Embed Size (px)

Citation preview

February 2, 2017

Fourth quarter 2016 earnings call

Forward-looking statements

This presentation, as well as other statements made by Delphi Automotive PLC (the “Company”), contain

forward-looking statements that reflect, when made, the Company’s current views with respect to current

events, certain investments and acquisitions and financial performance. Such forward-looking statements are

subject to many risks, uncertainties and factors relating to the Company’s operations and business environment,

which may cause the actual results of the Company to be materially different from any future results. All

statements that address future operating, financial or business performance or the Company’s strategies or

expectations are forward-looking statements. Factors that could cause actual results to differ materially from

these forward-looking statements are discussed under the captions “Risk Factors” and “Management’s

Discussion and Analysis of Financial Condition and Results of Operations” in the Company’s filings with the

Securities and Exchange Commission. New risks and uncertainties arise from time to time, and it is impossible

for us to predict these events or how they may affect the Company. It should be remembered that the price of

the ordinary shares and any income from them can go down as well as up. The Company disclaims any

intention or obligation to update or revise any forward-looking statements, whether as a result of new

information, future events and/or otherwise, except as may be required by law.

2

Agenda

3

Operations overview

• Q4 2016 summary

• Strategic update

Financial overview

• Q4 2016 results

• 2017 guidance

Q&A

Kevin Clark Chief Executive Officer

Joe Massaro Chief Financial Officer

Kevin Clark / Joe Massaro

Operations overview

Kevin Clark President and Chief Executive Officer

Q4 and 2016 highlights

Well positioned for 2017

5 Note: Revenue growth excludes impact of FX, commodities, the E&S divestitures and HellermannTyton acquisition;

EPS and operating income adjusted for restructuring and other special items; see Appendix for detail and reconciliation to US GAAP

$4.3B Q4 Up 10%

$16.7B 2016 Up 8%

$0.6B Q4 Up 20%

$2.2B 2016 Up 13%

$1.83 Q4 Up 32%

$6.28 2016 Up 20%

• Advanced technologies drive higher growth across the portfolio

• New business bookings of $26B for the year driven by large conquest wins

• Confident in 2017 outlook – strong growth in sales, earnings and cash flow

Operating income Earnings per share Revenue growth

CES highlights

Showcased industry-leading innovation and expertise

6

Over 1,800 customers from over 60 companies

3,000 total

visitors including

8 VIP events

8 demo vehicles:

4 Automated

2 V2X

2 48V

over 230 drives

150 pavilion tours

“The best

automated drive

we’ve ever

experienced.” – Automotive News

“If CES gave an award

for the best in show,

Delphi would win it.”

– Major US OEM Customer

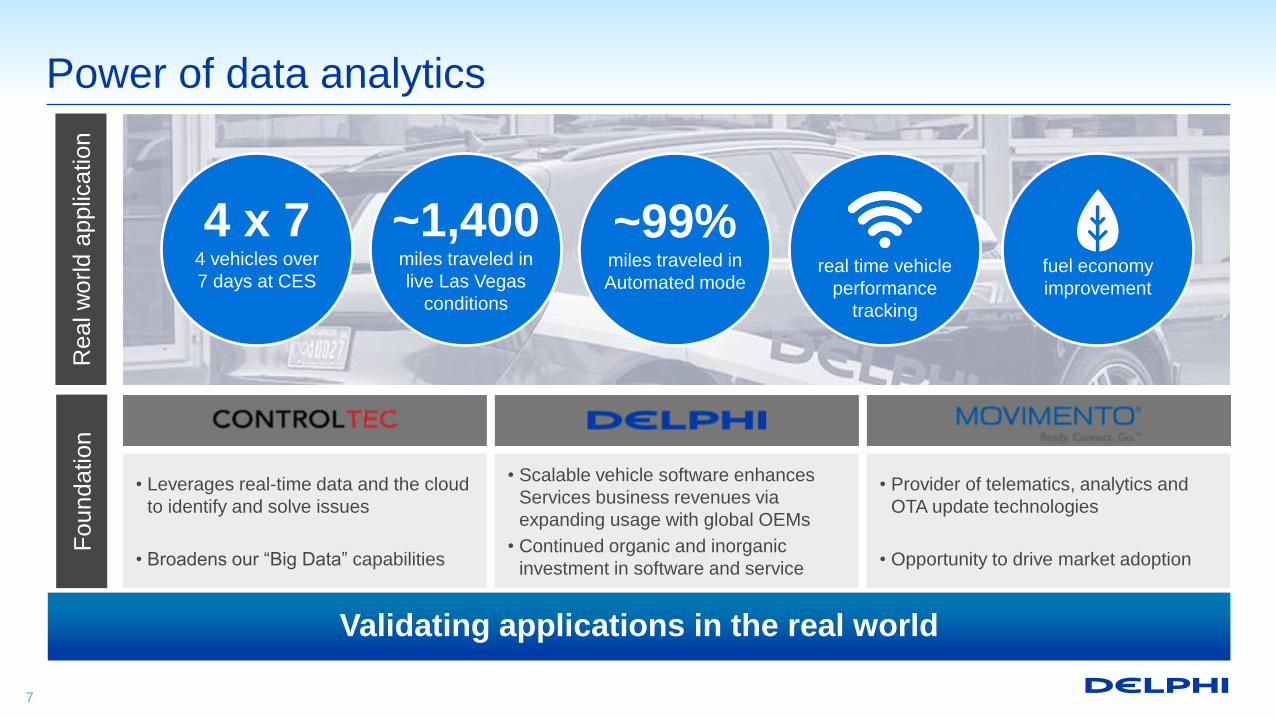

• Scalable vehicle software enhances

Services business revenues via

expanding usage with global OEMs

• Continued organic and inorganic

investment in software and service

Power of data analytics

Validating applications in the real world

7

• Provider of telematics, analytics and

OTA update technologies

• Opportunity to drive market adoption

• Leverages real-time data and the cloud

to identify and solve issues

• Broadens our “Big Data” capabilities

Foundation

Real w

orld a

pplic

ation

~99% miles traveled in

Automated mode

~1,400 miles traveled in

live Las Vegas

conditions

fuel economy

improvement

4 x 7 4 vehicles over

7 days at CES real time vehicle

performance

tracking

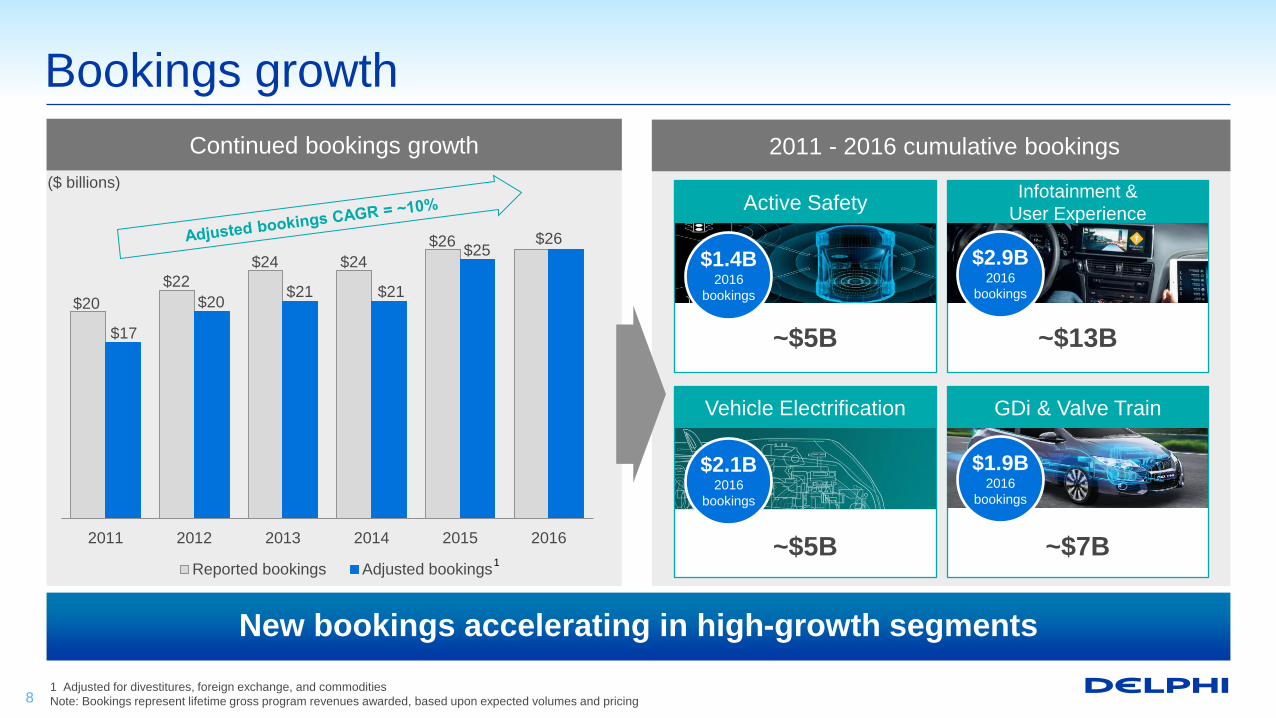

$20

$22

$24 $24

$26

$17

$20 $21 $21

$25 $26

2011 2012 2013 2014 2015 2016

Reported bookings Adjusted bookings1

Bookings growth

New bookings accelerating in high-growth segments

2011 - 2016 cumulative bookings Continued bookings growth

($ billions)

GDi & Valve Train

Infotainment &

User Experience

Vehicle Electrification

Active Safety

8

~$5B ~$13B

~$7B ~$5B

$1.4B 2016

bookings

$2.9B 2016

bookings

$2.1B 2016

bookings

$1.9B 2016

bookings

1 Adjusted for divestitures, foreign exchange, and commodities

Note: Bookings represent lifetime gross program revenues awarded, based upon expected volumes and pricing

Select fourth quarter bookings

Strong wins in every business

9

E&S Powertrain E/EA

DEEDS Infotainment GDi

>$1B

lifetime

revenue

>$1B

lifetime

revenue

>$0.5B

lifetime

revenue

North American

OEM

Delivering technology innovation

Innovation creates value through best-in-class technologies

10

Leader in centralized computing platforms

• Scalable domain integration

• More efficient architectures

• Automated driving and cockpit

• First to market

Industry-leading autonomous capabilities

• CSLP platform partnership with MBLY

• Commercialization on track for 2019

• Unprecedented interest following CES

• First to market

Intelligent electrification 48V solutions

• Builds on HV E/EA competency

• Integration with full Delphi product suite

• Better functionality, performance, efficiency

• Uniquely positioned

Autonomous capabilities Intelligent electrification Centralized computing

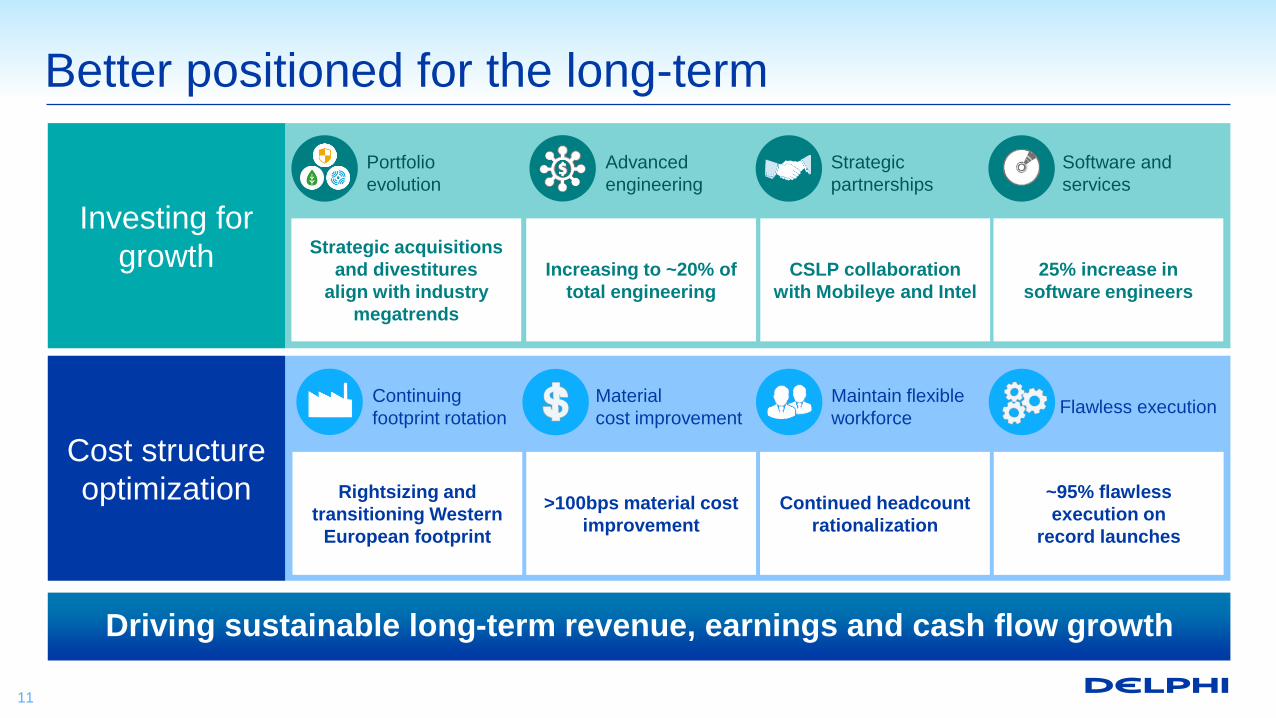

Better positioned for the long-term

Driving sustainable long-term revenue, earnings and cash flow growth

11

Continuing

footprint rotation

Rightsizing and

transitioning Western

European footprint

Cost structure

optimization

Investing for

growth

>100bps material cost

improvement

Continued headcount

rationalization

~95% flawless

execution on

record launches

Material

cost improvement

Maintain flexible

workforce Flawless execution

Strategic acquisitions

and divestitures

align with industry

megatrends

25% increase in

software engineers

Portfolio

evolution

Strategic

partnerships

Software and

services

CSLP collaboration

with Mobileye and Intel

Advanced

engineering

Increasing to ~20% of

total engineering

Financial overview

Joe Massaro Chief Financial Officer and Senior Vice President

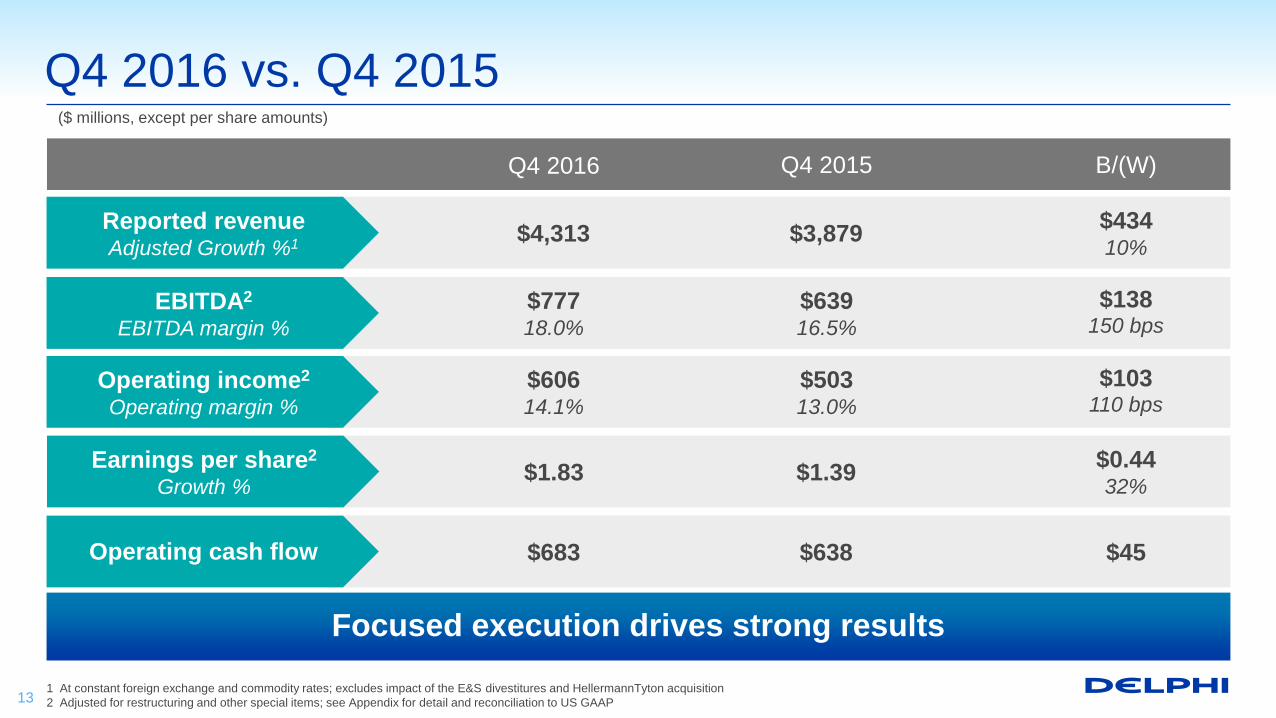

Q4 2016 vs. Q4 2015 ($ millions, except per share amounts)

13

Focused execution drives strong results

Reported revenue Adjusted Growth %1

Earnings per share2

Growth %

Operating cash flow

Q4 2016 Q4 2015 B/(W)

$4,313 $3,879 $434 10%

$777 18.0%

$639 16.5%

$138 150 bps

$1.83 $1.39 $0.44 32%

$683 $638 $45

EBITDA2

EBITDA margin %

$606 14.1%

$503 13.0%

$103 110 bps

Operating income2

Operating margin %

1 At constant foreign exchange and commodity rates; excludes impact of the E&S divestitures and HellermannTyton acquisition

2 Adjusted for restructuring and other special items; see Appendix for detail and reconciliation to US GAAP

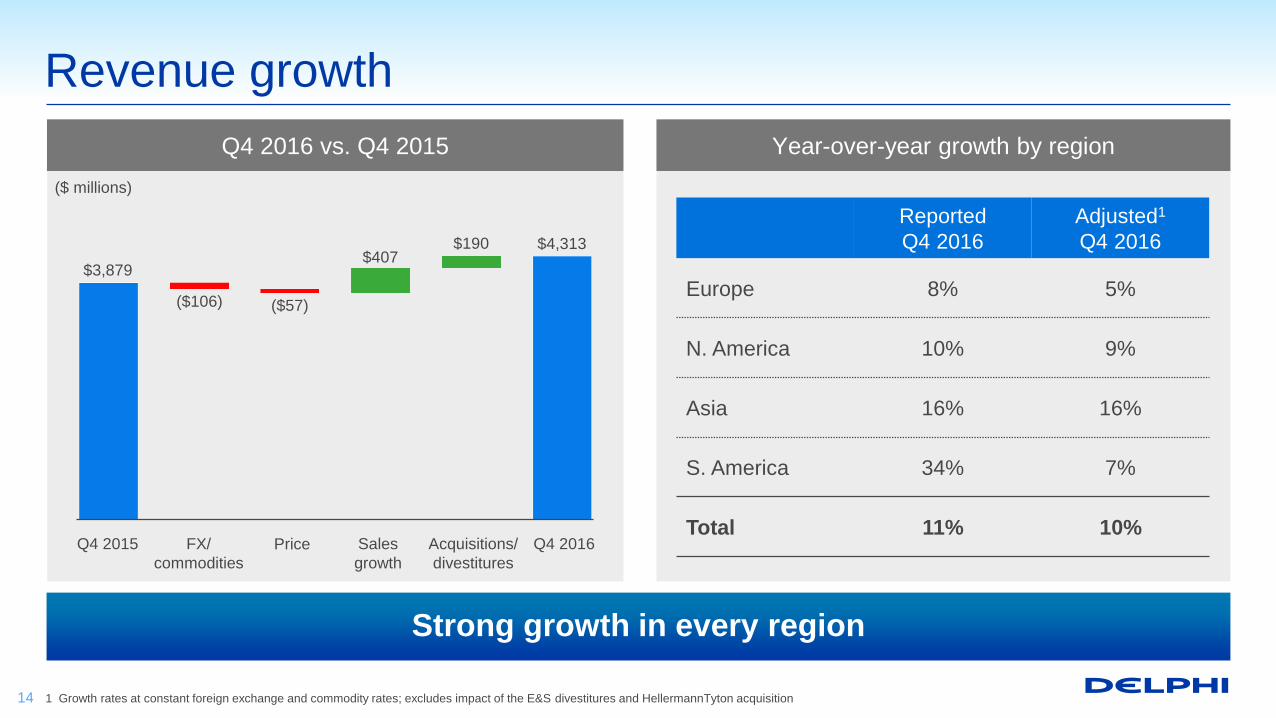

Year-over-year growth by region Q4 2016 vs. Q4 2015

14

Revenue growth

Strong growth in every region

$3,879

($106) ($57)

$407 $190 $4,313

Q4 2015 FX/

commodities

Sales

growth

Acquisitions/

divestitures

Q4 2016

Reported

Q4 2016

Adjusted1

Q4 2016

Europe 8% 5%

N. America 10% 9%

Asia 16% 16%

S. America 34% 7%

Total 11% 10%

($ millions)

Price

1 Growth rates at constant foreign exchange and commodity rates; excludes impact of the E&S divestitures and HellermannTyton acquisition

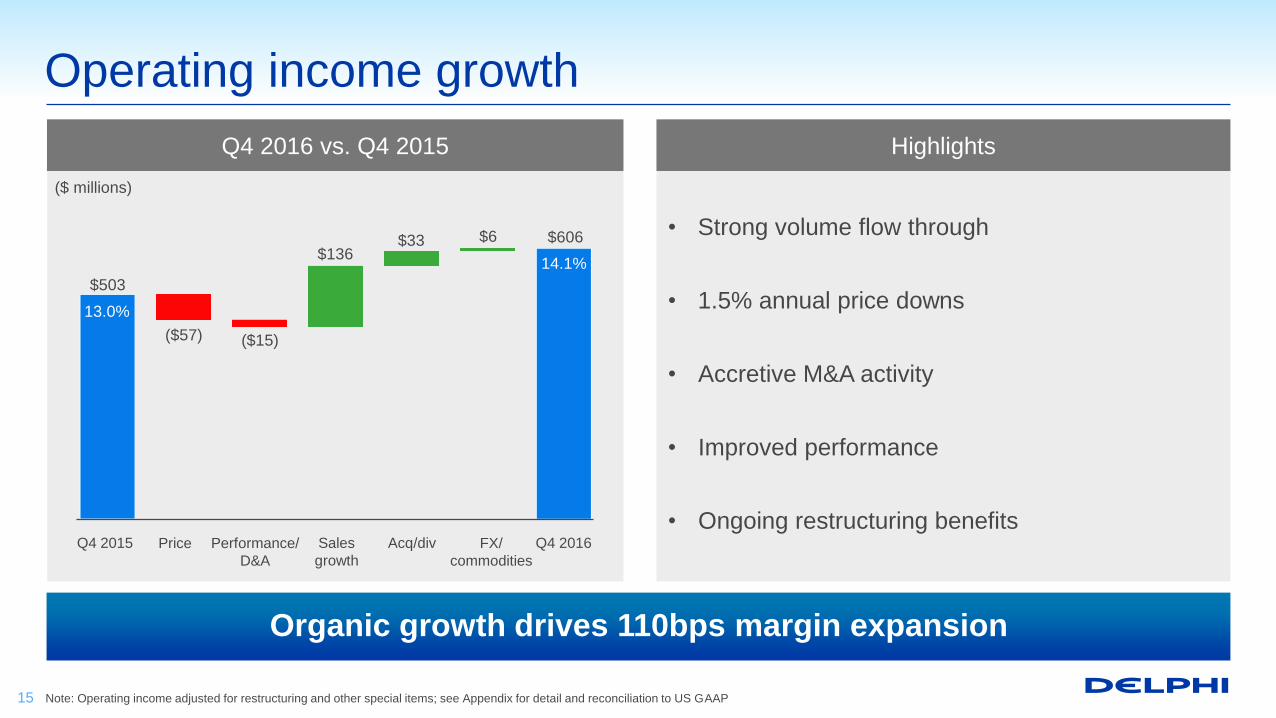

$503

($57) ($15)

$136 $33 $6 $606

Highlights Q4 2016 vs. Q4 2015

15

Operating income growth

Organic growth drives 110bps margin expansion

Price Sales

growth

Acq/div

($ millions)

Performance/

D&A

Note: Operating income adjusted for restructuring and other special items; see Appendix for detail and reconciliation to US GAAP

• Strong volume flow through

• 1.5% annual price downs

• Accretive M&A activity

• Improved performance

• Ongoing restructuring benefits Q4 2015 Q4 2016 FX/

commodities

13.0%

14.1%

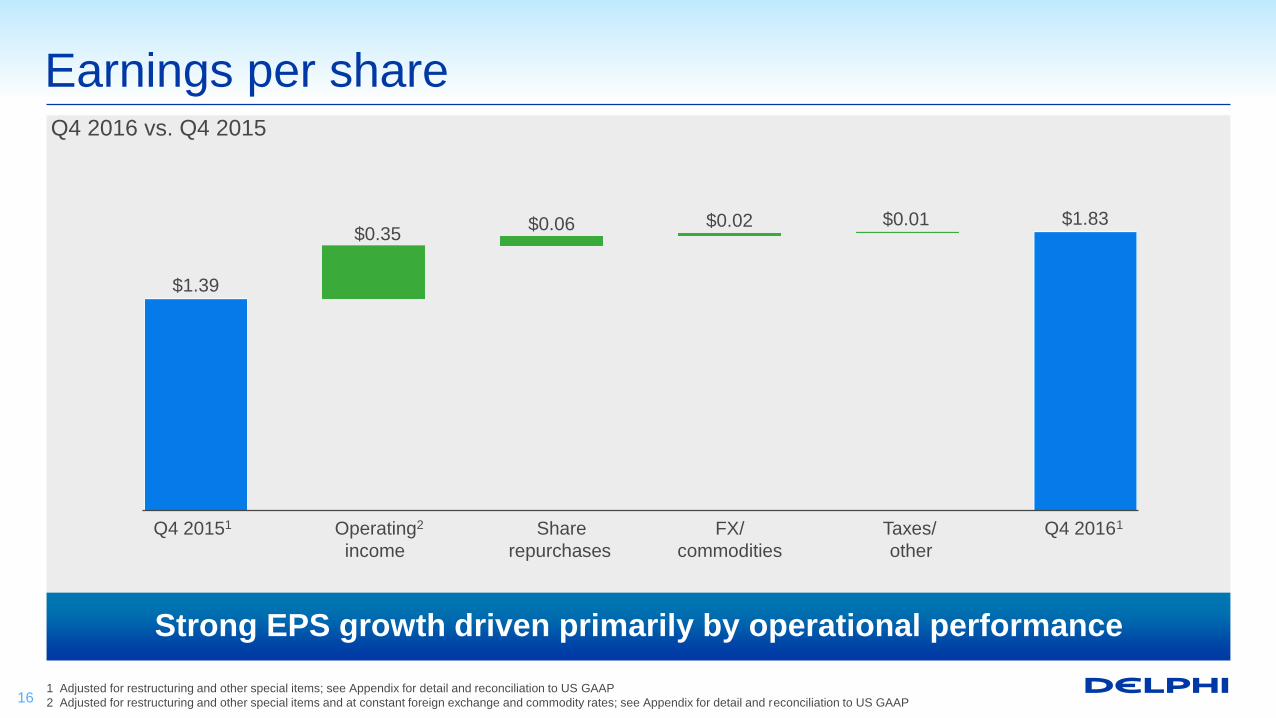

$1.39

$0.35 $0.06 $0.02 $0.01 $1.83

Q4 20151 Operating2 Share FX/ Taxes/ Q4 20161

income repurchases commodities other

Earnings per share

1 Adjusted for restructuring and other special items; see Appendix for detail and reconciliation to US GAAP

2 Adjusted for restructuring and other special items and at constant foreign exchange and commodity rates; see Appendix for detail and reconciliation to US GAAP 16

Q4 2016 vs. Q4 2015

Strong EPS growth driven primarily by operational performance

17

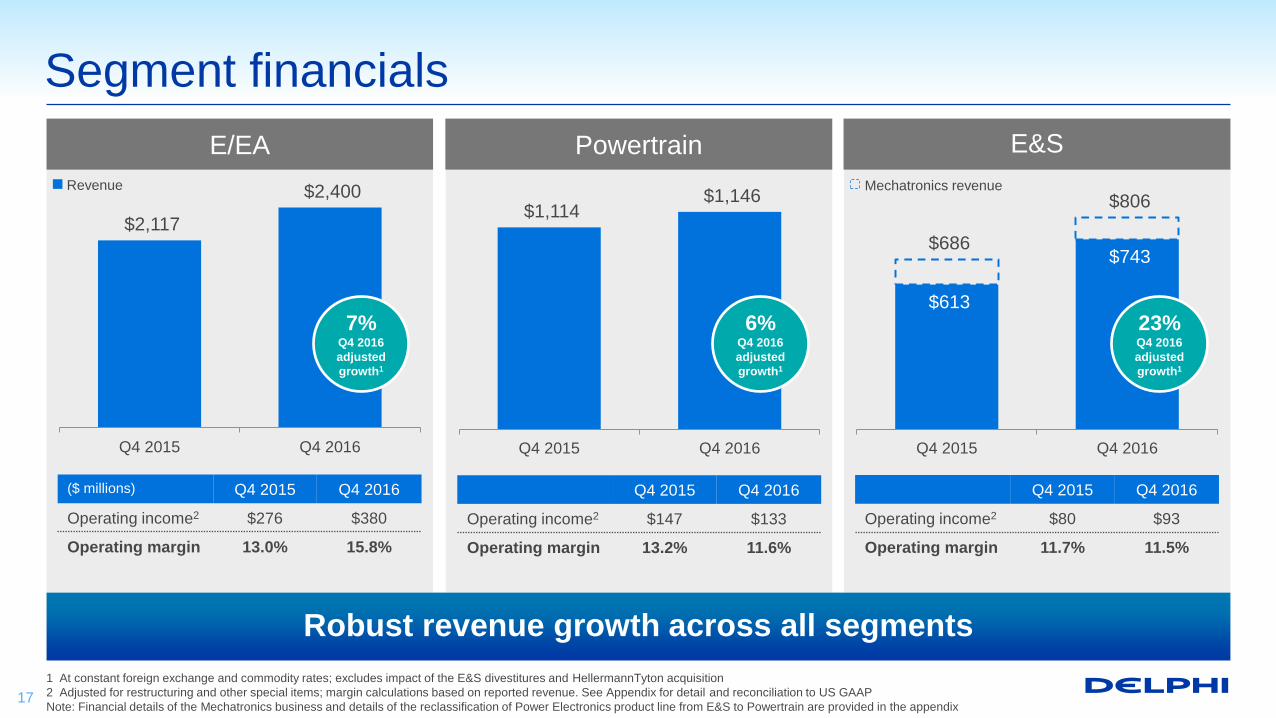

Segment financials

Robust revenue growth across all segments

Powertrain E&S E/EA

($ millions) Q4 2015 Q4 2016

Operating income2 $276 $380

Operating margin 13.0% 15.8%

Q4 2015 Q4 2016

Operating income2 $147 $133

Operating margin 13.2% 11.6%

Q4 2015 Q4 2016

Operating income2 $80 $93

Operating margin 11.7% 11.5%

$2,117

$2,400

Q4 2015 Q4 2016

Revenue

$1,114 $1,146

Q4 2015 Q4 2016

$613

$743 $686

$806

Q4 2015 Q4 2016

Mechatronics revenue

7% Q4 2016

adjusted

growth1

6% Q4 2016

adjusted

growth1

23% Q4 2016

adjusted

growth1

1 At constant foreign exchange and commodity rates; excludes impact of the E&S divestitures and HellermannTyton acquisition

2 Adjusted for restructuring and other special items; margin calculations based on reported revenue. See Appendix for detail and reconciliation to US GAAP

Note: Financial details of the Mechatronics business and details of the reclassification of Power Electronics product line from E&S to Powertrain are provided in the appendix

18

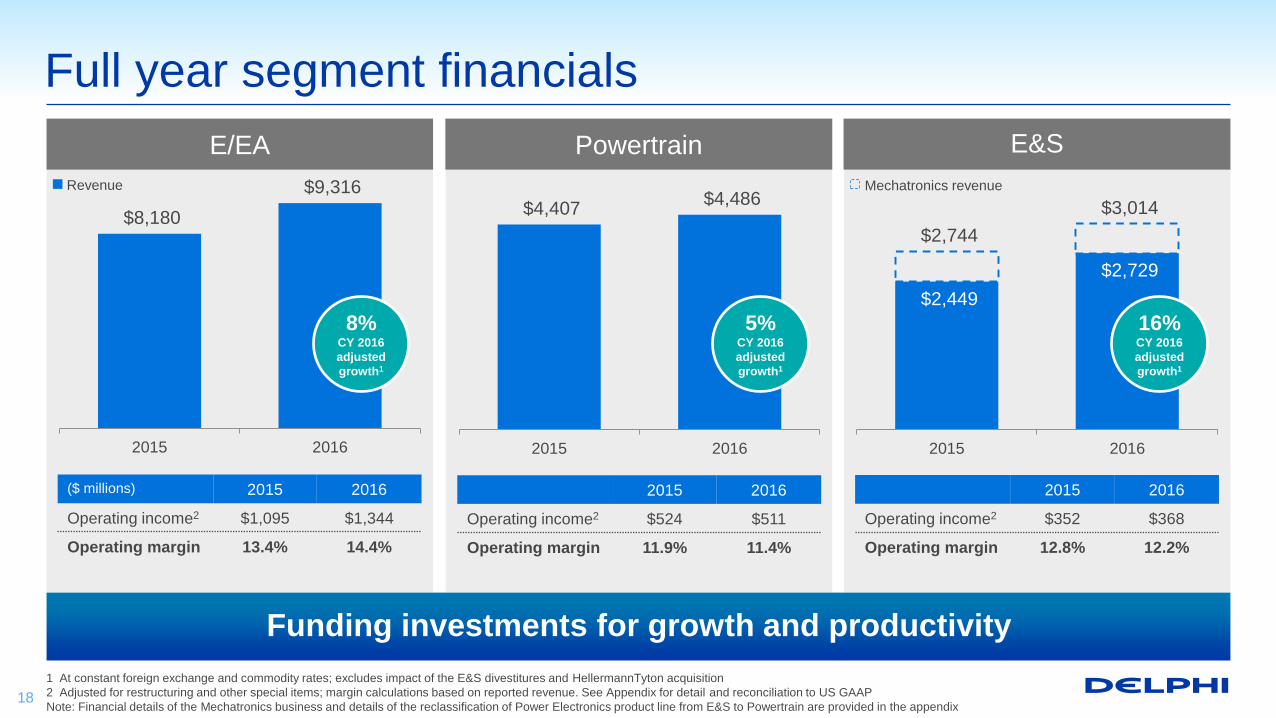

Full year segment financials

Funding investments for growth and productivity

Powertrain E&S E/EA

($ millions) 2015 2016

Operating income2 $1,095 $1,344

Operating margin 13.4% 14.4%

2015 2016

Operating income2 $524 $511

Operating margin 11.9% 11.4%

2015 2016

Operating income2 $352 $368

Operating margin 12.8% 12.2%

$8,180

$9,316

2015 2016

Revenue

$4,407 $4,486

2015 2016

$2,449

$2,729

$2,744

$3,014

2015 2016

8% CY 2016

adjusted

growth1

Mechatronics revenue

5% CY 2016

adjusted

growth1

16% CY 2016

adjusted

growth1

1 At constant foreign exchange and commodity rates; excludes impact of the E&S divestitures and HellermannTyton acquisition

2 Adjusted for restructuring and other special items; margin calculations based on reported revenue. See Appendix for detail and reconciliation to US GAAP

Note: Financial details of the Mechatronics business and details of the reclassification of Power Electronics product line from E&S to Powertrain are provided in the appendix

2016 vs. 2015 ($ millions, except per share amounts)

19

Outstanding performance consistent with outlook

Reported revenue Adjusted Growth %1

Earnings per share2

Growth %

Operating cash flow

2016 2015 B/(W)

$16,661 $15,165 $1,496

8%

$2,897 17.4%

$2,495 16.5%

$402 90 bps

$6.28 $5.22 $1.06 20%

$1,941 $1,667 $274

EBITDA2

EBITDA margin %

$2,223 13.3%

$1,971 13.0%

$252 30 bps

Operating income2

Operating margin %

1 At constant foreign exchange and commodity rates; excludes impact of the E&S divestitures and HellermannTyton acquisition

2 Adjusted for restructuring and other special items; see Appendix for detail and reconciliation to US GAAP

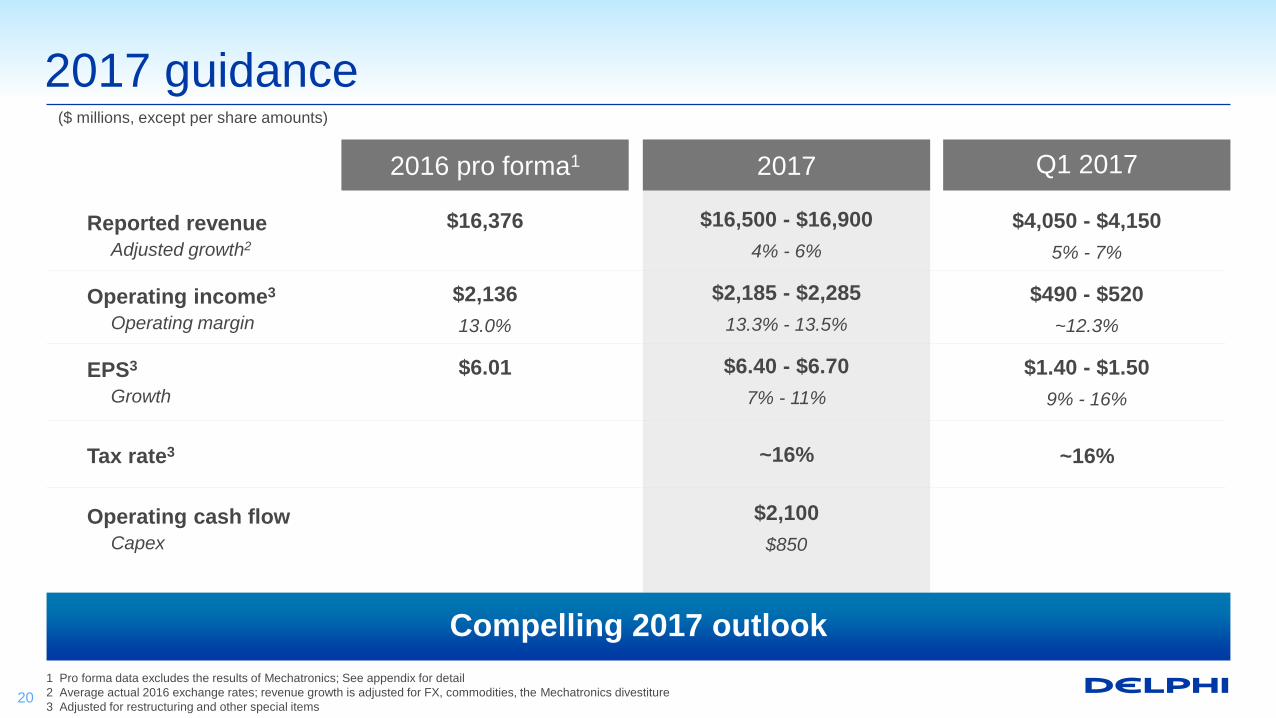

2017 Q1 2017

2017 guidance

20

Compelling 2017 outlook

$4,050 - $4,150

5% - 7%

$490 - $520

~12.3%

~16%

$1.40 - $1.50

9% - 16%

$16,500 - $16,900

4% - 6%

$2,185 - $2,285

13.3% - 13.5%

~16%

$6.40 - $6.70

7% - 11%

$2,100

$850

Reported revenue

Adjusted growth2

Operating income3

Operating margin

Tax rate3

EPS3

Growth

Operating cash flow

Capex

($ millions, except per share amounts)

2016 pro forma1

$16,376

$2,136

13.0%

$6.01

1 Pro forma data excludes the results of Mechatronics; See appendix for detail

2 Average actual 2016 exchange rates; revenue growth is adjusted for FX, commodities, the Mechatronics divestiture

3 Adjusted for restructuring and other special items

Wrap up

21

• Delivered continued outperformance in 2016 – Strong sales growth above market and 30 bps of margin expansion yielding 20% EPS growth

– Continued traction on portfolio rotation, strengthening position to leverage secular growth trends

• Confident in 2017 outlook – Mid-single digit organic revenue growth driven by portfolio of advanced technologies

– Solid operating margin expansion while continuing investments for growth

• Strong, sustainable competitive advantages – Industry-leading technology portfolio driving record new business wins

– Attractive cost structure and flexible business model

– Efficient capital structure drives more cash yielding industry-leading shareholder returns

21

Creating shareholder value remains highest priority

Making it possible.

Appendix

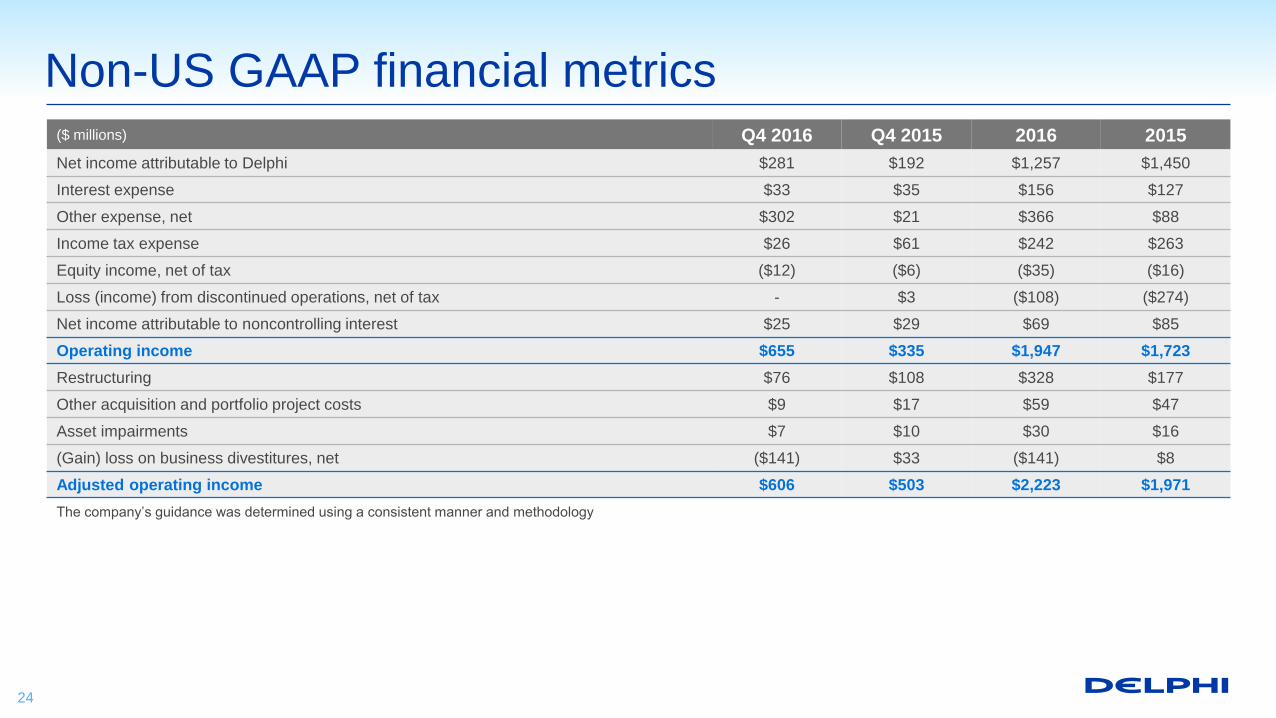

($ millions) Q4 2016 Q4 2015 2016 2015

Net income attributable to Delphi $281 $192 $1,257 $1,450

Interest expense $33 $35 $156 $127

Other expense, net $302 $21 $366 $88

Income tax expense $26 $61 $242 $263

Equity income, net of tax ($12) ($6) ($35) ($16)

Loss (income) from discontinued operations, net of tax - $3 ($108) ($274)

Net income attributable to noncontrolling interest $25 $29 $69 $85

Operating income $655 $335 $1,947 $1,723

Restructuring $76 $108 $328 $177

Other acquisition and portfolio project costs $9 $17 $59 $47

Asset impairments $7 $10 $30 $16

(Gain) loss on business divestitures, net ($141) $33 ($141) $8

Adjusted operating income $606 $503 $2,223 $1,971

The company’s guidance was determined using a consistent manner and methodology

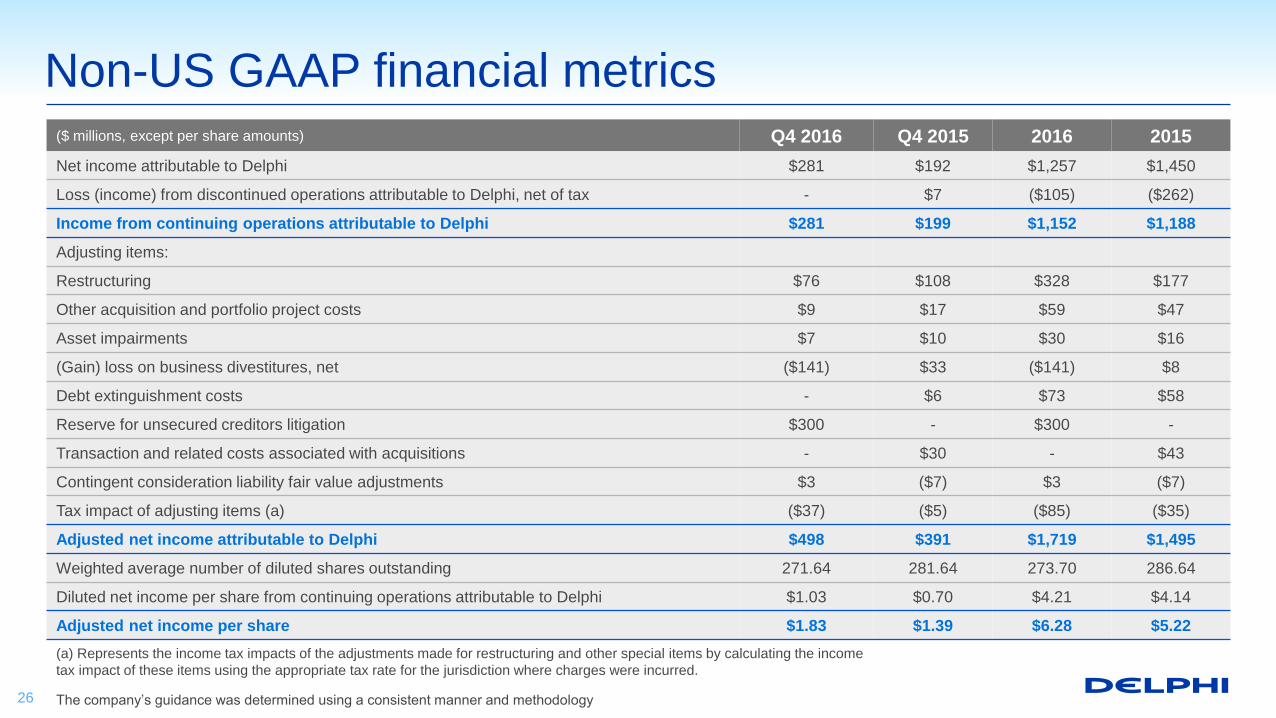

Non-US GAAP financial metrics

24

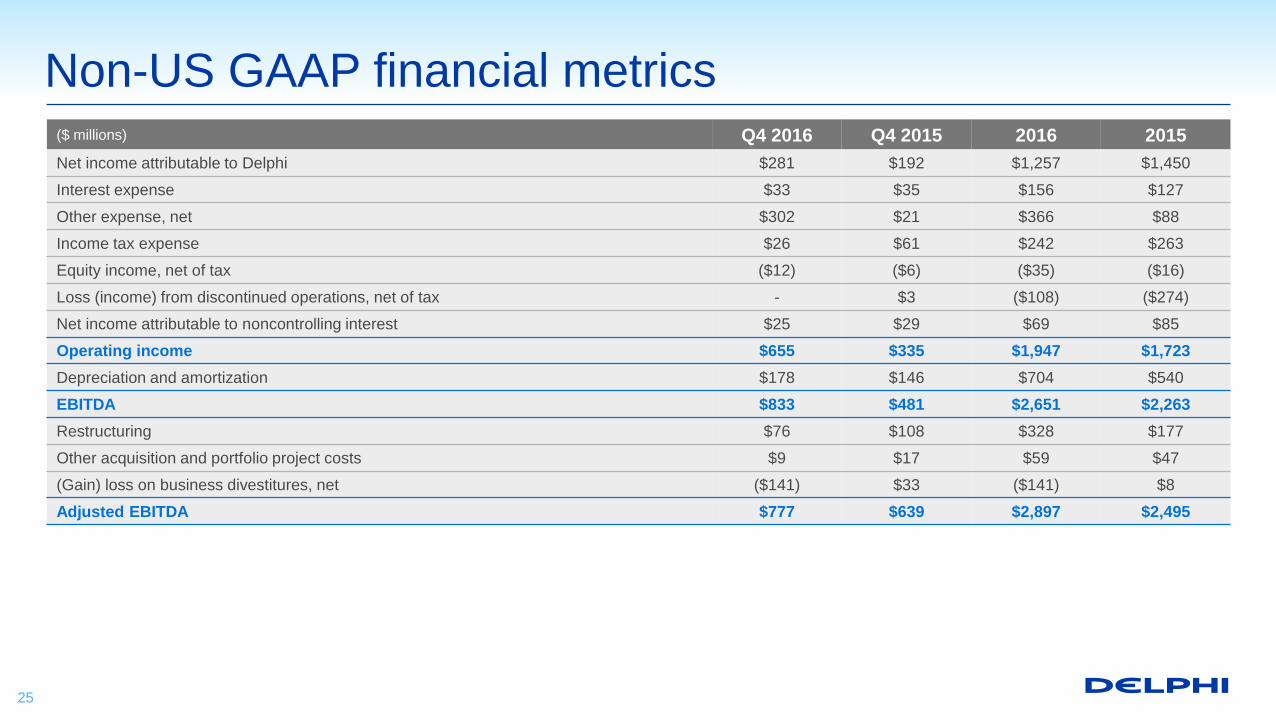

Non-US GAAP financial metrics ($ millions) Q4 2016 Q4 2015 2016 2015

Net income attributable to Delphi $281 $192 $1,257 $1,450

Interest expense $33 $35 $156 $127

Other expense, net $302 $21 $366 $88

Income tax expense $26 $61 $242 $263

Equity income, net of tax ($12) ($6) ($35) ($16)

Loss (income) from discontinued operations, net of tax - $3 ($108) ($274)

Net income attributable to noncontrolling interest $25 $29 $69 $85

Operating income $655 $335 $1,947 $1,723

Depreciation and amortization $178 $146 $704 $540

EBITDA $833 $481 $2,651 $2,263

Restructuring $76 $108 $328 $177

Other acquisition and portfolio project costs $9 $17 $59 $47

(Gain) loss on business divestitures, net ($141) $33 ($141) $8

Adjusted EBITDA $777 $639 $2,897 $2,495

25

($ millions, except per share amounts) Q4 2016 Q4 2015 2016 2015

Net income attributable to Delphi $281 $192 $1,257 $1,450

Loss (income) from discontinued operations attributable to Delphi, net of tax - $7 ($105) ($262)

Income from continuing operations attributable to Delphi $281 $199 $1,152 $1,188

Adjusting items:

Restructuring $76 $108 $328 $177

Other acquisition and portfolio project costs $9 $17 $59 $47

Asset impairments $7 $10 $30 $16

(Gain) loss on business divestitures, net ($141) $33 ($141) $8

Debt extinguishment costs - $6 $73 $58

Reserve for unsecured creditors litigation $300 - $300 -

Transaction and related costs associated with acquisitions - $30 - $43

Contingent consideration liability fair value adjustments $3 ($7) $3 ($7)

Tax impact of adjusting items (a) ($37) ($5) ($85) ($35)

Adjusted net income attributable to Delphi $498 $391 $1,719 $1,495

Weighted average number of diluted shares outstanding 271.64 281.64 273.70 286.64

Diluted net income per share from continuing operations attributable to Delphi $1.03 $0.70 $4.21 $4.14

Adjusted net income per share $1.83 $1.39 $6.28 $5.22

(a) Represents the income tax impacts of the adjustments made for restructuring and other special items by calculating the income

tax impact of these items using the appropriate tax rate for the jurisdiction where charges were incurred.

The company’s guidance was determined using a consistent manner and methodology

Non-US GAAP financial metrics

26

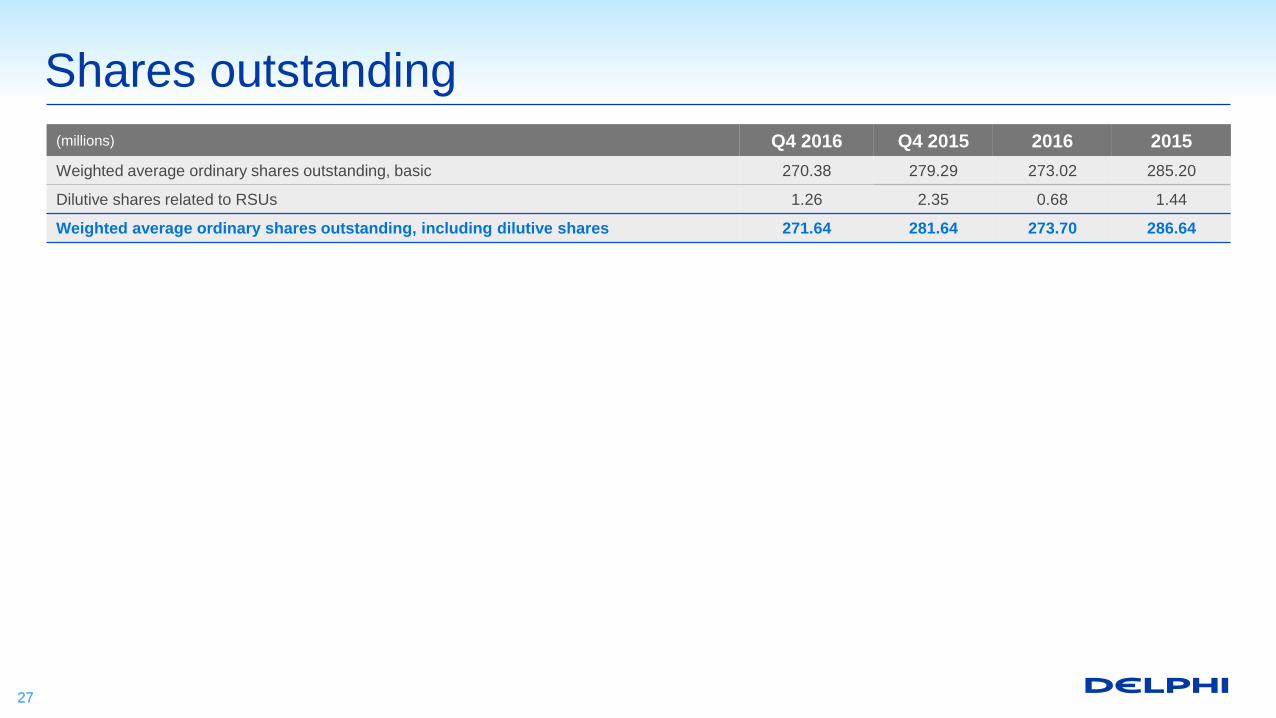

Shares outstanding

27

(millions) Q4 2016 Q4 2015 2016 2015

Weighted average ordinary shares outstanding, basic 270.38 279.29 273.02 285.20

Dilutive shares related to RSUs 1.26 2.35 0.68 1.44

Weighted average ordinary shares outstanding, including dilutive shares 271.64 281.64 273.70 286.64

27

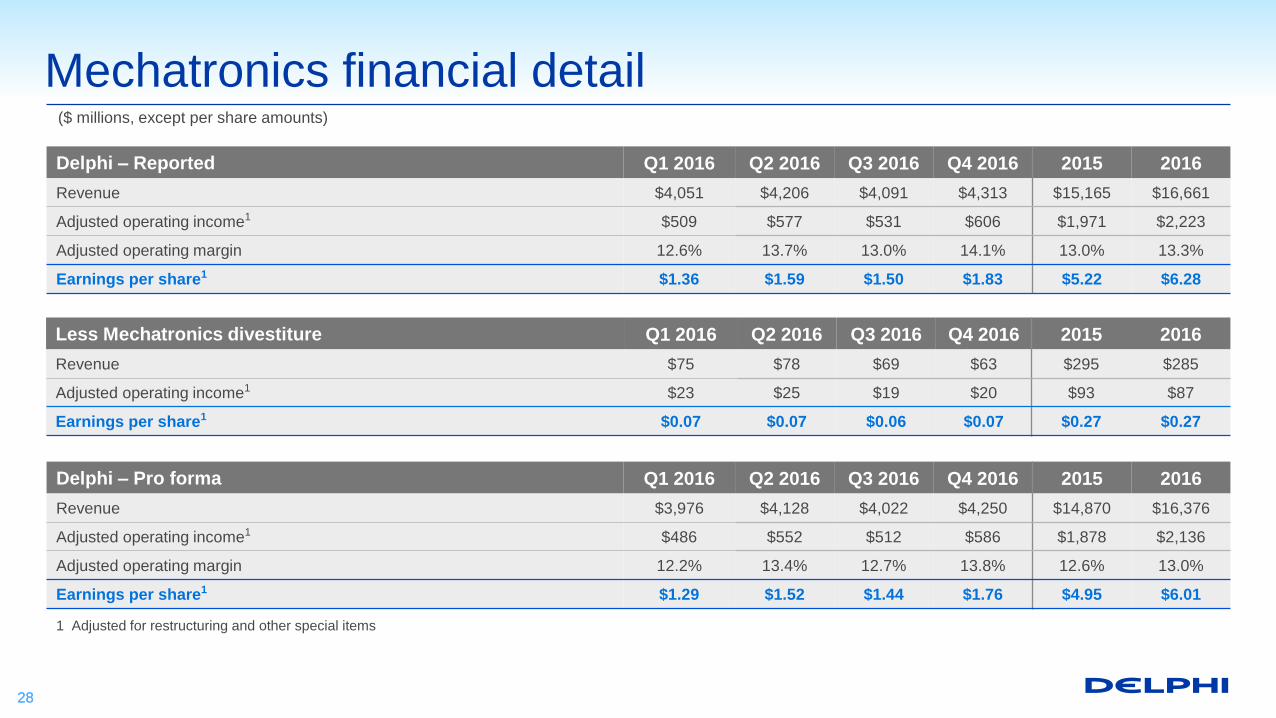

Mechatronics financial detail

28 28

Delphi – Reported Q1 2016 Q2 2016 Q3 2016 Q4 2016 2015 2016

Revenue $4,051 $4,206 $4,091 $4,313 $15,165 $16,661

Adjusted operating income1 $509 $577 $531 $606 $1,971 $2,223

Adjusted operating margin 12.6% 13.7% 13.0% 14.1% 13.0% 13.3%

Earnings per share1 $1.36 $1.59 $1.50 $1.83 $5.22 $6.28

($ millions, except per share amounts)

Less Mechatronics divestiture Q1 2016 Q2 2016 Q3 2016 Q4 2016 2015 2016

Revenue $75 $78 $69 $63 $295 $285

Adjusted operating income1 $23 $25 $19 $20 $93 $87

Earnings per share1 $0.07 $0.07 $0.06 $0.07 $0.27 $0.27

Delphi – Pro forma Q1 2016 Q2 2016 Q3 2016 Q4 2016 2015 2016

Revenue $3,976 $4,128 $4,022 $4,250 $14,870 $16,376

Adjusted operating income1 $486 $552 $512 $586 $1,878 $2,136

Adjusted operating margin 12.2% 13.4% 12.7% 13.8% 12.6% 13.0%

Earnings per share1 $1.29 $1.52 $1.44 $1.76 $4.95 $6.01

1 Adjusted for restructuring and other special items

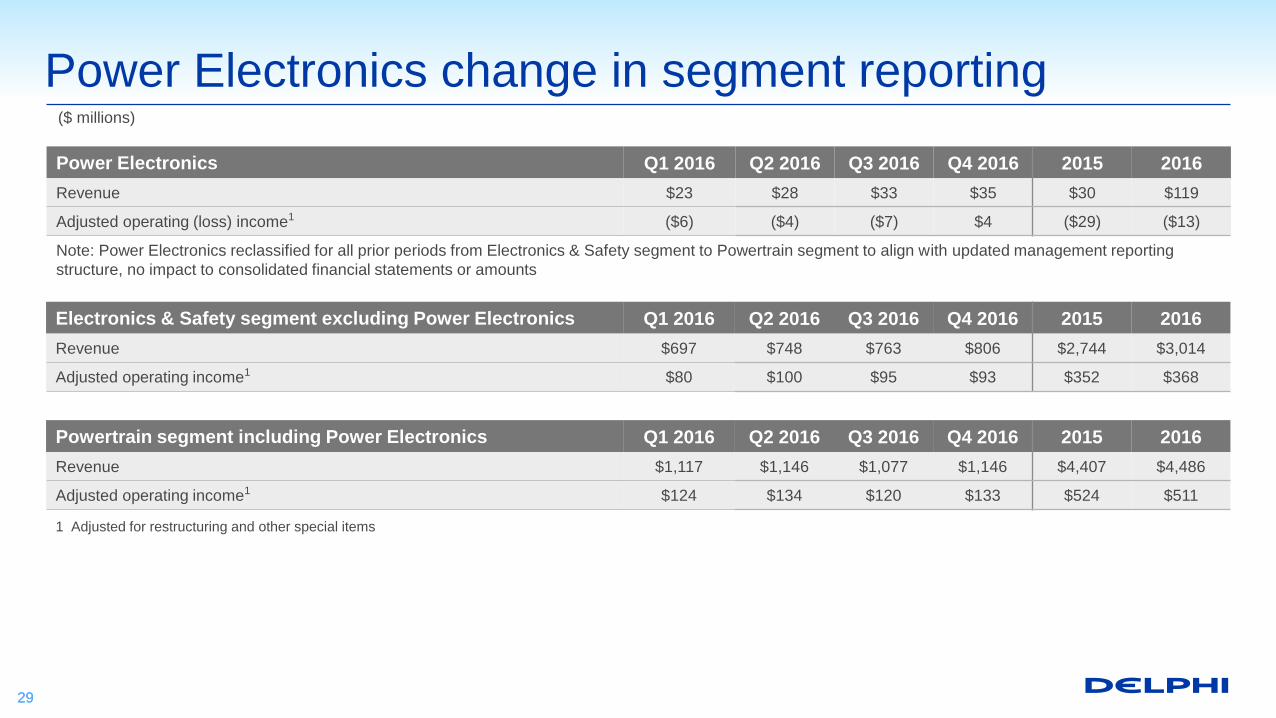

Power Electronics change in segment reporting

29 29

Power Electronics Q1 2016 Q2 2016 Q3 2016 Q4 2016 2015 2016

Revenue $23 $28 $33 $35 $30 $119

Adjusted operating (loss) income1 ($6) ($4) ($7) $4 ($29) ($13)

Note: Power Electronics reclassified for all prior periods from Electronics & Safety segment to Powertrain segment to align with updated management reporting

structure, no impact to consolidated financial statements or amounts

($ millions)

Electronics & Safety segment excluding Power Electronics Q1 2016 Q2 2016 Q3 2016 Q4 2016 2015 2016

Revenue $697 $748 $763 $806 $2,744 $3,014

Adjusted operating income1 $80 $100 $95 $93 $352 $368

Powertrain segment including Power Electronics Q1 2016 Q2 2016 Q3 2016 Q4 2016 2015 2016

Revenue $1,117 $1,146 $1,077 $1,146 $4,407 $4,486

Adjusted operating income1 $124 $134 $120 $133 $524 $511

1 Adjusted for restructuring and other special items

![WELCOME [s22.q4cdn.com]s22.q4cdn.com/364334381/files/doc_presentations/NVIDIA_Investor... · drivable L3/L4 self-driving car, connected to all HD maps, continuously driving/testing/refining,](https://img.pdfslide.us/doc/110x75/5afb225b7f8b9ae92b8ea0e5/welcome-s22q4cdncoms22q4cdncom364334381filesdocpresentationsnvidiainvestordrivable.jpg)