authenticating

TDS certificates and in practice, TDS credit is also being allowed based on

such TDS certificates (albeit, because the field officers have the ability to

cross check on-line the TDS credits claimed with the TDS Returns filed by

the deductors through Form 26AS)

…Use of Digital Signature for Excise and

Service Tax Invoices…

17

• VAT authorities in Maharashtra and Gujarat have also made provisions /

issued dispensations allowing dealers to issue digitally signed :

- invoices, based on which VAT credit is availed by buyers; and

- C Forms

• Study Group headed by Sh. M. K. Gupta for making recommendations on

CENVAT Credit Scheme has also recommended in its Report issued in 2012

that e-invoices should be declared as eligible documents for allowing

CENVAT Credit in case of services.

…Use of Digital Signature for Excise and

Service Tax Invoices

In „Digital India‟, CBEC should expeditiously issue necessary guidance permitting CENAT credit based on digitally signed invoices – this will save enormous amount of time, efforts and resources for the entire economy

18

Re-introduction of service

tax on specified „sale of

space for advertisements‟

19

• From 1 July`12, „sale of space or time slots for advertisements‟ like the

following, were excluded from purview of service tax through negative list entry

(g) in Section 66D :

− Bill boards, public places, buildings, conveyance

− Film screens in theatres

− Tickets / invoices

− Cell phones

− ATM

− Internet

− Arial advertising

• From 1 Oct ‟14, these have been once again brought into service tax net by

amending negative list entry (g) as under:

− “selling of space or time slots for advertisements in print media other than

advertisements broadcast by radio or television”

Re-introduction of service tax on specified

„sale of space for advertisements‟…

20

• Now „sale of space for advertisements in print media‟ only are outside the purview

of service tax

• Entry 55 of List II of Seventh Schedule to the Constitution gives power only

to States to levy “Taxes on (all types of) advertisements other than

advertisements published in the newspapers and advertisements broadcast

by radio or television‟

• Entry 92 of List I gives power to Centre to levy “Taxes on the sale or

purchase of newspapers and on advertisements published therein‟”

20

…Reintroduction of service tax on

specified „sale of space for advertisements‟

Centre has encroached on the power of States – Why have States or

industry not yet raised this issue?

21

Service tax on Joint Venture

arrangements

• CBEC has recently issued Circular No. 179 dated 24 September 2014 clarifying

various issues concerning JV arrangements

• Circular appears to cover unincorporated temporary associations like the following:

- consortium

- association of persons

- production sharing arrangements

• It does not appear to cover formal JVs where a separate company or partnership

firm or LLP is formed by the JV partners

• Explanation 3(a) of the definition of „service‟ in Section 65B (44) provides that “an

unincorporated association or a body of persons, as the case may be, and a

member thereof shall be treated as distinct persons”

Service tax on Joint Venture arrangements…

22

• „Cash calls‟ (i.e. „capital contributions‟) which are merely „transactions in money‟, do

not attract service tax

• Terms of JV arrangement will determine whether „cash calls‟ are merely

„transactions in money‟ or not

• Circular gives some illustrations of cash calls which can attract service tax:

- Advance payment by members towards taxable services to be provided by JV to

the members e.g. granting of right, reserving production capacity, providing an

option on future supplies

- Payments made by JV (out of cash calls) towards taxable services received from

a member or a third party

…Service tax on Joint Venture arrangements…

23

- Consideration (in cash or in kind) received by a member from the JV for managing

cash calls pursuant to a contractual agreement

- Support / administrative services (e.g. setting up or management of project / site

office) provided by a member to the JV for consideration (in cash or in kind)

• Case by case examination required by field formations to examine applicability of

service tax on transactions a) inter se the members; and b) between the members

and the JV

…Service tax on Joint Venture arrangements

24

Several issues likely to arise for existing JV arrangements

26

• Following proviso inserted in Rule 4(1) and Rule 4(7) of CCR w.e.f. from

1 September 2014:

“Provided also that the manufacturer or the provider of output service shall

not take CENVAT credit after six months of the date of issue of any of the

documents specified in sub-rule (1) of rule 9”

• Six month time limit now applicable for availing credit on inputs as well as

input services – but not on capital goods

26

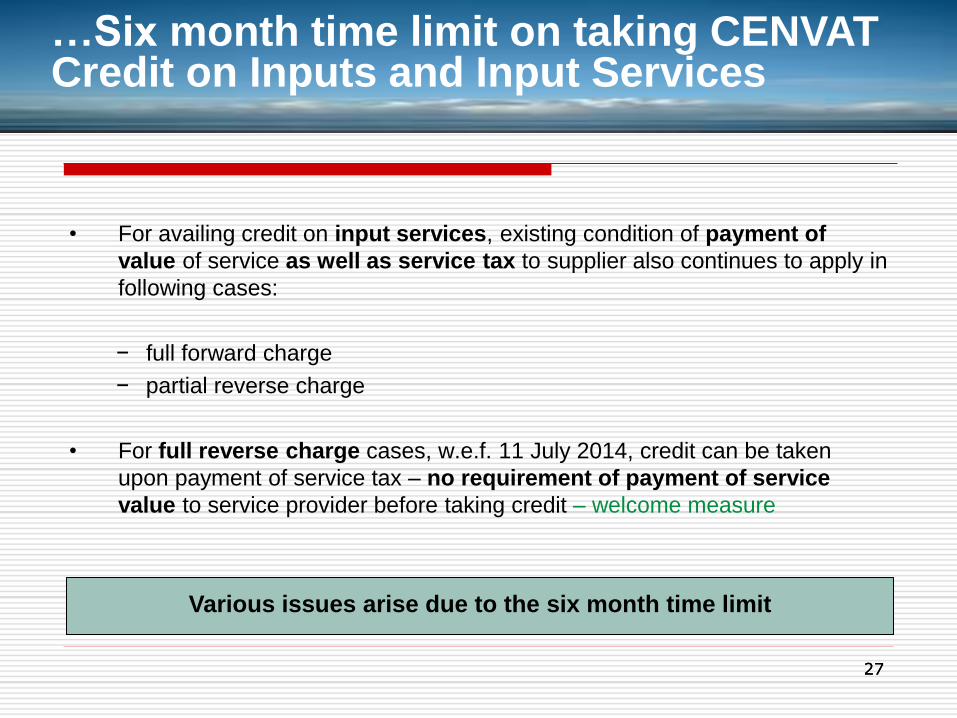

Six month time limit on taking CENVAT Credit on Inputs and Input Services…

27

• For availing credit on input services, existing condition of payment of

value of service as well as service tax to supplier also continues to apply in

following cases:

− full forward charge

− partial reverse charge

• For full reverse charge cases, w.e.f. 11 July 2014, credit can be taken

upon payment of service tax – no requirement of payment of service

value to service provider before taking credit – welcome measure

27

…Six month time limit on taking CENVAT Credit on Inputs and Input Services

Various issues arise due to the six month time limit

28

Issues arising for CENAT

credit on Inputs

29

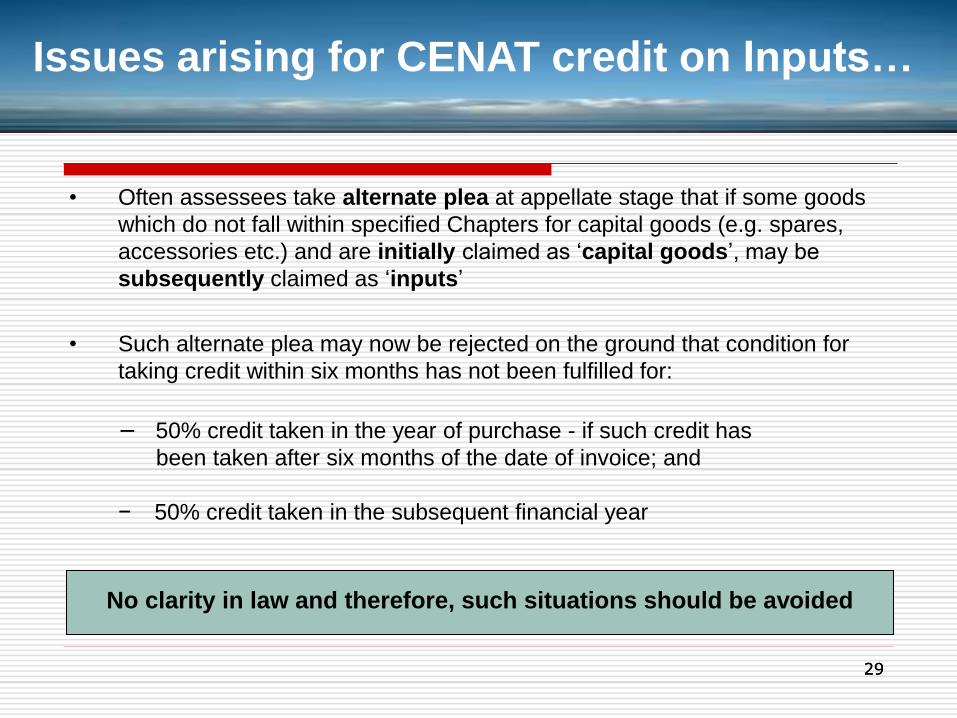

• Often assessees take alternate plea at appellate stage that if some goods

which do not fall within specified Chapters for capital goods (e.g. spares,

accessories etc.) and are initially claimed as „capital goods‟, may be

subsequently claimed as „inputs‟

• Such alternate plea may now be rejected on the ground that condition for

taking credit within six months has not been fulfilled for:

− 50% credit taken in the year of purchase - if such credit has

been taken after six months of the date of invoice; and

− 50% credit taken in the subsequent financial year

29

Issues arising for CENAT credit on Inputs…

No clarity in law and therefore, such situations should be avoided

30

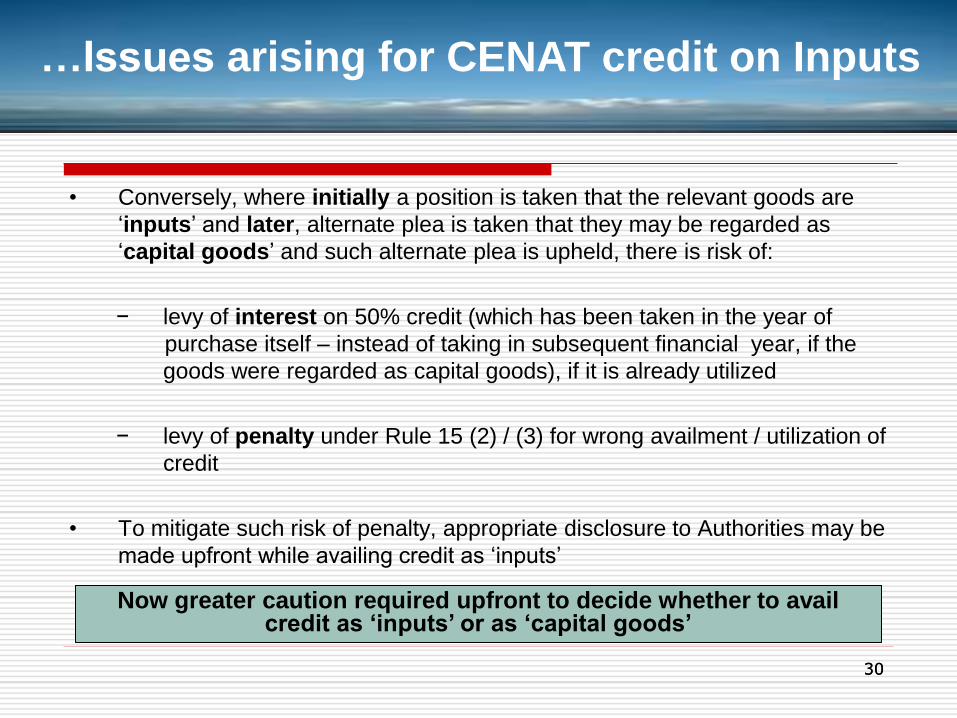

• Conversely, where initially a position is taken that the relevant goods are

„inputs‟ and later, alternate plea is taken that they may be regarded as

„capital goods‟ and such alternate plea is upheld, there is risk of:

− levy of interest on 50% credit (which has been taken in the year of

purchase itself – instead of taking in subsequent financial year, if the

goods were regarded as capital goods), if it is already utilized

− levy of penalty under Rule 15 (2) / (3) for wrong availment / utilization of

credit

• To mitigate such risk of penalty, appropriate disclosure to Authorities may be

made upfront while availing credit as „inputs‟

30

…Issues arising for CENAT credit on Inputs

Now greater caution required upfront to decide whether to avail credit as „inputs‟ or as „capital goods‟

31

Issues arising for CENVAT

credit on Input Services

32

• Hardship likely to be caused to service recipients who are allowed genuine

credit / deferred payment option by service providers for making payment

beyond six months of date of invoice due to twin condition of:

a. payment to service provider; and

b. time limit of six months (from date of invoice)

for availing CENVAT credit

• In such cases, as provided in Rule 4(7), one approach could be as under:

− take credit upon receipt of invoice;

− reverse such credit at the end of three months of the date of invoice (third

proviso)

− re-instate the reversed credit as and when payment is made to the vendor

32

Issues arising for CENVAT credit on Input Services…

In the interest of trade / industry, CBEC should clarify that such re-instatement of reversed credit is not governed by six month time limit

33

• Invoices for supply of excisable goods are sent along with the goods and

therefore, buyers of goods may not encounter difficulty in availing CENVAT

credit within six months of date of invoice

• Service providers will now be required to send their invoices to service

recipients promptly after issuance, to enable them to adhere to six month

time limit

• Businesses need to re-visit their current verification processes for service

invoices, including in particular, the following, to ensure taking of credit

within six months of dates of invoices:

− Certification of receipt of services

− Settling disputes with service providers with regard to quality / quantity of

service

− Removal of defects in invoices by service providers

33

…Issues arising for CENVAT credit on Input Services…

34

• Hardship likely to be caused to service recipients partially liable under

reverse charge due to second proviso to Rule 4(7) now providing as under:

“Provided further that in respect of an input service, where the service

recipient is liable to pay a part of service tax and the service provider is liable

to pay the remaining part, the CENVAT credit in respect of such input

service shall be allowed on or after the day on which payment is made of

the value of input service and the service tax paid or payable as indicated

in invoice, bill or, as the case may be, challan referred to in rule 9.”

• Thus, in such cases, to take credit, not only service tax is required to be paid, but

value of service is also required to be paid – unlike in case of full reverse charge

34

…Issues arising for CENVAT credit on Input Services…

35

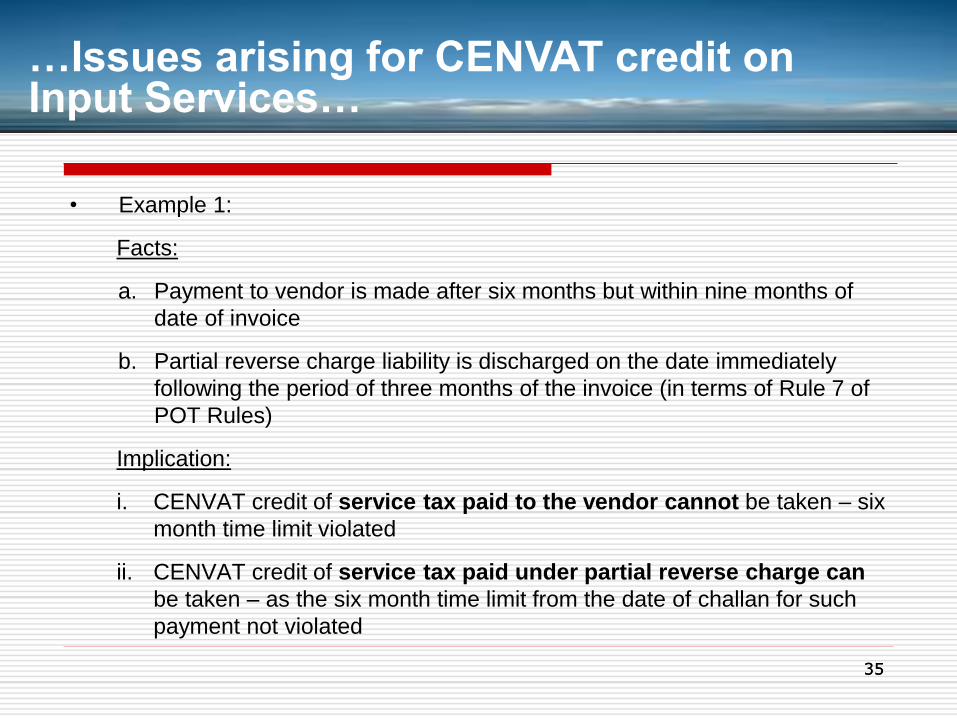

• Example 1:

Facts:

a. Payment to vendor is made after six months but within nine months of

date of invoice

b. Partial reverse charge liability is discharged on the date immediately

following the period of three months of the invoice (in terms of Rule 7 of

POT Rules)

Implication:

i. CENVAT credit of service tax paid to the vendor cannot be taken – six

month time limit violated

ii. CENVAT credit of service tax paid under partial reverse charge can

be taken – as the six month time limit from the date of challan for such

payment not violated

35

…Issues arising for CENVAT credit on Input Services…

36

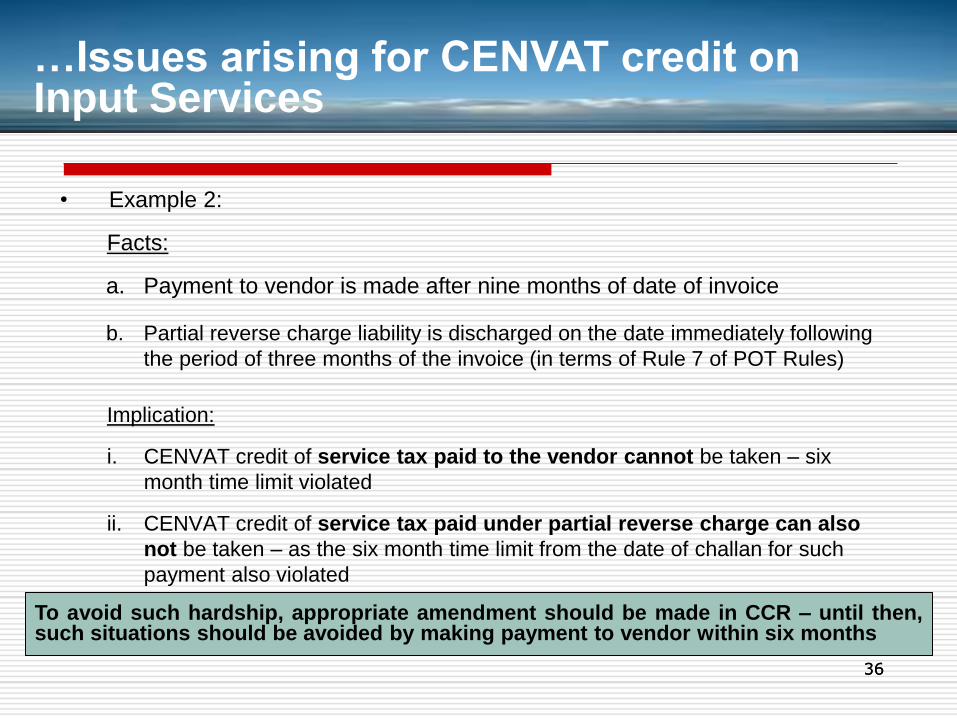

• Example 2:

Facts:

a. Payment to vendor is made after nine months of date of invoice

b. Partial reverse charge liability is discharged on the date immediately following

the period of three months of the invoice (in terms of Rule 7 of POT Rules)

Implication:

i. CENVAT credit of service tax paid to the vendor cannot be taken – six

month time limit violated

ii. CENVAT credit of service tax paid under partial reverse charge can also

not be taken – as the six month time limit from the date of challan for such

payment also violated

36

…Issues arising for CENVAT credit on Input Services

To avoid such hardship, appropriate amendment should be made in CCR – until then, such situations should be avoided by making payment to vendor within six months

37

Removal of scrap or waste

of used capital goods

by service provider

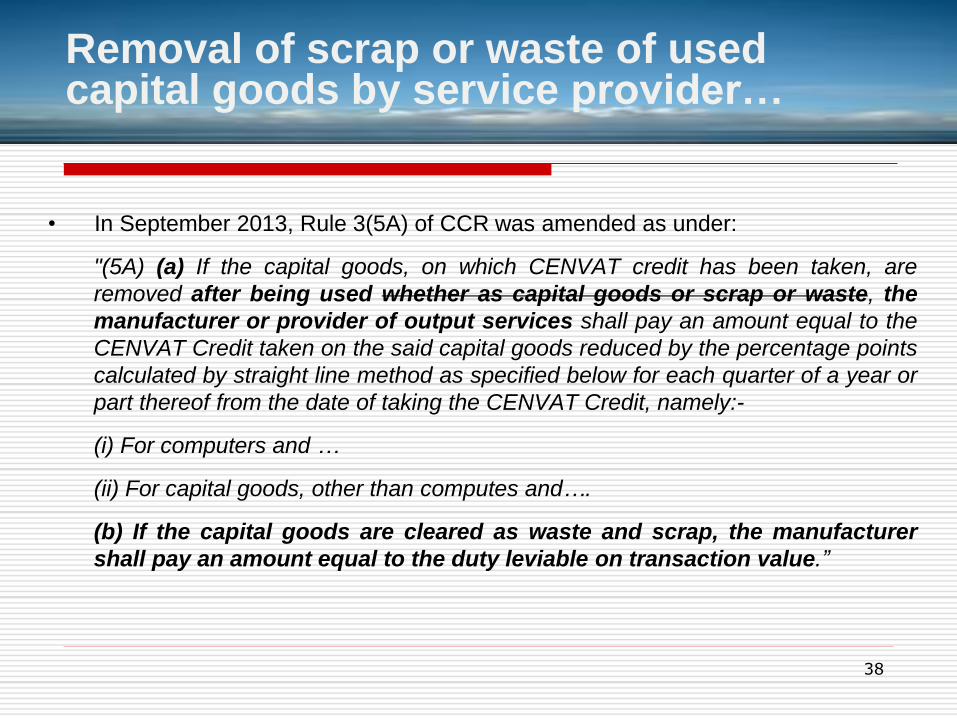

• In September 2013, Rule 3(5A) of CCR was amended as under:

"(5A) (a) If the capital goods, on which CENVAT credit has been taken, are

removed after being used whether as capital goods or scrap or waste, the

manufacturer or provider of output services shall pay an amount equal to the

CENVAT Credit taken on the said capital goods reduced by the percentage points

calculated by straight line method as specified below for each quarter of a year or

part thereof from the date of taking the CENVAT Credit, namely:-

(i) For computers and …

(ii) For capital goods, other than computes and….

(b) If the capital goods are cleared as waste and scrap, the manufacturer

shall pay an amount equal to the duty leviable on transaction value.”

Removal of scrap or waste of used capital goods by service provider…

38

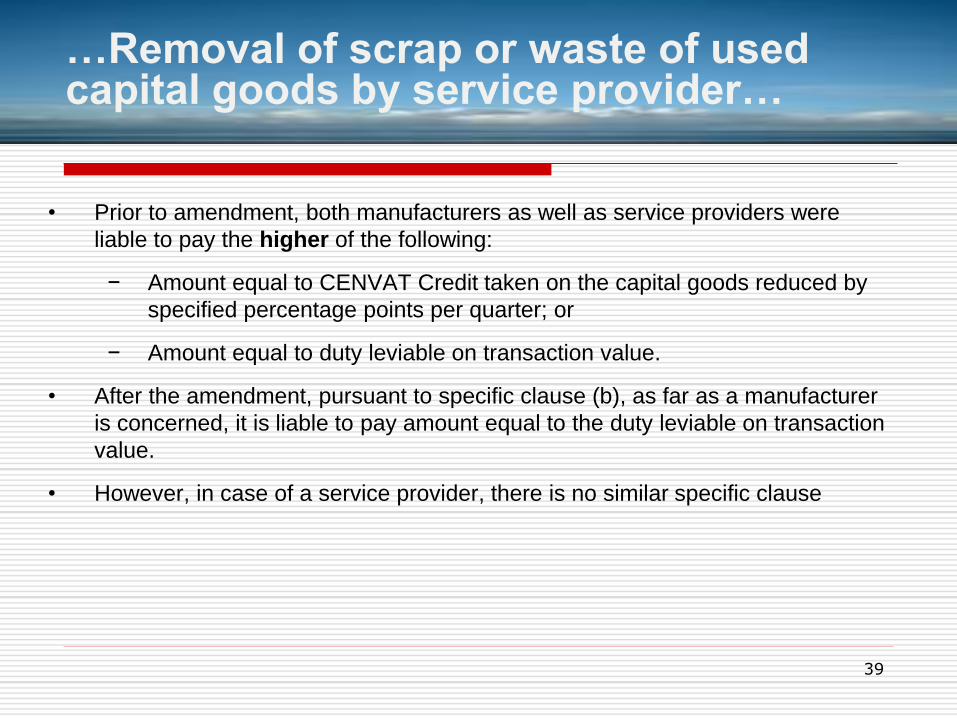

• Prior to amendment, both manufacturers as well as service providers were

liable to pay the higher of the following:

− Amount equal to CENVAT Credit taken on the capital goods reduced by

specified percentage points per quarter; or

− Amount equal to duty leviable on transaction value.

• After the amendment, pursuant to specific clause (b), as far as a manufacturer

is concerned, it is liable to pay amount equal to the duty leviable on transaction

value.

• However, in case of a service provider, there is no similar specific clause

…Removal of scrap or waste of used capital goods by service provider…

39

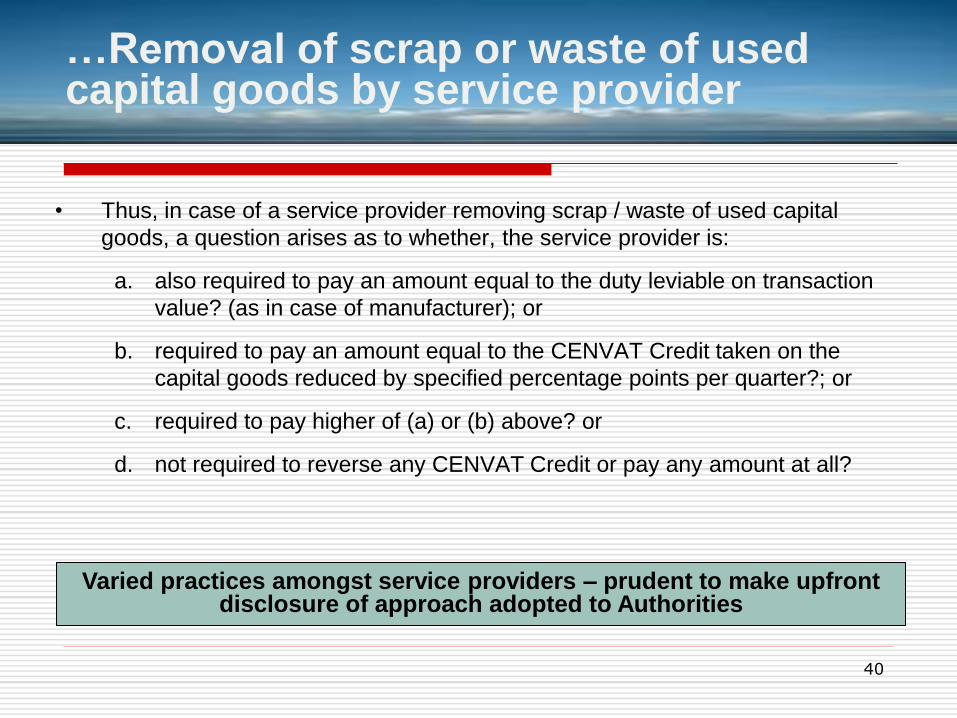

• Thus, in case of a service provider removing scrap / waste of used capital

goods, a question arises as to whether, the service provider is:

a. also required to pay an amount equal to the duty leviable on transaction

value? (as in case of manufacturer); or

b. required to pay an amount equal to the CENVAT Credit taken on the

capital goods reduced by specified percentage points per quarter?; or

c. required to pay higher of (a) or (b) above? or

d. not required to reverse any CENVAT Credit or pay any amount at all?

…Removal of scrap or waste of used capital goods by service provider

40

Varied practices amongst service providers – prudent to make upfront disclosure of approach adopted to Authorities

41

Loss of CENVAT credit for

service providers

whose services attract

full reverse charge

• Rule 3(1) of CCR allows only a provider of output service (or manufacturer) to

take credit of excise duty and service tax paid

• Rule 2(p) defines „output service‟ to exclude a service „where the whole of the

service tax is liable to be paid by the recipient of service‟ (i.e. reverse charge)

• In various cases, including in particular the following, whole of service tax is

payable by recipient of service:

− Sponsorship service

− Legal service of individual advocate or firm of advocate to business entity

− Insurance agents

Loss of CENVAT credit for service providers whose services attract full reverse charge…

42

• Thus, services provided by these service providers do not quality as „output

service‟ and therefore, they are not eligible to take credit of excise duty or service

tax paid by them on their procurement of goods and services to carry out their

activities / businesses

• Hence, such irrecoverable excise duty and service tax becomes their sunk cost,

thereby making their services more expensive for the recipients of such services

• At least in case of organized service providers like:

- persons providing sponsorship services for sports events, award functions etc.

- law firms

- corporate insurance agents

Government should consider giving them an option to pay service tax under

forward charge so as to be able to avail CENVAT credit or allow them to claim

refund of excise duty and service tax paid on their procurements

…Loss of CENVAT credit for service providers whose services attract full reverse charge

43

44

Telecom towers whether

„capital goods‟ or

„inputs‟?

• Bombay HC in the case of Bharti Airtel Ltd. [2014-TIOL-1452-HC-MUM-ST] (judgement

dated 26 August 2014) has recently held that telecom towers installed by a telecom

operator are neither „capital goods‟ nor „inputs‟ and therefore, CENVAT credit is not

allowable on these items

• Bombay HC upheld the order of Mumbai CESTAT [2012-TIOL-209-CESTAT-MUM]

disallowing such CENVAT credit to Bharti Airtel

• However, Mumbai CESTAT in the case of GTL Infrastructure Ltd. [2014-TIOL-1768-

CESTAT-MUM] (judgment dated 22 August 2014) has held that telecom towers

installed by Tower Company (i.e. Infrastructure Provider) which provides services

using these towers to telecom operators, are „inputs‟ and therefore, CENVAT credit

is allowable on them

Telecom towers whether „capital goods‟ or „inputs‟?...

45

• GTL Infra judgement was delivered:

- before aforesaid decision was delivered by Bombay HC in the case of Bharti Airtel

- after considering Mumbai CESAT decision in Bharti Airtel‟s case and it has

distinguished GTL‟s case involving provision of „business auxiliary service‟ from

provision of „telecommunication service‟ by Bharati Airtel

• In Bharti Airtel‟s case, Bombay HC did not consider telecom towers as „capital goods‟

or „inputs‟ primarily on the following grounds:

- telecom towers are immovable

- they are not „accessories‟ of antenna, BTS equipment etc. as they can function

without towers

- towers are not integral part of the output service viz. telecommunication service

- towers are not „directly used‟ for providing the output service

…Telecom towers whether „capital goods‟ or „inputs‟?

46

Is Bombay HC judgment laying down correct position in law?

Uncertainty and litigation will continue for all telecom operators till SC gives final verdict

• Two recent landmark rulings of SC in the area of Works Contracts :

− L & T v. State of Karnataka [2013-TIOL-46-SC-CT-LB]

− Kone Elevator India Pvt. Ltd. v. State of Tamil Nadu & Others [2014-TIOL-57-SC-

CT-CB]

• Some of the key takeaways from L & T‟s ruling:

− Decision of Larger Bench comprising three judges

− Division Bench of SC had referred this matter to this Larger Bench [2008-TIOL-

186-SC-CT]

− Upheld SC‟s earlier ruling in case of Raheja Development Corporation [2005-

TIOL-77- SC-CT]

Whether “Dominant nature / intention test” is still relevant?

48

- The Larger Bench, inter alia, held that:

i. contracts for under construction buildings are „works contracts‟ liable to VAT

ii. “building contracts are species of the works contract”

iii. “dominant nature test” has no application where transactions are of the

nature contemplated in Article 366(29A):

“Even if the dominant intention of the contract is not to transfer the property in

goods and rather it is rendering of service or the ultimate transaction is

transfer of immovable property, then also it is open to the States to levy sales

tax on the materials used in such contract if such contract otherwise has

elements of works contract” (Para 101)

− However, SC has not explicitly explained as to what is a „works contract‟ per se

…Whether “Dominant nature / intention test” is still relevant?...

49

• Some of the key takeaways from Kone Elevator‟s ruling:

− Decision of Constitution Bench comprising five judges

− Larger Bench (comprising three judges) of SC had referred this matter to

this Constitution Bench [(2010) 14 SCC 788]

− Overruled SC‟s Larger Bench (comprising three judges) ruling in State of

A.P. v. Kone Elevators (India) Ltd. [2005-TIOL-30-SC-CT-LB] holding that

contract for manufacture, supply and installation of lifts in a building is a

contract for „sale of goods‟ and not a „works contract‟

− Majority judgment of four judges held that such a contract is a „works

contract‟ and not a contract for „sale of goods‟

− Dissenting judgment delivered by Justice Kalifulla

…Whether “Dominant nature / intention test” is still relevant?...

50

− Majority judges also held that:

“the dominant nature test" or "overwhelming component test" or "the degree of

labour and service test" are really not applicable. If the contract is a composite

one which falls under the definition of works contracts as engrafted

under clause (29A)(b) of Article 366 of the Constitution, the incidental part

as regards labour and service pales into total insignificance for the purpose of

determining the nature of the contract.” (Para 63)

− However, in this case too, SC has not explicitly explained as to what is a

„works contract‟ per se

…Whether “Dominant nature / intention test” is still relevant?...

51

• Article 366(29A) defines “tax on the sale or purchase of goods” to include the

following:

a. a tax on the transfer, otherwise than in pursuance of a contract, of property in

any goods for cash, deferred payment or other valuable consideration;

b. a tax on the transfer of property in goods (whether as goods or in some

other form) involved in the execution of a works contract;

c. a tax on the delivery of goods on hire purchase or any system of payment by

instalments;

d. a tax on the transfer of the right to use any goods for any purpose (whether or

not for a specified period) for cash, deferred payment or other valuable

consideration;

e. a tax on the supply of goods by any unincorporated association or body of

persons to a member thereof for cash, deferred payment or other valuable

consideration;

…Whether “Dominant nature / intention test” is still relevant?...

52

f. a tax on the supply, by way of or as part of any service or in any other manner

whatsoever, of goods, being food or any other article for human consumption or

any drink (whether or not intoxicating), where such supply or service is for cash,

deferred payment or other valuable consideration

• Do the following transactions qualify as „works contract‟ within the ambit of clause (b)

of Article 366(29A)?:

- supply of SIM card by a telecom operator to a subscriber against „activation charge‟

- supply of a credit card by a bank to a customer against „joining fee‟

- supply of medicines by a doctor treating a patient in his clinic

- supply of goods like stents, knee, artificial limbs etc. by a hospital treating a patient

…Whether “Dominant nature / intention test” is still relevant?

53

Isn‟t “dominant nature / intention test” still relevant to contracts not falling within Article 366(29A)?

Thank You

55

![Cenvat Accounting[1]](https://img.pdfslide.us/doc/110x75/54193e3a7bef0a05088b4642/cenvat-accounting1.jpg)