Embed Size (px)

Citation preview

Summer Internship Report

On

MAHARSHI DAYANAND UNIVERSITY, ROTHAK

Operational & Financial Viability of Distribution Utilities

in Major States of India

Under the Guidance of

Mr. Sunil Varma Marri (Head-Energy)

iMaCS(ICRA)

&

Mrs Indu Maheshwari, Director

National Power Training Institute, Faridabad

ICRA Management Consulting Services Ltd

Submitted by

Ashish Garg

Roll No 21, Batch 2012-14

MBA (POWER MANAGEMENT)

NATIONAL POWER TRAINING INSTITUTE

Affiliated to

Center for Advanced Management and Power StudiesCenter for Advanced Management and Power StudiesCenter for Advanced Management and Power StudiesCenter for Advanced Management and Power Studies

NATIONAL POWER TRAINING INSTITUTE NATIONAL POWER TRAINING INSTITUTE NATIONAL POWER TRAINING INSTITUTE NATIONAL POWER TRAINING INSTITUTE (Under Ministry of Power, Govt. of India)

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 1

CERTIFICATE

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 2

DECLARATION

I, Ashish Garg, Roll no. 21 / Semester 3rd / Class of 2012-14 of the MBA (Power Management)

of the National Power Training Institute, Faridabad hereby declare that the Summer Training

Report entitled:

Operational & Financial Viability of Distribution Utilities in Major States of India

is an original work and the same has not been submitted to any institute for the award of any

other degree.

Project In charge Signature of Candidate (Faculty)

Countersigned

Director/Principal of the Institute

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 3

ACKNOWLEDGEMENT

The projects done by me under this internship program wouldn’t have been completed, if not for

the active help and guidance of various people.

I express my sincere thanks to Mr. Sunil Varma Marri (Head – Energy Sector), IMaCS for giving

me a great opportunity to work in such a dynamic organization and for guiding me in all stages of

the project. I am thankful to Mr. Rohit Singh (Analyst), IMaCS for his guidance and support. I

have a deep sense of gratitude and respect for the entire staff of IMaCS for sharing their knowledge

and for assisting me.

I would like to thank my Project In-charge Mrs. Indu Maheshwari, Director, NPTI, Faridabad for

her support and guidance throughout the course of summer internship.

A special thanks to Mr. S.K Choudhary, Director (CAMPS), Mrs. Manju Mam, Director, NPTI

for their guidance throughout my summer internship and all faculty members for arranging my

internship at iMacs and being a constant source of motivation and guidance throughout the course

of my internship.

Ashish Garg

MBA (Power Management)

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 4

TABLE OF CONTENTS

CERTIFICATE ........................................................................................................................................... 1

DECLARATION......................................................................................................................................... 2

ACKNOWLEDGEMENT .......................................................................................................................... 3

LIST OF FIGURES .................................................................................................................................... 7

ABBREVIATIONS ..................................................................................................................................... 9

EXECUTIVE SUMMARY ...................................................................................................................... 10

CHAPTER 1: INTRODUCTION ............................................................................................................ 12

1.1 POWER DISTRIBUTION SECTOR-SNAPSHOT .............................................................................. 12

1.2 OBJECTIVE OF THE PROJECT: ............................................................................................................... 13

1.3 SCOPE OF THE PROJECT: ......................................................................................................................... 13

1.4 SIGNIFICANCE OF THE PROJECT: ......................................................................................................... 14

CHAPTER 2: INTRODUCTION TO THE ORGANISATION ........................................................... 15

2.1 ABOUT THE ORGANISATION: ................................................................................................................. 15

2.1.1 CONSULTING SERVICES .............................................................................................................. 16

2.1.2 SOFTWARE DEVELOPMENT ....................................................................................................... 16

2.1.3 ONLINE SOFTWARE & KNOWLEDGE PROCESS OUTSOURCING .................................... 16

2.2 THE ICRA FACTOR: .................................................................................................................................... 17

2.3 IMACS-ENERGY: .......................................................................................................................................... 21

2.4 BRIEF DESCRIPTION ABOUT FUNCTIONAL AREAS: ....................................................................... 21

2.4.1 REFORM, REGULATION AND PUBLIC POLICY: .................................................................... 21

2.4.2 RISK MANAGEMENT: .................................................................................................................... 22

2.4.3 TRANSACTION SUPPORT: ............................................................................................................ 22

2.4.4 STRATEGY & OPERATIONS: ....................................................................................................... 23

CHAPTER 3: REVIEW OF EXISTING LITERATURE & RESEARCH METHODOLOGY ....... 25

3.1 LITERATURE REVIEW ............................................................................................................................... 25

3.1.1 NATIONAL TARIFF POLICY: ....................................................................................................... 25

3.1.2 NATIONAL ELECTRICITY POLICY: .......................................................................................... 25

3.1.3 OTHER LITERATURES .................................................................................................................. 26

3.2. RESEARCH METHODOLOGY .................................................................................................................. 28

3.2.1 FILTERING OF DATA ..................................................................................................................... 28

3.3 APPROACH .................................................................................................................................................... 30

3.4 RISK PROFILING OF STATES ................................................................................................................... 30

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 5

CHAPTER 4: FACTS AND ANALYSIS OF ANDHRA PRADESH ................................................... 31

4.1 OVERALL SCENARIO ................................................................................................................................. 31

4.1.1 General Background and Political Economy ................................................................................... 31

4.1.2 Power Sector – Overview & Evolution of Reforms ......................................................................... 32

4.1.3. Current Industry Structure .............................................................................................................. 32

4.2 APNPDCL ........................................................................................................................................................ 33

(Northern Power Distribution Company of Andhra Pradesh Ltd.) ................................................................. 33

4.2.1 Operational Performance .................................................................................................................. 34

4.2.2 Financial Performance ....................................................................................................................... 35

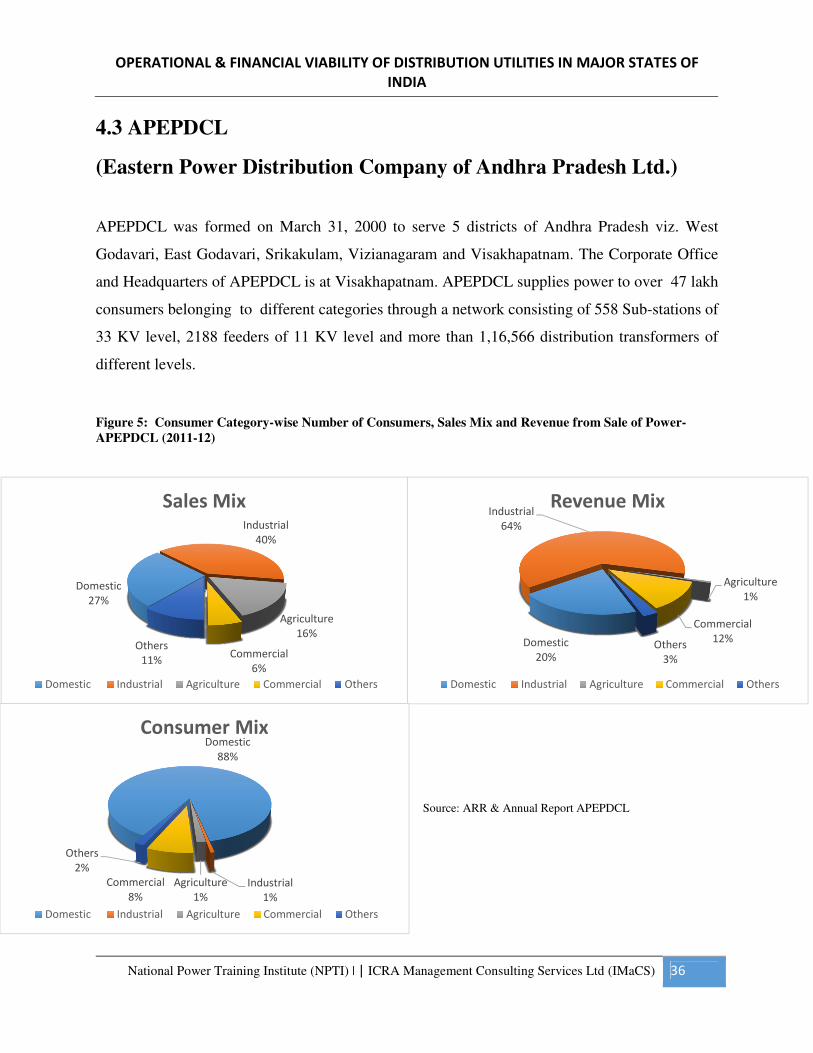

4.3 APEPDCL ........................................................................................................................................................ 36

(Eastern Power Distribution Company of Andhra Pradesh Ltd.) .................................................................... 36

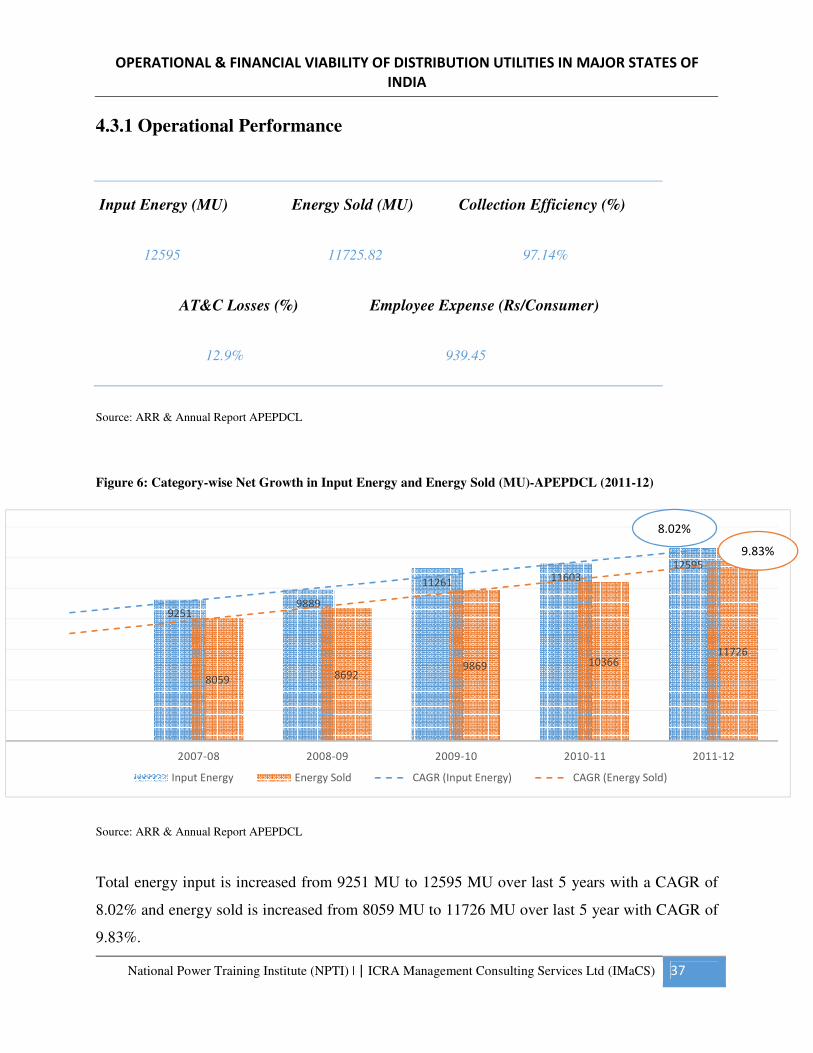

4.3.1 Operational Performance .................................................................................................................. 37

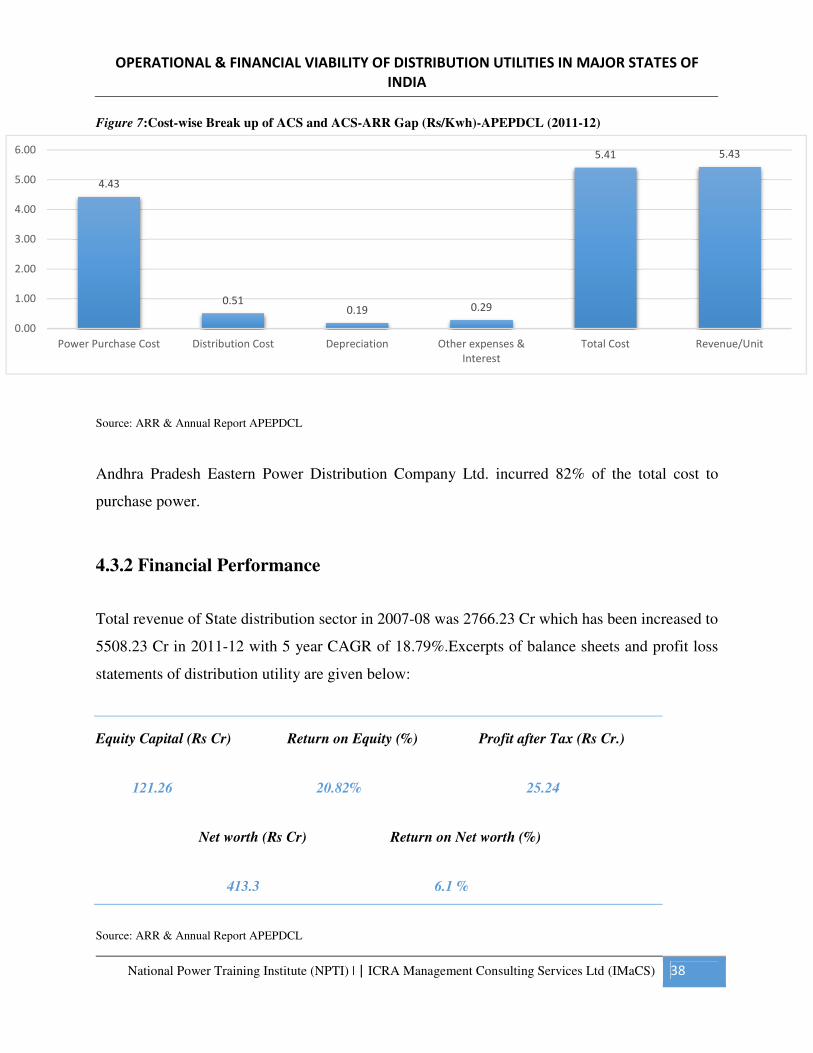

4.3.2 Financial Performance ....................................................................................................................... 38

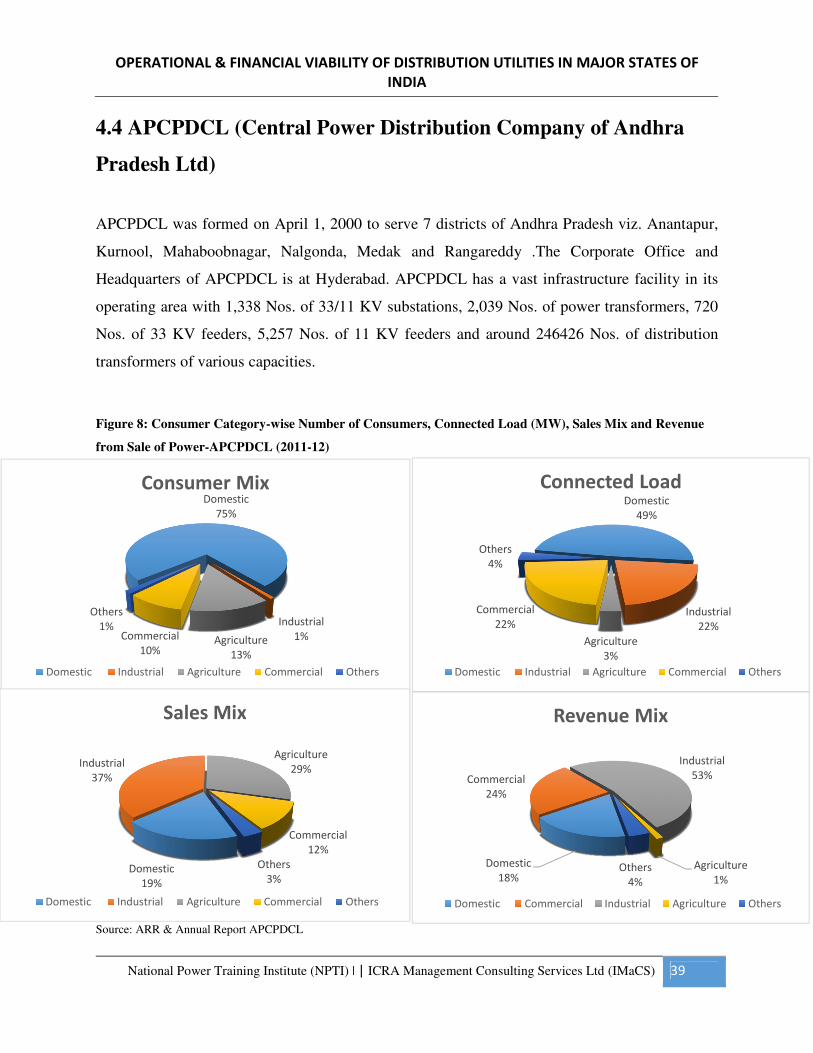

4.4 APCPDCL (Central Power Distribution Company of Andhra Pradesh Ltd) ........................................... 39

4.4.1 Operational Performance .................................................................................................................. 40

4.4.2 Financial Performance ....................................................................................................................... 41

Chapter 5: FACTS AND ANALYSIS OF GUJARAT .......................................................................... 43

5.1 OVERALL SCENARIO ................................................................................................................................. 43

5.1.1 General Background & Political Economy ...................................................................................... 43

5.1.2 Power Sector – Overview & Evolution of Reforms ......................................................................... 44

5.1.3 Current Industry Structure ............................................................................................................... 44

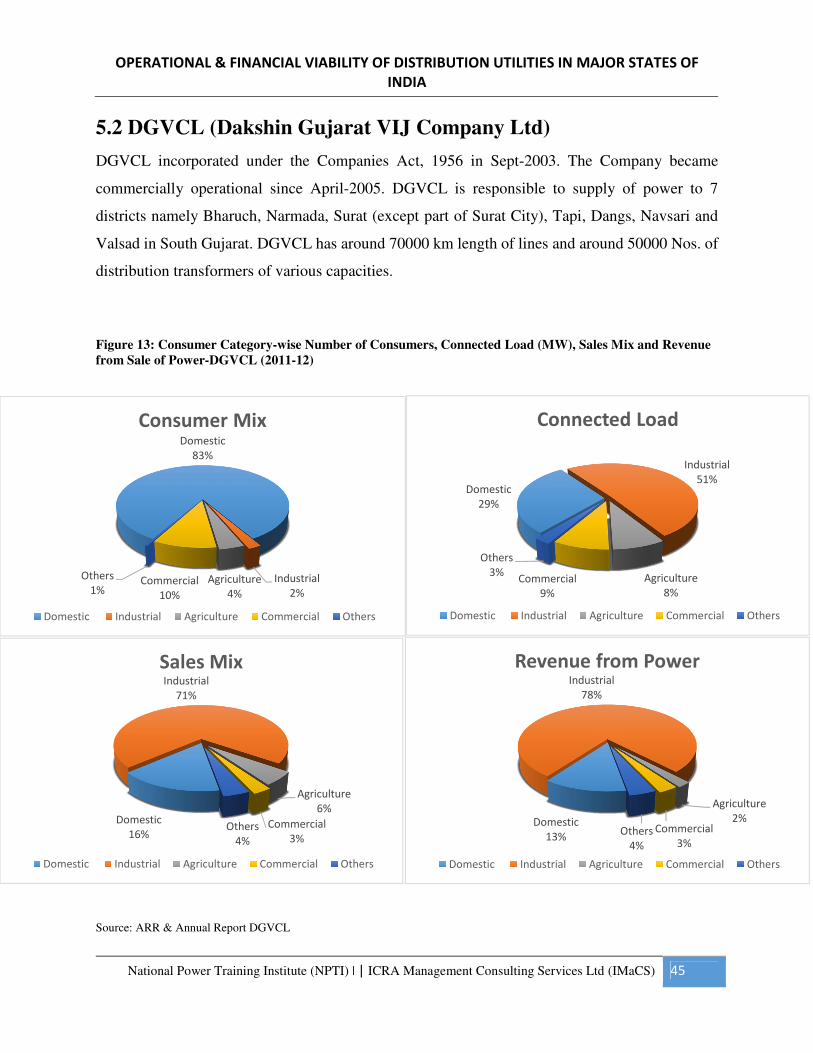

5.2 DGVCL (Dakshin Gujarat VIJ Company Ltd) ............................................................................................ 45

5.2.1 Operational Performance .................................................................................................................. 46

5.2.2 Financial Performance ....................................................................................................................... 47

5.3 PGVCL (Paschim Gujarat Vij Company Ltd) ............................................................................................. 48

5.3.1 Operational Performance .................................................................................................................. 49

5.2.2 Financial Performance ....................................................................................................................... 50

Chapter 6: FACTS AND ANALYSIS OF MAHARASHTRA ............................................................. 52

6.1 OVERALL SCENARIO ................................................................................................................................. 52

6.1.1 General Background & Political Economy ...................................................................................... 52

6.1.2 Power Sector – Overview & Evolution of Reforms ......................................................................... 53

6.1.3. Current Industry Structure .............................................................................................................. 53

6.2 MSEDCL (Maharashtra State Electricity Distribution Company Ltd) ..................................................... 54

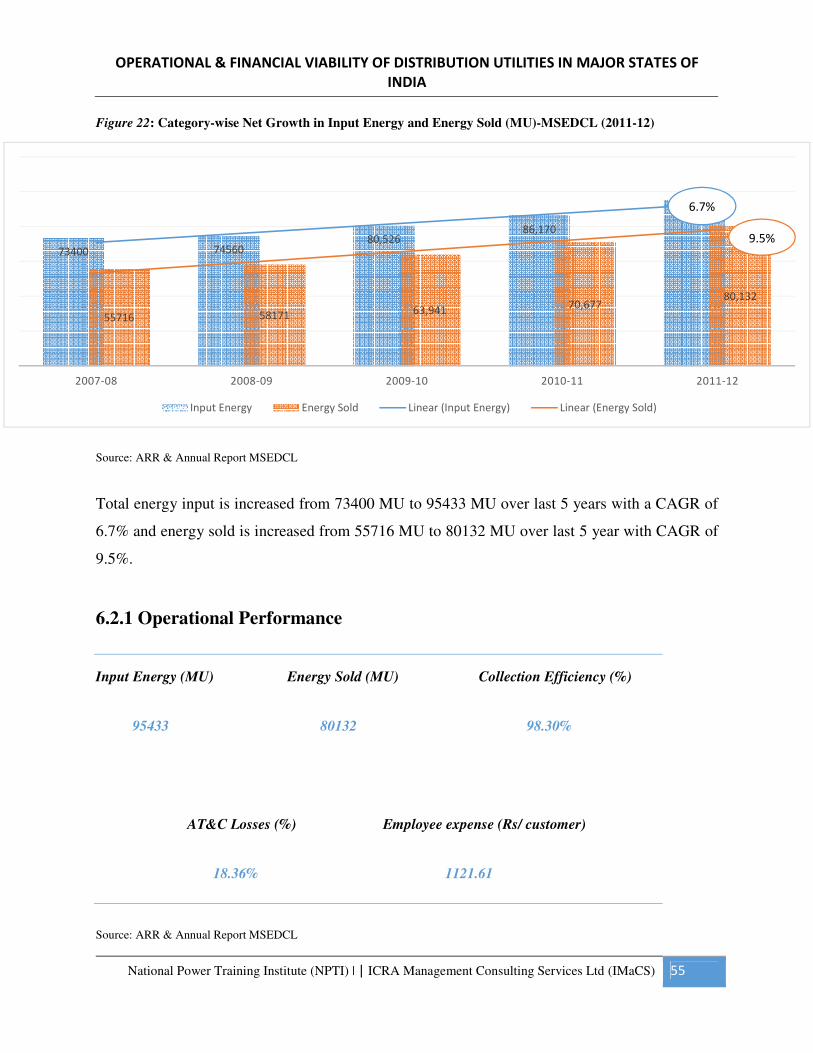

6.2.1 Operational Performance .................................................................................................................. 55

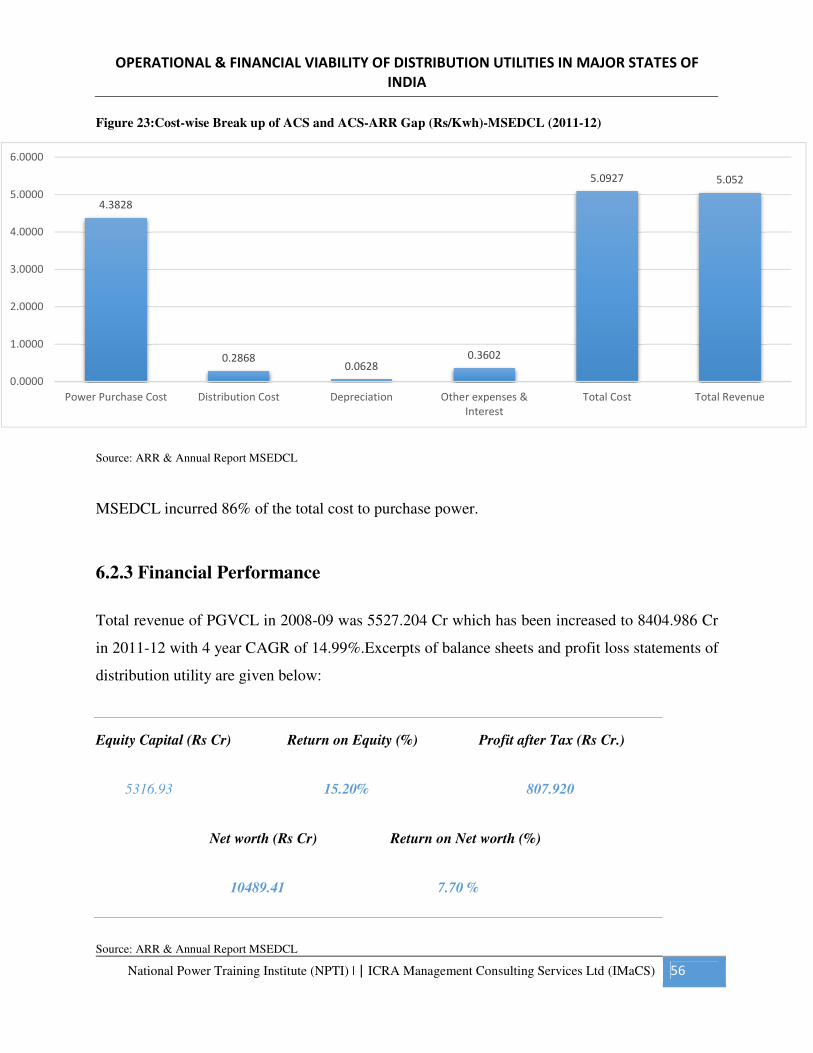

6.2.3 Financial Performance ....................................................................................................................... 56

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 6

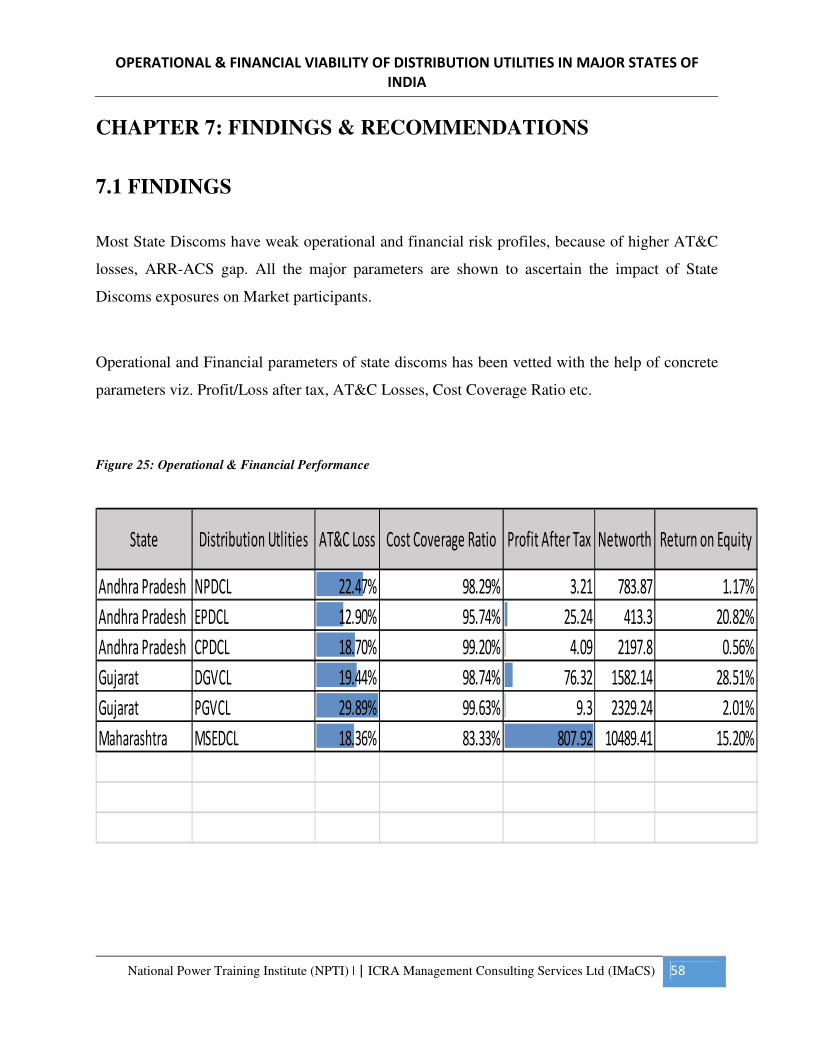

CHAPTER 7: FINDINGS & RECOMMENDATIONS ........................................................................ 58

7.1 FINDINGS ....................................................................................................................................................... 58

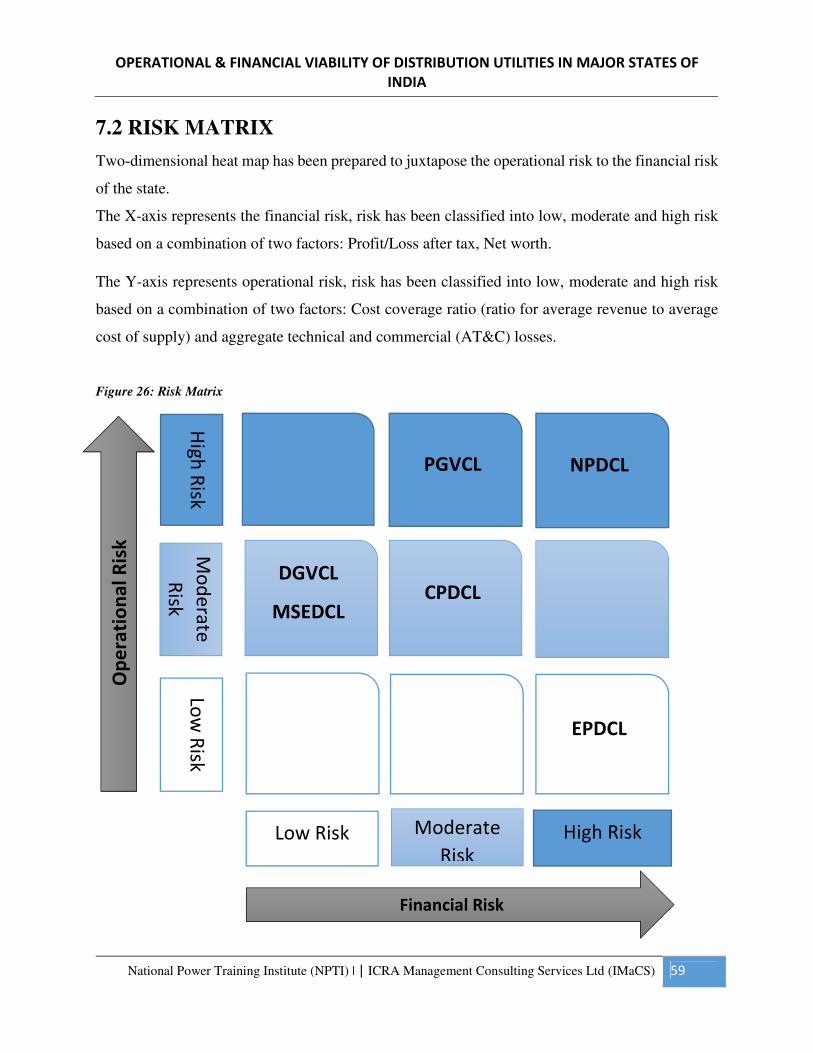

7.2 RISK MATRIX ............................................................................................................................................... 59

7.3 RECOMMENDATIONS: ............................................................................................................................... 60

BIBLIOGRAPHY & REFERENCES ..................................................................................................... 61

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 7

LIST OF FIGURES

Figure 1: Distribution Reforms-AP............................................................................................................. 32

Figure 2: Consumer Category-wise Number of Consumers, Connected Load (MW), Sales Mix and

Revenue from Sale of Power-APNPDCL (2011-12) .................................................................................. 33

Figure 3: Category-wise Net Growth in Input Energy and Energy Sold (MU)-APNPDCL (2011-12) ...... 34

Figure 4:Cost-wise Break up of ACS and ACS-ARR Gap (Rs/Kwh)-APNPDCL (2011-12) .................... 35

Figure 5: Consumer Category-wise Number of Consumers, Sales Mix and Revenue from Sale of Power-

APEPDCL (2011-12) .................................................................................................................................. 36

Figure 6: Category-wise Net Growth in Input Energy and Energy Sold (MU)-APEPDCL (2011-12) ...... 37

Figure 7:Cost-wise Break up of ACS and ACS-ARR Gap (Rs/Kwh)-APEPDCL (2011-12) .................... 38

Figure 8: Consumer Category-wise Number of Consumers, Connected Load (MW), Sales Mix and

Revenue from Sale of Power-APCPDCL (2011-12) .................................................................................. 39

Figure 9: Category-wise Net Growth in Input Energy and Energy Sold (MU)-APCPDCL (2011-12) ...... 40

Figure 10: Cost-wise Break up of ACS and ACS-ARR Gap (Rs/Kwh)-APCPDCL (2011-12) ................. 41

Figure 11: SNAPSHOT – ANDHRA PRADESH ...................................................................................... 42

Figure 12: Distribution Reforms-Gujarat .................................................................................................... 44

Figure 13: Consumer Category-wise Number of Consumers, Connected Load (MW), Sales Mix and

Revenue from Sale of Power-DGVCL (2011-12) ...................................................................................... 45

Figure 14: Category-wise Net Growth in Input Energy and Energy Sold (MU)-DGVCL (2011-12) ........ 46

Figure 15:Cost-wise Break up of ACS and ACS-ARR Gap (Rs/Kwh)-DGVCL (2011-12) ...................... 47

Figure 16: Consumer Category-wise Number of Consumers, Connected Load (MW), Sales Mix and

Revenue from Sale of Power-PGVCL (2011-12) ....................................................................................... 48

Figure 17: Category-wise Net Growth in Input Energy and Energy Sold (MU)-PGVCL (2011-12) ......... 49

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 8

Figure 18: Cost-wise Break up of ACS and ACS-ARR Gap (Rs/Kwh)-PGVCL (2011-12) ...................... 50

Figure 19: SNAPSHOT – GUJARAT ........................................................................................................ 51

Figure 20: Distribution Reforms-Maharashtra ............................................................................................ 53

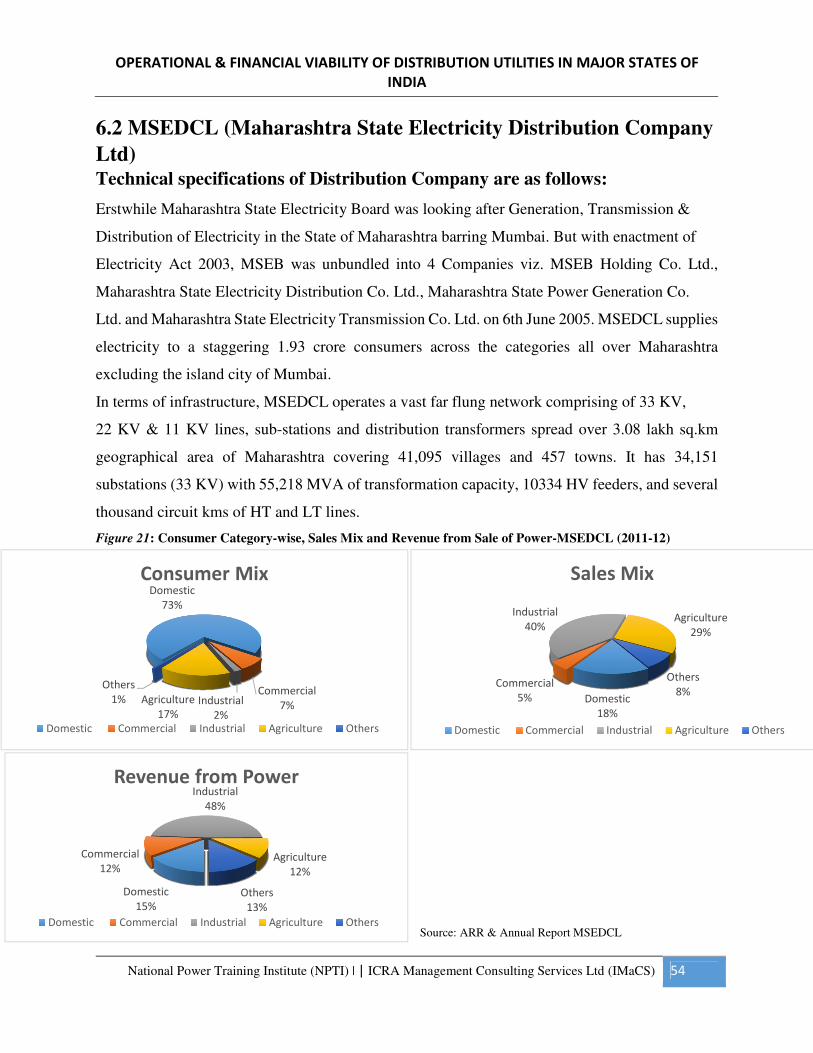

Figure 21: Consumer Category-wise, Sales Mix and Revenue from Sale of Power-MSEDCL (2011-12) 54

Figure 22: Category-wise Net Growth in Input Energy and Energy Sold (MU)-MSEDCL (2011-12) ...... 55

Figure 23:Cost-wise Break up of ACS and ACS-ARR Gap (Rs/Kwh)-MSEDCL (2011-12) .................... 56

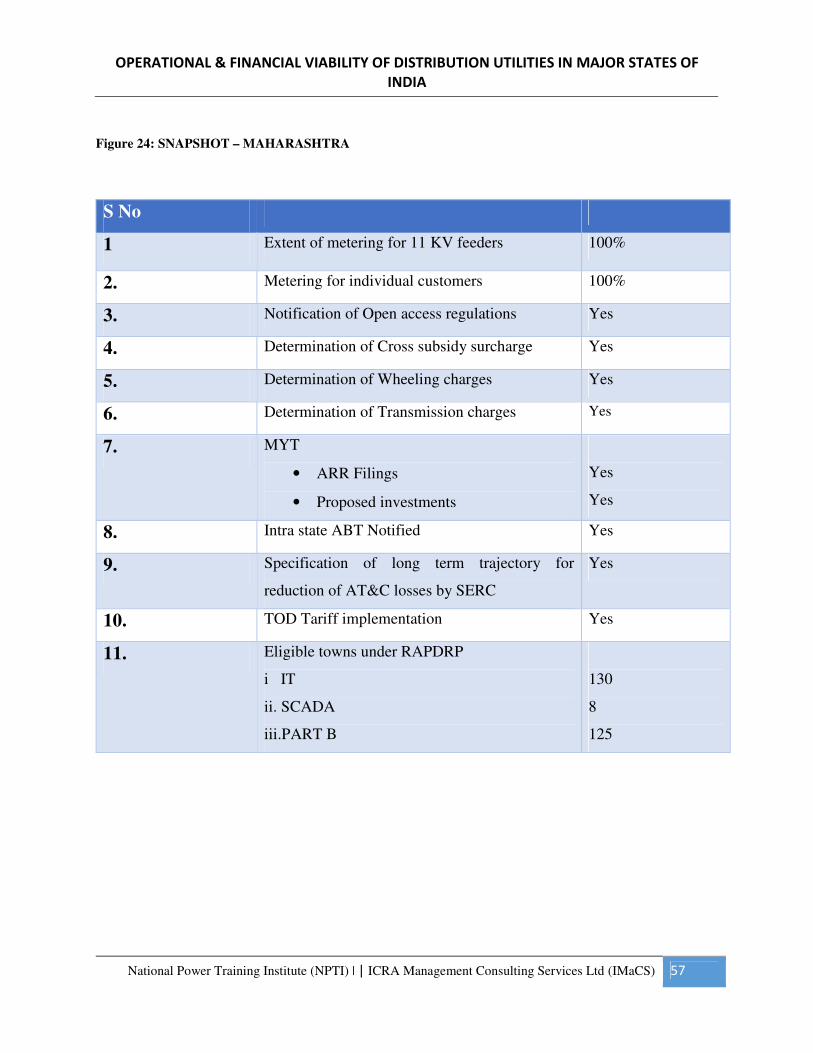

Figure 24: SNAPSHOT – MAHARASHTRA ............................................................................................ 57

Figure 25: Operational & Financial Performance ....................................................................................... 58

Figure 26: Risk Matrix ................................................................................................................................ 59

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 9

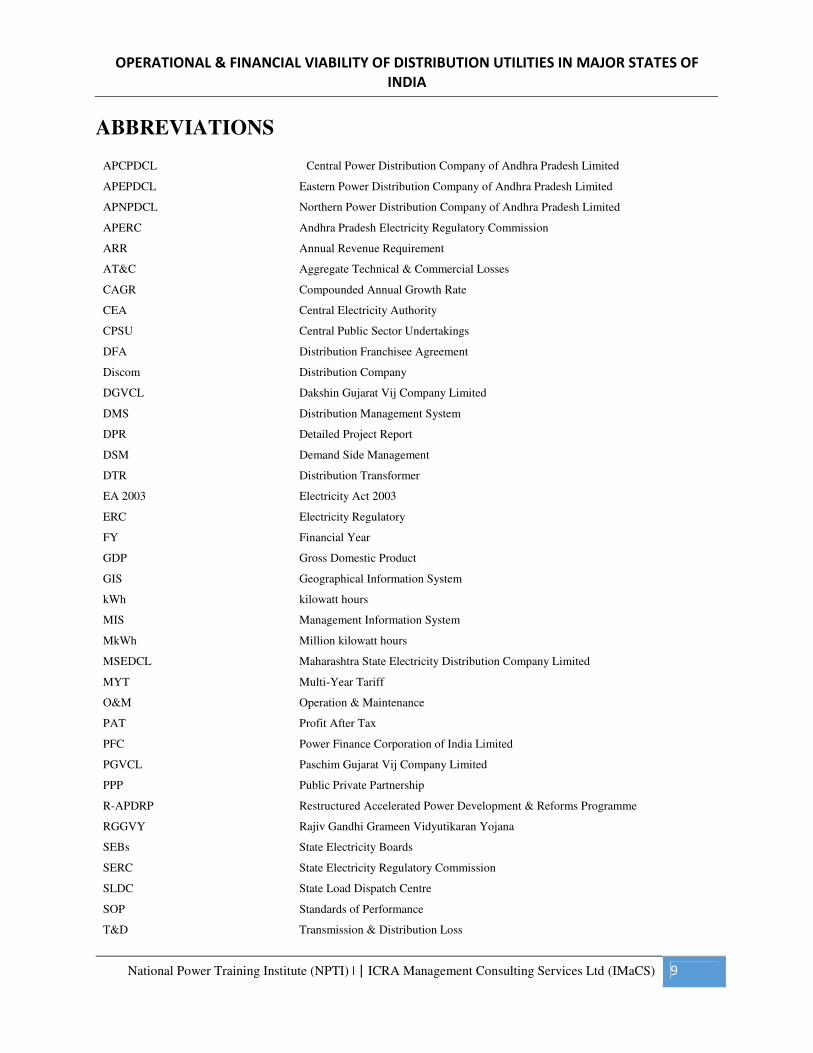

ABBREVIATIONS

APCPDCL Central Power Distribution Company of Andhra Pradesh Limited

APEPDCL Eastern Power Distribution Company of Andhra Pradesh Limited

APNPDCL Northern Power Distribution Company of Andhra Pradesh Limited

APERC Andhra Pradesh Electricity Regulatory Commission

ARR Annual Revenue Requirement

AT&C Aggregate Technical & Commercial Losses

CAGR Compounded Annual Growth Rate

CEA Central Electricity Authority

CPSU Central Public Sector Undertakings

DFA Distribution Franchisee Agreement

Discom Distribution Company

DGVCL Dakshin Gujarat Vij Company Limited

DMS Distribution Management System

DPR Detailed Project Report

DSM Demand Side Management

DTR Distribution Transformer

EA 2003 Electricity Act 2003

ERC Electricity Regulatory

FY Financial Year

GDP Gross Domestic Product

GIS Geographical Information System

kWh kilowatt hours

MIS Management Information System

MkWh Million kilowatt hours

MSEDCL Maharashtra State Electricity Distribution Company Limited

MYT Multi-Year Tariff

O&M Operation & Maintenance

PAT Profit After Tax

PFC Power Finance Corporation of India Limited

PGVCL Paschim Gujarat Vij Company Limited

PPP Public Private Partnership

R-APDRP Restructured Accelerated Power Development & Reforms Programme

RGGVY Rajiv Gandhi Grameen Vidyutikaran Yojana

SEBs State Electricity Boards

SERC State Electricity Regulatory Commission

SLDC State Load Dispatch Centre

SOP Standards of Performance

T&D Transmission & Distribution Loss

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 10

EXECUTIVE SUMMARY

Electricity is the fulcrum of economic development in any country. India has installed power

generation capacity of 210 GW as on November 30, 2012, which is about 154 times the installed

capacity in 1947 (1362 MW). Electricity generation growth has been steadily improving year after

year, and in the year 2011-12, the total electricity generation was about 876.8 billion units of

energy with a growth of around 8% over the previous year. During the XI plan, the power sector

made considerable progress with a capacity addition of approximately 58 GW which was

significantly more than the capacity commissioned in the previous plans. Such an improvement in

performance was possible mainly because of strong private sector participation.

However, India still faces the challenge of poor reliability and quality of electricity, leading to

occasional blackouts. Even as availability of power has increased substantially with significant

investments on the supply side, the demand has consistently outstripped supply.

Distribution and Retail Supply is the most critical link in the electricity market, which interfaces

with the end-customers and provides revenue for the entire value chain. It owes to the fact of

sustenance of other elements in the sector such as generation, transmission, equipment

manufacturing; which depends on its operational performance and commercial viability. However,

despite of its critical importance, generation segment has always been on the agenda of the

government, in light of high energy deficit, necessitating need of huge capacity addition. Lack of

focus has resulted in poor operational and financial performance of the sector, thereby creating

greater need of sector transformation, with high calls for private participation in terms of Private

Franchising, Public-Private-Partnership (PPP) and Equipment Suppliers. As a result, tremendous

opportunities lie on fore in the sector, for various stakeholders.

The weakest part of the power sector remains distribution, which is incurring large losses. AT&C

losses are reported to be around 24 percent. This leads to high financial losses. The constant losses

of State Electricity Boards have created a debt trap. The estimated total loss run up by the SEBs

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 11

has been pegged at Rs 2.4 lakh Crores.These are likely to rise to even higher levels because of the

increasing share of short-term purchase of power at high prices and losses have been funded largely

by short-term loans from banks/financial institutions, and discoms with their weak financial

position seem incapable of repaying these loans.

The report will develop a better understanding of the reasons for continued under-performance of

the sector on key dimensions. This report aimed at identifying successful state’s utilities and

learning from their experience. More specifically, the review will examine the implementation of

reforms, current operational and financial scenario of states and risk profiling of these states on

the basis of these performances.

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 12

CHAPTER 1: INTRODUCTION

1.1 POWER DISTRIBUTION SECTOR-SNAPSHOT

Distribution and retail supply is the most important cog in the power sector value chain which

interfaces with end customers and provides revenue for the entire value chain. Indian electricity

distribution caters to nearly 200 million consumers with a connected load of about 400 GW that

places the country among the largest electricity consumer bases in the world. The consumers are

served by around 73 distribution utilities – 13 electricity departments, 17 private distribution

companies, 40 corporatized distribution companies and 3 State Electricity Boards. Sustenance of

other elements in the sector like generation, transmission, equipment manufacturing is dependent

on the commercial performance and financial viability of the distribution sector in India. Over the

past 15-16 years, a number of states have worked to improve the commercial performance of their

state utilities, unbundling state entities, creating independent regulatory systems, and putting in

place measures to control losses and theft. However, progress has been difficult, and slower than

envisaged

“India’s power sector is a leaking bucket; the holes deliberately crafted and the leaks carefully

collected as economic rents by various stakeholders that control the system. The logical thing to

do would be to fix the bucket rather than to persistently emphasize shortages of power and forever

make exaggerated estimates of future demands for power. Most initiatives in the power sector

(IPPs and mega power projects) are nothing but ways of pouring more water into the bucket so

that the consistency and quantity of leaks are assured...”

Twenty years after reforms were introduced in the Indian electricity sector, the above remark still

holds good. The ‘bucket’ in the above remark is the Indian electricity distribution sector, which

consumes no matter how much is generated, without adequately compensating the producers of

electricity for the same.

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 13

Recently, Planning Commission had appointed a High Level Panel headed by Shri V.K. Shunglu,

former Comptroller &Auditor General in July, 2010 to look into the financial problems of State

Electricity Boards and to identify corrective steps. The terms of reference of this Committee

included reviewing the accounts of State Electricity Boards and State Distribution Companies as

on March, 2010 and to project their losses by 2017, reviewing the electricity tariff and also

examining the role of the State Governments, Electricity Regulatory Commissions and

Distribution Companies, assessing system improvement measures accomplished in distribution of

power etc. and finally, to recommend a plan of action to achieve financial viability in distribution

of power by 2017. The Shunglu Committee presented its Report to the Deputy Chairman, Planning

Commission on 15 December, 2011.It is time that we look at the underlying problems of this sector

and constructively work towards removing the bottlenecks to make it more efficient and customer

oriented.

1.2 OBJECTIVE OF THE PROJECT:

• To get a Policy & Regulatory Overview of the distribution sector in major states of India.

• To analyze the operational and financial performance of the respective state SEBs and compare

them accordingly on various parameters.

1.3 SCOPE OF THE PROJECT:

The scope of this project includes the following:

• This project covers 3 major states and 6 distribution utilities of India which play a key role in

distribution sector.

• To study the various regulations and policies implemented by the state from time to time.

• To assess comparatively, the operational and financial performance of various SEBs

• Risk profiling of the states on the basis of operational and financial performance.

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 14

1.4 SIGNIFICANCE OF THE PROJECT:

There have been huge financial losses incurring to the state SEBs in the recent years.

Reduction of AT&C losses remains a major problem in almost every state. It is also very important

that the state actually implements various policies and different regulations from time to time. This

study helps us to locate the various drawbacks of state utilities, their operational and financial

performance and a comparison among the state utilities finally shows where the utilities of the

states stand upon.

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 15

CHAPTER 2: INTRODUCTION TO THE ORGANISATION

2.1 ABOUT THE ORGANISATION:

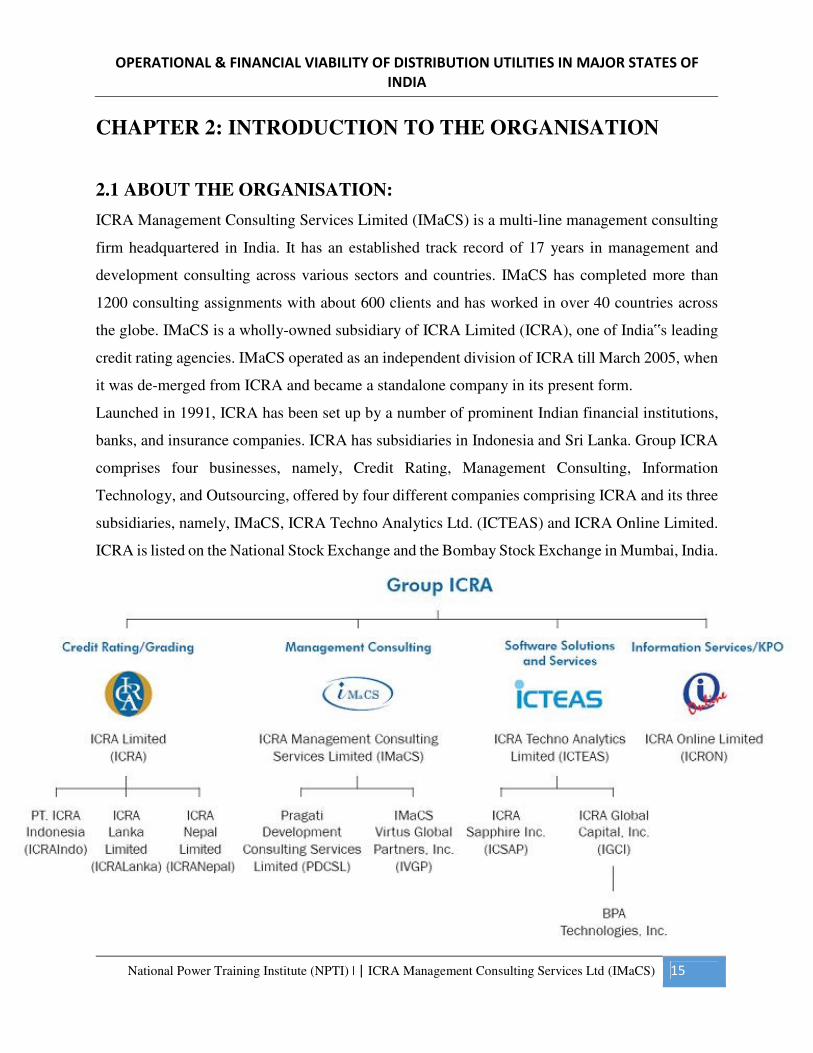

ICRA Management Consulting Services Limited (IMaCS) is a multi-line management consulting

firm headquartered in India. It has an established track record of 17 years in management and

development consulting across various sectors and countries. IMaCS has completed more than

1200 consulting assignments with about 600 clients and has worked in over 40 countries across

the globe. IMaCS is a wholly-owned subsidiary of ICRA Limited (ICRA), one of India‟s leading

credit rating agencies. IMaCS operated as an independent division of ICRA till March 2005, when

it was de-merged from ICRA and became a standalone company in its present form.

Launched in 1991, ICRA has been set up by a number of prominent Indian financial institutions,

banks, and insurance companies. ICRA has subsidiaries in Indonesia and Sri Lanka. Group ICRA

comprises four businesses, namely, Credit Rating, Management Consulting, Information

Technology, and Outsourcing, offered by four different companies comprising ICRA and its three

subsidiaries, namely, IMaCS, ICRA Techno Analytics Ltd. (ICTEAS) and ICRA Online Limited.

ICRA is listed on the National Stock Exchange and the Bombay Stock Exchange in Mumbai, India.

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 16

2.1.1 CONSULTING SERVICES

ICRA Management Consulting Services Limited (IMaCS), a wholly-owned subsidiary of ICRA

Limited, is a multi-line consulting firm with a global operating footprint. IMaCS offers Consulting

Services in Strategy, Risk Management, Regulatory Economics, Transaction Advisory, and

Process Re-engineering. IMaCS' clientele includes Banks & Financial Service Companies,

Corporate Entities, Institutional Investors, Governments, Regulators, and Multilateral Agencies.

Besides India, IMaCS has consulting experience across 35 countries in South East Asia, Northern

Asia, West Asia, Africa, Western Europe, and North America.

2.1.2 SOFTWARE DEVELOPMENT

ICRA Techno Analytics Limited (ICTEAS), a subsidiary of ICRA Limited, offers a complete

portfolio of Information Technology (IT) solutions to meet the dynamic needs of present-day

businesses. The services range from the traditional development of client-server, web-centric and

mobile applications to the generation of cutting-edge business analytics.

Axiom Technologies Private Limited, a wholly-owned subsidiary of ICTEAS specializes in

customization and implementation services on Oracle E-Business Suite. Its services include

process study, fitment analysis, customization, implementation, and post implementation

maintenance services.

2.1.3 ONLINE SOFTWARE & KNOWLEDGE PROCESS OUTSOURCING

ICRA Online Limited (Online) is a leading information services, outsourcing solutions provider

and technology solutions provider and caters for some of the biggest names in the financial services

sector in India and abroad, which is a testimony to its product quality, commitment and credibility.

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 17

Online has two Strategic Business Units (SBUs) with a list of reputed global and domestic clients:

• The Information Services and Technology Solutions Division (MFI Division)

• The Knowledge Process Outsourcing Division (KPO Division)

The MFI Division leverages its domain expertise to provide high quality technology solutions, in

the form of products, to a large number of Banks, Mutual Funds, Financial Institutions, Third Party

Products‟ Distributors, Insurance Companies, Investment Advisors, Portfolio Managers, Stock

Brokers, Treasury Managers, and Academic Institutions, among others.

The KPO Division of Online offers Knowledge Process Outsourcing services that combine

advanced analytical abilities and deep domain expertise to deliver value by translating data and

information into structured business inputs.

2.2 THE ICRA FACTOR:

Facilitating efficiency in business ICRA information products, Ratings, and solutions reflect

independent, professional and impartial opinions, which assist businesses enhance the quality of

their decisions and help issuers access a broader investor base and even lesser known companies

approach the money and capital markets. They strongly believe that quality and authenticity of

information are derivatives of an organization’s research base. We have dedicated teams for

Monetary, Fiscal, Industry and Sector research, and a panel of Advisors to enhance our in-house

capabilities. Our research base enables us to maintain the highest standards of quality and

credibility committed to the development of the financial market.

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 18

IMACS

(ICRA MANAGEMENT CONSULTING SERVICES LIMITED)

“Two significant feature of IMaCS growth story are that their large

Number of repeat clients and a high level of referral work”

IMaCS (ICRA Management Consulting Services Limited) is a wholly-owned subsidiary of ICRA

Limited (referred to as ICRA in this document)

• IMaCS is a management consulting firm headquartered in India.

• Seven offices in India and an operating footprint across 35 countries.

• Over the past 15 years, IMaCS has completed about 900 projects with 400 clients.

• IMaCS operated as a division of ICRA till March 31, 2005 when it was demerged.

• The clients comprise Governments, multilateral agencies, regulators and banks, corporate

and institutional investors.

• Three lines of service: (1) Consulting (2) Analytics (3) Transaction Advisory.

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 19

• Expertise in Strategy, Risk Analytics, Process Re-engineering, Corporate Finance,

Regulatory Economics, and Development Consulting.

• IMaCS has executed assignments for multilateral agencies such as The World Bank, World

Bank Institute (WBI), Commonwealth Development Corporation (CDC), United Nations

Development Programme (UNDP), United States Agency for International Development

(USAID), Department for International Development (DfID), African Development Bank

(AfDB), Asian Development Bank (ADB) and International Finance Corporation (IFC).

• The main driver for IMaCS ‟ growth has been a growing need for unbiased and

professional views on adopting best business practices arising from economic deregulation,

growing international trade & integration, and the increasing need to be globally

competitive. Building on a carefully nurtured knowledge bank of global benchmarks for

business and management practices and a repository of high-quality analytical talent,

iMaCS has executed over 700 consulting assignments for a variety of Indian and

international organizations, Governments, and regulatory authorities

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 20

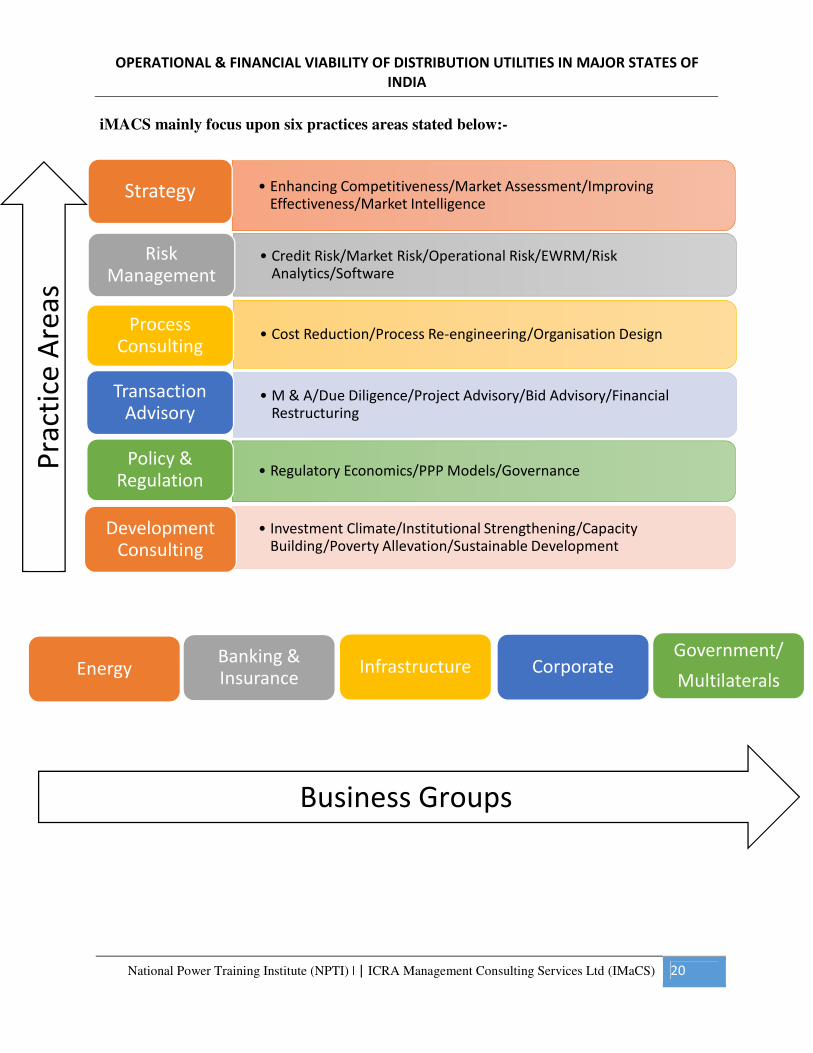

iMACS mainly focus upon six practices areas stated below:-

• Enhancing Competitiveness/Market Assessment/Improving Effectiveness/Market Intelligence

Strategy

• Credit Risk/Market Risk/Operational Risk/EWRM/Risk Analytics/Software

Risk Management

• Cost Reduction/Process Re-engineering/Organisation DesignProcess

Consulting

• M & A/Due Diligence/Project Advisory/Bid Advisory/Financial Restructuring

Transaction Advisory

• Regulatory Economics/PPP Models/GovernancePolicy &

Regulation

• Investment Climate/Institutional Strengthening/Capacity Building/Poverty Allevation/Sustainable Development

Development Consulting

Banking & Insurance

Infrastructure CorporateGovernment/

MultilateralsEnergy

Business Groups

Pra

ctic

e A

rea

s

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 21

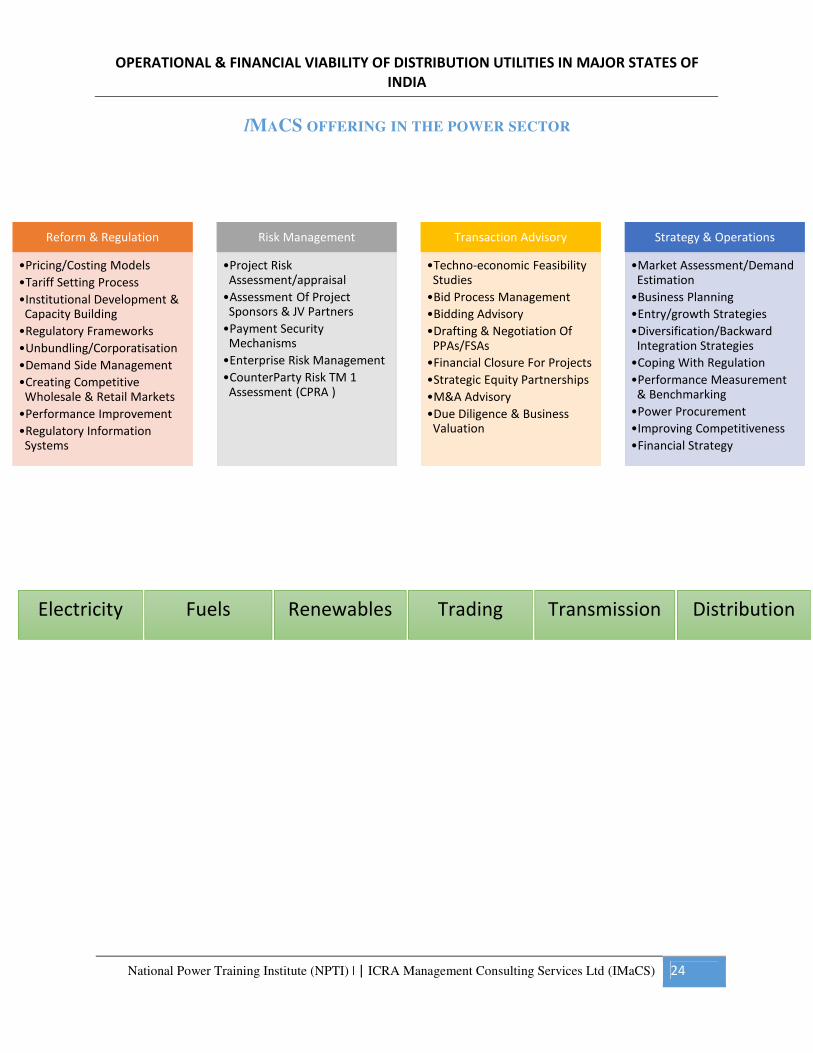

2.3 IMACS-ENERGY:

IMaCS Consulting Services in the Power Sector

IMaCS Energy Group is a leading provider of policy, regulatory consulting and transaction

advisory services to various stakeholders in the Energy sector. With a core team of in-house

consultants and partnerships with national and international organizations, IMaCS Energy

Group strives to help its clients become more competitive, effective and successful. Service which

ICRA offers are grouped across the following four broad functional areas:

• Reform & Regulation

• Risk Management

• Transaction/Project Advisory and

• Strategy & Operations.

Their services in the Power sector include restructuring vertically integrated state owned

enterprises, privatization of utilities, building capacity of public institutions, developing PPP

mechanisms, assisting project developers by providing project/financial advisory services,

providing strategic advice to utilities, and in fuel management.

2.4 BRIEF DESCRIPTION ABOUT FUNCTIONAL AREAS:

2.4.1 REFORM, REGULATION AND PUBLIC POLICY:

IMaCS assists governments, regulators and utilities seeking to establish and strengthen energy

sector reforms, which involves

• Policy analysis and formulation

• Market structure and competition

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 22

• Regulatory frameworks

• Pricing

• Power sector restructuring

• Institutional reform

• Private sector participation

• Financial and operational restructuring

2.4.2 RISK MANAGEMENT:

IMaCS offers diagnostic and advisory services to project sponsors, developers, regulators,

financiers, and other parties by making a comprehensive analysis of project risks, which includes

• Risk assessment and mitigation

• Assessment of project sponsors and JV partners

• Credit risk assessment

• Investment risk assessment for equity/debt

• Payment security mechanisms

• Evaluation of credit structure

• Fuel price risk management

2.4.3 TRANSACTION SUPPORT:

IMaCS assists both governments in promoting private sector participation as well as private

developers to participate in infrastructure development through contract /project structuring,

designing / reviewing concession agreements, and structuring solutions for payment and security

mechanisms, developing financial models, assessing risks and providing assistance in bidding for

energy sector projects. Service offerings in this function include

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 23

• Investment advisory

• Project valuation

• Project / structured finance – debt, equity, mezzanine finance, credit enhancement

• Preparation of bid documents

• Evaluation of bids

• Preparation and review of contractual agreements

• EPC bid-process management

• Power Purchase Agreements

• Fuel Supply Agreements

2.4.4 STRATEGY & OPERATIONS:

IMaCS helps its clients to decide which lines of business to pursue; to decide their entry strategy

into the energy sector, to divest assets no longer consistent with their strategy; to improve

operational efficiency and productivity and to develop sourcing, bidding, trading, and contracting

strategies. Service offerings include

• Business plans for utilities

• Power and fuel market assessment

• Organizational design and restructuring

• Performance measurement and benchmarking

• Process improvement

• Operational strategy

• Competitiveness study

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 24

IMACS OFFERING IN THE POWER SECTOR

Reform & Regulation

•Pricing/Costing Models

•Tariff Setting Process

•Institutional Development & Capacity Building

•Regulatory Frameworks

•Unbundling/Corporatisation

•Demand Side Management

•Creating Competitive Wholesale & Retail Markets

•Performance Improvement

•Regulatory Information Systems

Risk Management

•Project Risk Assessment/appraisal

•Assessment Of Project Sponsors & JV Partners

•Payment Security Mechanisms

•Enterprise Risk Management

•CounterParty Risk TM 1 Assessment (CPRA )

Transaction Advisory

•Techno-economic Feasibility Studies

•Bid Process Management

•Bidding Advisory

•Drafting & Negotiation Of PPAs/FSAs

•Financial Closure For Projects

•Strategic Equity Partnerships

•M&A Advisory

•Due Diligence & Business Valuation

Strategy & Operations

•Market Assessment/Demand Estimation

•Business Planning

•Entry/growth Strategies

•Diversification/Backward Integration Strategies

•Coping With Regulation

•Performance Measurement & Benchmarking

•Power Procurement

•Improving Competitiveness

•Financial Strategy

Electricity Fuels Renewables Trading Transmission Distribution

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 25

CHAPTER 3: REVIEW OF EXISTING LITERATURE &

RESEARCH METHODOLOGY

3.1 LITERATURE REVIEW

3.1.1 NATIONAL TARIFF POLICY:

Supply of reliable and quality power of specified standards in an efficient manner and at reasonable

rates is one of the main objectives of the National Electricity Policy. The State Commission should

determine and notify the standards of performance of licensees with respect to quality, continuity

and reliability of service for all consumers. Making the distribution segment of the industry

efficient and solvent is the key to success of power sector reforms and provision of services of

specified standards. Therefore, the Regulatory Commissions need to strike the right balance

between the requirements of the commercial viability of distribution licensees and consumer

interests. Loss making utilities need to be transformed into profitable ventures which can raise

necessary resources from the capital markets to provide services of international standards to

enable India to achieve its full growth potential.

• Implementation of MYT Framework

• Framework for revenue and cost requirements

• Tariff design: Linkage of cost to service

• Cross subsidy surcharge and additional surcharge for open access

3.1.2 NATIONAL ELECTRICITY POLICY:

The Act provides for a robust regulatory framework for distribution licensees to safeguard

consumer interests. It also creates a competitive framework for the distribution business, offering

options to consumers, through the concepts of open access and multiple licensees in the same area

of supply. Multi-Year Tariff (MYT) framework is an important structural incentive to minimize

risks for utilities and consumers, promote efficiency and rapid reduction of system losses. It would

serve public interest through economic efficiency and improved service quality. A time-bound

programme should be drawn up by the State Electricity Regulatory Commissions (SERC) for

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 26

segregation of technical and commercial losses through energy audits resort to cherry picking by

demanding unreasonable connection charges from consumers.

The Act mandates supply of electricity through a correct meter within a stipulated period. The

Authority should develop regulations as required under Section 55 of the Act within three months.

The Act requires all consumers to be metered within two years. SCADA and data management

systems are useful for efficient working of Distribution Systems. High Voltage Distribution

System is an effective method for reduction of technical losses, prevention of theft, improved

voltage profile and better consumer service. It should be promoted to reduce LT/HT ratios keeping

in view the techno economic considerations.

3.1.3 OTHER LITERATURES

Anoop Singh in his studies - Policy Environment and Regulatory Reforms for Private and Foreign

Investment in Developing Countries: A Case of the Indian Power Sector undertook a review of the

policy and regulatory developments in the Indian power sector. A review of the literature and a

comparative policy analysis helped us to unravel some of the lessons to be learned for the process

of reform in developing countries in general. The initial phase of power sector reform in India

allowed commercially-oriented IPPs to sell power to financially weak SEBs, which do not rely on

sound commercial principles. This marriage of convenience is not sustainable. The experience of

private sector investment in Latin American countries relied on the introduction of commercial

interest in the bulk power market by inviting IPPs as well as introducing commercial principles at

the end of buyer utilities through their divestiture. The long-term interest of the consumers can

only be served if reasonably priced electricity is available over the long-run. Political interests

would best be served by depoliticizing tariffs, which would be beneficial to consumers in the long-

term through improved quality and reliability of supply. Given the objective to electrify all villages

by 2010 and to double the generating capacity in the country by 2012, the need to improve the

policy environment and strengthen the regulatory framework cannot be ignored.

Sanjeeb Kumar Dey in his studies – Revenue Sustainability through Electricity Distribution

Franchisee; suggested that after completing the infrastructure development, improving the quality

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 27

of services than the third step of revenue sustainability i.e bridge the gap of revenue and

expenditure is again a mind boggling task. It is imperative to bridge the gap and there are three

easy ways: Increase the Tariff – the consumer has to pay more – impossible for the rural

consumers, Government Subsidies – the taxpayer has to pay more – not acceptable under the

present arena when the taxpayer are paying more and Utilities bearing the gap – till the coffer

extinct- again U turn to the pre-reform era. To address the above it’s only imperative towards the

approach of Revenue sustainability. They also explain the distribution franchisee functioning with

the help of SHGs and contribution towards revenue sustainability in Electricity sector.

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 28

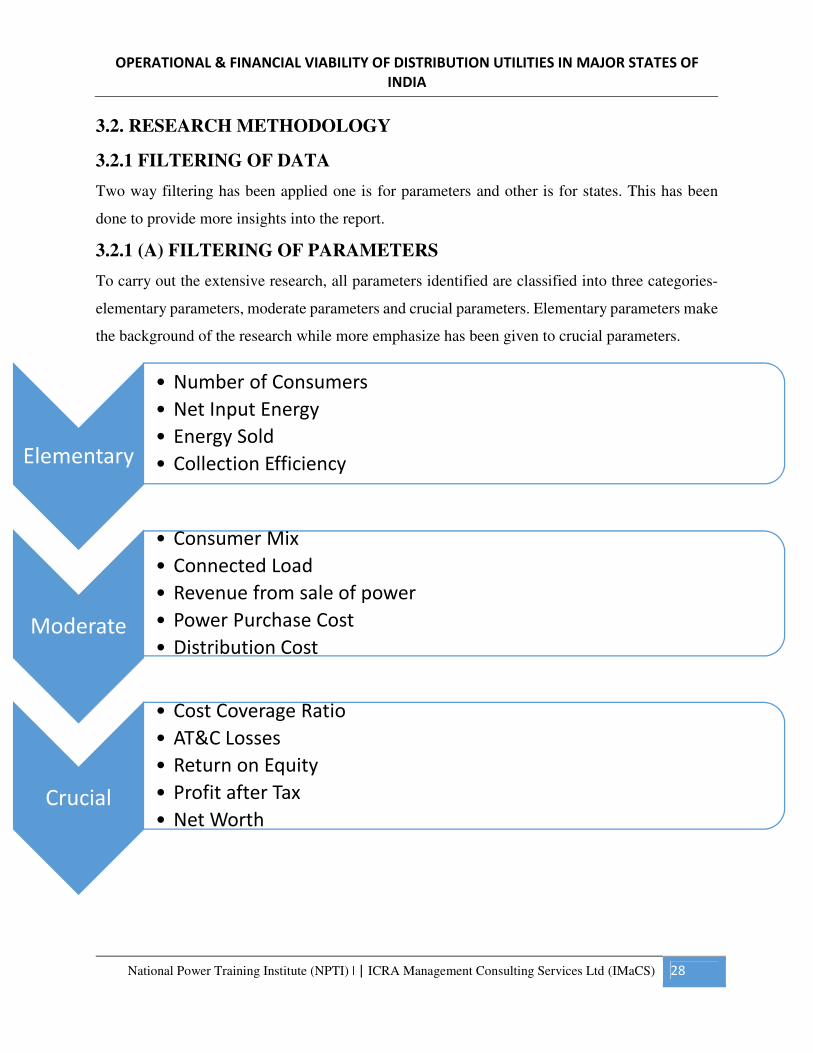

3.2. RESEARCH METHODOLOGY

3.2.1 FILTERING OF DATA

Two way filtering has been applied one is for parameters and other is for states. This has been

done to provide more insights into the report.

3.2.1 (A) FILTERING OF PARAMETERS

To carry out the extensive research, all parameters identified are classified into three categories-

elementary parameters, moderate parameters and crucial parameters. Elementary parameters make

the background of the research while more emphasize has been given to crucial parameters.

Elementary

• Number of Consumers

• Net Input Energy

• Energy Sold

• Collection Efficiency

Moderate

• Consumer Mix

• Connected Load

• Revenue from sale of power

• Power Purchase Cost

• Distribution Cost

Crucial

• Cost Coverage Ratio

• AT&C Losses

• Return on Equity

• Profit after Tax

• Net Worth

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 29

3.2.1 (B) FILTERING OF STATES

Filtering of states has been done on the basis of anticipated

power supply position in FY-14.

From filtering, distribution utilities of top contributing states

has been taken for report which constitute majorly for the total

requirement of power in country.

However some distribution companies are not a part of this

report due to unavailability of their financial statements.

State/UT Requirement (MU)

Maharashtra 118455

Andhra Pradesh 109293

Tamil Nadu 99765

Uttar Pradesh 97785

Gujarat 76808

Karnataka 75947

Rajasthan 59770 Madhya Pradesh 59431

Punjab 50850

West Bengal 48489

Haryana 44700

Orissa 27130

Delhi 26910

Kerala 22384

Chhattisgarh 21410

DVC 19605 Jammu & Kashmir 16240

Bihar 15268

Uttarakhand 12455

Himachal Pradesh 9425

Jharkhand 8609 Assam 7031

D.N. Haveli 5315

Goa 3219

Puducherry 2451

Daman & Diu 2115

Meghalaya 1905

Chandigarh 1750

Tripura 1216

Arunachal Pradesh 655

Manipur 596

Nagaland 591 Sikkim 531

Mizoram 430

Source: - CEA

Anticipated Power Supply Position in the Country during 2013-14

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 30

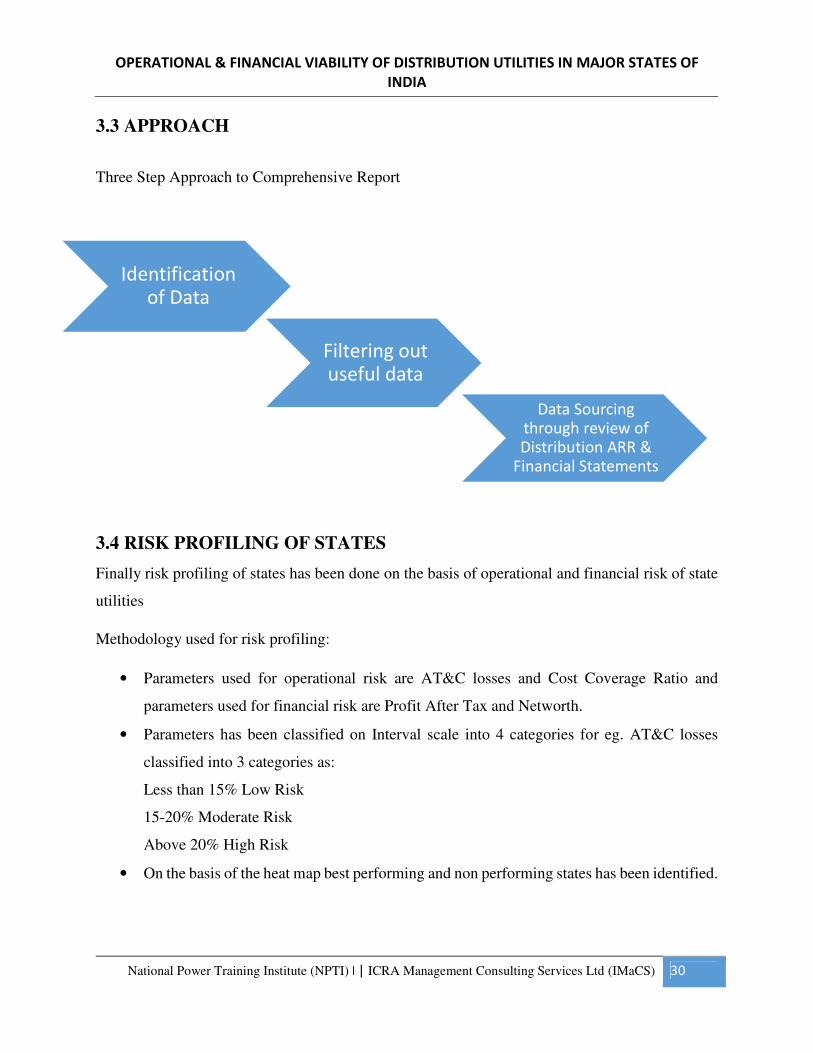

3.3 APPROACH

Three Step Approach to Comprehensive Report

3.4 RISK PROFILING OF STATES

Finally risk profiling of states has been done on the basis of operational and financial risk of state

utilities

Methodology used for risk profiling:

• Parameters used for operational risk are AT&C losses and Cost Coverage Ratio and

parameters used for financial risk are Profit After Tax and Networth.

• Parameters has been classified on Interval scale into 4 categories for eg. AT&C losses

classified into 3 categories as:

Less than 15% Low Risk

15-20% Moderate Risk

Above 20% High Risk

• On the basis of the heat map best performing and non performing states has been identified.

Identification of Data

Filtering out useful data

Data Sourcing through review of Distribution ARR &

Financial Statements

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 31

CHAPTER 4: FACTS AND ANALYSIS OF ANDHRA PRADESH

4.1 OVERALL SCENARIO

4.1.1 General Background and Political Economy

In terms of geography, the state has a varied terrain because of

which the climate of Andhra Pradesh varies considerably

depending on the geographical region. The two main rivers are

the Godavari and Krishna of which Krishna roughly divides the

state into two parts, the northern and southern regions.

Andhra Pradesh receives heavy rainfall mostly in the months of

July to September. This heavy rainfall, in conjunction with its

agricultural based economy, helps it produce large amounts of

rice which account for 77% of its total crop production and earn

it the nickname, “the rice bowl of India‟. In the financial year

2011-12 the state was second in nominal GDP, and in GDP per

capital it ranks fourth. Two of the mega cities of the state - Hyderabad and Visakhapatnam - were

listed among the top 15 cities contributing to India's overall product. Andhra Pradesh ranks tenth

compared to all Indian States in the Human Development Index scores with a score of

0.473.Andhra Pradesh had a series of governments headed by Indian National Congress (INC)

Party until 1982. N. Chandrababu Naidu held the record for the longest serving Chief Minister

(1995 to 2004).

Population Supply Area (Sq.KM)

84665533 275045

Number of consumer’s Per Capita Consumption (KWh)

22761686 966.99

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 32

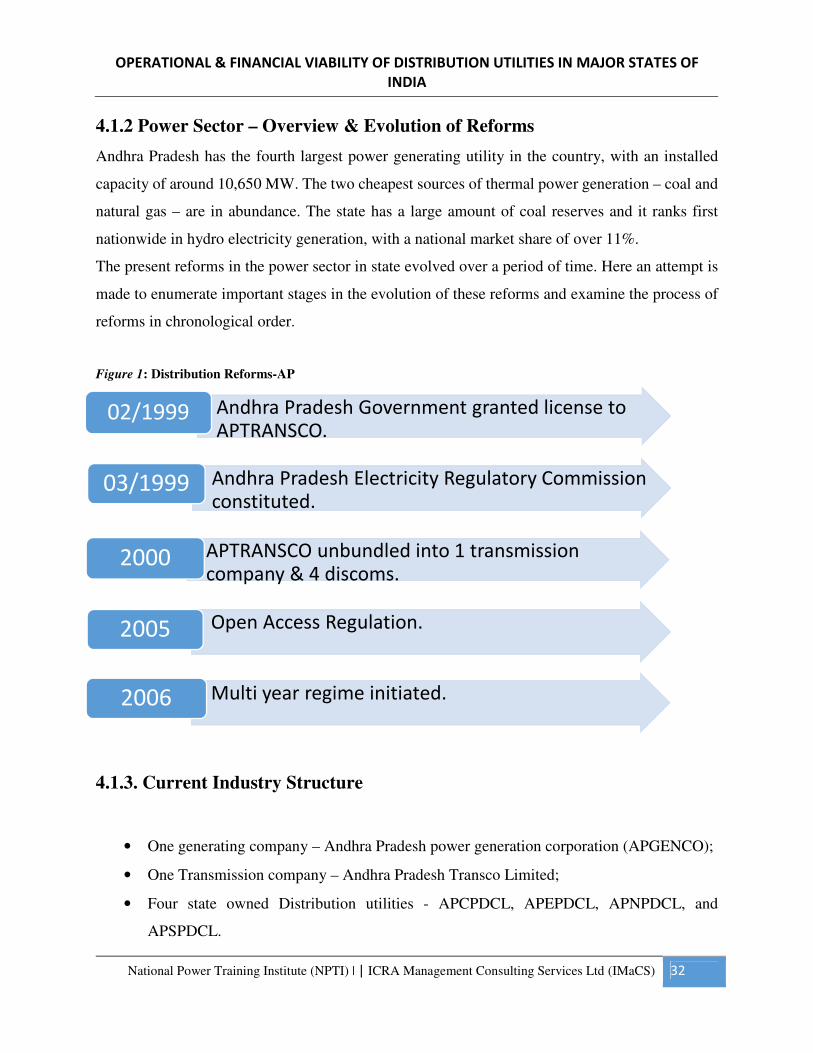

4.1.2 Power Sector – Overview & Evolution of Reforms

Andhra Pradesh has the fourth largest power generating utility in the country, with an installed

capacity of around 10,650 MW. The two cheapest sources of thermal power generation – coal and

natural gas – are in abundance. The state has a large amount of coal reserves and it ranks first

nationwide in hydro electricity generation, with a national market share of over 11%.

The present reforms in the power sector in state evolved over a period of time. Here an attempt is

made to enumerate important stages in the evolution of these reforms and examine the process of

reforms in chronological order.

Figure 1: Distribution Reforms-AP

4.1.3. Current Industry Structure

• One generating company – Andhra Pradesh power generation corporation (APGENCO);

• One Transmission company – Andhra Pradesh Transco Limited;

• Four state owned Distribution utilities - APCPDCL, APEPDCL, APNPDCL, and

APSPDCL.

• Andhra Pradesh Government granted license to APTRANSCO.

02/1999

• Andhra Pradesh Electricity Regulatory Commission constituted.

03/1999

• APTRANSCO unbundled into 1 transmission company & 4 discoms.

2000

• Open Access Regulation.2005

• Multi year regime initiated.2006

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 33

4.2 APNPDCL

(Northern Power Distribution Company of Andhra Pradesh Ltd.)

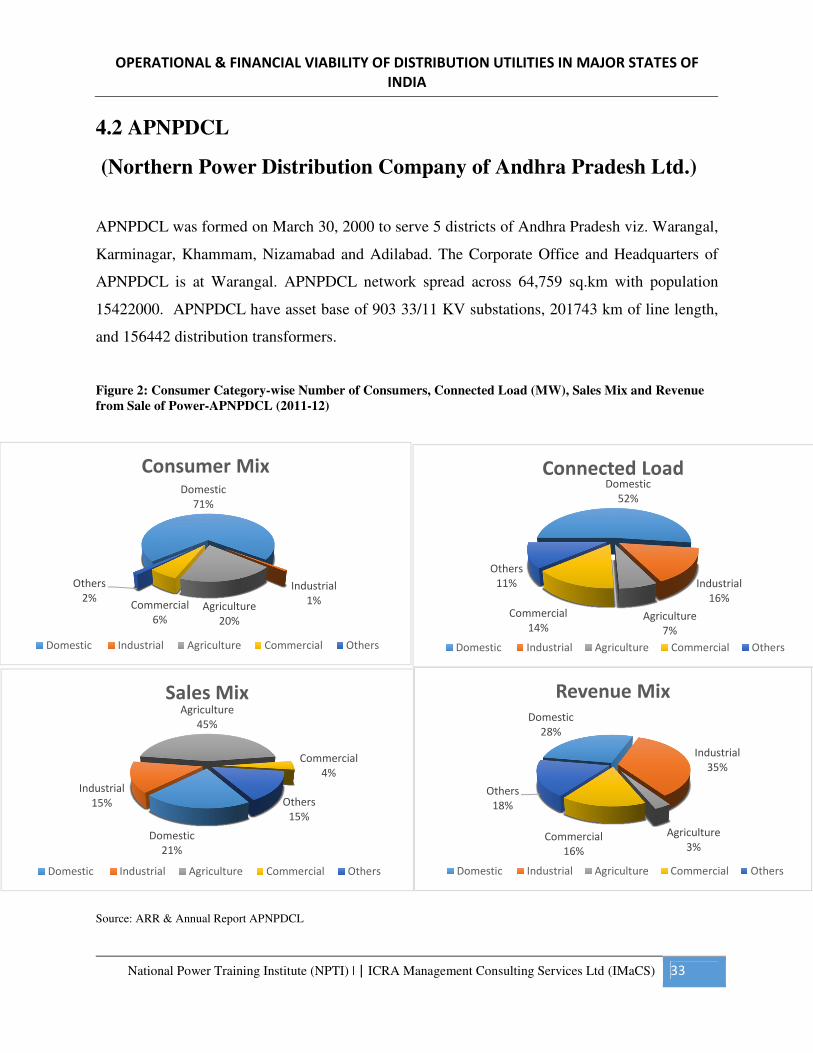

APNPDCL was formed on March 30, 2000 to serve 5 districts of Andhra Pradesh viz. Warangal,

Karminagar, Khammam, Nizamabad and Adilabad. The Corporate Office and Headquarters of

APNPDCL is at Warangal. APNPDCL network spread across 64,759 sq.km with population

15422000. APNPDCL have asset base of 903 33/11 KV substations, 201743 km of line length,

and 156442 distribution transformers.

Figure 2: Consumer Category-wise Number of Consumers, Connected Load (MW), Sales Mix and Revenue

from Sale of Power-APNPDCL (2011-12)

Source: ARR & Annual Report APNPDCL

Domestic

71%

Industrial

1%Agriculture

20%

Commercial

6%

Others

2%

Consumer Mix

Domestic Industrial Agriculture Commercial Others

Domestic

52%

Industrial

16%

Agriculture

7%

Commercial

14%

Others

11%

Connected Load

Domestic Industrial Agriculture Commercial Others

Domestic

28%

Industrial

35%

Agriculture

3%Commercial

16%

Others

18%

Revenue Mix

Domestic Industrial Agriculture Commercial Others

Domestic

21%

Industrial

15%

Agriculture

45%

Commercial

4%

Others

15%

Sales Mix

Domestic Industrial Agriculture Commercial Others

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 34

4.2.1 Operational Performance

Input Energy (MU) Energy Sold (MU) Collection Efficiency (%)

11913.8 10243.93 97.74%

AT&C Losses (%) Employee Expense (Rs/Consumer)

22.47% 771.18

Source: ARR & Annual Report APNPDCL

Figure 3: Category-wise Net Growth in Input Energy and Energy Sold (MU)-APNPDCL (2011-12)

Source: ARR & Annual Report APNPDCL

Total energy input is increased from 9203 MU to 11914 MU over last 5 years with a CAGR of

6.7% and energy sold is increased from 7748 MU to 10244 MU over last 5 year with CAGR of

7.2%.

9203

10070 10463 1061011914

77488545 8943 9102

10244

2007-08 2008-09 2009-10 2010-11 2011-12

Input Energy Energy Sold CAGR (Input Energy) CAGR (Energy Sold)

6.7%

7.2%

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 35

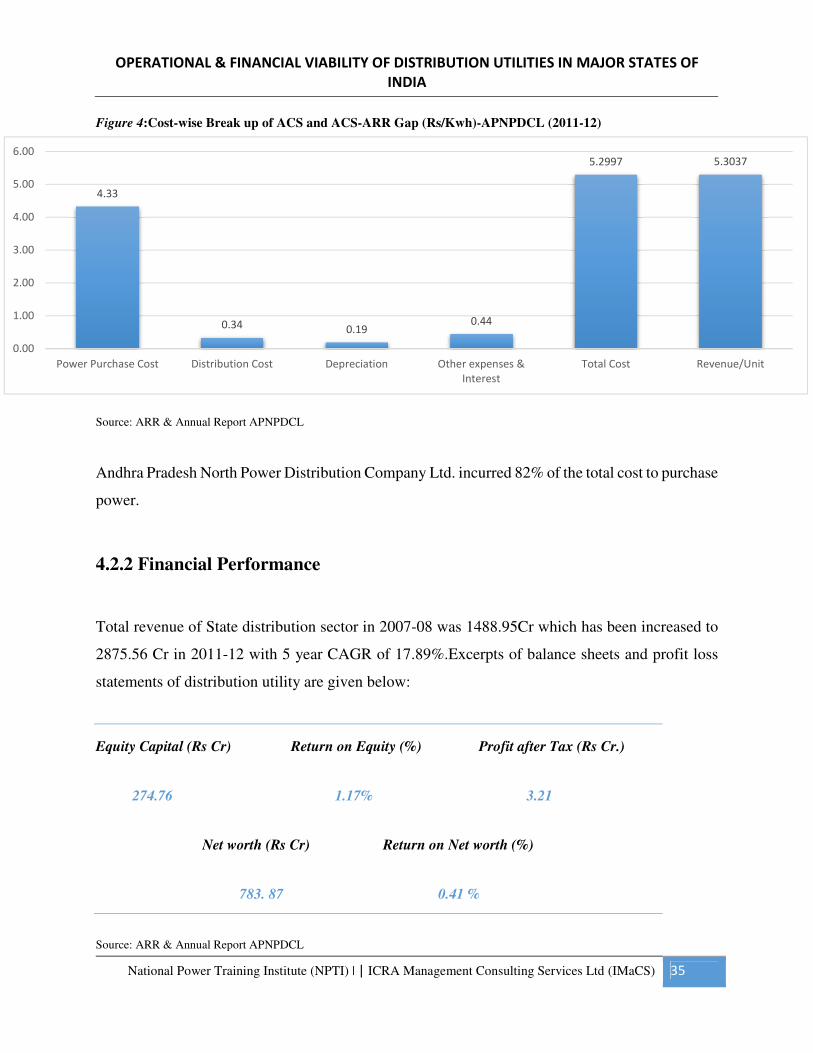

Figure 4:Cost-wise Break up of ACS and ACS-ARR Gap (Rs/Kwh)-APNPDCL (2011-12)

Source: ARR & Annual Report APNPDCL

Andhra Pradesh North Power Distribution Company Ltd. incurred 82% of the total cost to purchase

power.

4.2.2 Financial Performance

Total revenue of State distribution sector in 2007-08 was 1488.95Cr which has been increased to

2875.56 Cr in 2011-12 with 5 year CAGR of 17.89%.Excerpts of balance sheets and profit loss

statements of distribution utility are given below:

Equity Capital (Rs Cr) Return on Equity (%) Profit after Tax (Rs Cr.)

274.76 1.17% 3.21

Net worth (Rs Cr) Return on Net worth (%)

783. 87 0.41 %

Source: ARR & Annual Report APNPDCL

4.33

0.34 0.190.44

5.2997 5.3037

0.00

1.00

2.00

3.00

4.00

5.00

6.00

Power Purchase Cost Distribution Cost Depreciation Other expenses &

Interest

Total Cost Revenue/Unit

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 36

4.3 APEPDCL

(Eastern Power Distribution Company of Andhra Pradesh Ltd.)

APEPDCL was formed on March 31, 2000 to serve 5 districts of Andhra Pradesh viz. West

Godavari, East Godavari, Srikakulam, Vizianagaram and Visakhapatnam. The Corporate Office

and Headquarters of APEPDCL is at Visakhapatnam. APEPDCL supplies power to over 47 lakh

consumers belonging to different categories through a network consisting of 558 Sub-stations of

33 KV level, 2188 feeders of 11 KV level and more than 1,16,566 distribution transformers of

different levels.

Figure 5: Consumer Category-wise Number of Consumers, Sales Mix and Revenue from Sale of Power-

APEPDCL (2011-12)

Source: ARR & Annual Report APEPDCL

Domestic

27%

Industrial

40%

Agriculture

16%

Commercial

6%

Others

11%

Sales Mix

Domestic Industrial Agriculture Commercial Others

Domestic

20%

Industrial

64%

Agriculture

1%

Commercial

12%Others

3%

Revenue Mix

Domestic Industrial Agriculture Commercial Others

Domestic

88%

Industrial

1%

Agriculture

1%

Commercial

8%

Others

2%

Consumer Mix

Domestic Industrial Agriculture Commercial Others

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 37

4.3.1 Operational Performance

Input Energy (MU) Energy Sold (MU) Collection Efficiency (%)

12595 11725.82 97.14%

AT&C Losses (%) Employee Expense (Rs/Consumer)

12.9% 939.45

Source: ARR & Annual Report APEPDCL

Figure 6: Category-wise Net Growth in Input Energy and Energy Sold (MU)-APEPDCL (2011-12)

Source: ARR & Annual Report APEPDCL

Total energy input is increased from 9251 MU to 12595 MU over last 5 years with a CAGR of

8.02% and energy sold is increased from 8059 MU to 11726 MU over last 5 year with CAGR of

9.83%.

92519889

11261 1160312595

8059 86929869 10366

11726

2007-08 2008-09 2009-10 2010-11 2011-12

Input Energy Energy Sold CAGR (Input Energy) CAGR (Energy Sold)

8.02%

9.83%

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 38

Figure 7:Cost-wise Break up of ACS and ACS-ARR Gap (Rs/Kwh)-APEPDCL (2011-12)

Source: ARR & Annual Report APEPDCL

Andhra Pradesh Eastern Power Distribution Company Ltd. incurred 82% of the total cost to

purchase power.

4.3.2 Financial Performance

Total revenue of State distribution sector in 2007-08 was 2766.23 Cr which has been increased to

5508.23 Cr in 2011-12 with 5 year CAGR of 18.79%.Excerpts of balance sheets and profit loss

statements of distribution utility are given below:

Equity Capital (Rs Cr) Return on Equity (%) Profit after Tax (Rs Cr.)

121.26 20.82% 25.24

Net worth (Rs Cr) Return on Net worth (%)

413.3 6.1 %

Source: ARR & Annual Report APEPDCL

4.43

0.510.19 0.29

5.41 5.43

0.00

1.00

2.00

3.00

4.00

5.00

6.00

Power Purchase Cost Distribution Cost Depreciation Other expenses &

Interest

Total Cost Revenue/Unit

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 39

4.4 APCPDCL (Central Power Distribution Company of Andhra

Pradesh Ltd)

APCPDCL was formed on April 1, 2000 to serve 7 districts of Andhra Pradesh viz. Anantapur,

Kurnool, Mahaboobnagar, Nalgonda, Medak and Rangareddy .The Corporate Office and

Headquarters of APCPDCL is at Hyderabad. APCPDCL has a vast infrastructure facility in its

operating area with 1,338 Nos. of 33/11 KV substations, 2,039 Nos. of power transformers, 720

Nos. of 33 KV feeders, 5,257 Nos. of 11 KV feeders and around 246426 Nos. of distribution

transformers of various capacities.

Figure 8: Consumer Category-wise Number of Consumers, Connected Load (MW), Sales Mix and Revenue

from Sale of Power-APCPDCL (2011-12)

Source: ARR & Annual Report APCPDCL

Domestic

75%

Industrial

1%Agriculture

13%

Commercial

10%

Others

1%

Consumer Mix

Domestic Industrial Agriculture Commercial Others

Domestic

49%

Industrial

22%

Agriculture

3%

Commercial

22%

Others

4%

Connected Load

Domestic Industrial Agriculture Commercial Others

Domestic

19%

Industrial

37%

Agriculture

29%

Commercial

12%

Others

3%

Sales Mix

Domestic Industrial Agriculture Commercial Others

Domestic

18%

Commercial

24%

Industrial

53%

Agriculture

1%Others

4%

Revenue Mix

Domestic Commercial Industrial Agriculture Others

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 40

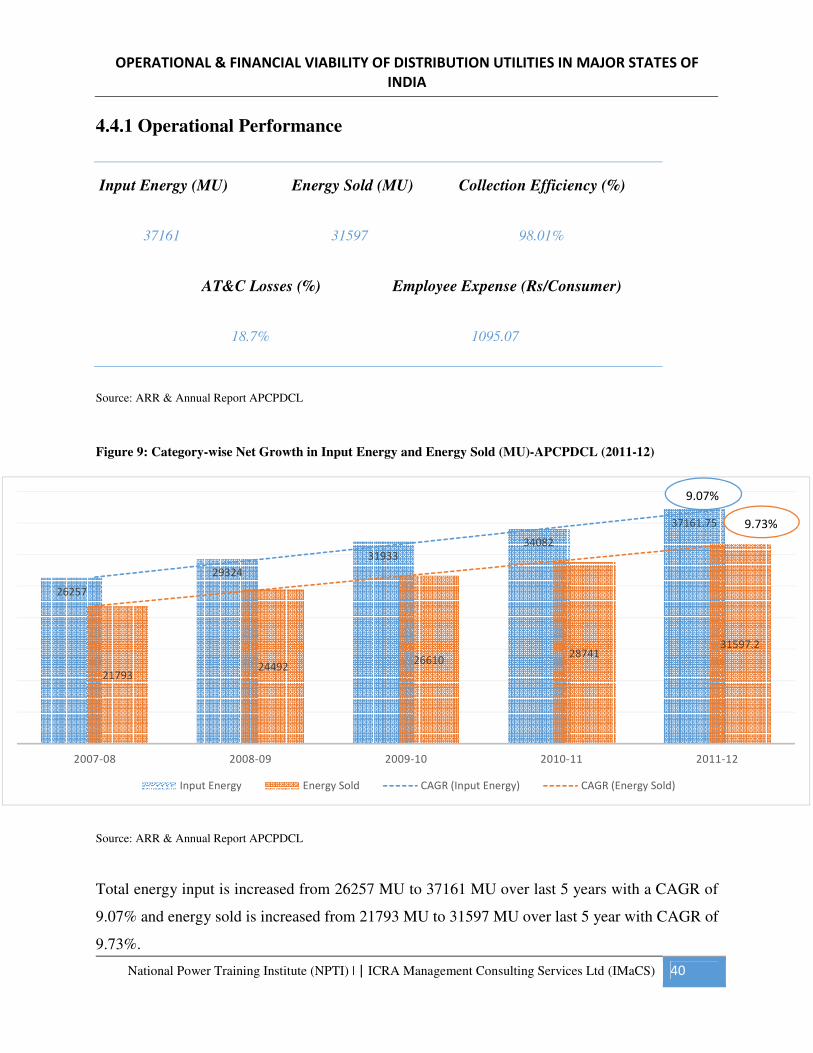

4.4.1 Operational Performance

Input Energy (MU) Energy Sold (MU) Collection Efficiency (%)

37161 31597 98.01%

AT&C Losses (%) Employee Expense (Rs/Consumer)

18.7% 1095.07

Source: ARR & Annual Report APCPDCL

Figure 9: Category-wise Net Growth in Input Energy and Energy Sold (MU)-APCPDCL (2011-12)

Source: ARR & Annual Report APCPDCL

Total energy input is increased from 26257 MU to 37161 MU over last 5 years with a CAGR of

9.07% and energy sold is increased from 21793 MU to 31597 MU over last 5 year with CAGR of

9.73%.

26257

29324

31933

34082

37161.75

2179324492

2661028741

31597.2

2007-08 2008-09 2009-10 2010-11 2011-12

Input Energy Energy Sold CAGR (Input Energy) CAGR (Energy Sold)

9.07%

9.73%

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 41

Figure 10: Cost-wise Break up of ACS and ACS-ARR Gap (Rs/Kwh)-APCPDCL (2011-12)

Source: ARR & Annual Report APCPDCL

Andhra Pradesh Central Power Distribution Company Ltd. incurred 84% of the total cost to

purchase power.

4.4.2 Financial Performance

Total revenue of State distribution sector in 2007-08 was 2766.23 Cr which has been increased to

5508.23 Cr in 2011-12 with 5 year CAGR of 18.79%. Excerpts of balance sheets and profit loss

statements of distribution utility are given below:

Equity Capital (Rs Cr) Return on Equity (%) Profit after Tax (Rs Cr.)

728.48 0.56% 4.09

Net worth (Rs Cr) Return on Net worth (%)

2197.80 0.18 %

Source: ARR & Annual Report APCPDCL

4.01

0.350.12

0.30

4.78 4.79

0.00

1.00

2.00

3.00

4.00

5.00

6.00

Power Purchase Cost Distribution Cost Depreciation Other expenses &

Interest

Total Cost Revenue/Unit

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 42

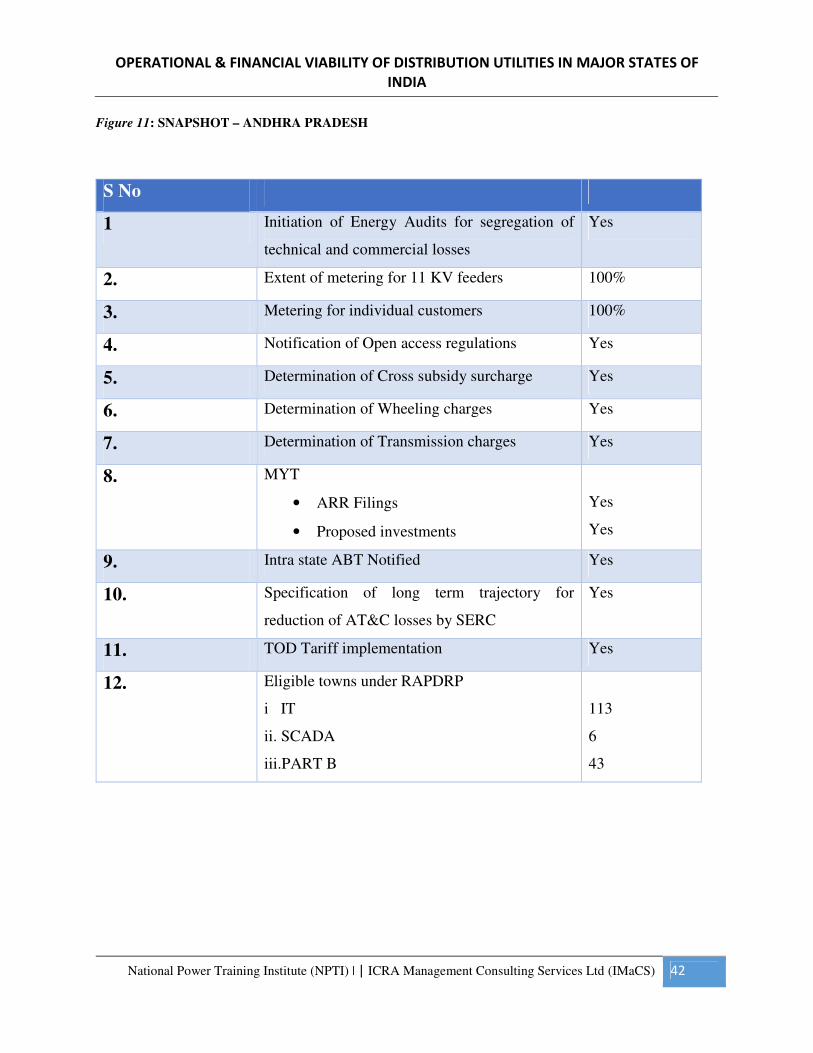

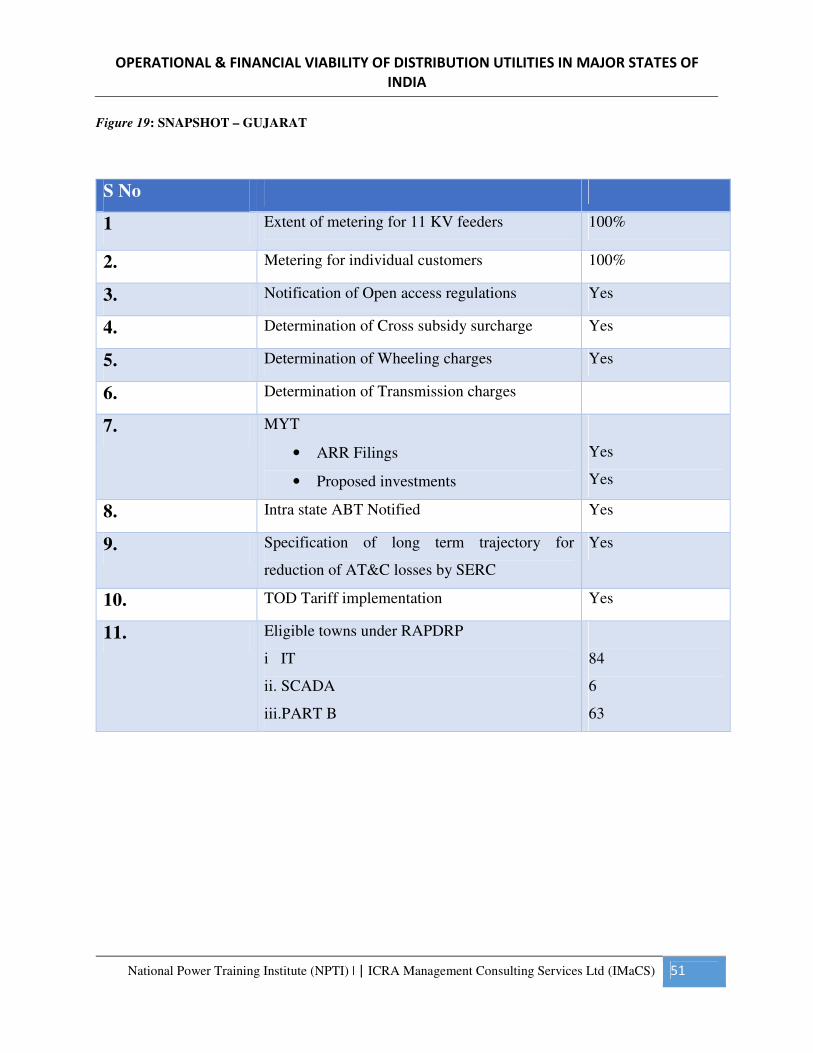

Figure 11: SNAPSHOT – ANDHRA PRADESH

S No

1 Initiation of Energy Audits for segregation of

technical and commercial losses

Yes

2. Extent of metering for 11 KV feeders 100%

3. Metering for individual customers 100%

4. Notification of Open access regulations Yes

5. Determination of Cross subsidy surcharge Yes

6. Determination of Wheeling charges Yes

7. Determination of Transmission charges Yes

8. MYT

• ARR Filings

• Proposed investments

Yes

Yes

9. Intra state ABT Notified Yes

10. Specification of long term trajectory for

reduction of AT&C losses by SERC

Yes

11. TOD Tariff implementation Yes

12. Eligible towns under RAPDRP

i IT

ii. SCADA

iii.PART B

113

6

43

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 43

Chapter 5: FACTS AND ANALYSIS OF GUJARAT

5.1 OVERALL SCENARIO

5.1.1 General Background & Political Economy

Gujarat has an area of 196,204 km2 (75,755 sq mi) with a

coastline of 1,600 km (990 mi), most of which lies on the

Kathiawar peninsula, and a population in excess of 60

million. The state is bordered by Rajasthan to the north,

Maharashtra to the south, Madhya Pradesh to the east, and

the Arabian Sea as well as the Pakistani province of Sindh

on the west. Its capital city is Gandhinagar, whilst its largest

city is Ahmedabad. Gujarat is home to the Gujarati-speaking

people of India.

Gujarat has some of the largest businesses in India includes

cotton, groundnuts (peanuts), dates, sugar cane, milk and milk products. Industrial products

include cement and petrol. The world's largest shipbreaking yard is in Gujarat near Bhavnagar at

Alang. India’s only Liquid Chemical Port Terminal at Dahej. On 20 December 2012, the BJP won

the state elections in Gujarat for the fifth time in a row and Narendra Modi again returned to power

by achieving a hat-trick and has completed 11 years of governance on 7 October 2012 in the state

by winning the state assembly elections.

Population Supply Area (Sq.KM)

60383628 196024

Number of consumer’s Per Capita Consumption (KWh)

1, 18, 14,349 1615.24

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 44

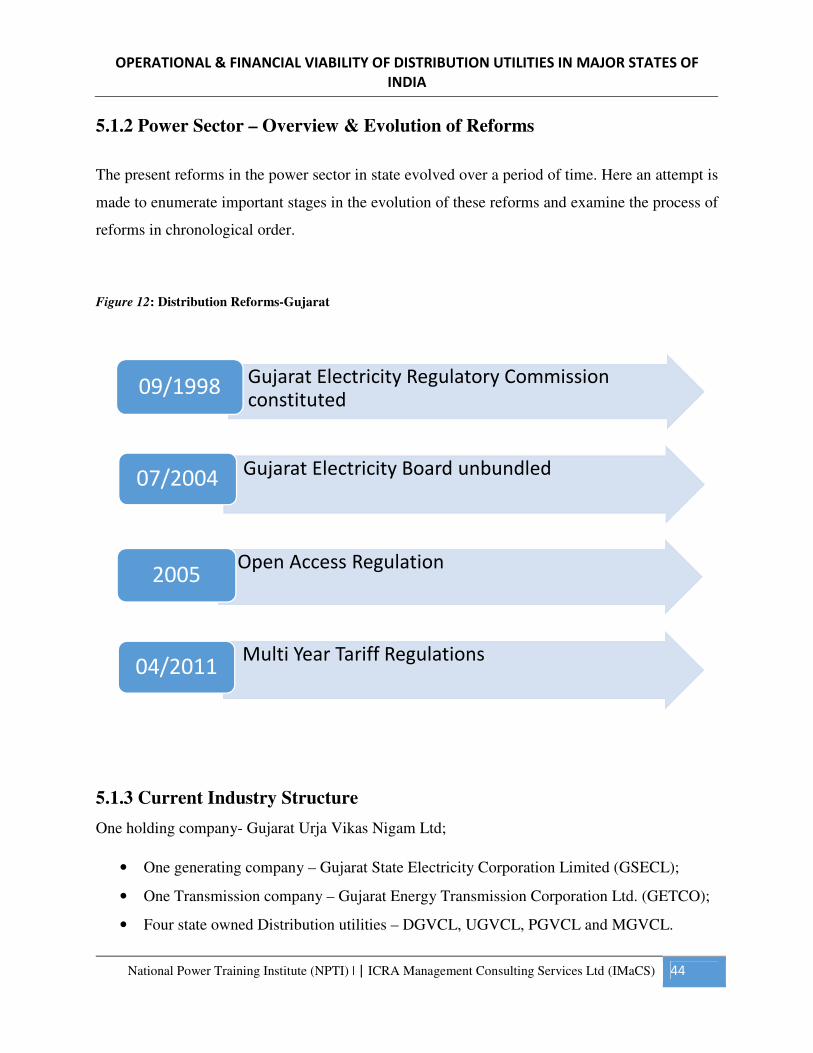

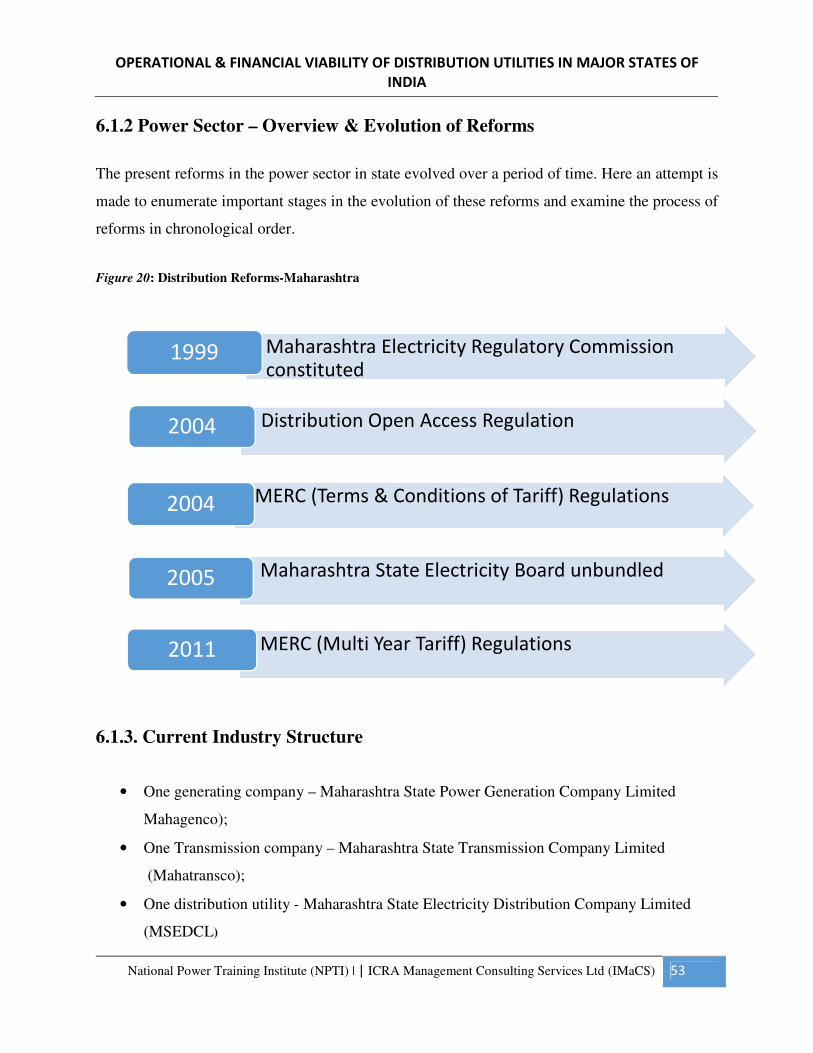

5.1.2 Power Sector – Overview & Evolution of Reforms

The present reforms in the power sector in state evolved over a period of time. Here an attempt is

made to enumerate important stages in the evolution of these reforms and examine the process of

reforms in chronological order.

Figure 12: Distribution Reforms-Gujarat

5.1.3 Current Industry Structure

One holding company- Gujarat Urja Vikas Nigam Ltd;

• One generating company – Gujarat State Electricity Corporation Limited (GSECL);

• One Transmission company – Gujarat Energy Transmission Corporation Ltd. (GETCO);

• Four state owned Distribution utilities – DGVCL, UGVCL, PGVCL and MGVCL.

• Gujarat Electricity Regulatory Commission constituted

09/1998

• Gujarat Electricity Board unbundled07/2004

• Open Access Regulation2005

• Multi Year Tariff Regulations04/2011

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 45

5.2 DGVCL (Dakshin Gujarat VIJ Company Ltd)

DGVCL incorporated under the Companies Act, 1956 in Sept-2003. The Company became

commercially operational since April-2005. DGVCL is responsible to supply of power to 7

districts namely Bharuch, Narmada, Surat (except part of Surat City), Tapi, Dangs, Navsari and

Valsad in South Gujarat. DGVCL has around 70000 km length of lines and around 50000 Nos. of

distribution transformers of various capacities.

Figure 13: Consumer Category-wise Number of Consumers, Connected Load (MW), Sales Mix and Revenue

from Sale of Power-DGVCL (2011-12)

Source: ARR & Annual Report DGVCL

Domestic

83%

Industrial

2%

Agriculture

4%Commercial

10%

Others

1%

Consumer Mix

Domestic Industrial Agriculture Commercial Others

Domestic

29%

Industrial

51%

Agriculture

8%

Commercial

9%

Others

3%

Connected Load

Domestic Industrial Agriculture Commercial Others

Domestic

16%

Industrial

71%

Agriculture

6%

Commercial

3%Others

4%

Sales Mix

Domestic Industrial Agriculture Commercial Others

Domestic

13%

Industrial

78%

Agriculture

2%Commercial

3%Others

4%

Revenue from Power

Domestic Industrial Agriculture Commercial Others

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 46

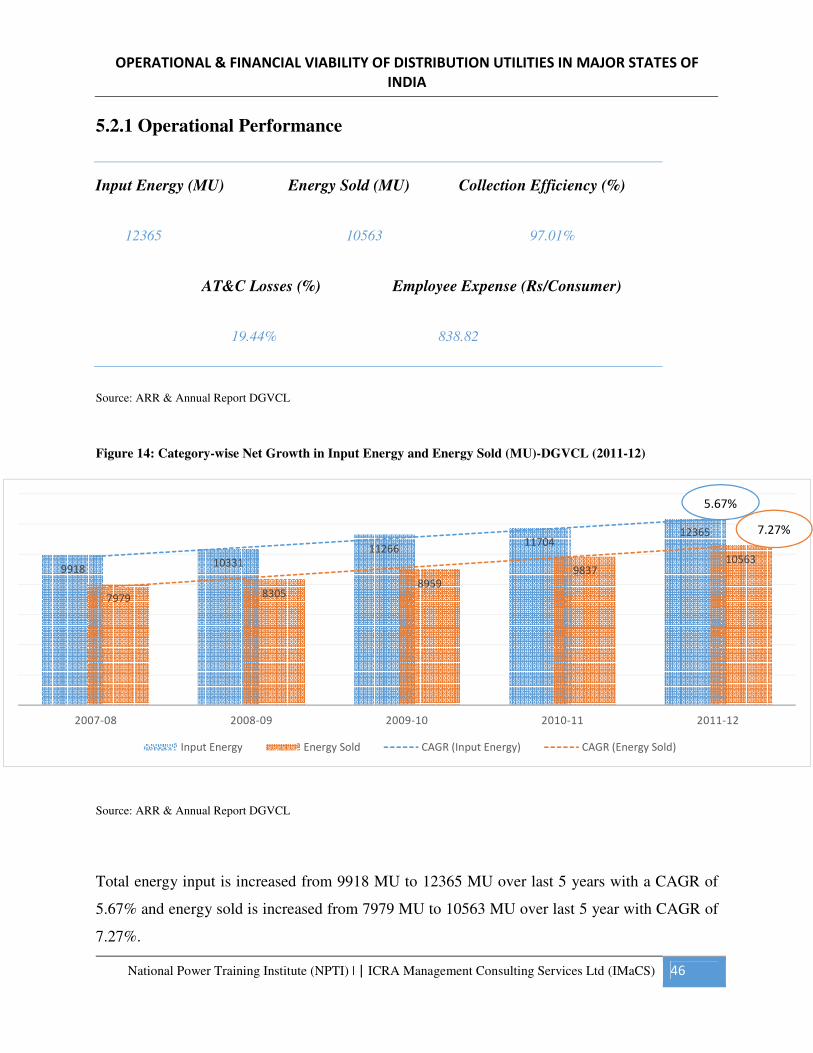

5.2.1 Operational Performance

Input Energy (MU) Energy Sold (MU) Collection Efficiency (%)

12365 10563 97.01%

AT&C Losses (%) Employee Expense (Rs/Consumer)

19.44% 838.82

Source: ARR & Annual Report DGVCL

Figure 14: Category-wise Net Growth in Input Energy and Energy Sold (MU)-DGVCL (2011-12)

Source: ARR & Annual Report DGVCL

Total energy input is increased from 9918 MU to 12365 MU over last 5 years with a CAGR of

5.67% and energy sold is increased from 7979 MU to 10563 MU over last 5 year with CAGR of

7.27%.

991810331

1126611704

12365

7979 83058959

983710563

2007-08 2008-09 2009-10 2010-11 2011-12

Input Energy Energy Sold CAGR (Input Energy) CAGR (Energy Sold)

5.67%

7.27%

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 47

Figure 15:Cost-wise Break up of ACS and ACS-ARR Gap (Rs/Kwh)-DGVCL (2011-12)

Source: ARR & Annual Report DGVCL

Dakshin Gujarat Vij Company Ltd. incurred 90% of the total cost to purchase power.

5.2.2 Financial Performance

Total revenue of DGVCL in 2007-08 was 3361.85 Cr which has been increased to 6290.46 Cr in

2011-12 with 5 year CAGR of 16.96%.Excerpts of balance sheets and profit loss statements of

distribution utility are given below:

Equity Capital (Rs Cr) Return on Equity (%) Profit after Tax (Rs Cr.)

267.73 28.51% 76.32

Net worth (Rs Cr) Return on Net worth (%)

1582.14 4.82 %

Source: ARR & Annual Report DGVCL

5.49

0.19 0.10 0.13

5.90 5.95

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Power Purchase Cost Distribution Cost Depreciation Other expenses &

Interest

Total Cost Revenue/Unit

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 48

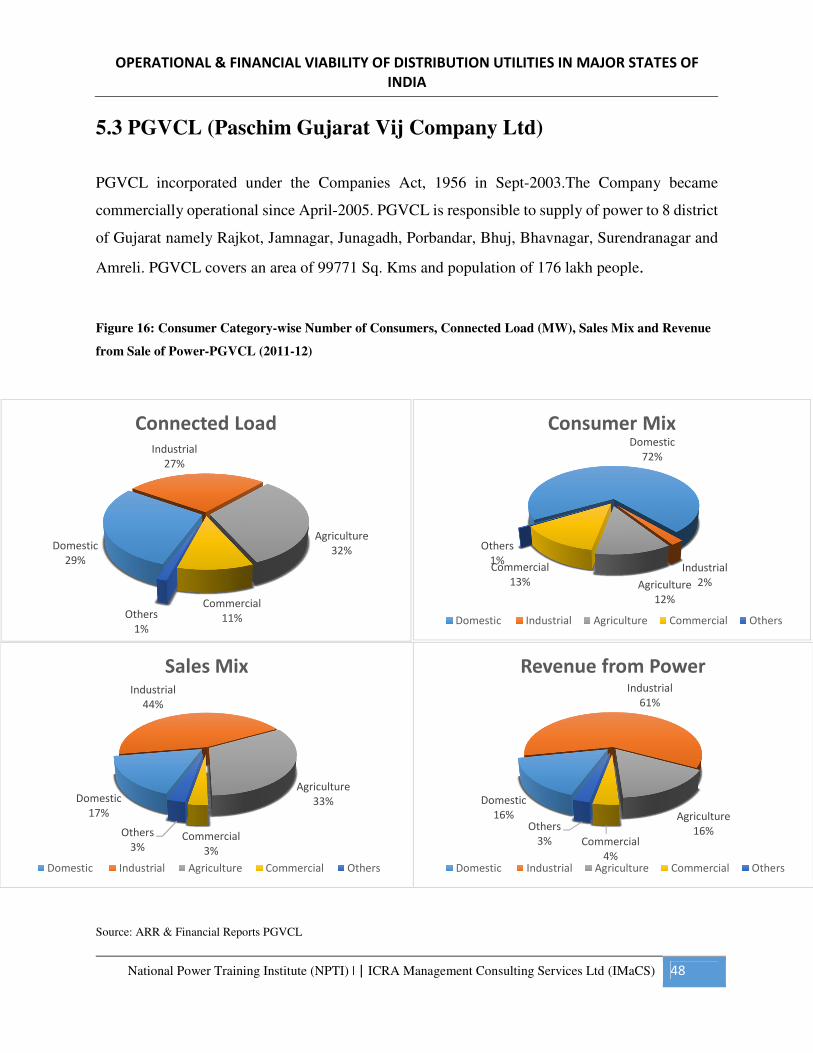

5.3 PGVCL (Paschim Gujarat Vij Company Ltd)

PGVCL incorporated under the Companies Act, 1956 in Sept-2003.The Company became

commercially operational since April-2005. PGVCL is responsible to supply of power to 8 district

of Gujarat namely Rajkot, Jamnagar, Junagadh, Porbandar, Bhuj, Bhavnagar, Surendranagar and

Amreli. PGVCL covers an area of 99771 Sq. Kms and population of 176 lakh people.

Figure 16: Consumer Category-wise Number of Consumers, Connected Load (MW), Sales Mix and Revenue

from Sale of Power-PGVCL (2011-12)

Source: ARR & Financial Reports PGVCL

Domestic

16%

Industrial

61%

Agriculture

16%Commercial

4%

Others

3%

Revenue from Power

Domestic Industrial Agriculture Commercial Others

Domestic

17%

Industrial

44%

Agriculture

33%

Commercial

3%

Others

3%

Sales Mix

Domestic Industrial Agriculture Commercial Others

Domestic

29%

Industrial

27%

Agriculture

32%

Commercial

11%Others

1%

Connected LoadDomestic

72%

Industrial

2%Agriculture

12%

Commercial

13%

Others

1%

Consumer Mix

Domestic Industrial Agriculture Commercial Others

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 49

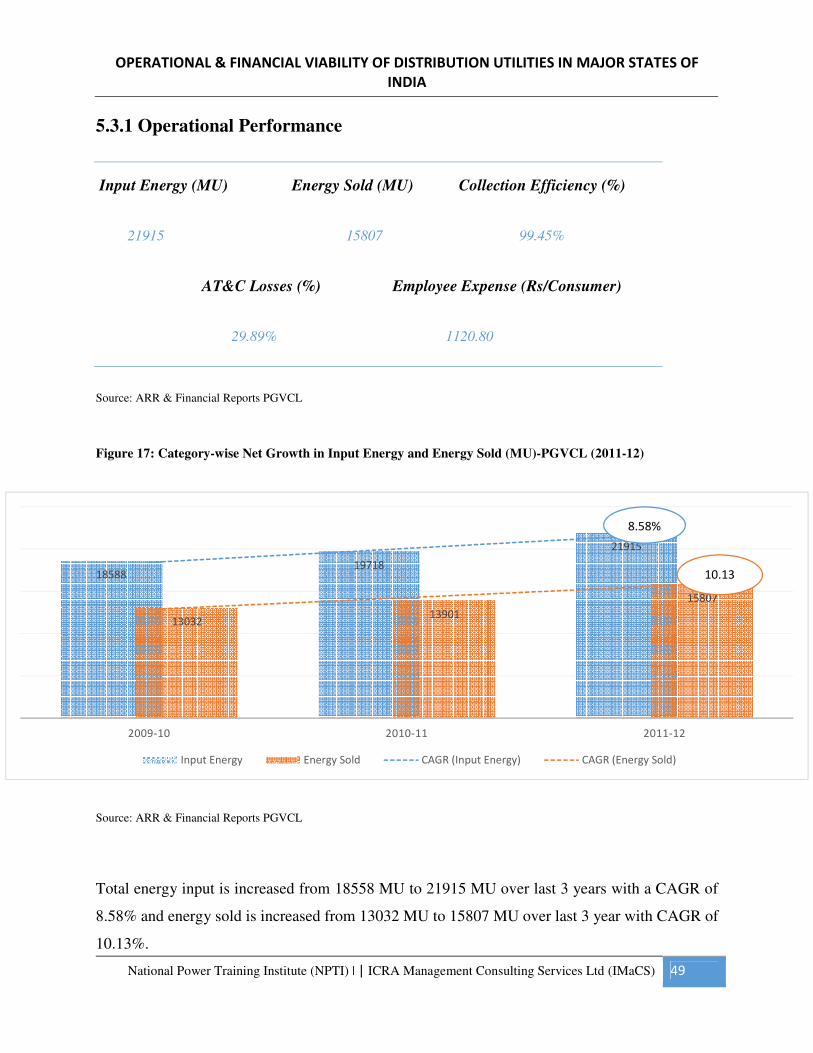

5.3.1 Operational Performance

Input Energy (MU) Energy Sold (MU) Collection Efficiency (%)

21915 15807 99.45%

AT&C Losses (%) Employee Expense (Rs/Consumer)

29.89% 1120.80

Source: ARR & Financial Reports PGVCL

Figure 17: Category-wise Net Growth in Input Energy and Energy Sold (MU)-PGVCL (2011-12)

Source: ARR & Financial Reports PGVCL

Total energy input is increased from 18558 MU to 21915 MU over last 3 years with a CAGR of

8.58% and energy sold is increased from 13032 MU to 15807 MU over last 3 year with CAGR of

10.13%.

1858819718

21915

1303213901

15807

2009-10 2010-11 2011-12

Input Energy Energy Sold CAGR (Input Energy) CAGR (Energy Sold)

8.58%

10.13

OPERATIONAL & FINANCIAL VIABILITY OF DISTRIBUTION UTILITIES IN MAJOR STATES OF

INDIA

National Power Training Institute (NPTI) | | ICRA Management Consulting Services Ltd (IMaCS) 50

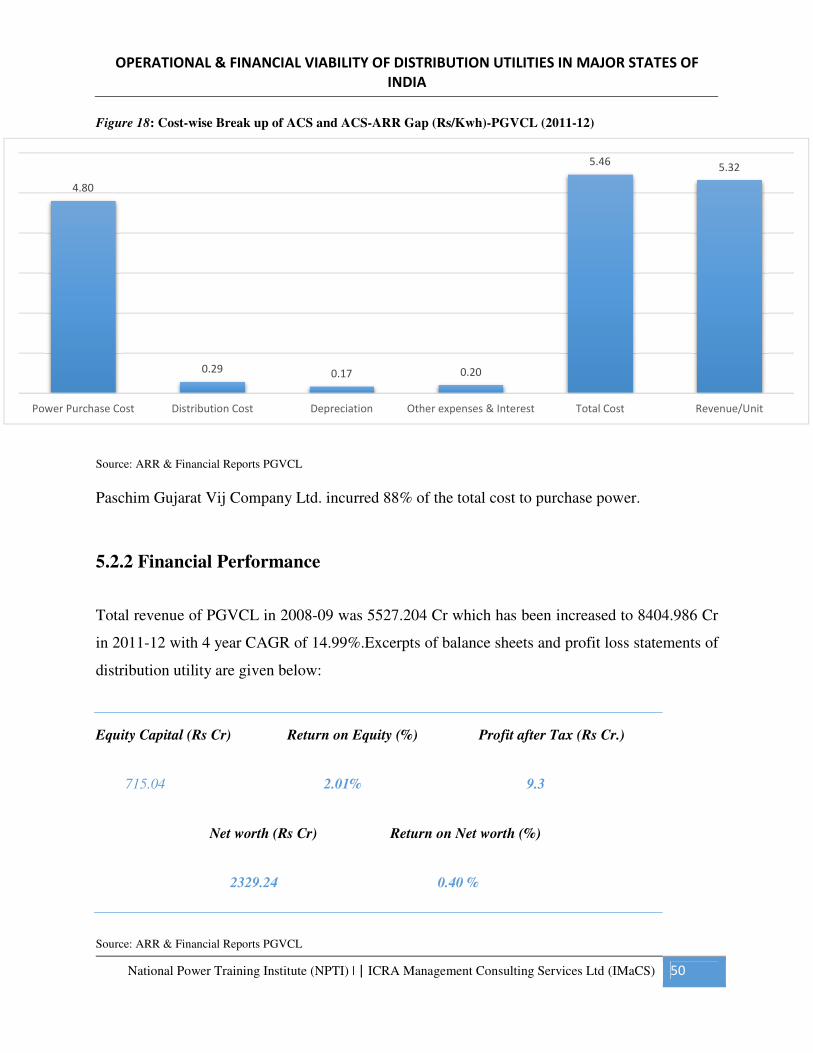

Figure 18: Cost-wise Break up of ACS and ACS-ARR Gap (Rs/Kwh)-PGVCL (2011-12)

Source: ARR & Financial Reports PGVCL

Paschim Gujarat Vij Company Ltd. incurred 88% of the total cost to purchase power.

5.2.2 Financial Performance

Total revenue of PGVCL in 2008-09 was 5527.204 Cr which has been increased to 8404.986 Cr

in 2011-12 with 4 year CAGR of 14.99%.Excerpts of balance sheets and profit loss statements of

distribution utility are given below:

Equity Capital (Rs Cr) Return on Equity (%) Profit after Tax (Rs Cr.)

715.04 2.01% 9.3