Embed Size (px)

Citation preview

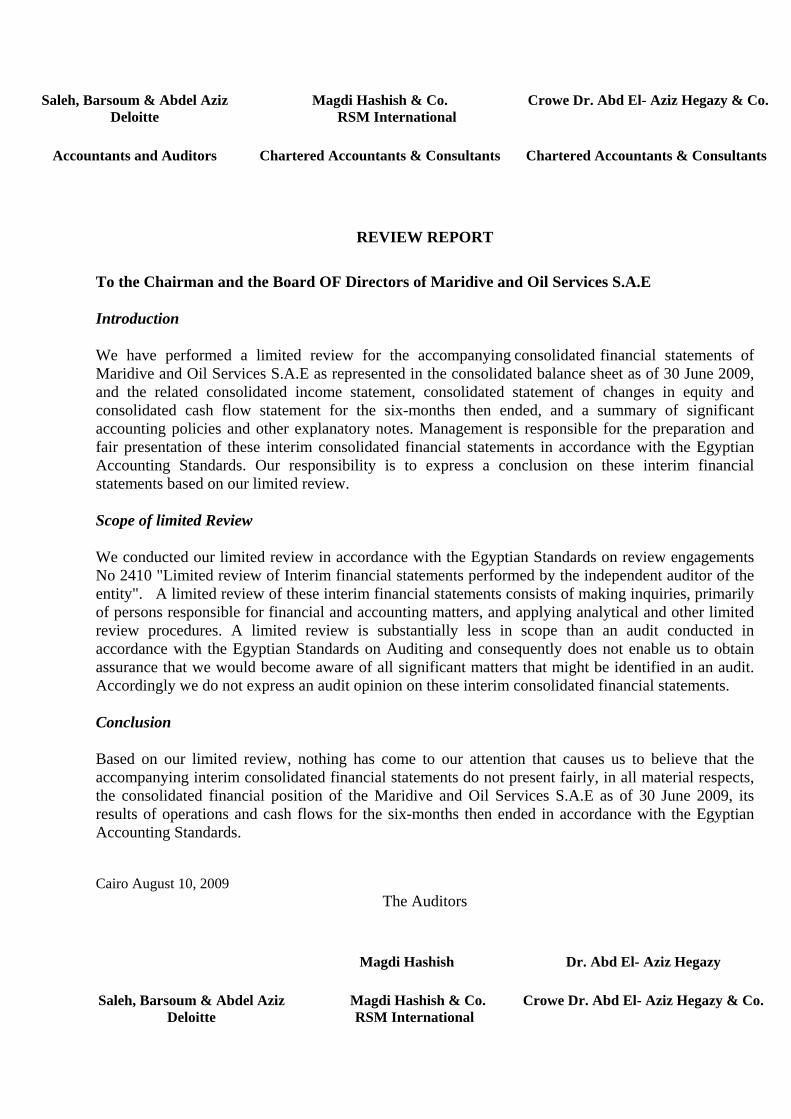

Crowe Dr. Abd El- Aziz Hegazy & Co.

Magdi Hashish & Co. RSM International

Saleh, Barsoum & Abdel Aziz Deloitte

Chartered Accountants & Consultants Chartered Accountants & Consultants Accountants and Auditors

REVIEW REPORT

To the Chairman and the Board OF Directors of Maridive and Oil Services S.A.E Introduction We have performed a limited review for the accompanying consolidated financial statements of Maridive and Oil Services S.A.E as represented in the consolidated balance sheet as of 30 June 2009, and the related consolidated income statement, consolidated statement of changes in equity and consolidated cash flow statement for the six-months then ended, and a summary of significant accounting policies and other explanatory notes. Management is responsible for the preparation and fair presentation of these interim consolidated financial statements in accordance with the Egyptian Accounting Standards. Our responsibility is to express a conclusion on these interim financial statements based on our limited review. Scope of limited Review We conducted our limited review in accordance with the Egyptian Standards on review engagements No 2410 "Limited review of Interim financial statements performed by the independent auditor of the entity". A limited review of these interim financial statements consists of making inquiries, primarily of persons responsible for financial and accounting matters, and applying analytical and other limited review procedures. A limited review is substantially less in scope than an audit conducted in accordance with the Egyptian Standards on Auditing and consequently does not enable us to obtain assurance that we would become aware of all significant matters that might be identified in an audit. Accordingly we do not express an audit opinion on these interim consolidated financial statements. Conclusion Based on our limited review, nothing has come to our attention that causes us to believe that the accompanying interim consolidated financial statements do not present fairly, in all material respects, the consolidated financial position of the Maridive and Oil Services S.A.E as of 30 June 2009, its results of operations and cash flows for the six-months then ended in accordance with the Egyptian Accounting Standards. Cairo August 10, 2009

The Auditors

Dr. Abd El- Aziz Hegazy Magdi Hashish

Crowe Dr. Abd El- Aziz Hegazy & Co.

Magdi Hashish & Co. RSM International

Saleh, Barsoum & Abdel Aziz Deloitte

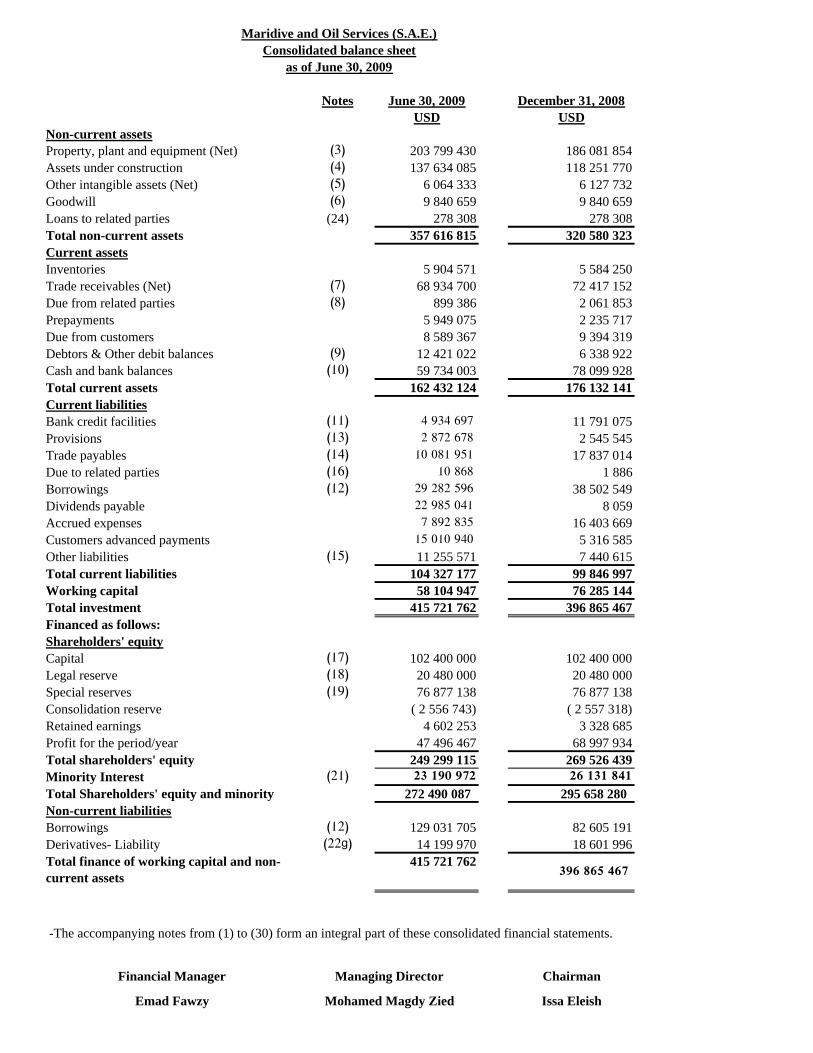

Notes June 30, 2009 December 31, 2008USD USD

Non-current assetsProperty, plant and equipment (Net) (3) 203 799 430 186 081 854Assets under construction (4) 137 634 085 118 251 770Other intangible assets (Net) (5) 6 064 333 6 127 732Goodwill (6) 9 840 659 9 840 659Loans to related parties (24) 278 308 278 308Total non-current assets 357 616 815 320 580 323Current assetsInventories 5 904 571 5 584 250Trade receivables (Net) (7) 68 934 700 72 417 152Due from related parties (8) 899 386 2 061 853Prepayments 5 949 075 2 235 717Due from customers 8 589 367 9 394 319Debtors & Other debit balances (9) 12 421 022 6 338 922Cash and bank balances (10) 59 734 003 78 099 928Total current assets 162 432 124 176 132 141Current liabilitiesBank credit facilities (11) 4 934 697 11 791 075Provisions (13) 2 872 678 2 545 545Trade payables (14) 10 081 951 17 837 014Due to related parties (16) 10 868 1 886Borrowings (12) 29 282 596 38 502 549Dividends payable 22 985 041 8 059Accrued expenses 7 892 835 16 403 669Customers advanced payments 15 010 940 5 316 585Other liabilities (15) 11 255 571 7 440 615Total current liabilities 104 327 177 99 846 997Working capital 58 104 947 76 285 144Total investment 415 721 762 396 865 467Financed as follows:Shareholders' equityCapital (17) 102 400 000 102 400 000 Legal reserve (18) 20 480 000 20 480 000 Special reserves (19) 76 877 138 76 877 138 Consolidation reserve ( 2 556 743) ( 2 557 318)Retained earnings 4 602 253 3 328 685 Profit for the period/year 47 496 467 68 997 934 Total shareholders' equity 249 299 115 269 526 439Minority Interest (21) 23 190 972 26 131 841Total Shareholders' equity and minority 272 490 087 295 658 280Non-current liabilitiesBorrowings (12) 129 031 705 82 605 191Derivatives- Liability (22g) 14 199 970 18 601 996Total finance of working capital and non-current assets

415 721 762 396 865 467

-The accompanying notes from (1) to (30) form an integral part of these consolidated financial statements.

Financial Manager Chairman

Emad Fawzy Issa Eleish

Managing Director

Mohamed Magdy Zied

Maridive and Oil Services (S.A.E.)

as of June 30, 2009Consolidated balance sheet

Notes2009 2008 2009 2008USD USD USD USD

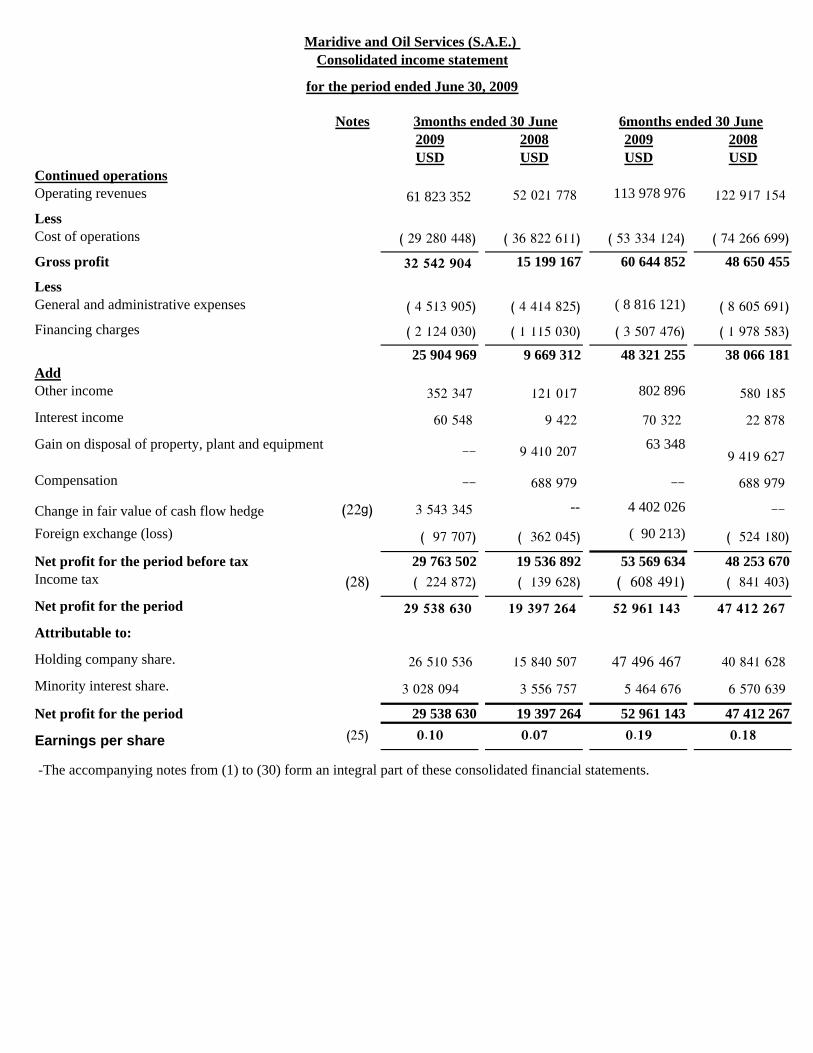

Continued operationsOperating revenues 61 823 352 52 021 778 113 978 976 122 917 154

LessCost of operations ( 29 280 448) ( 36 822 611) ( 53 334 124) ( 74 266 699)

Gross profit 32 542 904 15 199 167 60 644 852 48 650 455

LessGeneral and administrative expenses ( 4 513 905) ( 4 414 825) ( 8 816 121) ( 8 605 691)

Financing charges ( 2 124 030) ( 1 115 030) ( 3 507 476) ( 1 978 583)

25 904 969 9 669 312 48 321 255 38 066 181AddOther income 352 347 121 017 802 896 580 185

Interest income 60 548 9 422 70 322 22 878

Gain on disposal of property, plant and equipment -- 9 410 207 63 348 9 419 627

Compensation -- 688 979 -- 688 979

Change in fair value of cash flow hedge (22g) 3 543 345 -- 4 402 026 --

Foreign exchange (loss) ( 97 707) ( 362 045) ( 90 213) ( 524 180)

Net profit for the period before tax 29 763 502 19 536 892 53 569 634 48 253 670Income tax (28) ( 224 872) ( 139 628) ( 608 491) ( 841 403)

Net profit for the period 29 538 630 19 397 264 52 961 143 47 412 267

Attributable to:

Holding company share. 26 510 536 15 840 507 47 496 467 40 841 628

Minority interest share. 3 028 094 3 556 757 5 464 676 6 570 639

Net profit for the period 29 538 630 19 397 264 52 961 143 47 412 267

Earnings per share (25) 0.10 0.07 0.19 0.18

-The accompanying notes from (1) to (30) form an integral part of these consolidated financial statements.

6months ended 30 June

Maridive and Oil Services (S.A.E.) Consolidated income statement

for the period ended June 30, 2009

3months ended 30 June

June 30 June 302009 2008USD USD

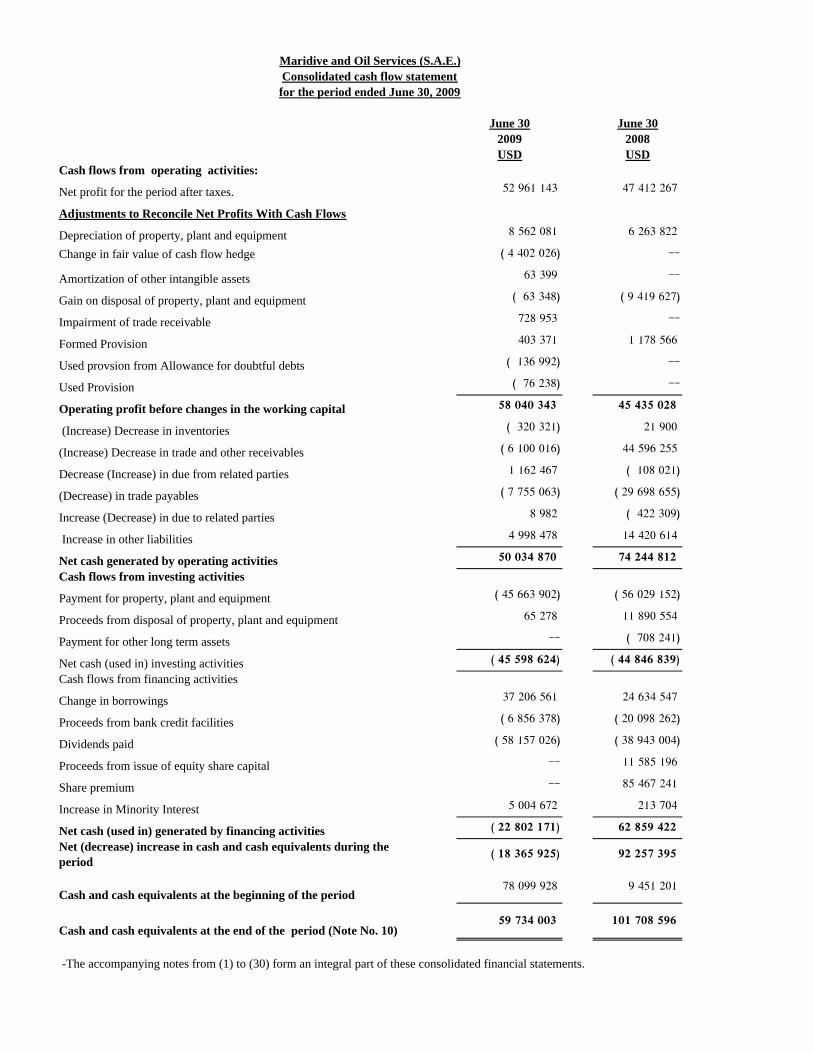

Cash flows from operating activities:

Net profit for the period after taxes. 52 961 143 47 412 267

Adjustments to Reconcile Net Profits With Cash Flows

Depreciation of property, plant and equipment 8 562 081 6 263 822

Change in fair value of cash flow hedge ( 4 402 026) --

Amortization of other intangible assets 63 399 --

Gain on disposal of property, plant and equipment ( 63 348) ( 9 419 627)

Impairment of trade receivable 728 953 --

Formed Provision 403 371 1 178 566

Used provsion from Allowance for doubtful debts ( 136 992) --

Used Provision ( 76 238) --

Operating profit before changes in the working capital 58 040 343 45 435 028

(Increase) Decrease in inventories ( 320 321) 21 900

(Increase) Decrease in trade and other receivables ( 6 100 016) 44 596 255

Decrease (Increase) in due from related parties 1 162 467 ( 108 021)

(Decrease) in trade payables ( 7 755 063) ( 29 698 655)

Increase (Decrease) in due to related parties 8 982 ( 422 309)

Increase in other liabilities 4 998 478 14 420 614

Net cash generated by operating activities 50 034 870 74 244 812

Cash flows from investing activities

Payment for property, plant and equipment ( 45 663 902) ( 56 029 152)

Proceeds from disposal of property, plant and equipment 65 278 11 890 554

Payment for other long term assets -- ( 708 241)

Net cash (used in) investing activities ( 45 598 624) ( 44 846 839)

Cash flows from financing activities

Change in borrowings 37 206 561 24 634 547

Proceeds from bank credit facilities ( 6 856 378) ( 20 098 262)

Dividends paid ( 58 157 026) ( 38 943 004)

Proceeds from issue of equity share capital -- 11 585 196

Share premium -- 85 467 241

Increase in Minority Interest 5 004 672 213 704

Net cash (used in) generated by financing activities ( 22 802 171) 62 859 422

Net (decrease) increase in cash and cash equivalents during the period

( 18 365 925) 92 257 395

Cash and cash equivalents at the beginning of the period 78 099 928 9 451 201

Cash and cash equivalents at the end of the period (Note No. 10) 59 734 003 101 708 596

-The accompanying notes from (1) to (30) form an integral part of these consolidated financial statements.

Maridive and Oil Services (S.A.E.)Consolidated cash flow statementfor the period ended June 30, 2009

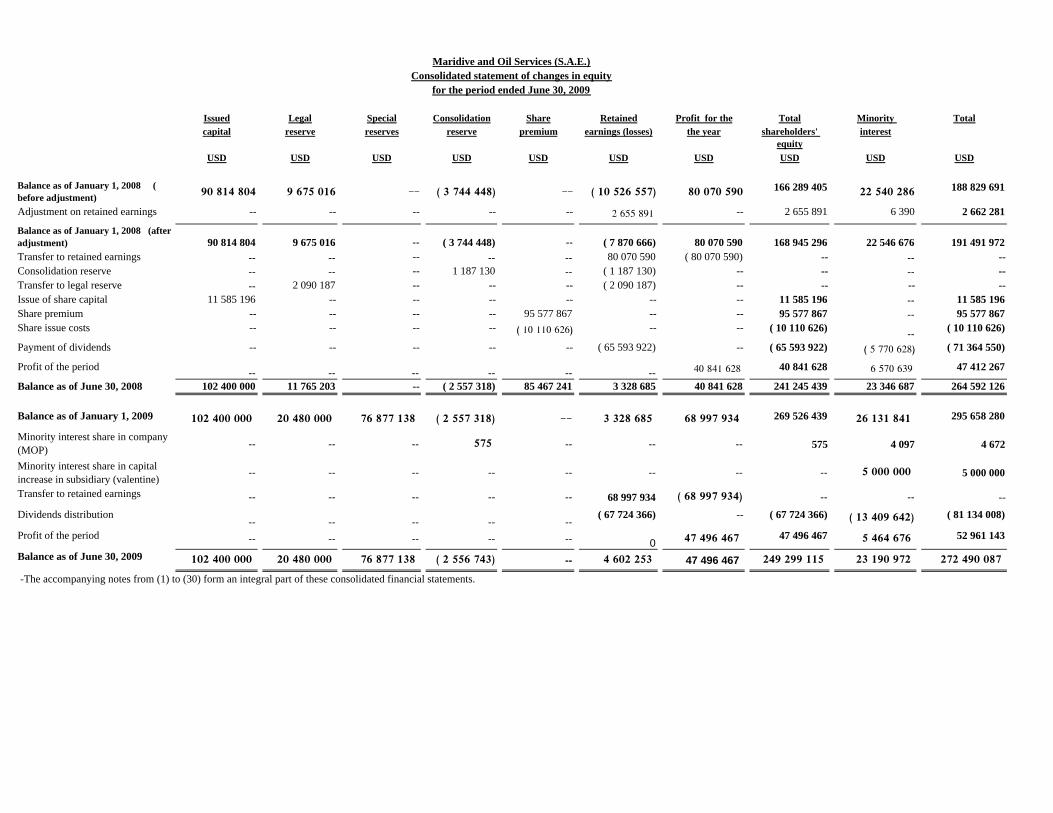

Issued Legal Special Consolidation Share Retained Profit for the Total Minority Totalcapital reserve reserves reserve premium earnings (losses) the year shareholders'

equityinterest

USD USD USD USD USD USD USD USD USD USD

Balance as of January 1, 2008 ( before adjustment) 90 814 804 9 675 016 -- ( 3 744 448) -- ( 10 526 557) 80 070 590 166 289 405 22 540 286 188 829 691

Adjustment on retained earnings -- -- -- -- -- 2 655 891 -- 2 655 891 6 390 2 662 281

Balance as of January 1, 2008 (after adjustment) 90 814 804 9 675 016 -- ( 3 744 448) -- ( 7 870 666) 80 070 590 168 945 296 22 546 676 191 491 972 Transfer to retained earnings -- -- -- -- -- 80 070 590 ( 80 070 590) -- -- --Consolidation reserve -- -- -- 1 187 130 -- ( 1 187 130) -- -- -- --Transfer to legal reserve -- 2 090 187 -- -- -- ( 2 090 187) -- -- -- --Issue of share capital 11 585 196 -- -- -- -- -- -- 11 585 196 -- 11 585 196 Share premium -- -- -- -- 95 577 867 -- -- 95 577 867 -- 95 577 867 Share issue costs -- -- -- -- ( 10 110 626) -- -- ( 10 110 626) -- ( 10 110 626)

Payment of dividends -- -- -- -- -- ( 65 593 922) -- ( 65 593 922) ( 5 770 628) ( 71 364 550)

Profit of the period -- -- -- -- -- -- 40 841 628 40 841 628 6 570 639 47 412 267

Balance as of June 30, 2008 102 400 000 11 765 203 -- ( 2 557 318) 85 467 241 3 328 685 40 841 628 241 245 439 23 346 687 264 592 126

Balance as of January 1, 2009 102 400 000 20 480 000 76 877 138 ( 2 557 318) -- 3 328 685 68 997 934 269 526 439 26 131 841 295 658 280

Minority interest share in company (MOP) -- -- -- 575 -- -- -- 575 4 097 4 672

Minority interest share in capital increase in subsidiary (valentine) -- -- -- -- -- -- -- -- 5 000 000 5 000 000

Transfer to retained earnings -- -- -- -- -- 68 997 934 ( 68 997 934) -- -- --Dividends distribution

-- -- -- -- --( 67 724 366) -- ( 67 724 366) ( 13 409 642) ( 81 134 008)

Profit of the period -- -- -- -- -- 0 47 496 467 47 496 467 5 464 676 52 961 143

Balance as of June 30, 2009 102 400 000 20 480 000 76 877 138 ( 2 556 743) -- 4 602 253 47 496 467 249 299 115 23 190 972 272 490 087

-The accompanying notes from (1) to (30) form an integral part of these consolidated financial statements.

Maridive and Oil Services (S.A.E.)Consolidated statement of changes in equity

for the period ended June 30, 2009

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

1

Maridive and Oil Services (S.A.E.) Notes to the consolidated financial statements

for the priod ended June 30, 2009

1- General

Maridive and Oil Services S.A.E. "MOS" was incorporated in accordance with the prevailing laws and regulations of the Arab Republic of Egypt pursuant to the framework of the provisions of the Arab and Foreign Investment and Free Zones Law No. 43 of 1974 which was replaced by the Investment Law No. 230 of 1989 and subsequently replaced by the Investment Guarantees and Incentives Law No. 8 of 1997. The Ministerial Decree of the incorporation of the Company and its articles of incorporation were published in the Egyptian Gazette issue No. 29 dated February 2, 1978.

The Company was registered in the Commercial Register on February 5, 1978 under number 19564.

In 1993, the Company established a branch in Abu Dhabi in the United Arab Emirates; which was registered under No. 25391 dated June 26, 1993. This branch has not yet been registered in the commercial register of the company in Egypt.

Maridive and Oil Services S.A.E. and its principal shareholders own directly the following subsidiaries:

Company name Classification Ownereship percentage and voting rights

June 30, 2009 December 31, 2008

Maritide Offshore Oil Services S.A.E. Subsidiary 99.46% 99.46%

Valentine Maritime Ltd. Subsidiary 75% 75%

Maridive Offshore Projects S.A.E. Subsidiary 99.98 % 100%

The accompanying financial statements include the consolidated financial statements of Maridive and Oil Services S.A.E. "MOS" (Parent) and its subsidiaries:

a. Valentine Maritime Ltd and its subsidiaries "Valentine" b. Maritide Offshore Oil Services S.A.E. "Maritide" c. Maridive Offshore Projects S.A.E. "MOP"

MOS and its subsidiaries are referred to as the "Group".

a- Group companies under consolidation level In accordance with the Egyptian Accounting Standards (EAS) and the prevailing laws and regulations, MOS presents statutory consolidated financial statements, which incorporates the financial statements of the following companies:

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

2

1. Maridive and Oil Services S.A.E. "MOS" the parent company of the Group.

2. Valentine Maritime Ltd "Valentine" which was incorporated on June 15, 1990 in the Republic of Liberia pursuant to the Liberian Business Corporation Act of 1997. Maridive and Oil Services S.A.E. have acquired 75% of the issued capital of the Company in 1996 and is able to govern Valentine Maritime Ltd financial and operating policies to obtain the benefits of its activities. Valentine Maritime Ltd has the following subsidiaries consolidated under its control:

• Valentine Maritime (Gulf) LLC, which was incorporated in the United Arab Emirates. Valentine Maritime Ltd owns 49% of its shares and is considered its major shareholder. Valentine Maritime Ltd has control over Valentine Maritime (Gulf) LLC financial and operating policies in accordance with the management agreement dated March 13, 1997.

• Valentine Maritime (Mauritius) Ltd, which was incorporated in the Republic of Mauritius and is a wholly owned subsidiary of Valentine Maritime Ltd.

• Ocean Marine FZC, which was incorporated in the United Arab Emirates. and is a wholly owned subsidiary of Valentine Maritime Ltd.

• Valentine Maritime – Kingdom Saudi Arabia, which was incorporated in the Kingdom Saudi Arabia. Valentine Maritime Ltd owns 60% of its shares.

3. Maritide Offshore Oil Services S.A.E. "Maritide" is an Egyptian joint stock Company initially incorporated according to the agreement made in 1988 between Maridive and Oil Services (S.A.E.) and Zapata Gulf Marine Operators under the name of MZ – Offshore Oil Services S.A.E.

Maritide was incorporated in accordance with the provisions of the Arab and Foreign Investment Law and Free Zones Law No. 43 of 1974, which was replaced by the Investment Law No. 230 of 1989 and subsequently replaced by the Investment Guarantees and Incentives Law No. 8 of 1997.

On March 31, 1994, the name of the Company was changed to Maritide Offshore Oil Services S.A.E. - Free Zone according to the ministerial decree No. 87 of 1994. The decree was published in the Egyptian Gazette issue No. 70 dated March 27, 1994.

Maridive and Oil Services S.A.E. has acquired 99.46% of the issued capital of Maritide Offshore Oil Services S.A.E. on three stages in 1999, 2001 and 2002, to be able to govern its financial and operating policies.

4. Maridive Offshore Projects S.A.E. is an Egyptian Joint stock Company that was incorporated under the provisions of Investment Law No. 230 of 1989, which was replaced by the Investment Guarantees and Incentives Law No. 8 of 1997. The ministerial decree for the incorporation of company and its articles of association were published in the Egyptian Gazette issue number 245 dated October 31, 1993. MOP was registered in the commercial register under number 29875 – Port Said on October 27, 1993.

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

3

On April 9, 2008 Maridive and Oil Services S.A.E. has acquired 100% of Maridive Offshore Projects S.A.E through a shares swap agreement, of the shares of the increase in MOS share capital by MOP shares, with a rate of 32.27 share. Accordingly, Maridive Offshore Projects S.A.E. became a subsidiary of Maridive and Oil Services S.A.E. (Refer to Notes 2d).

b- Purposes of the companies

1. The purpose of Maridive and Oil Services S.A.E. is to provide in the free zone of the Arab Republic of Egypt all marine services, including the supply of services, maintenance, construction, establishment, and rescue operations whether under or above the level of the sea and all works related to manufacturing services for marine and land establishments including cleaning, maintenance, construction, transportation, supplies and all related equipment and spare parts required for those services.

2. The purpose of Maritide Offshore Oil Services S.A.E. is to provide technical

services to oil and gas companies and other companies specializing in this field including the supplies, tugging, anchor handling, fire fighting, pollution treatment and support to diving operations as well as assistance work required for offshore field operations in the areas of oil and gas companies concessions, and also to own marine units recently built.

3. The purpose of Valentine Maritime Ltd. is to conduct commercial activities and

maritime services. The Company conducts work in different parts of the world out of a principal base in Abu Dhabi - United Arab Emirates.

4. The purpose of Maridive Offshore Projects S.A.E. is performing the technical

offshore services activities in the Public Free Zone Area in Port Said (Egypt), except for consultation services. The main activities of the Company include the specialized technical offshore service above and under water or onshore in the field of offshore oil projects and all other offshore activities and their related engineering and construction works such as diving, salvage and all kinds of maintenance works, maintenance of platforms, wells, marine units, metals treating and coating, performing offshore survey and seabed research works, installing cables and pipelines laying under water or onshore, ports and lights offshore services in and out the Egyptian territorial waters. The company owns, leases and rents marine units, equipment, motorboats, barges, and elevators necessary for its puposes.

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

4

2- Significant accounting policies

a. Basis of preparation

The accompanying consolidated financial statements have been prepared on the historical cost basis. The principal accounting policies are set out below.

b. Statement of compliance

The accompanying consolidated financial statements have been prepared in accordance with the Egyptian Accounting Standards "EAS", and the prevailing Egyptian laws and regulations.

According to the EAS, reference to International Financial Reporting Standards (IFRS) is required regarding issues not covered by the EAS.

c. Critical accounting judgments and key sources of estimation uncertainty

Management of the Group is required to make certain judgments, estimates and assumption that are not readily apparent from other sources. The estimates and associated assumptions are based on historical experience and other factors that are considered to be relevant. Actual results may differ from these estimates. The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in which the estimate is revised if the revision affects only the current period or in the period of the revision and future periods if the revision affects both current and future periods. The significant judgments and estimates made by management are summarized as follows:

i- Impairment of goodwill

Determining whether goodwill is impaired requires an estimation of the value in use of the cash-generating units to which goodwill has been allocated. The value in use calculation requires the Company management to estimate the future cash flows expected to arise from the cash-generating unit and a suitable discount rate in order to calculate present value.

ii- Useful lives of property, plant and equipment

The useful lives, residual values of the property, plant and equipment and depreciation method are based on management's judgment of the historical pattern of useful lives and the general standards in industry. The useful lives and residual values are reviewed for reasonableness by management on an annual basis.

iii- Spare parts inventories When inventories become old or obsolete, an estimate is made of their net realizable value. Inventories items are categorized based on their movements during the year and, accordingly, different proportions of the value of each category are recognized as provision for impaired inventories.

iv- Trade and other receivables An estimate of the collectible amount of trade and other receivables is made when collection of the full amount is no longer probable. For individually significant amounts, this estimation is performed on an individual basis.

d. Basis of consolidation

These consolidated financial statements incorporate the financial statements of Maridive and Oil Services S.A.E. (the parent company) and entities controlled by MOS (its subsidiaries). Control is achieved where the company has the power to

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

5

govern the financial and operating policies of an entity so as to obtain benefits from its activities. The results of subsidiaries acquired or disposed of during the year are included in the consolidated income statement from the effective date of acquisition or up to the effective date of disposal, as appropriate. Where necessary, adjustments are made to the financial statements of subsidiaries to bring their accounting policies in line with those used by other members of the Group. All intra-group transactions, balances, income and expenses were eliminated in full on consolidation . Minority interests in the net assets (excluding goodwill) of consolidated subsidiaries are identified separately from the Group’s equity therein. Minority interests consist of the amount of those interests at the date of the original business combination and the minority’s share of changes in equity since the date of the combination. Losses applicable to the minority in excess of the minority’s interest in the subsidiary’s equity are allocated against the interests of the Group except to the extent that the minority has a binding obligation and is able to make an additional investment to cover the losses. On April 9, 2008 Maridive and Oil Services S.A.E. has acquired 100% of Maridive Offshore Projects (S.A.E) through a shares swap agreement, of the shares of the increase in MOS share capital by MOP shares, with a rate of 32.27 share. Accordingly, Maridive Offshore Projects S.A.E. became a subsidiary of Maridive and Oil Services S.A.E. Since Maridive Offshore Projects S.A.E. is ultimately controlled by the principle shareholders of Maridive and Oil Services S.A.E., before and after the above mentioned share swap agreement, therefore the substance of the acquisition is a business combination involving entities under common control, and that control is not transitory. Since EAS 29 "Business Combinations" does not apply to business combinations involving entities under common control, and in the absence of a standard or an interpretation that specifically applies to this transaction, and in accordance with EAS 5 "Accounting Policies, Changes in Accounting Estimates and errors. " management has used its judgements in developing an accounting policy that results in information that is relevant to the economic decision making needs of users and reliable financial statements. Management has developped and implemeted an accounting policy, to consolidate the operations subject to common control, throught which the company includes the financial statements of Maridive Offshore Projects S.A.E. in the consolidated financial statements as follows:

1. Recognition of the difference between purchase price consideration and net assets transferred as adjustment to shareholder’s equity.

2. The operating results of Maridive Offshore Projects S.A.E were included in the consolidated income statement, since Maridive Offshore Projects S.A.E and Maridive and Oil Services S.A.E. were under common control before and after the share swap agreement.

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

6

e. Subsidiaries

Subsidiaries are entities controlled by the group. Control exist when the group has the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities. In assessing control, potential voting rights that are exercisable are taken into account.

f. Goodwill

Goodwill arising on the acquisition of a subsidiaries represents the excess of the cost of acquisition over the Group’s interest in the net fair value of the identifiable assets, liabilities and contingent liabilities of the subsidiary recognised at the date of acquisition. Goodwill is initially recognised as an asset at cost and is subsequently measured at cost less any accumulated impairment losses. For the purpose of impairment testing, goodwill is allocated to each of the Group’s cash-generating units expected to benefit from the synergies of the combination. Cash-generating units to which goodwill has been allocated are tested for impairment annually, or more frequently when there is an indication that the unit may be impaired. If the recoverable amount of the cash-generating unit is less than the carrying amount of the unit, the impairment loss is allocated first to reduce the carrying amount of any goodwill allocated to the unit and then to the other assets of the unit pro-rata on the basis of the carrying amount of each asset in the unit. An impairment loss recognised for goodwill is not reversed in a subsequent period. On disposal of a subsidiary, the attributable amount of goodwill is included in the determination of the profit or loss on disposal.

g. Inventories Inventories of spare parts for projects are stated at the lower of cost and net realizable value. Costs are those expenses incurred in bringing each item to its present location and condition. Inventories are priced using the weighted average method. Inventories are represented in Valentine Maritime Ltd. materials and spare parts used in its projects. The cost of spare parts of marine units is charged to the income statement when incurred.

h. Revenue recognition Revenue is measured at the fair value of the consideration received or receivable.

1- Rendering service Revenue from the rendering of services is recognized when all the following conditions are satisfied: The amount of revenue can be measured reliably; It is probable that the economic benefits associated with the transaction will

flow to the entity; the stage of completion of the service at the balance sheet date can be measured

reliably; and The costs incurred for the transaction and the costs to complete the transaction

can be measured reliably.

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

7

2- Installation of projects

Contract revenue is recognized under the percentage of completion method. When the outcome of the contract can be reliably estimated. is recognized by reference to the proportion that accumulated costs up to the period end bear to the estimated total costs of the contract. When the contract is at an early stage and its outcome can not be reliably estimated, revenue is recognized to the extent of costs incurred up to the period end which are considered recoverable.

Contract revenues and its relevant costs are recognized as revenues and expenses respectively in the light of the percentage of completion of the project as of the date of the financial statements, any anticipated loss is recognized immidiately

In determining contract costs incurred up to the period end, any costs relating to future activity on a contract are excluded and shown as work in progress. The aggregate of the costs incurred and the profit/loss recognized on each contract is compared against the progress billings up to the year end. Where the sum of the costs incurred and recognized profit or recognized loss exceeds the progress billings, the balance is shown under trade and other receivables as due from customers on contracts. Where the progress billings exceed the sum of costs incurred and recognized profit or recognized loss, the balance is shown under trade and other payables as due to customers on contracts.

3- Interest income and other income

Interest and other income are recognized on accrual basis.

i. Foreign currency transactions

The Group companies are using US dollar as their functional and reporting currency, as the Group companies revenues are billed in US dollar. In preparing the financial statements, transactions in currencies other than the entities’ functional currency (foreign currencies) are recorded at the rates of exchange prevailing at the date of the transactions. At each balance sheet date, monetary items denominated in foreign currencies are retranslated at the rates prevailing at the balance sheet date. Non-monetary items carried at fair value that are denominated in foreign currencies are retranslated at the rates prevailing at the date when the fair value was determined. Non-monetary items that are measured in terms of historical cost in a foreign currency are not retranslated. Exchange differences are recognized in profit or loss in the period in which they arise.

j. Property, plant and equipment

Property, plant and equipment are stated at cost less accumulated depreciation and any accumulated impairment losses.

The gain or loss arising on the disposal or retirement of an item of property, plant and equipment is determined as the difference between the sales proceeds and the carrying amount of the asset and is recognized in income statement.

Property, in the course of construction for production, rental or administrative purposes, or for purposes not yet determined, are carried at cost.

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

8

Cost comprises its purchase price, including import duties, non-refundable purchase taxes and any directly attributable costs of bringing the asset to its working condition and location for its intended use and for qualifying assets, borrowing costs are capitalized in accordance with the Group Companies’ accounting policy.

Depreciation of these assets commences when the assets are ready for their intended use.

Depreciation is charged so as to write off the cost, other than land and properties under construction, over their estimated useful lives, using the straight-line method.

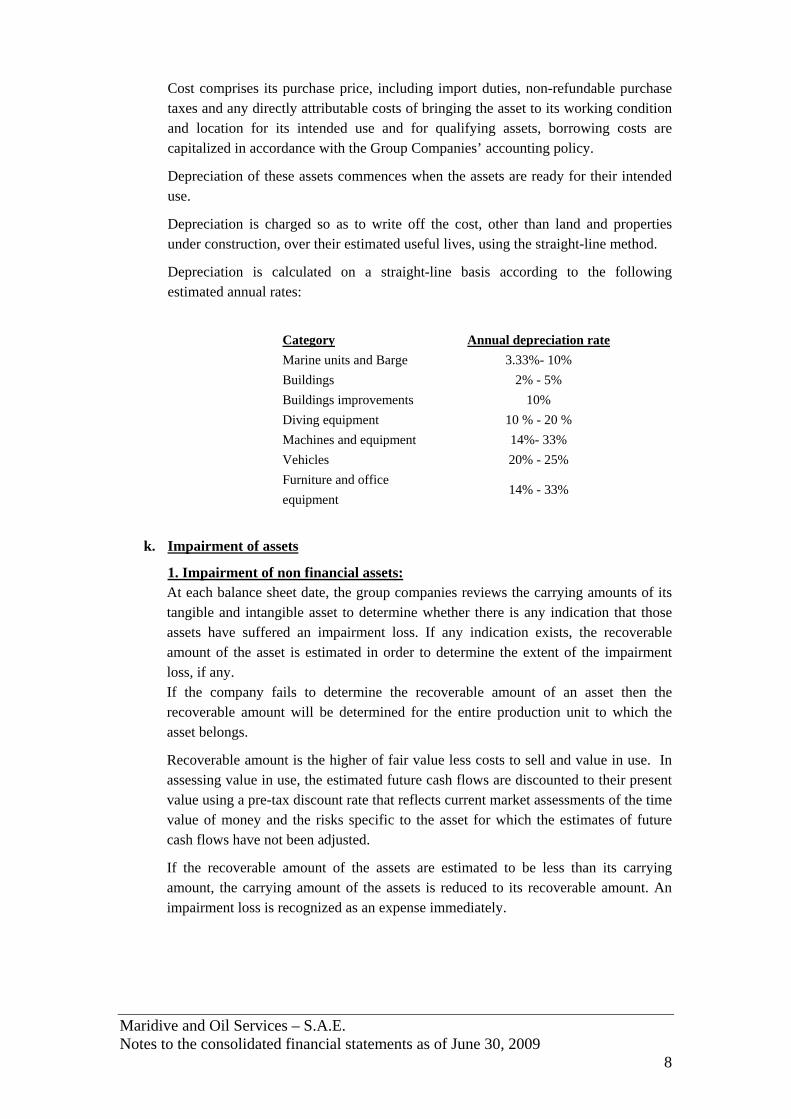

Depreciation is calculated on a straight-line basis according to the following estimated annual rates:

Category Annual depreciation rate Marine units and Barge 3.33%- 10% Buildings 2% - 5% Buildings improvements 10% Diving equipment 10 % - 20 % Machines and equipment 14%- 33% Vehicles 20% - 25% Furniture and office equipment

14% - 33%

k. Impairment of assets

1. Impairment of non financial assets: At each balance sheet date, the group companies reviews the carrying amounts of its tangible and intangible asset to determine whether there is any indication that those assets have suffered an impairment loss. If any indication exists, the recoverable amount of the asset is estimated in order to determine the extent of the impairment loss, if any. If the company fails to determine the recoverable amount of an asset then the recoverable amount will be determined for the entire production unit to which the asset belongs.

Recoverable amount is the higher of fair value less costs to sell and value in use. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset for which the estimates of future cash flows have not been adjusted.

If the recoverable amount of the assets are estimated to be less than its carrying amount, the carrying amount of the assets is reduced to its recoverable amount. An impairment loss is recognized as an expense immediately.

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

9

Where an impairment loss subsequently reverses, the carrying amount of the assets is increased to the revised estimate of its recoverable amount, so that the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognized for the cash-generating unit in prior years. A reversal of an impairment loss is recognized as income immediately.

2. Impairment of financial assets:

An entity shall assess at the end of each reporting period whether there is any objective evidence that a financial asset or group of financial assets is impaired.

A financial asset or a group of financial assets is impaired and impairment losses are incurred if, and only if, there is objective evidence of impairment as a result of one or more events that occurred after the initial recognition of the asset (a ‘loss event’) and that loss event (or events) has an impact on the estimated future cash flows of the financial asset or group of financial assets that can be reliably estimated

The Financial assets carried at amortised cost it’s amount of loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows (excluding future credit losses that have not been incurred) discounted at the financial asset’s original effective interest rate.

The carrying amount of the asset shall be reduced directly in exception of the client accounts which is reduced by using an allowance account and an execution of the Bad debt which is confirmed not to be paid from that allowance.

The recognised impairment loss shall be reversed either directly or by adjusting an allowance account. The reversal shall not result in a carrying amount of the financial asset that exceeds what the amortised cost would have been had the impairment not been recognised at the date the impairment is reversed. The amount of the reversal shall be recognised in profit or loss.

l. Provisions Provisions are recognized when the Group has a present legal or constructive obligation as a result of past events, and it is probable that the Group will be required to settle the obligation, and a reliable estimate can be made of the amount of the obligation. The amount recognised as a provision is the best estimate of the consideration required to settle the present obligation at the balance sheet date, taking into account the risks and uncertainties surrounding the obligation. Where a provision is measured using the cash flows estimated to settle the present obligation, its carrying amount is the present value of those cash flows. When some or all of the economic benefits required to settle a provision are expected to be recovered from a third party, the receivable is recognised as an asset if it is virtually certain that reimbursement will be received and the amount of the receivable can be measured reliably.

m. Taxation MOS , MOP and Maritide have been established as Egyptian Free Zone companies in accordance with the provisions of the Investment Guarantees and Incentives Law No. 8 of 1997, and its executive regulations, the companies are not subject to the Egyptain

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

10

Income Tax Law No. 91 of 2005 with specified conditions that rule the free zone system as follows:

1. The recognized revenue must be within the limit of authorized purpose of activity. 2. Operating activities must be carried out within the free zone borders.

These companies withhold salary taxes from the employees and remit the withheld tax to the relevant Tax Authority on regular basis.

Valentine Maritime Ltd. and its subsidaries are not subject to Corporate Income Tax except Valentine Maritime (Mauritius) Ltd which is subject to Income Tax.

n. Financial instruments

Financial assets and financial liabilities carried on the balance sheet include cash and cash equivalents, marketable securities, trade and other accounts receivable and payable, long-term receivables, borrowings and investments. Financial instruments are classified as assets or liabilities in accordance with the substance of the contractual arrangement. Therefore interest, dividends, gains and losses relating to these financial instruments classified as an asset or a liability are reported as expense or income.

Financial instruments are offset when the Company has a legally enforceable right to offset and intends to settle either on a net basis or to realize the asset and settle the liability simultaneously.

The Company’s activities are exposed to a variety of financial risks, including the effects of foreign exchange risk, interest rates risk, credit risk and liquidity risk. The Company’s overall risk management program seeks to minimize the potential adverse effects of these risks on the financial performance of the Company.

Derivative Financial Instruments

Derivatives financial instruments are financial instruments or other contracts with all three of the following characteristics:-

Its value changes in response to the change in a specified interest rate, financial instrument price, commodity price, foreign exchange rate, index of prices or rates, credit rating or credit index, or other variable (sometimes called the underlying); It requires no initial net investment or an initial net investment that is smaller than would be required for other types of contracts that would be expected to have a similar response to changes in market factors; and it is settled at a future date.

Accordingly, the company and in order to manage its exposure to interest rate risk enters into derivative financial instruments in particular, Interest Rate Swaps (IRS). Further details of derivative financial instruments are disclosed in Note 22 to the financial statements.

Derivatives are initially recognized at fair value at the date a derivative contract is entered into and are subsequently re-measured to their fair value at each balance sheet date. The resulting gain or loss is recognized in profit or loss immediately unless the derivative is designated and effective as a hedging instrument, in which event the timing of the recognition in profit or loss depends on the nature of the hedge relationship. The Group designated IRS contracts as a cash flow hedges.

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

11

The fair value of hedging derivatives is classified as a non-current asset or a non-current liability if the remaining maturity of the hedge relationship is more than 12 months and as a current asset or a current liability if the remaining maturity of the hedge relationship is less than 12 months.

Hedge accounting is discontinued when the Group revokes the hedging relationship, the hedging instrument expires or is sold, terminated, or exercised, or no longer qualifies for hedge accounting.

Any cumulative gain or loss deferred in equity at that time remains in equity and is recognized when the forecast transaction is ultimately recognized in profit or loss. When a forecast transaction is no longer expected to occur, the cumulative gain or loss that was deferred in equity is recognized immediately in profit or loss.

Cash flow hedge

Cash flow hedge is a hedge of the exposure to variability in cash flows that is attributable to a particular risk associated with a recognized asset or liability, such as all or some future interest payments on variable rate debt or a highly probable forecast transaction and could affect profit or loss. The company uses Interest Rate Swap (IRS) contracts to hedge its risks associated with interest rate fluctuations relating to Term Loan Facility. Such derivatives are initially recorded at cost, if any, and are re-measured to fair value at subsequent reporting dates.

A hedge is normally regarded as highly effective if, at inception and throughout the life of the hedge, the enterprise can expect changes in the cash flows of the hedged item to be almost fully offset by the changes in the cash flows of the hedging instrument, and actual results are within a range of 80 to 125 per cent.

The Group relied on the NPV of IRS future cash flows, received from its counterparties. Hence, the IRS hedge effectiveness was measured, at each year-end, using the Ratio Analysis method as follows:

Those IRS derivatives are shown as long-term assets or liabilities. Changes in the fair value of those derivative financial instruments, designated and effective as hedges of future cash flows, are charged directly to the hedging reserve in equity, whereas the ineffective portion is recognized immediately in profit or loss. Amounts previously deferred in equity are recognized in profit or loss in the same period in which the hedged item affects profit or loss.

o. Cash and cash equivalents

Cash and cash equivalents include cash in hand, current accounts at banks, short-term deposits with an original maturity of three months or less.

p. Cash flow statement

The cash flow statement is prepared by applying the indirect method. For the purpose of preparing the statement of cash flows, the cash and cash equivalents represent cash in hand and at banks and placement with banks.

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

12

q. Legal reserve

(i) MOS, Maritide, and MOP: According to these companies statutes and by laws, 5% of the net profit of the year is appropriated to form the legal reserve provided that the balance would not exceed 20% of the paid-up capital. According to the Egyptian Companies Law no. 159 of 1981, the legal reserve can only be used in covering the Company’s losses and in increasing the Company’s capital.

The legal reserve’s balance for Maritide reached USD 1 million, which is equivalent to 20% of its paid-up capital; therefore, the appropriation of 5% of the net profit of the year to form the legal reserve is no longer required.

(ii) Valentine Maritime Ltd.: No legislative requirements to form legal reserves.

r. Recognition of expenses

Expenses are recognized in the income statement when a decrease in future economic benefits related to a decrease in an asset or an increase of a liability has arisen that can be measured reliably. This means, in effect, that recognition of expenses occurs simultaneously with the recognition of an increase in liabilities or a decrease in assets.

Expenses are recognized in the income statement on the basis of a direct association between the costs incurred and the earning of specific items of income (matching).

When economic benefits are expected to arise over several accounting periods and the association with income can only be broadly or indirectly determined, expenses are recognized in the income statement on the basis of systematic and rational allocation procedures.

An expense is recognized immediately in the income statement when an expenditure produces no future economic benefits or when, and to the extent that; future economic benefits do not qualify, or cease to qualify, for recognition in the balance sheet as an asset.

s. Borrowings

Borrowings are recorded at fair value of the cash proceeds received and subsequently measured at amortized cost using the effective interest method.

t. Borrowing costs

Borrowing costs are recognized as an expense in the period in which they are incurred, however, the Group companies follow the alternative treatment allowed under Egyptian Accounting Standards by which borrowing costs directly attributable to the acquisition, construction or production of qualifying assets, which are assets that necessarily take a substantial period of time to get ready for their intended use or sale, are added to the cost of those assets, until such time as the assets are substantially ready for their intended use or sale. Investment income earned on the temporary investment of specific borrowings pending their expenditure on qualifying assets is deducted from the borrowing costs eligible for capitalization.

u. Loan Arrangement fees

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

13

The arrangement fees for borrowings is amortized over the borrowing period, and it is charged to the income statement unless the borrowing is related to an asset eligible for capitalization, a capitalization of amortized arrangement fees take place.

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

14

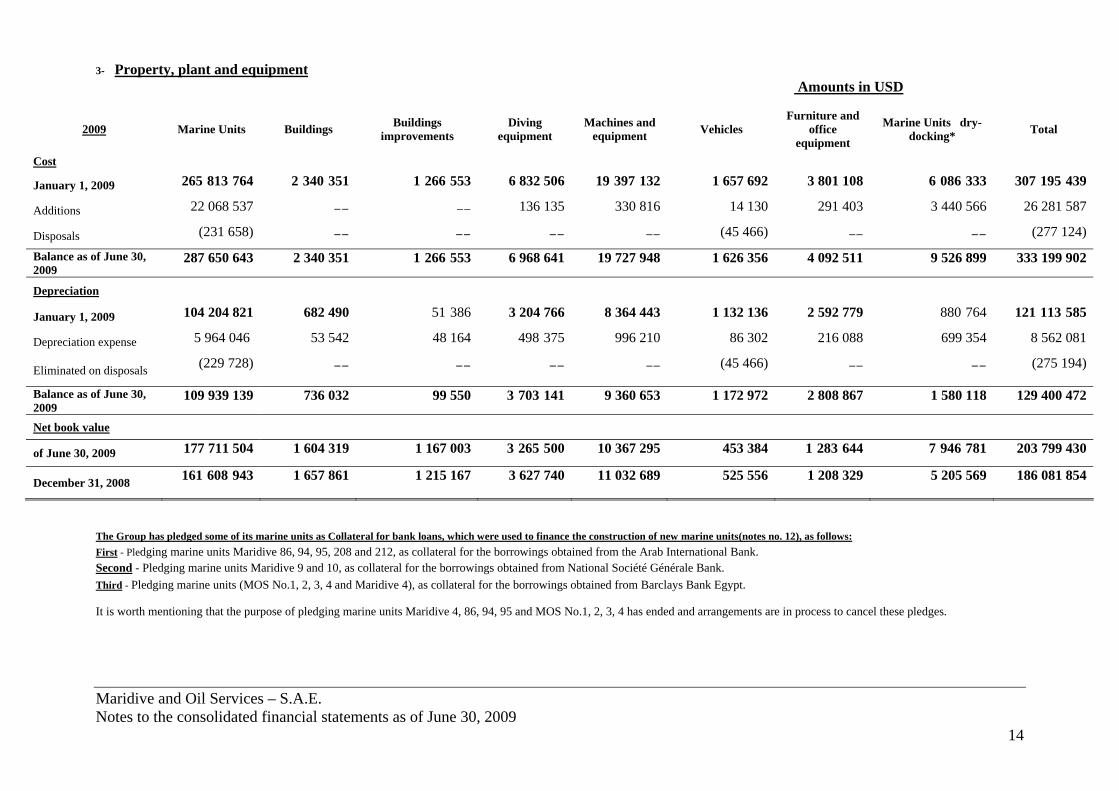

3- Property, plant and equipment Amounts in USD

The Group has pledged some of its marine units as Collateral for bank loans, which were used to finance the construction of new marine units(notes no. 12), as follows: First - Pledging marine units Maridive 86, 94, 95, 208 and 212, as collateral for the borrowings obtained from the Arab International Bank. Second - Pledging marine units Maridive 9 and 10, as collateral for the borrowings obtained from National Société Générale Bank. Third - Pledging marine units (MOS No.1, 2, 3, 4 and Maridive 4), as collateral for the borrowings obtained from Barclays Bank Egypt. It is worth mentioning that the purpose of pledging marine units Maridive 4, 86, 94, 95 and MOS No.1, 2, 3, 4 has ended and arrangements are in process to cancel these pledges.

2009 Marine Units Buildings Buildings improvements

Diving equipment

Machines and equipment Vehicles

Furniture and office

equipment

Marine Units dry-docking* Total

Cost

January 1, 2009 764 813 265 351 340 2 553 266 1 6 832 506 132 397 19 1 657 692 3 801 108 333 086 6 439 195 307

Additions 22 068 537 -- -- 136 135 330 816 14 130 291 403 3 440 566 26 281 587

Disposals (231 658) -- -- -- -- (45 466) -- -- (277 124)

Balance as of June 30, 2009

287 650 643 2 340 351 553 266 1 6 968 641 19 727 948 1 626 356 4 092 511 9 526 899 333 199 902

Depreciation

January 1, 2009 104 204 821 682 490 386 51 3 204 766 8 364 443 1 132 136 2 592 779 764 880 585 113 121

Depreciation expense 5 964 046 53 542 48 164 375 498 996 210 86 302 216 088 699 354 8 562 081

Eliminated on disposals (229 728) -- -- -- -- (45 466) -- -- (275 194)

Balance as of June 30, 2009

109 939 139 736 032 99 550 141 703 3 9 360 653 1 172 972 2 808 867 1 580 118 129 400 472

Net book value

of June 30, 2009 177 711 504 1 604 319 1 167 003 500 265 3 10 367 295 453 384 644 283 1 781 946 7 203 799 430

December 31, 2008 943 608 161 1 657 861 1 215 167 3 627 740 11 032 689 525 556 1 208 329 5 205 569 186 081 854

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

15

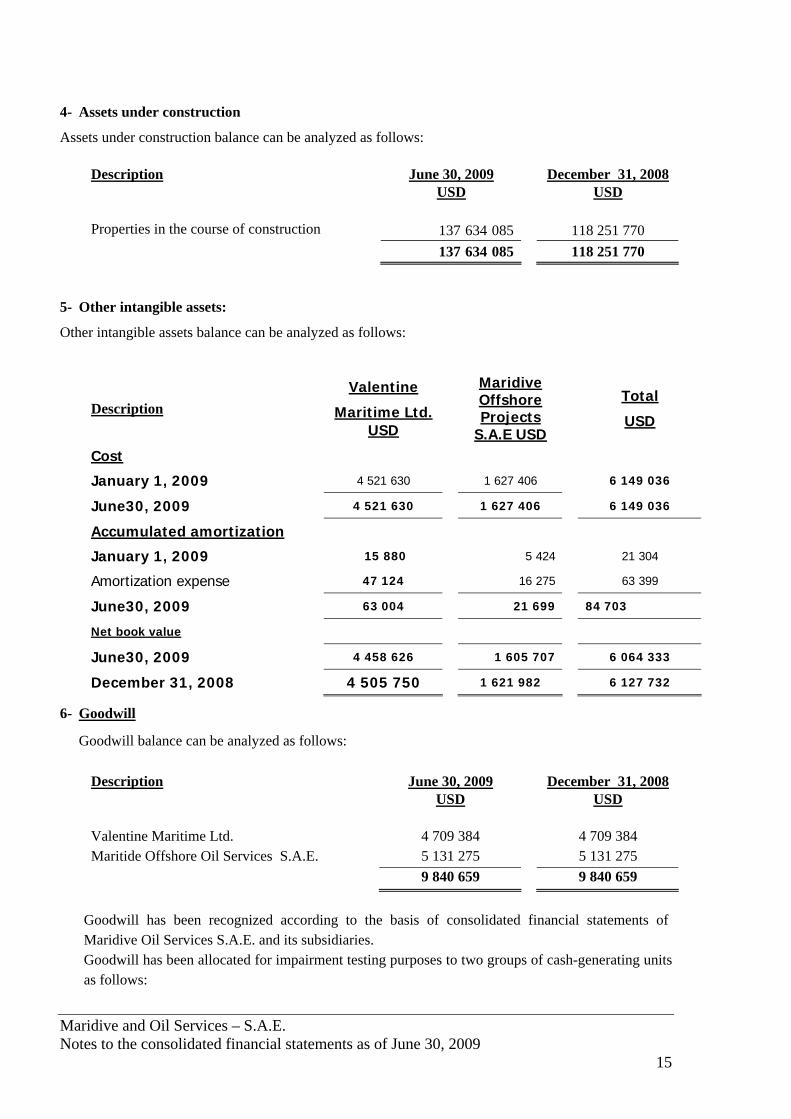

4- Assets under construction

Assets under construction balance can be analyzed as follows:

Description June 30, 2009 December 31, 2008 USD USD Properties in the course of construction 085 634 137 118 251 770 085 634 137 118 251 770

5- Other intangible assets:

Other intangible assets balance can be analyzed as follows:

Description Valentine

Maritime Ltd. USD

Maridive Offshore Projects

S.A.E USD

Total

USD

Cost

January 1, 2009 630 521 4 406 627 1 036 149 6

June30, 2009 630 521 4 406 627 1 036 149 6

Accumulated amortization

January 1, 2009 880 15 424 5 304 21

Amortization expense 47 124 275 16 63 399

June30, 2009 63 004 699 21 84 703

Net book value

June30, 2009 626 458 4 707 605 1 333 064 6

December 31, 2008 4 505 750 982 621 1 732 127 6

6- Goodwill

Goodwill balance can be analyzed as follows:

Description June 30, 2009 December 31, 2008 USD USD Valentine Maritime Ltd. 4 709 384 4 709 384 Maritide Offshore Oil Services S.A.E. 5 131 275 5 131 275 9 840 659 9 840 659

Goodwill has been recognized according to the basis of consolidated financial statements of Maridive Oil Services S.A.E. and its subsidiaries. Goodwill has been allocated for impairment testing purposes to two groups of cash-generating units as follows:

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

16

1- Projects segment: represented in the individual cash generating units of Valentine Maritime Ltd. The recoverable amount of this cash-generating unit is determined based on a value in use calculation which uses cash flow projections based on financial budgets generated from historical data which reflect past experience and are consistent with external sources of information approved by the Group companies Managment covering a five-year period using a discount rate of 16.43% per annum.

Cash flow projections during the budget period are based on 38% gross margins during the budget period. The cash flows within five year period have been extrapolated using a steady 3% to 4% per annum growth rate in order to limit the fluctuations of rates to arrive to an average value that reflects the fair value of the Group companies.

The Group Companies’ Management believes that any reasonably possible further change in the key assumptions on which recoverable amount is based would not cause the aggregate carrying amount to exceed the aggregate recoverable amount of the cash-generating unit.

2- Marine segment: represented in the individual cash-generating units of Maritide Offshore Oil Services S.A.E.

The recoverable amount of this cash-generating unit is determined based on a value in use calculation which uses cash flow projections based on financial budgets generated from historical data which reflect past experience and are consistent with external sources of information approved by the Group Companies’ Managment covering a five-year period using a discount rate of 14.89% per annum.

Cash flow projections during the budget period are between 30% to 33% gross margins during the budget period. The cash flows within five-year period have been extrapolated using a steady 3% to 4% per annum growth rate in order to limit the fluctation of rates to arrive to an average value that reflects the fair value of the company.

The Group Companies Management believes that any reasonably possible further change in the key assumptions on which recoverable amount is based would not cause the aggregate carrying amount to exceed the aggregate recoverable amount of the cash-generating unit.

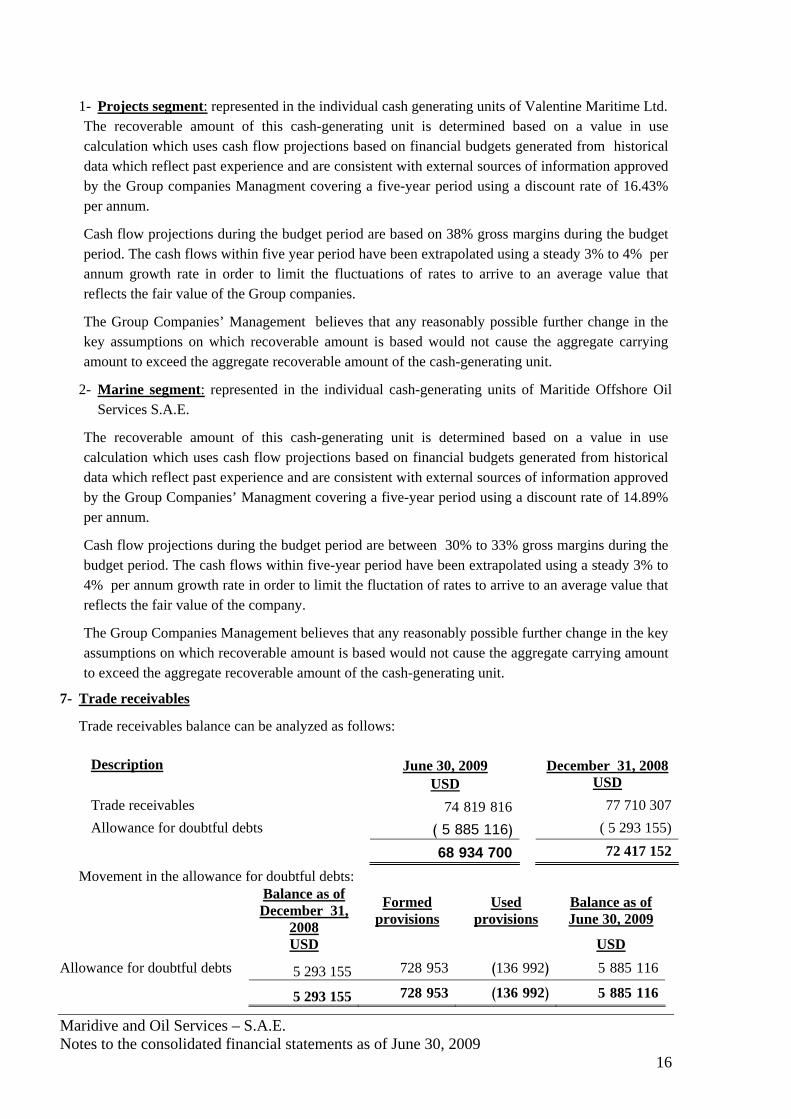

7- Trade receivables

Trade receivables balance can be analyzed as follows:

Description June 30, 2009 December 31, 2008 USD USD Trade receivables 816 819 74 307 710 77Allowance for doubtful debts )116 885 5( )155 293 5(

700 934 68 152 417 72

Movement in the allowance for doubtful debts:

Balance as of December 31,

2008

Formed provisions

Used provisions

Balance as of June 30, 2009

USD USD Allowance for doubtful debts 5 293 155 953 728 )992 136( 116 885 5

5 293 155 953 728 )992 136( 116 885 5

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

17

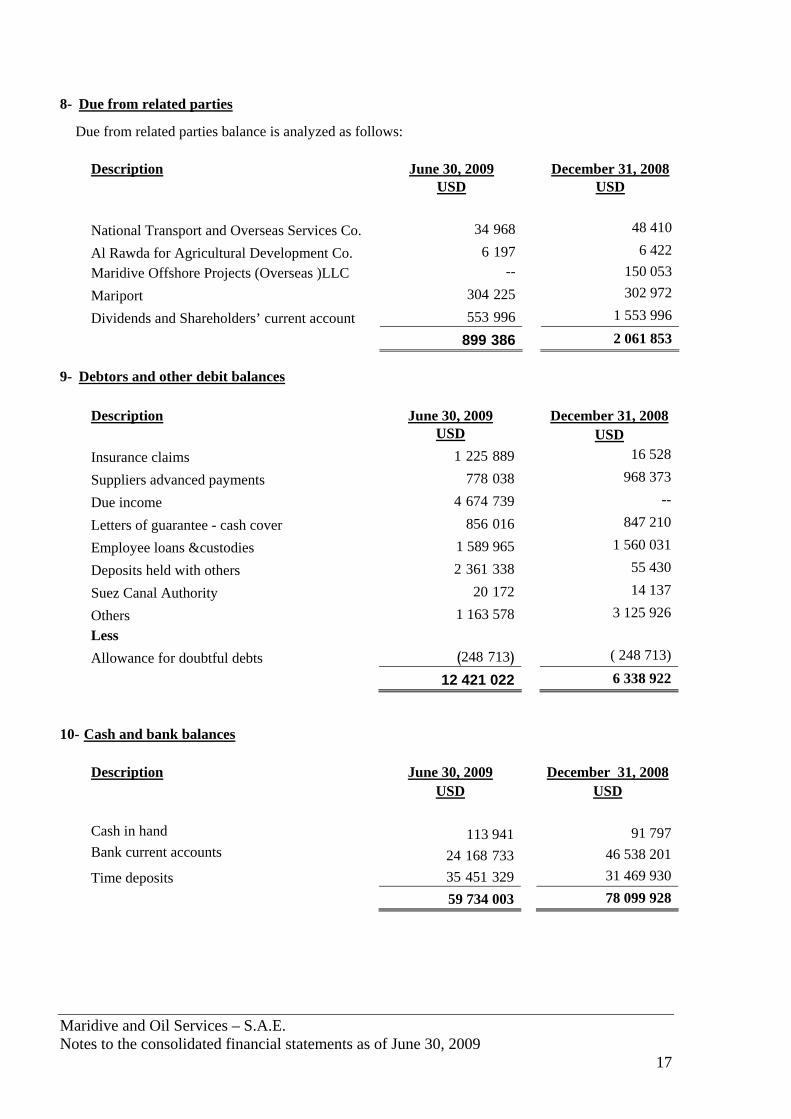

8- Due from related parties

Due from related parties balance is analyzed as follows:

Description June 30, 2009 December 31, 2008 USD USD

National Transport and Overseas Services Co. 968 34 410 48

Al Rawda for Agricultural Development Co. 197 6 422 6 Maridive Offshore Projects (Overseas )LLC -- 053 150

Mariport 225 304 972 302

Dividends and Shareholders’ current account 996 553 996 553 1

386 899 853 061 2

9- Debtors and other debit balances

Description June 30, 2009 December 31, 2008 USD USD Insurance claims 889 225 1 528 16

Suppliers advanced payments 038 778 373 968

Due income 739 674 4 --

Letters of guarantee - cash cover 016 856 210 847

Employee loans &custodies 1 589 965 031 560 1

Deposits held with others 338 361 2 430 55

Suez Canal Authority 172 20 137 14

Others 1 163 578 926 125 3 Less Allowance for doubtful debts )713 248( )713 248(

12 421 022 922 338 6

10- Cash and bank balances Description June 30, 2009 December 31, 2008

USD USD

Cash in hand 113 941 797 91Bank current accounts 733 168 24 201 538 46Time deposits 329 451 35 930 469 31

59 734 003 928 099 78

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

18

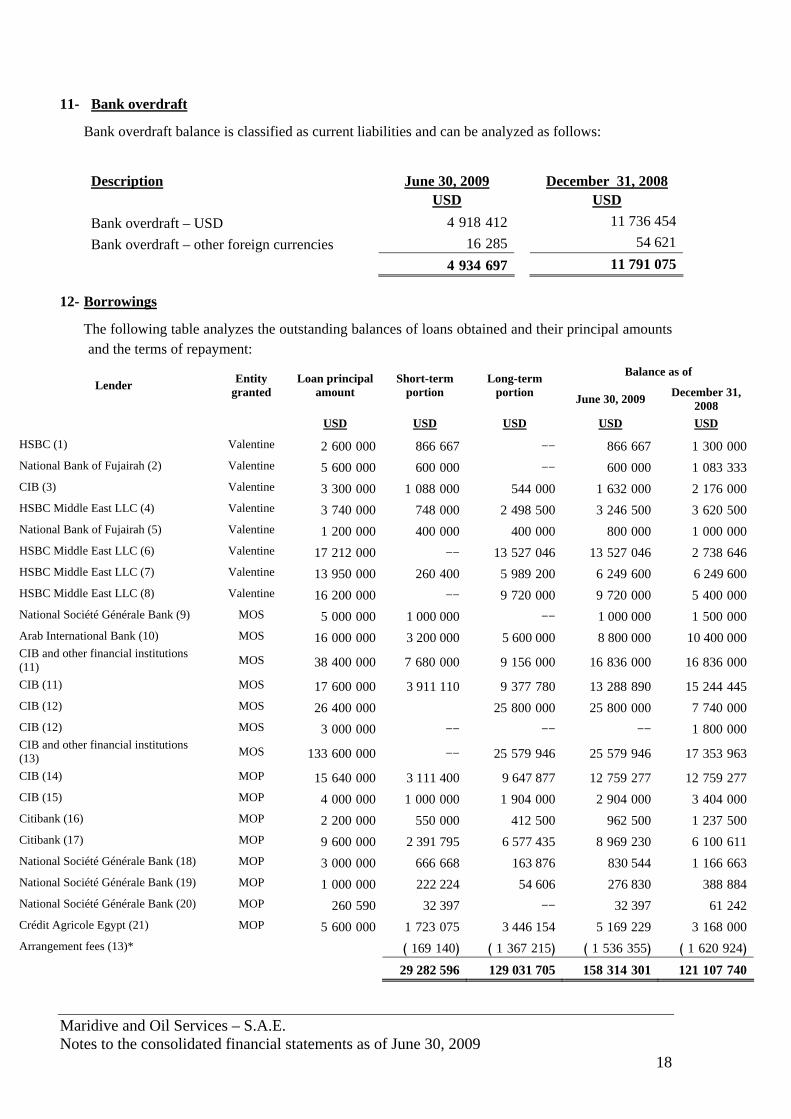

11- 1Bank overdraft

Bank overdraft balance is classified as current liabilities and can be analyzed as follows:

Description June 30, 2009 December 31, 2008 USD USD Bank overdraft – USD 412 918 4 454 736 11Bank overdraft – other foreign currencies 285 16 621 54

697 934 4 075 791 11

12- Borrowings

The following table analyzes the outstanding balances of loans obtained and their principal amounts and the terms of repayment:

Balance as of Lender Entity

granted Loan principal

amount Short-term

portion Long-term

portion June 30, 2009 December 31, 2008

USD USD USD USD USD

HSBC (1) Valentine 000 600 2 667 866 -- 667 866 000 300 1 National Bank of Fujairah (2) Valentine 000 600 5 000 600 -- 000 600 333 083 1 CIB (3) Valentine 000 300 3 000 088 1 000 544 000 632 1 000 176 2 HSBC Middle East LLC (4) Valentine 000 740 3 000 748 500 498 2 500 246 3 500 620 3 National Bank of Fujairah (5) Valentine 000 200 1 000 400 000 400 000 800 000 000 1 HSBC Middle East LLC (6) Valentine 000 212 17 -- 046 527 13 046 527 13 646 738 2 HSBC Middle East LLC (7) Valentine 000 950 13 400 260 200 989 5 600 249 6 6 249 600 HSBC Middle East LLC (8) Valentine 000 200 16 -- 000 720 9 000 720 9 000 400 5 National Société Générale Bank (9) MOS 000 000 5 1 000 000 -- 1 000 000 000 500 1 Arab International Bank (10) MOS 000 000 16 3 200 000 5 600 000 8 800 000 10 400 000 CIB and other financial institutions (11) MOS 000 400 38 000 680 7 000 156 9 000 836 16 000 836 16

CIB (11) MOS 000 600 17 3 911 110 780 377 9 890 288 13 445 244 15 CIB (12) MOS 000 400 26 000 800 25 000 800 25 000 740 7 CIB (12) MOS 000 000 3 -- -- -- 000 800 1 CIB and other financial institutions (13) MOS 000 600 133 -- 946 579 25 946 579 25 963 353 17

CIB (14) MOP 000 640 15 3 111 400 9 647 877 277 759 12 277 759 12 CIB (15) MOP 000 000 4 000 000 1 000 904 1 000 904 2 000 404 3 Citibank (16) MOP 000 200 2 000 550 500 412 500 962 500 237 1 Citibank (17) MOP 000 600 9 2 391 795 6 577 435 230 969 8 611 100 6 National Société Générale Bank (18) MOP 000 000 3 668 666 163 876 830 544 663 166 1 National Société Générale Bank (19) MOP 000 000 1 222 224 54 606 276 830 884 388 National Société Générale Bank (20) MOP 590 260 32 397 -- 32 397 242 61 Crédit Agricole Egypt (21) MOP 000 600 5 075 723 1 3 446 154 229 169 5 000 168 3 Arrangement fees (13)* )140 169( )215 367 1( )355 536 1( )924 620 1( 29 282 596 129 031 705 301 314 158 740 107 121

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

19

*Arrangement fees were decreased from loan balances whereas they are regarded as financial burdens.

(1) HSBC Middle East LLC – Valentine

In June 2007, a loan agreement was signed between Valentine Maritime Ltd and HSBC Middle East LLC for a total amount of USD 2.6 million. The loan was obtained to finance the acquisition of Ocean Marine FZC from Winco, bearing an interest rate of LIBOR plus a margin of 1.5%. The loan is repayable over 12 equal quarterly installments of USD 216 667 each.

(2) National Bank of Fujairah – Valentine

In April 2003, a loan agreement was signed between Valentine Maritime Ltd and National Bank of Fujairah for a total amount of USD 2.7 million. During 2006 , the loan amount was increased with an additional amount of 1.5 million. The proceeds of the loan were used to finance the purchase of a new vessel. The loan is repayable over 12 equal quarterly installments of USD 125 000 each. An additional amount of USD 1.4 million was obtained during 2007, bearing an interest rate of LIBOR plus a margin of 1.25%, and is repayable over 12 equal quarterly installments of USD 116 667 each.

(3) Commercial International Bank – Valentine

In September 2007 a loan agreement was signed between Valentine Maritime Ltd and Commercial International Bank for a total amount of USD 3.3 million to finance 80% of the purchase of a new marine unit, bearing an interest rate of LIBOR plus a margin of 1.3% . The loan is repayable over 12 equal quarterly installments of USD 272 000 each Starting from January 2008.

(4) HSBC Middle East LLC – Valentine

In November 2007, a loan agreement was signed between Valentine Maritime Ltd and HSBC Middle East LLC for a total amount of USD 1.18 million. The total amount per loan agreement after increase amounted to USD 3.74 million and is repayable over 19 equal installments of USD 187000 additon to installment USD 67500 commencing after completion of drawdown period. The loan was obtained to lease a piece of land at the Bahrain Investment Wharf.

(5) National Bank of Fujairah – Valentine

In March 2008 a loan agreement was signed between Valentine Maritime Ltd and National Bank of Fujairah for the amount of USD 1.2 million to finance the purchase of a new marine unit. The loan is repayable over 12 equal quarterly installments of USD 100 000 each.

(6) HSBC Middle East LLC – Valentine

In January 2008 a loan agreement was signed between Valentine Maritime Ltd and HSBC Middle East LLC for the amount of USD.17.212 million and is repayable over 48 equal quarterly installments of USD 358 583 each, commencing six months after completion of drawdown period. The loan was obtained to finance the purchase of a new marine unit.

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

20

(7) HSBC Middle East LLC – Valentine

In March 2008 a loan agreement was signed between Valentine Maritime Ltd and HSBC Middle East LLC for the amount of USD 13.95 million and is repayable over 48 equal quarterly installaments of USD 290 625 each. The loan was obtained to finance the purchase of a new marine unit.

(8) HSBC Middle East LLC – Valentine

In December 2008 a loan agreement was signed between Valentine Maritime Ltd and HSBC Middle East LLC for the amount of USD 16.2 million and is repayable over 48 equal quarterly installaments of USD 337 500 each, commencing after the completion of the drawdown of the whole amount or 24 months from the beginning of the drawdown period, with a grace period of six months. The loan was obtained to finance 75% of the purchase of equipment for the barge.

The above term loans granted to Valentine are secured by pledging its marine units, personal guarantees of the Managing Director and joint collateral of Valantine Maritime Ltd and Maridive & Oil Services S.A.E., bearing interest rates ranging from LIBOR plus a margin of 1.25% per annum to LIBOR plus a margin of 1.75% per annum.

(9) National Société Générale Bank (NSGB) - MOS

In June 2005 a loan agreement was signed between MOS and NSGB for a total amount of USD 5 million. The loan proceeds were to finance the working capital of the Company, bearing an interest of 1 month LIBOR plus a margin of 1% to be paid quarterly. The loan is repayable in 20 equal quarterly installments of USD 250 000 each, starting from June 2005.

(10) Arab International Bank - MOS

In April 2004, a loan agreement was signed between MOS and Arab International Bank for a total amount of 16 million. The loan proceeds were to finance 80% of the cost of the construction of two marine units, bearing an interest of 1 month LIBOR plus a margin of 1.5% to be paid monthly. The loan is repayable over 20 equal quarterly installments of USD 800 000 each, starting from January 2007.

(11) Commercial international Bank and other financial institutions - MOS

In January 2005, a syndicated financing contract was signed between MOS and CIB (financing director & agent of joint lenders) and other financial institutions (NSGB, Arab Bank, Egyptian American Bank and the OPEC Fund for International Development) for a total amount of USD 48 million. The loan proceeds were to finance 80% of the total cost of constructing of four marine units and the purchase of two used marine units, bearing an interest of 3 months LIBOR plus a margin of 1.75% to be paid quarterly.

In June 5, 2008, an approval was taken from the CIB to increase the loan by an amount of USD 8 million, to finance the increase in the cost resulting from the construction of two marine units instead of purchasing the used ones, so the total amount of the loan from the CIB amounted to USD 56.6 million,

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

21

The financing will be on two tranches as follows:

A- Tranche 1: An amount not more than USD 17.6 million, for a period not more than December 31,2008. This tranche is repayable over 9 equal quarterly installments of USD 1 955 555 each, starting from October1,2008 and ending October1, 2012.

B- Tranche 2: An amount not more than USD 38.4 million, This tranche is repayable over 10 equal quarterly installments of USD 3 840 000 each, starting from July1,2009 and ending January , 2014.

(12) Commercial international Bank - MOS

During 2007, a loan agreement was signed between MOS and Commercial International Bank for a total amount of USD 26.4 million. The loan proceed were used to finance 80% of the total cost of constructing three marine units, bearing an interest of 6 months LIBOR plus a margin of 1.3% to be paid quarterly during the first 3 years from financing period, a margin of 1.5% to be paid quarterly from the 4 th year up to the 7 th year and a margin of 1.8% to be paid quarterly 1.8% from the 8 th year up to the end of financing period. The loan is repayable over 28 quarterly installments of USD 942 857 each, and the last installment with an amount of USD 942 861, starting from January 2010 and ending on April 2017.

The company was also given a short–term loan from the Commercial International Bank for a total amount of USD 3 million, The company repaid the loan in full in February,2009.

(13) Commercial International Bank & Other Financial Institutions - MOS

In April 2008 a syndicated financing contract was signed between MOS and CIB (financing director & agent of joint lenders) and Credit Agricole Egypt (as financing director agent, and marketing and distribution agent) and other Banks and financial institutions (Arab African International Bank, National Bank of Egypt, United Bank, Bank of Alexandria and the Export Development Bank of Egypt) for a total amount of USD 133.6 million. The loan proceeds were to finance 80% of the total cost of constructing of nine marine units, bearing an interest of 3 months LIBOR plus a margin of 1.4% to be paid quarterly during the first three years, a margin of 1.6% annually during the fourth and the fifth years, and a margin of 1.75 % from the sixth year till the end of the financing.

The financing will be on two tranches as follows:

A- Tranche 1: An amount not more than USD 73.6 million, for a period not more than ten years from the contract date, it is also worth mentioning that the drawdown period will end on November 30, 2010 at most or withdrawing the total amount of this tranche, the grace period will end on December 1, 2010. This tranche is repayable over 28 equal quarterly installments of USD 2 628 571 each, starting from December 1, 2010 and ending September 1, 2017.

B- Tranche 2: An amount not more than USD 60 million, for a period not more than ten years from the contract date, it is also worth mentioning that the drawdown period will end on May 30, 2011 or withdrawing the total amount of this tranche, the grace period will end on June 1, 2011. This tranche is repayable over 28 equal quarterly installments of

USD 2142857 each, starting from June 1, 2011 and ending March 1, 2018.

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

22

The arrangement fees for this syndicated loan amounted to USD 1 691 400, and it is amortized over the contract period, which is 10 years.

(14) Commercial International Bank (CIB) – MOP

A long term loan agreement was signed between Maridive Offshore Projects S.A.E. and the Commercial International Bank for a total amount of USD 7.2 million. The proceeds of the loan were to finance the construction of a new barge “Maridive Constructor”, the loan was increased by an amount of USD 3.44 million to become USD 10.640 million, this increase was to finance 80% of the construction cost of pipelaying equipment for the barge, the loan was increased by an additional amount of USD 5 million to finance 80% of the increase in the construction cost of the barge, bearing an interest of 3 months LIBOR plus a margin of 1.75% to be paid quarterly. This loan is repayable over 20 equal quarterly installments of USD 777 850 each, starting from September 30, 2009 and ending June 31,2014.

(15) Commercial International Bank (CIB) – MOP

A long term loan agreement was signed between Maridive Offshore Projects S.A.E. and the Commercial International Bank for a total amount of USD 4 million. The proceeds of the loan were to finance 80% from the construction of marine unit “Maridive 35”, bearing an interest of 6 months LIBOR plus a margin of 1.3% during the first three years, an interest of 6 months LIBOR plus a margin of 1.5% from the fourth year until the end of the loan term. This loan is repayable over 16 equal quarterly installments of USD 250 000 each, starting from July 31, 2008 and ending April 30, 2012.

(16) Citibank Loan – MOP

A long term loan agreement was signed between Maridive Offshore Projects S.A.E. and Citibank for a total amount of USD 2.2 million. The proceeds of the loan were to refinance the cost of marine unit “MOP 50”, bearing an interest of 3 months LIBOR plus a margin of 1.25% to be paid quarterly. This loan is repayable in 16 equal quarterly installments of USD 137 500 each, starting from May 31,2007 and ending Febuarury 28, 2011.

(17) Citibank Loan – MOP

A long term loan agreement was signed between Maridive Offshore Projects S.A.E and Citibank for total amount USD 9.6 million. The proceeds of the loan were to finance 80% from the construction cost of two Marine vessels “Maridive 32” and “Maridive 36”, bearing an interest of 3 months LIBOR plus a margin of 1.25% to be paid quarterly. This loan is repayable over 16 equal quarterly installments of USD 600 000 each, starting from May28, 2009 and ending Febuarury 28, 2013. and Registrer That in the Commercial Register of the company on February14,2008

(18) National Société Générale Bank (NSGB) - MOP

A long term loan agreement was signed between MOP and NSGB for a total amount of USD 3 million. The proceeds of the loan were to finance 80% from the construction cost of the barge “Offshore Base”. The loan is repayable over 18 quarterly installments consisting of 17 equal quarterly installments of USD 166 667 each and an installment of USD 166 661, starting from May 30, 2006 and ending August 30, 2010.

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

23

(19) National Société Générale Bank (NSGB) - MOP

A long term loan agreement was signed between MOP and NSGB for a total amount of USD 1 million. The proceeds of the loan were to finance the barge “Offshore Base”. This loan is repayable over 18 quarterly installments consisting of 17 equal quarterly installments of USD 55 556 each and an installment of USD 54 606, starting from June 1, 2006 and ending September 1, 2010.

(20) National Société Générale Bank (NSGB) - MOP

A long term loan agreement was signed between MOP and NSGB for a total amount of USD 260 590. The proceeds of the loan were to finance the barge “Offshore Base”. This loan is repayable over 16 quarterly installments consisting of 15 equal quarterly installments of USD 16 286 each and an installment of USD 16 111, starting from January 28, 2006 and ending October 28, 2009.

(21) Credit Agricole Egypt - MOP

A long term loan agreement was signed between MOP and Credit Agricole Egypt for a total amount of USD 5.6 million. The proceeds of the loan were to finance 80% from the construction cost of a “Diving Saturation System”, bearing an interest of 3 months LIBOR plus a margin of 0.95% to be paid quarterly. This loan is repayable over 13 equal annual installments of USD 430 769 each, starting from April 1, 2009 and ending April 2, 2012.

13- Provisions

The movement in provisions can be analyzed as follows:

Description Balance as of December 31,

2008 Provision

formed Provision Used Balance as of June 30, 2009

USD USD USD USD Legal claims 640 171 617 41 -- 257 213 End of service benefit 905 373 2 754 361 )238 76( 421 659 2

545 545 2 371 403 )238 76( 678 872 2

Legal claims provision

The legal claims provisions are related to claims expected to be made by a third party in connection with the business operations. The information usually required to be disclosed by accounting standards is not disclosed because management believes that disclosing such information would seriously prejudice the outcome of the negotiation with that third party. These provisions are reviewed by management every year and adjustments to the amounts provided are based on the latest development, discussions and agreements with the third party.

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

24

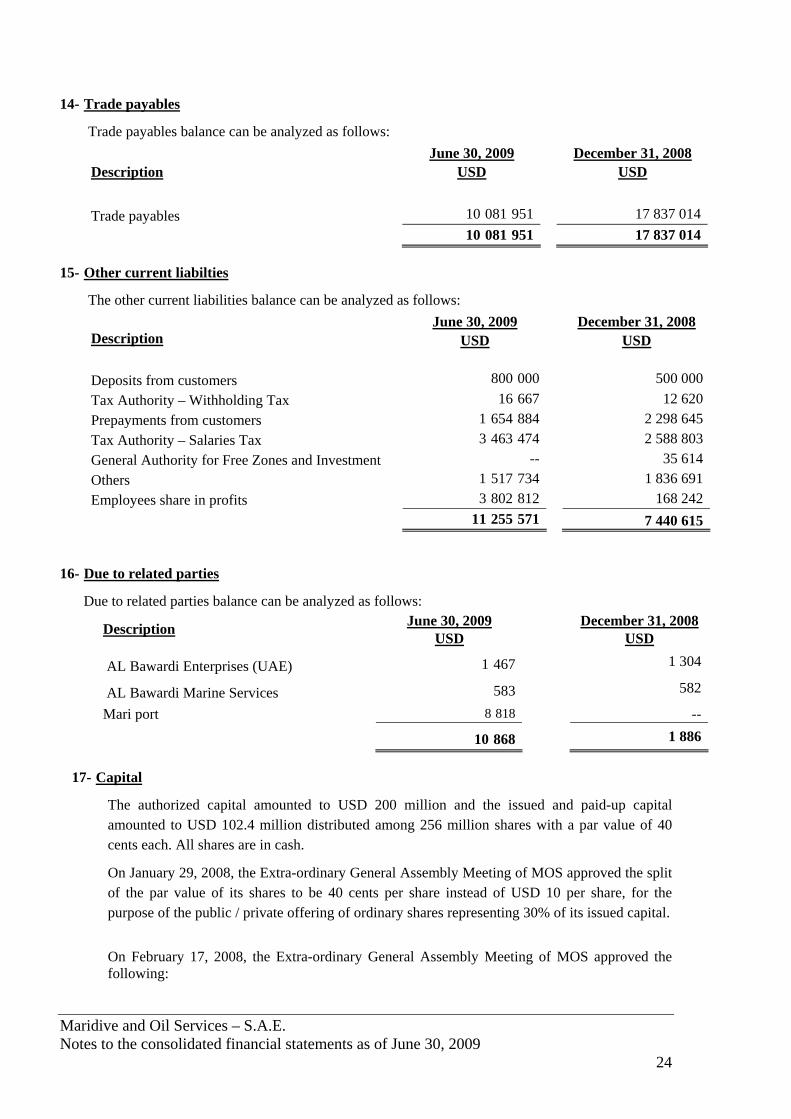

14- Trade payables

Trade payables balance can be analyzed as follows: June 30, 2009 December 31, 2008

USD USD Description

Trade payables 951 081 10 014 837 17 951 081 10 014 837 17

15- Other current liabilties

The other current liabilities balance can be analyzed as follows: June 30, 2009 December 31, 2008

USD USD Description

Deposits from customers 000 800 000 500Tax Authority – Withholding Tax 667 16 620 12Prepayments from customers 884 654 1 645 298 2 Tax Authority – Salaries Tax 474 463 3 803 588 2 General Authority for Free Zones and Investment -- 614 35Others 734 517 1 691 836 1Employees share in profits 812 802 3 242 168 571 255 11 7 440 615

16- Due to related parties

Due to related parties balance can be analyzed as follows: June 30, 2009 December 31, 2008 Description USD USD

AL Bawardi Enterprises (UAE) 467 1 1 304

AL Bawardi Marine Services 583 582

Mari port 818 8 --

868 10 1 886

17- Capital

The authorized capital amounted to USD 200 million and the issued and paid-up capital amounted to USD 102.4 million distributed among 256 million shares with a par value of 40 cents each. All shares are in cash.

On January 29, 2008, the Extra-ordinary General Assembly Meeting of MOS approved the split of the par value of its shares to be 40 cents per share instead of USD 10 per share, for the purpose of the public / private offering of ordinary shares representing 30% of its issued capital. On February 17, 2008, the Extra-ordinary General Assembly Meeting of MOS approved the following:

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

25

First: Approving the fair value of the company’s shares, in the light of the study prepared by the independent financial consultant, being USD 610 918 174, accordingly the fair value of each share amounted to USD 3.76, and also approved the shares swap rate being 32,27 share of MOS equal to 1 share of MOP.

Second: Increasing the issued capital by 64 537 010 shares equivalent to USD 25 814 804, through the exchange of these capital increase shares (after being registered at the Stock Exchange) with 100% of MOP's shares, the acquired company, (after being registered at the Stock Exchange).

All the procedures of the share swap agreement were completed and registered in the commercial register. The Extra-ordinary General Assembly Meeting of MOS held on April 14, 2008 decided to delegate its Board of Directors in increasing the issued capital within the limits of the authorized capital, through issuing a number of shares not exceeding 28 962 990 shares, and offering these capital increase shares to the shareholders whom offered their shares in a secondary offer, at the same price used in the private placement in the secondary market, provided that the difference between the par value and the subscription value should be transferred to the reserve account. The paid-up capital was increased by USD 11 585 196 through a subscription by the old shareholders for an amount of USD 107 163 063 among which USD 11 585 196 is par value and USD 95 577 867 is share premium, therefore the issued and paid-up capital reached USD 102.4 million.

18- Legal reserve

The legal reserve balance as of June 30, 2009 amounted to USD 20 480 000, an amount equal to 5% of the net profit of the year is appropriated to form the legal reserve provided that the balance would not exceed 20% of the paid-up capital.

19- Special reserve

During the year the share premium was transferred, in accordance with the requirements of law No. 159 for 1981, to both the legal reserve by an amount of USD 8 714 797, to reach 20% of the paid-up capital, and the special reserve by an amount of USD 76 877 138.

June 30, 2009 December 31, 2008 USD USD Balance at the beginning of the year 20 480 000 016 675 9

Transferred from previous year’s profit -- 187 090 2

Transferred from share premium (Note 20) -- 797 714 8

Balance at the end of the / (period) year 20 480 000 20 480 000

June 30, 2009 December 31, 2008 USD USD Transferred from share premium 138 877 76 138 877 76 138 877 76 138 877 76

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

26

20- Share premium

* The General Assembly Meeting held on March 14,2009 approved to transfer the share premium to both the legal reserve and the special reserve **The share premium represents the difference between the collected cash and the issued capital, as follows:

Collected cash

No. of shares

Par value per share

Issued capital

Share premium

Private subscription (old shareholders) 107 163 063

28 962 990 40 cents 11 585 196 95 577 867

107 163 063 11 585 196 95 577 867

** *Share issue cost The share issue costs amounted to USD 9 985 932 represents the fees of offering the capital increase shares, these costs includes registration, marketing, legal and other professional fees.

21- Minority interest

22- Financial instruments - fair value and risk management

The financial instruments are represented in balances of cash and banks, debtors, creditors, borrowings and bank overdraft. The carrying amounts of these financial instruments represent a reasonable estimate of their fair values.

a. Capital risk management

Management of the Group manages its capital to ensure that the Group will be able to continue as a going concern, while maximizing the return to shareholders through the optimization of the debt and equity balances. The Group's overall strategy remains unchanged from 2007.

The capital structure of the Group consists of debt, comprising bank overdraft, borrowings, cash banks as disclosed in notes 10, 11 and 12 respectively, and total shareholders' equity.

June 31, 2009 December 31, 2007 USD USD *Premium collected upon subscription -- 95 577 867** Share issue costs -- (9 985 932)***Transferred to reserves -- (85 591 935) -- --

June 30, 2009 December 31, 2008 Description USD USD Minority interest in Valentine Maritime Ltd 839 146 23 26 093 586Minority interest in Maritide Offshore Oil Services 333 36 38 255Minority interest in Maridive Offshore Projects 7 800 -- 972 190 23 26 131 841

Maridive and Oil Services – S.A.E. Notes to the consolidated financial statements as of June 30, 2009

27

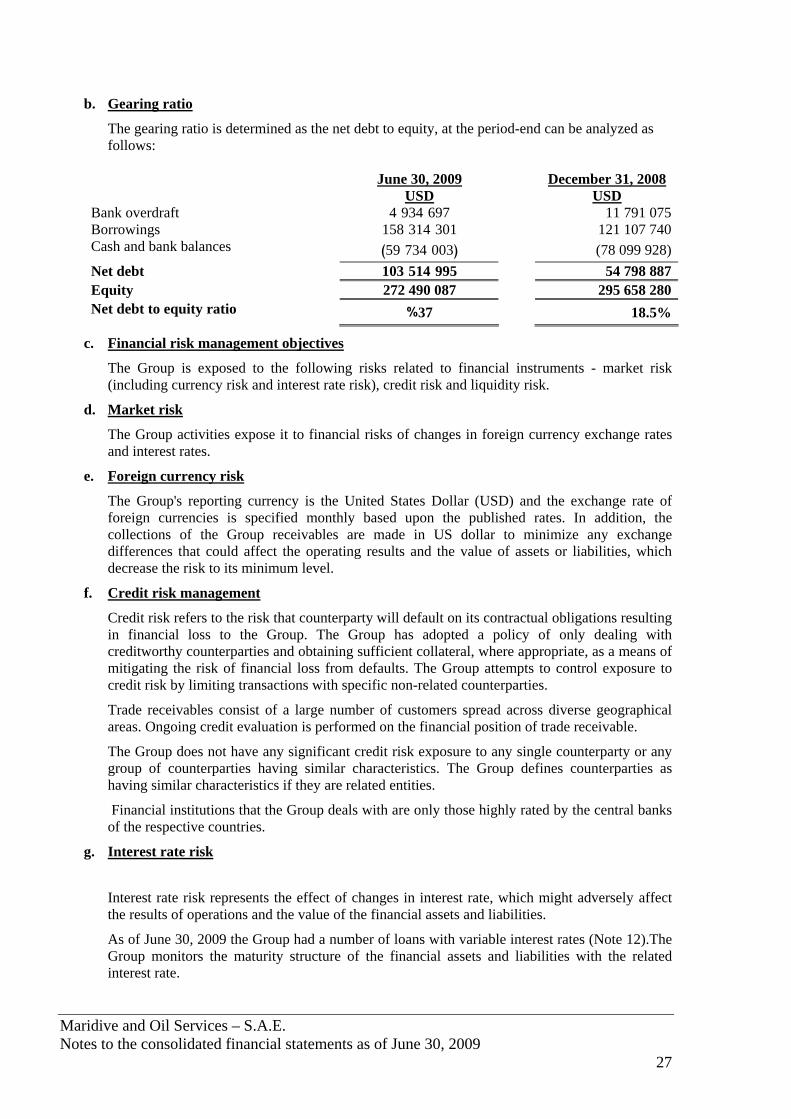

b. Gearing ratio

The gearing ratio is determined as the net debt to equity, at the period-end can be analyzed as follows:

June 30, 2009 December 31, 2008 USD USD Bank overdraft 697 934 4 11 791 075Borrowings 301 314 158 121 107 740Cash and bank balances )003 734 59( (78 099 928)Net debt 995 514 103 54 798 887Equity 272 490 087 295 658 280Net debt to equity ratio 37% 18.5%

c. Financial risk management objectives

The Group is exposed to the following risks related to financial instruments - market risk (including currency risk and interest rate risk), credit risk and liquidity risk.

d. Market risk

The Group activities expose it to financial risks of changes in foreign currency exchange rates and interest rates.

e. Foreign currency risk