Embed Size (px)

Citation preview

RELATIONSHIP BETWEEN THE MANAGING AUTHORITIES AND THE PAYING AGENCIES

IN THE MANAGEMENT OF RURAL DEVELOPMENT PROGRAMMES 2007-2013. Felix Lozano, Head of Unit of Financial Coordination

of Rural Development, European CommissionOviedo, 29/04/2010

2

TOPICS

I. Basic principles

II. National authorities involved in the implementation of RDP

III. Improving the implementation of programmes

IV. Particular aspects of the Axis 4 management

3

Basic principles

Basic management rules Legal framework 2007-2013 for rural development The delegation principle

4

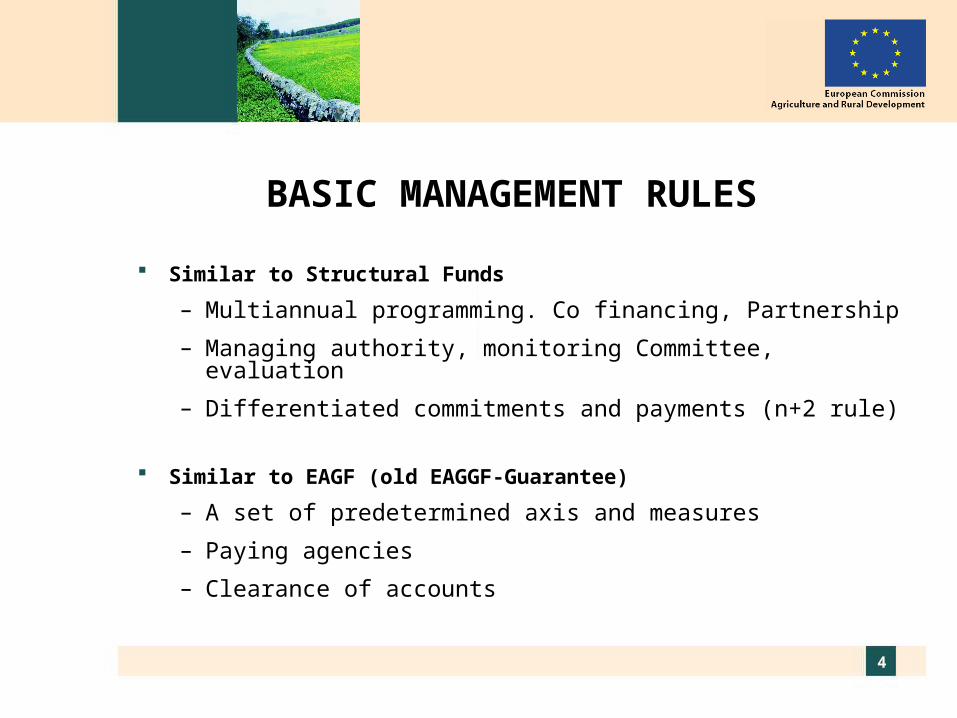

BASIC MANAGEMENT RULES

Similar to Structural Funds

– Multiannual programming. Co financing, Partnership

– Managing authority, monitoring Committee, evaluation

– Differentiated commitments and payments (n+2 rule)

Similar to EAGF (old EAGGF-Guarantee)

– A set of predetermined axis and measures

– Paying agencies

– Clearance of accounts

5

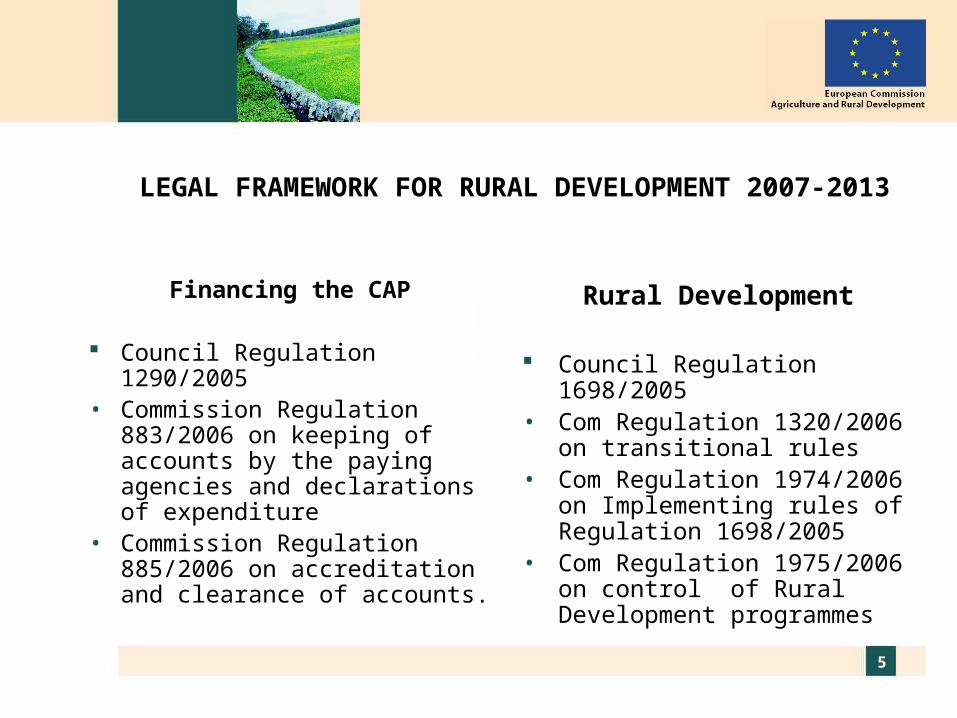

LEGAL FRAMEWORK FOR RURAL DEVELOPMENT 2007-2013

Financing the CAP

Council Regulation 1290/2005• Commission Regulation

883/2006 on keeping of accounts by the paying agencies and declarations of expenditure

• Commission Regulation 885/2006 on accreditation and clearance of accounts.

Rural Development

Council Regulation 1698/2005• Com Regulation 1320/2006 on

transitional rules• Com Regulation 1974/2006 on

Implementing rules of Regulation 1698/2005

• Com Regulation 1975/2006 on control of Rural Development programmes

6

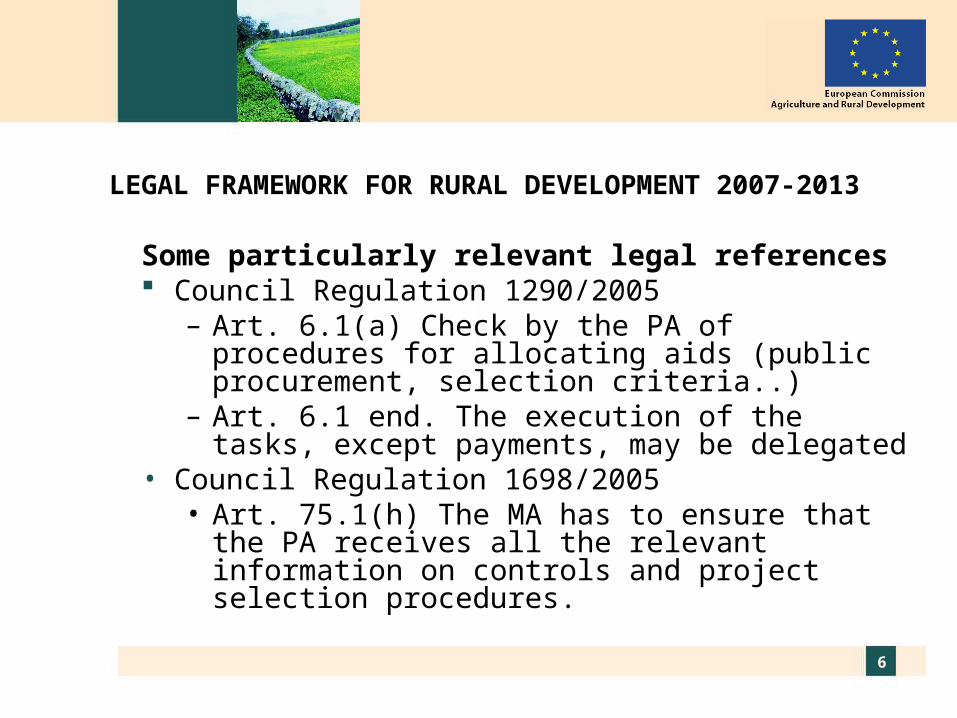

LEGAL FRAMEWORK FOR RURAL DEVELOPMENT 2007-2013

Some particularly relevant legal references Council Regulation 1290/2005

– Art. 6.1(a) Check by the PA of procedures for allocating aids (public procurement, selection criteria..)

– Art. 6.1 end. The execution of the tasks, except payments, may be delegated

• Council Regulation 1698/2005 • Art. 75.1(h) The MA has to ensure that the PA

receives all the relevant information on controls and project selection procedures.

7

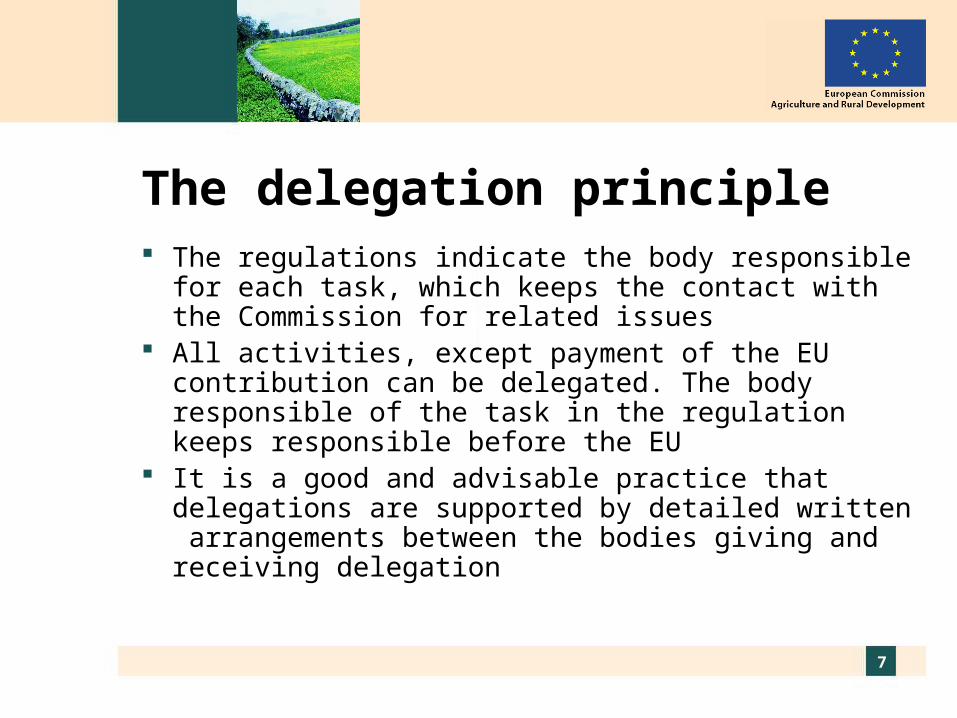

The delegation principle The regulations indicate the body responsible for

each task, which keeps the contact with the Commission for related issues

All activities, except payment of the EU contribution can be delegated. The body responsible of the task in the regulation keeps responsible before the EU

It is a good and advisable practice that delegations are supported by detailed written arrangements between the bodies giving and receiving delegation

8

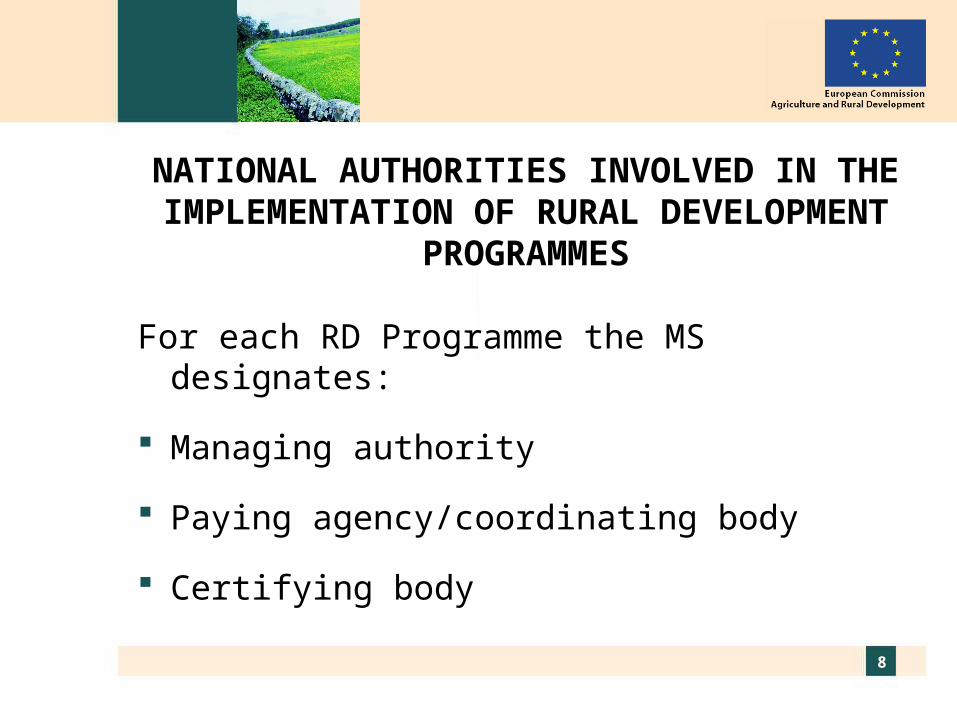

NATIONAL AUTHORITIES INVOLVED IN THE IMPLEMENTATION OF RURAL DEVELOPMENT

PROGRAMMES

For each RD Programme the MS designates:

Managing authority

Paying agency/coordinating body

Certifying body

9

The Managing Authority main functions

In charge of rural development policy and definition of the RD strategy and the RD programme

Chairs the monitoring committee and ensures the participation of local, economical and social partners

Selects projects for financing in accordance with selection criteria

Collects information on execution, output and impact indicators, for monitoring and evaluation purposes

Organizes preparation and submission of annual reports and evaluations.

10

The Managing Authority responsibilities Ensuring that operations are selected in accordance

with the selection criteria and public procurement procedures

Ensuring that there is a system to record and maintain statistical information on implementation

Ensuring that beneficiaries and other bodies involved are informed of their obligations resulting from the aid granted (audit trail and report obligations)

Ensuring that the paying agency receives all necessary information, in particular on internal procedures and controls operated

11

The Paying Agency main Functions

- Makes payments to beneficiaries

- Controls the eligibility of requests and, for rural development, the procedures for allocating aids and their compliance with EU rules

- Keeps the accounts and issues the annual accounts

- Issues an annual statement of assurance signed by the Director of the Paying Agency

- Pursues and recover irregularities.

12

The Paying Agency Responsibilities

- Ensures that the eligibility of the requests and the procedures for allocating aids have been checked before authorizing payments

- Ensures accurate and exhaustive accounts

- Ensures the checks and controls laid down by EU legislation

- Ensures that the requisite documents (expenditure declarations and annual accounts), are presented within the deadline and under the form required

- Ensures that complete, valid and legible documents are accessible and kept overtime

13

THE CERTIFYING BODY

• Private or public legal entity independent of the paying agency and coordinating body

• Annually issues an audit opinion on the truthfulness, completeness and accuracy of the annual accounts of the paying agency

• Assess the administrative structure and control procedures for the new paying agencies

• Annually reports on the PA compliance with the accreditation criteria

14

IMPROVING THE IMPLEMENTATION OF RURAL DEVELOPMENT PROGRAMMES

Main findings of the Commission’s audit reports Main findings in the Court of Auditors’ audits Statistics on error rate

15

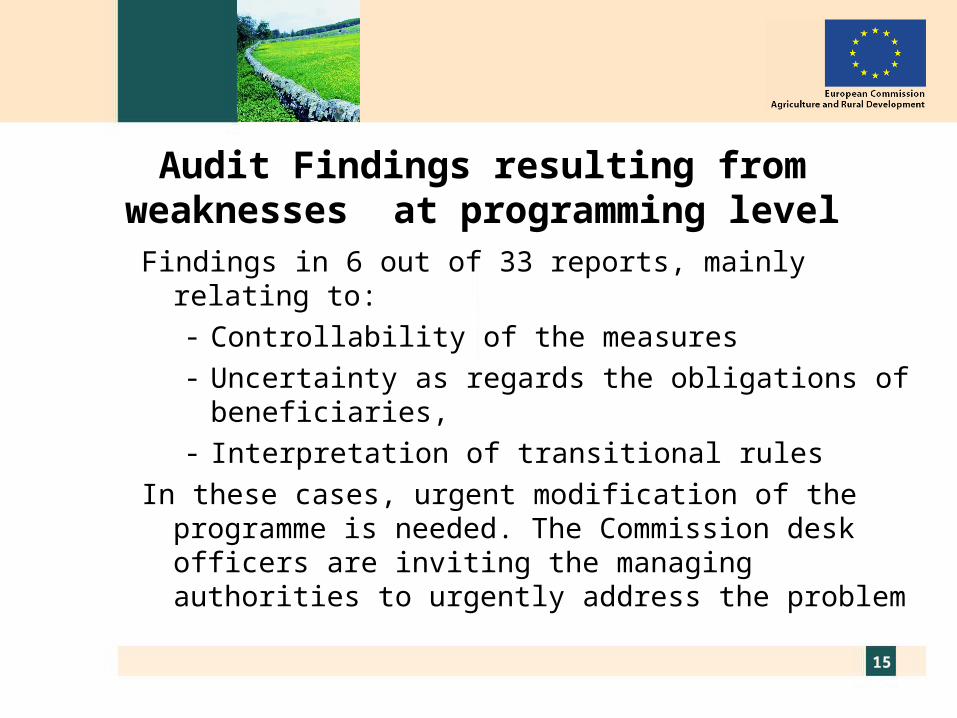

Audit Findings resulting from weaknesses at programming level

Findings in 6 out of 33 reports, mainly relating to:- Controllability of the measures- Uncertainty as regards the obligations of

beneficiaries, - Interpretation of transitional rules

In these cases, urgent modification of the programme is needed. The Commission desk officers are inviting the managing authorities to urgently address the problem

16

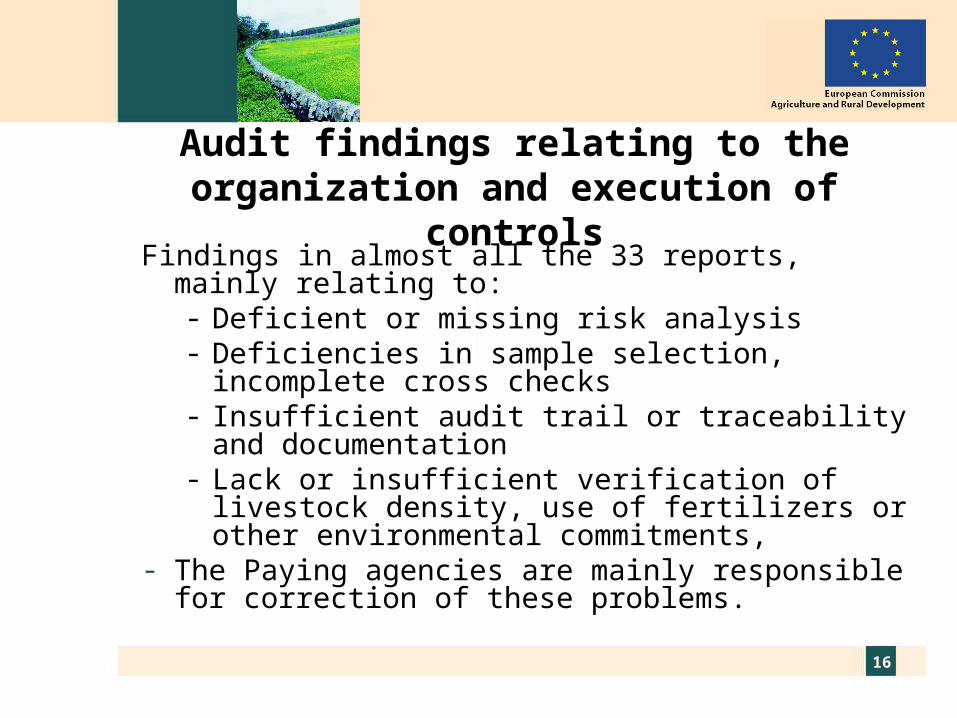

Audit findings relating to the organization and execution of controls

Findings in almost all the 33 reports, mainly relating to:- Deficient or missing risk analysis- Deficiencies in sample selection, incomplete

cross checks- Insufficient audit trail or traceability and

documentation - Lack or insufficient verification of livestock

density, use of fertilizers or other environmental commitments,

- The Paying agencies are mainly responsible for correction of these problems.

17

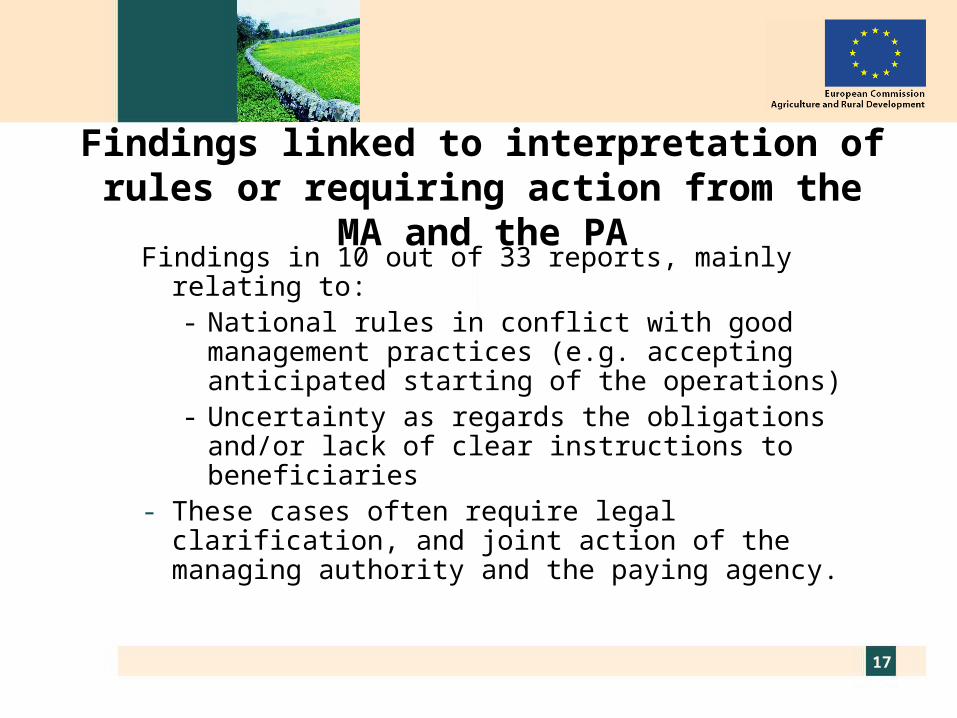

Findings linked to interpretation of rules or requiring action from the MA and the PAFindings in 10 out of 33 reports, mainly relating to:

- National rules in conflict with good management practices (e.g. accepting anticipated starting of the operations)

- Uncertainty as regards the obligations and/or lack of clear instructions to beneficiaries

- These cases often require legal clarification, and joint action of the managing authority and the paying agency.

18

COURT OF AUDITORS FINDINGS

7 audit from the European Court of Auditors issued in the DAS (statement of assurance) context at the end of 2009 reported 85 preliminary findings of which:- 4 findings related to problems to be addressed at the level

of the RDP (controllability, ambiguous requirements..) - 50 findings referred to weaknesses in the management

and control systems (low number of checks, low reliability of area information, weak risk analysis…)

- 31 findings related to errors in underlying transactions (data input errors, over payments, over declaration, non respect of eligibility conditions

19

Main findings from the Paying Agency Does the Paying Agency analyse the results

of its individual controls and summarise them in the form of main findings?

Does the Paying Agency report to the managing authority its main findings?

Do the Paying Agency and the Management Authority organise on a yearly basis a dialogue on possible improvements to the programmes ?

20

Article 34 statistics, the necessary tool for a structured dialogue Error rates per measure are a good indicator

of implementing difficulties They allow monitoring the impact of

previous improvements They allow identifying areas where further

improvements are necessary They shall be available in due time

21

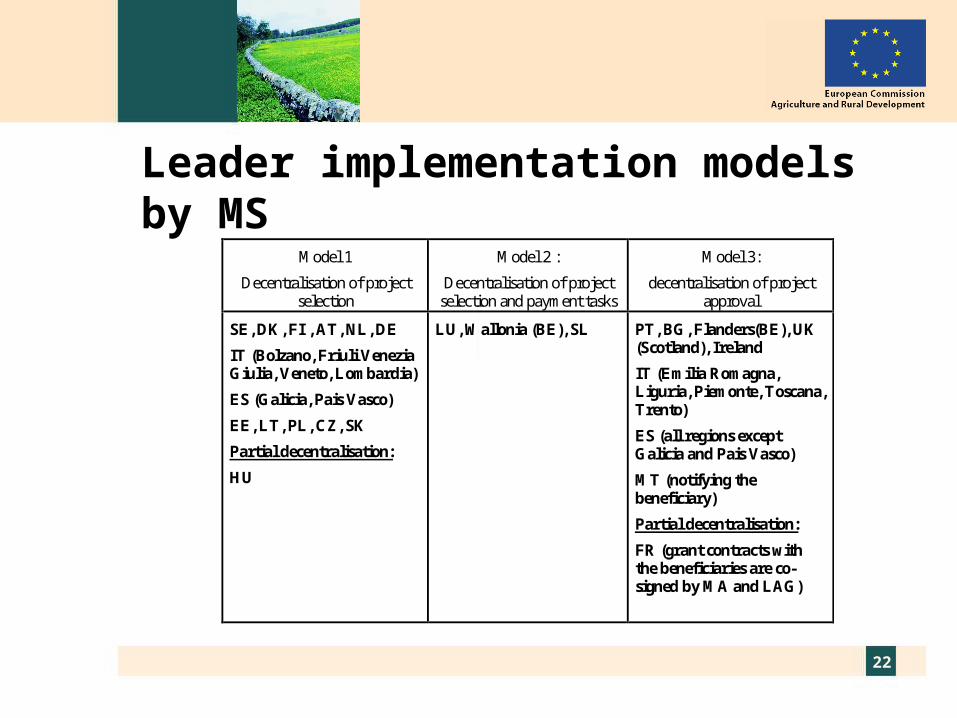

Implementing Axis 4 A typology of Leader implementation models

– Decentralisation of project selection competence (The LAG calls for tenders, assess projects and proposes projects for approval)

– Decentralisation of project selection and payment competence. The LAG also pays the public aid

– Decentralisation of project formal approval. The LAG formally approves the project and legally commits the aid toward the beneficiary

22

Leader implementation models by MS

Model 1

Decentralisation of project selection

Model 2 :

Decentralisation of project selection and payment tasks

Model 3:

decentralisation of project approval

SE, DK, FI , AT, NL, DE

IT (Bolzano, Friuli Venezia Giulia, Veneto, Lombardia)

ES (Galicia, Pais Vasco)

EE, LT, PL, CZ, SK

Partial decentralisation:

HU

LU, Wallonia (BE), SL

PT, BG, Flanders(BE), UK (Scotland), Ireland

IT (Emilia Romagna, Liguria, Piemonte, Toscana, Trento)

ES (all regions except Galicia and Pais Vasco)

MT (notifying the beneficiary)

Partial decentralisation:

FR (grant contracts with the beneficiaries are co-signed by MA and LAG)

23

Controlling Axis 4 actions To be agreed ex-ante:

– Clear definition and controllability of the actions implementing the local strategy and of the obligations of beneficiaries

– Written-ex ante arrangements between the local action group (public-private partnership), and the managing authority as regards delegated tasks, management and responsibilities

– Clear distribution of tasks and responsibilities between the managing authority and the paying agency as regards control of operations.

24

Thank you for your attention