Embed Size (px)

Citation preview

Copyright HDC 2012

Presentation to:

Potential Business Partners, New Zealand

Opportunities in Halal Economy

13.07.2012

Content

1. Understanding the Concept of Halal and Thoyyib

2. Why Halal Industry?

3. Food Security Issues as a Driver of the Global Halal Market

4. Business Opportunities

2

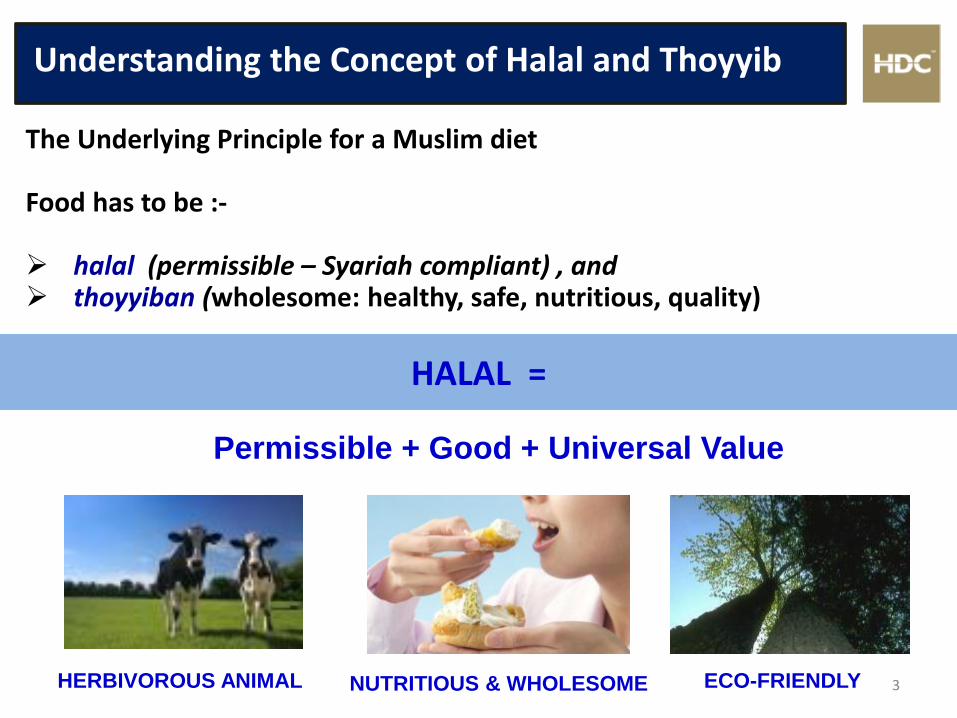

Understanding the Concept of Halal and Thoyyib

3

The Underlying Principle for a Muslim diet Food has to be :- halal (permissible – Syariah compliant) , and thoyyiban (wholesome: healthy, safe, nutritious, quality)

HALAL =

Permissible + Good + Universal Value

NUTRITIOUS & WHOLESOME HERBIVOROUS ANIMAL ECO-FRIENDLY

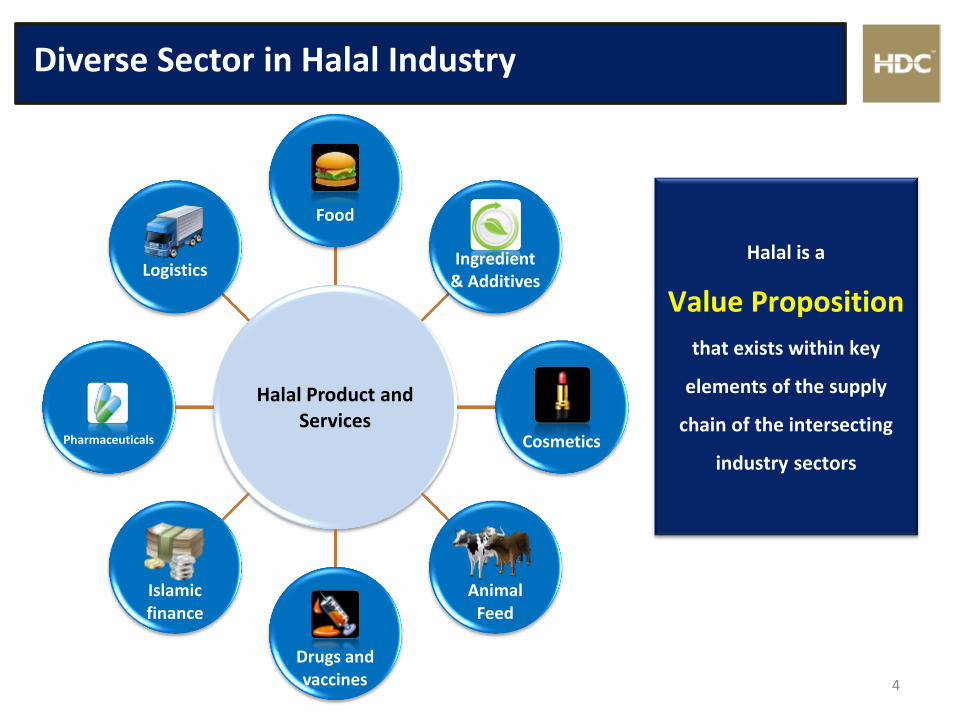

Diverse Sector in Halal Industry

Halal Product and Services

Food

Ingredient & Additives

Cosmetics

Animal Feed

Drugs and vaccines

Islamic finance

Pharmaceuticals

Logistics

Halal is a

Value Proposition

that exists within key

elements of the supply

chain of the intersecting

industry sectors

4

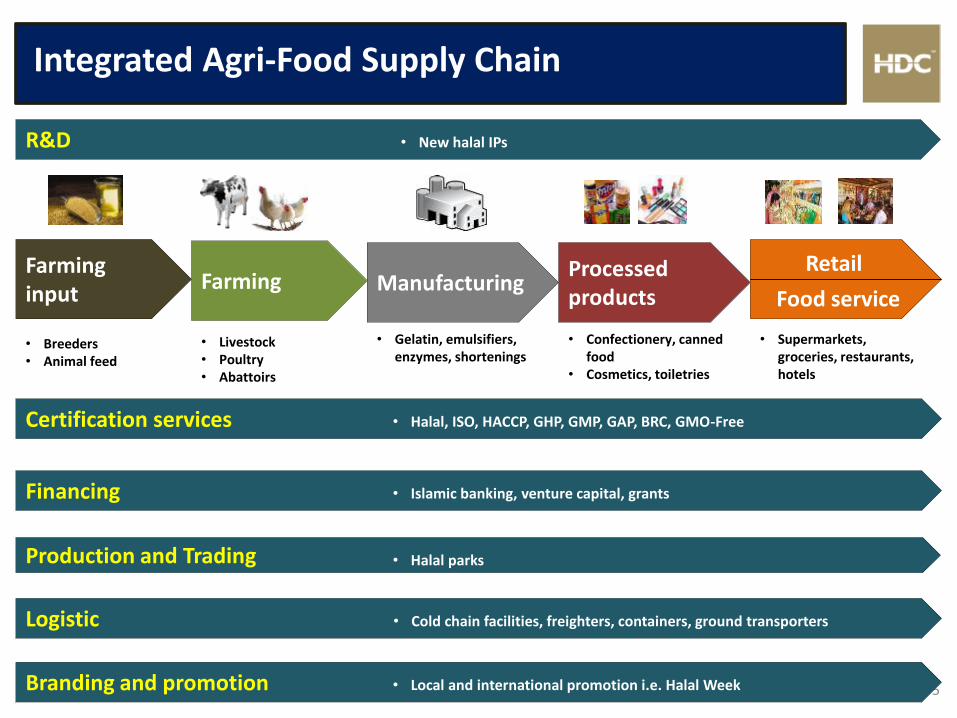

Integrated Agri-Food Supply Chain

5

R&D

Certification services

Financing

Production and Trading

Logistic

Branding and promotion

• New halal IPs

Farming input

Farming Manufacturing Processed products

Retail

Food service

• Breeders • Animal feed

• Livestock • Poultry • Abattoirs

• Gelatin, emulsifiers, enzymes, shortenings

• Confectionery, canned food

• Cosmetics, toiletries

• Supermarkets, groceries, restaurants, hotels

• Halal, ISO, HACCP, GHP, GMP, GAP, BRC, GMO-Free

• Islamic banking, venture capital, grants

• Cold chain facilities, freighters, containers, ground transporters

• Local and international promotion i.e. Halal Week

• Halal parks

Knowing Your Supply Chain

6

Don’t associate your products with these!

Poor hygiene practices

Animal cruelty

Excessive / unpermitted

chemicals

Knowing Your Supply Chain

7

Associate your products with being Halal and more ….

Good hygiene practices

Proper meat processing

Permitted chemicals / ingredients

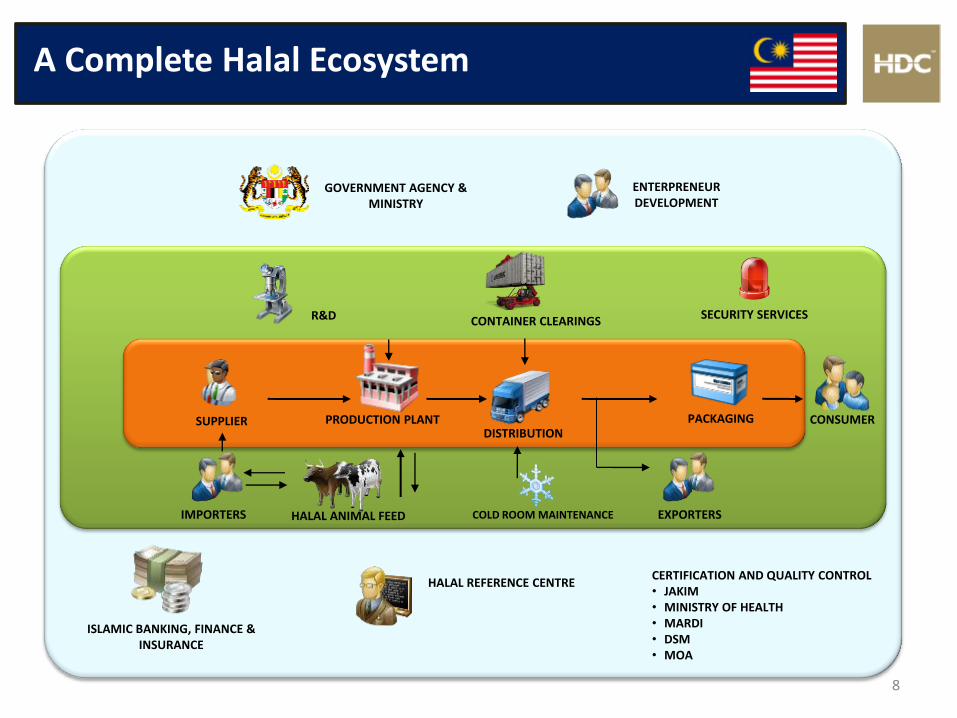

A Complete Halal Ecosystem

8

DISTRIBUTION PRODUCTION PLANT SUPPLIER CONSUMER

SECURITY SERVICES

PACKAGING

EXPORTERS IMPORTERS HALAL ANIMAL FEED COLD ROOM MAINTENANCE

ISLAMIC BANKING, FINANCE & INSURANCE

GOVERNMENT AGENCY & MINISTRY

CONTAINER CLEARINGS

ENTERPRENEUR DEVELOPMENT

R&D

HALAL REFERENCE CENTRE CERTIFICATION AND QUALITY CONTROL • JAKIM • MINISTRY OF HEALTH • MARDI • DSM • MOA

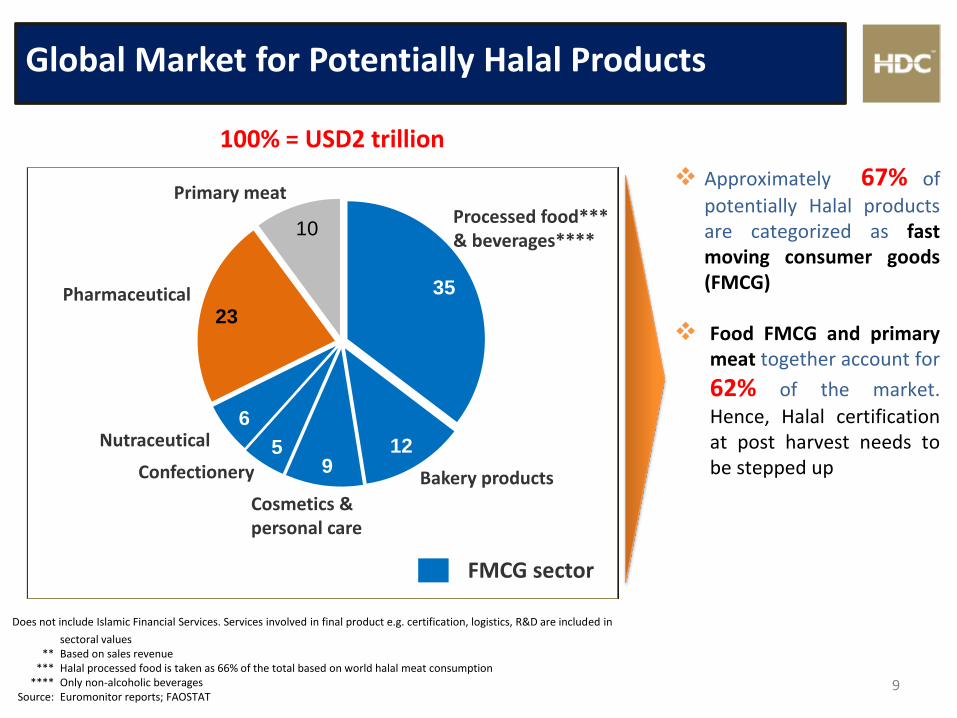

Global Market for Potentially Halal Products

9

35

129

5

6

23

10

FMCG sector

Nutraceutical

Confectionery

Cosmetics & personal care

Bakery products

Processed food*** & beverages****

Primary meat Approximately 67% of

potentially Halal products are categorized as fast moving consumer goods (FMCG)

Food FMCG and primary

meat together account for

62% of the market.

Hence, Halal certification at post harvest needs to be stepped up

Does not include Islamic Financial Services. Services involved in final product e.g. certification, logistics, R&D are included in

sectoral values ** Based on sales revenue *** Halal processed food is taken as 66% of the total based on world halal meat consumption **** Only non-alcoholic beverages Source: Euromonitor reports; FAOSTAT

Pharmaceutical

100% = USD2 trillion

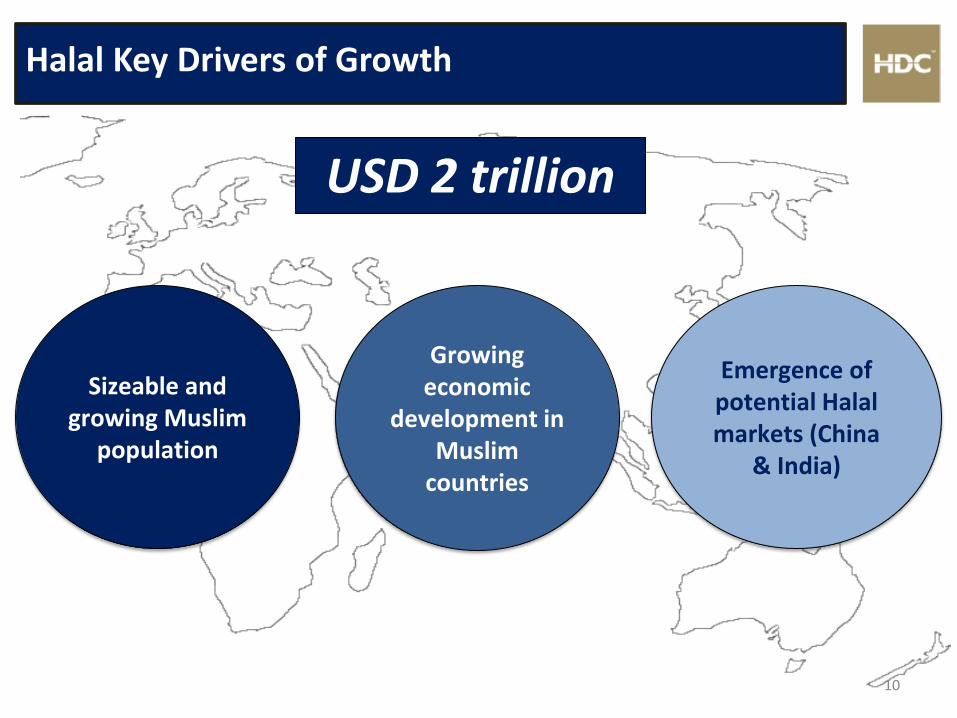

Halal Key Drivers of Growth

USD 2 trillion

Sizeable and growing Muslim

population

Growing economic

development in Muslim

countries

Emergence of potential Halal markets (China

& India)

10

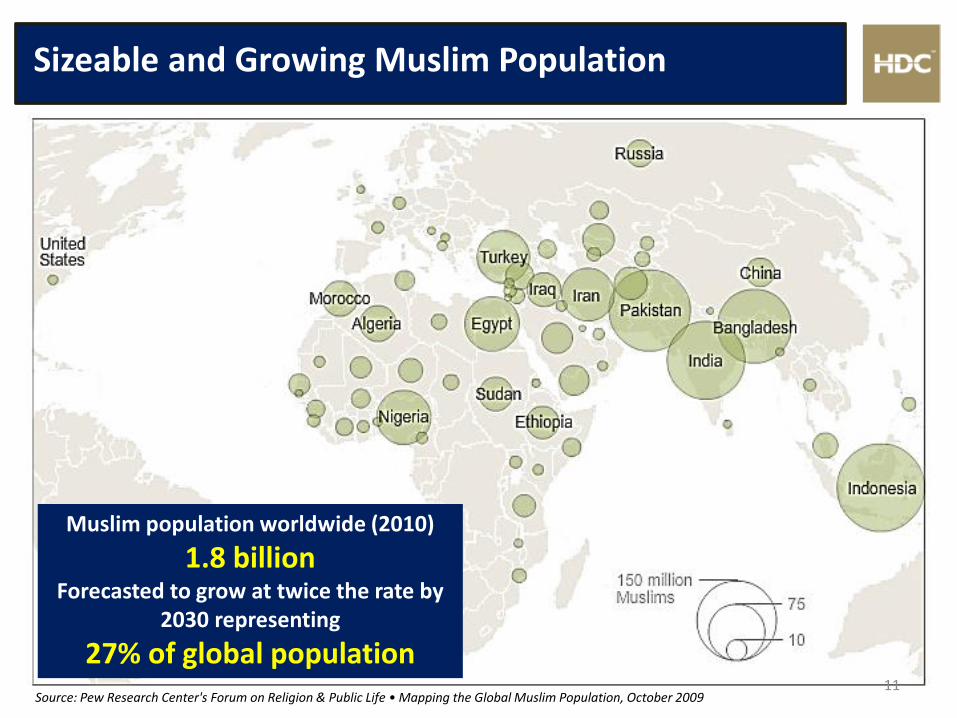

Sizeable and Growing Muslim Population

Source: Pew Research Center's Forum on Religion & Public Life • Mapping the Global Muslim Population, October 2009

Muslim population worldwide (2010)

1.8 billion Forecasted to grow at twice the rate by

2030 representing

27% of global population 11

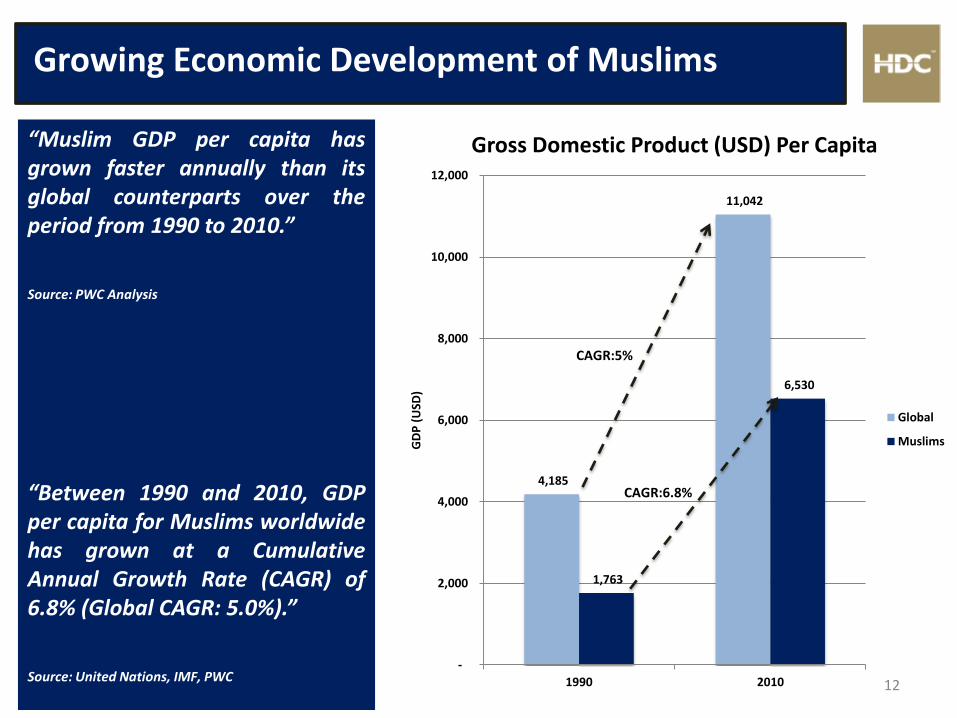

Growing Economic Development of Muslims

“Muslim GDP per capita has grown faster annually than its global counterparts over the period from 1990 to 2010.”

Source: PWC Analysis

“Between 1990 and 2010, GDP per capita for Muslims worldwide has grown at a Cumulative Annual Growth Rate (CAGR) of 6.8% (Global CAGR: 5.0%).”

Source: United Nations, IMF, PWC

4,185

11,042

1,763

6,530

-

2,000

4,000

6,000

8,000

10,000

12,000

1990 2010

GD

P (

USD

)

Gross Domestic Product (USD) Per Capita

Global

Muslims

CAGR:5%

CAGR:6.8%

12

China and India – Emerging Halal Markets

13

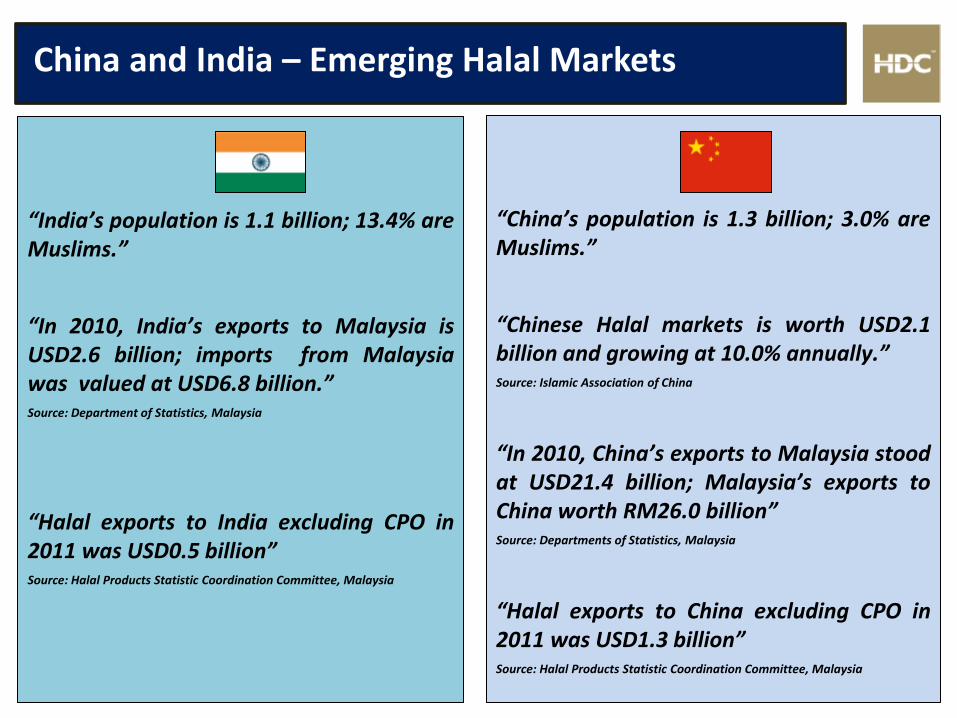

“India’s population is 1.1 billion; 13.4% are Muslims.”

“In 2010, India’s exports to Malaysia is USD2.6 billion; imports from Malaysia was valued at USD6.8 billion.” Source: Department of Statistics, Malaysia

“Halal exports to India excluding CPO in 2011 was USD0.5 billion” Source: Halal Products Statistic Coordination Committee, Malaysia

“China’s population is 1.3 billion; 3.0% are Muslims.”

“Chinese Halal markets is worth USD2.1 billion and growing at 10.0% annually.” Source: Islamic Association of China

“In 2010, China’s exports to Malaysia stood at USD21.4 billion; Malaysia’s exports to China worth RM26.0 billion” Source: Departments of Statistics, Malaysia

“Halal exports to China excluding CPO in 2011 was USD1.3 billion” Source: Halal Products Statistic Coordination Committee, Malaysia

Content

Food Security Issues as a Driver of the Global Halal Market

14

Global Food Hunger Index (2009)

“Undernourishment in Sub-Saharan Africa has increased by 11.8% - highest prevalence of hunger (32%)”

“Asia and Asia Pacific has the highest number of undernourished people in the world”

(Source: FAO)

(Source: IDB)

Global Hunger Index in IDB Member Countries (2009)

15

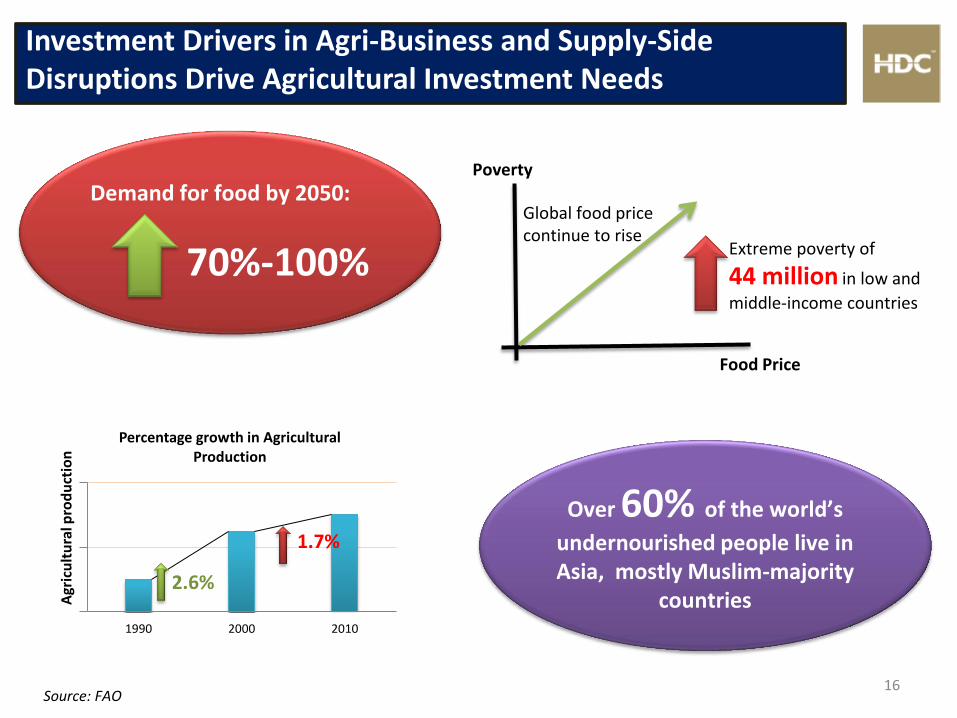

Demand for food by 2050:

70%-100%

Over 60% of the world’s

undernourished people live in Asia, mostly Muslim-majority

countries

Extreme poverty of

44 million in low and

middle-income countries

Poverty

Food Price

Global food price continue to rise

1990 2000 2010

Agr

icu

ltu

ral p

rod

uct

ion

Percentage growth in Agricultural Production

2.6%

1.7%

Source: FAO 16

Investment Drivers in Agri-Business and Supply-Side Disruptions Drive Agricultural Investment Needs

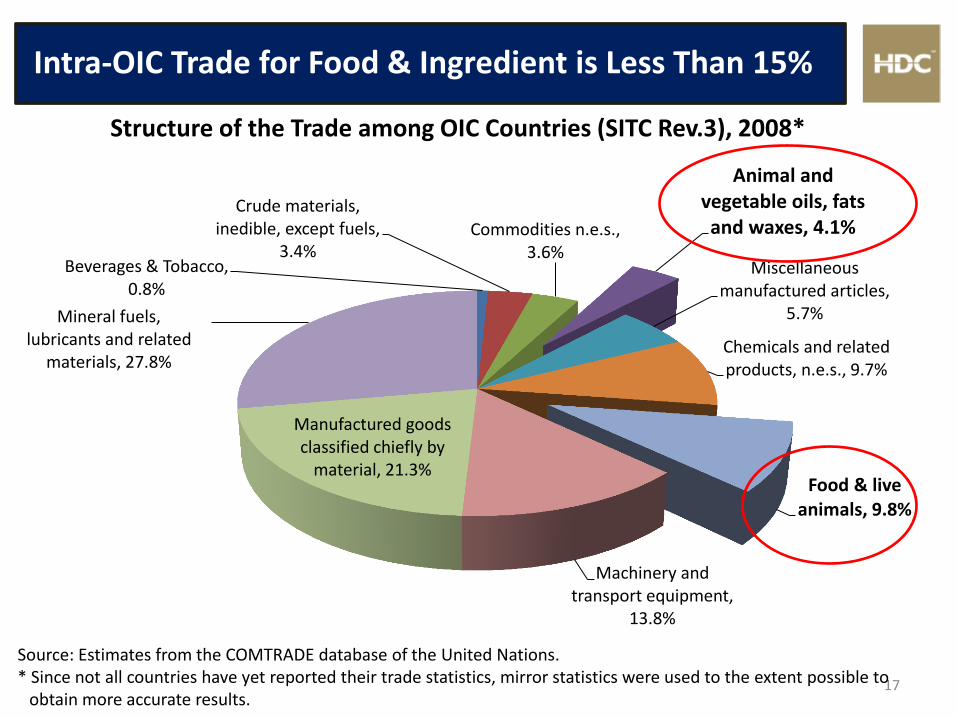

Intra-OIC Trade for Food & Ingredient is Less Than 15%

17

Beverages & Tobacco, 0.8%

Crude materials, inedible, except fuels,

3.4% Commodities n.e.s.,

3.6%

Animal and vegetable oils, fats and waxes, 4.1%

Miscellaneous manufactured articles,

5.7%

Chemicals and related products, n.e.s., 9.7%

Food & live animals, 9.8%

Machinery and transport equipment,

13.8%

Manufactured goods classified chiefly by

material, 21.3%

Mineral fuels, lubricants and related

materials, 27.8%

Structure of the Trade among OIC Countries (SITC Rev.3), 2008*

Source: Estimates from the COMTRADE database of the United Nations. * Since not all countries have yet reported their trade statistics, mirror statistics were used to the extent possible to

obtain more accurate results.

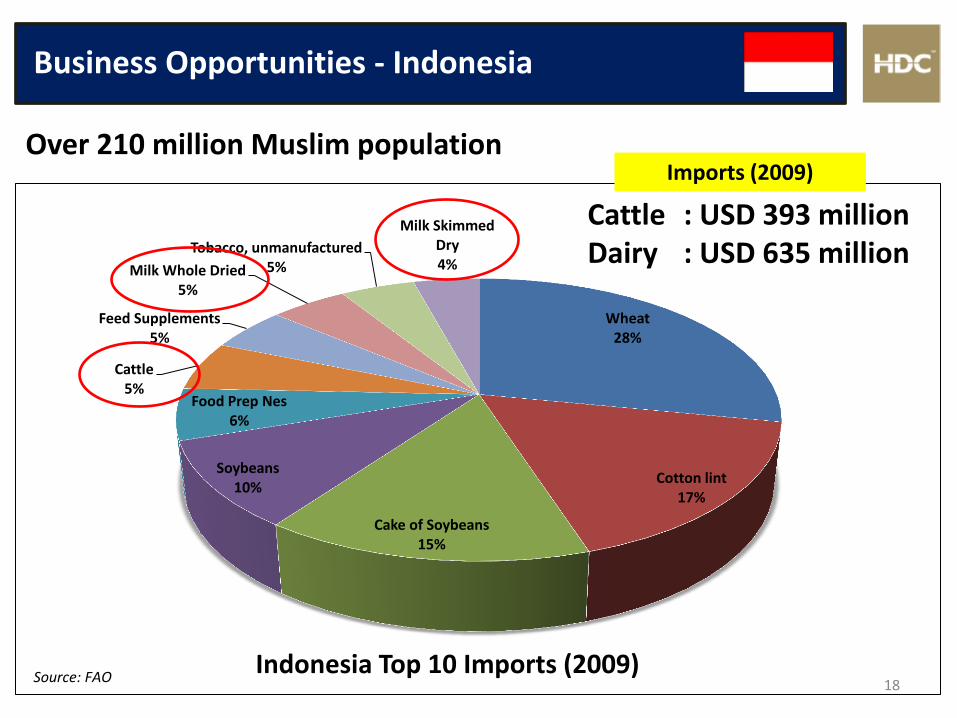

Business Opportunities - Indonesia

18

Wheat 28%

Cotton lint 17%

Cake of Soybeans 15%

Soybeans 10%

Food Prep Nes 6%

Cattle 5%

Feed Supplements 5%

Milk Whole Dried 5%

Tobacco, unmanufactured 5%

Milk Skimmed Dry 4%

Indonesia Top 10 Imports (2009)

Over 210 million Muslim population

Cattle : USD 393 million Dairy : USD 635 million

Source: FAO

Imports (2009)

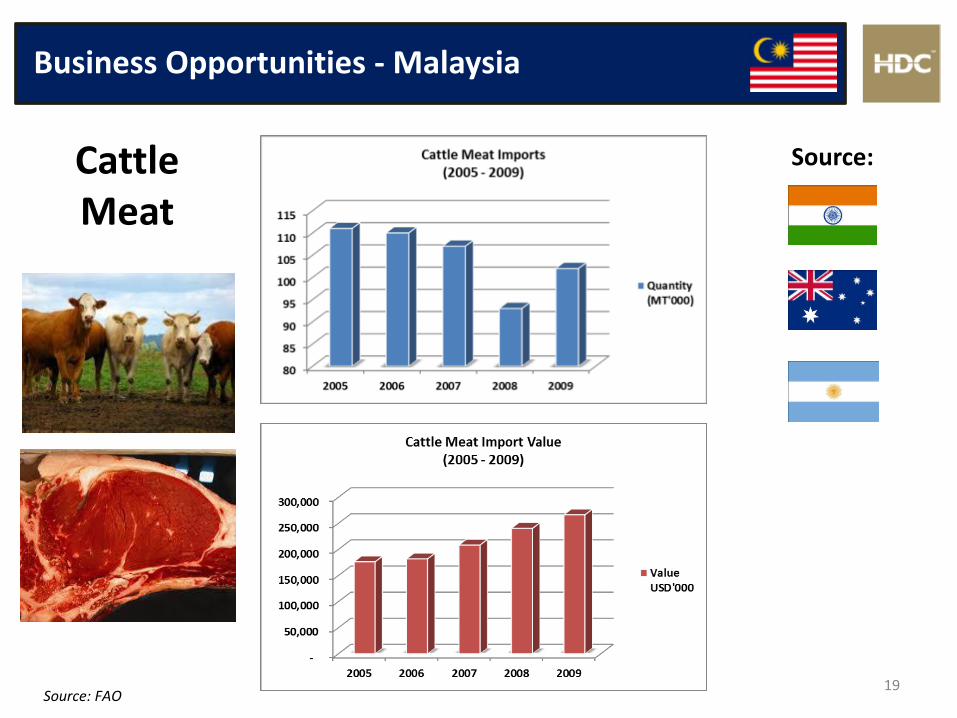

Business Opportunities - Malaysia

19

Cattle Meat

Source: FAO

Source:

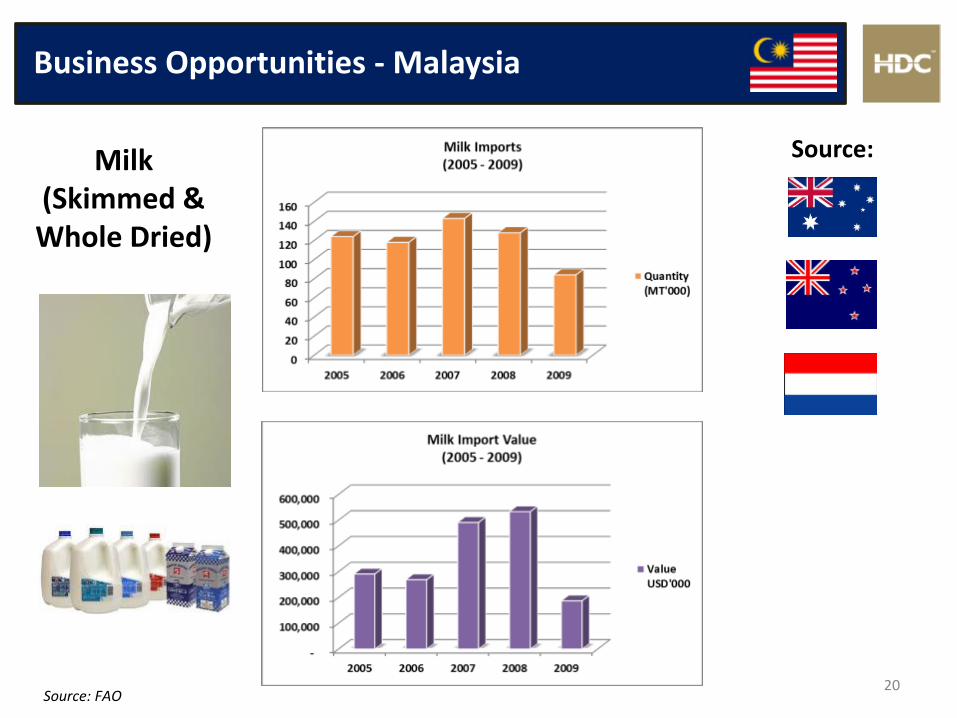

Business Opportunities - Malaysia

20

Milk (Skimmed & Whole Dried)

Source: FAO

Source:

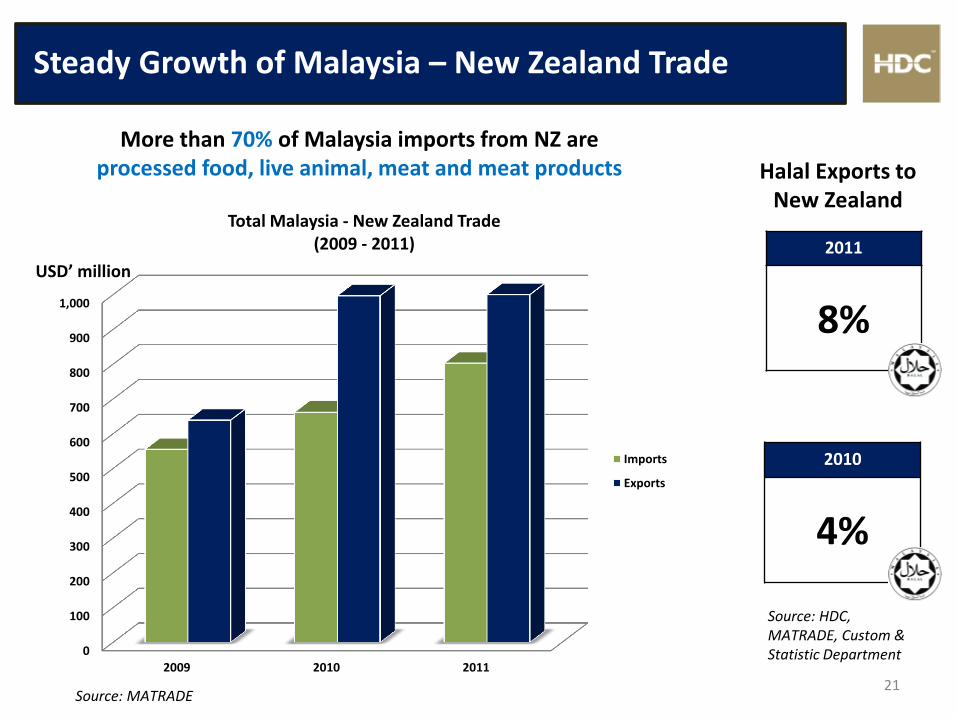

Steady Growth of Malaysia – New Zealand Trade

21

Halal Exports to New Zealand

2010

4%

2011

8%

Source: HDC, MATRADE, Custom & Statistic Department

Source: MATRADE

0

100

200

300

400

500

600

700

800

900

1,000

2009 2010 2011

Total Malaysia - New Zealand Trade (2009 - 2011)

Imports

Exports

USD’ million

More than 70% of Malaysia imports from NZ are processed food, live animal, meat and meat products

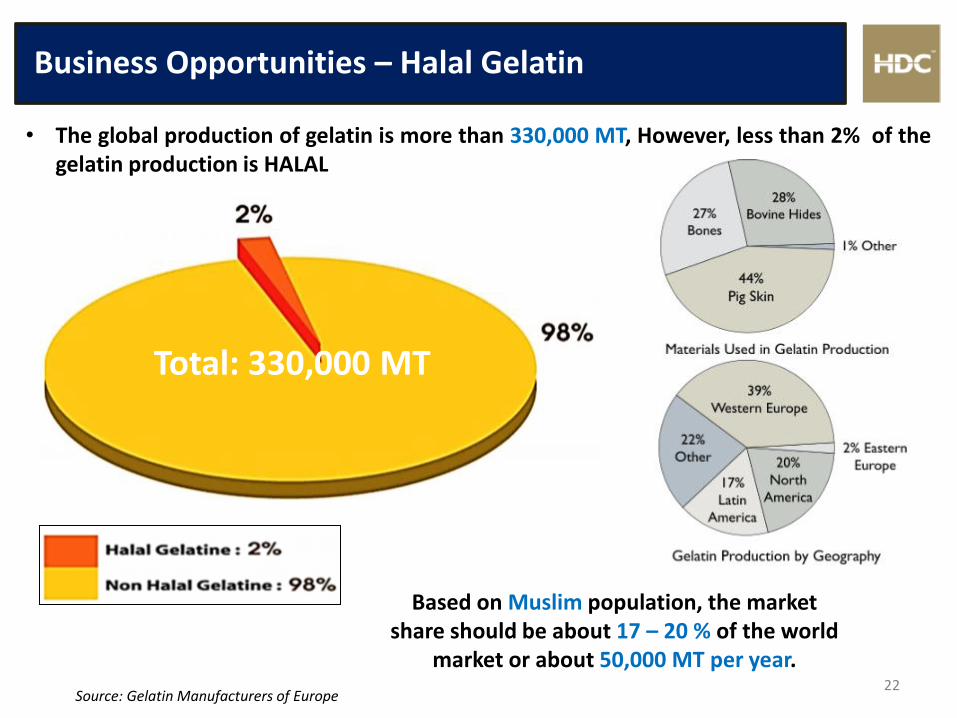

Republic of Guinea Food Import 2009 Business Opportunities – Halal Gelatin

22

• The global production of gelatin is more than 330,000 MT, However, less than 2% of the gelatin production is HALAL

Total: 330,000 MT

Source: Gelatin Manufacturers of Europe

Based on Muslim population, the market share should be about 17 – 20 % of the world

market or about 50,000 MT per year.

Republic of Guinea Food Import 2009 Business Opportunities – Halal Gelatin

23

Total: 330,000 MT

Gelatin

Bakery Products

Canned Ham

Wine and Juices

Dairy Products

Cosmetics

Marshmallow

Pharmaceuticals

Uses of Gelatin

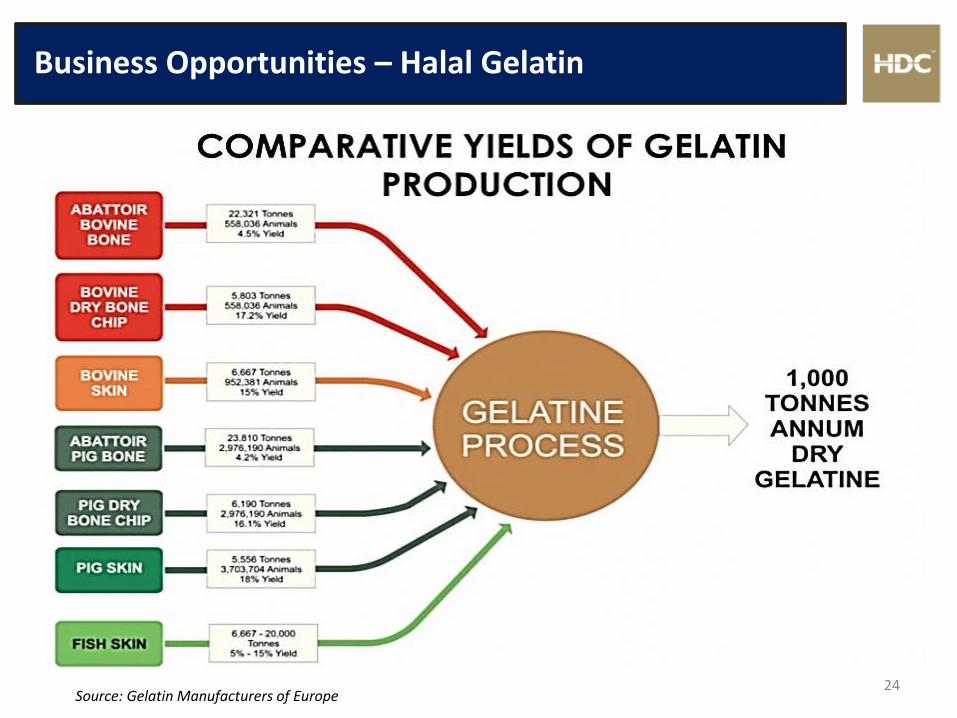

Republic of Guinea Food Import 2009 Business Opportunities – Halal Gelatin

24

Total: 330,000 MT

Source: Gelatin Manufacturers of Europe

Malaysia

Sabah, Malaysia

Qingdao, China

Ningxia, China

Xinjiang, China

China: 1.3 billion population

(3% Muslim)

Indonesia: 250 million population

(80% Muslim)

• Ingredients • Livestock • Seafood • Animal feed • Fertilizer

• Processed food • Livestock • Rice • Corn

• Livestock • Wheat • Corn

• Corn • Sugar • Soybean

Cambodia

• Olive oil • Potatoes • Vegetables & fruits

AUSTRALIA

Tunisia

Europe: 739 million population

(7% Muslim)

Central Asia: 65 million population

(85% Muslim)

AFRICA

EUROPE

Africa: 1 billion population

(40% Muslim)

Middle East: 350 million population

(90% Muslim)

Dubai, UAE

25

Halal Superhighway Link the Global Supply Chain

Business Opportunities

New Zealand

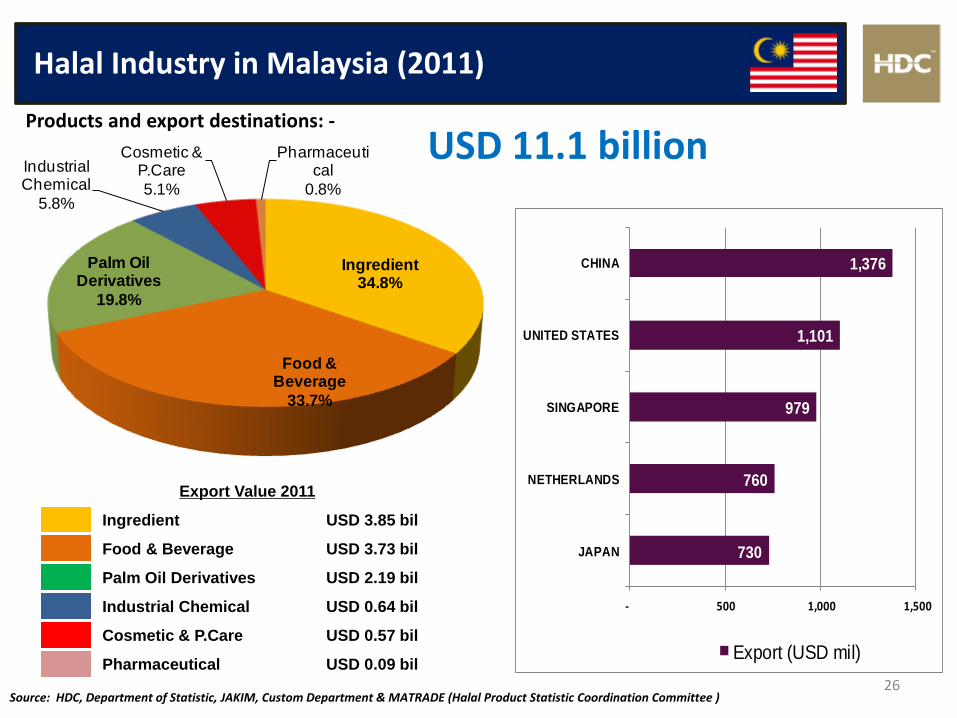

Halal Industry in Malaysia (2011)

Ingredient34.8%

Food & Beverage

33.7%

Palm Oil Derivatives

19.8%

Industrial Chemical

5.8%

Cosmetic & P.Care

5.1%

Pharmaceutical

0.8%

Export Value 2011

Ingredient USD 3.85 bil

Food & Beverage USD 3.73 bil

Palm Oil Derivatives USD 2.19 bil

Industrial Chemical USD 0.64 bil

Cosmetic & P.Care USD 0.57 bil

Pharmaceutical USD 0.09 bil

Products and export destinations: -

Source: HDC, Department of Statistic, JAKIM, Custom Department & MATRADE (Halal Product Statistic Coordination Committee )

USD 11.1 billion

730

760

979

1,101

1,376

- 500 1,000 1,500

JAPAN

NETHERLANDS

SINGAPORE

UNITED STATES

CHINA

Export (USD mil)

26

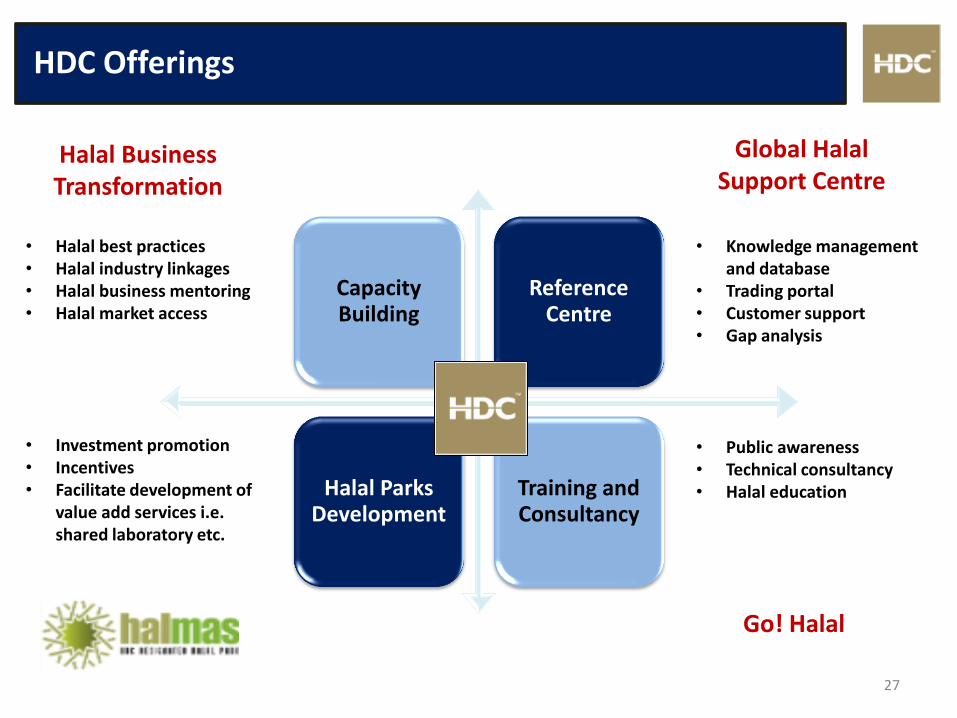

HDC Offerings

Capacity Building

Reference Centre

Halal Parks Development

Training and Consultancy

• Halal best practices • Halal industry linkages • Halal business mentoring • Halal market access

• Knowledge management and database

• Trading portal • Customer support • Gap analysis

• Public awareness • Technical consultancy • Halal education

• Investment promotion • Incentives • Facilitate development of

value add services i.e. shared laboratory etc.

Halal Business Transformation

Global Halal Support Centre

Go! Halal

27

Halal Industrial Parks in Malaysia

28

Incentive for Halal Parks Operator

• 100% tax exemption for 10 years

• Exemption on import duty for cold room equipment

Incentive for Halal companies operating within Halal Parks

• 100% tax exemption on export revenue for 5 years

• Double deduction on expenses incurred in obtaining international certification

Incentive for Halal Logistic Operators

• 100% tax exemption for 5 years

• Exemption on import duty for cold room equipment

Major Investors

Republic of Guinea Food Import 2009 Halal Agribusiness Fund (Con’td)

Sharia-compliant Investment

Vehicle

Fund management

company

Institutional Investor

Company

a. Company; or b.Unit trust fund

Step 1: Equity

Step 4: Dividend/distribution; or Capital gains

Step 2: Equity; or Sukuk

Step 3: Dividend; or periodic payments and capital gains

• Tax incentives available

• Tax incentives available

• Tax incentives available

Institutional Investors Can Participate in the Fund

29

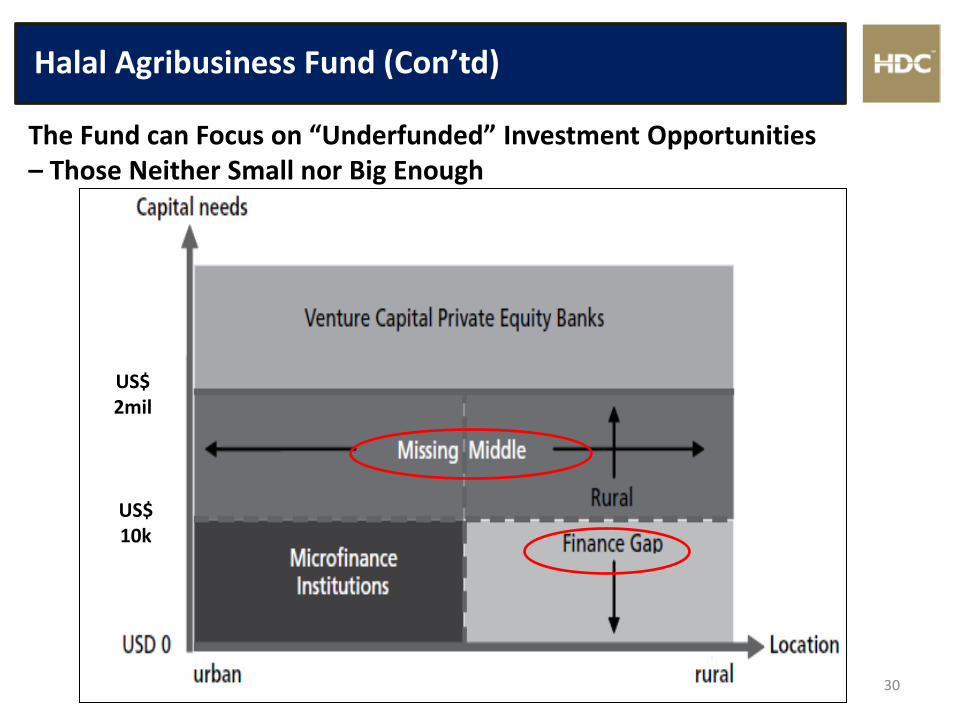

Republic of Guinea Food Import 2009 Halal Agribusiness Fund (Con’td)

The Fund can Focus on “Underfunded” Investment Opportunities – Those Neither Small nor Big Enough

30

US$ 2mil

US$ 10k

Republic of Guinea Food Import 2009 Halal Agribusiness Fund (Con’td)

The Final Structure of the Fund can Vary Depending on the Stakeholders Involved and Financing Facilities Provided

31

Halal Industry Development Corporation (HDC)

5.02, Level 5,

KPMG Tower, First Avenue, Persiaran Bandar Utama,

47800 Petaling Jaya, Selangor DarulEhsan,

Malaysia.

Tel : +603 - 7965 5555

Fax : +603 - 7965 5500

Hotline : 1800 - 880 - 555 (within Malaysia)

+603 7965 5400 (outside Malaysia)

www.hdcglobal.com

Thank you

Q&A

![Guideline: Halal Standard and Halal Certification Procedures and Halal... · 2 0 1 4 Guideline: Halal Standard and Halal Certification Procedures Jamiat ul Ulama of Mauritius [JUM]](https://img.pdfslide.us/doc/110x75/5e0eedcb96a29326060514bb/guideline-halal-standard-and-halal-certification-and-halal-2-0-1-4-guideline.jpg)