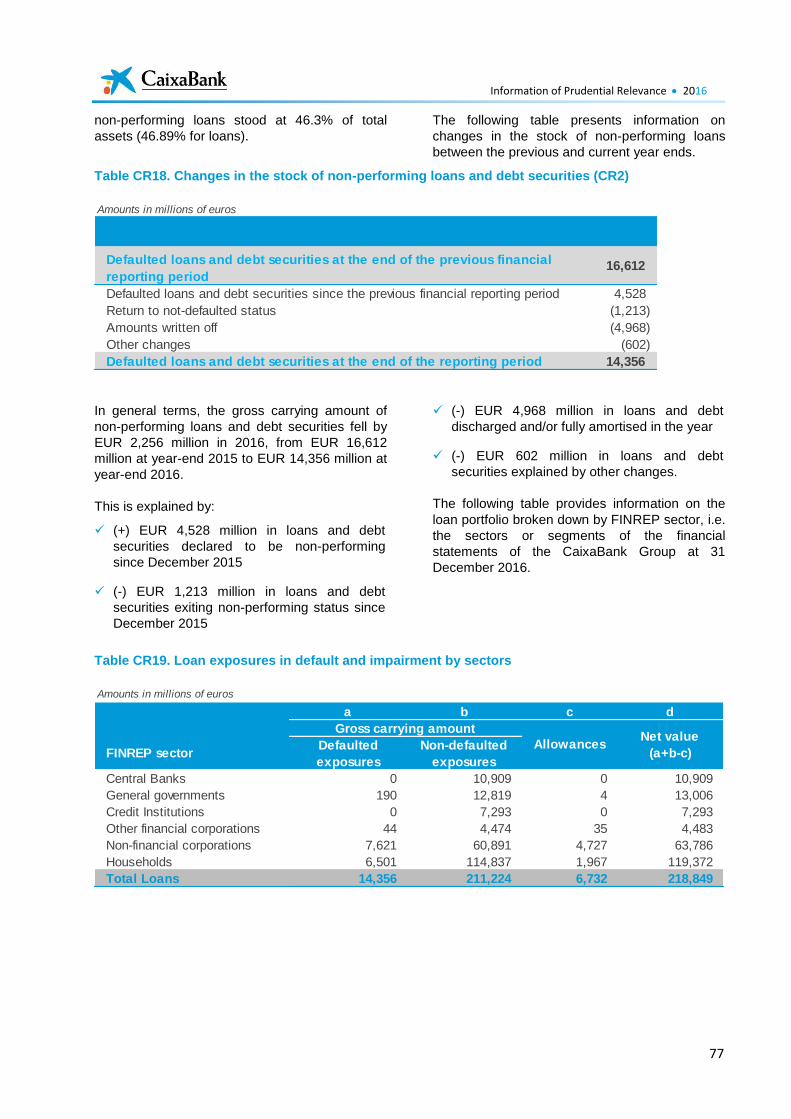

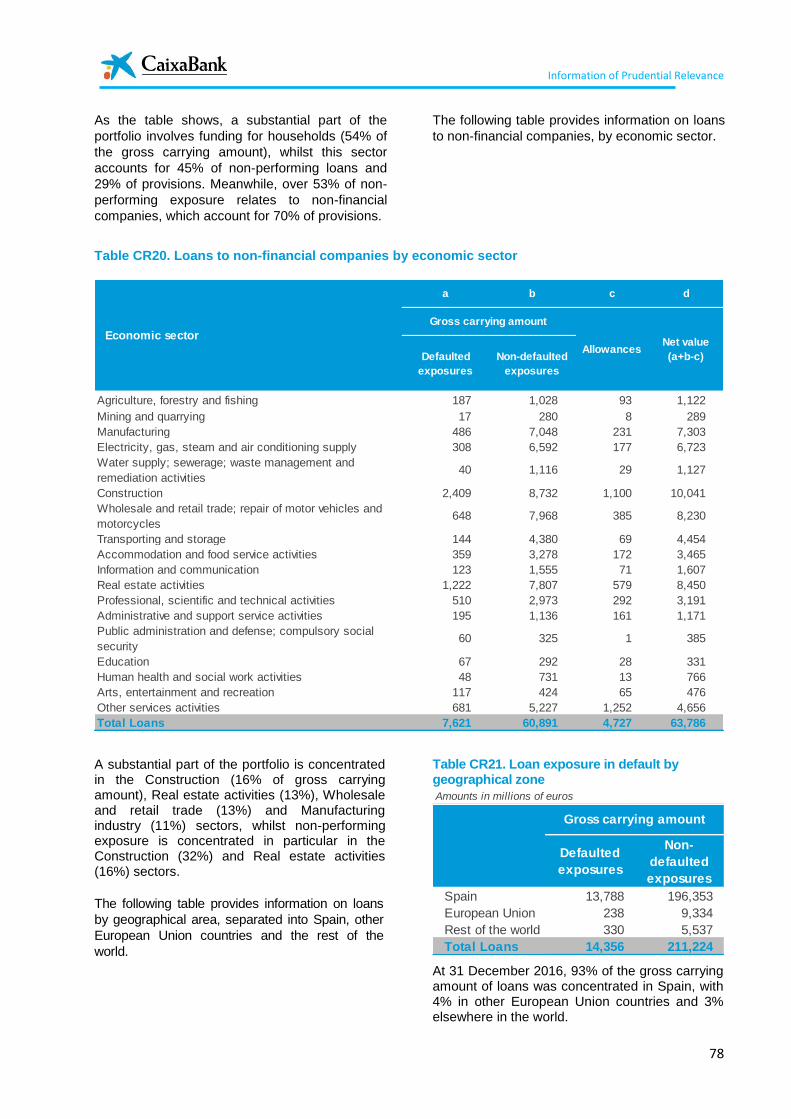

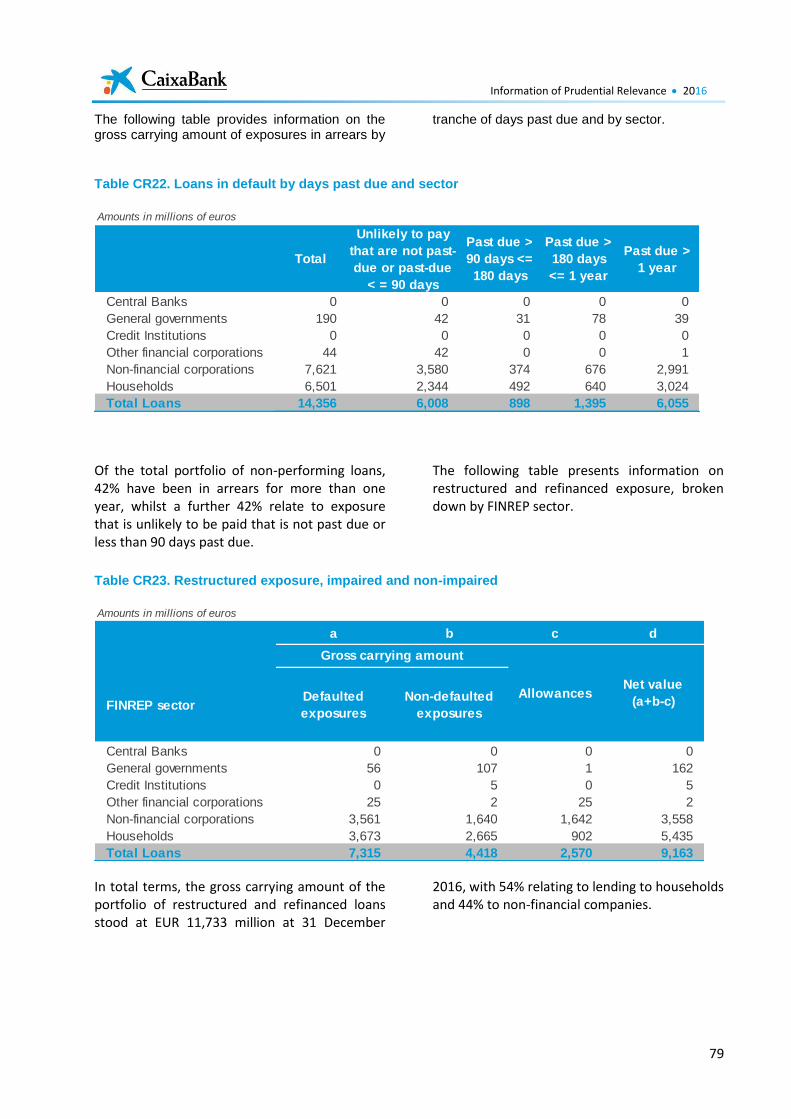

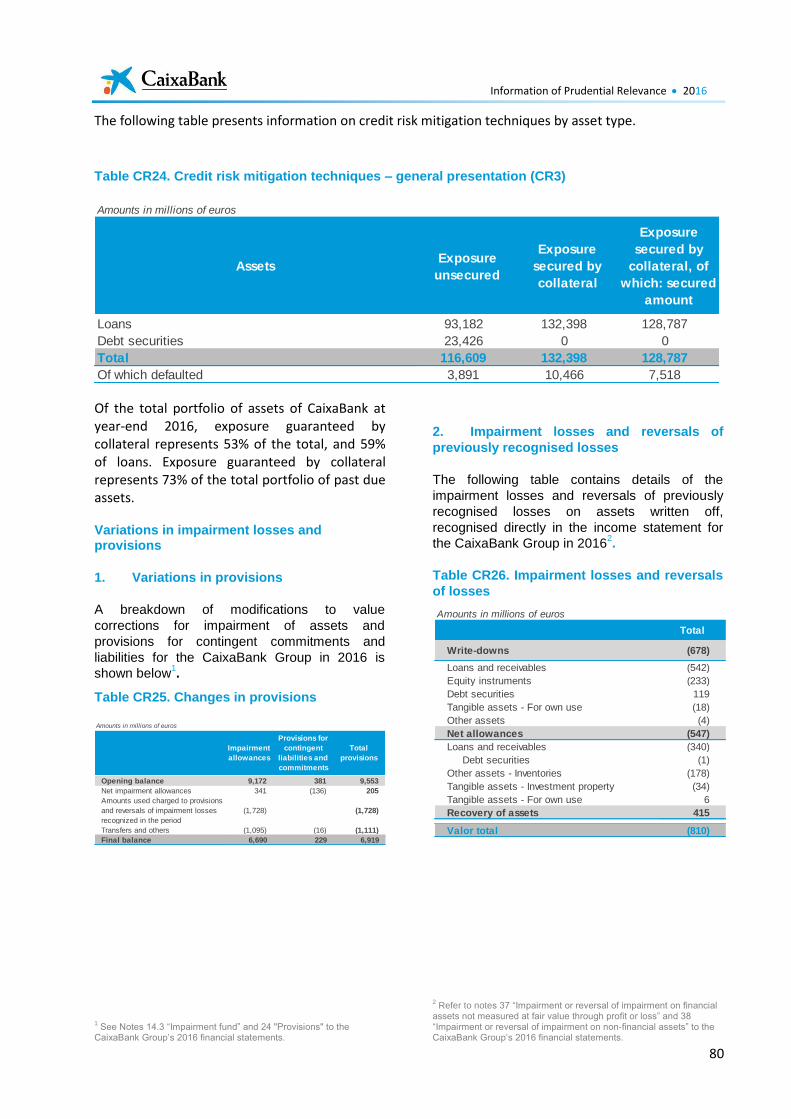

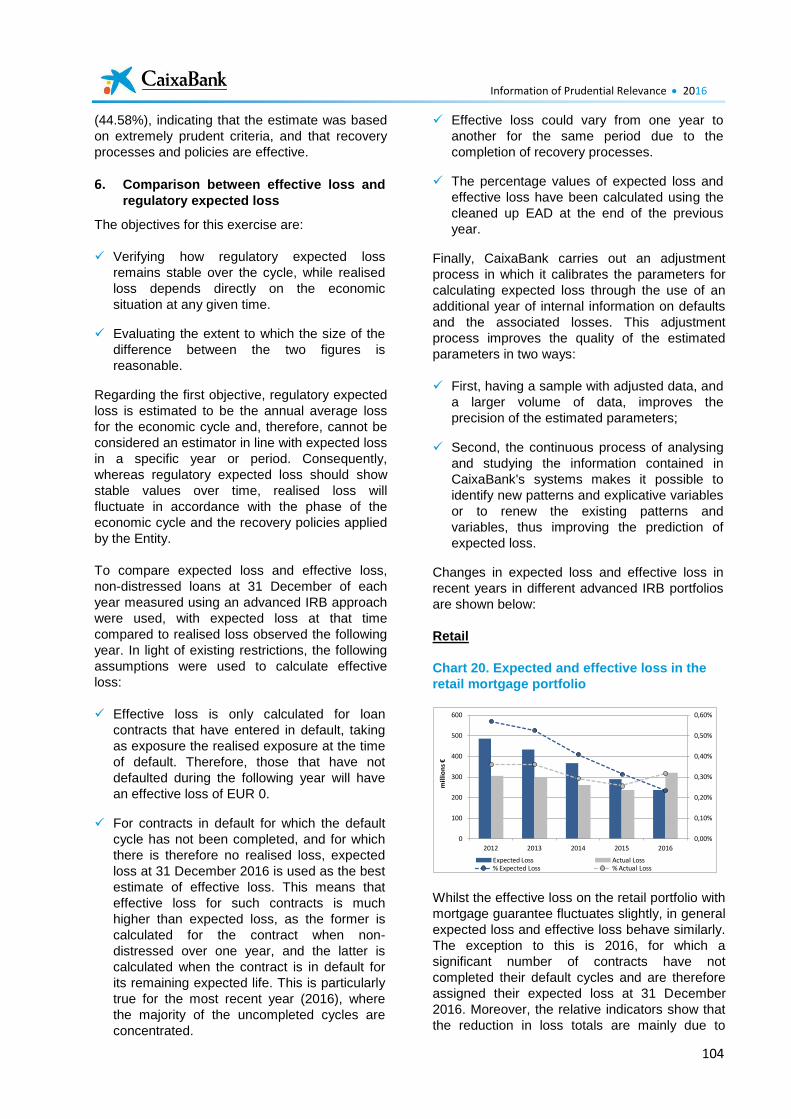

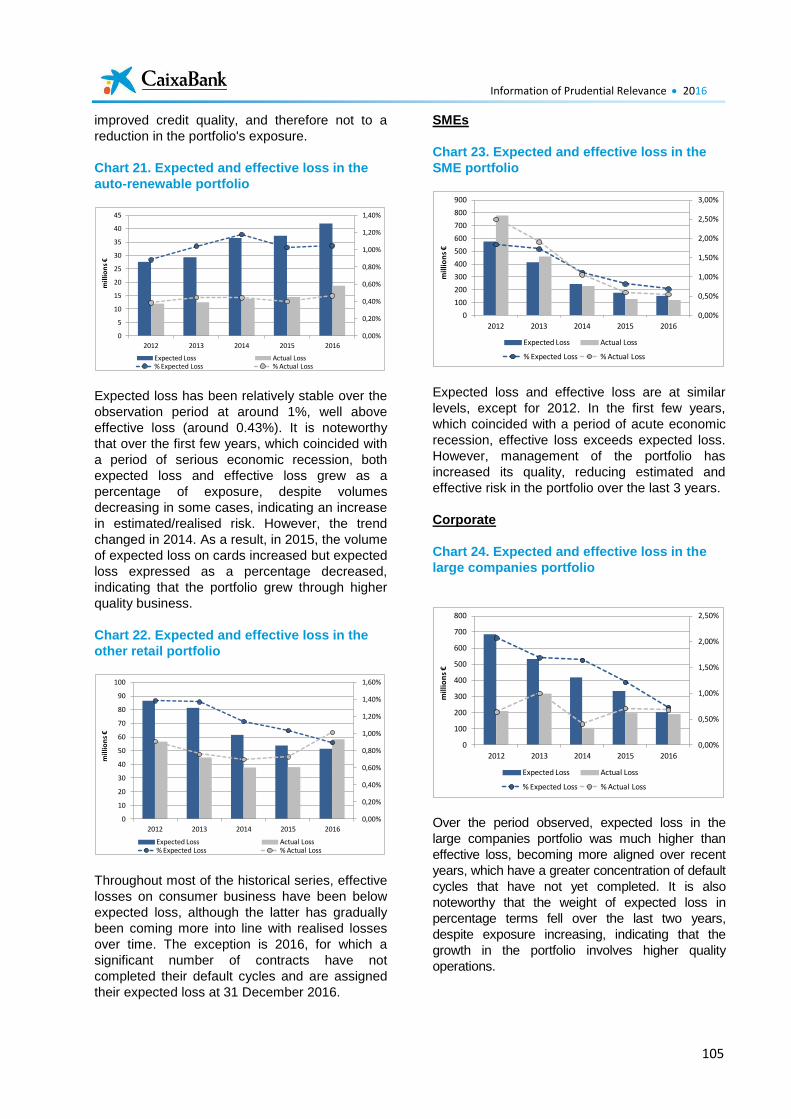

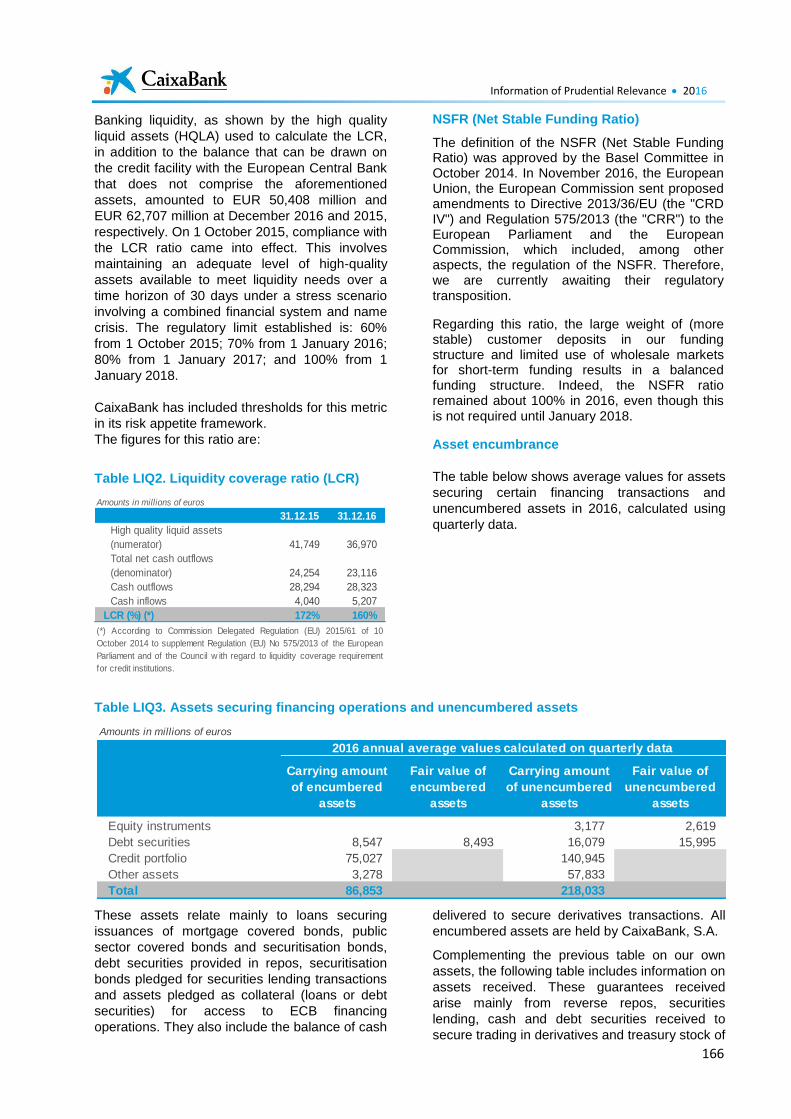

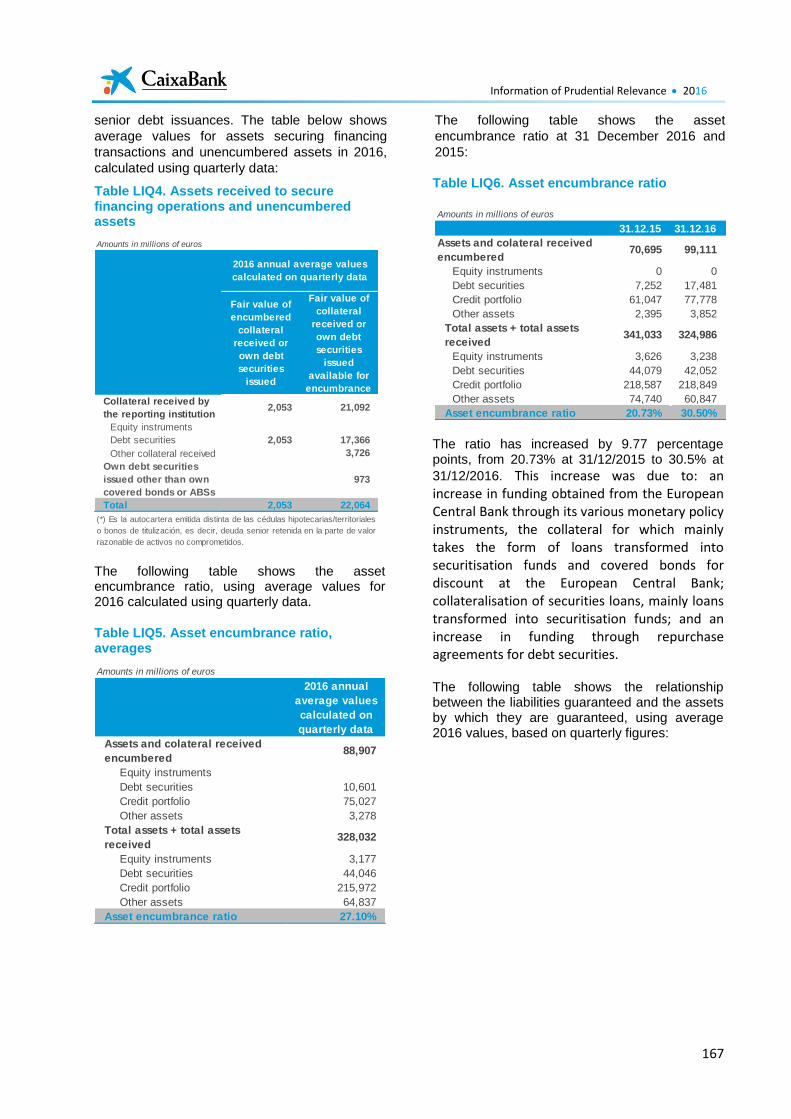

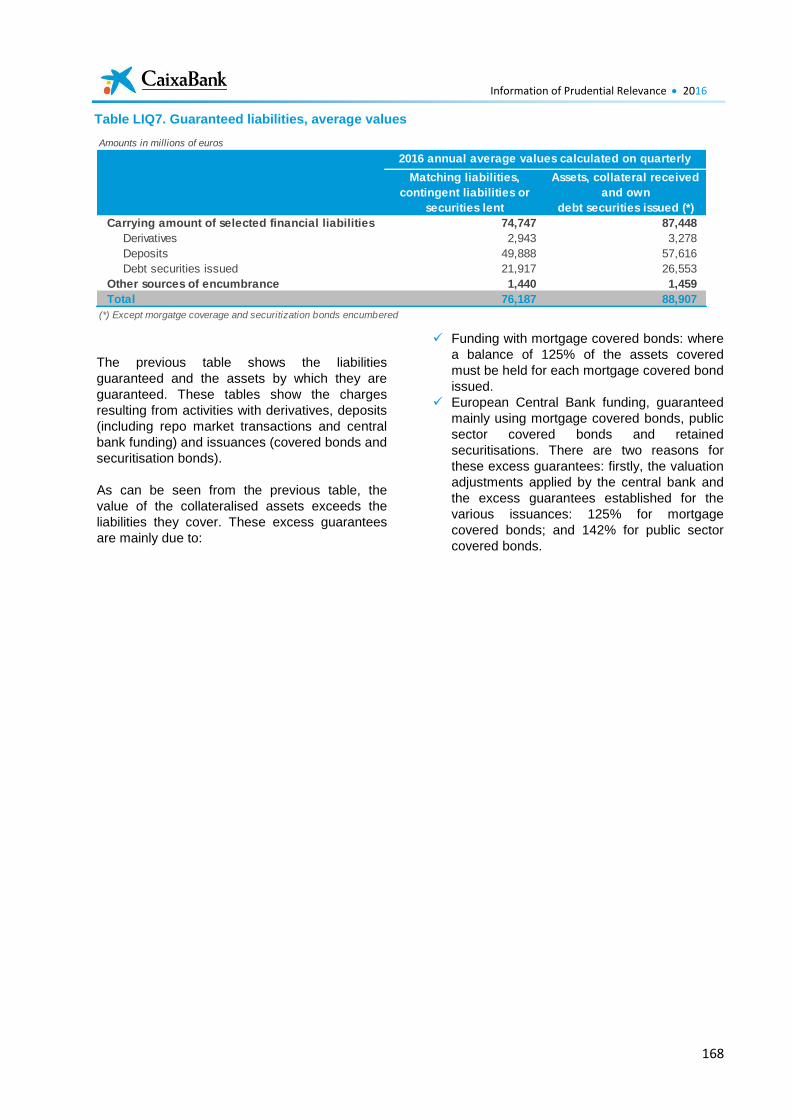

Embed Size (px)

Citation preview

Pillar 3 Disclosures CriteriaCaixa Group

at 31 December 2016

(*) This English version is a translation, for information purposes only, of the original document issued and prepared in Spanish. In the event of a discrepancy, the original Spanish-language version prevails.

2

Introduction

The Basel regulatory framework for banking is based on three pillars:

Pillar 1: Minimum capital requirements

Pillar 2: Supervisory review

Pillar 3: Market discipline

This report complies with the requirements of Part Eight of EU Regulation 575/2013 of the European Parliament and of the Council (hereinafter, the CRR), which constitutes Pillar 3 of the Basel regulations, with regard to public disclosure of the entity's risk profile, risk management system, control of own funds and solvency levels. In preparing this report, we have also taken into consideration a number of additional developments and best practices, established by the EBA (European Banking Authority).

The report was prepared taking into consideration Article 432.2 of the CRR concerning information regarded as confidential. The purpose of this report is to provide market players with an assessment of the capital adequacy of the CriteriaCaixa Group (Criteria Group) at 31 December 2016. Specifically, it contains disclosures on own funds, exposures and risk assessment processes in the scope of prudential consolidation at the Criteria Group. As the CaixaBank Group, which forms part of the Criteria Group, is also subject to Regulation (EU) No 575/2013 and has its own “Pillar 3 Disclosures” report (attached in Appendix IV), the purpose of this report is to provide additional information on the contribution made by Criteria, as the parent company of CaixaBank, to the scope of prudential consolidation of the Criteria Group, other than the contribution made by the CaixaBank Group.

In compliance with Regulation (EU) No 575/2013, in February 2015, the Board of Directors approved the adaptation of the formal policy for disclosing the “Pillar 3 Disclosures” report to the regulatory requirements.

At its 28 April 2017 meeting and following the review carried out by the Audit and Control Committee, Criteria's Board approved the present “Pillar 3 Disclosures”.

The report is published in the economic-financial information section of Criteria’s website.

3

Contents Contents .................................................................................................................. 3

1. General disclosure requirements .......................................................................... 7

1.1. Scope of application .............................................................................................................. 7

1.1.1. Accounting reconciliation between the Public Balance Sheet and the Confidential Balance Sheet ............................................................................................ 9

1.1.2. Description of the consolidated group ........................................................................ 11

1.1.3. Other general information ........................................................................................... 12

1.1.4. Nature of the investment in CaixaBank ....................................................................... 13

1.2. Governance and organisation ............................................................................................. 14

1.2.1. Criteria Internal governance ........................................................................................ 14

1.2.1.1. Board of Directors ................................................................................................. 14

1.2.1.2. Audit and Control Committee ............................................................................... 15

1.2.1.3. Appointments and Remuneration Committee ..................................................... 16

1.2.1.4. Risk management .................................................................................................. 17

1.2.2. Risk management structure and objectives ................................................................ 17

1.2.2.1 Structural organisation of the risk function .......................................................... 20

1.2.2.2. Corporate Risk Map............................................................................................... 22

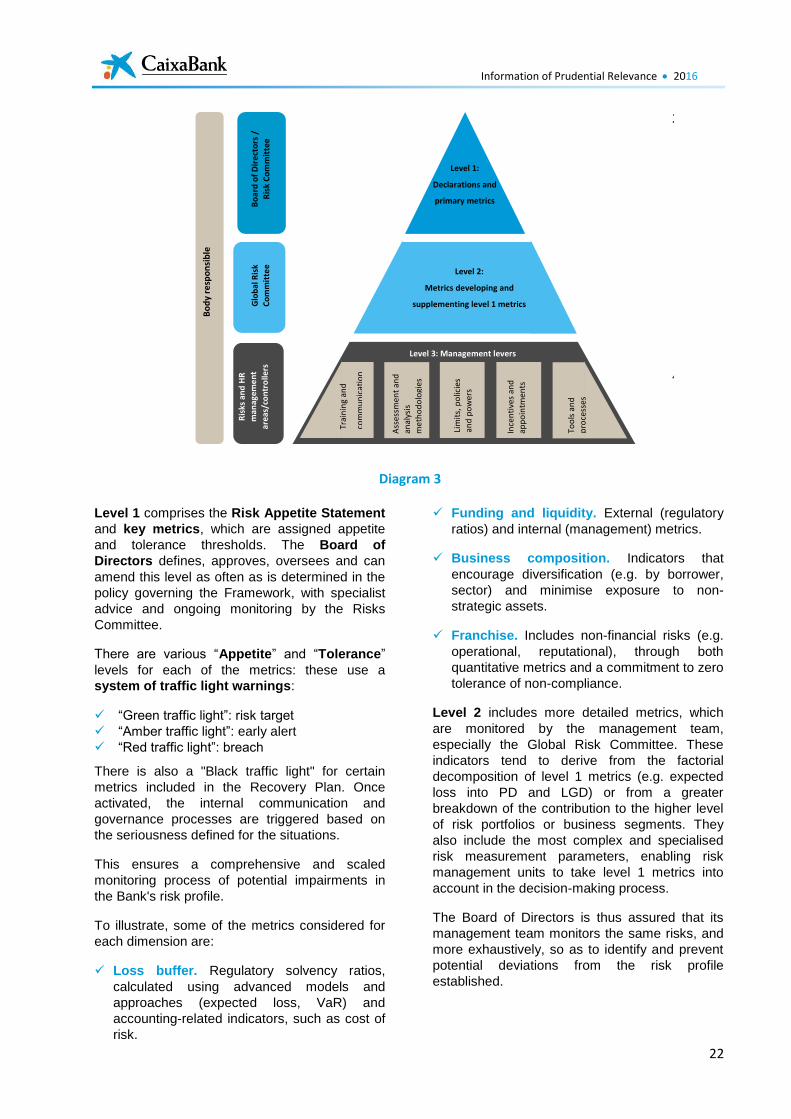

1.2.2.3. Risk Appetite Framework (RAF) ............................................................................ 23

1.2.3. Risk assessment and planning ..................................................................................... 27

1.2.4. Financial conglomerate................................................................................................ 27

1.2.5. Internal Control Model ................................................................................................ 28

1.3. Risk management policies and objectives ........................................................................... 30

1.3.1. Risk associated with equity investments ..................................................................... 30

1.3.2. Real estate risk ............................................................................................................. 34

1.3.3. Market risk ................................................................................................................... 36

1.3.4. Operational risk ........................................................................................................... 36

1.3.5. Liquidity risk ................................................................................................................. 37

1.3.6. Business risk ................................................................................................................. 39

1.3.7. Regulatory Compliance Risk ........................................................................................ 39

1.3.8. Legal / regulatory risk .................................................................................................. 41

2. Information on eligible own funds ...................................................................... 41

2.1. Regulatory framework ......................................................................................................... 41

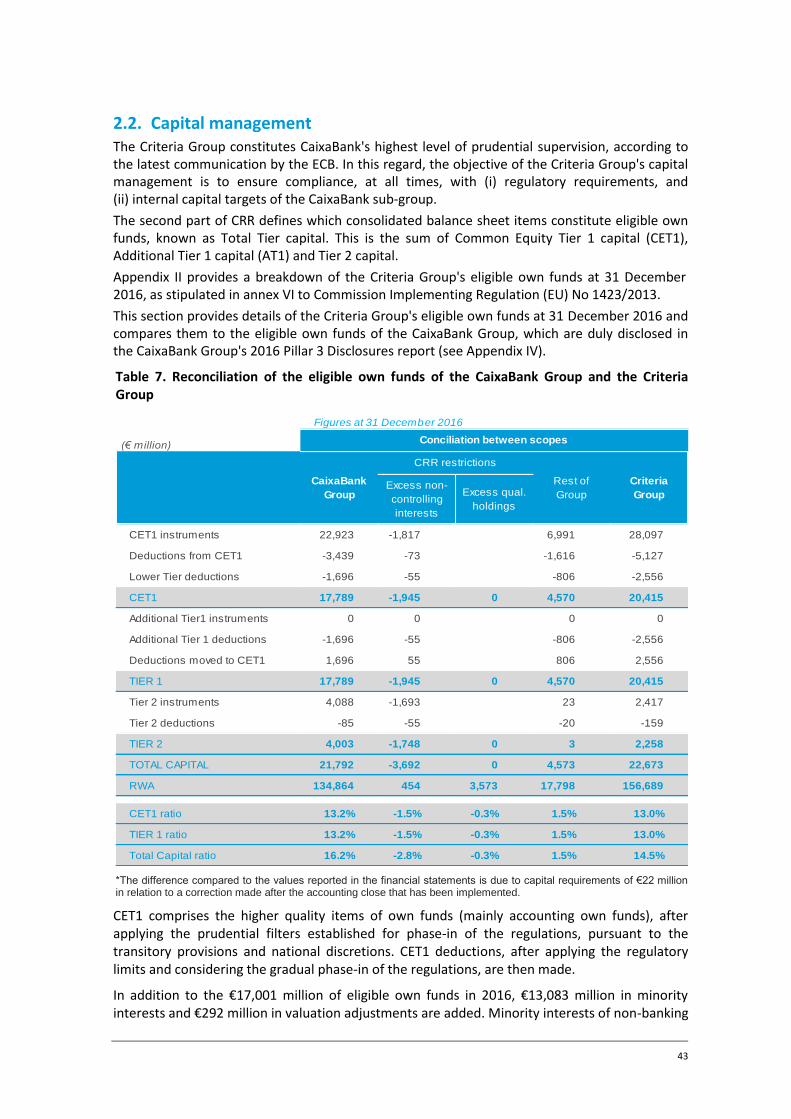

2.2. Capital management ........................................................................................................... 43

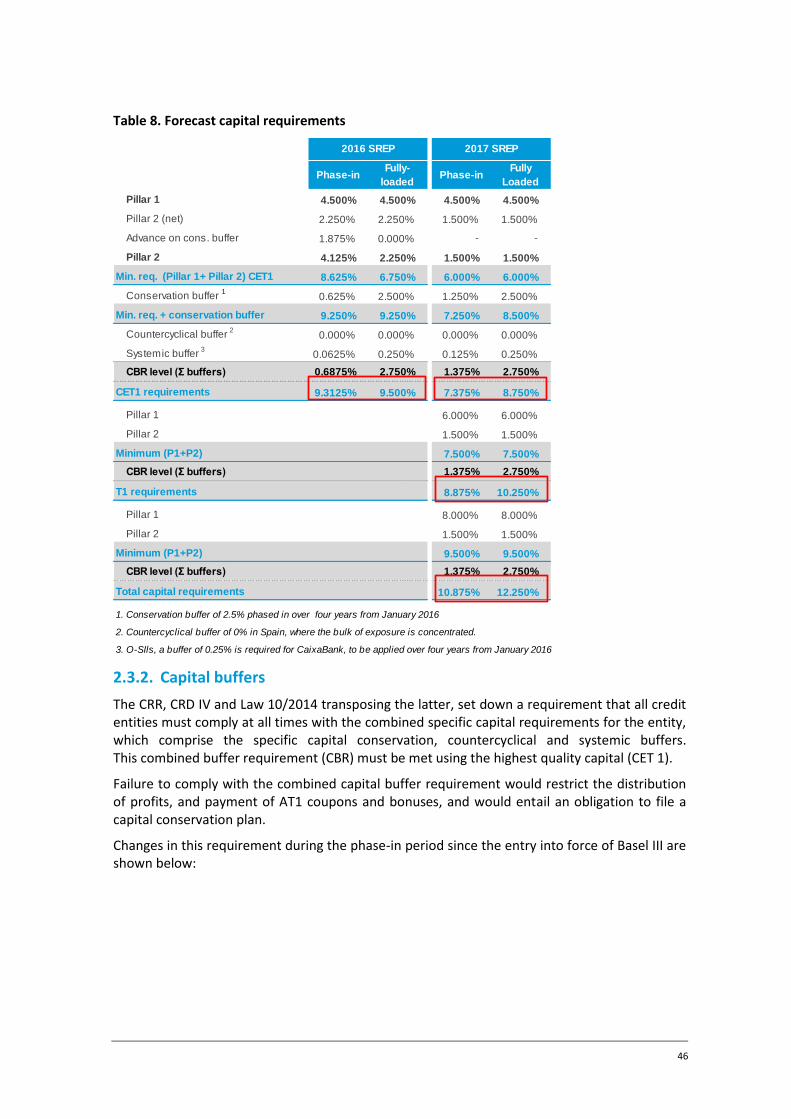

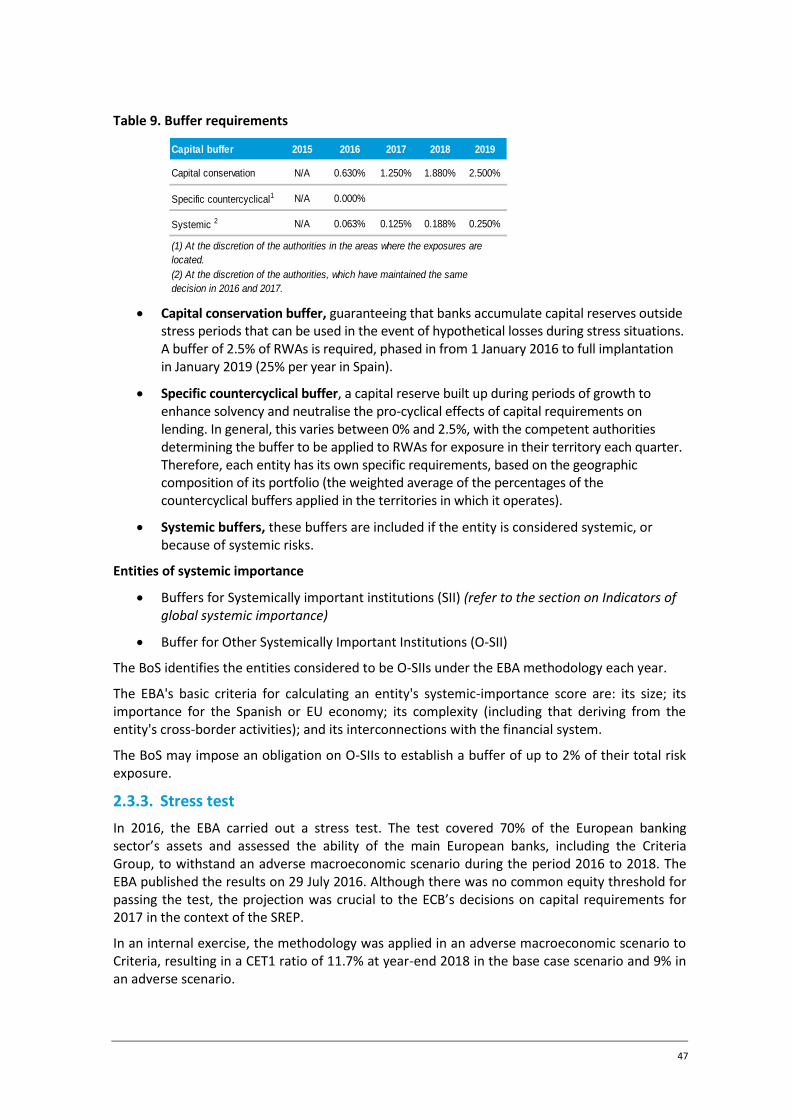

2.3. Capital buffers ..................................................................................................................... 44

2.3.1. Pillar 2: Internal Capital Adequacy Assessment........................................................... 44

4

2.3.2. Capital buffers .............................................................................................................. 46

2.3.3. Stress test .................................................................................................................... 47

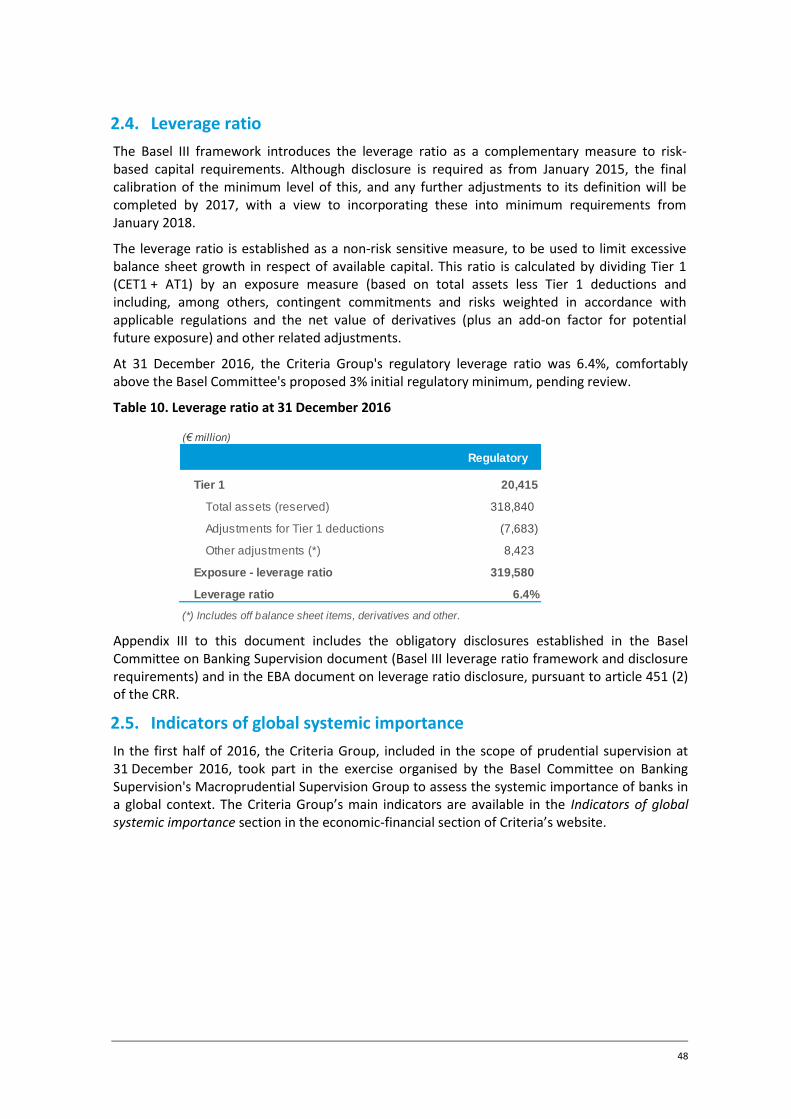

2.4. Leverage ratio ...................................................................................................................... 48

2.5. Indicators of global systemic importance ........................................................................... 48

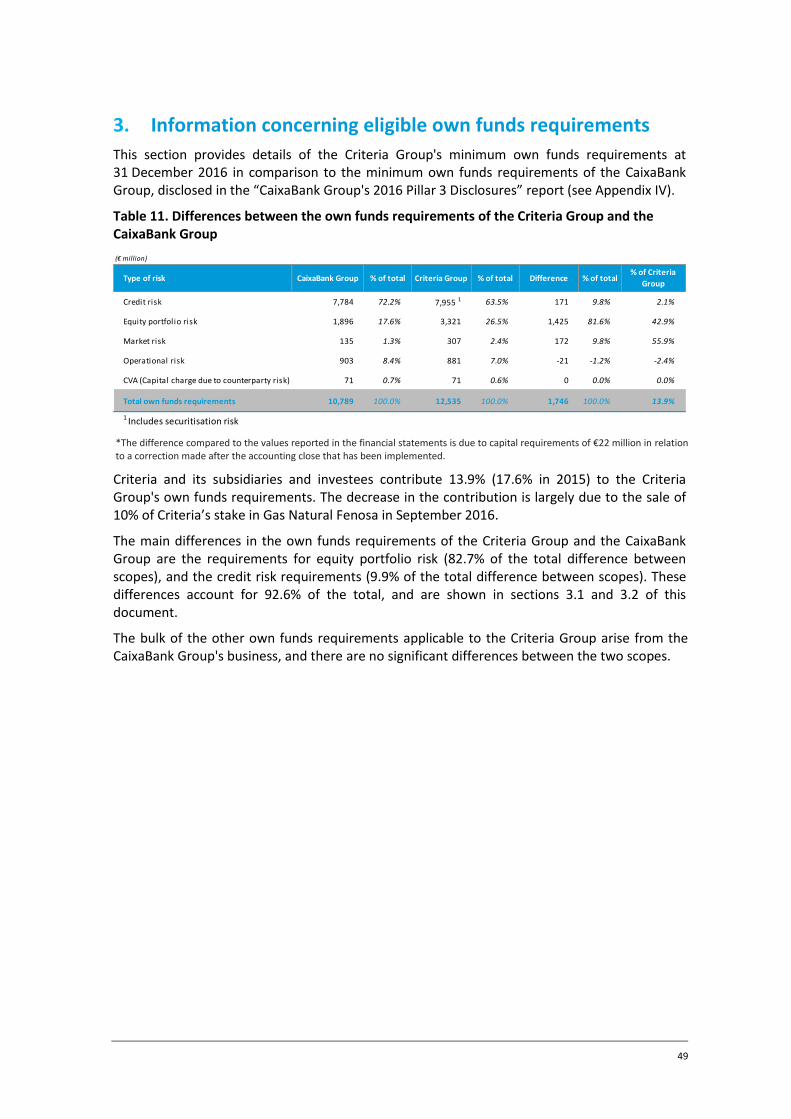

3. Information concerning eligible own funds requirements ................................... 49

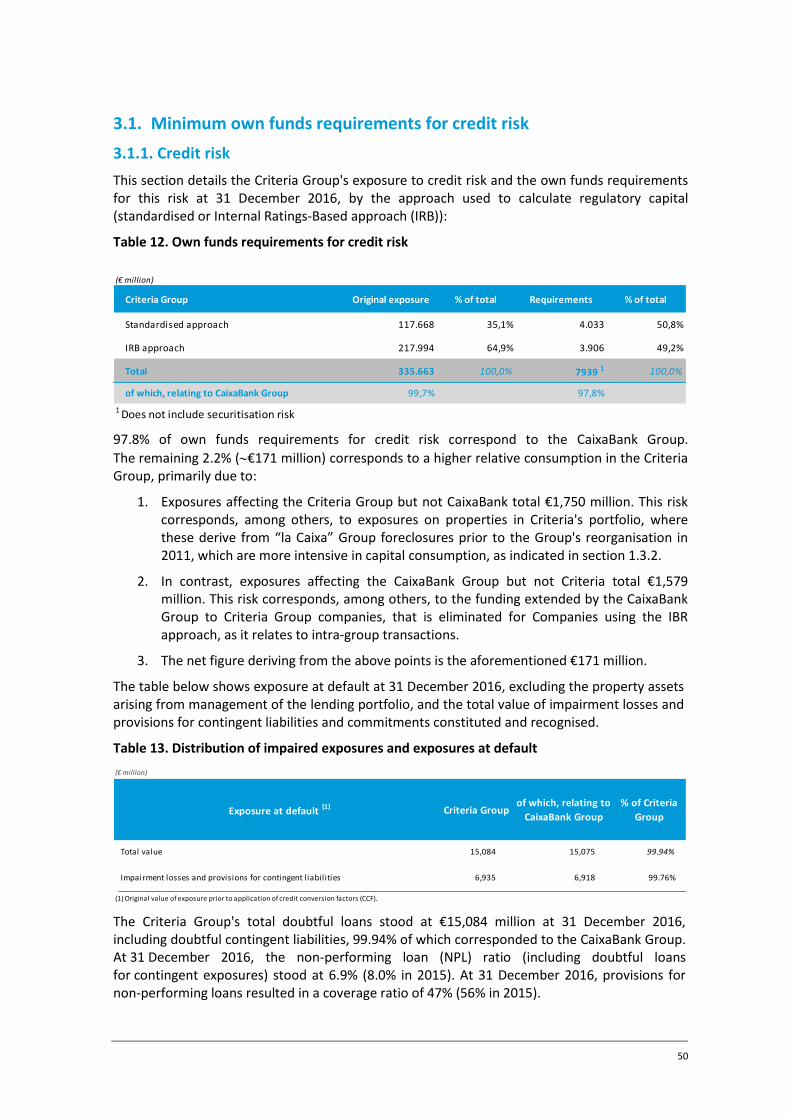

3.1. Minimum own funds requirements for credit risk .............................................................. 50

3.1.1. Credit risk ..................................................................................................................... 50

3.1.2. Counterparty risk ......................................................................................................... 51

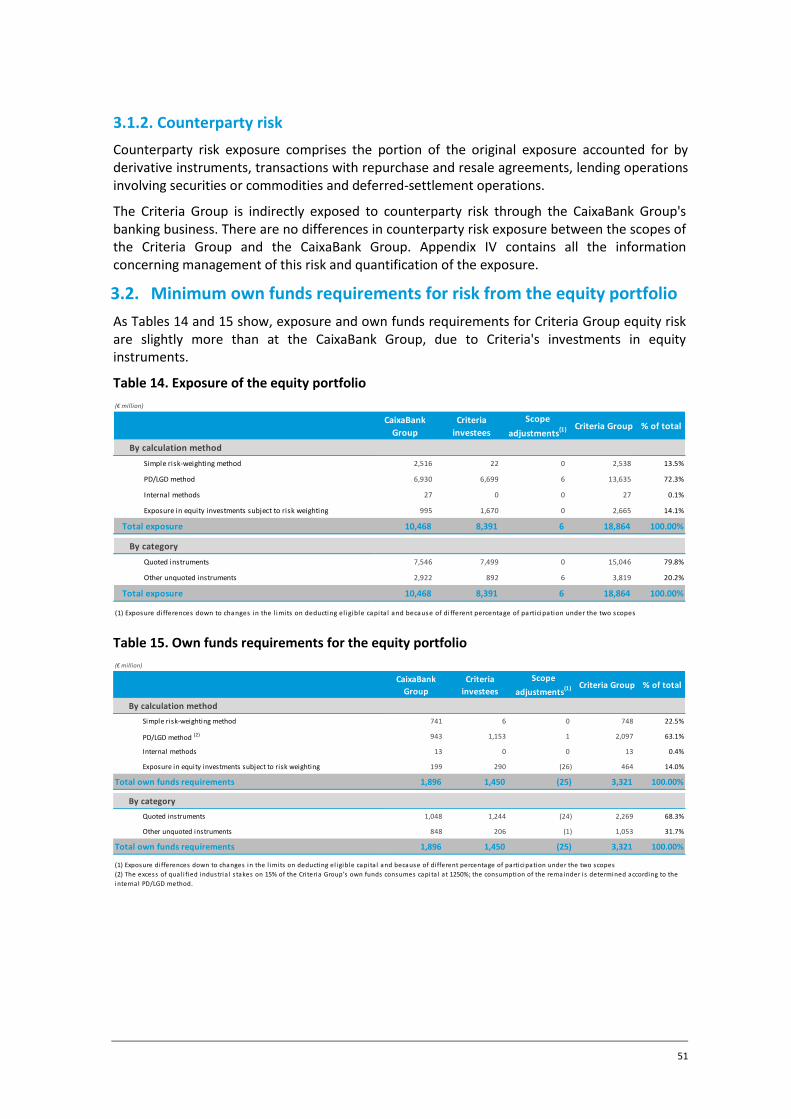

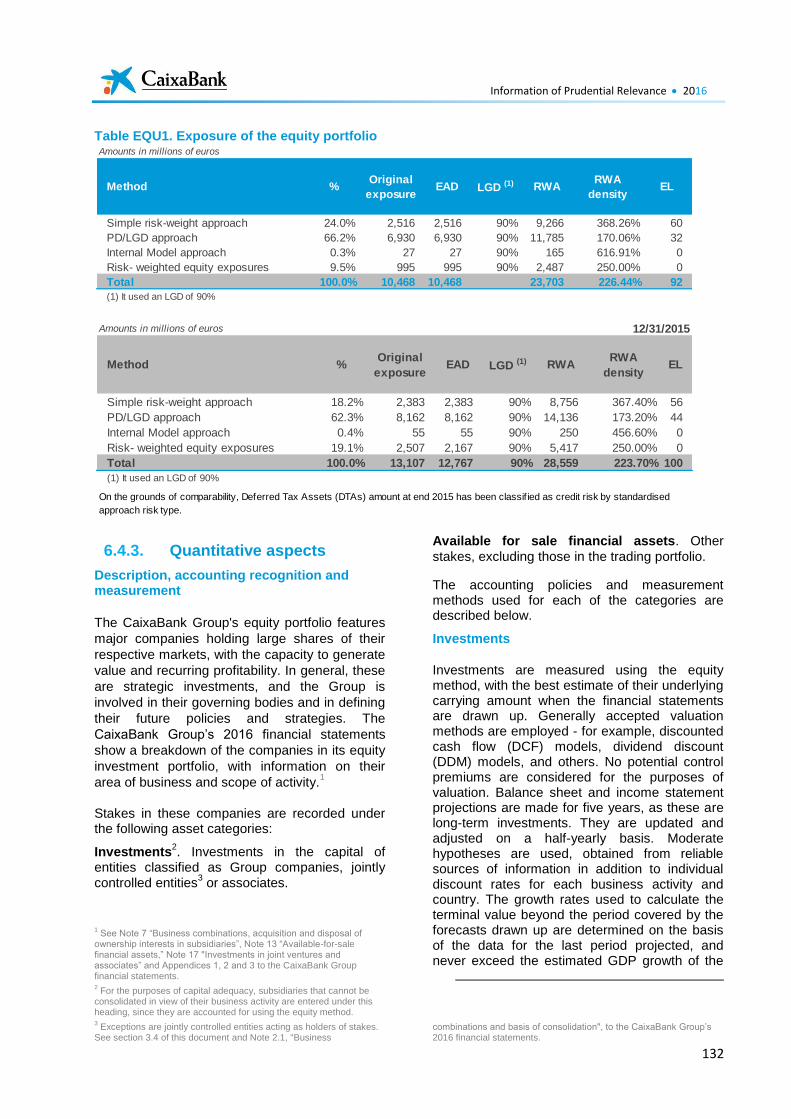

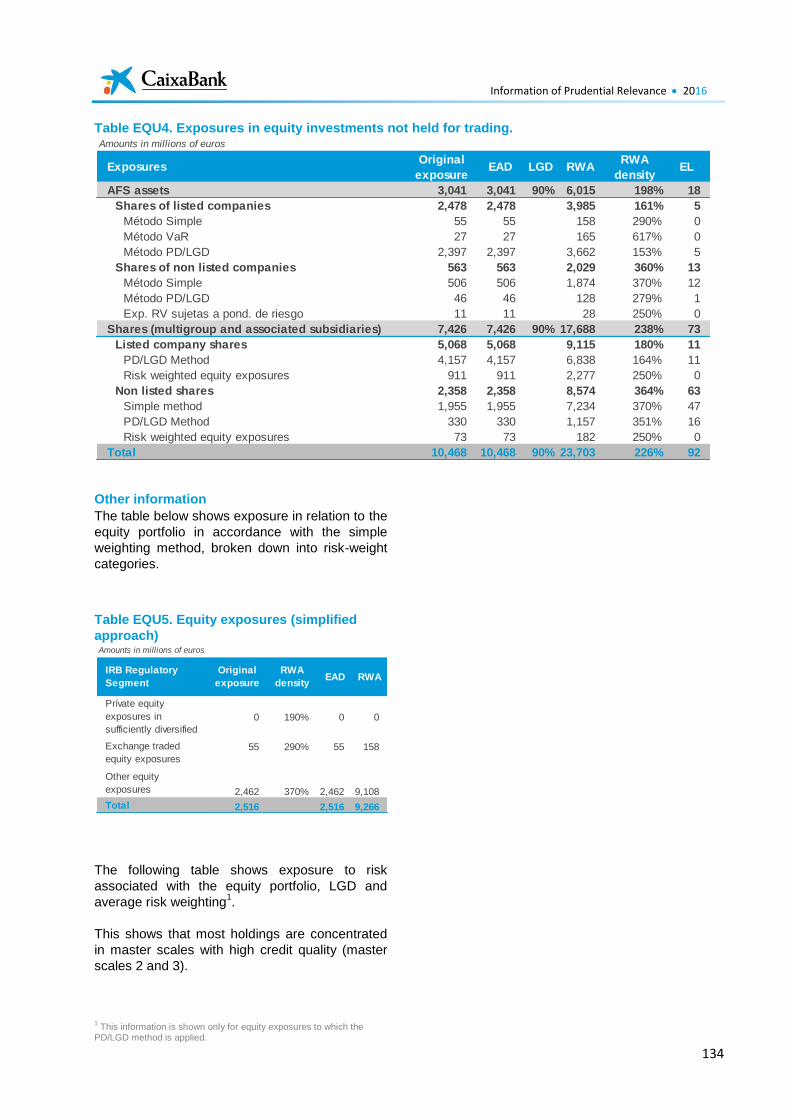

3.2. Minimum own funds requirements for risk from the equity portfolio ............................... 51

3.2.1. Description, accounting recognition and measurement ............................................. 52

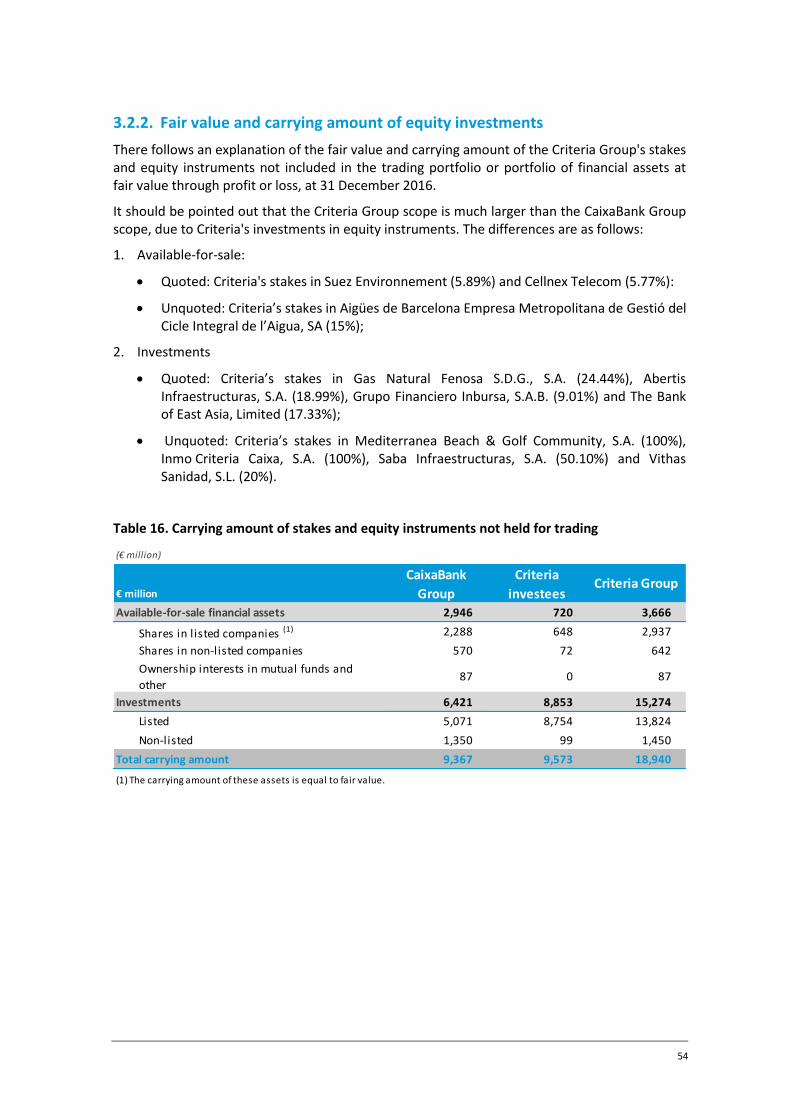

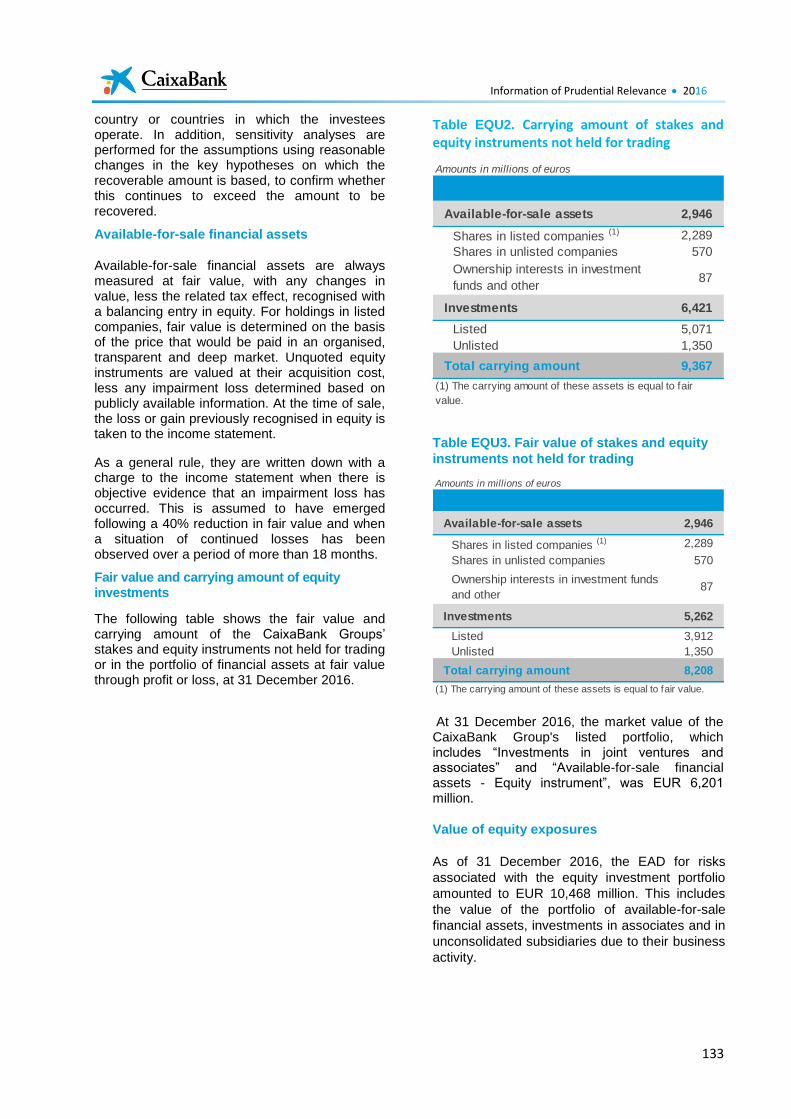

3.2.2. Fair value and carrying amount of equity investments ............................................... 54

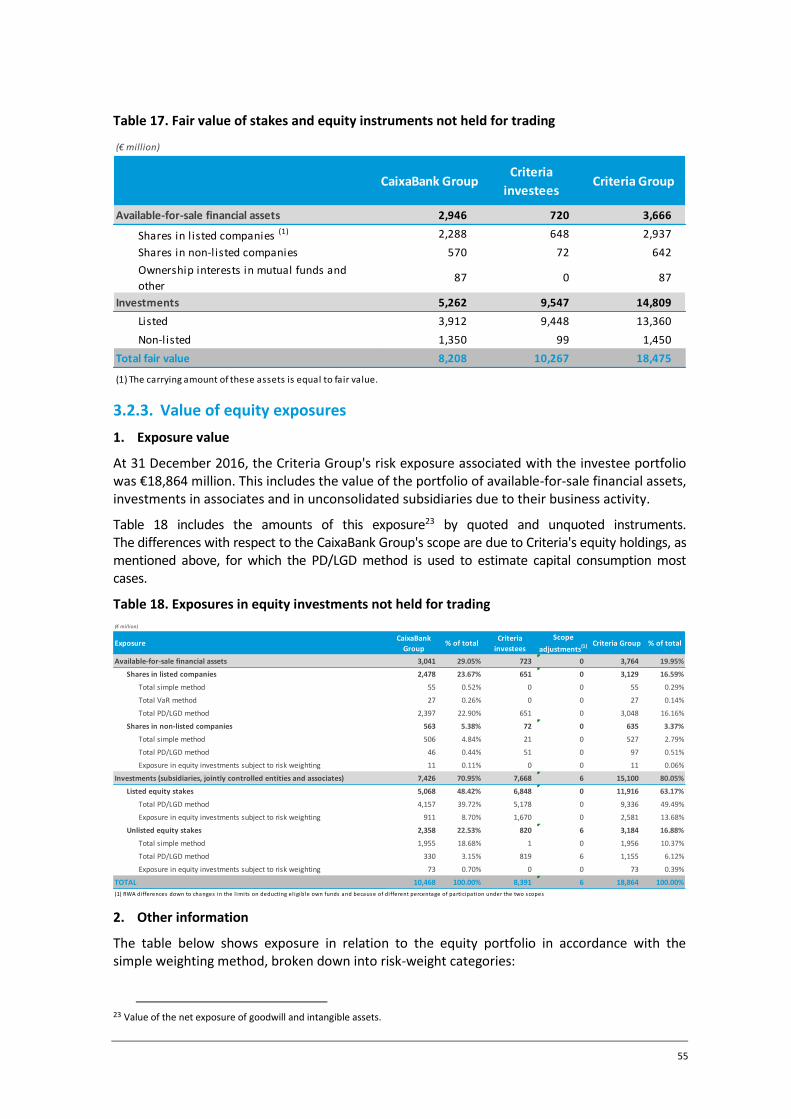

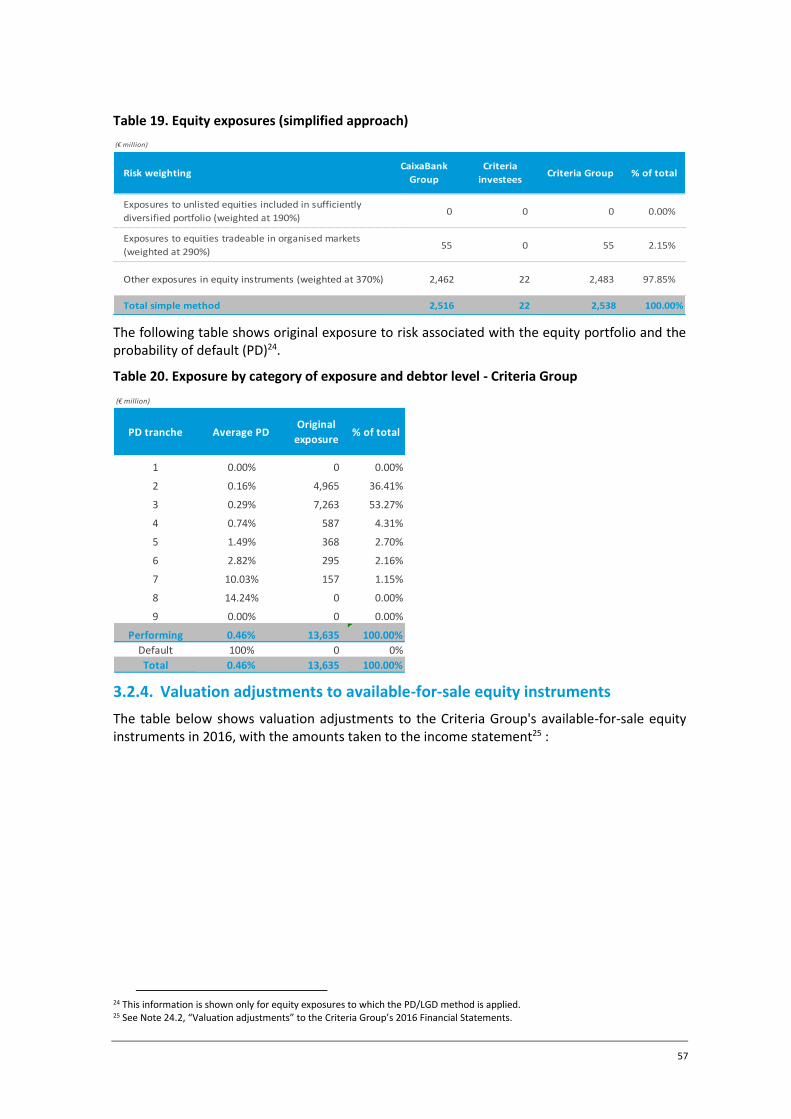

3.2.3. Value of equity exposures ........................................................................................... 55

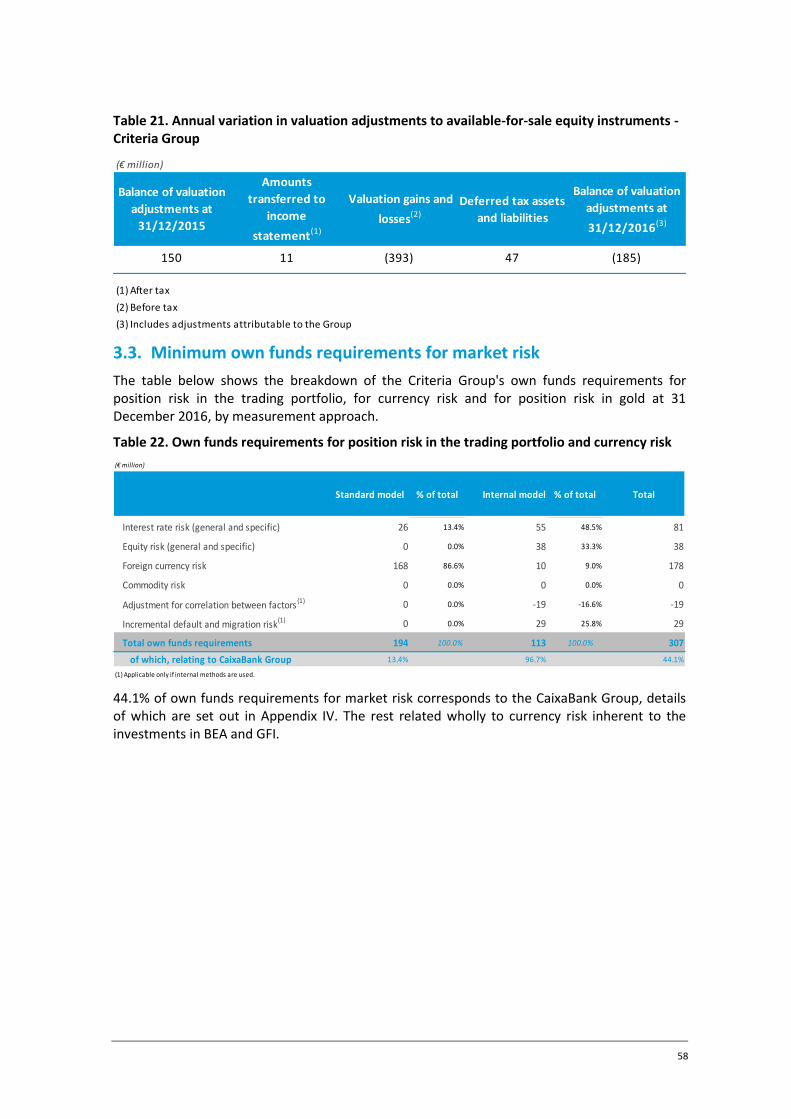

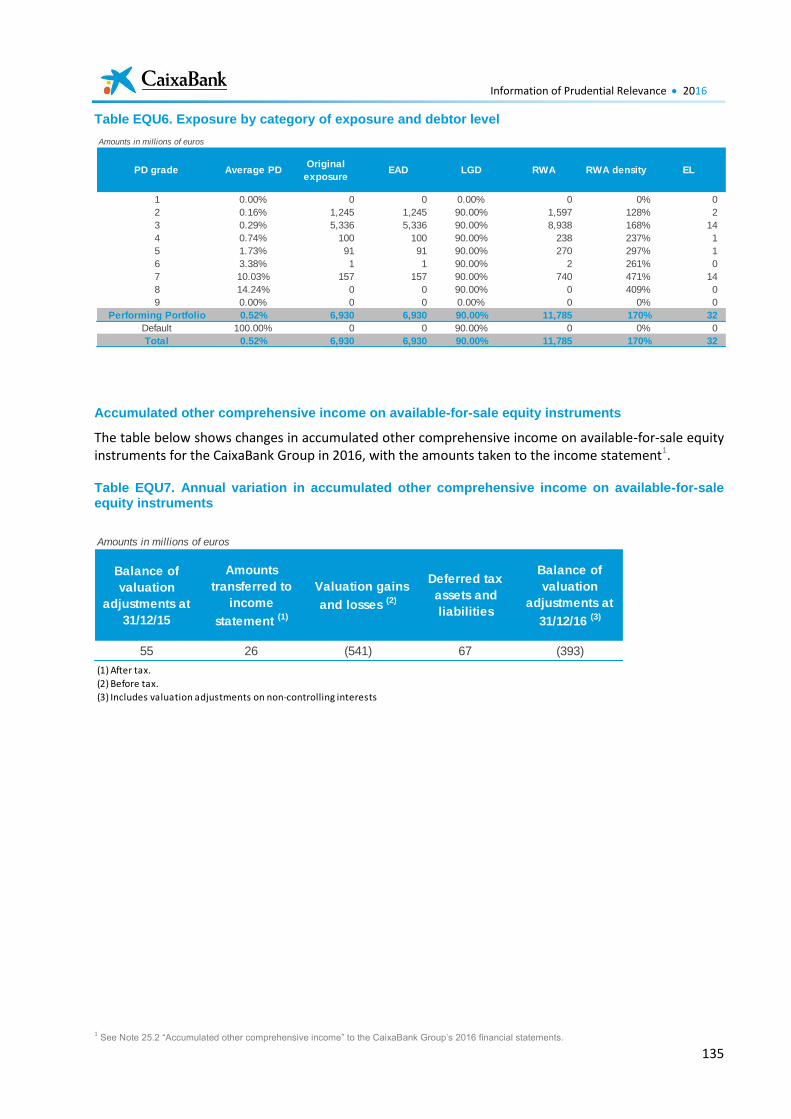

3.2.4. Valuation adjustments to available-for-sale equity instruments ................................ 57

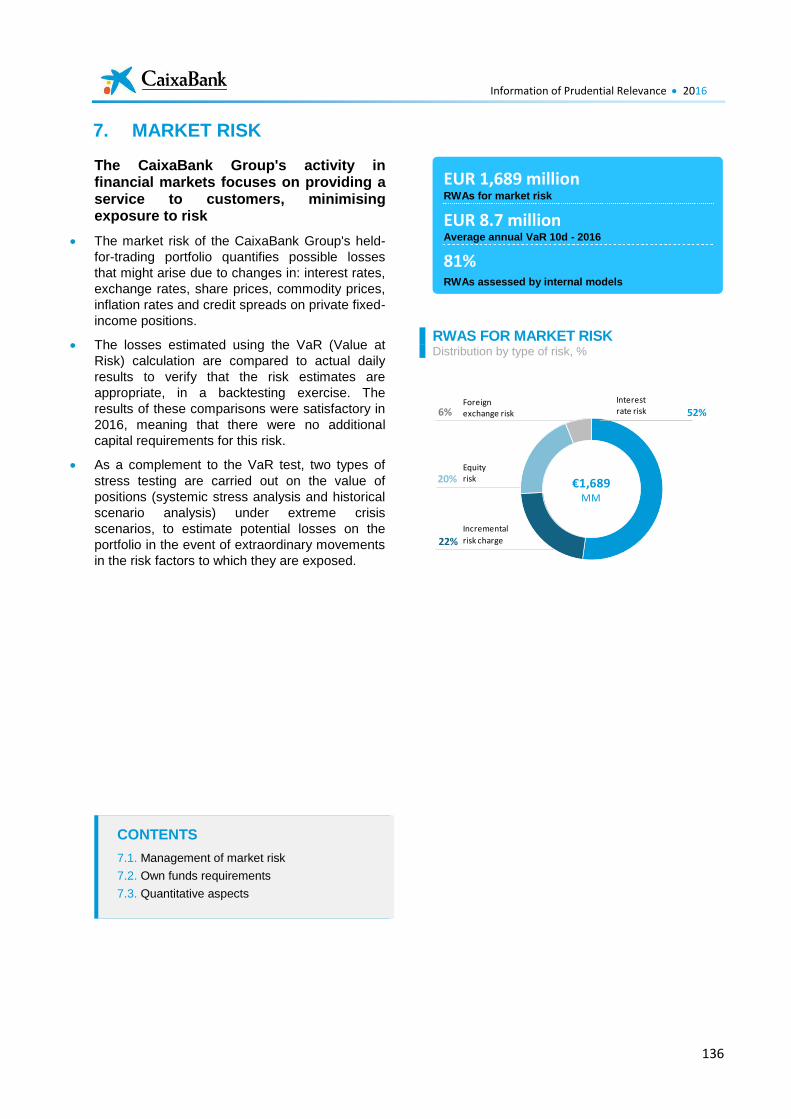

3.3. Minimum own funds requirements for market risk ............................................................ 58

3.4. Minimum own funds requirements for operational risk ..................................................... 59

3.5. Internal capital adequacy assessment procedure ............................................................... 59

4. Information concerning remuneration ............................................................... 61

Appendix I. Main features of capital instruments .................................................... 69

Appendix II. Transitional own funds ........................................................................ 71

Appendix III. Information on leverage ratio............................................................. 74

Appendix IV. CaixaBank Group's Pillar 3 Disclosures - 2016 ..................................... 77

5

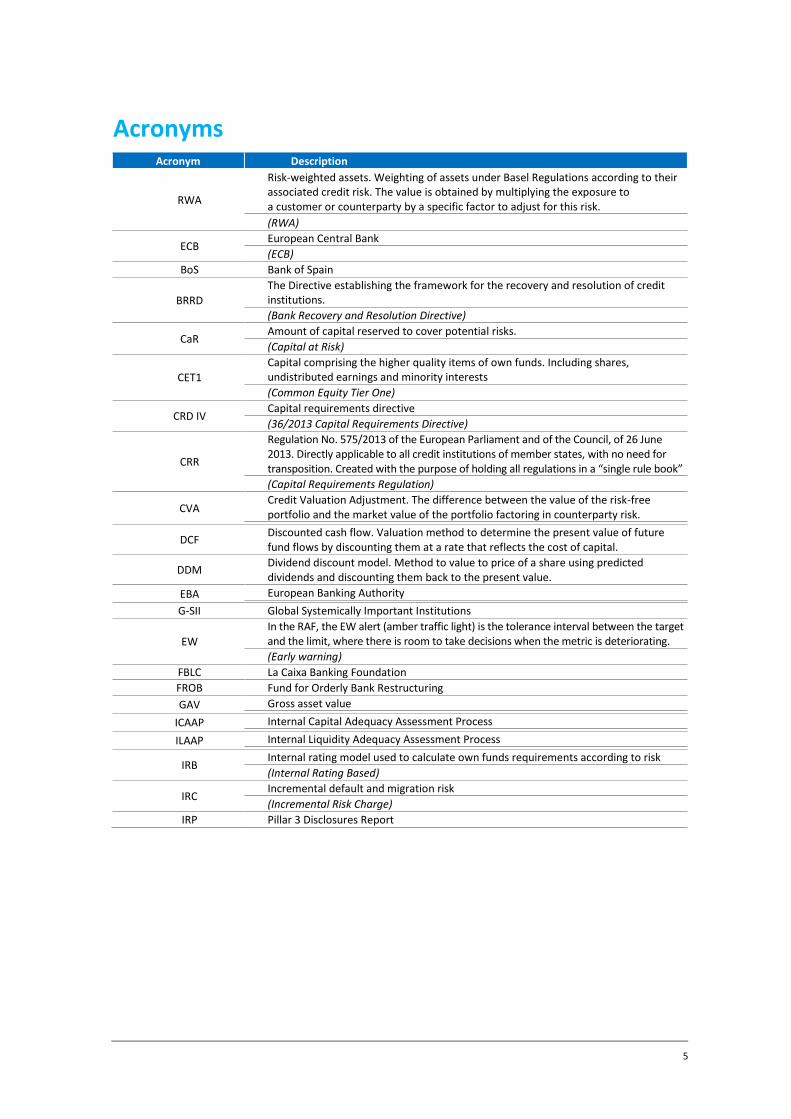

Acronyms Acronym Description

RWA

Risk-weighted assets. Weighting of assets under Basel Regulations according to their associated credit risk. The value is obtained by multiplying the exposure to a customer or counterparty by a specific factor to adjust for this risk.

(RWA)

ECB European Central Bank

(ECB)

BoS Bank of Spain

BRRD

The Directive establishing the framework for the recovery and resolution of credit institutions.

(Bank Recovery and Resolution Directive)

CaR Amount of capital reserved to cover potential risks.

(Capital at Risk)

CET1

Capital comprising the higher quality items of own funds. Including shares, undistributed earnings and minority interests

(Common Equity Tier One)

CRD IV Capital requirements directive

(36/2013 Capital Requirements Directive)

CRR

Regulation No. 575/2013 of the European Parliament and of the Council, of 26 June 2013. Directly applicable to all credit institutions of member states, with no need for transposition. Created with the purpose of holding all regulations in a “single rule book”

(Capital Requirements Regulation)

CVA Credit Valuation Adjustment. The difference between the value of the risk-free portfolio and the market value of the portfolio factoring in counterparty risk.

DCF

Discounted cash flow. Valuation method to determine the present value of future fund flows by discounting them at a rate that reflects the cost of capital.

DDM Dividend discount model. Method to value to price of a share using predicted dividends and discounting them back to the present value.

EBA European Banking Authority

G-SII Global Systemically Important Institutions

EW

In the RAF, the EW alert (amber traffic light) is the tolerance interval between the target and the limit, where there is room to take decisions when the metric is deteriorating.

(Early warning)

FBLC La Caixa Banking Foundation

FROB Fund for Orderly Bank Restructuring

GAV Gross asset value

ICAAP Internal Capital Adequacy Assessment Process

ILAAP Internal Liquidity Adequacy Assessment Process

IRB

Internal rating model used to calculate own funds requirements according to risk

(Internal Rating Based)

IRC Incremental default and migration risk

(Incremental Risk Charge)

IRP Pillar 3 Disclosures Report

6

Acronym Description

LGD Loss Given Default. Percentage of exposure to risk that is not expected to be recovered in the event of default

MDA

Maximum distributable amount payable in the form of dividends

(Maximum distributable amount)

MREL

Requirement that entities must have sufficient eligible instruments to absorb losses, and where applicable, recapitalise the entity

(Minimum Requirement of Eligible Liabilities)

SRM

Single Resolution Mechanism

EU system to manage crises in unviable financial institutions, to ensure an orderly resolution of failing banks with minimal costs to taxpayers and to the real economy

SSM Single Supervisory Mechanism

Comprising the ECB and supervisory authorities in participant EU countries

NAV Net Asset Value

IFRS International Financial Reporting Standards

O-SII Other Systemically Important Institution

PD Credit rating measurement to assess the probability of default on a one year horizon

(Probability of Default)

RAF Risk Appetite Framework

ICFRS

Internal Control over Financial Reporting System. A series of processes carried out by the Board of Directors, the Audit Committee, Senior Management and relevant employees to provide reasonable assurance of the reliability of the financial information disclosed to the markets.

SREP Supervisory Review and Evaluation Process

Additional TIER1 (AT1)

Capital mainly comprising hybrid instruments able to absorb losses on a going concern basis They must meet the following requirements: 1. Subordinated instruments, 2. Non-cumulative discretionary coupons or dividends, 3. No maturity date or incentive to redeem, 4. Retail products meeting requirements 1, 2 and 3, with quantitative limits

(Additional Tier 1 Capital)

TIER2 - T2

Capital mainly comprising hybrid instruments able to absorb losses on a gone concern basis They must meet the following requirements: 1. Subordinated instruments, 2. With a minimum residual life of 5 years, and 3. The investor has no rights to step up the payment of future flows (coupons or principal) except in the event of failure and liquidation

EU European Union

VaR Value at Risk

7

1. General disclosure requirements

1.1. Scope of application

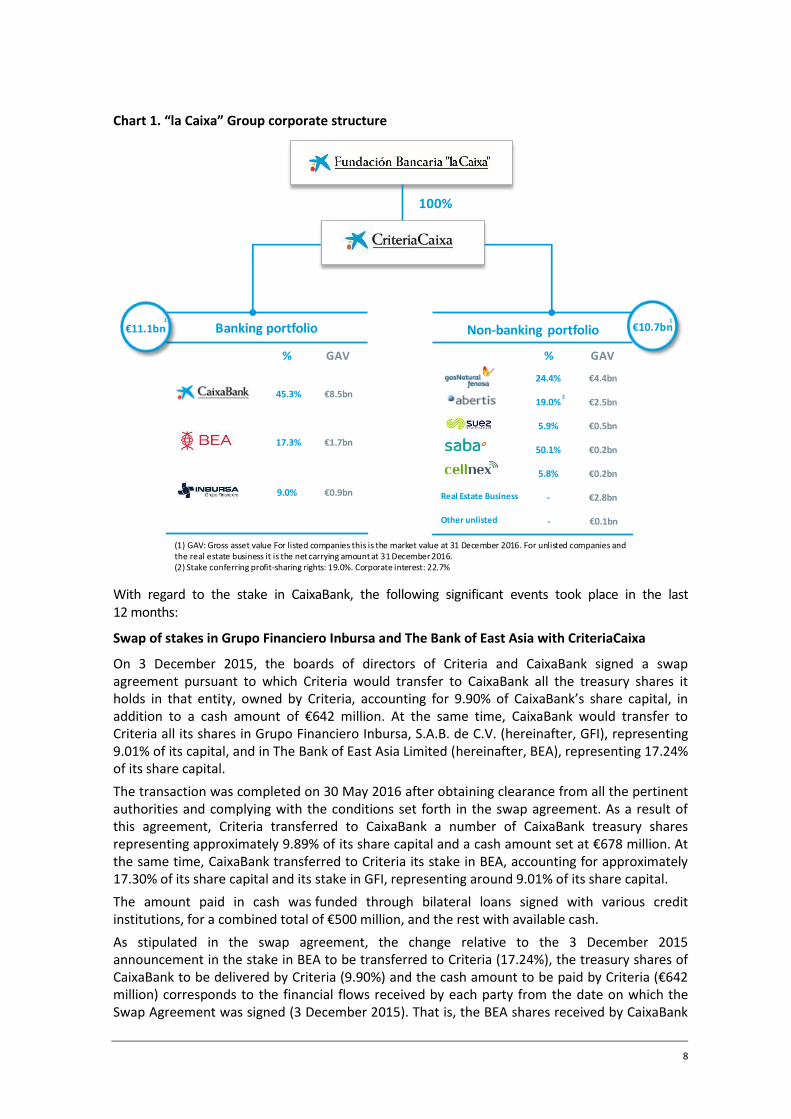

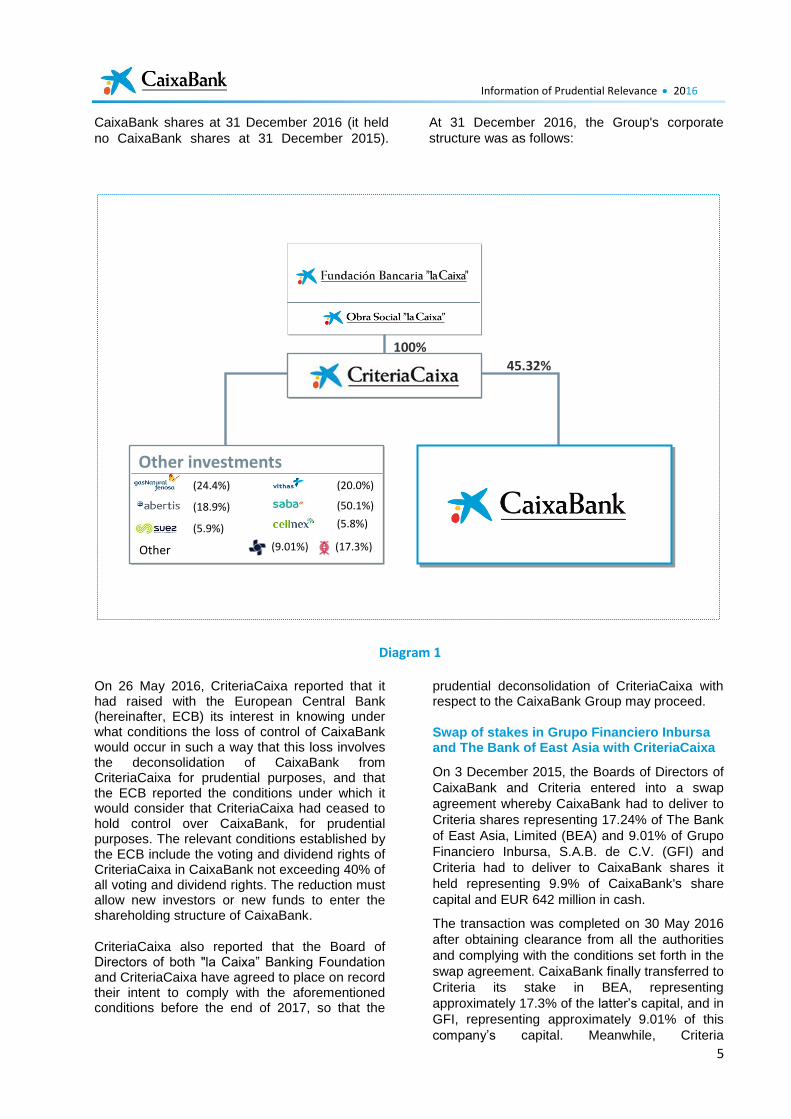

The financial information set out in this report concerns the Criteria Group, the parent company of which is Criteria Caixa, SAU (hereinafter, “Criteria”), which at 31 December 2016 held a 45.32% stake in CaixaBank, SA.

Criteria forms part of Grupo Fundación Bancaria Caixa d’Estalvis i Pensions de Barcelona “la Caixa” (formerly Grupo Caixa d’Estalvis i Pensions de Barcelona) (hereinafter, the “la Caixa” Group), the parent company of which is Fundació Bancària “la Caixa”, Criteria's sole shareholder (hereinafter, “FBLC”).

Following completion of the corporate restructuring process in October 2014, FBLC is primarily engaged in the direct management of its welfare projects and, through Criteria (a wholly-owned company), manages the “la Caixa” Group's business assets, essentially comprising shareholdings in strategic sectors, including domestic and international banking, through its stake in CaixaBank (the leading financial group in the Spanish retail banking market), energy, infrastructure, services and real estate.

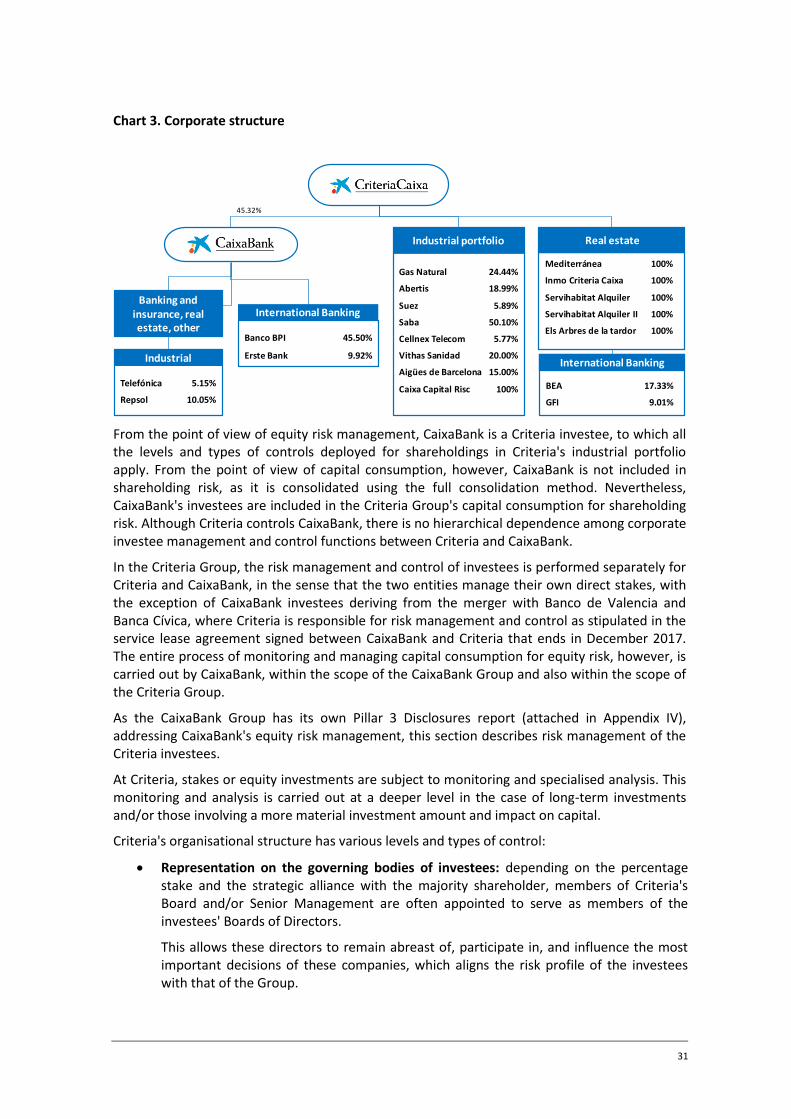

It should be pointed out that by consolidating a banking group such as CaixaBank using the full consolidation method (the CaixaBank Group contributes 96% of the total assets of the Criteria Group), most risks faced and managed by the Criteria Group relate to the CaixaBank Group's banking and insurance business. Since the CaixaBank Group has its own “Pillar 3 Disclosures” report, attached in Appendix IV, setting out all the risks arising from its business and associated capital requirements, the purpose of this report is to disclose additional information on the contribution made by Criteria, as the parent company of CaixaBank, to the scope of prudential consolidation of the Criteria Group, other than the contribution made by the CaixaBank Group (see scope of application in Chart 1). CaixaBank's Senior Management and governance bodies manage the risks arising from the CaixaBank Group's business activities.

8

Chart 1. “la Caixa” Group corporate structure

With regard to the stake in CaixaBank, the following significant events took place in the last 12 months:

Swap of stakes in Grupo Financiero Inbursa and The Bank of East Asia with CriteriaCaixa

On 3 December 2015, the boards of directors of Criteria and CaixaBank signed a swap agreement pursuant to which Criteria would transfer to CaixaBank all the treasury shares it holds in that entity, owned by Criteria, accounting for 9.90% of CaixaBank’s share capital, in addition to a cash amount of €642 million. At the same time, CaixaBank would transfer to Criteria all its shares in Grupo Financiero Inbursa, S.A.B. de C.V. (hereinafter, GFI), representing 9.01% of its capital, and in The Bank of East Asia Limited (hereinafter, BEA), representing 17.24% of its share capital.

The transaction was completed on 30 May 2016 after obtaining clearance from all the pertinent authorities and complying with the conditions set forth in the swap agreement. As a result of this agreement, Criteria transferred to CaixaBank a number of CaixaBank treasury shares representing approximately 9.89% of its share capital and a cash amount set at €678 million. At the same time, CaixaBank transferred to Criteria its stake in BEA, accounting for approximately 17.30% of its share capital and its stake in GFI, representing around 9.01% of its share capital.

The amount paid in cash was funded through bilateral loans signed with various credit institutions, for a combined total of €500 million, and the rest with available cash.

As stipulated in the swap agreement, the change relative to the 3 December 2015 announcement in the stake in BEA to be transferred to Criteria (17.24%), the treasury shares of CaixaBank to be delivered by Criteria (9.90%) and the cash amount to be paid by Criteria (€642 million) corresponds to the financial flows received by each party from the date on which the Swap Agreement was signed (3 December 2015). That is, the BEA shares received by CaixaBank

Banking portfolio

45.3%

17.3%

9.0%

Non-banking portfolio

24.4%

19.0%

5.9%

5.8%

50.1%

€11.1bn €10.7bn

€8.5bn

€1.7bn

€0.9bn

€4.4bn

€2.5bn

€0.5bn

€0.2bn

€0.2bn

€2.8bnReal Estate Business -

% GAV % GAV

€0.1bnOther unlisted -

100%

2

1 1

(1) GAV: Gross asset value For listed companies this is the market value at 31 December 2016. For unlisted companies andthe real estate business it is the net carrying amount at 31 December 2016.(2) Stake conferring profit-sharing rights: 19.0%. Corporate interest: 22.7%

9

as a scrip dividend, the CaixaBank shares received by Criteria as a scrip dividend and the net adjustment for the dividends received in cash by Criteria and CaixaBank corresponding to the shares being transferred under the swap agreement.

As a result of the swap, the shareholder agreements relating to BEA and GFI were amended accordingly in order for Criteria to take over CaixaBank’s position as the new shareholder. CaixaBank will remain as a banking partner to both banks to continue cooperating with them in commercial activities. When making strategic investments in banks that operate on the American continent and in the Asia-Pacific area, Criteria and CaixaBank will continue to operate through GFI and BEA, respectively, except where GFI decides not to take part in the investment.

CaixaBank’s takeover bid for Banco BPI

The acceptance period for CaixaBank’s takeover bid for Banco BPI, S.A. ended on 7 February 2017. Acceptance of the offer totalled 568,362,308 Banco BPI, S.A. shares, representing 39.01% of its share capital. The price offered was €1.134 per share, with a total pay-out of €644,522,857.27.

As a result of the bid, CaixaBank’s stake in Banco BPI, S.A. has increased from 45.5% to 84.51% of its share capital.

The impact of this transaction has not been included in this report. For further information, see Appendix IV. CaixaBank Group's Pillar 3 Disclosures report.

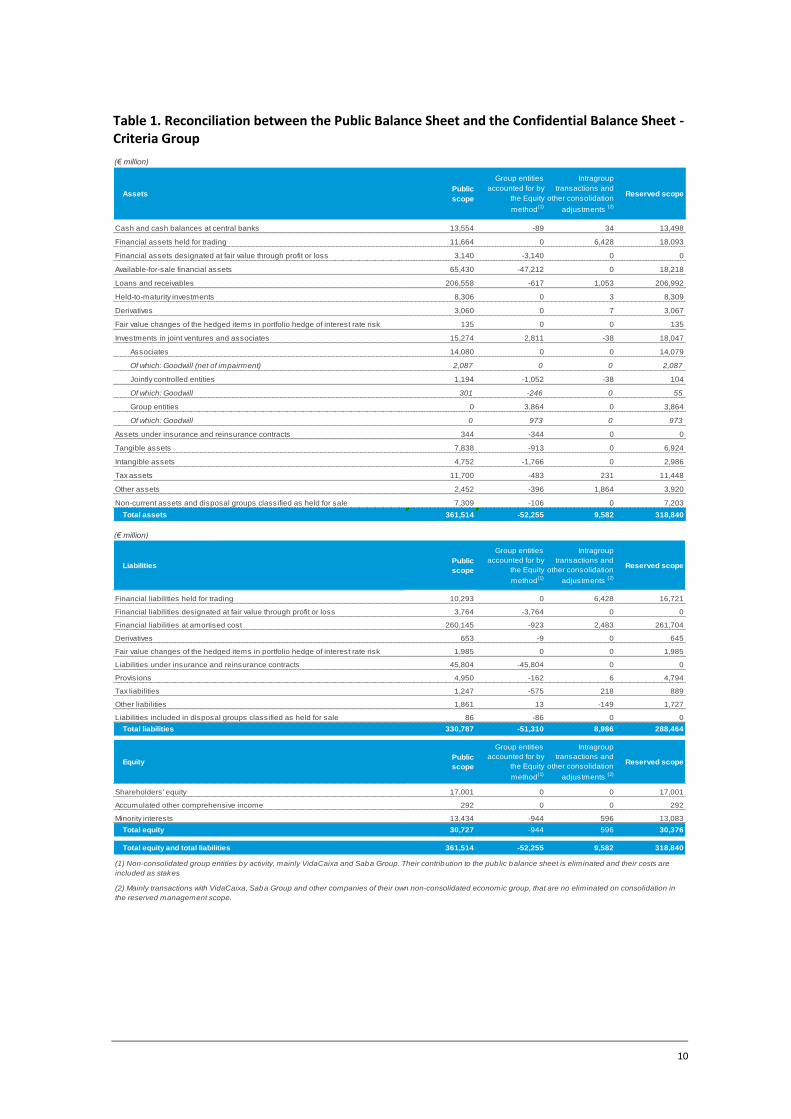

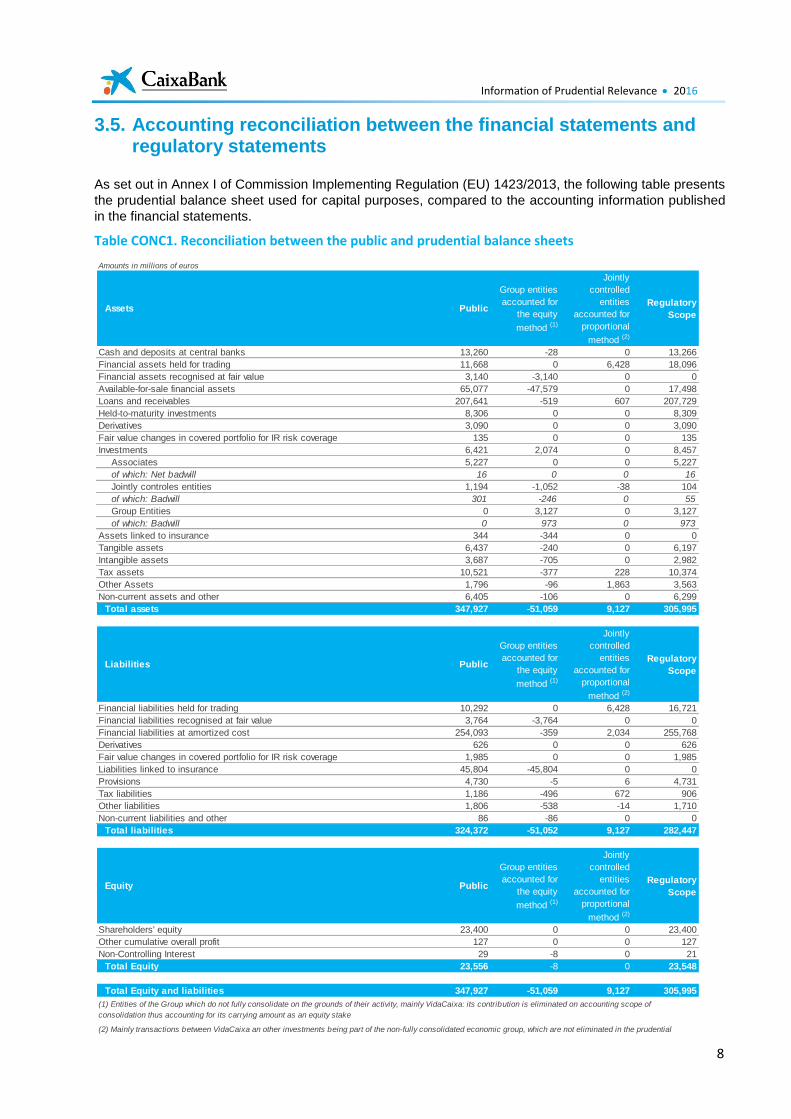

1.1.1. Accounting reconciliation between the Public Balance Sheet and the Confidential Balance Sheet

As set out in Annex I of Commission Implementing Regulation (EU) 1423/2013, the following table reconciles the balance sheet items used to calculate eligible own funds and regulatory own funds, comparing the accounting information disclosed in the financial statements with the confidential balance sheet regulatory information included in this report.

10

Table 1. Reconciliation between the Public Balance Sheet and the Confidential Balance Sheet - Criteria Group

Amounts in millions of euros

AssetsPublic

scope

Group entities

accounted for by

the Equity

method(1)

Intragroup

transactions and

other consolidation

adjustments (2)

Reserved scope

Cash and cash balances at central banks 13,554 -89 34 13,498

Financial assets held for trading 11,664 0 6,428 18,093

Financial assets designated at fair value through profit or loss 3,140 -3,140 0 0

Available-for-sale financial assets 65,430 -47,212 0 18,218

Loans and receivables 206,558 -617 1,053 206,992

Held-to-maturity investments 8,306 0 3 8,309

Derivatives 3,060 0 7 3,067

Fair value changes of the hedged items in portfolio hedge of interest rate risk 135 0 0 135

Investments in joint ventures and associates 15,274 2,811 -38 18,047

Associates 14,080 0 0 14,079

Of which: Goodwill (net of impairment) 2,087 0 0 2,087

Jointly controlled entities 1,194 -1,052 -38 104

Of which: Goodwill 301 -246 0 55

Group entities 0 3,864 0 3,864

Of which: Goodwill 0 973 0 973

Assets under insurance and reinsurance contracts 344 -344 0 0

Tangible assets 7,838 -913 0 6,924

Intangible assets 4,752 -1,766 0 2,986

Tax assets 11,700 -483 231 11,448

Other assets 2,452 -396 1,864 3,920

Non-current assets and disposal groups classified as held for sale 7,309 -106 0 7,203

Total assets 361,514 -52,255 9,582 318,840

Amounts in millions of euros

LiabilitiesPublic

scope

Group entities

accounted for by

the Equity

method(1)

Intragroup

transactions and

other consolidation

adjustments (2)

Reserved scope

Financial liabilities held for trading 10,293 0 6,428 16,721

Financial liabilities designated at fair value through profit or loss 3,764 -3,764 0 0

Financial liabilities at amortised cost 260,145 -923 2,483 261,704

Derivatives 653 -9 0 645

Fair value changes of the hedged items in portfolio hedge of interest rate risk 1,985 0 0 1,985

Liabilities under insurance and reinsurance contracts 45,804 -45,804 0 0

Provisions 4,950 -162 6 4,794

Tax liabilities 1,247 -575 218 889

Other liabilities 1,861 13 -149 1,727

Liabilities included in disposal groups classified as held for sale 86 -86 0 0

Total liabilities 330,787 -51,310 8,986 288,464

EquityPublic

scope

Group entities

accounted for by

the Equity

method(1)

Intragroup

transactions and

other consolidation

adjustments (2)

Reserved scope

Shareholders' equity 17,001 0 0 17,001

Accumulated other comprehensive income 292 0 0 292

Minority interests 13,434 -944 596 13,083

Total equity 30,727 -944 596 30,376

Total equity and total liabilities 361,514 -52,255 9,582 318,840

(1) Non-consolidated group entities by activity, mainly VidaCaixa and Saba Group. Their contribution to the public balance sheet is eliminated and their costs are

included as stakes

(2) Mainly transactions with VidaCaixa, Saba Group and other companies of their own non-consolidated economic group, that are no eliminated on consolidation in

the reserved management scope.

(€ million)

(€ million)

11

1.1.2. Description of the consolidated group

The following provides a summary of the main differences in relation to the consolidation scope and methods applied to prepare information on the Criteria Group in this report and to prepare its consolidated financial statements:

1. For the preparation of the Criteria Group's consolidated financial statements, all the subsidiary undertakings (companies controlled by the parent undertaking) were fully consolidated. Jointly controlled entities (undertakings managed jointly) were accounted for using the equity method, with the exception of financial holding undertakings, which were consolidated using proportionate consolidation.

2. For the purposes of solvency, subsidiary undertakings with a different activity to that of a credit institution or of investment undertakings as defined in Directive 2013/36/EU and Regulation (EU) 575/2013, both of 26 June 2013, are accounted for using the equity method. Jointly controlled entities that are financial institutions were proportionately consolidated, regardless of the method applied in the financial statements.

Table 1 details the treatment applied to each of the undertakings comprising the consolidation scope of the Criteria Group that do not form part of the CaixaBank Group (listed in Appendix IV), for the purposes of determining capital adequacy and preparing their consolidated financial statements.

12

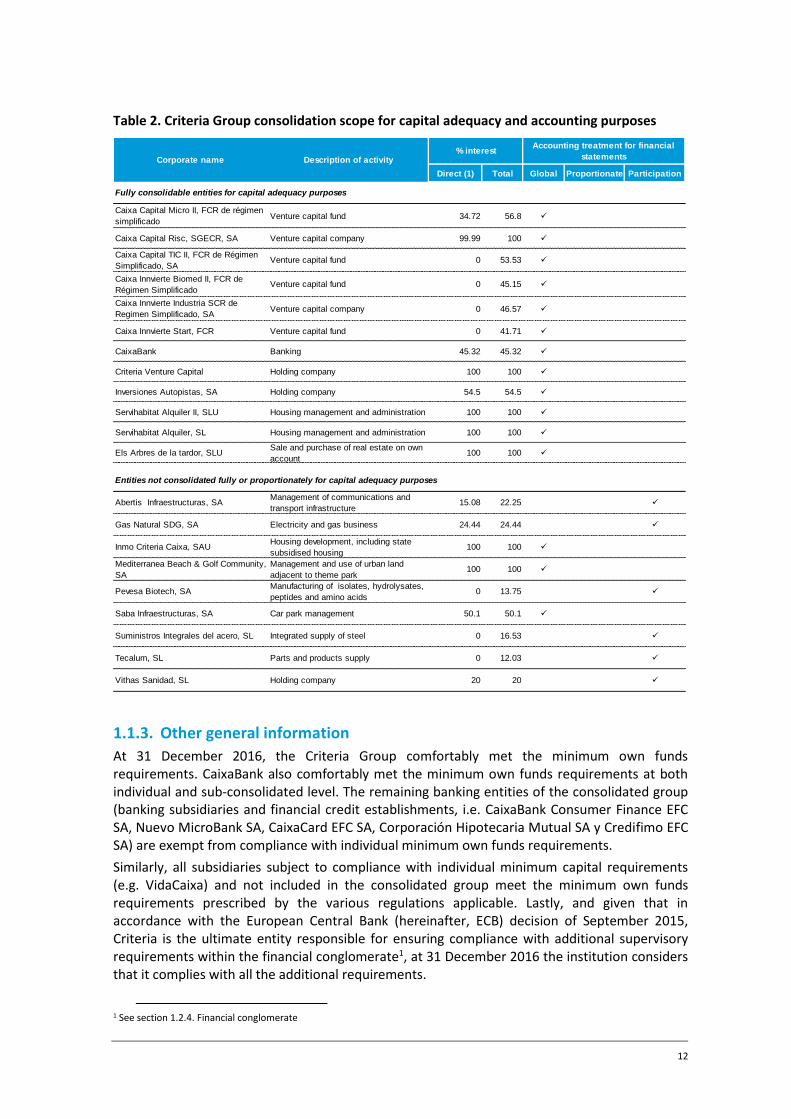

Table 2. Criteria Group consolidation scope for capital adequacy and accounting purposes

1.1.3. Other general information

At 31 December 2016, the Criteria Group comfortably met the minimum own funds requirements. CaixaBank also comfortably met the minimum own funds requirements at both individual and sub-consolidated level. The remaining banking entities of the consolidated group (banking subsidiaries and financial credit establishments, i.e. CaixaBank Consumer Finance EFC SA, Nuevo MicroBank SA, CaixaCard EFC SA, Corporación Hipotecaria Mutual SA y Credifimo EFC SA) are exempt from compliance with individual minimum own funds requirements.

Similarly, all subsidiaries subject to compliance with individual minimum capital requirements (e.g. VidaCaixa) and not included in the consolidated group meet the minimum own funds requirements prescribed by the various regulations applicable. Lastly, and given that in accordance with the European Central Bank (hereinafter, ECB) decision of September 2015, Criteria is the ultimate entity responsible for ensuring compliance with additional supervisory requirements within the financial conglomerate1, at 31 December 2016 the institution considers that it complies with all the additional requirements.

1 See section 1.2.4. Financial conglomerate

Direct (1) Total Global Proportionate Participation

Caixa Capital Micro II, FCR de régimen

simplificadoVenture capital fund 34.72 56.8

Caixa Capital Risc, SGECR, SA Venture capital company 99.99 100

Caixa Capital TIC II, FCR de Régimen

Simplificado, SAVenture capital fund 0 53.53

Caixa Innvierte Biomed II, FCR de

Régimen SimplificadoVenture capital fund 0 45.15

Caixa Innvierte Industria SCR de

Regimen Simplificado, SAVenture capital company 0 46.57

Caixa Innvierte Start, FCR Venture capital fund 0 41.71

CaixaBank Banking 45.32 45.32

Criteria Venture Capital Holding company 100 100

Inversiones Autopistas, SA Holding company 54.5 54.5

Servihabitat Alquiler II, SLU Housing management and administration 100 100

Servihabitat Alquiler, SL Housing management and administration 100 100

Els Arbres de la tardor, SLUSale and purchase of real estate on own

account100 100

Abertis Infraestructuras, SAManagement of communications and

transport infrastructure15.08 22.25

Gas Natural SDG, SA Electricity and gas business 24.44 24.44

Inmo Criteria Caixa, SAUHousing development, including state

subsidised housing100 100

Mediterranea Beach & Golf Community,

SA

Management and use of urban land

adjacent to theme park100 100

Pevesa Biotech, SAManufacturing of isolates, hydrolysates,

peptides and amino acids0 13.75

Saba Infraestructuras, SA Car park management 50.1 50.1

Suministros Integrales del acero, SL Integrated supply of steel 0 16.53

Tecalum, SL Parts and products supply 0 12.03

Vithas Sanidad, SL Holding company 20 20

Accounting treatment for financial

statements% interest

Description of activityCorporate name

Entities not consolidated fully or proportionately for capital adequacy purposes

Fully consolidable entities for capital adequacy purposes

13

1.1.4. Nature of the investment in CaixaBank

In May 2016, the Board of Trustees of FBLC and Criteria’s Board of Directors agreed to place on record their intent to comply, before the end of 2017, with the requirements announced by the ECB in order for Criteria to effectively relinquish control of CaixaBank for prudential deconsolidation purposes, in view also of the fact that the European banking resolution authorities will likely decide that the scope of resolution lies at the Criteria Group level, which would effectively tie all of Criteria’s sole shareholder’s net worth to one single investment.

The conditions and requirements established by the ECB are essentially threefold:

a) Criteria’s stake in CaixaBank

Limited to 40% for both voting and dividend rights.

b) Corporate governance

Various measures to be implemented to limit Criteria’s influence on CaixaBank’s governance bodies.

c) Intra-group financing

Restrictions to be placed on CaixaBank lending to the Criteria Group/FBLC and its investees, and a first limit must be complied with in order to achieve deconsolidation, which must be reduced in the year after deconsolidation.

If the conditions set by the ECB are met, then the ECB will determine whether Criteria has effectively relinquished control of CaixaBank for prudential purposes. If the ECB confirms that control over CaixaBank has been relinquished and in the absence of other controlling stakes in other banks, Criteria would cease to be a mixed financial holding company for the purposes of Regulation (EU) No 575/2013, and consequently Criteria would no longer be required to comply with the capital requirements set out in that regulation.

Under International Financial Reporting Standards (IFRS 10 Consolidated Financial Statements) the fulfilment of the above-mentioned conditions, which would lead to the loss of control of CaixaBank by Criteria, would also imply the accounting deconsolidation.

At 31 December 2016, Criteria continued to consider CaixaBank as a subsidiary because none of the conditions that would imply a change of Criteria's control over CaixaBank had been met.

At 31 December 2016, the Company’s Directors had not started to formalise an active plan to monitor and comply with the conditions established by the ECB. In light of this and the materiality and uncertainty surrounding the changes required for compliance and to obtain the necessary regulatory approvals, at this date it is not considered highly probable that compliance will be achieved in 2017. That said, this situation does not undermine the Company’s commitment to try to complete the deconsolidation in 2017. Consequently, at 31 December 2016 the conditions set down in IFRS 5 for classification as a non-current asset held for sale have not been fulfilled.

After the reporting date, at a meeting in early February 2017, Criteria’s Audit and Control Committee responded to the improved financial market conditions at the beginning of 2017 by instructing Criteria’s CEO to start exploring the best alternative for reducing the economic stake in CaixaBank. As a result, on 6 February 2017, 318,305,355 shares representing approximately 5.322% of CaixaBank’s share capital were sold, thus bringing Criteria’s economic stake in CaixaBank to 40% (see section on Subsequent events). The CEO was also authorised in February 2017 to initiate a period for analysing the implications of the other deconsolidation conditions established by the European Central Bank, to enable the Board of Directors and/or the Audit and Control Committee to evaluate whether, given those implications, Criteria would be in a position to draw up an active plan to achieve the deconsolidation, entailing a substantial

14

change in the nature of the investment in CaixaBank. Ultimately, authorisation is required from the ECB.

1.2. Governance and organisation

1.2.1. Criteria Internal governance

By virtue of the provisions of the Law, Criteria's governing bodies are the Annual General Meeting and the Board of Directors.

At 31 December 2016 there was no executive or delegate committee. Nor is there a strategy and investment committee, or any committees other than the Audit and Control Committee and the Appointments and Remuneration Committee.

However, since Criteria is controlled by FBLC, its Governing Bodies are also influenced by the Board of Trustees, the supreme body of FBLC and several of its trustees sit on Criteria’s Board of Directors. The function of the Board of Trustees is to meet FBLC's objectives and carefully administer its assets and rights, maintaining their profitability and utility. It is also responsible for control and supervision, and reports to the Bank of Spain (hereinafter, BoS).

1.2.1.1. Board of Directors

With the exception of issues reserved for Annual General Meetings, the Board of Directors is Criteria's supreme decision-making body. Its duties are described in the company bylaws. Through the CEO, in turn advised by the Management Committee, it is responsible for reviewing and approving the organisational structure and reporting lines.

The Board of Directors' risk management responsibilities include the following:

Setting suitable internal control policies and basic risk management policies.

Supervising performance of the investee portfolio.

Approving and regularly updating Criteria's Risk Appetite Framework (hereinafter, the “RAF”), which lays down the limits and alerts for measuring and managing risk (at least once a year), as well as supervising and monitoring the effective risk profile.

Approving the Recovery Plan and other regulatory documents, and updating these at least once a year. For the Recovery Plan specifically, the Board of Directors bears the ultimate responsibility for approving the activation phase, as well as its deactivation, in the pertinent circumstances, and for transmitting this decision to the Supervisor.

Complying with the consolidated obligations as a Financial Conglomerate.2

The Board of Directors may appoint an executive committee and one or more chief executives from among its number. It may also create other committees formed by directors to carry out any functions it may deem appropriate.

Members of the Board of Directors need not be shareholders. The Annual General Meeting is responsible for appointing the members of the Board of Directors.

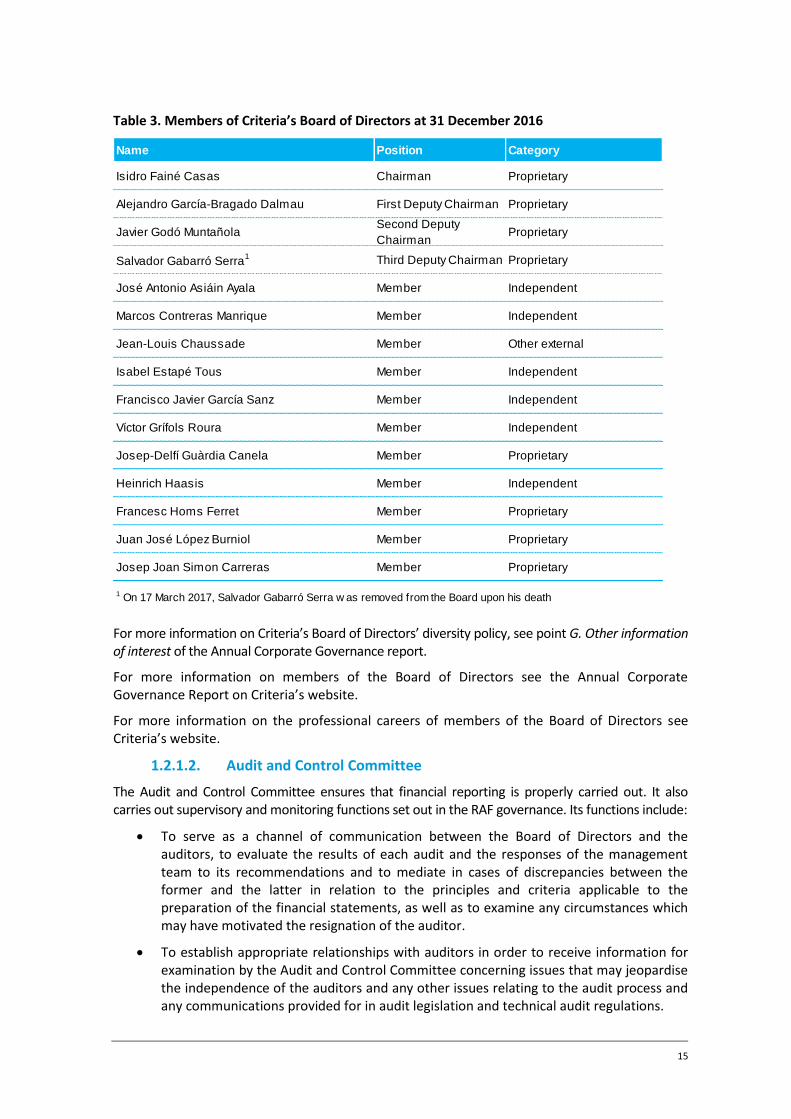

The breakdown of the Board of Directors is as follows:

2 See section 1.2.4. Financial conglomerate

15

Table 3. Members of Criteria’s Board of Directors at 31 December 2016

For more information on Criteria’s Board of Directors’ diversity policy, see point G. Other information of interest of the Annual Corporate Governance report.

For more information on members of the Board of Directors see the Annual Corporate Governance Report on Criteria’s website.

For more information on the professional careers of members of the Board of Directors see Criteria’s website.

1.2.1.2. Audit and Control Committee

The Audit and Control Committee ensures that financial reporting is properly carried out. It also carries out supervisory and monitoring functions set out in the RAF governance. Its functions include:

To serve as a channel of communication between the Board of Directors and the auditors, to evaluate the results of each audit and the responses of the management team to its recommendations and to mediate in cases of discrepancies between the former and the latter in relation to the principles and criteria applicable to the preparation of the financial statements, as well as to examine any circumstances which may have motivated the resignation of the auditor.

To establish appropriate relationships with auditors in order to receive information for examination by the Audit and Control Committee concerning issues that may jeopardise the independence of the auditors and any other issues relating to the audit process and any communications provided for in audit legislation and technical audit regulations.

Name Position Category

Isidro Fainé Casas Chairman Proprietary

Alejandro García-Bragado Dalmau First Deputy Chairman Proprietary

Javier Godó MuntañolaSecond Deputy

Chairman Proprietary

Salvador Gabarró Serra1 Third Deputy Chairman Proprietary

José Antonio Asiáin Ayala Member Independent

Marcos Contreras Manrique Member Independent

Jean-Louis Chaussade Member Other external

Isabel Estapé Tous Member Independent

Francisco Javier García Sanz Member Independent

Víctor Grífols Roura Member Independent

Josep-Delfí Guàrdia Canela Member Proprietary

Heinrich Haasis Member Independent

Francesc Homs Ferret Member Proprietary

Juan José López Burniol Member Proprietary

Josep Joan Simon Carreras Member Proprietary

1 On 17 March 2017, Salvador Gabarró Serra w as removed from the Board upon his death

16

To supervise compliance with the auditing contract, striving to ensure that the opinion on the financial statements and the main contents of the audit report are drafted clearly and precisely.

To review the company’s accounts and periodic financial reporting that the Board must furnish to the markets and their supervisory bodies and, in general, to monitor compliance with legal requisites on this subject matter and the correct application of generally accepted accounting principles, and to report on proposals for modification of accounting principles and criteria suggested by management.

To supervise the internal auditing services, verifying the adequacy and integrity thereof, and proposing the selection, appointment and substitution of the persons responsible for said services, to propose the budget for such services, and to verify that Senior Management bears in mind the conclusions and recommendations of their reports.

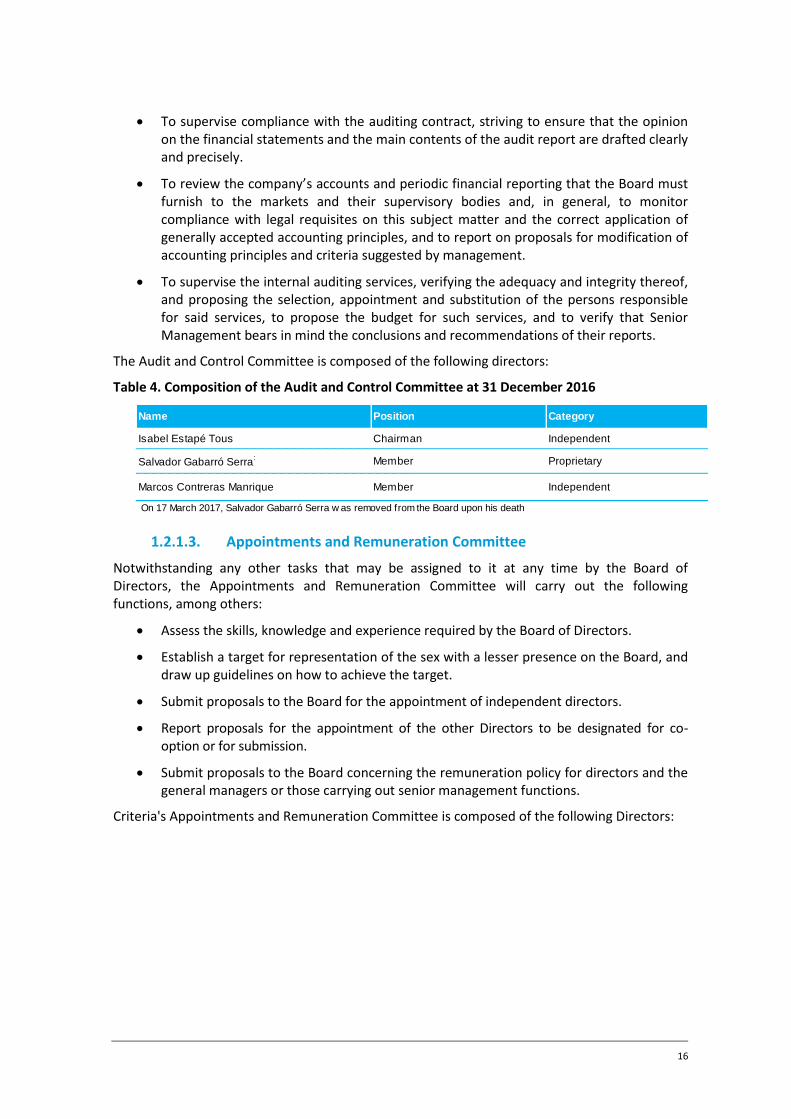

The Audit and Control Committee is composed of the following directors:

Table 4. Composition of the Audit and Control Committee at 31 December 2016

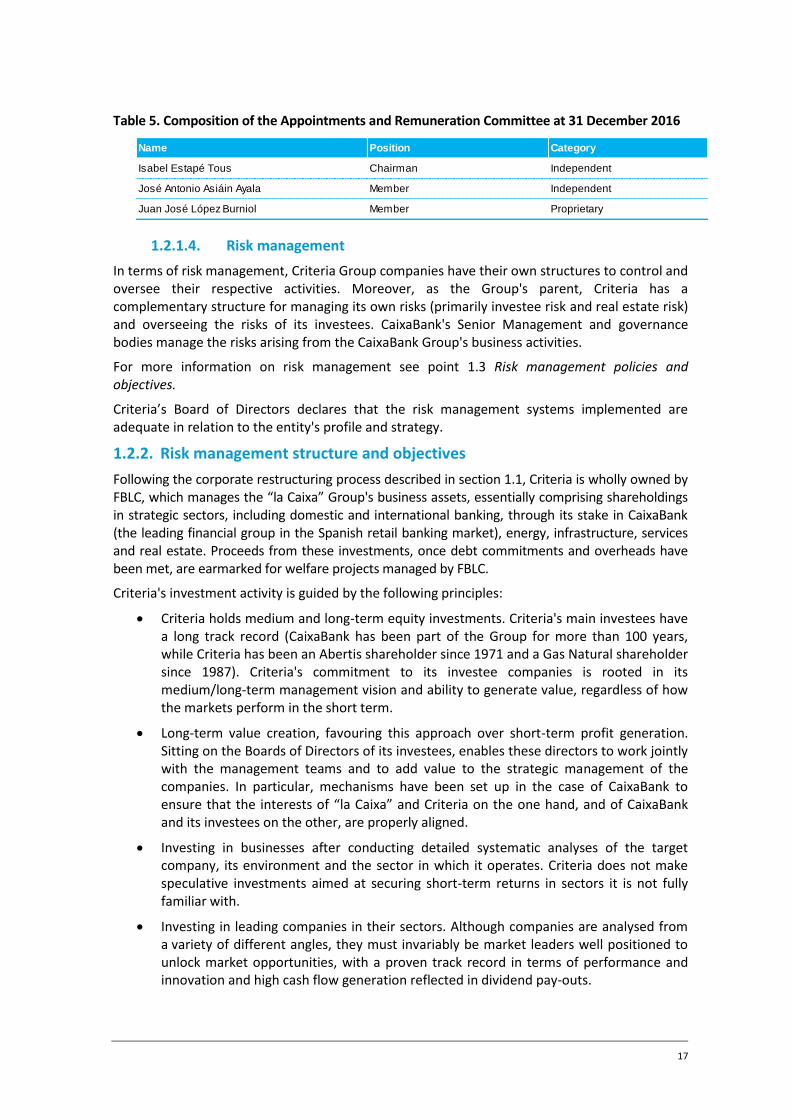

1.2.1.3. Appointments and Remuneration Committee

Notwithstanding any other tasks that may be assigned to it at any time by the Board of Directors, the Appointments and Remuneration Committee will carry out the following functions, among others:

Assess the skills, knowledge and experience required by the Board of Directors.

Establish a target for representation of the sex with a lesser presence on the Board, and draw up guidelines on how to achieve the target.

Submit proposals to the Board for the appointment of independent directors.

Report proposals for the appointment of the other Directors to be designated for co-option or for submission.

Submit proposals to the Board concerning the remuneration policy for directors and the general managers or those carrying out senior management functions.

Criteria's Appointments and Remuneration Committee is composed of the following Directors:

Name Position Category

Isabel Estapé Tous Chairman Independent

Salvador Gabarró Serra: Member Proprietary

Marcos Contreras Manrique Member Independent

On 17 March 2017, Salvador Gabarró Serra w as removed from the Board upon his death

17

Table 5. Composition of the Appointments and Remuneration Committee at 31 December 2016

1.2.1.4. Risk management

In terms of risk management, Criteria Group companies have their own structures to control and oversee their respective activities. Moreover, as the Group's parent, Criteria has a complementary structure for managing its own risks (primarily investee risk and real estate risk) and overseeing the risks of its investees. CaixaBank's Senior Management and governance bodies manage the risks arising from the CaixaBank Group's business activities.

For more information on risk management see point 1.3 Risk management policies and objectives.

Criteria’s Board of Directors declares that the risk management systems implemented are adequate in relation to the entity's profile and strategy.

1.2.2. Risk management structure and objectives

Following the corporate restructuring process described in section 1.1, Criteria is wholly owned by FBLC, which manages the “la Caixa” Group's business assets, essentially comprising shareholdings in strategic sectors, including domestic and international banking, through its stake in CaixaBank (the leading financial group in the Spanish retail banking market), energy, infrastructure, services and real estate. Proceeds from these investments, once debt commitments and overheads have been met, are earmarked for welfare projects managed by FBLC.

Criteria's investment activity is guided by the following principles:

Criteria holds medium and long-term equity investments. Criteria's main investees have a long track record (CaixaBank has been part of the Group for more than 100 years, while Criteria has been an Abertis shareholder since 1971 and a Gas Natural shareholder since 1987). Criteria's commitment to its investee companies is rooted in its medium/long-term management vision and ability to generate value, regardless of how the markets perform in the short term.

Long-term value creation, favouring this approach over short-term profit generation. Sitting on the Boards of Directors of its investees, enables these directors to work jointly with the management teams and to add value to the strategic management of the companies. In particular, mechanisms have been set up in the case of CaixaBank to ensure that the interests of “la Caixa” and Criteria on the one hand, and of CaixaBank and its investees on the other, are properly aligned.

Investing in businesses after conducting detailed systematic analyses of the target company, its environment and the sector in which it operates. Criteria does not make speculative investments aimed at securing short-term returns in sectors it is not fully familiar with.

Investing in leading companies in their sectors. Although companies are analysed from a variety of different angles, they must invariably be market leaders well positioned to unlock market opportunities, with a proven track record in terms of performance and innovation and high cash flow generation reflected in dividend pay-outs.

Name Position Category

Isabel Estapé Tous Chairman Independent

José Antonio Asiáin Ayala Member Independent

Juan José López Burniol Member Proprietary

18

Criteria maintains a financial structure that allows it to obtain financing whenever investment opportunities arise and to guarantee continuity of the company.

To comply with these policies, Criteria's Board of Directors carries out supervisory functions to oversee the performance of its investees and periodically monitors the internal control and risk management systems in place for these investees.

In addition, Criteria's management monitors these holdings on an ongoing case-by-case basis to be able, at any time, to take the most appropriate decisions on the basis of predicted and observed market performance and of Criteria’s business plan.

To provide the necessary information, Criteria has set up specialised teams that continually monitor the operations of its investees, with the extent of this oversight depending on the degree of influence Criteria has over these companies. The teams use a combination of indicators that are updated periodically. By way of example, every six months the team tests all its investments for impairment and recognises any corrections to their carrying amounts required.

As explained earlier, the objective of this is the disclosure of additional information regarding Criteria's contribution, as the parent of CaixaBank, to the Criteria Group's scope of prudential consolidation, other than the contribution by the CaixaBank Group. CaixaBank's Senior Management and Governance Bodies manage the risks arising from the CaixaBank Group's business activities.

This two-fold nature is reflected in the reference scope for Criteria's risk analysis, using Criteria's consolidated figures without fully consolidating CaixaBank, which coincides with the risk management perimeter. This is known as the “management scope” and is the most suitable and representative view for managing the Company's risks.

Meanwhile, the consolidated scope of the Criteria Group, including CaixaBank, is used to calculate the regulatory limits that must be met by the company as an entity under prudential supervision and as a financial conglomerate3.

The composition of Criteria's assets on an individual basis is presented below, expressed in terms of market value or Gross Asset Value (GAV), demonstrating the extent to which each investee/asset contributes to the Company.

3 See section 1.2.4. Financial conglomerate

19

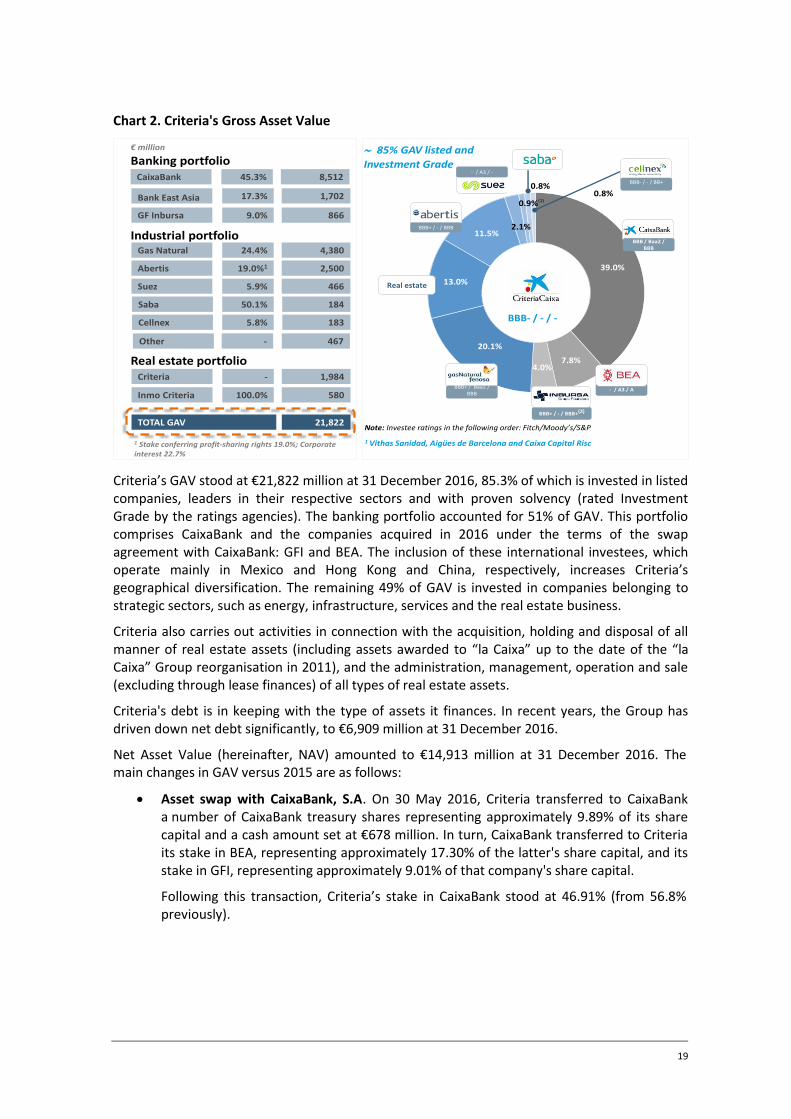

Chart 2. Criteria's Gross Asset Value

Criteria’s GAV stood at €21,822 million at 31 December 2016, 85.3% of which is invested in listed companies, leaders in their respective sectors and with proven solvency (rated Investment Grade by the ratings agencies). The banking portfolio accounted for 51% of GAV. This portfolio comprises CaixaBank and the companies acquired in 2016 under the terms of the swap agreement with CaixaBank: GFI and BEA. The inclusion of these international investees, which operate mainly in Mexico and Hong Kong and China, respectively, increases Criteria’s geographical diversification. The remaining 49% of GAV is invested in companies belonging to strategic sectors, such as energy, infrastructure, services and the real estate business.

Criteria also carries out activities in connection with the acquisition, holding and disposal of all manner of real estate assets (including assets awarded to “la Caixa” up to the date of the “la Caixa” Group reorganisation in 2011), and the administration, management, operation and sale (excluding through lease finances) of all types of real estate assets.

Criteria's debt is in keeping with the type of assets it finances. In recent years, the Group has driven down net debt significantly, to €6,909 million at 31 December 2016.

Net Asset Value (hereinafter, NAV) amounted to €14,913 million at 31 December 2016. The main changes in GAV versus 2015 are as follows:

Asset swap with CaixaBank, S.A. On 30 May 2016, Criteria transferred to CaixaBank a number of CaixaBank treasury shares representing approximately 9.89% of its share capital and a cash amount set at €678 million. In turn, CaixaBank transferred to Criteria its stake in BEA, representing approximately 17.30% of the latter's share capital, and its stake in GFI, representing approximately 9.01% of that company's share capital.

Following this transaction, Criteria’s stake in CaixaBank stood at 46.91% (from 56.8% previously).

CaixaBank 45.3% 8,512

Gas Natural 24.4% 4,380

Industrial portfolio

Abertis 19.0%1 2,500

Suez 5.9% 466

Cellnex 183

Real estate portfolioCriteria - 1,984

Inmo Criteria 100.0% 580

TOTAL GAV 21,822

€ million

1 Stake conferring profit-sharing rights 19.0%; Corporate interest 22.7%

Banking portfolio

Saba 50.1% 184

1 Vithas Sanidad, Aigües de Barcelona and Caixa Capital Risc

85% GAV listed and

Investment Grade

Note: Investee ratings in the following order: Fitch/Moody’s/S&P

Other - 467

5.8%

Bank East Asia 17.3% 1,702

GF Inbursa 9.0% 866

39.0%

7.8%4.0%

20.1%

13.0%

11.5%2.1%

0.9%

0.8%0.8%

BBB- / - / -

Real estate

BBB+ / - / BBB

- / A3 / -

BBB- / - / BB+

BBB / Baa2 /BBB

BBB+ / Baa2 / BBB

- / A3 / A

BBB+ / - / BBB+(2)

(1)

20

Sale of Gas Natural SDG, S.A. On 21 September 2016, Criteria and Repsol sold to GIP III Canary 1, S.À R.L shares representing 20% (10% corresponding to Criteria and 10% to Repsol) of the share capital of Gas Natural SDG, S.A for an amount of €1,901 million, equivalent to a price of €19 per share.

Following this transaction, Criteria’s stake in Gas Natural stands at 24.44% (from 34.44% previously).

Sale of CaixaBank S.A. shares. On 13 December 2016, Criteria carried out an accelerated bookbuild among institutional and/or qualified investors for a package of 100,000,000 CaixaBank shares representing 1.7% of the Bank's share capital. The share placement amounted to €315 million, at a sale price of €3.15 per share.

Following this transaction, Criteria’s stake in CaixaBank stands at 45.32% (from 46.91% previously).

1.2.2.1 Structural organisation of the risk function

In terms of risk management, Criteria Group companies have their own structures to control and oversee their respective activities. Moreover, as the Group's parent, Criteria has a complementary structure for managing its own risks (primarily investee risk and real estate risk) and overseeing the risks of its investees. CaixaBank's Senior Management and Governance Bodies manage the risks arising from the CaixaBank Group's business activities.

In accordance with prevailing legislation, Criteria's governance bodies are the Annual General Meeting and the Board of Directors.

However, since Criteria is controlled by FBLC, its governance bodies are also influenced by the Board of Trustees, the supreme body of FBLC. The function of the Board of Trustees is to meet FBLC's objectives and carefully administer its assets and rights, maintaining their profitability and utility. It is also responsible for control and supervision, and reports to the BoS.

For more information on the Board of Directors' risk management responsibilities see point 1.2.1.1. The Board of Directors.

Criteria's Audit and Control Committee is entrusted with supervising the preparation and presentation of the regulated financial information4 and the efficacy of the Company's internal control and risk management systems. It also carries out the supervisory and monitoring functions set out in the RAF Governance5.

Criteria’s Management Committee is composed of the Company’s senior executives and the CEO. It meets as a minimum every two weeks. Its duties are to advise the Chief Executive Management and guarantee coordination between its members.

The responsibilities of the Management Committee in relation to risk management include (i) reviewing and approving the methodology, processes and results of regulatory reports and their subsequent submission to the Board for approval; (ii) reviewing the RAF and coordinating control over compliance with limits and approved risk targets at least once a month; and (iii) within the framework of Regulatory Compliance, fostering a culture of compliance across the company, in addition to monitoring compliance risk and established mitigation measures.

The appointment of senior managers is the exclusive responsibility of the Board of Directors, which receives advice and a report from the Appointments Committee.

The composition of the Management Committee is as follows:

4 See information on ICFR in section 1.2.5. Internal control framework 5 and 7 See section 1.2.3. Risk Appetite Framework

21

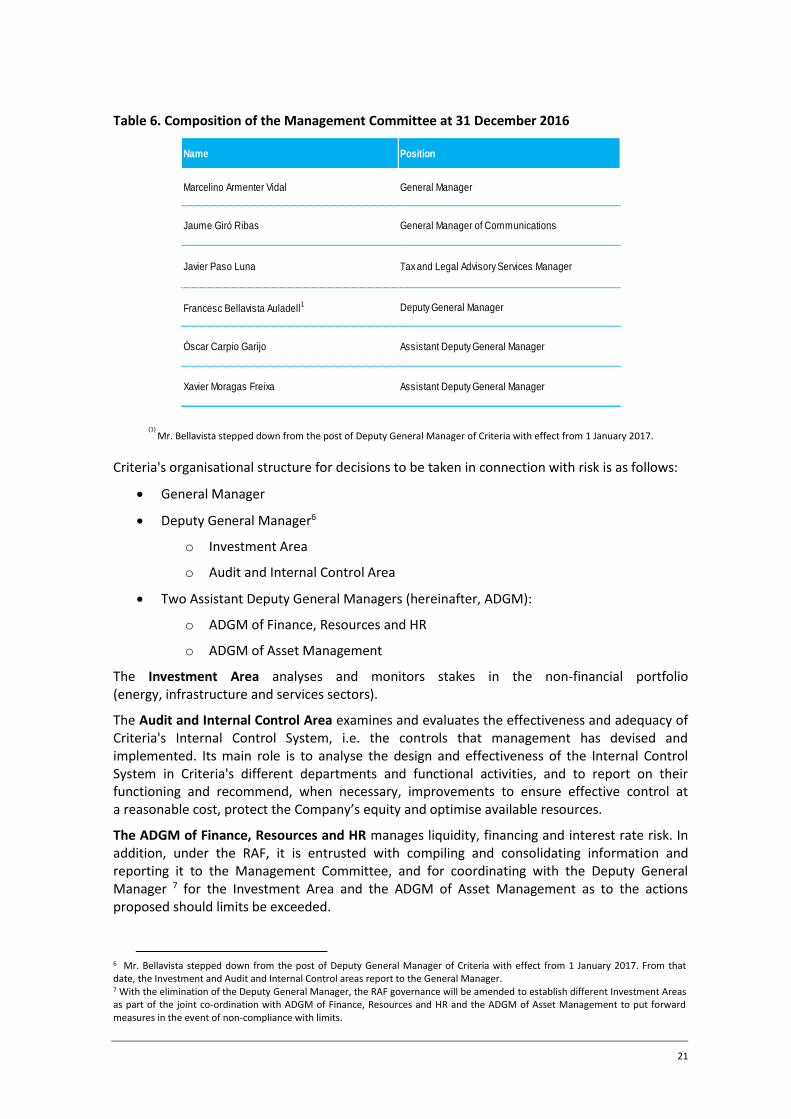

Table 6. Composition of the Management Committee at 31 December 2016

(1) Mr. Bellavista stepped down from the post of Deputy General Manager of Criteria with effect from 1 January 2017.

Criteria's organisational structure for decisions to be taken in connection with risk is as follows:

General Manager

Deputy General Manager6

o Investment Area

o Audit and Internal Control Area

Two Assistant Deputy General Managers (hereinafter, ADGM):

o ADGM of Finance, Resources and HR

o ADGM of Asset Management

The Investment Area analyses and monitors stakes in the non-financial portfolio (energy, infrastructure and services sectors).

The Audit and Internal Control Area examines and evaluates the effectiveness and adequacy of Criteria's Internal Control System, i.e. the controls that management has devised and implemented. Its main role is to analyse the design and effectiveness of the Internal Control System in Criteria's different departments and functional activities, and to report on their functioning and recommend, when necessary, improvements to ensure effective control at a reasonable cost, protect the Company’s equity and optimise available resources.

The ADGM of Finance, Resources and HR manages liquidity, financing and interest rate risk. In addition, under the RAF, it is entrusted with compiling and consolidating information and reporting it to the Management Committee, and for coordinating with the Deputy General Manager 7 for the Investment Area and the ADGM of Asset Management as to the actions proposed should limits be exceeded.

6 Mr. Bellavista stepped down from the post of Deputy General Manager of Criteria with effect from 1 January 2017. From that date, the Investment and Audit and Internal Control areas report to the General Manager. 7 With the elimination of the Deputy General Manager, the RAF governance will be amended to establish different Investment Areas as part of the joint co-ordination with ADGM of Finance, Resources and HR and the ADGM of Asset Management to put forward measures in the event of non-compliance with limits.

Name Position

Marcelino Armenter Vidal General Manager

Jaume Giró Ribas General Manager of Communications

Javier Paso Luna Tax and Legal Advisory Services Manager

Francesc Bellavista Auladell1 Deputy General Manager

Óscar Carpio Garijo Assistant Deputy General Manager

Xavier Moragas Freixa Assistant Deputy General Manager

(1) Mr. Bellavista stepped dow n from the post of Deputy General Manager of Criteria w ith effect from 1 January 2017.

22

The ADGM of Asset Management8: monitors investments in the financial portfolio (formed by CaixaBank, BEA and GFI) and actively manages the real estate portfolio and supervises the services received by Servihabitat Servicios Inmobiliarios.

In the context of Criteria’s action plan for compliance with obligations relating to the Financial Conglomerate9, a new risk control function was created under this ADGM. Its basic mandate is to ensure compliance with the obligations and requirements established at any time by the prudential regulations applicable to Criteria.

In order to fulfil this mandate, the function will coordinate with CaixaBank's Executive Global Risk Management Division, its Planning and Capital Division and potentially with other CaixaBank teams that are involved in the function's objective, namely to ensure compliance with the prudential regulations applicable to Criteria.

1.2.2.2. Corporate Risk Map

The Internal Control Area has developed Criteria's Corporate Risk Map to identify, measure, monitor, control and report the different risks affecting the Company. This map offers a comprehensive vision of the risks associated with corporate activities and the control environment.

The Activities Map and the Corporate Risks Catalogue were approved by the Board of Directors in July 2015. The Catalogue was updated in July 2016.

Activities Map: map of the main activities associated with key areas in Criteria.

Corporate Risks Catalogue: facilitates monitoring and internal and external reporting of the Company's risks, based on whether they are specific risks of the financial activity or risks for continuity of the activity. Criteria's Catalogue is in line with the Single Supervisory Mechanism (SSM) Risk Catalogue.

Although Criteria's Catalogue reflects the risks arising from the Company's assets (“financial risks”), it also includes other risks that, due to their nature, could affect continuity of the business itself.

The main risks included in this Catalogue and periodically reported to Management and the Governance Bodies are:

Financial risks

o Credit

o Impairment of assets, both of equity holdings and of non-financial assets (primarily real estate)

o Interest rate risk in the banking book and currency risk

o Liquidity

o Market

o Business profitability

o Regulatory own funds

Non-financial risks

o Compliance

8 After 31 December 2016, the analysis, monitoring and management of stakes in the financial portfolio (banking stakes) and the risk control function (Financial Conglomerate) were separated from the ADGM of Asset Management. 9 See section 1.2.4. Financial conglomerate

23

o Reliability of financial reporting

o Legal/Regulatory

o Operational

o Reputational

Further information on the main risks in this list is provided in section 1.3.1. “Risk associated with equity investments” and the following sections.

1.2.2.3. Risk Appetite Framework (RAF)

The RAF enables all prudential obligations to be monitored and controlled. This framework sets out the policies, governance processes and indicators used to establish, disclose and monitor Criteria's risk appetite. The representative scope for the RAF is the Criteria consolidated management scope without fully consolidating CaixaBank, which coincides with the risk management scope. However, as Criteria is the head of the Financial Conglomerate and subject to prudential supervision requirements, the RAF includes regulatory indicators.

The RAF is a key risk management tool that enables the Board to determine the risk types and thresholds that Criteria, as an unlisted investment holding company that manages the assets of FBLC, can tolerate in order to achieve its business targets, while always seeking to keep a balance between risk and return.

Criteria’s RAF is a comprehensive and forward-looking tool based the best corporate governance practices and standards applicable10 to financial institutions, factoring in the Company's status as a holding company.

Governance of the RAF includes an annual updating process, except where sufficiently significant changes in the situation occur that may require the risk appetite to be changed at particular moments in time.

In 2016, the Board of Directors updated the RAF in terms of regulatory capital requirements by adapting to the new minimum capital requirements stipulated by the ECB, within the Supervisory Review and Evaluation Process (hereinafter, “SREP”11). The Management Committee performs a monthly follow up of the RAF, reviewing the RAF metrics scorecard.

10 Principles for an Effective Risk Appetite Framework, FSB (2013) and Report on Risk Appetite Frameworks and IT Infrastructure, SSG (2010) 11 Further information is provided in section 2.1. Regulatory Framework and in section 2.3.1. Pillar II: Internal Capital Adequacy Assessment

24

1. Risk appetite statement

Through the RAF, the Board has determined Criteria's risk appetite statement, focused on achieving a medium-low risk profile through prudent management and a business model of a holding company under the aforementioned principles.

Criteria's objective is to comply with all legal and compliance requirements, financial information reliability and regulatory requirements, and to minimise the incidence of operational and reputational risk, in order to avoid activities that may involve a negative reputational impact on the Group.

2. RAF Risk Map

As mentioned in section 1.2.2 Risk management objectives and structure, it is important to note that Criteria's risk analysis has a different reference scope depending on the particular focus given, either (1) the Company's management scope (Criteria consolidated scope, without fully consolidating CaixaBank), known as the “management scope”, which is the most appropriate and representative view for managing the Company's risks; or (ii) the calculation and analysis of mandatory regulatory ratios as an entity under prudential supervision and as a financial conglomerate, using the Criteria Group's consolidated scope including CaixaBank.

For the purposes of the RAF, Criteria’s risk map is drawn on the risk factors contained in its management scope and those relating to its prudential obligations and obligations as a financial conglomerate. Risks are also grouped according to the following dimensions:

Management indicators (management scope): Liquidity; Profitability; Impairment of investees; Market and interest and currency rates.

Regulatory indicators (consolidated perimeter): Own funds, credit and liquidity.

Risks are based on the Risks Catalogue, although certain risks, such as asset impairment, are excluded based on the specific classification of assets.

3. RAF structure

The RAF is based on a series of metrics with thresholds. The metrics, which synthesise the objectives defined in the risk appetite statement set by the Board of Directors, are standardised throughout the entity. Thresholds are defined and calibrated for each metric, specifying the risk tolerance levels acceptable by Criteria.

“Target”, “Alert” and “Limit” thresholds are established for each of the metrics through a system of warning traffic lights:

Target (“green traffic light”): represents the desired level of risk at which Criteria wishes to conduct its activities and business.

Early warning or EW (“amber traffic light”): The EW alert is the tolerance interval between the target and the limit, where there is room to take decisions when the metric is deteriorating.

If the EW threshold is crossed, the Management Committee is informed to assess whether an action plan should be implemented to remedy the situation. The Audit and Control Committee is also informed accordingly.

Limit (“red traffic light”): If this threshold is crossed, the risk has exceeded the limits of compliance.

In this scenario, the Management Committee reports the breach of limit, and proposed response, to the Board of Directors and the Audit and Control Committee. Once the response has been approved by the Board, the Management Committee will give the necessary instructions to carry out the measures approved.

25

The metrics defined in Criteria’s Recovery Plan have also been included, defining a Recovery Indicator (“black traffic light”) which, when activated, triggers a series of communications and governance processes predefined in the communication plan, in accordance with the severity of the situation.

The periodic metric calibration process has become a key process, as it leads to the (re)establishment of the thresholds described. The calibration is revised at least once a year as part of the RAF update process and whenever the Board considers it necessary. All changes must be approved by Criteria’s Board of Directors. Therefore, on 19 December 2016, the Board of Directors approved the recalibration to adapt the metrics and threshold values to the SREP's12 decision of November 2016.

The foregoing serves to ensure a comprehensive and gradual process for monitoring and scaling potential impairment in Criteria's risk profile, by proactively and progressively managing the possible impairment of the Company's financial position, while affording greater flexibility and prevention and reaction capacity in the event of a crisis scenario.

At year-end 2016, none of the RAF metrics had fallen in beyond the limit zone (red traffic light).

4. Reporting and governance of the RAF

The RAF scorecard, showing metrics trends, is submitted each month to Criteria's Management Committee and at least every six months to the Audit and Control Committee meetings and Board of Directors meetings, unless an ad hoc report is submitted earlier as a result of a request from the governance bodies or as required by the framework governance (non-compliance in metrics).

The reporting and governance framework linked to RAF thresholds allows the entity to proactively identify possible defaults and guarantees specific actions allowing it to attain the target levels of returns.

In this regard, Criteria’s Board of Directors approved the Group Recovery Plan (which includes the CaixaBank Recovery Plan as an Appendix) in September 2016. Issues addressed in this plan include a wide range of different types of measures (sale of assets, margin loans, etc.) that could raise capital and contingent liquidity and restore Criteria’s financial position in different crisis scenarios proposed and analysed.

The measures defined in Criteria’s Recovery Plan offer specific additional guarantees to ensure that the levels defined in the RAF are restored.

In line with the above, Criteria’s Board of Directors is responsible for updating and approving the RAF (at least annually) and for supervising and monitoring the effective risk profile. It is also responsible for ensuring that the risk culture is suitably transmitted.

Criteria’s Audit and Control Committee is tasked with supervising the process to prepare, approve, review and update the RAF and revise the RAF proposal submitted by the Management Committee, transmitting its opinion to the Board of Directors. Similarly:

In a normal situation, the Audit and Control Committee verifies that the RAF is being correctly monitored.

If there is a breach of the thresholds set down in the RAF, it evaluates and reviews the mode of action proposed by the Management Committee and submits opinion and recommendation reports to the Board of Directors.

12 Further information is provided in section 2.1. Regulatory Framework et al

26

Criteria’s Management Committee is responsible for reviewing the information on the RAF submitted by the ADGM of Finance, Resources and HR and coordinating control over compliance with the thresholds and targets approved in the RAF on a quarterly basis as a minimum. In particular:

In a normal situation, the Management Committee coordinates the monitoring of the RAF and refers the information reported by the ADGM of Finance, Resources and HR to the Audit and Control Committee and the Board of Directors on a half-yearly basis or whenever any of the indicators exceeds the established limit.

If the protocol for a breach of the alert levels is activated (“amber traffic light”), the Management Committee is responsible for approving the action to be taken by the ADGM of Finance, Resources and HR in coordination with the Deputy General Manager 13 for the Investment Area, and the ADGM of Asset Management, and report to the Audit and Control committee, in addition to instructing the execution of the measures approved and controlling their implementation.

If the protocol for a breach of limits is activated (“red traffic light”), the Management Committee is responsible for proposing the measures required to remedy the situation to the Audit and Control Committee and the Board of Directors. Once the response has been approved by the Board, the Management Committee will give the necessary instructions to carry out the measures approved and monitor their implementation.

The ADGM of Finance, Resources and HR prepares the draft during the process to prepare, approve, review or update the RAF and refers it to the Management Committee. This area is also responsible for compiling and consolidating the information necessary to monitor RAF indicators:

In a normal situation, the ADGM of Finance, Resources and HR reports to the Management Committee on a monthly basis.

If the protocol is activated due to a breach of either early warning levels (“amber traffic light”) or limits (“red traffic light”), the ADGM of Finance, Resources and HR scales this breach and, in coordination with the Deputy General Manager 14 for Investment and the ADGM of Asset Management, submits a proposal to the Management Committee on the mode of action to be taken. In either case, once the response is approved (by the Management Committee or by the Board of Directors, as appropriate):

o The ADGM of Finance, Resources and HR measures and reports the results of the implementation of these measures.

o The ADGM of Asset Management and the Deputy General Manager15 for the Investment Area participate in the implementation of the measures.

The governance system described ensures the involvement of both Criteria’s Senior Management and its Board of Directors and the latter is ultimately responsible for defining, updating and supervising the risk profile and monitoring the effective risk profile. Additionally, monitoring the RAF and regularly reporting to Senior Management ensures that the RAF is integrated into the Company’s risk management.

13 Following the elimination of the Deputy General Manager, the RAF governance will be amended to establish different Investment Areas as part of the joint co-ordination with ADGM of Finance, Resources and HR and the ADGM of Asset Management to put forward measures in the event of activation of the protocol for a breach of alert levels. 14 Following the elimination of the Deputy General Manager, the RAF governance will be amended to establish different Investment Areas as part of the joint co-ordination with ADGM of Finance, Resources and HR and the ADGM of Asset Management to put forward measures in the event of activation of the protocol for a breach of alert levels. 15 Following the elimination of the Deputy General Manager, RAF governance will be amended to include the different Investment Areas as parties involved in the implementation of measures.

27

The RAF is factored into the preparation of the ICAAP and ILAAP, which project the main RAF management metrics in the different scenarios. In particular, for the baseline scenario an exercise is carried out to confirm that the RAF indicators obtained are consistent with the stated appetite.

1.2.3. Risk assessment and planning

As a complement and reinforcement that feeds back into both the Corporate Risk Map and the Risk Appetite Framework, Criteria has put in place institutional processes and mechanisms to evaluate both the evolution of the risk profile (recent, future and hypothetical in stress scenarios), and to evaluate its own ability to ensure appropriate governance, management and control.

Risk Assessment

Annual procedure in which the Entity seeks to:

Identify, assess, classify and internally report significant changes in inherent risks assumed by the Entity in its environment and business model, due to changes in the level of risk (evolving) or to the appearance of other risks that could potentially become significant (emerging), and

Make a self-assessment of its risk management, control and governance capacity, as a tool to help detect best practices and weaknesses in relation to risks. All with the aim of maximising internal transparency and the risk culture, and to prioritise efforts and investments with a larger potential impact on the Group’s residual risk profile.

The scope and depth of this process, which originated in the context of the Internal Capital Adequacy Assessment (ICAAP) report, has been evolving in line with the self-defined goal of continuous improvement, and through the inclusion of the guidelines and recommendations published by European regulatory and supervisory bodies in recent years. These include the EBA consultation document on Draft Guidelines on internal governance and the EBA's Final Guidelines for consistent ICAAP assessments by supervision teams.

It is currently performed on a stand-alone basis, using quantitative information (based on compliance with RAF thresholds) and qualitative input provided by the internal representatives of internal areas involved in risk management and input from control areas. This information is supplemented with an external view from the Investor Relations area based on its knowledge of external stakeholders (e.g. rating agencies), providing an objective view of the self-assessments carried out by the areas taking part in risk management and control. This exercise is presented to the entity's governance bodies for review and approval, with the Board of Directors having the ultimate responsibility for approval, within the framework of the ICAAP report.

At 31 December 2016, Criteria had a medium-low risk profile, in line with the business model and risk tolerance defined by its Board of Directors. Its levels of solvency and leverage are also consistent with this profile and strategy.

The risk profile is consistent with the risk appetite statement issued by the Board. See Risk appetite statement

1.2.4. Financial conglomerate

In addition to the foregoing, in September 2015 the ECB stated that following the corporate modification carried out in 2014 (see section 1.1), FBLC (until that time the head of the “la Caixa” financial conglomerate) could no longer be considered a mixed financial holding company and, therefore, able to be the parent of the financial conglomerate. The ECB stated that, instead, Criteria is a mixed financial holding company and the parent of the “Criteria Group” financial conglomerate, including within the CaixaBank Group. This implies that, firstly, Criteria is subject to the CaixaBank Group's scope for prudential supervision, as determined in the applicable regulations16 (with CaixaBank as the Entity ultimately responsible for compliance with

16 Further information is provided in section 2.1. Regulatory framework

28

this prudential supervision) and, secondly, Criteria is the entity responsible for ensuring compliance with certain additional supervisory requirements at financial conglomerate level.

These additional requirements are derived from Law 5/2005 of 22 April, on supervision of financial conglomerates and modifying other financial sector laws, Royal Decree 1332/2005 of 11 November, implementing the aforementioned law, and its subsequent amendments. All of the above transposing Directive 2002/87/EC into Spanish law.

In particular, these requirements are as follows:

Provision of additional capital, calculated pursuant to articles 6 and 7 of the aforementioned Royal Decree. At 31 December 2016, the financial conglomerate's ratio was 146.2%.

Control of significant intragroup transactions within the financial conglomerate. Those transactions amounting to over 5% of the financial conglomerate's eligible own funds are considered significant.

Control of significant risk concentration in the financial conglomerate. Those risks amounting to over 10% of the financial conglomerate's eligible own funds are considered significant.

Ensuring internal control mechanism and risk management procedures in line with the conglomerate level.

To strengthen the internal control mechanism and risk management procedures, Criteria constantly collaborates with CaixaBank on an improvement framework. To do so, it has implemented a series of governance, risk control and internal control procedures to strengthen the standards of regulatory compliance for Financial Conglomerates.

At the date of this report, all these obligations are deemed to be met. 1.2.5. Internal Control Model

Developments in the financial system, macroeconomic trends and the transformation of the regulatory framework indicate the growing importance of assessing risk and the control environment of entities, imposing greater demands and responsibility on Senior Management and Governance Bodies.

Following the same criteria as CaixaBank and using the same corporate risk monitoring and internal control model, Criteria's model provides reasonable assurance that the Company will meet its objectives. This internal control model is based on the methodology and infrastructure designed for the CaixaBank Group, as detailed in Appendix IV.

Criteria's internal control environment operates in accordance with guidelines issued by the regulator and best practices in the financial sector, and is structured in accordance with the Three Lines of Defence model:

The first line of defence comprises the business units and support areas, which are responsible for identifying, measuring, controlling, mitigating and reporting the key risks affecting the Company as it carries out its business.

The second line of defence acts independently and is designed to identify, measure, monitor and report all material risks, as well as to establish and develop management and control systems for these risks, and design compliance policies. The second line of defence includes, inter alia, the Risk Control function (financial conglomerate), Regulatory Compliance and Internal Control.

The second line of defence was reinforced in 2016 through the inclusion of an additional resource in the Internal Control area.

29

The third line of defence, which comprises Internal Audit, is responsible for assessing the effectiveness and efficiency of risk management and the internal control systems, applying principles of independence and objectivity.

Audit and Internal Control

Criteria's Audit and Internal Control Area is in charge of ensuring the correct performance of and supervising the Entity's internal control system. It reports to Criteria's Chief Executive Management and the Audit and Control Committee, the body responsible for overseeing Criteria's Internal Control System.

Internal Control and Internal Audit operate independently from other Criteria Group areas and companies in accordance with guidelines issued by Regulatory and Supervisory Authorities.

The objective of Criteria's Internal Control area is to analyse and ensure, with reasonable assurance, that correctly designed and effectively applied Policies and Procedures are in place in the organisation, along with an appropriate internal control system at Criteria in order to inform the Audit and Control Committee of the status thereof.

Its main duties include:

Coordinating the Corporate Risk Map.

Advising Senior Management on the control protocols and action plans needed to resolve any control deficiencies.