Embed Size (px)

Citation preview

Serbia Investment andExport Promotion Agency

Vlajkoviceva 311000 Belgrade

phone: +381 11 3398 550fax: +381 11 3398 814

[email protected] Real Estate Industry in Serbia

Contents

Plaza Centers in Serbia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2Key Information on Serbia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3Why Invest in the Real Estate Industry in Serbia . . . . . . . 4Overview of the Real Estate Industry

Basic Industry Indicators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6Office Market Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7Residential Market Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9Retail Market Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10FDI in the Real Estate Industry . . . . . . . . . . . . . . . . . . . . . . . 11

Africa-Israel Corporation & Tidhar Group in Serbia . . . 12Acquiring Construction Land

Land Classification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14Leasing Municipality Land . . . . . . . . . . . . . . . . . . . . . . . . . . . 15Acquiring the Right to Use Land . . . . . . . . . . . . . . . . . . . . . 16Conversion of Agricultural Land . . . . . . . . . . . . . . . . . . . . . 17

GTC International in Serbia . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18Construction Procedure

Assessment of Urban Conditions . . . . . . . . . . . . . . . . . . . . 19Construction Approval . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19Land Development Fee Payment andMain Project Preparation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20Notice of the Start of Construction. . . . . . . . . . . . . . . . . . . 20Construction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20Occupancy Permit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20Registration in the Cadastre. . . . . . . . . . . . . . . . . . . . . . . . . . 21Financing Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Real Estate TransferReal Estate Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Related Contacts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23SIEPA Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

2

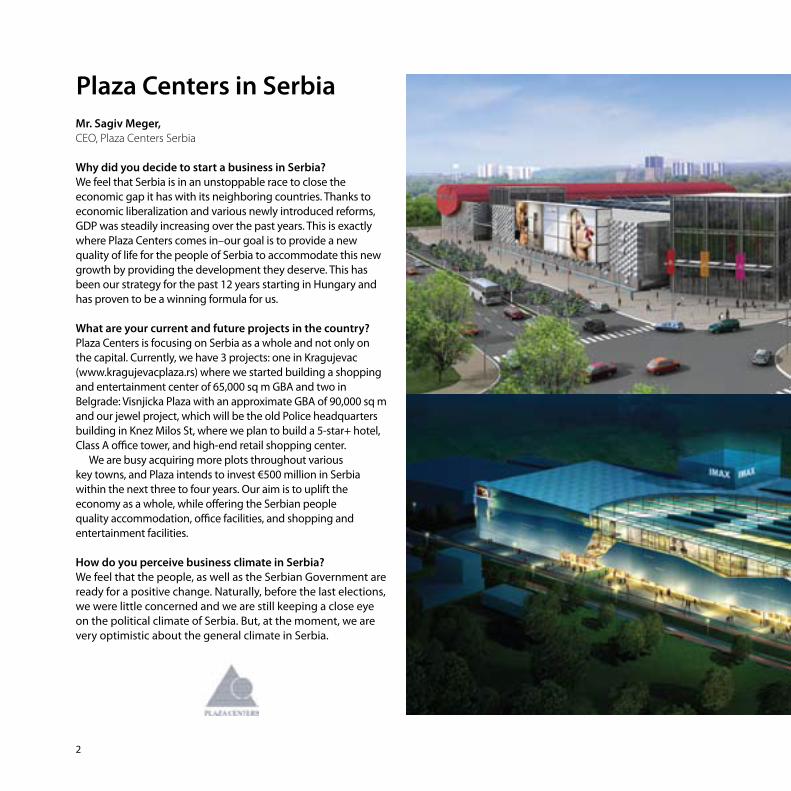

Mr. Sagiv Meger,CEO, Plaza Centers Serbia

Why did you decide to start a business in Serbia?We feel that Serbia is in an unstoppable race to close the economic gap it has with its neighboring countries. Thanks to economic liberalization and various newly introduced reforms, GDP was steadily increasing over the past years. This is exactly where Plaza Centers comes in–our goal is to provide a new quality of life for the people of Serbia to accommodate this new growth by providing the development they deserve. This has been our strategy for the past 12 years starting in Hungary and has proven to be a winning formula for us.

What are your current and future projects in the country?Plaza Centers is focusing on Serbia as a whole and not only on the capital. Currently, we have 3 projects: one in Kragujevac (www.kragujevacplaza.rs) where we started building a shopping and entertainment center of 65,000 sq m GBA and two in Belgrade: Visnjicka Plaza with an approximate GBA of 90,000 sq m and our jewel project, which will be the old Police headquarters building in Knez Milos St, where we plan to build a 5-star+ hotel, Class A office tower, and high-end retail shopping center.

We are busy acquiring more plots throughout various key towns, and Plaza intends to invest €500 million in Serbia within the next three to four years. Our aim is to uplift the economy as a whole, while offering the Serbian people quality accommodation, office facilities, and shopping and entertainment facilities.

How do you perceive business climate in Serbia?We feel that the people, as well as the Serbian Government are ready for a positive change. Naturally, before the last elections, we were little concerned and we are still keeping a close eye on the political climate of Serbia. But, at the moment, we are very optimistic about the general climate in Serbia.

Plaza Centers in Serbia

3

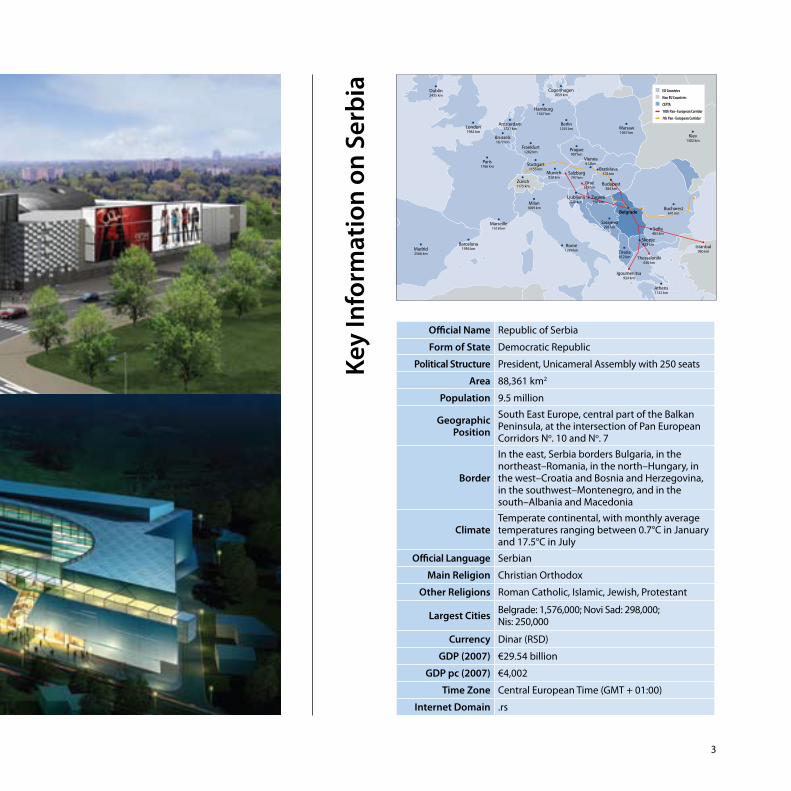

Official Name Republic of Serbia

Form of State Democratic Republic

Political Structure President, Unicameral Assembly with 250 seats

Area 88,361 km2

Population 9.5 million

GeographicPosition

South East Europe, central part of the Balkan Peninsula, at the intersection of Pan European Corridors No. 10 and No. 7

Border

In the east, Serbia borders Bulgaria, in the northeast–Romania, in the north–Hungary, in the west–Croatia and Bosnia and Herzegovina, in the southwest–Montenegro, and in the south–Albania and Macedonia

ClimateTemperate continental, with monthly average temperatures ranging between 0.7°C in January and 17.5°C in July

Official Language Serbian

Main Religion Christian Orthodox

Other Religions Roman Catholic, Islamic, Jewish, Protestant

Largest Cities Belgrade: 1,576,000; Novi Sad: 298,000;Nis: 250,000

Currency Dinar (RSD)

GDP (2007) €29.54 billion

GDP pc (2007) €4,002

Time Zone Central European Time (GMT + 01:00)

Internet Domain .rs

Bucharest641 km

Kiev1302 km

Warsaw1067 km

Berlin1255 km

Hamburg1547 km

Copenhagen1659 km

Oslo2109 km

Stockholm2154 km

Prague907 km

Stuttgart1155 km

Frankfurt1282 km

Munich930 km

Paris1766 km

London1982 km

Dublin2435 km

Amsterdam1721 km

Brussels1672 km

Riga1768 km

Helsinki2083 km

Tallinn2075 km

So�a403 km

Belgrade

Sarajevo291 km

Zagreb390 km

Salzburg797 km

Graz575 km

Vienna612km

Bratislava578 km

Rome1289 km

Milan1009 km

Zürich1175 km

Marseille1518 km

Barcelona1956 kmMadrid

2566 km

Budapest384 km

Ljubljana520 km

Istanbul980 km

Skopje423 km

Thessaloniki630 km

Igoumenitsa924 km

Tirana612 km

Athens1132 km

EU Countries

Non EU Countries

CEFTA

10th Pan–European Corridor

7th Pan–European Corridor

Key

Info

rmat

ion

on S

erbi

a

4

Competitive tax SyStem

Serbia’s tax regime is highly conducive to doing business. Corporate profit tax is the second lowest in Europe, while VAT is among the most competitive ones in Central and Eastern Europe. In addition, businesses in the country can take advantage of a broad range of tax incentives.

RobuSt ReCent GRowth

For years, Serbia was among Europe’s fastest growing economies. Between 2004 and 2008, economic growth averaged 6.3%, while GDP per capita almost doubled. Strong GDP performance was largely driven by service sectors such as telecommunications, retail, and banking. In addition, local food, beverage and construction industries expanded rapidly. Based on the metal, food, textile, chemical, machinery, and furniture sectors, Serbian exports also increased at a sharp rate of more than 33% annually.

GDP Growth Rate

2007 6.9%

2008 5.4%

2006 5.2%

2005 5.6%

2004 8.3%Source: Statistical O�ce of the Republic of Serbia

Why Invest in the Real Estate Industry in Serbia

Principal Tax Rates and Tax Incentives

VAT Standard rate – 18%Lower rate – 8%

Corporate Profit Tax Uniform rate – 10%

Withholding Tax20% (for dividends, shares in profits, royalties, interest income, capital gains, lease payments for real estate, and other assets)

Personal Income Tax Salaries – 12%Other income – 20%

Annual Income Tax 10% (for annual income above 5 average annual salaries)

Social Insurance Contributions

Pension and disability insurance – 11%Health insurance – 6.15%Unemployment insurance – 0.75%

Tax Incentives

A 10-year corporate profit tax holiday for investments of over €7 million that create at least 100 new jobs

A corporate profit tax credit of 20% of the fixed assets investment

Carrying forward of losses over a period of up to 10 years

Accelerated depreciation of fixed assets

Salary tax base deduction in the fixed amount of RSD 5,938 (app. €65)

Salary tax exemptions for employees below 30 and above 45 years

Social insurance contributions exemptions for employees below 30 and above 45 years

Annual income tax deductions of up to 50% of the taxable income

Customs-free imports of equipment based on foreign investment

5

StRonG FDi FiGuReS

Since the onset of economic reforms in 2001, Serbia has grown into one of the premier emerging investment locations in Central and Eastern Europe, with the FDI inflow of over €12 billion. The list of leading foreign investors is topped by world-class companies and banks such as Telenor, Philip Morris, Mobilkom, Banca Intesa, AB InBev, and many others.

According to PwC, Serbia is the 3rd most attractive manufacturing and 7th most attractive services destination among emerging economies. Additionally, E&Y recorded over 100 inward investment projects in Serbia in 2007 and 2008–the 2nd best performance in the South East Europe region.

boominG maRket potential

In Serbia, there is strong demand in the office, residential, and retail market. As a result of robust economic growth and strong FDI forecast, demand for quality office space has been on a steady rise. Likewise, a residential market is forecast to experience an upward trend due to a steady increase in household income and a wide availability of mortgage loans. Furthermore, yields in the real estate sector tend to be higher than in other CEE countries, amounting to 10% in the office market.

low oveRheaD CoStS

One of the key advantages of doing business in Serbia compared to other CEE countries are lower operating costs. Labor costs in Serbia are comparable to those in South East European countries, while standing at less than 50% of their level in Eastern European EU member states. In addition, electricity, gas, and other utilities are available at very favorable prices.

Inward FDI (EUR mn)

2007 2,601

2006 4,279

2005 1,329

2004 788

2008 2,255

Source: National Bank of Serbia

Prime Office Yields (Q1 2009)

City Office Space Yields

Belgrade 10.00%

Sofia 10.00%

Bucharest 9.50%

Zagreb 8.50%

Budapest 7.75%

Bratislava 7.25%

Prague 7.00%

Warsaw 6.75%Source: CB Richard Ellis

Total Monthly Labor Costs in EUR (2007)

Czech Republic 1,201

Source: EUROSTAT, Croatian Central Bureau of Statistics, Statistical O�ce the Republic of Serbia

Poland 997

Croatia 973

Slovakia 927

Hungary 1,055

Serbia 566

Romania 527

6

Basic Industry Indicators

GDPAccording to the latest data available, 2007 GDP in the industry gained 10.35% in nominal terms against the previous year. With GDP of around €2.72 billion, the industry accounted for over 9% of the total economic output.

CompaniesBy mid-2008, there were 1,325 companies in the real estate industry, encompassing the following sectors:

• Real Estate Development,• Real Estate Trade,• Real Estate Renting,• Real Estate Agencies,• Real Estate Management.

Employment and SalariesThe industry employed 39,105 staff in September 2008. The qualification structure is dominated by high school and university-degree holders accounting for 35% and 28% of total industry employment, respectively. They are followed by qualified workers, with a 11% share, while other categories make up a lesser portion of the real estate labor force.

In 2008, the average monthly net salary in the real estate sector amounted to €778.

Employment by Quali�cations (September 2008)

13,902

11,039

4,164

2,8182,240

HighSchool

University Quali�ed

2,1662-Year

College

991HighlyQuali�ed

Unquali�ed

SemiQuali�ed

1,785 Elementary SchoolSource: Statistical O�ce of the Republic of Serbia

Overview of the Real Estate Industry

Average Net Monthly Salary (EUR)

2004 2005 2006 2007 2008

Net salary 424 422 491 605 778

Source: Statistical Office of the Republic of Serbia

GDP in the Real Estate Industry

2004 2005 2006 2007

GDP (EUR bn) 2.01 2.09 2.35 2.72

Share in Total Economy (%) 10.6 10.3 10.0 9.2

Source: Statistical Office of the Republic of Serbia

Total Number of Companies by Sectors (2008)

650

272

192

18031

Real Estate Development Real Estate Agencies

Real EstateTrade

Real Estate RentingReal Estate ManagementSource: Statistical O�ce of the Republic of Serbia

7

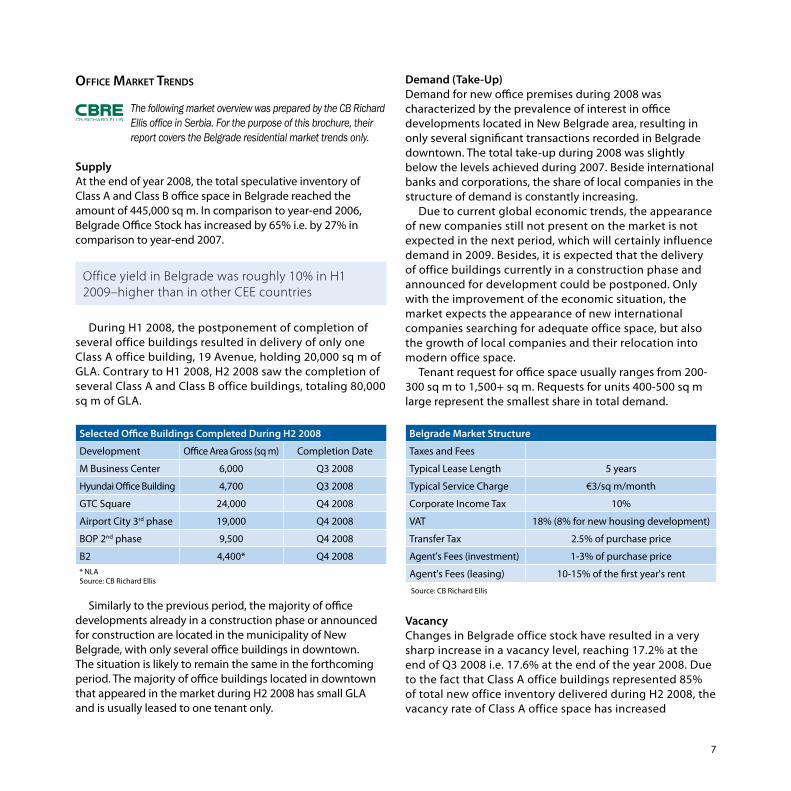

oFFiCe maRket tRenDS

The following market overview was prepared by the CB Richard Ellis office in Serbia. For the purpose of this brochure, their report covers the Belgrade residential market trends only.

SupplyAt the end of year 2008, the total speculative inventory of Class A and Class B office space in Belgrade reached the amount of 445,000 sq m. In comparison to year-end 2006, Belgrade Office Stock has increased by 65% i.e. by 27% in comparison to year-end 2007.

During H1 2008, the postponement of completion of several office buildings resulted in delivery of only one Class A office building, 19 Avenue, holding 20,000 sq m of GLA. Contrary to H1 2008, H2 2008 saw the completion of several Class A and Class B office buildings, totaling 80,000 sq m of GLA.

Similarly to the previous period, the majority of office developments already in a construction phase or announced for construction are located in the municipality of New Belgrade, with only several office buildings in downtown. The situation is likely to remain the same in the forthcoming period. The majority of office buildings located in downtown that appeared in the market during H2 2008 has small GLA and is usually leased to one tenant only.

Demand (Take-Up)Demand for new office premises during 2008 was characterized by the prevalence of interest in office developments located in New Belgrade area, resulting in only several significant transactions recorded in Belgrade downtown. The total take-up during 2008 was slightly below the levels achieved during 2007. Beside international banks and corporations, the share of local companies in the structure of demand is constantly increasing.

Due to current global economic trends, the appearance of new companies still not present on the market is not expected in the next period, which will certainly influence demand in 2009. Besides, it is expected that the delivery of office buildings currently in a construction phase and announced for development could be postponed. Only with the improvement of the economic situation, the market expects the appearance of new international companies searching for adequate office space, but also the growth of local companies and their relocation into modern office space.

Tenant request for office space usually ranges from 200-300 sq m to 1,500+ sq m. Requests for units 400-500 sq m large represent the smallest share in total demand.

VacancyChanges in Belgrade office stock have resulted in a very sharp increase in a vacancy level, reaching 17.2% at the end of Q3 2008 i.e. 17.6% at the end of the year 2008. Due to the fact that Class A office buildings represented 85% of total new office inventory delivered during H2 2008, the vacancy rate of Class A office space has increased

Office yield in Belgrade was roughly 10% in H1 2009–higher than in other CEE countries

Belgrade Market Structure

Taxes and Fees

Typical Lease Length 5 years

Typical Service Charge €3/sq m/month

Corporate Income Tax 10%

VAT 18% (8% for new housing development)

Transfer Tax 2.5% of purchase price

Agent's Fees (investment) 1-3% of purchase price

Agent's Fees (leasing) 10-15% of the first year's rent

Source: CB Richard Ellis

Selected Office Buildings Completed During H2 2008

Development Office Area Gross (sq m) Completion Date

M Business Center 6,000 Q3 2008

Hyundai Office Building 4,700 Q3 2008

GTC Square 24,000 Q4 2008

Airport City 3rd phase 19,000 Q4 2008

BOP 2nd phase 9,500 Q4 2008

B2 4,400* Q4 2008* NLASource: CB Richard Ellis

8

much more significantly than the vacancy rate of Class B office space. Pipeline developments due for completion in Q1 2009 are not expected to change the vacancy rate significantly.

Rental LevelsRental levels of Class A office space during 2008 have slightly decreased in comparison to 2007. Recently finished Class A office buildings command asking rental values of €16.5-18.0/sq m/month, while for office space under construction, they range between €15-17/sq m/month. Brand new properties situated at some of the most attractive locations in Belgrade have recorded asking rents of up to €19/sq m/month. Rents for Grade B stock vary between €11 and €13/sq m/month.

Future SupplyDuring Q1 2009, the completion of additional 65,000 sq m of quality office space is expected, while all projects announced for completion by year-end 2009 should increase Belgrade Office stock by a total of 130,000 sq m of GLA. By the end of year 2010, Belgrade Office stock should reach the level of 625,000 sq m.

Belgrade Prime Office Rents

Office Class €/sq m/month

Class A 15.00 to 17.00

Class B 11.00 to 13.00

Class C 9.00 to 12.00

Source: CB Richard Ellis

Selected Pipeline Developments

Development GLA (sq m) Completion Date

Airport City 1700 11,800 2009

Bluehouse block 26 35,000 2009

Sava Business Center 21,000 2009

Belville Office building 28,000 2009

Tri lista duvana 8,500 2009

B23 53,000 2010

VIG Plaza 9,000 2010

Source: CB Richard Ellis

Belgrade Office Vacancy Rates

Office Class Vacancy Rate

Class A To 15.0%

Class B To 21.0%

Overall 17.6%

Source: CB Richard Ellis

9

ReSiDential maRket tRenDS

The following market overview was prepared by the CB Richard Ellis office in Serbia. For the purpose of this brochure, their report covers the Belgrade residential market trends only.

The residential market in Belgrade continues its expansion, recording a high construction activity. Nevertheless, supply is not keeping up with demand. A considerable discrepancy between the two does exist and will continue so in the foreseeable future.

Beside local developers, several international developers have announced the construction of large projects in the next few years.

SupplyAccording to the Belgrade Statistical Bureau, 7,601 residential units were constructed in Belgrade during 2007, only 222 units more than in 2006. Regarding the structure of those units, 31.6% of them are studios, while the percentage of one-bedroom apartments is 26.6%.

According to the official statistics and CB Richard Ellis research, New Belgrade and Zvezdara areas experienced the largest increase in residential projects during 2007, with 1,340 residential units constructed in each municipality. There is a difference though in an average apartment size, totaling 57.8 sq m in Zvezdara and 66.9 sq m in New Belgrade. The average size of apartments constructed during 2007 in whole Belgrade area was 71.2 sq m, only slightly above average for year 2006, standing at 70.1 sq m.

Two very attractive municipalities in Belgrade, Vracar and Stari Grad, are faced with a limited availability of construction sites. Projects located in these areas are of

a modest size, totaling on average 15-20 units. Vracar municipality has marked a significant decrease in the number of completed units, totaling only 232 units in 2007 in comparison to 805 units brought to the market during 2006. Stari Grad municipality marked an increase of 66% with 93 units in 2007 in comparison to 56 in 2006.

Besides mid-end residential projects, supply of high-end residential developments is constantly increasing. New Belgrade area becomes more and more interesting, with two high-end residential developments currently in a construction phase, located in close proximity of rivers Sava and Danube.

DemandDuring the last five years, there was strong demand for apartments of smaller sizes on the mid-end market. Investors were oriented towards the creation of complexes with a high share of small, affordable apartments–mostly studios and one-bedroom apartments. Demand for high-end apartment units comes mostly from wealthy locals and Serbian Diaspora, as well as from companies purchasing apartments for their expatriates or their employees, buying apartments for themselves.

Very strong demand recorded during the first three months of the second year-half of 2008 has taken the slower pace starting from September.

A current global economic crisis has made the potential buyers more prudent when taking a loan, previously the main source of financing for a large portion of buyers. According to data provided by the National Bank of Serbia, at the end of the year 2008, housing loans taken by Serbian citizens amounted to RSD 170 billion (€1.92 billion), 59% more than at the end of the year 2007.

Selected Projects Announced for Development

Name Size Gross (sq m)Date ofDelivery

Kalemegdan Park Apartments 12,000 2009/2010

Airport City residential project 66,000 n/a

Lamda, Juzni Boulevard 10,000 n/a

Yu Kapital, Kraljice Marije Street 7,200 n/a

Neimar – V, Radoja Dakica Street 7,000 n/a

Source: CB Richard Ellis

Selected Biggest Current Projects

Name Size Gross (sq m) Date of Delivery

Block 11 c 15,500 Q1 2009

Savograd 12,000 Q1 2009

Belville 120,000 Q4 2009

Galerija Apartments 18,500 Q4 2009

Block 11 a 22,000 Q2 2010Source: CB Richard Ellis

10

Sales PricesAccording to the Belgrade Statistical Office, average net prices of new apartments in Belgrade reached €1,459/sq m at the end of the year 2007 (in comparison to €1,407/sq m at the end of H1 2007). This figure includes the price of construction land, construction costs, and additional costs.

During the first three months of H2 2008, asking prices have recorded an increase of 5-10%, depending on a municipality. A global financial crisis has slowed down or even stopped a further price increase in 2008 second year-half.

Mid-end residential developments located in the municipality of New Belgrade recorded asking prices of €1,700-2,500/sq m, while those located in the municipalities of Vracar, Stari Grad, and Dedinje were marketed at €2,000-3,000/sq m. High-end developments located at very attractive locations in New Belgrade and downtown have recorded the levels of even €3,500-4,000/sq m. (All prices indicated are net of VAT).

Rental LevelsRental prices have retained the levels achieved during H1 2008. Demand is primarily oriented towards the municipalities of Dedinje, Senjak, and Vracar, proven to be most attractive for employees of foreign embassies and international organizations. An upward trend in demand has also been marked in the municipality of New Belgrade, especially in the area near Arena Sports Hall.

Retail maRket tRenDS

The following market overview was prepared by theCB Richard Ellis office in Serbia.

According to data provided by the Statistical Office of the Republic of Serbia, compared to the same period of the previous year, the turnover of retail trade in Q3 2008 noted 22.3% growth at current prices in the Republic of Serbia, 28.3% growth in Central Serbia, and 5.2% growth in Vojvodina. With regard to the same period, the wholesale trade at current prices noted growth of 18.9% in the Republic of Serbia, growth of 12.4% in Central Serbia, and 39.3% growth in Vojvodina. (Ø2007=100)

Shopping CentersH2 2008 witnessed no new shopping center openings in Belgrade. The current stock of modern shopping centers in both Belgrade and Serbia still lags behind the trends in more

developed countries of Central and Eastern Europe (CEE). The fact that, in comparison to other CEE capitals, the shopping center stock per capita in Belgrade is very low provides possibilities for significant development.

International retailers with established regional presence, as well as domestic brands and retailers are the driving force of demand for retail units in Belgrade modern shopping centers. Although there were changes in tenant mix in some of the biggest shopping centers in Belgrade, they still record zero vacancy. The interest of retailers for old-style shopping centers decreases, even for shopping centers located in the close proximity of Belgrade pedestrian zone.

Usce shopping center, located in New Belgrade block 16, featuring 50,000 sq m of GLA is scheduled for completion in Q1 2009. Once opened, it will be the biggest modern shopping center in Belgrade.

The very first modern shopping center in Belgrade downtown is to be constructed in Rajiceva Street, in the immediate proximity of a pedestrian zone. Preparation works for the construction of this mixed-use development have started and the completion is announced for 2011. This modern complex with a total area of 46,000 sq m will comprise a shopping mall, the first five-star hotel with the capacity of 240 hotel units, and underground garages.

Prime rental values in modern shopping centers retained the same levels as in H1 2008 and stand at €40-60/sq m/month.

The interest of both international and local developers in Serbian retail market is constantly increasing, which reflects the number of shopping centers planned for construction. Beside Belgrade, Novi Sad and Nis, other Serbian cities like Kragujevac, Subotica, Sabac, and Valjevo will see new developments in the next three years.

Modern Shopping Centers in the Pipeline in Serbia

Project Location GBA (sq m) Opening Year

Usce Belgrade 130,000 Q1 2009

Mercator Sabac 23,000 2009

Plaza Kragujevac 65,000 2010

GTC Subotica 25,000 2010

MPC Nis 22,000 2010

Source: CB Richard Ellis

11

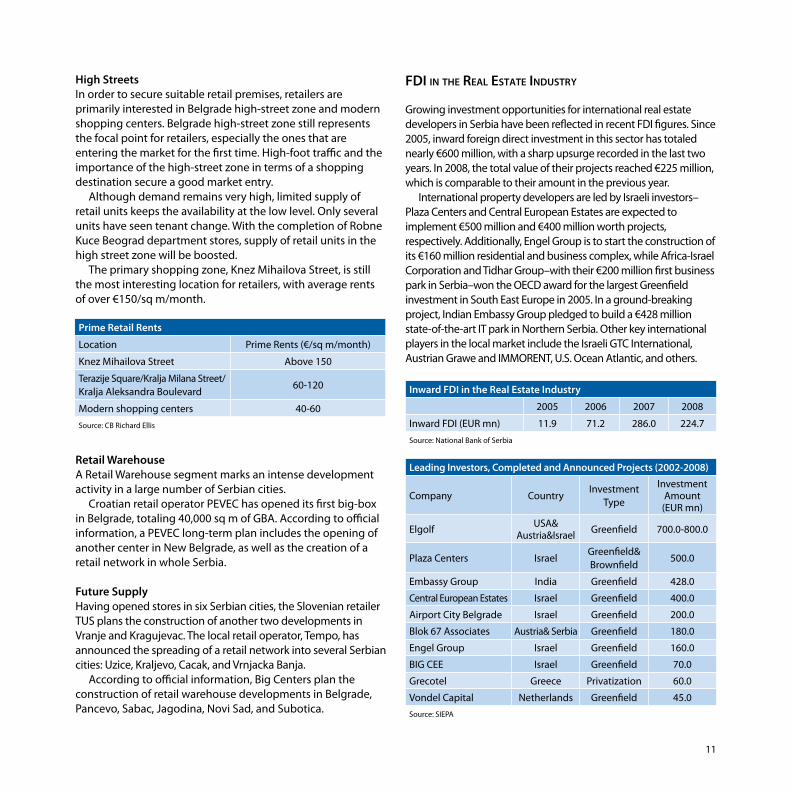

High StreetsIn order to secure suitable retail premises, retailers are primarily interested in Belgrade high-street zone and modern shopping centers. Belgrade high-street zone still represents the focal point for retailers, especially the ones that are entering the market for the first time. High-foot traffic and the importance of the high-street zone in terms of a shopping destination secure a good market entry.

Although demand remains very high, limited supply of retail units keeps the availability at the low level. Only several units have seen tenant change. With the completion of Robne Kuce Beograd department stores, supply of retail units in the high street zone will be boosted.

The primary shopping zone, Knez Mihailova Street, is still the most interesting location for retailers, with average rents of over €150/sq m/month.

Retail WarehouseA Retail Warehouse segment marks an intense development activity in a large number of Serbian cities.

Croatian retail operator PEVEC has opened its first big-box in Belgrade, totaling 40,000 sq m of GBA. According to official information, a PEVEC long-term plan includes the opening of another center in New Belgrade, as well as the creation of a retail network in whole Serbia.

Future SupplyHaving opened stores in six Serbian cities, the Slovenian retailer TUS plans the construction of another two developments in Vranje and Kragujevac. The local retail operator, Tempo, has announced the spreading of a retail network into several Serbian cities: Uzice, Kraljevo, Cacak, and Vrnjacka Banja.

According to official information, Big Centers plan the construction of retail warehouse developments in Belgrade, Pancevo, Sabac, Jagodina, Novi Sad, and Subotica.

FDi in the Real eState inDuStRy

Growing investment opportunities for international real estate developers in Serbia have been reflected in recent FDI figures. Since 2005, inward foreign direct investment in this sector has totaled nearly €600 million, with a sharp upsurge recorded in the last two years. In 2008, the total value of their projects reached €225 million, which is comparable to their amount in the previous year.

International property developers are led by Israeli investors–Plaza Centers and Central European Estates are expected to implement €500 million and €400 million worth projects, respectively. Additionally, Engel Group is to start the construction of its €160 million residential and business complex, while Africa-Israel Corporation and Tidhar Group–with their €200 million first business park in Serbia–won the OECD award for the largest Greenfield investment in South East Europe in 2005. In a ground-breaking project, Indian Embassy Group pledged to build a €428 million state-of-the-art IT park in Northern Serbia. Other key international players in the local market include the Israeli GTC International, Austrian Grawe and IMMORENT, U.S. Ocean Atlantic, and others.

Inward FDI in the Real Estate Industry

2005 2006 2007 2008

Inward FDI (EUR mn) 11.9 71.2 286.0 224.7Source: National Bank of Serbia

Leading Investors, Completed and Announced Projects (2002-2008)

Company CountryInvestment

Type

Investment Amount(EUR mn)

Elgolf USA&Austria&Israel Greenfield 700.0-800.0

Plaza Centers IsraelGreenfield& Brownfield

500.0

Embassy Group India Greenfield 428.0

Central European Estates Israel Greenfield 400.0

Airport City Belgrade Israel Greenfield 200.0

Blok 67 Associates Austria& Serbia Greenfield 180.0

Engel Group Israel Greenfield 160.0

BIG CEE Israel Greenfield 70.0

Grecotel Greece Privatization 60.0

Vondel Capital Netherlands Greenfield 45.0Source: SIEPA

Prime Retail Rents

Location Prime Rents (€/sq m/month)

Knez Mihailova Street Above 150

Terazije Square/Kralja Milana Street/Kralja Aleksandra Boulevard

60-120

Modern shopping centers 40-60Source: CB Richard Ellis

12

Afr

ica-

Isra

el C

orpo

ratio

n &

Tid

har G

roup

in S

erbi

a Mr. Gili DekelCEO, Airport City Belgrade

Why did you decide to start a business in Serbia?Airport City Belgrade (ACB) is owned by Africa-Israel Corporation and Tidhar Group, one of Israel’s most successful construction companies. I came to Serbia around seven years ago to explore real estate business opportunities, already having in mind the introduction of something different from the standard office building. Developers normally identify a piece of land, acquire it, build on it, and then lease or sell the property. However, our approach is to build a complete modern business and residential complex beyond the boundaries of the city center. Airport City Belgrade is currently the biggest real estate development in Belgrade, with six buildings delivered by the end of 2008. Altogether, it is a 120,000 sq m plot of land–the largest piece of land owned by a private company in Belgrade.

Prior to arrival in Serbia, our companyhad completed developments in Russia, Ukraine, Czech Republic, Poland, and Hungary. We chose Belgrade after a thorough research of all other major sites in the region. Apart from Ljubljana, which is already well-developed, our research included cities such as Skopje, Zagreb, and Sarajevo. Among those cities, Belgrade seemed an apparent priority, with its 1.6 million population, strong economic growth, rapid internationalization of business activities, and a highly developed construction industry.

13

I would also like to emphasize that Serbia boasts skilled and capable people and we are very satisfied with our Serbian staff performance and cooperation with local construction companies.

What are your current and future projects in the country?Our development is situated in the part of the city called New Belgrade, in the close vicinity of the International E-75 Highway. Due to the lack of parking space and traffic congestion, an increasing number of local companies are now shifting their headquarters from the old part of the city to New Belgrade. I am confident that our company will be strong enough to face the rising competition in New Belgrade and erect a competitive real estate development, not only in terms of standards, but also in terms of pricing. One of the advantages of the Airport City Belgrade development is its largest ratio of parking space in Belgrade.

We believe that in the future the Serbian economy will experience steady growth and the number of cars per 1,000 people will increase significantly. Our customers are mostly foreign companies that appreciate Class A office space, the right environment for their employees, and know the advantages of being located out of the city center. We are very optimistic about the future growth prospects, otherwise we would not be ready to invest €200 million in Serbia.

How do you perceive the business climate in Serbia?Investors look for performance enhancement possibilities, and I see Serbia in terms of the future profit. At the moment, one can get better deals than those available in Serbia, but conditions will certainly get better. Therefore, investors with long-term orientation could benefit well from great opportunities in this market.

14

Acquiring Construction LandlanD ClaSSiFiCation

In Serbia, land is classified into two categories:• construction land,• agricultural land.

Construction land is the land on which structures have been built and the land that serves for the regular use of these structures, as well as the land that is designated by the corresponding plan for the construction of structures and their regular use.Construction land can be:

• public construction land,• other construction land.

Public construction land is the land on which public structures of common interest (roads, schools, hospitals, infrastructure, etc.) have been built, as well as the land designated for the construction of such structures. This kind of construction land is exclusively in state property.

Other construction land is designated for the construction of other structures–residential, offices, industrial facilities, etc. Other construction land is transferable and can be found in all types of ownership.

Construction land may be used as developed or non-developed land. Developed construction land is the land improved with structures, which are constructed and intended for permanent use.Non-developed construction land is land on which:

• No structures are erected;• Existing structures were constructed contrary to the law;• Temporary structures exist.

Agricultural land is subdivided into:• cultivable,• uncultivable.Cultivable agricultural land encompasses fields, gardens,

orchards, vineyards, and grazing fields. A cultivable land user has the obligation to till the soil or use it in accordance with its purpose.

Non-cultivable land encompasses all other unlisted types of agricultural land.

15

Agricultural land can be re-classified, i.e. it can be converted into construction land.Other construction land can be acquired in the following ways:

• By leasing land–for the period of up to 99 years, with a possibility of extension through a public bidding procedure (for land under 10,000 sq m) or a tender procedure (for building structures over10,000 sq m);

• By obtaining the “right to use” land–by acquiring a legally built structure, an investor acquires the “right to use” land under that structure, with a possibility to build new premises of even greater area, according to the master plan;

• By acquiring land through the conversion of agricultural land into construction land–by acquiring agricultural land under private ownership, with a possibility of conversion into construction land, an investor acquires the right to build a construction.

leaSinG muniCipality lanD

Other construction land under state ownership can be leased for up to 99 years under conditions prescribed only by the municipal authorities. The land is leased through either public bidding or a public tender.

The duration of a leasing contract is being determined based on the land area, purpose, depreciation period etc. Before the expiry of the leasing period, a lessor and a leasee can extend the contract period by a mutual agreement. The right of use can be obtained through a direct bargain between the municipality in question and the interested party in the following cases:

• Construction of structures for the purpose of carrying out activities of state administration and agencies, administration and agencies of autonomous provinces and of units of local self-government, and organizations in charge of public services who operate with state funds and assets, as well as other state-owned structures;

• Leasing the land to an owner of a structure who has constructed that structure without a building permit, for the purposes of obtaining construction permission, if erecting such an object is in accordance with the provisions of the Urban Plan;

• Correction of boundaries of adjacent cadastral or construction parcels.

16

Most building land can be leased from a municipality for up to 99 years, with a possibility of extension

Apart from the land fee, pad only once, the user continuously pays a fee for land use, as a type of rental fee. The fee for using developed public construction land and other construction land in state property is paid by the owner of the structure. As an exception, when the object or a part of it is leased, the fee is paid by the lessee of the object or part thereof. The fee for the use of non-developed public construction land and other construction land in state property is to be paid by the user. The amount of the fee is determined depending on the scope and degree of the property’s development, its location, access to amenities, transportation connections to the local or city center, business areas, etc.

The land fee varies heavily at the local level. There is an increasing number of municipalities, offering building land for lease free-of-charge, or at very low prices. By contrast, in Belgrade and other large cities (e.g. Novi Sad or Subotica) the fees can run over €100/sq m. However, the final price is based on the plot location, availability of utilities, number of bidders, and other factors.

All city plots are under the state property regime. Even though the land itself is public, the structures built on it are private. A person, who owns real estate built on a city plot, automatically enjoys an exclusive “right-of-use” of the plot. Upon the sale of premises, all the rights on the land under the premises and the land that serves for the regular use of the premises are transferred as well.

aCquiRinG the RiGht to uSe lanD

As opposed to long-term lease (up to 99 years), the “right to use” land is granted for an indefinite period of time based on either:

• The ownership of a building on urban land in accordance with the Urban Plan;

• The intention to construct a building on urban land (the “right to use” is related to the ownership of a building located on urban land, entitling users to permanently use the land for as long as they own the building).

17

The “right to use” is irrevocable and permanently “attached” to the ownership of a building located on a particular land plot–it is acquired, transferred, and terminated automatically, with acquisition, transfer or termination of the ownership of the building.

The “right to use” can only be acquired from previous holders of that right, including privatization. An investor may acquire the “right to use” on a plot of building land from the party who was initially allocated the “right to use” for a sole use or may enter a joint venture with the original holder of the “right to use”.

In addition to the costs of acquiring the construction designated for deconstruction, as well as the costs of acquiring companies through privatization, an investor is obliged to pay the fee for the development of other construction land.

ConveRSion oF aGRiCultuRal lanD

A plot of agricultural land may be converted into construction land, with the consent of the Ministry of Agriculture and the payment of a fee for the change of the land use, if approved. The amount of the fee is as follows:

1. The land is converted for a definite period of time: the fee is paid annually, amounting to 10% of the market value of cultivable agricultural land;

2. The land is converted for an indefinite period of time: the fee is paid only once, amounting to 50% of the market value of cultivable agricultural land on the day of submitting the application; the fee must not exceed €1,500/ha, except for the land of the 1st and 2nd cadastral class.

For the change of the land use, an investor must submit a formal application, containing the following: a) information on the current and intended use of the land in question; b) a certificate of the title or the right of use; c) an Extract from the Detailed Urban Plan, detailing the possibility of obtaining a building permit, and d) the consent of the Ministry of Agriculture.

By acquiring privately owned agricultural land, with a possibility of the conversion into urban construction land, an investor also acquires the right to build structures on it. The fee amount is determined by local/city authorities.

18

GTC International in SerbiaMr. Robert SnowManaging Director, GTC Serbia

Why did you decide to start a business in Serbia?There are, of course, many reasons for entering a new market. Serbia presented both a challenge and an opportunity for GTC. Firstly, as it is an emerging market, one of the principle reasons is that we perceived a large gap in the real estate sector and a need for more offices, hotels, shopping malls, and quality mid-to-upper level residential buildings. Choosing to come here also reflected our confidence that Serbia is full of promise–everything exists here in terms of opportunity, resources, and skilled workers for the country to catch up to its more developed neighbors in a short time.

The world of business buildings is one which has a very long-term vision of the future. The needs of today are of critical importance, but those of tomorrow are paramount. GTC has seen in Belgrade a vision of a major European center of commerce, business, industry, and transport. Belgrade is in the very heart of the Balkans and at the epicenter of all movement throughout South East Europe. As the importance of Belgrade grows, so too will its requirements for office space and business parks.

What are your current and future projects in the country?GTC HOUSE is the first of GTC International’s investment in Serbia. The building–completed in April 2005–appeared as the long anticipated building, offering Class A office facilities for leasing to the leading international companies in Belgrade. The modern building is fully equipped with all high-tech facilities, sophisticated telecommunications, and elegant double height entrance lobby, leading into a covered central atrium.

Our new office project 19 Avenue consists of two 1st class office buildings with a unique design of 20,000 sq m. The 19 Avenue is completely equipped with high-tech telecommunication devices, offering not only exceptional

working environment, but also facilities such as a restaurant, bar, storage, and underground garage.

Other GTC International’s projects include GTC Square and Park Apartments. GTC Square is the newest innovative office project located in New Belgrade, with ample parking space, an open interior courtyard overarched by translucent catwalks, and an expansive and majestic atrium. Park Apartments is a top of the range residential building, introducing a new concept of living, with 200 apartments, 2-level underground parking, retail stores, fitness center, 24-hour reception desk, security services, maintenance services on the spot, and a video interphone.

How do you perceive the business climate in Serbia?This is a very exciting time to be doing business in Serbia. In the context of its

19

Cons

truc

tion

Proc

edur

etransition, Serbia has launched itself resolutely onto the path of joining the rest of Europe in terms of its economy and business. Foreign investment continues to come into Serbia from across the spectrum of industry sectors: banking, telecommunications, and, naturally, construction. Investors continue to view Serbia not only as an important investment destination in itself, but as a gateway to the region, as well. We at GTC are committed to open and transparent business practices, and have been very encouraged by the country’s efforts to align itself with the best practices for business development, as witnessed in the EU and neighboring countries.

In short, we are very optimistic about the business climate in Serbia and have already experienced many of the benefits of investing here.

aSSeSSment oF uRban ConDitionS

This assessment is done based on the Extract from the Urban Plan or the Act on Urban Conditions. These documents are issued by the city/municipal authorities in charge of urbanism, planning, and construction. In Belgrade, the Extract and other documents for structures with the area of up to 800 sq m can be obtained in the Department for Property Rights Relations and Construction of the city municipality where the structure is located. For structures of over 800 sq m, necessary documents can be obtained in the Secretariat for Urban Planning and Construction. In other cities and municipalities in Serbia, the documentation is obtained in the office of the city or municipality where the structure is erected. Lastly, for structures of national significance, the documents are issued by the Ministry of Infrastructure.

Prior to submitting the Application for Issuing the Extract from the Urban Plan or the Act on Urban Conditions, an investor must obtain the Evidence of Ownership (Leasehold Rights) or the Extract from the Land Books and the Conceptual Project. This Application should be accompanied by separate Applications for Granting Consent on the Prior Conditions for utilities (sewage, electricity, telephone, gas, remote heating, and bomb shelters construction).

ConStRuCtion appRoval

Prior to the construction of a structure, a potential investor is obliged to obtain a Construction Approval and prepare the technical documentation for the construction (General Project, Conceptual Project, Main Project, Execution Project, and As-Built Project).

As part of the application, the following should be submitted:• The Extract from the Urban Plan, not older than 6 months;• A Conceptual Project, in compliance with the Extract;• The evidence of ownership, or leasehold rights to the

construction land, or property rights in an object, or the right to use undeveloped construction land;

• The Report on Setting Out the Building Plot and the Regulation Protocol issued by the Republic Geodetic Authority, including the appropriate copy of the plot plan;

• Other evidence required in the Urban Plan.The approval for infrastructural works is issued by the

Ministry of Infrastructure, while the issuance of the

20

approval for other structures is the responsibility of the city or municipality. The approval is not obligatory for the construction of auxiliary structures, nor is it necessary for adaptation or renovation, but it is required for the reconstruction of premises.

lanD Development Fee payment anD main pRojeCt pRepaRation

Upon granting the Construction Approval to the investor, construction land development fees are determined by city/municipal authorities and public companies. In this project stage, the investor is obliged to prepare a Main Project, which has to undergo a revision before submitting to the competent institutions.

notiCe oF the StaRt oF ConStRuCtion

After the completion of building documents, the investor should select the contractor who will be responsible for the whole building site and notify the city or municipality of the start of works. The investor is obliged to provide the office in charge of issuing the Construction Approval with the name of the contractor, construction start date, and completion target date within a period of 8 days before the construction starts. Also, an investor must submit:

• a confirmed Main Project,• a report on Completed Technical Control,• a Construction Approval,• the evidence of payment of land development fees, and• the evidence that the administrative fee has been

paid. In addition, the investor must also report to the municipality office in charge of inspection that the construction of the structure has started.

The investor can start construction works when the relevant municipal department confirms the receipt of the Notification on the Commencement of Works.

ConStRuCtion

Prior to construction, the surveyor should set out the building site, after which he will be possible to commence excavations for the foundation. Upon the construction of the foundation, the contractor should submit the geodetic survey of a built-up foundation, so that the competent body can inspect its conformity with the Main Project. Within 3 days, if everything is in order, a written certificate will be received and the works can be continued.

Throughout the construction stage, the investor must have construction documents (if the Main Project does not contain details required for the construction process) and provide supervision.

oCCupanCy peRmit

A technical inspection of a structure is done upon the completion of construction, i.e. the completion of all the works specified in the Construction Approval and defined in the Main Project, or upon the completion of a part of the structure for which an Occupancy Permit may be issued. Upon the submission of the investor’s request for the technical inspection, this assessment may also be carried out simultaneously with the construction

21

A Construction ProcedureStage Steps Documents Institution

Construction Preparation

Act on Urban ConditionsExtract from Urban Plan

1. Evidence of Ownership (Leasehold Rights)2. Extract from Land Books3. Conceptual Project4. Consent on Prior Conditions for Utilities5. Extract from the Urban Plan6. Act on Zoning Conditions

1. Municipal Court2. Cadastre3. Project Consultancy4. Public Companies5. Urbanism and Construction Office6. Urbanism and Construction Office

Construction Approval 1. Construction Approval 1. Urbanism and Construction Office

Land Development Fee PaymentMain Project

1. Main Project2. Revised Main Project3. Decision on Land Development Fees4. Decision on Other Fees

1. Project Consultancy2. Project Consultancy3. Urbanism and Construction Office4. Public Companies

Notice of the Start of Construction 1. Confirmation of Main Project 1. Urbanism and Construction Office

Construction Construction 1. Certificate on Conformity of Built-Up Foundation with Main Project 1. Inspection Office

Occupancy PermitRegistration in Cadastre

Occupancy Permit1. Report on Technical Receipt of Structure2. Consent on Utility Hook-Ups3. Occupancy Permit

1. Technical Inspection Commission2. Public Companies3. Urbanism and Construction Office

Registration in Cadastre

1. Extract from Cadastre(Decision on Registration) 1. Cadastre

process, if the verification of the actual condition of certain parts of the structure is not possible after its completion.

The inspection includes the control of compatibility of as-built conditions with the Construction Approval and technical documentation on the basis of which the structure was constructed, as well as with the technical regulations and standards applicable to certain trades of materials, equipment, and installations. To ensure the suitability for the use of a structure, an assessment and verification of installations, devices, machinery, stability, or safety of structure, devices and equipment for environmental protection may take place. If envisaged by the technical documentation, the commission in charge of a technical inspection may propose to the relevant office to approve probation occupancy, provided the conditions are met. The probation period cannot last longer than 1 year. Upon the expiration of a probation period, the investor is obliged

to submit the results of the probation occupancy to the relevant office.

The structure may be put in operation only upon obtaining the Occupancy Permit, which is issued based on the technical inspection findings and appropriate consents for utilities (sewage, electricity, and telecomm hook-ups, fire-fighting and chimney-sweeping systems).

ReGiStRation in the CaDaStRe

The final stage in the construction process is the registration of a structure in the Real Estate Cadastre, after the Occupancy Permit is obtained.

The process of establishing the Real Estate Cadastre on the entire territory of Serbia is under way. By 2010, a comprehensive system of tracking real estate and real estate property rights will replace the existing records on real estate–the Land Cadastre and Land Books.

22

The Real Estate Cadastre contains the data on real estate, its shape and position, surface area, form of use, land fertility, cadastral income, real rights and rights holders, as well as the data on encumbrances and limitations.

Unlike the Real Estate Cadastre, the Land Cadastre contains no data on real estate property rights, featuring information on plots and structures built on land, with respect to their position, shape, area, type of land, land fertility, class, cadastral income, and users.

Lastly, the Land Book is a public record, registering real estate (land and structures), real rights, encumbrances, and limitations related to such real estate.

Once the unified Real Estate Cadastre is introduced, registration of real estate will be done in one place–with a local office of the Republic Geodetic Authority. Currently, the procedure is handled by a competent court.

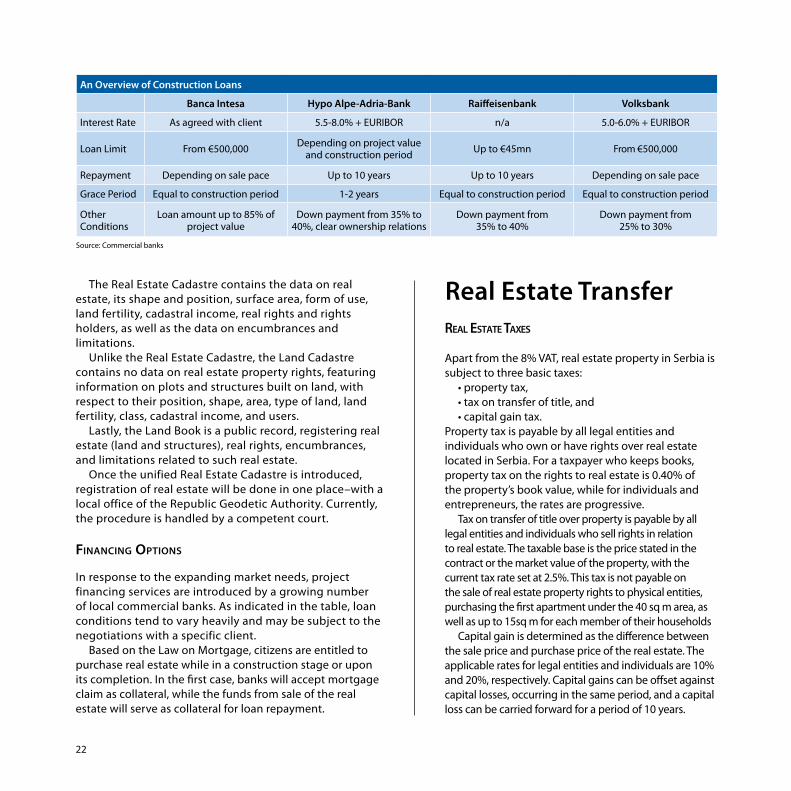

FinanCinG optionS

In response to the expanding market needs, project financing services are introduced by a growing number of local commercial banks. As indicated in the table, loan conditions tend to vary heavily and may be subject to the negotiations with a specific client.

Based on the Law on Mortgage, citizens are entitled to purchase real estate while in a construction stage or upon its completion. In the first case, banks will accept mortgage claim as collateral, while the funds from sale of the real estate will serve as collateral for loan repayment.

Real Estate Transfer

An Overview of Construction Loans

Banca Intesa Hypo Alpe-Adria-Bank Raiffeisenbank Volksbank

Interest Rate As agreed with client 5.5-8.0% + EURIBOR n/a 5.0-6.0% + EURIBOR

Loan Limit From €500,000 Depending on project value and construction period Up to €45mn From €500,000

Repayment Depending on sale pace Up to 10 years Up to 10 years Depending on sale pace

Grace Period Equal to construction period 1-2 years Equal to construction period Equal to construction period

OtherConditions

Loan amount up to 85% of project value

Down payment from 35% to 40%, clear ownership relations

Down payment from35% to 40%

Down payment from25% to 30%

Source: Commercial banks

Real eState taxeS

Apart from the 8% VAT, real estate property in Serbia is subject to three basic taxes:

• property tax,• tax on transfer of title, and• capital gain tax.

Property tax is payable by all legal entities and individuals who own or have rights over real estate located in Serbia. For a taxpayer who keeps books, property tax on the rights to real estate is 0.40% of the property’s book value, while for individuals and entrepreneurs, the rates are progressive.

Tax on transfer of title over property is payable by all legal entities and individuals who sell rights in relation to real estate. The taxable base is the price stated in the contract or the market value of the property, with the current tax rate set at 2.5%. This tax is not payable on the sale of real estate property rights to physical entities, purchasing the first apartment under the 40 sq m area, as well as up to 15sq m for each member of their households

Capital gain is determined as the difference between the sale price and purchase price of the real estate. The applicable rates for legal entities and individuals are 10% and 20%, respectively. Capital gains can be offset against capital losses, occurring in the same period, and a capital loss can be carried forward for a period of 10 years.

23

Related Contacts

State inStitutionS

Serbia Investmentand Export Promotion Agency3, Vlajkoviceva St. 11000 BelgradePhone: +381 11 3398 550Fax: +381 11 3398 [email protected]

Office of the Prime Minister11, Nemanjina St. 11000 BelgradePhone: +381 11 3617 719Fax: +381 11 3617 609 [email protected]

Business Registration Agency5, Nikole Pasica Sq. 11000 BelgradePhone: +381 11 3331 444Fax: +381 11 3331 [email protected]

National Bank of Serbia12, Kralja Petra St. 11000 BelgradePhone: +381 11 3027 194Fax: +381 11 3027 [email protected]

Statistical Office of the Republic of Serbia5, Milana Rakica St. 11000 BelgradePhone: +381 11 2412 922Fax: +381 11 2411 [email protected] www.stat.gov.rs

Republic Geodetic Authority39, Vojvode Misica Blvd. 11000 BelgradePhone: +381 11 2650 886Fax: +381 11 2651 [email protected]

Real eState pRoviDeRS

CB Richard EllisAirport City Belgrade,88b, Omladinskih brigada St. 11070 BelgradePhone: +381 11 2258 777Fax: +381 11 2281 [email protected]

Colliers International Serbia115D, Mihajla Pupina Blvd.11070 BelgradePhone: +381 11 3139 955Fax: +381 11 3139 [email protected]

EC Harris87, Zorana Djindjica Blvd. 11070 BelgradePhone: +381 11 2120 334Fax: +381 11 3132 [email protected]

EFG Property Services62-64, Cara Dusana St. 11000 Belgrade Phone: + 381 11 2022 413Fax: + 381 11 3287 [email protected]

Forton5, Zmaj Jovina St. 11000 BelgradePhone: +381 11 2635 432Fax: +381 11 30 37 50 [email protected]

King Sturge6, Mihajla Pupina Blvd. Usce Tower11070 BelgradePhone: +381 11 2200 101Fax: +381 11 2200 [email protected]

Mace6, Mihajla Pupina Blvd. Usce Tower11070 BelgradePhone: +381 11 2200 250Fax: +381 11 2200 [email protected]

SHM Smith Hodgkinson10v/I apt 503, Mihajla Pupina Blvd.11070 BelgradePhone: +381 11 3018 624Fax: +381 11 3149 [email protected]

Beobuild14a, Misarska St. 11224 Vrcin, BelgradePhone: +381 63 8212 [email protected]

24

To be able to set up or expand your business at a low cost and in the minimum amount of time, you can rely on the services offered by the country’s central investment institution–Serbia Investment and Export Promotion Agency (SIEPA).

We are proud to offer our reference list that includes some of the biggest multinational companies, namely FIAT, Coca-Cola, Ball Corporation, Grundfos, Knauf, and many others.

SIEPA puts a special focus on the real estate industry, reflecting the importance of its development to the Serbian economy by providing the following:

• Promotion of cities and developers at renowned international fairs;

• The database of investment locations in Serbia; • Regular surveys and detailed analyses of the sector; • Working with investors in finding the right location and

assisting in the legal processes; • Information on business service providers in the real

estate industry. Please join us at our national stands at Real Vienna and

other world’s leading fairs, where selected Serbian cities and developers are exhibiting and offering their ready-to-invest locations and projects.

Thus, we would like to invite you to contact our specialized staff ready to assist you and your business interests. Working with us is simple, effective and free of charge.

Serbia Investment andExport Promotion Agency

Vlajkoviceva 311000 Belgrade

phone: +381 11 3398 550fax: +381 11 3398 814

[email protected] Real Estate Industry in Serbia