Embed Size (px)

Citation preview

Prepared for Port Macquarie Hastings Council

Updated October 2015

Port Macquarie Hastings Retail Strategy Review

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 2 | 53

QUALITY ASSURANCE

Report Contacts

ANETA MICEVSKA

Bachelors of Psyc (Hons) and Commerce (Economics), AHPRA

Consultant

Supervisor

ADRIAN HACK

M. Land Econ. B.Town Planning (Hons). MPIA

Principal Urban and Retail Economics

Quality Control

This document is for discussion purposes only unless signed and dated

by a Principal of HillPDA.

Reviewed by:

Dated

6/10/2015

Report Details

Job Ref No: C15223

Version: FINAL

File Name: C15223 Port Macquarie Hastings Centres Strategy Review

110915

Date Printed: 6/10/2015

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 3 | 53

CONTENTS

Executive Summary .................................................................................. 5 1

Introduction.............................................................................................. 8 2

Study Objectives ....................................................................................... 8

Methodology ............................................................................................ 8

Historical Overview ................................................................................ 10 3

Council Studies and Policies ................................................................... 10

NSW Policies ........................................................................................... 11

Section 79C of the EPA Act ..................................................................... 16

Retail Trends ........................................................................................... 17 4

Lifestyle Trends ...................................................................................... 17

1. Centralisation and Diversification in large centres ............................. 18

2. Larger supermarkets in smaller centres ............................................. 19

3. Increasing demand for residential uses in centres ............................. 20

4. The emergence of dark stores ............................................................ 21

5. Continued evolution of online retail .................................................. 21

6. Continued expansion of new and existing international retailers ..... 23

7. Ongoing renewal and reconfiguration of stores and centres ............. 23

8. The Trend in Out-of-Centre Retailing ................................................. 24

Retail Centres ......................................................................................... 28 5

Supply of Retail Floor Space ................................................................... 28

Port Macquarie Greater CBD .................................................................. 30

Local Centres .......................................................................................... 31

Development Proposals ......................................................................... 32

Demand for Retail Space ........................................................................ 34 6

Resident Projections ............................................................................... 34

Resident Spending .................................................................................. 35

Tourism and Regional Spending ............................................................. 37

Demand for Retail Floor Space ............................................................... 38

Forecast Supply and Demand ................................................................. 39

Out-of-Centre Retailing .......................................................................... 41

Long-Term Growth ................................................................................. 43

Retail Strategy ........................................................................................ 45 7

Objectives of the Strategy ...................................................................... 45

New Centres ........................................................................................... 46

Greater CBD ............................................................................................ 46

Out of Centre Retailing ........................................................................... 47

Draft Retail Policies ................................................................................ 49

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 4 | 53

TABLES

Table 1 - No. of Shop Front Establishments in Port Macquarie Hasting Shire ......................................................................................................... 29

Table 2 - Total Retail and Shop Front Floor Space by Retail Centre (sqm)* ..... 30

Table 3 – Population Forecasts for Port Macquarie Hastings .......................... 35

Table 4 - Forecast Household Expenditure Generated by Port Macquarie Hastings LGA ($m2014) ............................................................................ 36

Table 5 - Expenditure by Retail Store Type ($m2019) ...................................... 36

Table 6 - Forecast Total Expenditure in Hastings ($m) ................................... 38

Table 7 - Expenditure by Retail Store Type ($m) ............................................. 38

Table 8 - Demand for Retail Floor Space in Port Macquarie Hastings LGA (sqm GLA) ................................................................................................. 39

Table 9 - Increase in Supply (sqm GLA) ........................................................... 40

Table 10 - Centres Hierarchy – Floor Space to 2026 ........................................ 50

FIGURES

Figure 1 - Cumulative Supply and Demand for “In-Centres” Retail Floor Space to 2036 sqm GLA) .......................................................................... 40

Figure 2 - Cumulative Supply and Demand for Bulky Goods Retail Floor Space to 2036 sqm (GLA) ......................................................................... 43

LIST OF ABBREVIATIONS

ABS Australian Bureau of Statistics

CBD Central Business District

DoP NSW Department of Planning (as it was)

FSR Floor Space Ratio

GLA Gross Lettable Area

Ha Hectares

LEP Local Environmental Plan

LGA Local Government Area

NLA Net Lettable Area

SEPP State Environmental Planning Policy

SLA Statistical Local Area

Sqm Square metre

TZ Travel Zone

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 5 | 53

EXECUTIVE SUMMARY 1

This report has been prepared by HillPDA for Port Macquarie Hastings

Council as a review of Council’s Retail Strategy adopted in 2004. This

report presents the findings of an analysis of the future needs for retail

and commercial services in the LGA to the year 2036, as well as current

proposals and the implications on Council’s existing retail strategy.

This report feeds into the Local Growth Management Strategy.

Port Macquarie Hastings LGA has around 800 shop front premises

totalling some 142,000sqm of lettable floor space. Floor space is

spatially separated into a number of retail centres. The largest

concentration is the Greater Port Macquarie CBD which comprises

Settlement City, Port Macquarie Town Centre (which includes Port

Central and surrounding shop front spaces), Gordon Street precinct

and Munster Village. The Greater CBD comprises 93,000sqm (65% of

the LGA shop front floor space). The balance is distributed into 14

centres of varying sizes – Wauchope and Laurieton being the next 2

largest centres with approximately 12,000 and 11,000sqm respectively.

Of the 142,000sqm of shop front space around 117,000sqm is occupied

retail space (excluding retail space outside the centres). The balance is

vacant space and non-retail commercial uses.

Port Macquarie Hastings LGA had a population of 75,000 people in

2011 and is expected to reach 103,000 people by 2036. Population

growth (from 1.1% increasing to 1.2% per annum) as well as real

growth in retail spend per capita (expected to be around 1.0% per

annum) translates to growth in expenditure from $972m in 2014 to a

forecast of $1.6 billion in 2036. Tourism and spending in the Port

Macquarie Hastings centres from residents outside the LGA account

for a further $136m to $146m per annum. Demand for retail space in

the LGA is 197,000sqm in 2016 increasing to 274,000sqm by 2036 of

which one quarter is expected to be in “out-of-centre” or bulky goods

locations.

There are a number of mooted proposals or plans for expansion of

retail floor space – the main ones being, Thrumster (likely to be in two

stages up to 10,000sqm), St Joseph's School site (6,300sqm of

approved retail floorpsace in Stage 1) and Lake Cathie / Bonny Hills

(5,000sqm). Assuming all notional proposals are completed by 2026

then there will be 14,000sqm of undersupply of non-bulky goods retail

floor space in the LGA.

It is expected that the former “Food for Less” site and adjoining car

park would be developed well before 2026 although at this stage its

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 6 | 53

retail mix is unknown. This could potentially add a further 5,000sqm or

more retail space. Settlement City had approval to add a further

10,000sqm although that consent has now lapsed.

To ensure the viability of the Port Macquarie Town Centre it is

recommended the Retail Policy in the Port Macquarie Hastings LGA

adopt the following objectives:

1. Provide quantity, quality and convenience for consumers as well as

a wide range of shopping opportunities and commercial

experiences;

2. Provide for further growth in retail and commercial space to meet

growth in demand generated by population and household

growth;

3. Protect the integrity and viability of existing centres to the extent

that they continue to perform a valuable community function;

4. Protect current employment levels in retailing and hospitality

industries for the residents of the LGA and expand opportunities

for further employment;

5. Provide for adaptability and flexibility overtime to allow for

growth, changes in demographics, consumer needs, emergence of

new or innovative retail formats and retailers;

6. Include medium to high density inner city housing and shop-top

housing as a key driver of economic viability and growth.

7. To maintain and enhance the present hierarchy of retail centres

throughout the Port Macquarie Hastings Local Government Area.

8. Protect the integrity and viability of the Port Macquarie Town

Centre;

9. To encourage new retail development to occur within the existing

identified Commercial Business Districts of the LGA (Greater Port

Macquarie CBD, Laurieton and Wauchope); and

10. New retail centres to be restricted to Area 13 (Thrumster) and

Area 14 (Bonny Hills).

Growth in demand will continue post 2031. The majority of demand is

expected to be west of Port Macquarie. Solutions to growth include:

An enlarged Thrumster (20,000sqm or more to include a discount

department store or equivalent) or a new centre south of

Thrumster (post 2031). Moreover, the larger scale mixed use zone

at Thrumster could incorporate a larger scale retail offer in the

longer term assuming Councils opts to amend the planning control

for that area;

An expansion of Major Innes Road to say 10,000sqm. This would

be warranted given the expansion of population in the area with

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 7 | 53

more than 3,000 additional residents and 5,000 students over the

next 20 years;

Continued expansion of the CBD should be encouraged to

reinforce its role as the major centre for the Mid-North Coast. In

the long term higher density mixed use development and above

ground floor retail space may be possible and viable;

Some expansions may be warranted in Camden Haven and

Wauchope given some expected growth. Expansion of other

existing centres is unlikely to be warranted given modest growth

forecast in these areas;

Maintain the retail hierarchy, with the Greater Port Macquarie CBD

serving as the primary regional shopping destination and the

remaining centres operating as secondary centres; and

Local retail centres should be central to the populations that they

intend to serve.

The following table provides recommendations on the maximum

leasable retail floor areas by retail centre to 2036.

Classification Centres Appropriate Size (sqm GLA)*

Greater Port Macquarie CBD Includes Settlement City, Port Central and surrounding retail and Gordon Street

120,000

Town Centres Wauchope 12,000

Laurieton 12,000

Large Villages Lakewood 5,000

Lake Innes 10,000

Lake Cathie 5,000

Lighthouse Plaza 5,000

Bonny Hills (Future Centre) 5,000

Thrumster (Future Centre) 10,000

Small Villages North Haven, Kew, Kendall, Lighthouse Beach, Flynn's Beach, Waniora Parkway, Bonny Hills and Clifton

Various but around 2,000sqm per centre

TOTAL Approx 200,000

* Excludes non-retail shop front space such as real estate agents, medical, travel agents, etc

The strategy and above floor areas should be reviewed every 5 years.

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 8 | 53

INTRODUCTION 2

This report is a review of the Council's Retail Strategy for Port

Macquarie-Hastings Council (‘Council’) prepared previously in

December 2010. As part of this review HillPDA analysed the future

needs for retail and commercial services in the LGA to the year 2036,

as well as current proposals at the time and their implications on

Council’s existing retail strategy.

This review includes an update of the demand modelling based on

revised population projections and changes to the competitive

environment. This report will be used to inform the Port Macquarie-

Hastings Urban Growth Management Strategy (UGMS) 2011 which is

currently under review. The new Strategy will provide planning for all

forms of land uses to 2036.

Study Objectives

In order to develop and evaluate a range of options for the planning

and management of retailing in the LGA it is necessary to have a clear

set of objectives. At the commencement of the study key objectives

were established – these being:

Provide quantity, quality and convenience for consumers as well as

a wide range of shopping opportunities and commercial

experiences;

Provide for further growth in retail and commercial space to meet

growth in demand generated by population and household

growth;

Protect the integrity and viability of existing centres to the extent

that they continue to perform a valuable community function;

Protect the integrity and viability of the Greater Port Macquarie

CBD; and

Protect current employment levels in retailing and hospitality

industries for the residents of the LGA and expand opportunities

for further employment.

Methodology

The tasks undertaken in the preparation of this report included:

Forecast population growth, resident and tourism spend in the LGA

to 2036;

Forecast demand for retail floor space based on forecast retail

spending;

Identify areas of shortfall in supply by area and retail store type;

Identify proposals that will increase supply;

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 9 | 53

Review Council’s existing strategy in its ability to address current

and foreseeable issues; and

Make recommendations regarding the planning for, and control of,

retail provisions in the LGA; and

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 10 | 53

HISTORICAL OVERVIEW 3

Council Studies and Policies

Early Studies

The first major study on retailing in Port Macquarie Hastings was

undertaken by Plant Location International (PLI) in 1985. The study

included a series of recommendations including the recognition of Port

Macquarie as the major centre and the need for a discount

department store to reinforce this role. In 1990 the study was updated

by PLI.

1999 Review

In 1999 Council reviewed the earlier studies with two background

reports prepared by G. W. Smith of Design Collaborative including “A

Report on a Retail Policy Plan” for Hastings Council and a discussion

paper titled “Shopping After 2000”. The papers included recognition of

a hierarchy of centres, measures to protect the Greater CBD of Port

Macquarie and a number of other related issues. The reports did not

agree with the “Greater CBD” concept as the distances between

Settlement City, Port Macquarie central and Gordon Street were too

excessive for the Greater CBD to function as a single centre.

The report suggested that a better long term alternative to expansions

in the Greater CBD is a new “out-of-town” centre in the Sancrox-

Thrumster area to ultimately include a department store and a large

range of retailers. An area of at least 20 hectares was recommended

to be preserved for this option.

2004 Retail Strategy Review

In 2004 Leyshon Consulting prepared a “Retail Strategy Review” which

was largely adopted by Council for its centres policy. Council largely

dismissed the idea of a large regional or sub-regional centre outside

the existing Greater CBD. Instead it has maintained the hierarchy with

the Greater CBD as the main centre, Wauchope and Laurieton as the

district CBD (or town centres) and the remaining centres as villages or

neighbourhoods.

Only three new centres were identified – all being neighbourhood

centres in:

Major Innes Drive (now operating);

Area 13 (Thrumster); and

Area 14 (Bonny Hills).

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 11 | 53

Each of these centres was to be capped in size to a retail floor space of

5,000sqm. The capped area for Thrumster was increased to 7,500sqm

following a review of the economic impacts by HillPDA in 2007.

Port Macquarie Hastings Retail Strategy Review 2010

In 2010 HillPDA prepared a 5 year review of the Council's Retail

Strategy. That report fed into the Local Growth Management Strategy.

The Report identified the following three Strategies:

Prohibit any new centres with the exception of Thrumster (with an

approximate capacity of 10,000sqm GLA) and Area 14 Lake Cathie /

Bonny Hills (with a maximum size of 5,000sqm);

In order to ensure the viability of the Port Macquarie Town Centre

it was recommended that any proposals for redevelopment and

expansion of retail space in the Town Centre be supported –

particularly proposals that will introduce new retailers and new

formats – even if it results in some oversupply of retail space; and

Discourage or prohibit out-of-centre retailing unless it (a) complies

with the definition of bulky goods retailing under the LEP or

Standard LEP Template and is located on Lake Road, Hastings River

Drive or the B5 Business Development zones on the Oxley Highway

at Port Macquarie, or (b) complies with the definition of a

neighbourhood shop and is no larger than 200sqm.

NSW Policies

Regional Strategies

The Mid-North Coast Regional Strategy identifies a hierarchy of centres

with Port Macquarie being a major regional centre (as well as Taree,

Grafton and Coffs Harbour), Kempsey as a major town, Laurieton,

Wauchope and Lake Cathie/Bonny Hills as town centres.

As a major regional centre Port Macquarie has the majority of growth

and employment opportunities and is the major centre for state and

regional services. These centres are also expected to have “a

concentration of medium to high density living, business employment

and professional services, higher order shopping, warehouses,

transport logistics and bulky goods operations”.

Town centres have more limited trade areas. They have a small to

medium scale concentration of retail, health and other services with

lower density residential. They are reliant on major regional centres

and major towns for high order services, retailing and employment.

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 12 | 53

Page 25 of the Strategy states that "Fragmentation and out-of centre

retailing should be resisted unless compelling reasons exist in order to

maintain the healthy retail and service functioning of particular centres

in the region." This is key strategy enabling Council to protect and

maintain the retail hierarchy and the viability of existing centres.

In June 2014 the NSW Government released new draft regional

boundaries for NSW. Once the boundaries are finalised for each

region, they will provide the basis for a new generation of strategic

plans called Regional Growth Plans.

The proposed North Coast Region will incorporate areas in the Far

North Coast and Mid North Coast as well as Great Lakes and

Gloucester. The major regional city centres include Port Macquarie,

Coffs Harbour and Tweed Heads.

A North Coast Regional Growth and Infrastructure Plan will facilitate

and deliver the growth needed on the North Coast

This process will review and build on the plans contained within the

2006 Far North Coast Regional Strategy and 2008 Mid North Coast

Strategy, and set an agreed government and community vision for the

region. Once finalised, the Regional Growth and Infrastructure Plan will

replace the regional strategy.

Until a Regional Growth Plan is prepared, the Mid-North Coast

Regional Strategy will continue to apply to the region.

NSW Draft Centres Policy

Recently there has been the growing awareness and investigation of

barriers to competition in Australia, particularly in the retail industry.

As a result of these investigations the Australian Government directed

state governments and planning authorities to review the flexibility of

planning regulations and policies regarding retail development. In

response the NSW Department of Planning released the draft Centres

Policy in April 2009.

The sensitivity of Australian households to retail prices is particularly

acute given that Australians spend between 12 and 14% of their after

tax income per annum on basic grocery items1. Coupled with the

pressures of the economy, Australians experienced an increase in basic

grocery prices over the previous five years. In fact the rate of grocery

1 Based on Household Expenditure Survey (ABS cat.no. 6530.0) and Census of Population and Housing (ABS cat. No. 2003.0) data

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 13 | 53

price increased significantly greater (an estimated 6%2) above the

headline Australian inflation rate and showed no signs of abatement.

The growth of grocery prices raised significant political interest and

debate over the course of 2008 and 2009. In response the Australian

Government instructed the Australian Competition and Consumer

Commission (ACCC) to undertake a full inquiry into factors potentially

affecting retail prices including the competitiveness of the retail

industry and barriers to the entry of new retailers.

Relevant to this study, the ACCC Inquiry identified the ‘very significant

barriers to entry for large-format, one stop shop supermarkets’ as a

prominent issue. The identified barriers included:

Access to retail units within shopping centres owing to restrictive

provisions on centre leases;

Tactics applied by major retailers to protect their interests against

prospective retail developments; and

Access to suitable development sites owing to land use zones.

To address the matter of access to sites for the retail industry, the

inquiry recommended that governments across Australia look at new

ways to incorporate competition into planning decisions. It stated that

“Particular regard should be had to whether the [development]

proposal will facilitate the entry of a supermarket operator not

currently trading in the area”.3

In response to the planning recommendations provided by the ACCC

Inquiry and the current economic climate, the NSW Department of

Planning prepared and released the Draft Centres Policy for

commercial and retail development in NSW.

The Policy, released in April 2009, recognised that the market is best

placed to determine the need for development and the supply of

available floor space to accommodate demand. The role of the

planning system is to accommodate this need whilst regulating its

location and scale.

In light of these fundamental principles, the Draft Centres Policy

focused around six key principles. The principles relate to:

1. The need to reinforce the importance of centres and clustering

business activities;

2 Urbis Retail Perspectives, June 2009 3 Report to the ACCC Inquiry into the Competitiveness of Retail Prices for Standard Groceries, July 2008, Australian Competition and Consumer Commission (Page xix)

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 14 | 53

2. The need to ensure the planning system is flexible, allows centres

to grow and new centres to form;

3. The market is best placed to determine need. The planning system

should accommodate this need whilst regulating its location and

scale.

4. Councils should zone sufficient land to accommodate demand

including larger retail formats;

5. Centres should have a mix of retail types that encourage

competition; and

6. Centres should be well designed to encourage people to visit and

stay longer.

The six key principles are discussed below.

Principle 1: Retail and Commercial Activity should be Located within Centres

The first principle of the Draft Centres Policy reinforces the

longstanding strategy to concentrate the predominant share of retail

and business floor space within town centres. The clustering of uses

within centres is justified for environmental and economic reasons. By

way of example, focusing uses within centres makes efficient use of

existing infrastructure including public transport, can improve business

efficiency and productivity and allow for a range of uses to be provided

to meet consumer needs.

Principle 2: Centres should be able to Grow and New Centres Form

The Draft Centres Policy identifies that areas experiencing significant

increases in population and real income must be dynamic and respond

to “prevailing market demands” through the extension of existing

centres or the growth of new ones.

Principle 2 of the Draft Centres Policy recommends the rezoning of

land in appropriate centre locations or locations adjacent to centres in

order to facilitate business expansion and to enable new businesses to

enter the market.

Principle 3: Market Determines Need for Development, Planning Regulates Location and Scale

The third principle of the Draft Centres Policy identifies that the market

is best placed to determine demand for retail and commercial

development. Accordingly, the role of the planning system is not to

assess the appropriateness of development on the basis of demand,

but rather to make an assessment as to the external costs and

benefits.

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 15 | 53

There have been a number of criticisms with the policy including

ambiguity with and potential inconsistency or conflicts between the

principles. We understand that the NSW Department of Planning is

currently working to remove these ambiguities and inconsistencies for

the final policy and that there may also be differences between

metropolitan and non-metropolitan policies.

Principle 4: Ensuring the Supply of Floor Space Accommodates Market Demand

The fourth principle of the Draft Centres Policy emphasises the

importance of competition between retailers. The key intention of this

principle is to create better quality, cheaper and more accessible goods

for all consumers through enhanced competition. To support

opportunities for greater competition, the Draft Policy requires

councils to ensure that there is sufficient zoned land to enable

additional (and new) large format retailers to enter the NSW retail

market.

Principle 5: Support a Wide Range of Retail and Commercial Premises and Contribute to a Competitive Retail Market

Principle 5 of the Draft Centres Policy states that, subject to meeting

the appropriate location and design criteria, the zoning and

development assessment process should not consider impacts

between existing and proposed retailers as a planning consideration.

Whilst the Principle seeks to extract the matter of individual business

impact from planning assessment (in keeping with the findings of

various Land and Environment Cases – refer to Section 79C below) the

effect of a proposed development to the function and vitality of

existing and planned centres will remain as an important local issue.

Principle 6: Contributing to the Amenity, Accessibility, Urban Context and Sustainability of Centres

Principle 6 of the Draft Centres Policy highlights the importance of

design quality, development layout, connectivity and integration. The

Policy recognises that good design supports the vitality and function of

a town centre as well as the viability and success of a retail

development. Accordingly good quality design is in the interests of

planning authorities, retailers and consumer alike.

Post 2010

The Draft Centres Policy was publicly exhibited and the then NSW

Department of Planning and Environment amended it with a Draft

Activity Centres Policy. However this policy was not publically

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 16 | 53

exhibited. To date there remains no adopted State wide centres

policy.

Section 79C of the EPA Act

Section 79C provides the matters for consideration by consent

authorities in the determination of development applications. This

includes an assessment of the likely economic and social impacts of a

development proposal. Judgements have provided some guidance in

determining which matters are relevant.

In Fabcot Pty Ltd v Hawkesbury City Council (97) LGERA, Justice Lloyd

noted "economic competition between individual trade competitors is

not an environmental or planning consideration to which the economic

effect described in s 90(1)(d) is directed. The Trade Practices Act 1974

(Cth) and the Fair Trading Act 1987 (NSW) are the appropriate vehicles

for regulating competition. Neither the Council nor this Court is

concerned with the mere threat of economic competition between

competing business…. It seems to me that the only relevance of the

economic impact of a development is its effect ‘in the locality’…”.

In Kentucky Fried Chicken Pty Ltd v Gantidis (1979) 140 CLR 675 at 687

Justice Stephen noted that “if the shopping facilities presently enjoyed

by a community or planned for it in the future are put in jeopardy by

some proposed development, whether that jeopardy be due to

physical or financial causes, and if the resultant community detriment

will not be made good by the proposed development itself, that

appears to me to be a consideration proper to be taken into account as

a matter of town planning... However, the mere threat of competition

to existing businesses if not accompanied by a prospect of a resultant

overall adverse effect upon the extent and adequacy of facilities

available to the local community if the development be proceeded

with, will not be a relevant town planning consideration.”

The LEC has stated that Councils should not be concerned about

competition between individual stores as this is a matter of fair

trading. But it should concern itself with impact on established retail

centres. These principles were reiterated by Justice Pearlman in

Cartier Holdings Pty Ltd v Newcastle City Council and Anor [2001]

NSWLEC 170. “It follows that Section 79C(1)(b) does not require the

consent authority to take an approach in consideration of the relevant

matter different from the approach formerly taken in the application

of 90(1)(d).”

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 17 | 53

RETAIL TRENDS 4

The retail industry is a dynamic one with a range of trends influencing

its shape, form and composition. The following Chapter explores some

of the trends likely to influence the nature of retail within Port

Macquarie-Hasting and the needs of the residents it serves.

Lifestyle Trends

Traditionally retailing followed a hierarchy from regional through to

district to small local centres. More recently that hierarchy has been

challenged by the following social and economic trends:

Increase in the proportion of working women;

Increase in the proportion of part-time and casual employment

and reduction in full-time employment;

Reduction in the proportion of households that match the

‘traditional family’ model and an increase in the number of single

persons and single parent households;

Increase disparity of household income, ranging from high double

income households to households that rely on welfare;

Ageing of the population; and

Increasing working hours for those in full-time employment.

Since 1980 the industry’s response to these changes has led to the

growth and introduction of:

The regional centre which incorporate a large diversity of shops,

including department stores, complemented by leisure activities

and other facilities with an extensive trade area;

‘Convenience community centres’ usually dominated by a

supermarket to meet daily and weekly shopping needs and

‘standalone supermarkets’ offering a just-in-time ‘one stop shop’

(petrol, video, pharmacy, groceries, fast food, etc.);

‘Convenience service centres’ being petrol stations on main

highways but offering a just-in-time shop with a range of groceries

and fast foods (e.g. 7 Eleven and Five Star);

‘Category killers’ that provide an extensive range and depth of

competitively priced merchandise within a single market segment

(– e.g. Bunnings, BabyCo, Harvey Norman, Freedom, Toys R Us,

etc).

Bulky Goods that integrate warehousing with retailing and ‘Power

Centres’ that incorporate multiple category killers and bulky goods

retailers in one large centre.

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 18 | 53

Factory Outlets usually in fringe industrial areas providing a cluster

of out of season clothing and homeware stock.

More recently internet shopping has allowed consumers to

research products and prices on line and to have goods delivered.

All the above demographic and employment trends point to the need

for more flexible trading hours to provide convenience for what is

termed the “time-poor” shopper. In other words, we are steadily

replacing the once-a-week shop with a series of small shopping trips as

and when we need to buy various goods. This is called “just in time”

shopping.

In terms of future retail trends, HillPDA has identified the eight most

significant trends likely to influence the retail sector over the next

decade. It is important to note that this is not an exhaustive list, nor

does it purport to comment on trends which would affect the in-store

experience (e.g. the increasing emphasis on personalised marketing).

Some of the key trends identified include the following:

1. Consolidation of demand within larger centres;

2. Larger supermarkets in smaller centres;

3. Increasing demand for residential uses in centres;

4. The emergence of ‘dark stores’;

5. Continued evolution of online retail;

6. Continued expansion of new and existing international retailers;

7. Ongoing renewal and reconfiguration of stores and centres; and

8. Increasing demand for out-of-centre sites to be developed for

retail purposes.

For the purposes of context, each of these trends are explored further

below. Some of these trends currently relate only to Sydney

Metropolitan, but we expect that some of the trends may appear in

large coastal towns – particularly those towns where high density living

and land scarcity

1. Centralisation and Diversification in large centres

Large retail centres are attractive to consumers because of their retail

choice, product range and the mixed-use nature of their offer which

extends well beyond purely retail. Larger centres are also more

attractive to retailers comparative to smaller centres due to their

larger catchment areas. It is anticipated that larger centres will

continue to strengthen their offer as a result of the expansion of new

international retailers in the NSW market (see below).

International retailers seek to locate in the largest centres with the

most extensive trade areas first, before potentially expanding to

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 19 | 53

smaller centres lower down the hierarchy. As consumers are becoming

more brand savvy and are increasingly looking for particular brand

names, it is expected that they will be increasingly attracted to the

larger centres which provide this retail offer.

As a result of these considerations we expect the largest quantum of

comparison floorspace growth over the next decade to be

consolidated in the largest centres in the Metropolitan centres

hierarchy. Notwithstanding the above, over time international retailers

(who we expect to shape the future retail landscape over the next

decade) will widen their scope to look for opportunities for smaller

stores in lower order centres and large regional towns. As such we

would expect a substantial lag in international retailers locating to the

Port Macquarie-Hasting region.

2. Larger supermarkets in smaller centres

A recent trend which is likely to continue to influence the market

relates to demand for larger supermarkets in smaller centres and inner

metropolitan locations. This trend will see an increase in proposals

seeking to develop supermarkets of up to 1,400sqm in neighbourhood

centres where previously smaller supermarkets or convenience stores

may have prevailed. Increasingly split level supermarkets will be used

as models to maximise the potential of available sites.

It is anticipated that this trend will continue owing to:

Growing demand for additional supermarket facilities in inner city

locations as a result of urban infill development;

The cost of land and scarcity of sites capable of accommodating

full-line supermarkets in inner city locations and existing centres;

Increasing consumer habits towards undertaking multiple smaller

convenience shopping trips;

Increasing desire from consumers for walkable, convenient access

to food and grocery shopping reflecting declining vehicle

ownership/ usage and expectations for access to retail facilities

outside of traditional trading hours; and

Strong activity from smaller supermarket operators including ALDI

and Harris Farm with Coles and Woolworths increasingly

competing at this end of the market.

For these reasons, it may be argued that the categorisation of centres

at different levels of the hierarchy should be limited, with particular

respect to the number and type of retailers they should contain

because this will evolve over time. Rather, a more effective

categorisation could relate to the role and function of a centre and the

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 20 | 53

manner in which it should operate. Development applications could

then be assessed against the extent to which they would accord with

the desired centre role and function.

We envisage this trend to continue in the inner metropolitan area but

also middle ring priority precincts to service future high density

housing as land becomes increasingly scarce.

We are yet to witness this trend in regional NSW including Port

Macquarie-Hasting LGA; this may be a longer term trend.

3. Increasing demand for residential uses in centres

Demand for housing within centres is increasing as a result of:

Historically low housing starts since 2003 and pent up demand for

residential stock followed by the recent housing boom;

Demand for smaller dwellings in accessible locations to support

affordable living; and

Lifestyle changes with residents increasingly favouring the

accessibility, retail and service provision of centres. This reflects

the increasing preference of young households to live in highly

accessible and well serviced locations, retirees seeking to remain in

in their local neighbourhoods and downsize accordingly and

continued immigration from the Asian demographic who

traditionally favour in-centre living.

As a result competition for land, and rising land values in many centres

have increased and will continue to do so. There is a need to recognise

this as a key dynamic influencing centre development and plan centres

carefully as a result. However this is not an issue for all centres, with

pressure from residential uses most acute in those in established urban

areas.

In Doncaster, Victoria, an application for a 10,500sqm multi-level

Bunnings store with 385 residential units above was approved on a 1.1

hectare site adjacent to Westfield Shoppingtown4. This demonstrates

that a range of retail store types could potentially be developed in

metropolitan locations for mixed-use purposes in the future.

In a number of coastal cities and towns we are seeing population

growth combined with an ageing population and a growing demand for

retirement. These people will increasingly desire proximity to retail,

commercial, health and personal services and rely less on private

motor vehicle travel and as such we would expect this trend to

4 Source: Council Agenda, Manningham City Council (28 May 2013)

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 21 | 53

accelerate over the coming decade, including in Port Macquarie-

Hasting .

4. The emergence of dark stores

As demand for supermarket and grocery store related floorspace

continues to grow with NSW’s population growth, we expect asset

owners and retailers to seek greater floorspace efficiencies from

existing stores. This may support a higher propensity for online

supermarket orders to be met by dark stores located in industrial/

employment areas rather than existing supermarkets. This trend has

been evolving in the UK and in time we expect to see it emerge in

Australia.

Dark stores effectively operate as dispatch warehouses that provide

products directly to customers without first being channelled through

a local store. This creates supply chain efficiencies and reduces the

demand for in-centre floorspace, the latter being a matter we were

told by Stakeholders during consultation to inform the Report in one

respect can be challenging to secure. Whilst dark stores comprise

warehouses they can in effect broaden the land use zones in which

supermarkets are able to operate. Conversely it could be argued that

dark stores allow existing in-centre floorspace to be better utilised to

serve the needs of in-store shoppers. This emerging trend may present

opportunities for Port Macquarie-Hasting in the future.

5. Continued evolution of online retail

A major topic of debate regarding the future of retail in Australia is the

continued growth of online retail and the impact this may have to

‘bricks and mortar’ retail.

The latest data from National Australia Bank (NAB) indicates that in the

year to October 2013 online sales accounted for some 6.4% of

traditional retail spending overall, although market penetration rates

vary significantly across category types5. Retail analysts agree that this

will grow in the future although there is no consensus as to the

amount of growth that can be expected.

It is likely that the growth of online retail will change the way shoppers

interact with physical retail stores but current industry forecasts

suggest this may not lead to a significant decline in demand for high

street floorspace (with particular regard to supermarket and other

food retail floorspace) largely on account of the scale of forecast

population growth.

5 Source: NAB Online Retail Sales Index, October 2013 (December 2013); Mapinfo Anysite 2014; IBIS World Report

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 22 | 53

However in areas of inland regional NSW that are subject to stagnant

or even declining population, the evolution of online retail may present

more of a challenge. Defining a point of difference for physical centres

in these locations will be key as explored below.

Notwithstanding the fact that floorspace will not substantially increase

in the future within the Port Macquarie LGA, the following trends will

influence the nature of retailing in centres in the future as follows:

The evolution of stores as showrooms. Whilst shoppers may

research various options and purchase the final product online in

many cases they will still seek to touch, feel, weigh and operate

the items in store before purchasing. As such although the sale

may be conducted via an online median this trend is not expected

to lead to a direct decline in demand for high street

representation. Examples of this trend include the format of Apple

stores and the increasing trend for clothing store operators such as

G-Star, Glue and General Pants to direct customers to online sales

for dispatch. This would allow retail operators to make more

efficient use of existing stores with less requirement for store stock

to be kept on-site;

Increased need for engaging store experiences. Retailers will need

to work harder to attract shoppers into stores. Stores are less likely

to be able to compete on price comparative to the internet but by

promoting shopping as an experience through, for example,

outstanding in store service, engaging shopfronts/ storefronts,

fitouts and interactive design. Examples of this trend include

Hollister and Apple;

Engaging shopping centre experiences. Combined with the point

above, shopping centres will also have to focus more on in-centre

experiences to compete with online retail and with competing

retailers in other centres. With the continued growth of shopping

as a leisure activity rather than being purely functional and with

the increasing desire of customers to undertake shopping and

leisure activities at the same time, it is expected that investment in

food courts, entertainment facilities and in centre experiences will

continue;

Multi-media integration. This trend will see the merging of virtual

multi-media with the in-store and in-centre experience enabling

customers to check prices and product ranges on smartphones in

real time; and

Click and Collect. This trend refers to the process through which a

shopper pays for goods online but collects goods from a local store

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 23 | 53

or drop-off point. The growth of technology and multi-media

integration will see greater numbers of businesses offering ‘click

and collect’ and the positioning of centres as convenient hubs for

collecting goods ordered online. Westfield London has recently

been trialling Collect+ @ Westfield, a service in which shoppers try

products in store before committing to purchase them online. This

in-store service provides a lounge area, fitting room and one hour

free parking for customers and, if successful, is expected to emerge

in Australia.

6. Continued expansion of new and existing international retailers

Australia has experienced an influx of international retail brands over

the last few years, with this trend forecast to continue. International

brands have realised the potential of Australia for market share

expansion often pre-empted by sound online spending from Australian

based customers.

Sydney has already witnessed brands like Zara, TopShop, Pottery Barn,

Hollister and TM Lewin open flagship stores in higher order centres.

However, as these brands become established we expect aggressive

store roll-outs to occur in regional and subregional shopping centres.

This is a consumer benefit despite the potential for adverse impacts

upon existing retailers who will be forced to compete harder for trade.

The influx of new retailers into Australia will continue with brands

including H&M, Uniqlo, Victoria’s Secret and Forever 21 actively

seeking floorspace. Coupled with this we expect some retraction in the

department store market which will require the remodelling of existing

floorspace.

7. Ongoing renewal and reconfiguration of stores and centres

As a result of increased interest and demand in centres at the largest

and smallest ends of the retail spectrum, we expect that there may be

some challenges for middle-sized centres. This may require such

locations to redesign their offer and use more innovative approaches

towards retaining and gaining market share. Examples of this approach

in NSW include:

A new approach to Coles’ in-store retail offer in higher socio-

economic areas;

The remodelling of centres to place greater emphasis on the

provision for cafes and restaurants to support the evolution of

shopping as a leisure and entertainment activity; and

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 24 | 53

Reduction in floorspace accounted for by department stores and

an increase in the presence of branded designers to entice

shoppers e.g. Nike in Myer and the roll-out of local brands in David

Jones stores (e.g. Ginger & Smart, Zimmermann, Camilla, Ellery,

Willow, and Camilla & Marc).

International examples include:

Tesco Extra hypermarkets (large supermarkets of around

8,000sqm) which in response to declining market share and

profitability in the UK have sought to diversify their offer away

from purely convenience retail towards ‘lifestyle and leisure

centres’ which include children’s play centres, cafes and toy stores;

The growth of smaller supermarkets in accessible locations

responding to the demands of the growing cash-rich but time poor

demographic market sector in the UK, for example Marks and

Spencer Simply Food stores (500-1,500sqm) in rail stations;

Retail formats in the US have transitioned towards operating as a

showroom for particular brands and with an emphasis on fresh,

good quality food. In this manner they operate more as

showrooms and markets than a cohesive store. This is a trend we

expect to emerge in NSW as department stores adapt to stronger

competition from international retailers and changing consumer

tastes; and

In Hong Kong the evolution of entire shopping malls to target niche

market sectors such as the youth sector or the food and drink

sector. In doing so such localities seek to establish a point of

difference from traditional shopping malls and in this manner

capture market share.

As discussed above we would expect a substantial lag in

international retailers locating to the Port Macquarie-Hasting

region.

8. The Trend in Out-of-Centre Retailing

The continuing level of demand for floorspace from bulky goods

operators and other retailers such as Costco and supermarkets will

lead to continued pressure to develop on out-of-centre industrial and

employment sites for such uses given the constraints on in centre

development.

In this section we examine the trend in bulky goods retailing and the

requirements for successful bulky goods centres.

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 25 | 53

Bulky goods retailing is often described as low cost / high bulk retail

goods and ancillary products. Retailers of these goods and products

have identified financial benefits in lower occupancy costs and

economies of scale outside of established high-rent and high-cost retail

centres.

Bulky goods retailing first appeared as showrooms attached to

distribution and warehousing industries. Over time bulky goods strip

retailing and centres have attracted a number of furniture, appliance

retailers and hardware stores such as Harvey Norman, Domayne, Bing

Lee, BabyCo, Bunnings, bedding shops, lighting shops, etc. This is

despite the fact that these shops: ·

Do not necessarily use the same site for their head office,

distribution or warehousing; and

Sell many items that are not bulky.

This trend has occurred because these stores require or desire:

More floor space with cheaper rent;

Convenient and ample car parking; and

Convenient loading and unloading areas.

Many of these stores have become destination centres and therefore

do not require central location in traditional shopping centres. They

have become attractive destinations for shoppers that are searching

for lower prices and convenience of parking and loading.

More recently the bulky goods retail sector has been evolving from

former industrial premises to purpose built bulky goods retail parks

that allow brand awareness, enhanced economies of scale and

consumers the benefit of comparison shopping. Some recent examples

include the development of:

Large hardware houses;

Supacentas; and

Homemaker centres.

The hardware houses (Bunnings and Masters) sell an extensive range

of hardware, building supplies outdoor furniture and garden supplies

and some domestic appliances in one large building (4,000 to

14,000sqm). A Supacenta is a single building comprising multiple

tenants that trade predominantly in bulky goods. Examples include the

Moore Park, Caringbah and Auburn Supacentas. Homemaker centres

are similar except that there is a stronger emphasis on hardware and

building materials in addition to furniture and appliances. Furthermore

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 26 | 53

they have a significant proportion of trade to contractors (i.e.

wholesaling). Requirements for successful bulky goods centres include:

Having a large and extensive trade area of 100,000 or more

people;

being in a central position in the trade area or near the main entry

point of a large trade area (This is why Kotara for example has

been far more successful than Newcastle or Newcastle West-end);

Cheap and plentiful land (often zoned industrial) to enable

plentiful parking and loading and unloading facilities; and

Being located on a major road with high visibility and accessibility.

Desirable requirements include:

Having a trade area that is expanding as new homes generate

higher demand for bulky goods than established homes; and

Having a wealthy trade area with high disposable incomes. Higher

income households spend considerably more on bulky goods than

lower income households.

In a number of instances retail centres have been unable to

accommodate the emerging style of bulky goods retailing. Bulky goods

retailers require relatively large sites that are often not available within

existing retail centre zones. And, even where sufficiently large centre

zone sites exist, it is claimed by retailers that high rentals preclude

bulky goods retail developments.

The locational preferences of bulky goods retailers have therefore led

to some conflict with regulatory authorities on the basis that retailers

do not always desire to locate in centres.

Bulky goods retailing has experienced, and still is experiencing, a

period of considerable change both nationally and internationally.

Perhaps the most significant changes are:

The trend towards bulky goods retailers grouping together in large,

purpose-built bulky goods centres;

The emergence of 'category killer' superstores; and

Retailers looking to expand both within a city and nationally, once

a successful store format has been established. Many of these

retailers were not established 20 years ago.

In some overseas markets there has been a trend towards purpose-

built bulky goods centres evolving into more of a mixed use retail

format which includes non-bulky goods uses. For example,

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 27 | 53

complementary uses such as cafes, clothing retailing, brand direct

retailing etc, are locating with bulky goods retailers.

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 28 | 53

RETAIL CENTRES 5

Supply of Retail Floor Space

Since the 2010 update of the Retail Centres Study there has been

several additions to supply. The main additions were:

Construction of a new retail centre at 28 Hayward Street which

includes a 4,200sqm Coles supermarket and 2 specialty stores. The

new Coles replaced the former Coles store on Short Street which

has since been converted to Officeworks and JB Hi-Fi stores;

Construction of a 1,300sqm Dan Murphys on Horton Street;

Expansion of the IGA supermarket in Wauchope to 1,600sqm plus

3 additional specialty stores including liquor;

Some internal modification and tenancy changes in Settlement

City; and

ALDI Foodstore in Hastings River Drive (although this is outside the

defined centres).

Reduction in floor space includes the closure of the former Food for

Less supermarket and adjoining specialty stores.

Excluding the industrial areas Port Macquarie Hastings has almost 800

shop front premises distributed in around 18 centres of varying sizes.

Around 600 of these premises are being used for retailing of goods,

167 are being used for non-retail commercial purposes (such as real

estate, travel agents, finance, medical, etc) and 25 are vacant. The

number of businesses in the retail centres is provided in the table

below.

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 29 | 53

Table 1 - No. of Shop Front Establishments in Port Macquarie Hasting Shire

Retail Centre Super-

markets

Large

format

mini-

majors

Restau

rants Retail

Personal

Services

Total

Retail

Non

Retail Vacant Total

CBD 4 1 42 94 23 164 83 18 265

Settlement City 2 5 2 44 6 59 2 10 71

Gordon St 1 3 10 23 9 46 48 5 99

Munster Village 0 1 0 6 0 7 2 0 9

Total CBD 7 10 54 167 38 276 135 33 444

Bonny Hills 0 0 0 3 0 3 1 0 4

Clifton 0 1 2 5 3 11 3 0 14

Flynns Beach 1 0 4 2 1 8 0 2 10

Lake Innes 1 0 3 4 1 9 2 1 12

Lighthouse Shops 2 0 7 3 1 13 2 0 15

Lighthouse Plaza 1 0 3 6 1 11 3 3 17

Lord St 0 0 2 4 3 9 30 3 42

Waniora 1 1 1 2 3 8 0 0 8

Kendall 0 0 0 3 0 3 2 0 5

Kew 0 0 1 4 0 5 2 1 8

Lake Cathie 1 2 2 5 0 10 4 3 17

Lake Cathie Nth 0 0 2 4 0 6 0 0 6

Laurieton 3 1 15 44 10 73 24 3 100

Lakewood 1 2 1 3 2 9 1 0 10

North Haven 1 0 3 6 3 13 2 0 15

Timbertown 0 1 2 3 0 6 3 0 9

Wauchope 1 0 7 67 11 86 43 11 140

Total 20 18 109 335 77 559 257 60 876

Supply of retail floor space is measured by a combination of the

number of stores and floor space (square metres). Floor space is

measured by lettable area (the area leased or potentially leased to a

store operator and includes back of house storage and office) but

excludes common areas, plant rooms and loading docks. In the case of

indoor centres such as Settlement City and Port Central, it includes the

area leased to the shop owners but excludes common areas, car

parking, toilets, plant rooms, fire egress, etc.

Presently there is around 142,000sqm of shop front space in the LGA

of which around 117,300sqm is being used for retailing. Total Retail

floor space is shown in the table below:

Sources: Port Macquarie Hastings Council.

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 30 | 53

Table 2 - Total Retail and Shop Front Floor Space by Retail Centre (sqm)*

Centre Supermarkets & Grocery Stores

Other Retail Total Retail Non-Retail Shop Front

Total Shop Front Space

Greater CBD

Port Central 2,450 12,350 14,800 300 15,100

Other CBD 4,200 27,750 31,950 12,900 44,850

Settlement City 4,250 13,850 18,100 1,200 19,300

Adjacent to Settlement City 0 4,200 4,200 400 4,600

Gordon Street West 1,600 5,700 7,300 1,400 8,700

Munster Shopping Village 500 250 750 0 750

TOTAL CBD 13,000 64,100 77,100 16,200 93,300

Wauchope 1,600 7,650 9,250 3,000 12,250

Laurieton 2,400 5,450 7,850 2,800 10,650

Lakewood 3,250 600 3,850 450 4,300

Lake Innes 3,000 900 3,900 500 4,400

Lake Cathie 2,800 950 3,750 500 4,250

Lighthouse Plaza 3,000 1,000 4,000 0 4,000

North Haven 200 1,900 2,100 100 2,200

Kew 200 100 300 200 500

Kendall 200 700 900 200 1,100

Lighthouse Beach 100 650 750 150 900

Flynn's Beach 100 800 900 0 900

Waniora Parkway 300 700 1,000 0 1,000

Bonny Hills 0 450 450 250 700

Clifton 200 1,000 1,200 0 1,200

TOTAL 30,350 9,600 117,300 19,250 141,600

Australian Property Council Shopping Directory, Draft Retail Strategy Review (Leyshon Consulting), HillPDA Floor Space Source:Surveys 2007 and recent development applications. Excludes industrial zoned areas.

A description of the retail centres in the LGA is given below.

Port Macquarie Greater CBD

Port Macquarie Greater CBD has over 90,000sqm of shop front space,

of which 38% is in two large indoor shopping centres – Port Central

and Settlement City.

Port Central is located at 40 Horton Street in the CBD. The major

anchor tenants include Target (7,078sqm) and Ritchies IGA

Supermarket (2,458sqm). Port Central has 54 specialty shops and a

total area of 15,100sqm.

Port Central

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 31 | 53

Around Port Central the CBD has around 280 shop-front premises

totalling some 45,000sqm of space fronting Horton Street, Hay

Street, Clarence Street and William Street. Anchor tenants include

a new 4,200sqm Coles supermarket, JB Hi-Fi, Officeworks and The

Warehouse.

Settlement City is west of Port Central shopping centre. The major

tenants include Big W (6,618sqm) and Woolworths supermarket

(4,253sqm). There are 58 specialty shops and the centre has a total

area of 19,300sqm. Adjacent to Settlement City are some 22

retailers with around 5,000sqm of retail space. Anchor tenants

include McDonalds, Go-Lo and a large Rivers Clothing store.

Munster shopping centre is a small centre on the corner of

Munster Street and Gordon Street. It comprises a 500sqm Five

Star supermarket, fruit market, butcher and bakery.

There are a number of strip shops and an open court shopping

centre on Gordon Street between Gore Street and Hastings River

Drive. The centre is anchored by a 1,600sqm IGA supermarket, a

1,000sqm fruit and veg store and a 1,500sqm Rebel Sports store.

Total number of premises is around 40 with a total area of around

8,000sqm.

Local Centres

Wauchope

Wauchope is approximately 16km west from Port Macquarie town

centre. The shopping centre had 93 shop front premises of which 26

were being used for non-retail commercial services. Total leasable

floor space is just over 12,000sqm of which around 2,000sqm is

occupied by four hardware stores and 3,000sqm is occupied by non-

retail commercial services. There were no vacancies in 2007 at the

time of survey. Anchor tenants included two recently expanded IGA

supermarkets of 1,620sqm and the 1,300sqm Co-op Department Store

(excluding the hardware component). A 130sqm liquor store and three

50sqm specialty stores has also located near the IGA supermarket

since 2010.

Laurieton

Laurieton is the largest retail centre in the southern part of the LGA.

Its trade area includes North Haven, Laurieton, Dunbogan and Kew.

The centre comprises 84 shop front establishments of which 22 are

used for non-retail commercial services and four are vacant. Total

shop front space is around 10,500sqm of which 7,800sqm is used for

retail. The main anchor tenant is a 2,400sqm Coles supermarket

Settlement City

Wauchope Shopping Centre

Laurieton Main Street

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 32 | 53

Lake Cathie

Lake Cathie is approximately 15km South of Port Macquarie town

centre. The shopping centre is anchored by 2,800sqm Woolworths

supermarket and there are 1,100sqm of specialty retail shops. The

total centre is in the order of 4,000sqm. This is a popular centre for

shopping due to its high level of ample and convenient parking.

Lighthouse Plaza (Tacking Point)

Lighthouse Plaza is a village centre comprising 12 shops anchored by a

large 3,012sqm Coles supermarket.

Lake Innes (West Port Macquarie)

Lake Innes Shopping Centre on the corner of John Oxley Drive and

Major Innes Drive is the most recent addition to the hierarchy of

centres. It is a local village centre which includes a 3,000sqm Coles

supermarket and 12 specialty shops.

Lakewood

Lakewood is the second youngest centre and is located on Ocean

Drive. It comprises 4,300sqm of space anchored by a 3,250sqm

Woolworths supermarket.

Other Centres

Other centres in the local government area are generally small village

or neighbourhood centres of less than 1,500sqm. These centres,

including Flynns Beach, Lighthouse Beach, Shellys Beach, North Haven,

Kew, Kendall and Clifton Drive, are usually anchored by a small or mini-

supermarket – less than 1,000sqm in size.

Development Proposals

Current development proposals include the following:

A proposal for some expansion in Laurieton including a new Coles

Supermarket and the conversion of the former Bi-Lo supermarket

into a Target Country store was approved more than 5 years ago.

Consent has now lapsed.

A development application for a pharmacy of approximately

420sqm along Bold Street in Laurieton was granted development

consent.

Approval was given to Settlement City for expansion of around

12,300sqm of which 4,117sqm was for additional retail, 2,924sqm

Woolworths Lake Cathie

Lighthouse Beach Shopping Centre

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 33 | 53

was for additional commercial and 5,223sqm was for recreational

facilities including a cinema. Approval has since lapsed.

Council has rezoned the land at Warlters Street, adjoining

Settlement City, to B3 Core Business. Subsequently a Kmart

discount department store with additional specialty retail totalling

6,300sqm (GLA) has been approved on part of this site.

Sovereign Hills (Thrumster Area 13) will ultimately have a centre

capacity of around 10,000sqm to service the future 10,000-11,000

residents of Thrumster. Approval for a Woolworths based centre

for the first stage comprising 2,500sqm supermarket, 1,100sqm of

specialty shops and 800sqm market hall has lapsed and has not

been assumed in this analysis.

Development consent was granted for Stage 3 of Timbertown to

include seven retail shopfronts and three commercial shopfronts

totalling 974sqm. The project has substantially commenced.

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 34 | 53

DEMAND FOR RETAIL SPACE 6

This section forecasts demand for retail space in the Port Macquarie-

Hastings LGA during the period from 2006 to 2036. Demand comes

from three main sources of expenditure:

Residents of Hastings;

Residents of surrounding local government areas; and

Tourists and visitors.

Resident Projections

The increase in availability of private motor transport over this post-

war period resulted in significant demand for residential development

in coastal areas away from traditional rail-based inland townships. The

primary housing market role that Port Macquarie-Hastings played

during the post-war period was to attract families and retirees from

areas further south, in particular the Sydney region. There has also

been demand for housing resulting from the children of those families

setting up their own households. This pattern is likely to continue into

the future, driving development on the outskirts of Port Macquarie

and in the Camden Haven.

In 2011, the total population of Port Macquarie-Hastings Council area

was estimated to be 74,955 people. It is expected to increase by over

16,300 people to 91,276 by 2026 (at an average annual growth rate of

1.32%) and to 102,926 persons by 2036. This is based on an increase of

over 7,100 households during this period.

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 35 | 53

Table 3 – Population Forecasts for Port Macquarie Hastings

Locality 2011 2016 2021 2026 2031 2036

Camden Haven East 5,941 6,023 6,156 6,250 6,347 6,451

Camden Haven West 3,084 3,205 3,673 4,015 4,407 4,753

Flynns Beach 2,144 2,181 2,231 2,244 2,267 2,301

Hastings River Canals 2,513 2,762 2,891 2,895 2,884 2,880

Inner West Port 2,343 2,337 2,439 2,590 2,814 3,033

Innes Peninsula 3,110 4,109 5,151 6,276 7,030 7,318

Lake Cathie - Bonny Hills 6,024 6,559 7,433 8,341 9,219 10,143

Lighthouse Beach - Greenmeadows 11,805 11,950 12,441 12,825 12,979 13,016

Lord Street 1,739 1,862 1,963 2,124 2,357 2,592

Port Macquarie Rural Fringe 3,386 3,596 3,866 4,119 4,664 5,320

Rural 6,564 6,801 7,024 7,258 7,478 7,675

Shelly Beach - Bellevue Hill 11,060 11,242 11,371 11,452 11,556 11,693

Thrumster 162 754 2,362 3,958 5,647 7,682

Town Beach - CBD 900 1,118 1,241 1,384 1,484 1,611

Wauchope 6,911 7,290 7,661 8,063 8,446 8,883

Westport 7,268 7,354 7,378 7,481 7,493 7,575

Total 74,955 79,144 85,280 91,276 97,072 102,926

Source: Forecast.ID

Resident Spending

In addition to population growth there has been real growth in retail

spend resulting from increasing affluence and economic materialism.

From 1991 to 2005 growth in retail spend per capita was around 1.9%.

There have been periods however where growth has been negative

such as 1986 to 1991 and during 2007 to 2008 when rising interest

rates and petrol prices saw households reducing spend. The GFC and

worsening job security had some negative impacts but government

stimulus measures combined with a lowering of petrol prices and

interest rates maintained levels of retail spend. The average per

annum growth rate in retail spend per capita since 1986 has been

around 1.0% and the long term trend has been around 1.3%. For the

purpose of forecasting we have adopted a rate of 1.0%.

Household expenditure was sourced from Anysite 2014 data which

provides household expenditure by broad commodity type.

The tables below show that Port Macquarie - Hastings LGA will

generate considerable growth in expenditure to 2036.

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 36 | 53

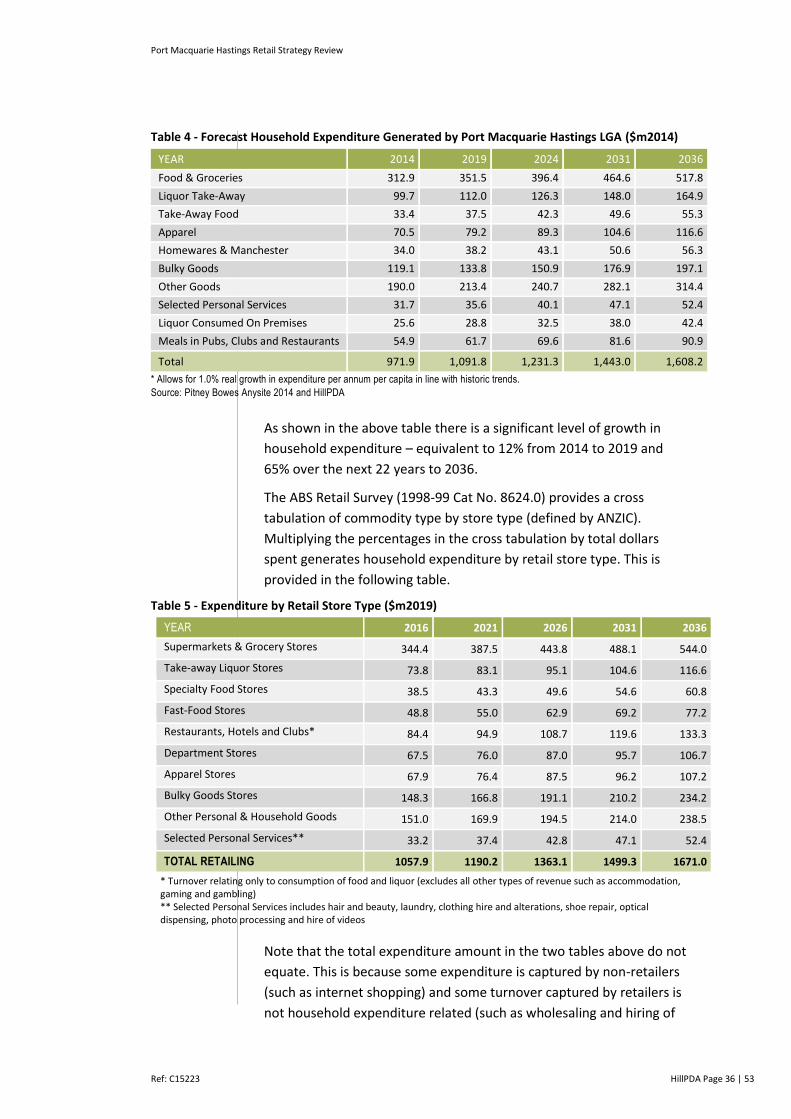

Table 4 - Forecast Household Expenditure Generated by Port Macquarie Hastings LGA ($m2014)

YEAR 2014 2019 2024 2031 2036

Food & Groceries 312.9 351.5 396.4 464.6 517.8

Liquor Take-Away 99.7 112.0 126.3 148.0 164.9

Take-Away Food 33.4 37.5 42.3 49.6 55.3

Apparel 70.5 79.2 89.3 104.6 116.6

Homewares & Manchester 34.0 38.2 43.1 50.6 56.3

Bulky Goods 119.1 133.8 150.9 176.9 197.1

Other Goods 190.0 213.4 240.7 282.1 314.4

Selected Personal Services 31.7 35.6 40.1 47.1 52.4

Liquor Consumed On Premises 25.6 28.8 32.5 38.0 42.4

Meals in Pubs, Clubs and Restaurants 54.9 61.7 69.6 81.6 90.9

Total 971.9 1,091.8 1,231.3 1,443.0 1,608.2

* Allows for 1.0% real growth in expenditure per annum per capita in line with historic trends.

Source: Pitney Bowes Anysite 2014 and HillPDA

As shown in the above table there is a significant level of growth in

household expenditure – equivalent to 12% from 2014 to 2019 and

65% over the next 22 years to 2036.

The ABS Retail Survey (1998-99 Cat No. 8624.0) provides a cross

tabulation of commodity type by store type (defined by ANZIC).

Multiplying the percentages in the cross tabulation by total dollars

spent generates household expenditure by retail store type. This is

provided in the following table.

Table 5 - Expenditure by Retail Store Type ($m2019)

YEAR 2016 2021 2026 2031 2036

Supermarkets & Grocery Stores 344.4 387.5 443.8 488.1 544.0

Take-away Liquor Stores 73.8 83.1 95.1 104.6 116.6

Specialty Food Stores 38.5 43.3 49.6 54.6 60.8

Fast-Food Stores 48.8 55.0 62.9 69.2 77.2

Restaurants, Hotels and Clubs* 84.4 94.9 108.7 119.6 133.3

Department Stores 67.5 76.0 87.0 95.7 106.7

Apparel Stores 67.9 76.4 87.5 96.2 107.2

Bulky Goods Stores 148.3 166.8 191.1 210.2 234.2

Other Personal & Household Goods 151.0 169.9 194.5 214.0 238.5

Selected Personal Services** 33.2 37.4 42.8 47.1 52.4

TOTAL RETAILING 1057.9 1190.2 1363.1 1499.3 1671.0

* Turnover relating only to consumption of food and liquor (excludes all other types of revenue such as accommodation, gaming and gambling) ** Selected Personal Services includes hair and beauty, laundry, clothing hire and alterations, shoe repair, optical dispensing, photo processing and hire of videos

Note that the total expenditure amount in the two tables above do not

equate. This is because some expenditure is captured by non-retailers

(such as internet shopping) and some turnover captured by retailers is

not household expenditure related (such as wholesaling and hiring of

Port Macquarie Hastings Retail Strategy Review

Ref: C15223 HillPDA Page 37 | 53

equipment). Note also that the above tables show turnover generated

by household expenditure. It does not show where that turnover is

captured.

Tourism and Regional Spending

Port Macquarie is known to capture some expenditure from the

neighbouring LGAs of Greater Taree and Kempsey. In 2011 Greater

Taree had around 46,541 residents and Kempsey had around 28,000