Embed Size (px)

DESCRIPTION

ECONOMICS OF MULTILEVEL GOVERNANCE - Securing Energy Supply - Who is Taking Care within the EU’s Multilevel Governance Regime?

Citation preview

ECONOMICS OF MULTILEVEL GOVERNANCE Securing Energy Supply -

Who is Taking Care within the EU’s Multilevel Governance Regime?

Jean-Michel Glachant and Nicole Ahner | European University Institute

Florence, 17th November 2011

Outline 1. What do we mean when we speak about ‘EU energy

security’? 2. What is the general policy framework governing EU

energy security? 3. Actors, tools & angles - who is taking care? 4. Excursus: a new era in EU energy governance?

1. What do we mean when we speak about ‘energy security’ in Europe?

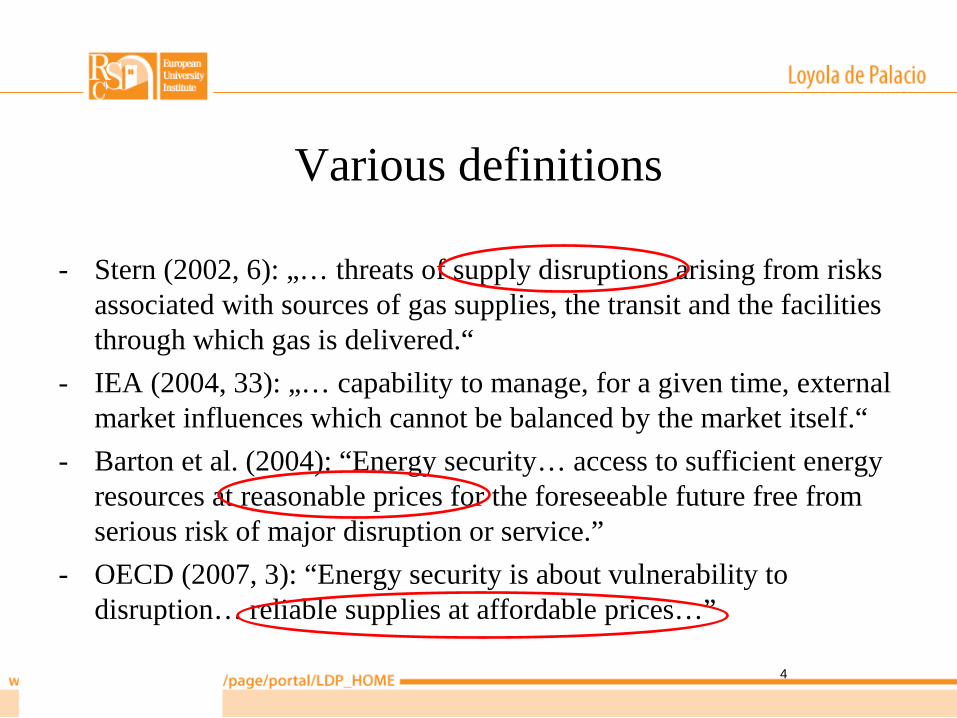

Various definitions

- Stern (2002, 6): „… threats of supply disruptions arising from risks associated with sources of gas supplies, the transit and the facilities through which gas is delivered.“

- IEA (2004, 33): „… capability to manage, for a given time, external market influences which cannot be balanced by the market itself.“

- Barton et al. (2004): “Energy security… access to sufficient energy resources at reasonable prices for the foreseeable future free from serious risk of major disruption or service.”

- OECD (2007, 3): “Energy security is about vulnerability to disruption… reliable supplies at affordable prices…”

4

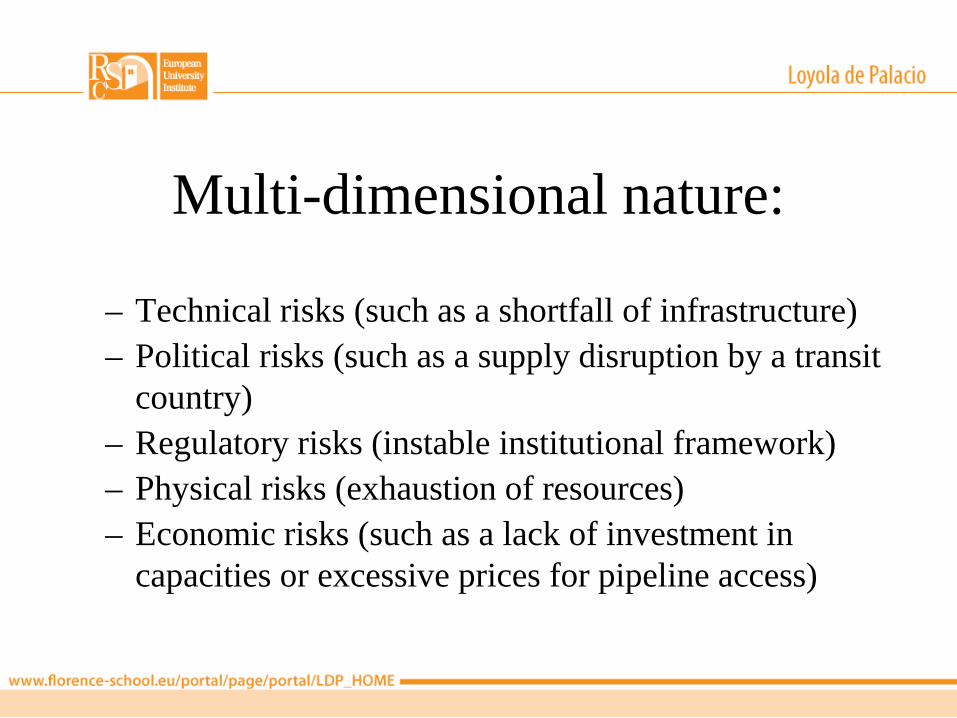

Multi-dimensional nature:

– Technical risks (such as a shortfall of infrastructure) – Political risks (such as a supply disruption by a transit

country) – Regulatory risks (instable institutional framework) – Physical risks (exhaustion of resources) – Economic risks (such as a lack of investment in

capacities or excessive prices for pipeline access)

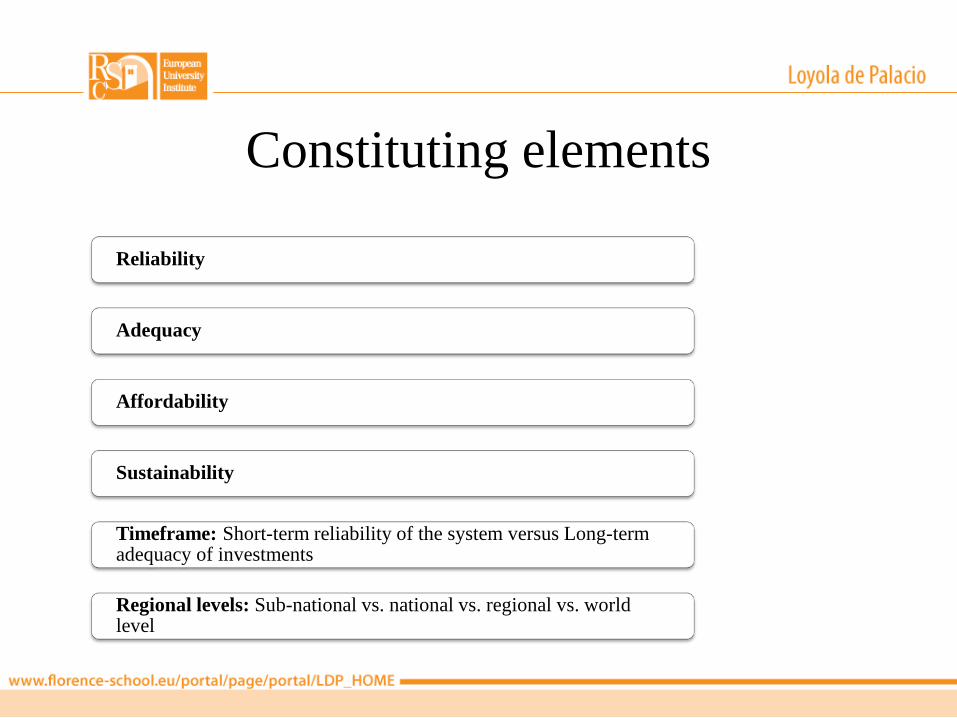

Constituting elements

Reliability

Adequacy

Affordability

Sustainability

Timeframe: Short-term reliability of the system versus Long-term adequacy of investments

Regional levels: Sub-national vs. national vs. regional vs. world level

2. What is the policy framework governing energy security in Europe?

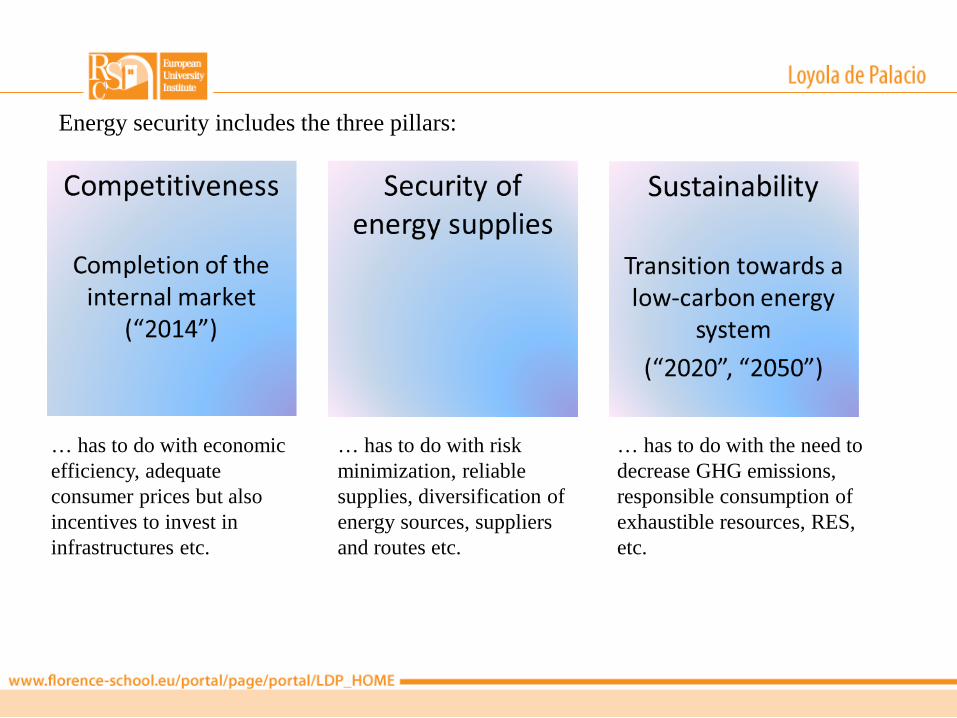

… has to do with economic efficiency, adequate consumer prices but also incentives to invest in infrastructures etc.

… has to do with risk minimization, reliable supplies, diversification of energy sources, suppliers and routes etc.

… has to do with the need to decrease GHG emissions, responsible consumption of exhaustible resources, RES, etc.

Energy security includes the three pillars:

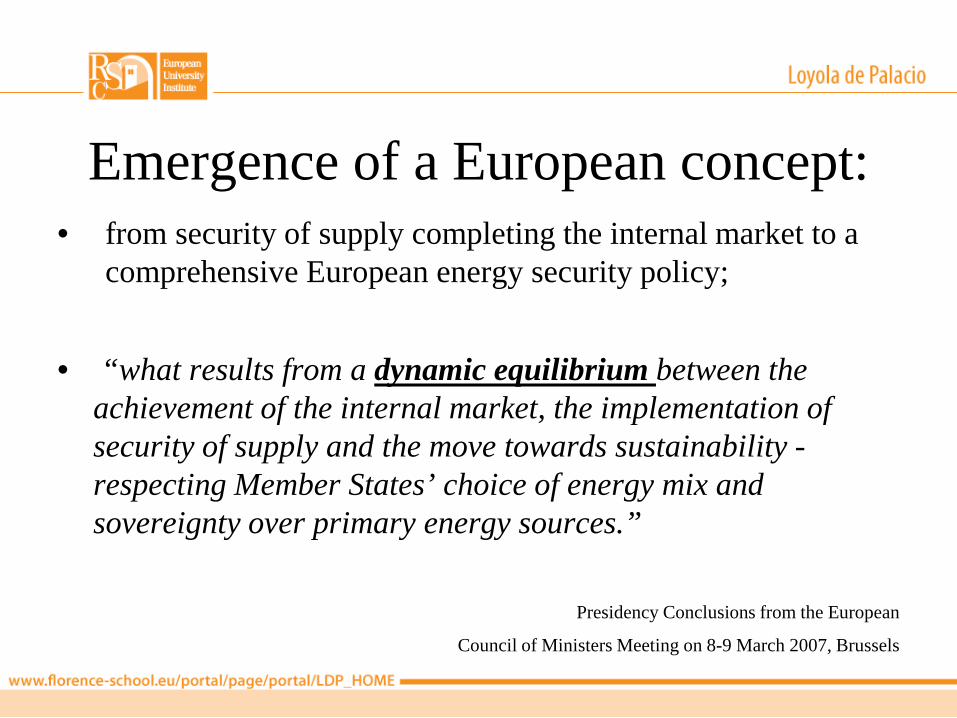

Emergence of a European concept:

• from security of supply completing the internal market to a comprehensive European energy security policy;

• “what results from a dynamic equilibrium between the

achievement of the internal market, the implementation of security of supply and the move towards sustainability - respecting Member States’ choice of energy mix and sovereignty over primary energy sources.”

Presidency Conclusions from the European

Council of Ministers Meeting on 8-9 March 2007, Brussels

3. Actors, tools & angles - who is taking care?

Competitiveness

Background

• Under normal circumstances the market guarantees security of supply • Before EU liberalized energy markets, most MS‘ supply was organized by

national or regional companies regulated by the state, price set by the government.

• Liberalization created a market where price formation acted as the guarantee of security of supply

• The better the market functions-the less risk for market failure- the less reason for governments to interfere in market functioning. Price formation as mechanism to match supply and demand, both short- and long-term.

The Liberalization Process: Energy through the Prism of the Internal Market

1996/1998, 2003, 2009 Gas and Electricity Directives • (third party) grid access and regulation • rules on separation (unbundling) of supply/production activities on the one

hand, and grid related activities on the other hand. These rules apply to both Community and non-Community undertakings.

• MS required to appoint independent national regulatory authorities (NRAs) complemented by Regulation promoting cross-border trade in electricity (2003); Regulation setting up non-discriminatory rules for access conditions to gas transmission networks (2005)

The market did not function properly…

• Again: liberalization measures faced a market structure characterized by State intervention and the mono- or oligopolistic presence of incumbent firms. Heritage of the past could not simply be regulated away.

• 2005 EC launched large scale sector inquiry into the causes of the improper functioning of the market mechanism in gas/electricity sectors.

• Result: energy markets still highly concentrated and national in scope • EU action: 1) enforcement of competition rules; 2) new EU level rules eg

on unbundling => a new 2009 Third Energy Package

…after the Third Package

• fundamental restructuring of EU sector-specific regulation = greater supranational presence on national legislation;

• NRAs coordinated at EU level: Agency for the Cooperation of Energy Regulators (ACER); ACER will monitor the transmission system operators’ (TSO) 10-years investment plans and the cooperation between TSOs. The agency is also responsible for taking individual decisions on specific cross border issues.

• ! The 2nd Package has still not been implemented by the MS. In 2009 the EC started infringement proceedings against 25 MSs.

Competition policy tool

• Key tool (exclusive competence) • Antitrust law, merger regulation and state aid control

contribute to protect openness and innovation in energy markets;

• an indispensable base to establish robust markets in an energy sector having been monopolized or state-run for decades.

Trans-European Networks (TENs) policy

• completion of the IEM requires energy infrastructure development, particularly cross-border infrastructure

• TEN-E pioneer of action at EU level • European investment projects corresponding to European

network priorities (small budget) • Similar important financing tool: European Recovery Fund

(covers several gas and electricity interconnector projects, Carbon Capture and Storage and offshore wind energy projects. )

Security of supply

Background

• EU heavily dependent on imports from third countries • Oil imports above 90% of concumption; • Gas imports close to 65%, same coal/uranium. • Russia is the first energy supplier of the EU (30% oil; 24% gas; 20%coal,

40%uranium • Oil: international commodity, globally available, price set by the world

markets • Gas: mainly set by long-term contracts incl. Indexation clause

Internal dimension

• Starting point January 2009 gas crisis • Revision of the oil stocks Regulation • Gas Security of Supply – from Directive

2004/67 to Regulation 994/2010

Example: the new Regulation • Top-down infrastructure standards

– „… in the event of a disruption of the largest gas supply infrastructure, the remaining infrastructure (N-1) has the capacity to deliver the necessary volume of gas to satisfy total gas demand of the calculated area during a period of sixty days of exceptionally high gas demand during the coldest period statistically occurring every twenty years” [may be fulfilled at the regional level]

– TSOs shall enable permanent physical capacity to transport gas in both directions on all interconnections

• Bottom-up risk assessments – Running various scenarios of exceptionally high demand and supply disruption

• Preventive Action Plan – Containing measures needed to meet N-1 standard and to mitigate risks identified [to be updated

every two years]

• Emergency Plan

The new Regulation on gas SoS

Profound shift to the EU level: • Binding EU law standards for infrastructure and supply security; • Stronger Commission role; • Much greater range and detail of EU law obligations on Member States,

their authorities and undertakings.

The external dimenison – diversification especially in the gas area needed

• Gas crisis 2006 and 2009 showed vulnerability • Need for further EU relationship with key suppliers

and transit countries • Eg Russia • Eg Souther gas corridor (all MSs in Sept. 2011 gave

EC mandate to negotiate an agreement with Turkmenistand and Azerbadjan)

External dimension-Tools

• various hard law and soft law measures • Key concern: we do not speak with one voice • Energy Community Treaty signed in 2005 that expands the core parts of

the internal market acquis communautaire for oil, gas and electricity to the Central and South East European region, and now also includes Ukraine as one of the key transit countries.

• Energy Charter Treaty, MoUs, European Neighbourhood Policy, Roadmaps and energy dialogues such as with Russia, Norway etc.

Sustainability

Background

EU strategy: 20-20-20 by 2020 • Minus 20 % GHG levels • Minus 20 % energy consumption • Plus 20% Renewables in energy mix ⇒Translated into the “Green package”

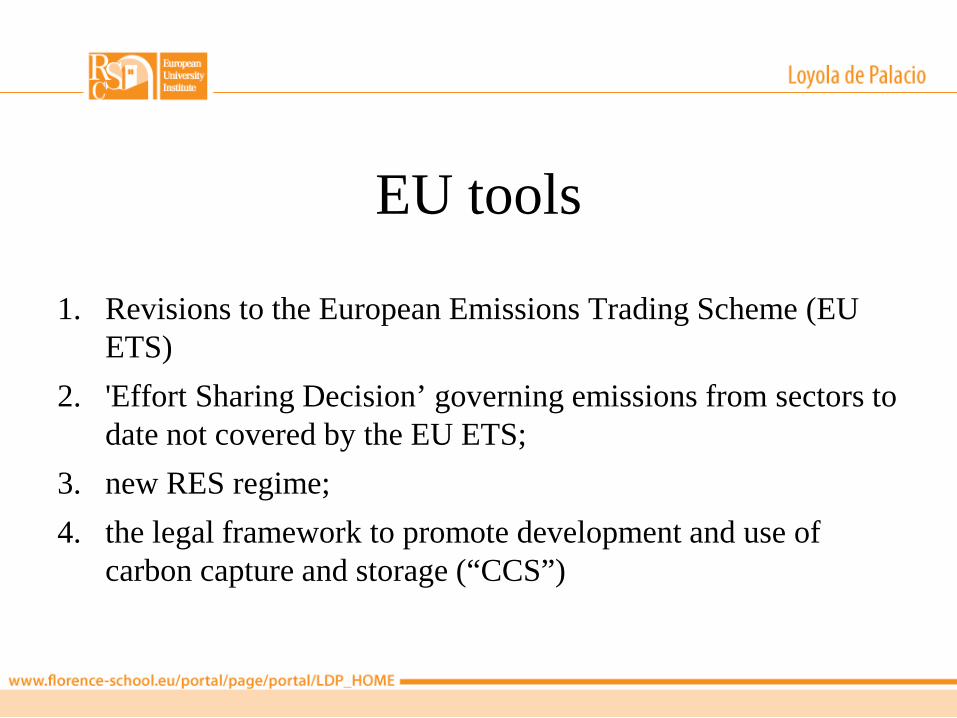

EU tools

1. Revisions to the European Emissions Trading Scheme (EU ETS)

2. 'Effort Sharing Decision’ governing emissions from sectors to date not covered by the EU ETS;

3. new RES regime; 4. the legal framework to promote development and use of

carbon capture and storage (“CCS”)

The EU ETS – why?

• 29 April 1998 EC + 15 EU Member States signed the Kyoto Protocol

• Commitment to jointly reduce GHG 2008-2012 by 8% below 1990 levels (EU bubble)

• Legally binding burden sharing agreement • EU explored ETS to help MSs (KP ‘may’) • EU ETS adopted October 2003

Florence School of Regulation Cyprus Training 2010

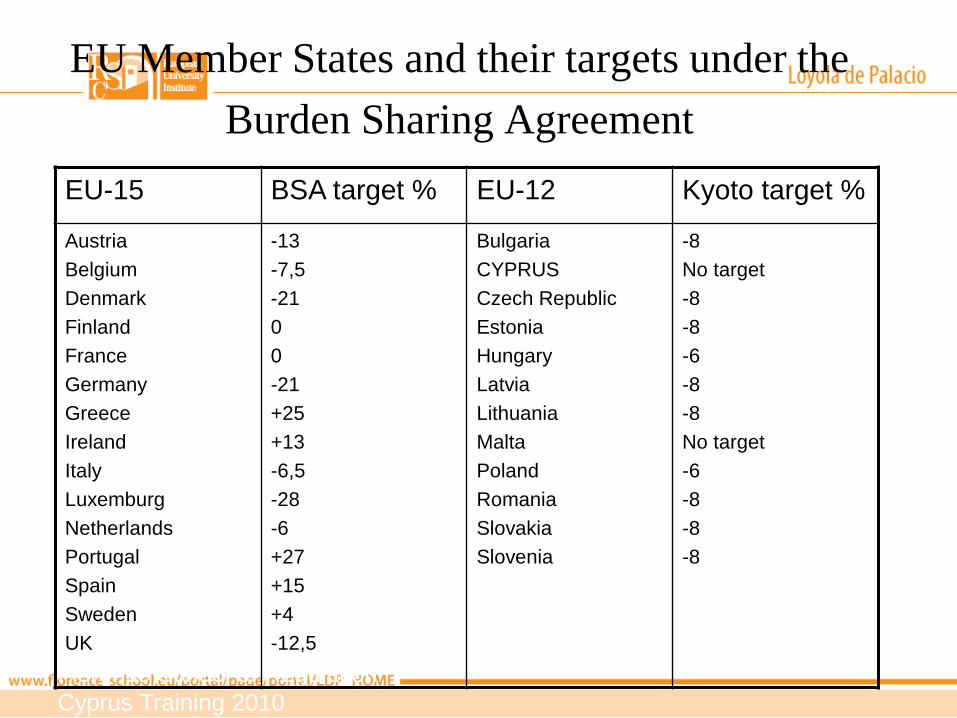

EU Member States and their targets under the Burden Sharing Agreement

EU-15 BSA target % EU-12 Kyoto target %

Austria Belgium Denmark Finland France Germany Greece Ireland Italy Luxemburg Netherlands Portugal Spain Sweden UK

-13 -7,5 -21 0 0 -21 +25 +13 -6,5 -28 -6 +27 +15 +4 -12,5

Bulgaria CYPRUS Czech Republic Estonia Hungary Latvia Lithuania Malta Poland Romania Slovakia Slovenia

-8 No target -8 -8 -6 -8 -8 No target -6 -8 -8 -8

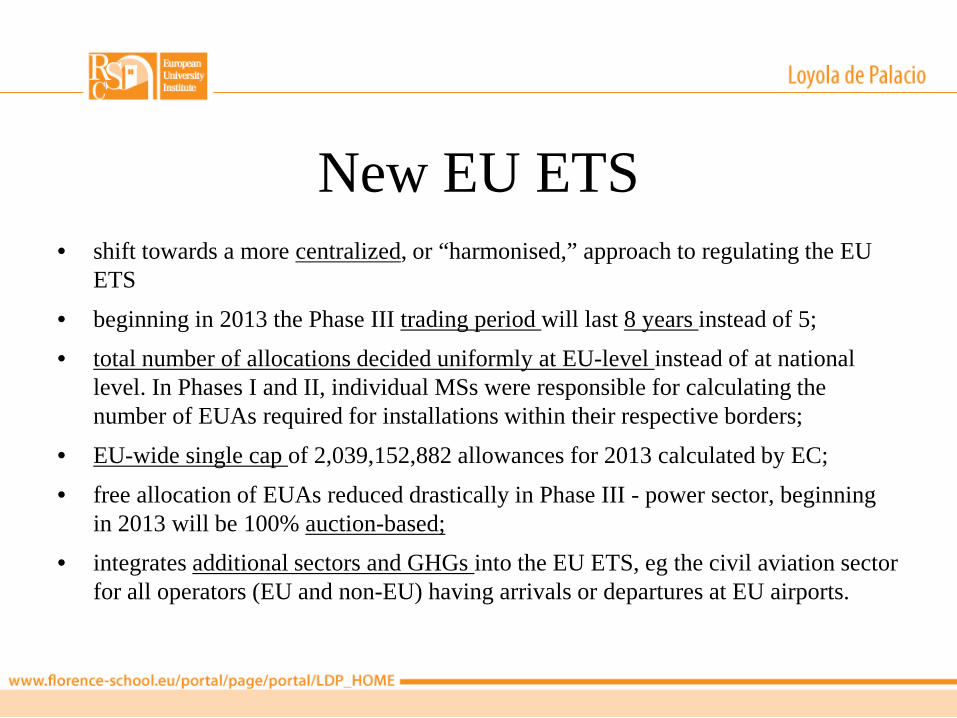

New EU ETS • shift towards a more centralized, or “harmonised,” approach to regulating the EU

ETS

• beginning in 2013 the Phase III trading period will last 8 years instead of 5; • total number of allocations decided uniformly at EU-level instead of at national

level. In Phases I and II, individual MSs were responsible for calculating the number of EUAs required for installations within their respective borders;

• EU-wide single cap of 2,039,152,882 allowances for 2013 calculated by EC;

• free allocation of EUAs reduced drastically in Phase III - power sector, beginning in 2013 will be 100% auction-based;

• integrates additional sectors and GHGs into the EU ETS, eg the civil aviation sector for all operators (EU and non-EU) having arrivals or departures at EU airports.

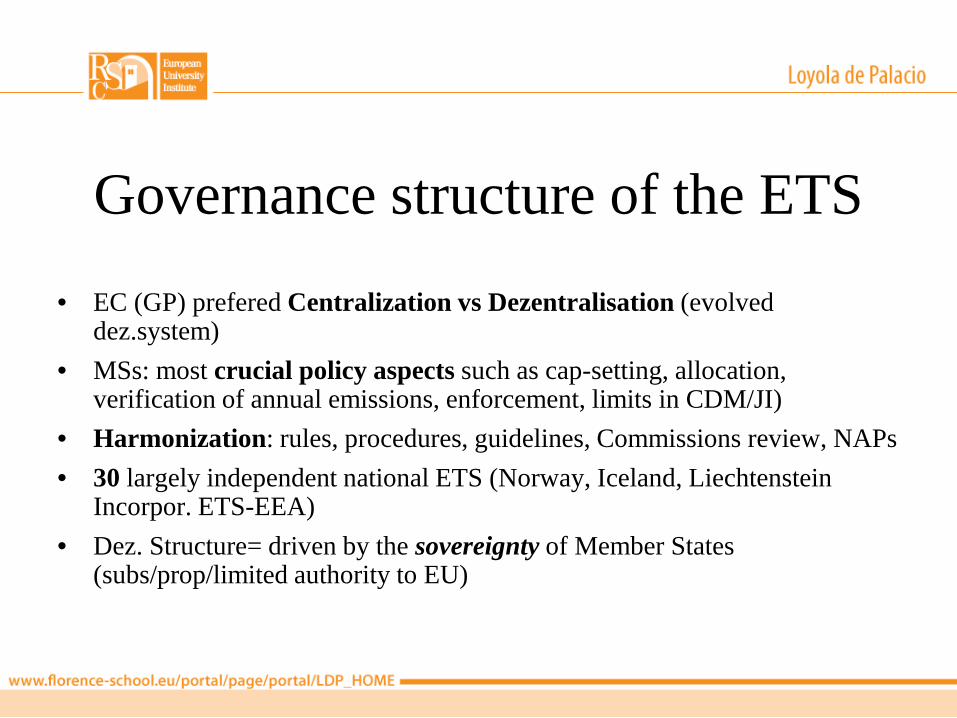

Governance structure of the ETS

• EC (GP) prefered Centralization vs Dezentralisation (evolved dez.system)

• MSs: most crucial policy aspects such as cap-setting, allocation, verification of annual emissions, enforcement, limits in CDM/JI)

• Harmonization: rules, procedures, guidelines, Commissions review, NAPs • 30 largely independent national ETS (Norway, Iceland, Liechtenstein

Incorpor. ETS-EEA) • Dez. Structure= driven by the sovereignty of Member States

(subs/prop/limited authority to EU)

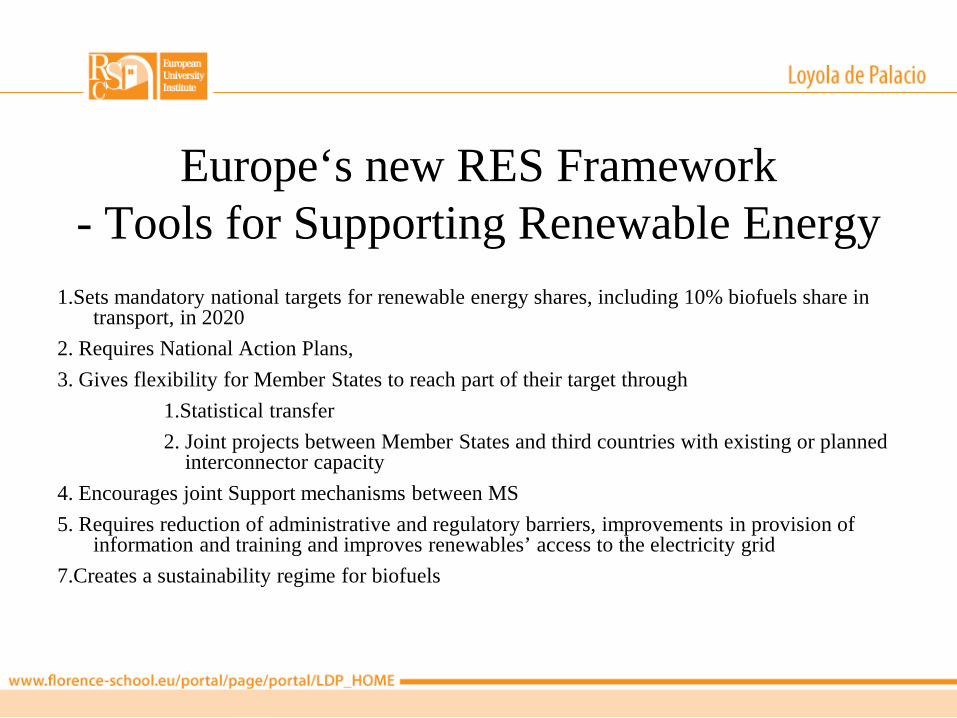

Europe‘s new RES Framework - Tools for Supporting Renewable Energy

1.Sets mandatory national targets for renewable energy shares, including 10% biofuels share in transport, in 2020

2. Requires National Action Plans, 3. Gives flexibility for Member States to reach part of their target through 1.Statistical transfer 2. Joint projects between Member States and third countries with existing or planned

interconnector capacity 4. Encourages joint Support mechanisms between MS 5. Requires reduction of administrative and regulatory barriers, improvements in provision of

information and training and improves renewables’ access to the electricity grid 7.Creates a sustainability regime for biofuels

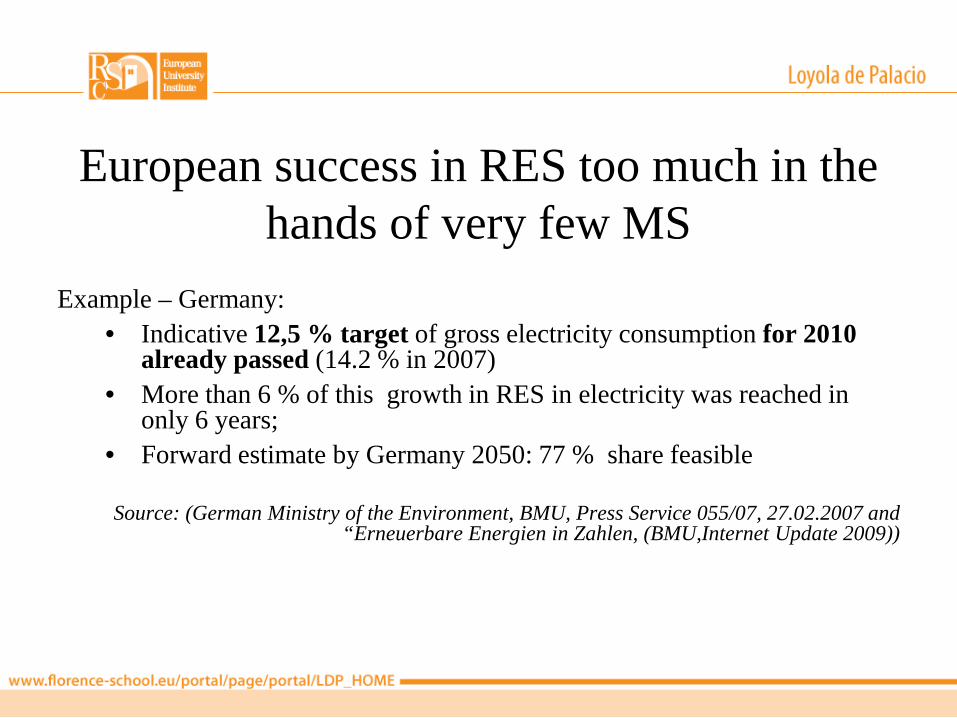

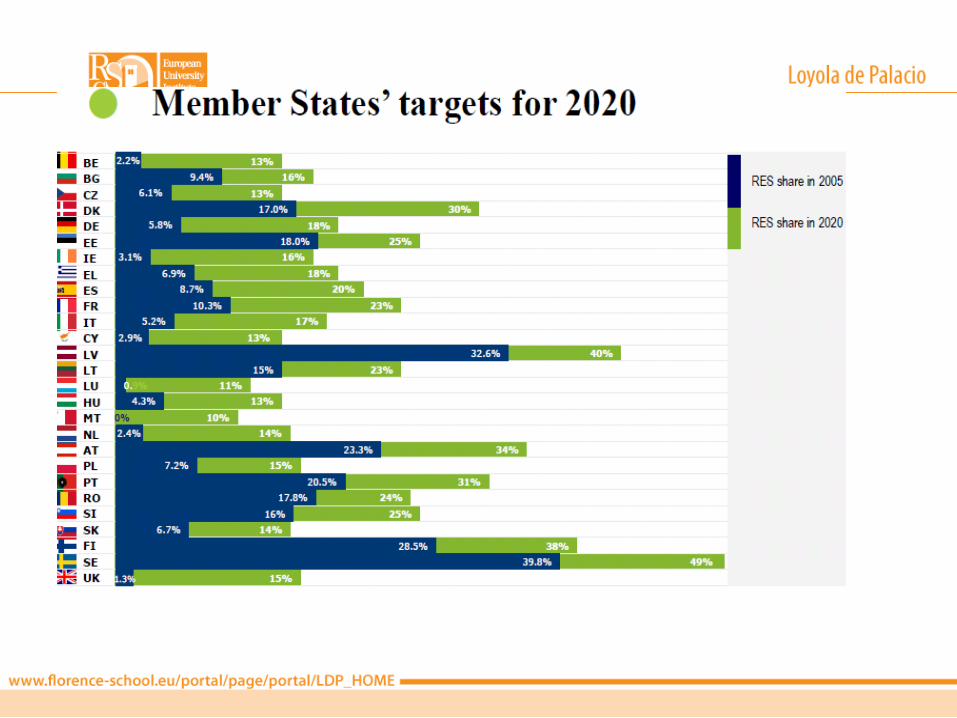

European success in RES too much in the hands of very few MS

Example – Germany: • Indicative 12,5 % target of gross electricity consumption for 2010

already passed (14.2 % in 2007) • More than 6 % of this growth in RES in electricity was reached in

only 6 years; • Forward estimate by Germany 2050: 77 % share feasible

Source: (German Ministry of the Environment, BMU, Press Service 055/07, 27.02.2007 and

“Erneuerbare Energien in Zahlen, (BMU,Internet Update 2009))

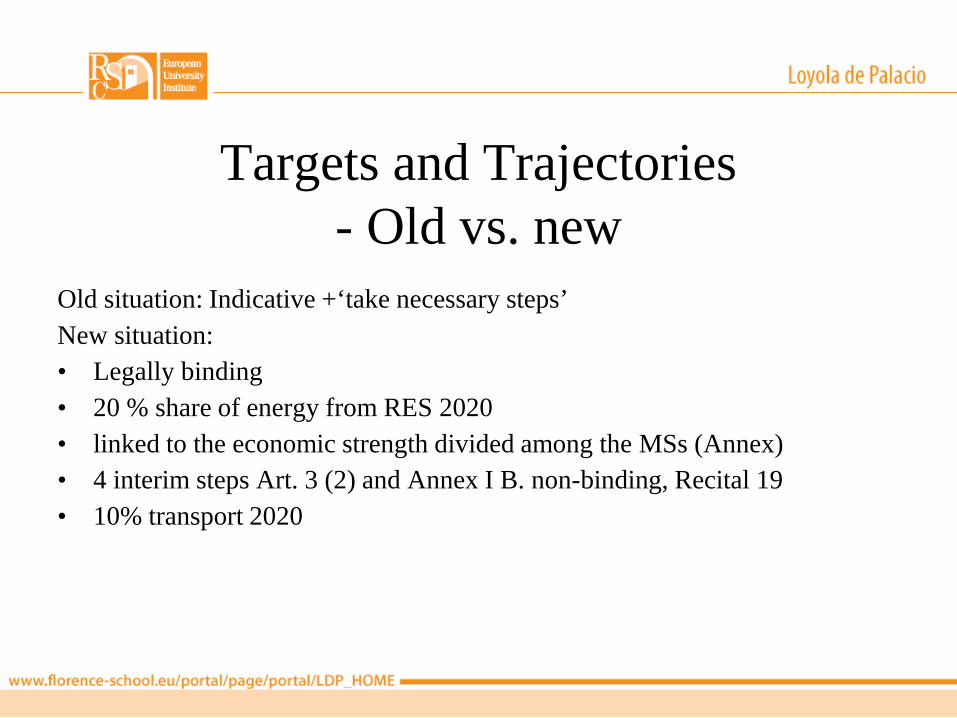

Targets and Trajectories - Old vs. new

Old situation: Indicative +‘take necessary steps’ New situation: • Legally binding • 20 % share of energy from RES 2020 • linked to the economic strength divided among the MSs (Annex) • 4 interim steps Art. 3 (2) and Annex I B. non-binding, Recital 19 • 10% transport 2020

with one small exception are exactly as proposed by the commission in its initial proposal for the directive

NREAPs – key features

• EC evaluates the appropriateness/ can give recommendations • Monitoring/ enforcement function • Up-date function – trajectories • full transparency of the renewable energy sectors: ‘EU

transparency platform’ •

http://ec.europa.eu/energy/renewables/transparency_platform/transparency_platform_en.htm

Authorization, certification, and licensing of renewable energy technologies

• No harmonisation – matter of national sovereignty – 2009 idea is abolishment!

• informal discussions (respective land use plan), planning permit, environmental permit, supply permit, permit to operate installation after construction, safety permits, grid issues

⇒Multitude of authorities in the 27 (BE/ES not even the same inside).

⇒On average 9.5 under old Directive

Cost estimations

• Total investments in RES are currently about 35bn/year

• Has to DOUBLE to reach 2020 targets • renewable energy should be produced where

cheapest + where the potential highest, • So => ?

Cooperation mechanisms 1. Statistical transfers a MS can agree to statistically transfer to another MS a

quantity of the renewable energy produced on its territory (either generally or associated with a specific new installation)

2. Joint projects between MS or MS-3rd countries New plants in neighbouring countries also qualify if the electricity is imported (e.g. Desertec)

3. Joint support schemes Member States can harmonise all or part of their support schemes (e.g. Norway-Sweden)

! Article 6 to 11 of the 2009 Directive (enumeration is conclusive)

4. Excursus: new era in EU energy governance?

Traditional Legal Basis

• 1952 Coal and Steel Community (ECSC) • 1958 European Atomic Energy Community

(Euratom)

Economic Community

• Never energy chapter in EEC or EC Treaty • Several instruments that EU Institutions used

rather successfully

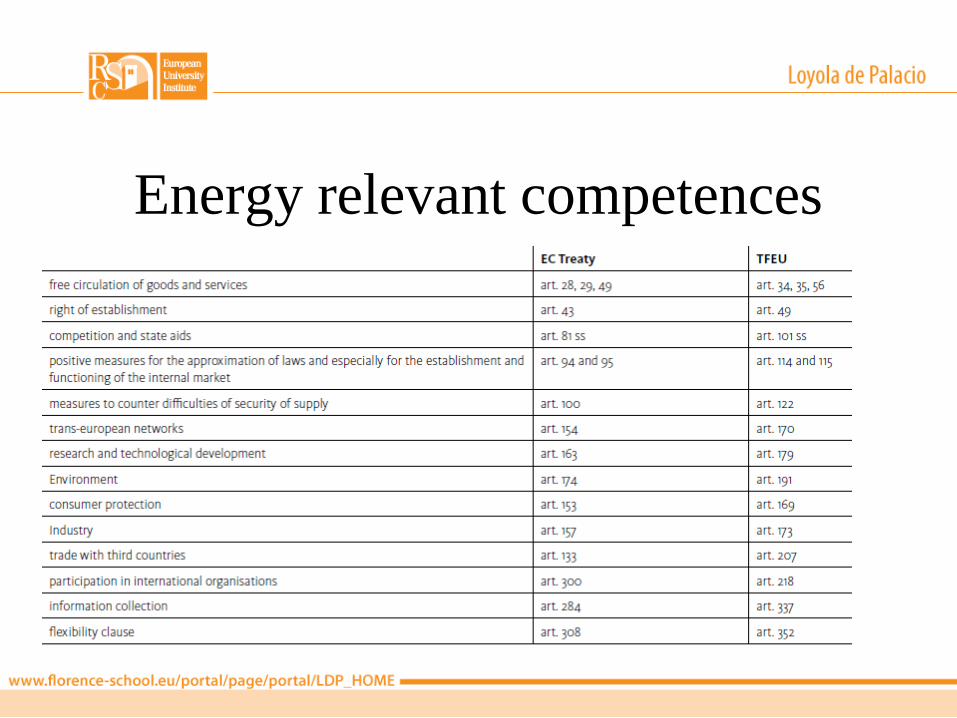

Energy relevant competences

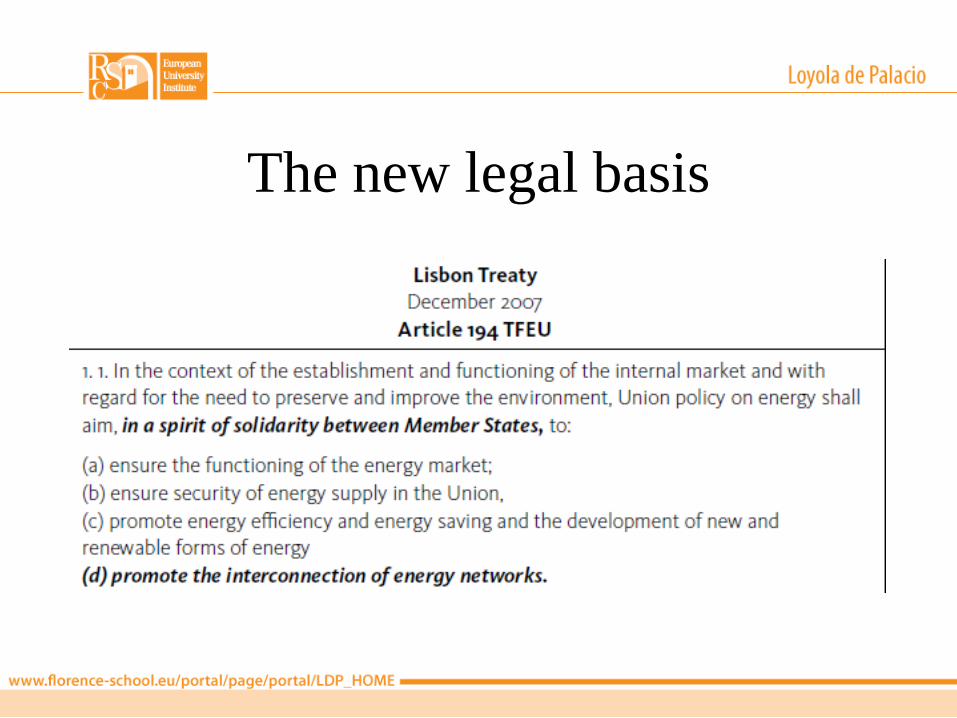

The new legal basis

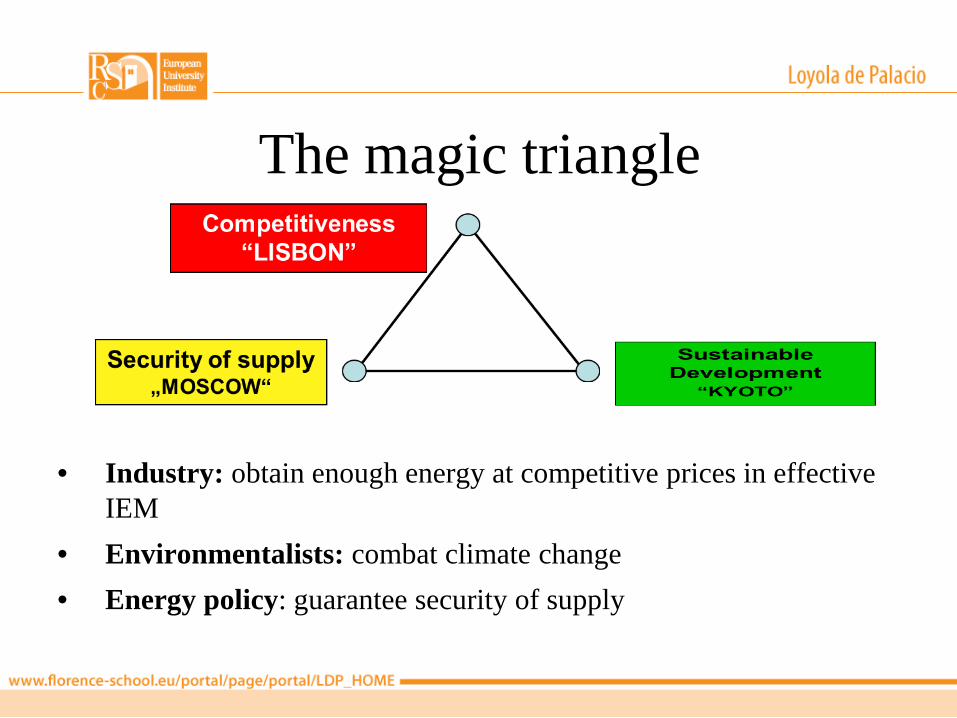

The magic triangle

• Industry: obtain enough energy at competitive prices in effective IEM

• Environmentalists: combat climate change • Energy policy: guarantee security of supply

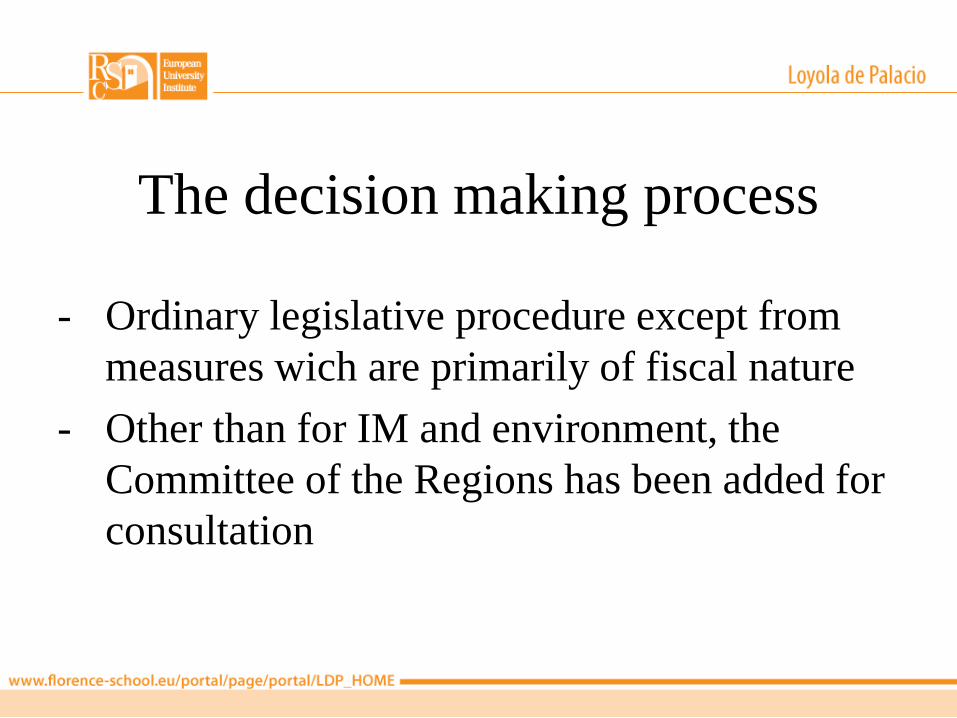

The decision making process

- Ordinary legislative procedure except from measures wich are primarily of fiscal nature

- Other than for IM and environment, the Committee of the Regions has been added for consultation

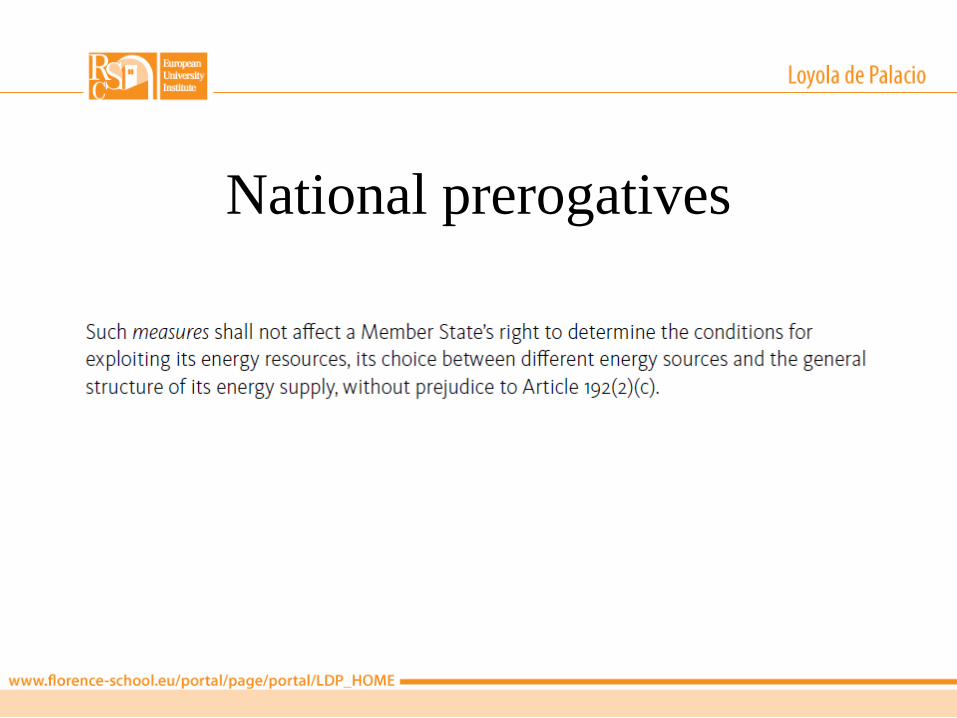

National prerogatives

The systemic role of Art. 194

How does Art. 194 interact with the other – mostly well established parts – of the TFEU?

⇒Derogation, a lex specialis? Choice of legislator?

⇒Founded on single legal basis: predominant purpose

Common market

• Lisbon: exclusive competence “customs union” and essential competition rules, but shared competence for the “internal market”.

• Art. 194 par. 1 distinguishes between the “internal” and the “energy” market. => energy includes external actions

Competition Policy

• Non-tariff barriers that stem from behaviour of private companies

• Eliminated according to the competition rules 101 TFEU

= exclusive competence; no room for Art. 194

Foreign energy policy 1

• Union exclusive competence for trade – including energy trade with third countries

• Given that legislation IEM provides complete set of rules for the operation of E/G markets – external competence also derives from here

• But: problems

Foreign energy policy 2

• Transparency 1st step • EC proposed 7th Sept 2011 “information

exchange mechanism with regard to intergovernmental agreements MS-TC”

• Based on Art. 194 (voluntary did not work/ “sincere cooperation clause” too general

So – new energy governance era?

• Not much added in substance • Success will be influenced by the national

derogation clause in practice • New reform initiative needed, European

strategy to make national desire for derogation disappear