Embed Size (px)

Citation preview

OTC Derivatives Reforms: Considerations and Challenges

ESRC Conference on Diversity in MacroeconomicsMark Manning, Reserve Bank of Australia

Overview

• Policy motivation

• An initial contribution

− Methodology

− Exposures and collateral demands

− Financial stability under different clearing

structures

• Policy messages and future work

Policy Motivation

• Fundamental changes to core financial markets

− G20 financial reform agenda

− Strengthen risk management; reduce

interconnectedness

• Collateralisation and central clearing

− Trade-off between counterparty risk and liquidity

risk

− Encumbrance; funding and liquidity

• Assess implications for stability, market functioning

and real economic outcomes

Initial Contribution

• OTC Derivatives: Netting and Networks

− Joint work with Alex Heath and Gerard Kelly

• Simulation approach

− Static: Exposures and collateral demands

− Dynamic: Financial stability

• Flexible, but stylised

• Can examine a variety of clearing structures

• Stylised ‘world’: network structure; balance

sheets

Links to Literature

• Duffie and Zhu (2011)

− Model dealer exposures in alternative clearing

settings; consider fragmentation and un-netting

• Macroeconomic Assessment Group on Derivatives

(2013)

− Examine costs/benefits of G20 reforms: net long-

run impact on GDP

• Duffie (2014)

− Model collateral demand in alternative clearing

settings using bilateral CDS exposure data

Basic set-up

• Two agent types: banks (b) and investors (i)

• Core/Periphery network structure

• Draw derivative positions from a transaction matrix

Static Analysis: Exposure and Collateral

• Bilateral clearing:

• Central clearing, single CCP:

• Central clearing, separate CCPs:

• Mixed clearing:

• Split clearing: and

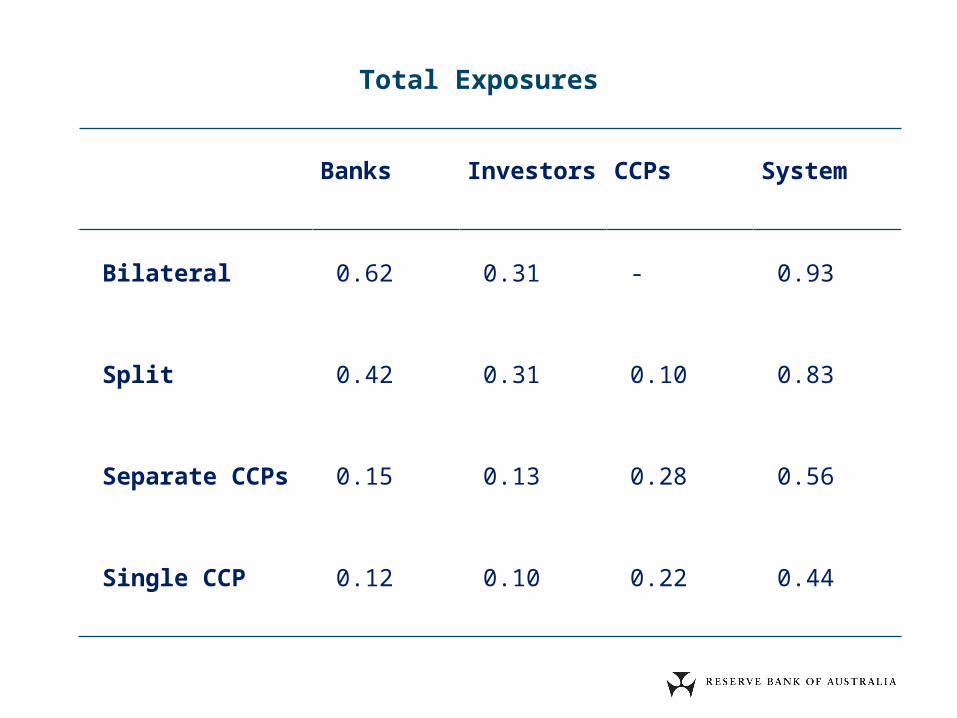

Banks Investors CCPs System

Bilateral 0.62 0.31 - 0.93

Split 0.42 0.31 0.10 0.83

Separate CCPs 0.15 0.13 0.28 0.56

Single CCP 0.12 0.10 0.22 0.44

Total Exposures

Changing the Size of the CoreExposure relative to notional outstanding

2 4 6 8 10 120

1

2

3

4

5

0

1

2

3

4

5

Number of banks

Single CCP

%

Separate CCPs

Bilateral

Split clearing

%

Changing the Directionality of the PeripheryExposure relative to notional outstanding

0 6 12 18 24 300

1

2

3

4

5

0

1

2

3

4

5

Number of directional investors

Single CCP

%

Separate CCPs

Bilateral

%

Dynamic Analysis: Networks (1)

Previous model extended by giving agents balance

sheets

• Banks and investors hold a composite ‘illiquid

asset’

• Can be sold/transformed into a ‘liquid asset’ to

meet collateral needs

• Liabilities comprise debt and equity for banks and

equity only for investors

− Both banks and investors can default due to

illiquidity; banks can also default due to

insolvency

Dynamic Analysis: Networks (2)

Models the dynamic interaction between derivative

exposure and other balance sheet items under

alternative clearing arrangements

• Focus is on how price shocks are transmitted to

balance sheets and how they may trigger liquidity

shortages or defaults

• Examines also the dynamics of collateral

transformation

Simulation and Timeline

Monte Carlo simulation with 70 000 iterations. Seven

steps:

• Populate transaction matrix

• Draw illiquid asset price change

• Draw derivative price change

• Calculate variation margin payment obligations

• Sell/transform illiquid assets to obtain liquidity for

variation margin payments; could trigger default

• Default could impose losses on others

• Update balance sheets

Bank Default and Collateral CoverageExpected number of defaults

Bilateral

50.00 69.15 84.13 93.32 97.72 99.38 99.87 99.985

6

7

8

9

10

5

6

7

8

9

10

Coverage level (%)

Mixed clearing

Single CCP

No No

Policy Messages

• The appropriate scope of central clearing and

collateralisation will depend on product and agent

characteristics

• There is likely to be an ‘optimal’ level of

collateralisation, which will vary with the structure

of clearing arrangements

Future Work

• Economic significance of the results

− Take the model to ‘real’ data

• Add richness to banks’ and investors’ balance

sheets

• Endogenise pricing and agents’ trading choices

![[ESRC][K55]TankGame Project](https://img.pdfslide.us/doc/110x75/577cd6c01a28ab9e789d27bf/esrck55tankgame-project.jpg)

![ESRC Report [English]](https://img.pdfslide.us/doc/110x75/577d1fa91a28ab4e1e910c34/esrc-report-english.jpg)