Embed Size (px)

Citation preview

Report No. 11583-SW

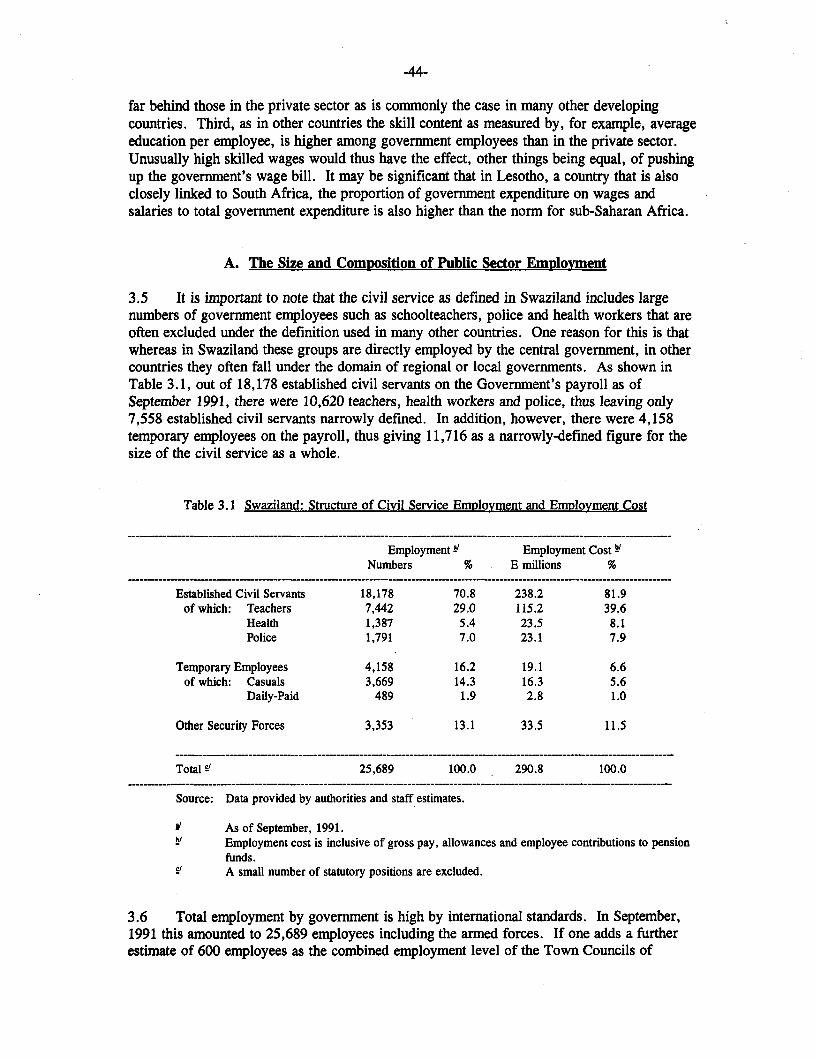

SwazilandPublic Expenditure Review

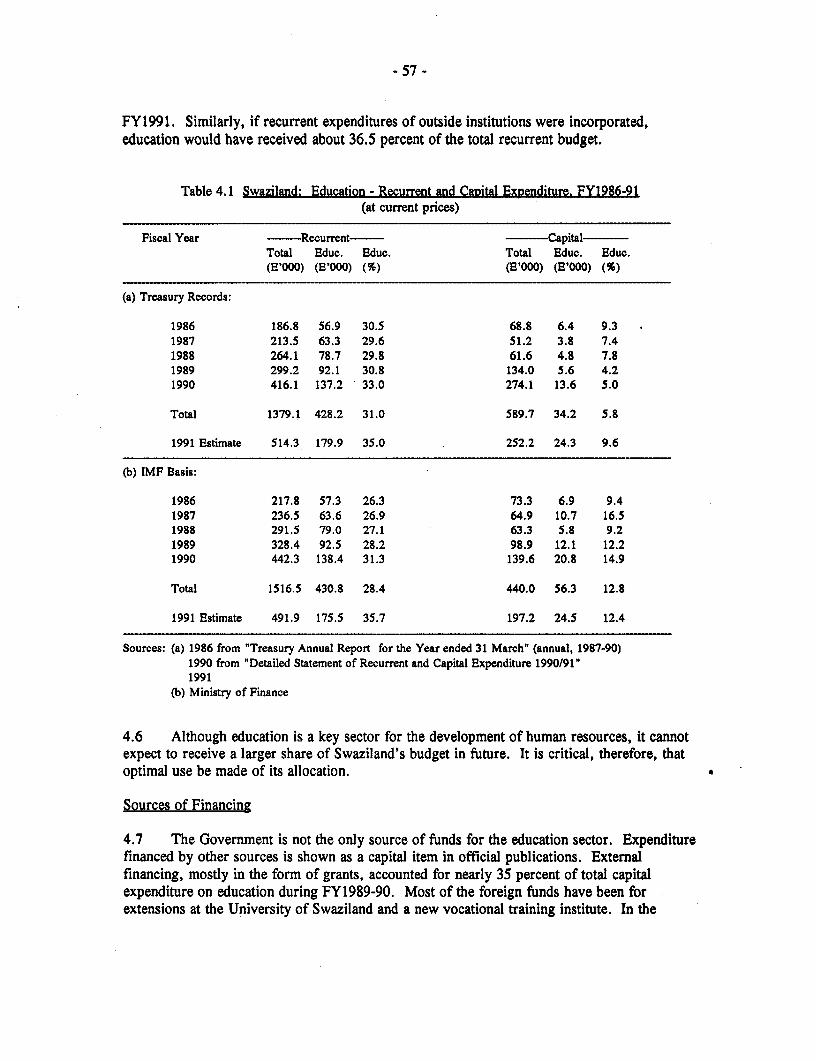

July 1, 1993

Country Operations DivisionSouthern Africa Department

FOR OFFICIAL USE ONLY

Document of the World Bank

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may not otherwisebe disclosed without World Bank authorization.

Pub

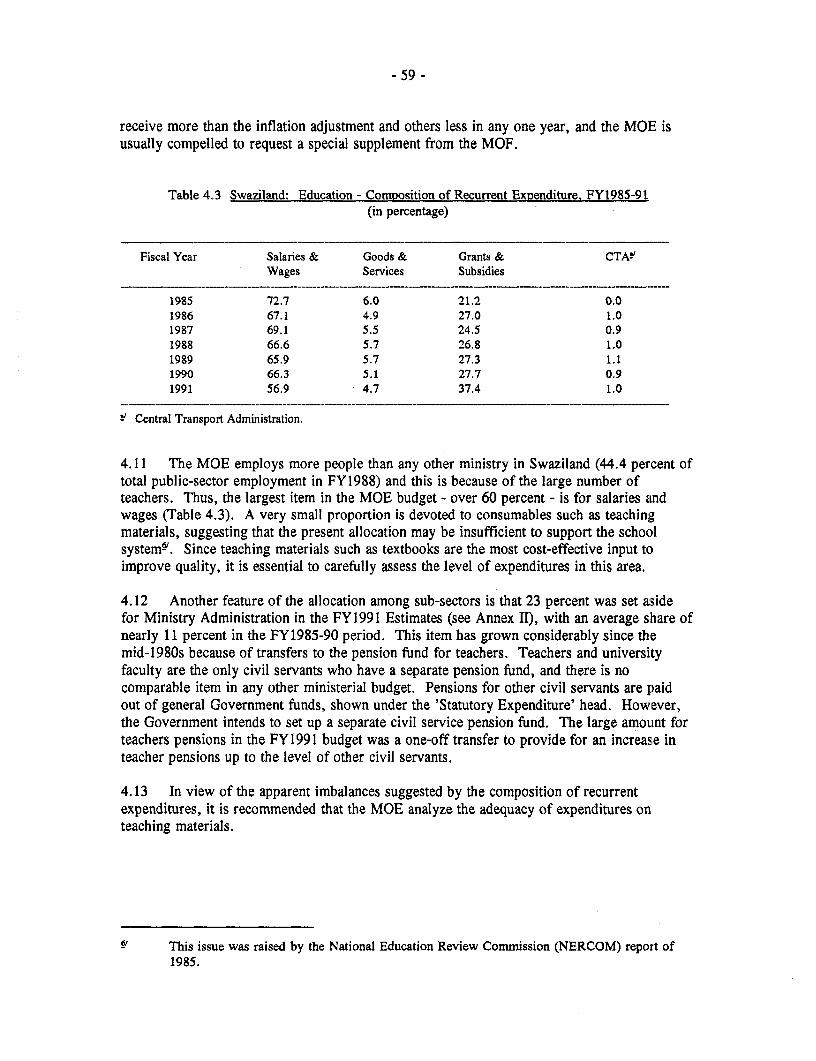

lic D

iscl

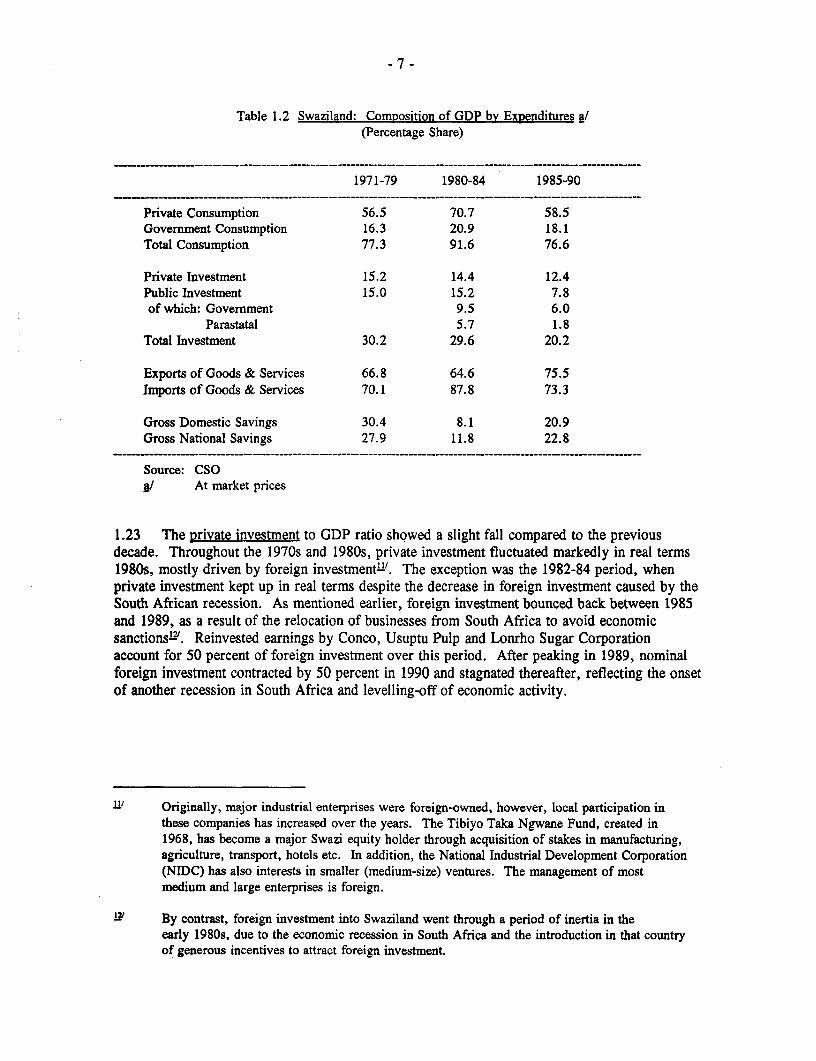

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

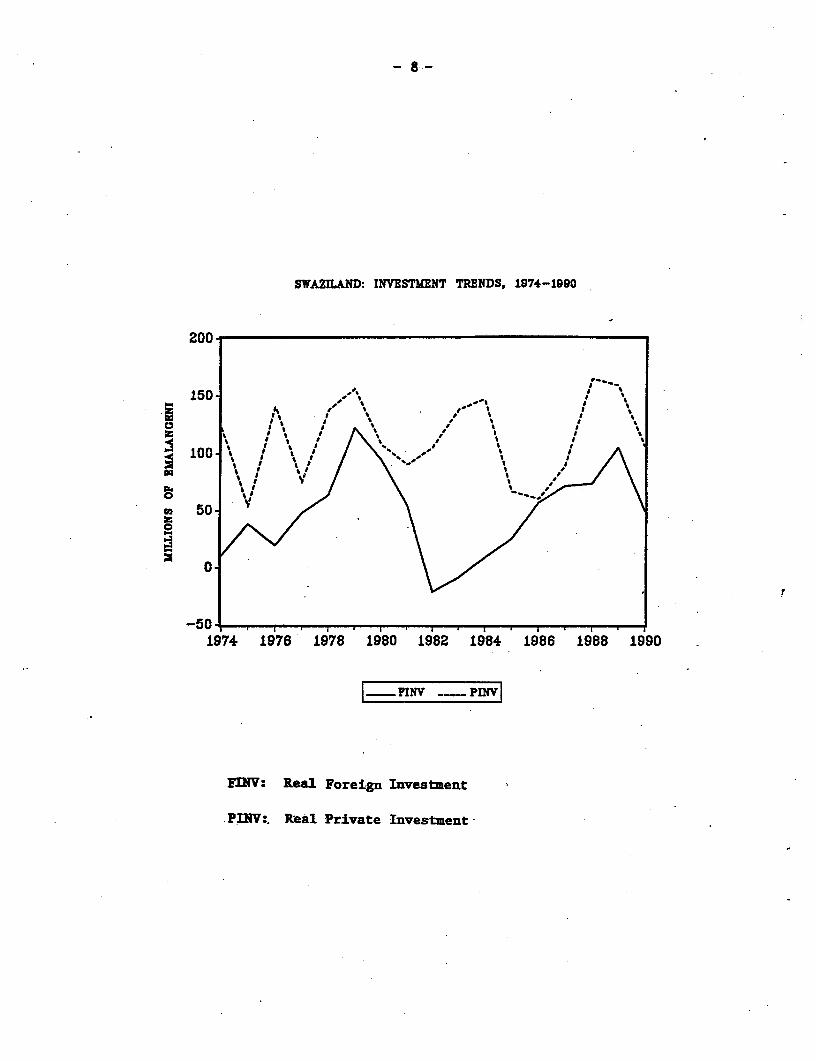

Pub

lic D

iscl

osur

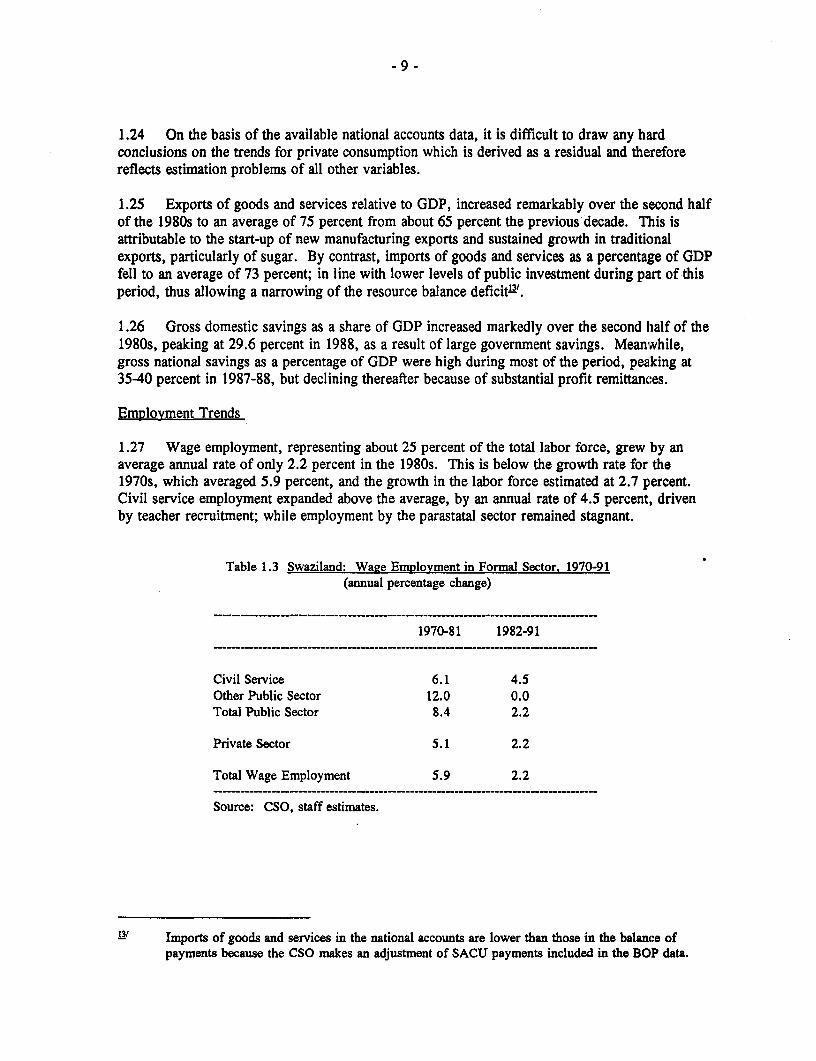

e A

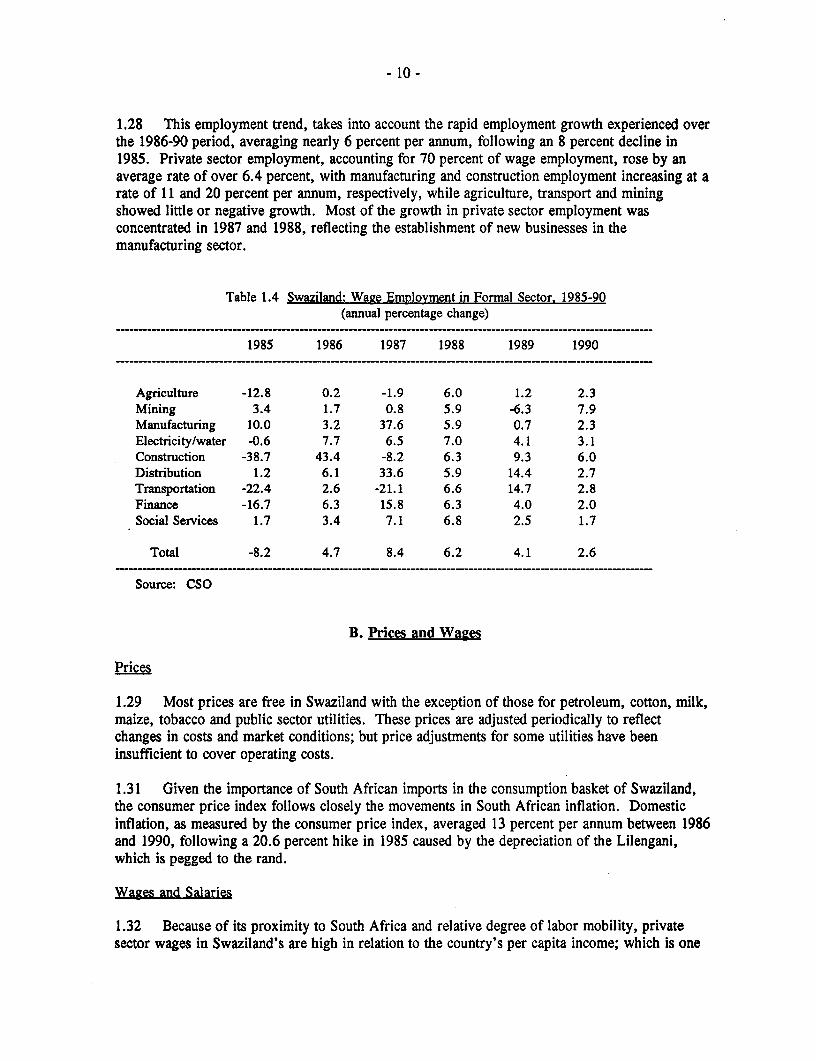

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

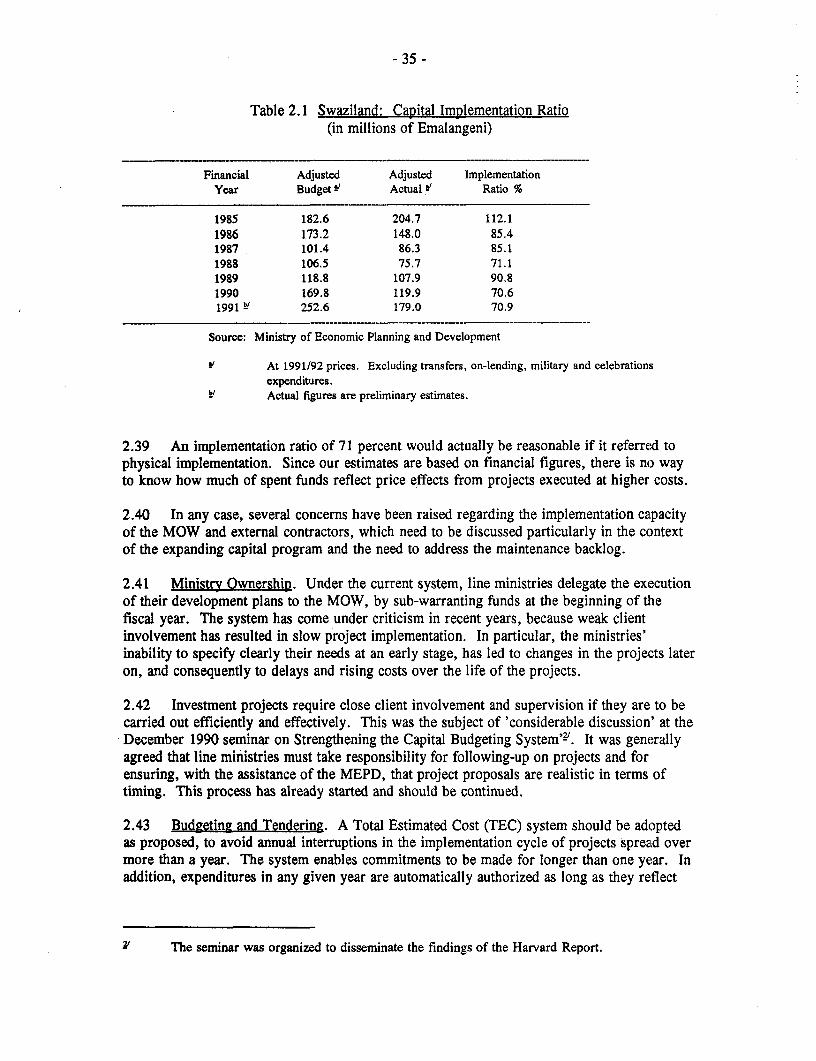

Pub

lic D

iscl

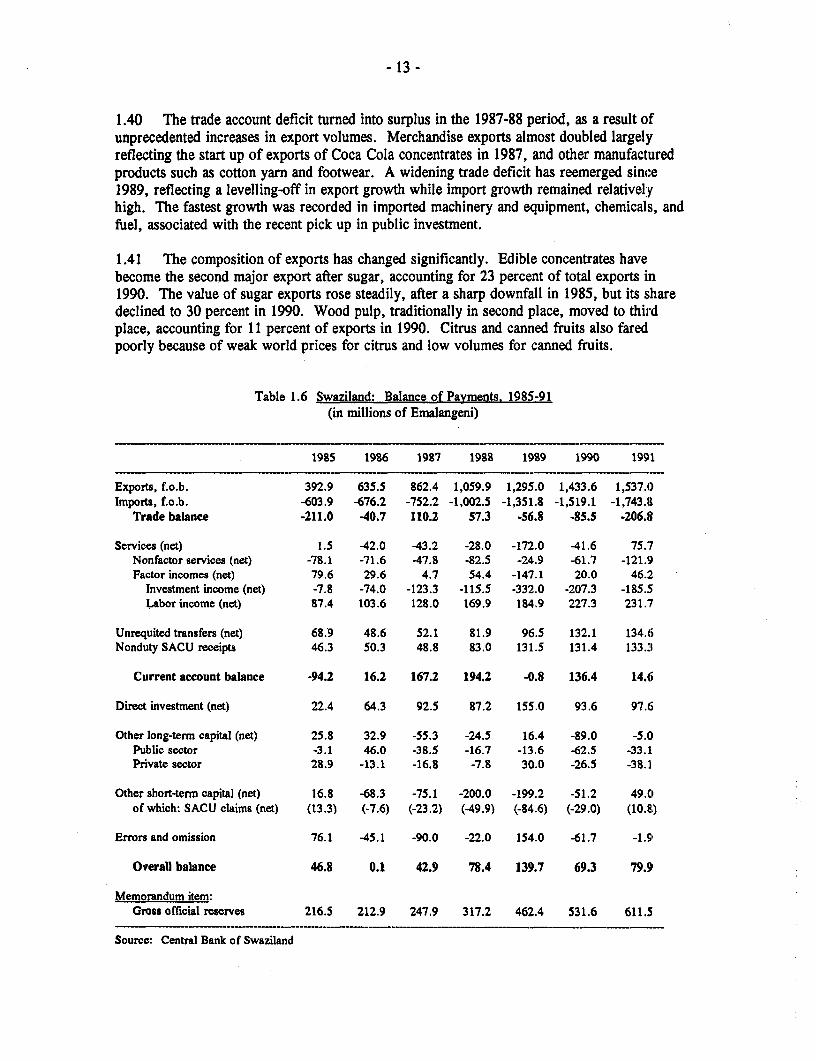

osur

e A

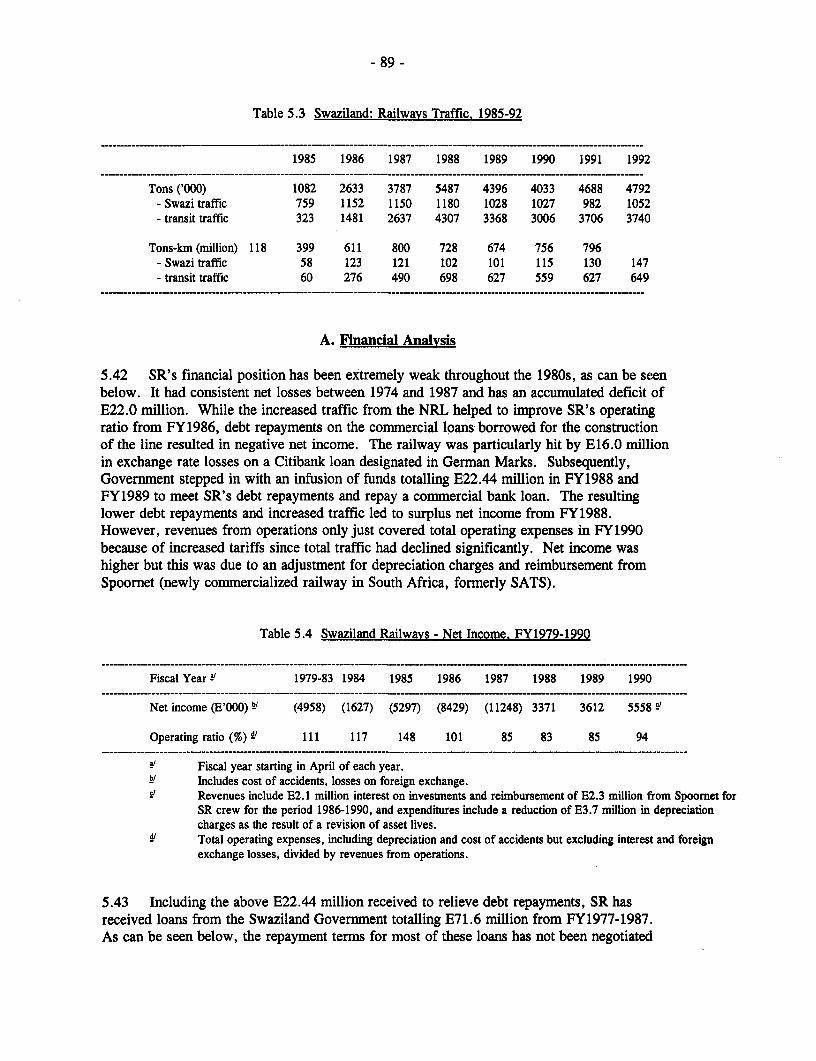

utho

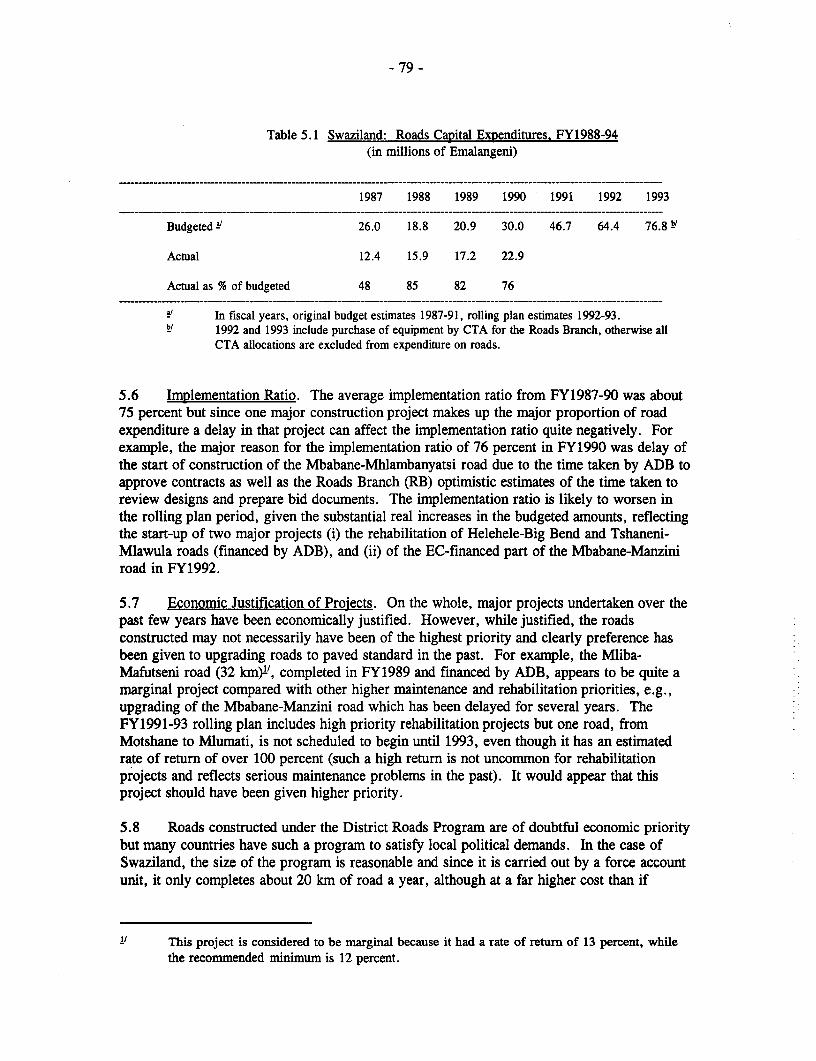

rized

Pub

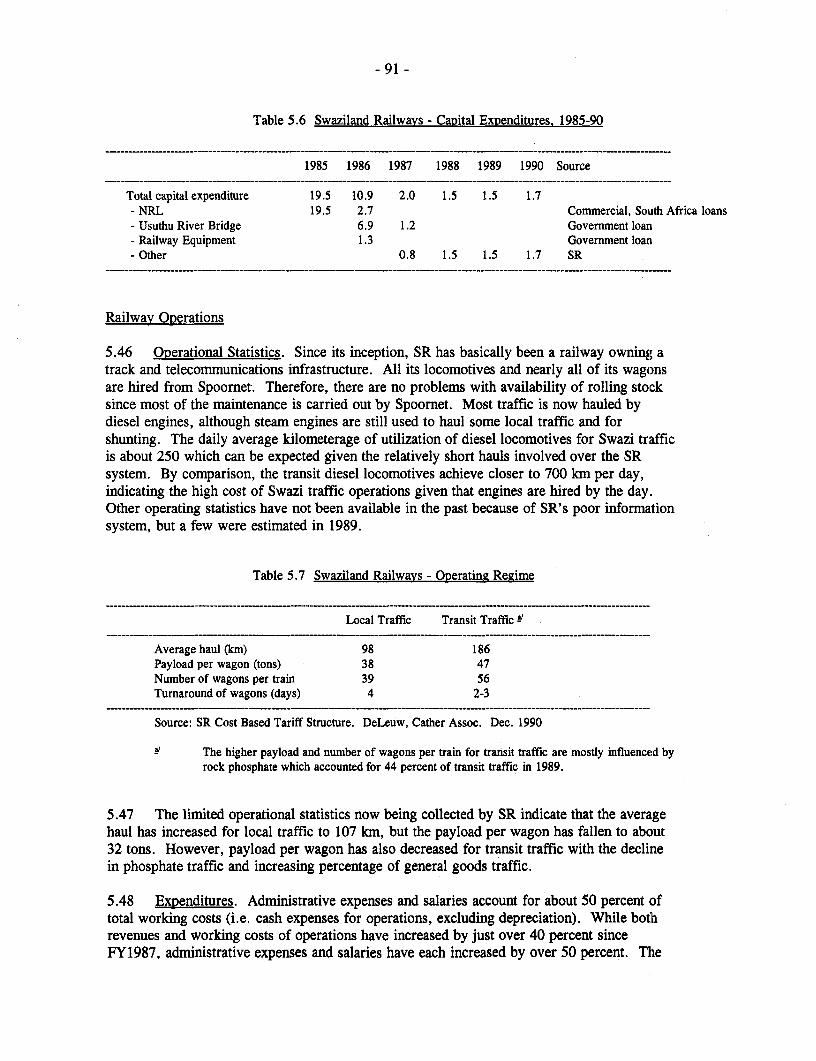

lic D

iscl

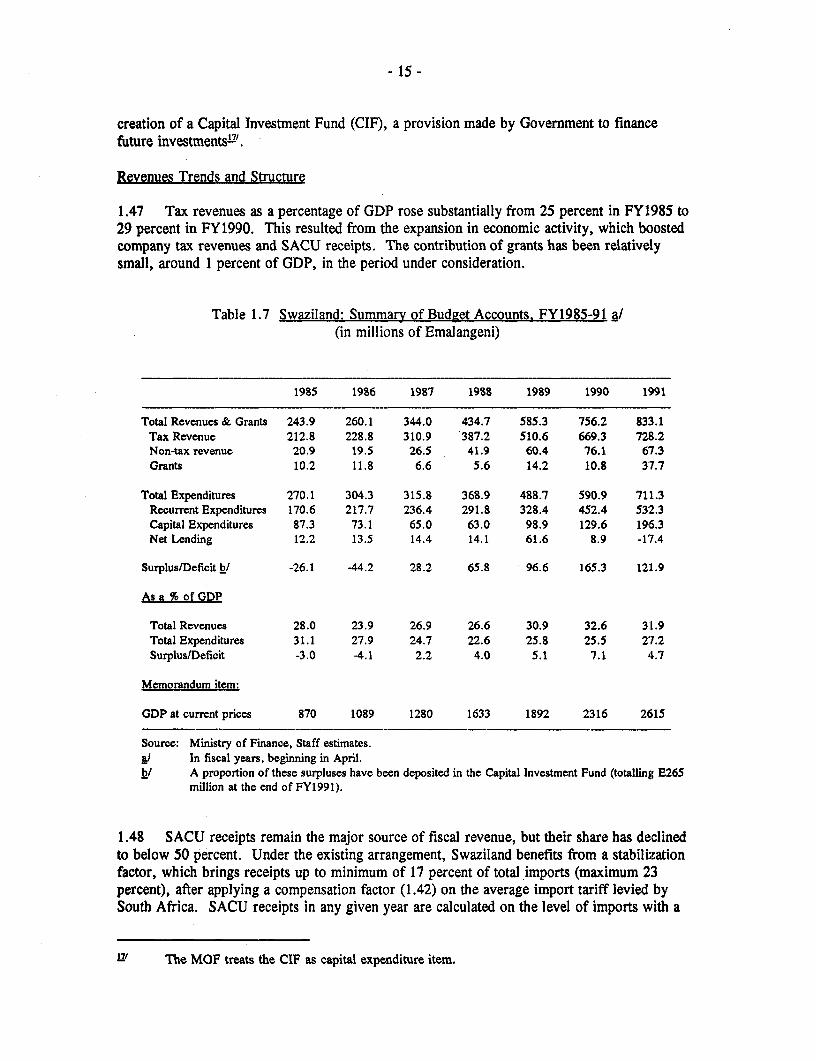

osur

e A

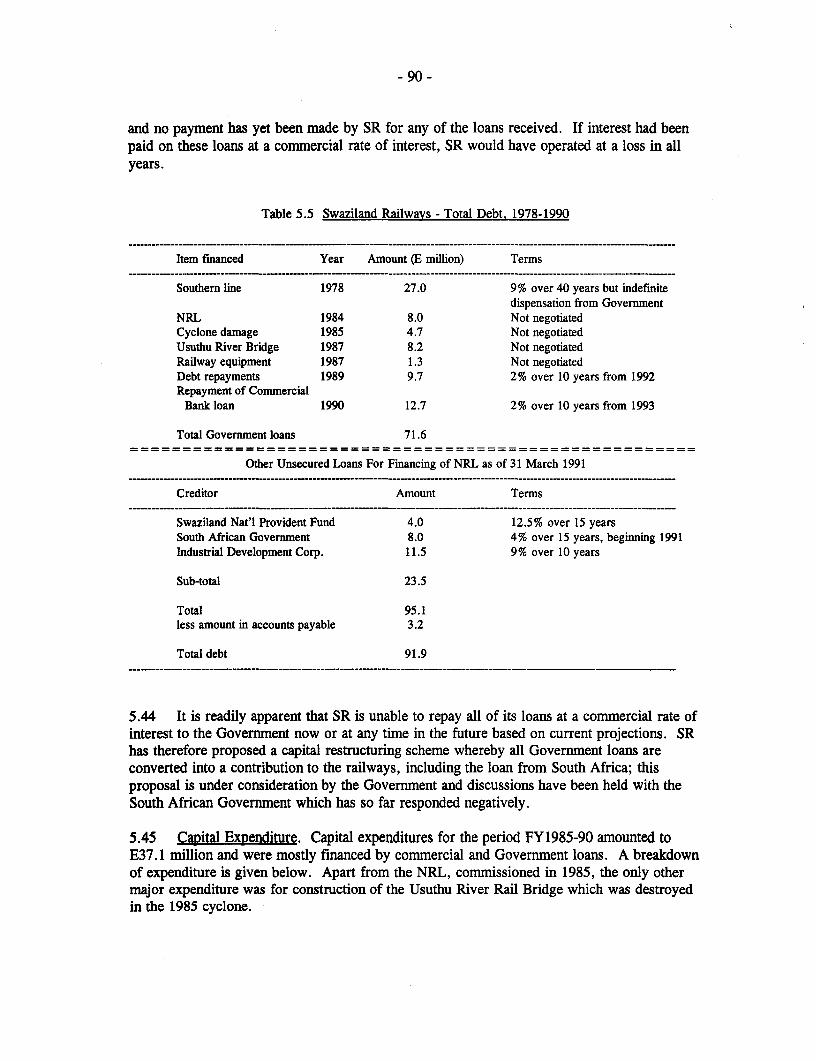

utho

rized

Pub

lic D

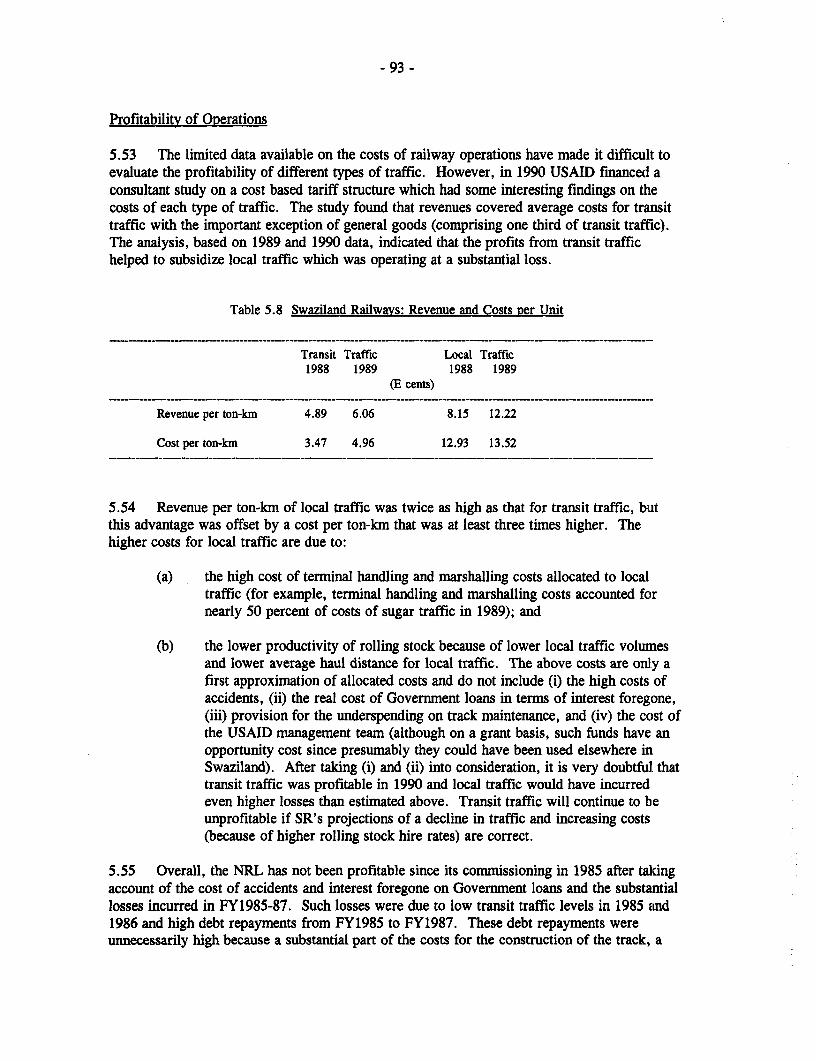

iscl

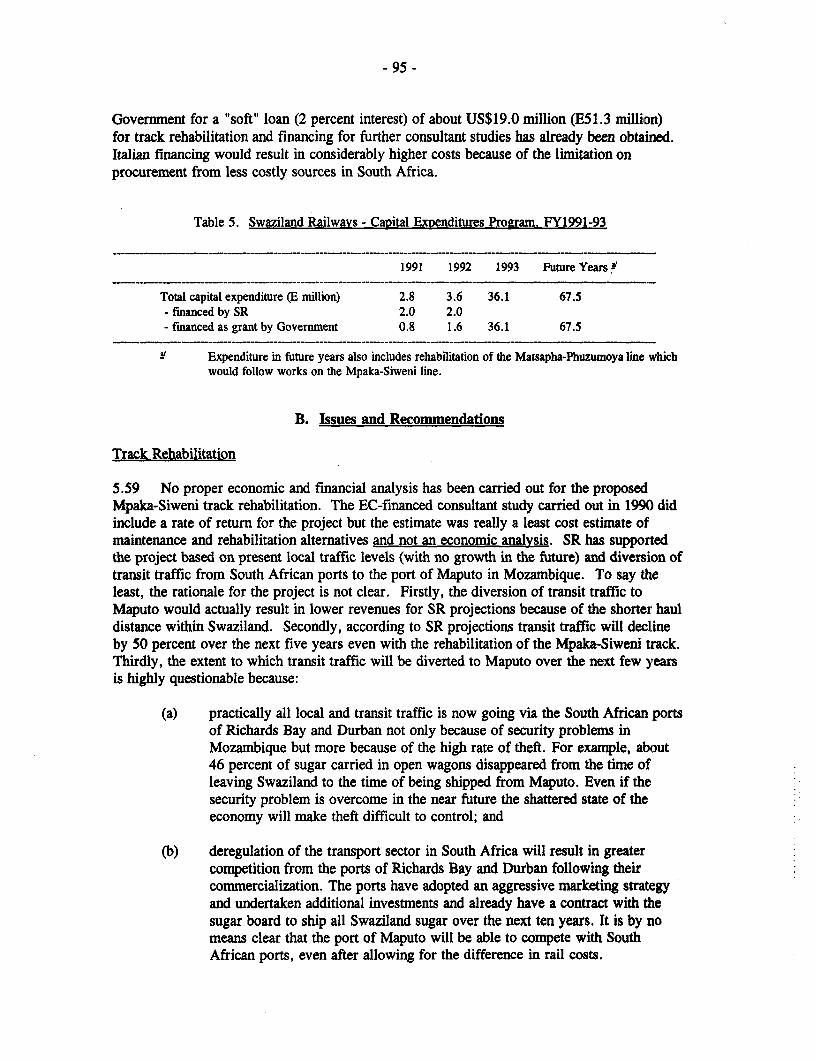

osur

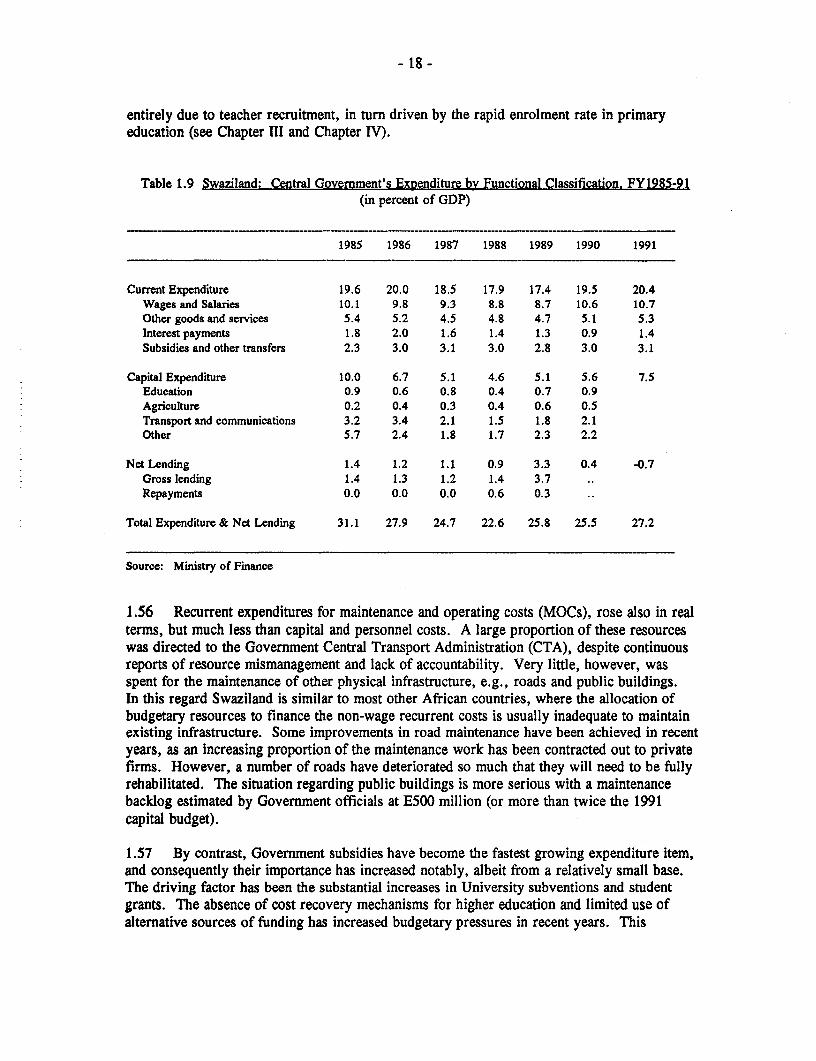

e A

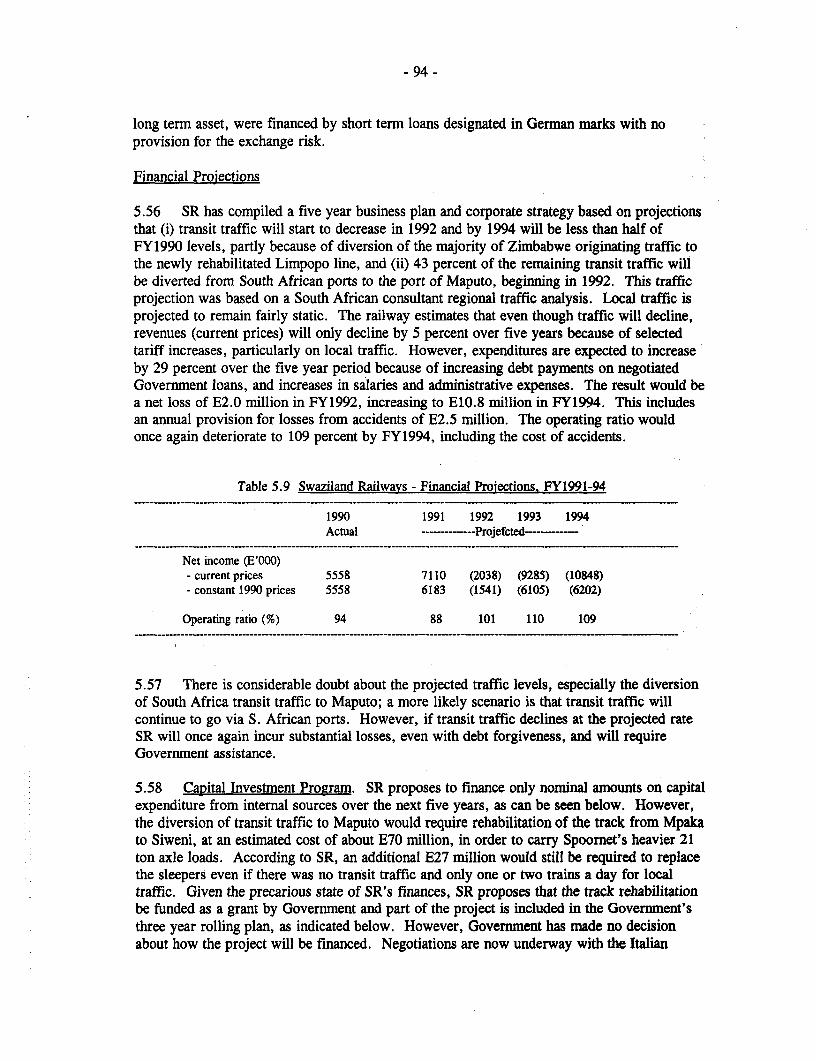

utho

rized

Pub

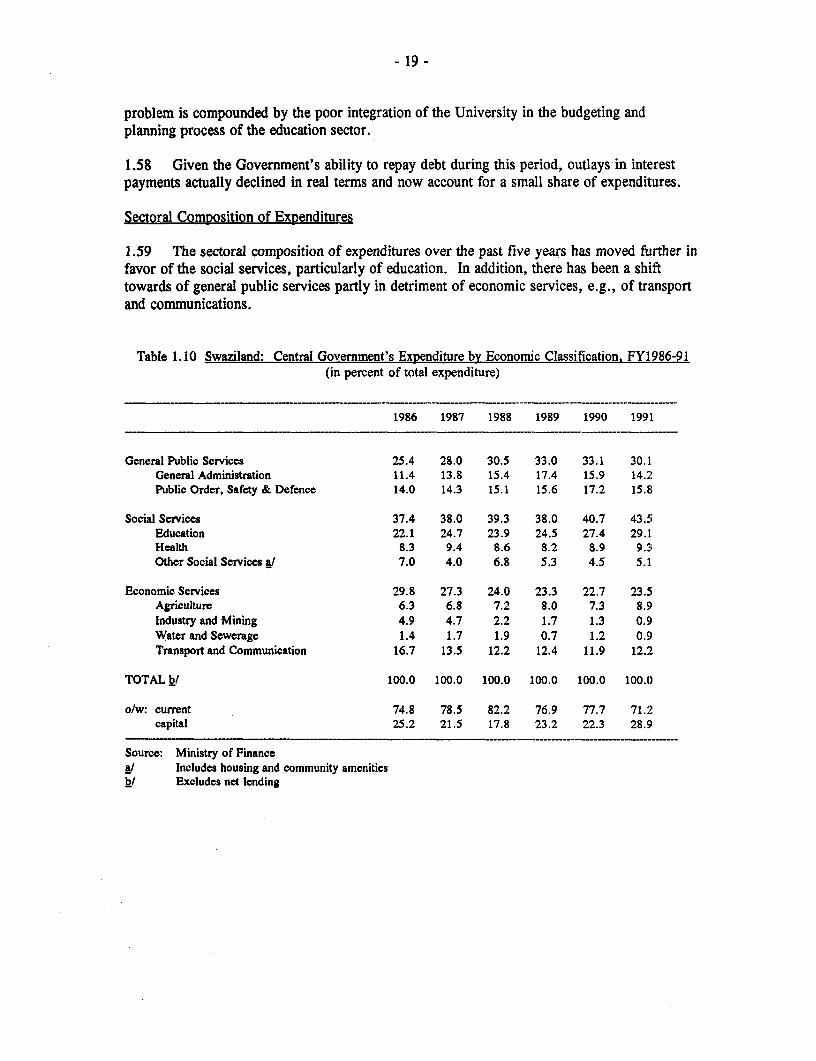

lic D

iscl

osur

e A

utho

rized

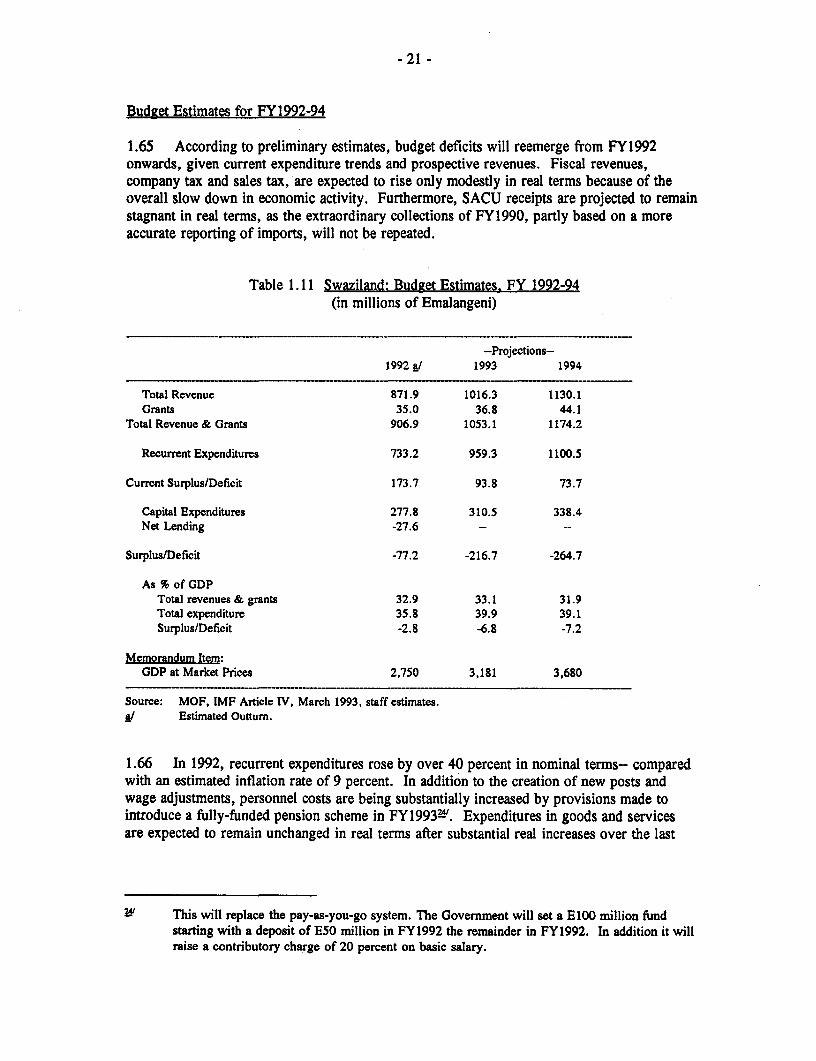

CURRENCY EQUIVALENTSUSD 1.00 = 2.7 Emalangeni

Fiscal Year: April 1 to March 31

ABBREVIATIONS AND ACRONYMS

ADB African Dvelopment BankCBPMS Capital Budgeting, Planning and Monitoring SystemCBS Central Bank of SwazilandCEF Capital Investment FundCMA Common Monetary AreaCSO Central Statistical OfficeCTA Central Transport AuthorityCTA Central Transport AdministrationCTB Central Tender BoardEAU External Assistance UnitEC European ConununityEFAs External Financing AgenciesEPO Economic Planning OfficeESKOM South African Electricity CommissionHIID Harvard International Institute of DevelopmentLAM Mozambique AirwaysLRMC Long-Run Marginal CostsMEPD Ministry of Economic Planning DevelopmentMHUD Ministry of Housing and Urban DevelopmentMNLUE Ministry of Natural Resources, Land Utilization and EnergyMOE Ministry of EducationMOF Minsitry of FinanceMOLPS Ministry of Labor and Public ServiceMOW Ministry of WorksMOWC Ministry of Works and CommunicationsMPUs Ministerial Planning UnitsMT Ministry of TransportNATCAP National Technical Corporation Assessment and ProgramNERCOM National Education Review CommissionNIDC National Industrial Development CorporationNRL Northern Rail LinkNWA National Water AuthorityPBC Planning and Budgeting CommitteePEU Public Enterprise UnitPTC Post and Telecommunications CorporationPU Planning UnitRB Roads BranchRRA Recruitment and Retention AllowanceRWSB Rural Water Supply BoardSACU Sothern AFrica Customs UnionSATS South African RailwaysSCOT Swaziland College of TechnologySEB Swaziland Electricity BoardSEDCO Small Enterprise Development CompanySIDC Swaziland Industrial Development CompanySIHS Swaziland Institute of Health SciencesSIMPA Swaziland Institute of Management and Public AdministrationSNACS Swaziland National Association of Civil ServantsSNAT Swaziland National Association of Civil TeachersSNL Swazi Nation LandSR Swaziland RailwaysTCS Technical Cooperation SectionTDL Title Deed LandTEC Total Estimated CostUPS Uninterruptible Power SupplyVAT Value Added TaxVOCTIM Vocational Training Institute MatsaphaWSB Water and Sewage BoardZC Royal Swazi National Airways

FOR OFFICIAL USE ONLY

Preface

This World Bank Report is based on the findings of a mission to Swaziland inOctober 1991. The Bank mission comprised Rocio Castro (mission leader), Peter Fallon andAnna Muganda from AF6CO, Melody Mason, Christopher Joubert, and Gavin Maasdorp(Consultants). In addition, Asamenetch Fantaye (AF6IN) prepared the Chapter on the Waterand Sewerage Board and Caroline Sullivan (Consultant) contributed to the Chapter on thLeSwaziland Electricity Board. Mike Stevens, adviser from OPRPG, provided valuableguidance throughout the preparation of the report. The green cover draft of the Report wasdiscussed with the Swaziland authorities in February 1993.

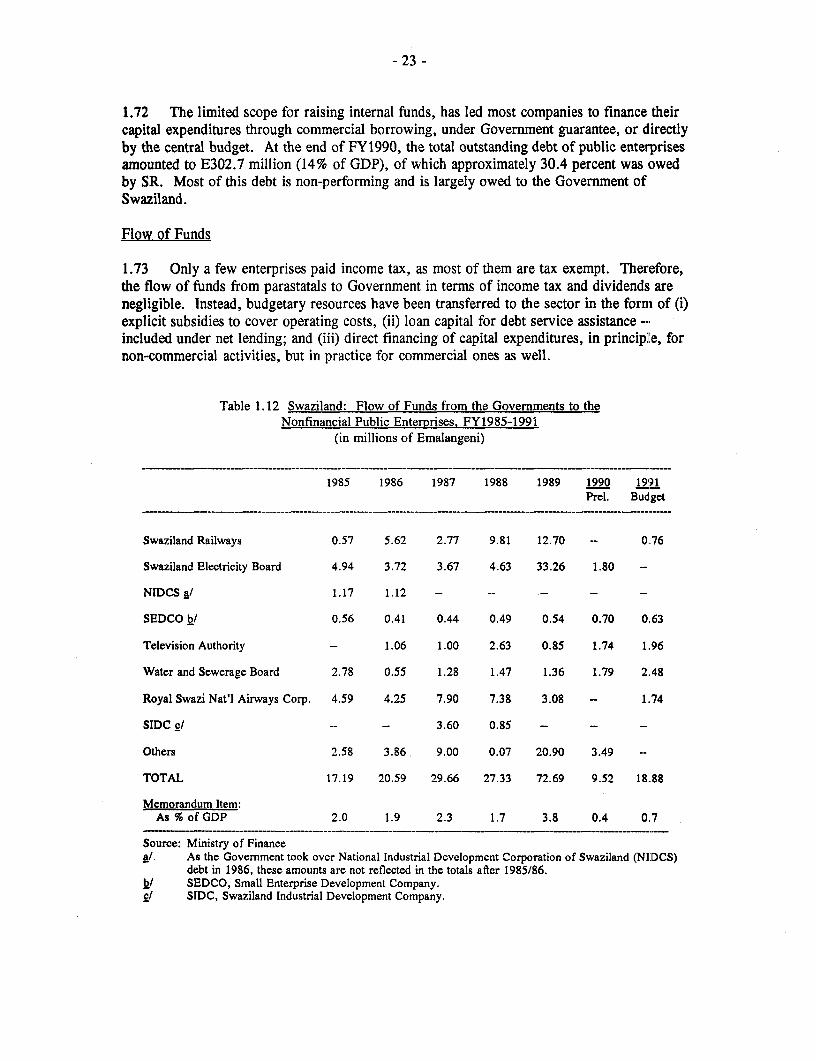

This document has a restricted distribution and may be used by recipients only in theperfornance of their official duties. Its contents may not otherwise be disclosed withoutWorld Bank authorization.

TABLE OF CONTENTS

Pape

EXECUTIVE SUMMARY ................................... i--xv

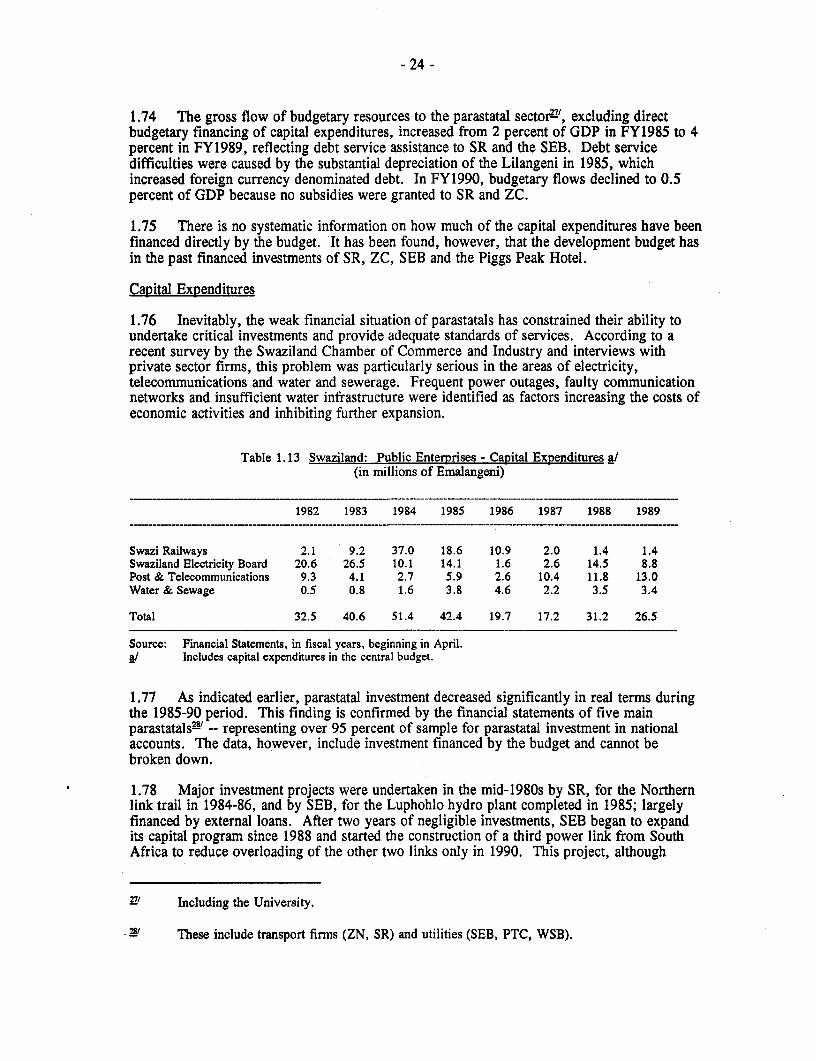

I. MACROECONOMIC FRAMEWORKIntroduction ..A. Output, Demand and Employment Trends. 2B. Prices and Wages .10C. Money and Credit .11D. External Trade and Payments .12E. Public Sector Finance .14F. Conclusions and Recommendations .25

II. PUBLIC SECTOR MANAGEMENTIntroduction ............. ............. 29A. Institutional Setting ............................ 29B. The Development Planning System ........... .......... 30C. Institutional Issues . ........................... 40D. External Financing Issues ........................... 42

III. PUBLIC PAY AND EMPLOYMENT ISSUESIntroduction ............... .... 43A. The Size and Composition of Public Sector Employmen4 .... ... 46B. Public Sector Pay .......... ...................... 47C. Policy Analysis .......... ....................... 53

IV. EDUCATION SECTORIntroduction ............. ............. 56A. Financial Analysis ............................ 56B. Analysis of Performance Indicators ............ ......... 63C. Policy Considerations ........................... 63D. Conclusions and Recommendations ............ ......... 74

V. TRANSPORT SECTORIntroduction ............ ............ 781. Roads Sub-Sector .......... .............. 78

A. Budgetary Expenditures ......................... 78B. Issues and Recommendations ....................... 81

2. Swaziland Railways .............. ........... 88A. Financial Analysis ......................... 89B. Issues and Recommendations ....................... 95

3. Royal Swazi National Airways ........................ 99

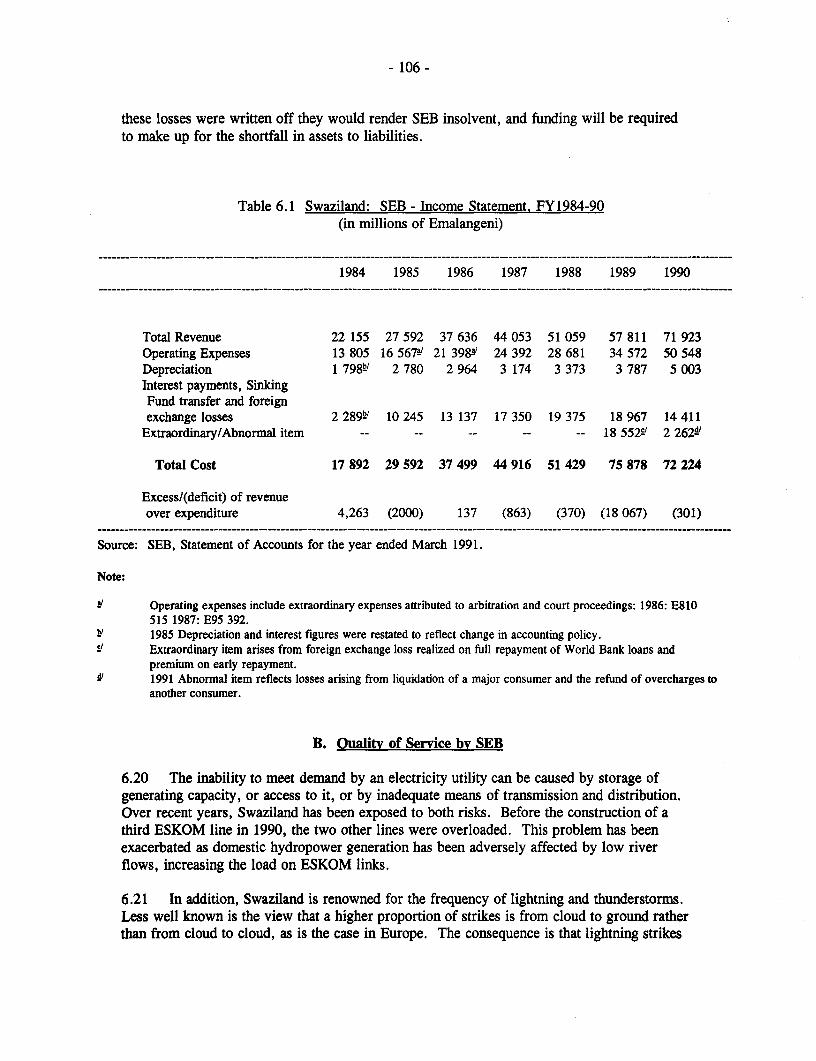

VI. SWAZILAND ELECTRICITY BOARDIntroduction .... ............... 103A. Operating Regime ................... 103B. Quality of Service by SEB ......... .......... 106C. Capital Expenditures ...... ............. 108D. Management Systems ...... ............. 109E. Conclusions. ................................... 113

VII. WATER AND SEWERAGE BOARDIntroduction ....... .......... 115A. Intersectoral Allocation ................. 116B. Financial Performance ................. 117

ANNEXES

Annex I - Macroeconomic DataAnnex II - Education Sector Data

SWAZILAND

PUBLIC EXPENDITURE REVIEW1 '

EXECUTIVE SUMMARY

Swaziland faces the prospect of a serious deterioration in its budgetary situationunless timely measures are adopted to control the level of expenditures and improve overallpublic sector efficiency. An upsurge in economic activity experienced in the late 1980s, ledto substantial increases in fiscal revenues and large budget surpluses. On this basis,expenditures have been allowed to increase at a rapid pace but will be not be sustainable inthe medium term as economic growth has now levelled-off. Furthermore, given theuncertain regional situation, fiscal revenues are highly vulnerable to (i) changes in theSouthern African Customs Union (SACU) 2', which finances about half of the budge, and(ii) the stability of foreign investment flows which spurred the economic boom of the late1980s in the wake of the tightening of sanctions against South Africa.

Main Economic Features

1. Swaziland is a small landlocked country bordered mainly by South Africa with apopulation of around 800,000. Membership in SACU and the Common Monetary Area(CMA) have further reinforced economic ties with South Africa, which accounts for 80 and30 percent of merchandise imports and exports, respectively. In addition, workers'remittances, mostly from Swazis employed in South African mines, represent over 15 percentof GNP.

2. The economy relies on agro-forestry based activities, under a dualistic land ternuresystem. This comprises (i)a highly developed commercial subsector, dominated by capitalintensive export oriented industries, e.g., sugar and wood pulp, developed by foreign privatecapital; and (ii) a basically stagnant smallholder subsector, characterized by semi-subsistenceproduction, communal grazing and traditional tenure on the Swazi Nation Land (SNL); withlow productivity and vulnerable to droughts and changes in rainfall patterns.

3. As a small open economy, Swaziland is highly vulnerable to external shocks andsubject to wide fluctuations, typically related to changes in goods/factor flows with SouthAfrica, commodity prices and, climatic conditions. Fiscal revenues have fluctuated wiitheconomic activity while public expenditures have been rather countercyclical, e.g., higher inyears of low economic growth, not as a deliberate measure, but because they have tended tolag behind revenue changes.

IBRD lending operations with Swaziland have been inactive since the mid-1980s. This presentreport constitutes the first economic work prepared by the World Bank in several years. Thelast Country Economic Memorandum (CEM) was published November 1, 1985.

In addition to South Africa, SACU members include Botswana and Lesotho and CMA, includesNamibia and Lesotho.

- ii -

5. Since real GDP growth has, on average, outpaced population growth, per capitaincomes have increased overtime, albeit with fluctuations. Thus, with a per capita GNP ofUS$840, Swaziland falls in the category of a middle income country 3/. However, becauseof its dual system, income distribution is probably fairly uneven. Furthermore, formal sectorwages are high relative to per capita GDP, partly reflecting labor mobility with South Africa,which ultimately exerts pressures on civil service wages.

6. Swaziland's good growth record has, so far, been based on a market oriented policyand a relatively prudent fiscal stance. First, favorable conditions for foreign investment,including political stability, a number of fiscal incentives, and liberal regulations on profitremittances, have been the basis for the development of a large, mostly South African based,private sector. Second, the pursuance of a cautious fiscal policy, avoiding large budgetdeficits and limiting the size of the public sector, has ensured a stable macroeconomicframework.

7. However, Swaziland's growth outlook is colored by a great deal of uncertainty overthe future of South Africa. In addition, the fiscal situation could deteriorate rapidly as aresult of fast spending, stagnating revenues and financial pressures from the parastatal sector.

A. The Macroeconomic Framework

Recent Economic Developments

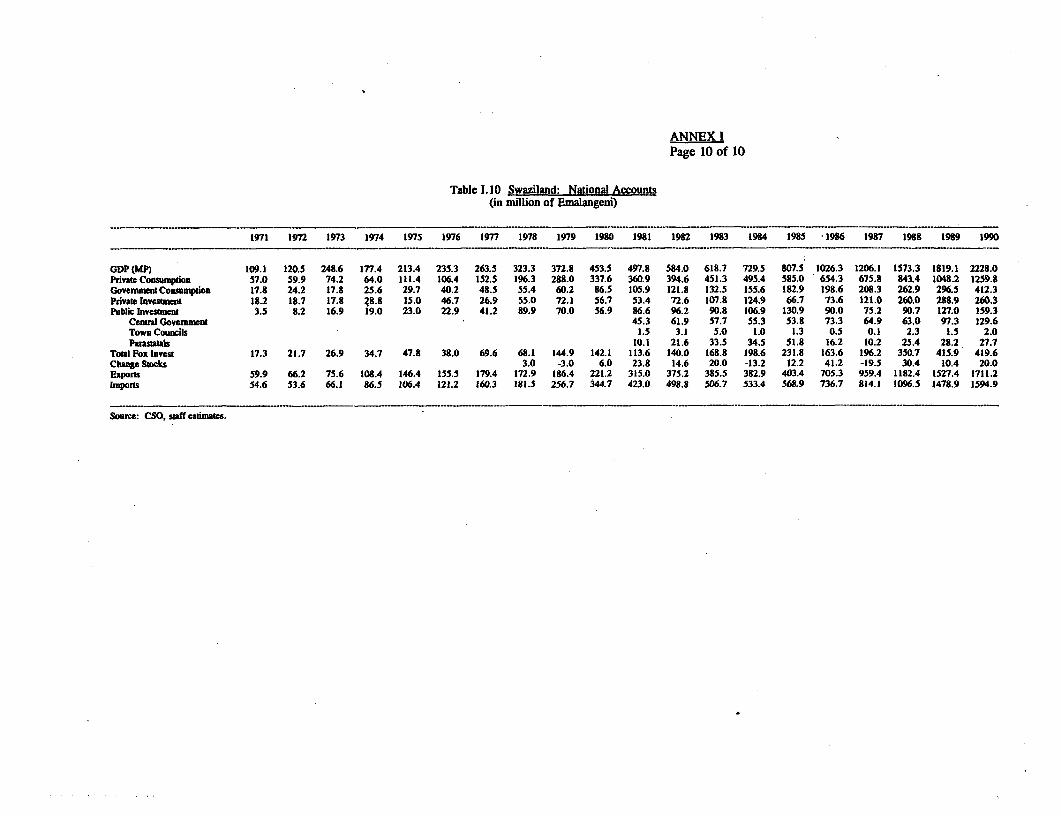

8. The Swazi economy expanded by over 5 percent per annum in real termis during thesecond half of 1980s. Real GDP growth peaked in 1986-87, at 8 percent per annum, led by aan impressive 35 percent annual increase in manufacturing output 4/. This reflected mainlythe relocation of key investments into Swaziland prompted by the tightening of sanctionsagainst South Africa. Improved export prices for sugar, reinforced by the depreciation of theLilangeni, and favorable weather conditions were also contributing factors. With the onset ofanother recession in South Africa, economic growth has recently slowed and foreigninvestment is now half the level reached in 1989. In 1992, real GDP fell by an estimated 2percent as a result of the severe drought affecting the region.

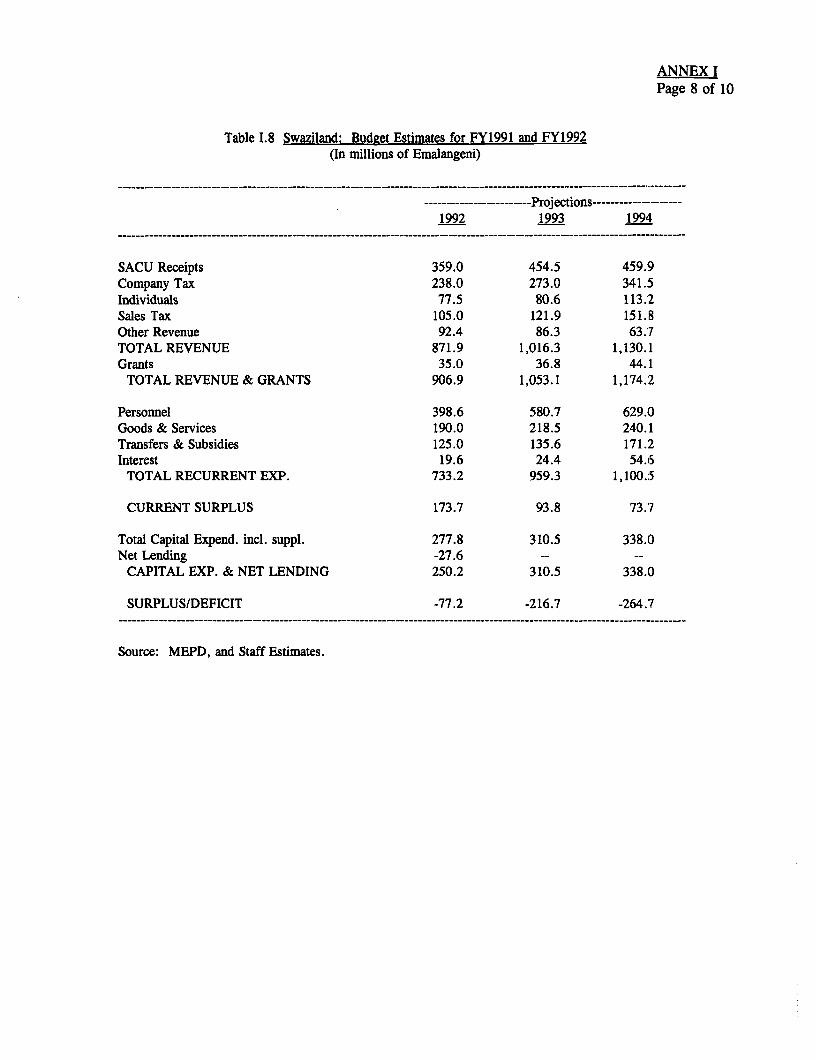

9. In line with the expansion in economic activity fiscal revenues boomed, notablycompany tax and SACU receipts, which combined with lagging expenditures resulted in largebudget surpluses in the 1987-91 period. However, budgetary deficits are expected to re-emerge from 1992 onwards, as modest revenue increases resulting from slackening economicactivity will be outpaced by increasing personnel and capital expenditures.

10. The balance of payments position was strong during the second half of 1980s as grossforeign reserves continued to build up despite substantial short term capital outflows triggeredby interest rate differentials with South Africa. Since 1988, the Central Bank has deliberatelykept interest rates below those in South Africa with the objective of encouraging investment

2' As of 1990, based on World Bank Atlas methodology.

Based on staff estimates, see Chapter 1.

- iii -

and reducing banks' liquidity. While banks' liquidity has actually been reduced, this policyhas failed to promote productive investment because the deposit structure resulting fromnegative real interest rates has favored short term lending, and interest differentials haveencouraged capital flight. As interest differentials are narrowed, this trend is gradually beingreversed.

Growth Trends and Development Constraints

11. There is concern about the long term sustainability of economic growth in SwaLziland,not only because of the unstable nature of the factors behind the economic upswing of the late1980s, but also given recent trends in other macroeconomic aggregates. In particular, thedecline in investment relative to GDP and the growth trend in wage employment.

12. The investment to GDP ratio decreased to an average of 20 percent in the late 1980s,from 30 percent the previous decade. In particular, public investment fell sharply as a resultof expenditure lags by central Government and serious financial difficulties faced by keypublic utilities. Private investment to GDP also decreased, albeit less markedly, despite theexceptional inflow of foreign investment experienced in the late 1980s. Moreover, followinga 50 percent nominal contraction in 1990, foreign investment has stagnated thereafter,suggesting that the recession in South Africa may play a determining role in the long run.

13. Another important indicator concerns the long term growth of wage employmentcompared to the labor force. In the 1980s, growth in wage employment was down to anannual average of only 2.2 percent, from 5.9 percent in the 1970s, and compared with anestimated labor force growth of 2.7 percent. This suggests that the level of unemployment inthe formal sector must be increasing.

14. The development of Swaziland will remain closely linked to South Africa. Thus, itsability to sustain economic growth and overall macroeconomic stability may be impaired byadverse developments in that country. While this dependence may limit Swaziland's scope tosustain investment and output growth, Government policy has a critical role in shaping theincentive structure for factor allocation of capital, labor, and land; through taxation and othernon-price regulations. Furthermore, Government can contribute to enhance the efficiency offactor use through investment in human resources and productive infrastructure. Thus, froma microeconomic perspective, active Government intervention is required in terms of:

(a) Human Resources. Despite Swaziland's success in expanding its educationsystem, overall quality is poor and consequently labor productivity, lo'w.Management and professional skills are in short supply and many keypositions in both private and public sector are filled by expatriates.

(b) Land. Limited flexibility for the commercial utilization of traditional land,the SNL, inhibits further development of agricultural activities and economicinfrastructure, including a housing market.

(c) Relative Factor Prices. It can be argued that current relative factor costs,tend to favor capital intensive techniques in the formal sector. Therefore,some incentive adjustments could be made to encourage more labor intensiveinvestments in the private sector.

- iv -

(d) Infrastructure. This aspect as well as (a) are concerned with the role of theGovernment as a provider of public services. As explained below, in manyinstances the government's expenditure program has not adequately respondedto the economy's needs in terms of maintenance, rehabilitation anddevelopment of physical infrastructure.

15. The country's development constraints must be addressed in the context of an updatedlong term strategy which defines priorities and policy options open to the country in themedium to long term. In this respect, the Government's decision to prepare a nationaldevelopment plan provides a suitable framework to undertake this task.

16. The national development plan should identify future sources of sustainable economicgrowth and the mechanisms for the efficient mobilization and use of public and privateresources. A few considerations need to be taken into account:

(a) The maintenance of appropriate levels of investment is a necessary but notsufficient condition for sustainable growth. Greater emphasis should be givento the quality of these investments, e.g., in terms of enhancement ofproductive infrastructure (public investment).

(b) The efficiency of public sector spending, both recurrent and capital, should beassessed within a well-defined framework of national and sectoral priorities,and taking into account existing macroeconomic constraints.

(c) Efficient mobilization and use of private resources requires appropriate priceincentives, including interest and taxation rates. In this regard, it is importantpositive real interest rates be restored, so as to reflect more closely theopportunity cost of capital, thereby promoting efficient financialintermediation.

17. The objective of this study has been twofold: first, to evaluate the sustainability offiscal expenditures from a macroeconomic perspective and second, the efficiency of publicexpenditures with particular emphasis on education and productive infrastructure, both ofwhich have been identified as potential constraints for future development.

B. Public Sector Expenditures

18. In view of the vulnerability of fiscal revenues to uncertain prospects for economicgrowth and SACU, and current expenditure trends, the Government will need to adopt criticalmeasures both to ensure sustainability and improve the efficiency of public expenditures.Otherwise, Swaziland faces the risk of undergoing even harsher stabilization measures andwasting scarce resources in the medium term.

Sustainability of Expenditures

19. The size of Government expenditures relative to GDP, about 30 percent of GDP in1991, is comparable with other countries in the region and other SACU members which have

also a large private sector 5/. However, the scope for increasing or even maintaining publicspending relative to GDP is constrained by two key factors: (i) limited prospects to raiserevenues in the medium term, (ii) the posibility of a reduction/elimination of extraordinaryreceipts obtained under SACU, representing roughly 5 percent of GDP or 20 percent of fiscalrevenue.

20. In 1992, expenditures jumped to 36 of GDP and are estimated to rise further to 40percent in 1993-94. With revenues expected to remain at around 33 percent, there is clearlyan issue of medium term sustainability if expenditure trends remain unchanged. The issue ofsustainability is further underscored by uncertainty over the future of SACU. In the mediumto long term, SACU receipts could be adversely affected by changes in the sharing agreementparticularly concerning the stabilization clause. Under this clause, Swaziland has received asa minimum 17 percent (maximum 23 percent) of total imports Y. This band could bereduced in the context of lower tariffs in South Africa and prospects of broadening its tradeagreements with other countries in the region.

21. On the revenue side, further measures need to be taken to reduce Swaziland'svulnerability to external shocks and possibly a downward adjustment in SACU receipts. Inthis regard, consideration must be given to the following aspects:

(a) Swaziland's ability to generate fiscal revenues in the long term will dependultimately on its capacity to attain sustained economic growth. From thispoint of view, the preparation of a long term development strategy, will helpto identify future sources of growth as well as appropriate incentivemechanisms. The tax structure itself, is an important element of the incentivemechanism and should be considered in that light.

(b) In view of the introduction in 1991 of a Value Added Tax (VAT) in SouthAfrica, Swaziland might need to adopt a similar system in order to avoid widediscrepancies in relative prices compared with South Africa. An evaluation ofthe economic and fiscal impact of introducing a VAT in Swaziland, to replacethe sales tax, needs to be made at the earliest opportunity.

(c) In addition, greater emphasis should be given to expanding the revenue basethrough cost-recovery mechanisms at all levels of Government service:s byraising/introducing charges and user fees, which now represent a smallproportion of total revenues. This will contribute to enhance efficiency.

22. The sterilization of past budgetary surpluses, through the Capital Investment .Fund(CIF), is a right step to cushion the impact of economic fluctuations, but will not be enoughto address longer term issues. Therefore, the Government should pursue a cautious fiscal

Compared for example with Lesotho (31 percent) and Botswana (39 percent).

SACU receipts are calculated applying a compensation factor (1.42) to the average importtariff levied by South Africa. Under the stabilization clause, receipts must fall within a bandof 17 to 23 percent of total imports with a two year lag. Typically, Swaziland has receivedthe lower end of the band.

- vi -

policy, emphasizing sustainability issues both with regard the central Governmentexpenditures and the parastatal sector.

23. The level of expenditures must be kept in line with the revenue base, which is notlikely to exceed 33 percent of GDP in the medium to long term. Priority must be given tolimiting the expansion of the wage bill through a prudent employment and wage policy. Inaddition, the Government needs to review its housing policy, which has implications for therecurrent and capital budget, and to take more into consideration the recurrent costs of itscapital program.

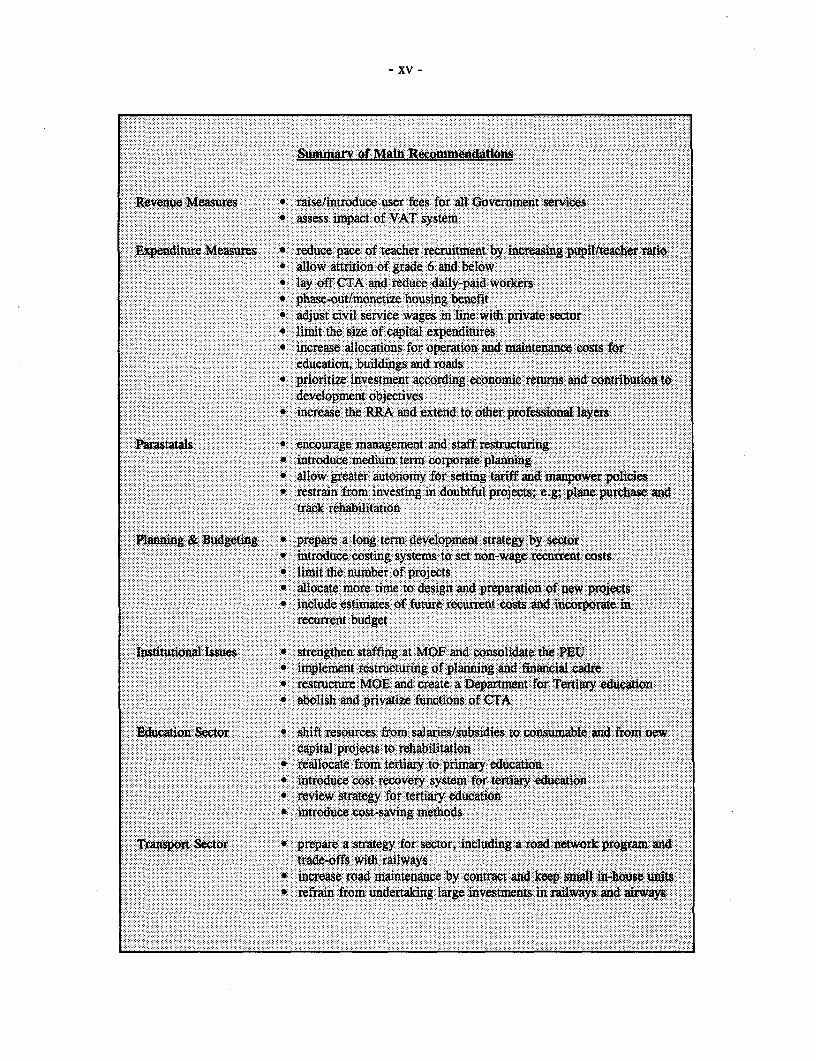

(a) Employment policy. A tight rein must be kept on the size of the civil service,which is large by international standards, through (i) reducing the pace ofteacher recruitment. This would imply an increase of the pupil/teacher ratiowhich at present is lower than other countries and the recommended norm; (ii)allowing posts at grades 6 and below to decline with natural wastage until astaffing reduction of one third in numbers have been achieved; (iii) laying-offstaff at the Central Transport Administration (CTA); and (iv) reducing thenumber of casual/daily paid workers.

(b) Wage Policy. Pay adjustments for most categories should be limited to paymovements in the private sector, while efforts should be made to narrow thesalary gap with the private sector for highly skilled civil servants.

(c) Housing Policy. The housing benefit for civil servants should be radicallyreviewed alongside measures to promote the development of a housingmarket. The provision of houses should be restricted to civil servants inremote areas, while the housing benefit should be monetized accross theboard: wage adjustments could be financed by raising all rents to marketvalues. This will eliminate inequities arising from the fact that many civilservants do not receive housing but a comparatively lower allowance. Thismeasure should be phased over several years to smooth out budgetarypressures and the impact of a redistribution in real incomes from civil servantscurrently receiving a house to those who receive an allowance.

(d) Capital Expenditures. The level of capital expenditures must be kept undercontrol, taking more fully into account (i) future recurrent costs; (ii) theimplementation capacity of the country; and (iii) the need to address thebuilding maintenance backlog, officially estimated at E500 million or twice thetotal capital budget for FY1991.

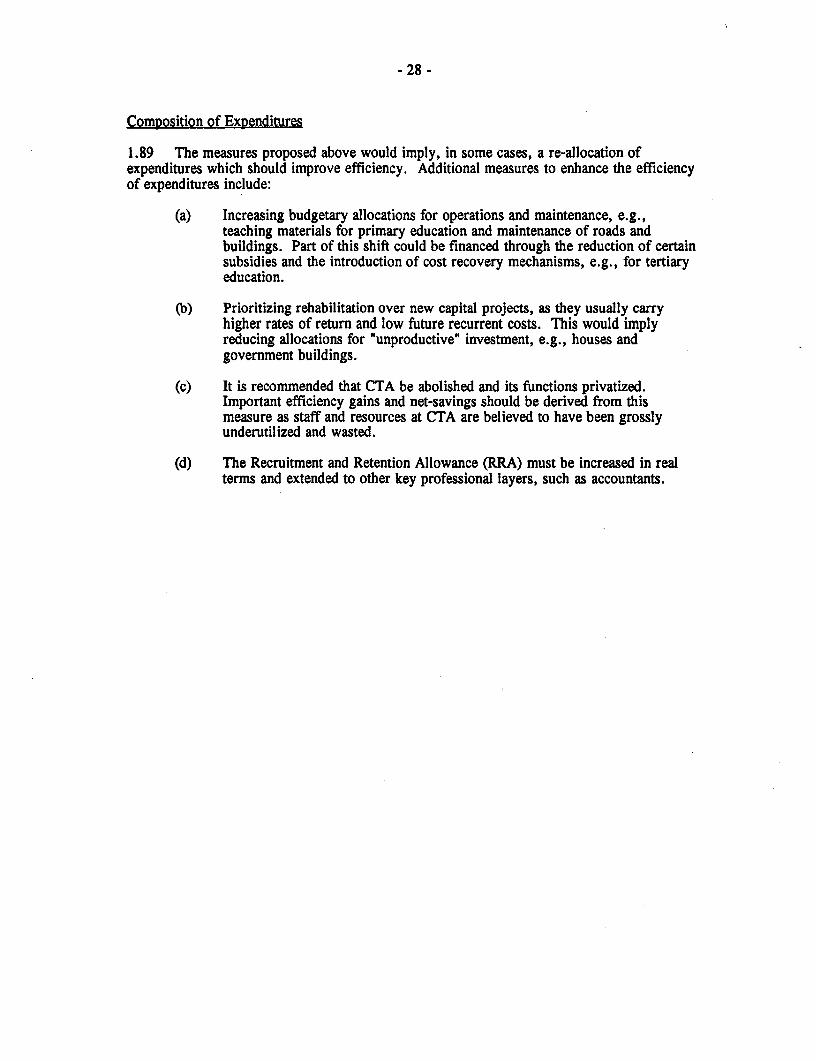

24. In particular, given the size of the proposed Komati River Basin Project, costed atE547 million, with a budgetary contribution of E276 million, additional studies need to beundertaken to establish the economic viability and appropriate phasing of the project.

25. In addition, it is critical that the posible financial impact of the parastatal sector beexplicitly factored in the central Government budgetary projections, particularly given thedifficulties faced by key public enterprises.

- vii -

Parastatal Subsector

26. The financial situation of key parastatals has been reflected in the significant level ofoperating losses accumulated over the years. Major loss making companies include; RoyalSwazi National Airways (ZC), Swaziland Electricity Board (SEB), Swaziland Railways (SR)and Water and Sewerage Board (WSB).

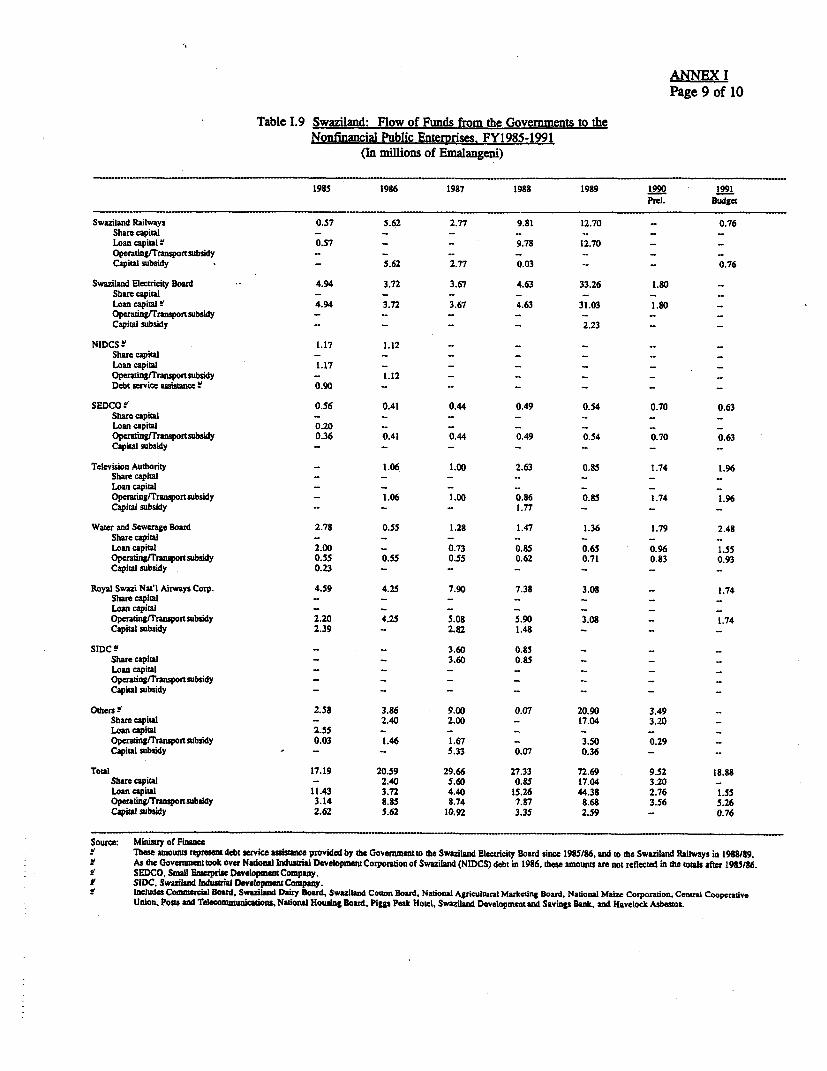

27. The flow of funds from parastatals to Government in terms of income tax anddividends are negligible. Instead, budgetary resources have been channelled to the sector inthe form of (i) explicit subsidies to cover operating costs, (ii) loan capital for debt serviceassistance--included under net lending; and (iii) direct financing of capital expenditures.

28. The gross flow of budgetary resources to parastatals, excluding direct financing ofcapital expenditures by the budget, increased from 2 percent of GDP in FY1985 to 4 percentin FY1989, reflecting debt service assistance to SR and the SEB. Debt service difficultieswere caused by the substantial depreciation of the Lilangeni in 1985, which increased foreigncurrency denominated debt.

29. According to proposed plans, investment requirements of five key parastatals ( ZC,SEB, SR, WSB and Post and Telecommunications Corporation - PTC) are projected at aboutE400 million over the next 3 to 4 years. Some of these investments such as the rehabilitationof the rail track (E70 million) and the acquisition of a new plane (E150 million) are ofdoubtful economic benefit and threfore should not be undertaken.

30. Most of these parastatals are highly indebted and would not be able to finance futurecapital expenditures unless they substantially improve their financial situation. In the interimperiod, they constitute a potential burden for the Government budget. In order to improve theperformance of parastatals, priority must be given to the following aspects:

(a) Management and staff restructuring. Lack of qualified managers at thefinancial and technical level are a key source of inefficiency in parastatals, andfirms face serious problems in recruiting and retaining highly qualifiedpersonnel.

(b) Introduction of medium term corporate planning. Most parastatals havelacked a medium term framework to assess their capital programs, andtherefore a strategic view to guide decision making. However, a number ofparastatals have now began to prepare corporate plans and this practice: shouldbe reinforced.

(c) Greater autonomy for setting tariffs and manpower policies. Ministerialapproval is needed for both tariff and salary adjustments but decisions aremade sometimes on political grounds and without the required technicalexpertise.

31. In 1989, the Public Enterprise Unit (PEU) was created at the Ministry of Finance(MOF), with the objective of establishing performance criteria for the parastatal sector. ThePEU has taken a number of positive steps including the liquidation/transfer of the HavelockAsbestos Mine, overseeing the preparation of management contracts for the public utilities

- viii -

including SEB, WSB and the PTC as well as the divestiture of the Swaziland Royal InsuranceCompany.

Efficiency of Expenditures

32. Increased efficiency in public expenditures could be achieved through a reallocation ofbudgetary resources into identified priority areas. These may be summarized as follows:

(a) The recommendations on staffing made above, will enhance the compositionof the civil service, by reducing the proportion of redundant staff.

(b) Increased funds should be allocated to finance operating and maintenance costsfor education, e.g., textbook, roads and buildings. The building maintenancebacklog needs to be urgently addressed.

(c) Priority must be given to rehabilitation over new capital projects, and lessemphasis to "unproductive" investment, eg., government buildings andhousing. Given the existing macroeconomic constraints and implementationcapacity, a careful assessment of public investment priorities should be madeacross the sectors, including the parastatals, measuring the opportunity cost ofimplementing large projects, e.g., the Komati River Basin project.

(d) Budgetary allocations to the CTA must be wholly re-assessed, in light of theGovernment's restructuring plans. The CTA absorbs a significant proportionof the budget but funds are believed to be grossly wasted. It is recommendedthat CTA be abolished and its functions privatized. In addition to enhancingefficiency, this should generate important net savings.

(e) The Recruitment and Retention Allowance (RRA) should be increased in realterms and extended to other professional layers, such as accountants. TheRRA was introduced in 1988 as an incentive to retain high level staff but hasbeen kept fixed in nominal value since its introduction.

C. Recurrent and Capital Budgeting Systems

33. Swaziland has made significant progress in developing fairly advanced budgeting andplanning systems at the central level. A three-year rolling development plan was introducedin 1989, based on a project-driven computerized system. The budgeting cycle, which runs forsix months, is dominated by the preparation of the three-year development plan. The budget,including recurrent estimates, is prepared for the first year of the plan as a by-product of thisprocess.

34. The problems with the system include (i) inadequate estimation of non-wage recurrentcosts and insufficient link between recurrent and capital budgeting; and (ii) uneven quality ofprojects. The budgeting of non-wage recurrent costs is based on inflation adjustments on theprevious year's allocations and bear no relation with the sectors actual or emerging needs, andonly a small proportion of projects include estimates of future recurrent costs. There is aconsensus that the quality of projects is frequently poor, partly because the large number of

- Ix -

projects strains the capacity of the limited number of qualified staff, and lack of a strategicframework in which to assess priorities.

35. The main recommendations to improve the budgeting and planning systems at theCentral Government level include:

(a) Preparation of a long term development strategy, so that decision making,including the allocation of public resources, can be made in the context ofnational and sectoral priorities.

(b) Introduction of costing systems, including standard costs, to estimate recurrentbudgets for operations and maintenance. This will allow expenditureprograms to be related to activity levels and other output indicators.

(c) Reduction in the number of projects, by consolidating small projects into asingle large project or, by transferring some to the recurrent budget.

(d) More time should be allocated to the design and preparation of new prcjects.All projects must include appropriate estimates of potential recurrent costs.

D. Institutional Issues

36. In the course of this review it became apparent that a number of institutional changesare required to implement some of the recommendations outlined above concerning thesustainability and efficiency of the expenditure program. Some of these changes are alreadyon-going:

(a) The highest priority must be given to strengthening the Ministry of Finance(MOF), which is seriously under-staffed at the technical level. Thesepositions, should be preferably filled with qualified local staff so as to ensurecontinuity and institutional development.

(b) Restructuring of the planning and financial cadre under the auspices of theMinistry of Economic Planning and Development (MEPD). This should helpimprove planning capabilities at line ministries and enhance decentralization.

(c) With the recent split of the Ministry of Works and Communications (MOWC)into the works and transport ministries, the MOW has kept the roadssubsector. Close coordination between the two ministries will be necessary toensure effective transport planning, which needs to be comprehensive giventhe trade-offs between railway and road transportation.

(d) The role of the PEU should be further consolidated within the institutionalframework. The unit became operational only in 1991, with the appointmentof a new director financed by USAID. It has few staff, mostly expatriates. Itis recommended that local counterparts be appointed to ensure continuity oncethe Director leaves.

x -

(e) A review of the organization and structure of the Ministry of Education(MOE) is strongly recommended. In particular, the creation of a Departmentof Tertiary Education at the MOE.

(f) In line with the Government's plans to radically restructure the CTA, it isrecommended that CTA be abolished and its activities privatized.

E. Sectoral Reviews

E.1 Education

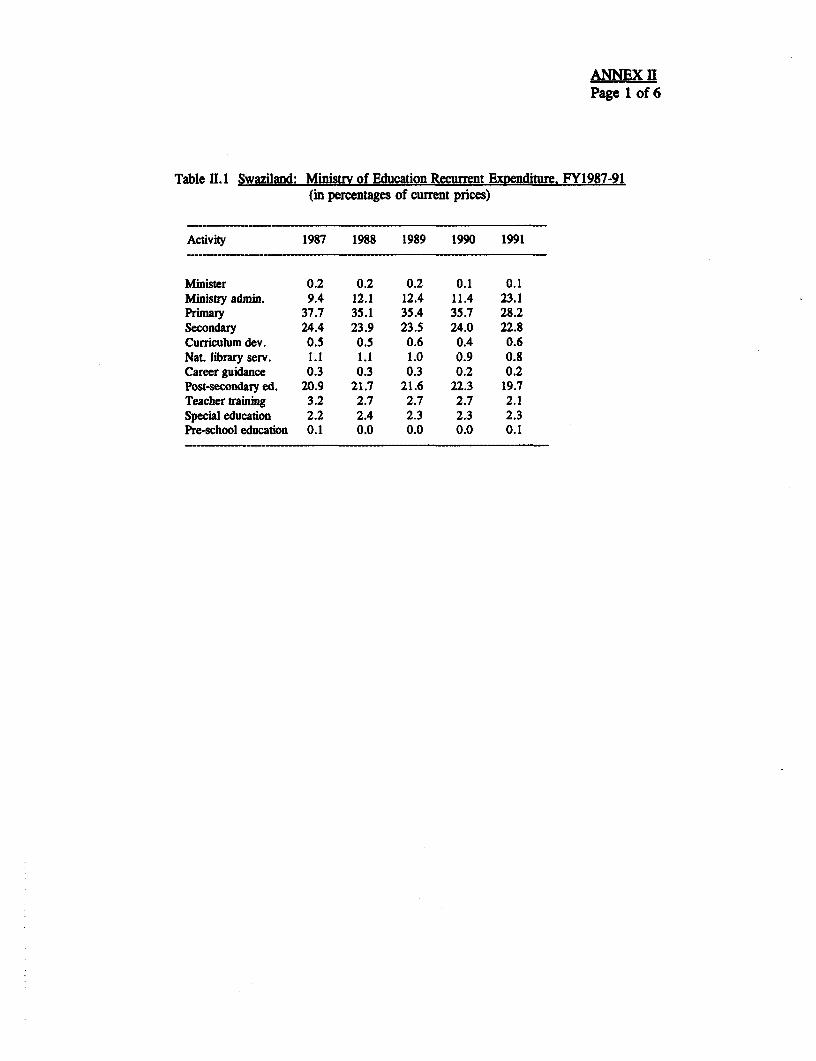

37. Education is the largest recipient of budgetary resources. Its share in the total budget,over 30 percent, is well above the average for Africa. Although the country has been able tosignificantly expand its school system since independence in 1968, cost efficiency is very low,particularly at the primary level, as evidenced by the high repetition and drop out rates. Inaddition, key management and professional skills are in short supply.

38. It is vitally important to improve the quality of the education system. To this endresources should be shifted within the sector from (i) salaries/subsidies to consumables,specifically teaching materials for primary education and maintenance of physical facilities and(ii) from new capital projects to rehabilitation of existing facilities.

39. In terms of sub-sectoral composition, resources should be shifted from post-secondaryto primary education. The share of the recurrent budget devoted to post-secondary education,notably grants and subsidies, is far higher than the average for Africa. The main source ofsuch a shift, should be the introduction of a cost recovery system from students at the tertiarylevel.

40. Increased resources should be spent in teacher training, as teachers themselves are theproduct of a poor education system. In addition consideration should be given to introducinginnovative methods of instruction, e.g., radio and audio-visual techniques, which have provedsuccessful in other countries.

41. A number of cost-saving methods should be adopted, including (i) increasing thepupil/teacher ratio; (ii) introducing double shifts; and (iii) introducing multigrade classes; and(iv) adopting continuous assessments to minimize repetition and dropout rates.

42. A review of the strategy for tertiary education should be undertaken. In the interim,University enrolment should be limited. Labor market surveys should be carried out on aregular basis so that the syllabus and disciplines offered at the post-secondary level match theneeds of the market.

- xi -

E.2 Roads Subsector

43. The roads subsector has typically accounted for the largest proportion of the capitalbudget, nearly 20 percent. Capital expenditures increased by about 19 percent in nominalterms, between 1987 and 1990; and were projected to rise by 50 over percent per annum inthe 1991-93 period.

44. Major capital projects undertaken over past few years have been, on the whole,economically justified. However, in some cases they were not the highest priority, andi somemarginal projects, e.g., the Miliba-Mafutseni road, were undertaken before more criticalones, e.g., the upgrading of the Mbabane-Manzini road.

45. The quality of feasibility studies is variable and the Planning Unit (PU), has beenoverstretched to carry out in-depth reviews. The restructuring of the planning cadre shouldhelp strengthen the PU and define clearly terms of reference for project evaluation and fornetwork planning.

46. Although the basic arterial road network has been put in place, some networkplanning is required, as some proposed upgrading projects will divert traffic from existingpaved roads and other proposed upgrading projects; thereby affecting economic returns.

47. The main problem in the roads subsector has been inadequate road maintenance. Thisresulted from inadequate budgeting and low availability of equipment at the CTA. Progresshas been made in estimating the costs maintenance needs and implementation has improvedbecause a large proportion is being contracted out to private firms. As a result, budgetaryallocations for maintenance were raised by 30 percent in FY1991, thereby meeting 70 percentof estimated requirements.

48. The costs of contracting out periodic maintenance work is lower than using the RoadsBranch units. Therefore, it is recommended that all re-graveling and re-sealing be put out tocontract and that these units be phased out; and only a small unit be retained for emergencywork and keep in-house expertise. This would save maintenance costs by E34 million peryear, or 15 percent of the projected costs.

E.3 Railways

49. Swaziland Railways (SR), is the parastatal running the railway system. It operates asouthern rail link (SRL)--built in 1978--and a northern rail link (NRL)--built in 1985--bothconnecting with the South African railways and providing access to South African ports.

50. SR incurred consistent net losses between 1977 and 1987, amounting to E22 million.Although the increased traffic from the NRL helped to improve SR's operating ratio since1987, inability to repay the commercial loan borrowed for the construction of the line,including a E16 million foreign exchange loss, forced a Government injection of E22.4million in 1988 and 1989. The reduced debt service burden resulting from the repayment ofthe loan, allowed small operating surpluses thereafter.

- xii -

51. In addition to financial difficulties, SR suffers from serious problems of managementand overstaffing; it employs 1100 workers. Maintenance of tracks has been poor with theresult that more costly rehabilitation will be needed in future. Furthermore, recurrentaccidents, have considerably added to SR's already high operating costs. If under-maintenance and accidents were explicitly costed out, net income in recent years would havebeen negative.

52. Apart from the construction of the NRL in 1985 and the rehabilitation of the Usuthubridge in 1986, destroyed by the 1985 cyclone, no major capital expenditures have beenundertaken by SR. Total investment between 1985-90 totalled E37.1 million, and wereeffectively financed by Central Government. SR received E71.6 million in Govermnent loansbetween 1977 and 1989, including the E22.4 million for debt relief; which will probablynever be repaid.

53. Financial projections indicate that SR will incur operating losses if transit trafficdeclines drastically because of its diversion to Maputo, or at best break even if traffic levelsremain at existing levels. These projections assume, substantial tariff adjustments on localtraffic and debt forgiveness by Government.

54. In response to expected future diversion of traffic to Maputo, a major trackrehabilitation program, the Mpaka-Siweni, is being proposed by SR. The estimated cost isE70 million, to be funded as a grant by Government. Part of the project has been included inthe three year rolling plan, although no proper economic analysis has been carried out.

55. It is essential that a long term view on the future of the railways be developed, withinthe context of a transport plan, which would include an cost/benefit analysis of alternativeoptions, including closure of the railways and/or leasing the North/South line to the SouthAfrican railways. Ideally, the study should include more accurate estimates of the costs oftransporting goods by road.

56. In the interim, no major track rehabilitation should be undertaken until the role of therailways is clearly defined and acceptable economic returns are properly estimated.

57. A major financial restructuring will be necessary, if the SR, or some of its activities,are to remain in operation. These would include (i) a significant staff retrenchment(ii) debt forgiveness, or conversion to equity of debt owed to Government; and (iii) costsavings measures to reduce administration costs and overheads, particularly in terms ofvehicle fleet, allowances and gratuities.

E.4 Airways

Airline

58. The Royal Swazi National Airways (ZC), is a parastatal running a single plane airline.The ZC has operated at a net loss since its establishment in 1978, although losses havegradually declined over the past four years. This improvement reflects the repayment of theloan to purchase an aircraft in 1988, which carried substantial foreign exchange losses, anddoubling of passenger traffic.

- xiii -

59. Government's accumulated subsidies to finance ZC's losses amounted to E30 millionbetween 1985 and 1989. No subsidies were granted in 1990. ZC plans to continueoperations at a loss, particularly given the decline in passenger traffic associated with therecession in South Africa, and the breakup of its joint venture with LAM.

60. No capital expenditures are planned over the rolling plan period, but there has beendiscussion of the need to acquire a "second" plane. A second plane, costed at about E43million, would not be economically or financially justified under any circumstances over thenext few years and Government should resist any suggestions to purchase another plane.

Airport

61. There is significant political pressure to undertake an airport expansion project, withan estimated cost of E46 million. The economic analysis shows negative returns, and fuirtherstudies have been included in the rolling plan to examine how improvements can be maclemore cost-effective. In any case, such expansion should be phased in a number of years.

E.5 Electricity

62. The Swaziland Electricity Board (SEB), is a public sector corporation, with amonopoly for the transmission, generation, and distribution of electricity within Swaziland,although it may grant licenses to third parties to generate electricity for their own use.

63. Over 50 percent of electricity sales by SEB are imported from the South AfricanElectricity Commission (ESKOM). Domestic capacity is basically hydro-based, andconsequently vulnerable to periodic droughts.

64. SEB's net income position has been negative since 1985, because of inadequate lariffadjustments and increased debt service burden. The depreciation of the Lilangeni resulted insizeable foreign exchange losses on World bank loans contracted to build a hydro-powerstation in 1984. The Government prepaid these loans in 1989, and converted them intoequity.

65. Between 1985 and 1989, SEB undertook limited investments. Because of its strainingfinancial situation, the construction of a third ESKOM line was postponed until 1990, wiith theresult that systems reliability was extremely poor for several years and has only now reachedacceptable levels. A fourth ESKOM line is planned for 1994, at a cost of E20 million. Inaddition, the Government is considering an additional E41 million for another hydro-powerstation, the Maguga dam, as part of the Komati River Basin irrigation project.

66. A management contract has recently been signed between SEB and Government,which is expected to improve the financial performance of the company. Under this contract,SEB will undergo significant financial and management restructuring.

67. It is essential that tariffs are allowed to increase to cover at least operating costs. Inaddition, the Government might need to make a capital injection to cover unrealized foreignexchange losses estimated at E36 million, which if included in the balance sheet would renderSEB insolvent.

- xiv -

E.6 Water and Sewerage

68. The Water and Sewerage Board (WSB) is not an independent body but operates asGovernment department responsible for servicing principal urban areas.

69. The financial and service performance of the WSB has reached a critical stage. It hascontinuously incurred net losses, partly because insufficient tariff adjustments, and precariousbilling and collection systems (35 percent of water produced is not accounted for). Inprinciple, the Government provides subsidies to finance recurrent deficits on non-viableactivities but has also covered payroll costs, about El million per annum.

70. Government's contributions to finance WSB capital expenditures have been negligible,while overall Government investments in the water sector, including rural areas, accountedfor a mere 4 percent of total Government capital expenditures between 1985 and 1989.

71. Financial and management weakness within the Board, compounded by insufficientsupport from central Government have resulted in under-investment, as evidenced by agedand leaking pipes, and subsequently in extremely poor standards of service in the urban areas.

72. A capital program of E55.6 million, largely for rehabilitation, is envisaged for theFY1992-96 period. Unless appropriate tariff adjustments are made, the Board will not beable to significantly contribute to finance these expenditures.

73. The highest priority should be given to implement the Government's decision tomake the WSB a corporation with full authority to conduct its affairs, e.g., tariff andmanpower policy.

.

- xv -

::::::::::::::::::::�:::::�::"...�.. . � �. � �.... . .. �' I .... .. 1. -1 � ... � .,.,...,. 1-1.1 ... .. .. .-. ,...,.".., .. .. .. .. "..'......' � 1. �. . � .'..'..'..� .... .. .. ...".--�- � .. '- --- -'.......... ::::::::::::::::::::::::::::7 ........ -.-. -- "..

..... �.... -::::�: '.. .. -.-- �� . .. :� :X: -:::-: :�::::: :x: :: .::::::::::::::::::::�::�::::::::�::::::::::::::::::...,.....� ..... I.... -- : : : : ! : ::::�:::::::: :: :: : X: �: -� I1, � �I."."..,..�..,..�..,..�..�...''�.�,� ,� .. . .. ..... ' :' �. ...1%."......'.........::. . . .I .. ,. -� .. ....'.....'..-I....%-:'X:X::::::::::::::::' .- . ,'',. -. ...... 1; : -::X; :V:::-.�:.. :� ...... ,....,.......,.:X::- :- : �::::::: �:: :: :: .1 �-...'..... - .,...,...,..�".,.,....,..,.....,.....,.,......,....,.,...�.,���,����� �". -'....'.'..-l -�'.'- -- '... . . �. - - .. .....,..,..,...........,..,....."",.�'. .. ''...1--l- ... �.....I.....-..... ."'...----- 1.1- .. 1. .. 1. 1. I-- ..... ''. -.. - �� -I 1. I.- 1. - 1. - - .. .. 1-1.1-1 ....................... ... - .. -- ............ �...............-� �-,-� -1. . ............... �..-... 1. ..--.... --- ..... .. ..... .. .. .. .. ........ .. I 1-.�,.. . --.b..-...-... .- :. . .�:;�:� .. -..... .. .. .. .. ........-- �-...... -.- -1-1. ... I.--................... 1-1- .... . . . . . .-. .....".....- :: ` . 1. .. .. I....... ''. ... I. I.. -.. .. ........ �:::�: , ,: :�::: : ::: '. ,. .: ...... ..... �:.:�:.:.:�:.:. ..: :� �: .�I--- .. ��11.. I.I.1.I........ ....... 11 .I.. .. -1.-..........-, , �:: : : : : I . .'% -X ".1-... I.......-::: :,.:, . ..... ........ : �. F�. ., ,. 1, �..�.. .. ,... :: � v :::::X�:: ::]::1:: ::]:: :: :: ::,.. �"... ��. � �., ,� I�1. � �� ,,-- I I., .'...........�.. �. %'.�,. ,�.. . , .1 .' .1 1, �. .I.. I.,..,....... ........'.....�'. .. ..-- :::: :�: :.: : X:::::: :: .: .. ::::::... - - ... .... ::: .. - ..... .. . I ..... .. . - , .. . . . - .1- 1.1 ..... - �.... - . 1. - .. .... '' '' '' ' ' .. .11.1. I . .1 . .':...' --::�:X: .. �..`-...... .. .. .. .. �.. -'.�.� .1 -I .� ... 1�.. �.'.....'..'..... -- -. � I .- �. � I .�. .- I. .1 . ..'..". -'.'.� ,. I.,............ .. . . . � . ,.. . . ... -::�::::: : � : : � : : 1 : : 1 :!- : X::�::� :�::: ::�'... .1 .. 1- ,. ." '.'... ....'..'....' . � .I.. �� 1, ,..�,��' ." .' 1-1 ........ .�.. . .. ,. 1,.I. ,. .. .'..'.. -. .. -, -1 . ." ..' .1 ...... . . . .11, -.. � : :-�: ,.' ..:j::: .:�:�:�:�:�:�:�:],.,:i::il�i��i::-1- ..... ���..�:�".i.:�.-:�::.:::�.:::::::::�:::.:�:�.'�'�:�:]�:�:'.�.,....,...........,.....,...",,....I ............. �. - � -..... ... ...'.'..,-..-.-.',.'.,, -1. - -1.-........'.....Z.. ----. ,.,..'-., .. .. .. I.-..-.%-.l'..l ultimar-y am: :ecom .- �::- ..... ......-4.".. - �����ii�:i�:������]�.i�������]���:��ii����i�iii�:����.,..,..,.�'.....�....�,.....,.,.:::�::: ..... --. .... '- 1:.I.R..I....,..,..,..�...."......,..,..�.�.....,.. :x' - �'�.�:�:�.]�:�:�Ws-mi�� -......I-- 11-11-1- ..... I....,......... -- l. 1.,..........I.- .. ....... .-:1 x ;:: : � � -- :::::::�::�::::::::::::::::::::::::: :X::::::: --..... . .---- .... �. � �. � � � i i�: I -� �:::x:::::::::::!:!z::�::!! --- ---- I-....''I.-I ..... -�� "",.,.,.,...�.�,�'..'�,.,.,.............,..I ........ .. .. ."....'....---- .... ..���. - - -1..1. I..., ........ ......' .... ..I..... ..�...�. . ......... � ::: .....�....,..-'-....l .. .. .. --- :-:.:.." .-'.. I.. --'." - 1. 1. 1.11, -'.'...'..�.......'-- -'.....--:-- ... .:::::::...... .. -- ::. ...' -.,.1-1. .1. -1.III-- -1-I'.'...'-..'-...- .... :.X..::::::::::::::: .--- " '. -" -�. ". -'. -' .... ..' .'. -�... ::::::::::::::::::::::::::::::::::::::::::::::�:::::::::::::::::�:::::::�::�::::::::::::::::::::::::::::::::::: ................ �.. 1. ... ,.,..�."..,..,.....,...."...,.,.,.,."..,..,.....,...''.''."......,...."..,.�'',.,.,."..1 ........ I-- ........ �.....�.........,.........�........�...........,..,...........I.11 I.- ...............-I ........... �.....'' . .......-.......I........�,�ilIi"..'......''. I.''..... -.... - -. 1-1-.- I-- - - - -'............-.-- .. .... �.. �.. � 1. �.......... I...., ..... .. .�:i::�::�i:�;i:�:�i::.�::::::::::::.-..I'' -.. �.. .................�...�... ... .................. -- ....-. ..... -'..- ..... .. ... .. .. .. ''''. I.......... .�I-- � � �� � �. 1, -, I .1. I ...... I..... ... ...'.:::.:i::::::.��::::i:::,�::�.i::::.:�:,�.:::......."..,."..,..,.,'..,....I .. .. .. .. I.. I.- -. '-.-- I .1. -...... -".'..' .. ................. ... -. '.,-.1- ---.. I -....... - I I''... .- - . -- '- ''�'..I..,..,....�..�..'�.....,..,..............�...,...,...��.�..",.,,..............�...�..�:�: �:::%.. ........,.,..''.,..,..,..,..''... I-- ..... I.- .. .. ..�.....-. �.. .. .. � � I � �. � 1, -'.....".....'..l.-...'... -...........�..�.- � '.'.�' ..... ..- --..- I.-I..."....�...............�........... �.... . -.... .--- .I I - -..... ..I.... I...:..::-:::- �X:-:::.: 1. I........... �.��.�....''�.I...�.�...�...�..........,.......,..........,...��..�..I . ........ .- , � '.- �-...........�.. .... .::. '..- .::::::---- ...... :::�::�::�'i-�-:::�:.::::--,...�"- ... ..... .._,.�..'. -. 1-.1- -11 I.I.- � 1. -- .. .....'' I... ................. �.I..�..�.I."..,..,..,.�'....�..........."�".,.�'.......::::::::::::::::::�:::::�::]::]�::::]::�::::::::::::�::::::�:: . .............. , -,:: �:�::::�::::::::::::::;::::;:::�:::::::�::::::::::::::::::.:::::::::::�::'...- -� --- '. ....1,-� -:-.,�.:�S. . ":::::..... ','....'..'....' fteala: 91 G "- IA � � ". .I....."�..'.*00 ....�.... mcasu=-. �. .:"��..'.. ....�..�.18:.:: ralgelm' " d te us:-, . Ve =- O.; M 1 M...... � -. ._ r*'U �. ".i :_0 It � t,...... -.1-1 ......-.... --- -1.1 - - ----. - - -.. .I_- ..- � -- I --- -.1. :;:::�::::::::::::::!;::X: .: ........�........",.- ......... .. .. ..�... :;:�--'. I.... .1-1-1 - -- �----- - -1- � 1. .1. 11-11-1-1-1- ...,....- -..... .---- :. ..... ......:,.::.: --.::.::::: .... .. .. .. .. .. .�.. -'. . .- -. 1 � . . � � - � I I...... ''...' .... I � .....�.� I.. .'...-.... � � ..... '. , �. �...... .:x:-::�-:::-::::p::: :-:::::p�.--'l ....... -."I....... ::::::.::::: .:: -:::::::::::::::: .: , I �, -- .1 .... ....... 6f:11-1 -�W ..�.�.�.��..�,-��...,.�.��l.,�l.,.,.,.,,.�I.I...�.,�'...,..'..�....,..,. .. ---.-.1 �:�' 0-1 : S.V,. m��i��:�:��:�:� ...... ::.:: :::::., .......... ::�:X�:::v- �:::.- .. .. ..I.. .. .. .. I.. ::::::::::::::::::::::::::,::::.:::::::: .......,i:�:�:.�:::,���:�:�:�:�:�:�:.�:�:�:]:�:�:�:�:i:�����]��::".:,..:,.I ... ... ...-::-:-:; , .*:,:.asses.sjm.W NAT �..::-:::: -:: -: ::-- :::.::::;::::::::::::.�::%.::..:..::::::::::.:.. , -,- ,. . . .�.........�.�....,....�,.�,.�'..,.....�..�..�.....,.."�'..I ... ... ..::::::::x....- ...�.. .'- -' ...�....... �.. I. ,:: "..b .- I.... ''. I.. I.. .� 1. - I I I......,..., -..."' � . I.... - �' 1. X I.... .- � : �:: ::.. �� 4..- I I -'I 1. .1. - 1. ......Z........., - 1 ........�..... ' '� ..'-''-'. I. ...:. .: ".:::::::::::::::::::;::::::::::::::::::.".......,.,...,........,.,.. �--'-"'..'.....-- -. -1- ...... -....-�.- "....'......-- I.---l..''.. ..'.................'.'.'..l'.'-... I'll ........ .. .... .1- I. . � . . .. " '�:::::�::::::-::-::::::::::.- :::: , , ,-- I ". '..'..'..' .. .. .. .. 0 � I .....Z.... � � - 1". � , , ' ':::z' :::::::::::::::::::: '::':x::::::::::.-.-"-'-- ..........�...... ..-..... ----- . ........... .. ''..' ..... ... --.... � I.I...- - -1. . ..... --- .....�..... ,�1.11.,..,....,.,......,.,...,.".,..�.....�.�......,.,...-1 ...�..... -::::: ::::::::x::::::-........I....... .. .1 � ---- :::: :::::::::::::::::::::::::::::::::::::.�..��.�.,�,::....'�,�:..,:..,:,.:...:...:]:::::.:,................�......,............. ---- ,.. - --.-.-- . ........... --- ..... -....-- , ........ .� ''.....- � " - . .1. I..., .....I... .-..::::. '. -, --- � -,�,,�,.�,.�,,��.,�.....�..�..�.. � .- I.I.--..'.."...."..."..".. ----I --� I I. I .I I ---I -... I -:-:Y::-:w �..�:::�.�:i::.�.i:::::.,:i::ii:�:�i::i��i��i�:i:I. ...,:�1111',t��. �.. 1. *-- '11.a�.. ,,' fd�r ..'..',� : ,:� ft �-.....:�:��Jtd �'of h 'TOPM, I. ....... � � b.:`1 ' "' P'..,P,';' " ' " 'h'."xpend�ur : �:���:�:�:. 'U'ce�:�eht�� 1v mliftfoc, I elatjol::: �...:: ...... ........-.......... : �:: � .. - -0.q.W., .....:,:::�� � ,W... -� -.-- M... �.. �.�....��. ,--'..-..l.. - � .�. �. �� -1 �l -1, I. .. .. ........ �. - , -Mw:':':.: .......... ..:. .. .....'.- ...... � .11- -.. -. I...�..1.11.1 .....--- � -- .. ... .. --- l- . .- ...' ..... - '' �.......... �.... -1-.I. .... I. - , , '- � � � � - 1, � --'. �. �. �. � --� I..... � �.. � I � � I .1. I... I I I I... I.. .. .. I...''. '"'...1-1.11.1 .............. - �'"... .. 1. . . � . �....... .,v...-'..'.l-- ....... .. .. ........ ... .p'.-� � �. . ....�.- ....... ::::: ::::::... -11 I � �.. ::::::::::::::::::,.:.:.:.:.:.:.:::: '....�...1.1.11.1 .....-.........1. �.�.0: � OW. -- �...... .. .......... �-: ..... :.,... ... .......-. 1 .......................--- - -..... .l.. .....�...1. . .. , -1. I...... . I- -,: :,.X:..1-1.1-1.1-1--,.1:1.1 ..... 1.11-I..........'..' . .-- d' 61fid be .... � ''.....' " '' ....'... -:::::::::::::::::::::.. ... .... :X�X::::X: -1- 1...,."."......"...........,.....,.....,.,....�'........ Xa'' �4tf j ''... ..... ''.11.---- ... I...".., ...........I.. .. .. .. I...""I---.4- � hfiowof isp_q �� u:l_'.'IQw '.,'.....-'-.':...- --". -.1 � ,� �..-1, � -. 11.1 .....''.-, ..... -:::::::.:,v.:..: .... ::.:.:,... 1.11.11, ..... - -. -1- -11 .. -..... 1-1. ::::::::::::::::::::::::::::::::::::::::::::::::::::,...,..,.......,..,..."..,.".,.....,...".,.."I . . � � 1. -�-1-1-F, ............ �.. .41.1....'�-'. � I .1-1 -.1 �'........,..,."...............,.�I."..,........�.....�..�,.".�.,.."�'I.I��... -w-". �.............I...-.. ........ ..............I.. .. ..I.. � : M., i�:.".".". :.. - '''.............,.....,......�...'�'...''..,."..,."........,.....,..,....'....'.''.'Iw-I. I-.1-1- '.... ............ ..'....'..' ........ I...I .: ce,�:f --�Jw0...�.............,.........,.,...."� ................ �.. ::::��:�:�:�:*:��j :off� : �. �V:�.:::::�:::::::::;:.�::�::,::�:::::-:--:-:-::::".�.."..."....,.................. �... :: -1-11''. : redu diii. d ik .q:::::::::::::::::::: .- ,:.::: .::::.:.�....... ..' .. 1.,I-.1--.: ... .. ........... ........-... :::::::::::-: ...-F. .'.'�..... 1.1-1 ... I. ........ ..... � "'.".1-1.1-.- I I.- I....:.:..,.".,..�..�..�..�...�,�.,..�'...�'. ." -..--- .... �..:�:.:.:.:.:.::::::::::::::::::::::::: .... .�, .�.,�,�..,.".,....,.........".."..,.,..,........,. ..'..-.--.-----.,..,.�..�....�.�,.��..,.....��.��..''.I ........ �.. �. � �. � :.,..,.....,.....,.....,..�..". " -'."..,."....,....... -:.. li ....... -� �:�.,.,.,..,........�.��...��.'',�,.�.�'. ....- ''"'' ''..'--l ........ � I � �.. �.. I.. I ...'.-...-.�..�..��.��. � "..............'.. .I.-.11.11 .......--.. "ll ... ........ �.. I. -.... -.....-- ..... --. 1 ....... ...'......�....... ---- , ...-. .. ..... ....'' ....... .1-1.11 ....... -1-1-1- .... -.......---- .... .. �.. �. � �.... I 0..'..�.....�..��.�.-.�� � � � 1� . ..... �......'�. ...... I.... ............ �..�... -- ........ �..�........,.,..."..,....-,.....,.,."".".."........�..,.�.......�....�....�...��...�.�"",..�.�.�.,.......�.....,.�",�...�...�.4������'.Pih re e hdu -bt'-fit: � � I � � , '.'........'.....� ......... I. � , � I., �.. .... � . . � . I . I I u " . :. � 7,..�.. �':,,.!.-:::�X::::�::�:- - .. . � � I � .. � � I I - I - � � . I. 0844001=..Wttz�". MII .. 'M--x:-::x:::::::: ,:::::,::::::::::: - �::�::�::�::;:::::::::::�::::::: -- ''-....'. .- - I - -_��. I -8 - 1. 11- :: : �:: -. 1-4.1 .........w.:.:.:.:..:�:.:,:,:��.:X:� ----l - � .� � � X��.:' ::�:::-.. .. ......Z. I.�. 1. -1-I..'.-I .... ..... I.. I. ........ �.. �... - I � .Z.. :�::::::::::: � �::�::�::�:::::::�::�:::�:�:::.::.:::---- --- : ��.��� 1-.-,."..... .�.I.�.'..'.'....'... .."ffi....I.-.., �.. .. , - I - . � .. :..- .............. ...- -1- -.. - I - �- �. ., --. ,- . ..-- -.......... I.- ... --- -- -- -- �, ,. �... .'.-,,-....... �..... ......... -- �:::�X::v�::X. iwi ....--.... '..'..:.: : ��i�::�4::]��� .. aseII.nVaclector. ...'' ..:::::: ' "''yug'tav:1.1.,..,."..,..,..::::::::::�:j:j:�:i:::::::::::::::::�,�.]:i:�i�:��:....' ..... .. - - .... '' . ... ..... I..''...., ........I..... I-.:::: - .I.....- I.I.- ''. -- -- I ., : �. WWSPI � mem:,.�::�:�i:�::i��i���������������]������������������i�����:���:: -. 11, - - ----- '.'--b.'--- Z..F....--l .... :. "....'..',1-1.11. I.. . - .. -...-- . .11 I-- .. ... . ........... ..... ..�..O- �.. � I � I.. 1. 1. �... .- -': ::-:::::1::1::-: ..:::::..,..�.,...,.,...",,....�'........�'... .............. .11.11.1-I....I.I...., - - I... . -- � � - I... �... � I... '' -. 1-1- .....�..... �. � � 'I.I.-.l.-...... -.1. - I .1. I � � I'' '''"..,.............,.....,..,..,..,..,.,.,.� ... .. ... "....'.. 1. I-- �11111 I I-- ,: ---. 1 � �11.1.''"..'."....'.....' ............�................................. I . ::-- ... -....''.--, .. .. ..�.,.,."".."...."".................... 1".. 1. - 1. 1. I- ,..'.. -I..."...'....'.. "--- I..... 1. ...................... .. ... ..... . .. � 1.�.11.1�.. -:::::X:X.."..'' '1. I � I � I-., I .�� �t ft 6.f. itaLtiDenditt' ..- �-.. 1. I.... II--. ::,�:::::]:::::::.:::.::::::::...:.:.:.::.:.:':.�.:::::X .. .. .. I.I�,.,.,..�,�..".".,.,.,.,...,.,.,.. ' ':4:'::'l'I-. . ....... 1.1--l-II.-I."..' -.'."'.'.'.'.'.'-'-- ":::; ::::::........l.l..... , " 1".-"..'.'.'.'.l'..l.- I.,..., I I I.- I I.- 1. I - I� . . �, - .... 1.11.1 ........ .11-1-1-1.1 ......... ::::::�:::::::.-.".- � ... :: - -1.1 -1-1-1.1-14--.... I..... --. ::::!:::..... 1. -- . - -: �::: .: .: ::��:.:: :::::::::�V:::::m::::::X: .- - --... I.''. - 1. --- ..... -.... 4."..."..'.....''..I....-........... ... 1. I. ..... I..''. " I. ..... . .1-1- - .' "' ".-�,..'''',..,.................,....,.,..",.,.,,.,.,.,..,........".,."..:..."..'','',:,i p - .11 1-I.. .. ... .-.- "'.'....'...�..�..�-. '�'-- -.- '.-� .. .. .. .. ,..."."-.'.-'-::X'.- I.f..i....,....�...'�".."....� ... --..............�.....�.. .. ............ %. .0 ;:::v::::::::::.::::". I.... I :...... ..... iqns.:.�.qfbper Wif: i�� ............' .......... flI- ....,'.-......,.��....�........��....��....:::::::::,:::::::::::::::: :::: .,�..'-.-'.- ... ....,.l.-,..'..'..-.. � :S�::�:::.::� increase.9 OMaiia vog :::::�...... . _m ... --.'.',." .... ..,F..-...."I-,,-,,, ....... :::::: � �::::::::::::::::� . 1. piaten.- 1.,. .......... .- 1-1.1-1--l ...... "."..'.......'...'-, '..'.. : ���.... _...---l-11 -- "..... ... -- .------- ' . .. .. ..... ........ -1-1 ...........-....'-- ..... -'' �.....I.......--- -. 1- .I.. I-- ... I.''......, ... I--, ...�................ "..'... - -::::::::'::-:-::�....-.... ---- .. .............. �.��....,.....,..�.....�......".,.I .... .l."..'........'.... I .I .I.. I...... - -.. ..... .- .1..... ---- .. . ....�...... --. 11. 1. -:: :�:Xxq ::::::::::::: . . ......�..... �:::::::::::-:!-:::::::::::.:,. � :::::::... �.... -- '...- .. ........�.... .. '' - .'42.4.: ..... .. - .. ::::.. ]::'e. -�::'�'::- ...l..l..-::::: ..... �.,."....".,....".,.."..,......,.,..�.I ... ... ..... �.:-:w:::::::;:::::::::::: �.. �.. .. ...... ----- bildiiidMd I..'', .. ... -.......,-.,:::::d',' ' ' " "'.."..", "". ",""'-,""-'F.I I....... I 1-1. -...- ,-- 1. ..-. �� � � I I � : � �:�� ucatim.]�l U � 9&ln XG &.1 .... -I-- ..... ''...' .........�..'..' ..... ...-1-1--l.....'... '- .... .. �.�.�-,�..�":..'�:.�.::.;.:�:.:�:�:�� :-'........'........�.- ::�::::::::X �::- --- - -- l.......l.''.I... ::::::::::::::::;:::::::::: ....... ..''. . ...... I... , - -. �..... .----- ... I ---- -- - - -.-- ". �.... .. �..,I....I...--.I... - - .- II-11- , - -.--- -........�- �. � 1. 1. 1. I.- -.....I....I...I........... ....' ............................. .- ......�............ -. 1-1--- ....... .. .� -- ... . �..--- ....-.............. .- -- ---.......- � o..'--- ". .. �� � � , "; .�.... ....'v..'..l.-'.....'....,w :' " ' "''.':::': t.:.::.::.......�.....�.......... -'-----'.'-- -- 41'..".I..'meneacc6idinittoonom" rmms:'.:3nd:::c6n-'t '�: 'O." '...-.....�.... -- .1. -. 1 �-,-.....�........ ....-- - -1. --...-.... �.. -....... 1-1.1---F.I...." ,� �i �� �� ��i����:i:....:�:�����'Dn4Dtttim.:.i��g.t,--z-,.,'l..'.' M,; ...... on: .- :'-:�:::::::,:: . ..... .�.I.",...,.�.�.���...�.��'..��.,�.�... '--. . . ..... xx�..'.::- "::."...,.,...,.,.."..�.I...,.. -.....�..�..��,�,,�1.11�.,�..�.��.�.��� :X:X �-:X::: .::::::::�::::::!:::::::::::::::::::::::::::::::::�::: ........... ...... ''....... x:::.:::::�::::;::: - -----.... -- .......�.... ---. -.- - --- '. ..' . ..........�... ::,:.:.:.:.:.:�:.:.:�:.:.:�:..:.:�::,.,..�.,� .............. _''.'.'-.-.-'__-'' . ........- - ....... - :::�:X-: .:.:::.:::.:: ::::: :::.��,.�.�.��.. I''' ''' ' ' ' ..�...�,.".,.,..,.,.�.�.,�.I..,."- -- --- -z.- .-.l- �. . - ..l- - .- .- .- .1. -- - -.... ,�..�..'�..�......�....."..........:::-:::::::::-:::::,,.'....l....-.�....'., ......... -1- ... '---.l.AI'' ii�fiv .. .. .. ..'..'........'-.. ---.- I-- ---.,---"""""''' ..'.'..'.-".'. I... � I � �....-M�il�i���i�� .�... .- , ,.-I... -, .1. --- �. : : .:��':-:::- .:.,-.,..'--------- .. -- �.11. I.- .- ---...,.. -WOW:& ,. "...'.... :", .�.�.-�'.-.',-.---'--.'.-'. �::::::::::::::::::::::::::::::...., .......... -� ....... �. -----.� -1-1-1-1-- � 111.11 ........ .� _':':.:: � -: �:: � -- �.I.�'I'�.11''�.I..,..........,:::�:::,.I I.--.����.�. , "-...... �'' , ,I-�::X:: ...'', I....,.....,..,........�..�..��....'�.�,,�,�....,.,.,..��::.:.:�:.",�.�. -1:-.- .... �.. ...... .".-,.........-F -- . - - �. .. ''..-.1. -1-1 .::::.--4 � 0:,�.. '..'..'.....,... .. .. .. �.::�afje ::to:: ", i'Ve .. ......�.I.:::���ii�i�:�i�i���i����;i�����������������������:�����i��������� '' 'I' '' �:�ii��:j:�:�:j:�:��������������'..�i��..�'...�������..,:.:..:::"....,,................�....'�.,.,.�.,.,,..,.,,,..,..,.,....''... '::;'::'::'�::'X: :i J=-RRAidd fid othlJ:'�v:'r'0.f4v':::"' id ....1.11.11 ............... . ........ :::::::::::�. , rease e,: , m,l�i�i��i��::::::��:j:�:�:�:�:�:�:i:::............... .. .. ...... .:. I-- I-, �.,..'..' --- �... , F. ... ".- �.. -1 -1.1.11.:.........I.: 1. I.. I.. �:::::::: - " ��:: :::^X: :::: �:::-:::- : � F:.::-:: -. 'l..--I-..".-..' ............I........................................I.. ........ I...I.. . ............ -. �.'.::: ,.: . ............................... ................ �..... - . -- �...... . ..-.. .. .. .. .. .. -. 1-1 . ..... I.................-'- ............... .. .. ............... .. .�....�... - ", , , , . . . , , , . ".. "....'.''. ''..''.."........�....�..'�,.�,,�.."�.�.�....��. ,, �...,.,�".,�"..�.,�"...�.....,.:.... ........ ' ' '-' ''..,.:,��i�i�ii�ii���:��]��]��]��i�����i:i:����ii��i:�i��i]���::�..�:. ::.:::::':.:..::. .'::::::::::::: ''-. .. .... ..... --- - -1.1. -"..'..'..''..'..'' '.... . �.. - .- ........... I.- 1. 1. - I-- - 1. � - 1.1-1-1--.1-1'' "':l:::::.::.'-'::::::::::::�.... :.,::::.:::::..............,...,..., ......... --- . ..-.. '..'.......�..�-' I �. " ,'. I-% �. �. .'-. � 1. 1. I . 1. �..... I.- I �.....-. 1-1- ....... :::::::::::::::::::::::::::::::]:::.''.,.."."..,."...".,.,.,�"I.I�.--.'...�..'..�..'..- .1- -- l:-: -.... l.-'-:::::�'::..--l . ..........-. .... : :::�::�:,.�:.:: - -.. ... I......%:.:�.::j �:�i:::]*:: ....... . .11".....................,."..,.".,."....."".,.I .1-1-1. . .- Il"'....'.11.1-1- - -1-1- . . ..... .-- .... .I.:.::�::::::::::::::::::�::. -: -�.... ..- �....... -1-1-l'.....''.- -- l."'....".-I-1-1. I....,..,."...",�....,..,..�..�..�.I --- ... .'.,:::� :..x.:::::::::::: :..'.1. 1..X: 4,�:::::::::,:::�:::::::]:]::::::::::::�:::::�:::: : ::: : : ': :: .!::,:::::::''..' .... .W-Itt ..',-- ... -, :�::: ...... f- �'.'..."......'.....--..... .l. '.x��]��e .......''ll.-.. .. ..I. .. ......... �. - ff ....I.-.1-1-1 ......:.......'�--... ".-4.: :- - .............. .. . ..... I 11 .... I.- .... .. ... ... .. .............. .. . ...... ........ .. .. . .: :::www. --. :]::]4]:'.0te �m -. 1 .1--l.-I .....:O'. gs.-'-l'.'..l ............ . , ''.�. ::vX::::::::::w::: d.-I..�.��..�.."..........,.....�....... . RCOU managemen �: g'R-TI .-... '...'.... rage��.:�::::::::::: �:�::' :::::::::::::::w::;--- 1-1-1 ..... -.-- .............. ''Ill: :1: �:::::::X::: �:: ... �....�. �.. �... I ll� I-. � �. ......l.".. ....",........... I.- .".,-'. , I...................... ....I.I.- ...... .- '...-.---.. - .1 . ........ I.. , ,.. .1-1.1 ......... ........--.'..-.--.... ... ......-.. .. ....... - - - -- 1. I... -.....-..... 11.1 ... --.- ....... .... ......-.'...-..-...l ..........I... - -.. �.. �.. � I I I I..... -.. ''. 11 1. 1. ...-.''...''.''....... 11 I-- ... ...-I., ---- ... 1.1'......-,'........ ...- ..... .... "..'..''...''.''... 1.11.11 ......... ...�....�.�,.���.�,.�.�,.�"..�"...�,.��.�...�..�.....��.�.�..�..,.,...........�'..,.�,�.I.. '..'..'..'........'.....'. -,'. - .. :::��::::�::::::�:::�..:::��l:��.-.�-, fWl�p ::'.-::::,:'.:w:.:.':: .... .:.- .. :.. ...:... -. 1 .... .. '':: �:::�� ̀:::::::::::::!:�::: ..::,:: .... -.-'-'..' -" - �.... ----'-'----l:-: ..... �.. -i''Aiwed-:.3-I' ''"' ... �'. �.:: :" '::::::::::::::�:;::::::::::::':::: :: ::: :: :::.Wlu :. tm: Do --............. "."."."..,........� ........ .I.I.I..-..-.-,,'.- .... �'....,.�...�..�..��...�.I..,..."..,...............-....,.I .. ..... 1: . .. .. ........ .A..,,.,o.nning.���:��:::::::::::::::.--- . -W.::::::::.�.�.::.:�'i.:.].:.:::I ............ ;:;::::::::�::-.-.. .. ..-..- ....... ....... .. .--- .. .. ........ .- .1.��,.�...'�.I.I...".,."..,..,..,.....,.....,.�..I :::::: -:::::.I..-1' '.....-'.....'....".... :::::::�::�::::: I.. ' ' '' '::':::::x-'-'..I.. ..... .-.1- .. I....-,..... ---...-- .t.t. -mg..�.,<�:'X.XX: ... .:::.....,..,..�..��..�..�"".. .,...'-........ -.....1.11.1'.. -1- .. .... �auq . .i i��nja:.:.:.:.:.:.::.:-:-X.:'X. ::�::�:::::::::::::::::::,.�'..,.�,.�......�..��.:::m1. .... --- -"�". ������������:�����:��*i�������aII6*.�itt3jorse. :- ,��ff ' ::::::::::::,......I....... .,'."."..'.'...'..�.'�....--rm:er,.M.. .. ... ..... .:"...... I--L,. .. �....... .W...., ': 6wi6w.:,��:.:,:�:.:.��:.:��:�:��..,.:::::::::-:::::w::::!::!"' -1. 1. .1-1. 1.11 .l.... 1.11 ....... ... .....T'.-':.:::::::::::j:.-::::!: 1. -- .I..''.--..-..::::::::�::�::�::::::::::::::::::�::::::::::::::::::::::::::::::::: :::�::::::::::::: ::!::: � �� � ". I. � � ---: ..'.1-1-1.11-1: ......... ..... ...... .. .....I........ :�:-: ::::::.....,.....,.�,.�,,�..............".

- �-. " "",��...e:'I --h'I. ... .... .::::,. .... . " ''....0. �.. -- ft .... I.I.....--..... 11,.::: �: -'::':':-..-.-:.:� AMC , 'idt.ig :.�-....'.:WI :x: - ... '. .x::v:::!��.: l: �. .. .. .r strawl v stm ::.dub fO c :..:.P.,..nIa..: 1�-.:.-::::::::: :::::::. .. . c-In .All n, �:W. ,, :1-4..C-4 .':::...... -- ........... -- ........:....%,:..:::::::.:,:,.:::�:,:,:.::::::�:::::::�.I..,..,.. , ,,",.---,.' .-.- �' . - PF - � -v ,W'. ��V=ll ...... W�iI-�. 1-1 ...�......... ...........-�. .. .... -- -1---- -- - - - - �. 1. .- 1. -..... -.- '"'" "'I...I....I.....-.....-.-I....- I.. ---- �.,.. I.. �.. �. � -- '.. .... 1-1-- ......... - -.. ..... -- ... ........ .-. 1-1 --- .... .. ''. -...... -.1--l .... .........�.......�..............,..�.�..'�.I..��'...'�..."".",..�'..�.,��.21���,��,�''::]:.:�:�.::::I.-I-l"I'l.'........-I .- --,'... �., ,.,.,..,.�..�...,.,.::.:.::.�::::::::::::::::::::::::::::::::::: .:: I.,-'' "'....... ....... ....-. ..... .. 1-1--l.... ....b...,..................'... ..... .....- �' �ftkkir&'Ailltitioft. ...' 1, I I ."-"....,...,... - ��-"'.......�.. - -� .1-1-1-I...'.....''.-I ... � .. � �:::::::::: �... �..I.....,.....�."..,:::::::::::::: -::�:: :�X::::::::!:::!: _.. _ �.-.."..."..'..I.-.1.1 .-I.... ......-- .......... :::::::��:::X::::X:�::!:� ''. . I.''. I-- ...... �..�..�.�l::�::::::::::�::.��:,.;�:::::::�:��:::::�::::::::�:::::�:::.::::�:::�::�:::::::::::]::�:.� .......... .. ........ -- ...:::::-:::- :::::: .......... .. .I..... ..... .. .. I-- --.. � - - I.. �� � �� �� - - -.- �l I........1-1-1 .---.- .... ..I.. ....-......- . . -11 .. .. .. . .. ..... .. �.. -:... 1-1. 1. -.... ''.....-I.. -........ ................- I-- -"------ -- � 1. - 1. �' I I I..... I.., -..'..'..'..�....��.�V--11.1- .. � .1. - �� - � � . . 11 I I 1. I.''. ....... I.-- 7:�::::::]::::.�:�:::�::::::::::�::::::].:.:.: :1::::::-: ..."'..i�����������:�����..��]���������������������������������:,'.i��..,..............,...,.,�'1. -1. -- -, - � -- � " -- � ., ".-.....,.- '' .. .. ..... .�,�'..�::�::::::::]:::::�:::::::::::�::��:�:�:::::�:::::�:::::]:: - ..'.-... I... I."�,.'..,..",�,.��.�...,......I'.... ' "-- ... - '':-'- '''<-'', .. ...... , ... ,.���,�,�l',�......�����"...,."��.1l.::�:::::: ::::::::::::::-: .-. "." .. .. .. .. 4-.1'..'