Embed Size (px)

Citation preview

LETTER OF OFFER

THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTIONThis Letter of Offer is sent to you as a shareholder(s) / beneficial owner(s) of Pfizer Limited. If you require any clarifications about the action tobe taken, you may consult your stock broker or investment consultant or the Manager / Registrar to the Offer. In case you have recently sold yourshares in the Target Company, please hand over this Letter of Offer and the accompanying Form of Acceptance-cum-Acknowledgement, Formof Withdrawal and Transfer Deed (in case of physical form) to the member of Stock Exchange through whom the said sale was effected.

CASH OFFER AT Rs. 675/- (Rupees Six Hundred and Seventy Five only)

PER FULLY PAID-UP EQUITY SHARE

(“Offer Price”)

Pursuant to The Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers)

Regulations, 1997 and subsequent amendments thereof (the “SEBI (SAST) Regulations” or “Regulations”)

TO ACQUIRE

10,078,143 Fully Paid-Up Equity Shares of face value Rs. 10/- each (“Offer”)

representing 33.77% of the Paid-Up Equity Share Capital

OF

Pfizer LimitedRegistered Office: Pfizer Centre, Patel Estate,Off S.V.Road, Jogeshwari(West), Mumbai – 400 102

Tel: +91 22 6693 2000 Fax: +91 22 6693 2377

(the “Target Company” or “Pfizer India”)

BY

Pfizer Investments Netherlands B.V.Registered Office: Rivium Westlaan 142, 2909 LD Capelle aan den IJssel, the Netherlands

Tel:31-10-406-4349 Fax: 31-10-406-4481

(the “Acquirer”)

and

Pfizer Inc.Registered Office: Corporation Trust Center, 1209 Orange Street, Wilmington, County of New Castle, Delaware 19801

Tel: 302-658-7581 Fax: 302-655-5049

The ultimate holding company of the Acquirer, which is acting in concert

(the “Person Acting in Concert” or “PAC”)

Note:

1. The Offer is being made pursuant to and in accordance with the provisions of Regulation 11(1) of the Regulations and subsequent amendments thereto.

2. On May 5, 2009, the Acquirer had filed an application with the RBI seeking its approval for acquisition of shares in the Offer from residents of India, non-resident Indians and

erstwhile overseas corporate bodies, as may be required, under the Foreign Exchange Management Act, 1999 and the regulations thereunder. Besides the above, no other approvals

are required to acquire shares tendered pursuant to this Offer.

3. The procedure for acceptance of this Offer is set out in this Letter of Offer. A Form of Acceptance-cum-Acknowledgement and Transfer Deed (where applicable) along with Form

of Withdrawal are enclosed with this Letter of Offer.

4. Should the Acquirer / PAC decide to revise the Offer Price upward, such upward revision will be made in terms of Regulation 26 of the Regulations not later than June 25, 2009. If

there is any upward revision in the Offer Price, the same would be notified by way of a public announcement in the same newspapers in which the Public Announcement (“PA”)

appeared. Such revised offer price would be payable to all shareholders who have accepted this Offer and tendered their shares at any time during the term of the Offer to the extent to

which their acceptance and tenders have been found valid and accepted by the Acquirer / PAC.

5. Shareholders who have accepted the Offer by tendering the requisite documents in accordance with the procedures set forth in the PA and this Letter of Offer can withdraw the

same up to three (3) working days prior to the date of closure of the Offer viz. Saturday, July 4, 2009.

6. A copy of the Public Announcement and Letter of Offer (including Form of Acceptance-cum-Acknowledgement and the Form of Withdrawal) would be available on SEBI’s

website at www.sebi.gov.in from the Offer opening date viz. Monday, June 15, 2009. The Form of Acceptance-cum-Acknowledgement may be downloaded and used to accept

the Offer only in jurisdictions where legally permissible. Persons outside India accessing these pages are required to inform themselves of and observe any relevant

restrictions.

7. This document has not been filed, registered or approved in any jurisdiction outside India. Recipients of this document resident in jurisdictions outside India should inform

themselves of and observe any applicable legal requirements.

8. If there is a competitive bid, the public offers under all the subsisting bids shall close on the same date. As the Offer Price cannot be revised during the 7 (seven) working

days prior to the closing date of the offers / bids, it would, therefore, be in the interest of shareholders to wait until the commencement of that period to know the final

offer price of each bid and tender their acceptance accordingly.

9. This Offer is not conditional upon any minimum level of acceptance.

10. This Offer is not a competitive bid. There has been no competitive bid as of the date of the Letter of Offer.

11. All future correspondence, if any, should be addressed to the Registrar to the Offer shown below:

Manager to the Offer Registrar to the Offer

HSBC Securities and Capital Markets (India) Private Limited Karvy Computershare Private Limited

52/60 M.G.Road, Fort Plot No 17-24, Vithalrao Nagar, Madhapur,

Mumbai 400 001 Hyderabad 500 081

Telephone: +91-22-2268 1285 Telephone: +91- 40-2342 0815-23

Facsimile: +91-22-2263 1984 Facsimile: +91- 40-2343 1551

Contact Person: Ms. Sonam Jalan Contact Person: Mr. M. Murali Krishna

Email: [email protected] E-mail: [email protected]

OFFER OPENS ON : Monday, June 15, 2009 OFFER CLOSES ON : Saturday, July 4, 2009

(For schedule of major activities relating to the Offer, please refer to the next page)

2

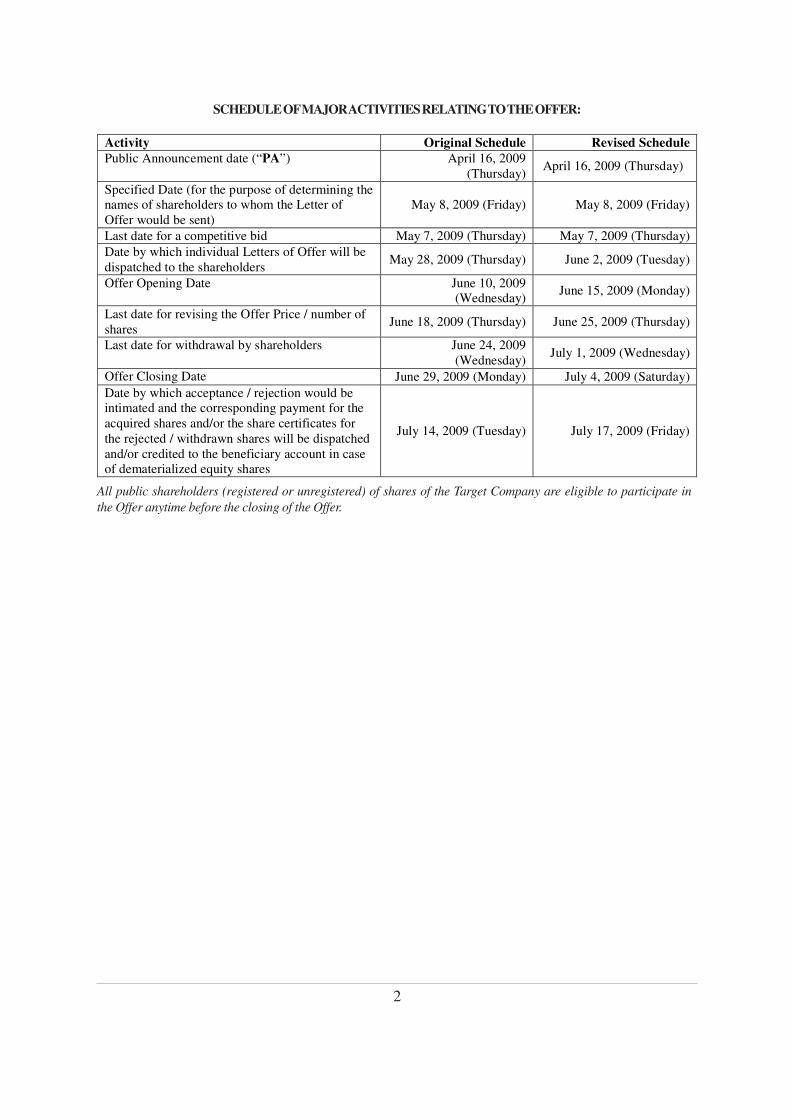

SCHEDULE OF MAJOR ACTIVITIES RELATING TO THE OFFER:

All public shareholders (registered or unregistered) of shares of the Target Company are eligible to participate in

the Offer anytime before the closing of the Offer.

Activity Original Schedule Revised Schedule

Public Announcement date (“PA”) April 16, 2009 (Thursday)

April 16, 2009 (Thursday)

Specified Date (for the purpose of determining the names of shareholders to whom the Letter of Offer would be sent)

May 8, 2009 (Friday) May 8, 2009 (Friday)

Last date for a competitive bid May 7, 2009 (Thursday) May 7, 2009 (Thursday)

Date by which individual Letters of Offer will be dispatched to the shareholders

May 28, 2009 (Thursday) June 2, 2009 (Tuesday)

Offer Opening Date June 10, 2009 (Wednesday)

June 15, 2009 (Monday)

Last date for revising the Offer Price / number of shares

June 18, 2009 (Thursday) June 25, 2009 (Thursday)

Last date for withdrawal by shareholders June 24, 2009 (Wednesday)

July 1, 2009 (Wednesday)

Offer Closing Date June 29, 2009 (Monday) July 4, 2009 (Saturday)

Date by which acceptance / rejection would be intimated and the corresponding payment for the acquired shares and/or the share certificates for the rejected / withdrawn shares will be dispatched and/or credited to the beneficiary account in case of dematerialized equity shares

July 14, 2009 (Tuesday) July 17, 2009 (Friday)

3

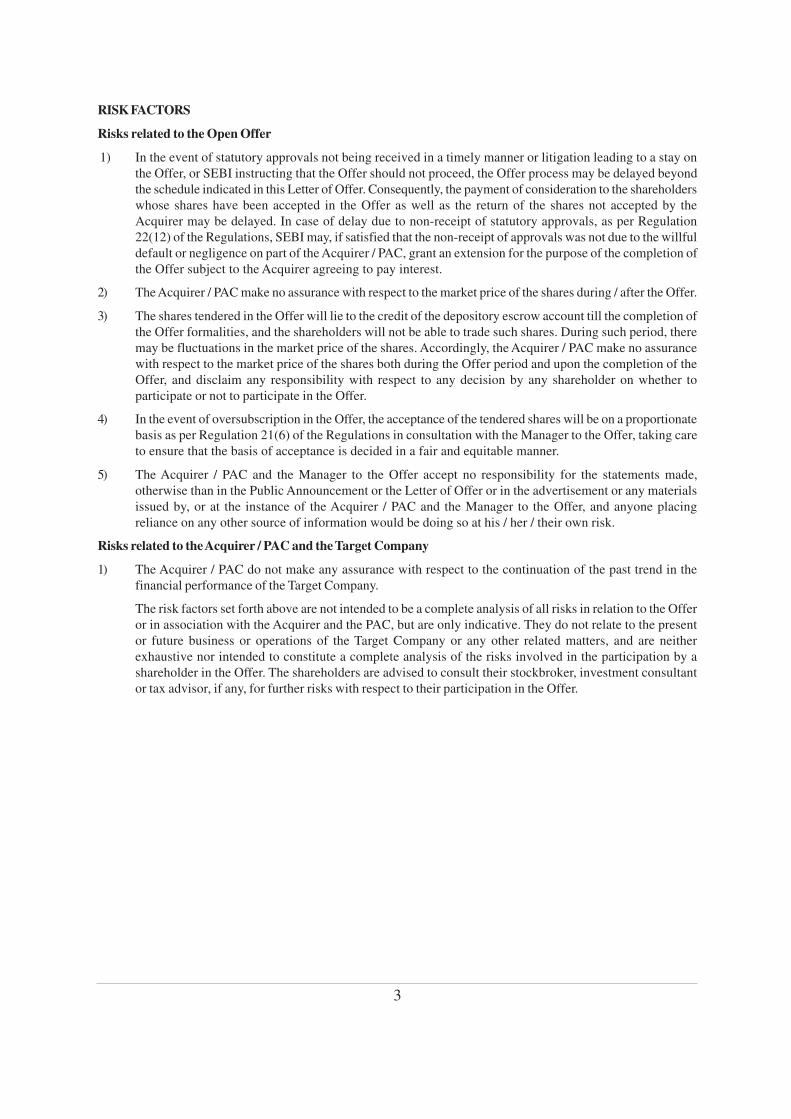

RISK FACTORS

Risks related to the Open Offer

1) In the event of statutory approvals not being received in a timely manner or litigation leading to a stay on

the Offer, or SEBI instructing that the Offer should not proceed, the Offer process may be delayed beyond

the schedule indicated in this Letter of Offer. Consequently, the payment of consideration to the shareholders

whose shares have been accepted in the Offer as well as the return of the shares not accepted by the

Acquirer may be delayed. In case of delay due to non-receipt of statutory approvals, as per Regulation

22(12) of the Regulations, SEBI may, if satisfied that the non-receipt of approvals was not due to the willful

default or negligence on part of the Acquirer / PAC, grant an extension for the purpose of the completion of

the Offer subject to the Acquirer agreeing to pay interest.

2) The Acquirer / PAC make no assurance with respect to the market price of the shares during / after the Offer.

3) The shares tendered in the Offer will lie to the credit of the depository escrow account till the completion of

the Offer formalities, and the shareholders will not be able to trade such shares. During such period, there

may be fluctuations in the market price of the shares. Accordingly, the Acquirer / PAC make no assurance

with respect to the market price of the shares both during the Offer period and upon the completion of the

Offer, and disclaim any responsibility with respect to any decision by any shareholder on whether to

participate or not to participate in the Offer.

4) In the event of oversubscription in the Offer, the acceptance of the tendered shares will be on a proportionate

basis as per Regulation 21(6) of the Regulations in consultation with the Manager to the Offer, taking care

to ensure that the basis of acceptance is decided in a fair and equitable manner.

5) The Acquirer / PAC and the Manager to the Offer accept no responsibility for the statements made,

otherwise than in the Public Announcement or the Letter of Offer or in the advertisement or any materials

issued by, or at the instance of the Acquirer / PAC and the Manager to the Offer, and anyone placing

reliance on any other source of information would be doing so at his / her / their own risk.

Risks related to the Acquirer / PAC and the Target Company

1) The Acquirer / PAC do not make any assurance with respect to the continuation of the past trend in the

financial performance of the Target Company.

The risk factors set forth above are not intended to be a complete analysis of all risks in relation to the Offer

or in association with the Acquirer and the PAC, but are only indicative. They do not relate to the present

or future business or operations of the Target Company or any other related matters, and are neither

exhaustive nor intended to constitute a complete analysis of the risks involved in the participation by a

shareholder in the Offer. The shareholders are advised to consult their stockbroker, investment consultant

or tax advisor, if any, for further risks with respect to their participation in the Offer.

4

TABLE OF CONTENTS

Disclaimer Clause ............................................................................................................................... 6

1. Background to the Offer ..................................................................................................................... 6

2. Details of the Offer .............................................................................................................................. 7

3. Object of the Acquisition / Offer ......................................................................................................... 8

4. Background of the Acquirer and PAC ................................................................................................ 8

5. Option in terms of Regulation 21(2) ................................................................................................. 44

6. Background of the Target Company ................................................................................................. 44

7. Offer Price and Financial Arrangements ......................................................................................... 56

8. Terms and Conditions of the Offer .................................................................................................... 58

9. Statutory Approvals ............................................................................................................................ 59

10. Procedure for Acceptance and Settlement ........................................................................................ 59

11. Documents for Inspection .................................................................................................................. 64

12. Declaration by the Acquirer and the PAC ......................................................................................... 64

Attached: Form of Acceptance-cum-Acknowledgement, Form of Withdrawal and Transfer Deed (where

applicable)

5

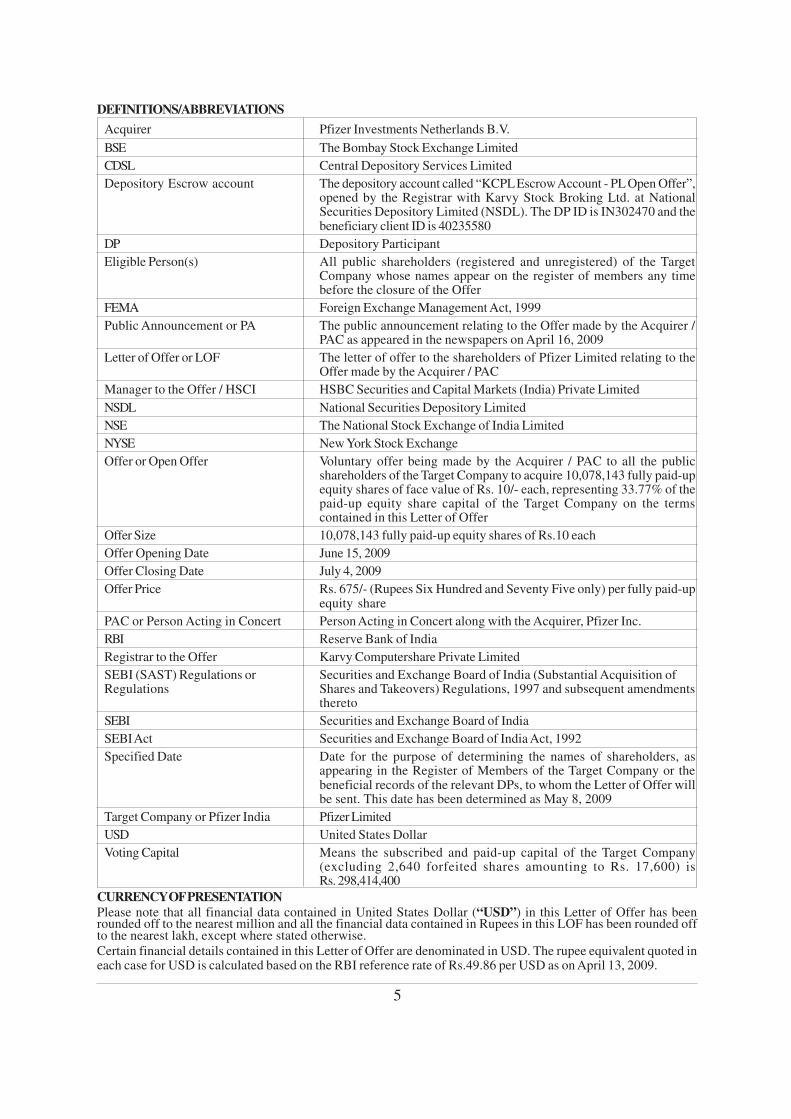

DEFINITIONS/ABBREVIATIONS

Acquirer Pfizer Investments Netherlands B.V.

BSE The Bombay Stock Exchange Limited

CDSL Central Depository Services Limited

Depository Escrow account The depository account called “KCPL Escrow Account - PL Open Offer”,opened by the Registrar with Karvy Stock Broking Ltd. at NationalSecurities Depository Limited (NSDL). The DP ID is IN302470 and thebeneficiary client ID is 40235580

DP Depository Participant

Eligible Person(s) All public shareholders (registered and unregistered) of the TargetCompany whose names appear on the register of members any timebefore the closure of the Offer

FEMA Foreign Exchange Management Act, 1999

Public Announcement or PA The public announcement relating to the Offer made by the Acquirer /PAC as appeared in the newspapers on April 16, 2009

Letter of Offer or LOF The letter of offer to the shareholders of Pfizer Limited relating to theOffer made by the Acquirer / PAC

Manager to the Offer / HSCI HSBC Securities and Capital Markets (India) Private Limited

NSDL National Securities Depository Limited

NSE The National Stock Exchange of India Limited

NYSE New York Stock Exchange

Offer or Open Offer Voluntary offer being made by the Acquirer / PAC to all the publicshareholders of the Target Company to acquire 10,078,143 fully paid-upequity shares of face value of Rs. 10/- each, representing 33.77% of thepaid-up equity share capital of the Target Company on the termscontained in this Letter of Offer

Offer Size 10,078,143 fully paid-up equity shares of Rs.10 each

Offer Opening Date June 15, 2009

Offer Closing Date July 4, 2009

Offer Price Rs. 675/- (Rupees Six Hundred and Seventy Five only) per fully paid-upequity share

PAC or Person Acting in Concert Person Acting in Concert along with the Acquirer, Pfizer Inc.

RBI Reserve Bank of India

Registrar to the Offer Karvy Computershare Private Limited

SEBI (SAST) Regulations or Securities and Exchange Board of India (Substantial Acquisition ofRegulations Shares and Takeovers) Regulations, 1997 and subsequent amendments

thereto

SEBI Securities and Exchange Board of India

SEBI Act Securities and Exchange Board of India Act, 1992

Specified Date Date for the purpose of determining the names of shareholders, asappearing in the Register of Members of the Target Company or thebeneficial records of the relevant DPs, to whom the Letter of Offer willbe sent. This date has been determined as May 8, 2009

Target Company or Pfizer India Pfizer Limited

USD United States Dollar

Voting Capital Means the subscribed and paid-up capital of the Target Company(excluding 2,640 forfeited shares amounting to Rs. 17,600) isRs. 298,414,400

CURRENCY OF PRESENTATION

Please note that all financial data contained in United States Dollar (“USD”) in this Letter of Offer has beenrounded off to the nearest million and all the financial data contained in Rupees in this LOF has been rounded offto the nearest lakh, except where stated otherwise.Certain financial details contained in this Letter of Offer are denominated in USD. The rupee equivalent quoted ineach case for USD is calculated based on the RBI reference rate of Rs.49.86 per USD as on April 13, 2009.

6

This Letter of Offer is being issued by HSBC Securities and Capital Markets (India) Private Limited (“HSCI” or the

“Manager to the Offer”), on behalf of the Acquirer and the PAC pursuant to Regulation 11(1) and other applicable

provisions of the Regulations.

Disclaimer

AS REQUIRED, A COPY OF THE DRAFT LETTER OF OFFER HAS BEEN SUBMITTED TO SEBI. IT IS TO BE

DISTINCTLY UNDERSTOOD THAT THE FILING OF THE DRAFT LETTER OF OFFER WITH SEBI SHOULD

NOT, IN ANY WAY, BE DEEMED OR CONSTRUED THAT THE SAME HAS BEEN CLEARED, VETTED OR

APPROVED BY SEBI. THE DRAFT LETTER OF OFFER HAS BEEN SUBMITTED TO SEBI FOR A LIMITED

PURPOSE OF OVERSEEING WHETHER THE DISCLOSURES CONTAINED THEREIN ARE GENERALLY

ADEQUATE AND ARE IN CONFORMITY WITH THE REGULATIONS. THIS REQUIREMENT IS TO FACILITATE

THE SHAREHOLDERS OF PFIZER LIMITED TO MAKE AN INFORMED DECISION WITH REGARD TO THE

OFFER. SEBI DOES NOT TAKE ANY RESPONSIBILITY EITHER FOR THE FINANCIAL SOUNDNESS OF THE

ACQUIRER, THE PAC OR OF THE TARGET COMPANY WHOSE SHARES / CONTROL ARE / IS PROPOSED TO

BE ACQUIRED OR FOR THE CORRECTNESS OF THE STATEMENTS MADE OR OPINIONS EXPRESSED IN

THE LETTER OF OFFER. IT SHOULD ALSO BE CLEARLY UNDERSTOOD THAT, WHILE THE ACQUIRER / PAC

ARE PRIMARILY RESPONSIBLE FOR THE CORRECTNESS, ADEQUACY, AND DISCLOSURE OF ALL RELEVANT

INFORMATION IN THIS LETTER OF OFFER, THE MANAGER TO THE OFFER IS EXPECTED TO EXERCISE

DUE DILIGENCE TO ENSURE THAT THE ACQUIRER / PAC DULY DISCHARGE THEIR RESPONSIBILITIES

ADEQUATELY. IN THIS BEHALF, AND TOWARDS THIS PURPOSE, HSBC SECURITIES AND CAPITAL

MARKETS (INDIA) PRIVATE LIMITED, THE MANAGER TO THE OFFER, HAS SUBMITTED A DUE DILIGENCE

CERTIFICATE DATED APRIL 29, 2009 TO SEBI IN ACCORDANCE WITH THE SEBI (SUBSTANTIAL

ACQUISITION OF SHARES AND TAKEOVERS) REGULATIONS 1997 AND SUBSEQUENT AMENDMENT(S)

THERETO. THE FILING OF THE LETTER OF OFFER DOES NOT, HOWEVER, ABSOLVE THE ACQUIRER / PAC

FROM THE REQUIREMENT OF OBTAINING SUCH STATUTORY CLEARANCES AS MAY BE REQUIRED FOR

THE PURPOSE OF THE OFFER.

1. Background to the Offer

1.1. The voluntary offer (the “Offer” or the “Open Offer”) is pursuant to the desire of Pfizer Inc. (“PAC”) and

Pfizer Investments Netherlands B.V. (“Acquirer”) to consolidate the holding of the Pfizer group in Pfizer

Limited (“Pfizer India” or “Target Company”) under Regulation 11(1) of the Regulations, while ensuring

that the public shareholding in the Target Company does not fall below the minimum level of shareholding

required to be maintained under the Listing Agreements, as amended from time to time, entered into by the

Target Company with the Bombay Stock Exchange (the “BSE”), and the National Stock Exchange of India

Limited (the “NSE”). Pursuant to Circular No. SEBI/CFDDIL/LA/2006/13/4 issued by the SEBI on April 13,

2006, the minimum level of public shareholding required to be maintained under the Listing Agreements as

amended from time to time, entered into by the Target Company with the BSE and NSE is 10%.

1.2. The Acquirer along with the PAC is making the Offer to the public shareholders of the Target Company to

acquire up to 10,078,143 fully paid-up equity shares of Rs.10 each (the “Offer Size”) constituting 33.77%

of the Voting Capital (as defined in Clause 2.2 below) of the Target Company. The Offer is being made at a

price of Rs.675/- (Rupees Six Hundred and Seventy Five only) per equity share (the “Offer Price”), to be

paid in cash, in accordance with the provisions of the Regulations and subject to the terms and conditions

mentioned in this Letter of Offer in relation to the Offer.

1.3. The Acquirer holds no shares in the Target Company. Subsidiaries of the PAC hold an aggregate of

12,302,937 equity shares of the Target Company constituting 41.23% of the voting equity share capital of

the Target Company. There are no partly paid-up shares in the Target Company or any instruments convertible

into shares of the Target Company at a future date.

1.4. Upon completion of the Offer, assuming full acceptances and taking into account the existing holding, the

Pfizer group will hold 75% of the Voting Capital (as defined in Clause 2.2 below) in the Target Company.

1.5. The Offer is voluntary and in accordance with Regulation 11(1) of the Regulations and has not been

triggered by any agreement of the Acquirer or the PAC with any person for the purpose of acquisition of

shares in the Target Company.

1.6. The Acquirer is a private company incorporated on March 27, 2009, under the laws of The Netherlands, with

its registered office located at Rivium Westlaan 142, 2909 LD Capelle aan den IJssel, the Netherlands.

7

1.7. The Target Company is a public limited company, incorporated on November 21, 1950 under the name

Dumex Limited. In 1958, Dumex Limited was taken over by the Pfizer group and its name was changed to

Pfizer Private Limited in 1961, which was further changed to Pfizer Limited in 1966. The Target Company is

a part of the Pfizer group and is engaged in the business of pharmaceuticals, animal health products and

services – medical and research division.

1.8. None of the Acquirer or PAC or Target Company has been prohibited by SEBI from dealing in securities, in

terms of direction issued under Section 11B of the SEBI Act or under any of the regulations made there

under.

1.9. The Acquirer does not have any intention to change the board of directors of Pfizer India during the offer

period, except to the extent permitted by applicable law.

1.10. The Manager to the Offer does not hold any equity shares of the Target Company as on the date of the PA.

In terms of Regulation 24(5A) of the SEBI (SAST) Regulations, the Manager to the Offer shall not deal in the

equity shares of the Target Company during the period commencing from the date of its appointment in

terms of Regulation 13 of the SEBI (SAST) Regulations till the expiry of (15) fifteen days from the date of

closure of the Offer.

2. Details of the Offer

2.1 The Public Announcement of the Offer appeared on April 16, 2009 in the following newspapers in accordance

with Regulation 15 of the Regulations:

A copy of the PA is also available on the SEBI website: www.sebi.gov.in

2.2 As of the date of the PA, the issued equity share capital of the Target Company is Rs. 298,440,800 divided

into 29,844,080 outstanding equity shares of face value of Rs. 10 each (including 2,640 forfeited shares).

The subscribed and paid-up capital of the Target Company (excluding 2,640 forfeited shares amounting to

Rs. 17,600) is Rs. 298,414,400 (“Voting Capital”) divided into fully paid-up 29,841,440 equity shares of face

value of Rs. 10 each. There are currently no outstanding partly paid-up shares or any other instruments

convertible into equity shares of the Target Company at a future date.

2.3 This Offer to all the public shareholders of the Target Company is to acquire 10,078,143 fully paid-up equity

shares of Rs. 10 each representing 33.77% of the present fully paid-up equity share capital of the Target

Company at the Offer Price of Rs. 675 (Rupees Six Hundred and Seventy Five only) per share, from all the

public shareholders of the Target Company who tender their shares and whose shares are acquired by the

Acquirer.

2.4 The Offer Price will be payable in cash, subject to the terms and conditions mentioned in this Letter of Offer.

2.5 The Offer is not conditional upon any minimum level of acceptance. Accordingly, the Acquirer / PAC will

accept all shares tendered by the public shareholders pursuant to the Offer at the Offer Price, subject to the

shares tendered, not exceeding 10,078,143 shares. In case the number of shares tendered exceeds this

number, the acceptance will be made on a proportionate basis in terms of Regulation 21(6) of the Regulations.

2.6 This is not a competitive bid and there has been no competitive bid to this Offer as on the date of this Letter

of Offer.

2.7 Neither the Acquirer, nor the PAC has acquired any shares of the Target Company after the date of the PA

and up to the date of this Letter of Offer.

2.8 Any decision for the upward revision in the Offer Price by the Acquirer up to the last date of revision (June

25, 2009) or withdrawal of the Offer would be communicated by way of a public announcement in the same

newspapers in which the PA had appeared. In case of an upward revision in the Offer Price, the Acquirer

would pay such revised price for all the shares validly tendered any time during the Offer and accepted

under the Offer. The acquisition of shares, which are validly tendered, by the Acquirer under this Offer will

take place on or before July 17, 2009, in accordance with the schedule of events set out in this Letter of Offer

and not at any point earlier in time.

Newspapers Language Edition

Business Standard English All Editions

Prathakal Hindi All Editions

Sakal Marathi Mumbai

8

2.9 As the Offer Price cannot be revised during 7 (seven) working days prior to the closure of the Offer, it

would, therefore, be in the interest of the shareholders to wait until the commencement of that period to

know the final offer price and tender their acceptance accordingly.

2.10 Shares that are subject to any charge, lien or encumbrance, any court order / any other attachment / dispute

are liable to be rejected in the Offer. Applications in respect of shares that are the subject matter of litigation

wherein the shareholders may be prohibited from transferring the shares during the pendency of such

litigation are liable to be rejected if the directions / orders permitting transfer of these shares are not

received together with the shares tendered under the Offer. The Acquirer will acquire the equity shares

together with all rights attached thereto, including the rights to all dividends, bonuses and rights

subsequently declared. The tender by any shareholder of any equity shares in the Offer must be absolute,

unconditional and unqualified.

2.11 As mentioned in this Letter of Offer, the Offer will close on July 4, 2009. The record date for determining the

shareholders entitled for payment of a dividend for the financial year ended November 2008 in respect of

shares held in electronic form is as on the closure of business hours on April 4, 2009 and in respect of shares

held in physical form as on April 15, 2009. The shareholders who tender their equity shares in the Open

Offer shall be eligible for receipt of the dividend declared for the financial year ended November 2008

subject to other applicable conditions for the same.

3. Object of the Acquisition / Offer

3.1 The Pfizer group has operations worldwide and has achieved a leading global position in the pharmaceutical

industry. The Acquirer and the PAC wish to consolidate and enhance the stake of the Pfizer group in order

to create more flexibility for how the Pfizer group organizes its commercial and financial activities in India.

3.2 Subsidiaries of the PAC hold an aggregate of 12,302,937 equity shares of the Target Company constituting

41.23% of the issued and paid-up equity share capital of the Target Company as of the date of the PA. The

Pfizer group wishes to further consolidate its shareholding to 75% by making this Offer to public shareholders

of Pfizer India in accordance with Regulation 11(1) of the SEBI (SAST) Regulations, while ensuring that the

public shareholding in the Target Company does not fall below 10%, the minimum level of public shareholding

required to be maintained under the Listing Agreements, as amended from time to time, entered into by the

Target Company with the BSE and NSE.

3.3 The Acquirer and the PAC do not have any specific future plans with respect to the Target Company. The

Acquirer and the PAC shall consider the merits of any future proposal for the disposal or encumbrance of

the assets of the Target Company as and when such opportunities arise. Under the second proviso to

Regulation 16(ix) of the extant SEBI (SAST) Regulations, the Acquirer shall not sell, dispose of or otherwise

encumber any substantial asset of the Target Company, except with the prior approval of the shareholders.

3.4 The Acquirer does not have any intention to change the board of directors of Pfizer India during the Offer

period, except to the extent permitted by applicable law.

4. Background of the Acquirer and PAC

4.1 The Acquirer

The Acquirer is an unlisted company incorporated on March 27, 2009, under the laws of The Netherlands.

Address of Corporate and Registered Office (with phone numbers)

4.1.1 Brief history & major areas of operation:

The Acquirer has been incorporated on March 27, 2009, among other things, to invest in one or more

companies in the South Asia region, as the board of directors of the Acquirer may decide from time to time.

4.1.2 Identity of promoters

The PAC is the ultimate parent company of the Acquirer.

Principal place of

business

Rivium Westlaan 142, 2909 LD Capelle aan den IJssel, the Netherlands Tel: 31-10-406-4349; Fax: 31-10-406-4481

Registered Office Rivium Westlaan 142, 2909 LD Capelle aan den IJssel, the Netherlands

Tel: 31-10-406-4349; Fax: 31-10-406-4481

9

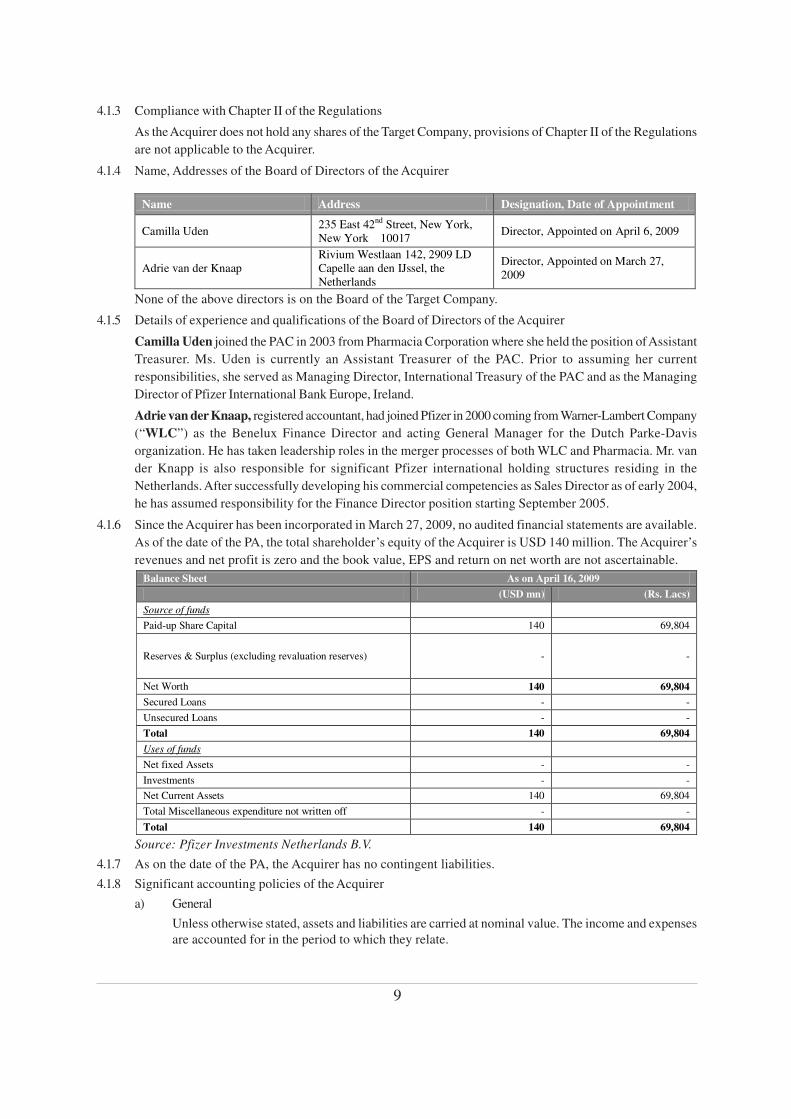

4.1.3 Compliance with Chapter II of the Regulations

As the Acquirer does not hold any shares of the Target Company, provisions of Chapter II of the Regulations

are not applicable to the Acquirer.

4.1.4 Name, Addresses of the Board of Directors of the Acquirer

None of the above directors is on the Board of the Target Company.

4.1.5 Details of experience and qualifications of the Board of Directors of the Acquirer

Camilla Uden joined the PAC in 2003 from Pharmacia Corporation where she held the position of Assistant

Treasurer. Ms. Uden is currently an Assistant Treasurer of the PAC. Prior to assuming her current

responsibilities, she served as Managing Director, International Treasury of the PAC and as the Managing

Director of Pfizer International Bank Europe, Ireland.

Adrie van der Knaap, registered accountant, had joined Pfizer in 2000 coming from Warner-Lambert Company

(“WLC”) as the Benelux Finance Director and acting General Manager for the Dutch Parke-Davis

organization. He has taken leadership roles in the merger processes of both WLC and Pharmacia. Mr. van

der Knapp is also responsible for significant Pfizer international holding structures residing in the

Netherlands. After successfully developing his commercial competencies as Sales Director as of early 2004,

he has assumed responsibility for the Finance Director position starting September 2005.

4.1.6 Since the Acquirer has been incorporated in March 27, 2009, no audited financial statements are available.

As of the date of the PA, the total shareholder’s equity of the Acquirer is USD 140 million. The Acquirer’s

revenues and net profit is zero and the book value, EPS and return on net worth are not ascertainable.

Source: Pfizer Investments Netherlands B.V.

4.1.7 As on the date of the PA, the Acquirer has no contingent liabilities.

4.1.8 Significant accounting policies of the Acquirer

a) General

Unless otherwise stated, assets and liabilities are carried at nominal value. The income and expenses

are accounted for in the period to which they relate.

Name Address Designation, Date of Appointment

Camilla Uden 235 East 42nd Street, New York, New York 10017

Director, Appointed on April 6, 2009

Adrie van der Knaap Rivium Westlaan 142, 2909 LD Capelle aan den IJssel, the Netherlands

Director, Appointed on March 27, 2009

Balance Sheet As on April 16, 2009

(USD mn) (Rs. Lacs)

Source of funds

Paid-up Share Capital 140 69,804

Reserves & Surplus (excluding revaluation reserves) - -

Net Worth 140 69,804

Secured Loans - -

Unsecured Loans - -

Total 140 69,804

Uses of funds

Net fixed Assets - -

Investments - -

Net Current Assets 140 69,804

Total Miscellaneous expenditure not written off - -

Total 140 69,804

10

b) Fixed Assets

The accounts of the Acquirer state intangible, tangible and financial fixed assets in accordance with

accounting principles generally accepted for financial reporting in the Netherlands. Pursuant to

these principles, long-lived assets should be assessed on impairment in the case of changes or

circumstances arising that lead to the suspicion that the book value of the asset may not be recovered.

The recoverability of the assets in use is determined by comparing the book value of an asset with

the recoverable amount as the higher of the discounted future net cash flow that the asset is

expected to generate or an asset’s fair value less costs to sell. If the book value of an asset exceeds

the fair value, an amount for impairment is charged to the result equal to the difference between the

book value and the recoverable amount of the asset. Assets for sale are stated at book value or lower

market value, less selling costs.

c) Intangible fixed assets

Intangible fixed assets other than goodwill acquired are capitalized and amortized against income

over the estimated useful life of the underlying assets, not exceeding 20 years.

d) Tangible fixed assets

Tangible fixed assets are stated at cost. With the exception of land, tangible fixed assets are depreciated

over their estimated economic lives by the straight line method.

e) Financial fixed assets

Participation in respect of which less than 20% of the voting rights are held are carried at cost or

lower realizable value.

Participations in respect of which 20% or more of the voting rights are held are carried at net asset

value. The net asset value is calculated on the basis of the accounting principles generally accepted

for financial reporting in the Netherlands. In case the net equity of such participation is a negative

amount, a provision is created and booked against (long term) receivables from subsidiaries or

affiliated companies, and the remaining amount is recognized as a provision.

Securities held to maturity and securities held-for-sale, presented under long term investments, are

carried at fair value (observable market quotes).

Long term loans are reported at their principal amount outstanding. Interest Income on loans is

credited to Income based on loan principal amounts outstanding at applicable interest rates. Any

profit or loss is accounted for under net financial income.

The deferred income taxes and the other financial fixed assets are valued at nominal value or lower

market value.

f) Receivables

Receivables are stated at nominal value reduced, where appropriate, by a provision for doubtful

debtors.

Securities available for sale, forward exchange contracts and interest rate swaps are carried at fair

value.

g) Minority interest

The minority interests are valued at net asset value, which is determined in accordance with

accounting principles generally accepted for financial reporting in the Netherlands.

h) Provisions – Deferred tax liabilities

Insofar as valuations of assets and liabilities for tax purposes differ from their carrying amounts, and

this results in deferred tax liabilities, a provision is formed for these liabilities, calculated at the tax

rates that are expected to apply to the period when the liability is settled. Deferred tax assets are only

recognized if it is probable that sufficient taxable profit will be available to realize such assets.

i) Long term liabilities

Securities and cross currency swaps are stated at fair value. Long term debt is stated at nominal

value reduced, where appropriate.

11

j) Net turnover

Net turnover is stated net of returns, commissions, discounts and value added tax

k) Revenues

Revenues are accounted for in the period to which they relate on the basis of the accounting

principles generally accepted for financial reporting in the Netherlands.

l) Taxation

The taxation on result comprises both taxes payable in the short term and deferred taxes, taking

account of tax facilities and non-deductible costs. No taxes are deducted from profits if and insofar

as profits can be offset against unrecognized losses from previous years.

Tax credits on losses are cognized if these can be offset against profits in previous years and this

results in a tax rebate. In addition, taxes may be deducted if and insofar as may be reasonably

expected that losses can be offset against future profits.

m) Result from participations

The share in the result of participating interests consists of dividends received from participations

carried at cost, the share of the group in the result of participating interests carried at net asset value

and the result of divestitures.

n) Foreign currencies

The reporting currency of the Acquirer is the USD.

For most international operations, local currencies have been determined to be the functional

currencies. The effects of converting non-functional currency assets and liabilities into the functional

currency are recorded in other expenses. The Acquirer translates functional currency assets and

liabilities to their U.S. dollar equivalents at rates in effect at the balance sheet date and records these

translation adjustments in Shareholder’s Account – Currency Translation Difference. The Acquirer

translates functional currency statement of Income amounts at average rates for the period. Assets

and liabilities at year end and transactions during the year denominated n foreign currencies are

translated into the reporting currency at exchange rates ruling at the end of the year and at the time

of the transaction, respectively. Any exchange gains or losses are recognized in the statement of

income under net financial income.

During consolidation intercompany exchange gains or losses recorded in net financial income are

eliminated against Shareholder’s Account – Currency Translation Difference.

For operations in highly inflationary economies, the Acquirer translates monetary items at rates in

effect at the balance sheet date with translation adjustments recorded in Net Financial Income and

non-monetary items at historical rates.

o) The use of estimates

The preparation of the financial statements requires the management to form opinions and to make

estimates and assumptions that influence the application of principles and the reported values of

assets and liabilities and of income and expenditure. The actual results may differ from these estimates.

The estimates and the underlying assumptions are constantly assessed. Revisions of estimates are

recognized in the period in which the estimate is revised and in future periods for which the revision

has consequences.

p) Financial instruments

• Foreign exchange risk

The Acquirer entered into financial instruments to hedge or offset by the same currency an

appropriate portion of the currency risk and the timing of the hedged or offset item.

All derivative contracts used to manage foreign currency risk are measured at fair value and

reported as assets or liabilities on the balance sheet. Changes in fair value are reported in the

profit and loss account or are deferred, depending on the nature and effectiveness of the

offset or hedging relationship.

Until recognition the fair value changes of cashflow hedges are taken to the Acquirer’s

12

accounts. The Acquirer recognizes the profit and loss account impact of foreign currency

swaps and foreign currency forward-exchange contracts designated as cash flow hedges in

the profit and loss account upon recognition of the foreign exchange gain or loss on the

translation to US dollars of the hedged items.

The Acquirer recognizes the profit and loss account impact of foreign currency swaps and

foreign currency forward-exchange contracts that are used to offset foreign currency assets

or liabilities in the profit and loss account during the terms of the contracts, along with the

profit and loss account impact of the items they generally offset.

Any ineffectiveness in a hedging relationship is recognized immediately into the profit and

loss account.

• Interest rate risk

The Acquirer entered into financial instruments to hedge variable interest rates to fixed

interest rates on the hedged items and convert fixed interest rates to variable interest rates,

matching the amount and timing of the hedged item.

All derivative contracts used to manage interest rate risk are measured at fair value and

reported as assets or liabilities on the balance sheet. Changes in fair value are reported in the

profit and loss account or are deferred, depending on the nature and effectiveness of the

offset or hedging relationship

Until recognition the fair value changes of cash flow hedges are taken to the Acquirer’s

accounts. The Acquirer recognizes the profit and loss account impact of interest rate swaps

designated as cash flow hedges in the profit and loss account upon the recognition of the

interest related to the hedged items.

The Acquirer recognizes the profit and loss account impact of interest rate swaps as fair

value hedges in the profit and loss account upon the recognition of the change in fair value

for interest rate risk related to the hedged items.

Any ineffectiveness in a hedging relationship is recognized immediately into the profit and

loss account.

4.1.9 The Acquirer has not made any earlier acquisitions in the Target Company.

4.1.10 The Acquirer has not undertaken any merger/demerger/spin-off during the last 3 years ended November 30,

2008, 2007 and 2006.

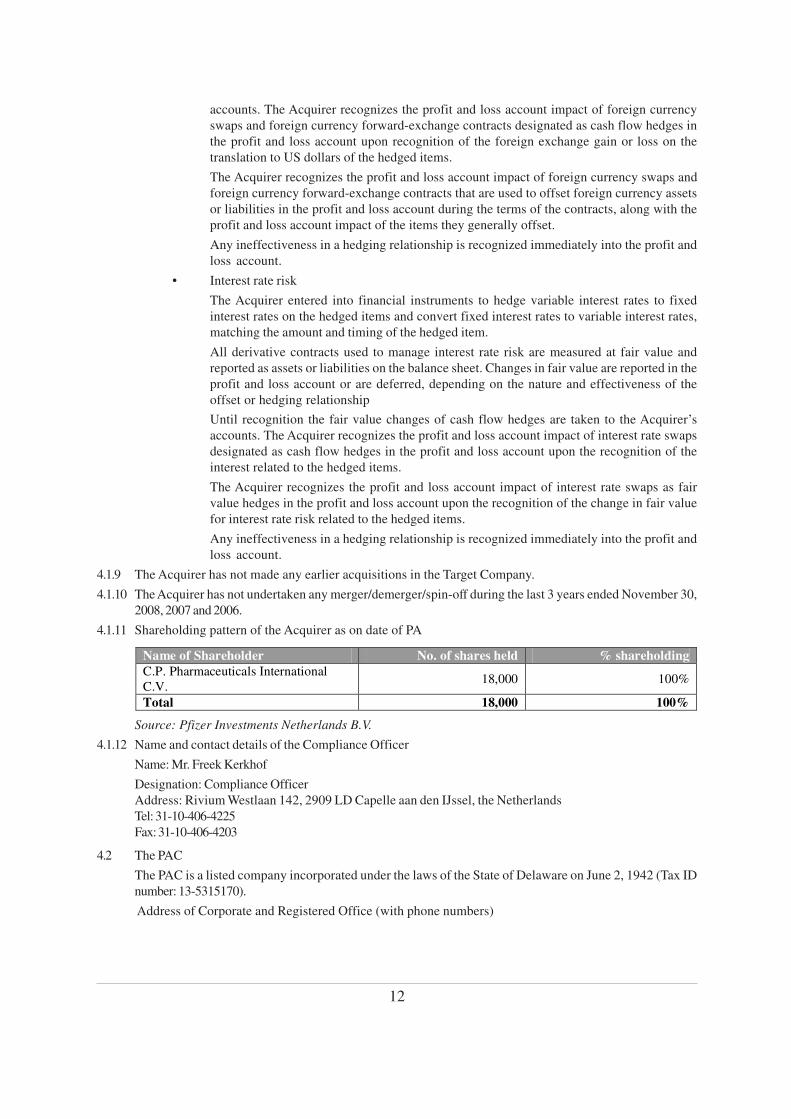

4.1.11 Shareholding pattern of the Acquirer as on date of PA

Source: Pfizer Investments Netherlands B.V.

4.1.12 Name and contact details of the Compliance Officer

Name: Mr. Freek Kerkhof

Designation: Compliance Officer

Address: Rivium Westlaan 142, 2909 LD Capelle aan den IJssel, the Netherlands

Tel: 31-10-406-4225

Fax: 31-10-406-4203

4.2 The PAC

The PAC is a listed company incorporated under the laws of the State of Delaware on June 2, 1942 (Tax ID

number: 13-5315170).

Address of Corporate and Registered Office (with phone numbers)

Name of Shareholder No. of shares held % shareholding

C.P. Pharmaceuticals International C.V.

18,000 100%

Total 18,000 100%

13

The principal trading market for PAC’s shares is the New York Stock Exchange (“NYSE”). Its shares are also

traded on the London, Euronext and Swiss Stock Exchanges.

4.2.1 Brief History & Major areas of operation:

4.2.1.1.The PAC was incorporated on June 2, 1942 as Chas. Pfizer & Co., Inc. It changed its name to Pfizer Inc. on

April 20, 1970.

4.2.1.2. The PAC’s brief history is as follows:

Source: Company website

4.2.1.3. The PAC is a research-based, global pharmaceutical company that discovers, develops, manufactures and

markets leading prescription medicines for humans and animals. It operates in 3 business segments namely

- pharmaceuticals, animal health and other businesses:

a) The PAC has medicines across 11 therapeutic areas of Cardiovascular and Metabolic diseases;

Central Nervous System disorders; Arthritis and Pain; Infectious and Respiratory diseases; Urology;

Oncology; Ophthalmology; and Endocrine disorders. Revenues from this segment contributed to

91.5% of total revenues in 2008.

b) It discovers, develops and sells products for the prevention and treatment of diseases in livestock

and companion animals.

c) It also operates several other businesses, including the manufacture of gelatin capsules, contract

manufacturing and bulk pharmaceutical chemicals. These businesses are relatively smaller in size.

4.2.2 Identity of promoters and major shareholders

The PAC is the ultimate parent company of the Pfizer group. The PAC is a listed company with circa 224,155

registered shareholders and circa 2.5 million beneficial shareholders as of April 16, 2009. The PAC currently

has no known beneficial owners of five percent (5%) or more of its common stock.

4.2.3 Compliance with Chapter II of the Regulations

As the PAC does not directly hold any shares of the Target Company, provisions of Chapter II of the

Regulations are not applicable to the PAC.

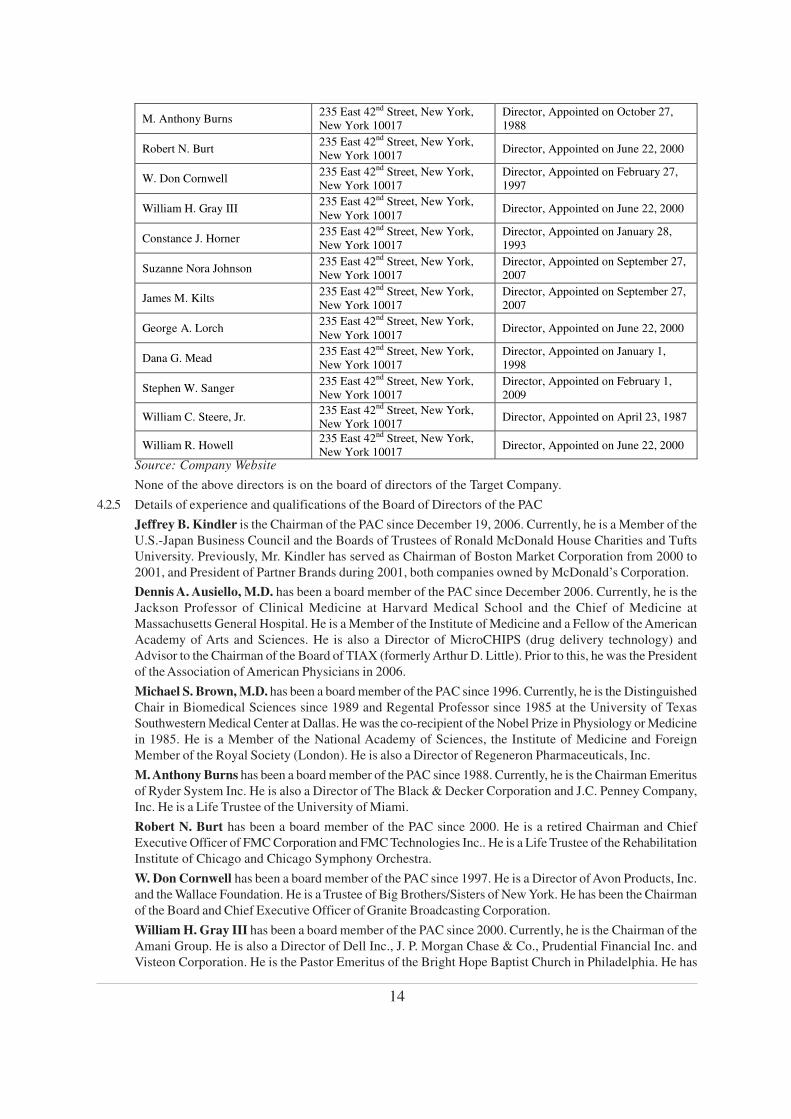

4.2.4 Name, Addresses of the board of directors of the PAC

Principal place of

business

235 East 42nd Street, New York, New York 10017 Tel: 212-573-2323 Fax: 212-573-1853

Registered Office Corporation Trust Center, 1209 Orange Street, Wilmington, County of New Castle, Delaware 19801. Tel: 302-658-7581 Fax: 302-655-5049

Period Event

1849 – 1899 In 1849, cousins Charles Pfizer and Charles Erhart founded Charles Pfizer & Company in Brooklyn, NY. Pfizer soon became America’s leading producer of citric acid and by 1899, was considered a leader in the American chemical business.

1900 - 1925 Successfully pioneered the mass production of citric acid from sugar through mold fermentation, which fueled its growth for years.

1926 - 1950 By the late 1940s, Pfizer was the established leader in the manufacture of vitamins, a leader in fermentation technology and the world’s largest producer of penicillin.

1951 - 1999 Major international expansion of Pfizer’s operations. The second half of the 1900´s saw intense pharmaceutical research and launch of several new innovative products.

2000 - 2009 After successfully merging with Warner-Lambert Company and Pharmacia Corporation, Pfizer became the fastest-growing major pharmaceutical company. Pfizer is included in the Dow Jones Industrial Average.

Name Address Designation, Date of Appointment

Jeffrey B. Kindler 235 East 42nd Street, New York, New York 10017

Chairman, Appointed on December 19, 2006

Dennis A. Ausiello, M.D. 235 East 42nd Street, New York, New York 10017

Director, Appointed on December 1, 2006

Michael S. Brown 235 East 42nd Street, New York, New York 10017

Director, Appointed on May 23, 1996

14

Source: Company Website

None of the above directors is on the board of directors of the Target Company.

4.2.5 Details of experience and qualifications of the Board of Directors of the PAC

Jeffrey B. Kindler is the Chairman of the PAC since December 19, 2006. Currently, he is a Member of the

U.S.-Japan Business Council and the Boards of Trustees of Ronald McDonald House Charities and Tufts

University. Previously, Mr. Kindler has served as Chairman of Boston Market Corporation from 2000 to

2001, and President of Partner Brands during 2001, both companies owned by McDonald’s Corporation.

Dennis A. Ausiello, M.D. has been a board member of the PAC since December 2006. Currently, he is the

Jackson Professor of Clinical Medicine at Harvard Medical School and the Chief of Medicine at

Massachusetts General Hospital. He is a Member of the Institute of Medicine and a Fellow of the American

Academy of Arts and Sciences. He is also a Director of MicroCHIPS (drug delivery technology) and

Advisor to the Chairman of the Board of TIAX (formerly Arthur D. Little). Prior to this, he was the President

of the Association of American Physicians in 2006.

Michael S. Brown, M.D. has been a board member of the PAC since 1996. Currently, he is the Distinguished

Chair in Biomedical Sciences since 1989 and Regental Professor since 1985 at the University of Texas

Southwestern Medical Center at Dallas. He was the co-recipient of the Nobel Prize in Physiology or Medicine

in 1985. He is a Member of the National Academy of Sciences, the Institute of Medicine and Foreign

Member of the Royal Society (London). He is also a Director of Regeneron Pharmaceuticals, Inc.

M. Anthony Burns has been a board member of the PAC since 1988. Currently, he is the Chairman Emeritus

of Ryder System Inc. He is also a Director of The Black & Decker Corporation and J.C. Penney Company,

Inc. He is a Life Trustee of the University of Miami.

Robert N. Burt has been a board member of the PAC since 2000. He is a retired Chairman and Chief

Executive Officer of FMC Corporation and FMC Technologies Inc.. He is a Life Trustee of the Rehabilitation

Institute of Chicago and Chicago Symphony Orchestra.

W. Don Cornwell has been a board member of the PAC since 1997. He is a Director of Avon Products, Inc.

and the Wallace Foundation. He is a Trustee of Big Brothers/Sisters of New York. He has been the Chairman

of the Board and Chief Executive Officer of Granite Broadcasting Corporation.

William H. Gray III has been a board member of the PAC since 2000. Currently, he is the Chairman of the

Amani Group. He is also a Director of Dell Inc., J. P. Morgan Chase & Co., Prudential Financial Inc. and

Visteon Corporation. He is the Pastor Emeritus of the Bright Hope Baptist Church in Philadelphia. He has

M. Anthony Burns 235 East 42nd Street, New York, New York 10017

Director, Appointed on October 27, 1988

Robert N. Burt 235 East 42nd Street, New York, New York 10017

Director, Appointed on June 22, 2000

W. Don Cornwell 235 East 42nd Street, New York, New York 10017

Director, Appointed on February 27, 1997

William H. Gray III 235 East 42nd Street, New York, New York 10017

Director, Appointed on June 22, 2000

Constance J. Horner 235 East 42nd Street, New York, New York 10017

Director, Appointed on January 28, 1993

Suzanne Nora Johnson 235 East 42nd Street, New York, New York 10017

Director, Appointed on September 27, 2007

James M. Kilts 235 East 42nd Street, New York, New York 10017

Director, Appointed on September 27, 2007

George A. Lorch 235 East 42nd Street, New York, New York 10017

Director, Appointed on June 22, 2000

Dana G. Mead 235 East 42nd Street, New York, New York 10017

Director, Appointed on January 1, 1998

Stephen W. Sanger 235 East 42nd Street, New York, New York 10017

Director, Appointed on February 1, 2009

William C. Steere, Jr. 235 East 42nd Street, New York, New York 10017

Director, Appointed on April 23, 1987

William R. Howell 235 East 42nd Street, New York, New York 10017

Director, Appointed on June 22, 2000

15

been the President and Chief Executive Officer of The College Fund/UNCF (Educational Assistance) and

has served as a Congressman from the Second District of Pennsylvania.

Constance J. Horner has been a board member of the PAC since 1993 and a Lead Director since February

2007. She is a Director of Ingersoll-Rand Company Limited, Prudential Financial, Inc., Fellow, National

Academy of Public Administration; Member of the Board of Trustees of the Prudential Foundation.

Previously, she has been a Guest Scholar at The Brookings Institution, Commissioner of the U.S. Commission

on Civil Rights, Assistant to President George H. W. Bush, Director of Presidential Personnel, Deputy

Secretary, U.S. Department of Health and Human Services.

James M. Kilts has been a board member of the PAC since September 2007. He is a Founding Partner of

Centerview Partners Management, LLC, Director of Metropolitan Life Insurance Company and

Meadwestvaco Corporation. He is a Trustee of Knox College and the University of Chicago and a member

of the Board of Overseers of Weill Cornell Medical College. He has been a Vice Chairman of The Procter &

Gamble Company, Chairman and CEO of the Gillette Company, President and CEO of the Nabisco Group

Holdings Corporation.

George A. Lorch has been a board member of the PAC since 2000. Currently, he is the Chairman Emeritus of

Armstrong Holdings, Inc. He is also a Director of Autoliv, Inc., The Williams Companies, Inc., HSBC

Finance Co. and HSBC North America Holding Company. Previously, he was the Chairman, President and

CEO of Armstrong World Industries, Inc.

Dana G. Mead, Ph.D. has been a board member of the PAC since 1998. Currently, he is the Chairman of

Massachusetts Institute of Technology Corporation, Chairman of the Board of the Ron Brown Award for

Corporate Leadership and a Lifetime Trustee of the Association of Graduates, U.S. Military Academy, West

Point. He has been the Chairman and CEO of Tenneco, Inc., Chairman of the Business Roundtable and the

National Association of Manufacturers.

Suzanne Nora Johnson has been a board member of the PAC since 2007. She is a Retired Vice Chairman of

Goldman Sachs Group, Inc., Director of American International Group, Inc., Director of Intuit and VISA,

Board member of the American Red Cross, Brookings Institution, the Carnegie Institution for Science and

the University of Southern California.

Stephen W. Sanger has been a board member of the PAC since February 2009. He is a Director of Target

Corporation and Wells Fargo & Company. Prior thereto, he has been the Chairman and CEO of General

Mills, Inc.

William C. Steere, Jr. has been a board member of the PAC since 1987. He is the Chairman Emeritus of the

PAC, Director of MetLife, Inc. and Health Management Associates, Inc., Director of the New York University

Medical Center and the New York Botanical Garden and a Member of the Board of Overseers of Memorial

Sloan-Kettering Cancer Center. He has been the Chairman and CEO of the PAC.

William R. Howell has been a board member of the PAC since 2000. He is a Chairman Emeritus of J. C.

Penney Company, Inc., Director of The Williams Companies, Inc., Director of Deutsche Bank Trust Corporation

and Deutsche Bank Trust Company Americas. He was a director on the board of directors of the PAC as on

the date of PA. He retired from the board of directors of the PAC on April 23, 2009 and no other director has

been appointed in his place.

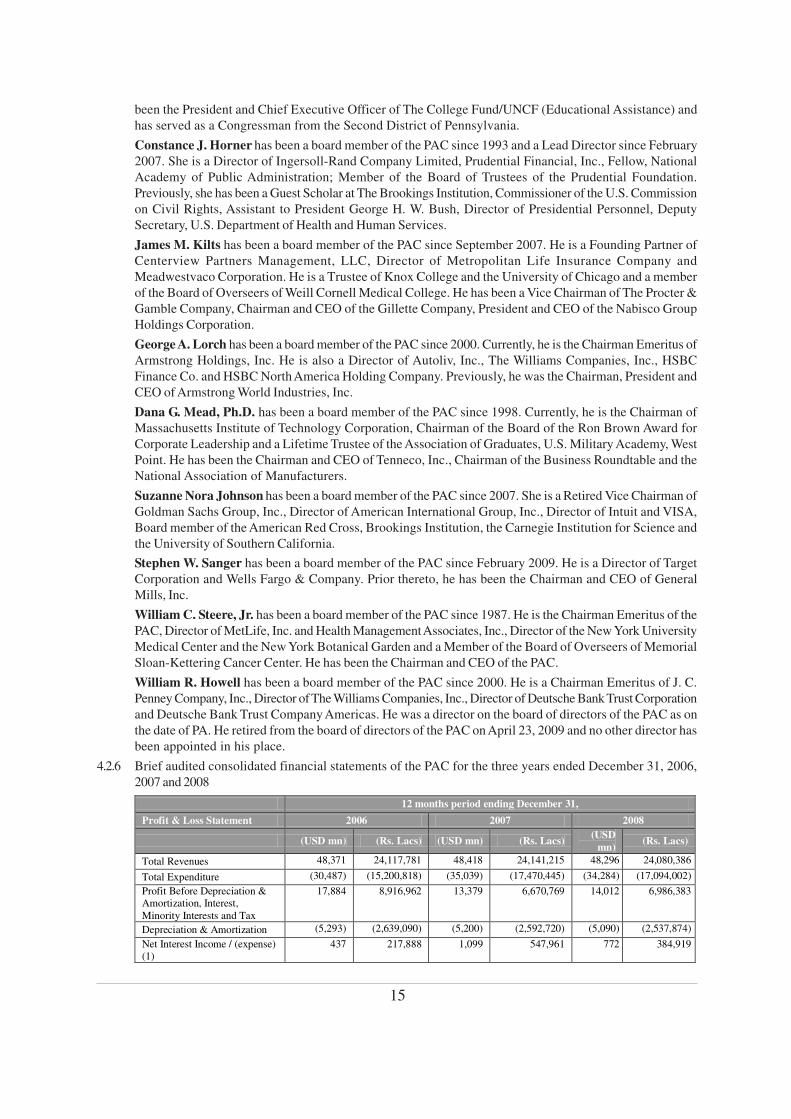

4.2.6 Brief audited consolidated financial statements of the PAC for the three years ended December 31, 2006,

2007 and 2008

12 months period ending December 31,

Profit & Loss Statement 2006 2007 2008

(USD mn) (Rs. Lacs) (USD mn) (Rs. Lacs) (USD

mn) (Rs. Lacs)

Total Revenues 48,371 24,117,781 48,418 24,141,215 48,296 24,080,386

Total Expenditure (30,487) (15,200,818) (35,039) (17,470,445) (34,284) (17,094,002)

Profit Before Depreciation & Amortization, Interest, Minority Interests and Tax

17,884 8,916,962 13,379 6,670,769 14,012 6,986,383

Depreciation & Amortization (5,293) (2,639,090) (5,200) (2,592,720) (5,090) (2,537,874)

Net Interest Income / (expense) (1)

437 217,888 1,099 547,961 772 384,919

16

Source: Annual Reports

4.2.7 Primary reasons for fall/rise in total revenues and net profit of the PAC are as under:

Year ended December 2008 compared to Year ended December 2007

a) Revenues

Revenues of USD 48,296 million were essentially flat when compared to 2007 with a decline in

revenues of -0.3%. This was due to the following factors:

• The favorable impact of foreign exchange, which increased revenues by approximately USD

Profit Before Tax 13,028 6,495,761 9,278 4,626,011 9,694 4,833,428

Provision for taxes (1,992) (993,211) (1,023) (510,068) (1,645) (820,197)

Minority Interest (12) (5,983) (42) (20,941) (23) (11,468)

Income from continuing operations

11,024 5,496,566 8,213 4,095,002 8,026 4,001,764

Income from discontinuing operations – net of tax

8,313 4,144,862 (69) (34,403) 78 38,891

Net income 19,337 9,641,428 8,144 4,060,598 8,104 4,040,654

12 months period ending December 31,

Balance Sheet 2006 2007 2008

(USD mn) (Rs. Lacs) (USD mn) (Rs. Lacs) (USD mn) (Rs. Lacs)

Source of funds

Paid-up Share Capital 441 219,883 442 220,381 443 220,880

Retained Earnings 49,669 24,764,963 49,660 24,760,476 49,142 24,502,201

Others (2) 21,248 10,594,253 14,908 7,433,129 7,971 3,974,341

Net Worth 71,358 35,579,099 65,010 32,413,986 57,556 28,697,422

Minority Interest 74 36,896 114 56,840 184 91,742

Loans - Secured and Unsecured 5,546 2,765,236 7,314 3,646,760 7,963 3,970,352

Non Current Liabilities (3) 8,454 4,215,164 13,299 6,630,881 15,477 7,716,832

Total 85,432 42,596,395 85,737 42,748,468 81,180 40,476,348

Uses of funds

Net fixed Assets (4) 16,632 8,292,715 15,734 7,844,972 13,287 6,624,898

Investments 3,892 1,940,551 4,856 2,421,202 11,478 5,722,931

Other non current assets (5) 45,226 22,549,684 41,880

20,881,368 39,185

19,537,641

Net Current Assets 25,559 12,743,717 25,014 12,471,980 16,067 8,011,006

Other assets, deferred tax assets (Net)

(5,877) (2,930,272) (1,747) (871,054) 1,163 579,872

Total 85,432 42,596,395 85,737 42,748,468 81,180 40,476,348

Note: (1) Includes capitalized interest income

(2) Includes preferred stock, additional paid in capital, employee benefit trust, treasury stock, accumulated other comprehensive income / (expense)

(3) Includes pension benefit obligations, postretirement benefit obligations, other taxes payable and other noncurrent liabilities

(4) Represents fixed assets net of accumulated depreciation

(5) Includes goodwill and other identifiable intangible assets

12 months period ending December 31,

Other Financial Data 2006 2007 2008

(USD) (Rs.) (USD) (Rs.) (USD) (Rs.)

Dividend (% of Net Income) 38% 100% 106%

Earnings per Common Share – Diluted

2.66 132.55 1.17 58.52 1.20 59.86

Earnings per Common Share – Basic

2.67 133.13 1.18 58.70 1.20 60.07

Return on Net Worth (%) 28.20% 11.94% 13.22%

Book Value per Share – Diluted

9.81 489.13 9.37 467.13 8.53 425.15

Book Value per Share – Basic 9.85 491.29 9.40 468.61 8.56 426.60

17

1.6 billion in 2008

• An aggregate year-over-year increase in revenues from Pharmaceutical products launched

since 2006

• Solid aggregate performance of the balance of the broad portfolio of patent-protected

medicines.

• This was offset by the impact of loss of U.S. exclusivity on Norvasc in March 2007, Camptosar

in February 2008 and the loss of U.S. exclusivity & cessation of selling of Zyrtec/ZyrtecD in

January 2008. Norvasc, Camptosar and Zyrtec/ZyrtecD collectively experienced a decline in

revenues of about USD 2.6 billion in 2008 compared to 2007.

b) Net Income

Net income reduced by -0.5% to USD 8,104 million. This was due to the following factors:

Income from continuing operations:

• A USD 2.3 billion, pre-tax and after-tax, charge resulting from an agreement in principle with

the U.S. Department of Justice to resolve the previously reported investigation regarding

allegations of past off-label promotional practices concerning Bextra, as well as certain other

open investigations, and a USD 640 million, after-tax charge related to agreements and

agreements in principle to resolve certain non-steroidal anti-inflammatory drugs (NSAID)

litigations and claims

• Higher Acquisition-related in-process research and development charges (IPR&D). In 2008,

USD 633 million of IPR&D was incurred, pre-tax primarily related to acquisitions of Serenex,

Encysive, CovX, Coley and a number of animal health product lines from Schering-Plough, as

well as 2 smaller acquisitions also related to Animal Health, compared with IPR&D of USD 283

million, pre-tax, in 2007, primarily related to acquisitions of BioRexis Pharmaceutical Corp. and

Embrex Inc.

• Up-front payment of USD 225 million to Medivation, Inc. in connection with the collaboration

to develop and commercialize Dimebon and the up-front payment of USD 75 million to Auxilium

Pharmaceuticals, Inc. in connection with the collaboration to develop and commercialize

Xiaflex

• Higher effective income tax rate, despite the tax benefits in 2008 related to favorable effectively

settled tax issues and sale of Esperion Therapeutics, Inc.

• Lower interest income compared to 2007, due primarily to lower average net financial assets

during 2008 as compared to 2007, reflecting proceeds of USD 16.6 billion from the sale of the

Consumer Healthcare business in December 2006, and lower interest rates.

• This was partially offset by lower asset impairment charges, primarily due to USD 1.8 billion,

after-tax, in 2007 related to the decision to exit Exubera; favorable impact of foreign exchange;

savings related to cost reduction initiatives and a payment recorded in 2007 to Bristol-Myers

Squibb Company in connection with the collaboration to develop and commercialize apixaban.

Income from discontinued operations – net of tax:

• A gain of USD 78 million in 2008, compared with a loss of USD 69 million in 2007

Year ended December 2007 compared to Year ended December 2006

a) Revenues

Revenues of USD 48,418 million were essentially flat when compared to 2006 with an increase in

revenues of 0.1%. This was due to the following factors:

• The favorable impact of foreign exchange

• An aggregate year-over-year increase in revenues from Pharmaceutical products launched in

the U.S. since 2005

• Solid aggregate performance of the balance of the broad portfolio of patent-protected

medicines. This was offset by the impact of loss of U.S. exclusivity on Zoloft in August 2006

and Norvasc in March 2007; which collectively led to a decline in revenues of about USD 3.5

18

billion in 2007 compared to 2006.

• These declines were offset by an aggregate revenue increase in new products and the balance

of the portfolio of patent-protected products and alliance revenues

b) Net Income

Net income reduced by 58% to USD 8,144 million. This was due to the following factors:

Income from continuing operations:

• Higher asset impairment charges. In 2007, USD 2.8 billion was expensed pre-tax related to the

decision to exit Exubera, compared to USD 320 million pre-tax in 2006 related to the impairment

of Depo-Provera intangible asset

• Higher restructuring charges and acquisition-related costs associated with expanded cost-

reduction initiatives.

• This was partially offset by lower acquisition-related IPR&D. In 2007, IPR&D expenses of

USD 283 million, pre-tax were incurred primarily related to acquisitions of BioRexis

Pharmaceutical Corp. and Embrex Inc., compared with IPR&D of USD 835 million, pre-tax, in

2006, primarily related to acquisitions of PowderMed ltd. and Rinat Neuroscience Corp.

• Higher interest income compared to 2006, due primarily to higher net financial assets during

2007 compared to 2006, reflecting proceeds of USD 16.6 billion from the sale of the Consumer

Healthcare business and higher interest rates

• A lower effective income tax rate. In 2007, the effective tax rate on continuing operations of

11% was lower than the 15.3% in 2006, which largely reflects the tax impact of the decision to

exit Exubera in 2007, the tax impact of higher cost reduction expenditures in 2007 compared to

2006 and the volume and geographic mix of product sales in 2007 compared to 2006

Income from discontinued operations – net of tax:

• Losses of USD 69 million in 2007, compared with an income of USD 8.3 billion in 2006. This

result in 2006 was primarily due to the sale of the Consumer Healthcare business.

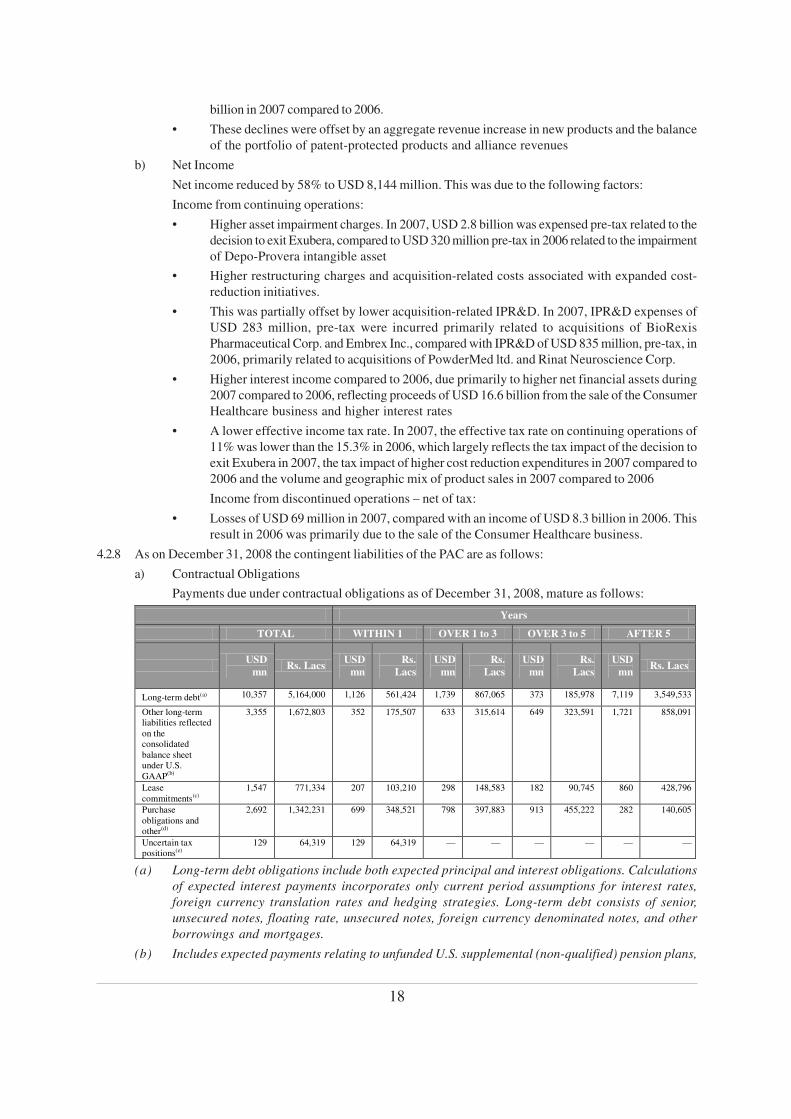

4.2.8 As on December 31, 2008 the contingent liabilities of the PAC are as follows:

a) Contractual Obligations

Payments due under contractual obligations as of December 31, 2008, mature as follows:

(a) Long-term debt obligations include both expected principal and interest obligations. Calculations

of expected interest payments incorporates only current period assumptions for interest rates,

foreign currency translation rates and hedging strategies. Long-term debt consists of senior,

unsecured notes, floating rate, unsecured notes, foreign currency denominated notes, and other

borrowings and mortgages.

(b) Includes expected payments relating to unfunded U.S. supplemental (non-qualified) pension plans,

Years

TOTAL WITHIN 1 OVER 1 to 3 OVER 3 to 5 AFTER 5

USD

mn Rs. Lacs

USD

mn

Rs.

Lacs

USD

mn

Rs.

Lacs

USD

mn

Rs.

Lacs

USD

mn Rs. Lacs

Long-term debt(a) 10,357 5,164,000 1,126 561,424 1,739 867,065 373 185,978 7,119 3,549,533

Other long-term liabilities reflected on the consolidated balance sheet under U.S. GAAP(b)

3,355 1,672,803 352 175,507 633 315,614 649 323,591 1,721 858,091

Lease commitments(c)

1,547 771,334 207 103,210 298 148,583 182 90,745 860 428,796

Purchase obligations and other(d)

2,692 1,342,231 699 348,521 798 397,883 913 455,222 282 140,605

Uncertain tax positions(e)

129 64,319 129 64,319 — — — — — —

19

postretirement plans and deferred compensation plans.

(c) Includes operating and capital lease obligations.

(d) Includes agreements to purchase goods and services that are enforceable and legally binding and

include amounts relating to advertising, information technology services, employee benefit

administration services, and potential milestone payments deemed reasonably likely to occur.

(e) Except for amounts reflected in Income taxes payable, the PAC is unable to predict the timing of tax

settlements, as tax audits can involve complex issues and the resolution of those issues may span

multiple years, particularly if subject to negotiation or litigation.

Source: Annual Report

In 2009, the PAC expects to spend approximately $1.6 billion on property, plant and equipment.

Due to significant operating cash flow, the PAC believes that it has the ability to meet its

capital investment needs and foresee no delays to planned capital expenditures.

b) Off-Balance Sheet Arrangements

In the ordinary course of business and in connection with the sale of assets and businesses,

the PAC often indemnifies its counterparties against certain liabilities that may arise in

connection with a transaction or that are related to activities prior to a transaction. These

indemnifications typically pertain to environmental, tax, employee and/or product-related

matters, and patent infringement claims. If the indemnified party were to make a successful

claim pursuant to the terms of the indemnification, the PAC would be required to reimburse

the loss. These indemnifications are generally subject to threshold amounts, specified claim

periods and other restrictions and limitations. Historically, the PAC has not paid significant

amounts under these provisions and as of December 31, 2008, recorded amounts for the

estimated fair value of these indemnifications are not significant.

Certain of the PAC’s co-promotion or license agreements gives its licensors or partners the

rights to negotiate for, or in some cases to obtain, under certain financial conditions, co-

promotion or other rights in specified countries with respect to certain of the PAC’s products.

c) Tax Contingencies

The PAC is subject to income tax in many jurisdictions and a certain degree of estimation is

required in recording the assets and liabilities related to income taxes. All of the PAC’s tax

positions are subject to audit by the local taxing authorities in each tax jurisdiction. Tax audits

can involve complex issues and the resolution of issues may span multiple years, particularly

if subject to negotiation or litigation.

The United States is one of the PAC’s major tax jurisdictions. The PAC is currently appealing

two issues related to the IRS’ audits of the PAC tax returns for the years 2002 through 2005.

The 2006, 2007 and 2008 tax years are currently under audit as part of the IRS Compliance

Assurance Process, a real-time audit process. All other tax years in the U.S. for the PAC are

closed under the statute of limitations. With respect to Pharmacia Corporation, the IRS is

currently conducting an audit for the year 2003 through the date of merger with Pfizer (April

16, 2003). In addition to the open audit years in the U.S., the PAC has open audit years in

other major tax jurisdictions, such as Canada (1998-2008), Japan (2006-2008), Europe (1996-

2008, primarily reflecting Ireland, the U.K., France, Italy, Spain and Germany) and Puerto Rico

(2004-2008).

The PAC regularly reevaluates its tax positions based on the results of audits of federal, state

and foreign income tax filings, statute of limitations expirations, and changes in tax law that

would either increase or decrease the technical merits of a position relative to the ‘more-

likely-than-not’ standard. The PAC believes that its accruals for tax liabilities are adequate for

all open years. Many factors are considered in making these evaluations, including past

history, recent interpretations of tax law, and the specifics of each matter. Because tax laws

and regulations are subject to interpretation and tax litigation is inherently uncertain, these

evaluations can involve a series of complex judgments about future events and can rely

heavily on estimates and assumptions. The PAC’s evaluations are based on estimates and

assumptions that have been deemed reasonable by management. However, if the estimates

20

and assumptions are not representative of actual outcomes, the PAC’s results could be

materially impacted.

In 2008, the PAC effectively settled certain issues common among multinational corporations

with various foreign tax authorities primarily relating to tax years 2000 to 2005. As a result, the

PAC recognized USD 305 million in tax benefits.

Because tax law is complex and often subject to varied interpretations, it is uncertain whether

some of the PAC’s tax positions will be sustained upon audit. The amounts associated with

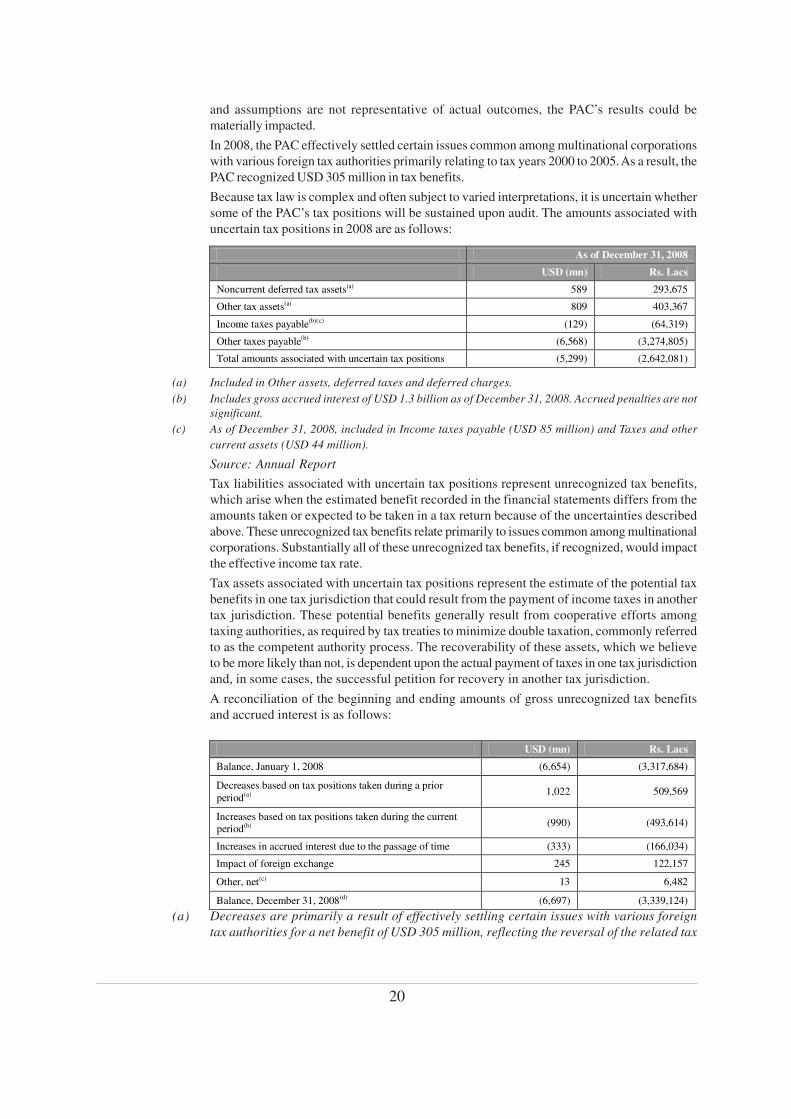

uncertain tax positions in 2008 are as follows:

(a) Included in Other assets, deferred taxes and deferred charges.

(b) Includes gross accrued interest of USD 1.3 billion as of December 31, 2008. Accrued penalties are not

significant.

(c) As of December 31, 2008, included in Income taxes payable (USD 85 million) and Taxes and other

current assets (USD 44 million).

Source: Annual Report

Tax liabilities associated with uncertain tax positions represent unrecognized tax benefits,

which arise when the estimated benefit recorded in the financial statements differs from the

amounts taken or expected to be taken in a tax return because of the uncertainties described

above. These unrecognized tax benefits relate primarily to issues common among multinational

corporations. Substantially all of these unrecognized tax benefits, if recognized, would impact

the effective income tax rate.

Tax assets associated with uncertain tax positions represent the estimate of the potential tax

benefits in one tax jurisdiction that could result from the payment of income taxes in another

tax jurisdiction. These potential benefits generally result from cooperative efforts among

taxing authorities, as required by tax treaties to minimize double taxation, commonly referred

to as the competent authority process. The recoverability of these assets, which we believe

to be more likely than not, is dependent upon the actual payment of taxes in one tax jurisdiction

and, in some cases, the successful petition for recovery in another tax jurisdiction.

A reconciliation of the beginning and ending amounts of gross unrecognized tax benefits

and accrued interest is as follows:

(a) Decreases are primarily a result of effectively settling certain issues with various foreign

tax authorities for a net benefit of USD 305 million, reflecting the reversal of the related tax

As of December 31, 2008

USD (mn) Rs. Lacs

Noncurrent deferred tax assets(a) 589 293,675

Other tax assets(a) 809 403,367

Income taxes payable(b)(c) (129) (64,319)

Other taxes payable(b) (6,568) (3,274,805)

Total amounts associated with uncertain tax positions (5,299) (2,642,081)

USD (mn) Rs. Lacs

Balance, January 1, 2008 (6,654) (3,317,684)

Decreases based on tax positions taken during a prior period(a)

1,022 509,569

Increases based on tax positions taken during the current period(b)

(990) (493,614)

Increases in accrued interest due to the passage of time (333) (166,034)

Impact of foreign exchange 245 122,157

Other, net(c) 13 6,482

Balance, December 31, 2008(d) (6,697) (3,339,124)

21

assets associated with the competent authority process

(b) Primarily included in Provision for taxes on income.

(c) Includes increases based on tax positions taken during a prior period, decreases due to

settlements with taxing authorities and decreases as a result of a lapse of the applicable

statute of limitations.

(d) In 2008, included in Income taxes payable (USD 85 million), Taxes and other current

assets (USD 44 million) and Other taxes payable (USD 6.6 billion).

Source: Annual Report

If the PAC’s estimates of unrecognized tax benefits and potential tax benefits are not

representative of actual outcomes, the PAC’s financial statements could be materially affected

in the period of settlement or when the statutes of limitations expire, as the PAC treats these

events as discrete items in the period of resolution. Finalizing audits with the relevant taxing

authorities can include formal administrative and legal proceedings and, as a result, it is

difficult to estimate the timing and range of possible change related to our uncertain tax

positions. However, any settlements or statute expirations would likely result in a significant

decrease in the PAC’s uncertain tax positions. The PAC estimates that within the next 12

months, its gross uncertain tax positions could decrease by as much as USD 200 million, as

a result of settlements with taxing authorities or the expiration of the statute of limitations.

4.2.9 Significant accounting policies of the PAC

a) Consolidation and Basis of Presentation

The consolidated financial statements include the PAC, the parent company and all subsidiaries,

including those operating outside the U.S., and are prepared in accordance with accounting principles

generally accepted in the United States of America (U.S. GAAP). The consolidation decision requires

consideration of majority voting interests, as well as effective economic or other control. For

subsidiaries operating outside the U.S., the financial information is included as of and for the year

ended November 30 for each year presented. Substantially all unremitted earnings of international

subsidiaries are free of legal and contractual restrictions. All significant transactions among the

businesses have been eliminated.

b) New Accounting Standards

Financial Instruments—Fair Value—As of January 1, 2008, the PAC adopted on a prospective basis

certain required provisions of SFAS No. 157, Fair Value Measurements. Those provisions relate to

its financial assets and liabilities carried at fair value and its fair value disclosures related to financial

assets and liabilities. SFAS No. 157, as amended, defines fair value, expands related disclosure

requirements and specifies a hierarchy of valuation techniques based on the nature of the inputs

used to develop the fair value measures. Fair value is defined as the price that would be received to

sell an asset or paid to transfer a liability in an orderly transaction between market participants at the

measurement date. There are three levels of inputs to fair value measurements—Level 1, meaning the

use of quoted prices for identical instruments in active markets; Level 2, meaning the use of quoted

prices for similar instruments in active markets or quoted prices for identical or similar instruments in

markets that are not active or are directly or indirectly observable; and Level 3, meaning the use of

unobservable inputs. Observable market data should be used when available.

Many, but not all, of the PAC’s financial instruments are carried at fair value. For example, substantially

all of its cash equivalents, short-term investments and long-term investments are classified as

available-for-sale securities and are carried at fair value, with unrealized gains and losses, net of tax,

reported in Other comprehensive income/(expense). Derivative financial instruments are carried at

fair value in various balance sheet categories, with changes in fair value reported in current earnings

or deferred on qualifying hedging relationships. Virtually all of its valuation measurements use Level

2 inputs. The adoption of SFAS No. 157, as amended, did not have a significant impact on the

consolidated financial statements. As of January 1, 2008, the PAC did not elect to adopt SFAS No.