Embed Size (px)

Citation preview

© Euromonitor International

1

PET CARE MARKET: TRENDS AND OPPORTUNITIES

NATIONAL PET INDUSTRY TRADE SHOW TORONTO, SEPTEMBER 19, 2011

© Euromonitor International

2

GLOBAL PET CARE MARKET OVERVIEW: 2011 AND BEYOND

NORTH AMERICA OVERVIEW: LOOK AT US AND CANADA

PRODUCT DEVELOPMENT TRENDS AND OPPORTUNITIES

LOOKING BEYOND RETAIL

© Euromonitor International

3

GLOBAL PET CARE MARKET OVERVIEW: 2011 AND BEYOND

© Euromonitor International

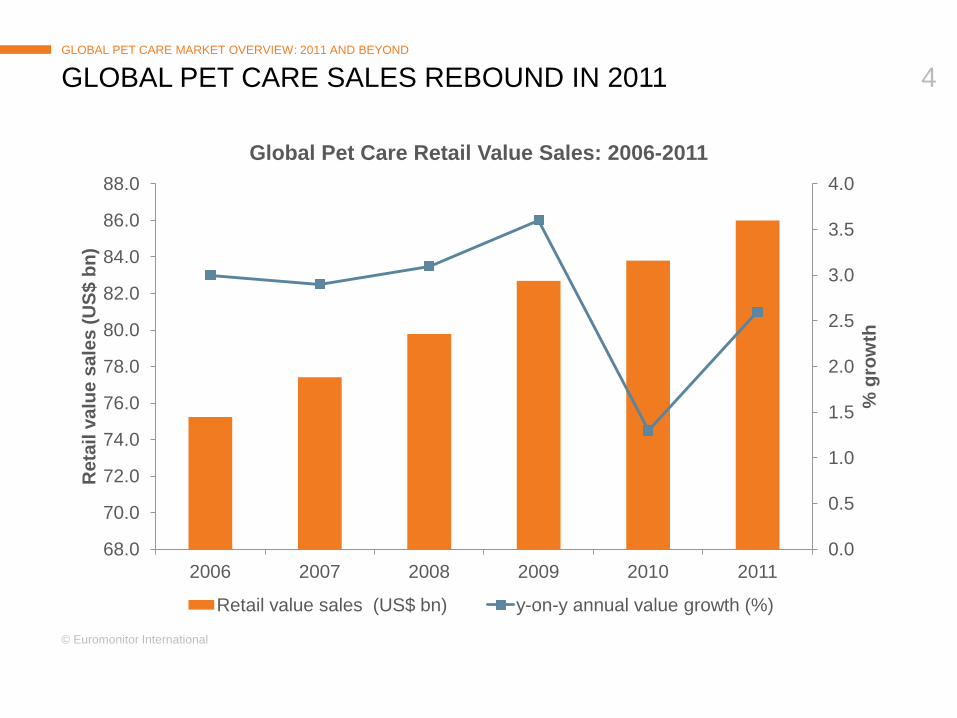

4

GLOBAL PET CARE SALES REBOUND IN 2011

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

68.0

70.0

72.0

74.0

76.0

78.0

80.0

82.0

84.0

86.0

88.0

2006 2007 2008 2009 2010 2011

% g

row

th

Ret

ail v

alue

sal

es (U

S$ b

n)

Global Pet Care Retail Value Sales: 2006-2011

Retail value sales (US$ bn) y-on-y annual value growth (%)

GLOBAL PET CARE MARKET OVERVIEW: 2011 AND BEYOND

© Euromonitor International

5

KEY GROWTH SEGMENTS – PREMIUM FOOD, TREATS, HEALTHCARE

0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0 9.0

0.0 2.0 4.0 6.0 8.0

10.0 12.0 14.0 16.0

% C

AGR

Ret

ail v

alue

sal

es (U

S$ b

n)

Global Pet Care Retail Value Sales: 2006-2011

Retail value sales (US$ bn) % CAGR 2006-11

GLOBAL PET CARE MARKET OVERVIEW: 2011 AND BEYOND

Average market growth – 2.7% CAGR

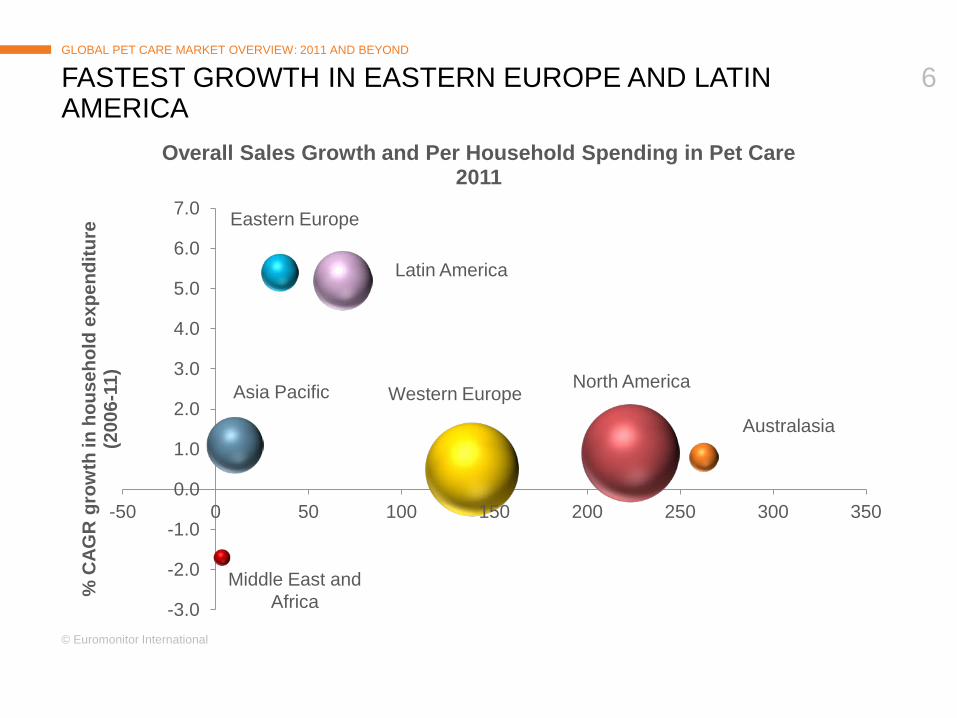

© Euromonitor International

6

FASTEST GROWTH IN EASTERN EUROPE AND LATIN AMERICA

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

-50 0 50 100 150 200 250 300 350

% C

AGR

gro

wth

in h

ouse

hold

exp

endi

ture

(2

006-

11)

Overall Sales Growth and Per Household Spending in Pet Care 2011

Australasia

North America Western Europe

Latin America

Eastern Europe

GLOBAL PET CARE MARKET OVERVIEW: 2011 AND BEYOND

Asia Pacific

Middle East and Africa

© Euromonitor International

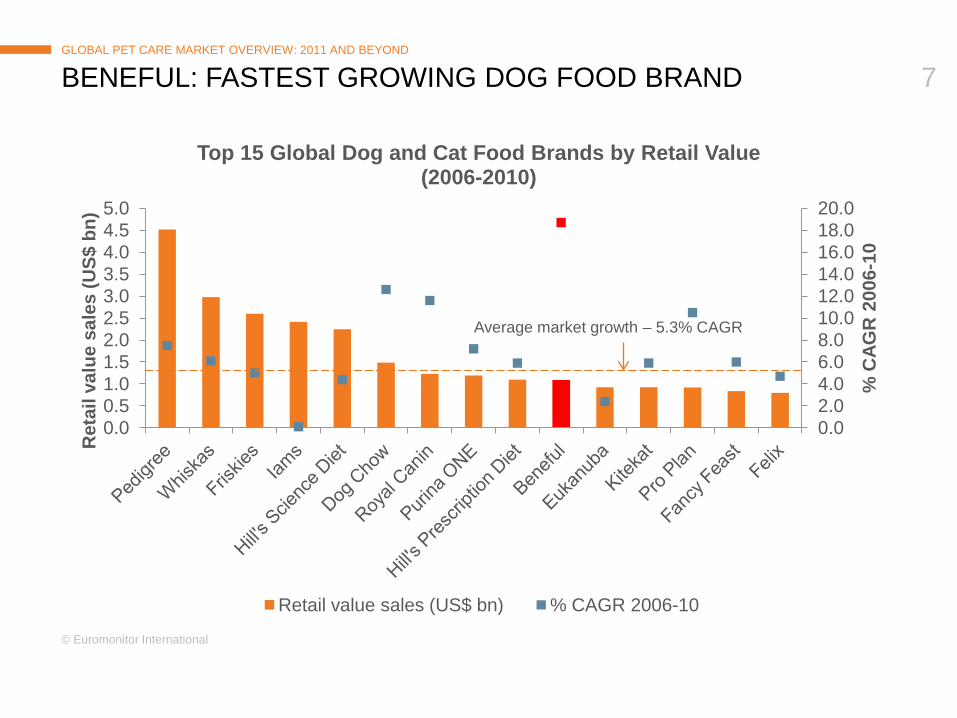

7

BENEFUL: FASTEST GROWING DOG FOOD BRAND

0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0 16.0 18.0 20.0

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0

% C

AGR

200

6-10

Ret

ail v

alue

sal

es (U

S$ b

n)

Top 15 Global Dog and Cat Food Brands by Retail Value (2006-2010)

Retail value sales (US$ bn) % CAGR 2006-10

GLOBAL PET CARE MARKET OVERVIEW: 2011 AND BEYOND

Average market growth – 5.3% CAGR

© Euromonitor International

8

0

0.5

1

1.5

2

2.5

3

3.5

75.00

80.00

85.00

90.00

95.00

100.00

2011 2012 2013 2014 2015 2016

Year

-on-

year

gro

wth

%

US$

bill

ion

(fixe

d ex

chan

ge ra

te)

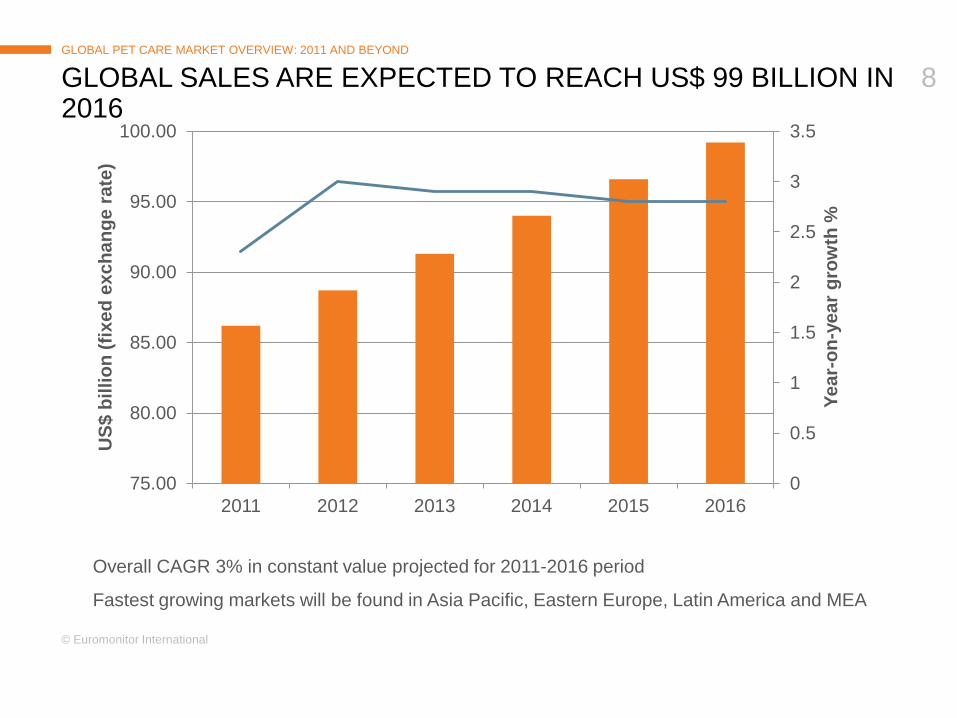

Overall CAGR 3% in constant value projected for 2011-2016 period

Fastest growing markets will be found in Asia Pacific, Eastern Europe, Latin America and MEA

GLOBAL SALES ARE EXPECTED TO REACH US$ 99 BILLION IN 2016

GLOBAL PET CARE MARKET OVERVIEW: 2011 AND BEYOND

© Euromonitor International

9

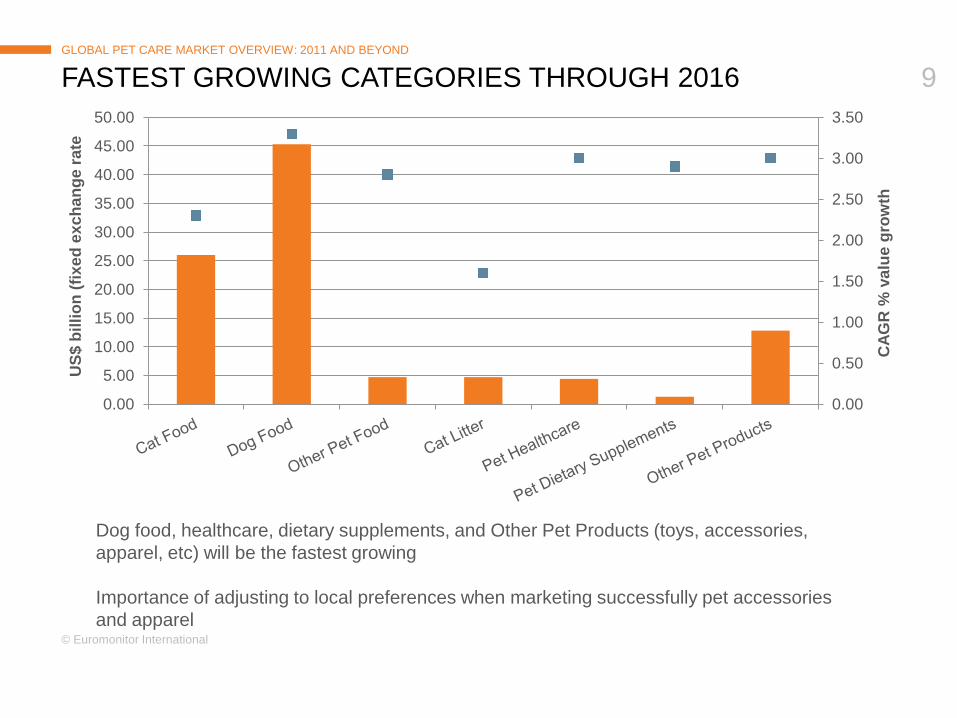

FASTEST GROWING CATEGORIES THROUGH 2016 GLOBAL PET CARE MARKET OVERVIEW: 2011 AND BEYOND

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

50.00

CAG

R %

val

ue g

row

th

US$

bill

ion

(fixe

d ex

chan

ge ra

te

Dog food, healthcare, dietary supplements, and Other Pet Products (toys, accessories, apparel, etc) will be the fastest growing Importance of adjusting to local preferences when marketing successfully pet accessories and apparel

© Euromonitor International

10

PREMIUM DOG AND CAT FOOD IS EXPECTED TO SEE THE FASTEST GROWTH THROUGH 2016

GLOBAL PET CARE MARKET OVERVIEW: 2011 AND BEYOND

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

0.00

5.00

10.00

15.00

20.00

25.00

30.00

Economy Dog and Cat Food

Mid-Priced Dog and Cat Food

Premium Dog and Cat Food

CA

GR

% g

row

th 2

011-

2016

US

$ bi

llion

(fix

ed e

xcha

nge

rate

)

Dog and cat food growth by price platform

Retail sales of premium dog and cat food are expected to surpass US$27 billion

Demand for economy food will be supported by emerging economies

© Euromonitor International

11

NORTH AMERICA OVERVIEW: LOOK AT US AND CANADA

© Euromonitor International

12

NORTH AMERICA OVERVIEW 2011 NORTH AMERICA OVERVIEW: LOOK AT US AND CANADA\

0

1

2

3

4

5

6

7

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

2006 2007 2008 2009 2010 2011

Y-on

-y g

row

th %

US$

bill

ion

(fixe

d ex

chan

ge ra

te

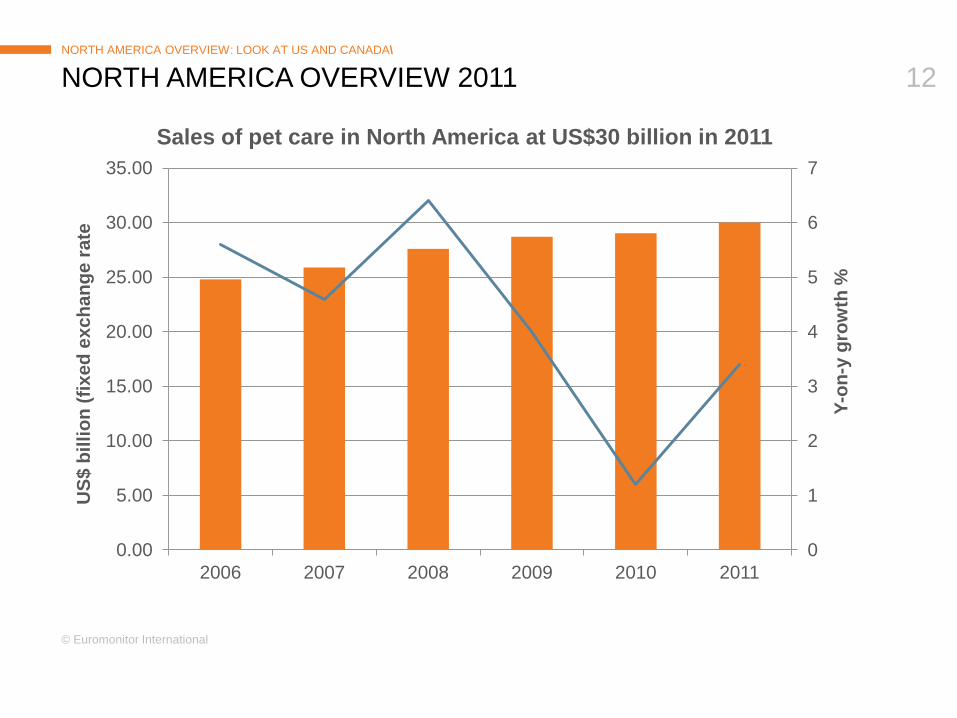

Sales of pet care in North America at US$30 billion in 2011

© Euromonitor International

13

NORTH AMERICA OVERVIEW 2011 NORTH AMERICA OVERVIEW: LOOK AT US AND CANADA

3.6

3.7

3.8

3.9

4

4.1

4.2

4.3

4.4

4.5

0.00

0.50

1.00

1.50

2.00

2.50

3.00

2006 2007 2008 2009 2010 2011

Yea-

on-y

ear g

row

th %

US$

bill

ion

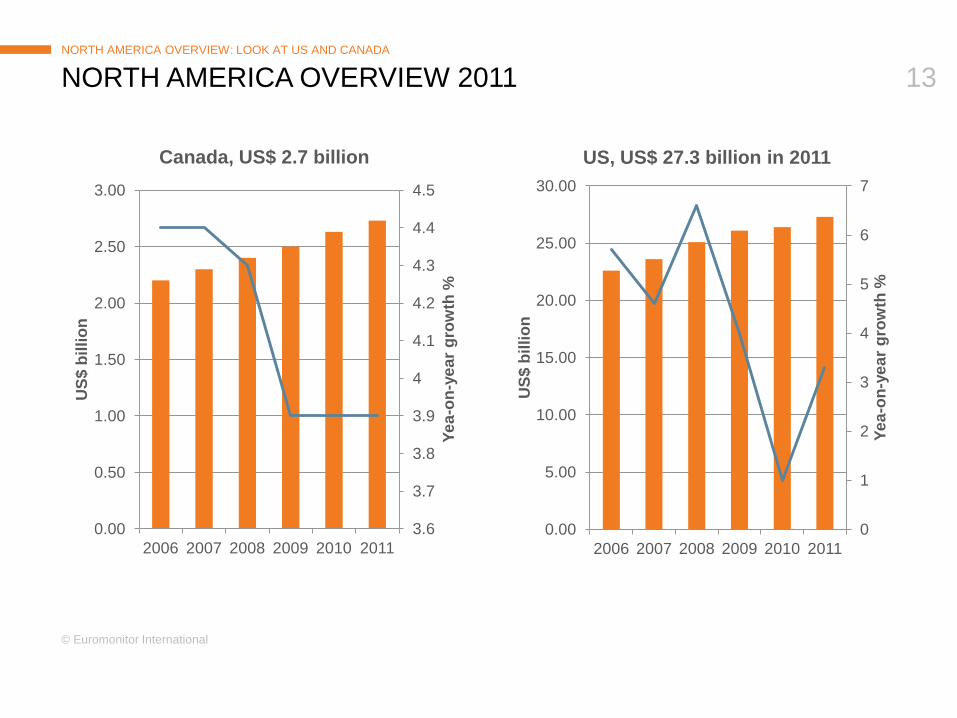

Canada, US$ 2.7 billion

0

1

2

3

4

5

6

7

0.00

5.00

10.00

15.00

20.00

25.00

30.00

2006 2007 2008 2009 2010 2011

Yea-

on-y

ear g

row

th %

US$

bill

ion

US, US$ 27.3 billion in 2011

© Euromonitor International

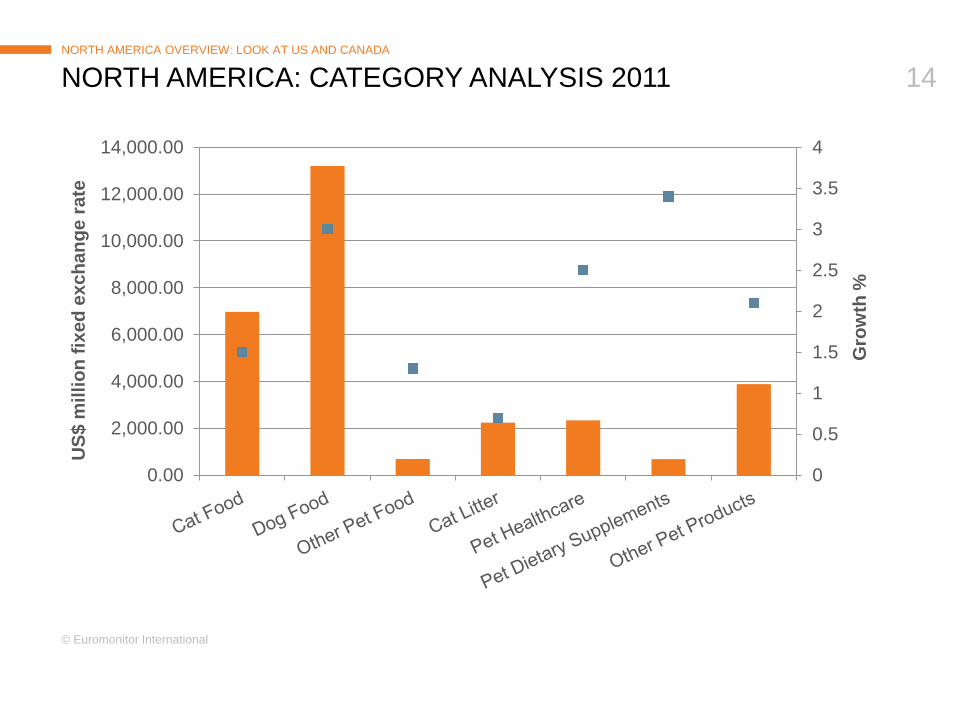

14

NORTH AMERICA: CATEGORY ANALYSIS 2011 NORTH AMERICA OVERVIEW: LOOK AT US AND CANADA

0

0.5

1

1.5

2

2.5

3

3.5

4

0.00

2,000.00

4,000.00

6,000.00

8,000.00

10,000.00

12,000.00

14,000.00

Gro

wth

%

US$

mill

ion

fixed

exc

hang

e ra

te

© Euromonitor International

15

NORTH AMERICA: LOOK AHEAD NORTH AMERICA OVERVIEW: LOOK AT US AND CANADA

1

2

3

4

28,000.00

29,000.00

30,000.00

31,000.00

32,000.00

33,000.00

34,000.00

35,000.00

36,000.00

2012 2013 2014 2015 2016

CAG

R %

gro

wth

US$

mill

ion

fixed

exc

hang

e ra

te

North America, US$ 35 billion in 2016

© Euromonitor International

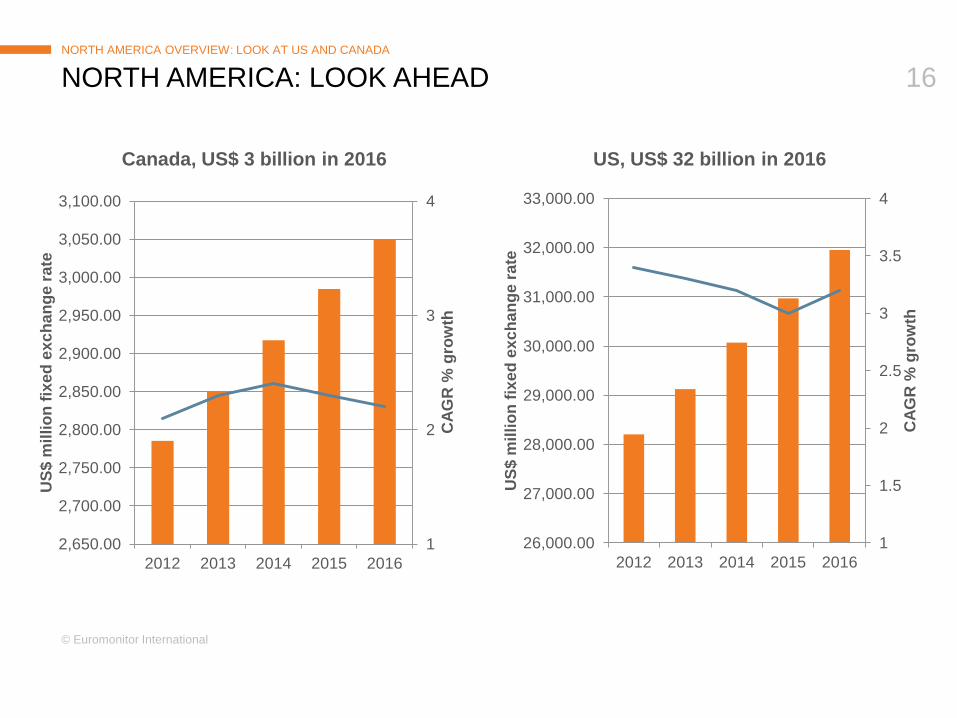

16

NORTH AMERICA: LOOK AHEAD NORTH AMERICA OVERVIEW: LOOK AT US AND CANADA

1

2

3

4

2,650.00

2,700.00

2,750.00

2,800.00

2,850.00

2,900.00

2,950.00

3,000.00

3,050.00

3,100.00

2012 2013 2014 2015 2016

CAG

R %

gro

wth

US$

mill

ion

fixed

exc

hang

e ra

te

Canada, US$ 3 billion in 2016

1

1.5

2

2.5

3

3.5

4

26,000.00

27,000.00

28,000.00

29,000.00

30,000.00

31,000.00

32,000.00

33,000.00

2012 2013 2014 2015 2016

CAG

R %

gro

wth

US$

mill

ion

fixed

exc

hang

e ra

te

US, US$ 32 billion in 2016

© Euromonitor International

17

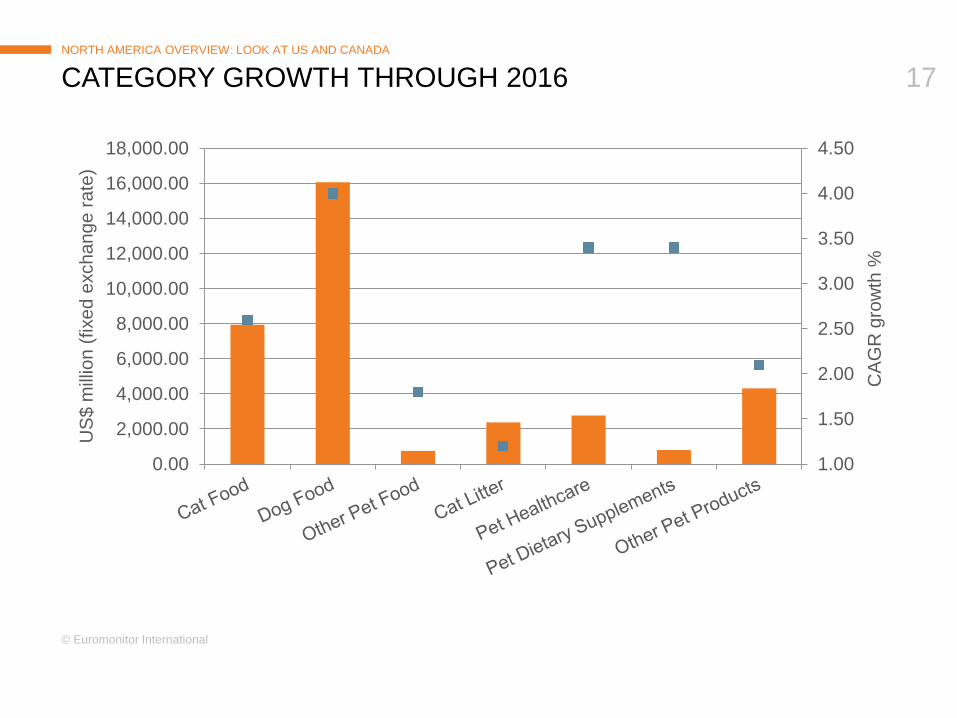

CATEGORY GROWTH THROUGH 2016 NORTH AMERICA OVERVIEW: LOOK AT US AND CANADA

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

0.00

2,000.00

4,000.00

6,000.00

8,000.00

10,000.00

12,000.00

14,000.00

16,000.00

18,000.00

CA

GR

gro

wth

%

US

$ m

illio

n (fi

xed

exch

ange

rate

)

© Euromonitor International

18

NORTH AMERICA: DOG AND CAT FOOD BY PRICE PLATFORM NORTH AMERICA OVERVIEW: LOOK AT US AND CANADA

0.00

2,000.00

4,000.00

6,000.00

8,000.00

10,000.00

12,000.00

14,000.00

Economy Dog and Cat Food

Mid-Priced Dog and Cat Food

Premium Dog and Cat Food

US$

mill

ion

fixed

exc

hang

e ra

te

2011 2016 While in Canada, mid-priced food accounts for the larger portion of sales in actual value and volume, in the US products positioned as premium significantly outsell mid-priced category Strong presence of natural and organic pet food products in the US feeds growth of premium category Economy segment is pose for decline in both Canada and the US, but the rate of decline is slower in the US

© Euromonitor International

19

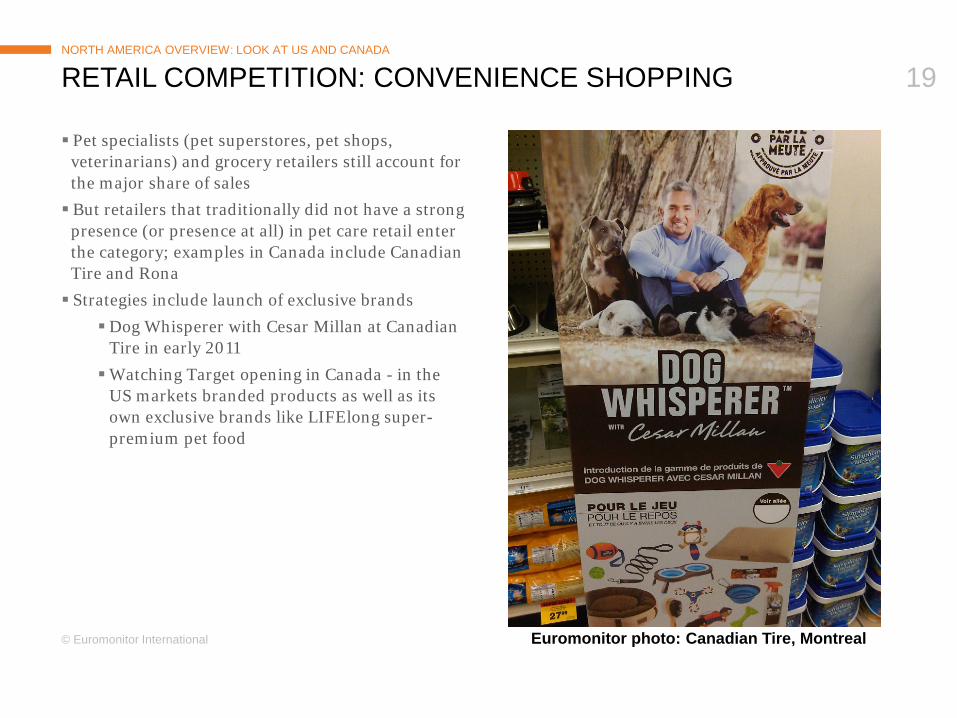

RETAIL COMPETITION: CONVENIENCE SHOPPING

Pet specialists (pet superstores, pet shops, veterinarians) and grocery retailers still account for the major share of sales But retailers that traditionally did not have a strong

presence (or presence at all) in pet care retail enter the category; examples in Canada include Canadian Tire and Rona Strategies include launch of exclusive brands

Dog Whisperer with Cesar Millan at Canadian Tire in early 2011 Watching Target opening in Canada - in the

US markets branded products as well as its own exclusive brands like LIFElong super-premium pet food

NORTH AMERICA OVERVIEW: LOOK AT US AND CANADA

Euromonitor photo: Canadian Tire, Montreal

© Euromonitor International

20

PRODUCT DEVELOPMENT: TRENDS AND OPPORTUNITIES

© Euromonitor International

21

INNOVATION TRENDS

Humanisation and

premiumisation

All natural/ organic/raw

food

Weight Management

Fortified and Functional

Convenience, functionality,

2-in-1

Sustainability

PRODUCT DEVELOPMENT: TRENDS AND OPPORTUNITIES

© Euromonitor International

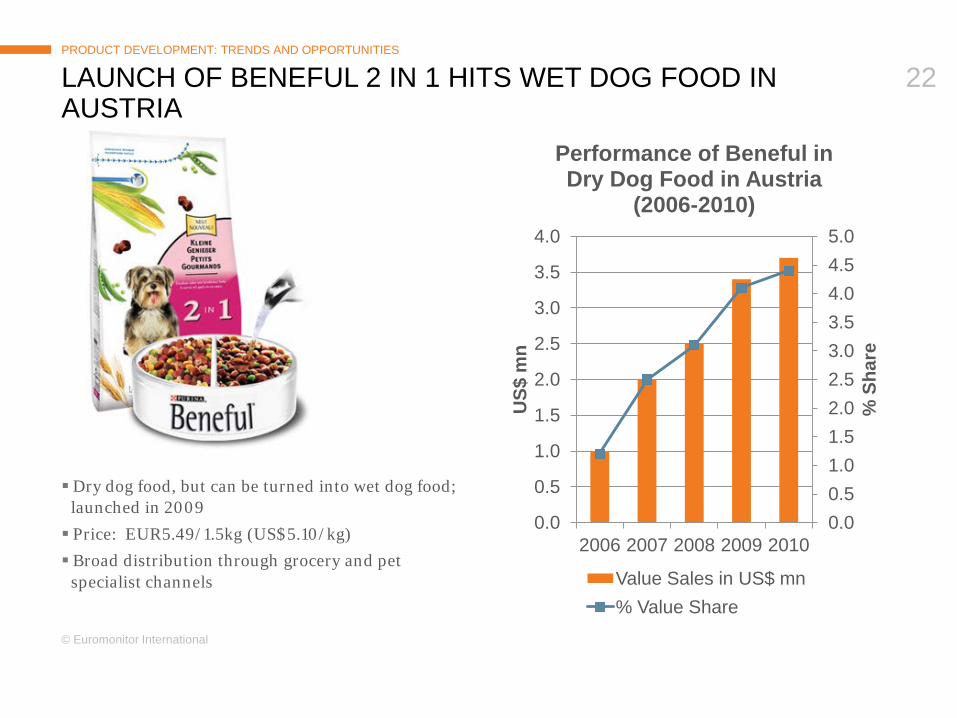

22

LAUNCH OF BENEFUL 2 IN 1 HITS WET DOG FOOD IN AUSTRIA

Dry dog food, but can be turned into wet dog food;

launched in 2009 Price: EUR5.49/1.5kg (US$5.10/kg) Broad distribution through grocery and pet

specialist channels

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2006 2007 2008 2009 2010

% S

hare

US$

mn

Performance of Beneful in Dry Dog Food in Austria

(2006-2010)

Value Sales in US$ mn % Value Share

PRODUCT DEVELOPMENT: TRENDS AND OPPORTUNITIES

© Euromonitor International

23

OTHER SIMILAR 2-IN-1 PRODUCTS

Product: Dry mid-priced dog food

Launch date: In mid-2010

Price: EUR 7.90/3 kg (US$3.68/kg)

Distribution: Broad distribution through grocery and pet specialist channels

Finland: Friskies 2 in 1 by Nestlé Purina

Product: Dry mid-priced cat food Launch date: Feb 2011 Price: R10.30/1kg (US$6.52/kg) Distribution: Broad distribution through grocery

and pet specialist channels

Brazil: Max 2 in 1 by Total Alimentos

PRODUCT DEVELOPMENT: TRENDS AND OPPORTUNITIES

© Euromonitor International

24

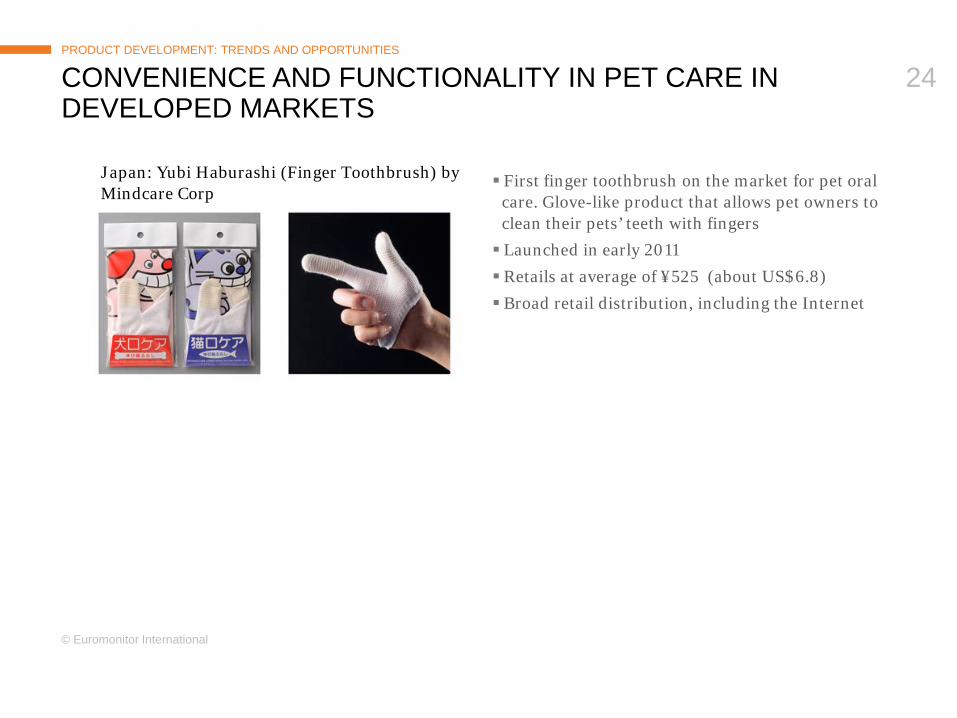

CONVENIENCE AND FUNCTIONALITY IN PET CARE IN DEVELOPED MARKETS

Japan: Yubi Haburashi (Finger Toothbrush) by Mindcare Corp

First finger toothbrush on the market for pet oral care. Glove-like product that allows pet owners to clean their pets’ teeth with fingers Launched in early 2011 Retails at average of ¥525 (about US$6.8) Broad retail distribution, including the Internet

PRODUCT DEVELOPMENT: TRENDS AND OPPORTUNITIES

© Euromonitor International

25

NATURAL AND ORGANIC PRODUCTS MOVE TO MAINSTREAM PRODUCT DEVELOPMENT: TRENDS AND OPPORTUNITIES

Whiskas Organic by Mars Inc (Sweden, 2010) - Wet cat food made with meat and vegetables sourced from controlled organic farming; marketed as suitable for the fussiest cats; packed in sealed foil pouches

Original Pet Food Co Organic Beef (US, 2011) - Line of wet dog food made from organic grass-fed beef, high in omega-3 fatty acids and conjugated linoleic acid

Bioplan by Fressnapf (Germany, 2009/2010) - an extensive range of dog and cat nutrition, made with 100% organic ingredients. Bioplan is marketed as a balanced, agreeable, light, and easy to digest organic animal food

© Euromonitor International

26

ORGANIC AND NATURAL TREND EXTENDS TO PET CARE PRODUCTS

PRODUCT DEVELOPMENT: TRENDS AND OPPORTUNITIES

Yarrah Organic Cat Litter by Yarrah Bio Petfood (Netherlands, 2010) - Yarrah Bio has expanded into organic/bio cat litter in response to growing consumer demand for natural and organic products for pets

Imperial Care by Geohellas S.A (Greece, 2011) - Natural, ultra compact clumping cat litter made of white clay. It is enriched with fresh baby powder scent which is released every time the cat uses the tray

Biogance by Laboratoire Biogance SA (Spain, 2010) - Waterless shampoo for cats made of natural and organic ingredients. Free from paraben, colourant, and detergent. Dry shampoo for convenience

© Euromonitor International

27

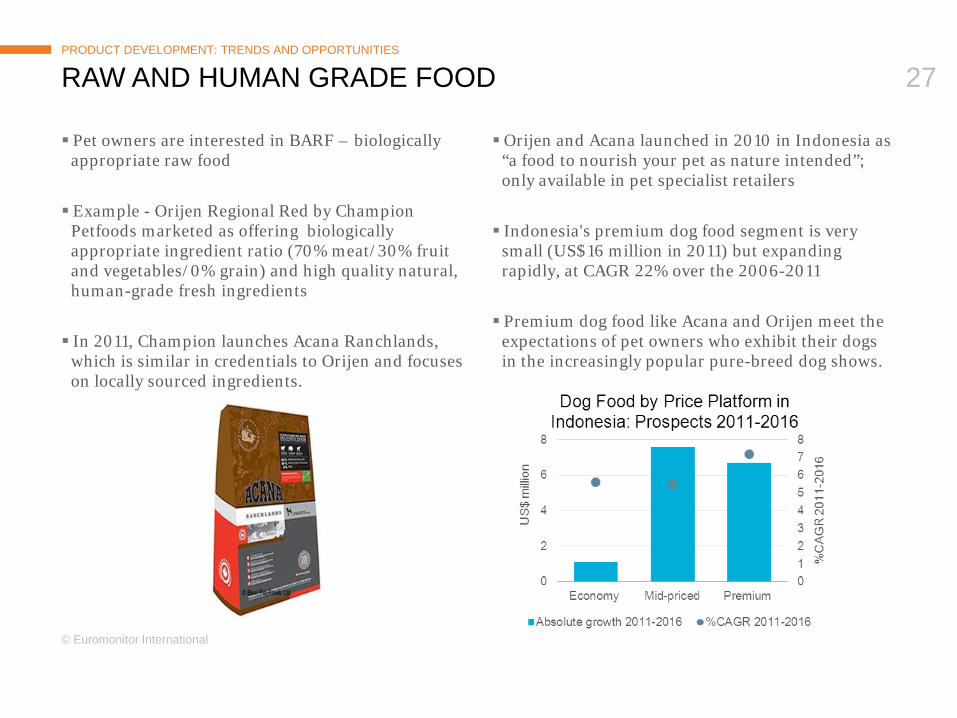

RAW AND HUMAN GRADE FOOD

Pet owners are interested in BARF – biologically appropriate raw food Example - Orijen Regional Red by Champion

Petfoods marketed as offering biologically appropriate ingredient ratio (70% meat/30% fruit and vegetables/0% grain) and high quality natural, human-grade fresh ingredients

In 2011, Champion launches Acana Ranchlands,

which is similar in credentials to Orijen and focuses on locally sourced ingredients.

Orijen and Acana launched in 2010 in Indonesia as “a food to nourish your pet as nature intended”; only available in pet specialist retailers Indonesia's premium dog food segment is very

small (US$16 million in 2011) but expanding rapidly, at CAGR 22% over the 2006-2011 Premium dog food like Acana and Orijen meet the

expectations of pet owners who exhibit their dogs in the increasingly popular pure-breed dog shows.

PRODUCT DEVELOPMENT: TRENDS AND OPPORTUNITIES

© Euromonitor International

28

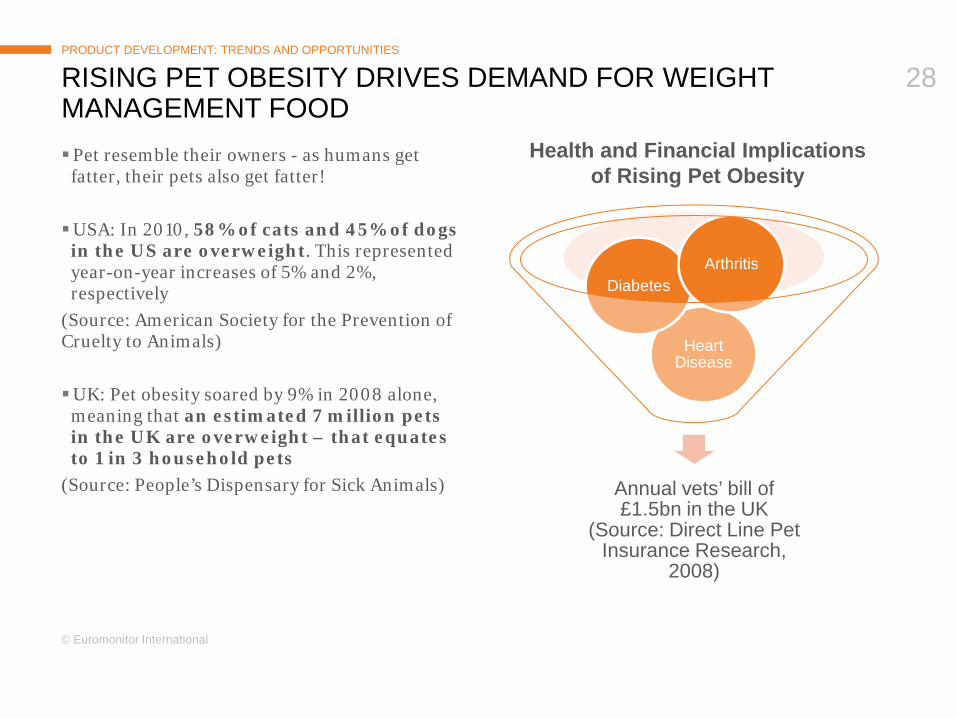

RISING PET OBESITY DRIVES DEMAND FOR WEIGHT MANAGEMENT FOOD Pet resemble their owners - as humans get

fatter, their pets also get fatter! USA: In 2010, 58% of cats and 45% of dogs

in the US are overweight. This represented year-on-year increases of 5% and 2%, respectively

(Source: American Society for the Prevention of Cruelty to Animals)

UK: Pet obesity soared by 9% in 2008 alone,

meaning that an estimated 7 million pets in the UK are overweight – that equates to 1 in 3 household pets

(Source: People’s Dispensary for Sick Animals)

Annual vets’ bill of £1.5bn in the UK

(Source: Direct Line Pet Insurance Research,

2008)

Heart Disease

Diabetes Arthritis

PRODUCT DEVELOPMENT: TRENDS AND OPPORTUNITIES

Health and Financial Implications of Rising Pet Obesity

© Euromonitor International

29

WEIGHT MANAGEMENT: PORTION CONTROL PRODUCTS PRODUCT DEVELOPMENT: TRENDS AND OPPORTUNITIES

Hill’s Science Diet Weight Loss System by Colgate Palmolive (USA) - Launched in Jan 2011 - This line consists of individually wrapped pre-measured

portions of food and treat. - Available in two sizes: small and medium to large breed - By taking the guesswork out of portion control, the Weight

Loss System makes it easy for owners to help their pets lose weight

Price: Retail at US$63.99 for a starter kit for medium dogs containing 66 food packs and 60 treat packs Distribution: Available through pet specialists and veterinary clinics

© Euromonitor International

30

PRODUCTS WITH FUNCTIONAL INGREDIENTS PRODUCT DEVELOPMENT: TRENDS AND OPPORTUNITIES

Purina One Actilea by Nestlé SA (Italy, 2010) - Actilea is based on three active ingredients (prebiotics, antioxidants and yeast) and it claims to support the cat's immune response and digestive system

Royal Canin Veterinary Diet – Mobility by Mars Inc (Sweden, 2010) - Dry formula for adult cats with or at risk of developing osteoarthritis; fortified with Joint Complex Plus from New Zealand green mussel and omega-3

ProBiotic Live by Bacterfield International (Luxembourg, 2011) - Dry dog food fortified with 109 live and highly concentrated probiotic bacteria for a healthy gut and strong immune system

Whiskas Salmon Pockets by Thien An JSC (Mars Inc), (Vietnam, 2010) -Premium dry cat food with taurine, Vitamin A, calcium, phosphorus, Omega 3 & 6

© Euromonitor International

31

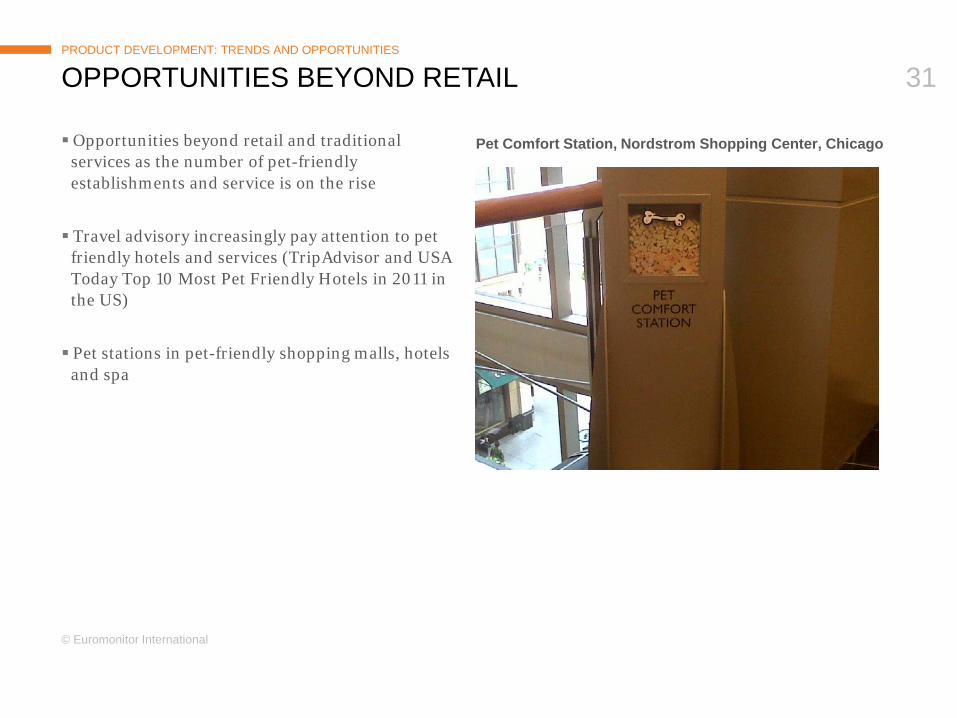

OPPORTUNITIES BEYOND RETAIL

Opportunities beyond retail and traditional services as the number of pet-friendly establishments and service is on the rise Travel advisory increasingly pay attention to pet

friendly hotels and services (TripAdvisor and USA Today Top 10 Most Pet Friendly Hotels in 2011 in the US) Pet stations in pet-friendly shopping malls, hotels

and spa

PRODUCT DEVELOPMENT: TRENDS AND OPPORTUNITIES

Pet Comfort Station, Nordstrom Shopping Center, Chicago

© Euromonitor International

32

SUMMARY

Products Focus on premium in food, but

there is room for value products Natural and sustainable (in all

their variations and product categories) Convenience and functionality

in pet care

Looking beyond retail Expanding array of pet friendly

locations creates possibilities for suppliers of pet food and pet care Use of online sources and social

network sites to identify underserved and growing niches

Retail Distribution Convenience shopping adds to

competition as new retailers seek share of dollar spending in pet retail Opportunities exist in the

development of exclusive brands and retail brands

PRODUCT DEVELOPMENT: TRENDS AND OPPORTUNITIES

THANK YOU FOR LISTENING Svetlana Uduslivaia Senior Research Analyst Euromonitor International Chicago 1-312-922-1115 ext 8302 E-mail: [email protected]