Embed Size (px)

Citation preview

Strategies in FocusUBS Asset Management | Your global investment challenges answered.

For professional clients / qualified / institutional investors only

Special topic

A turning tide: An institutional shift toward active

Interview

Barry Gill, Head of Active Equities

Second quarter 2018

Publishing information Strategies in Focus is released quarterly by UBS Asset ManagementEditorial deadline: March 2018

Contributors Mohammad Ahmad, Erin Browne, Massimiliano Castelli, Barry Gill, Suni Harford, Dan Heron, Aleksander Ivanovic, William Kennedy, Lavonne Kuykendall, Mirka Luoto, Thomas Rose, Philipp Salman, Spencer Sheehan, and their teams.

Editor Lavonne Kuykendall

Design UBS Asset Management Creative Studio, New York

Coordination Beth Roberts, Kelly Vives

Contents

3 Overview Volatility returned with a vengeance in February, which has institutional investors looking for ways to take advantage of a changing market environment.

4 Global environment The equity market sell-off in early February was more technical than fundamental in nature, and we believe the overall environment is still supportive to global equities—which remain attractively valued relative to bonds despite rise in yields.

10 Investment themes and strategies

11 Toward normalization—the uneven path to growth In our view, the expected continued rise in US policy rates is likely to be modest and gradual. Against this backdrop, after a protracted period during which beta (the market) has dominated returns, we see a shift toward portfolio manager skills (alpha) playing a much greater role in generating returns.

14 Opportunities in emerging markets Several emerging markets countries are poised to outperform based on their GDP growth. However, country-level GDP growth alone does not always translate into improved investment returns. There are a number of additional factors to consider.

16 Low yield The low yield backdrop certainly presents challenges. But even in this environment, there is still a broad range of investment solutions that mean investors’ experiences do not have to be negative—even if some government bond yields still are.

18 Sustainable and impact investing Backed by our significant expertise, proprietary sustainability data, and a sophisticated research platform, we build tailored strategies for institutional investors that help them meet both their financial and sustainability requirements.

28 Interview: A view from the front line

Barry Gill, Head of Active Equities

32 Why UBS Asset Management

34 Contacts

20Special topic A turning tide: An institutional shift toward activeWe expect the slow withdrawal of liquidity to place upward pressure on asset price volatility, creating a particularly supportive environment for high-conviction active managers.

Case studies1. Pension funds: favoring the niche2. Sovereign wealth funds: exercising the active3. Institutional investors: seeking growth in

emerging markets and China

3

William KennedyHead Client Coverage

Aleksandar IvanovicHead Institutional Client Coverage

Overview

Dear investor,

After more than a year of market calm, volatility returned with a vengeance in February amid investor concerns about rising bond yields and inflation in the US. It was a reminder that even though the global economy continues its steady growth, increased volatility creates opportunities for active managers to capture alpha. This has struck a chord with institutional investors, who are already on the hunt for yield and returns in a low interest-rate environment.

We are fielding questions about a variety of active strategies as our clients and prospects seek our best ideas for increasing an existing active allocation, or for broadening the range of active strategies in their portfolios, or both. This issue’s special focus topic, “A turning tide”, offers examples of how different client segments are incorporat-ing active strategies today. Following that is an interview with Barry Gill, our Head of Active Equities, who shares his front-line perspective on how equity markets will react to a changing volatility regime.

“We are fielding questions about a variety of active strategies as our clients and prospects seek our best ideas for increasing an existing active allocation, or for broadening the range of active strategies in their portfolios, or both.”

Sustainable and impact investing continues to attract interest from both active and passive investors who are aware of the growing body of evidence indicating that companies that operate sustainably gain a long-term advantage over competitors.

UBS Asset Management has extensive global expertise across asset classes to address these investor needs.

As always, we are happy to discuss these themes with you to explore ways we can help craft a solution that meets your needs.

Best regards,

William Kennedy & Aleksandar Ivanovic

4

We devote significant time and resources to analyzing the economic and financial market trends that are the key drivers of asset prices. Macroeconomic and market views, as well as behavioral analysis, play an important role in our investment strategy setting process.

On the following pages, we outline our analysis of the global economy and assess the attractiveness of the different asset classes in this environment.

Erin Browne, Head of Asset Allocation

Global environment

5

Earnings growth the key support to equities

In a nutshell – Solid and synchronized demand growth, strong corporate earnings and a

moderate acceleration in inflation from low levels are key features of the global economy

– We expect the pace of policy normalization from major central banks to be gradual against this backdrop

– Overall environment still supportive to global equities—which remain attractively valued relative to bonds despite rise in yields

– Broader range of outcomes for key macroeconomic variables likely to mean moderately higher volatility regime in all major asset classes

– Protectionism, China slowdown, faster-than-expected rise in inflation and interest rates in the US remain the principal risks to global equity markets

Erin Browne is Head of Asset Allocation in the Investment Solutions team at UBS Asset Management. Erin drives our macro research, capital market assumptions, tactical asset allocation and strategic asset alloca-tion views across asset classes. She contributes to strategic research initiatives and plays an active role in designing investment solutions for clients. Erin was most recently Head of Macro Investments at O’Connor, managing cross-asset class portfolios, with a specific focus on currencies and equities. She joined UBS in 2016 and has 16 years of industry experience.

“The overall environment is still supportive to global equities—which remain attractively valued relative to bonds despite the rise in yields.”

Erin Browne

Solid and synchronized demand growth, strong corporate earnings and a pick-up in inflation from low levels have been the principal features of the global macroeconomic backdrop in 2018 to date.

Risk assets enjoyed a strong start to the year in January before a brief but violent spike in risk aversion in early February. The S&P 500’s 4.1% fall on February 5th was the index’s largest one-day drop in over six years, and the 20-point spike in the widely-watched Cboe Volatility Index (VIX Index), Wall Street’s so-called ‘fear gauge’, was the largest one-day percent-age or absolute rise in the VIX’s history.

In our view, the catalyst to the equity sell-off was very clearly investor concerns about rising bond yields and inflation in the US. Equally clear to us was that the degree of subsequent downward momentum in US equity markets in particular was more technical than fundamental in nature—and largely driven by portfolio rebalancing in the large pool of short volatility, target volatility and risk parity funds. The absence of comparable moves in other risk asset classes including high yield bonds further supports this view.

6

Rising yields not an end to the bull equity marketNonetheless, we have long identified a faster-than-expected rise in inflation and interest rates as the principal risk to equity markets. As confidence has grown that economic growth rates have broken free of the ‘lower for longer’ environment, developed world government nominal bond yields, most notably in the US, have recently risen to multi-year highs.

But in our view it is premature to see the recent re-pricing of bonds as the end of the equity bull market. And while we believe investors should stay vigilant, the rise in yields must be viewed in context of the broader macro backdrop and still low absolute levels of rates.

We believe it is also important to understand what precisely is driving yields higher: inflation expectations or real interest rates. The distinction is important as real rates are a better measure of the underlying expected monetary tightness in the economy. To-date the rise in US 10-year nominal yields has been largely driven by rising inflation expectations.

first place. As the year progresses and evidence of the strength of the economic recovery in both Europe and Japan builds, it is likely that the European Central Bank (ECB), and potentially the Bank of Japan (BoJ), will make their first steps down the long road to policy normalization. We will also be watching closely the rhetoric of new Federal Reserve chair Jerome Powell for early indications of any change in approach or policy regime.

It is also worth remembering that despite the rise in both short and long-term US nominal bond yields, overall financial conditions in the US and other major developed economies remain accommodative. The continued expansion of central bank balance sheets in Europe and Japan is more than offsetting the gradual reversal of the Federal Reserve’s quantitative easing program in the US.

Fiscal policy is also likely to play a more meaningful role in supporting growth going forward. There is the prospect of direct wage rises or tax cuts in major

Are these expectations now too high? In developed economies, output gaps are closing and we further expect wage growth to accelerate from its current low levels relative to unemployment. But the structural deflationary forces including aging populations and low productivity have not suddenly disap-peared. In our view, the combination of cyclical inflationary momentum and structural deflationary forces is likely to result in moderate increases in the overall consumer price environment in the US and other developed economies throughout 2018 and 2019.

Gradual policy normalization Against this backdrop we expect the process of policy normalization in developed economies to continue gradually. It is increasingly clear that central bank confidence in the sustain-ability of growth and inflation is edging higher. But we do not expect monetary policy-setters to react violently to early signs of a more normalized pricing environment when achieving it was an explicit goal of monetary policy in the

7

economies including Germany and Japan in addition to the major program of tax cuts already legislated in the US.

And the synchronized global growth impulse that was the defining macroeconomic feature of 2017 persists. The drivers of growth remain broad geographically and sectorally with the rise in corporate capital expenditure reducing the global economy’s prior reliance on consumption. Nonetheless, given the very strong readings of global Purchasing Managers Indices (PMIs), we expect the pace of acceleration to slow over the coming months and for lead indicators to moderate to a level consistent with slightly lower but still healthy demand growth.

Corporate profits to boost equitiesAgainst this backdrop we retain a positive view of global equities, which we believe will be largely supported in the year ahead by strong corporate earnings growth. We see scope for corporate profits to beat expectations across developed and emerging markets

elsewhere and despite the recent rise in bond yields, equities globally remain attractively valued relative to bonds. We place the greatest weight on this valuation metric over the medium-term.

While we believe that a moderate rise in inflation is positive for corporate earnings and for equities, it is important to acknowledge that the range of potential growth, inflation and interest rate outcomes in the developed world is broadening from the very narrow range investors have been used to. All else equal, this is likely to result in a moderate increase in the volatility regime for all asset classes.

Europe, Japan and emerging market equities preferredOn a number of measures US equities in aggregate look fully valued relative to their own history, but in our view US valuations are not sufficiently stretched to be concerning or to preclude further upside given the strength in earnings growth. The most recent corporate earn-ings season was among the strongest on

as tax reforms boost cycle-prolonging capex and capital returns to sharehold-ers in the US, and as operational gearing kicks in as the recovery accelerates in Europe, Japan and in Emerging Markets.

We also believe that moderately rising global inflation is more support than threat to global equity markets given the potential for higher earnings via higher revenue growth and margin expansion. We believe it would take nominal 10-year US Treasury yields between 3.5%–4% with no change to growth and inflation expectations to restrict growth or to start impacting the overall earnings environment in a meaningful way.

Clearly, inflation that rises suddenly and violently suggests meaningful macroeco-nomic imbalances that likely warrant stronger corrective policy action. But given structural deflationary forces we ascribe a low probability to this outturn. Historically, equities have struggled most when nominal 10-year yields adjusted for inflation are higher than real GDP growth. Currently there is still a healthy gap between the two in the US and

8

record, with 86% of reporting companies ahead of expectations.1 Share buybacks, rising dividends and corporate activity are also likely to be key supports. Recent data suggests that while the economic cycle in the US is maturing, the residual growth rate is solidly positive and that overall momentum remains strong.

Europe continues to be home to the most consistent positive economic data surprises on both the manufacturing and services sides of the Eurozone economy. ECB policy, improving consumer and business sentiment, accelerating credit growth and a healthier banking sector are all contributing to the recovery.

The recent strength in the euro may act as a short-term headwind to profits. Geopolitical risks persist. But operational gearing has played a key role in driving European earnings ahead of expecta-tions over the past year. We believe that there is further to go in this process as the recovery continues and margins continue to grow.

Elsewhere, better-than-expected trade has helped propel demand growth in emerging markets (EM). While inflation is inflecting higher, we do not see it climbing sufficiently to warrant any major tightening from the present accommodative monetary stance. Importantly in our view, capex is starting to pick-up and there are strong arguments that EM are at an even earlier stage of their recovery than Europe. The China slowdown has not been as material as feared and despite their outperformance in 2017, we believe EM equities remain attractively valued relative to their own history

willing to move before the European Central Bank. Meanwhile, the Eurozone economy also continues to display strength and rate expectations reflected in German bund yields appear too modest in light of this backdrop.

Within credit markets, we do not expect any material pick-up in corporate debt defaults in the near-term given the strength of demand growth, cash-rich corporate balance sheets and still-loose financial conditions in developed economies. However, we do not view the risk/reward trade-off as sufficiently attractive within either Investment Grade or High Yield debt to warrant a positive stance after recent spread compression.

The one area within the credit universe that stands out to us from a more positive perspective is emerging market debt. The spreads between local currency and USD-denominated EM debt and US treasuries also remain low by historical standards. But in a world of low rates we see continued strong demand for EM debt’s attractive real yield.

Major risksThe major risks to market equilibrium have not changed materially in our view. As we have outlined, rising inflation and bond yields are not inconsistent with equity market progress. Equity markets globally posted strong returns in 2017 in the face of rising US interest rates and higher US 10-year nominal bond yields. They did so because of the strength of the demand environment and corporate earnings growth. These two fundamental supports remain in place. In our view, it is both the pace of change and the scale of change in inflation expectations and bond yields that

and to international peers given the strength of corporate earnings. EM economies and profits are also significant beneficiaries of a weaker US dollar.

The combination of accelerating economic recovery and attractive valuations supports a similarly constructive view of Japanese equities. In our view, Japanese equities are not priced for a sustained improvement in profitability despite the continued positive impact of improving corporate governance and the potential for further improvements in ROEs and margins. With the Japanese government nominating Haruhiko Kuroda for a second term as governor of the Bank of Japan, monetary policy is likely to stay highly accommodative despite the improvement in recent data. We expect fiscal stimulus to play a greater role in supporting Japanese growth going forward.

US Treasury yields attractive on a relative basisIn bond markets, we expect a degree of consolidation around the 3% level in nominal 10-year US Treasury yields. In the absence of a material pick-up in inflation, US 10-year yields are likely to remain range bound. However on a relative basis, US yields continue to look attractive in comparison to most other developed government bond markets. In particular, Swiss and German govern-ment bonds continue to look overvalued and, in our view, have an increasingly asymmetric risk profile. The Swiss economy is relatively strong and we see Swiss bonds as vulnerable to attempts to normalize monetary policy by a Swiss National Bank increasingly concerned by the strength of the housing market and

1 Source: S&P 500 4Q2017 Earnings Wrap up, Alliance Bernstein (as at 20 February 2018).

9

matters to investors. Any build-up of evidence that the inflation environment is materially stronger than markets currently discount and that warrants both a faster pace of policy tightening to a higher terminal rate is likely to trigger further volatility in risk assets.

Geopolitical risks in the Eurozone have dissipated but have not disappeared. With the Italian elections and German coalition vote now concluded, we point outside of the Eurozone to the potential

Our views on China are unchanged. The pace of reform to address high debt levels, pollution and capital inefficiency has accelerated. But the Chinese authorities face a difficult balancing act in sustaining a smooth demand trajectory as China transitions to a higher value, more service- oriented economy.

for rising trade protectionism as the biggest immediate geopolitical threat to global growth and markets. While ultimately we believe that the world’s largest economies are still pro-trade, the risks of a major international trade war have increased in the wake of recent announcements that the US intends to impose import tariffs on steel and aluminum, and further tariffs on targeted Chinese exports to the US in response to alleged intellectual property theft.

Overall signal =

NegativePositive

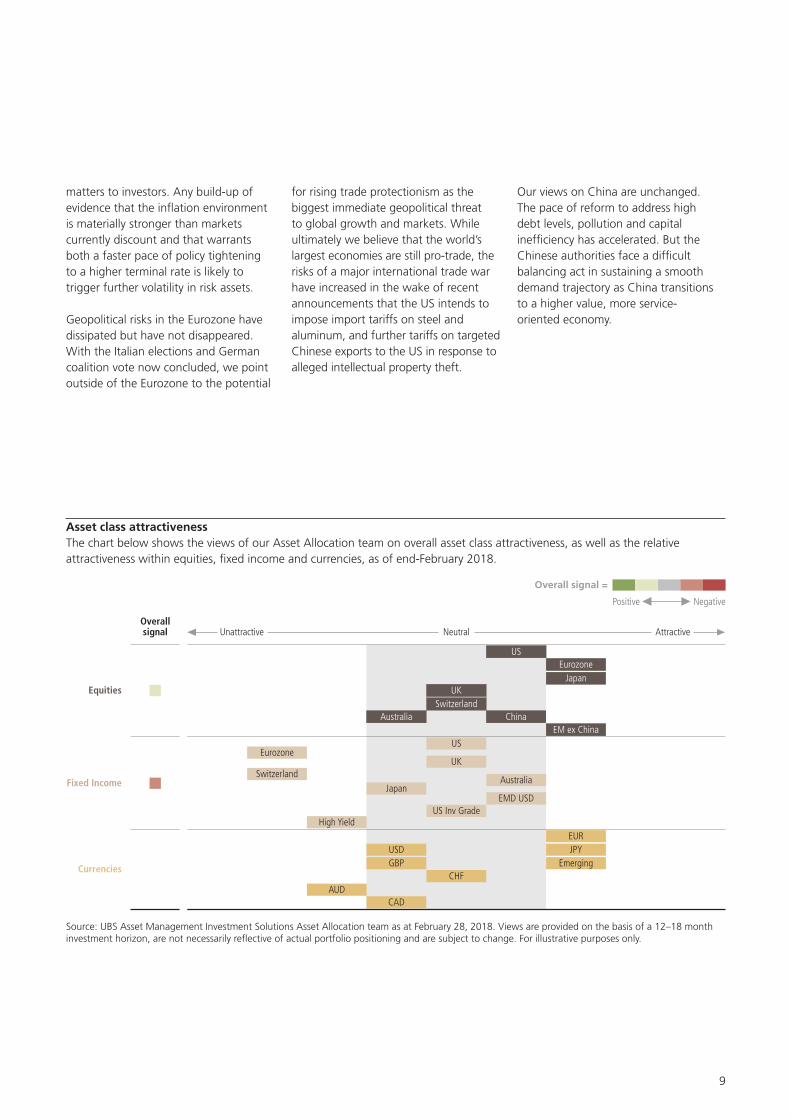

Asset class attractivenessThe chart below shows the views of our Asset Allocation team on overall asset class attractiveness, as well as the relative attractiveness within equities, fixed income and currencies, as of end-February 2018.

Source: UBS Asset Management Investment Solutions Asset Allocation team as at February 28, 2018. Views are provided on the basis of a 12–18 month investment horizon, are not necessarily reflective of actual portfolio positioning and are subject to change. For illustrative purposes only.

Equities

Neutral AttractiveUnattractiveOverallsignal

Fixed Income

Currencies

SwitzerlandChinaAustralia

Eurozone

Switzerland

High Yield

AUD

US

UK

US Inv Grade

Australia

EMD USDJapan

CHF

USDGBP

CAD

EUR

EmergingJPY

JapanEurozone

EM ex China

UK

US

10

Thomas Rose, Sales Offering

Investment themes and strategies

On the following pages, we present four medium- to long-term themes that we think matter to institutional investors.

As you look to navigate and capitalize on these themes, we are here to help answer your investment challenges by leveraging the depth and breadth of our active, passive, multi-asset and custom solution investment offerings.

11

Thomas Rose is responsible for UBS Asset Management’s Sales Offering. He joined the Economics department of the then Swiss Bank Corporation (SBC) in 1989. From 1995 he held different roles at UBS Asset Management. Thomas has spent his entire 28 year working career in the financial industry.

Toward normalization—the uneven path to growth

“Since excess liquidity has helped dampen market price swings and support risk assets, it seems only logical that its partial reversal may prompt a shift to a moderately higher market volatility regime.”

Thomas Rose

Risk assets had a strong start in 2018 until an equity sell-off in early February ended a long period of abnormally low volatility. We see the overall environment as still positive for equities. The gradual journey towards monetary policy normalization continues to be under-pinned by broad-based growth across the global economy. In 2017, the demand recoveries in both the Eurozone and in emerging markets gathered pace, while the US economy also strengthened despite rising interest rates. China’s transition from over-leveraged manufac-turing hub to a more diversified economy also has progressed more smoothly than many had expected. The breadth of the demand drivers—by geography and by sector—reduces the likelihood of a sharp reversal.

Monetary policy globally is also likely to remain accommodative for at least the first half of 2018 as on-going quantita-tive easing (QE) programs in Europe and Japan more than offset the slow reversal

of QE in the US. And while the Federal Reserve (Fed) is likely to continue raising short-term interest rates, we expect them to do so relatively gradually. Fiscal policy globally is also likely to play a more significant role in supporting demand globally in 2018. We see this backdrop as supportive to global growth and to global equities.

However, while 2017 was largely free of significant adverse shocks in geopolitics, demand or markets, we believe investors must face the reality of an investment journey that is unlikely to be as smooth going forward. We believe that there is further upside to global equities, but also believe returns from equity markets, while positive, may be more constrained than has been the case in recent years.

We do not ascribe a high probability to a full blown trade war.

12

The withdrawal of liquidity and the partial reversal of QE processes globally are likely to be gradual and well communicated to avoid shocking markets—as it has already been in the US. However, since excess liquidity has helped dampen market price swings and support risk assets, it seems only logical that its partial reversal may prompt a shift to a moderately higher market volatility regime.

Trade war worries and the erratic nature of US foreign policy are currently weighing on investor sentiment. We believe both the US and China are fundamentally pro trade. Both have left room for negotiation in the recent spat over intellectual property theft. But while we do not ascribe a high probabil-ity to a full blown trade war, the risks of major policy mistake have clearly risen.

Additional possible bumps along the road include the potential for higher inflation. We believe that there are structural forces weighing on inflation including ageing populations. However, as output gaps close and as very low unemployment in the developed world

starts to squeeze wages higher there is clearly the potential for consumer prices to rise. In China, we believe that authorities have a range of policy tools available to them to smooth the country’s economic transition—but note that there is still the possibility of a sharper-than-expected short-term slowdown as welcome regulatory improvements are imposed on China’s ‘shadow’ banking sector and high debt levels are addressed more forcibly.

Finally, while monetary policy globally remains accommodative, it is on the long road to normalization. As the year progresses it will likely slowly shift to a less accommodative bias.

Toward normalization—the uneven path to growth (cont.)

How to capture the ‘normalization’ theme

Possible solutions that can help you invest in the benign market backdrop due to moderate reflation, and in answering the growing importance of portfolio manager skills (alpha) to generate returns, include global systematic equity, merger arbitrage, infrastructure, US real estate, private equity strategies, and co-invest special opportunities strategies.

13

Example strategies

Global Systematic EquityOur Global Systematic Equity strategy follows a model-driven, quantitative approach to build a diversified global portfolio of large- and mid-cap equities. The strategy aims to provide consistent alpha over time with moderate levels of active risk. Within their investment process the team uses a proprietary multi-factor stock selection model based on fundamental company data to identify stocks which are expected to outperform their peers over the medium to long term.

Merger ArbitrageOur Merger Arbitrage strategy seeks to generate attractive risk-adjusted returns and low correlation to equity and credit markets by investing in securities involving corporate actions. The merger arbitrage investment team evaluates a global universe of M&A deals based on deal and risk specifics, which informs the portfolio construction process. As deal specifics evolve and the market digests announcement and activities, the grading process allows the team to shift risk allocations in the portfolio in an effort to protect capital and minimize drawdowns in performance.

US Real Estate—Enhanced Risk/Return Our US real estate business has a long history of value creation strategies with risk profiles ranging from acquiring buildings with significant vacancy and completing release, through to participa- tion in ground-up development joint ventures. We use a research-driven market selection that responds to changing regional and property-type market conditions to assess acquisition and disposition opportunities. We identify investments that are distressed or poorly capitalized, controlling and recapitalizing assets through the purchase of debt or equity positions, and benefiting from improved manage- ment and anticipated improvements in market conditions. The ongoing, long-term aim of the strategy is to produce attractive risk-adjusted returns.

Private EquityOur Private Equity strategy aims to invest in managers who focus on mature market leading growth companies, particularly those operating in segments that will not suffer in a low-growth environment. Based on our extensive experience and a selective, proven investment process, we target access- restricted private equity managers with longstanding and well-established track records. This focused global investment solution, with a well-diversified portfolio from a regional, sector, stage, style and vintage year perspective, is capable of weathering various economic cycles.

Co-Invest Special OpportunitiesThe strategy is a dedicated portfolio of hedge fund co-investments that will provide targeted exposure to select hedge funds’ highest conviction ideas. It will have the unique ability to utilize a wide range of investment types, trade structures and asset classes, including opportunities across the liquidity spectrum. A drawdown structure will be utilized to seek to limit cash drag and provide just-in-time capital deployment as opportunities present themselves.

InfrastructureThis strategy offers exposure to global infrastructure through investments with leading infrastructure managers. The strategy’s focus is on specialized managers, adding value through a regional or sector specialization and active management. The investments also include niche strategies such as small and mid-cap infrastructure. The focus is on operating assets with a recurring dividend yield, mainly in developed markets (OECD), with selective exposure to other markets. The strategy also covers investments with an expansion or growth component, and aims to provide a broad-based exposure to this asset class.

14

Opportunities in emerging markets

Are emerging markets vulnerable to US and developed world central bank policy, or are they backed by sufficiently powerful secular forces to suggest that the benign environment of the past two years may only be the start of a longer-term positive trend, under- pinned by a positive broad-based and improving global economic upswing?

Perhaps unsurprisingly for an investment universe with high levels of hard currency debt, emerging markets have historically shown a high sensitivity to the US dollar. However, we believe that the peak stress to US dollar strength lies behind us. 2017 surprised on several fronts: stronger and more balanced global growth, positive news from Europe, plus a strengthening euro. This stronger global growth, combined with expectations of very moderately rising interest rates across developed markets (which in turn implies confined debt servicing costs), is supportive to emerging market asset prices.

Until mid-2016, global developed markets experienced low economic growth and persistently low inflation. The ongoing upswing of global growth and moderate reflation are likely to benefit emerging markets which suffered during the years of weak growth. The current brighter growth outlook suggests a preference for investment themes which profit from an economic expansion.

From our perspective, several emerging markets countries are poised to outperform based on their GDP growth. However, country-level GDP growth alone does not always translate into improved investment returns. There are a number of additional factors to consider—for example, the strength of local corporate governance and the impact this may have on performance.

One example of a secular investment theme which specifically benefits many emerging market countries is their growing youthful and tech-savvy populations, whose incomes and propensity to consume are steadily rising. This, combined with a good supply of investible companies from different sectors, creates compelling investment opportunities.

We see consumer spending, healthcare, real estate, and information technology as the key growth themes in emerging markets.

However, the environment is dynamic. It is influenced by various diverging growth trends, and faces many political and economic challenges including industri-alization and the digital revolution. We therefore believe that an active country, sector and security selection, based on exhaustive top-down and bottom-up research, is a prerequisite to add value to emerging markets portfolios.

How to capture the ‘emerging markets’ theme

Examples of strategies that provide exposure to opportunities in emerging markets by well-informed decision-making are China equity, emerging markets equity high alpha, and emerging markets debt passive.

Strong global growth and low debt servicing costs are supportive for emerging markets

Active selection based on in-depth research is key

15

Example strategies

China Equity OpportunityChina Equity Opportunity is an actively managed strategy with a concentrated portfolio, investing mainly in selected Chinese companies with long-term structural growth potential. The portfolio is well positioned in sectors that are likely to benefit from ongoing structural reforms in China. These reforms are opening up new markets and segments in the economy to development and growth.

Emerging Markets Equity HALOOur Emerging Markets Equity HALO (High Alpha Long-Term Opportunity) strategy is a concentrated and unconstrained portfolio, investing in emerging markets, using a disciplined, fundamental investment process based on bottom-up stock selection. It comprises the best stock ideas identified by our team of seasoned investment specialists, who have a proven track record. We believe in long-term, fundamental bottom-up investing in quality companies at a reasonable valuation. Our approach means we pay great attention to investment fundamentals and expected cash flows when assessing investments as well as the quality of the underlying companies. Our investment process is highly flexible, taking focused views on significant opportunities that seek to provide higher returns.

Emerging Markets Debt PassiveOur Emerging Markets Debt Passive strategies invest in emerging markets sovereign and/or emerging markets corporate debt. Their aim is to benefit from improving economic and political conditions in emerging markets. Benchmark replication is based on stratified sampling. Given that trading costs are not mirrored in the bench- marks the portfolio management team strives to achieve an attractive perfor- mance by keeping turnover low and trading as efficiently as possible.

16

Low yield

Low yields have presented a significant challenge to investors for a number of years. With nominal 10-year US Treasury yields not far from 3%, the US economic cycle is clearly more mature than other developed nations, even if yields are well below the average of past recovery peaks. While the positive broad-based global upswing likely to continue, we expect yields to slowly grind higher in Europe (and to lesser extent in Japan) for the foreseeable future.

In our view, there are three paths which could offer potential returns to investors, while endeavoring to avoid assets with low yields and possibly negative returns.

These include:

– adding to higher yielding bond strategies with floating rate exposure to give protection from rising interest rates and an attractive yield pick-up relative to developed world government bonds

– within equities, a focus on unconstrained strategies capable of generating returns in differing environments due to more active and flexible investment approaches

– increasing exposure to alternative asset classes, such as hedge funds, real estate, and infrastructure, which can help to improve the overall risk-adjusted return potential of investors’ portfolios

In summary, the low yield backdrop certainly presents all investors with challenges. But even in this environ-ment, there is still a broad range of investment solutions that mean inves-tors’ experiences do not have to be negative—even if some government bond yields still are.

How to capture the ‘low yield’ theme

We see strategies across the fixed income, hedge fund as well as real estate and private markets space with which you can navigate the low yield environment. These include high yield credit, single manager multi strategy, broad-based neutral strategies, global and US real estate as well as infrastructure debt.

Yields are still at low or negative levels and we expect them to stay low

17

Example strategies

Euro High YieldOur Euro High Yield strategy is aimed at delivering higher yields and a steady income stream, anchored in fundamen- tal credit research. The investment style is defined by a rigorous investment process supported by our global research platform, local presence and strong risk management capabilities. The strategy employs a fundamental research-driven approach that draws on the extensive experience of our portfolio managers to combine top-down relative value views with bottom-up security selection.

Broad-based Neutral Strategies*Our Broad-based Neutral Strategies solution generally allocates to alternative investment strategies specializing in Credit, conservative Equity Hedged, Multi-Strategy, Relative Value, and Trading strategies. It strives to achieve risk-adjusted capital appreciation over the long term, while seeking to maintain zero to low correlation to traditional asset classes, and low volatility over an economic market cycle (typically 3 to 5 years). The investment team reallocates the portfolio as market opportunities arise with the intention of capturing positive returns from different asset classes when these present opportunities, while attempting to reduce downside risk when conditions are not as favorable.

Global Real EstateOur Global Real Estate strategy provides diversified exposure to core real estate globally. It invests predominantly in the office, retail, logistics and residential sectors. Investor benefits include the experience, local capabilities and network of our Global Real Estate Multi-Manager team, as well as the characteristics of the generated returns, such as low correlation and global diversification.

US Real Estate—Income Oriented Our US Real Estate income oriented capability provides a wide array of real estate and farmland investment management services to clients. The business focuses on core strategies ranging from acquiring existing, well-leased investment properties to investments in operating farmland. Our investment strategy is based on research that combines broad market and economic trends with property pricing and forecasts of future economic performance. We believe that a well-conceived real estate investment program recognizes long-term economic and real estate trends, capitalizes on short-term pricing opportunities, efficiently uses diversification to minimize risk, manages each investment as an operating business, and sells assets on a timely basis to enhance perfor- mance. The ongoing, long-term aim of our strategies is to produce attractive risk-adjusted returns.

Infrastructure Debt—Senior Secured Our Infrastructure Debt—Senior Secured strategy invests in private senior secured credit of infrastructure companies and projects predominantly located in European investment grade countries, targeting those that offer a significant pick-up in return versus comparable (same risk rating and tenor) listed corporate bonds. Senior secured infrastructure debt generally shows superior credit characteristics (lower default rates and higher recovery values) and less rating volatility than equivalent- ly rated corporate credits and so can offer diversification to traditional corporate fixed income investments. The investment team targets attractive risk/ reward opportunities leveraging its dedicated origination capabilities, sector experience, structuring skills and rigorous credit analysis.

*No such product is currently available for EU residents.

18

Sustainable and impact investing

Sustainable investing is about broadening the use of material, non-financial data in the investment analysis process to include ESG—or environmental, social and governance—metrics. Incorporating these metrics helps investors take a broader view of the potential upside and downside of their investments and so make better informed investment decisions.

Sustainable investing can provide a new kind of transparency for our invest-ments—achieved through new metrics that offer material, often quantitative, insights into how well a business is run, where its real risks lie, and how sustain-able its business model and practices really are. If fully embedded in the investment decision-making process,

these metrics can be powerful tech-niques. This is certainly the case with the ESG criteria mentioned above. Sustainable investing at its best can give investors a forward-looking perspective, providing insights into those qualitative aspects of a business, both good and bad, that further down the line may very well influence the decisions and perceptions of both customers and the public; decisions and perceptions which can ultimately impact that business’ bottom line.

In our view, it is the integration of material sustainability information within our financial analysis and investment process that provide those unique insights into the long-term risks, opportu-nities and competitive advantages of companies. How do we approach integration? Building on a strong legacy of over twenty years’ sustainable investing experience, our dedicated SI research team works closely with our equity and fixed income analysts to incorporate extra-financial information in analyses and investment decisions.

They draw on the most material sustainability data and information and then add their own knowledge of industries and companies to derive a proprietary and forward-looking view of how sustainability impacts financial performance.

Rather than employing sustainability information simply as a screen, based on reported data and historical information, we focus on the future impact that sustainability performance will have on long-term financial performance. It is our belief that this approach results in more holistic and better informed views of how a company will perform over time. In this way, we believe sustainable investing can add value to portfolios within the same risk-return profile.

How to capture the ‘Sustainable and impact investing’ theme

We offer a broad set of sustainable strategies and solutions designed to cater for the needs of institutional investors. These include, amongst others, climate aware rules-based global equity and global sustainable equity strategies.

Sustainable investing provides a new kind of transparency for our investments

We believe sustainable investing can add value to portfolios within the same risk-return profile

19

Example strategies

Climate Aware Rules-based Global EquityOur Climate Aware Rules-based Global Equity strategy is based on a proprietary methodology. By combining environ-mental data from several sources, we have developed a portfolio optimization model which reduces exposure to climate risk while simultaneously maintaining the restrictions on tracking error. Rather than simply reducing exposure to companies with higher CO2 emissions, the team also examined the trajectory of emissions reduction over time, as well as the commitment of company management toward emis-sions reduction, to orient the portfolio toward those companies that are better prepared for a low carbon future and

mitigation of global warming as outlined in the United Nation’s Paris Agreement. Moreover, the strategy reduces the exposure to, rather than excludes companies with higher carbon risk in order to minimize risks by not excluding significant parts of the market.

Global Sustainable EquityOur Global Sustainable Equity strategy invests worldwide in attractively valued companies that score high in financially material sustainability criteria. We believe that combining traditional financial valuation discipline with sustainability analysis enhances the possibilities for value-added returns.

Global Impact Equity Our Global Impact Equity strategy invests in companies that provide solutions via their products and services to significant global challenges such as climate change, air pollution, clean water and water scarcity, treatment of disease, poverty alleviation and food security. Our investment philosophy combines our bottom-up fundamental research, rigorous sustainability analysis with our unique science-based impact measurement methodology. The strategy intends to demonstrate a positive impact on human well-being and environmental quality.

20

21

A turning tide

Special topic

By Suni Harford, Head of Investments, UBS Asset Management

An institutional shift toward active

A view from the top

The global economy remains in good health. Monetary policy conditions, in aggregate, are still accommodative and we believe global recession risks are low. With corporate profit growth strong and likely to remain so, the overall environment remains, in our view, a positive one for global equities in particular. But there are clearly some important shifts taking place within markets, at the heart of which is the shifting narrative on inflation and interest rates in the developed world.

22

Moderate rises in inflation and interest rates have not prevented equity markets from rising in the past. But the range of potential growth, inflation and interest rate outcomes in the developed world is diverging from the ‘lower for longer’ narrative of the past several years. All else equal, this is likely to result in an increase in the volatility regime for all asset classes.

We don’t believe that this is just a short-term change in macroeconomic and market dynamics. The liquidity provided by central banks under quantitative easing programs has also been a key factor in keeping asset price volatility low. While we expect the process of policy normalization to be gradual and well communicated—and for central banks to retain significantly larger balance sheets than they had

prior to the financial crisis—the slow withdrawal of liquidity will place upward pressure on asset price volatility, albeit gradually.

The upside of volatilityWe see these shifts as creating a particularly supportive environment for high-conviction active managers.

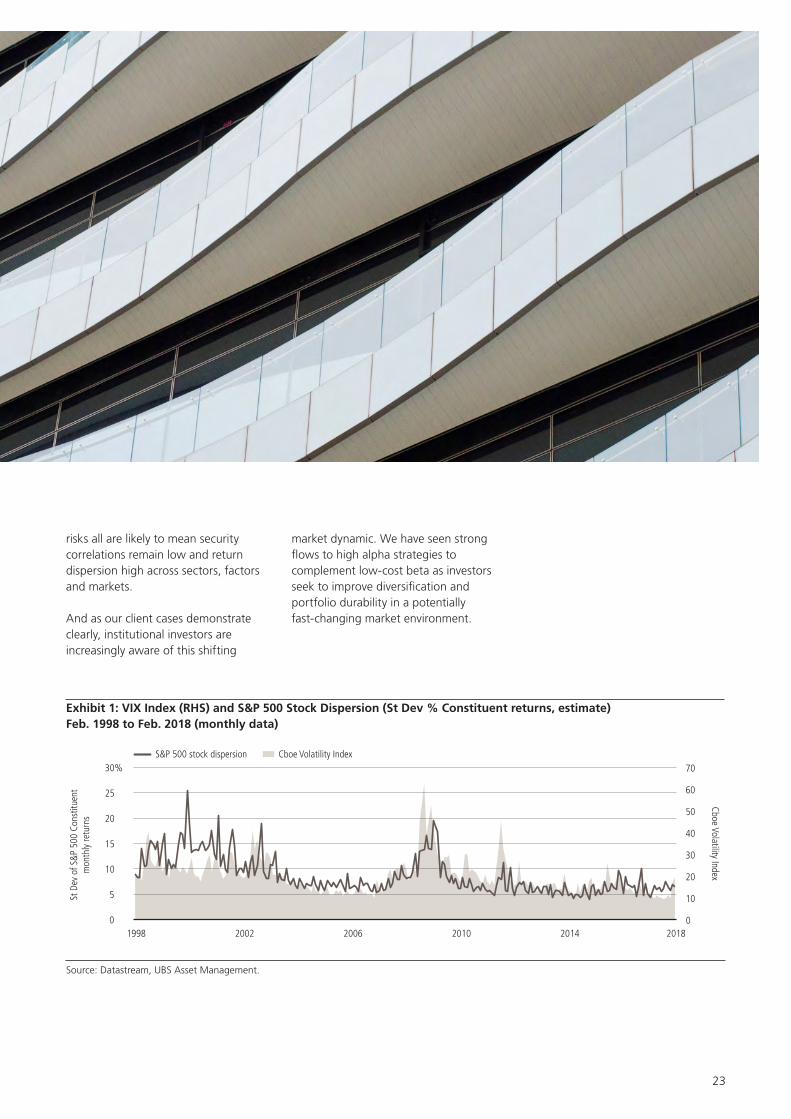

It is probably self-evident that the scope for active managers to add value is determined first and foremost by the scale of the opportunity set. For active managers, that opportunity set is largely determined by two statistical measures: security correlation and security dispersion. If all stocks move in the same direction (correlation) and the difference between returns (dispersion) is low, the potential to generate returns that are significantly different to the underlying index is limited.

With competing macroeconomic narratives, we expect stock return dispersion to follow index volatility higher. It is already beginning to do so. Like the rise in equity index volatility, we do not expect an increase in stock return dispersion to be short-lived. Our historical analysis shows that dispersion regimes have tended to persist over multi-year periods. (See Exhibit 1.) This suggests that the opportunity set for active managers to generate excess returns—and for higher conviction active managers in particular—is likely to be extensive over the coming years. Now is the time for institutional investors to look at the active side of their investment strategy.

At a lower level, geopolitics, fiscal policy, technology disruption, demo-graphics, changing consumer habits, plus a whole plethora of idiosyncratic

23

Exhibit 1: VIX Index (RHS) and S&P 500 Stock Dispersion (St Dev % Constituent returns, estimate) Feb. 1998 to Feb. 2018 (monthly data)

risks all are likely to mean security correlations remain low and return dispersion high across sectors, factors and markets.

And as our client cases demonstrate clearly, institutional investors are increasingly aware of this shifting

market dynamic. We have seen strong flows to high alpha strategies to complement low-cost beta as investors seek to improve diversification and portfolio durability in a potentially fast-changing market environment.

Source: Datastream, UBS Asset Management.

0

10

20

30

40

50

60

70S&P 500 stock dispersion

0

5

10

15

20

25

30%

201820142010200620021998

Cboe Volatility Index

St D

ev o

f S&P

500

Con

stitu

ent

mon

thly

retu

rns

Cboe Volatility Index

24

Large pension funds typically take a sophisticated core-satellite approach to portfolio construction. These investors look for active managers who can add value that can’t be replicated by their passive index holdings, and will adjust allocations in response to market changes. Over the past several quarters, merger arbitrage strategies that trade on announced corporate mergers have attracted interest as a potential alpha generator.

As close observers of market trends, the long-lived bull equity market already has these investors looking for downside protection and investments that are less correlated to other asset classes. The return of market volatility in early 2018 has also made an impression on these investors. We have met with a number of pension fund investment boards that are adding niche active trading strate-gies to their existing active allocations to further diversify their portfolios.

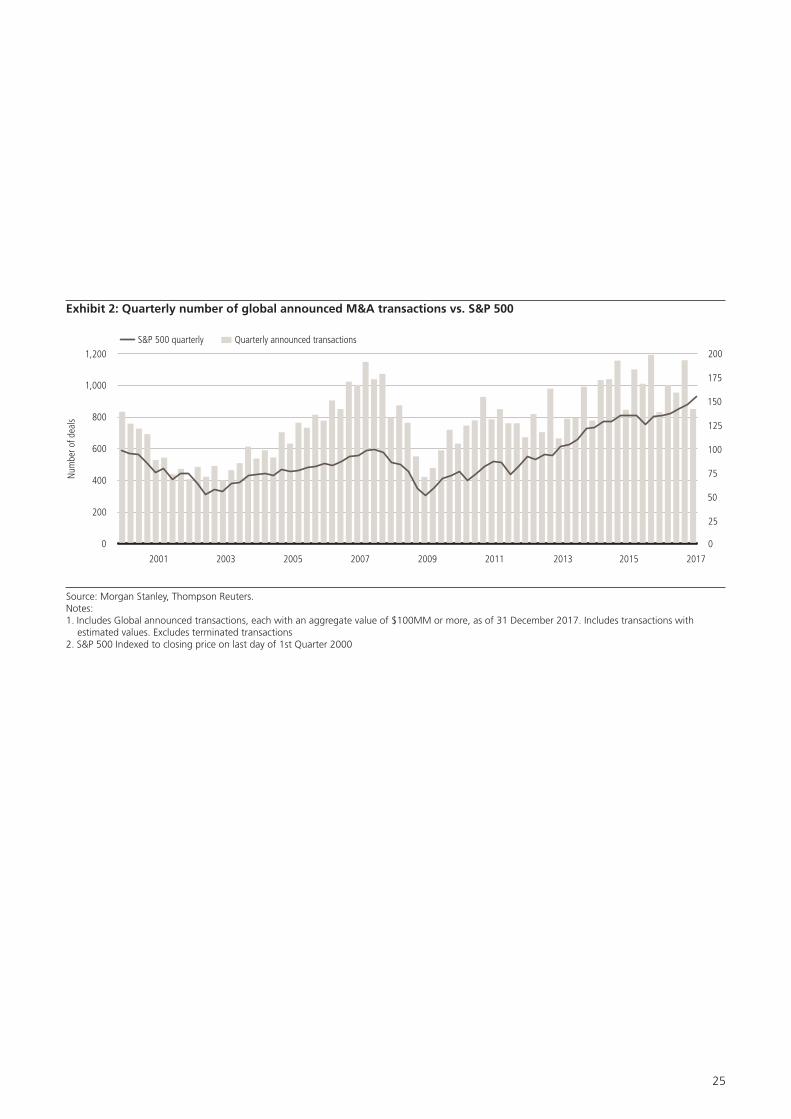

Steady economic growth and a strong equity market has supported mergers and acquisitions (M&A) activity over the last few years, providing a steady supply of deals to evaluate for merger arbi-trage. (See Exhibit 2.) Investors are drawn to a strategy that is less of a

‘black box’ than other active trading strategies and one that can offer relatively uncrowded trading opportuni-ties. The strategy historically exhibits downside protection and low equi-ty-market correlation. We have spoken to a number of pension fund managers who are either considering an allocation or have recently allocated to a merger arbitrage strategy.

The passage of US tax reform is expected to be a strong driver for merger activity going forward, providing a large selection of deals for an active strategy. The US Tax Cuts and Jobs Act reduced corporate taxes to a top rate of 21% from the previous 35%, and

created powerful incentives for the repatriation of overseas funds. US companies have kept their ex-US cash balances offshore to avoid paying high US corporate tax rates, and many have already announced plans to repatriate the cash, giving a boost to balance sheets.

Combined with a supportive market backdrop—including resurgent global economic growth and a healthy deal environment in Europe—skilled manag-ers have the opportunity to take advantage of what we believe is the most attractive merger environment in many years.

1 Case study:

Pension funds: favoring the niche

“We have met with a number of pension fund investment boards that are adding niche active trading strate gies to their existing active allocations to further diversify their portfolios.“

25

Exhibit 2: Quarterly number of global announced M&A transactions vs. S&P 500

Source: Morgan Stanley, Thompson Reuters.Notes:1. Includes Global announced transactions, each with an aggregate value of $100MM or more, as of 31 December 2017. Includes transactions with

estimated values. Excludes terminated transactions2. S&P 500 Indexed to closing price on last day of 1st Quarter 2000

Quarterly announced transactionsS&P 500 quarterly

Num

ber o

f dea

ls

0

200

400

600

800

1,000

1,200

201720152013201120092007200520032001

0

25

50

75

100

125

150

175

200

26

2 Case study:

Sovereign wealth funds: exercising the active

The ‘Goldilocks’ environment has seen supportive monetary policy drive volatility down to historic lows while steadily lifting equity indices. As that era comes to a gradual end, active managers have more opportunity to make a pronounced difference.

Sovereign institutions are keenly aware of the growing attractiveness of active strategies, and are taking a closer look at their portfolios. Sovereign wealth funds typically invest the bulk of their assets into passive strategies coupled with satellite high-octane differentiated active strategies aimed at adding alpha. Now, some sovereigns are diversifying their allocations across a more broad range of active alternative assets and concentrated, high-conviction equity strategies than they have been using.

One sovereign wealth fund client whose active allocation was held primarily in direct investment private equity assets, decided to invest in a broader range of alternative assets. More recent allocations went to active and illiquid alternative investments including infrastructure debt, venture capital and multi-strategy hedge fund strategies. For illiquid alternatives, they favored liquidity terms to match their liability profiles and sought investments that are uncorrelated to public equity markets.

With return expectations on the decline, sovereign investors we talk to are looking for ways to match investment liquidity to their individual needs. Customized co-investment strategies are attracting increased interest. Sustainable investing principles are also gaining traction among sovereign investors as evidence grows that sustainability data may be an early indicator of long-term outperformance.

“With return expectations on the decline, sovereign investors we talk to are looking for ways to match investment lock-up periods to their individual needs.“

27

3 Case study:

Institutional investors: seeking growth in emerging markets and China

Institutional investors are interested in the strong growth opportunities across emerging market countries. Within emerging markets, China’s moves to liberalize its financial markets have opened up a new opportunity set for global institutional investors. Our client, a major, Asia-based institution, wanted to get exposure to the growth story playing out there.

Bin Shi’s China-focused equities team delivered an active investment strategy focusing on Chinese companies that are either leading, or have the potential to lead, their sectors. Our clients found this highly rewarding, particularly because it allowed them to participate in the rapid growth in onshore markets, during which our strategies have delivered excellent outperformance.

Information contained herein is for informational purposes only and does not constitute investment advice or a recommendation to invest in any strategy or securities nor does it take into account the particular investment objectives, financial situations, or needs of any individual prospective investor. Investors should seek professional investment and tax advice.

“China’s moves to liberalize its financial markets have opened up a new opportunity set for global institutional investors, and our active strategies have delivered excellent results.“

28

View from the front line

An interview with Barry Gill, Head of Active Equities, UBS Asset Management

Barry, given the heightened volatility and market uncertainty so far this year, what approach have you been taking to managing your global equity book?While timing a rise in volatility is difficult, it was not unexpected given the combination of rich valuations, acceler-ated recent market price appreciation

and a slow but significant change in the monetary policy regime. But volatility, within bounds, is good for active managers because it creates mispricings we can take advantage of. Nonetheless, rising volatility could be a signal that we are getting late in the bull market, but the lessons from the last two cycles suggest there might be several more

Volatility can be good for active managers

Barry Gill is Head of Active Equities at UBS Asset Management. In addition, he is a member of the management group of UBS O’Connor, where he runs a concentrated long/short fund. Previously, Barry was head of the Fundamental Investment Group (Americas) for nearly six years within UBS Investment Bank, investing and trading the firm’s principal capital.

29

quarters before a top in the market is achieved. As such we are seeing the team generally stay the course, while slowly dialing down exposure to themes and factors that have performed.

In the US, the economic cycle is long in the tooth by traditional measures, but the same cannot be said for Europe. And globally there have been several instances of economic cycles lasting well over 10 years, so we have to constantly examine the data coming from the companies we invest in without prejudice.

Do you feel your portfolios have a tilt? The combination of ongoing technologi-cal disruption and the moribund level of economic activity have meant that growth stocks have materially outper-formed value stocks over the last decade. Fighting this dogmatically has been a fool’s errand, for all but the longest-term focused investors. As such, many of our portfolios have a tilt towards growth and momentum which is slowly being unwound.

Accelerating global GDP growth in 2016 pulled one leg from under this frame-work and it is possible that a peak in the disruption narrative ended in Q3 2017, so value has been mounting a come-back. We are optimistic that significant portfolio changes in our European Equity under the new leadership of Steve Magill position us well for this shift. Each market is different, though; the new economy part of China is very lightly regulated and is experiencing a boom in innovation, creating the first challenge to the Silicon Valley hegemony since the 1980s. This is exciting stuff and our team, led by Bin Shi, is doing a great job taking advantage of the opportunity set there.

As an active manager, what are the most memorable market regimes you have lived through?My (brief) 23 years doing this has included both the largest valuation bubble in history and the greatest economic and financial collapse in three generations; euphoria to despair and everything in between. The late 1990s taught me the power of flows; professional managers could not handicap the behavior of the average retail investor and it pushed many of them to the brink. There is an old Japanese saying, “The master swords-man is unlikely to be injured by his student, but may very well be killed by a man who has never before picked up a sword.” I think it is very apt. We active managers face similar challenges today with the growing constituency of “exposure” buyers in the market. Applying learnings from past market experiences can be invaluable.

“Globally there have been several instances of economic cycles lasting well over 10 years, so we have to constantly examine the data coming from the companies we invest in without prejudice.“

Have you observed an increased interest in active strategies from investors you have spoken to recently?Highly active strategies such as Global Emerging Markets HALO and China Equities have generated tremendous interest because of their terrific performance. Elsewhere it is much more muted—there continues to be a structural shift towards passive allocation and so fundamental investors need to continue to work on proving out a differentiated value proposition.

Since 2008, global markets have compounded at a double-digit rate, and this has infused the belief that one can rely on beta-driven returns alone to cover liability growth. But many believe that forward 10-year returns for indices are likely to materially underperform what we have recently experienced, while liabilities will continue to grow unabated. In a 3–4% appreciation environment for indices, every 100bps of alpha will be gold.

30

In your opinion, how should institutional investors add active strategies to their portfolios? Do you have any scenarios to share, any ‘typical’ cases?If we can deliver material alpha, this really adds up when you compound it over the multi-year horizon of most institutional investors. Remember, only active managers are equipped to deliver returns from all of beta, factor and idiosyncratic risks, so, done well, fundamental active management delivers the highest possible returns.

Where investors are committed to allocating a substantial amount of their AUM to passive strategies, they can take a lot more risk within their active allocations. For this reason we believe there is a pronounced trend to more concentrated, higher alpha-targeting strategies. Thinking about this from

“Remember, only active managers are equipped to deliver returns from all of beta, factor and idiosyncratic risks, so, done well, fundamental active management delivers the highest possible returns.”

another angle, many institutions are demanding value above and beyond pure returns; they want to know if the portfolio is being constructed with an eye to long-term societal well-being. Infusing sustainability into the analytical process and ultimately portfolio construction and using this to more deeply engage with corporates on behalf of asset owners is an area where active managers of scale are ideally placed to deliver value.

Passive strategies have gained so much portfolio share in the past several years, how does this play into actively managed portfolios?It is forcing active managers to focus on where they can deliver long-term value. When active management was the only game in town, the only way to buy beta was to own an active fund. Beta can now be created far more cheaply. With new evolutions like smart or alt beta, we are really seeing a disaggregation of the value stack, forcing fundamental investors to seek out where they have a defensible moat; this is in deep security and industry analysis. We believe that there are simply too many variables for quant models to (currently) compete effectively. Fortunately, we believe the total amount of alpha in the market is large and persistent, and analysis suggests that the great majority of that alpha comes from security and industry analysis. While it is still unclear how much more share is left to give up by active managers, we are confident that by driving excess return in a way that leverages our competitive advantages as fundamental investors, we will keep active management relevant for a very long time.

31

“While it is still unclear how much more share is left to give up by active managers, we are confident that by driving excess return in a way that leverages our competitive advantages as fundamental investors, we will keep active management relevant for a very long time.”

32

Drawing on the breadth and depth of our capabilities and our global reach, we turn challenges into opportunities. Together with you, we find the solution that you need.At UBS Asset Management we take a connected approach.

What we offerWhatever your investment profile or time horizon, we offer a comprehensive range of active and passive investment styles and strategies designed to meet your needs across all major traditional and alternative asset classes. Our invested assets total USD 796 billion16 and we have around 3,60017 employees, including over 900 investment professionals, located in 23 countries.

Who we areWe are one of the largest managers in Alternatives: the second largest fund of hedge funds manager18 and fifth largest manager globally of direct real estate.19 We are a leading fund house in Europe, the largest mutual fund manager in Switzerland,20 Europe’s third largest money manager21 and a major international firm in APAC. UBS’s unique passive offering, encompassing index and systematic strategies, provides smart beta, alternative indices, and other custom solutions to meet our clients’ needs. We are the second largest European-based passive player22 and the fourth largest ETF provider in Europe.23 We are a truly global firm with principal offices in Chicago, Frankfurt, Hartford, Hong Kong, London, New York, Singapore, Sydney, Tokyo and Zurich.

Past performance is not indicative of future results.16 As of 31 December 2017.17 Thereof around 1,300 internal and external FTE from Corporate Center; as of 31 December 2017.18 HFM InvestHedge Billion Dollar Club, published September 2017.19 FT/Towers Watson, based on data to 31 December 2016.20 Morningstar/Swiss Fund Data FundFlows, November 2017.21 Institutional Investor Euro 100, based on data to 30 June 2017 (based on discretionary assets only, UBS WM and AM combined,

excluding fund of funds assets).22 UBS Asset Management, December 2017.23 ETFGI European ETF and ETP industry insights, February 2018.

Why UBS Asset Management

Ideas and investment excellenceOur teams have distinct viewpoints and philosophies but they all share one goal— to provide you with access to the best ideas and superior investment performance.

A holistic perspectiveThe depth of our expertise and breadth of our capabilities allow us to have more insightful conversations and an active debate, all to help you make informed decisions.

Across marketsOur geographic reach means we can connect the parts of the investment world most relevant for you. That’s what makes us different—we are on the ground locally with you and truly global.

Solutions-based thinkingWe focus on finding the answers you need— and this defines the way we think. We draw on the best of our capabilities and insights to deliver a solution that is right for you.

33

Our active business

EquitiesWe have a wide spectrum of active investment strategies designed to meet your investment needs, whatever your risk and return objectives. Global, region-focused and thematic strategies are complemented by high alpha, growth and quantitative styles.

Fixed incomeYou can choose from a diverse range of active global, regional and local market-based fixed income investment strategies. Our capabilities include single-sector strategies such as government and corporate bond portfolios, multi-sector strategies such as core and core plus bond, and extended sector strategies which include high yield and emerging market debt. We also manage unconstrained fixed income and currency strategies.

Multi-asset and currencyYou can benefit from a diverse offering of commingled or bespoke global and regional asset allocation and currency investment strategies. These strategies may utilize a broad range of asset classes and span the risk/return spectrum, including balanced, growth, income, risk-managed, and unconstrained strategies. Our dynamic investment approach is designed to generate consistent returns across changing market conditions, while still maintaining a rigorous risk management discipline.

Hedge funds– Single manager: Through O’Connor, clients have access

to a global single-manager hedge fund platform, offering both multi-strategy and standalone capabilities. O’Connor’s fundamentally-driven investment processes are supplemented with sophisticated quantitative decision support and risk management tools, seeking to protect investor capital during periods of market turmoil through active risk management.

– Multi-manager: Our multi-manager and advisory services, provide exposure to hedge fund investments with tailored risk and return profiles, including commingled funds, customized discretionary portfolios and a range of potential advisory relationships. With the scale of one of the largest hedge fund intermediaries and fiduciaries, we work with clients globally in a consultative and collaborative manner to assist in effectively adding value to their hedge fund investment program.

Real estate, infrastructure and private equities– Direct real estate: You can access actively managed real

estate investments globally and regionally across the major real estate sectors. Our capabilities are focused on core and value-added strategies, but also include other strategies across the risk/return spectrum. These are available through open- and closed end private funds, REITs, customized investment structures, multi-manager funds, individually managed accounts and real estate securities.

– Direct infrastructure: We offer you direct exposure to infrastructure investments through fund solutions and separate, bespoke accounts. Our direct teams actively manage both equity and debt investments.

– Multi-managers: Our significant real estate multi-managers presence in major regions provides access to and manage-ment of unlisted real estate funds selected from a broad universe of managers. Our product offering ranges from core to opportunistic, from developed to emerging markets, and from customized segregated mandates to commingled funds. Through our multi-manager team you can also access the infrastructure and private equity market. They invest in the best-in-class, global managers in this field, offering significant diversification and vintage year benefits. Access can be made via fund solutions or separate, bespoke accounts.

34

Our tailored solutions

Contacts

Our passive business

If clients require a bespoke structure to meet their investment needs, our Investment Solutions team uses a continuous and unbiased client-centric approach that leverages the depth and breadth of our global investment resources to identify and solve clients’ specific challenges. We provide customized multi-asset solutions, advisory and fiduciary services, in the areas of global tactical asset allocation, alternative assets, risk-managed and structured strategies, manager selection, pension management, outsourced CIO and implementation.

If you are looking for passive exposure, we provide indexed, alternative beta and rules-based strategies across all major asset classes on a global and regional basis. You can draw on capabilities which include indexed equities, fixed income, commodities, real estate and alternatives with benchmarks ranging from mainstream to highly customized indices and rules-driven solutions. Products are available in a variety of structures including ETFs, pooled funds, structured funds and mandates.

Head Client CoverageWilliam Kennedy+41-44-234 11 [email protected]

Head Institutional Client CoverageAleksandar Ivanovic+41-44-234 11 [email protected]

Head Global Sovereign MarketsWillem van Breugel+44-20-7567 [email protected]

www.ubs.com/am

Head Institutional Client Coverage AmericasSusan Small+1-312-525 [email protected]

Head Institutional Client Coverage APACBeat Goetz+65-6495 [email protected]

Head Institutional Client Coverage EMEAFekko Ebbens+31-205-510 [email protected]

Head Institutional Client Coverage SwitzerlandAndreas Toscan+41-44-234 20 [email protected]

35

AmericasThe views expressed are a general guide to the views of UBS Asset Management as of April 2018. The information contained herein should not be considered a recommendation to purchase or sell securities or any particular strategy or fund. Commentary is at a macro level and is not with reference to any investment strategy, product or fund offered by UBS Asset Management. The information contained herein does not constitute investment research, has not been prepared in line with the requirements of any jurisdiction designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The information and opinions contained in this document have been compiled or arrived at based upon information obtained from sources believed to be reliable and in good faith. All such information and opinions are subject to change without notice. Care has been taken to ensure its accuracy but no responsibility is accepted for any errors or omissions herein. A number of the comments in this document are based on current expectations and are considered “forward-looking statements.” Actual future results, however, may prove to be different from expectations. The opinions expressed are a reflection of UBS Asset Management’s best judgment at the time this document was compiled, and any obligation to update or alter forward-looking statements as a result of new information, future events or otherwise is disclaimed. Furthermore, these views are not intended to predict or guarantee the future performance of any individual security, asset class or market generally, nor are they intended to predict the future performance of any UBS Asset Management account, portfolio or fund.

EMEA The information and opinions contained in this document have been compiled or arrived at based upon information obtained from sources believed to be reliable and in good faith, but is not guaranteed as being accurate, nor is it a complete statement or summary of the securities, markets or developments referred to in the document. UBS AG and / or other members of the UBS Group may have a position in and may make a purchase and / or sale of any of the securities or other financial instruments mentioned in this document.

Before investing in a product please read the latest prospectus carefully and thoroughly. Units of UBS funds mentioned herein may not be eligible for sale in all jurisdictions or to certain categories of investors and may not be offered, sold or delivered in the United States. The information mentioned herein is not intended to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not a reliable indicator of future results. The performance shown does not take account of any commissions and costs charged when subscribing to and redeeming units. Commissions and costs have a negative impact on performance. If the currency of a financial product or financial service is different from your reference currency, the return can increase or decrease as a result of currency fluctuations. This information pays no regard to the specific or future investment objectives, financial or tax situation or particular needs of any specific recipient.

The details and opinions contained in this document are provided by UBS without any guarantee or warranty and are for the recipient’s personal use and information purposes only. This document may not be reproduced, redistributed or republished for any purpose without the written permission of UBS AG.

This document contains statements that constitute “forward-looking statements”, including, but not limited to, statements relating to our future business development. While these forward-looking statements represent our judgments and future expectations concerning the development of our business, a number of risks, uncertainties and other important factors could cause actual developments and results to differ materially from our expectations.

UK Issued in the UK by UBS Asset Management (UK) Ltd. Authorised and regulated by the Financial Conduct Authority.

APAC This document and its contents have not been reviewed by, delivered to or registered with any regulatory or other relevant authority in APAC. This document is for informational purposes and should not be construed as an offer or invitation to the public, direct or indirect, to buy or sell securities. This document is intended for limited distribution and only to the extent permitted under applicable laws in your jurisdiction. No representations are made with respect to the eligibility of any recipients of this document to acquire interests in securities under the laws of your jurisdiction.

Using, copying, redistributing or republishing any part of this document without prior written permission from UBS Asset Management is prohibited. Any statements made regarding investment performance objectives, risk and/or return targets shall not constitute a representation or warranty that such objectives or expectations will be achieved or risks are fully disclosed. The information and opinions contained in this document is based upon information obtained from sources believed to be reliable and in good faith but no responsibility is accepted for any misrepresentation, errors or omissions. All such information and opinions are subject to change without notice. A number of comments in this document are based on current expectations and are considered “forward-looking statements”. Actual future results may prove to be different from expectations and any unforeseen risk or event may arise in the future. The opinions expressed are a reflection of UBS Asset Management’s judgment at the time this document is compiled and any obligation to update or alter forward-look-ing statements as a result of new information, future events, or otherwise is disclaimed.

You are advised to exercise caution in relation to this document. The information in this document does not constitute advice and does not take into consideration your investment objectives, legal, financial or tax situation or particular needs in any other respect. Investors should be aware that past performance of investment is not necessarily indicative of future performance. Potential for profit is accompanied by possibility of loss. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

Australia This document is provided by UBS Asset Management (Australia) Ltd, ABN 31 003 146 290 and AFS License No. 222605.

China The securities may not be offered or sold directly or indirectly in the People’s Republic of China (the “PRC”). Neither this document or information contained or incorporated by reference herein relating to the securities, which have not been and will not be submitted to or approved/verified by or registered with the China Securities Regulatory Commission (“CSRC”) or other relevant governmental authorities in the PRC pursuant to relevant laws and regulations, may be supplied to the public in the PRC or used in connection with any offer for the subscription or sale of the Securities in the PRC. The securities may only be offered or sold to the PRC investors that are authorized to engage in the purchase of Securities of the type being offered or sold. PRC investors are responsible for obtaining all relevant government regulatory approvals/licenses, verification and/or registrations themselves, including, but not limited to, any which may be required from the CSRC, the State Administration of Foreign Exchange and/or the China Banking Regulatory Commission, and complying with all relevant PRC regulations, including, but not limited to, all relevant foreign exchange regulations and/or foreign investment regulations.