Embed Size (px)

Citation preview

Transactions & Business

Practical Law Canada | Transactions &

Business

Fall 2015

CANADAA COMPANION TO PRACTICALLAW.CA | FALL 2015

Practical Law

Staying Ahead

COMPETITIONFor more information, call 1-844-717-4488 or visit practicallaw.ca

of the CompetitionPutting Compliance on the Agenda

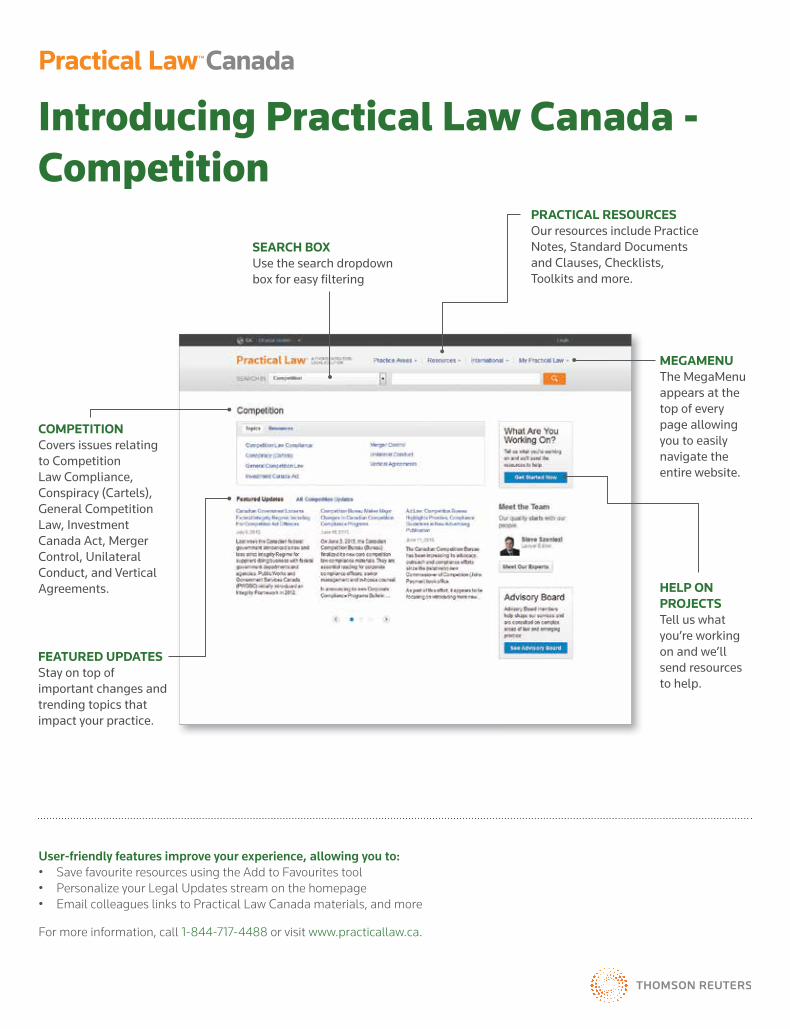

Introducing Practical Law Canada - Competition

COMPETITIONCovers issues relating to Competition Law Compliance, Conspiracy (Cartels), General Competition Law, Investment Canada Act, Merger Control, Unilateral Conduct, and Vertical Agreements. HELP ON

PROJECTSTell us what you’re working on and we’ll send resources to help.

PRACTICAL RESOURCESOur resources include Practice Notes, Standard Documents and Clauses, Checklists, Toolkits and more.

FEATURED UPDATESStay on top of important changes and trending topics that impact your practice.

User-friendly features improve your experience, allowing you to:• Save favourite resources using the Add to Favourites tool• Personalize your Legal Updates stream on the homepage• Email colleagues links to Practical Law Canada materials, and more

For more information, call 1-844-717-4488 or visit www.practicallaw.ca.

MEGAMENUThe MegaMenu appears at the top of every page allowing you to easily navigate the entire website.

SEARCH BOXUse the search dropdown box for easy fi ltering

On June 3, 2015, the Canadian Competition Bureau finalized its

new core competition law compliance materials. The message underscoring the Bureau’s new compliance materials is that companies, associations and other organizations need to consider adopting a credible and effective competition compliance program. In keeping with that important development, it is my great pleasure to introduce our latest Thomson Reuters Practical Law Canada - Transactions & Business magazine, issued to coincide with the launch of our new Competition service on Practical Law Canada.

As the new Managing Director of Thomson Reuter Legal for Canada, Australia & New Zealand, I couldn’t be prouder of the success we have had to date with Practical Law Canada. It started last year with the launch of our Corporate, M&A, Capital Markets and Securities services then this summer we launched our first Practical Law Canada litigation offering – Personal Injury Litigation, and now our third service on Competition Law.

As we all know, there is increasing pressure on law firms to manage costs wherever possible. In addition, clients are resistant to paying for what they perceive to be associate training. The heightened expectation of efficiency requires the right answers faster without compromising on quality. Practical Law Canada was developed precisely to respond to these expectations, by providing Canadian law firms and in-house counsel with expertly drafted, practical legal content, written with both specialists and non-specialists in mind.

Practical Law Canada’s new Competition service follows that same trusted model of our other modules supporting leading

lawyers in Canada and other major jurisdictions. It will be an indispensible resource for Competition law specialists, corporate lawyers and in-house counsel alike. For the specialist, the ambit of the service extends from merger review for hostile bids to competition compliance audits and to managing a cartel investigation. For non-specialists, the featured resources range from structuring joint ventures to competition compliance tailored to manage competition law risks. For example, the Competition Compliance Toolkit provides quick access to compliance overviews, a templated compliance program, hypotheticals for compliance training and checklists for key tasks — all researched, written and explained by lawyers with extensive and sophisticated practice experience.

As a complement to our online service, this magazine offers interesting insight into the lawyers who author Practical Law Canada as well as giving you a sampling of the valuable resources contained within the product. If you haven’t had the opportunity to experience Practical Law Canada yet, I hope you will soon! I look forward to hearing your feedback in the coming months.

Stay tuned for further expansion of the Practical Law Canada offering in the very near future.

On behalf of the Practical Law Canada team, Happy Reading and Thank You for your business.

Best Regards,

Neil SternthalManaging Director, Thomson Reuters Legal

A Message from Neil Sternthal

Welcome

3Practical Law Canada | Fall 2015

DIRECTOR/GROUP PUBLISHER: Jilean Bell

EDITOR IN CHIEF: Todd Pinsky

MANAGING EDITOR: Lisa Gordon

EDITORIAL CONSULTANT: Tim Wilbur

PRODUCTION CONSULTANT: Lisa Drummond

DIRECTOR, PRODUCT DEVELOPMENT OPERATIONS:

Mary Acimovic

MANAGER, PRODUCT DEVELOPMENT OPERATIONS:

Cameron Murchison

ART DIRECTOR: Dave Escuadro

COPY EDITOR: Donann Schloss

CONTRIBUTORS: Sean Farrell, Wayne Gray, Monique Rabideau, Steve Szentesi, Lynn van der Valk

MARKETING MANAGER: Andrew Lawetz

PRODUCT MARKETER: Natasha Mahendran

PRODUCTION CO-ORDINATOR: Tara Russell

FALL 2015 ONE-TIME PUBLICATIONISBN 978-0-7798-6796-7

One Corporate Plaza 2075 Kennedy Road Toronto, Ontario M1T 3V4

Practical LawCANADA

© 2015 Thomson Reuters. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of the publisher. No warranty is extended, express or implied, or liability assumed by the publisher or editor regarding the professional competence or financial integrity of any law firm or practitioner identified herein and this publication is sold on the understanding that no such reliance is made by the purchaser. The information contained in these texts is by necessity a generalized and abridged account of the matters described and should in no way be construed as the rendering of legal, accounting, financial or other professional advice by the author(s) of the text, the author’s firm, the publisher or editor of this publication.

For more information, call 1-844-717-4488 or visit www.practicallaw.ca

Vancouver

Calgary Toronto

Montréal

Ottawa

Hong Kong

Recognized leadership McMillan’s depth and breadth of experience in competition law is unsurpassed in Canada. We provide the guidance and practical advice you need so you can take the lead.

McMillan LLP | Vancouver | Calgary | Toronto | Ottawa | Montréal | Hong Kong | mcmillan.ca

Dr. A. Neil Campbell t: 416.865.7025 [email protected]

James B. Musgrove t: [email protected]

For competition advice in Canada, please contact:

5Practical Law Canada | Fall 2015

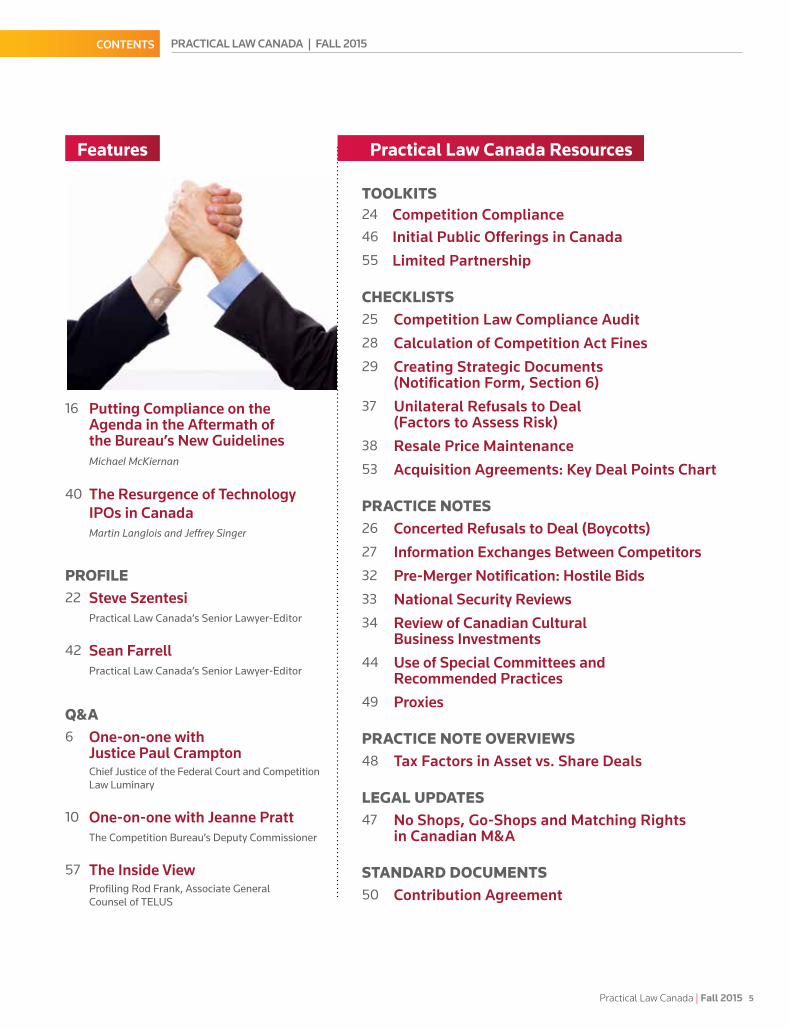

Features

16 Putting Compliance on the Agenda in the Aftermath of the Bureau’s New Guidelines

Michael McKiernan

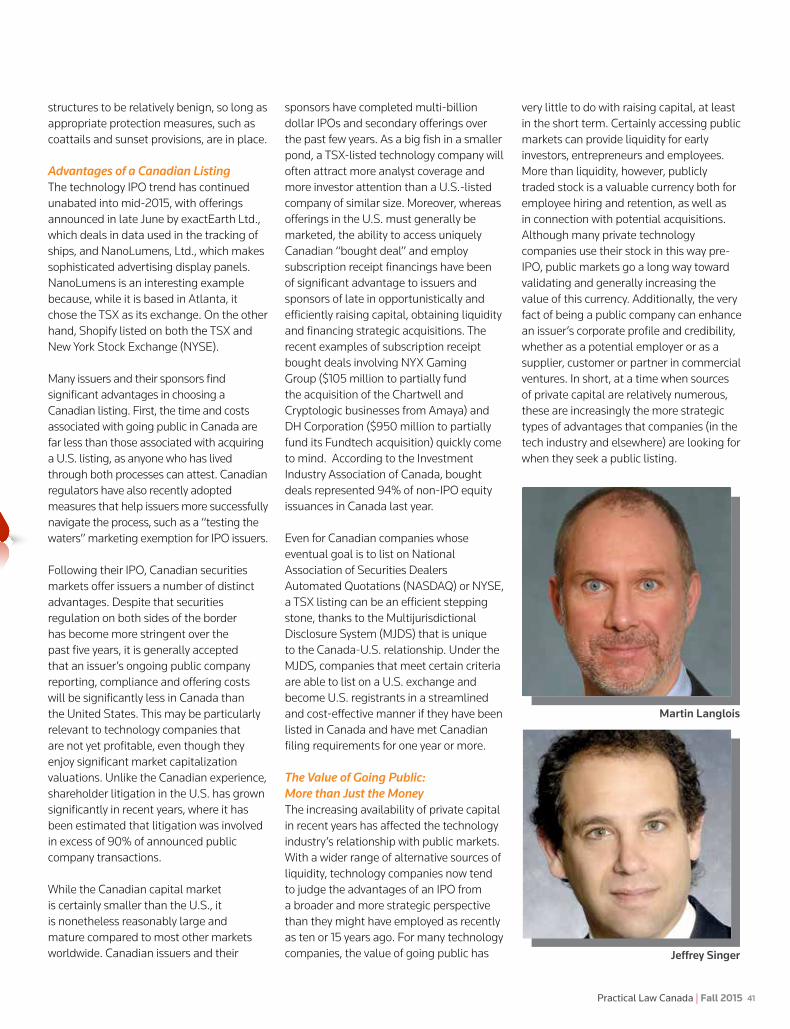

40 The Resurgence of Technology IPOs in Canada

Martin Langlois and Jeffrey Singer

PROFILE22 Steve Szentesi

Practical Law Canada’s Senior Lawyer-Editor

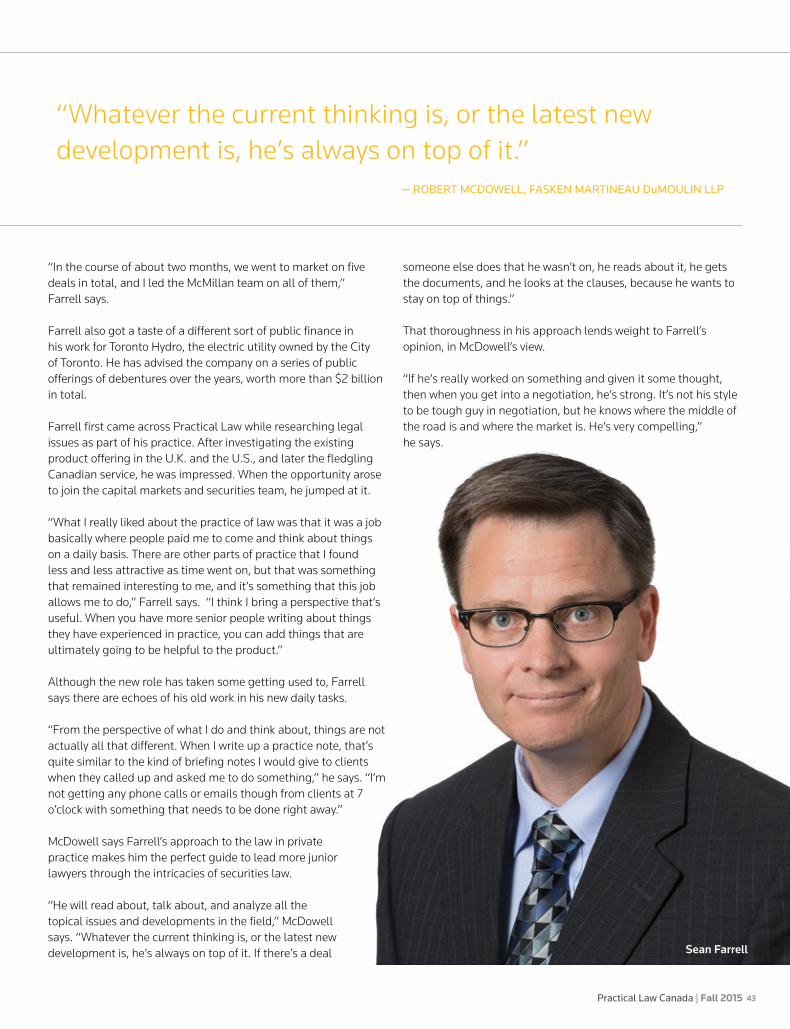

42 Sean FarrellPractical Law Canada’s Senior Lawyer-Editor

Q&A6 One-on-one with Justice Paul Crampton

Chief Justice of the Federal Court and Competition Law Luminary

10 One-on-one with Jeanne PrattThe Competition Bureau’s Deputy Commissioner

57 The Inside ViewProfiling Rod Frank, Associate General Counsel of TELUS

Practical Law Canada Resources

TOOLKITS24 Competition Compliance46 Initial Public Offerings in Canada55 Limited Partnership

CHECKLISTS25 Competition Law Compliance Audit28 Calculation of Competition Act Fines29 Creating Strategic Documents (Notification Form, Section 6)37 Unilateral Refusals to Deal (Factors to Assess Risk)38 Resale Price Maintenance53 Acquisition Agreements: Key Deal Points Chart

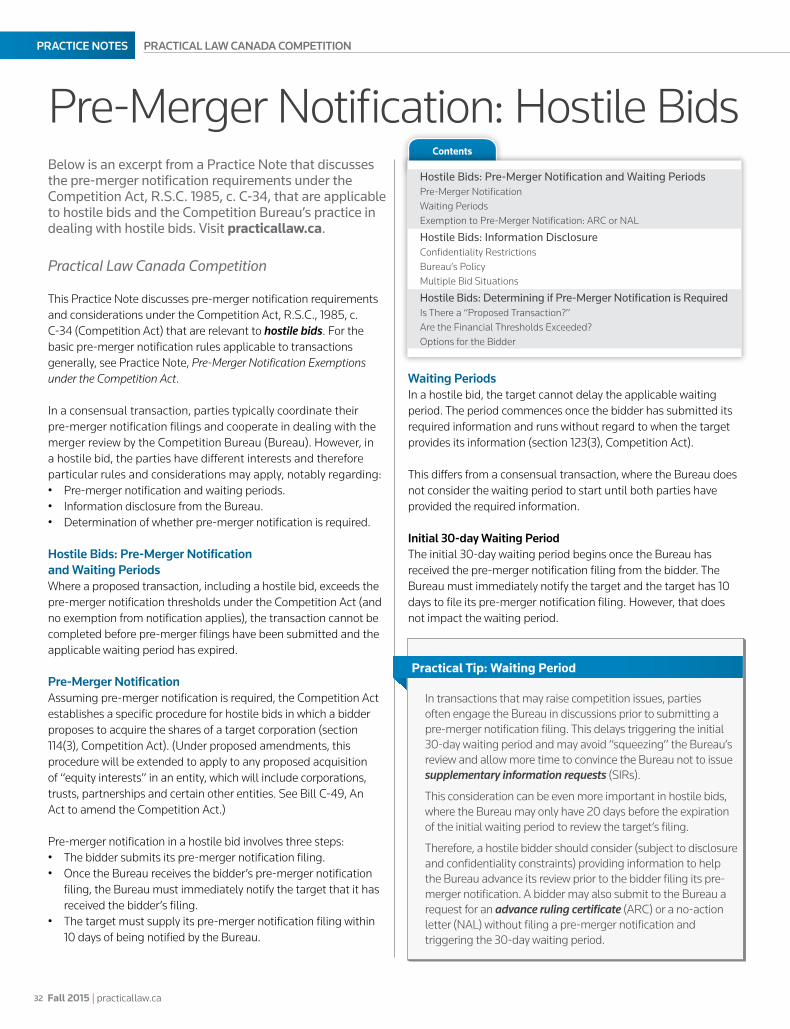

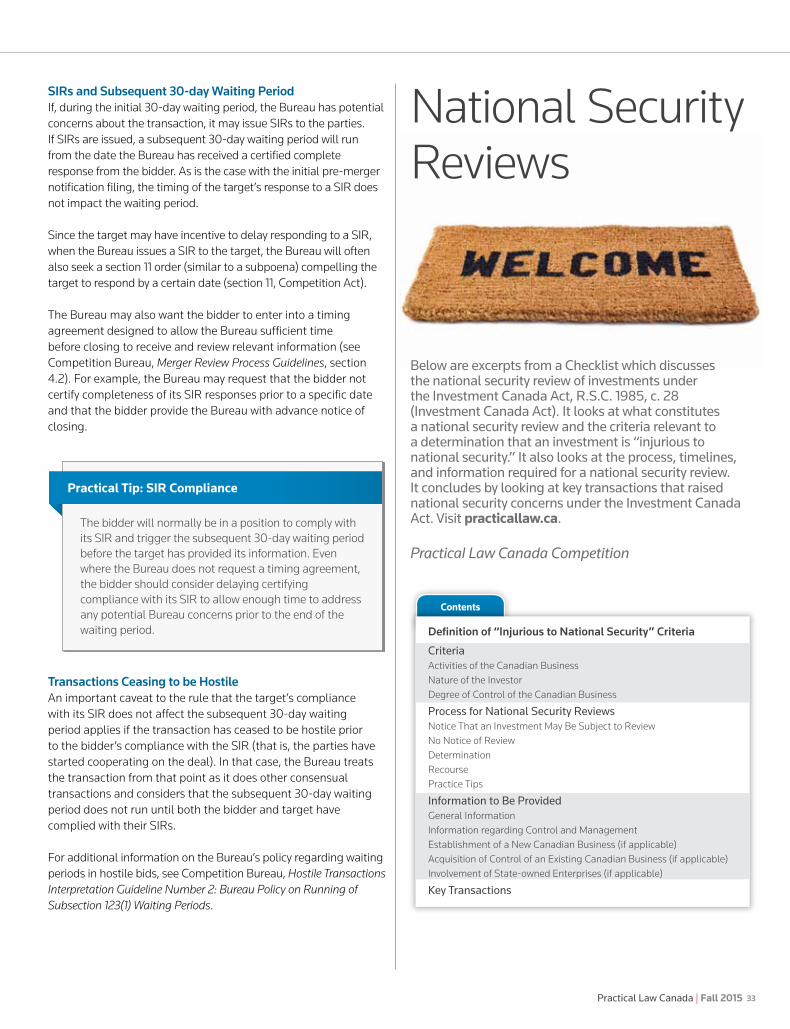

PRACTICE NOTES26 Concerted Refusals to Deal (Boycotts)27 Information Exchanges Between Competitors32 Pre-Merger Notification: Hostile Bids33 National Security Reviews34 Review of Canadian Cultural Business Investments44 Use of Special Committees and Recommended Practices49 Proxies

PRACTICE NOTE OVERVIEWS48 Tax Factors in Asset vs. Share Deals

LEGAL UPDATES47 No Shops, Go-Shops and Matching Rights in Canadian M&A

STANDARD DOCUMENTS50 Contribution Agreement

PRACTICAL LAW CANADA | FALL 2015CONTENTS

Fall 2015 | practicallaw.ca6

Q&A

Justice Paul Crampton

Practical Law Goes One-on-one with Chief Justice of the Federal Court and Competition Law Luminary

Credit: Andrew Balfour

7Practical Law Canada | Fall 2015

What got you interested in the law? Back in about 1981, I was just coming up to the end of my philosophy bachelor’s degree, and I started thinking about what I wanted to do after that. The law seemed like a good fit. Oddly enough, you will find a lot of philosophy majors going on to law school, who become lawyers and do very well. Philosophy is a fabulous base for the law.

When and why did you become inter-ested in competition law? About half way through my first year at law school, I decided to do a Master of Business Admin-istration (MBA). It happened when I was in business law class, just sitting there while people were asking all these sophisticated business questions. I had come from an arts background with almost six years of straight arts, so I thought it made a lot of sense to get that extra degree.

Subsequently, in my articles, I was wrestling between corporate law and litigation, and also between business and the law. It was only really towards the end of my articles that I stumbled across competition law. I was on a case that was the last criminal merger case, and it was like a eureka moment. I had found this area that allowed me to have a foot in corporate and a foot in litigation; a place where I could bring together my legal skills and my MBA skills.

At the time, it was a particularly fascinating area. They had just amended the Competition Act to decriminalize mergers and monopolization, so it was a bit like carte blanche. I decided to do

a master’s in that area, and then I went to the Competition Bureau where we were developing policies by the seats of our pants, in real cases, in real time, sometimes under a lot of pressure. It was a wonderful experience.

How do you think Canadian competition law has changed since you began? I think it has changed a lot. In those early days, once the Competition Act amendments came into force in mid-1986, including amending the name from the old Combines Investigation Act, it took a few years to settle policies and procedures and get the analytical framework down. Then the private sector had to get comfortable and up to speed with it. There have been some very helpful guidelines issued by the Competition Bureau over several different areas in the intervening 25 years. A lot of work has been done academically, and a lot of important helpful decisions have been issued by the Competition Tribunal, so things are starting to be clarified and fleshed out. There’s more business security now and more comfort within the bar and the Bureau about what’s needed to conduct a merger review or how to conduct a review of alleged abuse of dominance. There have also been important amendments to the Act that I think have reduced the chilling effect of the old Act and brought it into the modern area.

In addition to private practice, you did some very interesting competition policy work before joining the bench. Can you tell us a bit about what drew you to work with the OECD? That was another

wonderful experience. I was approached literally out of the blue about a week or two after 9/11. I did primarily mergers and acquisitions (M&A) work, and deal activity virtually came to a halt in the wake of 9/11. Then I was approached by the Head of the competition division at the OECD, who I had known from my work with the Asia-Pacific Economic Cooperation (APEC) forum. He called to offer me the position of Head of Outreach, who would be the person responsible for all the OECD’s work in the competition area with non-member countries. At the time, that basically meant everybody except the G-30. It was fascinating being responsible for the OECD’s work with Brazil, Russia, India and China, the BRIC countries, as well as smaller countries throughout Latin America, Africa, Asia and former Soviet countries in Eastern Europe and Central Asia.

It was like lawyers without borders. Helping these countries to transition towards market-based economies was really wonderful. One of the things I’m particularly pleased about from my time at the OECD was an idea we had of establishing a regional strategic partner in each of the four developing or transitioning areas of the world. For Asia, I chose the Koreans, and we got a regional training centre set up in Seoul. Then for Eastern Europe and Central Asia, I chose the Hungarians, and they also embraced the idea very enthusiastically. Both of those training centres are still going really well. I was only at the OECD for two years, so we didn’t end up getting the centres established for Central America or Africa, although we did have plans on that front. We also launched the Latin American Competition Forum, which was another very important initiative for Latin America, as well as the OECD-APEC initiative, which was a partnership that enabled the OECD to convey its content, information, and materials to the APEC countries.

How big of an adjustment was it when you joined the bench after so long in practice? It wasn’t that difficult at all. Obviously, it’s a big financial adjustment to take a 70% pay cut. It’s also a family

Justice Paul Crampton’s distinguished competition law career has taken him from some of Bay Street’s biggest beasts to the hallowed halls of the Federal Court in Ottawa, where he now sits as chief justice.

Having started out in the late 1980s at the Competition Bureau, Justice Crampton became a partner at Davies Ward Phillips and Vineberg LLP and later at Osler Hoskin and Harcourt LLP, working on some of the biggest deals of the last two decades.

This adventurous soul also found time for a two-year stint with the Organisation for Economic Co-operation and Development (OECD), helping developing countries transition to market-based economies.

Here, the Chief Justice discusses a career that has covered all bases in the competition law field and lets us in on a few of the secrets of his success.

Fall 2015 | practicallaw.ca8

adjustment, because our kids were older and all very much at home in Toronto, which meant they weren’t too enthusiastic about moving to Ottawa and establishing new relationships with friends here; however, the transition went really well. I had been doing public interest work at the OECD and the Competition Bureau, so it was easy for me to take off my private sector hat and put on a public interest hat again. I had also been very involved in the bar and other associations, which did a lot of public interest work, whether it was the Canadian Bar Association (CBA), the American Bar Association (ABA), the International Chamber of Commerce, or the Canadian Chamber of Commerce. That experience made it a lot easier for me.

What do you see as important competition law and policy areas for Canadians, and how do you see the Federal Court’s role in developing competition law? Right now, we are primarily involved in providing oversight of the Competition Bureau’s requests for production of documents and written returns. Those types of orders can be fairly intrusive, so we focus on ensuring that their ex parte requests are not inordinate, disproportionate or unduly burdensome. I think that is important work, and that we are coming close to striking the right balance. We have developed some templates with the Competition Bureau for our orders, but each case has to be assessed on its own merits.

The 2009 amendments to the Competition Act, which brought in what we call per se hardcore cartel provisions, are an important area. That area will continue to evolve as the courts address, for the first time, the new provisions in section 45 of the Competition Act in particular, but also the new civil provisions in section 90.1.

The Competition Tribunal, a hybrid tribunal that includes judges from the Federal Court and lay members, has a number of cases on the go right now. We have had some interesting cases in recent years, and we contribute, through our judges who sit on the Tribunal, to the evolution of jurisprudence in the

non-criminal area. On the criminal side, we have had some history in the area of guilty pleas, but I think the Crown and prosecutors appear to be more comfortable with the superior courts where they practise more often. As a result, we have had a lesser role to play in the criminal area.

How does it compare sitting as a member of the Competition Tribunal as opposed to the Federal Court? It is highly similar in many respects, in terms of how the proceeding unfolds, how evidence is introduced, and how we reach a decision. It is different in the sense that Federal Court judges sit as single judges, whereas

the Tribunal sits often as a panel of three. That means you are sitting almost like an appellate body, even though it’s a tribunal of first instance. It is certainly different, but it is a nice change to be able to work with other people.

What element of your work do you find most challenging? Trying to find time to sit. I’ve got a fairly heavy administrative burden as Chief Justice, but I think it is very important to also provide leadership through the Court’s jurisprudence. I think we’re the largest superior trial court in the country that doesn’t have an Associate Chief Justice. It’s a very high priority for us to hire one so that I can sit more and provide that leadership that other chief justices are able to provide.

What accomplishment are you proudest of? It is probably setting up those two training centres for the OECD in Seoul and Budapest. They are benefiting tens of millions of people each. I am motivated

by public interest work and by a desire to make a difference to society, so those training centres have probably made more of a difference than anything else I have done.

What one piece of advice would you offer junior competition law practitioners? It’s very important to be happy with what you are doing. Find something that motivates you and that you can be passionate about. Afterwards you’ll do really well. Also, try to maintain a good work-life balance because work really isn’t everything. If there is one thing I could do differently, I would have spent more time with my family in those crazy

M&A years in the 1990s, when I probably spent too much time down on Bay Street.

If you were not a judge, what would you wish to be? That’s a very difficult question, because I love being a judge, and I actually think this is what I should be doing. This is my highest and best-value use to society, so it’s hard for me to say what I would be doing if I weren’t a judge. Perhaps I would work for a non-governmental organization somewhere or other.

What do you do when you’re not being a judge? I love spending time with my immediate family; my wife, my kids. I come from a big Irish family, so I also have a large extended family, whom I also love spending time with. I love reading about non-legal things, and I still like to travel even though I’ve travelled to over 50 countries now. Adventure travel is something I love to do; going to Base Camp at Everest was a highlight. I’d like to do more of that type of thing.

Q&A

“We were developing policies by the seats of our pants, in real cases, in real time,

sometimes under a lot of pressure. It was a wonderful experience.”

— JUSTICE PAUL CRAMPTON

BY BEING BETTER THAN THEIR COMPETITION.

HOW DO ANIMALS THRIVE IN THE WILD?

Practical Law Canada subscribers have a leg up on the competition. With access to hundreds of practical legal know-how resources written by our expert lawyer-editors, leading law firms and law departments are securing their position at the head of the pack.

Discover how you can outperform your competition. Try Practical Law Canada today.www.practicallaw.ca

Fall 2015 | practicallaw.ca10

Q&A

Practical Law Goes One-on-one with the Competition Bureau’s Deputy Commissioner

When Jeanne Pratt signed up with Canada’s Competition Bureau in 2009 on an interchange program from her partnership at Bay Street heavyweight McCarthy Tétrault LLP, the two-year term always looked a little short.

As a child of two civil servants, public service was in her blood. Six years later, Pratt has ascended the ranks to become senior deputy commissioner, taking charge of the bureau’s mergers and monopolistic practices branch.

Having cut her teeth in private practice on the granddaddy of all Canadian competition cases, Air Canada’s combination with the ailing Canadian Airlines, Pratt quickly established herself as one of the leading lights in the field, practising exclusively in the area of competition law and litigation for a decade before joining the bureau.

Pratt shares her views below on some of the most pressing issues currently facing the Competition Bureau, including how she dealt with a merger of her own: one that brought together the bureau’s old mergers and monopolistic practices departments.

What is your legal background and practice history? I had no idea that the Competition Act really existed when I was at law school, other than reading some constitutional law cases that implicated the old Combines Investigation Act. After my articles, I actually took some time to work on Parliament Hill, and I was working for a senator during the time that Canadian Airlines was in financial difficulty. As a result, Air Canada took over Canadian Airlines, and there were a lot of competition law issues surrounding that takeover because that would basically have given Air Canada a monopoly over domestic services in Canada. In my capacity working on Parliament Hill, I was involved in supporting a senator through some public hearings with respect to legislation surrounding that takeover and became quite interested and intrigued by the competition law issues that transaction implied.

When I was looking to continue the practise of law was really the point where I started to specialize, and I ended up being really concentrating on all competition law, all the time, for the next 15 years or so.

I did basically the full array of competition law: merger work, advising companies on proposed transactions, cartel work, including investigations by the Competition Bureau, and immunity and leniency applications. I also did advisory work for large national and multinational companies with respect to unilateral conduct provisions and abuse of dominance.

My first competition case actually emanated from the airline matter. I ended up as junior counsel on a team of counsel to the Commissioner of Competition against Air Canada, alleging an abuse of dominance position with respect to routes in eastern Canada, when WestJet and CanJet were entering those markers back in the late 1990s and early 2000s.

What made you interested in the Competition Bureau’s work? I had the experience working as counsel to the commissioner in my early career. As I progressed on all these matters, I would be dealing with the staff at the Competition Bureau on behalf of clients in merger matters, cartel matters and any other unilateral conduct

investigations in which clients I was working with were implicated.

I joined the bureau on an interchange, and I was here for what was supposed to be a two-year period as special legal advisor to the then-Commissioner of Competition, Melanie Aitken. It was in 2009 when we had a brand new commissioner, and the Competition Act had just had its most significant amendments after 25 years. For me it was a phenomenal opportunity to be offered a position at such a particularly great time.

My role when I was legal advisor was to work with the Competition Bureau team on more high-profile matters, matters that were potentially in litigation, and also to provide advice to the commissioner at her request. I had been in the private sector for the better part of a decade at that point, so it was very interesting to come and work for the Competition Bureau where the work that we do implicates a lot of different interests and parties.

How big an adjustment was it from private practice? When you’re in the private sector, your stewardship role is with respect to a client. When you’re in the public sector, your stewardship role is much broader, and there are a lot of competing interests that you have to balance and manage to come to what you would hope would be the best result for competition and for consumers.

I didn’t find it a huge adjustment. It is changing your mindset from being a client lawyer to being a public sector legal advisor, which is something that I certainly embraced and that brought a lot of satisfaction to the work that I did. You feel like you may be having an impact that is broader than one company or one client.

11Practical Law Canada | Fall 2015

I’m also the child of two public servants, so that ethos was probably ingrained in me in my early life.

What do you see as priorities for the bureau’s new Mergers and Monopolistic Practices Branch, and are there any sectors that you are focussing on in particular? Our priorities really are the same as for the Competition Bureau at large. Our first priority is to increase compliance, both through preventing and deterring anti-competitive conduct, and mergers. That has always been our priority and will continue to be.

In terms of how that priority plays out, in the mergers context, we are largely responsive to developments in the marketplace because we are reviewing transactions as they occur. We don’t really pick and choose the sectors. It is about what is brought in the door and what transactions are occurring.

In terms of monopolistic practices, we generally follow issues in the marketplace that we are seeing. The digital economy is a space that is near and dear to consumers and also near and dear to our enforcement work. We are doing a lot in that digital space right now through some of our ongoing inquiries, such as the inquiry against Apple with respect to its iPhone.

We have cases before the Competition Tribunal with respect to retail gas, real estate and e-books. We have ongoing investigations that I can talk about and there are also a lot that goes on that I can’t tell you about.

We also had a significant supreme court decision in January, the Tervita case, which we are doing our homework on, looking at how we will implement the guidance that we received with respect to the analysis of efficiencies in merger reviews.

What kind of effect has the merging of the bureau’s mergers and monopolistic practices branches had? We want to make sure that we are best placed to be

able to address issues in the marketplace, and also to ensure that we have a merger review that is responsive to the realities of the economy as a whole. In addition, we also make it a priority to invest in the best resources to ensure that we can do our work in the most efficient way, using advanced economic theories and strategies. The merger of the mergers and monopolistic practices branches allows us to build on those efficiencies and the talent that we have in-house, to ensure that we are doing our work as efficiently as possible with the best resources possible.

How important are your relationships with competition watchdogs in other jurisdictions? International cooperation has and will continue to be a priority for us. In multinational mergers, it’s incredibly important for us to be able to coordinate effectively with other jurisdictions to ensure that we take a holistic approach to the competition issues that may arise.

We continue to build our relationships through multi-lateral organizations, such as the International Competition Network (ICN) and the Organization for Economic Cooperation and Development. The ICN is a practical organization, where competition authorities from around the world come together to share their best practices and lessons learned. This ultimately, for example in the mergers context, provides certainty and predictability for merging parties in numerous jurisdictions, so that they can know what we may be looking for in terms of our review and where remedies are required.

We also have bilateral and trilateral meetings with other anti-trust agencies, such as the U.S. Department of Justice, the U.S. Federal Trade Commission and the European Commission. I think the trend is towards more close cooperation. We certainly have had very close cooperation with the U.S. agencies because our economies are intertwined, and merging parties want the certainty of

Jeanne Pratt

Fall 2015 | practicallaw.ca12

Q&A

knowing that they are not going to be told different things by two different agencies in two different jurisdictions.

In consequence, we are increasingly working together with them. In May 2014, we put out some best practices that we use in our coordination with those two agencies to try to come to the best result as efficiently as possible, to give that certainty and predictability to merging parties, and to ensure that competition issues in both jurisdictions are indentified and addressed appropriately.

What are your thoughts on the Competition Bureau’s recently finalized new competition compliance materials for Canadian businesses as far as mergers are concerned? I think our commissioner and the Competition Bureau as a whole is a leader internationally, recognizing that preventing anti-competitive conduct is just as important as deterring it through our enforcement work. So we have recently put out a new information bulletin on compliance programs which is aimed at encouraging companies and market participants of all sizes to put in place compliance regimes that we think will encourage greater competition in the markets and deter anti-competitive behaviour as well.

In the merger space, one aspect of that is ensuring that companies pre-notify us of transactions that are required to be pre-notified under our Act. We put a recent information notice out about a particular company and their efforts to put in place a compliance program to address instances where they may not have notified where they should have. I think that demonstrates our willingness to ensure that the right mechanisms are in place and that companies are encouraged to comply with the law at the end of the day.

The bureau recently obtained a partial injunction in the Parkland/Pioneer merger in the gas-station market. Is this a sign of things to come in terms of the willingness to use all enforcement

tools at your disposal in the merger area? Some people have asked whether our application for an injunction in the Parkland case is indicative of a policy shift, and I don’t think so. We are always looking for, and continue to look for, the most appropriate method to resolve our competition issues, and we continue to have a preference for consensual resolutions.

I think we have always used our tools, and I don’t think this is any indication that we will use them any more than we have. We will continue to use them where we think it is appropriate.

Do you have any recommendations for merging parties in their dealings with the bureau? I think the vast majority of merger transactions do not raise issues under our Competition Act, so in the majority of mergers that we review in the course of the year, we meet our service standards almost all of the time.

For the small proportion of transactions where there are competition issues, we continue to encourage parties to come to us early to try to resolve our concerns.

Following the decision in Tervita, we also ask them to come to us with their submissions on the efficiencies that will result from the proposed transaction, so that we can consider them in the context of our ongoing review. Efficiencies act as a defence, so we would encourage parties to bring that information to us as early as possible. That way we can consider it in the context of our overall review of the proposed transaction, instead of waiting until we identify concerns and a potential challenge, because that will lead us to a place that may delay a proposed transaction or a resolution.

Merger activity in Canada appears to be picking up again. Is this the bureau’s sense as well? For our fiscal year 2014-2015, we had the highest number of filings in the post-recession period. It was about an 11 per cent increase over the prior fiscal year. That being said, by the end of the fiscal year, we were noticing a bit of a

drop, so we find that our filings are really following the flow of the economy. The first quarter saw the highest total filing volume in over a decade, but then when you look at the fourth quarter, we saw some of the lowest, so it is quite lumpy.

The bureau has expressed interest in bringing more unilateral conduct cases. Is there anything interesting on the horizon? We are continuing to advance a number of cases that we think have potentially high impact on the Canadian economy and consumers. Some of them are focussed on the digital economy and supporting innovation. We are moving forward with our inquiry concerning Apple’s use of restrictive clauses in its contracts with Canadian wireless carriers. We have been using our subpoena power to collect information in the context of that inquiry, and it is well under way. Our issue there is determining whether those clauses impact the manner in which carriers conduct their business, particularly with respect to how they price and market smartphones and corresponding wireless services. Our concern is really that they could foreclose the suppliers of competing smartphones from the market or reduce choice and innovation, and ultimately potentially increase the price of smartphones and wireless services for Canadian consumers. This obviously is an area that is near and dear to anyone that has a smartphone, which is pretty much the entire population.

Also in unilateral conduct, we have an ongoing case in litigation with respect to the Toronto Real Estate Board and its rules that impact the ability of virtual office websites to provide information to consumers who may want to collect information in a manner that does not use real estate agents. That case is headed for a rehearing in the fall, and we look forward to receiving additional guidance from the Competition Tribunal on it.

There remains relatively little activity under section 90.1 of the Competition Act dealing with competitor collaboration since the

Fall 2015 | practicallaw.ca14

2009 amendments. Are there any developments in this area you would like to share? Since 2009, we have had two applications that I can talk about implicating section 90.1. The first was an application that was challenging the joint venture between Air Canada, United Airlines and Continental Airlines. With that case, we raised concerns with respect to some of the coordinating agreements between those parties, and ultimately we came to a consensual resolution that resolved our concerns.

In addition, we have a pretty high-prolife case and very active investigation right now, which is with respect to e-books. We had come to a consensual resolution with four publishers, but that consent agreement was challenged by Kobo. Therefore, we are in ongoing litigation with respect to that consent agreement, but we have continued our investigation with respect to section 90.1 in that matter, so there are things to come on that front as well.

Are there any key advocacy or regulated areas you see as priorities for your new branch? I think our priorities are the bureau’s priorities. The bureau has recently put out a three-year strategic plan where we talked about increasing compliance. We also want to create an environment for competitive prices, greater product choice and informed decision-making for all Canadians.

We are promoting and advocating for a more competitive marketplace to empha-size smart regulation. A lot of the work being done by our advocacy group at the bureau is informed by the experiences in the Mergers and Monopolistic Practices Branch and the knowledge that we have gained from doing reviews and inquir-ies in those sectors. It really is a holistic approach, and we’re trying to get there as efficiently as we can, capitalizing on the great knowledge that we have gained through our enforcement work over the years.

You joined the Competition Bureau at a key moment in its history in 2009. Is it still an exciting time to be working there? I think now more than ever. We’ve got a lot of great work that is being done, and there are a lot of interesting issues happening because of the dynamic nature of our economy. Although the provisions in our Act are not changing, the situations we are seeing challenge us because there are new facts and new industries. We want to ensure that we are encouraging innovation, but also stressing anti-competitive conduct where it arises.

I think it’s generally a very interesting time to be involved in Canadian business and with what is going on globally in terms of the digital economy. There is a lot of change going on. Even if we reviewed an industry a year ago, there could be significant changes, which means that the nature of our work continues to be challenging and dynamic.

Start with Practical Law Canada – CompetitionSign up for a FREE TRIAL now at practicallaw.ca

BEGINNING AT SQUARE ONE IS FINE UNLESS YOU’RE MANAGING CHANGING COMPETITION RISK.

Practical Law Canada Advisory Board members help shape our services and are consulted on complex areas of law and emerging practice.

COMPETITION

Kevin Ackhurst Norton Rose Fulbright Canada LLP

George Addy Davies Ward Phillips & Vineberg LLP

Rodney Frank Telus Corporation

Mark Katz Davies Ward Phillips & Vineberg LLP

Robert Kwinter Blake, Cassels and Graydon LLP

Michelle Lally Osler, Hoskin & Harcourt LLP

James Musgrove McMillan LLP

Michael Osbourne Affleck Greene McMurtry LLP

Christopher Putney Insurance Corporation of British Columbia

Omar Wakil Torys LLP

Sandy Walker Dentons Canada LLP

Charles Wright Siskinds LLP

Kevin Wright DLA Piper (Canada) LLP

CORPORATE AND SECURITIES

James Beeby McCullough O’Connor Irwin LLP

Aaron Emes Torys LLP

John Hall Borden Ladner Gervais LLP

Carol Hansell Hansell LLP

Chris Hewat Blake, Cassels & Graydon LLP

Markus Koehnen McMillan LLP

Alison Manzer Cassels Brock & Blackwell LLP

Paul Martel Blake, Cassels & Graydon LLP

Paul Mingay Borden Ladner Gervais LLP

Alfred Page Borden Ladner Gervais LLP

Stephen Pincus Goodmans LLP

Emmanuel Pressman Osler, Hoskin & Harcourt LLP

Simon Romano Stikeman Elliott LLP

Jeffrey Singer Stikeman Elliott LLP

David Wilson Davies Ward Phillips & Vineberg LLP

COMMERCIAL – COMING SOON

John Chimienti Canadian Tire Corporation, Limited

Darrel Jarvis Fasken Martineau DuMoulin LLP

Jolanta Malicki St Marys Cement Group

Andrea Safer Royal Bank of Canada

Julia Shin Doi Ryerson University

FINANCE – COMING SOON

Robert A. Balcom George Weston Limited

Chris Besant Gardiner Roberts LLP

Timothy Brown Wells Fargo Bank, N.A.

Robyn Collver Canadian Tire Corporation, Limited

Guy David Gowlings LLP

Jonathan Fleisher Cassels Brock & Blackwell LLP

Lucie V. Gauvin Royal Bank of Canada

Lisa Mantello Goodmans LLP

Stephen Redican Borden Ladner Gervais LLP

Robert M. Scavone McMillan LLP

Jacqueline Shinfield Blake, Cassels & Graydon LLP

Ken Thorlakson Scotiabank

Derek Vesey Davies Ward Phillips & Vineberg LLP

Advisory Boards

Fall 2015 | practicallaw.ca16

Putting Compliancein the Aftermath of the

When it comes to competition law violations, prevention is better than cure.

That’s the message the Competition Bureau wants businesses to take from its newly updated Corporate

Compliance Programs bulletin.

Released in June, the 60-page document marked the first refresh in five years to the Bureau’s guidance on establishing a credible and effective compliance program, which it says is the best way for organizations of all shapes and sizes to steer clear of anti-competitive behaviour.

“The updated Corporate Compliance Programs bulletin provides Canadian businesses with the guidance needed to play by the rules and avoid the pitfalls of anti-competitive behaviour,” said

Commissioner of Competition John Pecman in a statement unveiling the new bulletin.

The new bulletin has a special focus on small- and medium-sized enterprises (SMEs), acknowledging their “different needs and concerns” from larger companies.

“Each business should implement and follow a corporate compliance program that is commensurate with its size and business activities,” reads the bulletin, which promises benefits for smaller companies that take the time and effort to do develop a compliance program.

“First, it enables SMEs to identify areas of high risk of contravention of the Acts. Second, it allows SMEs to determine circumstances where they may be the victim of anti-competitive conduct by other

on the Agenda Bureau’s New Guidelines

By Michael McKiernan

17Practical Law Canada | Fall 2015

parties,” the bulletin reads.

For those that do eventually run into trouble, the bulletin makes clear, for the first time, that a credible and effective compliance program in place at the time of a competition law offence will be considered a mitigating factor in the Bureau’s sentencing recommendations under its Leniency Program for criminal matters. A new Compliance Unit has been established within the Bureau to establish whether or not a particular program meets the required standard. In civil matters, the bulletin says the presence of a strong program could also reduce the size of a monetary penalty or any other punishment sought by the Bureau in deceptive marketing cases.

However, convincing the Compliance Unit that your program meets the Bureau’s exacting standards could prove tough, with the Bureau outlining seven basic requirements of a credible and effective corporate compliance program (up from five in the last version of the guidelines):• Active and continuous support from

management. • Risk-based corporate compliance

assessment to identify which business activities are most in danger of violating the law.

• Policies and procedures that reflect risk and address strategies for avoiding breaking the law in risky situations.

• Training and education for any employees involved in risk areas.

• Monitoring, verification and reporting mechanisms to check management and staff are actually abiding by the program.

• Disciplinary procedures for those who break the rules and incentives for employees who follow them.

• Compliance program evaluation to check whether it actually works.

To help them meet their compliance objectives, the bulletin suggests every company appoint a “Compliance Officer” to take responsibility for the compliance program. According to the Bureau, the title should go to someone in “a high level executive position” with high visibility in the company, as well as the independence and authority to enforce the program.

Practical Law Canada has assembled a round table of some of the most highly sought-after competition law practitioners in the country to give us their thoughts on the Competition Bureau’s new bulletin. Below we examine what they think it all means for lawyers and businesses across Canada.

What is your first reaction to the Bureau’s new compliance materials?Christopher: I think the materials are

helpful because they communicate the Bureau’s views, and I think it’s always good to know what the Bureau sees as important.

James: My reaction is frankly very positive. I think the tone is right; it encourages firms to pursue a compliance agenda. They also put their money where their mouth is in so far as they are prepared to give discounts for imperfect compliance efforts. It’s probably more symbolic than meaningful in a tangible sense, but I think it’s important.

Mark: I would put Canada among the global leaders in terms of providing helpful instructions and guidance on competition compliance, and I think this new bulletin takes it even further. My other general impression is that, in many ways, this really represents the gold standard of what companies in Canada should be doing in terms of competition compliance. I think to that extent it might be slightly unrealistic, so it will be interesting to see how the ideal works in the practical world.

“In a perfect world, it would mean that tomorrow morning, every company CEO and general counsel is going to wake up and say: ‘By God, I need one of these compliance programs, and I need a team of competition lawyers to do it.’”

– MARK KATZ, PARTNER IN THE COMPETITION AND FOREIGN INVESTMENT REVIEW PRACTICE GROUP AT DAVIES WARD PHILLIPS AND VINEBERG LLP

Meet our panellists:Omar Wakil: A partner in the Toronto office of Torys LLP in Toronto, Wakil advises domestic and international clients on the full spectrum of competition law issues.

Mark Katz: Toronto-based Katz is a partner in the competition and foreign investment review practice group at Davies Ward Phillips and Vineberg LLP.

Christopher Putney: In his role as senior legal counsel at Insurance Corporation of British Columbia in Vancouver, Putney advises on a variety of competition law issues.

James Musgrove: McMillan LLP partner Musgrove works out of the firm’s Toronto office and co-chairs its competition and anti-trust practice group.

Fall 2015 | practicallaw.ca18

Omar: It has a lot of positive features, but to be constructively critical, I do have concerns that some of the detailed requirements the Bureau mandates for what they call a “credible and effective” compliance program impose unrealistic burdens on businesses, particularly small- and medium-sized ones. Frankly, it is sometimes challenging to create a fully credible and effective compliance program for even large and sophisticated Canadian businesses, but in an environment where legal expenses are incurred on an as-needed basis, it’s going to be difficult for in-house groups to seek internal budgetary approval for expenses that are sometimes seen as not critical.

Mark: There’s recognition from the Bureau that simply having a bulletin like this that shows up on their website is not enough on its own. It’s really only by getting the competition message out there to industry and to the public that I think this practical compliance document is going to have any real impact. If there is a poor base level of knowledge out there, no one is going to know about or care about a compliance policy, and no one is going to have much of an incentive to adopt one.

Another thing I thought was good is there’s more of an emphasis on tailoring the compliance program to the specific company that you are involved with. It shows sensitivity to the fact that one size doesn’t fit all. The only way that they’re going to be able to get more companies to adopt competition compliance programs and to take the issue seriously, is if they’re sensitive to the fact that not everybody is going to adopt this gold standard.

What do you think prompted the Bureau to update its approach to compliance?Omar: I think compliance has been an important part of Commissioner Pecman’s mandate; it’s a recurring theme every time he has a public forum to talk about anything in the Competition Act, and appropriately so. I think he wants to perhaps differentiate himself from his predecessor, who was focussed on enforcement and bringing cases against companies. I think he would rather promote voluntary compliance with the Act and ensure businesses are doing what

they can to not get in trouble, as opposed to going after them when they do contravene the Act.

What do you see as the most important changes?Christopher: One thing was the introduction of this concept of a compliance officer. This person would ideally be responsible for administering the program, be appointed by the board of directors and accountable to it. I think for most businesses that might be a tall order, because it doesn’t quite fit within their business organization. In my own experience, it seems that senior management and the CEO want to manage the relationship between the company and the board, and I don’t know how anxious they would be to have a compliance officer that is solely accountable to the board. We are in the process now of reviewing the Bureau’s materials and deciding if we need a compliance officer, because it’s not something we have now.

Mark: None of the clients I deal with have anything that comes close to approximating the compliance officer envisioned by the Bureau. Usually the compliance function falls under the responsibility of the general counsel or someone in the legal department, and sometimes it’s hived off to someone in human resources. It’s a good thing to emphasize the importance of compliance, and it will be great if adopted, but we’ll have to see how many do.

How will the changes affect your work?James: I’ve already seen renewed interest from clients, typically in-house people who have compliance responsibilities. They want to check their compliance policies, update them, and see if they’re still appropriate, and this is a tool for them to use with management to encourage compliance efforts.

Omar: I think it’s going to be an important reference tool when preparing compliance programs, because it provides a checklist of things that ought to be in there when you do get a mandate from a client. It’ll be a useful guide, but I’m not sure if it, in and of itself, is going to provide an impetus for businesses to create compliance programs

where they haven’t existed previously.

Mark: In a perfect world, it would mean that tomorrow morning, every company CEO and general counsel is going to wake up and say: “By God, I need one of these compliance programs, and I need a team of competition lawyers to do it.” That’s not going to happen. When we do go out and tell clients that competition compliance is important, this will give us an additional resource, because it’s obvious that the Competition Bureau is paying attention.

Christopher: I don’t think it’s going to affect my work a great deal, simply because we already have a compliance policy, and in fact we updated it last year. We have also taken steps to raise awareness of competition law issues within our organization, so it’s something that we’re already doing quite a bit of work on.

Leniency Program discounts are now potentially available for effective compliance programs—what are the implications of this change?Omar: I welcome it in principle. I’ve had situations before this new bulletin where the Bureau was reluctant to assess the credibility and effectiveness of compliance programs. They said it’s not their job to take a detailed look at a compliance program and decide whether or not it was satisfactory. If the suggestion is that they will do that, then that’s a change in policy, and it will be interesting to see whether it’s going to work and what sort of burden it will place on the new Compliance Unit that will be responsible for assessments.

Mark: This is a big step that puts the Bureau ahead of some jurisdictions like the U.S., where the position is basically this, “If you had a really credible and effective compliance policy, you wouldn’t be in trouble to begin with, so we’re not going to give you credit for what you may or may not have done. We’ll only give you credit if now you take extraordinary steps to revamp your compliance culture.” It’s very much forward looking, rather than backward looking. I think what the Bureau is contemplating is something that is potentially more backward looking as well.

The only thing harder than fi nding the right legal document is losing it and trying to quickly fi nd it again.

With WestlawNext Canada, the information you fi nd remains found – and organized. Effortlessly drag and drop key cases and documents into folders. Easily highlight and annotate documents as you go.

Discover more at westlawnextcanada.com

00231LE-A52090

HELPING YOU TO BE MORE EFFICIENT, EFFECTIVE AND CONFIDENT.

The only thing harder than fi nding the right legal document is losing it and trying to quickly fi nd it again.

With WestlawNext Canada, the information you fi nd remains found – and organized. Effortlessly drag and drop key cases and documents into folders. Easily highlight and annotate documents as you go.

Discover more at westlawnextcanada.com

00231LE-A52090

HELPING YOU TO BE MORE EFFICIENT, EFFECTIVE AND CONFIDENT.

Fall 2015 | practicallaw.ca20

However, if the bureau’s guideline is the standard for what a credible and effective compliance program will be, the bar may be set unrealistically high. If they adhere to these requirements very strictly, it may very well mean that in practice, nobody is ever going to get credit in circumstances where otherwise it might seem possible.

Omar: I’m skeptical that the change is going to have a practical impact on the setting of fines. First, the bulletin doesn’t give any concrete numbers around the extent of the discount, so it’s not clear whether any discount is going to be material. Second, in practice, mitigating factors in sentencing fines are not particularized or transparent. The bureau has considerable discretion in fixing fines or discounts, so there’s nothing firm that you can point to and say, “Why are we not getting our 5% discount,” and have them justify it.

The bulletin also notes that where managers participated in the conduct or were willfully blind, contravening the legislation despite this program may be an aggravating factor. So you get out of the woods just by having a credible and effective compliance program, but you can still be faced with the situation of aggravating factors where managers were involved. This goes back to a tension that has always existed with compliance programs: if you have one that people were ignoring, is that worse than not having one at all? It shows you knew what you were doing was wrong, and you still did it and tried to cover up your illegal conduct.

Do you see more potential risk now for organizations without effective compliance programs?James: As a practical matter, I think there probably is more risk for them. If you’re in the soup with a decent policy that just didn’t succeed, obviously you’ve got things to talk about with the Bureau by way of mitigation. You’ve got less to talk about if you don’t have one at all. The other point that the policy makes is that even in cases where companies don’t have effective policies when things go awry, if they adopt one voluntarily, having discovered things have gone awry, that in itself is an advantageous

mark. So it’s better to have had it in place originally, but if you adopt one quickly that is going to be helpful too.

Trade associations are prominently featured in the new compliance materials—what are the key take-aways for them?James: Trade associations face risks, but it’s their members that face probably the bigger risks. Historically, a number of the cases the Bureau has brought arose out of a trade association context. That’s where discussions got started, where people got to know each other and then led themselves astray in some way. The bulletin is a reminder that this is one of those places where bad discussions can happen and do in fact happen.

I think it is a clever move to say that one of the indicia that the Bureau will look for in determining whether a particular company has an effective compliance policy is if they insist on the trade associations to which they belong also having one. All it takes is for one member to say, “Look, I don’t think our association has a robust enough compliance policy,” for that to happen, which will have beneficial effects.

What are some key things organizations need to do after the changes?Omar: I’m skeptical as to how many will actually do it, but it would be prudent for organizations to take a look at their compliance programs, compare it to what the bulletin identifies as constituting the critical elements, and think about whether or not their current policy is up to scratch. They should take this as an opportunity for an upgrade.

James: This is a perfect opportunity and incentive to get out your compliance policy, look at it, and ask how well it works. It won’t be perfect, because nothing ever is, but think about how you can make it better. Knowing your business, think about where the real risks are and about how you can devise a policy that helps minimize those danger points.

After that comes the hardest part: ongoing monitoring of the policy to make sure it’s

working. Think about how you’re going to institutionalize some sort of monitoring to check that things are okay and what steps you can take to improve if they’re not. Most organizations have pretty good looking policies written down, but the question is how they’re made alive. That is where relatively few organizations are effective, and I think this is an incentive to be.

Mark: The other part of it though is that the Competition Bureau has a job to do, and for the law to be taken seriously, it has to be enforced in a serious manner. In several cases recently, the Bureau has lost and has really taken it on the chin. I think it highlights a problem they have, which is that their litigation abilities and capabilities seem to be substandard.

To make sure that the competition law is taken seriously, they have to really look at what they are doing in terms of picking cases and, moving forward, prosecuting those cases. They need to take a really serious look at the criteria and procedures they use, , and figure out a way that if they are actually going to go out and enforce a case, that they’re going to win.

What are some key things you think in-house counsel will need to do after the changes?Christopher: If an organization doesn’t have a competition law compliance program, now would be a good time to get one. I also think the Bureau has made it quite easy to create one, because it does have a basic template in the materials that you can follow. If organizations do have a policy, it would be good to review it in light of the latest materials. The bulletin represents perhaps the Bureau’s view of an optimal program. For several organizations, the optimal program may be a bit too intensive, but I think it’s good to do as much as you can.

I think senior management support is essential, and you should be engaging them on a regular basis to raise awareness of competition law issues. I think the release of these materials is a great opportunity for in-house counsel to raise the issue in their organization.

SEAN FARRELL joined the Capital Markets and Securities team from McMillan LLP, where he was a partner specializing in securities and public markets transactions with a particular emphasis on domestic and cross-border offerings of securities and mergers and acquisitions. He has been recognized in Chambers Global for Corporate M&A, The

Canadian Legal Lexpert® Directory for Corporate Finance & Securities and the Legal Media Group’s Guide to the World’s Leading Corporate Governance Lawyers. Sean is also a counsel to Fasken Martineau DuMoulin LLP.

WAYNE GRAY, Corporate and M&A practice lead, joined from McMillan LLP, where he was a partner in the business law group, specializing in corporate law, M&A transactions and corporate governance. Previously he was a partner in the corporate-commercial group at Miller Thomson LLP. He is recognized as a leading corporate

mid-market lawyer in The Canadian Legal Lexpert® Directory and The Lexpert®/American Lawyer Guide to the Leading 500 Lawyers in Canada and for corporate law, private equity and secured lending in Martindale-Hubbell.

MONIQUE RABIDEAU, Capital Markets and Securities practice lead, joined from Fogler, Rubinoff LLP where she was a partner in the business law group, specializing in corporate and securities law. She assisted a variety of businesses with their legal needs and acted as secretary to many boards of directors. Clients ranged from private corporations to publicly-

traded conglomerates mostly operating in Canada and the US but also Europe, Asia and the Caribbean.

ANGELA SCOTT joined the Capital Markets and Securities team and is a sole practitioner in association with Cognition LLP where she advises private and public clients on corporate, commercial and securities law. Previously she was an associate with Blake, Cassels & Graydon LLP in the securities department, specializing in corporate,

securities, finance and merger and acquisition transactions.

CANDACE SOLOMON joined the Corporate and M&A team from Royal Bank of Canada, where she was senior counsel with the award-winning M&A legal team. Previously she was partner with Cassels Brock & Blackwell LLP in the securities group, specializing in corporate finance and M&A transactions.

STEVE SZENTEZI practised at some of Canada’s leading business law firms including Davies Ward Phillips & Vineberg LLP (Toronto) and McMillan LLP (Vancouver) as well as Linklaters LLP in the UK. Steve also practised as in-house competition counsel for The Canadian Real Estate Association in Ottawa. He has advised on numerous competition law

matters in the abuse of dominance, conspiracy, compliance, pricing and distribution and advertising and marketing law areas, among others. Steve has also spoken and published widely in the Canadian competition law area.

LYNN VAN DER VALK joined the Corporate and M&A team from Cara Operations Limited, where she was legal counsel, focusing on franchising, corporate governance, acquisitions, and commercial matters. Previously, Lynn was an associate with McMillan LLP’s business law group, specializing in M&A transactions, corporate law and corporate governance.

Meet our Team of Practical Law Canada ExpertsThe key to our online services is the editorial team behind them. Our lawyer-editors come from Canada’s leading law firms and legal departments. Meet the lawyer-editors that specialize in Corporate and M&A, Capital Markets and Securities and Competition law.

To learn more about the team, visit www.practicallaw.ca

00231LE-A51077

Fall 2015 | practicallaw.ca22

PROFILE GET TO KNOW THE PEOPLE WORKING FOR YOU

Steve SzentesiPRACTICAL LAW CANADA’S LAWYER-EDITOR

There aren’t many perspectives Steve Szentesi hasn’t taken on in the world of competition law.

During a 15-year legal career, he has criss-crossed Canada, practising competition law with two of the

country’s largest firms in offices on either side of the country before founding his own law firm offering competition and regulatory law advice to clients of all sizes.

In between, Szentesi also managed a stint in house, advising Canadian Real Estate Association (CREA) members on competition and anti-trust matters, as well as some time in the global capital of the financial world, working for London-based Linklaters LLP (a member of the fabled Magic Circle, a group of the U.K.’s five most prestigious commercial law firms). The latest port of call on Szentesi’s legal adventure is Practical Law Canada’s Toronto headquarters, where he takes on the role of lawyer-editor for the service’s newly launched competition law offering.

Richard Lyall, the president of RESCON, a Greater Toronto association of low-rise and high-rise builders that hired Szentesi as its competition counsel five years ago, says subscribers could not have a more accomplished guide to help lead them through the notoriously complicated field of competition law.

“He lives and breathes competition law,” Lyall says, adding that Szentesi’s international experience also came in useful during their dealings.

“He’s right up on the minutiae of the law in Canada, but he’s also very current on developments in other jurisdictions that could have a bearing on Canada,” Lyall says. “I love benchmarking stuff, so when I look at competition law, I’m not interested in just looking at the Canadian context. You’ve got to look at the U.K., Hong Kong, the U.S., and other places with similar laws to ours to see what developments are happening there.”

Szentesi never actually intended to be a competition lawyer. When he set out to study law at Dalhousie University in Halifax, he had a different end-game in mind.

“I went to law school to be a securities lawyer. I wanted to practice securities law in a big firm on Bay Street, which is exactly what I did,” Szentesi says.

However, it didn’t take long before he felt the pull of anti-trust work. As early as his articling year at Davies Ward Phillips and Vineberg LLP, Szentesi found himself drawn to the competition law practice group where he was able to work under the wings of some of the country’s most renowned practitioners in the area, including the future Federal Court Chief Justice Paul Crampton, who was then a competition law partner at Davies in Toronto.

“Before I went to Davies, I wasn’t at all familiar with competition law. I started out there working on corporate commercial and securities work, but I was very quickly roped into the competition group, where I was lucky enough to work with some very talented people,” says Szentesi. “I was very involved in competition work during my three years there, and I became completely captivated by the area.”

Since then, he’s never looked back.

“I love competition law because of the way it mixes the law and economics, but also policy, where the aim is to make the markets operate more efficiently,” Szentesi says. “One of the things I tell lawyers that are starting out about competition law is that it’s loaded with ideas. It literally does shape public policy and the markets. Competition is very important to the market, and I think all participants and all Canadians need to take an interest in the way markets operate. All of that is very fascinating to me and has remained fascinating over the last 15 years or so.”

Szentesi’s next step after Davies took him to Ottawa where he was in-house competition counsel to the CREA, advising the organization’s board of directors, as well as its 100 individual real estate boards and associations across Canada. The job also added another couple of dimensions to his competition practice.

“There was a compliance aspect, so the association needed to think about compliance measures. You need to have a relationship with the regulator so that you are seen as credible and trustworthy,” he says. “The other thing was advocacy and policy work, because large important associations are typically engaged with regulators in terms of issues that arise. It was a very interesting opportunity to have a job that was broader than just counselling for clients.”

“My time at CREA also got me interested in competition law

23Practical Law Canada | Fall 2015

and associations,” says Szentesi, noting that the area has attracted renewed recent attention from the Competition Bureau and, in turn, from the Practical Law Canada team as it constructs the competition law service.

Szentesi crossed the country again in 2005, leaving the CREA to return to private practice with Lang Michener LLP in Vancouver, before the firm changed its name following its merger with McMillan LLP. His next move was across the Atlantic Ocean, where he worked with global legal giant Linklaters on multi-jurisdictional merger deals.

“It gave me an opportunity to see competition on a global scale. At Davies and McMillan, you end up working on some impressive matters, but what I saw in London was different in terms of the scale and size of the deals. You see the cross-border aspect a lot more at global law firms,” he says. “Linklaters would often be leading the transaction, and we’d be working with local counsel in several jurisdictions. You really got a chance to see the global implications of your client’s business.”

The experience set Szentesi up perfectly to found his own law firm. “That training was a fantastic segue into my own practice,” he says. “It was very influential for me.”

With a focus on competition, regulatory and advertising law, Szentesi began servicing clients of all sizes from offices in both Vancouver and Toronto in 2008. Upon his return to Canada, he says he found clients more knowledgeable about competition law issues, thanks to the increasing public profile of competition law issues, and more willing than ever to experiment with their legal service providers.

“Clients are looking for lawyers who can work in an efficient and cost-effective manner, and there’s increasing flexibility in the provision of legal services,” he says.

According to Szentesi, Practical Law Canada’s competition law offering has arrived at the perfect time to take advantage of the upheaval going on in the legal sector at the moment.

“It goes with development of options in the provision of legal

services. This is a very innovative option for both general counsel and external counsel,” he says.

Szentesi says the checklists, standard documents, practice notes and legal updates produced by his team, covering core competition topics including abuse of dominance, cartels and compliance, will help lawyers translate competition law issues into terms clients can understand, whatever their own level of expertise.

“Clients increasingly want to better understand the advice they are getting. That can be a challenge even for lawyers who regularly practise competition law because it’s a very technical area of the law. It’s even more difficult for lawyers that don’t necessarily work in the area on a regular basis,” he says. “What I like is that the

format and style of the offering is to provide a very clear, very practical set of materials for both specialists and non-specialists. This is not your traditional lawyer boilerplate advice that may or may not be intelligible to clients.”

Lyall, for one, has faith in Szentesi’s ability to engage with subscribers on the new competition law service.

“Let’s face it, competition law, like so many other things, is complicated. I personally find it interesting, but for most business people, it’s something they have to pay attention to, not the really exciting part of their work. But Steve makes it interesting. He’s not a boring guy at all,” Lyall says. “He’s a great teacher. He’s very good at summarizing complex issues and, in response to what are very complex questions, he gives very clear answers.”

Steve Szentesi

Fall 2015 | practicallaw.ca24

Competition Compliance Toolkit

The federal Competition Act, R.S.C. 1985, c. C-34, contains criminal and civil sections prohibiting or regulating a range

of conduct that can arise in business activities (for example, in the course of supplier and customer relations, trade associations, dealings with competitors, mergers or commercial agreements).

The criminal parts of the Competition Act include offences relating to criminal conspiracies, bid-rigging, criminal misleading advertising, deceptive telemarketing and pyramid selling schemes. Civil reviewable matters under the Competition Act include abuse of dominance, civil misleading advertising, refusals to deal, price maintenance and certain types of vertical restraints that prevent or lessen competition substantially.

The potential penalties for violation of the Competition Act can be severe and include criminal fines of up to $25 million, imprisonment for up to 14 years, court orders to stop engaging in conduct and administrative monetary penalties of up to $10 million. Directors and officers are also potentially liable for Competition Act violations. In this respect, it is common for employees and directors and officers of companies to be involved in Competition Bureau (Bureau) investigations (and in some cases be convicted of competition law offences) and to be named as parties in competition law related civil actions.

Because a competition law investigation,

prosecution or civil action can have severe consequences, companies must ensure that they have an effective competition law compliance program in place. A competition law compliance program helps companies by:

• Educating employees about conduct that violates competition laws and the potential penalties.

• Providing employees and executives with efficient means to identify and report suspected violations.

• Encouraging early detection of any violations that do occur, allowing the company to take corrective measures or seek immunity or leniency from the Bureau.

The following is a selection of key content to help counsel create, implement and audit a company’s competition law compliance program, as well as compliance resources for specific types of activities.

PRACTICE NOTE: OVERVIEWSn Canadian Competition Law: Overview

PRACTICE NOTESn Competition Law Compliance Programsn Cooperating with Competitors –

Business Briefingn Document Creation and

Communicationsn Establishing and Avoiding a

Conspiracy Agreementn Information Exchanges

Between Competitors

STANDARD DOCUMENTSn Competition Law Compliance Programsn Competition Law Hypotheticals for

Compliance Training - Dealings with Competitors

n Employee Certification Lettern Memorandum – Document Creation in

Preperation for a Transactionn Memorandum – gun-jumping

CHECKLISTSn Avoiding Gun-jumping in Corporate

Transactions Checklistn Competition Law Audit Checklist For

Trade Associationsn Competition Law Compliance

Audit Checklistn Conduct of Meetings Checklistn Cooperating with Competitors

Checklistn Creating Strategic Documents Checklist

(Notification Form, Section 6)n Detecting Bid-rigging Checklistn Deterring Bid-rigging Checklistn Document Creation Checklistn Factors to Assess the Competition

Law Risk of Information Exchangesn How to Avoid Entering a Conspiracy

Agreement Checklistn Information Exchange Checklistn Joint Venture Competition

Compliance Checklistn Resale Price Maintenance Checklistn Search and Seizure Checklistn Trade Association Participation

Checklistn Unilateral Refusals to Deal Checklist

(Factors to Assess Risk)

TOOLKITS PRACTICAL LAW CANADA COMPETITION

Below is an excerpt from a Toolkit that provides resources to guide counsel in creating, implementing and auditing a company’s competition law compliance program. This Toolkit also includes materials that can be used for competition law compliance in specific circumstances (for example, in relation to document creation, information exchanges and surveys, preparation for a merger, meetings with competitors, trade association activities, and joint ventures). or the complete, continuously maintained version of this Toolkit, visit practicallaw.ca.

Practical Law Canada Competition

25Practical Law Canada | Fall 2015

Practical Law Canada Competition

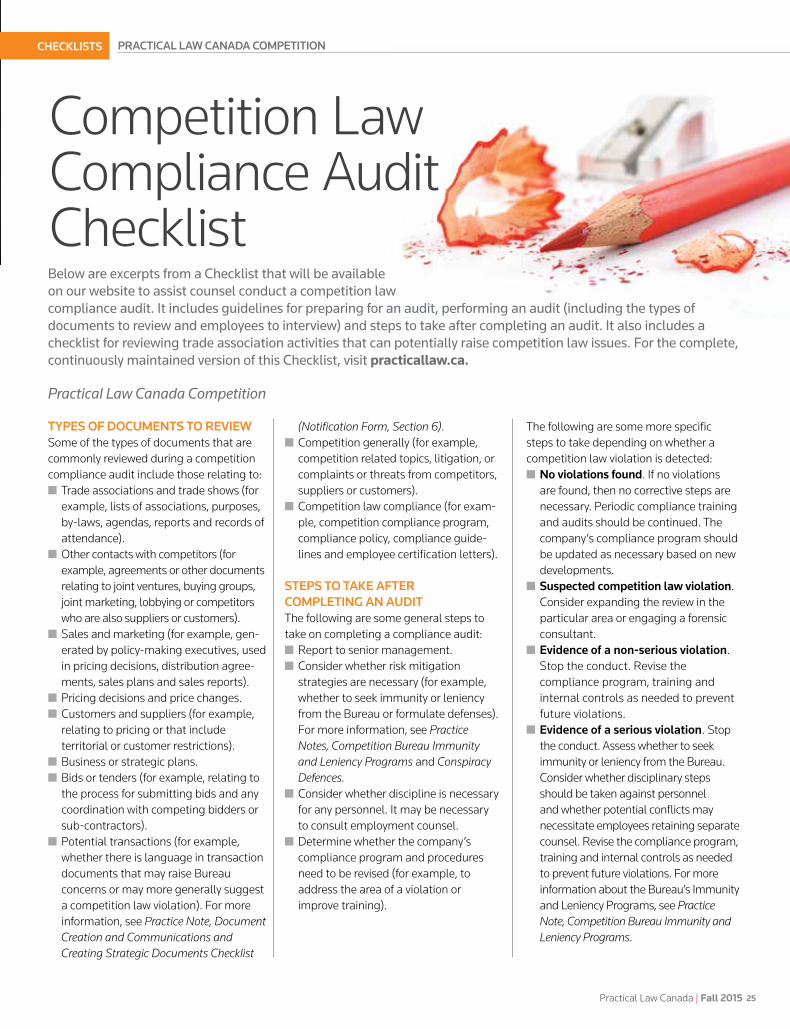

TYPES OF DOCUMENTS TO REVIEWSome of the types of documents that are commonly reviewed during a competition compliance audit include those relating to:n Trade associations and trade shows (for

example, lists of associations, purposes, by-laws, agendas, reports and records of attendance).

n Other contacts with competitors (for example, agreements or other documents relating to joint ventures, buying groups, joint marketing, lobbying or competitors who are also suppliers or customers).

n Sales and marketing (for example, gen-erated by policy-making executives, used in pricing decisions, distribution agree-ments, sales plans and sales reports).

n Pricing decisions and price changes.n Customers and suppliers (for example,

relating to pricing or that include territorial or customer restrictions).

n Business or strategic plans.n Bids or tenders (for example, relating to

the process for submitting bids and any coordination with competing bidders or sub-contractors).

n Potential transactions (for example, whether there is language in transaction documents that may raise Bureau concerns or may more generally suggest a competition law violation). For more information, see Practice Note, Document Creation and Communications and Creating Strategic Documents Checklist

(Notification Form, Section 6).n Competition generally (for example,

competition related topics, litigation, or complaints or threats from competitors, suppliers or customers).

n Competition law compliance (for exam-ple, competition compliance program, compliance policy, compliance guide-lines and employee certification letters).

STEPS TO TAKE AFTER COMPLETING AN AUDITThe following are some general steps to take on completing a compliance audit:n Report to senior management.n Consider whether risk mitigation

strategies are necessary (for example, whether to seek immunity or leniency from the Bureau or formulate defenses). For more information, see Practice Notes, Competition Bureau Immunity and Leniency Programs and Conspiracy Defences.

n Consider whether discipline is necessary for any personnel. It may be necessary to consult employment counsel.

n Determine whether the company’s compliance program and procedures need to be revised (for example, to address the area of a violation or improve training).

The following are some more specific steps to take depending on whether a competition law violation is detected:n No violations found. If no violations

are found, then no corrective steps are necessary. Periodic compliance training and audits should be continued. The company’s compliance program should be updated as necessary based on new developments.

n Suspected competition law violation. Consider expanding the review in the particular area or engaging a forensic consultant.

n Evidence of a non-serious violation. Stop the conduct. Revise the compliance program, training and internal controls as needed to prevent future violations.