Embed Size (px)

Citation preview

Presented by

Regional Economic Outlook

Dr. Steven G. Cochrane

Variation in State Job Growth Remains Narrow

0.5

1.0

1.5

2.0

2.5

3.0

75 80 85 90 95 100

Standard deviation of year-to-year state job growth by state

Trend Line Oil Price Shock90-91 Recession

PesoDevaluation

AsiaCrisis

00

Job Growth: Narrow Differences

Above AverageAverageBelow AverageU.S. = 2.3

% change year ago, 3-mo. moving average, July 2000Average is within 1/2 std. dev. of mean state growth rate of 2.0%

Variation in State Income Growth Is Beginning to Widen

0.5

1.0

1.5

2.0

2.5

3.0

75 80 85 90 95 100

Standard deviation of real, year-to-yearnon-farm household income growth by state

Trend Line

00

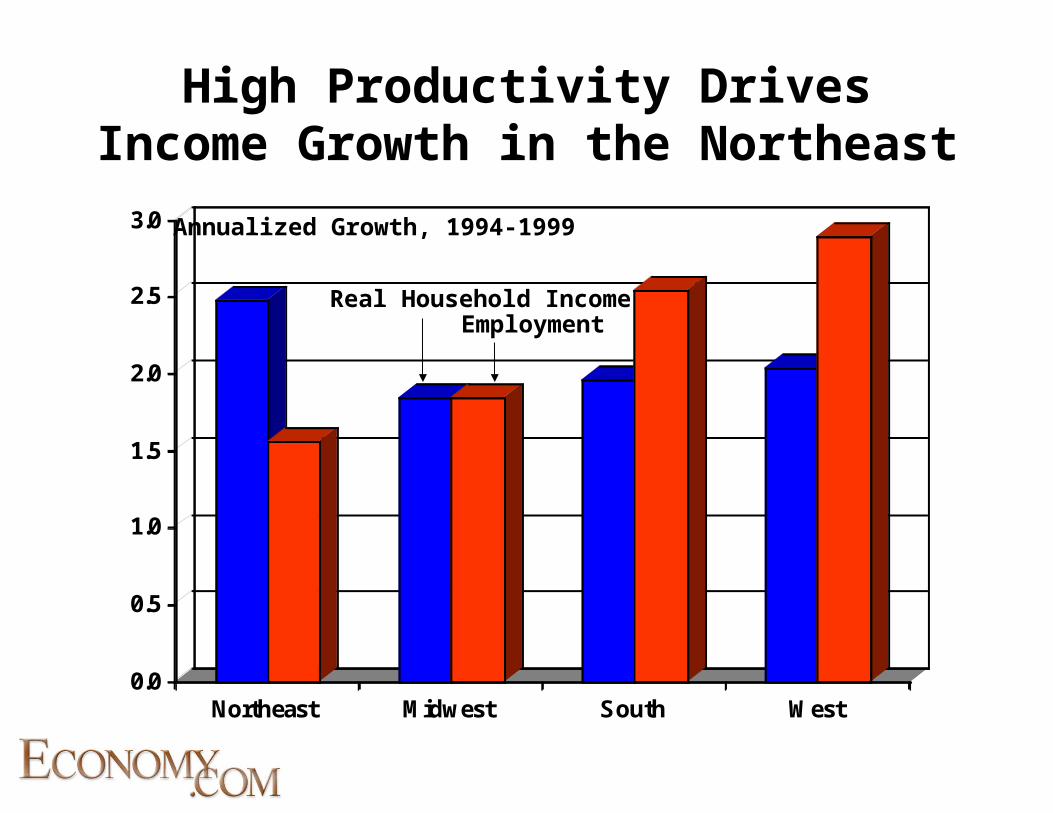

High Productivity Drives Income Growth in the Northeast

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Northeast Midwest South West

Real Household IncomeEmployment

Annualized Growth, 1994-1999

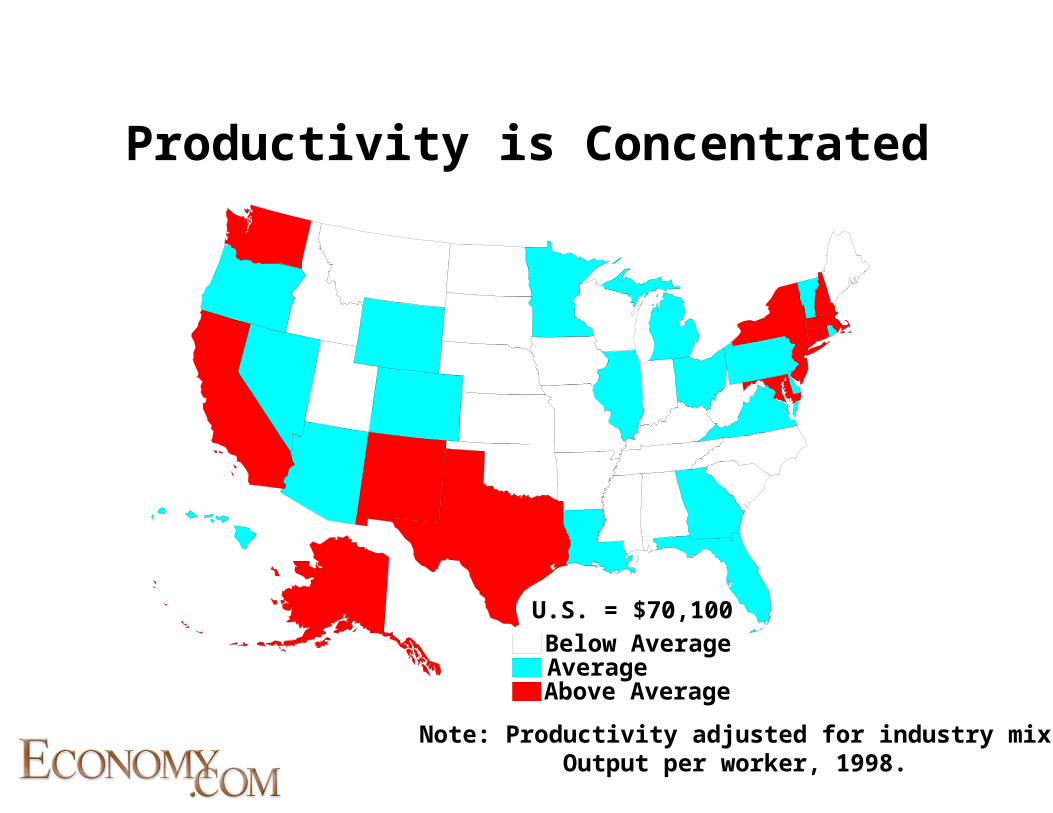

Productivity is Concentrated

U.S. = $70,100

Below AverageAverageAbove Average

Note: Productivity adjusted for industry mix. Output per worker, 1998.

Productivity Growth Fastest on the Coasts

0.0

0.5

1.0

1.5

2.0

2.5

Northeast Midwest South West

Output per worker, annualized growth, 1993-1998Productivity adjusted for industry mix

Income Growth is Accelerating Fastest in Northeast and West

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

15 year 10 year 5 year 1 year

Northeast Midwest South West

Real household incomeAnnualized growth rates (%), 1999

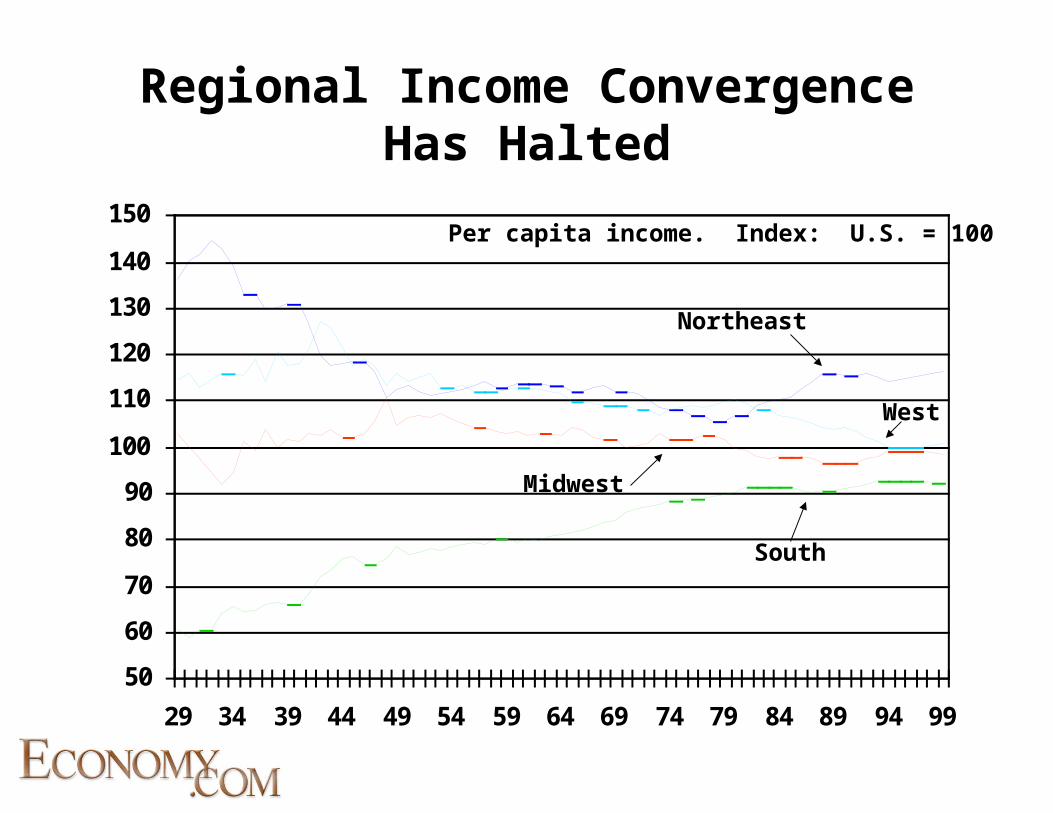

Regional Income Convergence Has Halted

50

60

70

80

90

100

110

120

130

140

150

29 34 39 44 49 54 59 64 69 74 79 84 89 94 99

Per capita income. Index: U.S. = 100

Northeast

South

Midwest

West

Capital Gains as a Share of Income

Below AverageAverageAbove Average

Note: Income is adjusted gross income

Venture Capital Supports the West

$ Bil.

Venture Capital Is ConcentratedV.C. placements as a % share of GDP, 1999

Below AverageAverageAbove Average

U.S. = 0.39%

Source: PricewaterhouseCoopers, BEA, RFA

West Is Home to More Internet Sites

South27%

West36%

Northeast22%

Midwest15%

Location of web site owners, based on approximately 75,000 sitesSource: Alexa Research, 2000

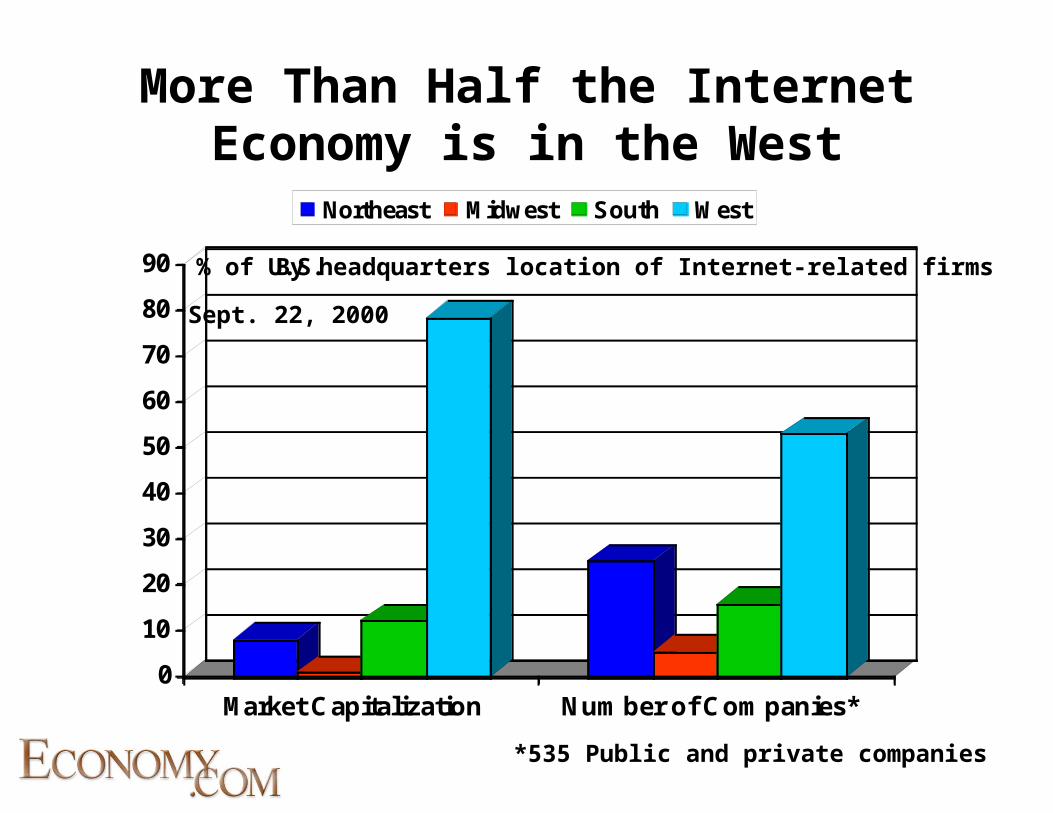

More Than Half the Internet Economy is in the West

0

10

20

30

40

50

60

70

80

90

Market Capitalization Number of Companies*

Northeast Midwest South West

% of U.S.

Sept. 22, 2000

By headquarters location of Internet-related firms

*535 Public and private companies

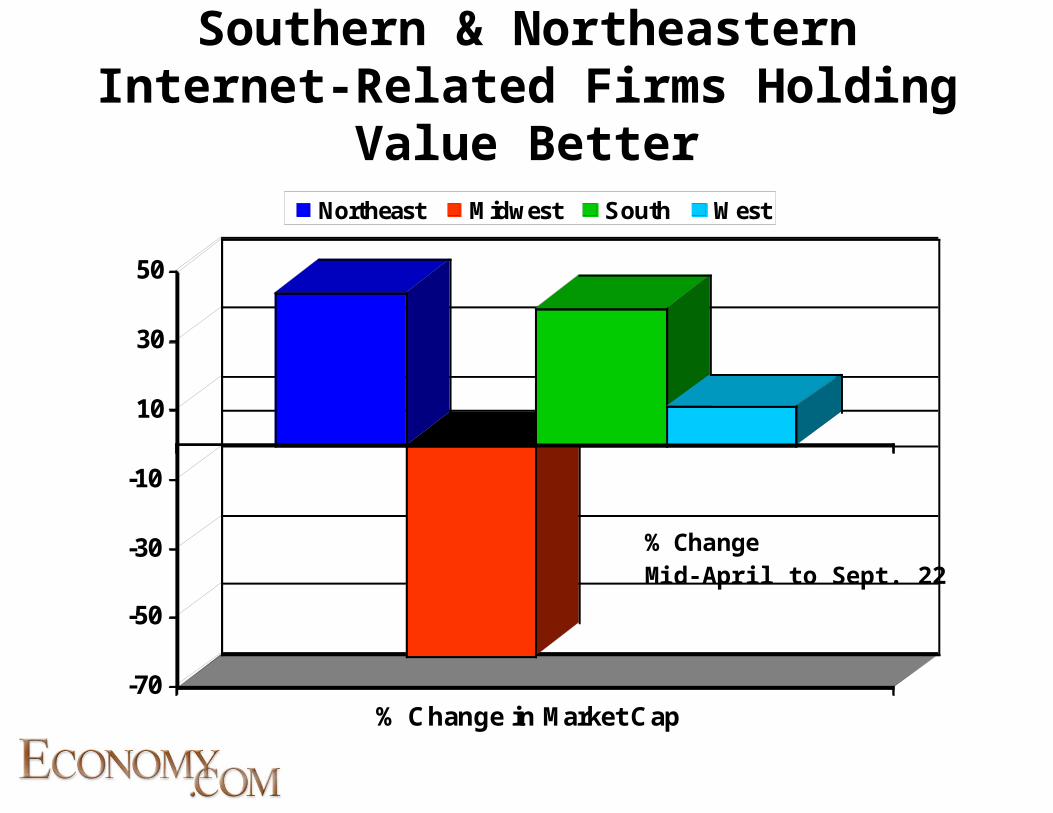

Southern & Northeastern Internet-Related Firms Holding Value Better

-70

-50

-30

-10

10

30

50

% Change in Market Cap

Northeast Midwest South West

% ChangeMid-April to Sept. 22

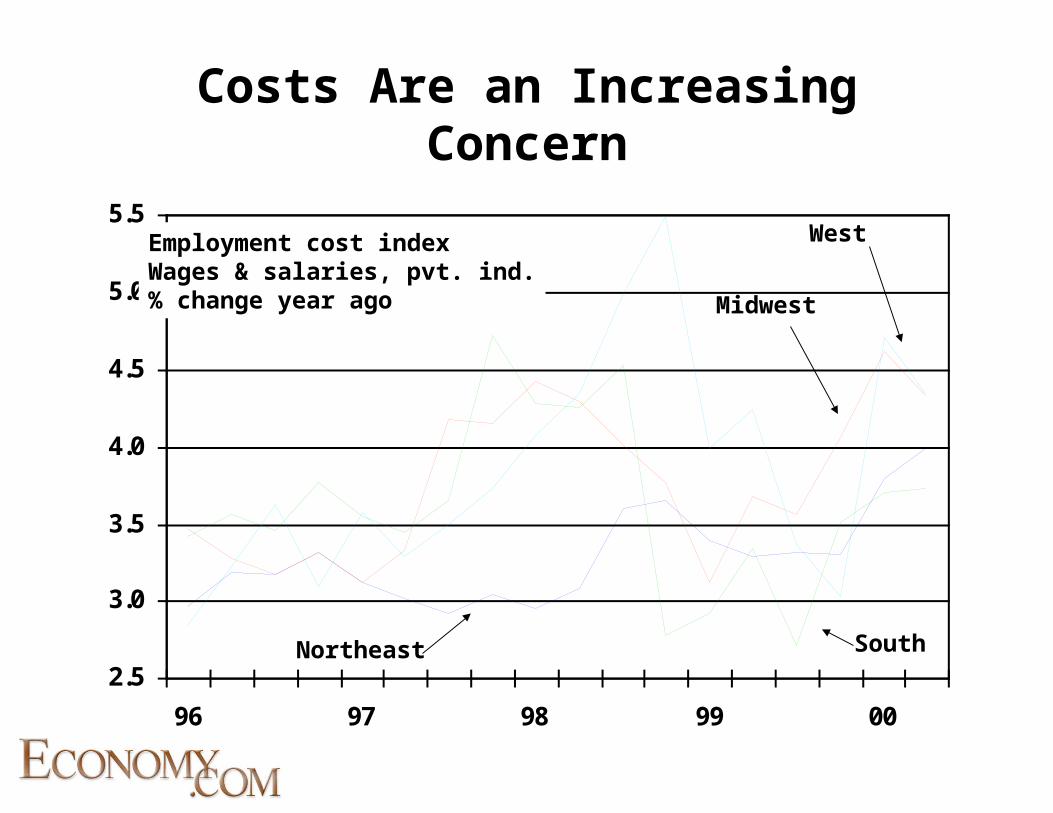

Costs Are an Increasing Concern

2.5

3.0

3.5

4.0

4.5

5.0

5.5

96 97 98 99 00

West

Midwest

SouthNortheast

Employment cost indexWages & salaries, pvt. ind.% change year ago

Cost of Doing Business

Above average

Below averageAverage

Costs include tax burden, unit labor costs and energy costs

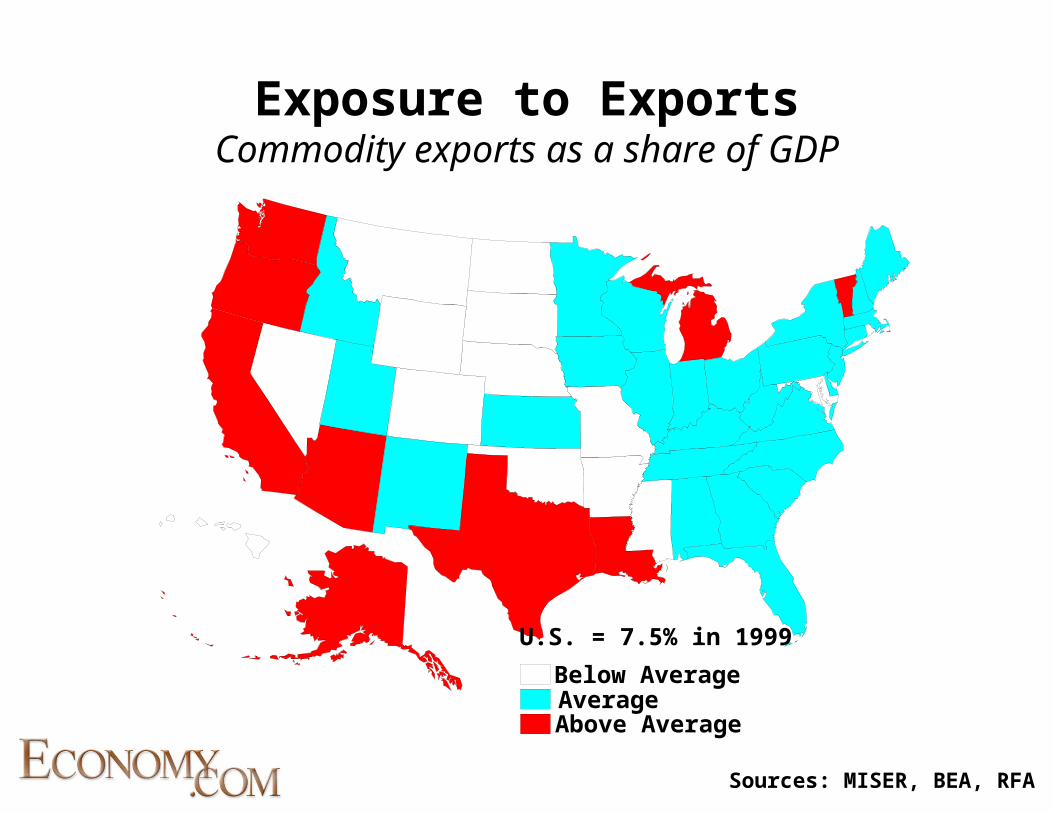

Commodity Exports Rebounding

-10

-5

0

5

10

15

20

25

97 98 99 00

West

Northeast

South

Midwest

% change year ago

Exposure to ExportsCommodity exports as a share of GDP

Below AverageAverageAbove Average

U.S. = 7.5% in 1999

Sources: MISER, BEA, RFA

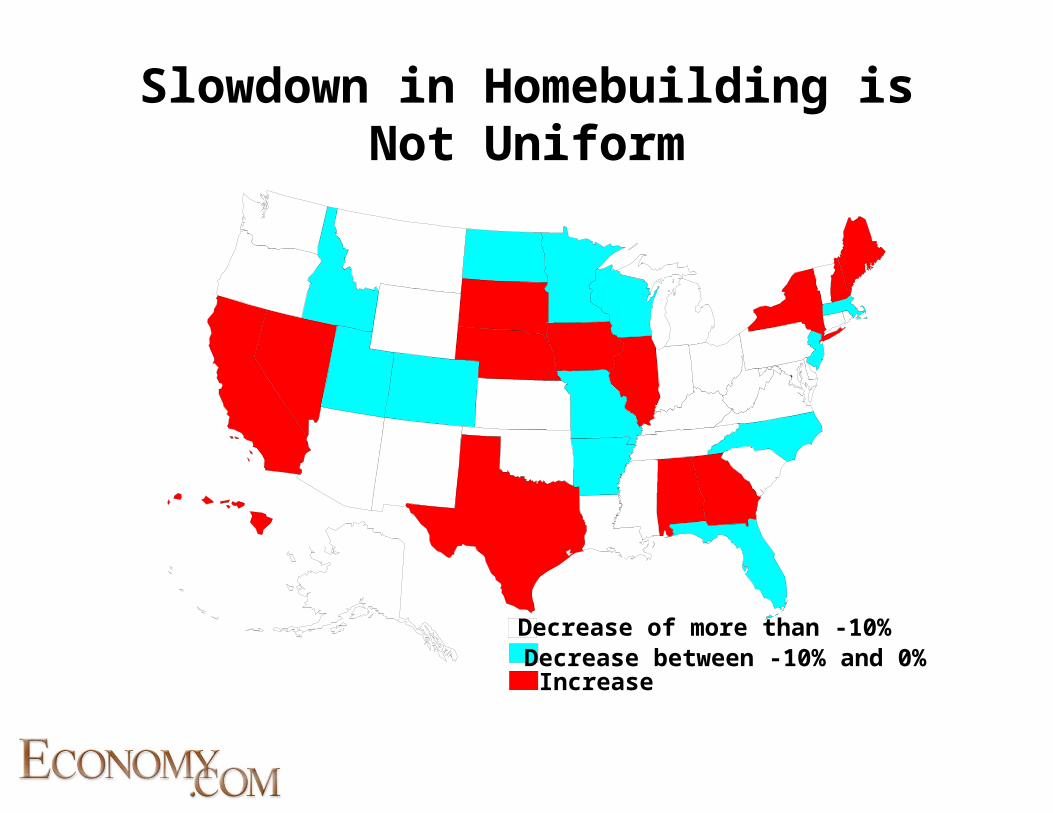

Slowdown in Homebuilding is Not Uniform

IncreaseDecrease between -10% and 0%Decrease of more than -10%

Job Growth Outlook 2000-2003

Above averageAverageBelow Average

U.S. = 1.3%

Note: Annualized growth