Embed Size (px)

Citation preview

Press conference: "Funds Outlook for 2012"

Steigenberger Hotel Herrenhof

Vienna, 24 January 2012

Funds Outlook 2012

Your dialogue partners

Heinz BEDNAR Chairman of the Managing Board (CEO)

Harald EGGERHead of the Investment Division (CIO)

Gerhard WINZER Chief economist

Review, update on investment policy

Heinz Bednar,

Chairman of the Managing Board (CEO)

Market review

Almost every asset class delivered positive returns in December

All markets were positive over the last 3 months as well, apart from CEE and eurozone bonds

But the negative trend still prevailed on the equity markets last year

Source: ERSTE-SPARINVEST, Datastream

-3M -12M

-3M -12M

Equities, developed markets 7.90% -5.00%

Equities, emerging markets 4.90% -12.50%

Inflation-indexed bonds -2.30% -1.10%

EUR government bonds -0.60% 3.30%

EUR investment-grade corporate bonds 1.30% 2.00%

EUR high-yield corporate bonds 4.30% -2.50%

USD government bonds 1.00% 10.00%

USD investment-grade corporate bonds 1.70% 8.00%

USD high-yield corporate bonds 6.00% 4.30%

US mortgage-backed securities 0.90% 6.70%

GBP government bonds 5.50% 17.40%

JPY government bonds 0.70% 3.20%

CEE government bonds -1.40% 1.40%

Corporate bonds, emerging markets, hard currency 5.40% 2.40%

Government bonds, emerging markets, hard currency 4.00% 6.80%

Government bonds, emerging markets, local currency 3.80% 1.50%

EUR money market 0.40% 1.30%

"Sustainable" experience

Fund volume based on sustainability criteria currently totals approximately

EUR 630 million

Funds Outlook 2012

"Cluster munitions" removed from portfolios

- Since 1 January 2012 there are no "cluster munitions" in the portfolios managed by ERSTE-SPARINVEST

- This is in line with the UN "Oslo Convention"

- Wolfgang Pinner appointed as "Chief Sustainability Investment Officer"

Hunting for returns with fund investment strategies for 2011 21.01.2011 - Page 6

Sovereign debt crisis: fragile, below-average recovery

Gerhard Winzer,

Chief economist

High sovereign debt

Sovereign debt growing

faster than nominal GDP.

Solutions:

real economic growth nominal economic growth insolvency transfers financial repression

=> stress in financial sector Crisis of confidence

Source: IMF, Bloomberg

Staatsschulden, % BIP

0

25

50

75

100

125

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Entwickelte Volkswirtschaften

Zentral- und Osteuropa

Gemeinschaft unabhängiger Staaten

Emerging Asien

Lateinamerika

Renditen von Staatsanleihen, 10 Jahre, %

0

1

2

3

4

5

6

7

8

9

10

11

12

01/99 01/00 01/01 01/02 01/03 01/04 01/05 01/06 01/07 01/08 01/09 01/10 01/11 01/12

UngarnItalienDeutschland

1) Fiscal and transfer union including federal bonds: not yet => Mitigating free-rider problem (moral hazard) => high consolidation pressure so far: expanded growth and stability pact (rules-based) required: ex ante approval of budget

2) Common economic policy: pro-cyclical fiscal policy Imbalances (current account, competition)

3) Provision of emergency liquidity (lender of last resort): ECB: so far only for banks (official) => Countries: EFSF, ESM, IMF

Moving slowly towards fiscal union?The less we see points one and two fulfilled, the more the pressure will mount on the ECB to prevent a collapse of EMU.

Does the euro have a future?

Fragile, below-average recovery Global slowdown in economic activity. Weak growth for 2012. Risks are on the downside.

Eurozone: escalation China: "hard" landing USA: budget consolidation Oil price, geopolitical situation (Iran)

Emerging Markets still have great potential

stable or improving credit ratings appreciating currencies

De-coupling not an option Global imbalances slowly evening out

Source: Erste-Sparinvest, IMF

BIP-Wachstum, %, pro Jahr

-4

-2

0

2

4

6

8

10

2004 2005 2006 2007 2008 2009 2010 2011 2012

Emerging Markets

Entwickelte Volkswirtschaften

BIP pro Kopf, Kaufkraftparitäten, USD

0

10,000

20,000

30,000

40,000

En

twic

kelt

eV

olk

swir

tsch

afte

n

Zen

tral

- u

nd

Ost

euro

pa

Gem

ein

sch

aft

un

abh

äng

iger

Sta

aten

Em

erg

ing

Asi

en

AS

EA

N-5

Lat

ein

amer

ika

Inflation low and falling

Low inflation / deflationary pressure in developed economies: Debt reduction Low utilisation of resources

Inflationary risks in developed economies: Growing supply of money

but demand for money rising too central bank could reduce money supply if

need be.

Emerging markets (sustained currency appreciation and higher prices) Sustained growth in commodity prices Tax hikes, higher regulated prices

Konsumentenpreisinflation, %, pro Jahr

0

2

4

6

8

2004 2005 2006 2007 2008 2009 2010 2011 2012

Emerging Markets

Entwickelte Volkswirtschaften

Source: ERSTE-SPARINVEST

Very loose monetary policy

Zero / low-interest policy Quantitative easing: purchase of assets (government and bank bonds) Provision of emergency liquidity for banks and governments (lender of last resort) Communication: higher transparency

This means the debt problem dominates inflation targets in many developed economies.

Emerging markets: scope for moderate interest cuts exception: countries with risks regarding inflation and currency depreciation

Source: Bloomberg, ECB

EZB, Gesamtvermögen, Euro, Milliarden

0

500

1,000

1,500

2,000

2,500

3,000

01/99 01/00 01/01 01/02 01/03 01/04 01/05 01/06 01/07 01/08 01/09 01/10 01/11 01/12

EWU, Bankensektor, Kredite, Milliarden

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

11000

06/99 06/00 06/01 06/02 06/03 06/04 06/05 06/06 06/07 06/08 06/09 06/10 06/11

Assessment of bond and equity markets

Heinz Bednar,

Chairman of the Management Board (CEO)

Harald Egger,

Chief Investment Officer (CIO)

Asset Allocation 2012

Note: analysis as of January 2012; changes may be made at any timeNote: analysis as of January 2012; changes may be made at any time

unattraktivwenig

attraktiv neutral attraktivsehr

attraktiv

Euro Staatsanleihen AAA-AA mEuro Staatsanleihen AAA-BBB mUS MBS mInvestment Grade Unternehmensanleihen EUR mInvestment Grade Unternehmensanleihen USD mHigh Yield Unternehmensanleihen EUR mHigh Yield Unternehmensanleihen USD mStaatsanleihen EM, Hartwärung mStaatsanleihen CEE mUnternehmensanleihen EM, Hartwährung mAktien, entwickelte Märkte mAktien EM mGold mImmobilien mRohstoffe m

Funds Outlook 2012

Eurozone: Government bonds

- Government debt crisis is pushing yields on top-quality government bonds to extremely low levels

- What is more, the downturn in economic activity, declining inflation and interest-rate cuts are keeping yields persistently low.

Source: Thomson Reuters Datastream

10jährige Rendite Deutschland

2007 2008 2009 2010 2011 20121.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

GERMANY GOVERNMENT BOND 10 YEARPrognose Erste Research

Funds Outlook 2012

Corporate bonds – investment grade

- Stable corporate figures

- Low interest rates, high liquidity

- Low bankruptcy rates

- Increased uncertainty is priced in

- Moderate economic growth in USA

- Mild recession in eurozone

- Corporate bonds: USA more attractive than eurozone

Source: Thomson Reuters Datastream

2007 2008 2009 2010 20113

4

5

6

7

8

3

4

5

6

7

8

2007 2008 2009 2010 201180

100

120

140

80

100

120

140

BOFA ML EMU CORP. (E) - RENDITEBOFA ML EMU CORP. (E) - PERFORMANCE

EUR corporate bonds IG: yield level and performance (-5 years) EUR corporate bonds IG: yield level and performance (-5 years)

Funds Outlook 2012

Emerging market bonds in hard currency

- Sovereign debt as percentage of nominal GDP is far lower than in developed economies on average.

- Chinese economic growth will be somewhat more moderate, but a "hard" landing can be avoided.

- EM credit ratings continue to improve. In the long run this means stable or falling yield spreads on credit risk.

Source: Thomson Reuters Datastream

2007 2008 2009 2010 20110

2

4

6

8

10

12

0

2

4

6

8

10

12

2007 2008 2009 2010 201150

100

150

50

100

150

JPM EMBI GLB.DIVERS COMPOSITE - RENDITEJPM EMBI GLB.DIVERS COMPOSITE - SPREADJPM EMBI GLB.DIVERS COMPOSITE - PERFORMANCE

Emerging market bonds, hard currencies: yield level and performance (-5 years) Emerging market bonds, hard currencies: yield level and performance (-5 years)

Hunting for returns with fund investment strategies for 2012 21.01.2011 - Page 18

Emerging market bonds in local currency

- Emerging markets (EM) still have great potential. This means real effective exchange rates will appreciate in the long run (by means of higher prices and stronger currencies) and average interest rates will also be higher than in the eurozone.

- With some exceptions, economic policies in many countries have greater room for manoeuvre than developed economies to compensate for contracting economic activity

Source: Thomson Reuters Datastream

2007 2008 2009 2010 20116.0

6.5

7.0

7.5

8.0

8.5

9.0

6.0

6.5

7.0

7.5

8.0

8.5

9.0

2007 2008 2009 2010 2011

100

120

140

160

100

120

140

160

JPM GBI-EM GLOBAL DIV in EUR - RENDITEJPM GBI-EM GLOBAL DIV in EUR - PERFORMANCE

Emerging market bonds, local currencies: yield level and performance (-5 years) Emerging market bonds, local currencies: yield level and performance (-5 years)

Funds Outlook 2012

Central and Eastern European bonds

- Economic growth in Central and Eastern Europe (including Turkey and Russia) will slow down considerably this year to roughly 2.4%, while the long-term growth potential sits around 4%.

- The Achilles heels of the CEE region are the high external debt (66% of GDP) and the current account deficit (5.4% of GDP).

- The crucial issue in Hungary is whether an agreement will be reached this year with the IMF on a loan.

Source: Thomson Reuters Datastream

2007 2008 2009 2010 20114.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

2007 2008 2009 2010 201180

100

120

140

80

100

120

140

BOFA ML EMERGING EURO GVT (E) - RENDITEBOFA ML EMERGING EURO GVT (E) - PERFORMANCE

CEE bonds: yield level and performance (-5 years) CEE bonds: yield level and performance (-5 years)

Equities as early indicators

Global equities (MSCI World in EUR)

Source: Bloomberg

The MSCI World Index (€) has made up the losses suffered in the last quarter of 2011 (mainly thanks to the strong dollar).

It is still on an upward trend.

This year we expect to see continued gains in prices, but there is also likely to be greater volatility.

700,00

750,00

800,00

850,00

900,00

950,00

1000,00

1050,00

15.0

1.20

10

15.0

2.20

10

15.0

3.20

10

15.0

4.20

10

15.0

5.20

10

15.0

6.20

10

15.0

7.20

10

15.0

8.20

10

15.0

9.20

10

15.1

0.20

10

15.1

1.20

10

15.1

2.20

10

15.0

1.20

11

15.0

2.20

11

15.0

3.20

11

15.0

4.20

11

15.0

5.20

11

15.0

6.20

11

15.0

7.20

11

15.0

8.20

11

15.0

9.20

11

15.1

0.20

11

15.1

1.20

11

15.1

2.20

11

15.0

1.20

12

Funds Outlook 2012

Markets undervalued – what is priced in?

Fair Value- USA

10

100

1000

10000

-60,0%

-40,0%

-20,0%

0,0%

20,0%

40,0%

60,0%

80,0%Abw. FV

Abw. FV

MSCI USA U$ - PRICE INDEX

FV

MSCI USA U$ - PRICE INDEX

FV

Source: own calculations, Datastream

"Fair value" model for US equities

Businesses are very profitable

Source: ERSTE-SPARINVEST, own calculations, as of end-2010

*) ROE = return on equity

6

8

10

12

14

16

Dez

.91

Dez

.92

Dez

.93

Dez

.94

Dez

.95

Dez

.96

Dez

.97

Dez

.98

Dez

.99

Dez

.00

Dez

.01

Dez

.02

Dez

.03

Dez

.04

Dez

.05

Dez

.06

Dez

.07

Dez

.08

Dez

.09

Dez

.10

Dez

.11

RoE durschn. RoE

Source: own calculations, DatastreamFunds Outlook 2012

Powerful recovery in return on equity in 2011 *)

Markets price in flat profits

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

Jän

.76

Jän

.78

Jän

.80

Jän

.82

Jän

.84

Jän

.86

Jän

.88

Jän

.90

Jän

.92

Jän

.94

Jän

.96

Jän

.98

Jän

.00

Jän

.02

Jän

.04

Jän

.06

Jän

.08

Jän

.10

EPS Gr 1Y

S&P 1Y

Annual earnings growth (corporate profits) compared to rolling 1-year performance of S&P Index

Source: own calculations, Datastream, January 2012

... priced attractively to "fair"

Indicators of global equity markets

Source: ERSTE-SPARINVEST, Bloomberg, January 2012

P/E Dvd YldS&P 500 13,6 2,07NASDAQ 23,27 1,04BRAZIL BOVESPA 9,83 3,82

Euro Stoxx 50 11,25 4,97FTSE 100 10,08 3,82CAC 40 9,53 4,77DAX 10,61 3,83IBEX 8,99 5,57SMX 14,81 2,49Russian RTS 5,33 2,35Turkey ISE 30 10,36 2,99

NIKKEI 225 10,09 2,21HANG SENG 8,92 3,48

- Equities attractively valued, especially by historical comparison.

- High dividend yield is striking (especially compared to bond yields).

- Equities attractively valued, especially by historical comparison.

- High dividend yield is striking (especially compared to bond yields).

Funds Outlook 2012

25

Source: Thomson Reuters Datastream

0,90

0,95

1,00

1,05

1,10

1,15

1,20

1,25

0,9

1,0

1,1

1,2

1,3

1,4

1,5

0,85

0,90

0,95

1,00

1,05

1,10

0,85

0,90

0,95

1,00

1,05

1,10

1,15

1,20

0,90

0,95

1,00

1,05

1,10

1,15

1,20

1,25

0,7

0,8

0,9

1,0

1,1

1,2

1,3

0,7

0,8

0,9

1,0

1,1

1,2

0,9

1,0

1,1

1,2

1,3

1,4

1,5

2008 2009 2010 20110,9

1,0

1,1

1,2

1,3

2008 2009 2010 20110,6

0,7

0,8

0,9

1,0

1,1

Consumer Discretionary Consumer Staples

Industrials Telecoms

Technology Utilities

Materials Health Care

Energy Financials

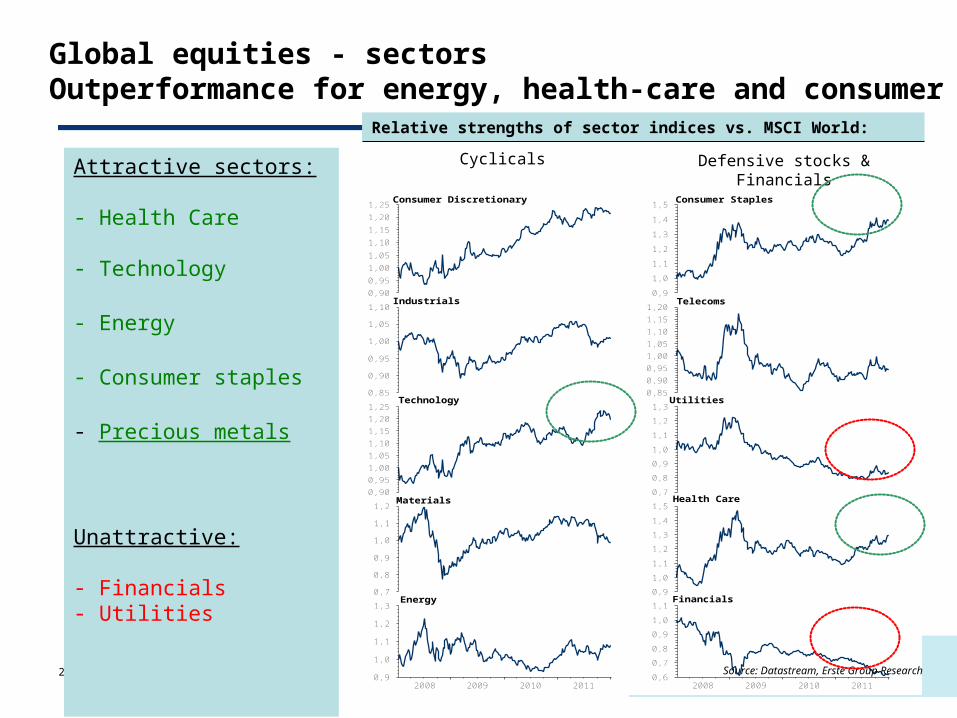

Global equities - sectors Outperformance for energy, health-care and consumer stocks

Source: Datastream, Erste Group Research

Relative strengths of sector indices vs. MSCI World:

Defensive stocks & FinancialsCyclicalsAttractive sectors:

- Health Care - Technology

- Energy

- Consumer staples

- Precious metals

Unattractive:

- Financials- Utilities

Regional allocation

Equity regions Weighting vs. MSCI World in EUR

North America

Western Europe

Japan

Emerging markets

Under Neutral Over

Note: analysis of equity regions as of January 2012; changes may be made at any time

Funds Outlook 2012

Recommendations

Heinz Bednar

Chairman of the Managing Board

Annual assessment - 2012

- Debt problem in developed economies: strong demand for top-quality government bonds that offer no yields

recommendation for emerging market government bonds where credit rating is improving

- To prevent a collapse, central banks in developed economies are creating a lot of liquidity. This is increasing the pressure for EM currency appreciation

local currencies in the emerging markets

- Moderate growth and high liquidity

USA, corporate bonds

- Countries where growth is no longer slowing; high liquidity and attractive valuations

USA, equities

Funds Outlook 2012

Funds in Focus

Asset class Investment fund Comment

Interest-bearing investments; bonds

ESPA BOND RISING MARKETS

Emerging market government bonds

Equities ESPA VINIS STOCK GLOBAL Global sustainable equities, focus on developed stock markets

Funds Outlook 2012

Disclaimer

This is an advertisement. Unless otherwise specified, the data comes from ERSTESPARINVEST KAG. We communicate in German and in English. The prospectus (together with any

amendments) was published in the "Official Gazette of the Wiener Zeitung" according to the provisions of the 1993 Investment Fund Act as amended, and is available free of charge at the head office of

ERSTE-SPARINVEST Kapitalanlagegesellschaft m.b.H. as well as at the head office of Erste Group Bank AG (custodian bank). The exact date of the last publication along with all the other places it can

be uplifted from are listed on the ERSTE-SPARINVEST KAG website (www.sparinvest.com). This document provides additional information for our investors and is based on the knowledge of those

entrusted with compiling the document as of the editorial deadline. Our analyses and conclusions are general in nature and do not take into account the individual requirements of our investors with regard

to return, taxation or risk appetite. Past performance is not a reliable indicator of the future performance of a fund. Please note that alongside the outlined opportunities, investing in securities

also implies risks. Subject to printing errors and mistakes.