TOP TRADE OPPORTUNITIES 2015 DailyFX Research Team

[email protected] | www.twitter.com/DailyFX Top Trading

Opportunities of 2015The past year was defined by a global capital

market that grew increasingly skeptical of the persistent reach for

yield and a substantial shift in the ranks for monetary policy.

Heading into 2015, speculation over central banks next moves (from

more ECB stimulus to the first Fed hike) will find even greater

prominence. Meanwhile, another 12 months without a 10 20 percent

correction in speculative benchmarks like the S&P 500 is

extremely unlikely. Below, the DailyFX Analysts list their top

trades with these scenarios in mind. John Kicklighter, Chief

Currency StrategistEURUSD | EURCHF The Effectiveness of Stimulus

David Rodriguez, Senior Currency Strategist Yen Selling to Extend a

Third Year Jamie Saettele, CMT, Senior Technical Strategist

Possible Long Term NZDUSD Double Top and a Long Term EURGBP Support

Zone Kristian Kerr, Senior Currency Strategist Apparently This Time

Is Different Ilya Spivak, Currency Strategist EURUSD Fed vs. ECB

Policy Divergence to Fuel Deeper Euro Losses Michael Boutros,

Currency Strategist GBPJPY- Troubled Waters Ahead But Steady as She

Goes Christopher Vecchio, Currency Strategist The ECBs Monetary

Policy Divergence David Song, Currency AnalystEuro Crosses to

Target Multi-Year Lows on ECB Easing Cycle David De Ferranti,

Currency Analyst Policy Divergence Bets May Remain Supportive For

the US Dollar Index In 2015 John Kicklighter, Chief Currency

Strategist EURUSD | EURCHF The Effectiveness of Stimulus EURUSD

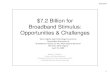

Through the second half of 2014, EURUSD dropped from 1.4000 to well

below 1.2500. While this decline encompasses a number of elements,

much of the momentum was a side effect of the European Central

Banks efforts. Whether you believe their efforts intentionally

targeted the exchange rate or are purely focused on ending

dis-inflation and recharging stagnant growth, the connection to

price is clear. Much of what we have seen from the Euros decline

through the end of the year though was in anticipation of a growing

ECB balance sheet. That

meansthemarkethasalreadyadjustedforthestimulusswelltosomeextent,butafullscaleeffortwilllikely

result in a much further decline.

Chart Created by John Kicklighter using Data from Bloomberg and

FXCMs Trading Station

Theimplementationofafull-scaleQuantitativeEasing(QE)programliketheFedsorBoJscouldhelpdrive

EURUSDto thenextphaseofa

medium-termbearishtrend.Yet,evenifitlacksasacatalyst,thereisalsothe

fallout from a global risk aversion shift that draws speculative

capital out of the low-return-high-cost European capital markets

and a likely rise in sovereign yields that will revive fiscal

concerns. I will watch this fundamental wave build with intentions

to short below 1.2200/1.2000 (a zone of support that shapes the

floor of a more than decade long wedge formation). EURCHF Through

2015, the European Central Bank will likely leverage the most

aggressive expansion of monetary policy accommodation of all the

major central banks. That will put pressure on all of its pairings,

including EURCHF. However, there is a very important quirk to this

pair: the Swiss National Banks primary policy agenda is to keep the

exchange rate above 1.2000. Having moved beyond a brief threat

posed by the Swiss Gold Referendum vote, the central bank can keep

to its policy of buying unlimited currency (largely Euro) to

sustain the floor. That effort will likely prevent the exchange

rate from dropping below the managed support, but it does little to

see the market move higher. I like the long side with a stop 25-50

pips below 1.2000. With the probability of a breakdown diminished

by the

SNBsvows,therearetwoscenariosthatIamconsidering.Thefirstisthatthegroupdoesnothingmorethan

maintain its floor, which means the market could be anchored to

1.2000 for many months much like the period in 2012. I have learned

from that last instance (this pair was also one of my top setups

for that year) to be patient. Alternatively, theSNB may recognizeit

will be fighting a constantuphill battle and adopt additional

policy that negates the tension. Negative rates on foreign capital

for examplecould divert outflows of Eurozone capital to

othercountriesandtake thepressureoff.Ascanbeseen with

theSwissLiborratebelow,themarketexpects more moving forward. Chart

Created by John Kicklighter using Data from Bloomberg and FXCMs

Trading Station David Rodriguez, Quantitative Strategist Yen

Selling Extend a Third Year For the third-consecutive year I

believe that selling the Japanese Yen will be one of the top trades

of the New Year. I somewhat-jokingly told my colleague Jamie

Saettele that I would simply re-submit what I wrote about the

USDJPY 12 months ago. I wont actually do that, but the perspective

offers context. The first line told the narrative I believe remains

central to any long-term Yen forecast:The Government of Japan and

the central Bank of Japan (BoJ)showevery intention to continue a

weak

JapaneseYenpolicy,andthey'reinauniquepositionofhavingplentyofammunitionleftinpotential

easing. That sentence could have been written yesterday and remains

every bit as true today as it did last year.BoJ officials sent the

Yen sharply lower by unexpectedly boosting Quantitative Easing

purchases at their October

31meeting,andthecurrentpaceofQEwillboosttheBankofJapansbalancesheettonearly60percentof

JapaneseGrossDomesticProductthrough2015.IftheyraiseQEevenfurther,whichIthinkislikely,that

percentage grows faster. The US Federal Reserve and Bank of

England, by comparison, seem likely to keep their total assets and

liabilities to approximately 25 percent of GDP.Last year I likewise

emphasized the political threat to the Yen as a key reason it could

fall further:Public debt is likewise a major reason that the BoJ

and the Japanese Government will keep its finger on the 'trigger'

of further easing. Extraordinarily large public debt mean that

central bank bond buying will be too difficult to resist.

Politicians will keep pressure on the central bank to continue

buying [debt]. This fact is still true, and I think economic and

fiscal underperformance will put further pressure on

politicians.What are the risks? I need to emphasize that, all else

remaining equal, I think these factors will send the Yen lower

versus the Dollar in 2015. Yet that statement is a bit ridiculous

in making forecasts. Market factors and conditions can and do

change in an instant, and there are always the unknown-unknown

risks (a.k.a. Black Swans) which can change the game entirely. But

even foreseeable events could materially change JPY trading

dynamics.Majorglobalequityindicescontinuetohitrecord-peaksandencouragerisk-taking.InFXthishasoftenmeant

selling JPY to buy higher-yielders, but a flight to safety

comparable to what we saw in 2007-2008 would likely force

substantial pullbacks in the USDJPY and JPY crosses. I should

further emphasize that nothing moves in a straight line, and USDJPY

corrections seem especially likely.Yet all else remaining equal I

expect the Yen will fall even further versus the US Dollar in 2015.

Jamie Saettele, CMT, Senior Technical Strategist Possible Long Term

NZDUSD Double Top and a Long Term EURGBP Support Zone In this space

last year, I presented ideas on EURNZD, AUDNZD, USDCAD, USDNOK and

crude. EURNZD didnt work and AUDNZD is actually net unchanged on

the year (as of December 5th). USDCAD, USDNOK, and crude worked

well. The point in referencing last years ideas is twofold; NZD

still looks poised to fall apart and the best ideas are the ones

that others arent looking at (dont recall many USDNOK bulls and

crude bears for example). So, 2 ideas that stick out for 2015 are

short NZDUSD and long EURGBP (from lower). NZDUSD Monthly Prepared

by Jamie Saettele, CMT NZDUSD exhibits a possible double top with

the 2011 and 2014 highs. A break of .7370 would complete the

pattern and yield an objective of .5900, which is in line with the

2004 and 2006 lows. Watch out for .7100-.7200 as support

though(1988high,1996high,February2004high,December2005high,March2011low),especiallyinJune

(intersection with a slope line). The underside of a broken

parallel could come into play as resistance early in the year near

.8200.

0.35000.40000.45000.50000.55000.60000.65000.70000.75000.80000.85000.90000.950006/1998

11/2002 10/2004 09/2006 08/2008 07/2010 06/2012 05/2014 04/2016

03/2018 02/20200.000 0.884151.000 0.736952.000 0.58975double top

target is in line with2004 and 2006 lows.7370 break confirms double

top with 2011 and 2014 higswatch this line for support thoughwatch

this one for

resistance0.884150.590900.709800.821300.770043040506070FXCM

Marketscope 2014 EURGBP Monthly

Prepared by Jamie Saettele, CMT EURGBP is interesting from a

pure levels perspective. A head and shoulders completed in December

2007. The breakout level from that pattern is .7253. Interestingly,

the 61.8% retracement of the rally from the 2000 low is .7259. The

decline from the 2008 high would consist of 2 zigzags (7 waves

labeled a-b-c-x-a-b-c) at .7345. Basically, were left with

.7250-.7350 as a zone that could produce an important low in the

cross. Ill note that the line off of the 2000 and 2007 lows (not

shown) is at about .7537 in January and increases 11 pips per

month.

0.55000.60000.65000.70000.75000.80000.85000.90000.95001.000012/1994

01/2000 12/2001 11/2003 10/2005 09/2007 08/2009 07/2011 06/2013

05/2015 04/20171.000 0.734480.000 0.980390.618 0.725901.000

0.56860SSHhead and shoulders re-test level lines up witha Fibonacci

confluence0.787963040506070FXCM Marketscope 2014 Kristian Kerr,

Senior Currency Strategist Apparently This Time Is Different I like

the US Dollar generally and believe that the move that started this

year probably has a lot more room to run. That said, I am skeptical

that the Buck can continue its advance at the current rate.

Aggregate positioning in USD on the IMM recently reached its

highest levels ever.

Whilethisdataonlycapturesasliverofthemarket,itdoesdoagoodjobofcapturingtheconvictionatthe

moment that the USD can only go up. All too predictably I keep

reading reasons why these extremes dont matter this time. I dont

buy it. Historically in the currency markets when conviction is so

high it is precisely the time to start looking to get out or go the

other way. A flush out of some sort seems likely to me and probably

sooner than

later.USD/JPYlooksespeciallyvulnerableinthisregardassentimentrecentlytouchedall-timehighlevelsof

optimism.Acontrariansdream.IsuspectUSD/JPYwillsurprisemostoverfirstpartoftheyearbyatleast

consolidating and probably weakening into the summer. Around the

3rd quarter USD/JPY should be a buy again.

80.0090.00100.00110.00120.00130.00140.00150.0003/1995 07/1998

11/1999 03/2001 07/2002 11/2003 03/2005 07/2006 11/2007 03/2009

07/2010 11/2011 03/2013 07/2014 11/2015 03/2017 07/20181997 1998

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

2012 2013 2014 2015 20160.382 94.1110.500 99.8430.618 105.5740.786

113.7350.886 118.5920.382 98.3170.500 105.3500.618 112.3830.786

122.3960.886 128.356Monthly0.618 108.2951.618 112.9270.382

103.1890.500 111.6960.618 120.2040.786 132.315FXCM Marketscope

2014121.097 Ilya Spivak, Currency Strategist Short EURUSD Fed vs.

ECB Policy Divergence to Fuel Deeper Euro Losses Selling the Euro

against the US Dollar was my top trade for 2014. I reasoned the

Feds move to taper QE3 asset purchases marked a hawkish policy

shift while the ECB looked likely to ramp up stimulus as realized

and expected Eurozoneinflation readings tumbled. This madefor

clear-cut policy divergence that promised to shiftthe yield spread

in favor of the greenback, pushing EURUSD downward. The trade

worked as expected. Prices found a top at the upper boundary of the

multi-year down trend guiding the pair lower since April 2008 and

turned downward.More of the same is likely in 2015. While

speculation about the timing of the Feds first post-QE interest

rate hike will make for volatility, the overall trajectory of FOMC

policy seems firmly pointed toward tightening. Meanwhile, a medley

of newECB stimulus measuresunveiled in 2014 is floundering, with

thecentral banksbalance sheet broadly flat since October. Not

surprisingly, ECB officials have taken to hinting the onset of

sovereign QE the purchase of government bonds with printed money

possibly as soon as the first quarter. Chart Created by Ilya Spivak

using FXCMs Trading Station Taken together, this is likely to see

the rates spread shift even more dramatically in the Dollars favor

and keep EURUSD firmly under pressure. Prices are flirting with

support at trend line support set from June 2010, with a

breakbelowthisandthe38.2%Fibonacciexpansionat1.2316exposingthenextmajordownsideobjectiveat

1.2140 (50% Fib). Michael Boutros, Currency Strategist GBPJPY-

Troubled Waters Ahead But Steady as She Goes Heading into 2014

trade, our focus was on the diverging monetary policy outlooks

across the globe with GBPJPY targeted higher while above

147.50-148.50. The pair remained largely range-bound throughout the

year before staging a sharp rally in the fourth quarter to achieve

our objective target at 184-188.27 in early December trade. The

GBPJPYis poised to close 2014 up more than 9%and as we lookahead to

2015, thebroader fundamental picture remains unchanged. Despite the

December election, the BoJ may have little choice but to further

expand its asset-purchase program as the weakening outlook for the

Asia/Pacific region threatens the central banks scope to achieve

the 2% inflation target over the policy horizon. However, as

BoEGovernor Mark Carney continuesto prepareUKhouseholds &

businessesforhigherborrowingcosts,theGBPJPYoutlookremainsunchangedonaccountofthecontinued

diverging policy stances. That said, the technical picture looks

more precarious as the pair eyes resistance into the close of

2014.

GBPJPY is trading with the confines of a well-defined pitchfork

formation off the 2009 low with the median line catching the highs

in early 2013. Interestingly enough, price action compromised this

threshold on the approach into our objective at 184-188.24. Note

that the weekly RSI signature is now coming into the former support

trigger and may cap the advance in the medium-term. That said, the

breach cannot be confirmed while within this zone and the potential

for a near-term correction heading into the start of 2015 is a real

threat.Initial support is eyed at the former 2014 opening range

highs at the 175-handle which converges with channel support in 1Q

of 2015. The outlook remains constructive while above key support

at 168.11 170.40 with a move below this region challenging the

broader rally off the 2011 lows. Bottom line: looking for a broad

pullback in 2015 to offer more favorable long entries with a

confirmed breach of the 184-188.27 resistance zone eyes subsequent

topside resistance objectives at 199.80 & 208.20. Christopher

Vecchio, Currency Strategist The ECBs Monetary Policy Divergence We

enter 2015 on the heels of pivots made by several of the major

central banks: the Bank of Englandand the Federal Reserveare

discussing rateliftoff timing; while the Bankof Japan, the European

Central Bank, and the Swiss National Bank are all pushing for more

aggressive easing measures. This time is different, however. In

years past, promises of pending stimulus had put a halt on the

declines seen by the Euro at times (notably in July 2012 when ECB

President Draghi made his now (in)famous whatever it takes

comment),butthenatureofthecurrentdeclineintheEuroisdifferentthanthosepreviouslycontextis

important.EURUSD Now that peripheral sovereign bond yields are

already low, so there is no latent risk-relief rally potential.

Coupled withplunginginflationexpectations,bytheend of

2014,theECBwaslayingtheground workforapotentially massive balance

sheet expansion in 2015. The oft-cited figure, a return to the

early-2012 levels, would call for the ECBs balance sheet to balloon

by 500 billion to 1 trillion (current size is roughly 2.05

trillion; range for early-2012 was roughly 2.60 to 3.10 trillion).

If a wave of stimulus is about to come crashing down on the shores

of the Euro-Zone, then the technical structures of two pairs stuck

in the ECBs policy divergence vacuum EURGBP and EURUSD could see

significantly lower prices over the next 12-months. David Song,

Currency AnalystEuro Crosses to Target Multi-Year Lows on ECB

Easing Cycle The growing deviation in monetary policy continues to

foster a bearish outlook for EUR/GBP and EUR/CAD as the European

Central Bank (ECB) struggles to achieve its one and only mandate

for price stability. Nevertheless, the Bank of England (BoE)

remains on track to raise the benchmark interest rate in 2015 as

the central bank anticipates

afasterrecoveryintheU.K,whiletheBankofCanada(BoC)maycomeunderincreasedpressuretofurther

normalize monetary policy amid the stickiness in price growth.

EURGBP Weekly EUR/GBP remains poised for a further decline in 2015

as it preserves the bearish trend carried over from back in

2009.Wewillcontinuetolookforaseriesoflowerhighs&lowsinEUR/GBPasBoEGovernorMarkCarney

prepares U.K. household and business for higher borrowing-costs

while the ECB keeps the door open for additional monetarysupport.

Withthatsaid,EUR/GBPmaymakea moremeaningfulrunatthe

2012low(0.7750)in the year ahead, and we will continue to favor the

downside targets in 2015 as the fundamentals and technicals point

to a further decline in the exchange rate. EURCAD Daily

Aftercarvingahead-and-shoulderstopin 2014,the

keyreversalinEUR/CADshouldcontinuetotake shapein 2015 as the Bank

of Canada scales back its dovish tone for monetary policy. Indeed,

the BoC may follow the Fed

andshowagreaterwillingnesstoraisethebenchmarkinterestratenextyearasinflationholdsabovethe2%

target, and Governor Stephen Poloz may continue to change his tune

over the near to medium-term as the central bankhead seesa

broadening recovery in Canada. With that said, wewill continueto

look for a series of lower highs & lows in EUR/CAD and favor

the downside targets especially as the fundamental outlook for the

euro-area remains clouded with high uncertainty.

1.07501.10001.12501.15001.17501.20001.22501.25001.275001/09/2013

02/28 03/25 04/17 05/10 06/04 06/27 07/22 08/14 09/06 10/01 10/24

11/18 12/11 12/28Mar May Jul Sep Nov0.236 1.128370.382 1.115190.500

1.104540.618 1.093880.786 1.078720.382 1.250820.500 1.211100.618

1.171390.786 1.114830.236 1.130870.382 1.109200.500 1.091690.618

1.07418[Template: DavidS]MVA(AUD/NZD.Open,10):

1.10157MVA(AUD/NZD.Close,20): 1.10898MVA(AUD/NZD.Close,50):

1.12679MVA(AUD/NZD.Close,100): 1.13310MVA(AUD/NZD.Close,200):

1.168951.085940305070100RSI(AUD/NZD.Close, 14): 25.65FXCM

Marketscope 2013 David De Ferranti, Currency Analyst Policy

Divergence Bets May Remain Supportive For The US Dollar Index In

2015 The US Dollar finally blossomed mid-way through 2014 after a

lackluster performance during the first half of the

year.2015mayyieldfurthergainsforthereservecurrencyastheUSeconomycontinuestoimproveandFed

policy normalisation bets strengthen. Leading indicators for the

health of the US economy offer encouraging signals for robust

economic growth. These

includeconsumerconfidencefiguresaswellasmanufacturingandservicessectorsurveydata.Meanwhile,

progressintheUSlabourmarkethascontinuedwithaslideintheunemploymentratealongsidehealthyjobs

added prints. With maximum employment as one of the Feds core

policy objectives a continued improvement in the labour data would

support the case for an eventual rate rise from the central bank in

2015.TheprospectofahikebytheFederalReservestandsinstarkcontrasttoexpectationsfromitsmajorpeers.

Disinflation in the Eurozone and deteriorating economic data is

likely to keep Draghi dovish over the near-term. Similarly, Kuroda

remains prepared to enact further stimulus following a slip back

into recession for the Japanese economy. Finally softlocal economic

data and a refocus for Chinese growth towards consumption, threaten

to deter a hike from the RBA and RBNZ. In turn this suggests the

prospect of continued gains for the US Dollar index with the

potential for the greenback to outperform most significantly

against the Euro and Yen. There are several potential downside

risks for the USD going into 2015. Chief amongst these is the

prospect of a

delayedratehikefromtheFederalReserve.USinflationremainssubduedandweakwagegrowthalongside

declining energy prices threaten to keep costs contained in the

near-term. Further, if asset prices for equities and housing begin

to decline, policy makers may be tempted to re-inflate them for

fear of the negative ramifications on the broader economy via the

wealth effect. Finally, if the recent pick up in implied volatility

fails to gain traction a reach for yield could see investors once

again turn their gaze outside the US for higher returns.On balance

the positives likely outweigh the risk factors and support the

prospect of another strong year for the US Dollar Index. DISCLAIMER

DailyFX Market Opinions Any opinions, news, research, analyses,

prices, or other information contained on this website is provided

as general market commentary and does not constitute investment

advice. FXCM will not accept liability for any loss or damage,

including without limitation to, any loss of profit, which may

arise directly or indirectly from use of or reliance on such

information. Accuracy of Information The content in this report is

subject to change at any time without notice, and is provided for

the sole purpose of assisting traders to make independent

investment decisions. DailyFX has taken reasonable measures to

ensure the accuracy of the information in the report, however, does

not guarantee its accuracy, and will not accept liability for any

loss or damage which may arise directly or indirectly from the

content or your inability to access the website, for any delay in

or failure of the transmission or the receipt of any instruction or

notifications sent through this website. Distribution This report

is not intended for distribution, or use by, any person in any

country where such distribution or use would be contrary to local

law or regulation. None of the services or investments referred to

in this report are available to persons residing in any country

where the provision of such services or investments would be

contrary to local law or regulation. It is the responsibility of

visitors to this website to ascertain the terms of and comply with

any local law or regulation to which they are subject. High Risk

Investment Trading foreign exchange on margin carries a high level

of risk and may not be suitable for all investors. The high degree

of leverage can work against you as well as for you. The

possibility exists that you could sustain a loss in excess to your

investment and therefore you should not invest money that you

cannot afford to lose. Before deciding to trade foreign exchange

you should carefully consider your investment objectives, level of

experience, and risk appetite. You should be aware of all the risks

associated with foreign exchange trading and seek advice from an

independent financial advisor if you have any doubts. 3