Embed Size (px)

Citation preview

Fixed Income MarketsThen and Now

September 8, 2014

Gilbert Andrew Garcia, CFAManaging Partner

2

Table of Contents

I. Market Quiz

II. Evolution of the Fixed Income Market

III. Fixed Income Excess Returns

IV. Valuation

V. Market Developments

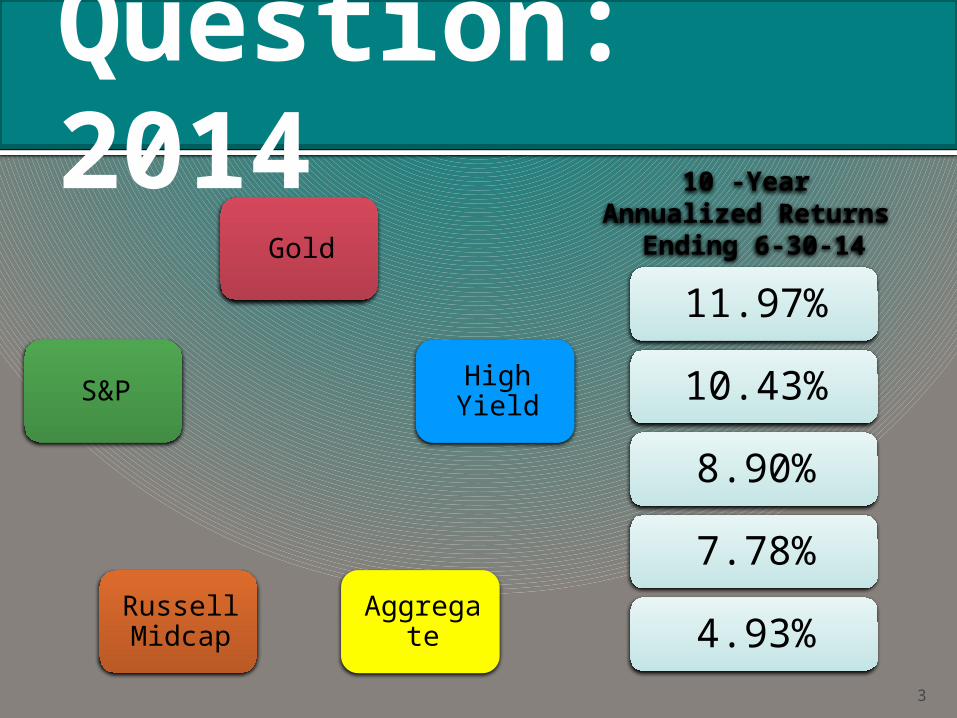

Question: 2014

Gold

High Yield

AggregateRussell Midcap

S&P

3

11.97%

10.43%

8.90%

7.78%

4.93%

10 -Year Annualized Returns

Ending 6-30-14

Answer: 2014

Gold

High Yield

Aggregate

Russell Midcap

S&P

4

11.97%

8.90%

4.93%

10.43%

7.78%

10 -Year Annualized Returns

Ending 6-30-14INDEX

Why is Return not enough?

Return doesn’t account for the risk.

Investors must be compensated for risk.

We should measure returns on a risk adjusted basis.

5

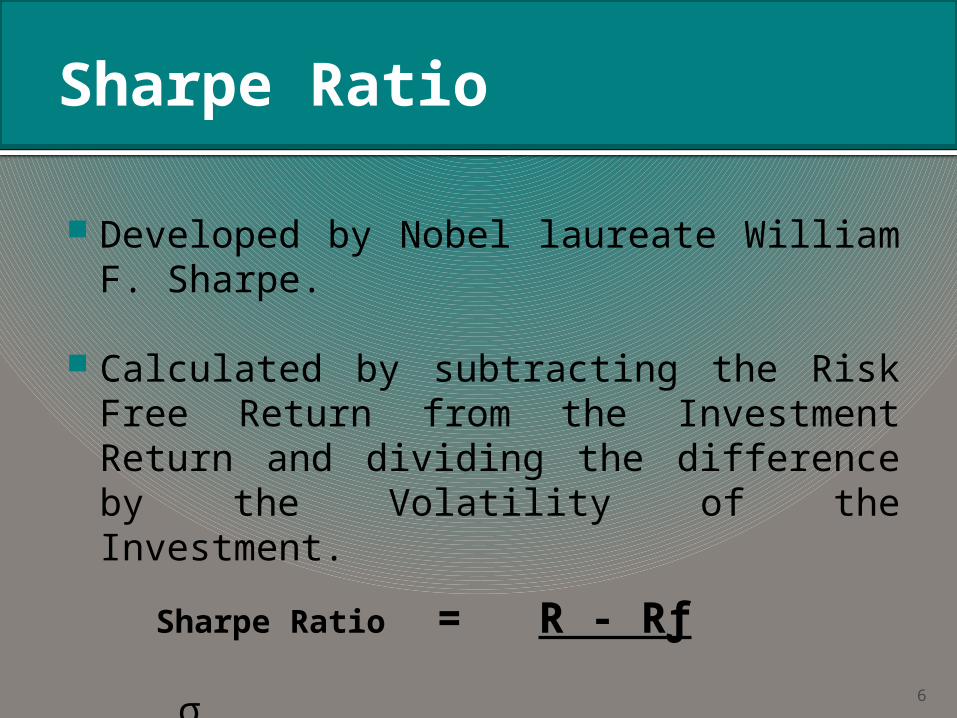

Sharpe Ratio

6

Developed by Nobel laureate William F. Sharpe.

Calculated by subtracting the Risk Free Return from the Investment Return and dividing the difference by the Volatility of the Investment.

Sharpe Ratio = R - Rƒ σ

A higher Sharpe ratio equates to better risk-adjusted performance.

Reality: 2014

Gold

High Yield

Aggregate

Russell Midcap

S&P

7

11.97%

8.90%

4.93%

10.43%

7.78%

10 -Year Annualized Returns

Ending 6-30-14INDEX

10 -Year Sharpe Ratio

Ending 6-30-14

1.04

0.54

0.71

0.50

0.42

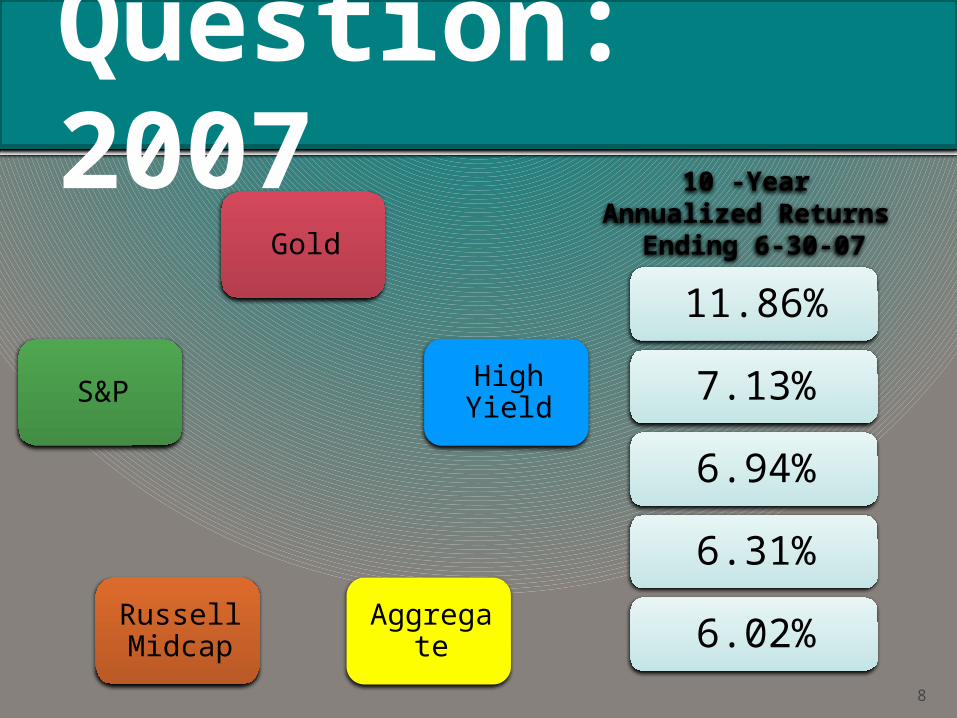

Question: 2007

Gold

High Yield

AggregateRussell Midcap

S&P

8

11.86%

7.13%

6.94%

6.31%

6.02%

10 -Year Annualized Returns

Ending 6-30-07

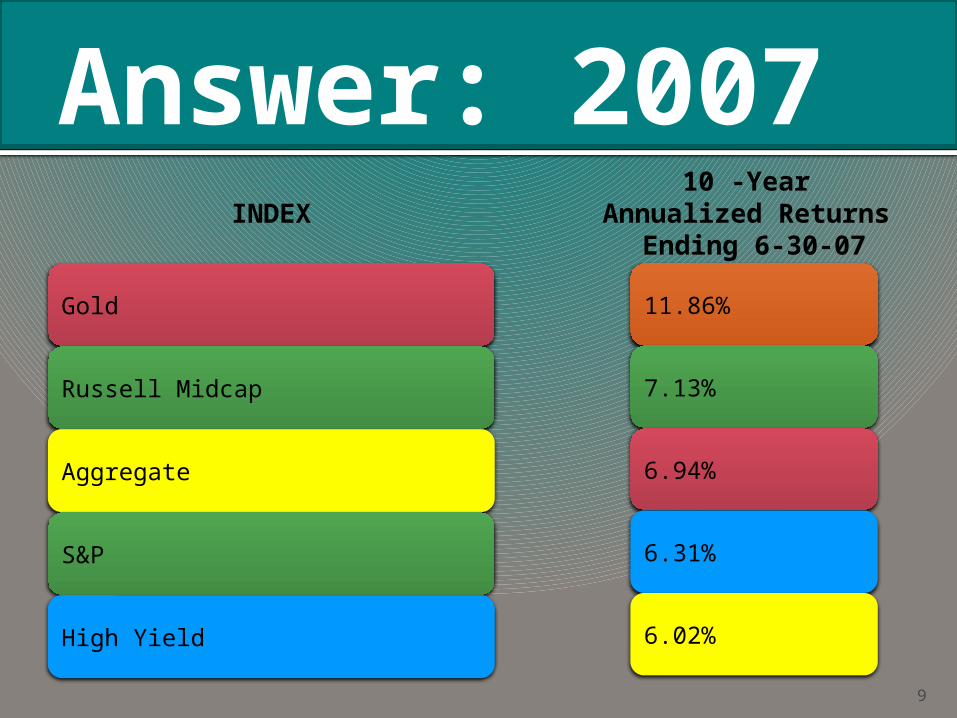

Answer: 2007

Gold

Russell Midcap

Aggregate

S&P

High Yield

9

11.86%

7.13%

6.94%

6.31%

6.02%

10 -Year Annualized Returns

Ending 6-30-07INDEX

Reality: 2007

Gold

Russell Midcap

Aggregate

S&P

High Yield

10

10 -Year Annualized Returns

Ending 6-30-07INDEX

10 -Year Sharpe Ratio

Ending 6-30-07

0.66

0.51

0.37

0.23

0.23

11.86%

7.13%

6.94%

6.31%

6.02%

Sharpe Ratio 2014 - vs- 2007

11

INDEX10 -Year

Sharpe RatioEnding 6-30-14

10 -Year Sharpe Ratio

Ending 6-30-07

Gold

High Yield

Aggregate

Russell Midcap

S&P

1.04

0.54

0.71

0.50

0.42

0.66

0.51

0.37

0.23

0.23

12

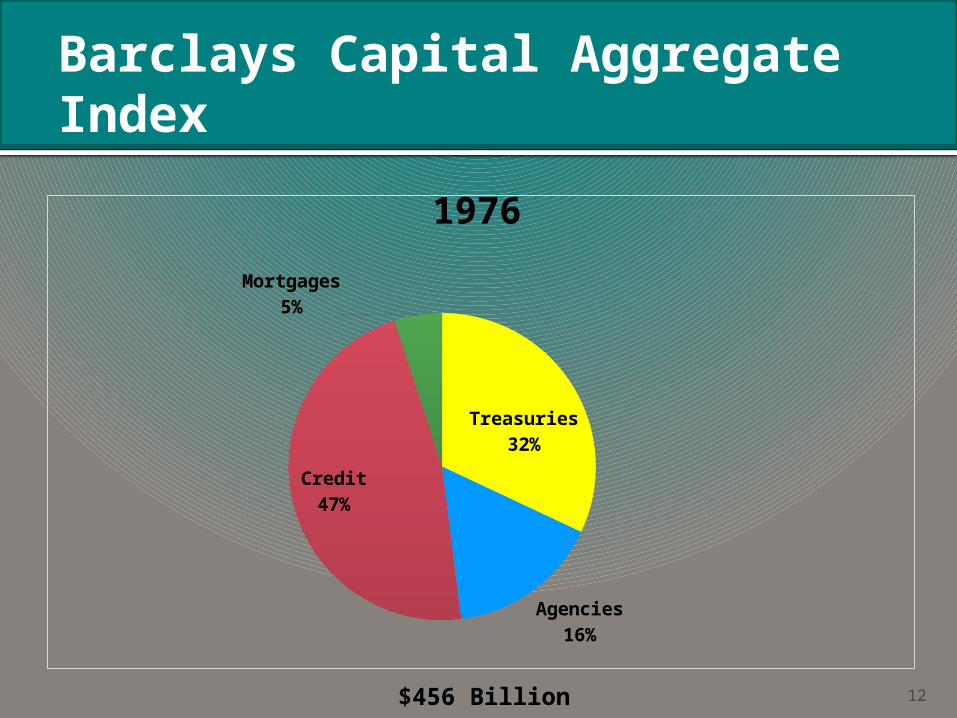

Barclays Capital Aggregate Index

Treasuries32%

Agencies16%

Credit47%

Mortgages5%

1976

$456 Billion

13

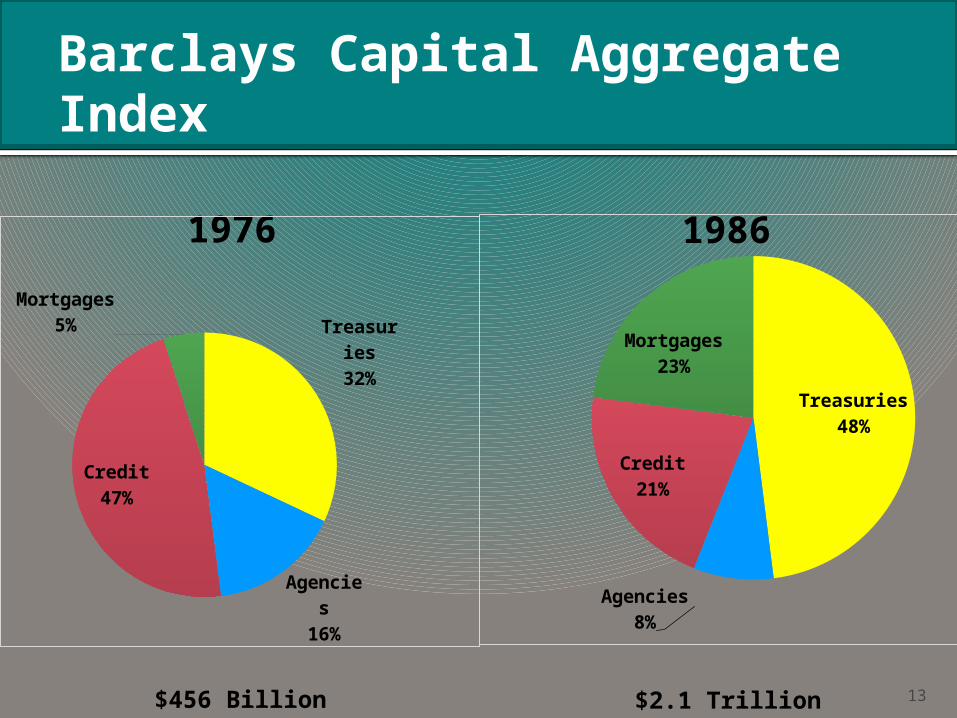

Barclays Capital Aggregate Index

Treasuries48%

Agencies8%

Credit21%

Mortgages23%

1976 1986

$2.1 Trillion

Treasuries32%

Agencies16%

Credit47%

Mortgages5%

$456 Billion

14

Barclays Capital Aggregate Index

Treasuries48%

Agencies8%

Credit21%

Mortgages23% CMO’s invented

MBS along the yield curve

Floating rate traunches

PAC’s

1986

$2.1 Trillion 14

15

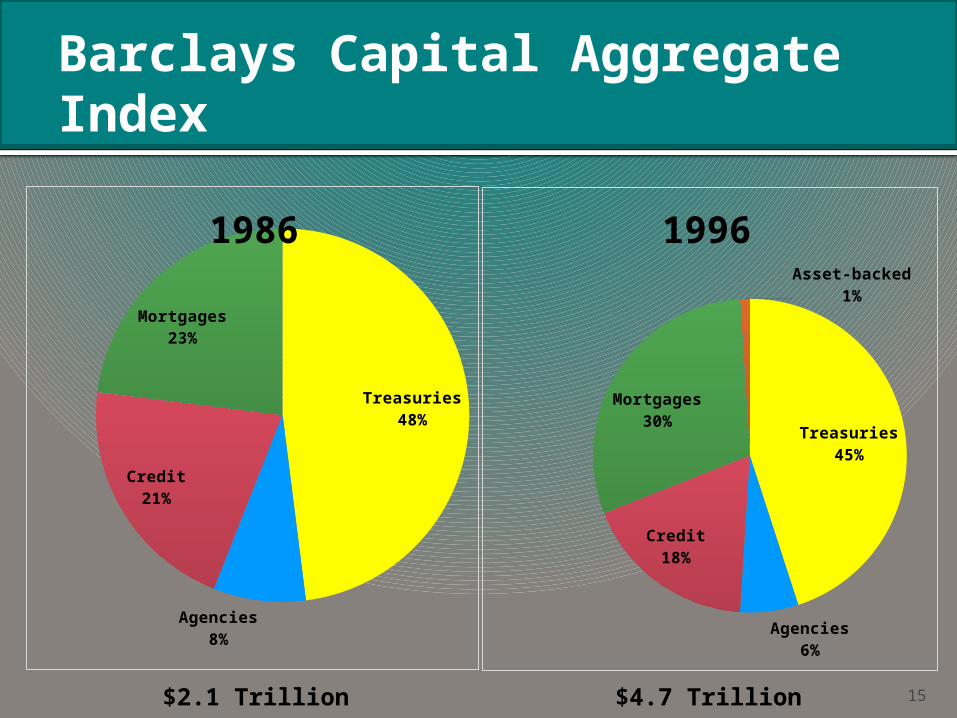

Barclays Capital Aggregate Index

Treasuries48%

Agencies8%

Credit21%

Mortgages23%

Treasuries45%

Agencies6%

Credit18%

Mortgages30%

Asset-backed1%

19961986

$2.1 Trillion $4.7 Trillion

16

Barclays Capital Aggregate Index

Treasuries35%

Agencies4%

Credit30%

Mortgages29%

Asset-Backed3%

NOW

$17.1 Trillion

17

Treasuries32%

Agencies16%

Credit47%

Mortgages5%

Barclays Capital Aggregate Index

Treasuries35%

Agencies4%

Credit30%

Mortgages29%

Asset-Backed3%

1976

$456 Billion

NOW

$17.1 Trillion

Question: 2014

Agency

ABS

Corporates

MBS

18

44.73%

30.38%

22.13%

16.81%

20 -Year Excess Return Ending 6-30-14

Answer: 2014

Agency

Corporates

ABS

MBS

19

44.73%

30.38%

22.13%

16.81%

20 -Year Excess Return Ending 6-30-14

INDEX

20

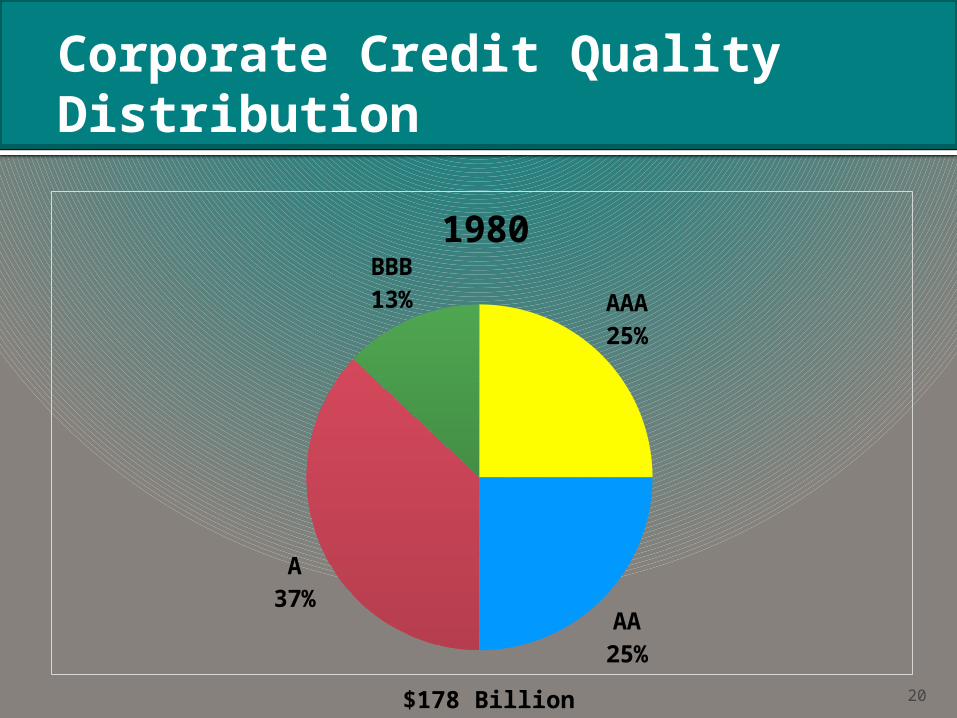

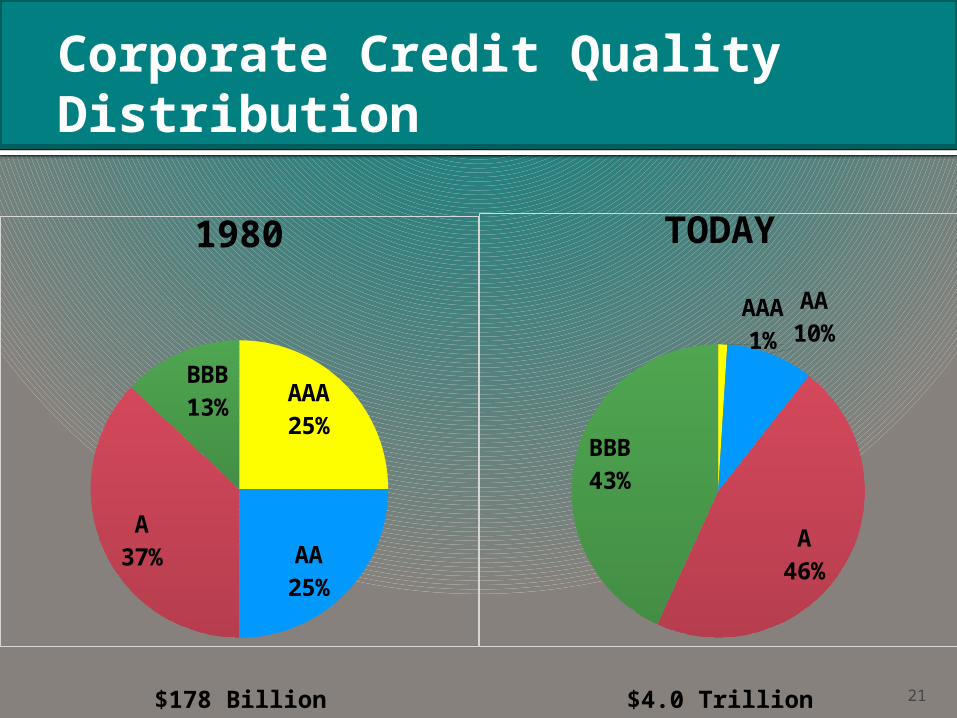

Corporate Credit Quality Distribution

AAA25%

AA25%

A37%

BBB13%

1980

$178 Billion

21

Corporate Credit Quality Distribution

AAA1%

AA10%

A46%

BBB43%

AAA25%

AA25%

A37%

BBB13%

1980 TODAY

$178 Billion $4.0 Trillion

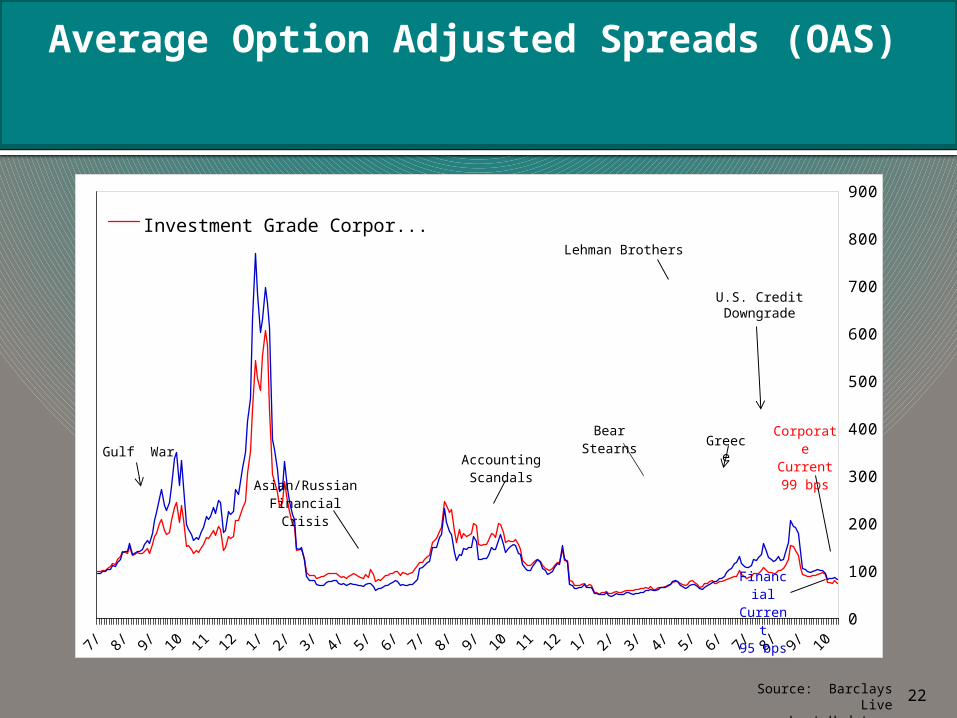

Average Option Adjusted Spreads (OAS)

22Source: Barclays Live

Last Update: 7/31/2014

'89 '90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '140

100

200

300

400

500

600

700

800

900

Investment Grade Corporate...

Asian/RussianFinancial Crisis

Accounting Scandals

Bear Stearns CorporateCurrent99 bps

Finan-cial

Current95 bps

Lehman Brothers

Greece

U.S. Credit Downgrade

Gulf War

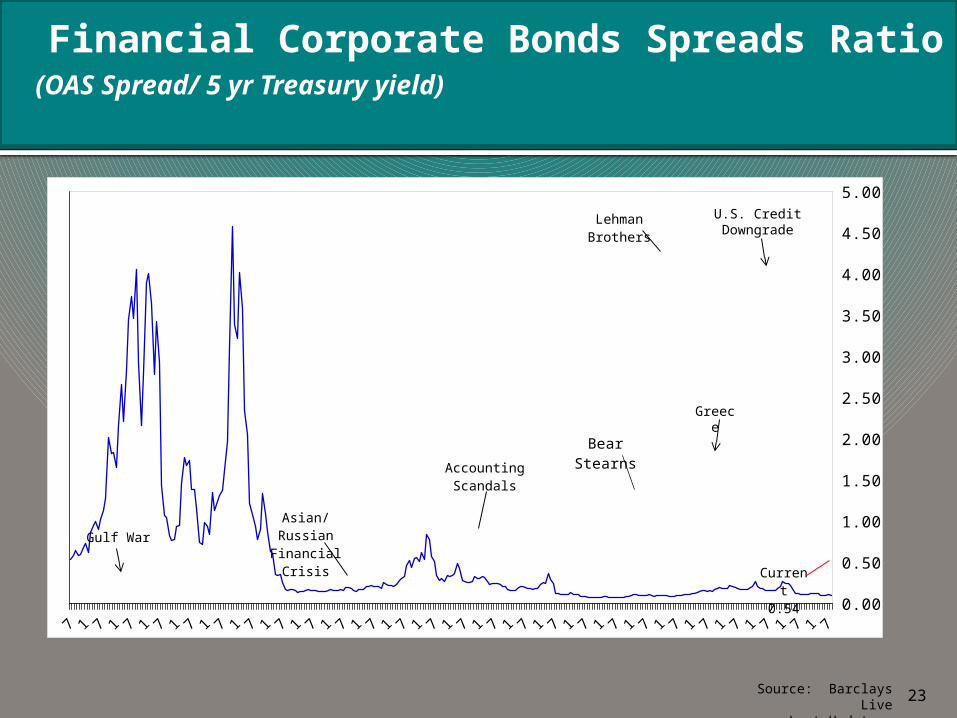

(OAS Spread/ 5 yr Treasury yield)

Financial Corporate Bonds Spreads Ratio

23Source: Barclays Live

Last Update: 7/31/2014

'89 '90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '140.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

Asian/RussianFinancial Crisis

Accounting Scandals

Bear Stearns

Current0.54

Lehman Brothers

Greece

U.S. Credit Downgrade

Gulf War

24

Market Developments

Electronic Trading

TRACE Data

25

TRACE Example