Embed Size (px)

Citation preview

Practical issues u/s 6(2) of Practical issues u/s 6(2) of the the

CST Act CST Act

Presentation by Presentation by CA Rajat Talati, Mumbai CA Rajat Talati, Mumbai

on 24.6.2014 on 24.6.2014

Organised by STPAMOrganised by STPAM1010thth Study Circle Meeting Study Circle Meeting

[email protected]@talatico.com

CA Rajat B. Talati, Mumbai.

Sec 6(2) – In-transit SaleSec 6(2) – In-transit Sale

Notwithstanding anything – 6(1) & 6(1A)Notwithstanding anything – 6(1) & 6(1A) Where sale – in the course of interstate Where sale – in the course of interstate

trade or commercetrade or commerce Has either occasioned the movement ORHas either occasioned the movement OR Has been effected by transfer of document of Has been effected by transfer of document of

tittle to such goods tittle to such goods To a RDTo a RD

Requires to read sec 3(b) along with sec Requires to read sec 3(b) along with sec 6(2)6(2)

2

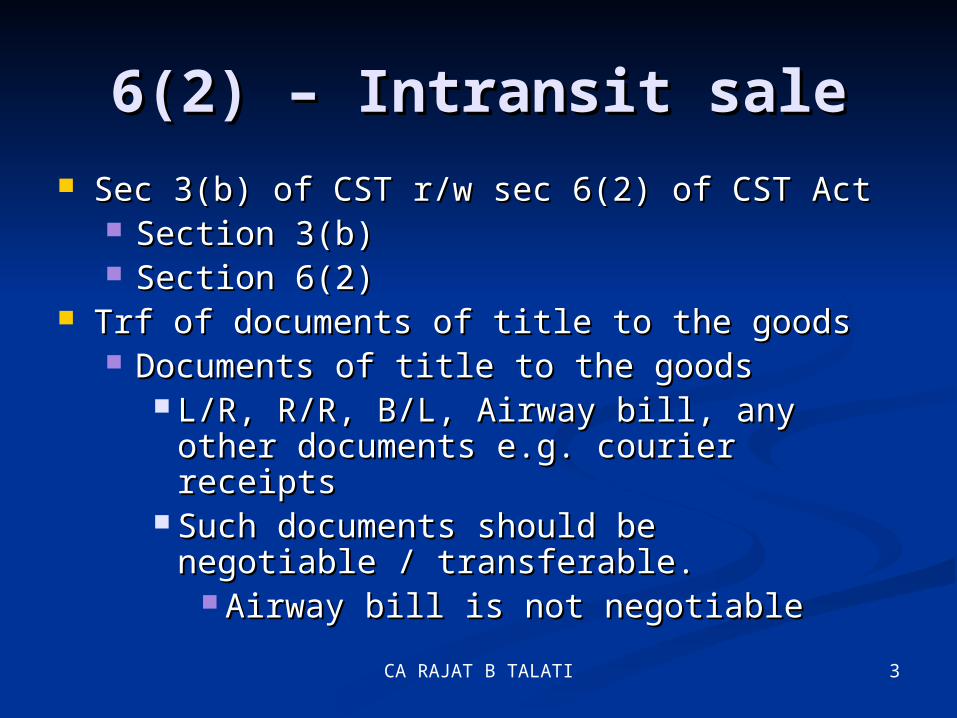

6(2) – Intransit sale6(2) – Intransit sale Sec 3(b) of CST r/w sec 6(2) of CST Act Sec 3(b) of CST r/w sec 6(2) of CST Act

Section 3(b)Section 3(b) Section 6(2)Section 6(2)

Trf of documents of title to the goods Trf of documents of title to the goods Documents of title to the goodsDocuments of title to the goods

L/R, R/R, B/L, Airway bill, any other L/R, R/R, B/L, Airway bill, any other documents e.g. courier receiptsdocuments e.g. courier receipts

Such documents should be negotiable / Such documents should be negotiable / transferable.transferable.

Airway bill is not negotiableAirway bill is not negotiable

CA RAJAT B TALATI 3

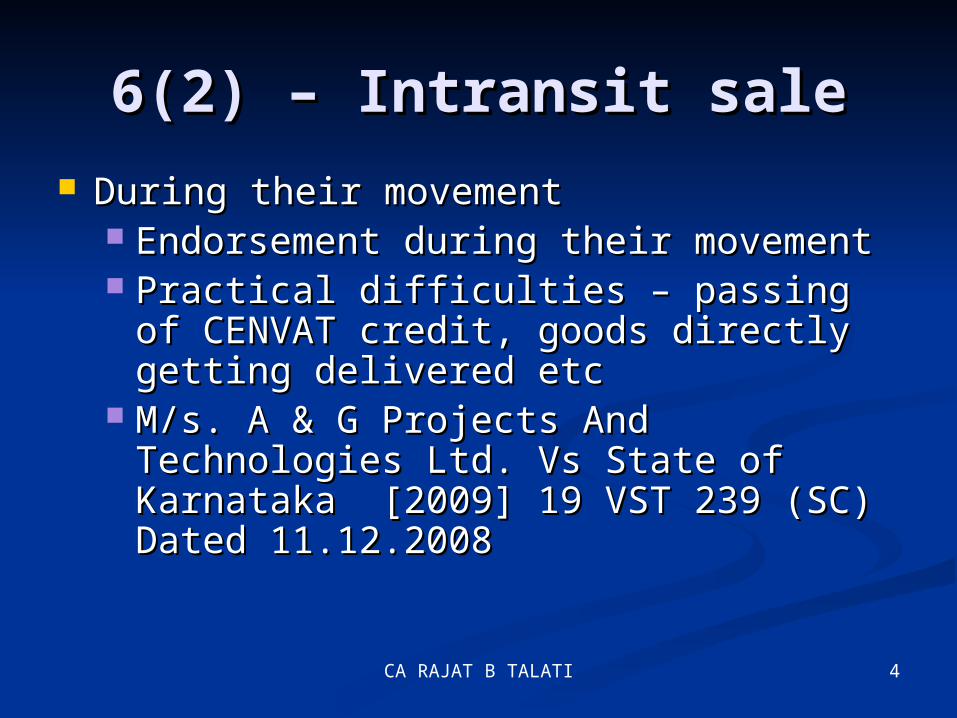

6(2) – Intransit sale6(2) – Intransit sale During their movement During their movement

Endorsement during their movementEndorsement during their movement Practical difficulties – passing of Practical difficulties – passing of

CENVAT credit, goods directly getting CENVAT credit, goods directly getting delivered etcdelivered etc

M/s. A & G Projects And Technologies M/s. A & G Projects And Technologies Ltd. Vs State of Karnataka [2009] 19 Ltd. Vs State of Karnataka [2009] 19 VST 239 (SC) Dated 11.12.2008VST 239 (SC) Dated 11.12.2008

CA RAJAT B TALATI 4

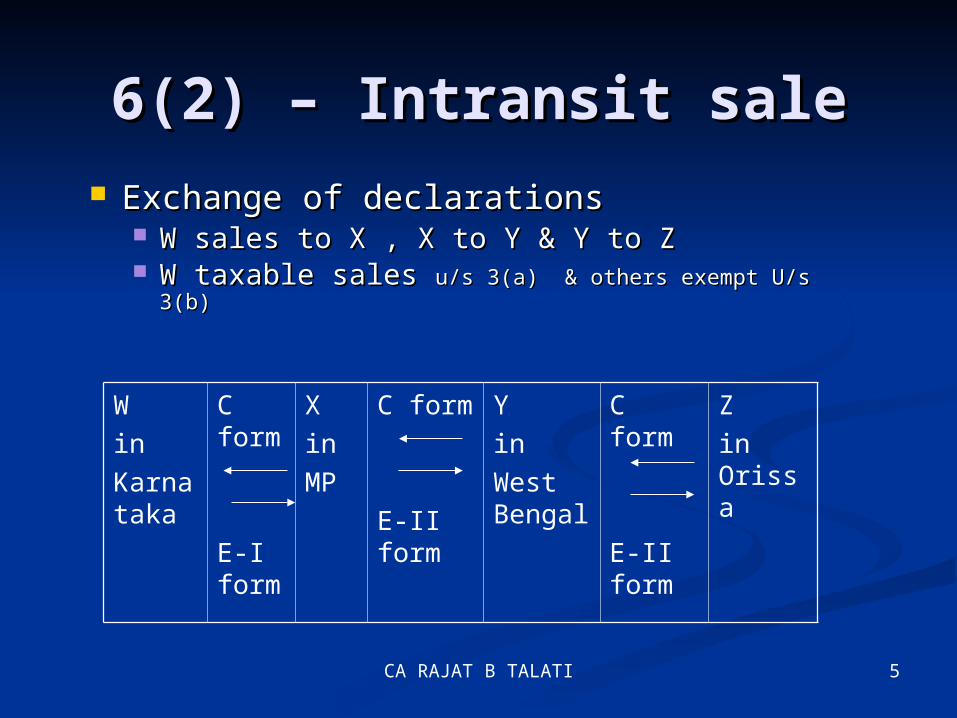

6(2) – Intransit sale6(2) – Intransit sale Exchange of declarations Exchange of declarations

W sales to X , X to Y & Y to ZW sales to X , X to Y & Y to Z W taxable sales W taxable sales u/s 3(a) & others exempt U/s 3(b)u/s 3(a) & others exempt U/s 3(b)

Win Karnataka

C form

E-I form

X in MP

C form

E-II form

Y in West Bengal

C form

E-II form

Z in Orissa

CA RAJAT B TALATI 5

6(2) – Intransit sale6(2) – Intransit sale Taxability of 6(2) transactionTaxability of 6(2) transaction

Non-receipt of forms – levy Non-receipt of forms – levy of tax of tax

STATUS OF THE TRANSACTION PRODUCT TAX RATE 4% 12.50% TAX RATE APPLICABLE

C & E1 BOTH NOT RECD As per the original trans

C RECEIVED E1 NOT RECD 2% 2%

E1 RECEIVED C NOT RECD 4% 12.50%

C & E1 BOTH NOT RECD 4% 12.5%

CA RAJAT B TALATI6

CA Rajat B. Talati, Mumbai.

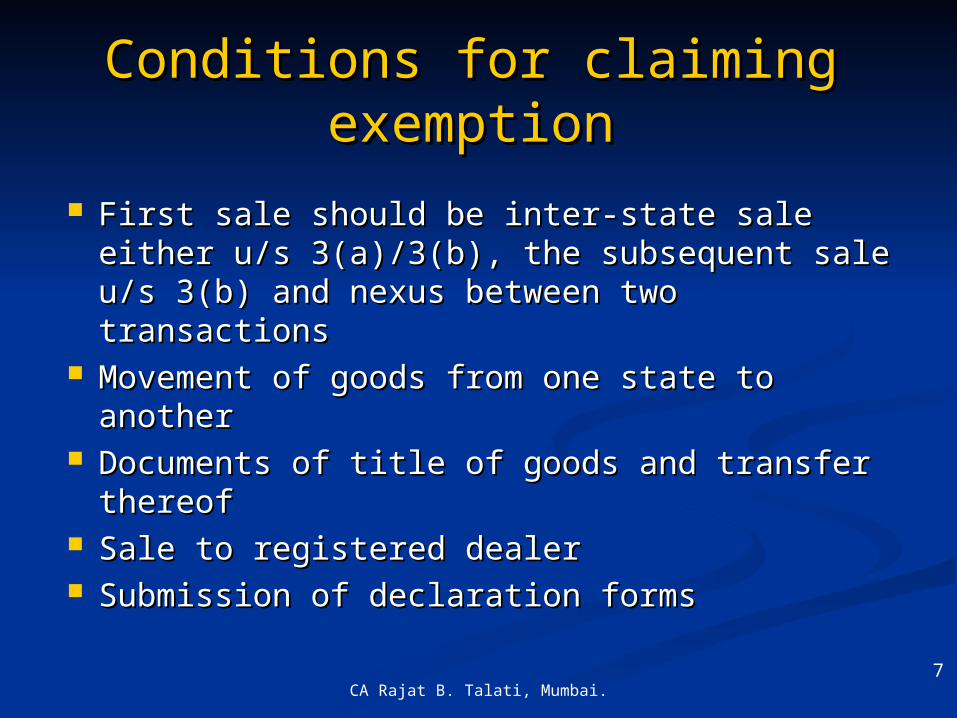

Conditions for claiming Conditions for claiming exemptionexemption

First sale should be inter-state sale either First sale should be inter-state sale either u/s 3(a)/3(b), the subsequent sale u/s 3(b) u/s 3(a)/3(b), the subsequent sale u/s 3(b) and nexus between two transactionsand nexus between two transactions

Movement of goods from one state to Movement of goods from one state to anotheranother

Documents of title of goods and transfer Documents of title of goods and transfer thereofthereof

Sale to registered dealerSale to registered dealer Submission of declaration formsSubmission of declaration forms

7

CA Rajat B. Talati, Mumbai.

During the movement - Sec During the movement - Sec 3(b) – Expl3(b) – Expl

CommencementCommencement – – deemed deemed – at the time of – at the time of delivery of such goods to the common delivery of such goods to the common carrier carrier or or baileebailee

TerminateTerminate – when delivery taken from – when delivery taken from common common carrier carrier or or baileebailee

If commencement & termination in same If commencement & termination in same state – not a interstate – sale – even if goods state – not a interstate – sale – even if goods pass through any other statepass through any other state

Between commencement & termination is Between commencement & termination is ‘during their movement’.‘during their movement’.

8

CA Rajat B. Talati, Mumbai.

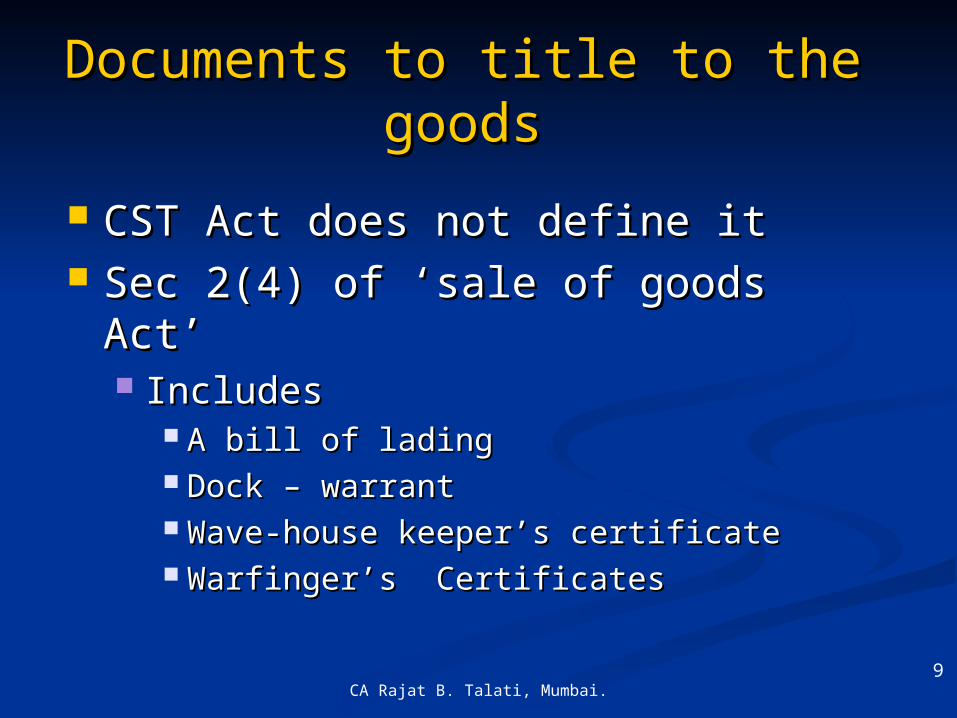

Documents to title to the Documents to title to the goodsgoods

CST Act does not define itCST Act does not define it Sec 2(4) of ‘sale of goods Act’Sec 2(4) of ‘sale of goods Act’

IncludesIncludes A bill of ladingA bill of lading Dock – warrantDock – warrant Wave-house keeper’s certificateWave-house keeper’s certificate Warfinger’s CertificatesWarfinger’s Certificates

9

CA Rajat B. Talati, Mumbai.

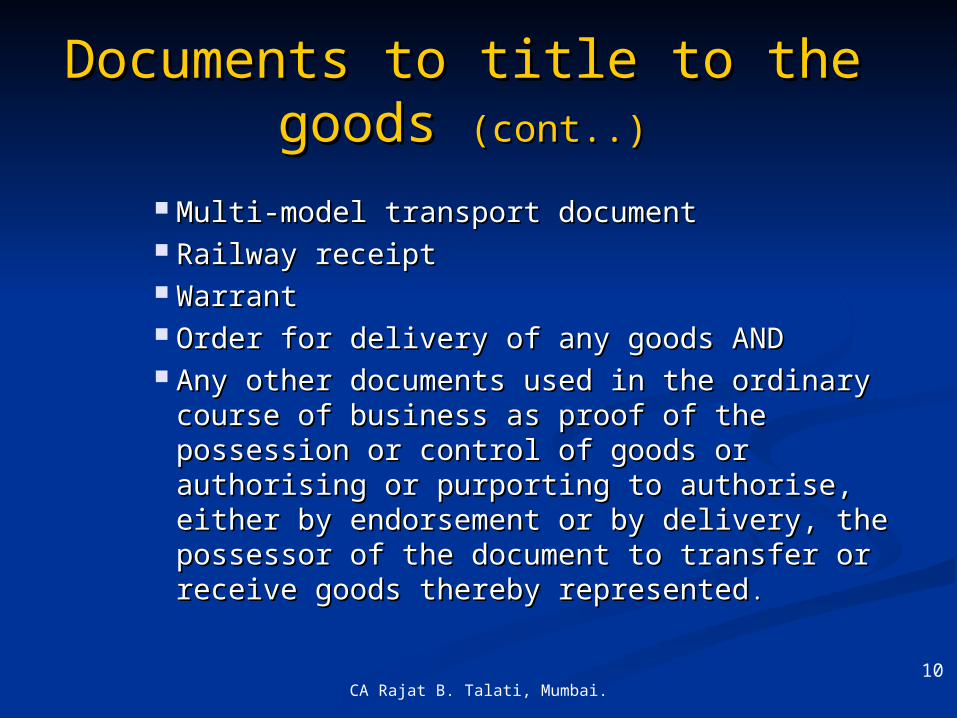

Documents to title to the Documents to title to the goods goods (cont..)(cont..)

Multi-model transport documentMulti-model transport document Railway receiptRailway receipt WarrantWarrant Order for delivery of any goods ANDOrder for delivery of any goods AND Any other documents used in the ordinary Any other documents used in the ordinary

course of business as proof of the course of business as proof of the possession or control of goods or possession or control of goods or authorising or purporting to authorise, authorising or purporting to authorise, either by endorsement or by delivery, the either by endorsement or by delivery, the possessor of the document to transfer or possessor of the document to transfer or receive goods thereby representedreceive goods thereby represented ..

10

CA Rajat B. Talati, Mumbai.

Where ‘not negotiable’ mentioned - not a Where ‘not negotiable’ mentioned - not a document of title to the goods. document of title to the goods.

Commonly taken as ‘document title to goods’.Commonly taken as ‘document title to goods’. Delivery order asking commission agent / Delivery order asking commission agent /

bankers to deliver.bankers to deliver. Angadia receiptAngadia receipt

Is it a document of tittle or ‘a delivery order’?Is it a document of tittle or ‘a delivery order’? Does customer to ask for further action to be done Does customer to ask for further action to be done

before goods are delivered? If yes, than it is not before goods are delivered? If yes, than it is not document of title to the goodsdocument of title to the goods

Courier receipt ………?Courier receipt ………?

11

Documents to title to the Documents to title to the goods goods (cont..)(cont..)

CA Rajat B. Talati, Mumbai.

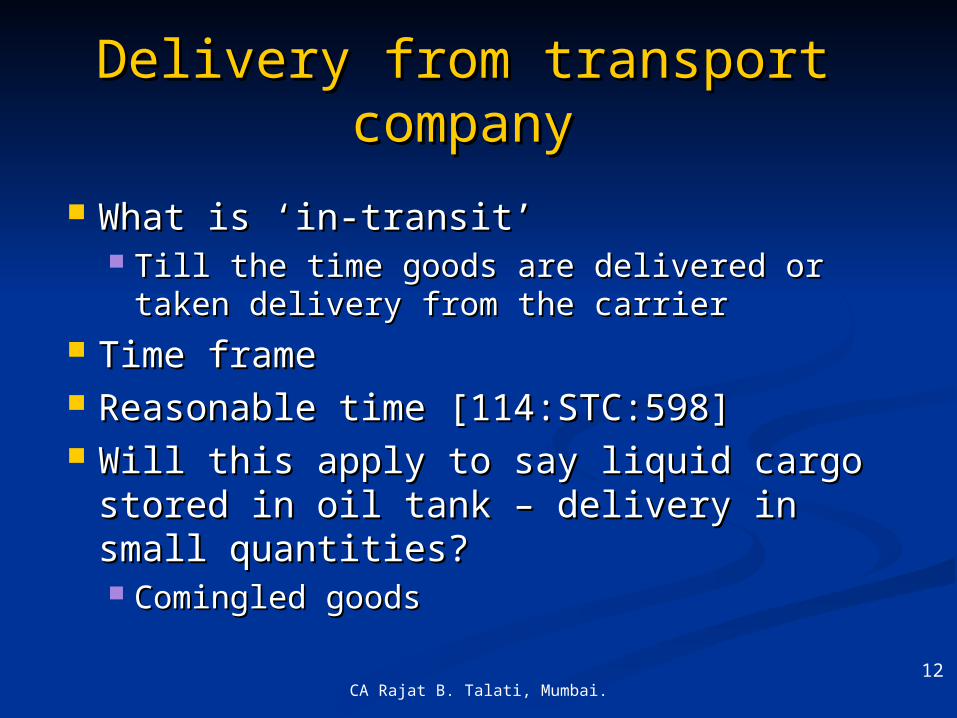

Delivery from transport Delivery from transport companycompany

What is ‘in-transit’What is ‘in-transit’ Till the time goods are delivered or taken Till the time goods are delivered or taken

delivery from the carrierdelivery from the carrier Time frameTime frame Reasonable time [114:STC:598]Reasonable time [114:STC:598] Will this apply to say liquid cargo stored Will this apply to say liquid cargo stored

in oil tank – delivery in small quantities?in oil tank – delivery in small quantities? Comingled goodsComingled goods

12

CA Rajat B. Talati, Mumbai.

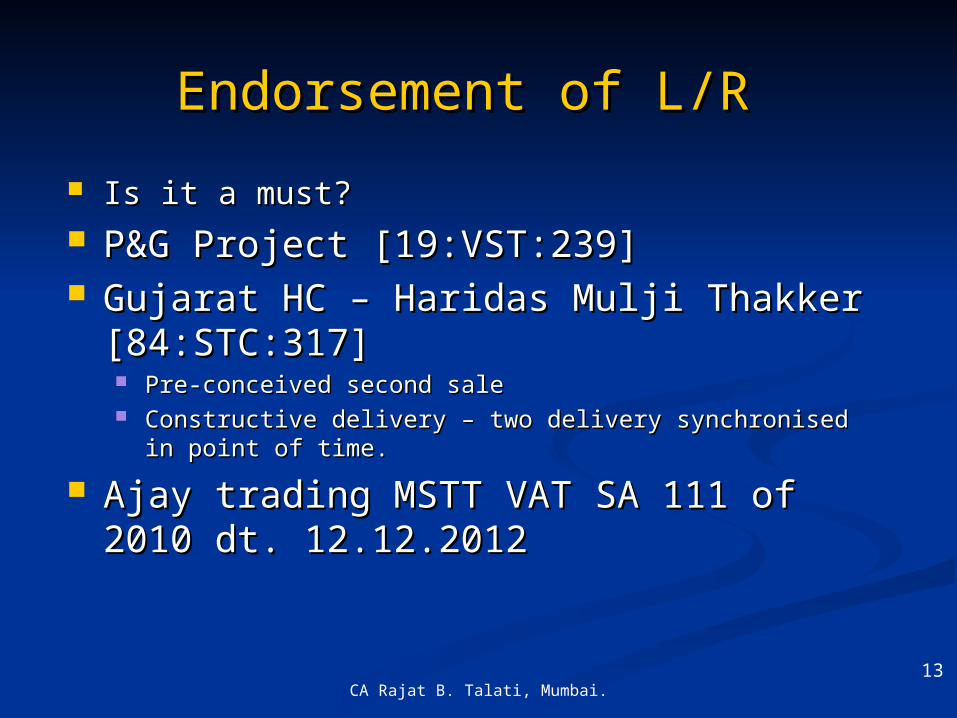

Endorsement of L/REndorsement of L/R

Is it a must? Is it a must? P&G Project [19:VST:239]P&G Project [19:VST:239] Gujarat HC – Haridas Mulji Thakker Gujarat HC – Haridas Mulji Thakker

[84:STC:317][84:STC:317] Pre-conceived second salePre-conceived second sale Constructive delivery – two delivery synchronised in point of Constructive delivery – two delivery synchronised in point of

time. time.

Ajay trading MSTT VAT SA 111 of 2010 Ajay trading MSTT VAT SA 111 of 2010 dt. 12.12.2012dt. 12.12.2012

13

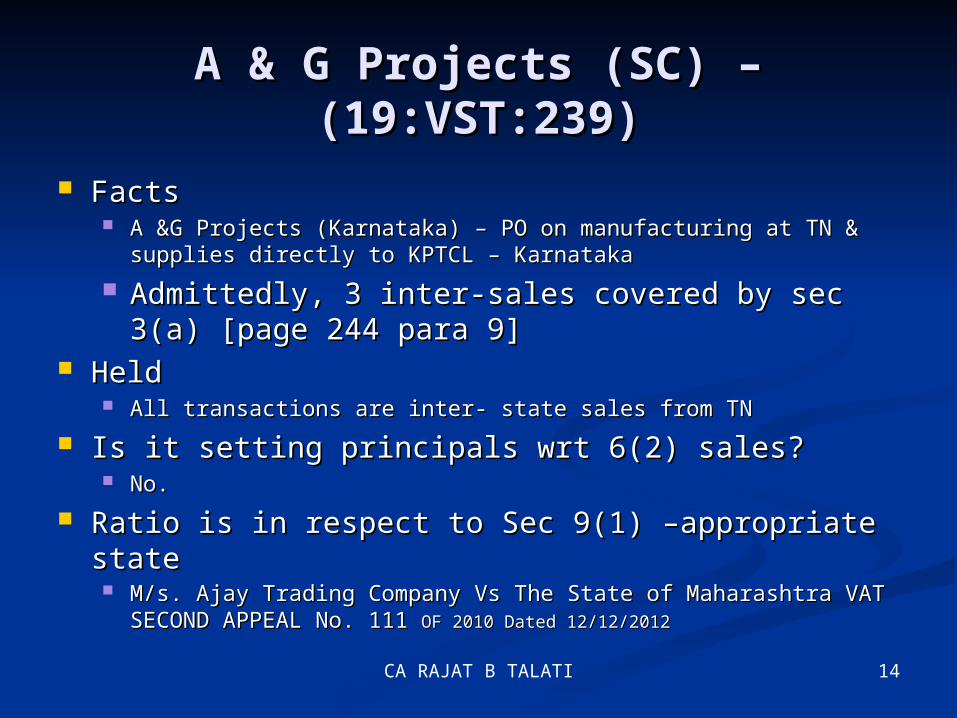

A & G Projects (SC) – A & G Projects (SC) – (19:VST:239)(19:VST:239)

FactsFacts A &G Projects (Karnataka) – PO on manufacturing at TN & A &G Projects (Karnataka) – PO on manufacturing at TN &

supplies directly to KPTCL – Karnatakasupplies directly to KPTCL – Karnataka

Admittedly, 3 inter-sales covered by sec 3(a) Admittedly, 3 inter-sales covered by sec 3(a) [page 244 para 9][page 244 para 9]

HeldHeld All transactions are inter- state sales from TNAll transactions are inter- state sales from TN

Is it setting principals wrt 6(2) sales?Is it setting principals wrt 6(2) sales? No.No.

Ratio is in respect to Sec 9(1) –appropriate stateRatio is in respect to Sec 9(1) –appropriate state M/s. Ajay Trading Company Vs The State of Maharashtra VAT M/s. Ajay Trading Company Vs The State of Maharashtra VAT

SECOND APPEAL No. 111 SECOND APPEAL No. 111 OF 2010 Dated 12/12/2012OF 2010 Dated 12/12/2012

CA RAJAT B TALATI 14

CA Rajat B. Talati, Mumbai.

Endorsement of L/REndorsement of L/R

‘‘self L/R’ – can it be endorsedself L/R’ – can it be endorsed Movement not ‘occasioned’ because of saleMovement not ‘occasioned’ because of sale

‘‘Re-booking’ – re-routing possible?Re-booking’ – re-routing possible? Notional delivery & fresh contractNotional delivery & fresh contract 89:STC:48189:STC:481

Splitting of L/RSplitting of L/R Is it possible?Is it possible? Trade practiseTrade practise

15

CA Rajat B. Talati, Mumbai.

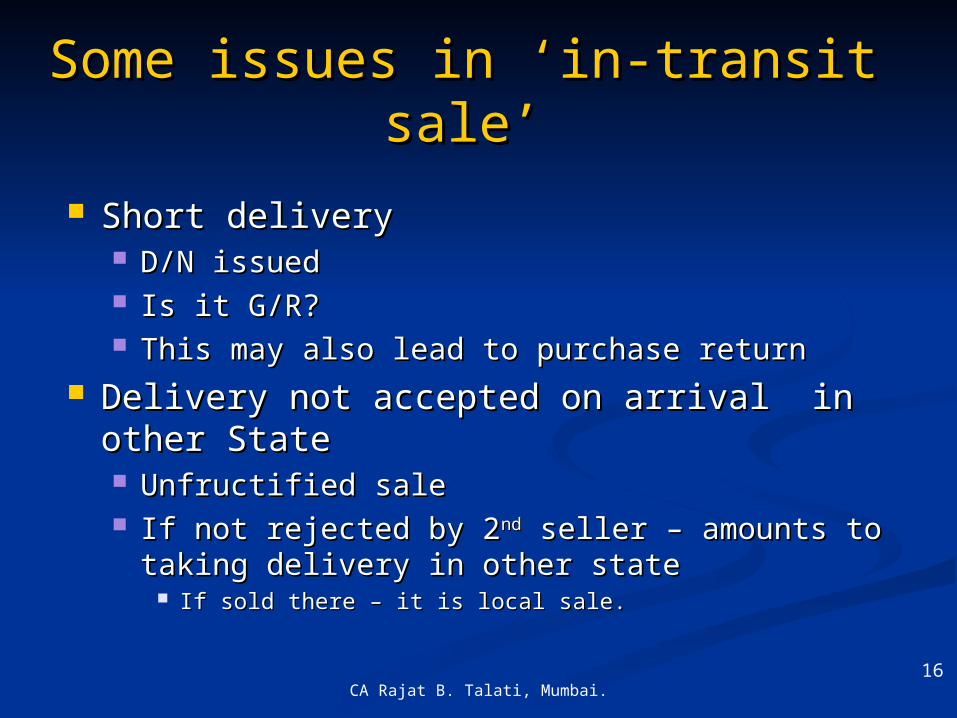

Some issues in ‘in-transit sale’Some issues in ‘in-transit sale’

Short delivery Short delivery D/N issued D/N issued Is it G/R?Is it G/R? This may also lead to purchase returnThis may also lead to purchase return

Delivery not accepted on arrival in other Delivery not accepted on arrival in other StateState Unfructified saleUnfructified sale If not rejected by 2If not rejected by 2ndnd seller – amounts to taking seller – amounts to taking

delivery in other statedelivery in other state If sold there – it is local sale.If sold there – it is local sale.

16

CA Rajat B. Talati, Mumbai.

Some issues in ‘in-transit sale’Some issues in ‘in-transit sale’

Goods returnGoods return 6(2) sales made, part quantity returned – is it possible 6(2) sales made, part quantity returned – is it possible

– yes– yes

Debit note / credit note Debit note / credit note Splitting L/R : is it possible to claim 6(2)? Splitting L/R : is it possible to claim 6(2)? Freight charges separately collected – Freight charges separately collected –

would it throw challenges in claim?would it throw challenges in claim? Would ‘agreement to sale’ allow 6(2) Would ‘agreement to sale’ allow 6(2)

claim?claim?

17

CA Rajat B. Talati, Mumbai.

Some issues in ‘in-transit sale’Some issues in ‘in-transit sale’

Goods to be approved on inspectionGoods to be approved on inspection Is claim allowable?Is claim allowable? Delivery of goods not associated with transfer of title – Delivery of goods not associated with transfer of title –

which takes place on fulfilment at later datewhich takes place on fulfilment at later date Chem dyes corp 83:STC:488 & 129:STC:3Chem dyes corp 83:STC:488 & 129:STC:3 Coffee board [46:STC:164](SC)Coffee board [46:STC:164](SC) Agreement of sale not covered in term ‘sale’ – Agreement of sale not covered in term ‘sale’ –

‘‘In-transit’ buyer – being a SEZ unitIn-transit’ buyer – being a SEZ unit Can he issue Form I?Can he issue Form I? Is it useless? No.Is it useless? No. See sec 8(6) – if overrides other provision sale exempt See sec 8(6) – if overrides other provision sale exempt

against form Iagainst form I

18

CA Rajat B. Talati, Mumbai.

Some issues in ‘in-transit sale’Some issues in ‘in-transit sale’

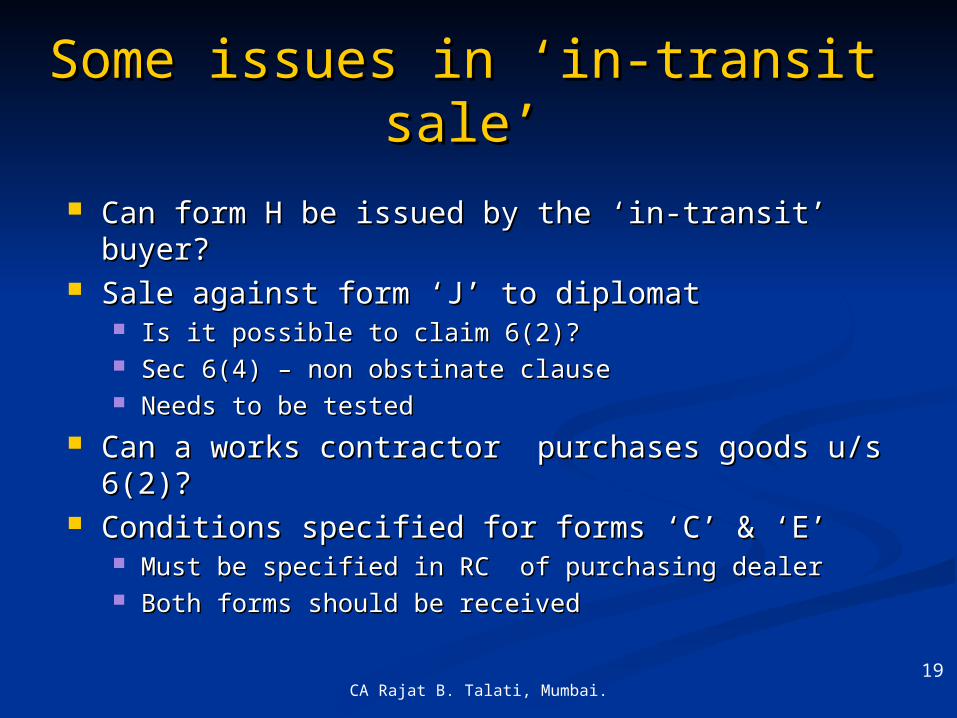

Can form H be issued by the ‘in-transit’ buyer?Can form H be issued by the ‘in-transit’ buyer? Sale against form ‘J’ to diplomatSale against form ‘J’ to diplomat

Is it possible to claim 6(2)?Is it possible to claim 6(2)? Sec 6(4) – non obstinate clauseSec 6(4) – non obstinate clause Needs to be testedNeeds to be tested

Can a works contractor purchases goods u/s Can a works contractor purchases goods u/s 6(2)?6(2)?

Conditions specified for forms ‘C’ & ‘E’ Conditions specified for forms ‘C’ & ‘E’ Must be specified in RC of purchasing dealerMust be specified in RC of purchasing dealer Both forms should be receivedBoth forms should be received

19

CA Rajat B. Talati, Mumbai.

Some issues in ‘in-transit sale’Some issues in ‘in-transit sale’

In the absence of C /E1 forms- transaction to be taxed In the absence of C /E1 forms- transaction to be taxed under the CST Act and not under the Local Sales Tax under the CST Act and not under the Local Sales Tax Act.Act. Sundaram Finance Ltd vs STO (2002) 125:STC:565(Ori) - Sundaram Finance Ltd vs STO (2002) 125:STC:565(Ori) -

under CST Actunder CST Act Chordia Electricals – 120:STC:34 appropriate stateChordia Electricals – 120:STC:34 appropriate state

Out & out – 6(2) – disallowedOut & out – 6(2) – disallowed Does Maharashtra has any jurisdiction to tax such Does Maharashtra has any jurisdiction to tax such

transaction where movement commenced from outside transaction where movement commenced from outside Maharashtra?Maharashtra?

Out & delivery in MaharashtraOut & delivery in Maharashtra Suvarna Enterprises – 85:STC120 (AP) & Mewar Oil – Suvarna Enterprises – 85:STC120 (AP) & Mewar Oil –

114:STC:547114:STC:547

20

CA Rajat B. Talati, Mumbai.

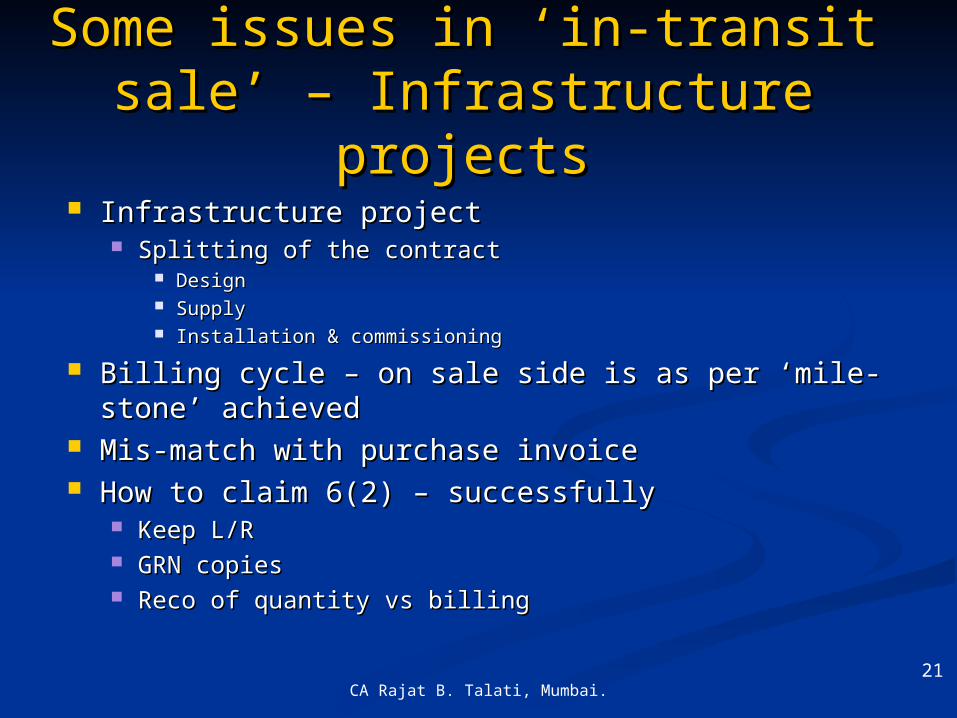

Some issues in ‘in-transit sale’ Some issues in ‘in-transit sale’ – Infrastructure projects– Infrastructure projects

Infrastructure projectInfrastructure project Splitting of the contractSplitting of the contract

DesignDesign SupplySupply Installation & commissioningInstallation & commissioning

Billing cycle – on sale side is as per ‘mile-stone’ Billing cycle – on sale side is as per ‘mile-stone’ achievedachieved

Mis-match with purchase invoiceMis-match with purchase invoice How to claim 6(2) – successfullyHow to claim 6(2) – successfully

Keep L/RKeep L/R GRN copiesGRN copies Reco of quantity vs billingReco of quantity vs billing

21

CA Rajat B. Talati, Mumbai.

Some issues in ‘in-transit sale’Some issues in ‘in-transit sale’

Description in purchase invoice & sale invoice Description in purchase invoice & sale invoice differsdiffers Seller matches description as per terminology used in Seller matches description as per terminology used in

tender.tender. If it can be proved there are some goods – 6(2) If it can be proved there are some goods – 6(2)

allowable [Van Vanaspathy Udyog [98:STC:376](Mad)allowable [Van Vanaspathy Udyog [98:STC:376](Mad) Other than forms – are other evidence like L/R Other than forms – are other evidence like L/R

etc. required?etc. required? No – P A George & Co 110:STC:253 (Ker)No – P A George & Co 110:STC:253 (Ker)

22

CA Rajat B. Talati, Mumbai.

Deemed sale – ‘in-transit sale’Deemed sale – ‘in-transit sale’

Can leasing transaction be claimed as exempt u/s 6(2)?Can leasing transaction be claimed as exempt u/s 6(2)? Is it possible to claim 6(2) sale in a hire purchase Is it possible to claim 6(2) sale in a hire purchase

transactiontransaction Whatever concessions available to ordinary sales are also Whatever concessions available to ordinary sales are also

available to HPavailable to HP Cholamandalam Investment & Finance Co Ltd vs State of Cholamandalam Investment & Finance Co Ltd vs State of

Tamil Nadu dt. 1.4.99 (Appeal no. 887/98 to 891/98)Tamil Nadu dt. 1.4.99 (Appeal no. 887/98 to 891/98) Can the ratio be used in leasing transaction?Can the ratio be used in leasing transaction?

Is 6(2) sales possible in works contract?Is 6(2) sales possible in works contract? Transfer of property by accretion & accessionTransfer of property by accretion & accession Can there be any transfer by endorsement of L/RCan there be any transfer by endorsement of L/R Divisible contract - Supply portionDivisible contract - Supply portion

23

CA Rajat B. Talati, Mumbai.

Deemed sale – ‘in-transit sale’Deemed sale – ‘in-transit sale’

Value of ‘C’ form short received although all Value of ‘C’ form short received although all transaction covered 35:STC: …. Orient Paper. transaction covered 35:STC: …. Orient Paper. MSTT followed – Kosan Indu. Ltd SA 1188 to 1190 of MSTT followed – Kosan Indu. Ltd SA 1188 to 1190 of

2000 dt. 19.7.20032000 dt. 19.7.2003 Loss of E1 & EIILoss of E1 & EII

Indemnity bond to be furnishedIndemnity bond to be furnished Rule 12(2) & 12(3) of CST(R&T) RulesRule 12(2) & 12(3) of CST(R&T) Rules

24

CA Rajat B. Talati, Mumbai.

Other Issues for referenceOther Issues for reference

Trade circular no.17 /2007 dt/ 6.12.2007 – Trade circular no.17 /2007 dt/ 6.12.2007 – C/F/H could be issued / received in quarter of C/F/H could be issued / received in quarter of sale or accounted.sale or accounted.

Inter-state sales to A – who refuses & another Inter-state sales to A – who refuses & another buyer takes the delivery – is 6(2) possible?buyer takes the delivery – is 6(2) possible? 14:STC:856 (MAD) – A Thiruvengadas Swami Iyenger14:STC:856 (MAD) – A Thiruvengadas Swami Iyenger

25

Thank youThank you