Embed Size (px)

Citation preview

For More Information: email [email protected] or call 1(800) 282-2839

�e Experts In Actuarial Career AdvancementP U B L I C A T I O N S

Product Preview

SECTION A

FINANCIAL REPORTING

LOMBARDI, Chapter 1

ACTEX 2014 SOA Exam: ILA – LFV, U.S.

A-1

LOMBARDI, CHAPTER 1, OVERVIEW OF VALUATION REQUIREMENTS

I. Introduction A. Determination of reserves is important actuarial function. B. Reserves include claim or loss reserves and policy reserves. C. Actuarial or policy reserves are determined using an actuarial valuation. II. Role of Reserves is to properly match revenues and costs. III. Actuarial Assumptions A. Expenses, investment returns, mortality, morbidity, voluntary terminations and taxes. B. Based on company’s past experience, industry studies, regulatory requirements and judgments about the future. C. They affect the timing of reported earnings. IV. Accounting Principles A. Statutory Accounting Principles (SAP) 1. Emphasis is on solvency. 2. Focus is on the balance sheet. 3. NAIC assists state officials to provide standards. B. Generally Accepted Accounting Principles (GAAP) 1. Established primarily by FASB. 2. Emphasis is on matching of current revenue with current costs. 3. Focus is on income statement. C. International Accounting Standards (IAS) 1. Developed by IASB. 2. Transparency and comparability are the objectives. D. Tax Basis Accounting 1. Tax reserves are computed according to DEFRA of 1984. 2. DAC tax is defined in the Revenue Reconciliation Act of 1990. E. Fair Value Accounting 1. SFAS 115 adopted in 1993, was a preliminary step toward fair value accounting. 2. Hierarchy for determining fair value a. Market value when available. b. Market value of similar instruments with appropriate adjustment. c. Present value of projected cash flows.

LOMBARDI, Chapter 1

ACTEX 2014 SOA Exam: ILA – LFV, U.S.

A-2

V. Types of Valuations A. Statutory Valuations 1. Conservative. 2. Prescribed in the US. 3. Increasingly, reliance on US valuation actuary. 4. In Canada, responsibility is on appointed actuary. 5. Canadian prescribed reserving method is CALM. B. GAAP Valuations 1. Based on company experience with modest PfADs. 2. Incorporate explicit recognition of all material actuarial assumptions. 3. Another difference with statutory valuation is the DAC asset. C. Tax Reserve Valuations 1. In US, from 1958 to 1984, based on statutory reserves with some adjustments. 2. Starting in 1984, Federally Prescribed Tax Reserves a. CRVM for life insurance and CARVM for annuities. b. Interest is larger of AFIR and prevailing state assumed interest rate. c. Prevailing Commissioners standard mortality table in at least 26 states. 3. In Canada, changes in 1978, 1988 and 1996. 4. In Canada, for policies issued prior to Jan 1, 1996 a. Max reserve is calculated using 1½ year preliminary term with a CV floor. b. Lower than NLP and 1 year preliminary term. c. For group term policies of less than 1 year, unearned premium reserve. 5. In Canada, for policies issued after Dec 31, 1995 a. Max reserve is lesser of reported reserves and policy liabilities. b. Both are calculated without reference to income or capital taxes. c. For group term policies, no change. D. Gross Premium Valuations 1. Best estimate value of liabilities. 2. In the case of merger and acquisition. 3. When company examined to determine solvency. 4. Little or no provision for conservatism.

LOMBARDI, Chapter 1

ACTEX 2014 SOA Exam: ILA – LFV, U.S.

A-3

E. Embedded Value

1. Sum of value of in force business and adjusted net worth.2. Value of in force business

a. PV of projected after-tax statutory earnings – change in required capital.b. Earnings are discounted using cost of capital.c. Cost of capital is rate of return offered by similar investments.d. CAPM cost of capital = risk-free rate + risk premium.

3. Adjusted net worth

a. Market value of assets supporting statutory surplus, plusb. PV of cost of capital for holding required capital.

VI. Effects of Statutory Valuation Requirements

A. Gross Premium Levels: indirect impact.B. Product Design.C. Federal Income Taxes: minor effects.D. Dividends to Policyholders: can have a significant effect.E. Statutory Earnings and appraisal value.F. Important Indicators,

VII. Statutory Valuation Requirements in Canada

A. Insurance Companies Act of 1992 created the role of the appointed actuary

1. Appointments made and terminated by board of directors.2. Actuary will value and report on actuarial liabilities.3. Actuary will report to board on current financial position of company.4. Actuary may be directed to report on future financial position of company.5. Actuary must have access to all company records and information.6. Actuary must report on material circumstances to management and board.7. If not corrected, must send report to OSFI.8. Actuary must render opinion on administration of dividend policy prior to

distributions.

B. Standards of Practice for the Appointed Actuary (AA)

1. Developed by CIA, the national organization of actuarial profession in Canada.2. Recommendations deal with

a. Verification of valuation data.b. Development of appropriate assumptions.c. Choice of valuation method.d. Text and implications of reports accompanying statements.e. Documentation of valuation actuary’s work.f. Use of approximations.g. Judgment regarding materiality.

LOMBARDI, Chapter 1

ACTEX 2014 SOA Exam: ILA – LFV, U.S.

A-4

3. Also, many CIA publications. 4. CLIFR and OSFI also provide annual documents. 5. OSFI Requirement of periodic external review a. To maintain and strengthen confidence. b. To narrow range of practice of Aas. c. To improve quality of AA’s work. d. To provide significant professional education for AA. 6. CIA developed standards of practice for external review process. C. The Canadian Asset Liability Method (CALM) is a prospective method using 1. Full gross premium for the policy. 2. Estimated expenses and obligations under the policy. 3. Current expected experience assumptions plus margin for adverse deviations. 4. Scenario testing for interest rate and market risks. D. Minimum Continuing Capital and Surplus Requirements (MCCSR) 1. Assuris is an association protecting policyholders against loss due to insolvency. 2. Every company is required to be a member. 3. Assuris facilitates transfer to solvent company. 4. Assuris is a not-for-profit organization funded by assessments of its members. 5. Assessment base is MCCSR, similar to RBC in the US. 6. Assessment may continue indefinitely at a rate of 1.33% of MCCSR. E. Dynamic Capital Adequacy Testing (DCAT) 1. Base and other scenarios suggested for investigation. 2. Other scenarios appropriate according to AA. 3. Scenarios include in force and anticipated new business. 4. Written report to board. F. Joint Policy Statement 1. Issued by CIA and CICA in 1991. 2. Recognizes that either the actuary or the auditor could use specialized work of other. 3. Aspects of the work that should be considered a. Qualifications, competence, integrity and objectivity. b. Appointment to do the work. c. Whether he followed standards. d. Appropriateness of findings and opinions.

LOMBARDI, Chapter 1

ACTEX 2014 SOA Exam: ILA – LFV, U.S.

A-5

VIII. Statutory Valuation Requirements in the United States A. Introduction 1. NAIC Manual published in 1998 a. Preamble. b. Statements of Statutory Accounting Principles (SSAPs). c. Appendices. 2. Does not preempt state laws and regulations. 3. Actuary should be familiar with concepts underlying RBC. B. SSAP No. 50 provides general framework to classify contracts into 1. Life Contracts. 2. Accident and Health Contracts. 3. Property and Casualty Contracts. 4. Deposit-type Contracts. C. SSAP No. 51 1. Establishes principles for income recognition and policy reserves. 2. For all contracts classified as life contracts. D. Appendices A-820 and A-822 1. Contains excerpts of a. NAIC model Standard Valuation Law (SVL). b. Model Actuarial Opinion and Memorandum Regulation. 2. Qualified actuary is appointed by board and called appointed actuary (AA). 3. AA must issue a statement of actuarial opinion. 4. Statement should list items and amounts for which AA expresses opinion. 5. Opinion is on adequacy of reserves in aggregate. 6. Statement frequently indicates reliance on others. 7. Statement should indicate relationship with company and scope of work. E. ASOP No. 22 1. Section 3.1: Review and apply ASOP No. 7. 2. Section 3.2: AA should meet qualification standards of AAA. 3. Section 3.3: Form, content and recommended language. 4. Section 3.4: Appropriate analysis methods.

LOMBARDI, Chapter 1

ACTEX 2014 SOA Exam: ILA – LFV, U.S.

A-6

LOMBARDI, Chapter 2

ACTEX 2014 SOA Exam: ILA – LFV, U.S.

A-7

LOMBARDI, CHAPTER 2, NAIC ANNUAL STATEMENT

I. Statutory Annual Statement

A. Introduction

1. Must comply with standards as adopted by each state.2. Format and content specified by NAIC.3. Many companies must file several different statements.

B. Primary Financial Statements

1. Balance Sheet.2. Summary of Operations.3. Capital and Surplus Account.*4. Cash Flow Statement.*5. Analysis of Operations by Lines of Business.

C. Primary Actuarial Schedules and Exhibits

1. Analysis of Increase in Reserves During the Year.*2. Exhibit 1 – Part 1 – Premiums and Annuity Considerations.3. Exhibit 5 – Aggregate Reserve for Life Policies and Contracts.4. Exhibit 8 – Policy and Contract Claims.5. Exhibit of Life Insurance.*6. Exhibit of # of Policies, Contracts, Certificates, Income Payable and Account Values

in Force for Supplementary Contracts, Annuities, A&H and Other Policies.*

D. Successive Equation

1. Value (E) = Value (B) + Increases – Decreases.2. Statements and exhibits using this feature are marked above with an asterisk.3. Balance sheet is as of a particular point in time.4. Summary of operations spans a period of time.

II. Balance Sheet

A. Introduction

1. Under GAAP, Assets = Liabilities + Equity.2. Under statutory accounting principles, Surplus = Assets – Liabilities.

B. Assets

1. Significant detail because industry has a lot of assets.2. Industry performs important role as financial intermediary.3. Bonds, Stocks, Mortgages, Real estate, Cash, Contract loans…

C. Liabilities and Surplus: Most of the liabilities are the policy reserve.

LOMBARDI, Chapter 2

ACTEX 2014 SOA Exam: ILA – LFV, U.S.

A-8

III. Summary of Operations A. It presents operating results of company for a period of time. B. Net gain = revenue – costs. C. Net income = net gain + realized capital gains (after taxes). D. Major revenue items are premium and annuity considerations and net investment income. E. Major cost items are benefit payments, increase in reserves, commissions and expenses. IV. Capital and Surplus Account A. It shows how surplus changed between 2 accounting dates. B. Surplus (E) = Surplus (B) + Net income – Dividends + Other Charges. C. Dividends represent dividends to shareholders. D. Over a long time period, net income is primary source by which surplus grows. E. Net income less dividends should exceed growth rate times Surplus (B). V. Cash Flow Statement A. It shows reconciliation of cash and short-term investments between 2 accounting dates. B. First section demonstrates the 3 primary sources and uses of cash flow 1. Cash from operations (CO). 2. Cash from investment activities (CI). 3. Cash from financing activities (CF). C. Second section shows how and why liquidity changed during the period. D. Cash (E) = Cash (B) + CO + CI + CF. VI. Analysis of Operations by Lines of Business A. It shows the gain from operations from major business segments of company. B. It provides information to do analysis of profitability. C. Also called Gain and Loss Exhibit. VII. Analysis of Increase in Reserves During the Year A. It shows how the policy reserve changed during the period. B. Res (E) = Res (B) + Net Premium + Tabular Interest – Tabular Cost + Other Changes. VIII. Exhibit 1 – Part 1: Premiums and Annuity Considerations A. Premium is major source of revenue for most companies. B. It shows how premiums have been adjusted from cash to accrual basis. C. It also shows effect of reinsurance. D. It splits total premiums into 1. Premiums earned on policies in first policy year (indication of sales). 2. Single premiums (indication of non-recurring premiums). 3. Premiums earned on policies after first policy year (renewal premiums). E. Premium = Direct premium + Reinsurance assumed – Reinsurance ceded.

LOMBARDI, Chapter 2

ACTEX 2014 SOA Exam: ILA – LFV, U.S.

A-9

F. Direct premium = Collected premium + ∆Deferred premium - ∆Advanced premium. G. Deferred premium reflects frequency of premium payments assumed in reserves and actual frequency of payments required. H. Advanced premium reflects premium received prior to valuation date but due only after that date.

IX. Exhibit 5 – Aggregate Reserve for Life Policies and Contracts

A. One of the most important actuarial exhibits in the statement.B. It shows policy reserves for current period by major product line and valuation standard.C. Valuation standard represents methodology and assumptions used.D. Life, Annuities, Suppl. Contr. With Life Cont., ADB, Dis. Active, Dis. Disabled, Misc.

X. Exhibit 8 – Policy and Contract Claims

A. It shows how certain benefit payments have been adjusted from cash to accrual basis. B. Due and unpaid, in course of settlements, incurred but not reported.

XI. Exhibit of Life Insurance

A. It shows the # of policies and amount of insurance in force.B. It demonstrates how these values changed during the period.C. In force (E) = In force (B) + Issues – Deaths – Other Terminations + Other Changes.D. Very useful.

XII. Exhibit of Annuities: Similar purpose as Exhibit of Life Insurance.

LOMBARDI, Chapter 2

ACTEX 2014 SOA Exam: ILA – LFV, U.S.

A-10

SECTION D

FINANCIAL MANAGEMENT AND

VALUE CREATION

SN LFV-106-07

ACTEX 2013 SOA Exam: ILA – LFV, U.S.

D-1

SN LFV-106-07 VALUATION TECHNIQUES,

TOOLE-HERGET, CHAPTER 4, SECTIONS 4.1 TO 4.6

I. Introduction: Valuation Techniques for Insurance M&A

A. Issue is to value the company as a going concern; company is not purchased for its assets, but the ability of the assets to generate income

B. A runoff business is generally worth less than it would be as a going concern.

C. A going concern valuation captures value of intangible assets

1. Distribution relationships. 2. Geographic reach. 3. Customer loyalty. 4. Market perception. D. Unique aspects of insurance industry 1. Liabilities can extend over very long period of time. 2. Liabilities involve great deal of uncertainty, requiring actuarial techniques. 3. Statutory accounting and capital requirements. E. Key assumptions—mortality, morbidity, persistency, investment returns, operating

expense, discount rate, cost of capital and taxes II. General Valuation Techniques A. Insurance Company Valuations

1. More complicated because skill set is highly specialized.

2. Challenges in valuing insurance industry a. Long duration of liabilities. b. Sensitivity to interest rate fluctuations and performance of capital markets. c. Inherently subjective and dynamic art of loss reserving. d. Cyclical nature of P&C insurance and reinsurance. e. Impact of reinsurance recoverables. f. Challenges associated with non-market competitors. g. Vicissitudes of state-by-state and occasional federal regulations. h. Impact of statutory accounting on operational decision-making. i. Influence of rating agencies. B. Valuation Techniques 1. Basic analytical tools

a. Comparable company analysis. b. Comparable transaction analysis. c. Discounted cash flow analysis. 2. Analyses must be considered as a whole.

3. Need to obtain or create set of detailed financial projections.

4. Base case standalone forecast should neither be optimistic or pessimistic

SN LFV-106-07

ACTEX 2013 SOA Exam: ILA – LFV, U.S.

D-2

5. Base lone should reflect run rate before extraordinary items

6. Must consider effect of merger itself. C. Comparable Company Analysis

1. Financial information of the seller is compared to same information from peer companies to develop multiples

2. Guidelines for peer group selection a. Must be large enough to be statistically significant. b. Companies should be subject to similar regulatory, accounting and tax rules. c. Must be similar to seller’s core or dominant segments. d. Must be similar performers in similar lines of business. e. Must have similar financial and operational performance. f. Products, competitive position, geography and distribution are also considered g. Eliminate companies based on size and risk profile

3. Next step is to review range of financial, operational and market metrics.

4. Choose market multiples most significant for the sector.

5. Book value and tangible book value multiples are given considerable weight.

6. Analysis identifies high and low multiple values.

7. Bankers evaluate premium buyers may pay, based on comparable transactions.

8. Buyers will pay more for a change in control

9. Above the line financial metrics reflect value of the entire enterprise

10. Below the line financial metrics reflect value of seller’s common equity

12. Example a. Comparable company data indicates price/book value range of 1.0 to 1.5. b. Change of control premium is 20%. c. Range of prices becomes: 1.2 to 1.8 times book value. D. Comparable Transaction Analysis

1. Multiples of comparable transactions determined

a. Similar to comparable company analysis b. Adjustments made to ensure the deal value multiples reflect common equity multiples

2. Considerations a. Asset or stock transaction. b. Type of consideration paid. c. Accounting treatment. d. Tax issues. e. Time value of money when consideration is deferred.

3. Advisor will then calculate a. Price multiples to book or embedded value. b. Estimated or trailing earnings. c. EBIT, EBITDA or other financial metric.

SN LFV-106-07

ACTEX 2013 SOA Exam: ILA – LFV, U.S.

D-3

E. Discounted Cash Flows (DCF)

1. PV of future streams of after-tax cash flows in foreseeable future (generally 5 years).

2. Must factor in projected dividend payout rate, earnings estimates and ultimate book value or terminal value.

3. Ultimate book value at terminal dale is projected earnings for that year multiplied by price to earning multiple

4. Discount rate used is weighted average cost of capital (WACC).

5. Sensitivity analysis is performed on discount rate

6. Insurance companies are subject to restrictions on capital dividends; assumption is that operating income can be paid out as dividend.

F. Other Considerations 1. Historical price performance of seller’s common stock and relationship with selected companies.

2. One-day and 30-day premiums and premiums to 52-week high and 52-week average paid-in transactions.

3. Bankers generally a. Do not assume any responsibility for independent verification of information. b. Assume forecasts are reasonably prepared. c. Assume proposed merger would be consummated upon terms of agreement. d. Do not include any actuarial determinations or evaluations. e. Make no analyses of adequacy of policy reserves. f. Do not make independent evaluation of assets or liabilities. g. Do not address underlying business decision to engage in merger.

4. Common for a seller of a small block of business to perform its own valuation using rules of thumb III. The Actuarial Appraisal A. General

1. Distributable cash flow (DCF) analysis.

2. DCF = After-tax Earnings – Increase in Required Capital (RC).

3. DCF = Premium + Investment Income – Benefits – Expenses – Commissions – Increase in Statutory Reserves – Taxes – Increase in RC. 4. Not done on basis of US GAAP accounting. 5. Basis is statutory earnings and capital.

SN LFV-106-07

ACTEX 2013 SOA Exam: ILA – LFV, U.S.

D-4

B. Components of the Actuarial Appraisal Value

1. Adjusted Book Value (ABV) a. Net worth on statutory basis = statutory assets – statutory liabilities. b. Asset valuation reserve (AVR) is included in ABV. 2. Value of inforce business a. PV of future profits of in force as of valuation date. b. On the basis of statutory regulatory accounting. c. Calculated reflecting best estimate assumptions. d. Includes opportunity cost of maintaining capital in company. 3. Value of future business capacity a. PV of future profits from future business. b. Limited to 5, 10 or 20 years. 4. Adjustments are made for items not in the appraisal that add or reduce value,

including branding or market position, buyer synergies and general market conditions C. Uses of an Actuarial Appraisal

1. Appraisal report includes a. Actuarial appraisal values. b. Projection of statutory earnings and capital requirements. c. Sensitivity analyses—reasonable deviations from expected levels. 2. Potential buyer will adjust seller’s analysis a. To reflect its internal view of appropriate discount rate. b. To adjust certain assumptions based on due diligence or internal views. c. To adjust new business values for its view. d. To reflect benefits from anticipated synergies or cost savings and from one- time acquisition costs. e. To reflect specific transaction and capital structure. 3. Uses of Actuarial Appraisal a. To market company or block of business. b. Key element in establishing opening balance sheet. c. Basis of alternative accounting methodologies. d. To calculate pro forma earnings projections on a US GAAP basis. e. Basis for ongoing performance measurements after acquisition. 4. Actuarial appraisal does not reflect the company’s debt and equity in an open market 5. Purchase or sales price relevant factors a. Perspective of buyer/seller and level of confidence regarding assumptions underlying projected earnings. b. Desired rate of return and associated cost of capital. c. Degree of urgency associated with sale or acquisition. d. Economies of scale and scope associated with potential transaction. e. Significant tax or other consequences/benefits. f. Value associated with branding or other intangibles. g. One-time expenses associated with transaction. h. Other assets and liabilities at holding company level.

SN LFV-106-07

ACTEX 2013 SOA Exam: ILA – LFV, U.S.

D-5

IV. Basis for Assumptions A. General 1. Assumptions are based on some combination of a. Company’s own experience. b. Company management expectations. c. Industry experience for comparable block of business. 2. Assumptions are intended to be a. Best estimates without margin for conservatism b. Discount rate provides risk adjustment 3. Development of assumptions requires considerable actuarial judgment. B. Mortality Assumptions

1. Based on company experience compared to standard table.

2. Considerations a. Type of underwriting. b. Sales distribution. c. Treatment of substandard risks. d. Credibility of data depending on size of exposure base 3. Effect of reinsurance should be reflected; explicitly modeled if significant. 4. Mortality anti-selection reflected on LOBs with high lapse rates. 5. Sensitivity test is appropriate to reflect impact of future improvement. C. Morbidity Assumptions 1. Based on company experience compared to standard table. 2. Considerations a. Type of underwriting. b. Sales distribution. c. Product characteristics. d. Ability of company to meet target loss ratios D. Persistency Assumptions 1. Considerations a. Product type and specific product design. b. Distribution system and sales technique. c. Lapse include voluntary lapse, lapse without value and premium suspension 2. May review sample illustrations to determine persistency at time of sale. 3. May need to consider shock lapses expected as result of transaction.

SN LFV-106-07

ACTEX 2013 SOA Exam: ILA – LFV, U.S.

D-6

E. Investment Returns and Spread Assumptions 1. May be based on either a. An assumed rate of return. b. An explicit model of existing asset portfolio with future investments.

2. Model based on a. Income from a seriatim list of assets with all characteristics on a statutory basis b. Expected defaults are based on quality of portfolio c. Investment expense is a reduction to gross yields d. To extent assets are sold or prepaid, capital gains and losses amortized in IMR 3. Reinvestments are generally based on current practices. 4. May be based on single underlying yield curve assumed to remain constant. 5. Future crediting rates are based on management strategy, competitive pressures and contract guarantees 6. Show impact of interest rate movements on the actuarial appraisal values 7. Stochastic testing is sometimes used when block is highly interest sensitive F. Operating Expenses 1. Generally determined based on one of the following

a. Fully absorbed unit expenses. i. Reflects an implicit assumption that expense reductions are not available on

normal growth of business ii. Used by companies too large to obtain further economies of scale iii. Appropriate if expense movements are expected to be passed back to

policyholders b. Target unit expenses and an unallocated expense: most common approach.

c. Target unit expenses without an unallocated expense. 2. Target unit expenses may be based on some combination of a. Company plan targets for fully allocated expenses at some future point. b. Company assumptions used in internal new business pricing analysis. c. Representative industry levels of target expenses (best practices). d. Representative unit expense levels charged by TPA with appropriate loading. 3. Projection of amount and period of unallocated expense is key item. 4. Marginal unit expenses are another alternative for projecting cost levels. 5. Expenses are important aspect of buy-side analysis. 6. Buyers add in a level of fixed cost and overhead allocation

SN LFV-106-07

ACTEX 2013 SOA Exam: ILA – LFV, U.S.

D-7

G. Discount Rate Determination

1. Common practice to illustrate range of reasonable discount rates which reasonably Reflect the risks inherent in the realization of earnings

2. It is generally viewed as an unleveraged not an equity discount rate because it is applied to earnings before debt cost 3. Capital Asset Pricing Model (CAPM)

a. Fundamental equation is r = rf + β (rm – rf), where

i. r = expected rate of return on acquisition.

ii. rf = risk-free rate of return.

iii. rm = expected rate of return for market as a whole.

iv. β = measure of risk of company relative to market as a whole. b. Reflecting leverage explicitly in CAPM results in r = rD x [D/(D+E)] + [E/(D+E)] x [rf + βE (rm – rf)], where i. r = weighted average cost of capital (WACC).

ii. rD = required return on debt.

iii. βE = beta of company’s stock.

iv. D = market value of company’s debt.

v. E = market value of company’s equity.

c. Under CAPM, WACC should be used as discount rate. d. Companies create value when the PV is positive after WACC discounting

e. Uncertainties should be captured in cash flows not in discount rate. f. Discount rates should float with movements in risk-free rate.

4. Internal Company Targets: Current hurdle rates and long-term targets may be used.

5. Cost of Funds for Transactions. a. Can be used as discount rate b. May be low if capital is trapped or not needed in other operations 6. M&A Marketplace Discount Rates a. They varied over time reflecting i. Supply and demand of sellers and buyers. ii. Nature of buyers and cost of financing, such as public debt markets. iii. Type of business being sold. b. In the 1980s and early 1990s: 15% or higher. c. Late 1990s: 10%-12%. d. 2002-2003: Slight increase.

SN LFV-106-07

ACTEX 2013 SOA Exam: ILA – LFV, U.S.

D-8

H. Cost of Required Capital (RC) 1. In late 1990s to early 1990s, actuarial appraisals reflected RC of 200%-250% of

RBC-CAL (Risk based capital – company action level).

2. Cost of Capitalt = RCt-1 x (discount rate – after-tax earnings ratet).

3. Appraisal Cost of Capital = Net Present Value at discount rate of Cost of Capitalt.

4. Total actuarial value = PV of after-tax earnings + Opportunity cost of capital.

5. Actuarial value can likewise be defined as PV of distributable earnings.

6. Demonstration: NPV (Distributable Earningst) =

a. Excess Capital0 + NPV (After-tax Earningst – Increase in RCt).

b. NPV (After-tax Earnings on the Businesst) + Excess Capital0 + NPV (After-tax Earnings on Capitalt) – NPV (Increase in RCt). c. NPV (After-tax Earnings on the Businesst) + Excess Capital0 + NPV (RCt-1 x it) – [NPV (RCt) – NPV (RCt-1)]. d. NPV (After-tax Earnings on the Businesst) + Excess Capital0 + NPV (RCt-1 x it) – [(1+d) NPV (RCt-1) – RC0 - NPV (RCt-1)]. e. NPV (After-tax Earnings on the Businesst) + Excess Capital0 + RC0 – NPV [RCt x (d – it)]. f. Value of Inforce and Future Business + Adjusted Book Value – Cost of Required Capital, where i. it = After-tax investment earnings rate on capital. ii. d = discount rate. I. Taxes 1. Federal income taxes = Tax rate (35%) x Taxable income. 2. Taxable income = Statutory pre-tax income adjusted for a. Difference between statutory and tax reserves. b. DAC proxy tax. c. Interest maintenance reserve (IMR). d. Asset basis differences; e.g. troubled securities, dpereciation. e. Dividends received deduction (DRD).

SN LFV-106-07

ACTEX 2013 SOA Exam: ILA – LFV, U.S.

D-9

V. Components of the Actuarial Appraisal (must be credible and transparent) A. Adjusted Book Value (ABV) 1. Capital and surplus. 2. Asset Valuation Reserve (AVR), considered surplus because a. Changes flow through surplus account, not net income. b. It counts as capital for purposes of RBC ratio. 3. Interest Maintenance Reserve (IMR) on a discounted basis. 4. Deferred tax asset. Deducted from ABV 5. Realizable value of non-admitted assets. 6. Surplus notes and other debt a. Debt at the holding company level not impact appraisal directly. b. Internal surplus notes valued as surplus. c. External surplus notes are included in appraisal or deducted. 7. Mark-to market on assets allocated to ABV. B. Existing Business Value

1. Value determined by developing detailed models.

2. Models project statutory earnings over lifetime of business.

3. Projection period determined such that extending it further would not materially affect appraisal

4. Typical projection period for individual life and annuity business is 30 years.

5. Minor blocks of business or ancillary coverages: Reflected in an aggregate manner.

6. In developing model, review ability of model to validate historical experience. C. Future Business Value 1. Valuation is less certain due to uncertainty over a. New business volumes to be produced in the future. b. Expected profit margins embedded in future pricing of products. c. Uncertainty in volume produced and profitability of new business

2. New Business Production

a. Based on marketing forecasts. b. Should indicate specific markets for expansion c. May be appropriate to have alternative production scenarios.

d. Consider changes in company ratings and distribution system.

SN LFV-106-07

ACTEX 2013 SOA Exam: ILA – LFV, U.S.

D-10

3. Probability of Future Business a. Usually based on pricing assumptions. b. Can be compared to general market conditions and profitability expectations. 4. Value of New Business: Traditionally reflected in one of 2 ways a. Actuarial value of future business is reflected under given production plan for specified number of years; advantages of this approach include i. Explicitly reflects management’s plan over planning period. ii. Allows for certain assumptions to change over time. iii. Produces a projected statutory income statement facilitating analysis. b. Actuarial value of future business is illustrated for just one year of issue and then multiplied by a multiplier; advantages of this approach include

i. Allows user of report to easily adjust for different growth rates, years of new business, etc.

ii. Provides straightforward basis for comparison of prices paid in transactions. c. Method a is typically used in US.

d. Method b is often used in emerging markets and in UK.

e. Multiplier may vary over time based on i. Business outlook. ii. Company and region. f. Good will premium i. Troubled companies have little goodwill; ii. High quality companies have substantial goodwlll VI. Individual Life & Annuity Product Line Issues A. Life Insurance 1. Possible funding buckets in UL models a. Premium-paying vs. non-premium-paying. b. Funding level split based on target premium. c. Funding level split based on projected charges. d. Depending on product design, funding level can be very sensitive 2. Assumptions of particular importance to life insurance business

a. Mortality improvement, from population improvement and improved underwriting.

b. Reinsurance: Consider recapture provisions, likelihood of reinsurers to change rates, or other items that may affect value of block.

c. Reserve issues: Reserves related to long-term guarantees and secondary guarantees may be more complex to model; insurers often reinsure deficiency reserves.

d. Low interest rate environment. e. Non-guaranteed elements—reflect implied guarantees in illustrations, sales

literature an company practice

SN LFV-106-07

ACTEX 2013 SOA Exam: ILA – LFV, U.S.

D-11

B. Fixed Deferred Annuities 1. Same as life insurance blocks except very little renewal premium. 2. Risks causing most concern a. Disintermediation and reinvestment risk. b. Ability to achieve required spread between earned and credited rates. 3. Often include analysis of impact on economic value of alternative interest scenarios. 4. Deterministic or stochastic scenarios may be used. 5. Characteristics of deterministic and stochastic analysis a. Deterministic analysis may point to specific interest exposures that would be buried in stochastic analysis. b. Stochastic analysis may do a more complete job at valuing options in products. c. Extreme scenarios do not provide a reasonable range for the appraisal 6. Assumptions regarding lapse rates are important driver of actuarial values. C. Fixed Immediate Annuities 1. Common to use seriatim projection and model does not need to be dynamic.

2. Primary risk is reinvestment risk.

3. Product is non-surrenderable

4. Mortality risk on substandard annuities may lack credible experience.

5. Projected future mortality improvement should be considered. D. Variable Annuities

1. Primary risk relates to future policyholder investment returns.

2. Risk associated with market movements should be sensitivity tested

3. Some carriers have implemented some form of hedging to limit exposure to market movements.

4. Embedded options or guarantees may be separately valued through option pricing techniques.

5. General account option requires similar considerations to those on fixed deferred annuities.

6. Consideration should be given to option policyholders have to move funds from general account to separate account

SECTION G

PROFESSIONAL STANDARDS

LOMBARDI, Chapter 15

ACTEX 2014 SOA Exam: ILA– LFV, U.S.

G-1

LOMBARDI, CHAPTER 15, THE VALUATION ACTUARY IN THE UNITED STATES

I. Introduction

A. In December 1990, the valuation actuary concept was introduced in Model Standard Valuation Law (SVL).

B. 1990 amendment was based on NY Regulation 126.

C. Required every life insurance company unless exempted to submit actuarial opinion that considers liabilities and that cash follows make good and sufficient provision for obligations

D. Actuarial Standards Board (ASB) of the American Academy of Actuaries (AAA) does not require rigid standards and endorses the “disclosed defendable deviation” approach

II. Model Standard Valuation Law

A. General Requirement

1. Requires an annual opinion of actuarial analysis of reserves and assets held in supportof reserves.

2. From a qualified actuary who is appointed to issue the opinion

3. As to whether reserve re computed appropriately

4. Based on assumptions that satisfy contract provisions and

5. Consistent with prior reported amounts and

B. Appointed Actuary

1. Member in good standing of American Academy of Actuaries

2. Appointed or retained by the Board of Directors

2. Qualified to sign statements of actuarial opinion for life and health companies.

3. Meets certain requirements set forth by commissioner.

C. Actuarial Opinion of Reserves

1. Reserves are computed appropriately.

2. Reserves are based on assumptions that satisfy contractual provisions.

3. Reserves are consistent with prior reported amounts.

4. Reserves comply with applicable laws of the state.

D. Professional Liability

1. Model SVL attempts to exempt actuary from third party liability.

2. In some states, actuary is not exempted.

E. Supporting Memorandum

1. Must be prepared in support of actuarial opinion.

2. Is a confidential document.

LOMBARDI, Chapter 15

ACTEX 2014 SOA Exam: ILA – LFV, U.S.

G-2

III. Actuarial Opinion and Memorandum Model Regulation

A. Prescribes actuarial opinion and actuarial memorandum requirements.

B. Prescribes rules governing appointment of appointed actuary.

C. Prescribes guidance as to meaning of adequacy of reserves.

D. Actuarial Opinion Requirements; an actuarial opinion shall consist of:

1. Paragraph identifying appointed actuary and qualifications.

2. Scope of opinion, tabulation of reserves, method of analysis and reserves not analyzed.

3. Extent to which appointed actuary has relied upon others who must also sign.

4. Opinion as to adequacy of assets held in support of liabilities.

5. Additional paragraphs to qualify opinion, disclose inconsistencies and briefly stateassumptions.

E. Actuarial Memorandum Requirements

1. Liability sectiona. Description of each product including marketing and underwriting.b. Source for liabilities in force.c. Policy reserve valuation methods and assumptions.d. Investment reserves.e. Reinsurance agreements.f. Explicit or implicit guarantees by general account for separate account.g. Documentation of assumptions used in asset adequacy analysis.

2. Asset sectiona. Description of asset portfolios, including risk profile on quality, distribution

and type of assets.b. Source for assets held in support of liabilities.c. Assumptions about future purchase and sales.d. Bases of asset valuation.e. Documentation of assumptions.

3. Analysis sectiona. Methodology used to perform asset adequacy analysis.b. Rationale for inclusion or exclusion of different blocks of business.c. Rationale for degree of rigor in analyzing different blocks of business.d. Criteria for determining asset adequacy.e. How reinsurance was handled.f. Whether impact of federal income taxes was considered.

4. Summary of material changes section: Changes in methods, procedures orassumptions from the prior year

5. Conclusion and Statement of conformity to Standards of Practice of the ASB.

LOMBARDI, Chapter 15

ACTEX 2014 SOA Exam: ILA– LFV, U.S.

G-3

IV. Actuarial Standards of Practice No. 22

A. Guidance for opinion prepared pursuant to applicable law such as

1. Law based on model SVL amended by NAIC in 1990 in conjunction with the ActuarialOpinion and Memorandum Regulation.

2. Law based on NAIC’s Synthetic Guaranteed Investment Contracts Model Regulation.

3. Law based on NAIC’s Separate Accounts Funding Guaranteed Minimum Benefitsunder Group Contracts Model Regulation.

4. Other applicable laws.

B. Items to consider in making judgment as to whether cash flow testing is required

1. Sensitivity of liability cash flows to changing investment environments.

2. Composition of assets supporting reserves.

3. Any significant reinvestment risk to which liabilities expose company.

C. Cash flow testing is not always required

D. Situations where cash flow testing may not be necessary

1. A gross premium valuation has shown results insensitive to economic changes.

2. Valuation actuary demonstrates that experience will be less severe than reservesprovide for.

3. Products where cash flows are insensitive to changes in economic conditions due toproduct design or investment strategy.

4. Short-term products.

V. Required Analysis

A. Model regulation no longer prescribes 7 scenarios similar to those in NY Regulation 126.

B. However, most actuaries continue this practice.

C. 2004 NY Regulation 126 required interest scenarios

1. Level.

2. Uniformly increasing 0.5% over 10 years and then level.

3. Uniformly increasing 1% over 5 years, decreasing 1% over 5 years and then level.

4. 3% pop-up and then level.

5. Uniformly decreasing 0.5% over 10 years and then level.

6. Uniformly decreasing 0.5% over 5 years, increasing 0.5% over 5 years and then level.

7. 3% pop-down and then level.

LOMBARDI, Chapter 15

ACTEX 2014 SOA Exam: ILA – LFV, U.S.

G-4

D. All rates are subject to minimum interest rate.

E. Additional analysis may be deemed necessary by appointed actuary.

F. Considerations

1. Point in time or period over which starting rates are based.

2. Shape of ultimate yield curve.

3. Application of minimum rate constraint.

G. Starting rates should be based on applicable investment yields close to the valuation date

H. Shape of yield curve

1. Decision must be made as to whether to keep the shape of the yield curve or assume theshape returns to normal

2. Reasons to maintain shape of starting yield curvea. Selection of shape of ultimate yield curve would be somewhat arbitrary.b. Shape may be dependent on level of rates suggesting selecting not one but a

multitude of curves.c. Desire for simplicity.

3. No regulatory or professional standards identify the number of scenarios that should betested

4. For a large number of scenarios tested, the failure of a mall percentage may not indicatethe need for additional reserves

SN LFV-804-07

ACTEX 2013 SOA Exam: ILA – LFV, U.S.

G-5

SN LFV-804-07 NAIC ACTUARIAL OPINION AND MEMORANDUM REGULATION

I. Purpose is to prescribe A. Requirements for statements of actuarial opinion (SAO) submitted in accordance with SVL and for memoranda in support thereof.

B. Rules applicable to appointment of appointed actuary.

C. Guidance as to meaning of “adequacy of reserves.” II. Scope

A. All life insurance companies and fraternal benefit societies doing business or authorized to reinsure business in this State.

B. Regulation shall be applicable to all annual statements filed with commissioner after effective date of this regulation.

C. Regulation should be applied in a manner that allows the appointed actuary to utilize professional judgment in performing an asset adequacy analysis in developing an actuarial opinion

D. However, the commissioner may specify explicit methods of analysis and assumptions when necessary for an acceptable actuarial opinion

E. Statement of opinion on adequacy of reserves shall be required each year. III. Definitions

A. Actuarial opinion—Opinion of the appointed actuary regarding the adequacy of reserves

B. Actuarial Standards Board (ASB)—Board established by the American Academy of Actuaries to promulgate standards of actuarial practice

C. Annual Statement—annual financial statement an insurance company files with the state

D. Appointed Actuary—individual appointed or retained to provide the actuarial opinion and supporting memorandum

SECTION Q

REVIEW QUESTIONS

ACTEX 2014 SOA Exam: LFV, U.S.

Introductory Note

This section of the study manual contains an array of review questions covering the entire syllabus. These questions were written to serve as an aid in assessing your understanding of the material after you have completely covered it through your studies. It is unlikely that you would see questions of this type on the actual exam, since those questions are developed with an eye toward application of multiple parts of the syllabus in actual job situations.

While these questions were not developed as possible exam questions by themselves, it is entirely possible that you could see some of these questions as parts of actual exam questions.

REVIEW QUESTIONS

ACTEX 2014 SOA Exam: LFV, U.S.

Q-1

Source: Atkinson-Dallas, Chapter 16, Financial Management Question 1 (83 Points) Describe the various components of:

(a) Market risk (b) Credit risk (c) Pricing risk

REVIEW QUESTIONS

ACTEX 2014 SOA Exam: LFV, U.S.

Q-29

Source: Tillers, Chapter 13, GAAP Accounting for Reinsurance Question 1 (9 Points) (a) List the primary elements of modeling the development of GAAP factors by a reinsurance

company for AAP reserves and DAC.

REVIEW QUESTIONS

ACTEX 2014 SOA Exam: LFV, U.S.

Q-82

Sources: ASOP 41, Actuarial Communications Lombardi, chapter 15 LFV-804-07, AOMR Integrated Question 2 (67 Points) As the appointed actuary for a life insurance company preparing your current year opinion, you have access to the following company experts:

James Bonds, VP of Investments Henry Hardware, VP of Administration and Systems Fred Johnson, Actuarial Student reporting to you

Henry Hardware is on vacation and cannot be reached before you can file your opinion. Fred Johnson is willing to certify the accuracy of the reserves. Prepare you opinion for this year.

SECTION S

SOLUTIONS TO

REVIEW QUESTIONS

REVIEW SOLUTIONS

ACTEX 2014 SOA Exam: LFV, U.S.

S-1

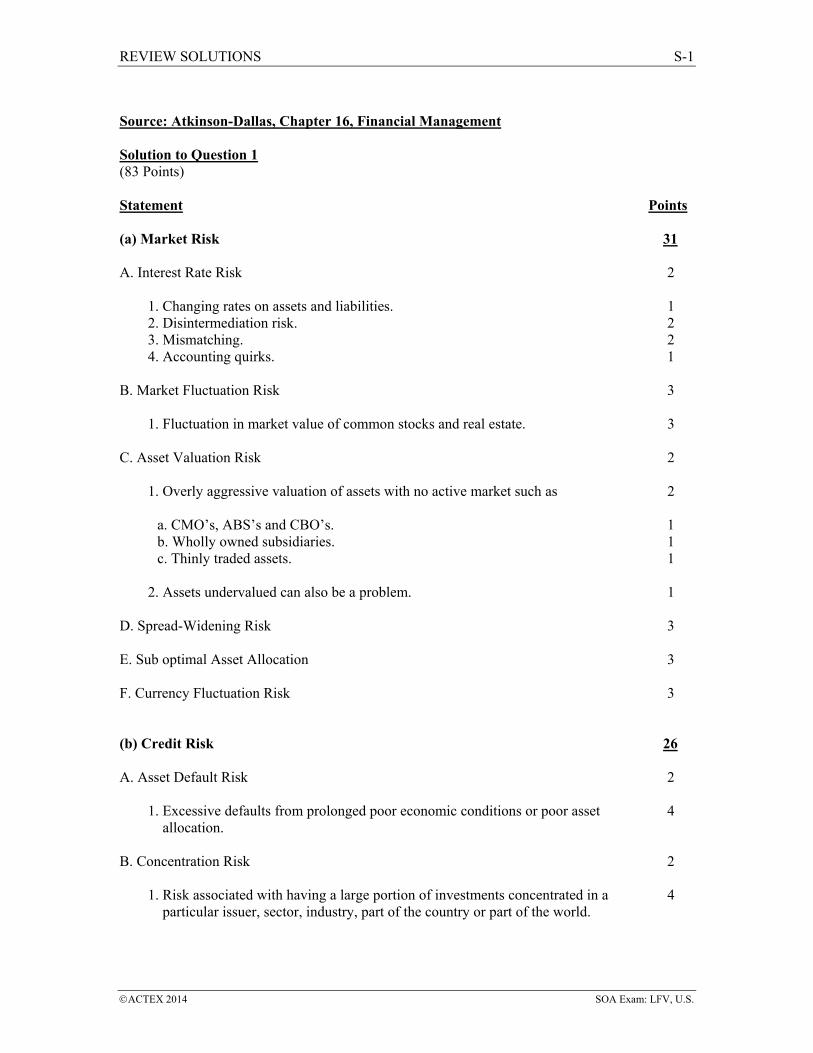

Source: Atkinson-Dallas, Chapter 16, Financial Management

Solution to Question 1 (83 Points)

Statement Points

(a) Market Risk 31

A. Interest Rate Risk 2

1. Changing rates on assets and liabilities. 1 2. Disintermediation risk. 2 3. Mismatching. 2 4. Accounting quirks. 1

B. Market Fluctuation Risk 3

1. Fluctuation in market value of common stocks and real estate. 3

C. Asset Valuation Risk 2

1. Overly aggressive valuation of assets with no active market such as 2

a. CMO’s, ABS’s and CBO’s. 1 b. Wholly owned subsidiaries. 1 c. Thinly traded assets. 1

2. Assets undervalued can also be a problem. 1

D. Spread-Widening Risk 3

E. Sub optimal Asset Allocation 3

F. Currency Fluctuation Risk 3

(b) Credit Risk 26

A. Asset Default Risk 2

1. Excessive defaults from prolonged poor economic conditions or poor asset 4 allocation.

B. Concentration Risk 2

1. Risk associated with having a large portion of investments concentrated in a 4 particular issuer, sector, industry, part of the country or part of the world.

REVIEW SOLUTIONS

ACTEX 2014 SOA Exam: LFV U.S.

S-2

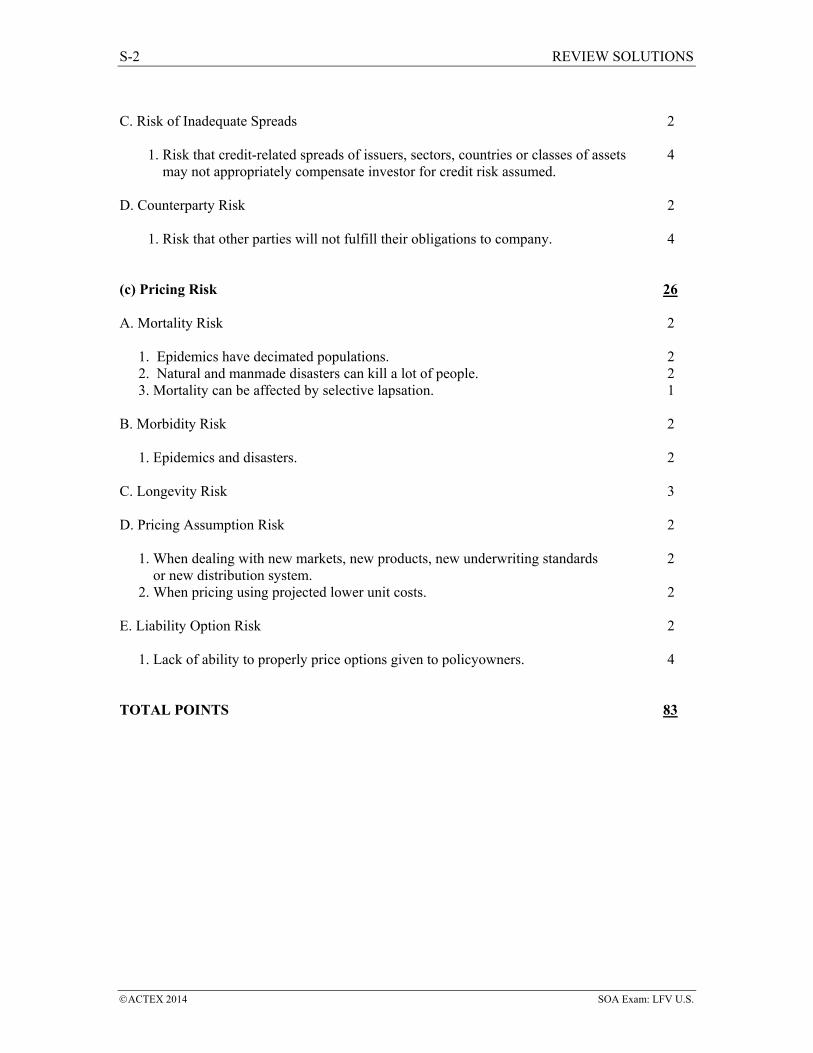

C. Risk of Inadequate Spreads 2

1. Risk that credit-related spreads of issuers, sectors, countries or classes of assets 4 may not appropriately compensate investor for credit risk assumed.

D. Counterparty Risk 2

1. Risk that other parties will not fulfill their obligations to company. 4

(c) Pricing Risk 26

A. Mortality Risk 2

1. Epidemics have decimated populations. 2 2. Natural and manmade disasters can kill a lot of people. 2 3. Mortality can be affected by selective lapsation. 1

B. Morbidity Risk 2

1. Epidemics and disasters. 2

C. Longevity Risk 3

D. Pricing Assumption Risk 2

1. When dealing with new markets, new products, new underwriting standards 2 or new distribution system.

2. When pricing using projected lower unit costs. 2

E. Liability Option Risk 2

1. Lack of ability to properly price options given to policyowners. 4

TOTAL POINTS 83

REVIEW SOLUTIONS

ACTEX 2014 SOA Exam: LFV, U.S.

S-3

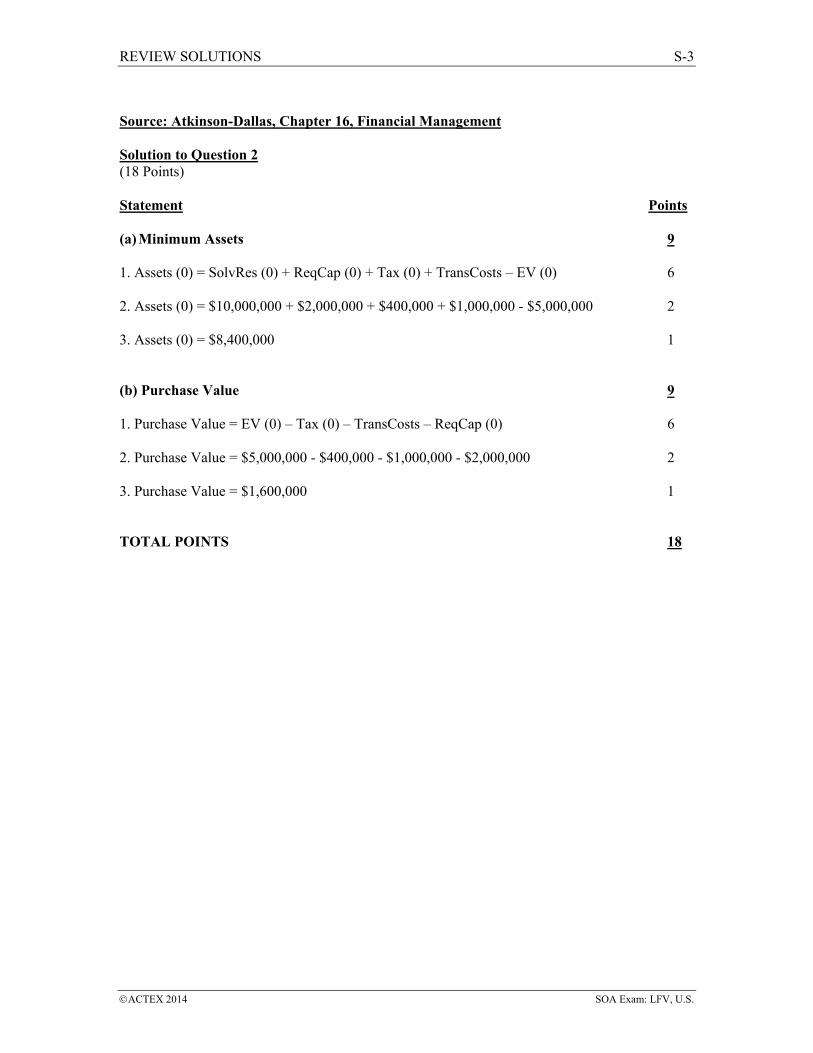

Source: Atkinson-Dallas, Chapter 16, Financial Management

Solution to Question 2 (18 Points)

Statement Points

(a) Minimum Assets 9

1. Assets (0) = SolvRes (0) + ReqCap (0) + Tax (0) + TransCosts – EV (0) 6

2. Assets (0) = $10,000,000 + $2,000,000 + $400,000 + $1,000,000 - $5,000,000 2

3. Assets (0) = $8,400,000 1

(b) Purchase Value 9

1. Purchase Value = EV (0) – Tax (0) – TransCosts – ReqCap (0) 6

2. Purchase Value = $5,000,000 - $400,000 - $1,000,000 - $2,000,000 2

3. Purchase Value = $1,600,000 1

TOTAL POINTS 18