Embed Size (px)

Citation preview

Presentation by Rodrigo Custodio

Iacutelhavo January 2019

Roland Bergeracutes global automotive supplier study highlights

2RB - Global automotive supplier study highlights 23012019pptx

We are one of the largest strategic consultancies with a strong expertise in the automotive area

Our profile Our competence matrix

Our automotive practice Our values

Created in 1967in Germany by Prof Dr Roland Berger

50 offices in36 countries with2400 employees

Over 240 Partners

~1000 international clients

1993Brussels | Kiev |

Prague |

1994Moscow

1995Beijing

1997Budapest | Zuumlrich

2002Amsterdam

1998Detroit | Shanghai

2000Warsaw

2003Zagreb

2006Manama

2007Chicago | Hong Kong |Beirut

2008Casablanca | Istanbul | Taipei

2009Doha

2010Stockholm | Goteborg |

Singapore

2011Dubai | Kuala Lumpur |

Lagos | Jakarta

2012Seoul | New Delhi |

Guangzhou |Montreal | Boston

2013Mumbai

2014Bangkok | Pune

1967

1969

1976

1982

1986

Munich

Milan

Satildeo Paulo

1987Stuttgart

Duumlsseldorf

Madrid

1989Frankfurt | Vienna

1990Berlin | Hamburg |Lisbon | London |Paris

1991Tokyo

1992Bucharest

Source Roland Berger

Overview of Roland Berger

ExcellenceWe achieve excellent results and develop global best practices to ensure measurable and sustainable success

EmpathyWe are insightful and responsible advisors and

we contribute to the greater good

EntrepreneurshipWe follow an entrepreneurial approach and provide creative and pragmatic solutions

3RB - Global automotive supplier study highlights 23012019pptx

The global automotive industry has presented a growth of 3 in recent years

World

North America Europe3) China4)

JapanKorea

CAGR2) 24 CAGR2) 29 CAGR2) 86

CAGR2) 31 CAGR2)-10

2018

170

2016

178

20172015

-2

174

2013

170

2012 2014

175154 162

2012 20152014

201 210

2013

222

2016

193 215195

2017

-1

2018

220 273

2016

-3

280274

2017

240

2014

230213

20152013

186

2012 2018

South America

CAGR2) -52

2018

35

2013

332731

2014

45

201720162015

+5

3843

2012

132

20182016

0

129

2015

133

2017

133137

20142013

135

2012

139

0

2017

947

20182013

874815

2012

888

2015

847

2016

931

2014

951

Global light vehicle production volume1) by region 2012-2017 [m units]

Source IHS Roland Berger

1) Incl light commercial vehicles 2) CAGR 2012-2017 3) Excluding CIS and Turkey 4) Greater China

4RB - Global automotive supplier study highlights 23012019pptxSource Company information analyst forecasts Lazard Roland Berger

The stability of past industry years have yielded consecutive years of good supplier performance have

Revenue growth EBIT1) margin []

33555413

29

142138131

124118

113

100

20122010 2011 2013 2014 2017e2015

~147

2016

72707371

686871

2015 2017e

~73

2012 20132010 2011 2014 2016

Key supplier performance indicators 2010-2017e (n=~650 suppliers)

1) EBIT after restructuring items

Indexed [2010=100]

YoY []

5RB - Global automotive supplier study highlights 23012019pptx

Valuation of suppliers have increased while of OEMs have remained under pressure

Sources Fact set Roland Berger

PE NTM1)

1x

3x

5x

7x

9x

11x

13x

15x

17x

19x

21x

23x

25x

27x

29x

nov-

07

nov-

08

nov-

09

nov-

10

nov-

11

nov-

12

nov-

13

nov-

14

nov-

15

oct-

16

nov-

17

gt In recent years the valuation figures for suppliers have been significantly higher than those for OEMs

gt The valuation gap has hit an all-time high ndash The valuations of suppliers are almost twice as high as those of OEMs

gt Risks arising from disruptive trends appear to have been priced in to OEM valuations ndashThat does not seem to be the case for supplier valuations

Selected automotive OEMs3) Selected automotive suppliers4)

Under the influence of the economic crisis

10-y-avg = 112x2)

80x

10-y-avg = 90x2)

133x

Trend in the valuations of OEMs and suppliers

1) NTM = next twelve months 2) Excluding the distortions triggered by the economic crisis (figures for Jan-Dec 2009) 3) BMW Daimler Ford General Motors Honda Toyota and Volkswagen 4) American Axle Autoliv BorgWarner Brembo Continental Dana Delphi Faurecia Hella Johnson Controls Magna Norma and Valeo

6RB - Global automotive supplier study highlights 23012019pptx

Tim Cook (CEO Apple Inc)

Dieter Zetsche (CEO Daimler AG)

The automotive industry

has reached a

dramatic turning

point with huge changes

Right now we are exper-

iencing the second

invention of the

automobile

Sources Press Roland Berger

The industry is being looked by its own executives and by new interested parties with different eyeshellip

7RB - Global automotive supplier study highlights 23012019pptx

hellipand therefore is already going through significant changes

Prices of used

diesel vehicles1) []

Time in stock with dealers for diesel

vehicles 2016-2018 [days]

Sources Schwacke DAT Roland Berger

Diesel trends

2016 2017 2018

110

105

100

95

90

85

80

75

0

+25

Diesel

Gasoline

1

102

89

12

102

85

11

110

85

10

85

86

3

87

90

2

85

93

1

88

94

100

81

9

96

77

8

101

80

7

94

78

6

95

79

5

99

85

4

94

82

3

98

89

2

99

91

1

97

92

12

96

88

11

95

86

10

94

87

9

92

86

8

88

83

7

81

80

6

80

79

5

83

82

4

56

55

54

53

52

51

50

0

20182017201620152014

Gasoline

Diesel

Avg relative residual price for 3-year-old vehicles with mileage of 60000 km

70

65

60

55

50

0115 0715 0116 0716 0117 0717 0118

0

45

30

35

40 FR

UK

DE

IT

ES

-12

-13

0

-15

-10

Diesel engines as a proportion of

new registrations 2015-12018 []

8RB - Global automotive supplier study highlights 23012019pptx

The speed is cacthing OEMs still unprepared eg difficult adaptation to the new WLTP regulation by OEMs impacted the value chain

Impact of WLTP on the automotive market

There have been several OEMs that have delayed projects that were expected for 2018 (especially during the second half of the year) due to their difficulties to cope with the WLTP1)

regulation

Tier 1 supplier (Spain)

The situation in the market is not stable and OEMs prefer to be conservative I think that most of the reasons are conjunctural We are living an uncertainty political situation and that is why the market is waiting but from my point of view automotive market will change very fast and the growth is going to be

important

Tier 1 supplier (Spain)

The automotive market has been very instable for players across the value chain with sales and profitability lower than expected (proven by the profit warnings issued by many companies in the industry) ndashAll the players are suffering due to the declines in volumes produced and the delays in vehicle launches We dont expect this situation to last any longer

Tier 1 supplier (Spain)

Source Expert Interviews Roland Berger

The OEMs had some projects planned from several years ago (eg some new models with diesel engines or facelifts of their traditional models) that could not be launched any more They are updating these projects or questioning if some of them still make sense Most of those projects will be launched in their new electric versions

from 2020 onwards

Mold manufacturer (Portugal)

9RB - Global automotive supplier study highlights 23012019pptx

There are mainly for disruptive trends that are transforming the automotive industry ndash MADE by Roland Berger

Automotive disruption

Technology andregulatory progress

High customer value and improved safety

Consequences for current cars small vehicles LCVs

After-salesserviceimpact

2 Autonomous

Connectivity

AI

Evolution of digital technologies and culture

Full integration of the connected vehicle in

customers everyday life

3 Digitization

Strategy

How to position

Transformation

How to transform

Alternative

fuels

Automated

driving

Non-traditional

entrants

ICE

advancement

Mobility

solutions

Startup

OEMs

Connectivity

Low-cost

brands

New

retail

Geographic

shift

Source Roland Berger

Changing customer behavior (sharing vs owning)

Urbanization changing traditional mobility and logistics

concepts

New mobility mix and new business modelsplayers

1 New mobility

Compliance with future emissions regulations

Electrification landscape including infrastructure

Profitability challenges

China as a benchmark

4 Electrified

Powertrain

electrification

Emissions

regulations

Light-

weighting

Fuel

cells

10RB - Global automotive supplier study highlights 23012019pptx

The automotive end game appears inevitable yet the transition period is marked by considerable uncertainty

TimeToday

Degree of change

2020 2025 2030

North Americagt Deep penetration of ride hailing in major metropolitan

areasgt Technology leadership in highly automated drivinggt Strong regulatory support

Chinagt Strong push and high maturity for electrificationgt Deep penetration of ride hailing in major

metropolitan areasgt Strong players pushing for

autonomous drivinggt Fast regulatory

decisions

Europegt High population density in cities ndash

ideal for robocabsgt Stringent emissions regulation

driving electrificationgt Slow regulatory processes

Emerging marketsgt Less stringent emissions regulations delaying

the spread of electric vehiclesgt Growing adoption of ride hailing in major citiesgt Autonomous driving limited by lacking

infrastructure and driving behavior

Scenario development (applicable to light vehicles)

Sources Lazard Roland Berger

2030+

11RB - Global automotive supplier study highlights 23012019pptx

New business models focused on short-duration use cases are carving out segments from traditional markets

Vehicle use cases by duration

Source Roland Berger

Car rentalCar sharing Ride sharing

Car ownership

Taxi

New business models

Days

gt Business trips

gt Car replacement during repairs

gt Vacations Road trips

gt Long distance moves

gt hellip

Hours

gt Shopping excursions (long dist)

gt Day trips

gt Back-up vehicle in emergencies

gt Short distance moves

gt hellip

Minutes

gt Shopping excursions (short dist)

gt Rides to places with limited parking

gt Trips home while intoxicated

gt hellip

Mobility

12RB - Global automotive supplier study highlights 23012019pptx

1 bn

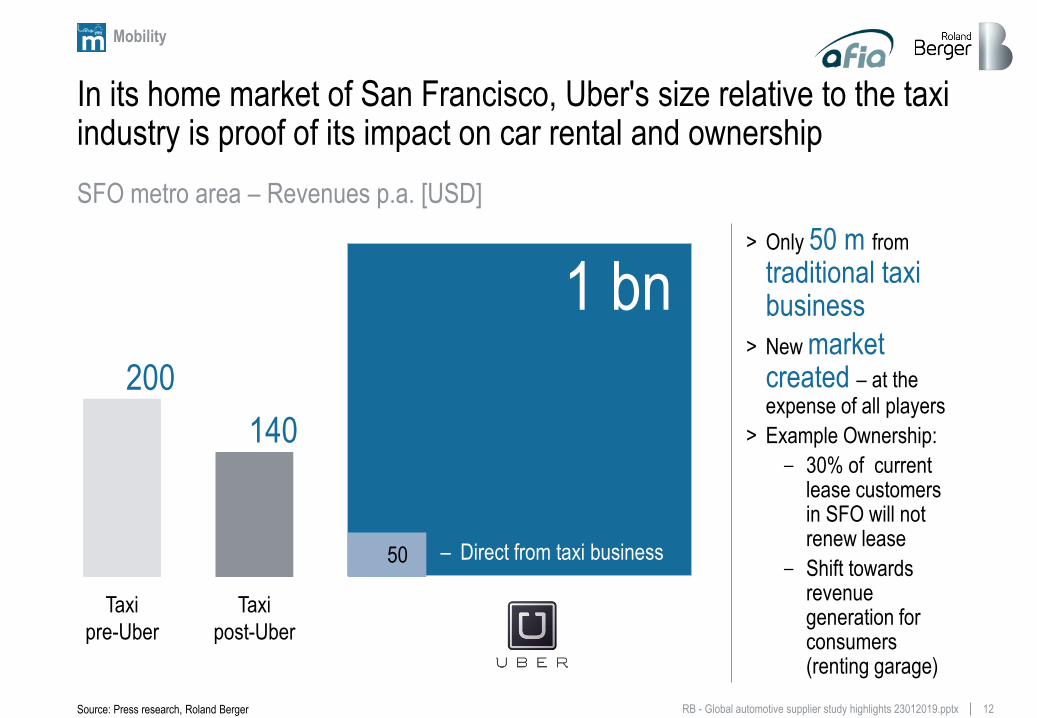

In its home market of San Francisco Ubers size relative to the taxi industry is proof of its impact on car rental and ownership

gt Only 50 m from

traditional taxi business

gt New market created ndash at the expense of all players

gt Example Ownership

- 30 of current lease customers in SFO will not renew lease

- Shift towards revenue generation for consumers (renting garage)

SFO metro area ndash Revenues pa [USD]

Source Press research Roland Berger

Taxi

post-Uber

Taxi

pre-Uber

ndash Direct from taxi business

200

140

50

Mobility

13RB - Global automotive supplier study highlights 23012019pptx

66

109

16

00 03

Singapore

27

00

00

01

27

China

07

88

0112

India

00

39

99

09

25

00

24

South Korea

01

0400 000004 03

08

01

Japan

03

04

Germany

06

00

0002

0408

00

France Italy

00

02

0002

0100

14 12 lt10

0800

09

UKNetherlands USA

0502

0000

Ride sharingCar Rental Taxi fleetCar sharing

1) PMV Purpose-built Mobility Vehicles

Mobility

The ratio of vehicles used for Mobility on demand is already at 10 of the car park in Singapore and China

Share of vehicles used for Mobility on demand on car parc [in 2015]

Source Euromonitor Desk Research Roland Berger

14RB - Global automotive supplier study highlights 23012019pptx

Vehicle sales for new mobility services are expected to exceed 10 of new car sales by 2025 in the US and the EU

9892 90

8 10

202520202015

2

OtherNew mobility1)

gt New mobility sales are expected to grow through 2025 due to

ndash Changes in car ownership patterns

ndash Growing urbanization

ndash Enhancements in technology amp mobility business models

gt The disruption potential in China is higher due to its relatively lower base of ownership levels today (1 car for 7 people vs 1 for 2 in EU and 1 for 125 in US)

gt Post 2025 the introduction of RoboCabs could drive a significantly larger share of sales to new mobility

9891

85

915

202520202015

2

United States EU-28

9791

65

9

35

2025

3

2015 2020

China

Share of vehicle sales for New Mobility1) [ passenger car sales]

1) Includes forecast for car sharing ride hailing ride sharing and Robocabs Does not include sales for conventional taxis or rental car fleets

Source Global RB Mobility Revenue and Profit Pool Model Lazard Roland Berger

Mobility

15RB - Global automotive supplier study highlights 23012019pptx

From 2020 to 2025 the addressable market for purpose-built vehicles for shared mobility is expected to grow by 21 a year

SourceSascha Birt (Illustration) Roland Berger

Mobility

16RB - Global automotive supplier study highlights 23012019pptx

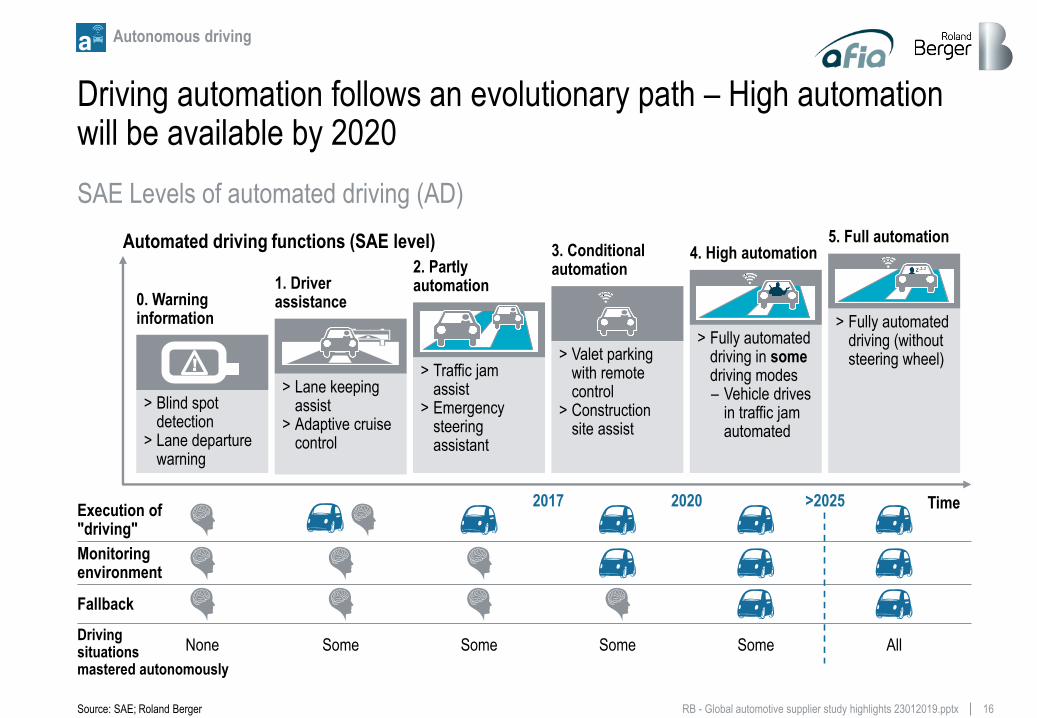

Driving automation follows an evolutionary path ndash High automation will be available by 2020

SAE Levels of automated driving (AD)

Source SAE Roland Berger

Automated driving functions (SAE level)

gt Blind spot detection

gt Lane departure warning

gt Lane keeping assist

gt Adaptive cruise control

gt Valet parking with remote control

gt Construction site assist

gt Fully automated driving in somedriving modesndash Vehicle drives

in traffic jam automated

gt Traffic jam assist

gt Emergency steering assistant

5 Full automation

gt Fully automated driving (without steering wheel)

Execution of driving

0 Warninginformation

1 Driver assistance

3 Conditionalautomation

4 High automation2 Partly automation

Timegt20252017 2020

Monitoring environment

Fallback

Drivingsituationsmastered autonomously

None Some Some Some Some All

zzz

Autonomous driving

17RB - Global automotive supplier study highlights 23012019pptx

All OEMs and players form the tech and mobility sectors are in a race to bring driverless mobility services on the road

Com

-pa

ny

Tes

t co

untr

y

Existing fleet (as of Q32017 20 vehicles) Planned test fleet by 2021 (as published as of of Q32017 20 vehicles) 600 Size of planned test fleet by 2021

320100gt100 6gt100 50 40 24 16

(has started a ride-hailing service in Arizona akin to Uber this year but with driverless cars ndashsigned contract with JLR to deliver 20000 Jaguar I-Pace and with FCA to deliver 50000 Chrysler Pacifica for that)

~70000

2000 (will deploy first commercial RoboCab fleet in San Francisco in 2019)

Autonomous driving

Existing amp planned L4L5-test-fleets (in units 2017 announcement until 2021)1)

Source Press clippings fka Roland Berger

1) Major companies not exhaustive

18RB - Global automotive supplier study highlights 23012019pptx

Future penetration of highly automated vehicles will depend on overcoming current hurdles and convergence on shared mobility

Autonomous driving ndash Penetration rate of highly automated cars (SAE Levels 45)1)

1) In passenger car sales includes RoboCabs and private autonomous cars

Source Global RB Mobility Revenue and Profit Pool Model Lazard Roland Berger

Autonomous driving

2020 20252015 2030

gt Shared mobility confined to early adopters in dense urban areas

gt Automated driving penetration primarily in flagship premium models

Low scenario (business as usual)

gt Sharing proliferates with high acceptance of carride sharing services

gt Autonomy achieves high penetration in shared fleets and privately owned premium and volume vehicle segments

High scenario (autonomous mobility)

32

26

8

Shared mobility

Autonomy

19RB - Global automotive supplier study highlights 23012019pptx

CAGR 2020-2030

79798686 89

101

60

111-35

+23

Business as usual Autonomous mobility

2015 20302020 2025 2015 20302020 2025

Autonomous driving

The impact of the transition on global vehicle production lies somewhere between steady growth and large declines after 2025

Global passenger car production [m vehicle] excl LCVs

Source Roland Berger Profit Pools model

20RB - Global automotive supplier study highlights 23012019pptx

Electrification in Japan and North America mainly achieved through HEV technology so far whereas China more focused on BEVPHEV

HEV Toyota only HEV excl Toyota BEV PHEV

101154

57

(652)

39

(455)

4

(41)

0

(6)

370

9

(32)

65

(239)

27

(98)

416

44

(185)

8

(32)

23

(95)

25

(104)

526

43

(228)

25

(132)

17

(89)

15

(76)

USA Europe2) China3) Japan3)South Korea RoW

284

464

621

1104

2475

Total

Electrification

Global light vehicles xEV1) sales volume by region 2016 [000 units]

HEV ndash Mild and full hybrid electric vehicles BEV ndash Battery electric vehicles PHEV ndash Plug-in hybrid electric vehicles xEV ndash Class of electrified vehicles from mild hybrids to battery electric1) Excludes fuel cell electric vehicles 2) Including Russia and Turkey 3) ChinaJapan sales data includes only domestically produced xEVs

Source MarkLines Press Research RB xEV forecast model Roland Berger

21RB - Global automotive supplier study highlights 23012019pptx

9790

80

11

60 7

2025

168

3

2020

172

2

2

2016

176

2

Lower battery costs and potentially rising oil prices may drive electrification penetration in the United States to ~ 20 by 2025

High xEV scenarioOil 65 USDbarrel | Battery cost low

Low xEV ScenarioOil 45 USDbarrel | Battery cost high

Mid xEV scenarioOil 55 USDbarrel | Battery cost medium

97 9388

7

2025

168

2

3

2020

172

23

2

2016

176

2 0

97 95 92

2

2025

168

33

2

2020

172

2 1

2016

176

2 0

ICE amp MHFHPHEVBEV

20812

USA ndash New sales1) propulsion share [2016-2025 m units of sales]

BEV ndash Battery electric vehicles PHEV ndash Plug-in hybrid electric vehicles FH ndash Full hybrid vehicles ICE amp MH ndash Internal combustion engine amp mild hybrid vehicles xEV ndash Class of electrified vehicles from mild hybrids to battery electric1) Passenger cars and light duty trucks

Source US EPA IHS RB xEV forecast model Roland Berger

Electrification

22RB - Global automotive supplier study highlights 23012019pptx

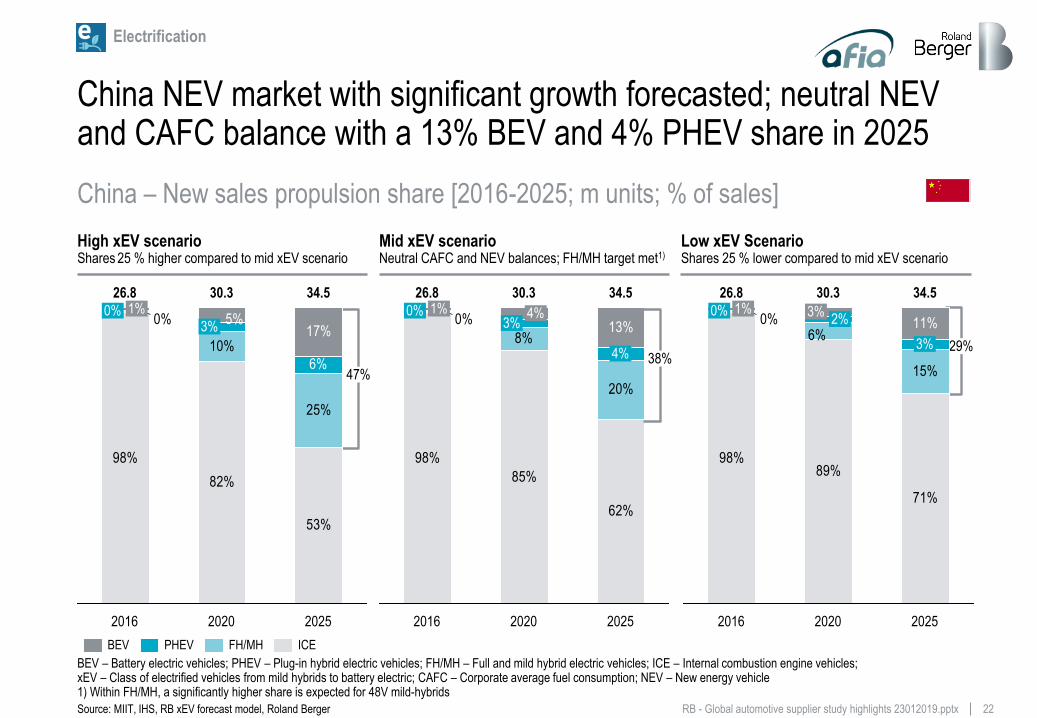

China NEV market with significant growth forecasted neutral NEVand CAFC balance with a 13 BEV and 4 PHEV share in 2025

High xEV scenario Shares 25 higher compared to mid xEV scenario

Low xEV ScenarioShares 25 lower compared to mid xEV scenario

Mid xEV scenarioNeutral CAFC and NEV balances FHMH target met1)

98

85

62

8

20

013

4

4

2025

03

303 345

2020

1

2016

268

47

2938

98

82

53

10

25

170

6

50

345303

2016

1268

2020

3

2025

9889

71

15

60 11

12

2020 2025

3

303

2016

268

3

345

0

ICEBEV FHMHPHEV

China ndash New sales propulsion share [2016-2025 m units of sales]

BEV ndash Battery electric vehicles PHEV ndash Plug-in hybrid electric vehicles FHMH ndash Full and mild hybrid electric vehicles ICE ndash Internal combustion engine vehicles xEV ndash Class of electrified vehicles from mild hybrids to battery electric CAFC ndash Corporate average fuel consumption NEV ndash New energy vehicle1) Within FHMH a significantly higher share is expected for 48V mild-hybrids

Source MIIT IHS RB xEV forecast model Roland Berger

Electrification

23RB - Global automotive supplier study highlights 23012019pptx

Electrification in Europe varies depending on CO2 emission targets ndash Share could reach between 20 a 32 for 2025

High xEV scenario 75 g CO2 km in 2025 (100 target)

Low xEV Scenario75 g CO2 km in 2025 (90 phase in)3)

Mid xEV scenario75 g CO2 km in 2025 (95 phase in)3)

51

30

18

4

6

44

47

33

9

12

5

61

18

20253)

173

2 2

2020

168

22

4

2016

162

2 2

51

3020

4

7

44

47

35

10

95

61

15

20253)

173

2 2

2

2020

168

22

4

2016

162

2

51

3021

4

7

44

47

39

11

75

61

11

20253)

173

2020

168

22

2 2 4

2016

162

2 2

PHEVBEV DieselMH DieselGasolineMH GasolineCNGLPGFH

32

2026

EU281) ndash New sales2) propulsion share [2016-2025 m units of sales]

BEV ndash Battery electric vehicles PHEV ndash Plug-in hybrid electric vehicles FH ndash Full hybrid vehicles CNGLPG ndash Compressed natural gasliquefied petroleum gas vehicles MD ndash Mild hybrid vehicles xEV ndash Class of electrified vehicles from mild hybrids to battery electric1) Incl UK 2) Passenger cars and light commercial vehicles 3) The top 9590 of the fleet need to meet the target 95 asymp 80 g CO2km 90 asymp 85 g CO2kmSource EEA IHS RB xEV forecast model Roland Berger

Electrification

24RB - Global automotive supplier study highlights 23012019pptx

Investments in electrification have fueled the sales of Electric vehicles since 2016 in Spain

Electrification in Spain at a glance

Source ACEA EAFO Roland Berger

BEV = Battery Electric Vehicle PHEV = Plug-in Hybrid Electric Vehicle ICE = Internal Combustion Engine1) ICE (Internal Combustion Engine) CNG (Compressed Natural Gas) LNG (Liquified Natural Gas) have been included

Charging points Car parc (2015) 58 M vehicles

Drivetrain type (new car sales)

800800400

400

91

2012 2014

909

2013

109

891

2015

142

1378

1520

2016

4525 4573

213

4312

2018

261

4312

+50 4573

2017

261

4312

04

020000

2012

0101

2013 20182015 2017

992

03

2014

0104

999

01

999

03

2016

994

998999

997

0101

00

Fast charge (gt22 kW)Normal charge (gt22 kW) Rest1)BEV PHEV

CAGR 12-15

+49

+153

Growth12-18

02

Diesel

401

Petrol

597

Alternative fuels

+03

+04

-07

Electrification

25RB - Global automotive supplier study highlights 23012019pptx

Subsidies given by the Goverment in Portugal have boosted theshare of EV in new car sales since 2017 ndash 2250 euro per EV

Electrification in Portugal at a glance

Source ACEA EAFO Roland Berger

Charging points Car parc (2015) 58 M vehicles

Drivetrain type (new car sales)

828279

+4

2018

1404

2016

1322 1340

2017

1401

1172

2015

17

1422

1322

1192

2014

17

1189

2013

1209

1154

2012

1128

7 17

1135 1171

01

03

2012 2015

040000

2014

998993

999

0102

998

01

2013 20182017

981

991

0504

965

16

1911

2016

08

Fast charge (gt22 kW)Normal charge (gt22 kW) PHEV Rest1)BEV

CAGR 12-15

+3

+51

Growth12-18

466

Diesel

518

15 Alternative fuels

Petrol

BEV = Battery Electric Vehicle PHEV = Plug-in Hybrid Electric Vehicle ICE = Internal Combustion Engine1) ) ICE (Internal Combustion Engine) CNG (Compressed Natural Gas) LNG (Liquified Natural Gas) have been included

+18

+16

-34

Electrification

26RB - Global automotive supplier study highlights 23012019pptx

There have been some bold claims made by OEMs promising to deliver more EV options ndash Far faster than IHS predictions

Major xEV product announcements

16

24

431

2020

42

10

315

16

74

42

2016

OtherxEVs

20

56

470

2024

ICEOnly

+49

BEVs

10 BEVs by 2022 Smart all-electric in NA starting 2018

26 xEVs by 2020

13 xEVs by 2021

30 new BEVs by 2025

All new Volvo platforms to be xEVs by 2019

All JLR products to have xEV option by 2020

1) Within North America and Europe Considers FH MH PHEV and BEV

Electrification

Number of xEV models offered in NA and Europe

Source Roland Berger

27RB - Global automotive supplier study highlights 23012019pptx

Obsoletecomponents

Heavily modified components

New components

Resultant challenges

gt Combustion engine (engine block valves camshaft sump oil filter etc)

gt Fuel systems

gt Injection systems

gt Clutch

gt Exhaust system

gt Auxiliary power units (oil pump turbocharger etc)

gt and so onhellip

gt Gearbox

gt Wheel suspension

gt Transmission

gt Air-conditioningheating

gt Cooling water system

gt Heat insulation

gt Noise reduction

gt Vehicle floor

gt Structural elements

gt and so onhellip

gt Electric motor andother drive components

gt Power electronics

gt Battery system (rechargeable battery battery management battery system)

gt Battery casing

gt Fuel cell system

gt and so onhellip

gt New components are being developed and produced by incumbent and new suppliers

Competition is forcing OEMs and suppliers to adopt new positions

SupplierSupplier Supplier

OEMOEM OEM

Influence of electrification on vehicle components (excerpt)

Electrification is changing the composition of the vehicle giving rise to new components relating to technology increasing wiring needs

Source Roland Berger

Electrification

28RB - Global automotive supplier study highlights 23012019pptx

AutomotiveEnd game zone

Automotive suppliers will need to prepare for five distinct changes that will emerge on the road to the end game

Emergence of software as a key differentiating factorgt Digital features determine value to the end-customergt Digitization offers new monetization options3

Vanishing growthgt Stagnation in mature marketsgt Increased usage of shared mobility solutions

1Accelerated change of technologies in focusgt Increasing proliferation of electrified powertrainsgt Strong industry push for ADAS and connectivity solutions2

OEMs encounter increasing investment needs and margin pressuregt New technologies require substantial investmentsgt OEMs challenged by new competitors

4Valuation levels of commoditized suppliers might come under pressuregt Outperformance of OEM valuation multiples might come to an endgt Outlook of commoditized supplier sub-sectors might be seen more critical

by equity investors as well as creditors

5

Emerging changes impacting automotive suppliers

Source Lazard Roland Berger

29RB - Global automotive supplier study highlights 23012019pptx

2 Technology shifts

Almost all vehicle domains will see a shift in growth focus over the next years ndash Disruption impact particularly high in powertrain

Impact of technology shifts by domain

Source Lazard Roland Berger

Disruption impact on current business

Supplier domain Low High

Interior

Exterior

Chassis

Powertrain

Powertrain gt E-motors and power electronics

gt Battery systems

gt Simple 1-2 step reduction gears

Interior gt New HMI display technologies

gt Extended Infotainment solutions

gt Increased interior insulation (NVH)

gt Integration of electronics and surfaces

Next generation vehicle concept

Substantial new requirements for the supply base

Chassis gt Advanced driver assistance systems and autonomous features

gt Adaptive suspensions

gt Active steering and braking systems

gt Shifting material focus and growing importance of multi-material applications

gt Growth of non-structural composites

Exterior

30RB - Global automotive supplier study highlights 23012019pptx

Electric powertrain components to experience high growth rates at the expense of many traditional ICE components

Implications for suppliers

gt ICE hardware commoditization

gt Battery systems and electronics provide differentiation opportunities

gt Limited potential in e-motors in part due to lower complexity vs ICE

Background

gt Increasing cost of ICEexhaust treatment

gt Mild and full hybrids aid in emissions improvement and enable ICEs with downgraded requirements

gt BEV penetration rates increase driven by regulation incentives and consumer demand

Technology trends ndash Winners

gt Future powertrain architectures are electrified resulting in several fast growing domains

ndash E-motors

ndash Inverterspower electronics

ndash Battery

ndash Battery cooling

ndash 1-2 step reduction gears

ndash Charging components

Technology trends ndash Losers

gt Consequently traditional ICE components and systems to experience below average growth rates

ndash Engine camshafts crankshafts valves lubricants

ndash Exhaust oil filters alternators ignition

ndash Transmission clutch gearbox propeller shaft

Technology shifts ndash Powertrain

Source Lazard Roland Berger

2 Technology shifts

31RB - Global automotive supplier study highlights 23012019pptx

The ADAS and AD component market will strongly grow providing an increasing revenue pool mainly for software focused suppliers

Implications for suppliers

gt Hardware standardization commoditization of traditional chassis components and systems

gt Intelligent systems integrated with ADAS are expected to offer growth potential within respective domains (eg steering suspension vision systems passenger safety systems)

Background

gt ADAS offers several benefits to society and industry including accident mitigation congestion reduction increased driving comfort and fuel efficiency gains

gt Advanced vehicle control and sensor systems are the main benefactors of the shift to greater advanced driver assistance systemsndash Advanced driver assistance systems and

autonomous features ndash Adaptive suspensionsndash Active steering + braking actuatorsndash E-Axles (as part of electrified powertrain)ndash Vision sensors (LiDAR cameras)

Technology trends ndash Winners

Technology trends ndash Losers

gt Meanwhile traditional vehicle control systems are at risk for reduced market sharendash Hydraulic steering systemsndash Traditional axlesndash Conventional suspensions

Technology shifts ndash Chassis

Source Lazard Roland Berger

2 Technology shifts

32RB - Global automotive supplier study highlights 23012019pptx

Emissions regulations push OEMs for increased lightweighting of body structures while ADAS and connectivity create new use cases

Implications for suppliers

gt Shifting materials competencies for non-structural components suppliers

gt New use cases for intelligent exterior systems may offer differentiation potential particularly when paired with ADAS solutions

Background

gt Shifting material focus and growing importance of multi-material applications

gt New technology integration potential for enhanced safety

gt New design possibilities due to missing ICE powertrain

gt Advanced material components and advanced safety features offer potential in exterior componentsndash Non-structural compositesndash Increased usage of plasticsndash Side and rear view cameras and screensndash Driving mode indication (autonomous vs human

driver)ndash Lock systems using cell phones

Technology trends ndash Winners

Technology trends ndash Losers

gt Traditional materials and exterior components most at risk for lost share includendash Cast partsndash Non-structural steel partsndash Traditional side and rear view mirrors

Technology shifts ndash Exterior

Source Lazard Roland Berger

2 Technology shifts

33RB - Global automotive supplier study highlights 23012019pptx

Autonomous driving will drastically change interior designs and provide innovation and growth potentials

Background

gt Growing importance of non-driving-related activities such as infotainment completing tasks while driving automated eating and drinking

gt Interior provides huge potential for innovation and continued growth

Technology trends ndash Winners

gt New possibilities to design the interior of a vehicle by electric powertrain connectivity and automated drivingndash New HMIs1) (Augmented reality head up displays

gesture recognition haptic feedback) and integration of electronics and surfaces (OLED2)

panels curved screens) ndash Extended infotainment solutionsndash New design possibilitiesrequirements eg luxury

lounge seating or increased interior insulation (NVH3))

Key success factors

gt Successful translation of customer needs in product innovation

gt Product differentiationgt Integration of EE to ensure

value creation

Technology trends ndash Losers

gt Traditional interior components that might face lower demandndash Analog instrument clustersndash Buttons and switchesndash Conventional valves pumps and compressors

Technology shifts ndash Interior

1) Human-machine interfaces 2) Organic light emitting diode 3) Noise vibration and harshness

Source Lazard Roland Berger

2 Technology shifts

34RB - Global automotive supplier study highlights 23012019pptx

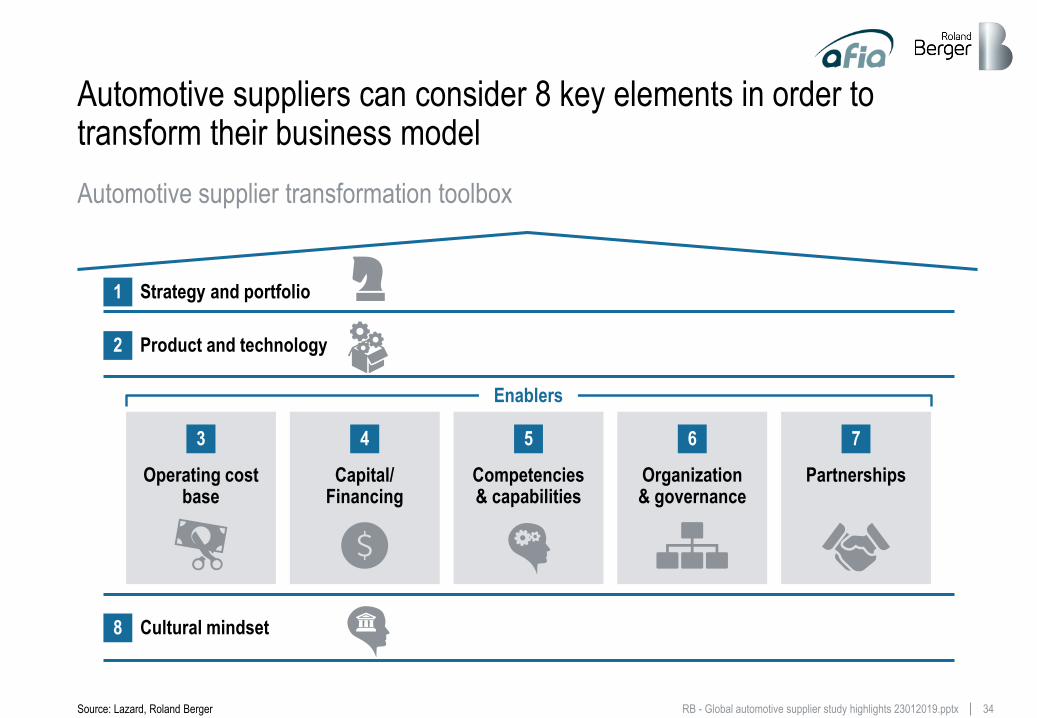

Automotive suppliers can consider 8 key elements in order to transform their business model

1 Strategy and portfolio

2 Product and technology

8 Cultural mindset

Operating cost base

Capital Financing

Competencies amp capabilities

Organization amp governance

Partnerships

3 4 5 6 7

Enablers

Automotive supplier transformation toolbox

Source Lazard Roland Berger

35RB - Global automotive supplier study highlights 23012019pptx

Active consolidation and harvesting are often financially viable strategies ndash Future sources for growth have to be identified

1 Strategic responses to declining segments 2 New sources for growth

ConsolidateMaintain

leadership

Harvest

Ramp-down business model

ExitDivest

Competitive Intensity

LowHigh

Co

mp

etit

ive

Po

siti

on

Wea

kS

tro

ng

gt Before the industry disruption reaches a tipping point suppliers should consider end-game strategies for their declining business areas

gt Suppliers can expand into new offerings and end markets to provide outlets for growth

gt Diversification into other industries leveraging current core competencies as an alternative

Core

Adjacent

Step-out

Incremental

innovation

New go-

to-market

Diversify into other

industries

New value-

chain position

New applications

Adjoining

value-chain

position

New technology

segment

New geographies

Strategic decision matrix and portfolio growth options

Source Lazard Roland Berger

Strategy amp Portfolio1

36RB - Global automotive supplier study highlights 23012019pptx

The cultural mindset has to be rethought along with the transformation of the business model

Transformation

Future

Past

Focus on methods processes and tools

Incremental processes

Tactics and pressure as drivers

Change of working style

Implementation of defined changes

Status Quo

Addressing existing mindsets and beliefs

Strategy-driven

Many connected initiatives

Reconfiguration and reinvention

Change of framework

Result of many changes

Solution-drivenProblem orientation

Limited initiatives

Project orientation Influence on the whole organization

Flat hierarchyagile decisions

Top-down decisions

Motivation as driver

IllustrativeCultural mindset transformation

Source Lazard Roland Berger

Cultural mindset8

37RB - Global automotive supplier study highlights 23012019pptx

Suppliers need to rethink their business model in order to be successful in the future

1Suppliers need to rethink their strategy and product portfolio in order to capture growth opportunities or consolidate the market around their existing portfolio

3Suppliers need to implement a new and lower operating cost base and at the same time ensure sufficient financing for the upcoming transition

4Suppliers need to build up new competencies and capabilities and adapt their organizational structure amp governance as well as cultural mindset to compete in the new technology areas

5Suppliers need to build up new partnerships and leverage this ecosystem to find new ways to innovate

New

bu

sin

ess

mo

del

2Suppliers need to define a long term technology roadmap as well as their strategic positioning in the value chain regarding their product and service offering

Summary Key actions for automotive suppliers

Source Lazard Roland Berger

38RB - Global automotive supplier study highlights 23012019pptx

But The one thing we have learned is that even the best predictions cannot say what will really happen with disruptive technology

I think there is a world market for maybe five computersTHOMAS WATSON PRESIDENT OF IBM 1943

Nuclear-powered vacuum cleaners will probably be a reality within ten yearsALEX LEWYT PRESIDENT OF LEWYT VACUUM COMPANY 1955

Two years from now spam will be solvedBILL GATES FOUNDER OF MICROSOFT 2004

39RB - Global automotive supplier study highlights 23012019pptx

Rodrigo Custodio

DirectorRoland Berger

RodrigoCustodiorolandbergercom

Stay tuned with our Automotive publications

httpswwwrolandbergercomenDossiersMADEhtml

Your discussion partner today

2RB - Global automotive supplier study highlights 23012019pptx

We are one of the largest strategic consultancies with a strong expertise in the automotive area

Our profile Our competence matrix

Our automotive practice Our values

Created in 1967in Germany by Prof Dr Roland Berger

50 offices in36 countries with2400 employees

Over 240 Partners

~1000 international clients

1993Brussels | Kiev |

Prague |

1994Moscow

1995Beijing

1997Budapest | Zuumlrich

2002Amsterdam

1998Detroit | Shanghai

2000Warsaw

2003Zagreb

2006Manama

2007Chicago | Hong Kong |Beirut

2008Casablanca | Istanbul | Taipei

2009Doha

2010Stockholm | Goteborg |

Singapore

2011Dubai | Kuala Lumpur |

Lagos | Jakarta

2012Seoul | New Delhi |

Guangzhou |Montreal | Boston

2013Mumbai

2014Bangkok | Pune

1967

1969

1976

1982

1986

Munich

Milan

Satildeo Paulo

1987Stuttgart

Duumlsseldorf

Madrid

1989Frankfurt | Vienna

1990Berlin | Hamburg |Lisbon | London |Paris

1991Tokyo

1992Bucharest

Source Roland Berger

Overview of Roland Berger

ExcellenceWe achieve excellent results and develop global best practices to ensure measurable and sustainable success

EmpathyWe are insightful and responsible advisors and

we contribute to the greater good

EntrepreneurshipWe follow an entrepreneurial approach and provide creative and pragmatic solutions

3RB - Global automotive supplier study highlights 23012019pptx

The global automotive industry has presented a growth of 3 in recent years

World

North America Europe3) China4)

JapanKorea

CAGR2) 24 CAGR2) 29 CAGR2) 86

CAGR2) 31 CAGR2)-10

2018

170

2016

178

20172015

-2

174

2013

170

2012 2014

175154 162

2012 20152014

201 210

2013

222

2016

193 215195

2017

-1

2018

220 273

2016

-3

280274

2017

240

2014

230213

20152013

186

2012 2018

South America

CAGR2) -52

2018

35

2013

332731

2014

45

201720162015

+5

3843

2012

132

20182016

0

129

2015

133

2017

133137

20142013

135

2012

139

0

2017

947

20182013

874815

2012

888

2015

847

2016

931

2014

951

Global light vehicle production volume1) by region 2012-2017 [m units]

Source IHS Roland Berger

1) Incl light commercial vehicles 2) CAGR 2012-2017 3) Excluding CIS and Turkey 4) Greater China

4RB - Global automotive supplier study highlights 23012019pptxSource Company information analyst forecasts Lazard Roland Berger

The stability of past industry years have yielded consecutive years of good supplier performance have

Revenue growth EBIT1) margin []

33555413

29

142138131

124118

113

100

20122010 2011 2013 2014 2017e2015

~147

2016

72707371

686871

2015 2017e

~73

2012 20132010 2011 2014 2016

Key supplier performance indicators 2010-2017e (n=~650 suppliers)

1) EBIT after restructuring items

Indexed [2010=100]

YoY []

5RB - Global automotive supplier study highlights 23012019pptx

Valuation of suppliers have increased while of OEMs have remained under pressure

Sources Fact set Roland Berger

PE NTM1)

1x

3x

5x

7x

9x

11x

13x

15x

17x

19x

21x

23x

25x

27x

29x

nov-

07

nov-

08

nov-

09

nov-

10

nov-

11

nov-

12

nov-

13

nov-

14

nov-

15

oct-

16

nov-

17

gt In recent years the valuation figures for suppliers have been significantly higher than those for OEMs

gt The valuation gap has hit an all-time high ndash The valuations of suppliers are almost twice as high as those of OEMs

gt Risks arising from disruptive trends appear to have been priced in to OEM valuations ndashThat does not seem to be the case for supplier valuations

Selected automotive OEMs3) Selected automotive suppliers4)

Under the influence of the economic crisis

10-y-avg = 112x2)

80x

10-y-avg = 90x2)

133x

Trend in the valuations of OEMs and suppliers

1) NTM = next twelve months 2) Excluding the distortions triggered by the economic crisis (figures for Jan-Dec 2009) 3) BMW Daimler Ford General Motors Honda Toyota and Volkswagen 4) American Axle Autoliv BorgWarner Brembo Continental Dana Delphi Faurecia Hella Johnson Controls Magna Norma and Valeo

6RB - Global automotive supplier study highlights 23012019pptx

Tim Cook (CEO Apple Inc)

Dieter Zetsche (CEO Daimler AG)

The automotive industry

has reached a

dramatic turning

point with huge changes

Right now we are exper-

iencing the second

invention of the

automobile

Sources Press Roland Berger

The industry is being looked by its own executives and by new interested parties with different eyeshellip

7RB - Global automotive supplier study highlights 23012019pptx

hellipand therefore is already going through significant changes

Prices of used

diesel vehicles1) []

Time in stock with dealers for diesel

vehicles 2016-2018 [days]

Sources Schwacke DAT Roland Berger

Diesel trends

2016 2017 2018

110

105

100

95

90

85

80

75

0

+25

Diesel

Gasoline

1

102

89

12

102

85

11

110

85

10

85

86

3

87

90

2

85

93

1

88

94

100

81

9

96

77

8

101

80

7

94

78

6

95

79

5

99

85

4

94

82

3

98

89

2

99

91

1

97

92

12

96

88

11

95

86

10

94

87

9

92

86

8

88

83

7

81

80

6

80

79

5

83

82

4

56

55

54

53

52

51

50

0

20182017201620152014

Gasoline

Diesel

Avg relative residual price for 3-year-old vehicles with mileage of 60000 km

70

65

60

55

50

0115 0715 0116 0716 0117 0717 0118

0

45

30

35

40 FR

UK

DE

IT

ES

-12

-13

0

-15

-10

Diesel engines as a proportion of

new registrations 2015-12018 []

8RB - Global automotive supplier study highlights 23012019pptx

The speed is cacthing OEMs still unprepared eg difficult adaptation to the new WLTP regulation by OEMs impacted the value chain

Impact of WLTP on the automotive market

There have been several OEMs that have delayed projects that were expected for 2018 (especially during the second half of the year) due to their difficulties to cope with the WLTP1)

regulation

Tier 1 supplier (Spain)

The situation in the market is not stable and OEMs prefer to be conservative I think that most of the reasons are conjunctural We are living an uncertainty political situation and that is why the market is waiting but from my point of view automotive market will change very fast and the growth is going to be

important

Tier 1 supplier (Spain)

The automotive market has been very instable for players across the value chain with sales and profitability lower than expected (proven by the profit warnings issued by many companies in the industry) ndashAll the players are suffering due to the declines in volumes produced and the delays in vehicle launches We dont expect this situation to last any longer

Tier 1 supplier (Spain)

Source Expert Interviews Roland Berger

The OEMs had some projects planned from several years ago (eg some new models with diesel engines or facelifts of their traditional models) that could not be launched any more They are updating these projects or questioning if some of them still make sense Most of those projects will be launched in their new electric versions

from 2020 onwards

Mold manufacturer (Portugal)

9RB - Global automotive supplier study highlights 23012019pptx

There are mainly for disruptive trends that are transforming the automotive industry ndash MADE by Roland Berger

Automotive disruption

Technology andregulatory progress

High customer value and improved safety

Consequences for current cars small vehicles LCVs

After-salesserviceimpact

2 Autonomous

Connectivity

AI

Evolution of digital technologies and culture

Full integration of the connected vehicle in

customers everyday life

3 Digitization

Strategy

How to position

Transformation

How to transform

Alternative

fuels

Automated

driving

Non-traditional

entrants

ICE

advancement

Mobility

solutions

Startup

OEMs

Connectivity

Low-cost

brands

New

retail

Geographic

shift

Source Roland Berger

Changing customer behavior (sharing vs owning)

Urbanization changing traditional mobility and logistics

concepts

New mobility mix and new business modelsplayers

1 New mobility

Compliance with future emissions regulations

Electrification landscape including infrastructure

Profitability challenges

China as a benchmark

4 Electrified

Powertrain

electrification

Emissions

regulations

Light-

weighting

Fuel

cells

10RB - Global automotive supplier study highlights 23012019pptx

The automotive end game appears inevitable yet the transition period is marked by considerable uncertainty

TimeToday

Degree of change

2020 2025 2030

North Americagt Deep penetration of ride hailing in major metropolitan

areasgt Technology leadership in highly automated drivinggt Strong regulatory support

Chinagt Strong push and high maturity for electrificationgt Deep penetration of ride hailing in major

metropolitan areasgt Strong players pushing for

autonomous drivinggt Fast regulatory

decisions

Europegt High population density in cities ndash

ideal for robocabsgt Stringent emissions regulation

driving electrificationgt Slow regulatory processes

Emerging marketsgt Less stringent emissions regulations delaying

the spread of electric vehiclesgt Growing adoption of ride hailing in major citiesgt Autonomous driving limited by lacking

infrastructure and driving behavior

Scenario development (applicable to light vehicles)

Sources Lazard Roland Berger

2030+

11RB - Global automotive supplier study highlights 23012019pptx

New business models focused on short-duration use cases are carving out segments from traditional markets

Vehicle use cases by duration

Source Roland Berger

Car rentalCar sharing Ride sharing

Car ownership

Taxi

New business models

Days

gt Business trips

gt Car replacement during repairs

gt Vacations Road trips

gt Long distance moves

gt hellip

Hours

gt Shopping excursions (long dist)

gt Day trips

gt Back-up vehicle in emergencies

gt Short distance moves

gt hellip

Minutes

gt Shopping excursions (short dist)

gt Rides to places with limited parking

gt Trips home while intoxicated

gt hellip

Mobility

12RB - Global automotive supplier study highlights 23012019pptx

1 bn

In its home market of San Francisco Ubers size relative to the taxi industry is proof of its impact on car rental and ownership

gt Only 50 m from

traditional taxi business

gt New market created ndash at the expense of all players

gt Example Ownership

- 30 of current lease customers in SFO will not renew lease

- Shift towards revenue generation for consumers (renting garage)

SFO metro area ndash Revenues pa [USD]

Source Press research Roland Berger

Taxi

post-Uber

Taxi

pre-Uber

ndash Direct from taxi business

200

140

50

Mobility

13RB - Global automotive supplier study highlights 23012019pptx

66

109

16

00 03

Singapore

27

00

00

01

27

China

07

88

0112

India

00

39

99

09

25

00

24

South Korea

01

0400 000004 03

08

01

Japan

03

04

Germany

06

00

0002

0408

00

France Italy

00

02

0002

0100

14 12 lt10

0800

09

UKNetherlands USA

0502

0000

Ride sharingCar Rental Taxi fleetCar sharing

1) PMV Purpose-built Mobility Vehicles

Mobility

The ratio of vehicles used for Mobility on demand is already at 10 of the car park in Singapore and China

Share of vehicles used for Mobility on demand on car parc [in 2015]

Source Euromonitor Desk Research Roland Berger

14RB - Global automotive supplier study highlights 23012019pptx

Vehicle sales for new mobility services are expected to exceed 10 of new car sales by 2025 in the US and the EU

9892 90

8 10

202520202015

2

OtherNew mobility1)

gt New mobility sales are expected to grow through 2025 due to

ndash Changes in car ownership patterns

ndash Growing urbanization

ndash Enhancements in technology amp mobility business models

gt The disruption potential in China is higher due to its relatively lower base of ownership levels today (1 car for 7 people vs 1 for 2 in EU and 1 for 125 in US)

gt Post 2025 the introduction of RoboCabs could drive a significantly larger share of sales to new mobility

9891

85

915

202520202015

2

United States EU-28

9791

65

9

35

2025

3

2015 2020

China

Share of vehicle sales for New Mobility1) [ passenger car sales]

1) Includes forecast for car sharing ride hailing ride sharing and Robocabs Does not include sales for conventional taxis or rental car fleets

Source Global RB Mobility Revenue and Profit Pool Model Lazard Roland Berger

Mobility

15RB - Global automotive supplier study highlights 23012019pptx

From 2020 to 2025 the addressable market for purpose-built vehicles for shared mobility is expected to grow by 21 a year

SourceSascha Birt (Illustration) Roland Berger

Mobility

16RB - Global automotive supplier study highlights 23012019pptx

Driving automation follows an evolutionary path ndash High automation will be available by 2020

SAE Levels of automated driving (AD)

Source SAE Roland Berger

Automated driving functions (SAE level)

gt Blind spot detection

gt Lane departure warning

gt Lane keeping assist

gt Adaptive cruise control

gt Valet parking with remote control

gt Construction site assist

gt Fully automated driving in somedriving modesndash Vehicle drives

in traffic jam automated

gt Traffic jam assist

gt Emergency steering assistant

5 Full automation

gt Fully automated driving (without steering wheel)

Execution of driving

0 Warninginformation

1 Driver assistance

3 Conditionalautomation

4 High automation2 Partly automation

Timegt20252017 2020

Monitoring environment

Fallback

Drivingsituationsmastered autonomously

None Some Some Some Some All

zzz

Autonomous driving

17RB - Global automotive supplier study highlights 23012019pptx

All OEMs and players form the tech and mobility sectors are in a race to bring driverless mobility services on the road

Com

-pa

ny

Tes

t co

untr

y

Existing fleet (as of Q32017 20 vehicles) Planned test fleet by 2021 (as published as of of Q32017 20 vehicles) 600 Size of planned test fleet by 2021

320100gt100 6gt100 50 40 24 16

(has started a ride-hailing service in Arizona akin to Uber this year but with driverless cars ndashsigned contract with JLR to deliver 20000 Jaguar I-Pace and with FCA to deliver 50000 Chrysler Pacifica for that)

~70000

2000 (will deploy first commercial RoboCab fleet in San Francisco in 2019)

Autonomous driving

Existing amp planned L4L5-test-fleets (in units 2017 announcement until 2021)1)

Source Press clippings fka Roland Berger

1) Major companies not exhaustive

18RB - Global automotive supplier study highlights 23012019pptx

Future penetration of highly automated vehicles will depend on overcoming current hurdles and convergence on shared mobility

Autonomous driving ndash Penetration rate of highly automated cars (SAE Levels 45)1)

1) In passenger car sales includes RoboCabs and private autonomous cars

Source Global RB Mobility Revenue and Profit Pool Model Lazard Roland Berger

Autonomous driving

2020 20252015 2030

gt Shared mobility confined to early adopters in dense urban areas

gt Automated driving penetration primarily in flagship premium models

Low scenario (business as usual)

gt Sharing proliferates with high acceptance of carride sharing services

gt Autonomy achieves high penetration in shared fleets and privately owned premium and volume vehicle segments

High scenario (autonomous mobility)

32

26

8

Shared mobility

Autonomy

19RB - Global automotive supplier study highlights 23012019pptx

CAGR 2020-2030

79798686 89

101

60

111-35

+23

Business as usual Autonomous mobility

2015 20302020 2025 2015 20302020 2025

Autonomous driving

The impact of the transition on global vehicle production lies somewhere between steady growth and large declines after 2025

Global passenger car production [m vehicle] excl LCVs

Source Roland Berger Profit Pools model

20RB - Global automotive supplier study highlights 23012019pptx

Electrification in Japan and North America mainly achieved through HEV technology so far whereas China more focused on BEVPHEV

HEV Toyota only HEV excl Toyota BEV PHEV

101154

57

(652)

39

(455)

4

(41)

0

(6)

370

9

(32)

65

(239)

27

(98)

416

44

(185)

8

(32)

23

(95)

25

(104)

526

43

(228)

25

(132)

17

(89)

15

(76)

USA Europe2) China3) Japan3)South Korea RoW

284

464

621

1104

2475

Total

Electrification

Global light vehicles xEV1) sales volume by region 2016 [000 units]

HEV ndash Mild and full hybrid electric vehicles BEV ndash Battery electric vehicles PHEV ndash Plug-in hybrid electric vehicles xEV ndash Class of electrified vehicles from mild hybrids to battery electric1) Excludes fuel cell electric vehicles 2) Including Russia and Turkey 3) ChinaJapan sales data includes only domestically produced xEVs

Source MarkLines Press Research RB xEV forecast model Roland Berger

21RB - Global automotive supplier study highlights 23012019pptx

9790

80

11

60 7

2025

168

3

2020

172

2

2

2016

176

2

Lower battery costs and potentially rising oil prices may drive electrification penetration in the United States to ~ 20 by 2025

High xEV scenarioOil 65 USDbarrel | Battery cost low

Low xEV ScenarioOil 45 USDbarrel | Battery cost high

Mid xEV scenarioOil 55 USDbarrel | Battery cost medium

97 9388

7

2025

168

2

3

2020

172

23

2

2016

176

2 0

97 95 92

2

2025

168

33

2

2020

172

2 1

2016

176

2 0

ICE amp MHFHPHEVBEV

20812

USA ndash New sales1) propulsion share [2016-2025 m units of sales]

BEV ndash Battery electric vehicles PHEV ndash Plug-in hybrid electric vehicles FH ndash Full hybrid vehicles ICE amp MH ndash Internal combustion engine amp mild hybrid vehicles xEV ndash Class of electrified vehicles from mild hybrids to battery electric1) Passenger cars and light duty trucks

Source US EPA IHS RB xEV forecast model Roland Berger

Electrification

22RB - Global automotive supplier study highlights 23012019pptx

China NEV market with significant growth forecasted neutral NEVand CAFC balance with a 13 BEV and 4 PHEV share in 2025

High xEV scenario Shares 25 higher compared to mid xEV scenario

Low xEV ScenarioShares 25 lower compared to mid xEV scenario

Mid xEV scenarioNeutral CAFC and NEV balances FHMH target met1)

98

85

62

8

20

013

4

4

2025

03

303 345

2020

1

2016

268

47

2938

98

82

53

10

25

170

6

50

345303

2016

1268

2020

3

2025

9889

71

15

60 11

12

2020 2025

3

303

2016

268

3

345

0

ICEBEV FHMHPHEV

China ndash New sales propulsion share [2016-2025 m units of sales]

BEV ndash Battery electric vehicles PHEV ndash Plug-in hybrid electric vehicles FHMH ndash Full and mild hybrid electric vehicles ICE ndash Internal combustion engine vehicles xEV ndash Class of electrified vehicles from mild hybrids to battery electric CAFC ndash Corporate average fuel consumption NEV ndash New energy vehicle1) Within FHMH a significantly higher share is expected for 48V mild-hybrids

Source MIIT IHS RB xEV forecast model Roland Berger

Electrification

23RB - Global automotive supplier study highlights 23012019pptx

Electrification in Europe varies depending on CO2 emission targets ndash Share could reach between 20 a 32 for 2025

High xEV scenario 75 g CO2 km in 2025 (100 target)

Low xEV Scenario75 g CO2 km in 2025 (90 phase in)3)

Mid xEV scenario75 g CO2 km in 2025 (95 phase in)3)

51

30

18

4

6

44

47

33

9

12

5

61

18

20253)

173

2 2

2020

168

22

4

2016

162

2 2

51

3020

4

7

44

47

35

10

95

61

15

20253)

173

2 2

2

2020

168

22

4

2016

162

2

51

3021

4

7

44

47

39

11

75

61

11

20253)

173

2020

168

22

2 2 4

2016

162

2 2

PHEVBEV DieselMH DieselGasolineMH GasolineCNGLPGFH

32

2026

EU281) ndash New sales2) propulsion share [2016-2025 m units of sales]

BEV ndash Battery electric vehicles PHEV ndash Plug-in hybrid electric vehicles FH ndash Full hybrid vehicles CNGLPG ndash Compressed natural gasliquefied petroleum gas vehicles MD ndash Mild hybrid vehicles xEV ndash Class of electrified vehicles from mild hybrids to battery electric1) Incl UK 2) Passenger cars and light commercial vehicles 3) The top 9590 of the fleet need to meet the target 95 asymp 80 g CO2km 90 asymp 85 g CO2kmSource EEA IHS RB xEV forecast model Roland Berger

Electrification

24RB - Global automotive supplier study highlights 23012019pptx

Investments in electrification have fueled the sales of Electric vehicles since 2016 in Spain

Electrification in Spain at a glance

Source ACEA EAFO Roland Berger

BEV = Battery Electric Vehicle PHEV = Plug-in Hybrid Electric Vehicle ICE = Internal Combustion Engine1) ICE (Internal Combustion Engine) CNG (Compressed Natural Gas) LNG (Liquified Natural Gas) have been included

Charging points Car parc (2015) 58 M vehicles

Drivetrain type (new car sales)

800800400

400

91

2012 2014

909

2013

109

891

2015

142

1378

1520

2016

4525 4573

213

4312

2018

261

4312

+50 4573

2017

261

4312

04

020000

2012

0101

2013 20182015 2017

992

03

2014

0104

999

01

999

03

2016

994

998999

997

0101

00

Fast charge (gt22 kW)Normal charge (gt22 kW) Rest1)BEV PHEV

CAGR 12-15

+49

+153

Growth12-18

02

Diesel

401

Petrol

597

Alternative fuels

+03

+04

-07

Electrification

25RB - Global automotive supplier study highlights 23012019pptx

Subsidies given by the Goverment in Portugal have boosted theshare of EV in new car sales since 2017 ndash 2250 euro per EV

Electrification in Portugal at a glance

Source ACEA EAFO Roland Berger

Charging points Car parc (2015) 58 M vehicles

Drivetrain type (new car sales)

828279

+4

2018

1404

2016

1322 1340

2017

1401

1172

2015

17

1422

1322

1192

2014

17

1189

2013

1209

1154

2012

1128

7 17

1135 1171

01

03

2012 2015

040000

2014

998993

999

0102

998

01

2013 20182017

981

991

0504

965

16

1911

2016

08

Fast charge (gt22 kW)Normal charge (gt22 kW) PHEV Rest1)BEV

CAGR 12-15

+3

+51

Growth12-18

466

Diesel

518

15 Alternative fuels

Petrol

BEV = Battery Electric Vehicle PHEV = Plug-in Hybrid Electric Vehicle ICE = Internal Combustion Engine1) ) ICE (Internal Combustion Engine) CNG (Compressed Natural Gas) LNG (Liquified Natural Gas) have been included

+18

+16

-34

Electrification

26RB - Global automotive supplier study highlights 23012019pptx

There have been some bold claims made by OEMs promising to deliver more EV options ndash Far faster than IHS predictions

Major xEV product announcements

16

24

431

2020

42

10

315

16

74

42

2016

OtherxEVs

20

56

470

2024

ICEOnly

+49

BEVs

10 BEVs by 2022 Smart all-electric in NA starting 2018

26 xEVs by 2020

13 xEVs by 2021

30 new BEVs by 2025

All new Volvo platforms to be xEVs by 2019

All JLR products to have xEV option by 2020

1) Within North America and Europe Considers FH MH PHEV and BEV

Electrification

Number of xEV models offered in NA and Europe

Source Roland Berger

27RB - Global automotive supplier study highlights 23012019pptx

Obsoletecomponents

Heavily modified components

New components

Resultant challenges

gt Combustion engine (engine block valves camshaft sump oil filter etc)

gt Fuel systems

gt Injection systems

gt Clutch

gt Exhaust system

gt Auxiliary power units (oil pump turbocharger etc)

gt and so onhellip

gt Gearbox

gt Wheel suspension

gt Transmission

gt Air-conditioningheating

gt Cooling water system

gt Heat insulation

gt Noise reduction

gt Vehicle floor

gt Structural elements

gt and so onhellip

gt Electric motor andother drive components

gt Power electronics

gt Battery system (rechargeable battery battery management battery system)

gt Battery casing

gt Fuel cell system

gt and so onhellip

gt New components are being developed and produced by incumbent and new suppliers

Competition is forcing OEMs and suppliers to adopt new positions

SupplierSupplier Supplier

OEMOEM OEM

Influence of electrification on vehicle components (excerpt)

Electrification is changing the composition of the vehicle giving rise to new components relating to technology increasing wiring needs

Source Roland Berger

Electrification

28RB - Global automotive supplier study highlights 23012019pptx

AutomotiveEnd game zone

Automotive suppliers will need to prepare for five distinct changes that will emerge on the road to the end game

Emergence of software as a key differentiating factorgt Digital features determine value to the end-customergt Digitization offers new monetization options3

Vanishing growthgt Stagnation in mature marketsgt Increased usage of shared mobility solutions

1Accelerated change of technologies in focusgt Increasing proliferation of electrified powertrainsgt Strong industry push for ADAS and connectivity solutions2

OEMs encounter increasing investment needs and margin pressuregt New technologies require substantial investmentsgt OEMs challenged by new competitors

4Valuation levels of commoditized suppliers might come under pressuregt Outperformance of OEM valuation multiples might come to an endgt Outlook of commoditized supplier sub-sectors might be seen more critical

by equity investors as well as creditors

5

Emerging changes impacting automotive suppliers

Source Lazard Roland Berger

29RB - Global automotive supplier study highlights 23012019pptx

2 Technology shifts

Almost all vehicle domains will see a shift in growth focus over the next years ndash Disruption impact particularly high in powertrain

Impact of technology shifts by domain

Source Lazard Roland Berger

Disruption impact on current business

Supplier domain Low High

Interior

Exterior

Chassis

Powertrain

Powertrain gt E-motors and power electronics

gt Battery systems

gt Simple 1-2 step reduction gears

Interior gt New HMI display technologies

gt Extended Infotainment solutions

gt Increased interior insulation (NVH)

gt Integration of electronics and surfaces

Next generation vehicle concept

Substantial new requirements for the supply base

Chassis gt Advanced driver assistance systems and autonomous features

gt Adaptive suspensions

gt Active steering and braking systems

gt Shifting material focus and growing importance of multi-material applications

gt Growth of non-structural composites

Exterior

30RB - Global automotive supplier study highlights 23012019pptx

Electric powertrain components to experience high growth rates at the expense of many traditional ICE components

Implications for suppliers

gt ICE hardware commoditization

gt Battery systems and electronics provide differentiation opportunities

gt Limited potential in e-motors in part due to lower complexity vs ICE

Background

gt Increasing cost of ICEexhaust treatment

gt Mild and full hybrids aid in emissions improvement and enable ICEs with downgraded requirements

gt BEV penetration rates increase driven by regulation incentives and consumer demand

Technology trends ndash Winners

gt Future powertrain architectures are electrified resulting in several fast growing domains

ndash E-motors

ndash Inverterspower electronics

ndash Battery

ndash Battery cooling

ndash 1-2 step reduction gears

ndash Charging components

Technology trends ndash Losers

gt Consequently traditional ICE components and systems to experience below average growth rates

ndash Engine camshafts crankshafts valves lubricants

ndash Exhaust oil filters alternators ignition

ndash Transmission clutch gearbox propeller shaft

Technology shifts ndash Powertrain

Source Lazard Roland Berger

2 Technology shifts

31RB - Global automotive supplier study highlights 23012019pptx

The ADAS and AD component market will strongly grow providing an increasing revenue pool mainly for software focused suppliers

Implications for suppliers

gt Hardware standardization commoditization of traditional chassis components and systems

gt Intelligent systems integrated with ADAS are expected to offer growth potential within respective domains (eg steering suspension vision systems passenger safety systems)

Background

gt ADAS offers several benefits to society and industry including accident mitigation congestion reduction increased driving comfort and fuel efficiency gains

gt Advanced vehicle control and sensor systems are the main benefactors of the shift to greater advanced driver assistance systemsndash Advanced driver assistance systems and

autonomous features ndash Adaptive suspensionsndash Active steering + braking actuatorsndash E-Axles (as part of electrified powertrain)ndash Vision sensors (LiDAR cameras)

Technology trends ndash Winners

Technology trends ndash Losers

gt Meanwhile traditional vehicle control systems are at risk for reduced market sharendash Hydraulic steering systemsndash Traditional axlesndash Conventional suspensions

Technology shifts ndash Chassis

Source Lazard Roland Berger

2 Technology shifts

32RB - Global automotive supplier study highlights 23012019pptx

Emissions regulations push OEMs for increased lightweighting of body structures while ADAS and connectivity create new use cases

Implications for suppliers

gt Shifting materials competencies for non-structural components suppliers

gt New use cases for intelligent exterior systems may offer differentiation potential particularly when paired with ADAS solutions

Background

gt Shifting material focus and growing importance of multi-material applications

gt New technology integration potential for enhanced safety

gt New design possibilities due to missing ICE powertrain

gt Advanced material components and advanced safety features offer potential in exterior componentsndash Non-structural compositesndash Increased usage of plasticsndash Side and rear view cameras and screensndash Driving mode indication (autonomous vs human

driver)ndash Lock systems using cell phones

Technology trends ndash Winners

Technology trends ndash Losers

gt Traditional materials and exterior components most at risk for lost share includendash Cast partsndash Non-structural steel partsndash Traditional side and rear view mirrors

Technology shifts ndash Exterior

Source Lazard Roland Berger

2 Technology shifts

33RB - Global automotive supplier study highlights 23012019pptx

Autonomous driving will drastically change interior designs and provide innovation and growth potentials

Background

gt Growing importance of non-driving-related activities such as infotainment completing tasks while driving automated eating and drinking

gt Interior provides huge potential for innovation and continued growth

Technology trends ndash Winners