Embed Size (px)

Citation preview

Regional Economic Report

October – December 2018

March 14, 2019

Outline

I. Regional Economic Report

II. Results October – December 2018

A. Economic activity

B. Inflation

C. Economic outlook (based on data obtained between January 7

and January 31, 2019)

III. Boxes

IV. Final remarks

1

Regional Economic Report

• The Regional Economic Report is a quarterly publication on the recent trends in economicactivity, inflation and business agents’ expectations in Mexico’s regions.1

• The information herein presented is taken into account by Banco de México’s Governing Boardwhen evaluating the economic situation and the forecast for the Mexican economy.

• The economic performance of the regions in Q4 2018 and the prospects for regional economicactivity and inflation over the following 12 months are analyzed herein.

2

1 For the purposes of this Report, the states of Mexico are grouped into the following four regions. Northern: Baja California, Chihuahua, Coahuila, Nuevo León, Sonora and Tamaulipas. North-Central: Aguascalientes, BajaCalifornia Sur, Colima, Durango, Jalisco, Michoacán, Nayarit, San Luis Potosí, Sinaloa and Zacatecas. Central: Ciudad de México, Estado de México, Guanajuato, Hidalgo, Morelos, Puebla, Querétaro and Tlaxcala.Southern: Campeche, Chiapas, Guerrero, Oaxaca, Quintana Roo, Tabasco, Veracruz and Yucatán.

Outline

I. Regional Economic Report

II. Results October – December 2018

A. Economic activity

B. Inflation

C. Economic outlook (based on data obtained between January 7

and January 31, 2019)

III. Boxes

IV. Final remarks

3

Economic Activity

• In Q4 2018, economic activity in Mexico decelerated significantly as compared to Q3, andsuch deceleration might extend to the early part of 2019.

This reflected both the slowdown of the global economy and the greater weakness of differentcomponents of domestic demand, and certain transitory factors.

• The weakness of domestic economic activity in Q4 was perceived across most regions of thecountry.

4

5

1/ The value of Gross Domestic Product (GDP) for Q4 2018 corresponds to the observed data. Source: Estimated by Banco de México with seasonally adjusted series of domestic GDP and Quarterly Indicator of Economic Activity by State, INEGI.

In Q4 the Southern region is estimated to have contracted and the Northern and Central regions, tohave stagnated. In contrast, in the North-Central region economic activity is expected to have grown ata faster rate.

Quarterly Indicator of Regional Economic Activity 1/

Index 2013=100

Total Non-oil

80

85

90

95

100

105

110

115

120

125

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Northern North-Central Central Southern GDP

Forecast

QIV80

85

90

95

100

105

110

115

120

125

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Northern North-Central Central Southern GDP

Forecast

QIV

6

Source: Estimated by Banco de México with seasonally adjusted series of the Monthly Indicator of Manufacturing Activity by State, INEGI.

During Q4 2018, manufacturing exhibited a weak performance, after the recovery observed in the firsthalf of 2018. This evolution was reflected in a fall in manufacturing activity in all Mexican regions.

Regional Manufacturing IndicatorIndex 2013=100, quarterly average

75

80

85

90

95

100

105

110

115

120

125

130

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Northern North-Central Central Southern

Forecast

QIV

Regional Indicator of Mining, Quarrying, and Oil and Gas Extraction 1/

Index 2013=100, quarterly average

7

1/ Values for Q4 2018 are preliminary. Source: Estimated and seasonally adjusted by Banco de México with the series of the Monthly Indicator of Mining Activity by State, INEGI.

The mining, quarrying, and oil and gas extraction sector remained on a downward trajectory in allregions, except for the Northern one. This mirrored the continuous fall of oil and gas extraction and thedecline in the item of metal ore mining and nonmetallic mineral mining in the Central, North-Centraland Southern regions.

60

70

80

90

100

110

120

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Northern North-Central Central Southern

QIV

8

The construction sector contracted in the Northern, Central and Southern regions, due to the negativeperformance of both public and private construction works. In contrast, in the North-Central region,construction expanded, essentially as a reflection of the favorable performance of private construction,which remains at particularly high levels in that region.

Real Value of Production in the Construction Industry by RegionIndex 2013=100, quarterly average

Source: Prepared and seasonally adjusted by Banco de México with data from the National Survey of Construction Companies, INEGI.

Total PublicPrivate

50

60

70

80

90

100

110

120

130

140

150

160

170

180

190

2008 2010 2012 2014 2016 2018

Northern North-CentralCentral Southern

QIV 30

40

50

60

70

80

90

100

110

120

130

140

150

160

2008 2010 2012 2014 2016 2018

Northern North-CentralCentral Southern

QIV30

40

50

60

70

80

90

100

110

120

130

140

150

160

2008 2010 2012 2014 2016 2018

Northern North-CentralCentral Southern

QIV

9

Trade, measured with the index of revenues from the supply of goods and services by retail business,contracted in the Northern and Southern regions, while in the central ones it underwent stagnation.

Regional Indicator of TradeIndex 2013=100, quarterly average

Source: Prepared and seasonally adjusted by Banco de México with the series of Revenues from the Supply of Goods and Services by Retail Business, by State, INEGI.

70

80

90

100

110

120

130

140

150

160

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Northern North-Central Central Southern

QIV

10

In Q4 the evolution of tourism, measured by hotel occupancy and inflow of passengers to airports, waspositive, in general terms, after the weakness exhibited in Q3.

Hotel Occupancy Inflow of Passengers to Airports

Regional Indicators of Activity in Tourism (Air Transportation and Traveler Accommodation)Index 2013=100, quarterly average

Source: Prepared and seasonally adjusted by Banco de México based on data from the Mexican Secretariat of Tourism and Auxiliary Services (ASA, for its acronym in Spanish).

50

60

70

80

90

100

110

120

130

140

150

160

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Northern North-Central Central Southern

QIV60

70

80

90

100

110

120

130

140

150

160

170

180

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Northern North-Central Central Southern

QIV

11

In Q4, the agricultural industry had a heterogeneous performance across regions. In the North-Centralregion production continued to expand, while in the Northern one it increased slightly, after havingcontracted in Q3. In contrast, in the Central and Southern regions production fell, after having increasedin Q3.

Index of Regional Agricultural ProductionIndex 2013=100, quarterly average

Source: Estimated and seasonally adjusted by Banco de México based on data from the Agricultural and Fisheries Information Service (SIAP). It should be noted that, unlike the GDP estimate, this indicator excludesinformation on the value generated by land cultivation and approximates a measurement of the gross production value, rather than that of added value generated in the sector.

60

70

80

90

100

110

120

130

140

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Northern North-Central Central Southern

QIV

12

Main Sources of Financing by Firms in Q4Percent of businesses that used each source of financing

Source: Banco de México.

Commercial banks Suppliers Own resources

Regarding the sources of financing, while the share of firms that resorted to financing by suppliers grewin all regions, the share of firms that used bank credit and own resources declined in a practicallygeneralized manner.

0

10

20

30

40

50

60

70

80

90

100

2016 2017 2018

Northern North-CentralCentral SouthernNational

QIV 0

10

20

30

40

50

60

70

80

90

100

2016 2017 2018

Northern North-CentralCentral SouthernNational

QIV0

10

20

30

40

50

60

70

80

90

100

2016 2017 2018

Northern North-CentralCentral SouthernNational

QIV

13

During Q4 2018, the increase in the number of IMSS-insured workers slowed down in most Mexicanregions.

Quarterly Seasonally Adjusted Change in the Number of IMSS-insured Workers 1/

Percent

1/ Permanent and temporary jobs in urban areas. Source: Estimated and seasonally adjusted by Banco de México with data from IMSS.

-4

-3

-2

-1

0

1

2

3

4

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Northern North-Central Central Southern

QIV

14

The Consumer Confidence Index registered particularly high levels from October 2018 to February 2019in the four regions of Mexico.

Consumer ConfidenceBalance of responses

Source: Prepared and seasonally adjusted by Banco de México with data from the series of the Consumer Confidence Index (INEGI) and Banco de México.

25

30

35

40

45

50

55

2014 2015 2016 2017 2018 2019

Northern North-Central Central Southern National

February

Activity

15

1/ Results obtained from responses to the question: “As a consequence of the recent situation regarding the fuel distribution in some states of Mexico, what is your assessment of the degree of impact in your firm on sale prices and production costs”, from interviews conducted by Banco de México between January 7 and January 31, 2019. Source: Banco de México.

According to most of the business agents interviewed, sales’ prices were not affected by the problemsof fuel distribution in early 2019. However, a significant share of business contacts reported certainimpact on economic activity, especially in the states of the Northern and Central regions.

Sales’ prices

Impact Level Reported by Firms as a result of Fuel Distribution Problems 1/

Share of responses

79%60%

46%

94%

69%

14%

19%32%

3%

18%

6%

12% 9%

2%

7%

1% 9% 13% 0% 6%

0%

20%

40%

60%

80%

100%

No

rth

ern

Nor

th-C

entr

al

Cen

tral

Sou

ther

n

Nat

iona

l

None Slight Medium High

95%98%

94% 93% 95%

4% 1% 5% 6% 4%

2% 1% 2% 1% 1%

50%

60%

70%

80%

90%

100%

Nor

ther

n

Nor

th-

Ce

ntr

al

Cen

tral

Sou

ther

n

Nat

iona

l

None Slight Medium-high

Outline

I. Regional Economic Report

II. Results October – December 2018

A. Economic activity

B. Inflation

C. Economic outlook (based on data obtained between January 7

and January 31, 2019)

III. Boxes

IV. Final remarks

16

Annual Headline Inflation, by RegionData in percent

Source: Prepared by Banco de México with data from INEGI and Banco de México.

Between Q2 and Q3 2018, annual headline inflation declined in all Mexican regions. This is essentiallyexplained by the lower levels of annual non-core inflation.

17

1

2

3

4

5

6

7

8

2013 2014 2015 2016 2017 2018 2019

Northern North-Central Central Southern National

February

18

Annual Core Inflation, by RegionData in percent

Core inflation showed a certain downward resistance in Q4 2018 in all regions, although it declinedmoderately in January and February 2019 in the Northern and central regions.

Source: Prepared by Banco de México with data from INEGI and own data.

1

2

3

4

5

6

7

8

2013 2014 2015 2016 2017 2018 2019

Northern North-Central Central Southern National

February

19

During Q4 2018, non-core inflation declined in all regions. The following contributed to the decline indomestic non-core inflation: the lower growth rates of the Central region –influenced by the evolutionof the agriculture and livestock sector– and those in the Northern border –as a result of the lowergrowth of energy goods, which was partly the result of the reduction of the VAT rate–.

Source: Prepared by Banco de México with data from INEGI and Banco de México.

Annual Non-core Inflation, by RegionData in percent

Impacts on Mexico’s Annual Non-core InflationIn percentage points

-2

0

2

4

6

8

10

12

14

2013 2014 2015 2016 2017 2018 2019

Southern

Central

North-Central

Northern border

Rest of the Northern region

Non-core February

0

3

6

9

12

15

2013 2014 2015 2016 2017 2018 2019

Northern North-Central Central Southern National

February

Outline

I. Regional Economic Report

II. Results October – December 2018

A. Economic activity

B. Inflation

C. Economic outlook (based on data obtained between January 7

and January 31, 2019)

III. Boxes

IV. Final remarks

20

21

Regional indices signal that both manufacturing and non-manufacturing activity will continue to expandin the next 3 months in all regional economies. In the manufacturing sector the signal of expansionstrengthened, at the margin, in the North-Central region, and weakened in the Southern region. In thenon-manufacturing sector the signal of expansion strengthened in the Northern and Southern regions.

Regional Index of Manufacturing and Non-manufacturing Orders: Activity Outlook, Next 3 Months 1/

Diffusion indices

Co

ntr

acti

on

Exp

ansi

on

Manufacturing Non-manufacturing

1/ Seasonally adjusted data.Source: Banco de México.

58

.4

57

.4

58

.2

57.5

57

.8

56.9

57

.5

57.059

.2

57.1

57.5

57.359

.5

58

.6

57

.7

55.4

0

10

20

30

40

50

60

70

80

Northern North-Central Central Southern

QI 2

01

8

QII

20

18

QII

I 20

18

QIV

20

18

QI 2

01

8

QII

20

18

QII

I 20

18

QIV

20

18

QI 2

01

8

QII

20

18

QII

I 20

18

QIV

20

18

QI 2

01

8

QII

20

18

QII

I 20

18

QIV

20

18

56.9

55.6

55

.9

54.6

56

.3

54.9

54.8

55

.1

55

.3

55

.0

55.1

53

.255

.9

54

.9

55

.3

55

.2

0

10

20

30

40

50

60

70

80

Northern North-Central Central Southern

QI 2

01

8

QII

20

18

QII

I 20

18

QIV

20

18

QI 2

01

8

QII

20

18

QII

II 2

01

8

QIV

20

18

QI 2

01

8

QII

20

18

QII

I 20

18

QIV

20

18

QI 2

01

8

QII

20

18

QII

I 20

18

QIV

20

18

22

Business Agents’ Expectations: Demand over Next 12 Months 1/

Diffusion indices

During the next twelve months, business agents consulted in the four regions anticipate a higherdemand for their goods and services. However, this signal was weaker than that in Q3 in all regions,except for the North-Central region, where it strengthened.

1/ Results obtained from responses to the question: “With respect to the volume of sales of your goods and services over the previous 12 months, how do you expect your sales’volume to change in the next 12 months?”, from interviews conducted by Banco de México.

Co

ntr

acti

on

Exp

ansi

on

92.9

84.189.4 88.5

84.187.9

73.4

81.4

0

10

20

30

40

50

60

70

80

90

100

Northern North-Central Central Southern

QIII

20

18

QIV

20

18

QIV

20

18

QIII

20

18

QIV

20

18

QIII

20

18

QIV

20

18

QIII

20

18

23

Consistent with the expected growth in demand for their own goods and services, business agentsanticipate an expansion of hired personnel and physical capital in all regions of Mexico, although forthese two indicators the signal weakened with respect to Q3.

Business Agents’ Expectations: Hired Personnel and Physical Capital, Next 12 Months 1/

Diffusion indices

Co

ntr

acti

on

Exp

ansi

on

Hired personnel Physical capital

1/ Results obtained from responses to questions: “With respect to the previous 12 months, how do you expect the total number of workers in your firm to change for the next 12 months?”, and “ With respect to your firm’s investmentin fixed assets during the previous 12 months, how do you expect investment levels to change in the following 12?”, from interviews conducted by Banco de México.

76.1 80.5

65.8

72.267.9

77.7

63.267.2

0

10

20

30

40

50

60

70

80

90

100

Northern North-Central Central Southern

QIV

20

18

QIV

20

18

QIII

20

18

QIV

20

18

QIII

20

18

QIV

20

18

QIII

20

18

QIII

20

18

90.689.1

77.172.8

82.486.3

73.670.1

0

10

20

30

40

50

60

70

80

90

100

Northern North-Central Central Southern

QIV

20

18

QIV

20

18

QIII

20

18

QIV

20

18

QIII

20

18

QIV

20

18

QIII

20

18

QIII

20

18

24

Factors Restricting Growth of Regional Economic Activity

• For the purposes of this Report, business contacts were interviewed about the factors restrictingeconomic growth during the next six months in the state in which the company is located.

• The information was collected as part of the Monthly Survey of Regional Economic Activity conductedby Banco de México among businesses of both manufacturing and non-manufacturing sectors. Inparticular, for this Report, the information was gathered between January 2 and January 30, 2019.

• Business contacts were consulted on the factors that could be grouped into 5 categories: i) governance;ii) inflation and monetary policy; iii) domestic economic conditions; iv) external conditions; and v)public finances.

The question is similar to that used by Banco de México to consult economic analysts regarding this issue inthe Survey of Professional Forecasters.

• In the future, this information will be collected on a quarterly basis to analyze long-term factors that,according to the interviewed business agents, could limit regional economic growth.

25

Share of Business Contacts' Responses regarding the Three Main Factors that could Hinder Economic Growth in Their Federal Entities

Percentage distribution of responses 1/

1/ Distribution relative to the total responses of business representatives, who can name up to three restricting factors for their respective state.

26

1/ Distribution relative to the total responses of business representatives, who can name up to three restricting factors for their respective state.

Governance

Inflation and monetary policy

Domestic economic conditions

External conditions

Public finances

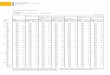

National Northern North-Central Central SouthernTotal 28.5 24.2 27.3 30.6 33.4Public safety issues 9.2 7.5 10.2 9.1 12.6Domestic political uncertainty 8.8 8.7 8.6 9.1 7.6Corruption 7.2 5.8 6.2 8.2 8.8Impunity 2.6 1.7 1.6 3.4 3.5Lack of rule of law 0.7 0.5 0.7 0.8 0.9Total 27.0 29.1 28.3 24.5 28.6Increase in input and commodity prices 11.3 12.6 11.2 10.1 12.1Inflation pressures in Mexico 5.2 4.6 6.3 5.1 5.1Monetary policy currently implemented 4.1 3.7 4.0 4.5 4.0Higher wage costs 3.6 5.3 4.0 2.2 4.1High cost of domestic financing 2.8 2.9 2.8 2.6 3.3Total 19.1 17.6 18.3 20.5 19.3Uncertainty regarding domestic economic situation 9.0 7.8 8.1 10.2 8.8Weakness of the domestic market 2.4 1.6 2.6 2.9 2.7Level of families' indebtedness 2.1 2.3 2.2 2.1 1.8Level of businesses' indebtedness 2.0 1.9 1.8 2.4 1.5Other

3/ 3.6 4.0 3.6 2.9 4.5Total 15.6 18.6 12.7 16.2 10.3Exchange rate uncertainty 4.8 6.4 5.1 4.3 2.6Level of the real exchange rate 2.7 2.8 1.0 3.8 1.6Foreign trade policy 2.2 2.9 1.6 2.1 1.4Other 4/ 5.9 6.5 5.0 6.0 4.7Total 9.8 10.5 13.4 8.2 8.4Fiscal policy 5.7 6.8 8.2 4.6 3.2Public spending policy 2.5 2.2 3.2 2.2 3.1Level of public sector indebtedness 1.6 1.5 2.0 1.4 2.1

Share of Business Contacts' Responses regarding The Three Main Factors that could Hinder Economic Growth in Their Federal Entities

Percentage distribution of responses 1/

Business Agents’ Opinion on Risks to Regional Economic Activity(based on data collected between January 7 and January 31, 2019) 1/

27

Upward risks Downward risks

That the announcements of the new tradeagreement between Mexico, the U.S. andCanada contribute to reactivate investment.

That new programs and projects areadequately implemented by the federalgovernment, which would contribute tolower the uncertainty prevailing amongbusiness agents.

That public safety conditions deteriorate.

That new episodes of fuel shortages occuror that those they were alreadyexperiencing extend for a longer period, orthat conflicts such as the blockage ofrailroads in Michoacán take place again.

That uncertainty over the public policies ofthe new administration persists orincreases, which could reduce investmentto levels below the expected.

1/ Results obtained from responses to the question: “What are the 2 main events/situations/facts that, if they should take place, would boost the economic performance of your state in the next 12 months?” and “What are the 2 mainevents/situations/facts that, if they should take place, would limit the economic performance of your state in the next 12 months?”, from Banco de México’s survey conducted during January 7-31, 2019.

28

Sales’ Prices Input Prices

Regarding sales’ prices of their own goods and services and their input prices, most interviewedbusiness contacts expect similar or lower annual changes, as compared to those observed in theprevious 12 months.

Business Agents’ Expectations: Annual Change of Sales’ Prices and Input Prices, Next 12 Months 1/

Percentage of responses

1/ Results obtained from responses to the question: “With respect to the previous 12 months, how do you expect sales’ prices in your sector to change over the next 12 months?”, and “With respect to theprevious 12 months, how do you expect input prices (goods and services) used in your sector to change over the next 12 months?”, from interviews conducted by Banco de México.

43

.33

2.7

32

.82

7.4

27

.3

42

.74

2.2

34

.0 39

.43

6.6

40

.5 46

.34

5.1

49

.64

8.2

38

.6 49

.5 56

.74

7.3

60

.8

41

.44

2.6

42

.04

0.9

42

.9

42

.55

4.2

56

.95

9.3

60

.9 39

.84

2.2

50

.0 48

.14

8.5

17

.12

1.3

23

.93

1.5 39

.3

39

.63

7.9

36

.53

7.5 2

0.6

34

.7 38

.84

1.8

44

.14

2.9

14

.21

3.1

10

.31

3.3

11

.8

17

.51

5.7

16

.01

2.5

14

.9

42

.3 32

.43

1.0 1

8.9 12

.5

21

.8 12

.6 6.7

15

.21

8.6

23

.9 18

.61

6.2

15

.01

4.3

0

20

40

60

80

100

IVQ

17

IQ1

8II

Q1

8III

Q1

8IV

Q1

8

IVQ

17

IQ1

8II

Q1

8III

Q1

8IV

Q1

8

IVQ

17

IQ1

8II

Q1

8II

IQ1

8IV

Q1

8

IVQ

17

IQ1

8II

Q1

8II

IQ1

8IV

Q1

8

IVQ

17

IQ1

8II

Q1

8III

Q1

8IV

Q1

8

Greaterchange

Similarchange

Lowerchange

Northern North-Central Central Southern National

25

.0 33

.32

9.7

21

.2 31

.0

17

.5 25

.01

3.9 19

.6 26

.7 36

.93

1.5 36

.33

1.3 4

1.4

31

.74

7.1

60

.64

1.4

54

.2

27

.8 34

.33

5.1

28

.5 38

.0

53

.35

0.0

49

.25

3.1

55

.8

51

.55

6.0

51

.55

6.9 49

.5

15

.32

7.9

20

.4 39

.33

6.0

35

.64

3.3

36

.54

2.3 2

6.0

39

.14

4.0

39

.24

7.7

42

.3

21

.7 16

.72

1.2

25

.7 13

.3

31

.1 19

.03

4.7 2

3.5

23

.8

47

.8 40

.54

3.4

29

.5 22

.5

32

.79

.6 2.9

16

.21

9.8

33

.1 21

.82

5.7

23

.71

9.7

0

20

40

60

80

100

IVQ

17IQ

18IIQ

18III

Q18

IVQ

18

IVQ

17IQ

18IIQ

18III

Q18

IVQ

18

IVQ

17IQ

18IIQ

18III

Q18

IVQ

18

IVQ

17IQ

18IIQ

18III

Q18

IVQ

18

IVQ

17IQ

18IIQ

18III

Q18

IVQ

18

Northern North-Central Central Southern National

29

By Region Northern region

Regarding the expected growth of wage costs for the next 12 months, although most business contactsexpect similar or lower changes, in all regions, except for the North-Central one, the share of businessagents who anticipate a greater change increased as compared to Q3, especially in the south and in thenorthern border strip.

Business Agents’ Expectations: Annual Change of Wage Costs, Next 12 Months 1/

Share of responses

1/ Results obtained from responses to the question: “With respect to the previous 12 months, how do you expect wages of your sector’s workers to change in the next 12 months?; from interviews conducted by Banco de México.2/ Northern border free zone.

14

.2

12

.4

17

.7

20

.6

19

.6 29

.5 41

.1

20

.2

23

.2

20

.7

73

.5

70

.8

63

.7 65

.7

61

.6

45

.5

46

.4

52

.1 61

.3

58

.7

12

.4

16

.8

18

.6

13

.7

18

.8

25

.0 12

.5

27

.7 15

.5

20

.70

20

40

60

80

100

IIIQ

18

IVQ

18

IIIQ

18

IVQ

18

IIIQ

18

IVQ

18

IIIQ

18

IVQ

18

IIIQ

18

IVQ

18

Greaterchange

Similarchange

Lowerchange

Northern North-Central Central Southern National

10

.8

3.3 15

.8

15

.7

73

.0

66

.7

73

.7

72

.3

16

.2

30

.0 10

.5

12

.0

0

20

40

60

80

100

IIIQ

18

IVQ

18

IIIQ

18

IVQ

18

GreaterChange

SimilarChange

LowerChange

ZLFN2/ Rest

30

Wage costs’ expectations evolved in a context in which the minimum wage in the northern borderregion doubled, while in the rest of Mexico it adjusted from 88.4 to 102.7 pesos a day.

Nominal Daily Wage of IMSS-insured Workers 1/

Annual percent change

1/ It includes the municipalities listed in the DOF on December 26, 2018, most of which are adjacent to the Mexicannorthern border.2/ This is the total of other Mexican municipalities.Source: Prepared by Banco de México with data from IMSS.

Ratio of Minimum Wage to MeanBase Wage, by Region

1/ Minimum wages for 2019, both in the Northern region and at the national level, are obtained by weighing the minimum wage of theNorthern border free zone (ZLFN, for its acronym in Spanish) and the minimum wage in the rest of Mexico, by the number of ZLFNworkers and the number of remaining workers, respectively.2/ Mean base wage calculated for the region of the respective column.Source: Banco de México with data from IMSS.

Total 1/ ZLFN Other

(%) 2/ 37.7 37.3 38.2 44.1 39.7 48.0 40.7

(%) 2/ 55.9 74.6 44.4 51.3 46.2 55.7 50.9

Increase (p.p.) 17.5 36.0 6.0 7.0 6.2 7.8 9.7

NorthernNorth-

CentralCentral Southern National 1/

4.1 4.3

4.5

4.9

5.0

4.8

4.8

4.8

5.0

5.1

4.9

5.5

5.1

5.4

5.9

5.8

5.4

5.8

5.9

5.9

5.8

5.8

5.9

5.4

6.9

0

2

4

6

8

10

12

14

16

Jan

-17

Ap

r-1

7

Jul-

17

Oct

-17

Jan

-18

Ap

r-1

8

Jul-

18

Oct

-18

Jan

-19

Total nominal

Nominal at the border strip 1/

Nominal in the rest of Mexico 2/

Outline

I. Regional Economic Report

II. Results October – December 2018

A. Economic activity

B. Inflation

C. Economic outlook (based on data collected between January 7

and January 31, 2019)

III. Boxes

IV. Final remarks

31

Boxes

32

Clusters of Related Industries in Regional Economies1

Interregional Labor Mobility of Skilled and Unskilled Workers in Mexico, 2000 - 2015

2

Factors Restricting Growth of Regional Economic Activity3

33

• This Box explores the relationships between different sectors of the Mexican economy in order todefine groups of related industries, called clusters.

• In order to do so, this Box implemented the methodology proposed by Delgado et al. (2016) toidentify industrial clusters.

• This method, unlike others, such as the one suggested by Feser et al. (2005), which only includespurchase and sale transactions among industries to select the adequate configuration of clusters,considers multiple links among industries in order to group them, such as the resemblance ingeographical distribution of employments and their establishments.

• 21 clusters were identified, out of which 4 concentrated over a third of the census gross valueadded: i) oil and gas extraction; ii) automobile and truck manufacturing; iii) head offices; and iv)wired communication carriers.

Box: Clusters of Related Industries in Regional Economies

34

Cluster configuration

1\ The main industry of a cluster is the industry with the largest share in the census gross added value registered in said cluster.Source: Prepared by Banco de México with data from 2014 Economic Census and 2012 Input-output matrix.

Box: Clusters of Related Industries in Regional Economies

Cluster Main industry 1\ Other industries in the cluster

Number of

industries in

the cluster

Share of

national output

Share of

national census

gross added

value

Share of national

employment in

2014 Economic

Census

Added value by

worker (thousands

of jobs)

1 2111 Oil and gas extraction

3241 Petroleum and coal products

manufacturing; 4831 Sea, coastal, and great

lakes transportation; 4869 Other pipeline

transportation

9 14.9 16.8 0.7 6,230.5

23361 Motor vehicle

manufacturing

3363 Motor vehicle parts manufacturing;

3336 Turbine and power transmission

equipment mfg; 3311 Iron and steel mills

and ferroalloy mfg.

6 12.5 7.7 3.5 602.2

35511 Management of

companies and enterprises

5616 Investigation and security services;

5611 Office administrative services; 5242

Insurance agencies and brokerages

32 7.9 10.0 6.8 405.2

43119 Other food

manufacturing

3113 Sugar and confectionery product

manufacturing; 4884 Support activities for

road transportation; 3116 Animal

slaughtering and processing

23 7.1 5.8 5.1 315.4

35

Number of Clusters in which the State has a Relative SpecializationShares

Source: Prepared by Banco de México based on data from 2014 Economic Census.

Box: Clusters of Related Industries in Regional Economies

• Once 21 industrial clusters have been identified; the number of clusters in which each state has arelative specialization is explored.

36

Presence of Clusters vs. Added Value by Worker, by State 1/

1/ Excludes oil and gas extraction cluster. 2/ Spearman’s correlation coefficient. ***Significant at 1% of confidence level.Source: Prepared by Banco de México with data from 2014 Economic Census.

Box: Clusters of Related Industries in Regional Economies

• It is observed that a greater economic diversity is positively associated with higher levels of laborproductivity.

0

20

40

60

80

100

120

0 2 4 6 8 10 12 14 16 18

Ad

ded

val

ue,

by

wo

rker

(I

nd

ex,

CD

MX

=10

0)

Number of clusters with relative specialization

NorthernNorth-CentralCentralSouthern

Correlation coefficient:2/ 0.45***

Boxes

37

Clusters of Related Industries in Regional Economies1

Interregional Labor Mobility of Skilled and Unskilled Workers in Mexico, 2000 - 2015

2

Factors Restricting Growth of Regional Economic Activity3

38

• As part of Mexico’s open trade policy and, particularly of NAFTA’s entry into force, theNorthern region experienced a higher demand for unskilled labor, which in turn raised therelative wages of this type of workers.

• However, labor demand in the manufacturing sector seems to have declined as a consequenceof China’s accession to the WTO and to the 2009 global financial crisis.

• Likewise, there is evidence that after 1994, the relative wages of skilled workers increased inthe Central region.

• Although labor mobility determinants are complex and diverse, this Box presents evidence ofchanges in the dynamics of interregional migratory flows in Mexico regarding both skilled andunskilled workers, which are consistent with the effects of trade openness.

Box: Interregional Labor Mobility of Skilled and Unskilled Workers in Mexico, 2000 - 2015

39

Note: %I is % of each region with respect to migrants’ inflow; %O is % of each region with respect to migrants’ outflow.Source: Estimated by Banco de México with data from 2000 Population Census and 2015 Inter-census Survey.

Flows of Unskilled Interregional Migration 2010 - 2015

Box: Interregional Labor Mobility of Skilled and Unskilled Workers in Mexico, 2000 - 2015

1995 - 2000

40

Note: %I is % of each region with respect to migrants’ inflow; %O is % of each region with respect to migrants’ outflow.Source: Estimated by Banco de México with data from 2000 Population Census and 2015 Inter-census Survey.

Flows of Skilled Interregional Migration 2010 - 2015

Box: Interregional Labor Mobility of Skilled and Unskilled Workers in Mexico, 2000 - 2015

1995 - 2000

41

Source: Estimated by Banco de México with data from 2000 Population Census and 2015 Inter-census Survey.

Box: Interregional Labor Mobility of Skilled and Unskilled Workers in Mexico, 2000 - 2015

Net Balance of MigrantsNumber of people

SkilledUnskilled

-250,000

-150,000

-50,000

50,000

150,000

250,000

350,000

Northern North- Central Central Southern

1995 - 2000 2005 - 2010 2010 - 2015

Ne

t in

flo

wN

et o

utf

low

-30,000

-20,000

-10,000

0

10,000

20,000

30,000

40,000

Northern North-Central Central Southern

1995 - 2000 2005 - 2010 2010 - 2015

Net

infl

ow

Net

ou

tflo

w

42

Relationship between Contribution on Regional Growth and Skilled Labor Intensity of a Sector 1/ 2010 -2015.

Percentage points

1/ A sector least intensive in skilled labor force is marked with a value of 1, and the most intensive one, with a value of 31.Source: Estimated by Banco de México based on GDP series by state and data from 2010 Economic Census, INEGI.

Northern

North-Central

Central

Southern

Box: Interregional Labor Mobility of Skilled and Unskilled Workers in Mexico, 2000 - 2015

y = 0.0116x + 0.4129

-1

0

1

2

3

4

0 5 10 15 20 25 30 35

Co

ntr

ibu

tio

n

on

Gro

wth

Skilled Labor Intensity

y = 0.0081x + 0.4796

-1

0

1

2

3

4

0 5 10 15 20 25 30 35

Co

ntr

ibu

tio

n

on

Gro

wth

Skilled Labor Intensity

y = 0.026x + 0.1571

-1

0

1

2

3

4

0 5 10 15 20 25 30 35

Co

ntr

ibu

tio

n

on

Gro

wth

Skilled Labor Intensity

y = -0.0004x + 0.1763

-4

-3

-2

-1

0

1

2

3

0 5 10 15 20 25 30 35

Co

ntr

ibu

tio

n

on

Gro

wth

Skilled Labor Intensity

Outline

I. Regional Economic Report

II. Results October – December 2018

A. Economic activity

B. Inflation

C. Economic outlook (based on data collected between January 7

and January 31, 2019)

III. Boxes

IV. Final remarks

43

Final Remarks

• For different regions of Mexico to attain a more dynamic and sustained growth that canraise the welfare of Mexico’s population, in addition to continuously strengthening themacroeconomic framework, structural and institutional problems need to be addressed,both at the national and local levels, which have prevented the economy from achievinghigher levels of productivity and which have discouraged investment.

• To reach these goals, the institutional design of incentives needs to be revised, so that valuecreation is favored, the adoption of cutting-edge technologies is encouraged, tradeopenness and investment flows are maintained, and economic competition is fostered. Inthe same way, it is necessary to adopt policies to fight public insecurity, corruption andimpunity, and to guarantee legal certainty and respect for private property in all regions ofMexico.

• By improving the efficiency of the economy and fostering the rule of law, the regionaleconomies will be in a better condition to address different challenges that may emerge andgrant a better quality of life to their population.

44

March 2019