Embed Size (px)

Citation preview

www.sookshm.co.in 0

Power transmission industry is expected to grow manifolds in coming years with the help of

ambitious “power for all” program by 2022 and with few other initiatives taken by the

government. This report gives a brief analysis of the role of SMEs in transmission industry and

assessment of the industry trends along with key success factors, opportunities, challenges,

future outlook and much more…

POWER TRANSMISSION CAN SMEs POWER UP THE SECTOR?

www.sookshm.co.in 1

Table of Contents ABOUT THE AUTHOR ..........................................................................................................................2

EXECUTIVE SUMMARY .......................................................................................................................3

INDUSTRY OVERVIEW ........................................................................................................................4

TRANSMISSION TOWERS MARKET ..................................................................................................5

CONDUCTORS MARKET ..................................................................................................................5

PROJECT CYCLE ..................................................................................................................................6

COMPETITION ....................................................................................................................................6

PROFITABILITY ...................................................................................................................................7

EXPORTS ............................................................................................................................................7

EXTERNAL ENVIRONMENT & ITS IMPACT ............................................................................................9

GOVERNMENT INITIATIVES ................................................................................................................9

OPPORTUNITIES FOR SMEs ............................................................................................................... 10

CHALLENGES FOR SMEs .................................................................................................................... 11

WAY FORWARD ............................................................................................................................... 12

www.sookshm.co.in 2

ABOUT THE AUTHOR

Rohan Agarwal has 2 years of experience in projectmanagement in Realty sector. He has keen interest in Operationsand Finance area and is currently pursuing MBA from InternationalManagement Institute (IMI) New Delhi. He is a graduate in CivilEngineering from Delhi Technological University.

Kumar Rishi is a Post Graduate in Marketing from IMTGhaziabad and a Mechanical Engineer from Thapar University,Patiala. He has experience in auto component industry andmarket research.

Ashwani Kumar holds wide experience helping SMEs growthin Steel & Automotive Component industries using Operationalexcellence, LEAN & Six Sigma concepts. He is a graduate fromIIM Rohtak with a Mechanical Engineering background from IITDelhi and currently running Sookshm Management ConsultingFirm catering to SMEs.

www.sookshm.co.in 3

EXECUTIVE SUMMARY India’s energy requirement displayed a growth at

CAGR of 5.5% during FY07-FY16. According to

ministry of power till Feb’17, India has generation

capacity installed of 315.4 GW and the Peak

Demand of about 159 GW.

Despite huge investments being planned for the

two 5-Year Plans (12th and 13th), investments in

power transmission sector are still not

satisfactory. For investments made in generation

of power, at least 50% should be invested in

transmission of power in addition to it. But in

India, this ratio stands at 30%.

When we are looking at the industry from SME

point of view, then understanding the cost

structure becomes crucial. In transmission

industry, few activities such as tower design,

supply of conductors and material amount for 80-

85% of the total costs and efforts of the project.

And project life cycle spans over 3-4 years for

completion including finalizing of plan and

conducting surveys.

PGCIL and state Transco award projects to various

private players. In the past, healthy profitability

levels (RoCE of 25-30%) attracted new players.

This heightened competition has deteriorated the

financials of players. The sharp drop in RoCE (from

earlier level to around 18%) was due to rising

working capital requirement and aggressive

bidding by smaller competitors.

The transmission tower EPC industry is expected

to generate revenues of INR 275 Billion in 2017-18

at CAGR of 7-9% over 2014-15 which is mainly due

to domestic demand. A sharp drop in global

commodity prices over the last year has squeezed

budgets of several resource-dependent

economies. Thus, impacting their investments and

international demand. But domestic projects

helped in arresting the decline.

Transmission towers has major export market in Middle East, South East Asia, Latin America and Europe. As Middle East countries look to expand as well as stabilize transmission network along with interconnection of grid. Germany is also looking for grid connectivity with neighboring countries to sell unused green power.

If we look at the external environment of the

industry, tariff based competitive bidding, land

acquisition, biological health effects, 100% FDI in

the sector and technological advances like FACTS

devices and HTLS Conductors all are impacting the

industry growth for good or bad.

Government initiatives like Make in India and

Union budget 2017 are aimed at promoting skill

development, 100% rural electrification by 2018,

Implementation of Indian Customs Single

Window, reduction in corporate tax on SMEs,

removed tariff protection, lowered custom duties

and mandated domestic sourcing of equipment

for all central and state funded projects.

SMEs are facing various challenges, be it Chinese

firms bidding for power transmission projects in

India or insufficient capabilities for R&D and

innovation or large Indian players who provide

complete solutions.

But the future outlook for the industry looks

promising, as it offers many exciting opportunities

for SMEs like estimated investments in power

transmission for 13th five-year plan is around INR

2.6 lakh crore, using technology in

implementation of project, market-oriented

reforms like ‘Power for All’ by 2022, target

capacity of 175GW in renewable energy and up

gradation of existing infrastructure are some of

the opportunities where SMEs needs to stay

competitive in future.

www.sookshm.co.in 4

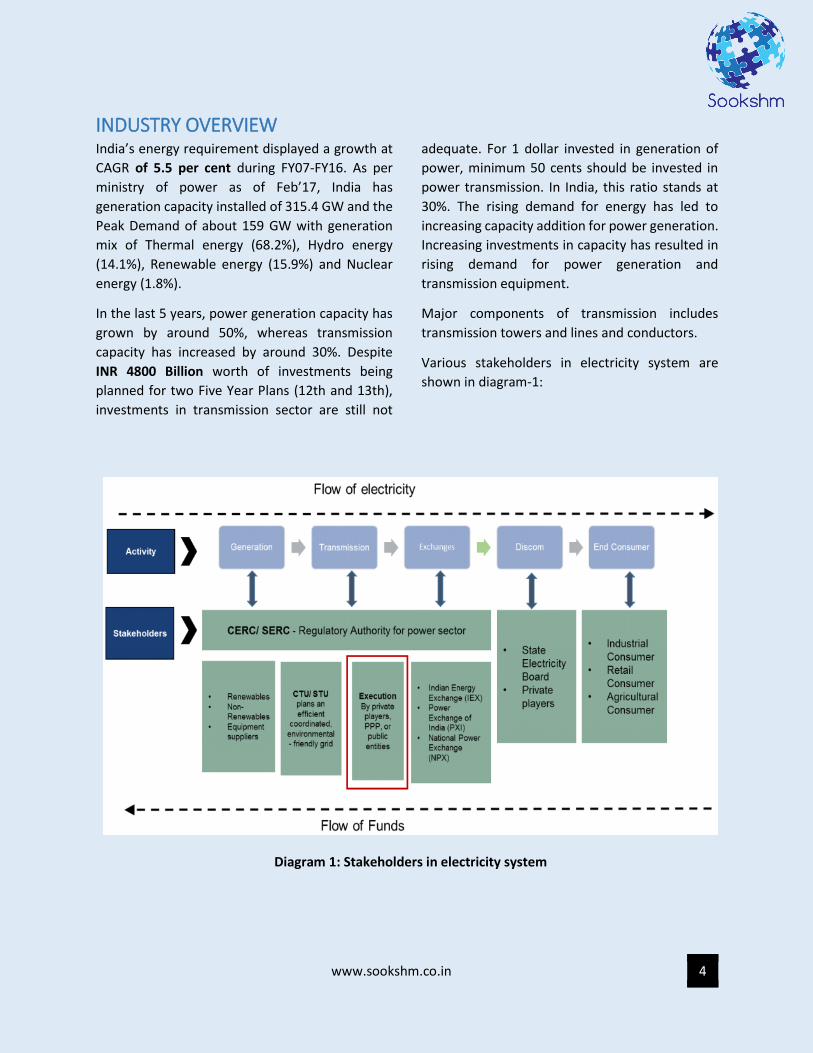

INDUSTRY OVERVIEW India’s energy requirement displayed a growth at

CAGR of 5.5 per cent during FY07-FY16. As per

ministry of power as of Feb’17, India has

generation capacity installed of 315.4 GW and the

Peak Demand of about 159 GW with generation

mix of Thermal energy (68.2%), Hydro energy

(14.1%), Renewable energy (15.9%) and Nuclear

energy (1.8%).

In the last 5 years, power generation capacity has

grown by around 50%, whereas transmission

capacity has increased by around 30%. Despite

INR 4800 Billion worth of investments being

planned for two Five Year Plans (12th and 13th),

investments in transmission sector are still not

adequate. For 1 dollar invested in generation of

power, minimum 50 cents should be invested in

power transmission. In India, this ratio stands at

30%. The rising demand for energy has led to

increasing capacity addition for power generation.

Increasing investments in capacity has resulted in

rising demand for power generation and

transmission equipment.

Major components of transmission includes

transmission towers and lines and conductors.

Various stakeholders in electricity system are

shown in diagram-1:

Diagram 1: Stakeholders in electricity system

www.sookshm.co.in 5

TRANSMISSION TOWERS MARKET The transmission tower EPC industry generated

INR 220 Billion in revenues in 2014-15 as given in

Fig-1. Of which domestic demand accounted for

INR 132 bn (60%) and international demand for

INR 88 bn (40%). Scope of the project differs

depending on whether it’s under PGCIL

(conductors supplied by PGCIL) or under state

transmission authority (conductor may or may not

be supplied).

Domestic market for towers declined in 2014-15

because of decline in PGCIL projects in 2012-13. As

projects generally spans over 2 years hence the

decline. But projects from states such as UP,

Gujarat, TN and Maharashtra helped in arresting

the decline. Market is expected to grow to INR 275

billion in 2017-18, translating into a CAGR of 7-9%

over 2014-15. This is mainly due to the domestic

demand.

CONDUCTORS MARKET Overall conductors market grew at CAGR of 4.7%

(in MT) and CAGR of 9.6% (in INR CR.) between FY

2010-11 to 2014-15 and has a market size of

around INR 100 Bn in 2016. Production of Indian

conductors industry was around 4.2 Lac MT of

conductors in FY 2010-11. Production figures were

at maximum in 2012-13 to around 5.5 Lac MT. The

industry witnessed production at around 4 Lac MT

in the last two years (i.e. 2013-14 and 2014-15).

This trend is largely a reflection

of PGCIL conductor contracts until FY 2011-12 and

swell in its inventory levels in the following years.

Three type of conductors considered are:

Aluminium Conductor (AAC), All Aluminium Alloy

Conductor (AAAC) and Aluminium Conductor Steel

Reinforced (ACSR). Amongst them ASCR

conductor market is on the rise as we can see in

the figure-2.

Figure-1: Transmission tower market size

132 136 152132

5362

7988

0

50

100

150

200

250

2011-12 2012-13 2013-14 2014-15

Rs

Bill

ion

FY

Domestic International

Generation capacity: 315 GW

MARKET SIZE:

Transmission tower EPC: INR 275 Bn

Conductors: INR 100 Bn

www.sookshm.co.in 6

PROJECT CYCLE The transmission project cycle consists of 5 main

phases, as mentioned: Attracting Players, Planning

& Project Award, Project Execution and

commissioning, Operations & Maintenance and

Exit. There are different challenges associated

with each phase.

Key steps in the development of a transmission

line are survey, tower design, type testing, laying

of the foundation, supply of the material, erection

of the towers, and stringing of the lines. Of these,

tower design, supply of conductors and material

amount for 80-85% of the total costs and efforts.

The entire process generally takes 3-4 years for

completion including finalizing of plan and

conducting surveys.

Figure-2: Conductors market trend

COMPETITION Established players like KEC, etc. captures about

60% PGCIL orders. For contracts bid out till August

in 2015-16, the share of relatively newer players

such as EMC, Skipper Ltd and Karmatara

Engineering Pvt Ltd was steady at around 40%. The

presence of foreign players is limited in the

transmission tower segment. In order to bid,

foreign players typically enter into joint ventures

with local players. For instance, Spanish firm Isolux

Corsan has entered into a joint venture with C&C

Constructions Ltd. Players in domestic market are

listed in table-1.

www.sookshm.co.in 7

PROFITABILITY As we can see in the figure-3, in the past, healthy

profitability levels, i.e., Return on Capital

employed (RoCE) of 25-30% attracted new players

from related businesses such as electric

equipment and construction. This heightened

competition deteriorated the financials of players.

The sharp drop in RoCE was due to rising working

capital requirement and aggressive bidding by

smaller competitors. As a result only few

companies are surviving in the industry with

sustainable profit margins.

Figure-3: RoCE trend for industry

EXPORTS The international market is expected to grow 8-

10% CAGR over the period 2014-15 to 2017-18, a

much slower pace compared to the earlier 18-20%

CAGR between 2011-12 and 2014-15. A sharp

drop in global commodity prices over the last year

has squeezed budgets of several resource-

dependent economies. Thus, impacting their

investments.

Indian Electrical Equipment Industry had an

estimated Production for 2014-15: INR 1280

billion and Exports worth INR 340 billion.

In FY14, for Conductor export market, African

countries accounted for more than 42% of Indian

Conductors exports. Over the last 5 years, Kenya

Table-1: PLAYERS IN DOMESTIC MARKET

MAJOR INDIAN EPC PLAYERS FOREIGN PLAYERS STR. & EQUIPMENT SUPPLIERS

Kalpataru transmission ltd, KEC international, Jyoti structures, L&T, Gammon India & TATA projects

Isolux, Cobra, Instalaciones Inabensa

Man structurals, Karamtara group, Sujana towers, Ramsarup industries, Skipper ltd.

www.sookshm.co.in 8

has been amongst the top 10 importers of Indian

conductor.

Transmission line towers has major export market

in Middle East (Saudi Arabia, UAE, Oman, and

GCC), South East Asia (Indonesia, Malaysia); Latin

America (Brazil) and Europe (Germany and UK). As

Middle East countries look to expand as well as

stabilize transmission network along with

interconnection of grid. Germany is also looking

for grid connectivity with neighboring countries to

sell unused green power.

Several African countries such as Zambia, Algeria, South Africa, Angola, Mozambique, etc., which are dependent on exports of key commodities, have

already witnessed sharp increases in their trade deficits and slower growth. Thus, affecting the exports as they are investing less in infrastructure.

Major international market for turnkey projects

are Africa, Central Asia and Middle East, whereas

North America was mainly supply only market,

due to strict norms.

India’s exports and imports market of electrical equipment industry from 2005-06 to 2014-15 are shown in Figure-4. Export market has seen a decline in trend post 2011-12 mainly due to economic slowdown whose effects were visible after 3-4 years due to the project life cycle in industry.

Figure-4: India's Exports & Imports of Electrical Equipment in INR Crores

www.sookshm.co.in 9

GOVERNMENT INITIATIVES Government has taken crucial steps for skill

development by promising 1500 multi-skill

training institutes, industry-academia

partnerships and certain service tax

exemptions for skill development and

vocational training services.

Excise duties and Custom duties have been

changed for T&D to promote “Make in India”.

Under MAKE IN INDIA, domestic sourcing of

equipment has been made mandatory for all

central and state funded projects.

Setting up of the Electrical Equipment Skill

Development Council (EESDC) which would

focus on identifying critical manufacturing skills

required for the electrical machinery industry.

VISION 2022 for electrical equipment industry:

Clusters will be established for electrical

equipment industry. And plans to make India

the country of choice for the production of

electrical equipment and reach an output of

US$100 billion by balancing exports and

imports.

Implementation of Indian Customs Single

Window project has made progress to promote

import/export of capital goods by reducing

dwell time and cost of doing business.

In Union budget’17, 100% rural electrification

by 1st May 2018 has been set as target. This

provides great opportunity for Transmission &

Distribution firms.

EXTERNAL ENVIRONMENT &

ITS IMPACT Adverse environmental and health impact:

Reduces the commercial value of the land,

often leading to protests from the land

owners. It also affects the nearby eco-

system, while passing through the forest

cover or populated areas.

Entrance of Chinese firms for bidding in

Central and State sector projects: It is likely

to increase competition for Indian

manufacturers including SMEs.

Differential treatment of private players

from PGCIL for award of forest clearances

and Section 164 authorization. Private

developers are required to acquire the

compensatory land for afforestation and

hand it over to the Forest Department

whereas PGCIL has to pay double the

afforestation compensation for getting the

clearance.

Tariff based competitive bidding has been

put in place for awarding projects over cost-

plus regime. This will increase the

transparency and competitiveness in the

system. But cost escalations in case of

project delays cannot be passed through in

this system.

www.sookshm.co.in 10

OPPORTUNITIES FOR SMEs

Market-oriented reforms, such as the target of ‘Power for All’ and plans to add 100 GW by 2022, provide high incentives for capacity addition in power generation, which would increase the demand for electrical machinery and transmission infrastructure.

Of the target capacity of 175GW in renewable energy, 100 GW from solar power, 60 GW from wind energy, 10 GW from biomass and 5 GW from small hydro power, according to the ministry of new and renewable energy. This push for green energy provides opportunities for T&D sector.

Majority of Power transmission in India is being currently carried out in the 220 KV and 400 KV range, is expected to move up to a higher range of 765 KV and high-voltage direct current. This presents a significant opportunity to manufacturers (both established and SMEs) with capabilities in high-voltage (HV) to develop technology that can handle the need of such high voltages in the country.

In 13th 5-year plan, PGCIL's focus is on undertaking system strengthening projects, particularly

in the South and North-East and increased ordering by PGCIL and state transmission

companies will drive domestic demand. As a result domestic transmission tower industry is

projected to expand at a CAGR of 6-8% between 2014-15 and 2017-18.

100% FDI in electrical machinery industry has facilitated the entry of global majors into the electrical machinery industry in India. There is an opportunity for SMEs to partner with these firms and use their resources and capabilities for various technological trends like HTLS conductors, FACTS devices and others.

Transmission of 1200 KV was started through National Test station at Bina (Madhya Pradesh)

in May 2016. This National Testing station will be monitored for 2 years and if successful will

be replicated. Thus, an opportunity for SMEs in UHVAC technology.

There is likely to be an estimated investments of INR 2.6 lakh crore in power transmission in 13th plan according to CEA (Central Electricity Authority). Of this INR 1 lakh crore will come from POWERGRID and rest INR 1.6 lakh crore from states. Thus, large number of projects are likely to come up in next 5 years.

www.sookshm.co.in 11

CHALLENGES FOR SMEs

Large players provide complete solutions or turnkey projects thus SMEs face a big challenge in winning projects as generally they have capability in one part of EPC.

Buyers are limited and majorly government agencies. Thus, buyer power is high and can frame eligibility criteria for awarding projects which might be difficult for SMEs to fulfill.

Deficiency in current transmission infrastructure leading to T&D losses of more than 20% over past 5 years. And focus is insufficient on up gradation of existing transmission lines.

There are major issues related to the slow pace of project commissioning and critical resources being under-utilized like land and Right of Way that have slackened the growth in transmission capacity.

Insufficient focus on innovation be it in terms of new conductors or transmission tower designs by SMEs is hindering their growth in fast changing times.

Poor Operations & Maintenance of existing systems by the existing players. Thus, affecting future prospects for winning the project bids as operations and maintenance is also an important criteria for awarding a contract.

www.sookshm.co.in 12

THE WAY FORWARD…

Even after facing various challenges, SMEs are able to sustain in the market and could grow manifolds

by partnering with firms having R&D capabilities of their own, this can be achieved through various

routes. This will help SMEs to compete against larger domestic players for power transmission projects

and helping SMEs grow by implementing various strategies and tools has been the objective of

Sookshm since inception. Some of the crucial aspects which the transmission industry and SMEs will

need to adopt for sustainable growth are as follows:

Reducing the concentration of projects with PSUs as PGCIL and other state entities. As of

March ‘16, private sector accounts for only 5.87% of transmission lines. Currently, there is no

substitute to transmission lines. And having 315 GW of installed capacity is not compensated

by adequate transmission infrastructure. Because of choked transmission infra, power surplus

region are not able to supply to power deficit regions. There is huge need for participation of

private sector investments or PPP mode for building up adequate infra.

Incentivize early commissioning and speedier execution. These norms should be made part of

the standard bidding documents.

Key areas where technology can be used while implementing projects are:

1. Survey: Carry out transmission line optimization through LiDAR survey (light detection and

ranging tech.)

2. Tower design: Use of green tower (least amount of steel), delta configuration for 765kv

line, etc.

3. Selection of conductor: Use of high performance conductors (HTLS: high temperature low

sag) needs to be taken up to increase power transfer intensity. Up gradation and re-

conductoring of existing lines can save valuable time, cost, row, and forest cover. This

would also mean lesser delays, and faster commissioning at a much lower cost to the

nation.

4. Mechanized construction methods: Transmission line erection and line stringing using

helicopters.

As power sector in India is expanding and need for independent transmission system

operators is increasing, stability and power flow will be important. Thus, FACTS (Flexible AC

Transmission Systems) will become the focus point such as SVC (Static Var Compensation) and

STATCOM (Static Synchronous Compensator) devices for better power quality. FSCs (fixed

series compensators) for improving existing lines. STATCOM can be used for weak power

generation sources like wind and solar.

www.sookshm.co.in 13

About Sookshm

Aiming to Achieve Growth through

CREATIVITY & INNOVATION

About Sookshm

Aiming to Achieve Growth through

CREATIVITY & INNOVATION

We believe that there is always a better way to manage a business.

At SOOKSHM, we are reinventing the way Businesses

think, operate and grow.

Our vision is to be India’s leading advisory

in Business Consulting for Indian Business

Houses

We seek to develop systems to help Businesses

work more efficiently, thereby raise themselves

to World Class Business Institutions.

In the next 5 years, we wish to impact 1000

businesses, hand holding them in their

journey towards Business Excellence.

OUR SERVICES

Marketing and growth

strategy

Operations optimization

Organizational Redesigning

Technology in Business

www.sookshm.co.in 14

B-44, Lajpat Nagar Part-2,

New Delhi- 110024

+91 9864305032, +91 9582143363

E-mail- [email protected]

www.sookshm.co.in