Embed Size (px)

Citation preview

eE / X,'L/iReport No. 681 -GU /

Memorandum on Recent EconomicDevelopment and Prospects ofGuatemalaMarch 31, 1975 FCLatin America and the CaribbeanRegional Office

Not for Public Use

U

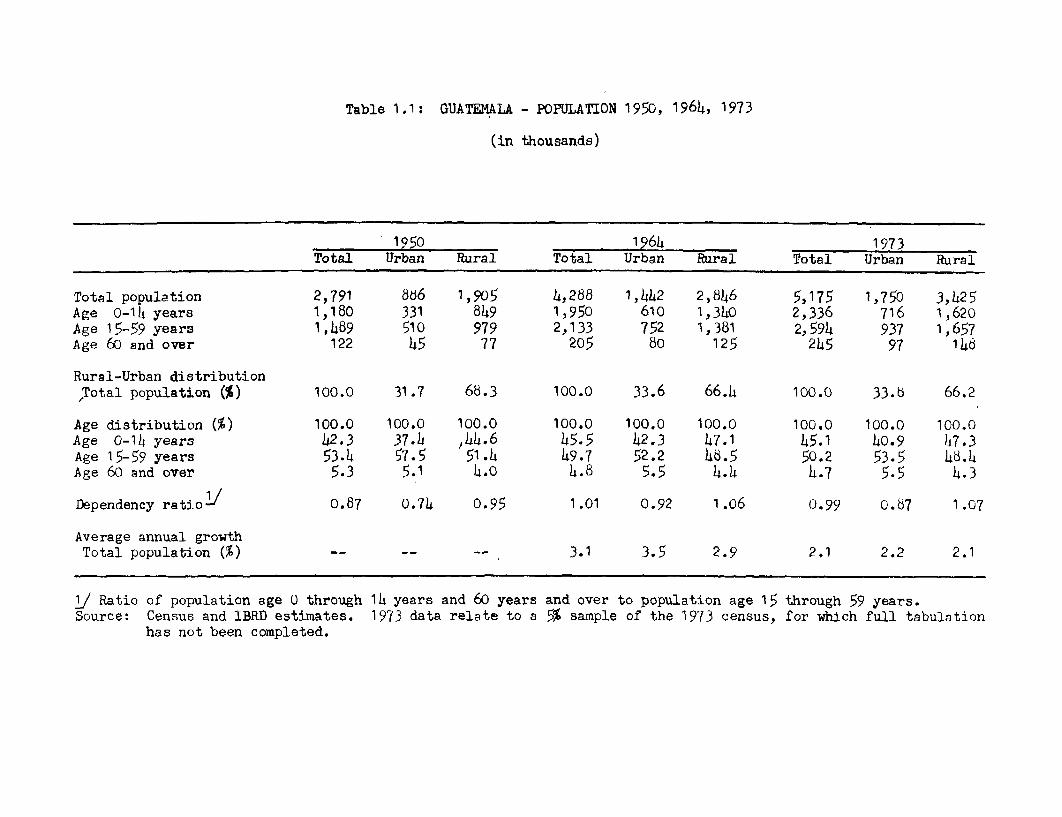

Document of the International Bank for Reconstruction and DevelopmentInternational Development Association

This report was prepared for official use only by the Bank Group. It may notbe published, quoted or cited without Bank Group authorization The Bank Group doesnot accept responsibility for the accuracy or completeness of the report.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

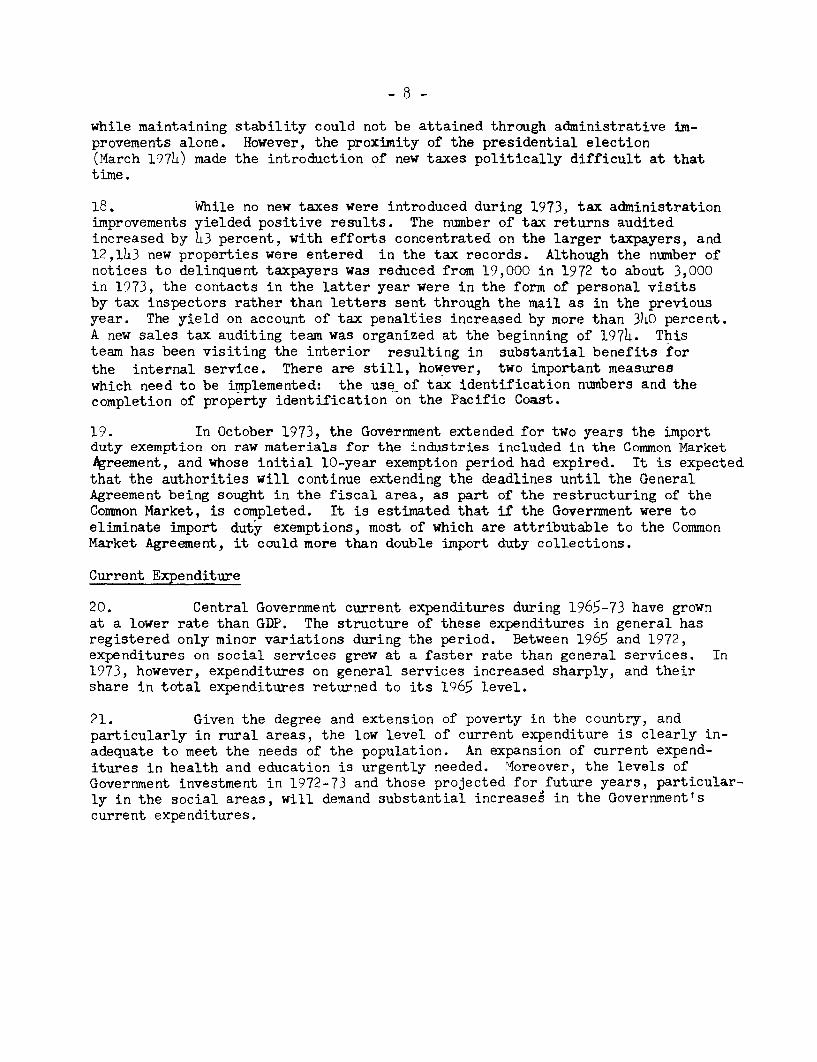

utho

rized

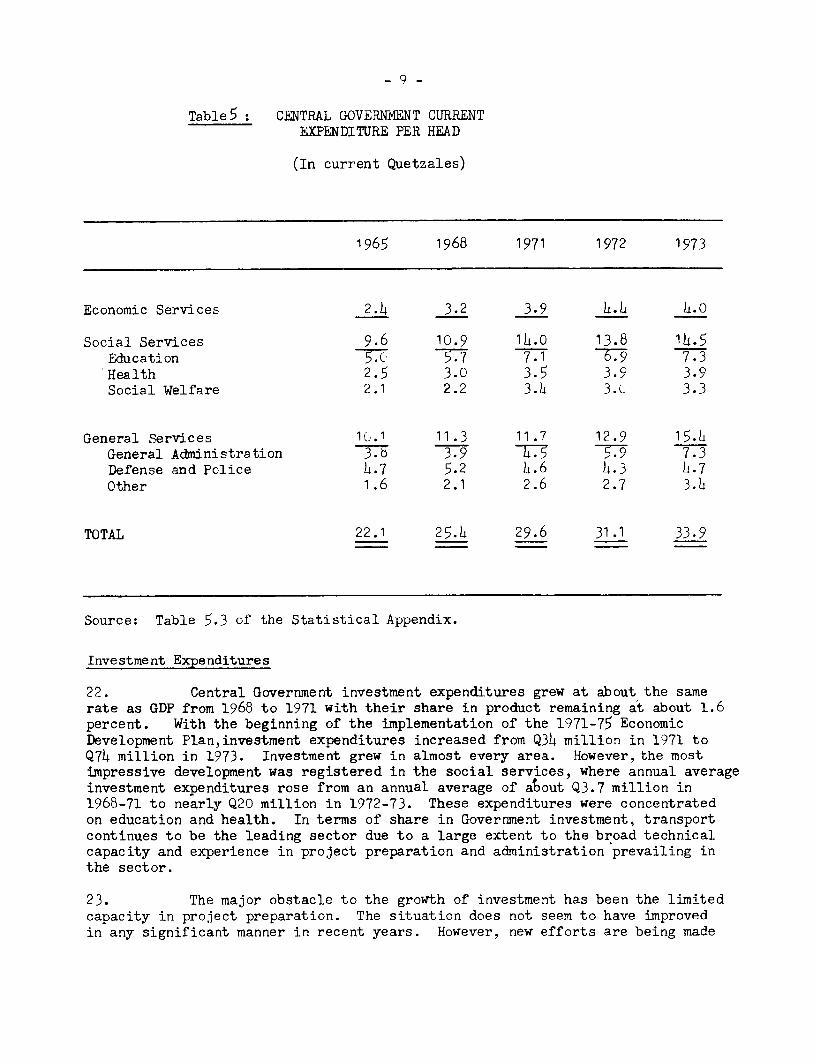

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

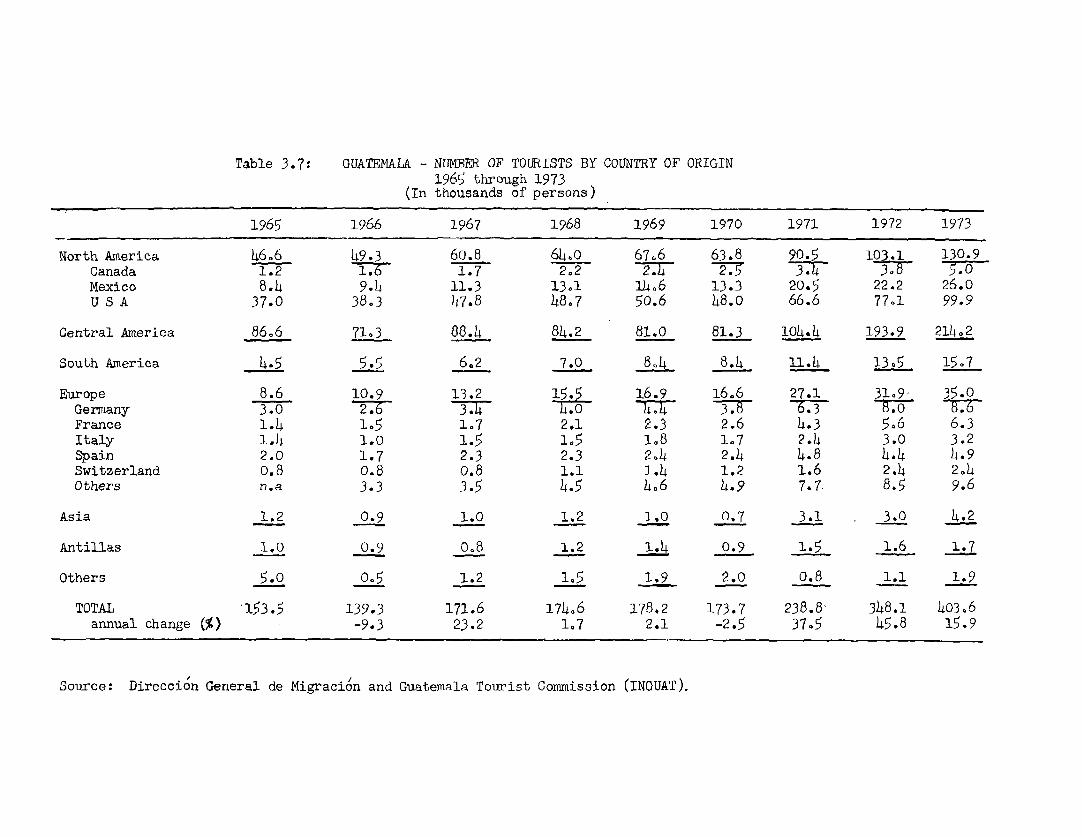

utho

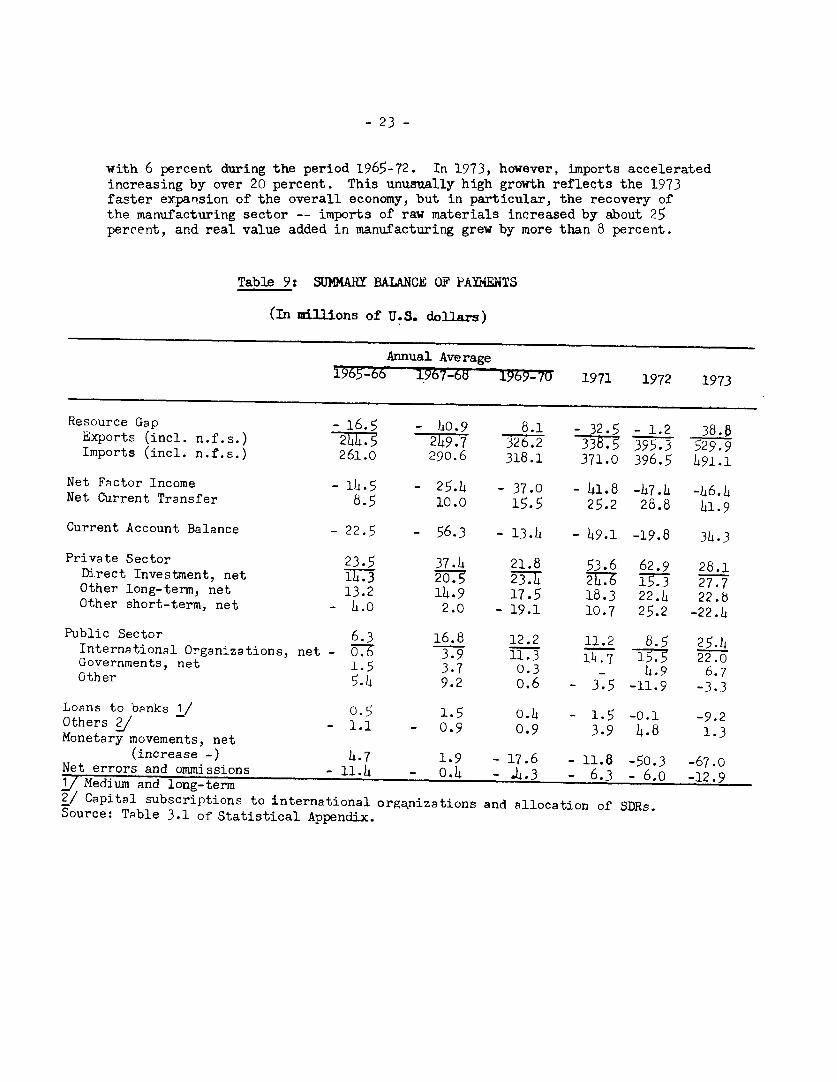

rized

CURRENCY EQUIVALENTS

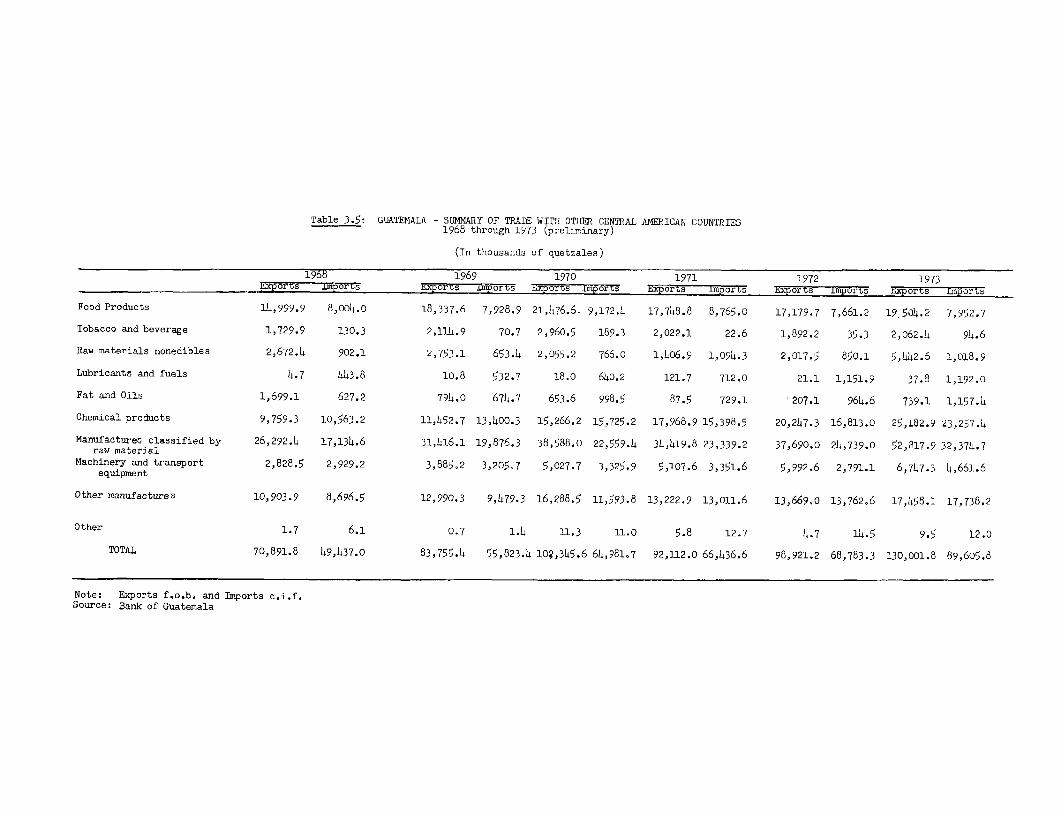

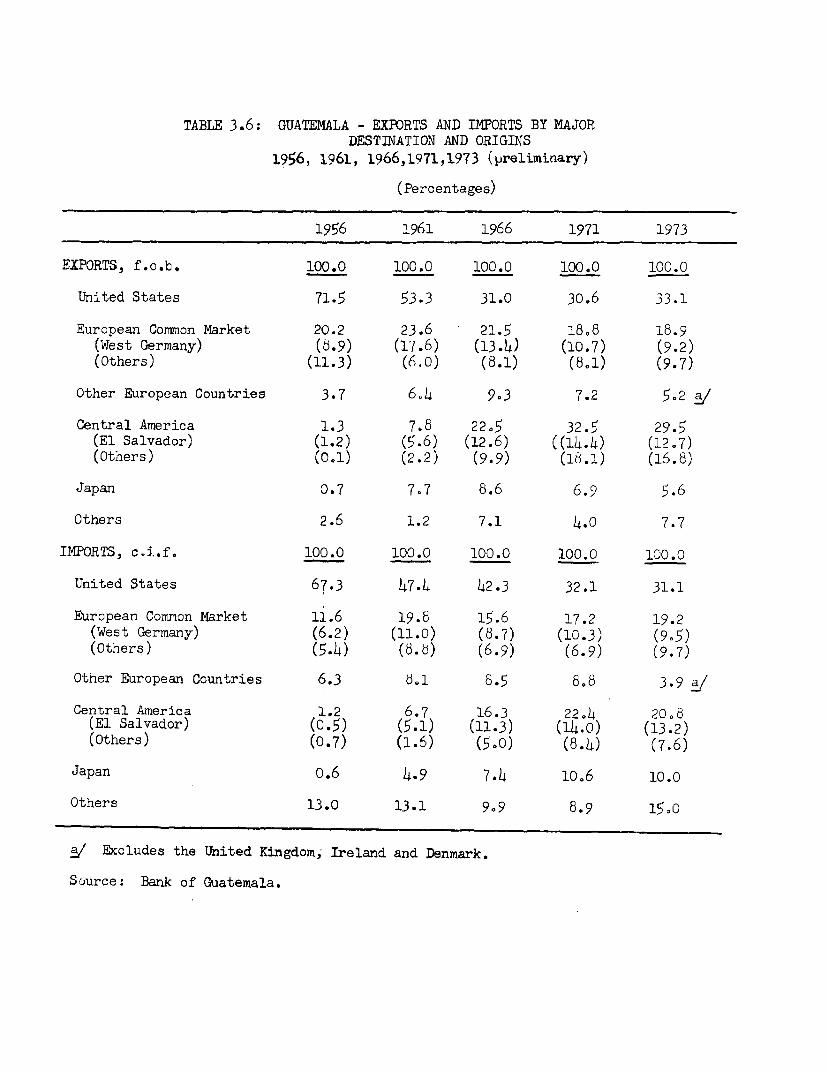

1 Quetzal (Q) = 1 U.S. dollar

GLOSSARY OF ABBREVIATIONS

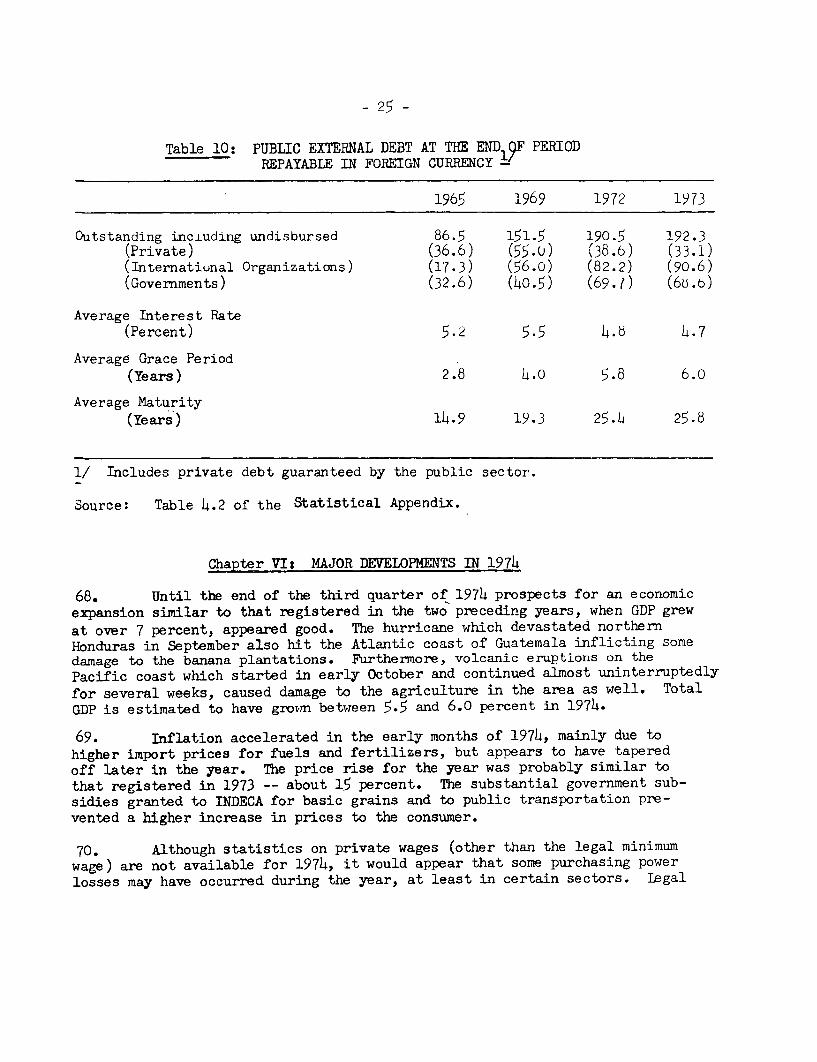

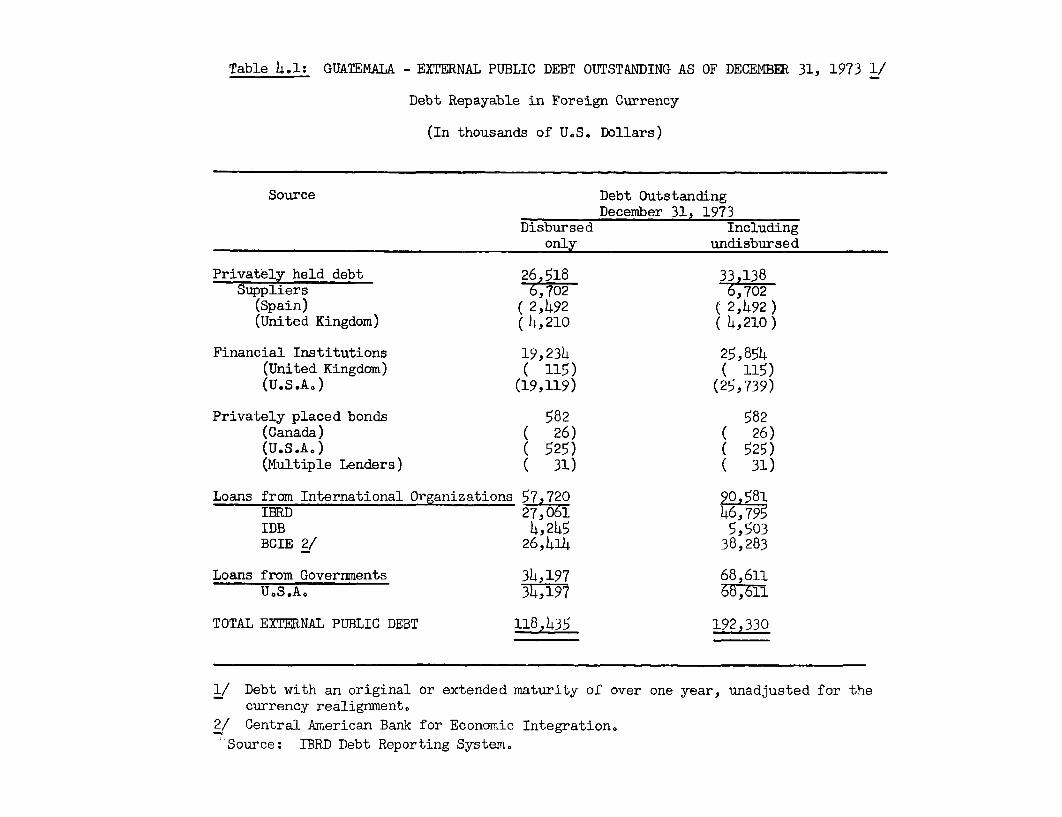

AID - U.S. Agency for International DevelopmentAVIATECA - Guatemalan AirlinesANACAFE - National Coffee AssociationBANDESA - National Bank for Agricultural DevelopmentBCIE - Central American Bank for Economic IntegrationCACM - Central American Common MarketOORFINA - National Finance CorporationEXMIBAL - Company for the Exploration and Exploitation of the

Izabal MinesFEGUA - Guatemalan RailroadsFYDEP - Peten Development AgencyGUATEL - Guatemala Telecommunications AdministrationGUATEXPRO - Guatemalan Export PromotionIDB - Inter-American Development BankIGSS - Guatemalan Social Security InstituteINDE - National Electricity InstituteINDECA - National Institute for the Commercialization of

Agricultural ProductsINFOM - Municipal Development InstituteINFOP - Institute for the Development of ProductionINGUAT - Guatemalan Tourism InstituteINTA - National Institute for Agrarian TransformationINTECAP - Technical Education InstituteINVI - National Housing Institute

FISCAL YEAR

January 1 to December 31

This report is based on thefindings of an economic missionto Guatemala in September 1974composed of:

Guillermo Castafeda ChiefJosefina-Vial Economist

GUATEMALA

TABLE OF CONTENTS

Page Number

COUNTRY DATA

SUMM.A.RY AND CONLUSIONS.i -i

I. INTRODUCTION ...................................... 1

II. ECONOMIC DEVELOPMENT ........................ ,.,, . 2

III. PUBLIC FINANCE ...................................... 5

A. Central Government ...... 6Revenue.. . . ... 7

Current Expenditure. 8

Investment Expenditure . . 9

B. Rest of the Public Sector .

IV. MONEY AND BANKING ................ .. i5

V. BALANCE OF PAYMENTS ................................. 19

Exports . ........ 19Imports ........................................... 22

Financing the Current Account Deficit ............ 2

VI. NAAJOR DEVELOPMENTS IN 1974 .......................... 25

VII. MEDIUM-TERM PROSPECTS ...... 30

MAP

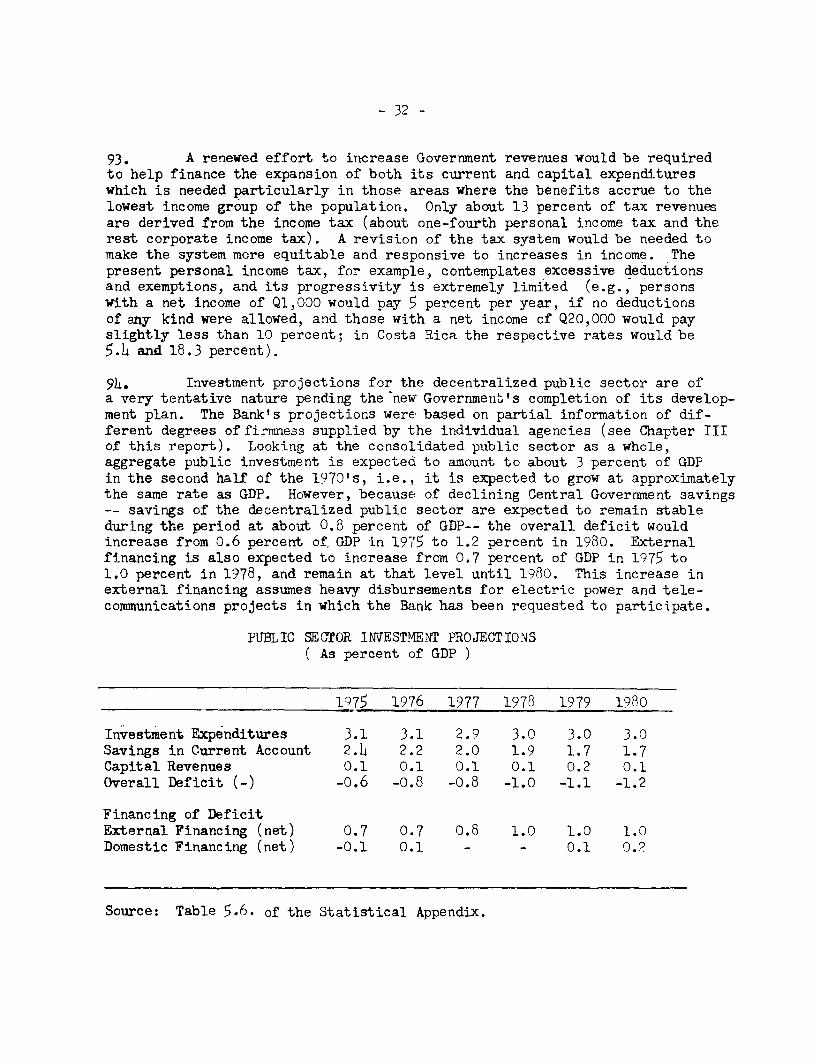

STATISTICAL APPENDIX

PopulationNational AccountsPublic FinanceBalance of PaymentsExternal Public DebtMoney and CreditPrice Indexes

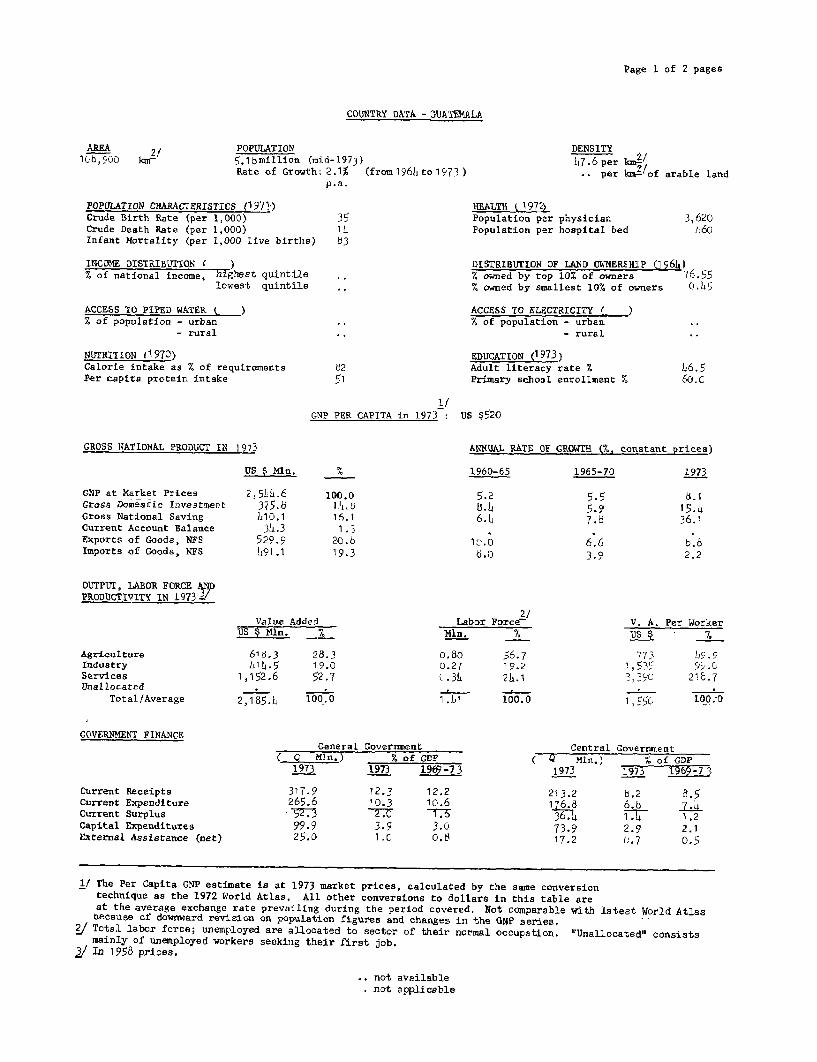

Page 1 of 2 pages

COUNTRY DATA - OUATEMALA

AREA 2/ POPULATION DENSITY1bG,900 ker 5.1bmillion (mid-1973) k7.6 per kn3t

Rate of Growth: 2.1% (from 196h to 17) .. per 2c /of arable landp.a.

POPULATION CHARACTERISTICS _1971-) HEALTH i 197i4Crude Birth Rate (per 1,000) 35 Population per physician 3,620Crude Death Rate (per 1,000) 14 Population per hospital bed L36Infant Mortality (per 1,000 live births) o3

INCOME DISTRIBUTION ( ) DISTRIBUTION OF LAND OWNERSHIP 0964)% of national income, highest quintile .. % owned by top 10% of owners 76.55

lowest quintile ., % owned by smallest 10% of owners 0.05

ACCESS TO PIPED WATER t ACCESS TO ELECTRICITY ( )% of population - urban .. 'A of population - urban

- rural .. - rural

NUTRITiON l970) EDUCATION (1973)Calorie intake as % of requirements 52 Adult literacy rate % h6. 5Per capita protein intake 51 Primary school enrollment Z 60.'

'IGNP PER CAPITA in 1973 : US $520

GROSS NIATIONAL PRODUCT IN 1973 ANNUAL RATE OF GROWTH (%. constant prices)

US $ Mn. x 1960-65 1965-70 1973

GCiP at Market Prices 2,5hh.6 100.0 5.2 5.5 6.1Gross Domestic Investment 375.8 Il .L5 5. 5.9 15.0Gross National Saving 010.1 16.1 6.4 7.6 36.1Current Account Balance 34.3 1 .3Exports of Goods, NPS 529.9 20.6 1'.0 6.6 b.6Imports of Goods, NPS 491.1 19.3 6.0 3.9 2.2

OUTPUT, 1ABOR FORCE pPRODUCTIVITY IN 1973_"

Value Added Labor Force2 V. A. Per WorkerUJS $Mln. %A Mln. 7US %

Agriculture 616.3 28.3 o.8o 56.7 773 1X5.5Industry 31l.5 19.0 0.27 19.2 i,535 959.Services 1,152.6 52.7 (.3 25.1 9.3.3 210.7Unallocated

Total/Average 2,185.0 100.0 1 .51 100.0 1,55, 100.-9

GOVERNMENT FINANCEGeneral Goverrmeat Central GovernmentMin.) 7. of CIP ( Q Mln.) 'A of GDP

1973 1973 1l26i2 1973 L973 1969-7 3

Current Receipts 317.9 12.3 12.2 213.2 5.2 8.5Current Expenditure 265.6 10.3 10.6 136k1 6.5 7 .Current Surplus 3273 2.C 7.6 .4h 1. 1.2Capital Expenditures 99.9 3.9 3.0 73.9 2.9 2.1External Assistance (net) 25.0 1.C 0.8 17.2 C.7 D.5

1/ The Per Capita CNP estimate is at 1973 market prices, calculated by the same conversiontechnique as the 1972 World Atlas. All other conversions to dollars in this table areat the average exchange rate prevailing during the period covered. Not comparable with latest World Atlasoecause of downward revision on population figures and changes in the GNP series.

2/ Total labor force; unemployed are allocated to sector of their normal occupation. '"Unallocated" consistsmainly of unemployed workers seeking their first job.

31 In 1958 prices.

not availablenot applicable

Page 2 of 2 pages

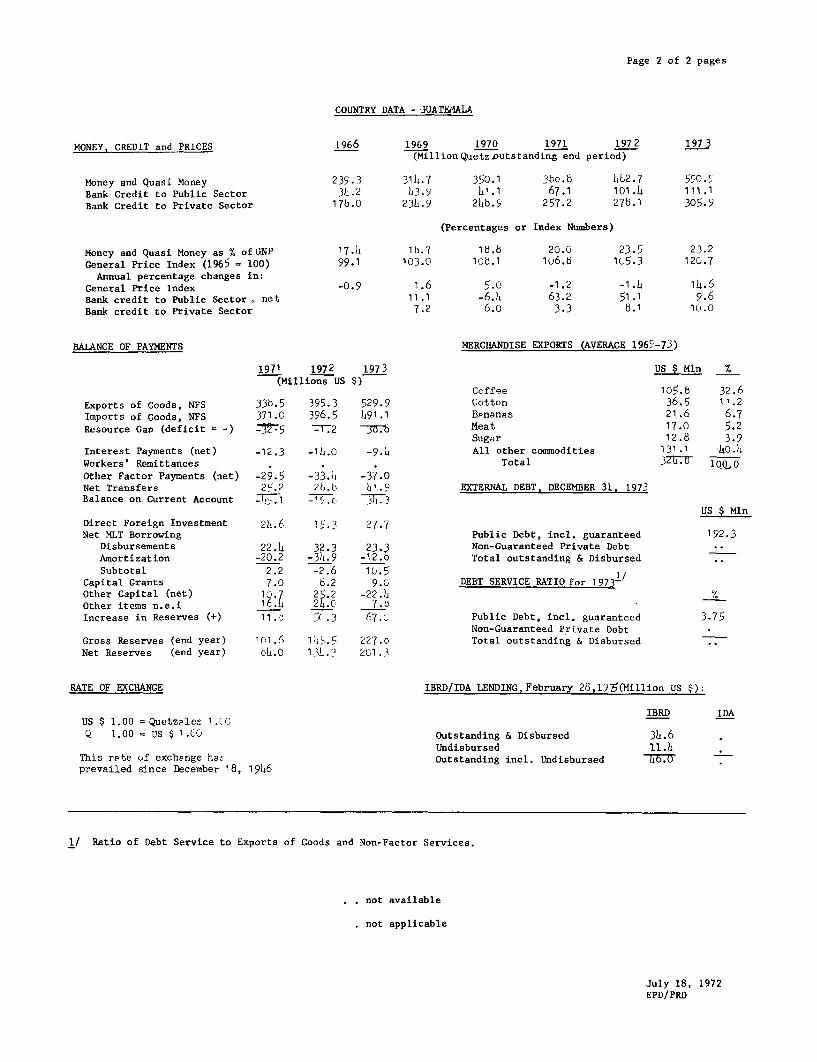

COUNTRY DATA - JUATEMALA

MONEY, CREDIT and PRICES 1966 1969 1970 1971 197 2 197 3(MillionQuetz outstanding end period)

Money and Quasi Money 239.3 31 I.7 350.1 3bb.& 462.7 590.5Bank Credit to Public Sector 3h.2 13.9 h1'.1 67.1 101.4 111.1Bank Credit to Private Sector 176.0 231h.9 24b.9 257.2 270.1 305.9

(Percentages or Index Numbers)

Money and Quasi Money as % of LNP 17.4 1.7 1ci.o 20.0 23.5 23.2General Price Index (1965 = 100) 99.1 103.0 108.1 lo6.o 1 u5.3 120.7

Annual percentage changes in:General Price Index -0.9 1.6 5.0 -1.2 -1.4 14.6Bank credit to Public Sector, net 11.1 -6.4 63.2 51.1 9.6Bank credit to Private Sector 7.2 6.o 3.3 8.1 10.0

BALANCE OF PAYMENTS MERCHANDISE EXPORTS (AVERAGE 1969-73)

1971 1972 1973 US $ Mln %(Millions US $)

Coffee 105.o 32.6Exports of Goods, NFS 33d.5 395.3 529.9 Cotton 36.5 11.2Imports of Goods, NFS 371.0 396.5 891.1 Bpnanss 21.6 6.7Resource Gap (deficit -) . 5 1TT2 jo.b Meat 17.0 5.2

Sugar 12.8 3.9Interest Payments (net) -12.3 -1h.o -9.4 All other commodities 131.1 140.4Workers' Remittances . . Total 32li.o T 8 QO

Other Factor Payments (net) -29.5 -33.1, -37.0Net Transfers 2'.2 20.0 8 .9 EXTERNAL DEBT. DECEMBER 31. 1973Balance on Current Account 38C.1 -15.c .3

US $ MlnDirect Foreign Investment 28i.6 15.3 2|.7Net MQT Borrowing Public Debt, incl. guaranteed 192.3

Disbursements 22.4 32.3 23.3 Non-Guaranteed Private DebtAmortization -20.2 -38.9 -12.8 Total outstanding & DisbursedSubtotal 2.2 -2.6 10.5 l/

Capital Grants 7.0 6.2 9.C DEBT SERVICE RATIO for 1973Other Capital (net) 1. 25.2 -22.4 %Other items n.e.i 16:L 2 c. 7.oIncrease in Reserves (+) 11.o 50.3 67.' Public Debt, incl. guaranteed 3.75

Non-Guaranteed Private DebtGross Reserves (end year) 101o.6 185.5 227.0 Total outstanding & DisbursedNet Reserves (end year) 08.0 13,.3 2C1.3

RATE OF EXCHANGE IBRD/IDA LENDING, February 28,l975(Million US $):

IBRD IDAUS $ 1.00 = Quetzples 1.CRQ 1.00 = US $ 1 .Co Outstanding & Disbursed 34.6

Undisbursed 11.4This rate uf exchenge hat Outstanding incl. Undisbursed 76rprevailed since December 18, 1946

1/ Ratio of Debt Service to Exports of Goods and Non-Factor Services.

not available

not applicable

July 18, 1972EPD/PRD

SUMMARY AND CONCLUSIONS

i. Guatemala's rate of economic growth has been accelerating since1950. Although the rate of growth fluctuated substantially during 1963-73,it never fell below h percent per annum; on average product grew by about5.8 percent per year. The average rate of growth of GDP for the years1972 and 1973 is estimated at more than 7 percent per annum. Populationgrowth seems to have decelerated significantly in the last decade, fallingfrom 3.1 percent during the period 1950-6h to 2.1 percent per annum during196h-73. The benefits of economic growth have been extremely concentratedand the standard of living of the rural poor -- who make up nearly 50 per-cent of the 5.2 million population -- does not seem to have improvedsignificantly. GNP per capita reached more than US$500 in 1973. Prelim-inary estimates for 1974 indicate output grew by some 5.7 percent.

ii. The Guatemalan public sector's role in promoting economic growthhas been limited. As emphasized in previous World Bank reports, a moreactive Government participation in the growth process is needed to attacksuccessfully the deep-seated long-term development problems of the country.Substantial increases in development expenditures (both capital and current)are needed to broaden the country's economic and social base and to inte-grate the large subsistence sector into the market economy. The Governmentthat left office in July 1974 is credited with some positive actions in thisdirection as part of the implementation of the 1971-75 Development Plan.Investment expenditures were doubled in 1972-73, with a large proportion ofthe increase occurring in health and education; thus from an annual averageof Q3.7 million for investment expenditures in these areas during 1968-71,they reached an average of Q20 million in the years 1972-73.-

iii. The major bottlenecks that prevented achievement of higher publicinvestment levels in the past were the inadequate capacity to prepare andexecute projects and an inadequate system of taxation. Nlew efforts are beingmade to enlarge project preparation capacity. Tax revenues are less than8 percent of GDP, which is among the lowest in the developing countries. Newtax measures were taken in l974, but these were primarily intended to compen-sate for the erosion of Government revenues resulting from the inelasticityof the tax system in the face of inflation. The new administration is cur-rently preparing a new economic development plan. In the meantime, however,some basic policy decisions have been made as part of the emergency programto fight inflation -- that is, the Government has provided fertilizers,extension services and storage, and has increased support prices in orderto stimulate production of basic grains. These measures should be integratedinto a compFehensive development program to improve the productivity ofsmall-scale subsistence agriculture in order to increase the lot of the poor-est sectors of the economy.

iv. Prices have been growing at an unusually fast rate in the recentpast. The force behind this new phenomenon in the Guatemalan economy

- ii -

originated mainly in the external sector. The Government has taken a seriesof measures to reduce the impact of world market conditions on the rest ofthe economy. The policies have been aimed mainly at increasing the supplyof goods which are considered essential. In addition, a temporary pricecontrol system was introdLuced to fight hoarding and artificial price escala-tion. Excess liquidity in the banking system prevailed in 1972 and 1973.The monetary authorities were slow in responding to this situation. Itwas not until September 1974 that an upward revision of interest rates andreserve requirements for the banking system was implemented.

v. In 1973 the balance of payments reached a record surplus ofUS$67.0 million, and the Central Bank's foreign reserves reached a recordof US$213.R million. However, mainly because of the increase in the priceof oil and speculative stockpiling of imported raw materials and intermediategoods, the balance in current account switched from a surplus of US$3h.0million in 1973 to a deficit of about. US$75.0 million in L97L4. In addition,there was a short-term capital outflow of about US$30.0 million last year.

vi. Despite higher costs of fuel and other imported inputs, the over-all economic prospects for Guatemala for the rest of the decade are reason-ably good. With no basic changes in policy, the economy could grow atabout 6 percent per year under fairly safe balance of payments conditions.However, a continuation of past trends would only have a very limited effecton the large segment of the population still on the margin of the casheconomy. If this segment of the population is to be integrated graduallyinto the modern economy, a more agressive development policy will have tobe implemented. The very low public debt service ratio (3.8 percent in1973), which will probably decline further, would easily allow the increasesin foreign indebtedness which are needed to accelerate development. However,this increase in the inflow of foreign resources could be brought aboutonly if the country were to expand its absorptive capacity through thestrengthening of the project preparation process and through a fiscal effortsufficient to generate the required additional counterpart financing.

ECONOMIC DEVELOPMENT AND PROSPECTS OF GUATEMALA

Chapter I: INTRODUCTION

1. Mountains divide Guatemala into four main regions: the highlands,the Pacific coastal plain, the Atlantic area and the Pet6n. Geologicalhistory has given this mountainous tropical country very fertile, volcanicsoil and a range of altitudes which offer a wide variety of climates. Thesevaried regional conditions are well-suited to the growth of almost any typeof agricultural product. The Pacific lowlands produce cotton, sugar cane,cattle, rice and other tropical crops. The upper Pacific piedmont is anexcellent coffee region and most of the coffee is produced in this area.The highlands produce most of the corn and beans, which are the principalitems in the country's diet, and the Atlantic area produces bananas andsome coffee. The Pet6n, which is the northernmost province, occupies abouta third of the country's area, but is largely unexploited. It containsthe most important archeological monuments of the Mayas, and produceschicle and some tropical woods.

2. On the other hand, the rugged and broken topography has hamperedtransport and created great obstacles to the development of the country,and has tended to perpetuate the cultural isolation of some segments of therural population. There has been no extensive exploitation of Guatemala'smineral resources. The first large commercial exploitation of nickel, nearLake Izabal in the Atlantic area, will be started in early 1977. Exploratorywork in potential petroleum areas has been carried out, apparently withencouraging results; however, while exploration continues, there are as yetno immediate plans for exploitation. The natural beauty of the country andits rich history, which has left archeological monuments and folklore ofrare quality, give Guatemala a high potential for tourism development.

3. Guatemala has the largest population among the Central Americancountries. Because of the good climate and soils, most of the populationand economic activity are concentrated in the central highlands and thePacific slopes. The population is mainly rural. Guatemala City, thecapital, has more than 717,000 inhabitants, but only two other cities haveover 30,000. Guatemala's population has been growing at about 2.1 percentper annum in the last decade and now totals 5.2 million. The most signif-icant characteristic of the population is its sharp ethnic division. Thepure Indians, who make up about 43 percent of the total population, areeconomically, culturally and linguistically separated from the rest of thepopulation, which is mainly of mixed Spanish and Indian origin. A largepart of the Indian population participate to a very limited extent in themoney economy and political life of the country. The main contribution ofthe Indians to output, apart from their subsistence agriculture, has beento provide a labor supply for the large coffee and cotton plantations atharvest time.

Chapter II: ECONOMIC DEVELOPMENT

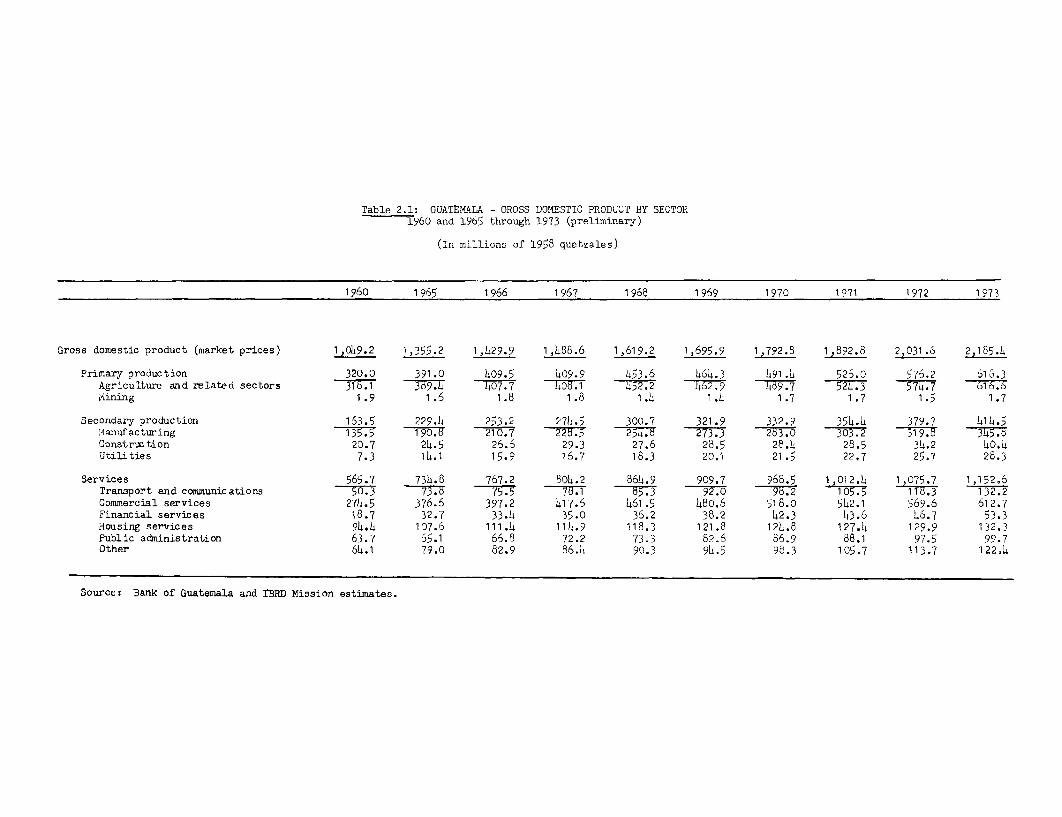

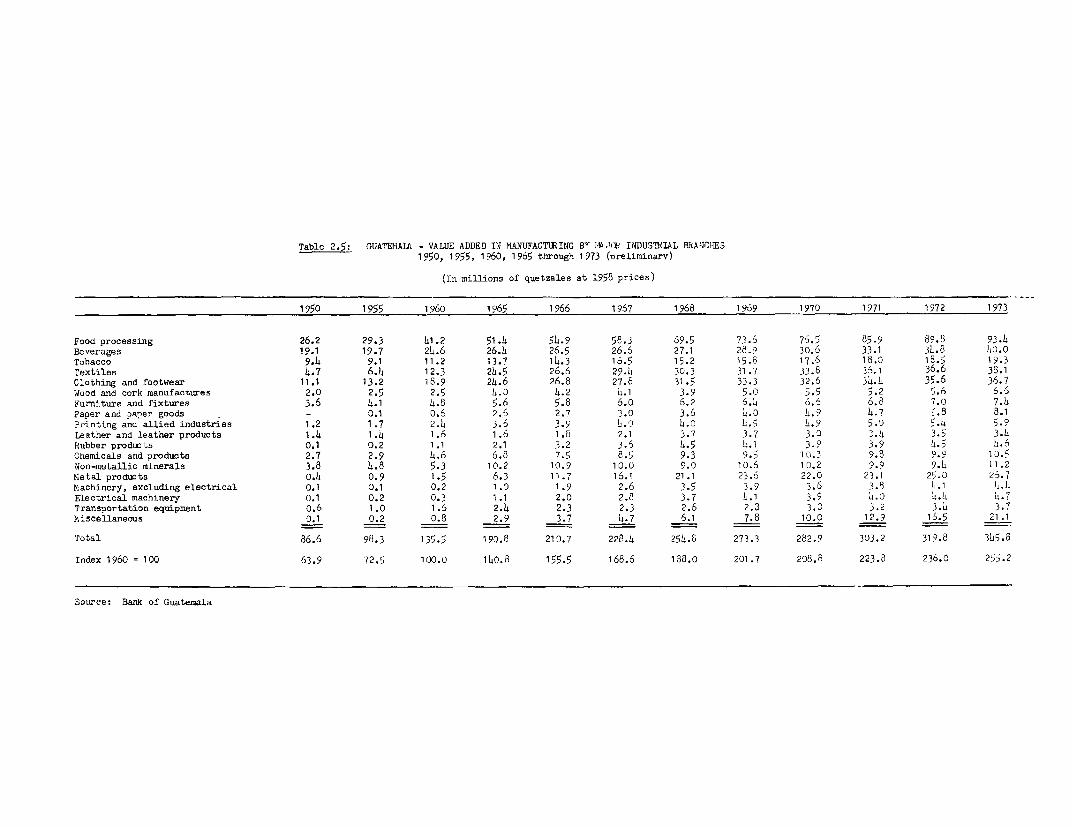

4. Guatemiala's rate of economic growth has been accelerating inthe last two decades. In the first five years of the L950's, despite thestimulating effects of the Korean War on the country's exports, the averagerate of growth was only about 2.5 percent per annum. Substantial improve-ments in world market conditions for coffee in 1956-57 stimulated theeconomy, and output increased at a yearly average of 6.9 percent. However,as world market conditions for primary commodities deteriorated in 1958,growth fell back to 2.3 percent. In subsequent years the rate of growthremained above 3.5 percent. In 1963 Guatemala achieved a record crop ofcoffee, and the production of cotton, which had expanded rapidly in pre-vious years, nearly doubled. Despite some deterioration in prices, thevalue of Guatemala's exports increased by about 30 percent and output by9.5 percent. After 1963 the annual rate of growth never fell below 4.0percent and on average product grew by about 5.8 percent per annum.

5. The improvements of the 60's and 70's have been the result oftwo main factors: first, the development of commercial agriculture in newareas on the Pacific Coast, and second, the creation of the Central AmericanCommon Market in 1960. The Common Market gave a powerful incentive to themanufacturing sector which grew at a high rate until the 1969 Honduras-ElSalvador border conflict, which disrupted the market and contributed toHonduras? withdrawal from it. However, an interim bilateral trade agreementwith Honduras and good market conditions for most of Cpntral Arnericanprimary products spilled over into the manufacturing sector, which resumedits high rate of growth early in 1973.

6. Preliminary results of the 1973 census indicate that, contraryto previous estimates, population growth has decelerated significantly in-the last decade, falling from 3.1 percent per year in the intercensus period1950-64 to 2.1 percent per year between 1964 and 1973. Moreover, the ratioof urban population to total population has remained almost unchanged be-tween the last two censuses. This would appear to be the result of a steep-er decline in urban birth rates rather than a halt in urban migration -- theshare of population aged 0-14 in the urban area has declined by 1.5 percentagepoints between 1964 and 1973, while the corresponding share in rural areashas been reduced by only half a percentage point.

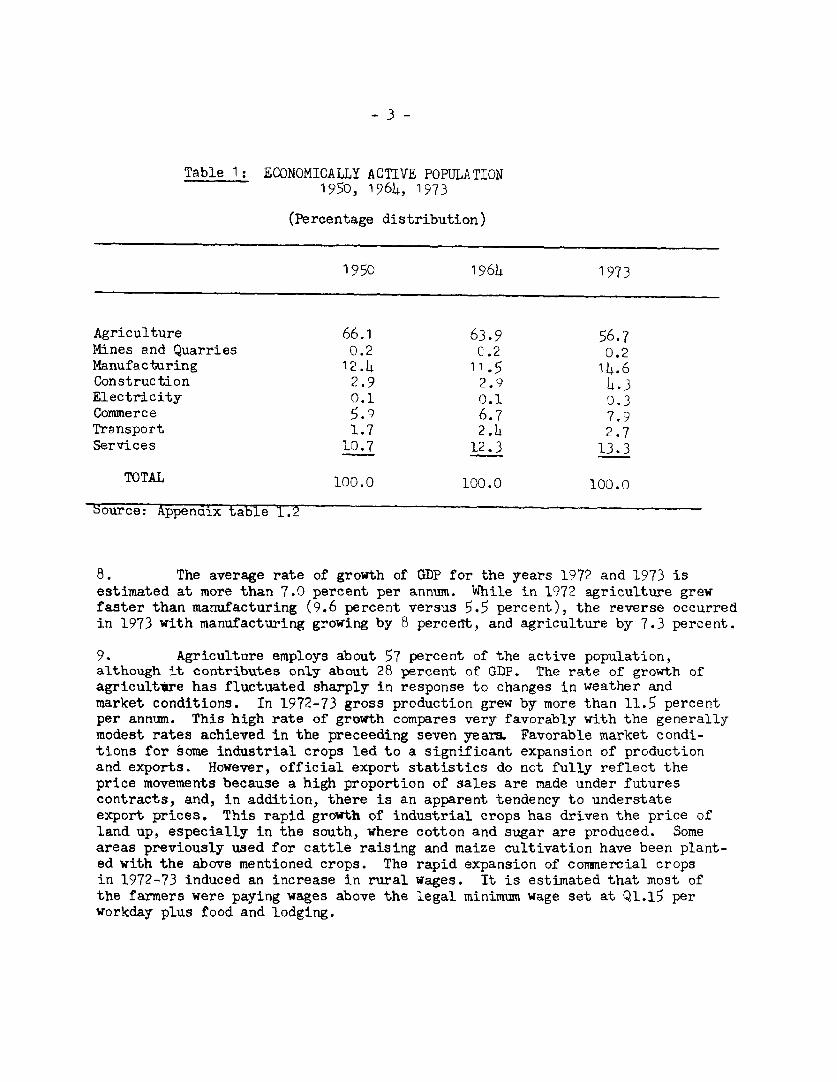

7. The change in structure of active population has followed thestandard pattern for countries at Guatemala's stage of development, withprimary activities losing their relative importance to secondary and tertiaryactivities. A major portion of the relative decline in the active agricul-tural population has been absorbed by manufacturing and construction -- theformer losing over seven percentage points of its share in the total, whilethe latter two together gained 5.5 percentage points (See Table 1).

Table 1: ECONOMICALLY ACTIVE POPULATION1950, 1964, 1973

(Percentage distribution)

1950 1964 1973

Agriculture 66.1 63.9 56.7

Mines and Quarries 0.2 0.2 0.2

Manufacturing 12.4 1265 14.6

Construction 2.9 2.9 4.3

Electricity 0.1 0.1 0.3

Commerce 5.9 6.7 7.9

Transport 1.7 2.h 2.7

Services L0.7 12.3 13.3

TOTAL 100.0 100.0 100.0

3ource: Appendix table 1.2

8. The average rate of growth of GDP for the years 1972 and 1973 is

estimated at more than 7.0 percent per annum. While in 1972 agriculture grew

faster than manufacturing (9.6 percent versus 5.5 percent), the reverse occurred

in 1973 with manufacturing growing by 8 percent, and agriculture by 7.3 percent.

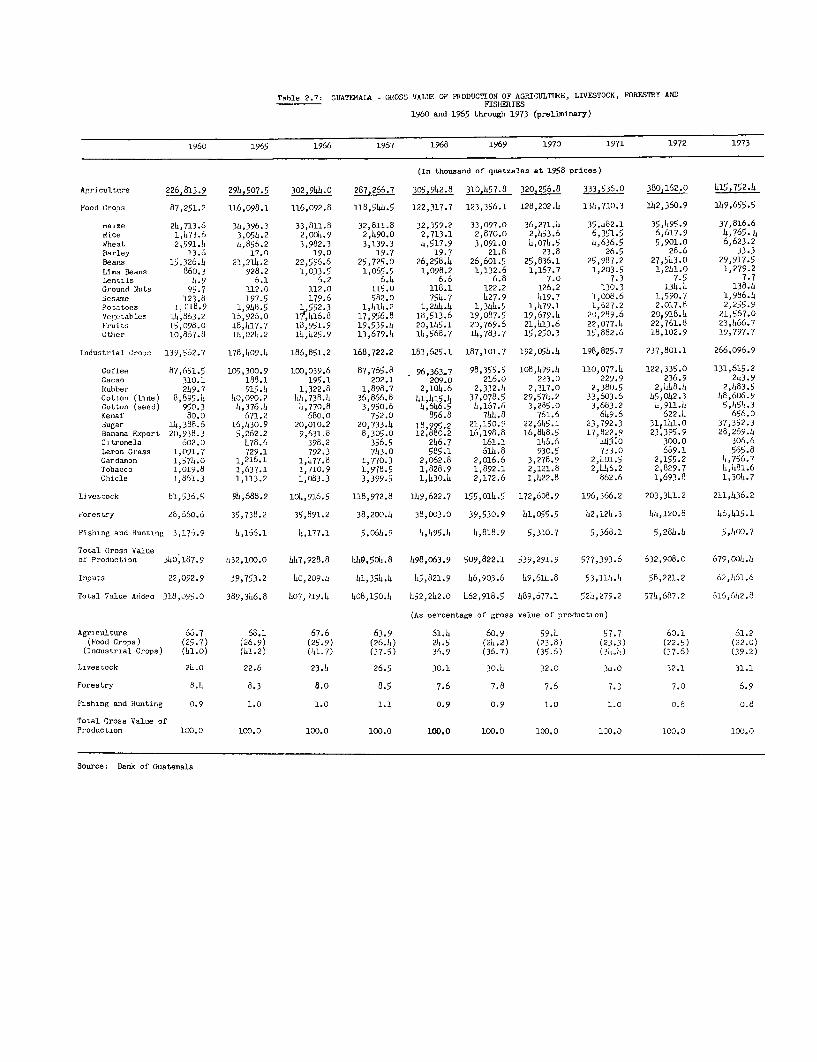

9. Agriculture employs about 57 percent of the active population,

although it contributes only about 28 percent of GDP. The rate of growth of

agricultire has fluctuated sharply in response to changes in weather and

market conditions. In 1972-73 gross production grew by more than 11.5 percent

per annum. This high rate of growth compares very favorably with the generally

modest rates achieved in the preceeding seven years. Favorable market condi-

tions for some industrial crops led to a significant expansion of production

and exports. However, official export statistics do not fully reflect the

price movements because a high proportion of sales are made under futures

contracts, and, in addition, there is an apparent tendency to understate

export prices. This rapid growth of industrial crops has driven the price of

land up, especially in the south, where cotton and sugar are produced. Some

areas previously used for cattle raising and maize cultivation have been plant-

ed with the above mentioned crops. The rapid expansion of commercial crops

in 1972-73 induced an increase in rural wages. It is estimated that most of

the farmers were paying wages above the legal minimum wage set at Ql.15 per

workday plus food and lodging.

Table 2 GDP BY TYPE OF ECONOMIC ACTIVITY1950 - 1973

(In percentage)

Annual Averages

t950-52 1957-59 1966-66 1971-73

Gross Domestic Product 100.0 100.0 100.0 100.C

Primary production 32.6 . 9.7 29.0 26.2Agriculture and related sectors 32.6 29.5 26.9 26.1

Mining 0.2 o.2 0.1 .1

Secondary production 15.4 16.4 17.1 1d.dManufacturing 12.1 12.6 1h.27 15.9Construction 2.6 3.1 1.9 1.7

Utilities o.5 0.7 1.0 1.2

Services 51.o 53.9 53.9 53.oTransport and Communications 3.7 -T:T5.1 5, 3 gCommercial services 26.3 226.4 27.7 26.2Financial services 1.3 1.6 2.4 2.3Housing services 8.6 6.6 7.9 6.4Public Administration 6.2 5.9 h.6 4.7Other 5.7 6.1 5.8 5.6

Source: IBRD report WH-132b and appendix table 2.1

10. The average growth rate of gross production of food crops has exceeded

5 percent per annum in 1971-73 after the very low growth registered in the pre-ceeding six years. However, the production of maize, the main staple of the

population, dropped in 1971 and 1972, while that of beans, the other basic food

crop, registered significant gains only in 1972 and 1973, The slow growth in

basic grains has forced the Gcvernment to import substantial amounts of corn

in the recent past. In view of the importance of basic grains, the Government

has taken measures to promote their production.

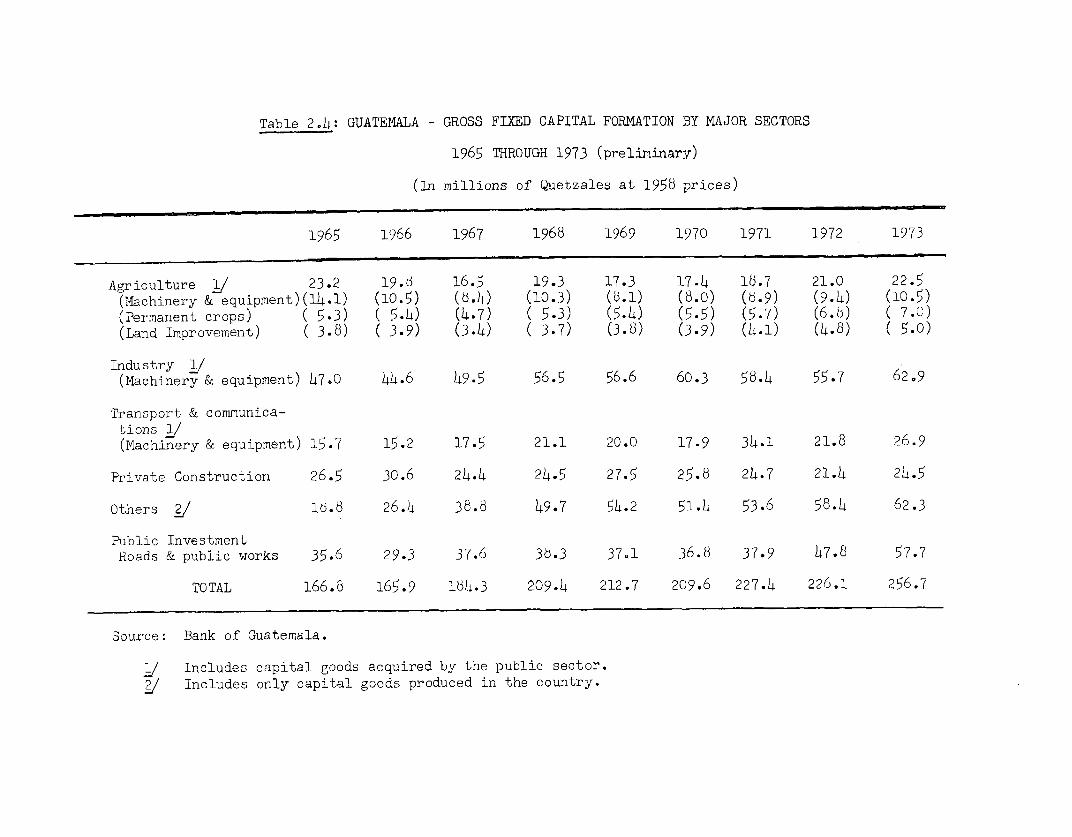

II. Although investment has fluctuated widely from year to year, for the

last 23 years it has been growing on the average at a faster pace than GDP.In 19g0 gross investment as a percentage of GDP was only about 9.3 percent.

In the second half of the l950's, the economic boom which crigina.ted in the

external sector, had a positive impact on investment -- in 1956-53 the rate

of investment attained a level of 15.3 percent. In the period l19:-62 investmentwas substantially depressed and the average rate of investment declined to about

9.6 percent of GDP. However, investment received renewed stimulus there-after as a result of the creation of the Central American Cormon Market,which brought with it generous exemptions from duties 'on imports of capital

goods and raw materials, tax holidays for new industries, and increasedimport duties on products which would be competitive with those of the

Commcn Market. Since 1963 the average rate of investment to GDP hasrema_ned at nearly 13 percent, with public investment increasing sub-stantially in 1972 and 1973.

12. The new more aggressive investment policy of the Governmentcompensated in part for the lower levels of investment in the privatesector in 1972. Private investment in the manufacturing sector declin-ed due to prevailing uncertainties in the Central American Common Marketand to the existence of substantial excess capacity in industries suchas textiles. Recent increases in demand for manufactured products haveled to an expansion of investment in stocks, particularly in the earlymonths of 197h. The strong external market for the main commodity exportsof Guatemala stimulated investment in agriculture in 1972-73. Moreover,as a result of the economic boom, the housing industry, which had stagnatedfor many years, was growing at about 19 percent per annun. Constructionactivity is mainly concentrated in Guatemala City.

13. The country's economic fortunes have traditionally depended onfluctuating prices and supply conditions for a few agricultural export crops.Development in the agricultural sector has been restricted almost exclusivelyto large commercial agriculture, which is concentrated in only a few areasof the country. The effects of rapid economic growth have not been spreadwidely through the economy. Real wages in plantation agriculture havetraditionally been low and it appears that only recently they have register-ed some improvements. Productivity in most of the highlands -- where mainlybasic grains are grown on small plots of land -- has made only small gains.Since the beginning of the 1960's the base for economic growth was broadenedwith the creation of the Central American Common Market, which became animportant outlet for Guatemala's industrial production. The size of themarket and the limited possibilities for futher import substitution willcontinue to be a major constraint to future growth of the manufacturingsector. However, the experience gained through the Common Market will bevery valuable in promoting non-traditional exports to third markets.

Chapter III: PUBLIC FINANCE

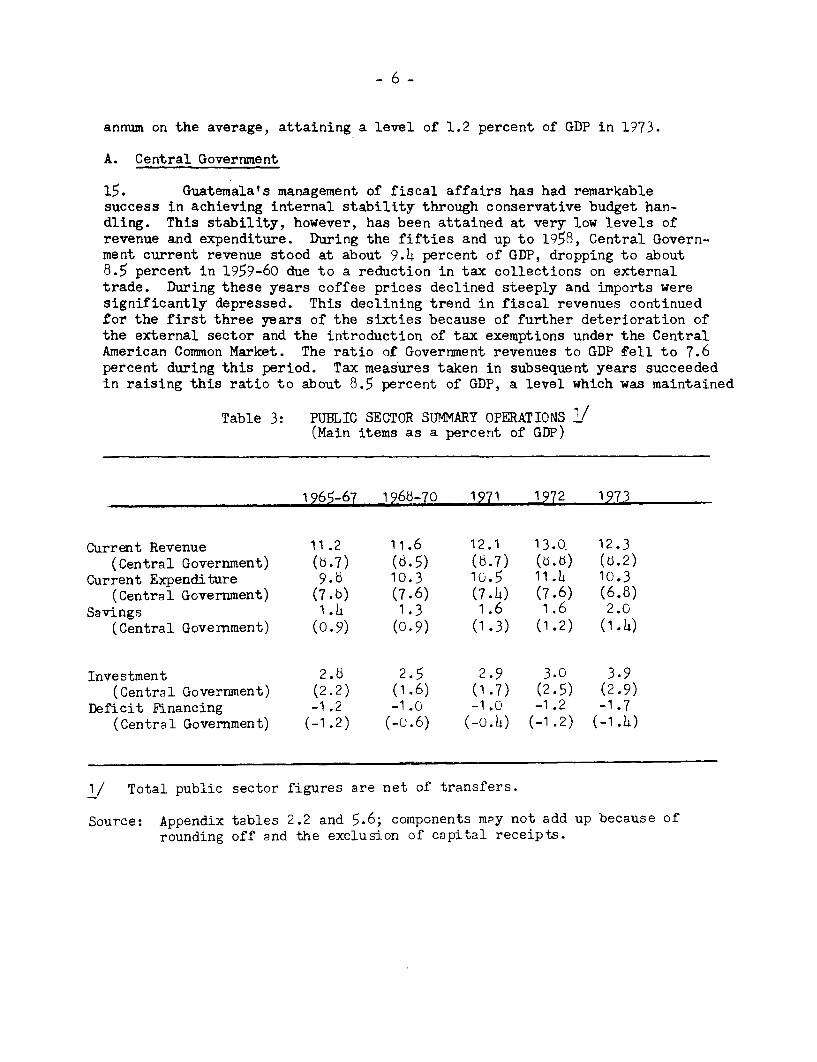

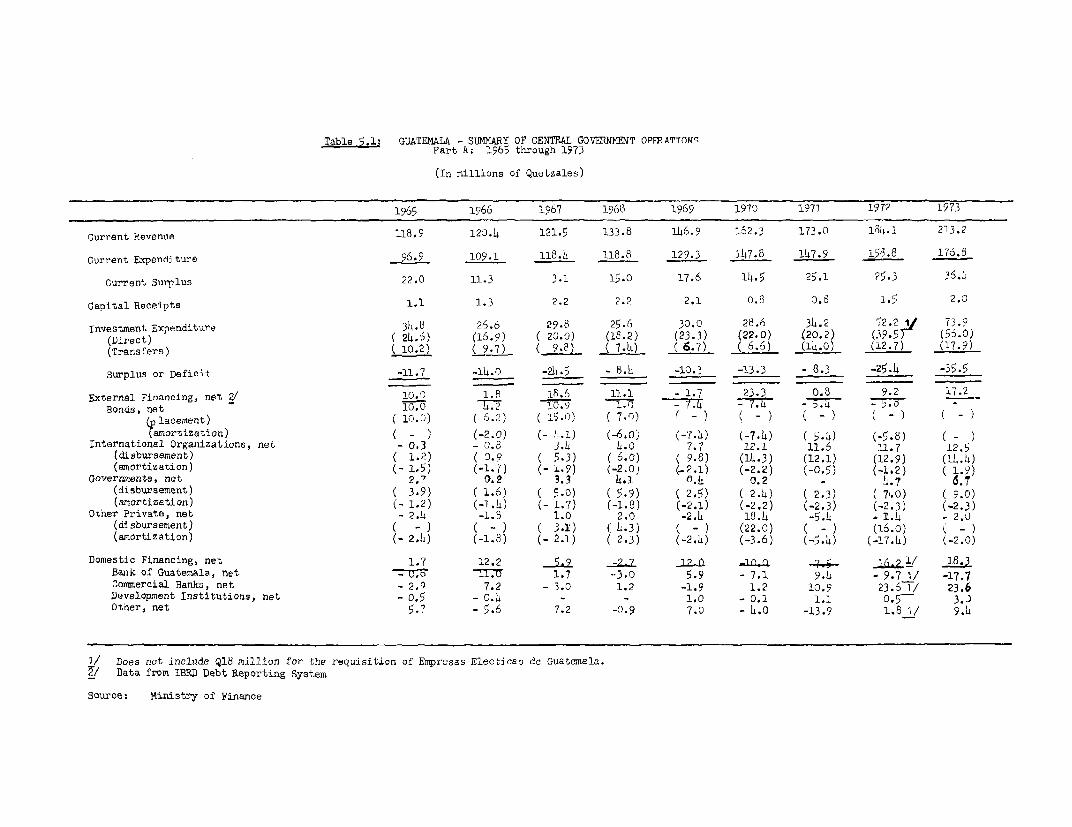

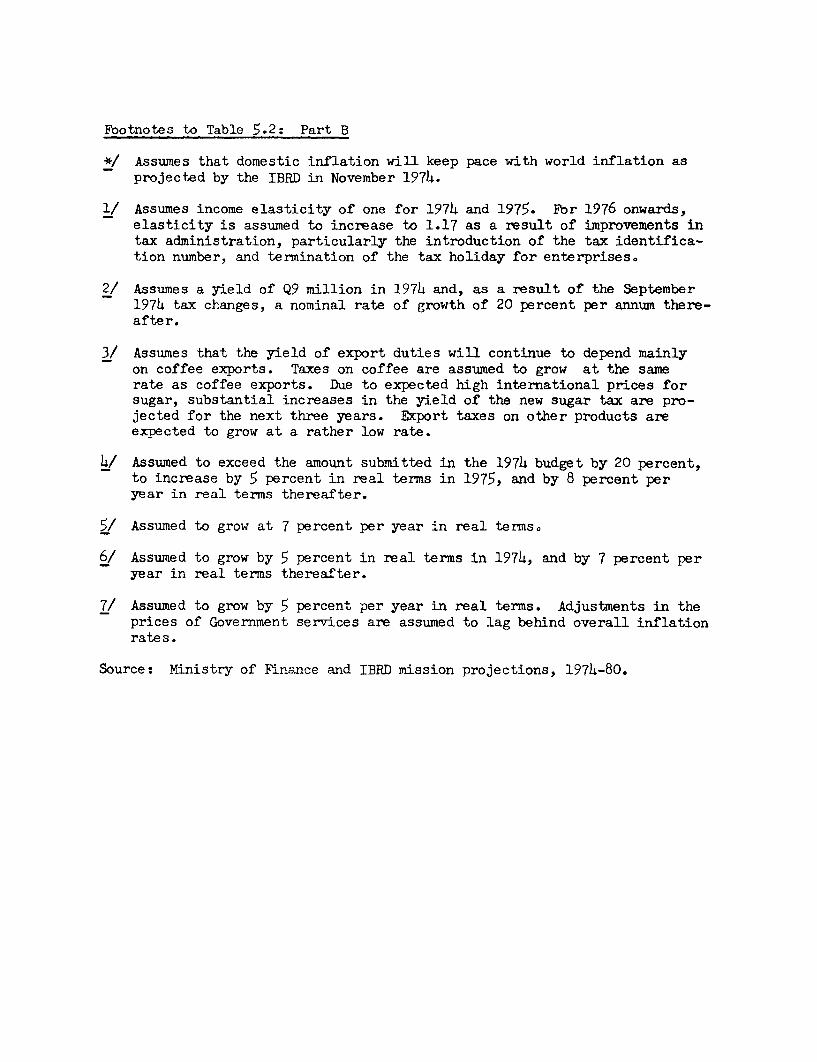

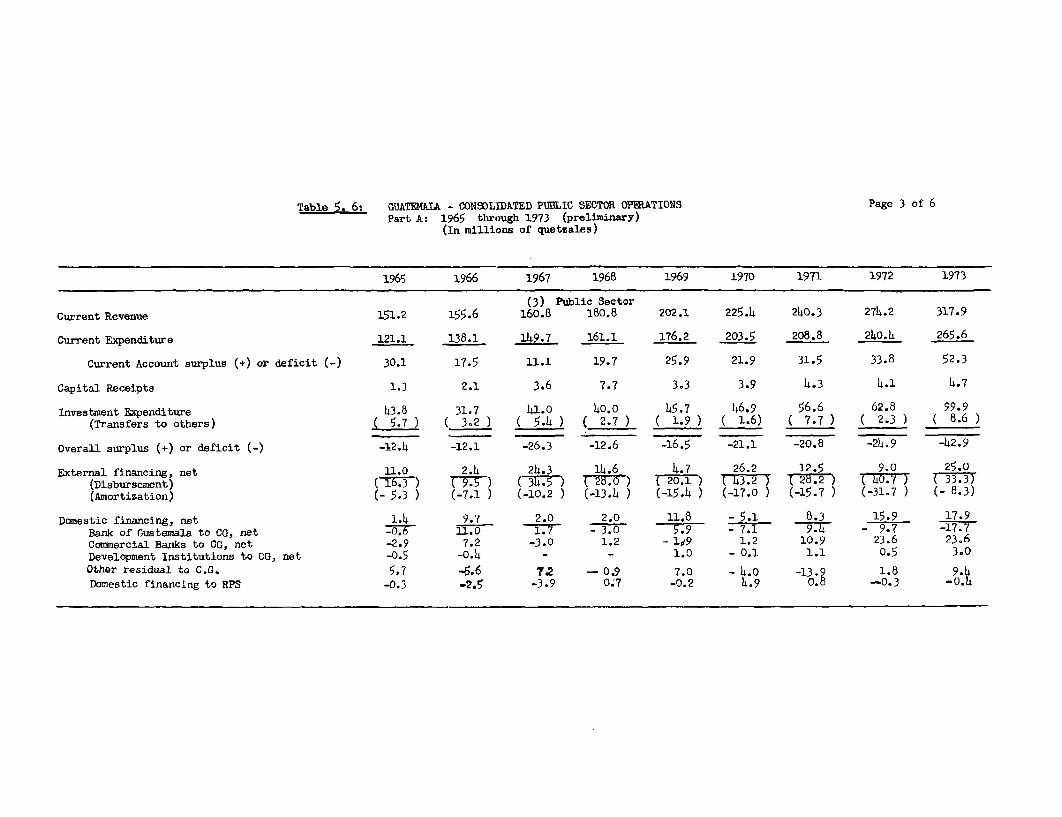

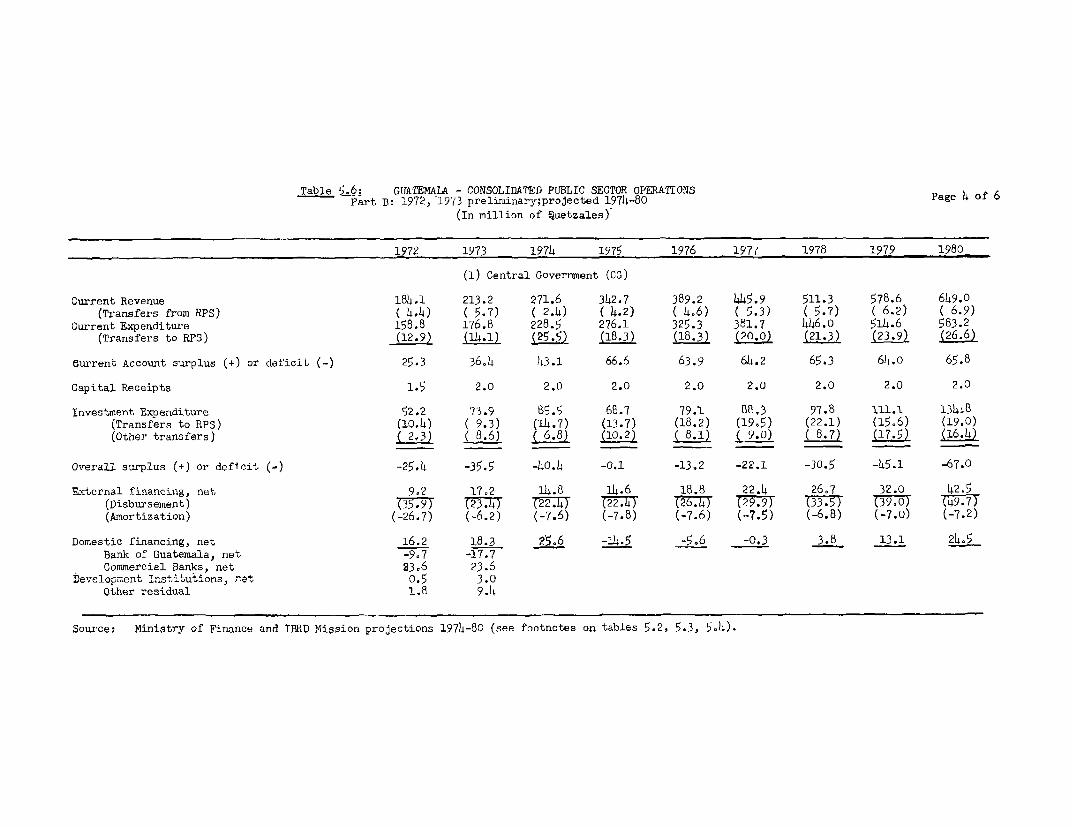

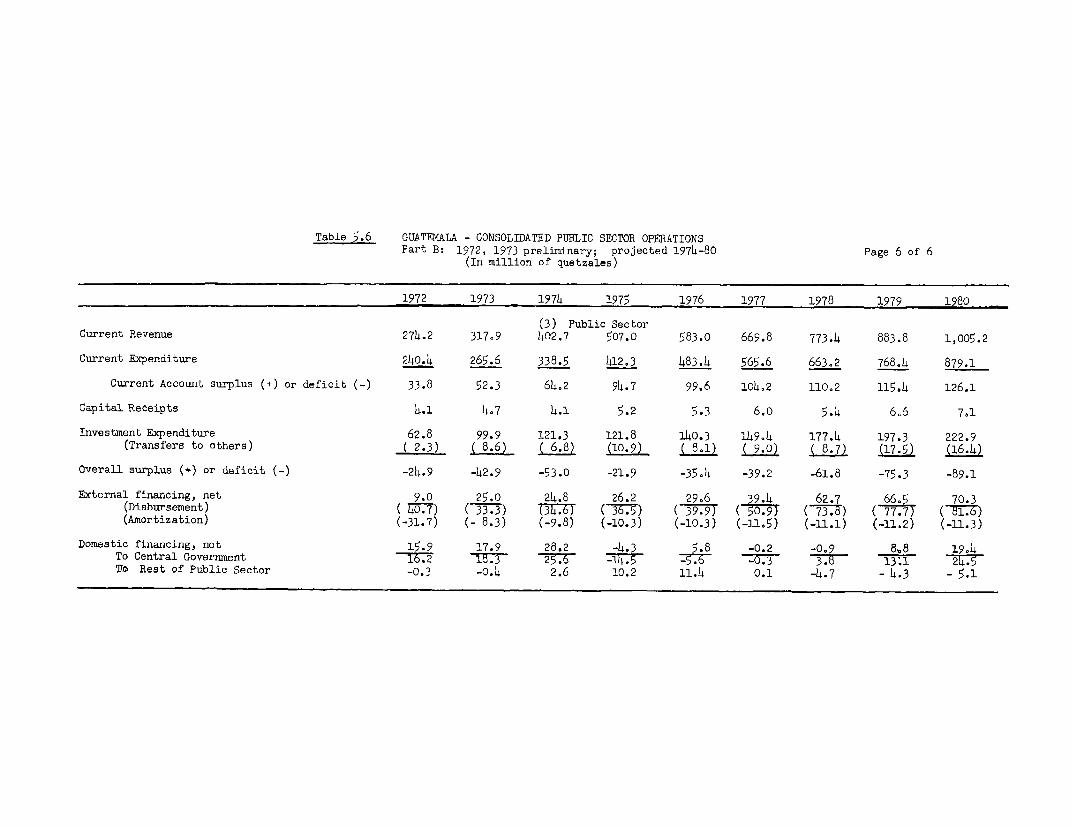

1[. Although Guatemala's public sector participation in GDP has increasedduring the last eight years, it still remains at a very low level. Duringthis period GDP in current terms grew at an average rgte of 8.2 percent perannum, while public sector current revenue grew at about 10 percent per annumand current expenditure at a slightly lower rate. This expansion of publicsector operations was due to the creation of new public entities and therapid development of some public utilities already in existence.. The averageannual rate of growth of public investment expenditure during the periodexceeded 11 percent. As there was only a modest increase in current savings,the overall deficit of the public sector increased by about 9.7 percent per

- 6 -

annum on the average, attaining a level of 1.2 percent of GDP in 1973.

A. Central Government

15. Guatemala's management of fiscal affairs has had remarkablesuccess in achieving internal stability through conservative budget han-dling. This stability, however, has been attained at very low levels ofrevenue and expenditure. During the fifties and up to 1958, Central Govern-ment current revenue stood at about 9.4 percent of GDP, dropping to about8.5 percent in 1959-60 due to a reduction in tax collections on externaltrade. During these years coffee prices declined steeply and imports weresignificantly depressed. This declining trend in fiscal revenues continuedfor the first three years of the sixties because of further deterioration ofthe external sector and the introduction of tax exemptions under the CentralAmerican Common Market. The ratio of Government revenues to GDP fell to 7.6percent during this period. Tax measures taken in subsequent years succeededin raising this ratio to about 8.5 percent of GDP, a level which was maintained

Table 3: PUBLIC SECTOR SUMMARY OPERATIONS 1/(Main items as a percent of GDP)

965-67 1968-70 l971 1972 1973

Current Revenue 11.2 11.6 12.1 13.0. 12.3(Central Government) (6.7) (6.5) (6.7) (b.b) (b.2)

Current Expenditure 9.8 10.3 10.5 11.4 10.3(Central Government) (7Mb) (7.6) (7.4) (7.6) (6.5)

Savings 1.h 1.3 1.6 1.6 2.0(Central Government) (0.9) (0.9) (1.3) (1.2) (1.h)

Investment 2.6 2.5 2.9 3.0 3.9(Central Government) (2.2) (1.6) (1.7) (2.5) (2.9)

Deficit Financing -1.2 -1.0 -1.0 -1.2 -1.7(Central Government) (-1.2) (-o.6) (-0.4) (-1.2) (-1.4)

1/ Total public sector figures are net of transfers.

Source: Appendix tables 2.2 and 5.6; components may not add up because ofrounding off and the exclusion of capital receipts.

- 7 -

until 1972. The traditional policy has been to adjust total expenditures tothe revenues available. Guatemala's various administrations have frequentlyresorted to austere measures to keep the deficit to very low levels. Since1959 the overall Central Government deficit has never exceeded 1.8 percentof GDP and has averaged only about 1.0 percent.

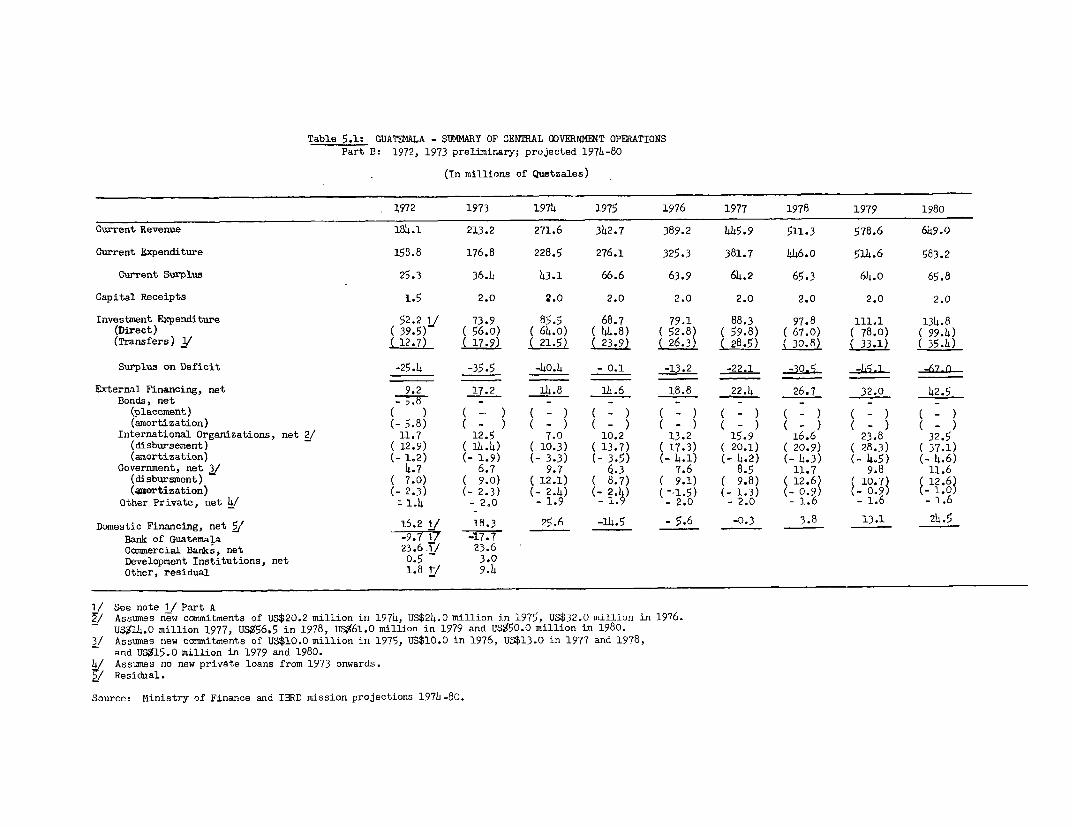

16. The administration that left office in July 1974 relied mainly onadministrative reforms to increase current revenue. Although some improvementswere made, the overall impact was limited. On the expenditure side the Govern-ment had adopted an ambitious development program for 1971-75. A necessaryprecondition for the implementation of the program, however, was the creationand reorganization of public sector entities, a task to which the Governmentgave high priority in 1971-72. In 1972-73 Central Government investmentexpenditures increased substantially.

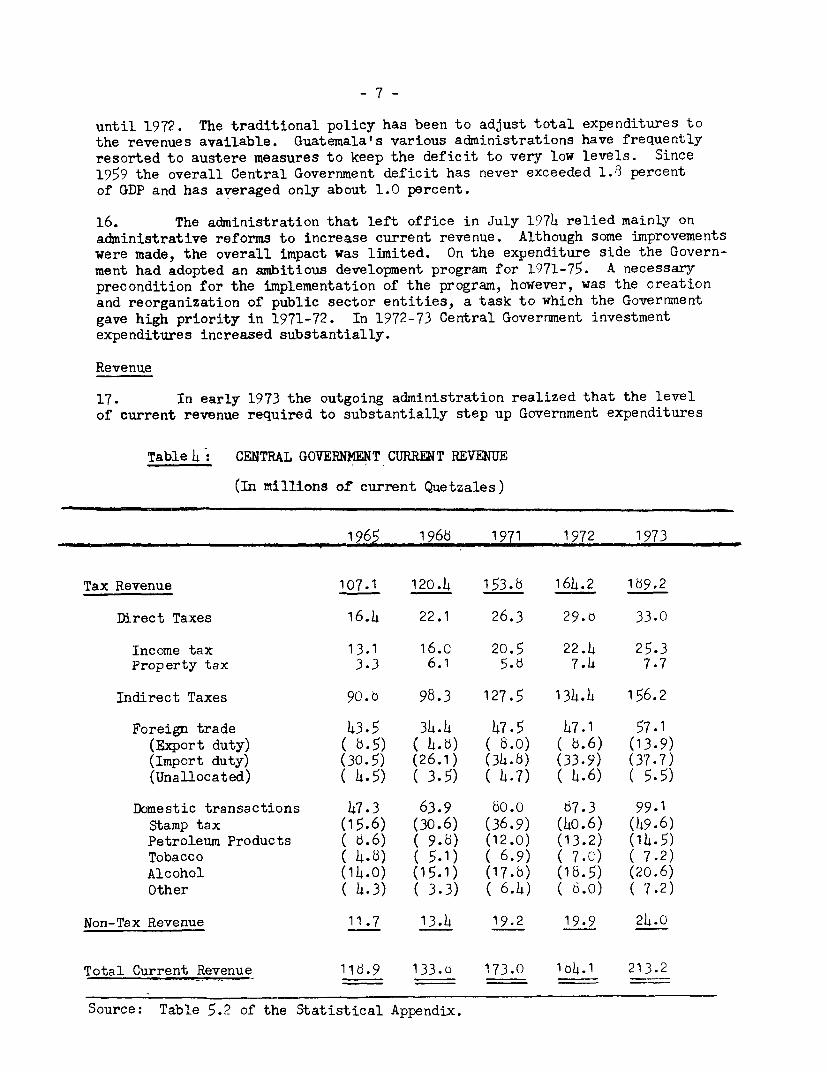

Revenue

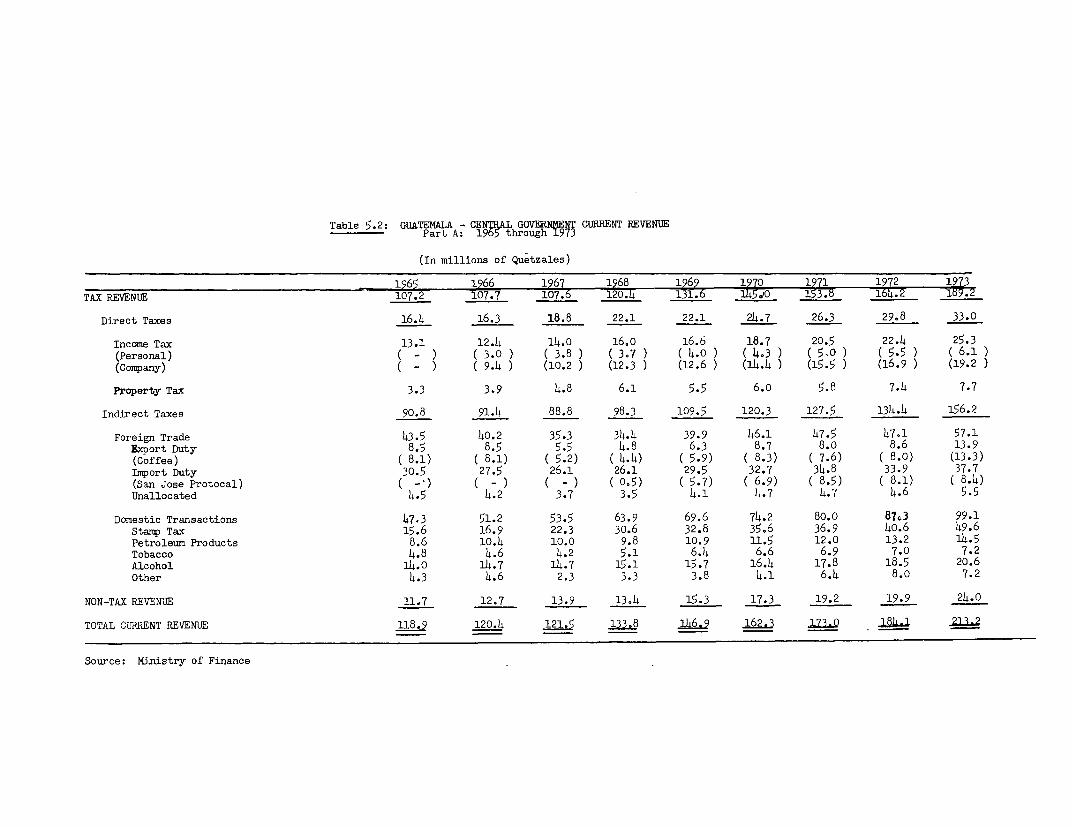

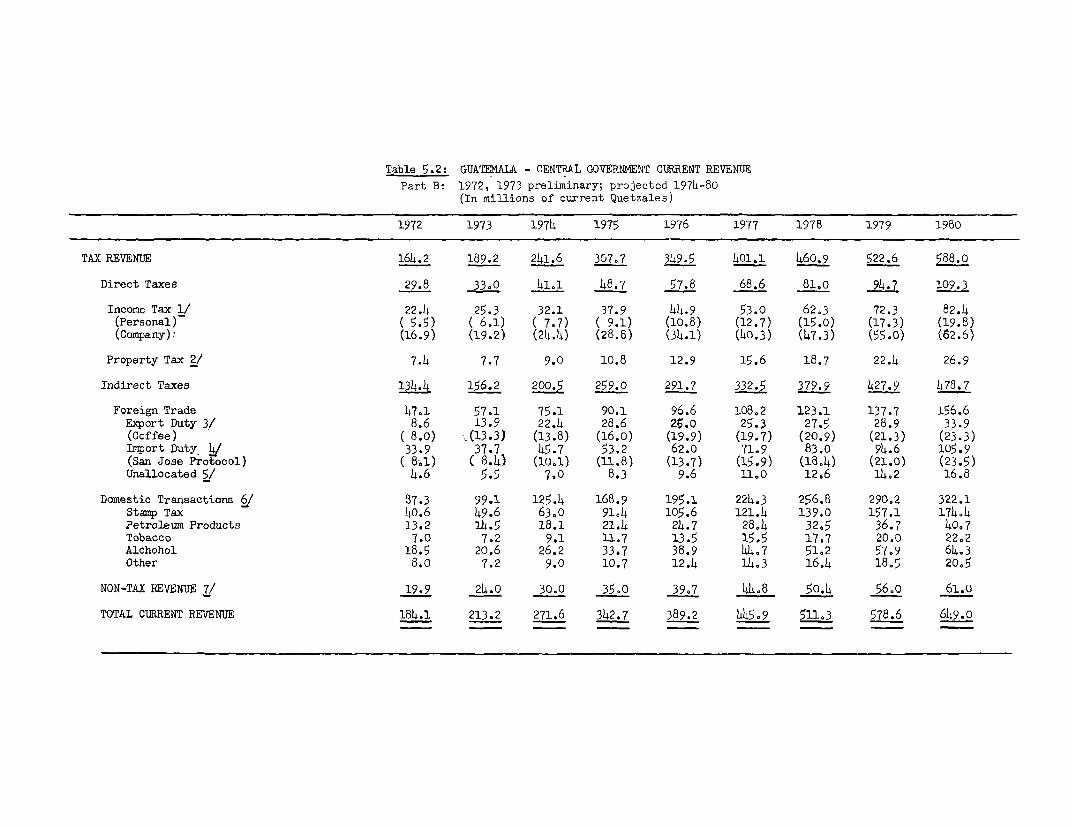

17. In early 1973 the outgoing administration realized that the levelof current revenue required to substantially step up Government expenditures

Table 4 CENTRAL GOVERNMENT CURRENT REVENUE

(In millions of current Quetzales)

1965 1965 1971 1972 1973

Tax Revenue 107.1 120.4 153.8 164.2 169.2

Direct Taxes 16.4 22.1 26.3 29.d 33.0

Income tax 13.1 16.c 20.5 22.4 25.3Property tax 3.3 6.1 5.o 7.4 7.7

Indirect Taxes 90.6 98.3 127.5 134.4 156.2

Foreign trade 43.5 34.4 47.5 47.1 57.1(Export duty) ( 5.5) ( 4.b) ( 6.0) ( 5.6) (13.9)(Import duty) (30.5) (26.1) (34.8) (33.9) (37.7)(Unallocated) 4 4.5) ( 3.5) ( 4.7) ( 4.6) ( 5.5)

Domestic transactions 47.3 63.9 80.0 67.3 99.1Stamp tax (15.6) (30.6) (36.9) (40.6) (49.6)Petroleum Products ( 6.6) ( 9.5) (12.0) (13.2) (14.5)Tobacco ( 4-8) ( 5.1) ( 6.9) ( 7.c) ( 7.2)Alcohol (14.0) (15.1) (17.5) (18.5) (20.6)Other ( 4.3) ( 3.3) ( 6.4) ( 6.o) ( 7.2)

Non-Tax Revenue 11.7 13.4 19.2 19.9 24.0

Total Current Revenue 118.9 133.o 173.0 104.1 213.2

Source: Table 5.2 of the Statistical Appendix.

- 8 -

while maintaining stability could not be attained through administrative im-provements alone. However, the proximity of the presidential election(March L974) made the introduction of new taxes politically difficult at thattime.

18. While no new taxes were introduced during 1973, tax administrationimprovements yielded positive results. The number of tax returns auditedincreased by 43 percent, with efforts concentrated on the larger taxpayers, and12,143 new properties were entered in the tax records. Although the number ofnotices to delinquent taxpayers was reduced from 19,000 in 1972 to about 3,000in 1973, the contacts in the latter year were in the form of personal visitsby tax inspectors rather than letters sent through the mail as in the previousyear. The yield on account of tax penalties increased by more than 3h0 percent.A new sales tax auditing team was organized at the beginning of 197h. Thisteam has been visiting the interior resulting in substantial benefits forthe internal service. There are still, however, two important measureswhich need to be implemented: the use of tax identification numbers and thecompletion of property identification on the Pacific Coast.

19. In October 1973, the Goverrment extended for two years the importduty exemption on raw materials for the industries included in the Common Market4greement, and whose initial 10-year exemption period had expired. It is expectedthat the authorities will continue extending the deadlines until the GeneralAgreement being sought in the fiscal area, as part of the restructuring of theCommon Market, is completed. It is estimated that if the Government were toeliminate import duty exemptions, most of which are attributable to the CommonMarket Agreement, it could more than double import duty collections.

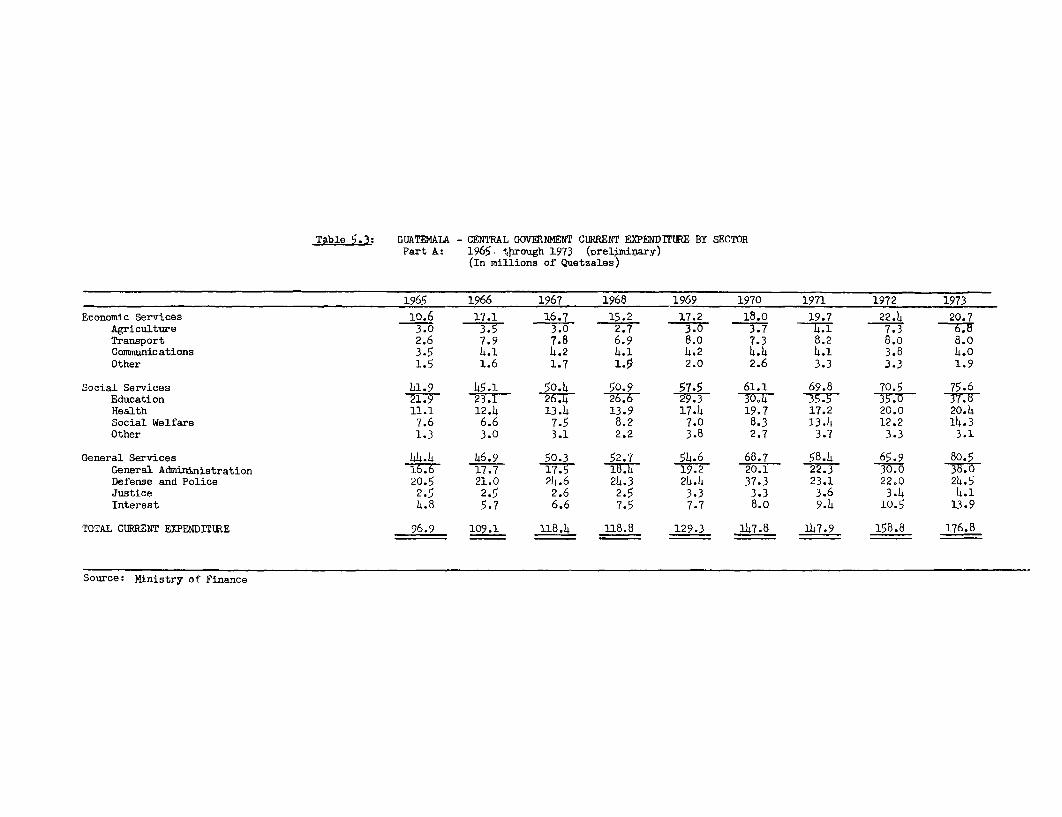

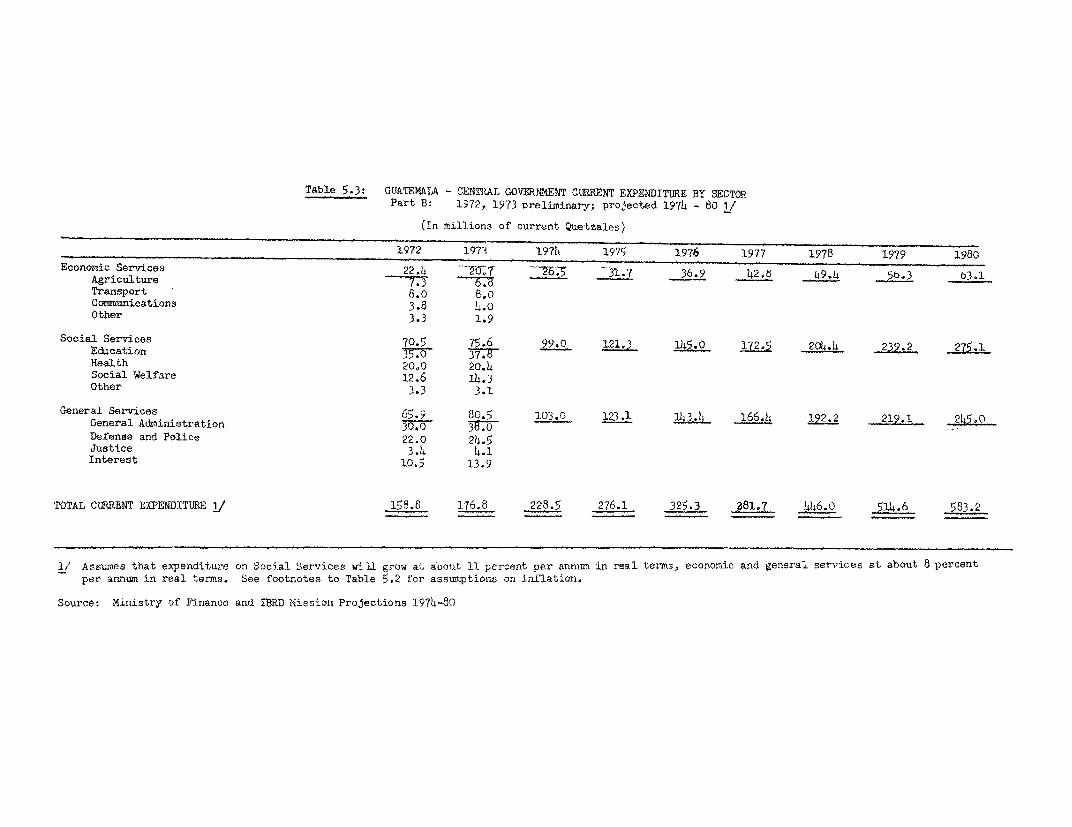

Current Expenditure

20. Central Government current expenditures during 1965-73 have grownat a lower rate than GDP. The structure of these expenditures in general hasregistered only minor variations during the period. Between 1965 and 1972,expenditures on social services grew at a faster rate than general services. In1973, however, expenditures on general services increased sharply, and theirshare in total expenditures returned to its 1965 level.

21. Given the degree and extension of poverty in the country, andparticularly in rural areas, the low level of current expenditure is clearly in-adequate to meet the needs of the population. An expansion of current expend-itures in health and education is urgently needed. Moreover, the levels ofGovernment investment in 1972-73 and those projected for future years, particular-ly in the social areas, will demand substantial increases in the Government'scurrent expenditures.

Table5 : CENTRAL GOVERYIENT CURRENTEXPENDITURE PER HEAD

(In current Quetzales)

1965 1968 1971 1972 1973

Economic Services 2.4 3.2 3.9 4.4 4.0

Social Services 9.6 10.9 14.0 13.8 14.5Education 57. -777 7.1 -h79 7.3Health 2.5 3.0 3.5 3.9 3.9Social Welfare 2.1 2.2 3.h 3.u 3.3

General Services 1Lc.1 11.3 11.7 12.9 15.4General Administration 37 3.9 T7§ 5.9 7.3Defense and Police 1.7 5.2 h.6 1.3 4.7Other 1.6 2.1 2.6 2.7 3.4

TOTAL 22.1 25.4 29.6 31.1 33.9

Source: Table 5.3 of the Statistical Appendix.

Investment Expenditures

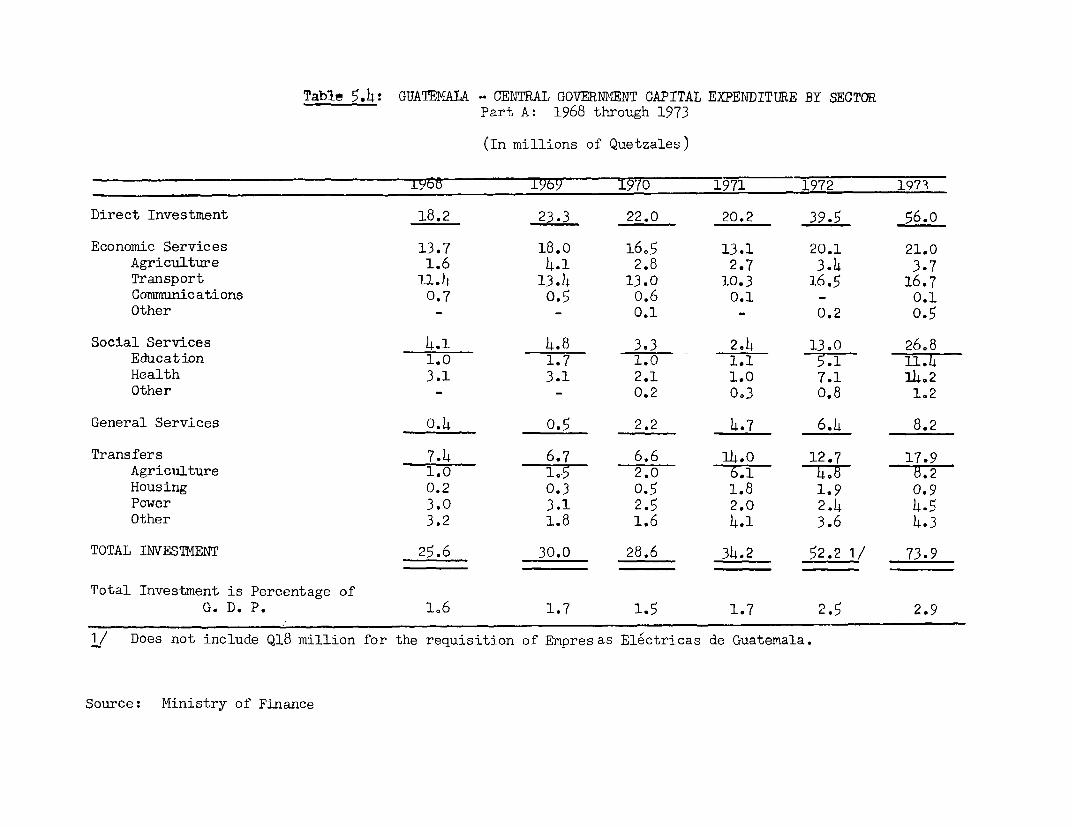

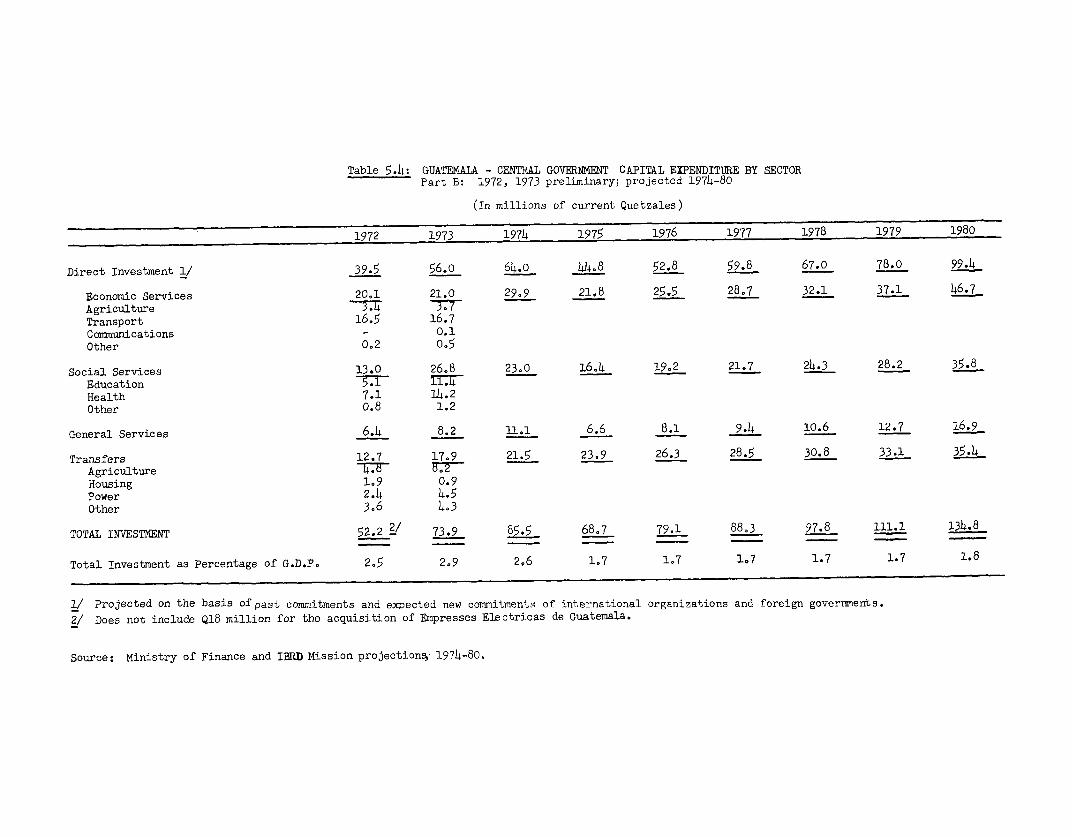

22. Central Government investment expenditures grew at about the samerate as GDP from 1968 to 1971 with their share in product remaining at about 1.6percent. With the beginning of the implementation of the 1971-75 EconomicDevelopment Plan,investment expenditures increased from Q34 million in 1971 toQ74 million in 1973. Investment grew in almost every area. However, the mostimpressive development was registered in the social services, where annual averageinvestment expenditures rose from an annual average of a!out Q3.7 million in1968-71 to nearly Q20 million in 1972-73. These expenditures were concentratedon education and health. In terms of share in Government investment, transportcontinues to be the leading sector due to a large extent to the broad technicalcapacity and experience in project preparation and administration prevailing inthe sector.

23. The major obstacle to the growth of investment has been the limitedcapacity in project preparation. The situation does not seem to have improvedin any significant manner in recent years. However, new efforts are being made

- 10- -

Table 6: GENrRAL GOVERNMENT INVESTMENT EXPENDITURE

( In million of current Quetzales )

1968 1969 1970 1971 1972 1973

Direct Investment 18.2 23.3 22.C 20.2 39.5 56.o

Agriculture 1.6 4.1 2.b 2.7 3.4 3.7Transport 11.4 13.4 13.0 10.3 16.5 16.7Communications 0.7 0.5 o.6 0.1 - C.1Education 1.0 1.7 1.0 1.1 5.1 11.4Health 3.1 3.1 2.1 1.C 7.1 14.2Other (.4 0.5 2.5 5.0 7.4 9.9

Transfers 7.4 6.7 6.6 14.0 12.7 17.9

TOTAL 25.6 30.0 28.6 34.2 52.2 73.9

Source: Table 5.4 of the Statistical Appendix.

to step up project preparation with technical aesistance from IDB and other inter-national agencies.

2h. The Government which took office in July 1974, is preparing a neweconomic development plan, and expects to complete it by mid - 1975. The authoritiesintend to give a high priority to investments in energy and agriculture (especiallyin the construction of feeder roads and provision of agricultural credit). Itis expected that investment in the social sectors will continue to grow and thattourism will receive special attention.

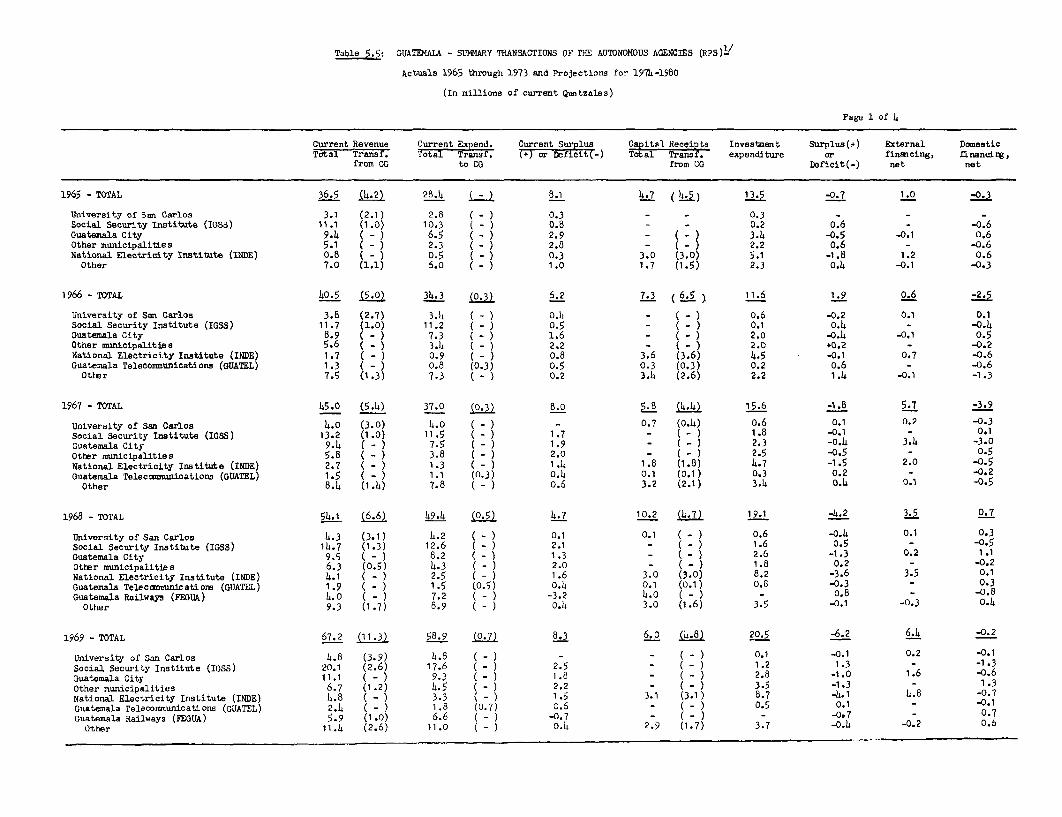

B. Rest of the Public Sector

25. The decentralized public sector 1/ has a rather limited role in thedevelopment of most sectors of the Guatemalan economy. This situation can beexplained by either one of two reasons: the autonomous entities are of too smalla size to have any measurable overall impact, or they operate as self-containedenclaves.

1/ Excluding banks and other financial institutions.

26. Electricity. An exception to the above-described situation isfound in the field of electricity, where two public institutions form the back-bone of the sector and are key determinants in Guatemala's economic development:the National Electricity Institute (INDE), which is mainly responsible forgenerating electricity, and the Guatemala Electricity Enterprise (EEG), whichalthough generating some of the electricity consumed in western Guatemala, ismainly responsible for electricity distribution. The latter enterprise, formerlyprivate, was acquired by the GuatemalanGovernment in 1972 (96 percent of theshares amounting to Q1-8 million were financed through a bond issue). Seriousproblems have arisen as a result of the low price charged by INDE to EEG on thesale of electricity, although this situation improved in September 1974 whena new contract with a price adjustment clause for changes in the price of oilinputs was signed between the two entities. Simultaneously, electricity tariffscharged to consumers were adjusted upwards to cover the increase in oil prices.The impact of these tariff increases on INDE's financial rate of return arepresently under study.

27. In 1973, the two enterprises generated 82h.3 million 1WH of elec-tricity ( a very small additional amount was privately generated), only slightlymore than one-third was hydro-electricity. The fuel cost for the enterprisesaccounted for about 15 percent of Guatemala's imports of oil products in 1973.With electricity demand growing at 10-12 percent per year and new projects forhydro or geothermal generating expansion in only a very early stage of prepara-tion, the volume of oil products import will have to grow by over 15 percentper year in the next two to three years. Moreover, if no early decision ismade in relation to the interconnection with El Salvador or other plans forincreasing generating capacity by 1976, the shortage of electricity may becomea bottleneck to the country's economic expansion. By the early 1980's the hydrc-electric plant on the Chixoy River, for which financing by IBRD and otherexternal lenders is being sought, should meet the increased demand. Thus theproblem which requires prompt resolution is how to cope with demand in theinterim period. Tentatively, investment for the period 197h-80 has been project-ed at about Q160 million, of which more than 50 percent could be financedinternally.

28. All expansion of generating capacity will be handled by INDE. Sub-stantial financial foreign assistance will be required in this endeavor. Withregard to EEG, an investment plan for expanding electricity distribution hasbeen prepared for 197h-78, which assumes that INDE will plan on new generatingunits for 1976. Investment projected at Q2.7 million in 1974 will graduallygrow to Q3.9 million in 1978. The substantial current surpluses the enterprisegenerates should cover all or a major portion of its investment expenditures inyears to come.

29. Transport. The bulk of public investment in the transport sectoris used for the road network, and is handled by the Central Government. Thisinvestment has traditionally been allotted the highest -- although declining --

- 12 -

share of the Government's direct investment. A fairly ambitious road invest-ment program has been designed for 197h-75, but considerable slippages can beexpected. The longer term plan is being prepared at present.

30. The four most important decentralized public entities in thetransport sector are: the railway (FEGUA), the airline (AVIATECA), the portauthority of Santo Tomas on the Atlantic, and the port authority of Champericoon the Pacific. The two former enterprises have traditionally run deficitsimposing a heavy burden on the Government's budget, while the two latter entitieshave generated profits which throughout the 1970's have allowed internal financingof their investments.

31. FEGUA, an enterprise formely owned by an American firm, was takenover by the Guatemalan Government in 1968. After the takeover, FEGUA continuedto run an operational deficit, using obsolete equipment and a staff which farexceeded requirements. Finally, in 1974 the Government decided to supply FEGUAwith the necessary resources to reduce personnel. The total cost of retirementand severance payments, with a reduction in the staff of approximately 45 per-cent, was Q9.5 million. This money was derived from a Government bond issue.The total bond issue amounted to Q15.0 million, with the remainder being allocatedto the renewal of equipment. The oil-steam engines are to be removed from usebecause they consume many times more fueL per mile than the diesel engines.Moreover, contracts for tariffs for cargo on concessionary terms were rescindedin May, thus increasing the average tariffs. With these changes, it is expectedthat at least the operational deficit may be considerably reduced or even eliminatedby 1975. The specific investment program for FEGUA is presently being preparedby the Planning Office.

32. AVIATECA has considerably improved its position with regard to inter-national flights in 1973 and 197h. The improvement is due in part to restric-tions imposed on foreign airlines transporting passengers to and from Guatemala.The overall operational deficit may be eliminated this year; however, the Gov-ernment intends to transform the entity into a mixed enterprise with privatesector participation in the near future. Thus, no long-term investment plansare available for the airline.

33. The Santo Tomas port is managed strictly as a commercial enterprise,deriving its revenue from fees for ship servicing, cargo handling, and storage.The enterprise generates considerable surpluses after depreciation, of which25 percent is transferred to the Central Government budget. The port handlescargo to and from Guatemala and transit cargo of neighboring countries. Atpresent two warehouses are being constructed and new investments for expansionand improvements are contemplated for the coming years at a total cost ofQ18 million. Foreign financial assistance will be needed.

3ht. The port of Champerico on the Pacific is at present awaiting adecision on the construction of a new port. At this time, only minor invest-ments financed from current surpluses are planned for Champerico for the nexttwo to three years. If the new port now under discussion for the Pacific coastis either withdrawn from the public investment plan or postponed, additionalinvestments will be required for Champerico.

- 13 -

35. Telecommunications. The Guatemalan telecommunications agency,GUATEL, is a public enterPriSe in charge of national and internationalcommunications. It also owns and operates the Guatemala section of theCentral American regional microwave network. Although the telephone networkhas been expanding in recent years with Bank assistance, Guatemala stillhas the next-to-lowest telephone density among the Central American countries- 0.77 per 100 people. GUATEL has a fairly ambitious expansion program withannual investments of about Q17 million per year for the next five years ascompared with Q3.2 million per year in 1970-7h. The bulk of the foreignexchange resources needed are expected to be supplied by IBRD and CABEI.GUATEL, being operated on a profit basis, will be able to finance the totalor at least a major part of the local component of its investment frominternally generated cash.

36. Agriculture. The National Institute for Agrarian Reform (INTA)plays a major role in the colonization efforts of the decentralized agricul-tural public sector. The main responsibility of this institute at presentis the issuance of property titles to new "colonos", which enable themto obtain credit from BANDESA and the services of the National Institutefor Agricultural Commerce (INDECA). It appears that there has been a slow-down in the establishment of new colonies, with efforts being concentratedon the consolidation of existing ones. The entity derives its revenues forcurrent expenditures mainly from budgetary transfers. The earmarked taxon idle land and other nontax revenue weigh only marginally in total revenues.Amortization payments on the sale of public land and additional Governmenttransfers account for total capital revenues. Investment expenditures,which have been fairly modest in recent years, are related to the implementa-tion of colonization schemes. In addition to the above-described functions,INTA is in charge of the management of some cooperative farms. Up to theagriculture year 1969-70 INTA had generated a deficit in this endeavor. Sub-sequently, increasing although still modest surpluses have resulted. (Theoperating results of cooperative farming, basically private in nature, havenot been included in INTA's revenue and expenditure projections).

37. INDECA, the public entity in charge of basic grains stabilizationprograms, acts as a marketing board for these grains. It finances itsadministrative expenditures from Central Government transfers and its invest-ment expenditures from additional Government transfers and foreign loans.The major investment program being carried out at present is the constructionof silos, both for the entity itself and for cooperatives. In 197h-80, theentity is projected to invest between Q3 and Qh million a year in the construc-tion of silos, cold storage facilities and warehouses. Additional foreignresources besides those already committed by AID and CABEI may be requested.The role of INDECA in the development of agriculture is projected to increasein importance when its operations become better coordinated with those of theMinistry of Agriculture and BANDESA. The accounts for INDECA do not includethe results of the purchase and sale of grains for which the Government assignsspecific subsidies.

- 14 -

38. A major public development in the rural sector is being under-taken by the Peten Development Enterprise (FYDEP). This is a typical enclavein the economy. It started with the sale of public land under very favorableprice and timing conditions. Eligibility for the purchase of public landwas determined solely on the basis of the potential buyer's financial capacityto clear and exploit the land; there was no limit on the size of the plot.The population of the area, which was 30,000 five years ago, is estimatedat 100,000 at present; a number of large farms have been established as wellas 27 cooperatives with a total of about 10,000 smaller farmers on plotsaveraging about 45 ha. The enterprise derives its current revenues from asmall transfer from the budget and charges made to chicle and pepper exploita-tion concessions. Capital revenues are obtained from the budget and fromthe sale of land. The entity generally builds its own roads, schools, healthcenters, etc. and appears to have only marginal connections with either theCentral Government or other public sector agencies. With abundant unopenedpublic land in the area, further expansion of FYDEP activities is expectedin future years.

39. Tlhe entities described above are the three most important in theagricultural decentralized public sector excluding financial institutions.Other agencies of minor importance are included under the heading "Other"in Table 5.5. Their investments are only of marginal nature.

LO. Municipalities. The rapid growth of Guatemala City has meantthat revenues and expen ures of the capital city have consistently exceededthose of all other municipalities in the country put together. The sourcesof municipal revenues are basically municipal taxes and license fees; inaddition, some small municipalities receive support from the Central Govern-ment budget. Investment expenditures are financed through current surpluses andexternal and internal borrowing. INFOM (Institute for Municipal Development)was created for the purpose of assisting in the development of municipalitiesexcluding Guatemala City. Considerable municipal investment has been financedthrough soft loans granted by INFOM with funds derived partly from loans bythe IDB. The rate of loan recovery of INFOM has been extremely high and oper-ations are expanding rapidly. Investment in Guatemala City exceeds the amountin the municipal budget because one of the most important projects, city watersupply, is being carried out by the Ministry of Public Works. Consideringthe process of industrialization and the fact that urban population is growingfaster than rural, investment expenditure of the municipalities will have toexpand at a rapid pace.

41. Although INGUAT (Guatemalan Tourism Institute) is not directlyrelated to municipal or urban development, its main investment project isthe development of the Tikal tourist complex. This project, which is expectedto receive CABEI and IDB financing, contemplates, in addition to forestclearing and restoration and maintenance of the Tikal Mayan ruins, the con-struction of a tourist resort on the northern part of Lake Peten Itza fromwhich excursions to the ruins -- 90 kms. from the lake -- would originate.The projected amoun s of external and Government resources for this projectwould appear to fa'li short of requirements if the development is to take placein a reasonable period of time (facilities are almost nonexistent at present).

- 15 -

The Tikal ruins are probably the most promising archeological attraction inCentral America. INGUAT could play a more aggresive role in planning tourismdevelopment in Guatemala and in devising policies to attract private invest-ment in the sector: tourism continues to be a potentially high foreign exchangeearner for Guatemala.

42. Social Security. The Guatemalan Social Security Institute (IGSS)services all civil servants and about three-fourths of the urban labor forceemployed in the private sector. The armed forces have their own social securityinstitute (IMP), whose income is less than 10 percent of that of the IGSS.The IGSS insures all its members against accidents, granting medical attentionin such cases, and paying disability pensions and life insurance. In addition,in the Guatemala Province only, the IGSS carries out a program of maternityservices and medical attention in case of sickness. Up to now, no unemploy-ment or retirement benefits are included in the institution's programs.

43. The sources of revenue of the IGSS are a 4 percent charge on allemployees' salaries, with 3 percent paid by the employer and 1 percent by theemployee under the accident program, and an additional charge for participantsin the sickness and maternity programs. The Central Government is obligatedto make an annual transfer from the budget over and above its contribution asemployer; however, this is seldom or never done and considerable arrears haveaccumulated on this account. Partly because of these Government arrearages,IGSS' ambitious program for hospital construction has lagged far behind schedule.In practice, the amount of annual investment is determined by the surplus oncurrent account of the institution. In the hospital investment program, verylittle coordination with the Ministry of Public Health has taken place,resulting in certain cases in duplication of medical facilities in particularareas and total neglect in others.

44. Other autonomous agencies. Of the remaining autonomous agencies,the University of San Carlos is the only important one in relation to typeand volume of operation. Other autonomous institutions deal with fire pro-tection, sports development, recreational facilities and similar activitiesinvolving only negligible investments. These agencies as well as the Univer-sity obtain an important share of their resources from the Central Governmentbudget. The University of San Carlos has received assistance for its invest-ment program from the IDB in the past -- the increasing demand for highereducation will require considerable expansion of budgetary allocations for theUniversity.

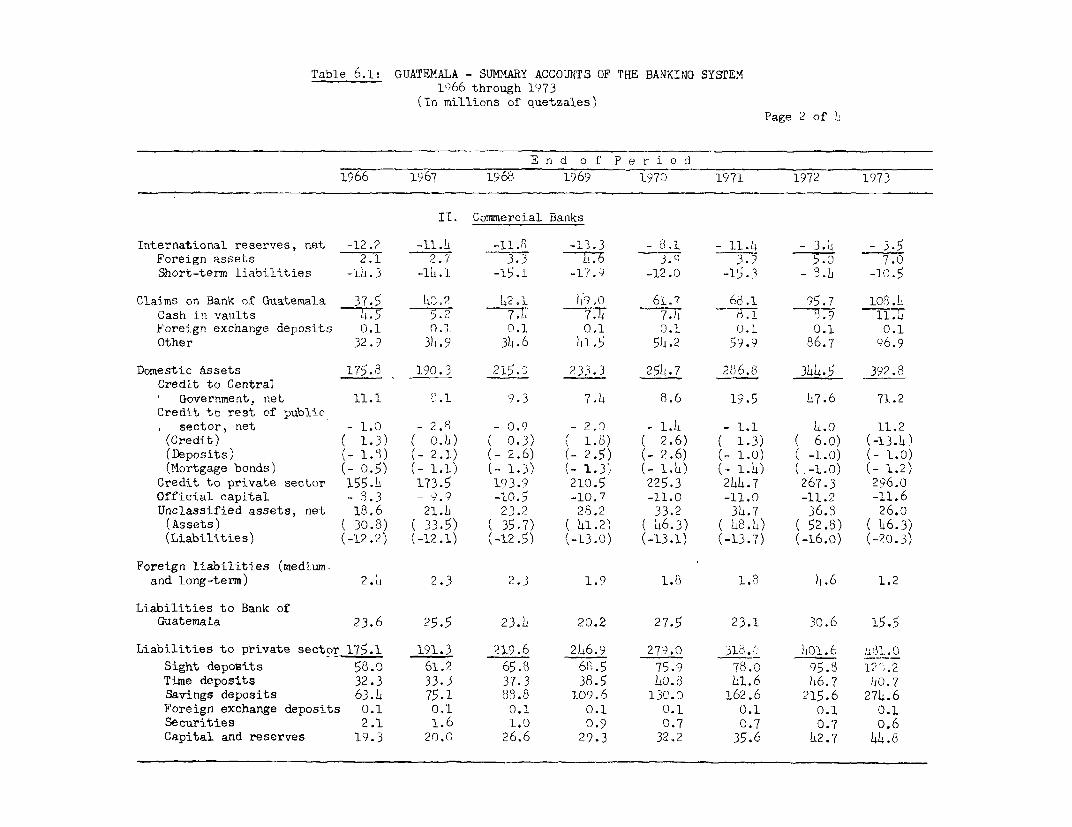

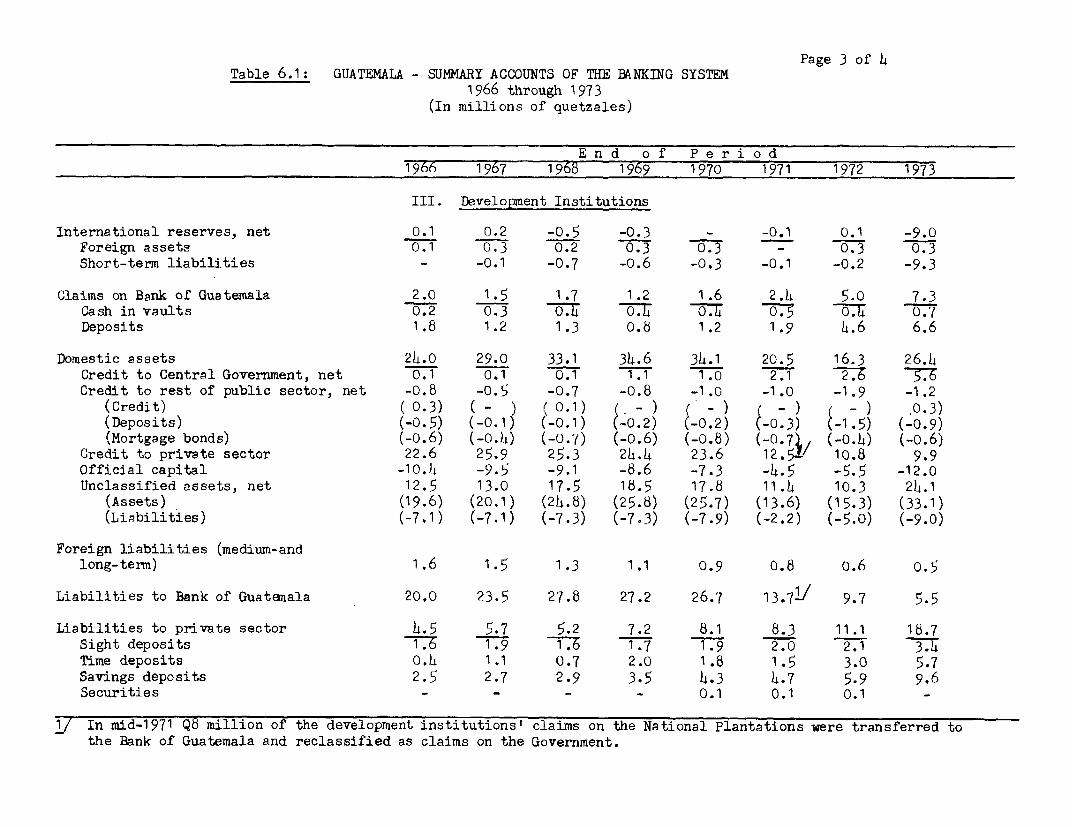

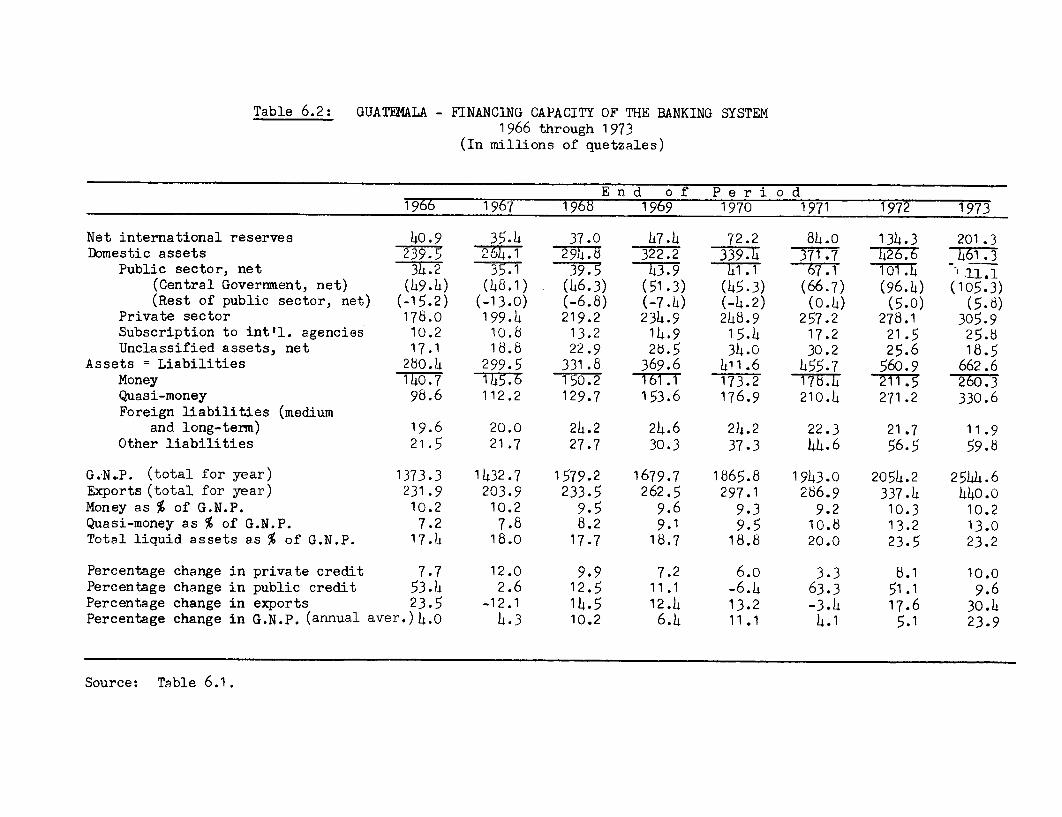

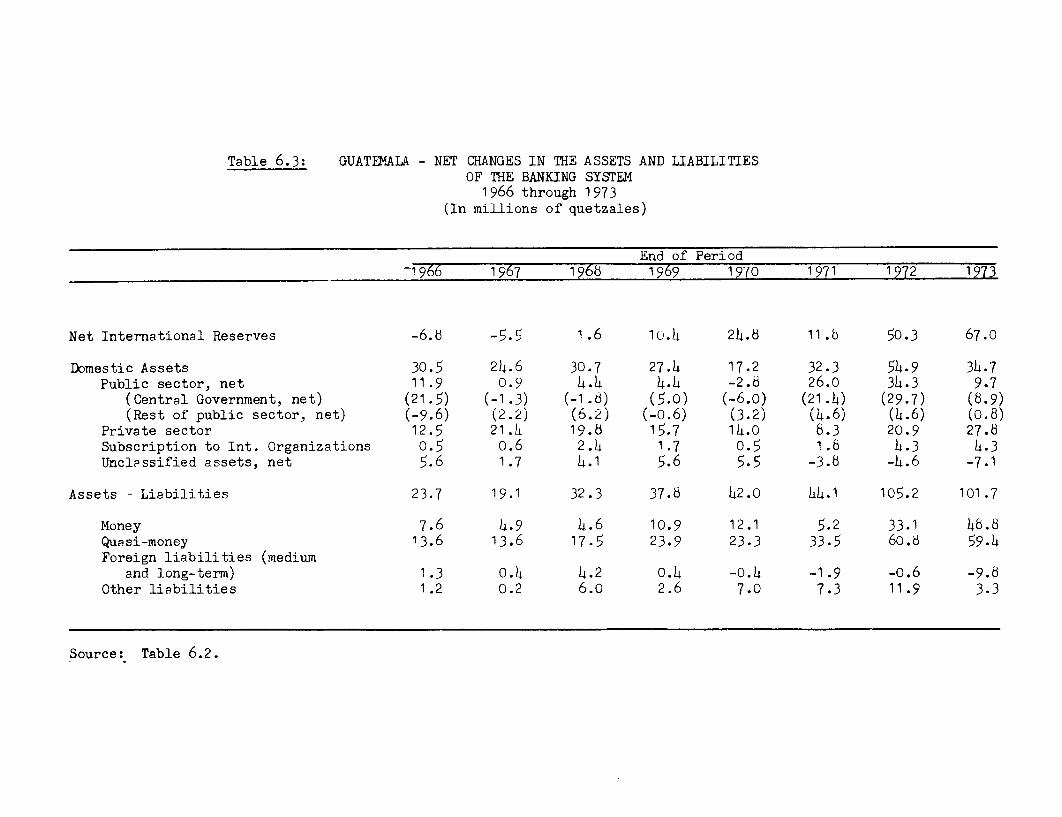

Chapter IV: MONEY AND BANKING

45. Guatemala has enjoyed many years of price and balance of paymentsstability. These results have been achieved to a large extent by conservativefiscal and monetary policies. However, while the balance of payments hascontinued to improve in the last few years, prices have been growing at unusuallyfast rates. Although fiscal policy has been more expansionary and monetary

- 16 -

policy looser mainly through lack of action, the factors behind the inflationarytrend stem basically from the external sector.

h6. Banking system liabilities grew at a faster rate than GNP duringthe period 1966-1973, especially in the laat two years -- the ratio of liquidassets to GNP increased from 20 percent in 1971 to more than 23 percent in 1973.While the money supply, defined as cash and sight deposits, has remained atabout the same percentage of GNP during the period 1966-73, savings and timedeposits grew at an average rate of more than 18.5 percent per annum, comparedto an average rate of 9.2 percent per annum for GNP. This substantial changein the banking system liabilities structure seems to have been encouraged by twomain forces: on one hand, the cash requirement ratio which allowed the banksto use a larger proportion of their quasi-money liabilities for lending purposes;and on the other hand, the lack of investment opportunities for investors, espe-cially farmers and small city capitalists. While the first factor must have beenthe main force up to 1971, the second consideration was undoubtedly responsiblefor the growth in the last two years. As a consequence of the change in struc-ture of the banking system liabilities, the effective average cash requirementratio for the commercial banks was reduced from 21.3 percent in 1966 to 17.3 per-cent in 1972. / The monetary authority modified the cash requirement ratio inAugust 1973, which helped bring the effective average rate up to 18.2 percentfor 1973. Y

b7. The rapid growth of banking system liabilities in 1972-73 was broughabout by the sizeable surplus on the balance of payments which produced anincrease in net international reserves of more than Q117.0 million. However,despite the large increase in deposits of more than 50 percent between 1971 and1973, the banking system's internal credit expanded at only a moderate rate.This caused banks to accumulate idle balances, forcing some of them to discouragethe public from increasing their deposits by reducing interest rates payed onsavings. 3/ While several commercial banks were to a certain extent limited bythe legal capital requirements,4/ only one bank requested authorization toincrease its capital. It appears that in most cases the banks were not readyto assume the higher risks involved in a more aggresive policy -- which wouldattract new customers.

1/ The requirements were 35 percent against sigh and sho'rt-term time deposits andundrawn balances on lines of credit, and 10 percent against long-term time andsavings.

2/ The new cash requirement rates effective after September 1, 1973 were 30 percentagainst sight and short-term time deposits and undrawn balances on lines ofcredit, and 15 percent against long-term time and saving deposits.

3/ Banks are not allowed to transfer abroad the financial resources collected inthe country.

Lj/ Banks are required to maintain their capital at a level equal to at least 5percent of bonds issued or guaranteed by the Government, 10 percent of allother loans and 50 percent of fixed assets.

- 17 -

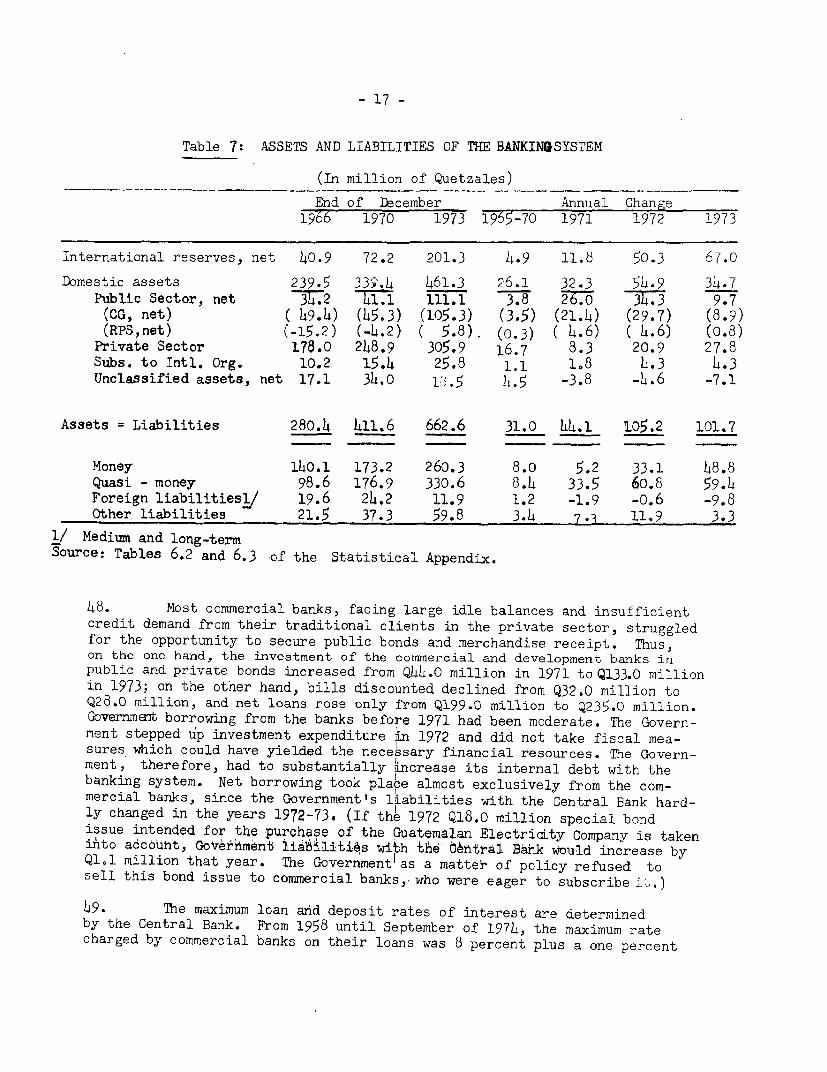

Table 7: ASSETS AND LIABILITIES OF THE BANKIN5SYSTEM

(In million of Quetzales)

End of December Annual Change1966 1970 1973 1955-70 1971 1972 1973

International reserves, net 40.9 72.2 201.3 4.9 11.8 50.3 67.0

Domestic assets 239.5 33;.4 461.3 26.1 32.3 54.9 34.7Public Sector, net 3 .2 -T.-1 111.1 3.8 3T 9.7(CG, net) ( 49.4) (45.3) (105.3) (3.5) (21.4) (29.7) (8.9)(RPS,net) (-15.2) (-4.2) ( 5.8). (0.3) ( 4.6) ( 4.6) (0.8)

Private Sector 178.0 248.9 305.9 16.7 3.3 20.9 27.8Subs. to Intl. Org. 10.2 15.4 25.8 1.1 1.8 4.3 4.3Unclassified assets, net 17.1 34.0 1,3.5 L.5 -3.8 -4.6 -7.1

Assets = Liabilities 280.4 411.6 662.6 31.0 44.1 105.2 101.7

Money 140.1 173.2 260.3 8.0 5.2 33.1 48.8Quasi - money 98.6 176.9 330.6 8.4 33.5 60.8 59.4Foreign liabilitiesl/ 19.6 24.2 11.9 1.2 -1.9 -o.6 -9.8Other liabilities 21.5 37.3 59.8 3.4 7.3 11.9 3.3

1/ Medium and long-termSource: Tables 6.2 and 6.3 of the Statistical Appendix.

48. Most commercial banks, facing large idle balances and insufficientcredit demand from their traditional clients in the private sector, struggledfor the opportunity to secure public bonds and merchandise receipt. Thus,on the one hand, the investment of the commercial and development banks inpublic and private bonds increased from Q44.0 million in 1971 to Q133.0 millionin 1973; on the other hand, bills discounted declined from Q32.0 million toQ28.0 million, and net loans rose only from Q199.0 million to Q235.0 million.Government borrowing from the banks before 1971 had been moderate. The Govern-ment stepped up investment expenditure in 1972 and did not take fiscal mea-sures which could have yielded the necessary financial resources. The Govern-ment, therefore, had to substantially increase its internal debt with thebanking system. Net borrowing took plalce almost exclusively from the com-mercial banks, since the Government's liabilities with the Central Bank hard-ly changed in the years 1972-73. (If thle 1972 Q18.0 million special bondissue intended for the -purchase of the Guatemalan Electricity Company is takeninto accOunt, Gov6iriment liaitilitihs with the C*nteal Bahk would increase byQl.l million that year. The Governmentlas a matter of policy refused tosell this bond issue to commercial banks, who were eager to subscribe --;.)

49. The maximum loan and deposit rates of interest are determinedby the Central Bank. From 1958 until September of 1974, the maximum ratecharged by commercial banks on their loans was 8 percent plus a one percent

- 18 -

commission; the maximum rate allowed to be paid on savings deposits was7 percent. The excess liquidity in the banking system created by theexternal sector has produced large variations in the rates of interestpaid on savings deposits. Thus, in early 1973 some banks reduced theirsavings rates from 6 percent, which was the standard for most banks, to4.5 percent and even 4 percent. The Industrial Bank -- a private organizationcreated by law --which was paying up to 6.5 percent on savings depositswas one of the few banks which did not alter its rate. This bank benefitsfrom an automatic capitalization, since its capital increases yearly bya contribution equivalent to 10 percent of the tax exemptions granted tomanufacturers under the Industrial Development Law. Thus, in order toobtain an acceptable yield on capital, the bank's management has to beaggressive in expanding operations.

50. The maintenance of a fixed rate of interest plus commission forlending operations tends to discriminate against medium-term loans. Ithas been more profitable for banks to lend at the shortest term possiblesince the effective rate increases due to the commission charged on loancontracts. The Central Bank estimates that in 1973, 90 percent of com-mercial bank loans were at less than one year. In addition, the mainte-nance of interest rates at substantially lower than world market levelsin the recent past, has encouraged the substitution of internal for ex-ternal credit, while in 1974 it also encouraged some capital flight.(However, investment opportunities had been very limited as well.)

51. The large increases in primary money through the balance of pay-ments surpluses in 1972-73 did not have a large expansionary effect onthe economy. This was a result mainly of the behavior of the banks them-selves in retaining large excess cash reserves. The expansionary fiscalpolicy, by reason of the small size of the public sector gave only moder-ate stimulus to monetary expansion. Even though there has been remarkablestability in the financial field, the experience of the last few years hasdemonstrated the need for the development of a system which would permitmore rapid and flexible excercise of the instruments of monetary control.Monetary measures were taken only late in 1974, when it was clear thatthe balance of payments was deteriorating and that inflation was continuingat a fast pace. The measures included, among others, raising interest ratesand cash requirerents for the banks.

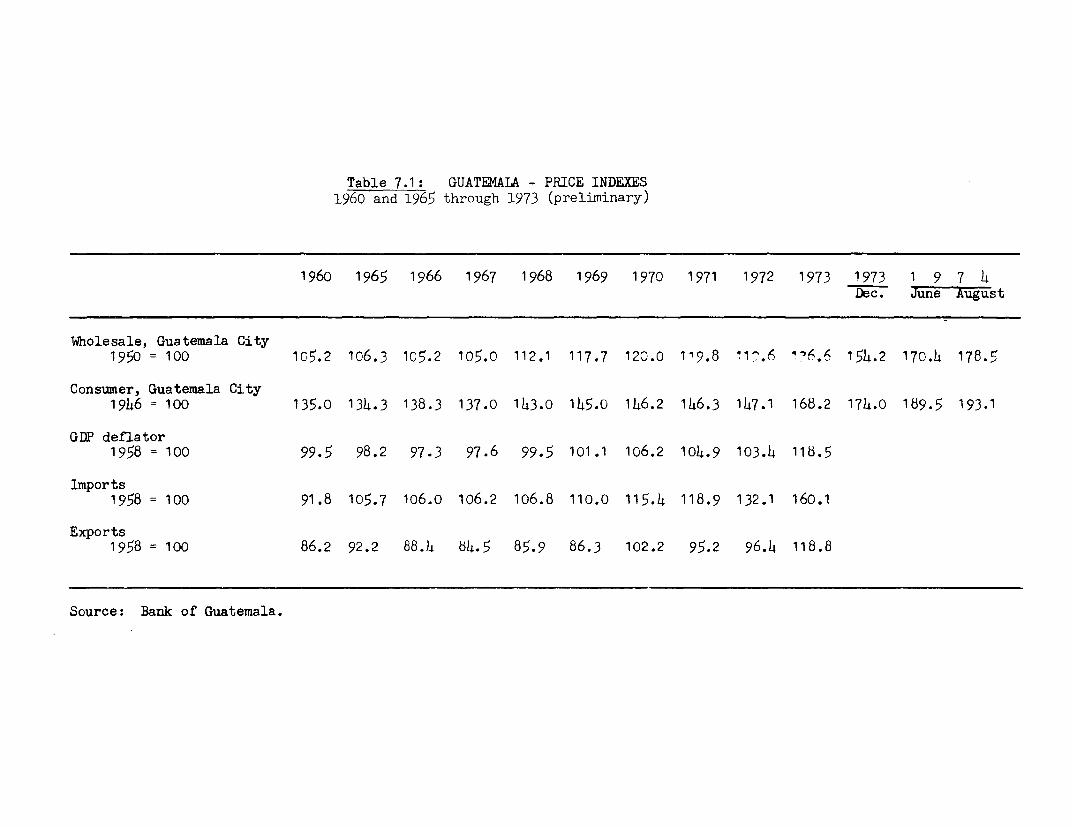

52. Statistics on prices, wages and salaries in Guatemala are weakand must be interpreted with caution. Guatemala has had a long traditionof price and exchange stability. During the period 1960-72 the averageannual price increase, measured by the GDP deflator, was 0.4 percent.Prices started to climb at the very beginning of 1973 when the first signsof basic grain5 sh6rtages app6gred. Th shortages were Pre6ipitated by thedrought that mainly affected grain-producing areas in the 1972 farmingseason. INDECA imports of the necessary grains to cover the deficit camerather late. At the same time in an open economy such as Guatemala's, theimprovement in export prices (e.g.,meat) probably contributed to inflation-ary pressures. Moreover, prices for Guatemalan imports also started toclimb.

- 19 -

53. The Government has launched a campaign to keep the rate of in-flation as low as possible. In broad terms, the approach was to increasethe supply of basic grains, control growth of the money supply -- andintroduce temporary price controls to fight unjustified price escalation.For this purpose, the Government issued a series of decrees and createdan office in the Ministry of Economy to implement the legislation. Theauithorities intended to keep the price level of the so-called essentialconsumer products, that is, food and some industrial inputs, constructionmaterials, and agricultural small tools, as low as possible. To thisend, the Government published a comprehensive price list of the articlessubject to price control. It intended to authorize price increases onbasic commodities, only if producers 'could demonstrate that they hadincurred cost increases and that the price increases would not raiseprofit margins. It also intended to follow market developments as close-ly as possible, to be able, if necessary, to induce imports of certainitems in the event that supply shortages 'were causing upward price pres-sures. Moreover, to the same end, in September 1973 the authorities haddecided to establish certain export controls by introducing a system ofexport licensing for essential food products and raw materials for whichdomestic and foreign markets competed.

CHAPTER V: BALANCE OF PAYMENTS

54. Although Guatemala's balance of payments has experienced some sharpfluctuations, in general it has improved in the last twenty years. It is moreresilient, relying on a more diversified export structure, with a relativelylow external public debt on favorable terms and a comfortable foreign reservelevel.

Exports

55. Until the end of the fi:ties, changes in the level of Guatemalarsexports mainly reflected fluctuations in coffee prices. Coffee constitutedabout 70 percent of export value, while bananas,the main second export,account-ed for about I''. percent. The change in structure of exports that has takenplace in subsequent years has been due to the slow growth of coffee exportsand to the emergence and expansion of new exports. Thus cotton, whichaccounted for only about 5 percent of the value of exports in the fifties,increased its relative importance to about 11 percent by 1973, while coffeefell to 33 percent and bananas to 5.5 percent. Industrial exports (includingmeat and sugar) which were negligible in the ffties and constituted onlyabout 8 percent of total export value by 1960, increased their relativeimportance to more than 44 percent by 1973. More recently, tourism hasbecome another important source of export earnings.

56. The volume of coffee exports grew at less than 3 percent per annumon the average during 1960-73. Prices experienced a sharp deterioration from1967 through 1969, improving on the average thereafter. However, Guatemalanunit values do not entirely reflect world price movements. The unit valueof Guatemala's coffee exports dropped in 1972 due to the unusually largesales to new markets, i.e., countries which are not members of the Inter-national Coffee Organization.

- 20. -

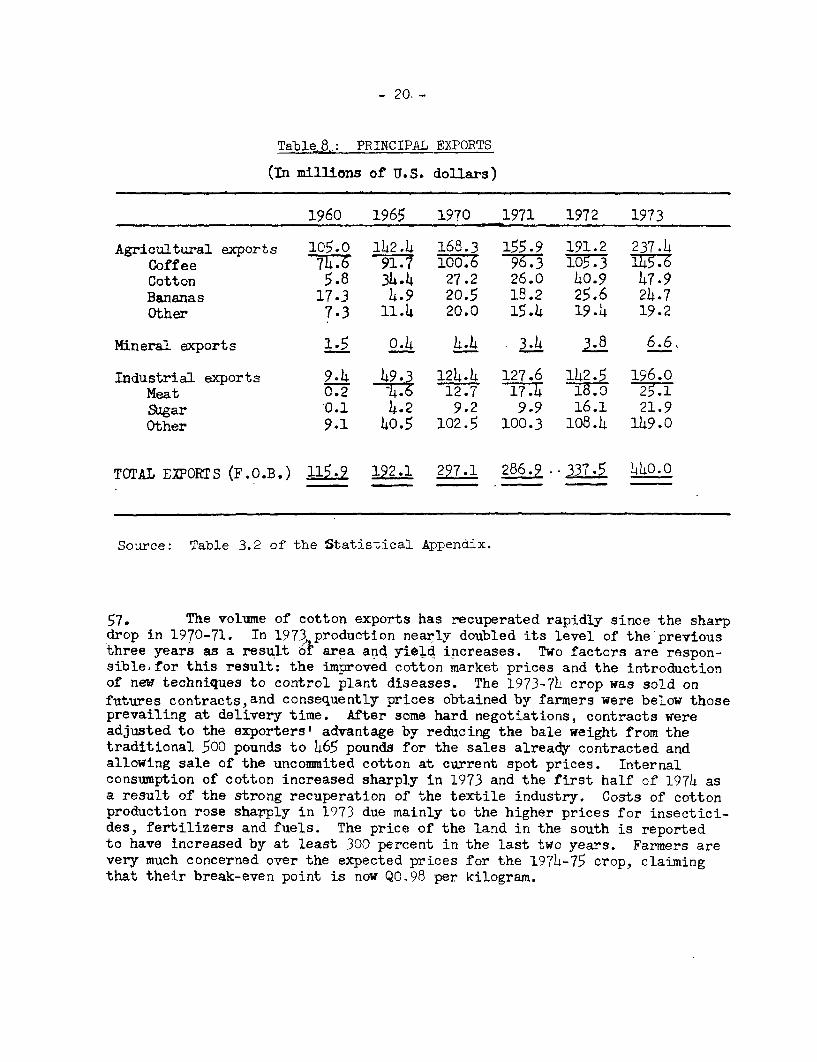

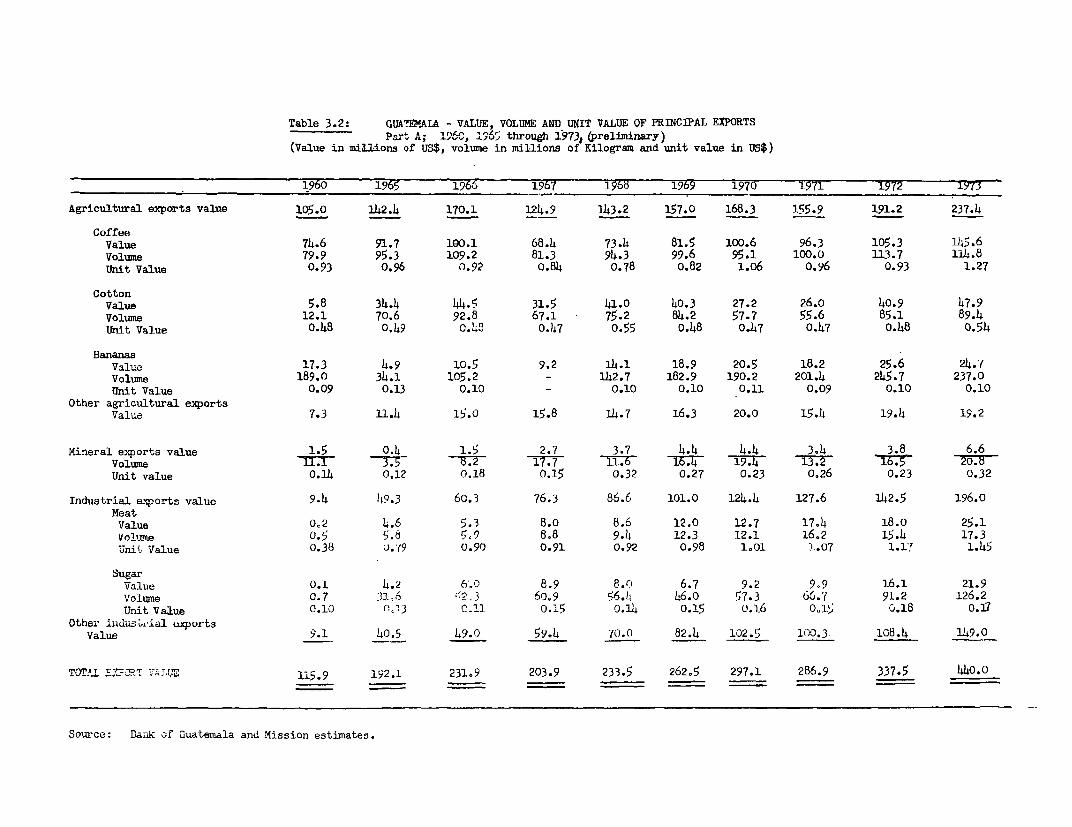

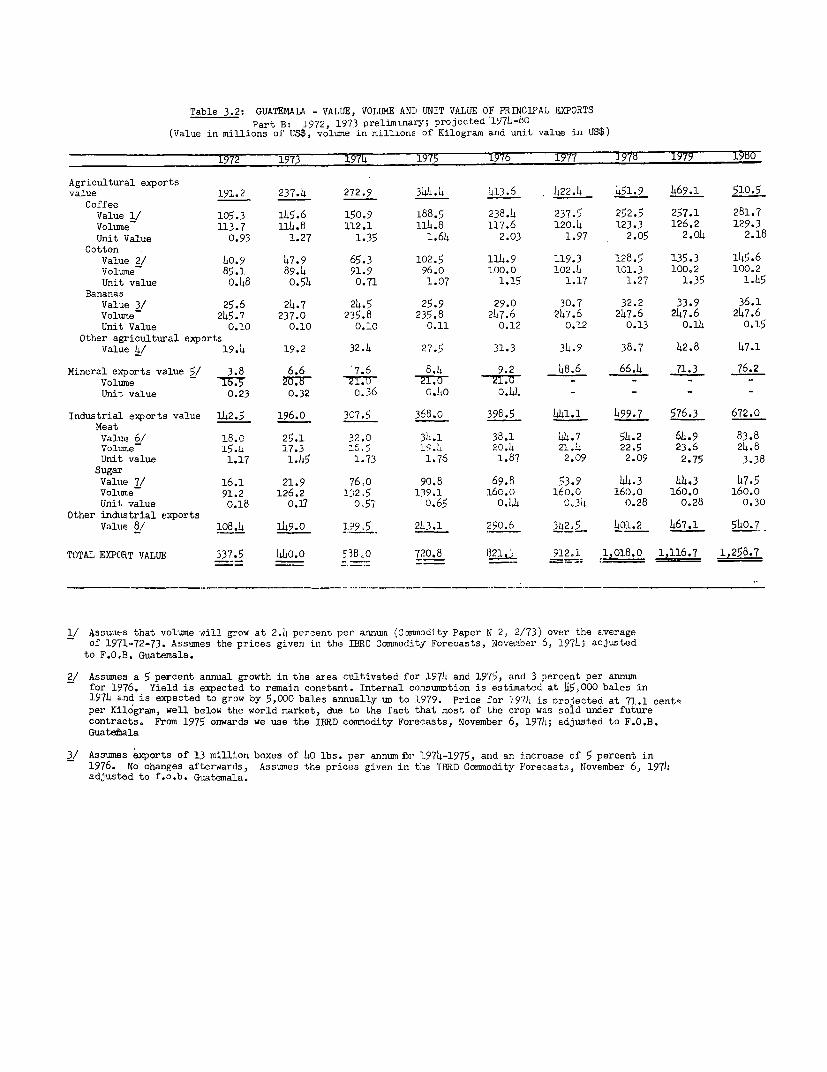

Table 8.: PRINCIPAL EXPORTS

(In millions of U.S. dollars)

1960 1965 1970 1971 1972 1973

Agricultural exports 105.0 142.4 168.3 155.9 191.2 237.4Coffee 7436 91.7 100.6 96.3 105.3 145.6Cotton 5.8 34.4 27.2 26.0 40.9 47.9Bananas 17.3 4.9 20.5 18.2 25.6 24.7Other 7.3 11.4 20.0 15.4 19.4 19.2

Mineral exports 1.5 0-4 4.4 3.4 8 6.6

Industrial exports 9.4 49.3 124.4 127.6 142.5 196.0Meat 0.2 4.6 12.7 17.4 18.0 25.1Sugar 041 .2 9.2 9.9 16.1 21.9Other 9.1 40.5 102.5 100.3 108.4 149.0

TOTAL EXPORTS (F.O.B.) IL5.2 192.1 297.1 286.9 -- 337.5 440.0

Source: Table 3.2 of the 5tatistical Appendix.

57. The volume of cotton exports has recuperated rapidly since the sharpdrop in 1970-71. In 197, production nearly doubled its level of the previousthree years as a result of area and yield increases. Two factors are respon-sible for this result: the improved cotton market prices and the introductionof new techniques to control plant diseases. The 1973-74 crop was sold onfutures contract8,and consequently prices obtained by farmers were below thoseprevailing at delivery time. After some hard negotiations, contracts wereadjusted to the exporters' advantage by reducing the bale weight from thetraditional 500 pounds to 465 pounds for the sales already contracted andallowing sale of the uncommited cotton at current spot prices. Internalconsumption of cotton increased sharply in 1973 and the first half of 1974 asa result of the strong recuperation of the textile industry. Costs of cottonproduction rose sharply in 1973 due mainly to the higher prices for insectici-des, fertilizers and fuels. The price of the land in the south is reportedto have increased by at least 300 percent in the last two years. Farmers arevery much concerned over the expected prices for the 1974-75 crop, claimingthat their break-even point is now QO 98 per kilogram.

- 21 -

58. The volume of meat exports grew at an average rate exceeding lL1 per-cent per annum during 1965-72, with prices improving constantly. A substantialpart of this meat came from cattle imported from other Central Americancountries. However, restrictions on the export of live animals except forbreeding purposes, have been imposed in the Central American countries in thelast few years. Cattle-raising activity has been concentrated mainly in thesouth of the country; however, sharp rises in land prices due to expansion ofthe cotton and sugar areas in the last two years are driving the cattle tonew zones in the north: Coban and the Izabal area. In these areas the climateis not appropriate for cotton but is for sugar: however, there are no sugarmills at present and cattle is among the more attractive activities since landis relatively cheap compared to the south. Until recently, the high levelof demand in the United States market has been the main incentive for thisrelatively new export. The Goverrment is trying to promote the developmentof cattle raising and dairying with technical and financial support from IDBand IBRD.. In 1972 the Goverrnment passed a-decree establishing a system ofexport quotas, in order to assure sufficient supplies for the internal market.These quotas are determined by the Ministry of Economy in February of eachyear. It seems that the quota system has not discouraged cattle raising.In September 1973, the Government issued a decree prohibiting the export ofrawhide and establishing prior export licensing for processed hides. Theaim has been to assure the necessary raw material for local industry inview of its increasing scarcity in the world market.

59. The volume of banana exports increased by 15 percent in 1972, butin 1973 it dropped by about 3.5 percent -- high winds had damaged bananaplantations. The increase of 1972 was the result of the establishment ofnew production areas on the Atlantic coast. The main banana producer inthe country is Bandegua, a subsidiary of Del Monte Corp., which purchasedthe banana and livestock farms and other agricultural holdings of UnitedBrands in December of 1972. Bandegua does not plan to expand banana planta-tions in the near future; it is exploring rather the posibility of producingpdneapple and papaya for export to the eastern coast of the USA. The Govern-ment of Guatemala, which is a member of the recently formed association ofbanana-exporting countries, has not imposed the export tax agreed by themembers for the reason that Bandegua has a contract approved by Congress whichprecludes the levying of the tax. The company, however, is negotiating withthe Government to find other means to compensate it for the revenue forgone.

60. Tlr voLume of sugar exports has nearly doubled in the last threeyears. The high level of demand in the international market has been theprimary incentive for this rapid development. The producing areas, likethose for cotton, are concentrated in the south, and on land formerly usedfor cattle raising and basic grains.

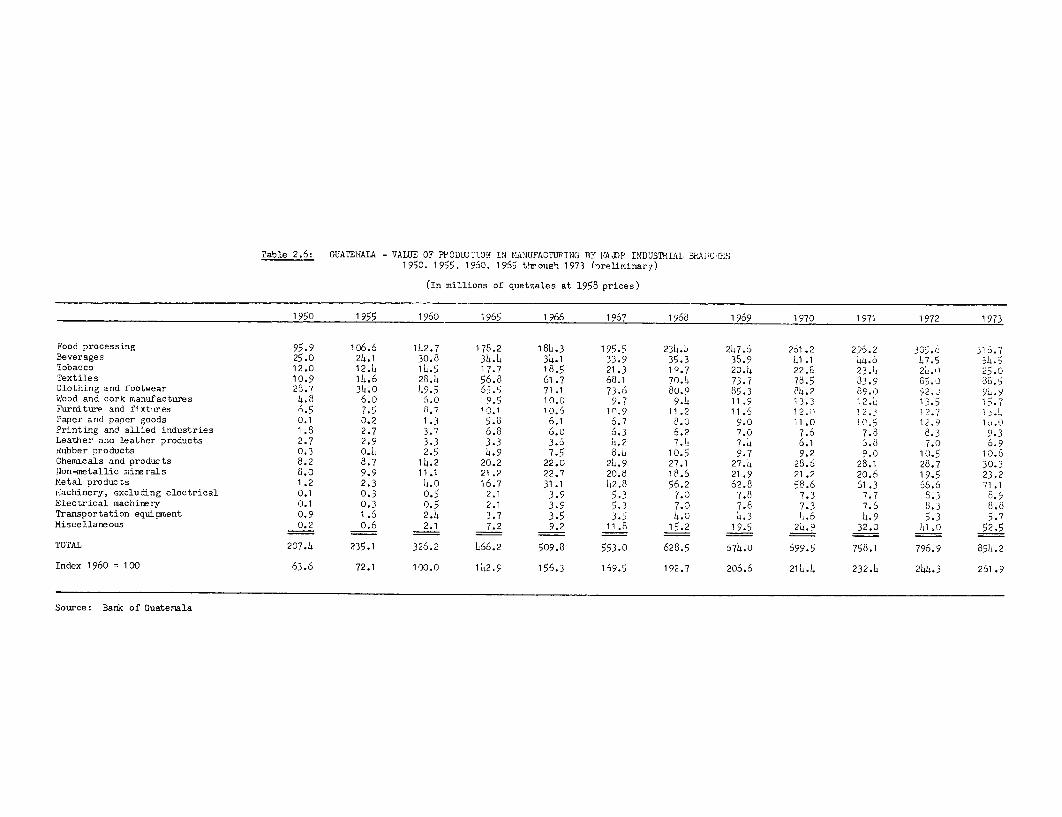

61. The value of exports of industrial products, excluding meat andsugar, grew at an averaxge rate of 24 percent per annum during 1960-73. Thisrapid development has increased the share of industrial products in totalexports from about 8 percent in 1960 to more than 33.5 percent in 1973. The rapid

- 22 -

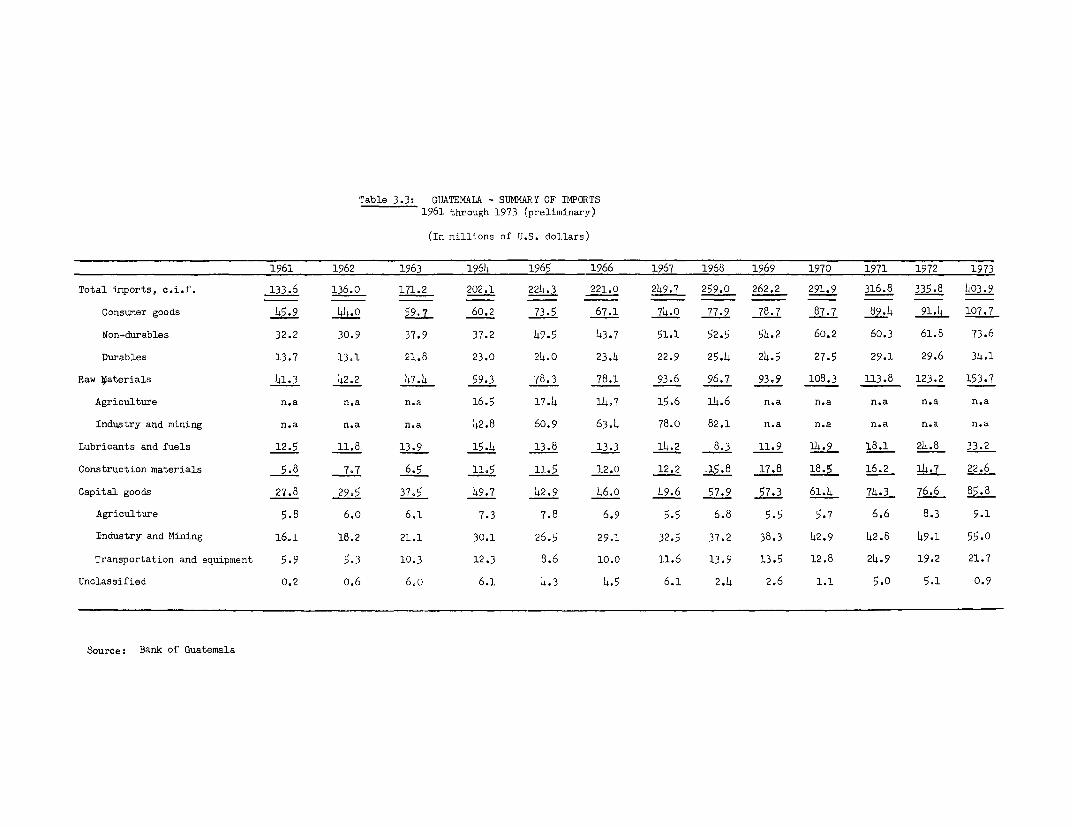

growth has been the result of incentives granted to the industrial sectorin 1960 with the establishment of the Central American Common Market, whichmeant a larger protected market plus generous tax holidays. The 1969 borderconflict between Honduras and El Salvador helped Guatemala's manufacturingexports. The country was able to capture part of the Honduran market whichhad been previously supplied by El Salvador. Guatemala's manufacturingexports increased by 24 percent in 1970, as compared with an annua.- averageof about 18 percent in the preceeding years. Honduras finally withdrewfrom the Central American Common Market trade agreement in December 1970,and Guatemala's manufacturing exports dropped by more than 2 percent in1971, the first decline since 1960. In 1972 these exports grew by only8 percent. However, the improvement of world market conditions for themain exports of Central America, which had begun in 1970, reached a boomsituation in 1973, and the demand for manufacturing products in the areaincreased substantially. Guatemala's manufacturing industry was able rapidlyto increase its output due to a large excess capacity which developed inthe second half of the sixties, and manufacturing exports grew by more than37 percent in 1973. The improved economic conditions in the area helpedinduce partial participation of Honduras in Common Market trade. Thus, inFebruary 1973, Guatemala signed a bilateral trade agreement with Honduras.

62. Tourism in Guatemala has continued to grow at a very fast pace.It is reported that the number of tourists increased by 16 percent in 1973,while their expenditure grew by nearly 50 percent. The industry could haveexpanded even faster but for the limited availability of hotel accommodations,especially in Guatemala city. At present new hotels are being built andothers are scheduled to be constructed in the next two years. This will addabout 1,000 first-class hotel rooms to the current 1,200 rooms in this cate-

gory. The Government has increased its interest in tourist industry developmentin view of its great potential which can be realized in a relatively short term.The Government intends to maintain the tourist sector as a high priority for thenext economic development plan. The archeological area in Tikal, in the PetenDepartment, will be developed with the financial assistance of the Central Amer-ican Bank for Economic Integration. Development of the area will include therestoration of a large group of Mayan pyramids, and the construction of a newairport in the Lake Peten Itza, which could receive international air traffic.(It is expected that construction will be initiated in early 1975.) In addi-tion, the road between Flores in Lake Peten Itz'a and Tikal will be improved,and the necessary infrastructure for hotel construction on the lake and pro-tection of its banks will be completed later on. Plaps for the development ofthe Izabal area on the Atlantic Coast; are advancing rather slowly.

Imports

63. Imports -/ in the first half of the 1960s grew at a considerably fasterpace than in subsequent years -- 14 percent per annum on the average as compared

1/ Imports of merchandise c.i.f., in current US$.

- 23 -

with 6 percent during the period 1965-72. In 1973, however, imports acceleratedincreasing by over 20 percent. This unusually high growth reflects the 1973faster expansion of the overall economy, but in particular, the recovery ofthe manufacturing sector -- imports of raw materials increased by about 25percent, and real value added in manufacturing grew by more than 8 percent.

Table 9: SUMKARY BALANCE OF PAY.MENTS

(In uillUons of U.S. dollars)

Annual Average

1965-66 1967-6 17969-70 1971 1972 1973

Resource Gap - 16.5 - 40.9 8.1 -32.5 - 1.2 38.0Exports (incl. n.f.s.) 7.7 2 326.2 338.5 395 3 529.9

Imports (incl. n.f.s.) 261.0 290.6 318.1 371.0 396.5 491.1

Net Factor Income - 14.5 _ 25.4 - 37.0 - 41.8 -47.h -46.4Net Current Transfer 8.5 10.0 15.5 25.2 28.8 41.9

Current Account Balance - 22.5 - 56.3 - 13.4 - 49.1 -19.8 34.3

Private Sector 23.5 37.4 21.8 53.6 62.9 28.1

Direct Investment, net Tb7 23.14 2b.67 13 27.7Other long-term, net 13.2 14.9 17.5 18.3 22.4 22.8Other short-term, net - 4.0 2.0 - 19.1 10.7 25.2 -22.4

Public Sector 6.3 16.8 12.2 11.2 8.5 25.4

International Organizations, net - 3.9 11.3 14.7 15.5 22.0Governments, net 1.5 3.7 0.3 - 14.9 6.7Other 5.4 9.2 o.6 - 3.5 -11.9 -3.3

Loans to banks 1/ 0.5 1.5 0.4 - 1.5 -0.1 -9.2

Others j - 1.1 - 0.9 0.9 3.9 4.8 1.3Monetary movements, net

(increase -) 14.7 1.9 - 17.6 - 11.8 -50.3 -67.0Net errors and ommissions - 11.4 - 0.4 - .4.3 - 6.3 - 6.o -12.9

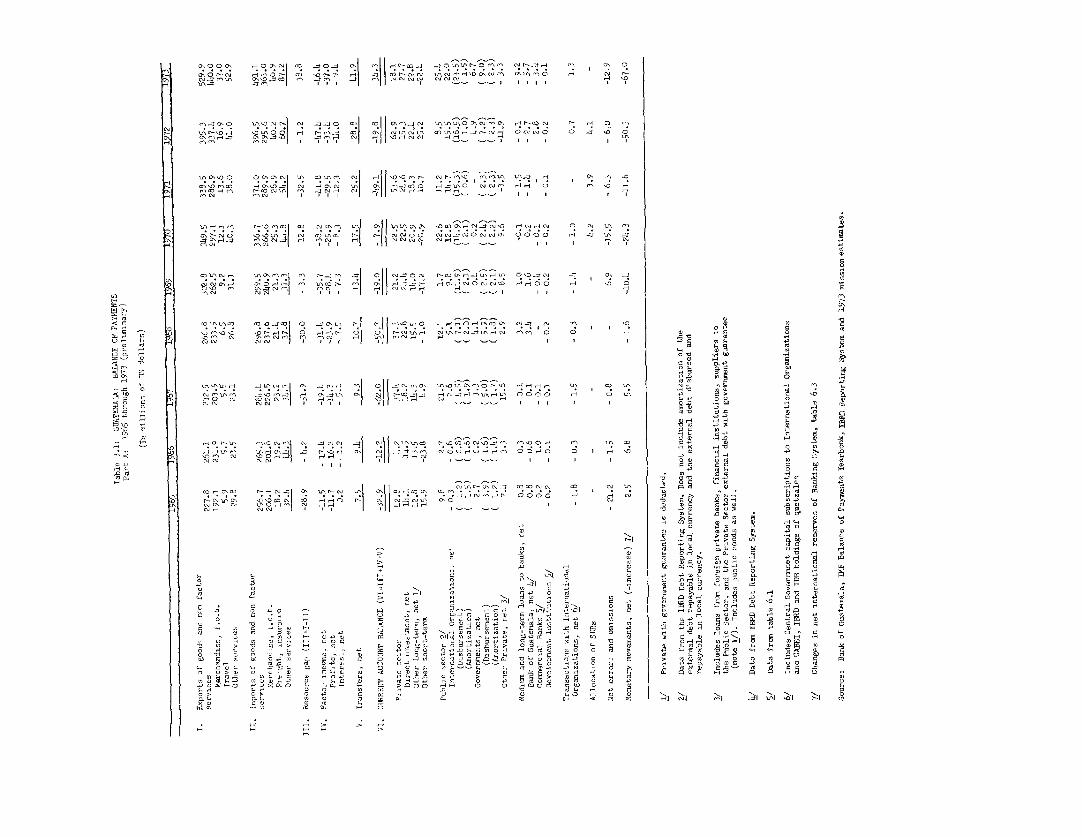

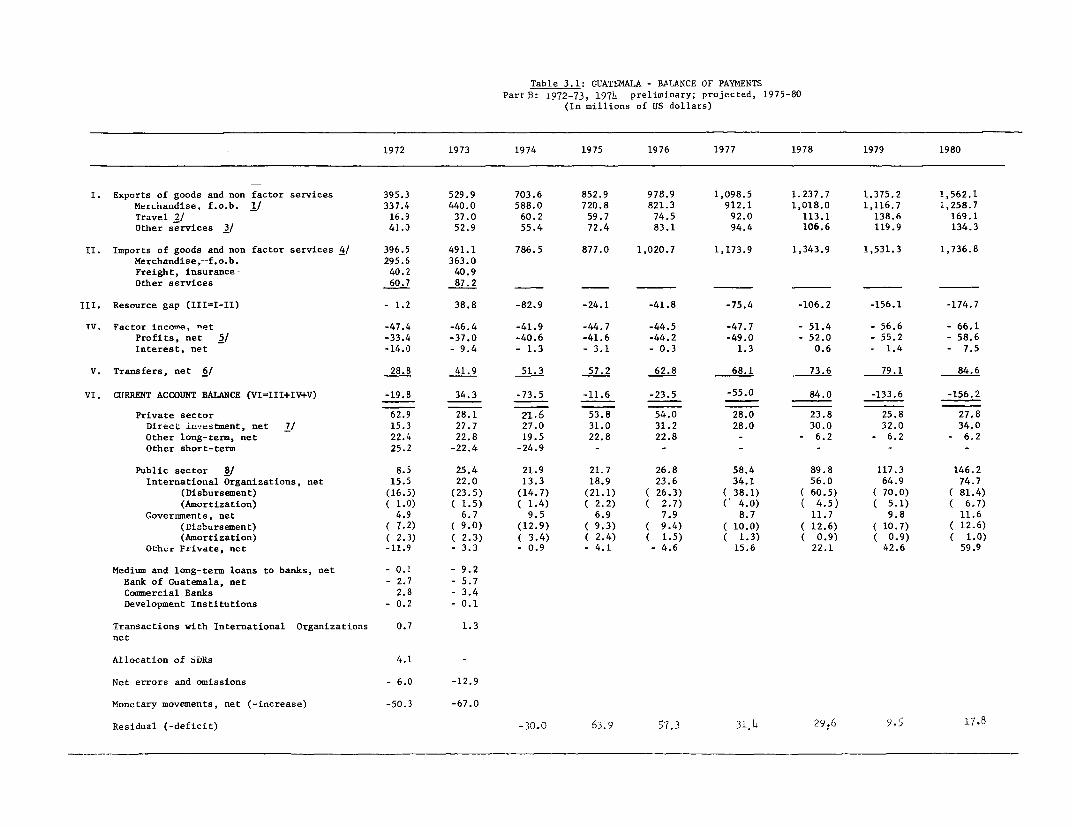

Medium and long-term2 Capital subscriptions to international orgaLnizations and allocation of SDRs.Source: Table 3.1 of Statistical Appendix.

- 24 -

6h. Since the early 1960s the structure of imports has undergone substan-tial changes. In 1960 consumer goods accounted for more than 31h percent oftotal imports, while raw materials for only about 30 percent. By 1973, therelative importance of consumer goods in the import bill had declined toabout 27 percent, while that of raw materials had attained a level of about38 percent. The main determinant of these changes has been the increasingparticipation of the industrial sector in national output.

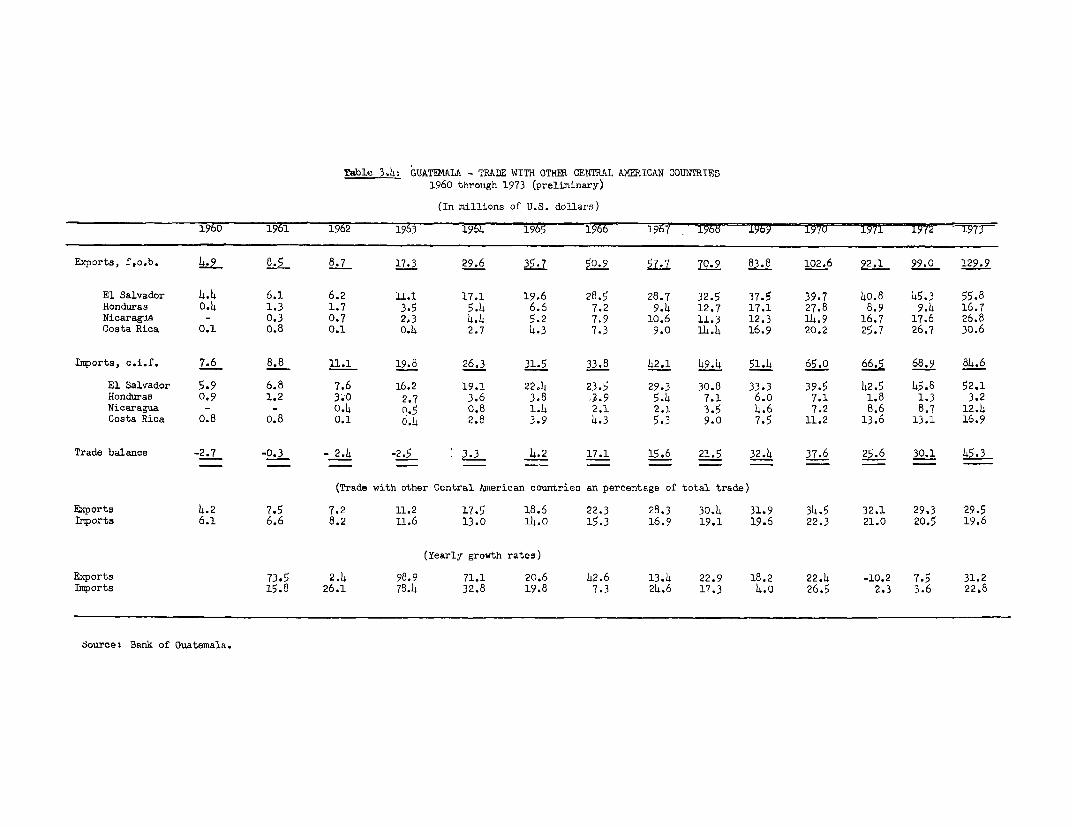

65. Simultaneously with the change in the structure of imports, a changein sources of imports to Guatemala has taken place. Although the UnitedStates continue to be the country's main supplier, its share in total importshas diminished significantly. While in 1956 over 67 percent of importsoriginated in the USA, by 1973 this share had declined to about 31 percent.This shift resulted primarily from the rapid increase in trade among CentralAmerican countries. Guatemala imported about 1.2 percent in 1956 and about7 percent in 1961 from the other Central American countries; by 1973, importsfrom the area were about 21 percent. After the USA and El Salvador, Japanhas become the single most important supplier of imports in the early seventies.

Financing the Current Account Deficit

66. Guatemala's balance of payments deficit on current account has beentraditionally financed mainly through capital inflows to the private sector.During the period 1965-72, on the average, the ratio of private to public netforeign borrowing has been 3:l. This broad difference originates in therelatively small size of the public sector and the rather conservative fiscalpolicies of the Central Government, which have kept the public external debtat a low level. Net disbursements to the private sector dropped from US$62.9million in 1972 to US$2V.1 million in 1973. -This change was prompted by areduction in short-term liabilities in the face of the tight internationalmoney market and lower interest rates within the country, and despite largeincreases in imports. Guatemala's overall balance of paynents ramained insurplus in 1963-73, the increase in reserves reaching an all-time record ofUS$67.0 million in 1973. The Central Bank's net international reserves hadreached US$213.8 million by the end of 1973.

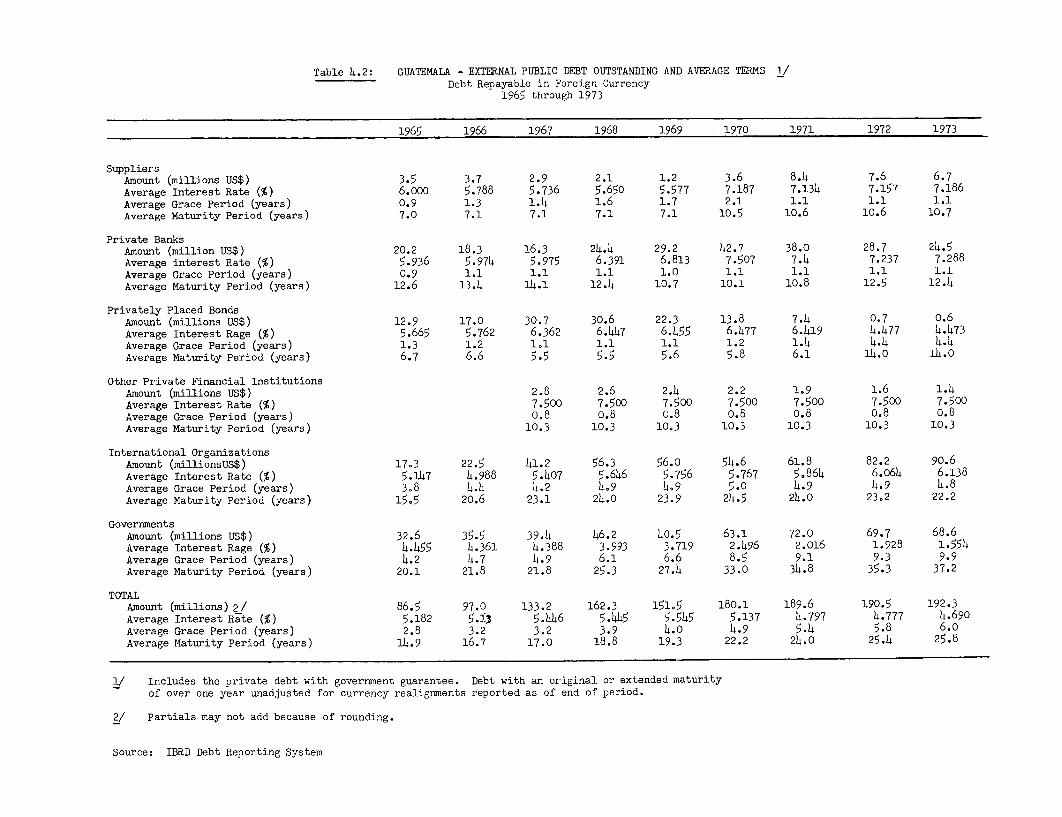

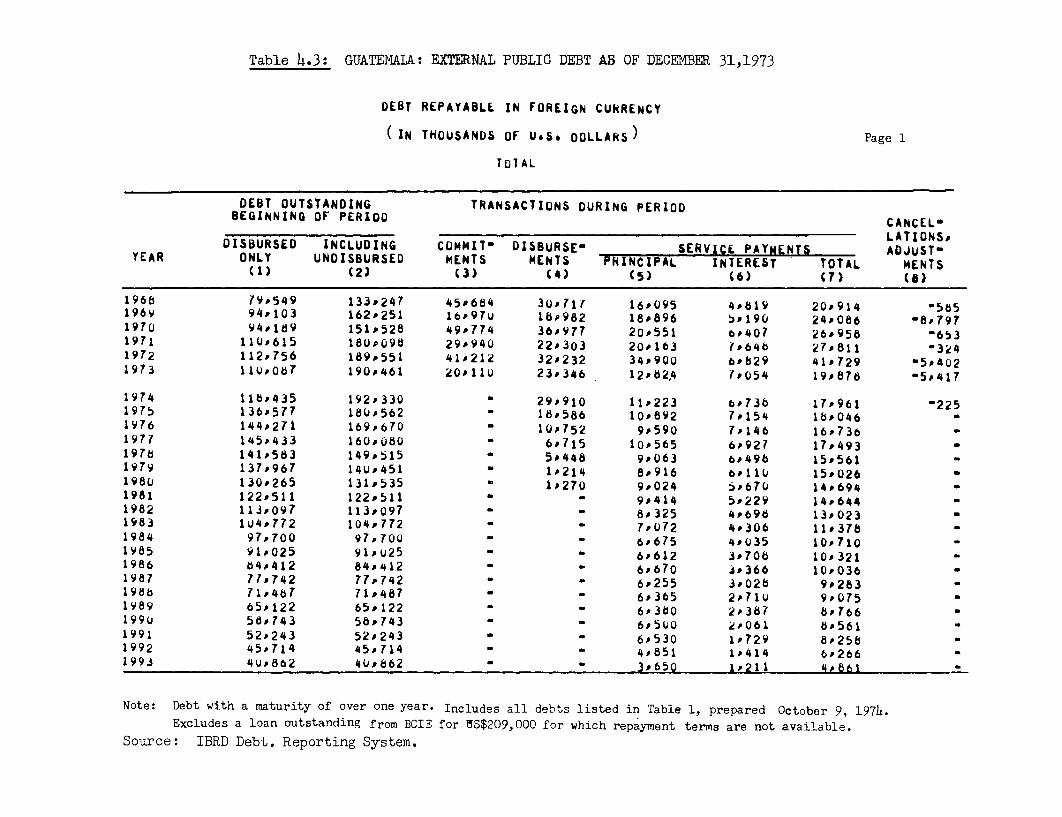

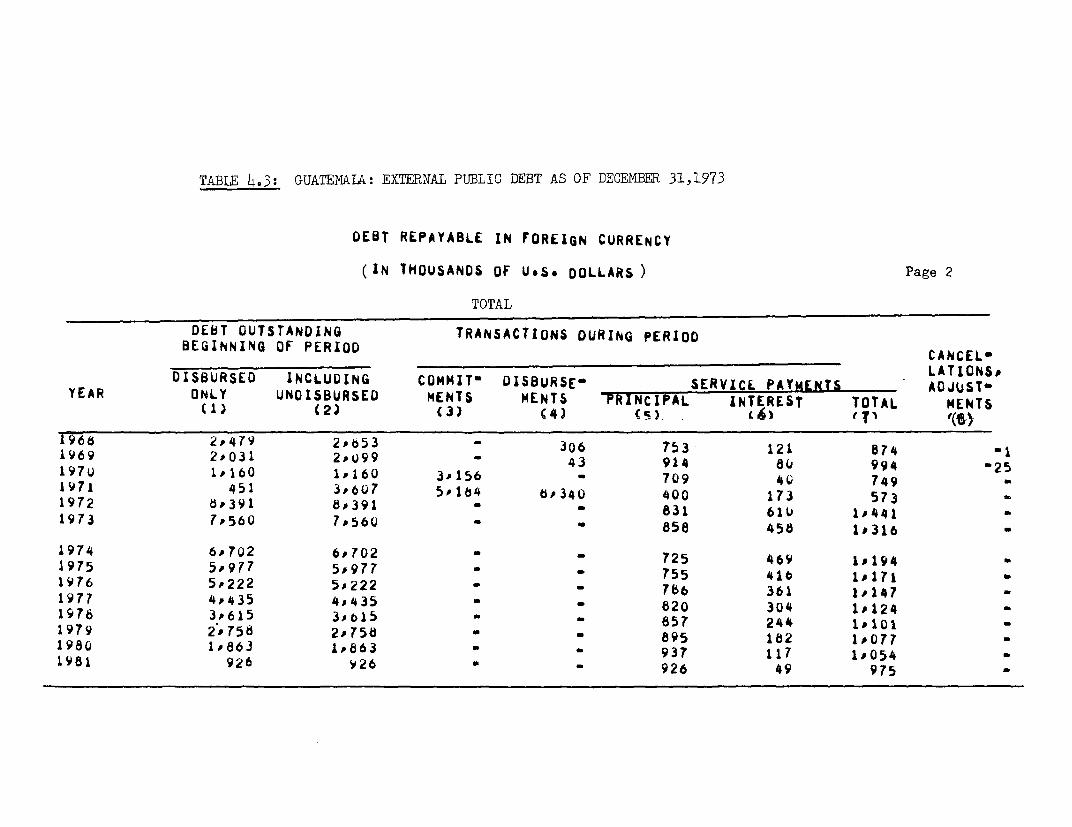

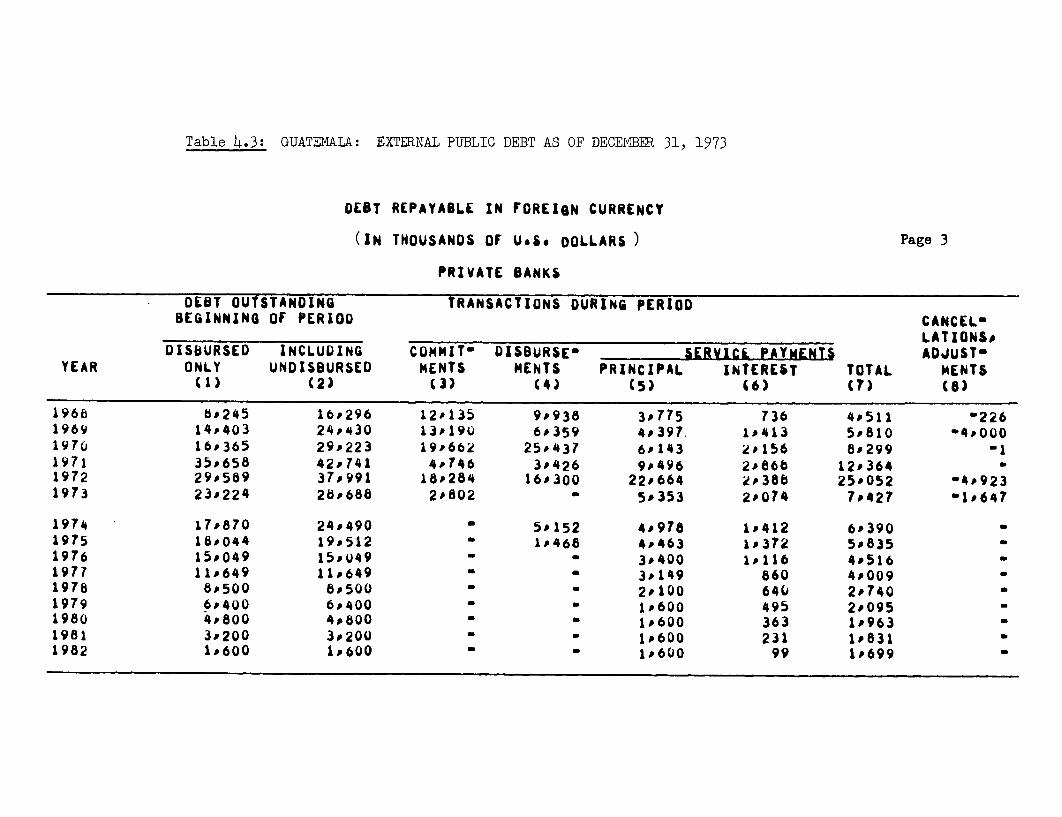

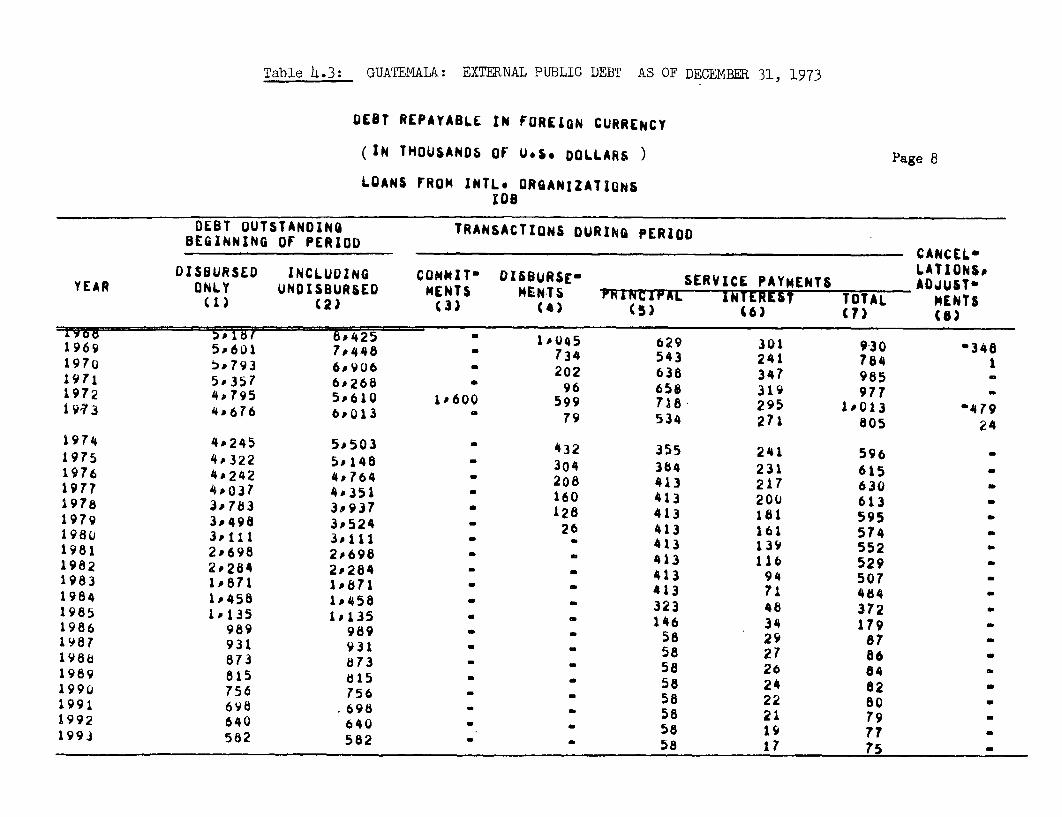

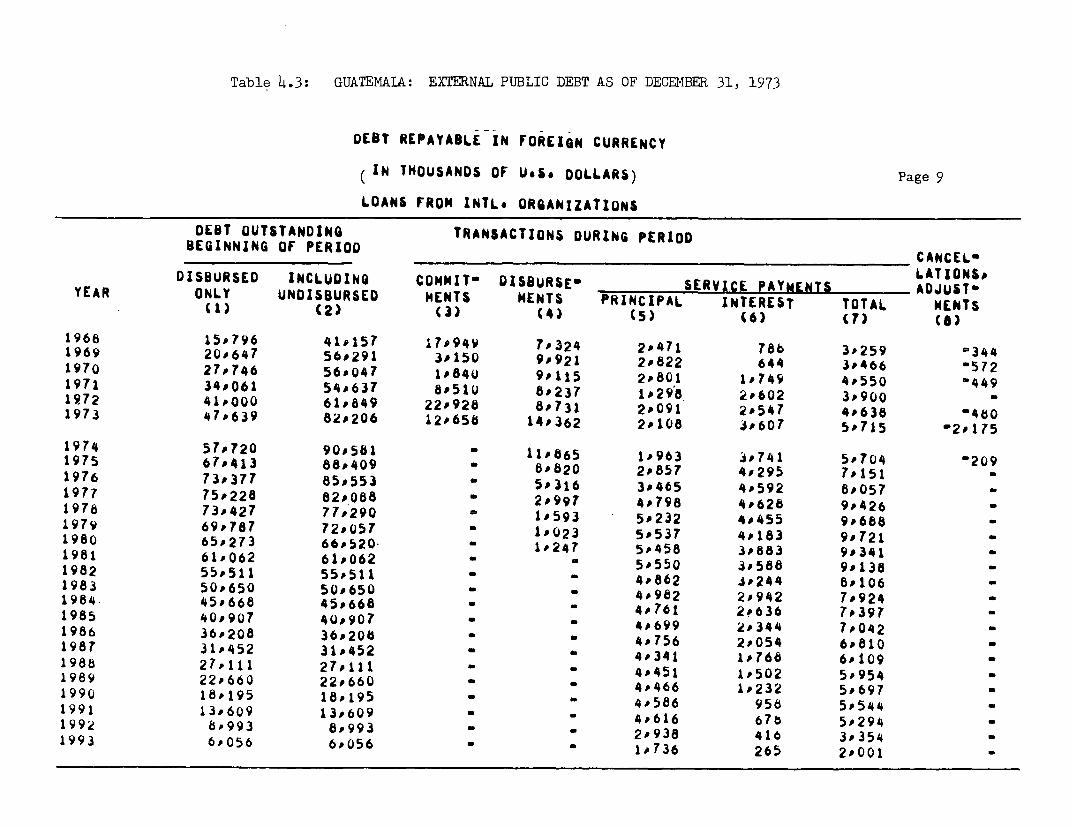

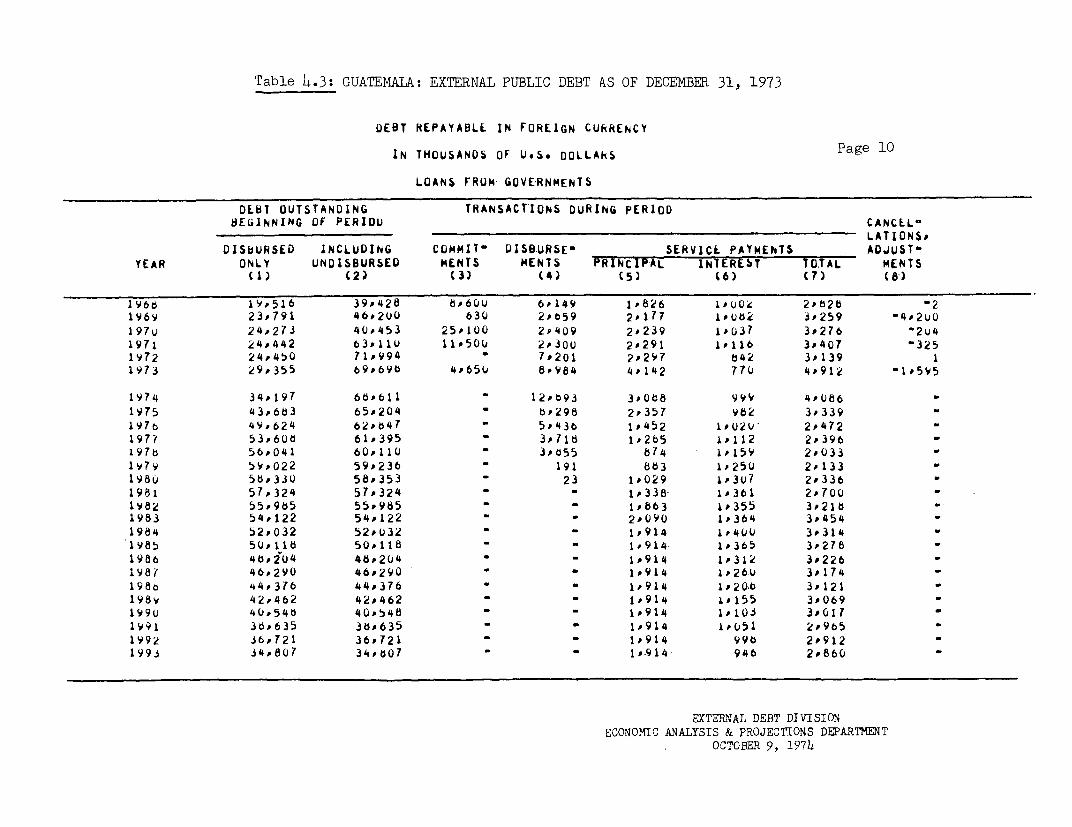

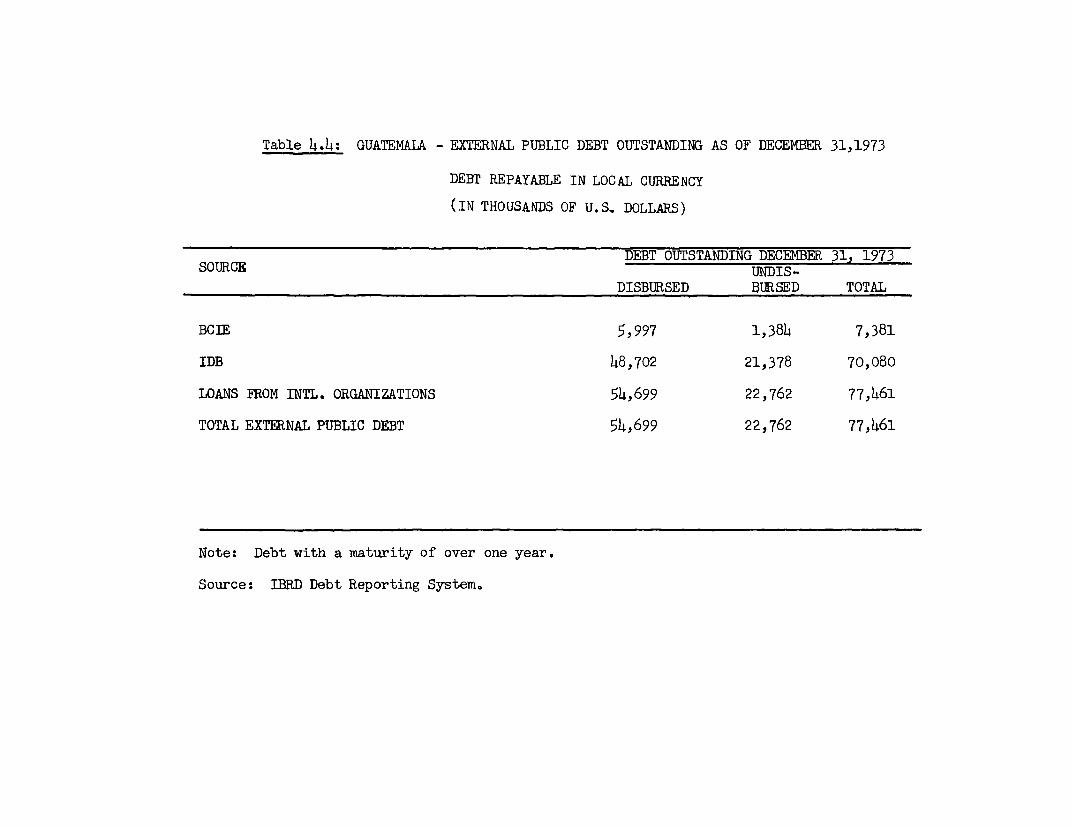

67. The terms of Guatemala's external public debt (interest rate, graceperiod and maturity) have been improving steadily since 1965. This has beenmainly due to increased borrowing from the international organizations. Whilein 1965, external private sources of credit to the public sector accountedfor more than h2 percent of the total outstanding public external debt includ-ing the undisb-ursed portion, by 1973 these sources accounted for less than18 percent. In con;rast, the share held by the international organizationsincreased from 20 percent in 1965 to more than 47 percent 1973. This increasein the share of the international lending agencies will help maintain Guate-a--'s public dcbt service ratio at levels srimriLar or lower than the oncattained in 1973 -- 3.9 percent of exports, down from a peak of 10.5 percentin 1972.

- 25 -

Table 10: PUBLIC EXTERNAL DEBT AT THE ENDI F PERIODREPAYABLE IN FOREIGN CURRENCY -

1965 1969 1972 1973

Outstanding including undisbursed 86.5 151.5 190.5 192.3(Private) (36.6) (55.0) (38.6) (33.1)(Internatiunal Organizations) (17.3) (56.u) (82.2) (90.6)(Governments) (32.6) (h0.5) (69.7) (6b.b)

Average Interest Rate(Percent) 5.2 5.5 4.5 .7

Average Grace Period(Years) 2.8 4.0 5.8 6.o

Average Maturity(Years) 14.9 19.3 25.4 25.8

1/ Includes private debt guaranteed by the public sector.

Source: Table 4.2 of the Statistical Appendix.

Chapter VI: MAJOR DEVELOPMENTS IN 1974

68. Until the end of the third quarter of 1974 prospects for an economicexpansion similar to that registered in the two preceding years, when GDP grew