Embed Size (px)

DESCRIPTION

Latest market data and analysis of the Perdido Key real estate market in September 2009.

Citation preview

CONDITIONS™ August 2009 By Peter King, Local Real Estate Expert

Perdido Key Market Report and Sales Analysis

It was a great summer season. Sales volume was the best since 2006. The high sales volume of the first few months of 2009 continued right into August Which is the best month on Perdido Key since 2005. WOW! We are way up over last year and approaching 2006 numbers. During the same period last year we had 74 total closed sales compared to 116 this first eight months. (Several WCI condos have sold but do not appear in the MLS due to WCI policy.) We have 31 additional properties contingent or pending as of the end of August, which is another note for optimism. We noted a continued decline in inventory to our current 294 units for sale. That number even dipped to 291 mid June. The proof of demand is the number of sales but coupled with this drop in supply we should expect price supports if we can get closer to 250 units for sale on the Key. Simply put the sales volume is out-stripping the property coming into the market…in economic terms we are seeing a faster absorption rate. Obviously we are seeing a dramatically better year than last year, surpassing total sales already just 2/3rds into 2009. Continued market improvement. Extrapolating the first quarter over historical norms should put us on a line to 150 plus sales and an inventory number in the 275 range by year end. Compare this projection to results of the previous two years. It is stunning, good news. This data is from the Multiple Listing Service data banks and will allow us to compare “apples to apples”.

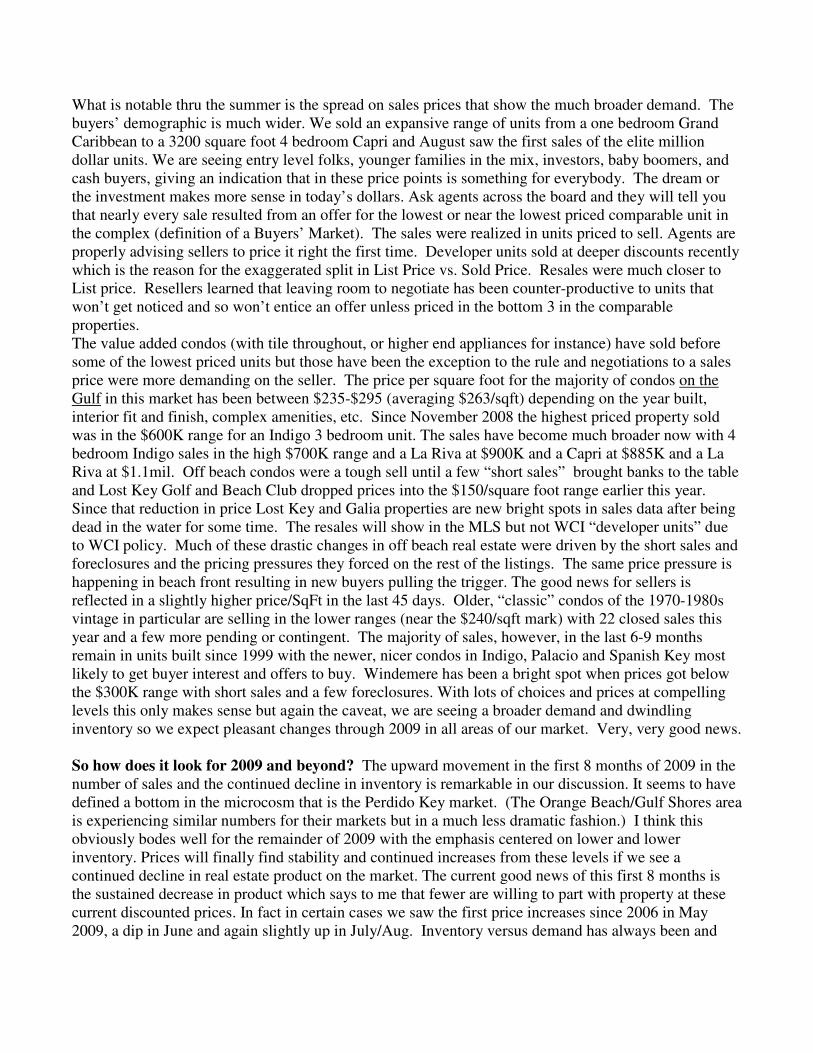

Category - Residential / Perdido Key 2007 Month Year’s Sales Avg ListPrice Avg Sale Price % Diff Sell/list Avg DOM Curr Inventory

Total 96 $675,004 $618,268 91.59% 245.1 420

Category - Residential / Perdido Key 2008

Month Year’s Sales Avg ListPrice Avg Sale Price % Diff Sell/list Avg DOM Curr Inventory

Total 108 $658,023 $601,276 91.38% 292.0 346

Category - Residential / Perdido Key Jan-June 2009

January 2009 6 $403,817 $397,233 98.37% 166.0 355 February 2009 10 $315,960 $293,650 92.94% 287.0 357

March 2009 7 $459,343 $427,271 93.02% 193.0 357 April 2009 13 $405,885 $363,938 89.67% 207.0 356 May 2009 14 $405,979 $377,429 92.97% 225.0 325 June 2009 24 $386,236 $350,161 90.66% 237.0 301 July 2009 17 $444,100 $416,578 93.21% 246.0 313

August 2009 25 $468,938 $392,126 83.62% 276.0 294

Total

116

Peter C. King Tel: 850-261-3938 [email protected] www.perdidopete.com

What is notable thru the summer is the spread on sales prices that show the much broader demand. The buyers’ demographic is much wider. We sold an expansive range of units from a one bedroom Grand Caribbean to a 3200 square foot 4 bedroom Capri and August saw the first sales of the elite million dollar units. We are seeing entry level folks, younger families in the mix, investors, baby boomers, and cash buyers, giving an indication that in these price points is something for everybody. The dream or the investment makes more sense in today’s dollars. Ask agents across the board and they will tell you that nearly every sale resulted from an offer for the lowest or near the lowest priced comparable unit in the complex (definition of a Buyers’ Market). The sales were realized in units priced to sell. Agents are properly advising sellers to price it right the first time. Developer units sold at deeper discounts recently which is the reason for the exaggerated split in List Price vs. Sold Price. Resales were much closer to List price. Resellers learned that leaving room to negotiate has been counter-productive to units that won’t get noticed and so won’t entice an offer unless priced in the bottom 3 in the comparable properties. The value added condos (with tile throughout, or higher end appliances for instance) have sold before some of the lowest priced units but those have been the exception to the rule and negotiations to a sales price were more demanding on the seller. The price per square foot for the majority of condos on the Gulf in this market has been between $235-$295 (averaging $263/sqft) depending on the year built, interior fit and finish, complex amenities, etc. Since November 2008 the highest priced property sold was in the $600K range for an Indigo 3 bedroom unit. The sales have become much broader now with 4 bedroom Indigo sales in the high $700K range and a La Riva at $900K and a Capri at $885K and a La Riva at $1.1mil. Off beach condos were a tough sell until a few “short sales” brought banks to the table and Lost Key Golf and Beach Club dropped prices into the $150/square foot range earlier this year. Since that reduction in price Lost Key and Galia properties are new bright spots in sales data after being dead in the water for some time. The resales will show in the MLS but not WCI “developer units” due to WCI policy. Much of these drastic changes in off beach real estate were driven by the short sales and foreclosures and the pricing pressures they forced on the rest of the listings. The same price pressure is happening in beach front resulting in new buyers pulling the trigger. The good news for sellers is reflected in a slightly higher price/SqFt in the last 45 days. Older, “classic” condos of the 1970-1980s vintage in particular are selling in the lower ranges (near the $240/sqft mark) with 22 closed sales this year and a few more pending or contingent. The majority of sales, however, in the last 6-9 months remain in units built since 1999 with the newer, nicer condos in Indigo, Palacio and Spanish Key most likely to get buyer interest and offers to buy. Windemere has been a bright spot when prices got below the $300K range with short sales and a few foreclosures. With lots of choices and prices at compelling levels this only makes sense but again the caveat, we are seeing a broader demand and dwindling inventory so we expect pleasant changes through 2009 in all areas of our market. Very, very good news. So how does it look for 2009 and beyond? The upward movement in the first 8 months of 2009 in the number of sales and the continued decline in inventory is remarkable in our discussion. It seems to have defined a bottom in the microcosm that is the Perdido Key market. (The Orange Beach/Gulf Shores area is experiencing similar numbers for their markets but in a much less dramatic fashion.) I think this obviously bodes well for the remainder of 2009 with the emphasis centered on lower and lower inventory. Prices will finally find stability and continued increases from these levels if we see a continued decline in real estate product on the market. The current good news of this first 8 months is the sustained decrease in product which says to me that fewer are willing to part with property at these current discounted prices. In fact in certain cases we saw the first price increases since 2006 in May 2009, a dip in June and again slightly up in July/Aug. Inventory versus demand has always been and

will continue to be the major factor (Supply and Demand of course) in the price points so I am particularly encouraged for the market in 2009 and even more optimistic than I was previously about 2010. Absorption will be based on price increases, or in other words, new units will not come on the MLS until price points obviously rebound off a bottom, which we think we have defined in the last few months. The seller psychology will take its cue from the sales data. I also anticipate interest rates and credit markets to influence a hoped for expansion of buyers in the market. Right now strong credit risks with significant down payments rule the roost with many cash buyers moving into real estate from equities. If credit does not loosen to some degree we might run out of qualified buyers. Cash has been king since the fall of 2008 but only a certain segment of the demand can come from cash buyers and superior credit risks. A continued drop in inventory and seller psychology will be crucial to these discussions and predictions. I think we are at a very tenuous point now waiting to see if more buyers come into the market than the number of units the sellers want to put into the market after the rental season. We currently have 294 units for sale compared to 435 last year at this juncture. Couple this trend with the activity reflected in the 48% increase in sales volume we are definitely in a positive market psychology. That should result, given the above caveats, in more sales, less inventory…price support and then continued price pressures to the upside. In summary then…..I think we will have an increasing rate in unit sales, continued whittling down of inventory, but likely no significant price increases until January 2010 depending on the inventory that comes on the market after peak season. Credit concerns may impact the overall picture. I think the inventory will be in the 270 units range in Sep-Dec. This number is directly impacted by the number of properties being held off the market awaiting the further recovery in price points. Absorption will be key if and when these properties hit the inventory and at what price. I know from anecdotal evidence (many conversations with my client base) that there will be a significant number of condos brought on the resale market as owners perceive they can get their price. If they come on too quickly it could derail an early recovery of price points, extending the buyers market fueled by high inventory that will result without a corresponding increase in number of units sold (again real estate loans may be a factor). May through Sep are of course our highest selling months but also our highest listing months so the good news of July and August portends a positive trend continuing into 2010. The absorption rates have been a true positive sign in the Perdido market. I think we need to be below a 2 to 1 average annual ratio for Inventory/Sales to see prices in 2009 make any significant movement. (If we have 270 in inventory we better have sold 135 units or more by year’s end). We are on a line to sell 150 but I expect that to be surpassed. This defined a great market in 2005, (post Ivan numbers in Dec2005 were 391 available and 215 sold). The monthly ratio (Inventory/Sales) to watch is 10/1 with 20+ units sold in an exceptional month (defining the peak price points of 2004/2005 with 200-300 units in inventory but selling at a fast clip.) We saw 25 sales in August so we are off to the races. Continue to watch those figures and ratios for your cue. They are your tipping points. My recommendation is to buy now in anticipation, with the knowledge that this looks more and more like recovery of the market, and bring offers if you can’t find your comfort zone in the list prices to flush out the possible bargain. There are less and less obvious “deals” after this flurry of activity but you can still find a gem in there if you get off the sidelines. Sitting on your hands now if you want to own a piece of paradise will likely cost you more going forward. If you own on Perdido Key, Orange Beach/Gulf Shores hold on to your property as long as possible into 2010 and stay informed.