Embed Size (px)

Citation preview

Raymond James 20th Equity ConferenceOctober 10, 2012

Continental ResourcesInvestor Relations Update

November 28, 2012

Forward-Looking Information

2

Cautionary Statement for the Purpose of the "Safe Harbor" Provisions of the Private Securities Litigation Reform Act of 1995:

This press release includes "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities

Exchange Act of 1934. All statements included in this press release other than statements of historical fact, including, but not limited to, statements or

information concerning the Company's future operations, performance, financial condition, production and reserves, schedules, plans, timing of

development, returns, budgets, costs, business strategy, objectives, and cash flow, are forward-looking statements. When used in this press release, the

words "could," "may," "believe," "anticipate," "intend," "estimate," "expect," "project," "budget," "plan," "continue," "potential," "guidance," "strategy,"

and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words.

Forward-looking statements are based on the Company's current expectations and assumptions about future events and currently available information

as to the outcome and timing of future events. Although the Company believes that the expectations reflected in the forward-looking statements are

reasonable and based on reasonable assumptions, no assurance can be given that such expectations will be correct or achieved or that the assumptions

are accurate. When considering forward-looking statements, readers should keep in mind the risk factors and other cautionary statements described

under Part I, Item 1A. Risk Factors included in the Company's Annual Report on Form 10-K for the year ended December 31, 2011, registration statements

and other reports filed from time to time with the Securities and Exchange Commission (SEC), and other announcements the Company makes from time

to time.

The Company cautions readers that these forward-looking statements are subject to all of the risks and uncertainties, most of which are difficult to predict

and many of which are beyond the Company's control, incident to the exploration for, and development, production, and sale of, crude oil and natural

gas. These risks include, but are not limited to, commodity price volatility, inflation, lack of availability of drilling and production equipment and services,

environmental risks, drilling and other operating risks, regulatory changes, the uncertainty inherent in estimating crude oil and natural gas reserves and in

projecting future rates of production, cash flows and access to capital, the timing of development expenditures, and the other risks described under Part I,

Item 1A. Risk Factors in the Company's Annual Report on Form 10-K for the year ended December 31, 2011, registration statements and other reports

filed from time to time with the SEC, and other announcements the Company makes from time to time.

Readers are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date hereof. Should one or more of the risks

or uncertainties described in this press release occur, or should underlying assumptions prove incorrect, the Company's actual results and plans could

differ materially from those expressed in any forward-looking statements. All forward-looking statements are expressly qualified in their entirety by this

cautionary statement. This cautionary statement should also be considered in connection with any subsequent written or oral forward-looking statements

that the Company, or persons acting on its behalf, may make.

Except as otherwise required by applicable law, the Company disclaims any duty to update any forward-looking statements to reflect events or

circumstances after the date of this press release.

Continental Resources, Inc.

#1 oil producer in Williston Basin

610 MMBoe* proved reserves at MY2012 – 20% growth

Strong 3Q 2012 results� Record production of 105,874 Boepd in September 2012

� Averaged 102,964 Boepd in 3Q – 55% increase over 3Q 2011

� $492.3 MM EBITDAX for 3Q 2012 – 46% increase from 3Q 2011

� $1,368.7 MM EBITDAX for YTD 9/30/12; +53% YOY**

� $1.2 billion of new 5% senior unsecured notes (yield 4.624%)

On track for 57-59% production growth in 2012 (YOY)

3

*CLR estimate of proved reserves at MY2012.

**See reconciliation of EBITDAX to GAAP net income in the Appendix at the end of this presentation.

Strong EBITDAX and Cash Margins

4

EBITDAX ($MM) Cash Margins

$451

$811

$1,304$1,369

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

2009 2010 2011 YTD 9/30/12

69%

73%

75%

73%

66%

67%

68%

69%

70%

71%

72%

73%

74%

75%

76%

2009 2010 2011 YTD 9/30/12

1 See reconciliation of EBITDAX to net income in the Appendix at the end of this presentation.

Bakken: King of Tight Oil Fields

5

Continuous oil field of unprecedented magnitude• 15,000 sq. miles, 87% proven productive

• 24 BBoe technically recoverable (Oct. 2010)

Field continues to grow• Deeper intervals

• Down-spacing

True oil play• Premium crude, refiner’s crude of choice

CLR: King of the Bakken & #1 Oil Producer

6

#1 Bakken producer, driller and leasehold owner• 13% production • 10% rigs• 10% acreage

Net unrisked potential (MB + TF1 only)• 1.5 BBoe• 3,988 locations

Assets continue to grow:• Vertically• Geographically• Strategically

As of 20102011-2012 producer

As of 2012

MB + TF1: Early Stages of Full Development

13,000 sq. miles under development

202 rigs operating• CLR: 19 operated rigs

Less than 1 well per 1280-acre unit on average

4-to-8 wells per zone for full development

Bakken producer Three Forks producer

Full Development Mode

Ongoing Expansion

120 Miles

7

No

rth

Da

ko

ta

Mo

nta

na

25 Miles

Exploring While Developing

8

Lower TF increases OOIP 57%

903 BBo in place (2012)• 32 BBo recoverable @ 3.5%

• 36 BBo @ 4%

• 45 BBo @ 5%

577 BBo in place (2010)• 24 BBoe recoverable

• 20 BBo (3.5% recovery factor)

• 320-acre spacing per zone

Gamma Ray Resistivity

BA

KK

EN

TH

RE

E F

OR

KS

Nisku

Lodgepole

Upper

Lower

Middle

MBKKN

BA

KK

EN

PE

TR

OLE

UM

SY

ST

EM

1

2

4

3

2010

308’

2012

No

rth

Dak

ota

Mo

nta

na

CLR: Three Forks Pioneer

9

25 Miles

160-acre development

Sunline 11-1TF1,023 Boepd IP

320-acre development

320-acre development

TF2, TF3

TF2, TF3, TF4

TF2, TF3, TF4

CLR Core Location

Charlotte 2-22H (TF2)1,396 Boepd IP

Charlotte 3-22H1st test of 3rd bench

Three Forks Isopach Map

Drilled 25% of all TF wells

Proved separation of MB + TF1

10-well coring program – oil shows in TF2, TF3 + TF4

Completed first TF2 producer

First TF3 test being completed

Capital for 2013• TF accelerated de-risking - $70MM

• 320 acre spacing pilot - $161MM

• 160 acre spacing pilot - $36MM

Type curve• 10,000’ lateral / 30 stages• 603 MBoe EUR• Completed well costs (CWC)

• Single well ($9.2MM)

• ECO-Pad well ($8.5MM)

• 82.5% NRI

0

3

6

9

12

15

18

21

0

100

200

300

400

500

600

700

0 100 200 300 400 500

Monthly

Oil

Equiv

(MBoe)

Cum

Oil

Equiv

(MBOE)

Months

Bakken Type Curve

Cum Oil Equiv (MBoe) Oil Equiv (MBoe)

Current Target

Single Well Economics

10

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

1 11 21 31 41 51 61 71 81 91 101 111 121 131 141 151 161 171 181 191 201

Foo

tage

Dril

led

Days

35% Reduction

Florida Alpha ECO-Pad: 6-well pad

129,321’ drilled in 128 days$21.8MM spud to rig

release cost

6 single wells201 days$29.3MM spud to rig release cost

$7.5MM Drilling Savings with Pad Drilling

Glimpse of the Future

11

Bakken Premium Light Sweet Crude vs. Other Benchmarks Improved Refinery Yield

12

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

0

5

10

15

20

25

30

35

40

45

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Light Ends

Gasoline

Jet Fuel

Distillate

Resid

Crude Quality: API Gravity & Sulfur Distillation Cuts

●API° ●Sulfur % wt

Williston Basin Evacuation Capacity

13

Pro

duct

ion

volu

me

(MM

Bop

d)

0.0

3.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

TransCanada East (42") Enbridge Sandpiper (24")

OneOk Bakken Express (24") TransCanada Keystone XL

SB - High Prairie (16") Western Fuels - NewTown

Enbridge - Berthold Plains - Ross

Hess - Tioga Savage - Trenton

Rangeland - Epping Musket - Dore

Various - Dickinson BOE - Dickinson

UET - Van Hook UET - Beulah

Various - Stampede EOG - Stanley

Pony Express (24") Enbridge BPEP

Plains - Bakken North Butte

Enbridge ND Tesoro Refinery

200 Rig Growth 250 Rig Growth

Bentek Forecast

Rail0.9 MMBopd

CommittedPipeline0.9 MMBopd

ProposedPipeline1.3 MMBopd

(CLR) (CLR)

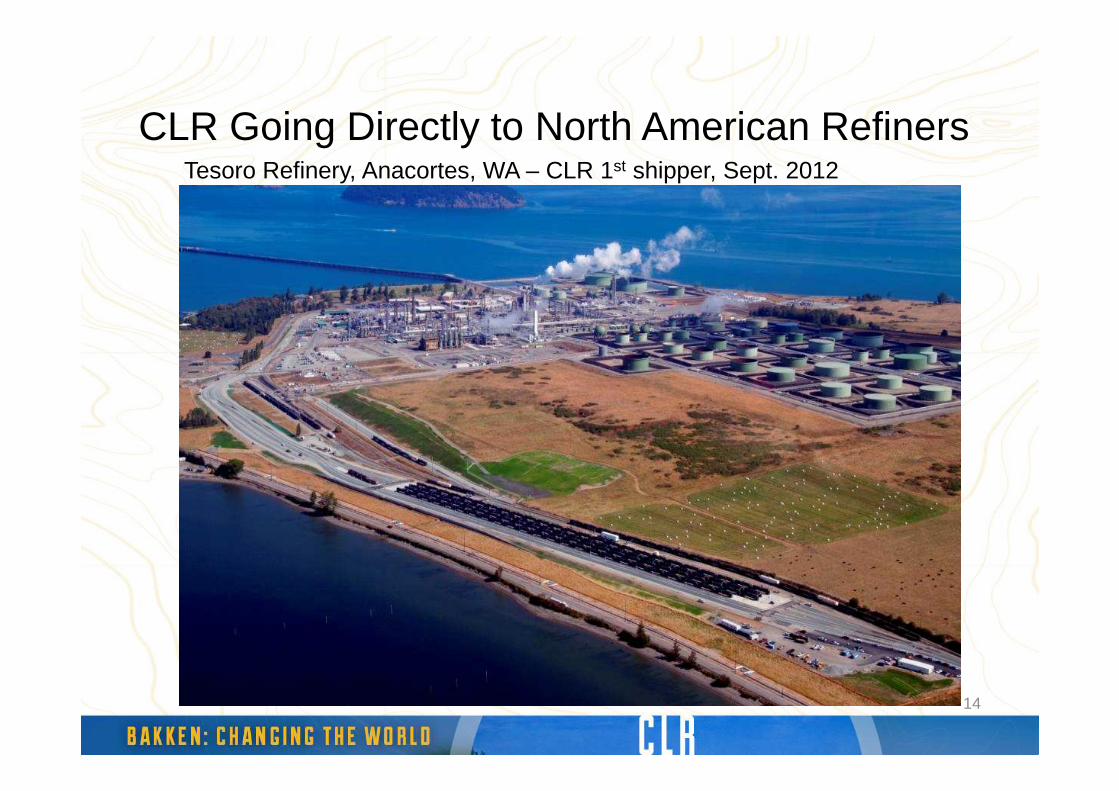

CLR Going Directly to North American Refiners

14

Tesoro Refinery, Anacortes, WA – CLR 1st shipper, Sept. 2012

What’s the “SCOOP”?

15

3 of the top oil-producing counties in Oklahoma

3.2 BBo produced

60 reservoirs

Epicenter of Oklahoma Oil

South Central Oklahoma Oil Province

“SCOOP”

Golden Trend (1945)590 MMBo

Sho-Vel-Tum (1905)1,433 MMBoHealdton (1913)

363 MMBo

Knox97 MMBo

“SCOOP”

SCOOP: A New, High-Impact Resource Play

Thick, high-quality resource shale reservoir

1.8 BBoe net reserve potential to CLR*• 2,200 net locations*

• 25-50% oil, 60-75% total liquids

40-55% ROR**

Commanding leasehold position with 197,340 net acres as of 9/30/2012

16*Based on 80-acre spacing ** $3.50 gas/$90 oil

Here’s the “SCOOP”

17

World-class resource shale• Up to 400’ of oil-rich shale

• Dual reservoir target

Excellent siliceous reservoir • Highly fractured

Source of the oil“SCOOP”

Cana Field

The Woodford Shale70 BBo remains in-situ

“SCOOP”

Okl

ahom

a

Texas

Woodford Shale

Thickness

>300 ft

100 ft

200 ft

25 Miles

Tex

as

Oklahoma

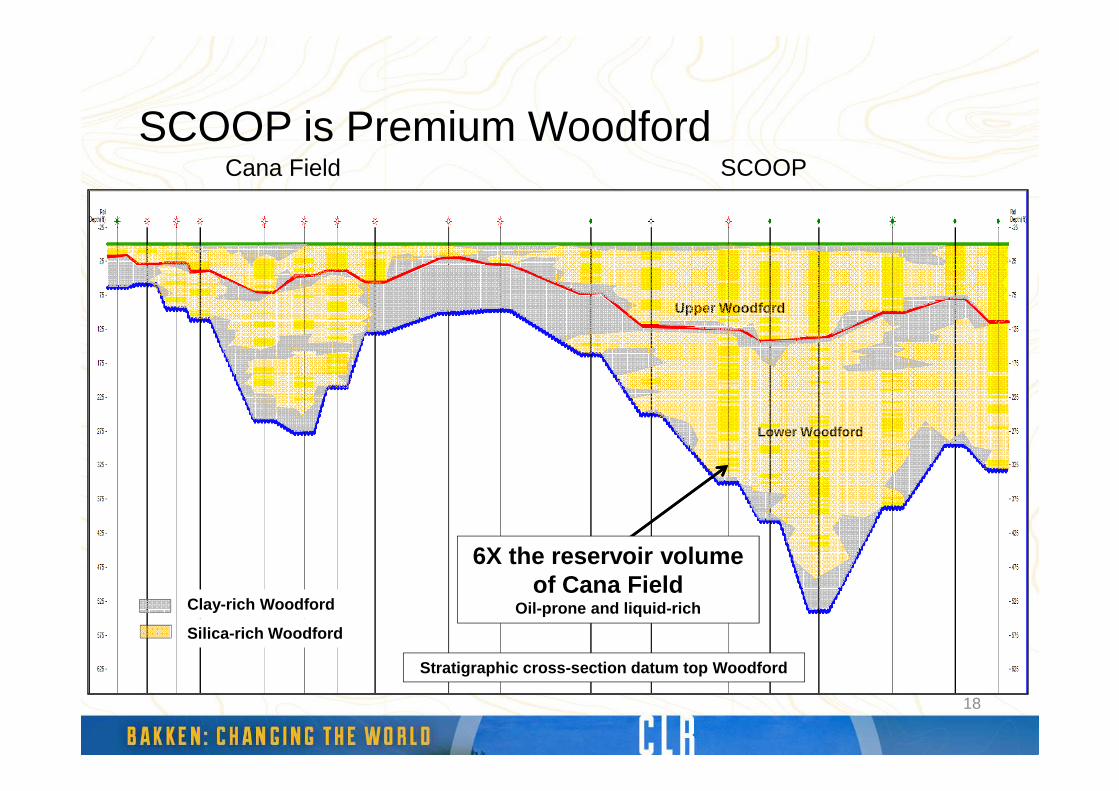

SCOOP is Premium Woodford

18

Cana Field SCOOP

Clay-rich Woodford

Silica-rich Woodford

Upper Woodford

Lower Woodford

6X the reservoir volume of Cana Field

Oil-prone and liquid-rich

Stratigraphic cross-section datum top Woodford

SCOOP: Why Stealth?

19

94,000 acres at YE 2010 (3% HBP)

197,340 acres as of 9/30/12 (20% HBP)

We’ve Been Leasing!

12 Miles

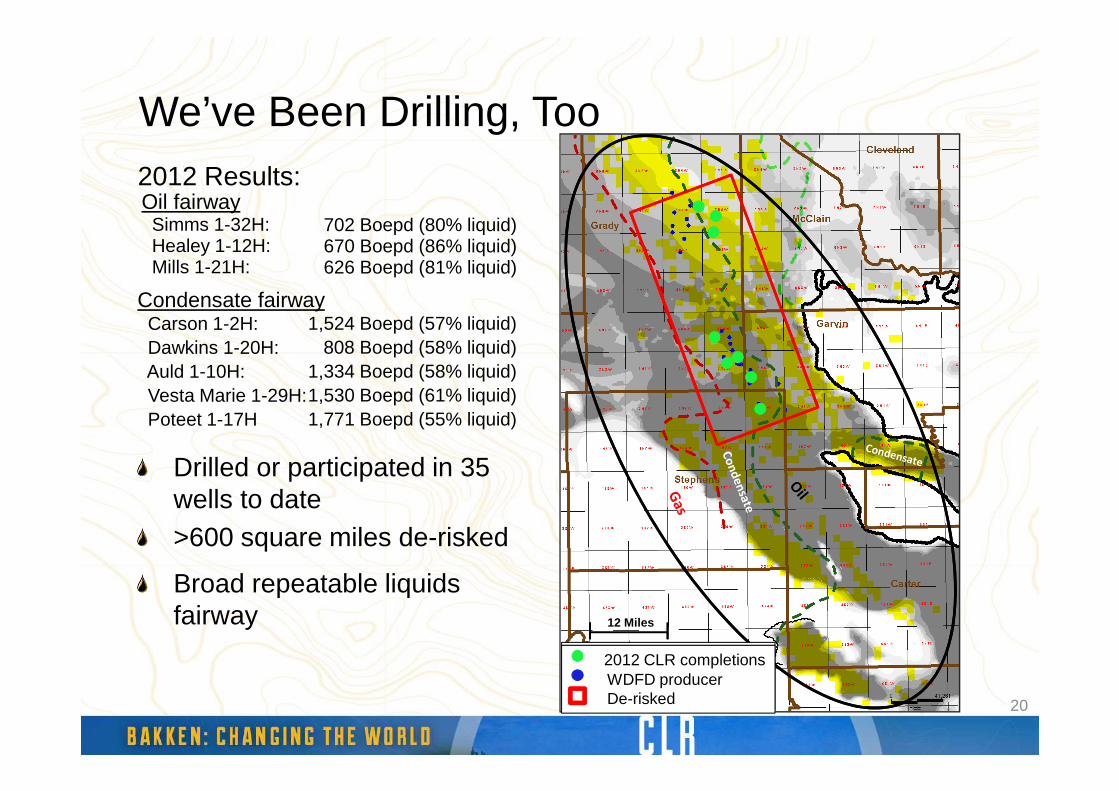

We’ve Been Drilling, Too

20

Drilled or participated in 35 wells to date

2012 Results:Oil fairwaySimms 1-32H: Healey 1-12H: Mills 1-21H:

702 Boepd (80% liquid)670 Boepd (86% liquid)626 Boepd (81% liquid)

Condensate fairwayCarson 1-2H:Dawkins 1-20H:Auld 1-10H:Vesta Marie 1-29H:Poteet 1-17H

1,524 Boepd (57% liquid)808 Boepd (58% liquid)

1,334 Boepd (58% liquid)1,530 Boepd (61% liquid)1,771 Boepd (55% liquid)

Broad repeatable liquids fairway

2012 CLR completionsWDFD producer

>600 square miles de-risked

2012 CLR completionsWDFD producerDe-risked

12 Miles

Oil $9.0 MMOil $8.5 MMCondensate $9.5 MMCondensate $9.0 MM

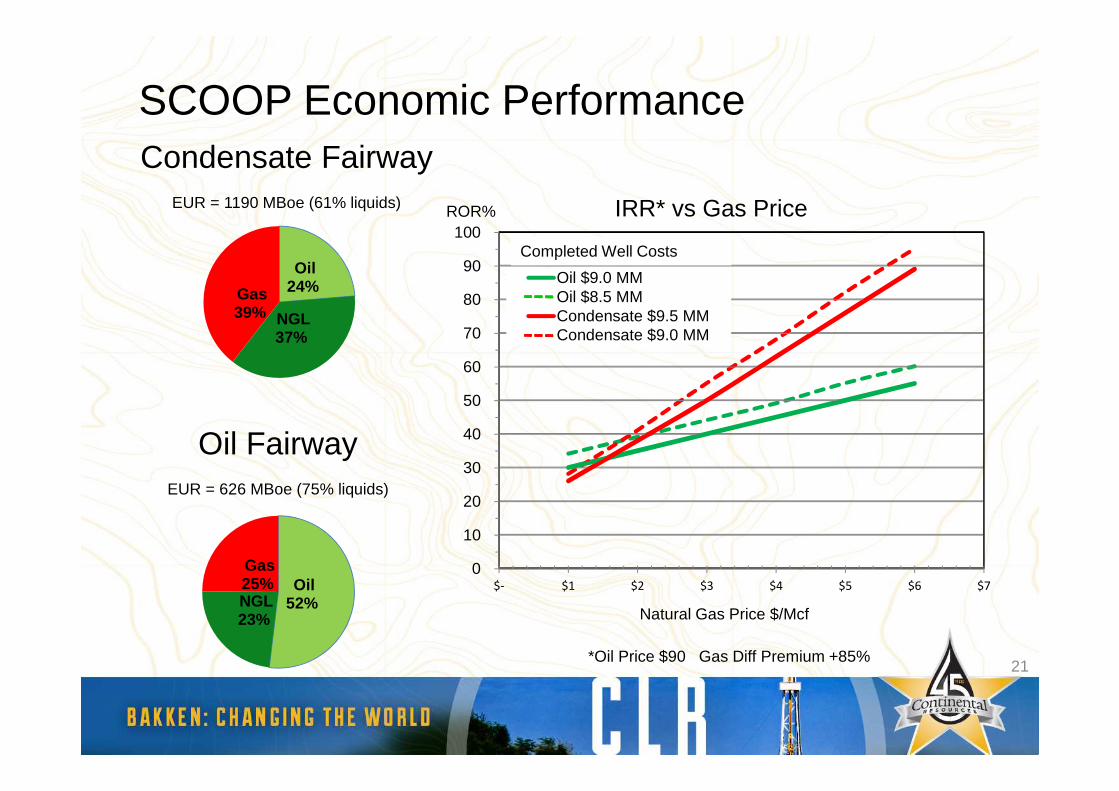

SCOOP Economic Performance

21

Oil24%

NGL37%

Gas39%

Condensate FairwayEUR = 1190 MBoe (61% liquids)

Oil52%NGL

23%

Gas25%

Oil FairwayEUR = 626 MBoe (75% liquids)

0

10

20

30

40

50

60

70

80

90

100

$- $1 $2 $3 $4 $5 $6 $7

IRR* vs Gas Price

Oil $9.0 MMOil $8.5 MMCondensate $9.5 MMCondensate $9.0 MM

Natural Gas Price $/Mcf

*Oil Price $90 Gas Diff Premium +85%

ROR%

Completed Well Costs

Realizing CLR’s Growth Potential

22

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

320 BK/TF-160WDFD Spacing

160 BK/TF-80WDFD Spacing

Other

NW Cana

SCOOP

TF3/TF4

TF2

Bakken/TF1

Unbooked Net Resource Potential(MMBoe)

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

320 BK/TF- 160WDFD Spacing

160 BK/TF-80WDFD Spacing

Other

NW Cana

SCOOP

TF3/TF4

TF2

Bakken/TF1

Unrisked Potential Net Wells(Net Wells)

Continental estimated proved reserves MY2012: 610 MMBoe

7,000

4,1008,850

16,950

* Calculations exclude non-prospective acreage.

5-Year Target: Another Triple!

23

0

30

60

90

120

2012* 2013** 2014 2015 2016 2017

48

108+

36

0

500

1000

1500

2000

2011 MY2012 2013 2014 2015 2016 2017

508

1,524

*Midpoint of 57%-to-59% guidance range.**Midpoint of 30% to 35% guidance range.

Production Proved Reserves

610*

97MBoepd

300MBoepd

*CLR Estimate

MMBoe MMBoe

Drilling Capital Allocation ($2.9B)

2013 Capital Expenditures Budget

Total Capital Expenditures ($3.4B)

Exploratory Drilling $430MM

Other$460MM

Development Drilling $2,510MM

Exploratory 15%

Other Development

4%

SCOOP15%

Average operated rigsGross wellsNet wells

201233

847286

201335

738300

24

Bakken 66%

25

$11.3 $2.1

$9.2

$0.4 $0.3 $0.3

$8.2

0

2

4

6

8

10

12

OSO AverageWell Cost (1H 12)

CLR CostEfficiencies

ISO Average WellCost (1H 12)

CompletionEfficiencies

DrillingEfficiencies

Multi-Well Pads Targeted ISOAverage Well Cost

(YE 2013)

$ Million

Low-Cost Bakken Operator$ Million

$9.5

Historical Target

18%Increase

8%Increase

*

*Weighted average well cost, pads and single wells.

2012 2013

OSO Average

Well Cost

(1H 2012)

ISO Average

Well Cost

(1H 2012)

Summary: CLR’s Clear Vision of Growth

Expand and de-risk plays while developing premier oily assets

Operating excellence and continued cost efficiency

Assure transportation/infrastructure gets built as we grow

Implement marketing strategy to reach premier markets

Bring value forward by• Accelerating growth• Managing the margins• Mitigating business risks

Maintain strong balance sheet and financial flexibility26

Appendix

27

2013 Operational and Financial Guidance

28

2013 Production growth range 30% to 35%

Capital expenditures* $3.4B

Price differentials:

WTI crude oil (per barrel of oil) $8 to $11

Henry Hub natural gas (per Mcf) +$1.00 to $1.50

Operating expenses:

Production expense per Boe $5.50 to $5.90

Production tax as a percent

of oil and gas revenues** 8% to 9%

DD&A per Boe $19 to $21

G&A expense per Boe*** $2.40 to $2.90

Non-cash equity compensation per Boe $0.70 to $0.90

Income tax rate 38%

Deferred taxes 90% to 95%

* Excludes acquisition capital expenditures

**Does not include other expenses, such as natural gas transportation fees, which could represent another 1%.

***Excludes non-cash equity compensation

Swaps and Collars As of 10/26/12

29

Crude Oil Derivative Positions SwapsBbls Wtd. Avg. Price Floor Ceiling

Swaps - WTI 1,840,000 $88.69Swaps - Brent 1,058,000 $111.17Collars - WTI 1,340,440 $80.00 $94.71

Swaps - WTI 11,862,500 $92.66Swaps - Brent 2,372,500 $109.19Collars - WTI 8,760,000 $86.92 $99.46

Swaps - WTI 10,311,250 $96.20Swaps - Brent 4,745,000 $100.43Collars - Brent 1,460,000 $90.00 $107.50

Swaps - Brent 1,277,500 $98.48

SwapsMMBtus Wtd. Avg. Price

Swaps - Henry Hub 18,250,000 $3.76

January 2014 - December 2014

Natural Gas Derivative PositionsPeriod and Type of Contract

January 2013 - December 2013

Collars Wtd. Avg. PricePeriod and Type of Contract

October 2012 - December 2012

January 2013 - December 2013

January 2015 - December 2015

Capital Efficiency

30

1 Recycle ratio is calculated as the 3-yr average profit per BOE divided by the 3-yr average F&D cost per BOE

2 Peers include APC, CHK, CXO, DNR, DVN, PXP, SD and WLL.

Source: KeyBanc

$0

$1

$2

$3

$4

$5

$6

CLR Peer 1 Peer 2 Peer 3 Peer 4 Peer 5 Peer 6 Peer 7 Peer 8

5.0x

3.2x

2.7x2.3x

2.1x1.8x 1.7x

1.2x 1.1x

Recycle Ratio – Industry Leader(1)(2)

EBITDAX Reconciliation to GAAP

31

We use a variety of financial and operational measures to asses our performance. Among these measures is EBITDAX. EBITDAX represents earnings (net income) before interest expense,

income taxes, depreciation, depletion, amortization and accretion, property impairments, exploration expenses, non-cash gains and losses resulting from the requirements of accounting for

derivatives, and non-cash equity compensation expense. EBITDAX is not a measure of net income or operating cash flows as determined by GAAP. Management believes EBITDAX is useful

because it allows us to more effectively evaluate our operating performance and compare the results of our operations from period to period without regard to our financing methods or

capital structure. We exclude the items listed above from net income in arriving at EBITDAX because those amounts can vary substantially from company to company within our industry

depending upon accounting methods and book values of assets, capital structures and the method by which the assets were acquired. EBITDAX should not be considered as an alternative to,

or more meaningful than, net income or operating cash flows as determined in accordance with GAAP or as an indicator of a company’s operating performance or liquidity. Certain items

excluded from EBITDAX are significant components in understanding and assessing a company’s financial performance, such as a company’s cost of capital and tax structure, as well as the

historic costs of depreciable assets, none of which are components of EBITDAX. Our computations of EBITDAX may not be comparable to other similarly titled measures of other companies.

We believe that EBITDAX is a widely followed measure of operating performance and may also be used by investors to measure our ability to meet future debt service requirements, if any.

Our revolving credit facility requires that we maintain a total funded debt to EBITDAX ratio of no greater than 4.0 to 1.0 on a rolling four-quarter basis. This ratio represents the sum of

outstanding borrowings and letters of credit under our revolving credit facility plus our note payable and senior note obligations, divided by total EBITDAX for the most recent four quarters.

We were in compliance with this covenant for all periods presented. The following table represents a reconciliation of our net income to EBITDAX for the periods presented:

Year Ended December 31,Three

Months Ended

YTD

2009 2010 2011 9/30/12 9/30/12in thousands

Net income $ 71,338 $ 168,255 $ 429,072 $ 44,096 $ 518,874 Interest expense 23,232 53,147 76,722 39,205 95,174Provision for income taxes 38,670 90,212 258,373 22,931 315,819Depreciation, depletion, amortization and accretion 207,602 243,601 390,899 189,374 499,847Property impairments 83,694 64,951 108,458 27,375 93,153Exploration expenses 12,615 12,763 27,920 4,899 17,752Impact from derivative instruments:

Total (gain) loss on derivatives, net 1,520 130,762 30,049 158,294 (144,377)

Total realized (cash flow) gain (loss) on derivatives, net 569 35,495 (34,106) (1,394) (48,375)

Non-cash (gain) loss on derivatives, net 2,089 166,257 (4,057) 156,900 (192,752)Non-cash equity compensation 11,408 11,691 16,572 7,499 20,804EBITDAX $ 450,648 $ 810,877 $ 1,303,959 $ 492,279 $ 1,368,671

CLR: 4.5 BBoe Bakken Resource Potential

32

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

320 BK/TFSpacing

160 BK/TFSpacing

TF3/TF4

TF2

Bakken/TF1

Unbooked Net Resource Potential

(MMBoe)

2,836

4,472

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

320 BK/TFSpacing

160 BK/TFSpacing

TF3/TF4

TF2

Bakken/TF1

Unrisked Potential Net Wells

(Net Wells)

6,718

13,285

CLR Bakken estimated proved reserves MY2012: 380 MMBoe(calculations exclude non-prospective acreage)

Decreasing Stimulation Costs per Stage

$0

$20

$40

$60

$80

$100

$120

$140

33

$114$124

$111 $108$98

$ ThousandsPer Stage

*Costs include pumping services, wireline, water, packers and plugs.

SCOOP: 1.8 BBoe Woodford Resource Potential

34

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

160 WoodfordSpacing

80 WoodfordSpacing

SCOOP

Net Unbooked Resource Potential

(MMBoe)

839

1,800

-

500

1,000

1,500

2,000

2,500

160 WoodfordSpacing

80 WoodfordSpacing

SCOOP

Unbooked Unrisked Potential Net Wells

(Net Wells)

1,114

2,242

SCOOP Type Curves

1350 BTU gas35

Condensate Fairway Type CurveEUR: 1190 MBoe (61% liquids)

Oil Fairway Type CurveEUR: 626 MBoe (75% liquids)

10

100

1000

10000

0 6 12 18 24 30 36 42 48

BO

PD

, MC

FD

Months

Gas Oil

10

100

1000

10000

0 6 12 18 24 30 36 42 48

BO

PD

, MC

FD

Months

Gas Oil