Embed Size (px)

Citation preview

Slide1LabyrinthConsultingServices,Inc. artberman.com

October 2017 Oil & Gas Discussion

MacroVoices

Art Berman Labyrinth Consulting Services, Inc.

October 19, 2017

Slide2LabyrinthConsultingServices,Inc. artberman.com

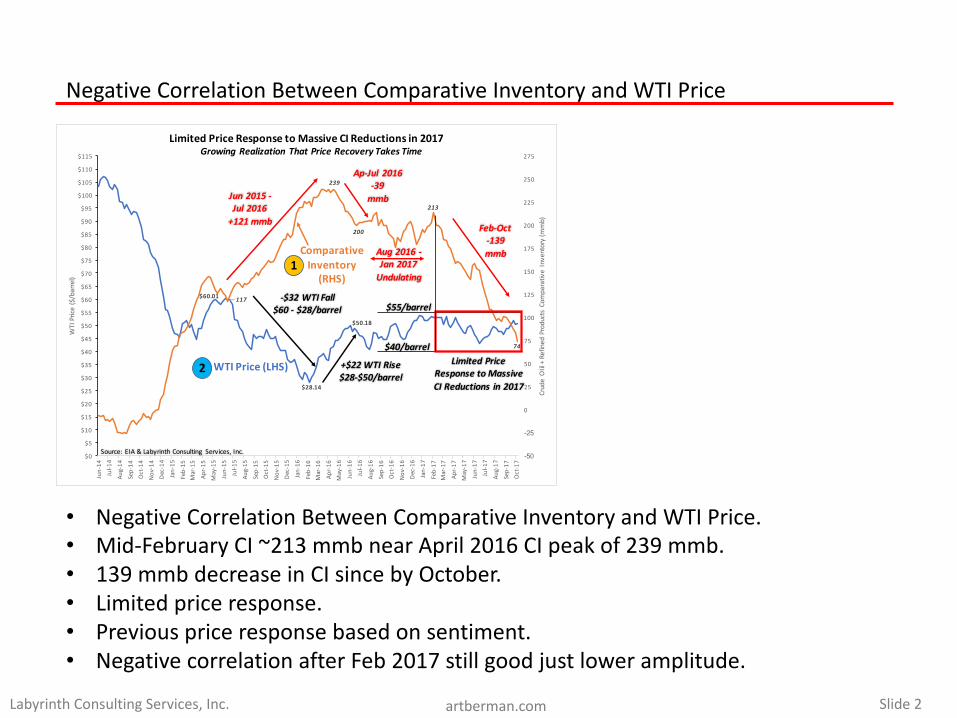

NegativeCorrelationBetweenComparativeInventoryandWTIPrice

$60.01

$28.14

$50.18

117

239

200

213

74

-50

-25

0

25

50

75

100

125

150

175

200

225

250

275

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

$55

$60

$65

$70

$75

$80

$85

$90

$95

$100

$105

$110

$115

Jun-14

Jul-1

4 Au

g-14

Sep-14

Oct-14

Nov-14

Dec-14

Jan-15

Feb-15

Mar-15

Apr-15

May-15

Jun-15

Jul-1

5 Au

g-15

Sep-15

Oct-15

Nov-15

Dec-15

Jan-16

Feb-16

Mar-16

Apr-16

May-16

Jun-16

Jul-1

6 Au

g-16

Sep-16

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

May-17

Jun-17

Jul-1

7 Au

g-17

Sep-17

Oct-17

CrudeOIil+RefinedProductsComparativeInventory(m

mb)

WTIPrice($/barrel)

LimitedPriceResponsetoMassiveCIReductionsin2017

Source:EIA&LabyrinthConsulting Services,Inc.

ComparativeInventory(RHS)

WTIPrice(LHS)

Feb-Oct-139mmb

Ap-Jul 2016-39mmb

Aug2016-Jan2017Undulating

Jun2015-Jul2016+121 mmb

-$32WTIFall$60- $28/barrel $55/barrel

$40/barrel

+$22WTIRise$28-$50/barrel

Limited PriceResponsetoMassiveCIReductionsin2017

GrowingRealization ThatPriceRecoveryTakesTime

1

2

• NegativeCorrelationBetweenComparativeInventoryandWTIPrice.• Mid-FebruaryCI~213mmb nearApril2016CIpeakof239mmb.• 139mmb decreaseinCIsincebyOctober.• Limitedpriceresponse.• Previouspriceresponsebasedonsentiment.• NegativecorrelationafterFeb2017stillgoodjustloweramplitude.

Slide3LabyrinthConsultingServices,Inc. artberman.com

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

$55

$60

$65

$70

$75

$80

$85

$90

$95

$100

$105

$110

$115

-50 -40 -30 -20 -10 0 10 20 30 40 50 60 70 80 90 100 110 120 130 140 150 160 170 180 190 200 210 220 230 240 250

SentimentHasBeenLargelyRemovedFromOilPriceResponsetoCIReductionGrowingRealizationThatPriceRecoveryTakesTime

Comparative Inventory (C.I.)Millionsof Barrels

WTIPrice($/barrel)

Source:EIA&La

byrinthConsultingServices,Inc.

$40

$55

Mar-June 2015Optimism

2014-2017Data Mid-cycleprice

(5-yearaverage)

Late 2015-Early2016Pessimisim(Cushing >

80%Capacity)

OPEC ProductionCutOptimismOct13

Mid-Feb

139mmb

YieldCurve

74mmb

Price responsewill bemorepronouncedgoing forward

becauseofincreasingcurvatureoftheYieldCurve

1

2

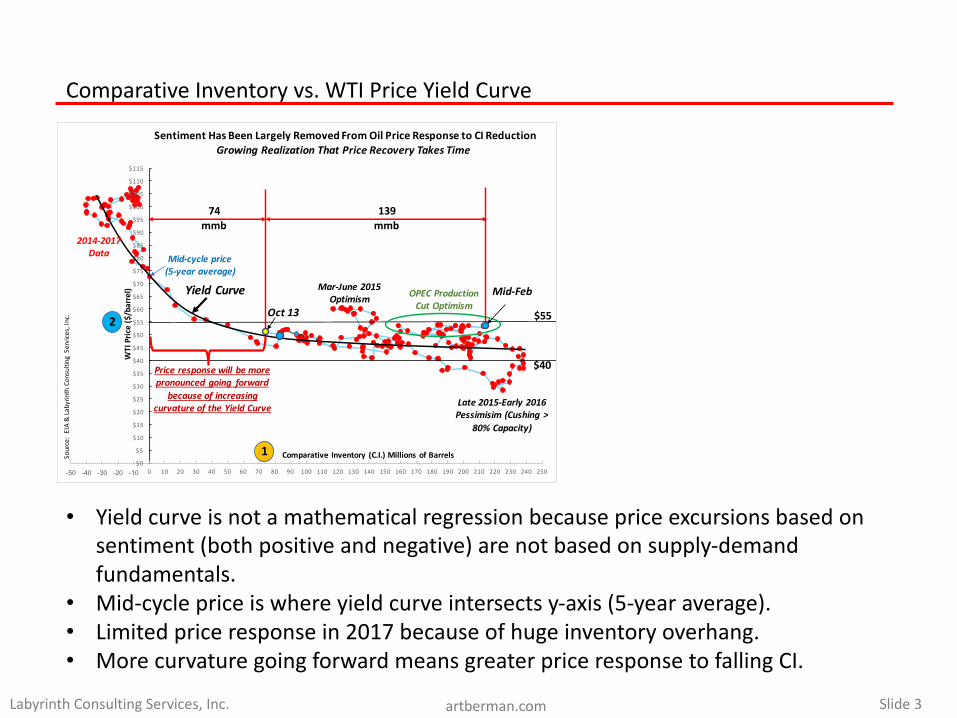

ComparativeInventoryvs.WTIPriceYieldCurve

• Yieldcurveisnotamathematicalregressionbecausepriceexcursionsbasedonsentiment(bothpositiveandnegative)arenotbasedonsupply-demandfundamentals.

• Mid-cyclepriceiswhereyieldcurveintersectsy-axis(5-yearaverage).• Limitedpriceresponsein2017becauseofhugeinventoryoverhang.• MorecurvaturegoingforwardmeansgreaterpriceresponsetofallingCI.

Slide4LabyrinthConsultingServices,Inc. artberman.com

$0

$20

$40

$60

$80

$100

$120

800

850

900

950

1,000

1,050

1,100

1,150

1,200

1/1/10 1/1/11 1/1/12 1/1/13 1/1/14 1/1/15 1/1/16 1/1/17

WTIPrice($/barrel)

IvnetoriesofCrudeOil+Products(m

mb)

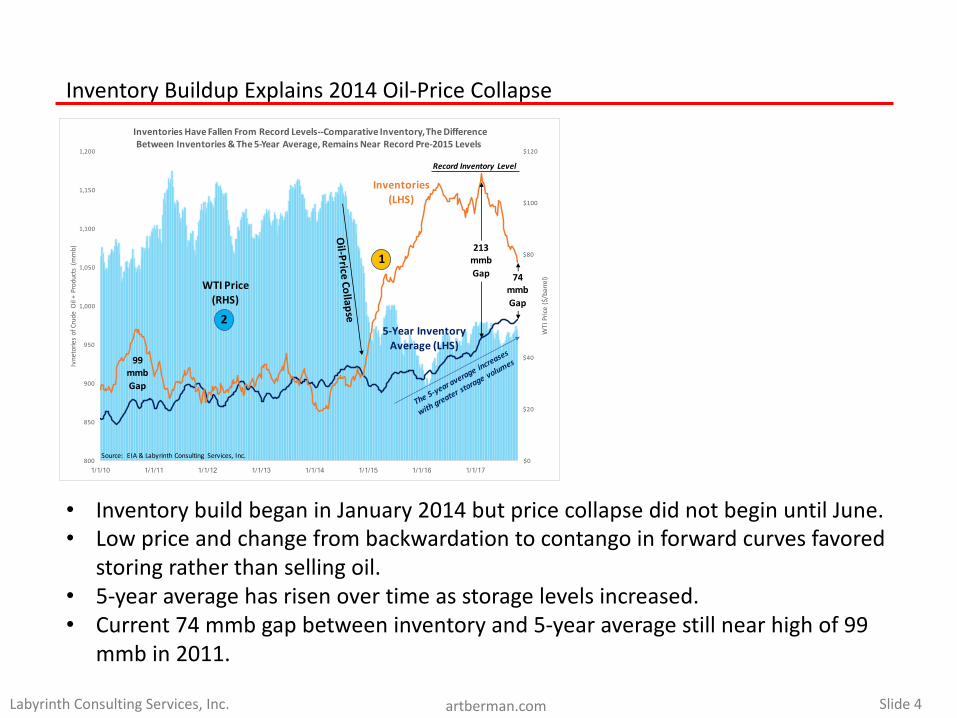

InventoriesHaveFallenFromRecordLevels--ComparativeInventory,TheDifferenceBetweenInventories&The5-YearAverage,RemainsNearRecordPre-2015Levels

Source:EIA &LabyrinthConsulting Services,Inc.

5-YearInventoryAverage(LHS)

WTIPrice(RHS)

Inventories(LHS)

99mmbGap

74mmbGap

RecordInventoryLevel

213mmbGap

1

2

• InventorybuildbeganinJanuary2014butpricecollapsedidnotbeginuntilJune.• Lowpriceandchangefrombackwardationtocontango inforwardcurvesfavored

storingratherthansellingoil.• 5-yearaveragehasrisenovertimeasstoragelevelsincreased.• Current74mmb gapbetweeninventoryand5-yearaveragestillnearhighof99

mmb in2011.

InventoryBuildupExplains2014Oil-PriceCollapse

Slide5LabyrinthConsultingServices,Inc. artberman.com

0

2

4

6

8

10

12

14

16

18

20

5

5.5

6

6.5

7

7.5

8

8.5

9

9.5

10

1/1/16

2/1/16

3/1/16

4/1/16

5/1/16

6/1/16

7/1/16

8/1/16

9/1/16

10/1/

16

11/1/

16

12/1/

16

1/1/17

2/1/17

3/1/17

4/1/17

5/1/17

6/1/17

7/1/17

8/1/17

9/1/17

10/1/

17

RefineryInput&

ImpliedStockChange(m

mb/d)

Production&NetIm

ports(m

mb/d)

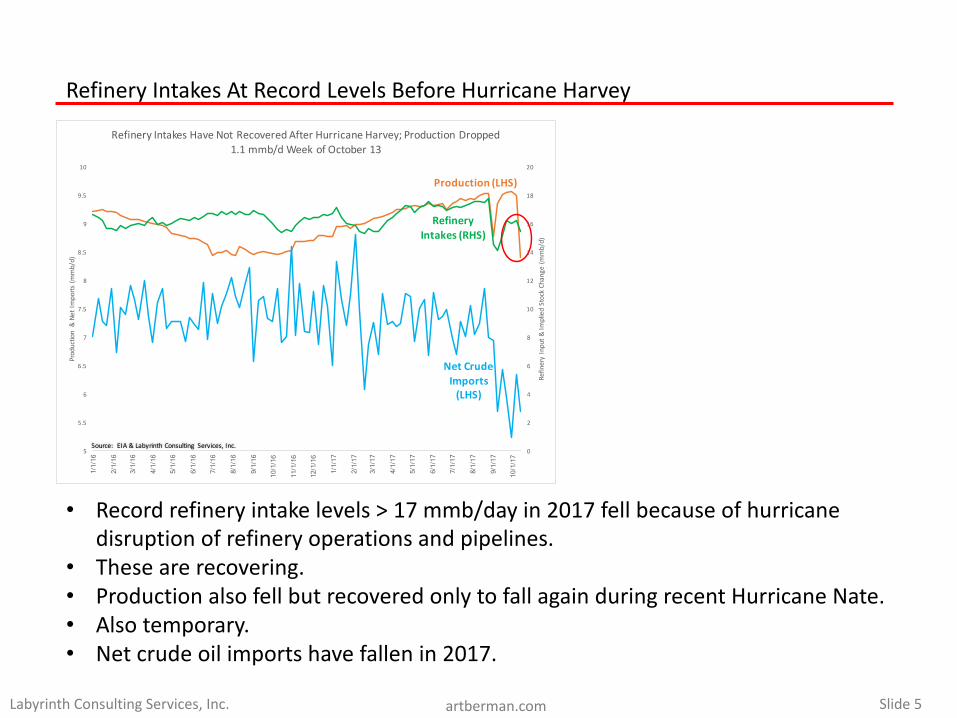

RefineryIntakesHaveNotRecoveredAfterHurricaneHarvey;ProductionDropped1.1mmb/dWeekofOctober13

Production(LHS)

NetCrudeImports(LHS)

RefineryIntakes(RHS)

Source:EIA &LabyrinthConsulting Services,Inc.

• Recordrefineryintakelevels>17mmb/dayin2017fellbecauseofhurricanedisruptionofrefineryoperationsandpipelines.

• Thesearerecovering.• ProductionalsofellbutrecoveredonlytofallagainduringrecentHurricaneNate.• Alsotemporary.• Netcrudeoilimportshavefallenin2017.

RefineryIntakesAtRecordLevelsBeforeHurricaneHarvey

Slide6LabyrinthConsultingServices,Inc. artberman.com

-100

-50

0

50

100

150

200

250

300

18.0

18.5

19.0

19.5

20.0

20.5

21.0

21.5

22.0

22.5

1/3/14

3/3/14

5/3/14

7/3/14

9/3/14

11/3/

14

1/3/15

3/3/15

5/3/15

7/3/15

9/3/15

11/3/

15

1/3/16

3/3/16

5/3/16

7/3/16

9/3/16

11/3/

16

1/3/17

3/3/17

5/3/17

7/3/17

9/3/17

CrudeOil+

RefinedProductsComparativeInventory(m

mb)

Csonum

ption(ProductSupplied)(m

mb/d)

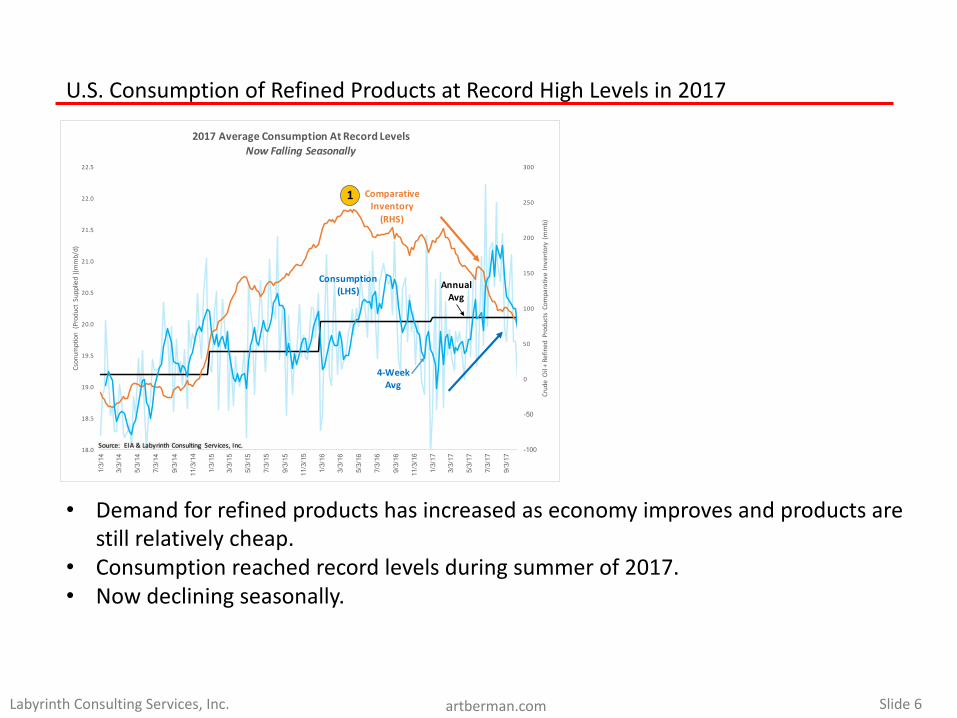

2017AverageConsumptionAtRecordLevelsNowFallingSeasonally

Consumption(LHS)

ComparativeInventory(RHS)

Source:EIA &LabyrinthConsulting Services,Inc.

4-WeekAvg

AnnualAvg

1

• Demandforrefinedproductshasincreasedaseconomyimprovesandproductsarestillrelativelycheap.

• Consumptionreachedrecordlevelsduringsummerof2017.• Nowdecliningseasonally.

U.S.ConsumptionofRefinedProductsatRecordHighLevelsin2017

Slide7LabyrinthConsultingServices,Inc. artberman.com

0

50

100

150

200

250

300

-4500

-4000

-3500

-3000

-2500

-2000

-1500

-1000

-500

0

1/1/16

1/1

5/16

1/29/1

6 2/1

2/16

2/26/1

6 3/1

1/16

3/25/1

6 4/8

/16

4/22/1

6 5/6

/16

5/20/1

6 6/3

/16

6/17/1

6 7/1

/16

7/15/1

6 7/2

9/16

8/12/1

6 8/2

6/16

9/9/16

9/2

3/16

10/7/

16

10/21

/16

11/4/

16

11/18

/16

12/2/

16

12/16

/16

12/30

/16

1/13/1

7 1/2

7/17

2/10/1

7 2/2

4/17

3/10/1

7 3/2

4/17

4/7/17

4/2

1/17

5/5/17

5/1

9/17

6/2/17

6/1

6/17

6/30/1

7 7/1

4/17

7/28/1

7 8/1

1/17

8/25/1

7 9/8

/17

9/22/1

7 10

/6/17

CrudeOIl+ProductsCom

parativeInventories(m

mb)

NetP

etroleum

ProductImports(m

mb/d)

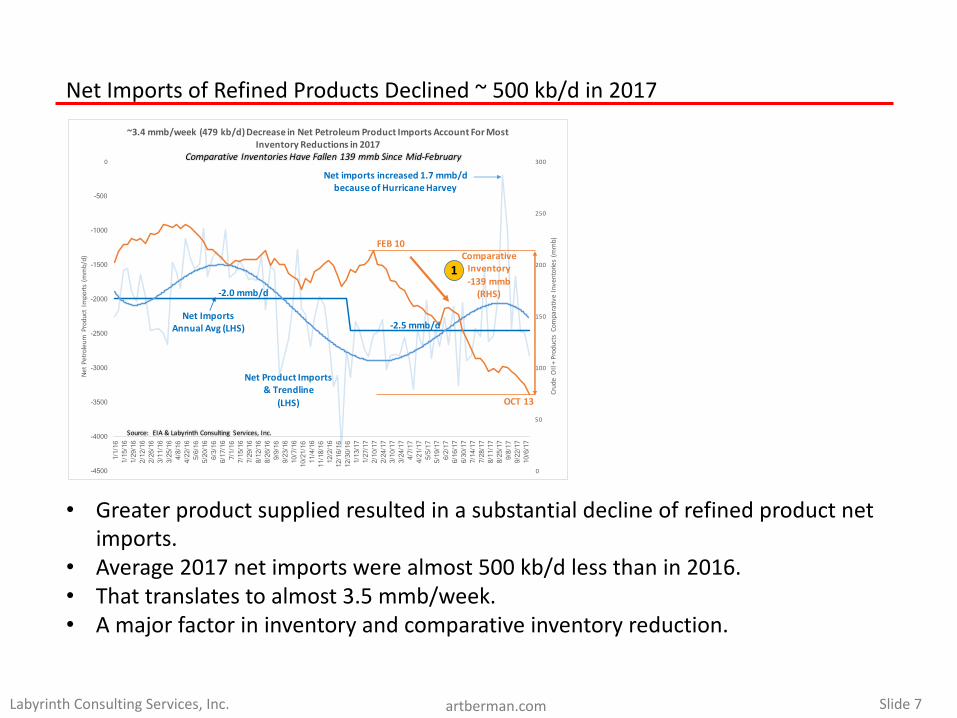

~3.4mmb/week(479kb/d)DecreaseinNetPetroleumProductImportsAccountForMostInventoryReductionsin2017

ComparativeInventory-139mmb(RHS)

NetImportsAnnual Avg(LHS)

NetProductImports&Trendline

(LHS)

-2.0mmb/d

-2.5mmb/d

Source:EIA &LabyrinthConsulting Services,Inc.

ComparativeInventoriesHaveFallen139mmbSinceMid-February

FEB10

OCT13

Netimportsincreased1.7mmb/dbecauseofHurricaneHarvey

1

• Greaterproductsuppliedresultedinasubstantialdeclineofrefinedproductnetimports.

• Average2017netimportswerealmost500kb/dlessthanin2016.• Thattranslatestoalmost3.5mmb/week.• Amajorfactorininventoryandcomparativeinventoryreduction.

NetImportsofRefinedProductsDeclined~500kb/din2017

Slide8LabyrinthConsultingServices,Inc. artberman.com

0

1

2

3

4

5

6

7

8

9

0

0.5

1

1.5

2

2.5

Jan-16

Feb-16

Mar-16

Apr-16

May-16

Jun-16

Jul-16

Aug-16

Sep-16

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

May-17

Jun-17

Jul-17

Aug-17

Sep-17

Oct-17

NetCrudeO

ilIm

ports(m

mb/d)

CrudeO

ilExports(m

mb/d)

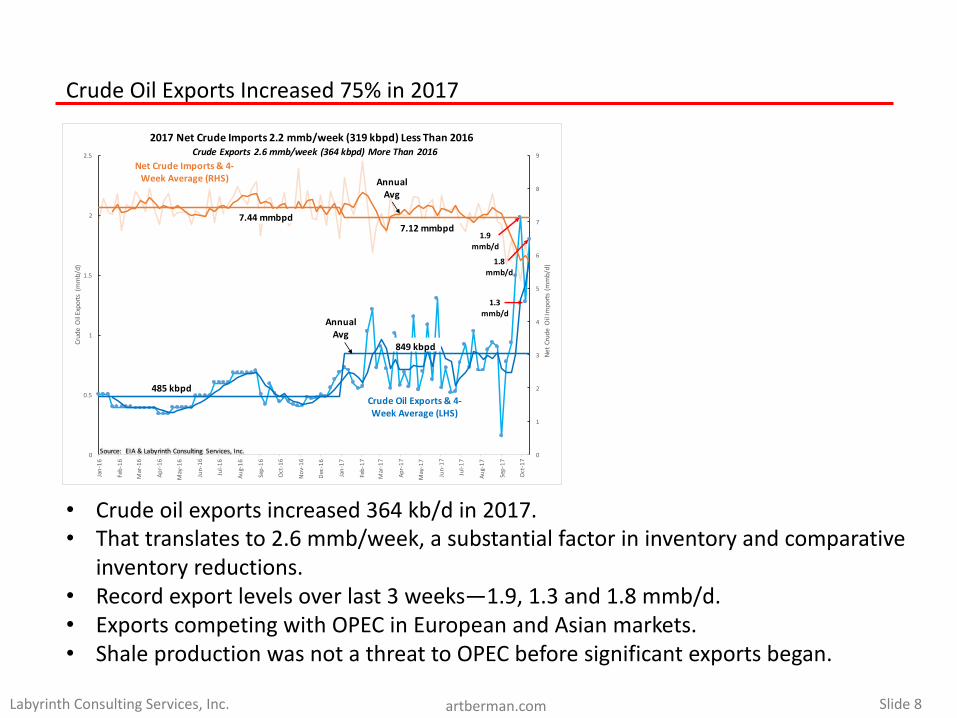

2017NetCrudeImports2.2mmb/week(319kbpd)LessThan2016

CrudeOilExports&4-

WeekAverage(LHS)

NetCrudeImports&4-

WeekAverage(RHS)

Source:EIA &LabyrinthConsulting Services,Inc.

Annual

Avg

Annual

Avg

849kbpd

485kbpd

7.44mmbpd

7.12mmbpd1.9

mmb/d

1.8

mmb/d

CrudeExports 2.6mmb/week(364kbpd)MoreThan2016

1.3

mmb/d

CrudeOilExportsIncreased75%in2017

• Crudeoilexportsincreased364kb/din2017.• Thattranslatesto2.6mmb/week,asubstantialfactorininventoryandcomparative

inventoryreductions.• Recordexportlevelsoverlast3weeks—1.9,1.3and1.8mmb/d.• ExportscompetingwithOPECinEuropeanandAsianmarkets.• ShaleproductionwasnotathreattoOPECbeforesignificantexportsbegan.

Slide9LabyrinthConsultingServices,Inc. artberman.com

-100

-50

0

50

100

150

200

250

300

350

400

1/1/16

2/1/16

3/1/16

4/1/16

5/1/16

6/1/16

7/1/16

8/1/16

9/1/16

10/1/

16

11/1/

16

12/1/

16

1/1/17

2/1/17

3/1/17

4/1/17

5/1/17

6/1/17

7/1/17

8/1/17

9/1/17

10/1/

17

Gasoline&Distilla

teCom

parativeInventory(m

mb)

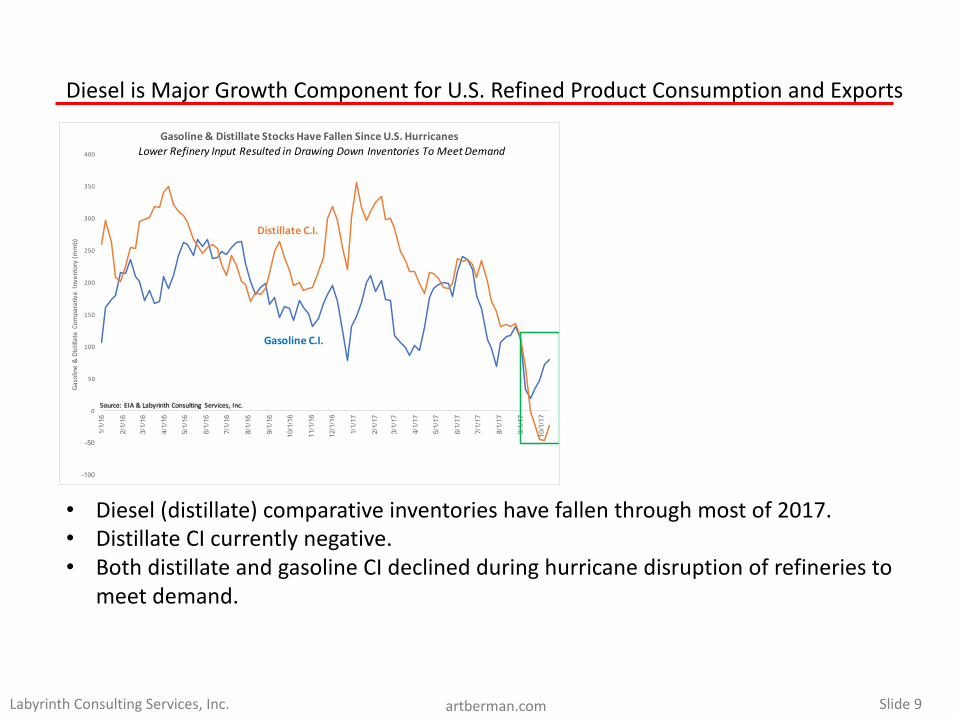

Gasoline&DistillateStocksHaveFallenSinceU.S.Hurricanes

Source:EIA&LabyrinthConsulting Services,Inc.

Gasoline C.I.

Distillate C.I.

LowerRefineryInputResultedinDrawingDownInventories ToMeetDemand

DieselisMajorGrowthComponentforU.S.RefinedProductConsumptionandExports

• Diesel(distillate)comparativeinventorieshavefallenthroughmostof2017.• DistillateCIcurrentlynegative.• BothdistillateandgasolineCIdeclinedduringhurricanedisruptionofrefineriesto

meetdemand.

Slide10LabyrinthConsultingServices,Inc. artberman.com

$44

$45

$46

$47

$48

$49

$50

$51

$52

$53

$54

Oct-17

Dec-17

Feb-18

Ap

r-18

Jun-18

Au

g-18

Oct-18

Dec-18

Feb-19

Ap

r-19

Jun-19

Au

g-19

Oct-19

Dec-19

Feb-20

Ap

r-20

Jun-20

Au

g-20

Oct-20

Dec-20

Feb-21

Ap

r-21

Jun-21

Au

g-21

Oct-21

Dec-21

Feb-22

Ap

r-22

Jun-22

Au

g-22

Oct-22

Dec-22

WTIFuturesPrice($/barrel)

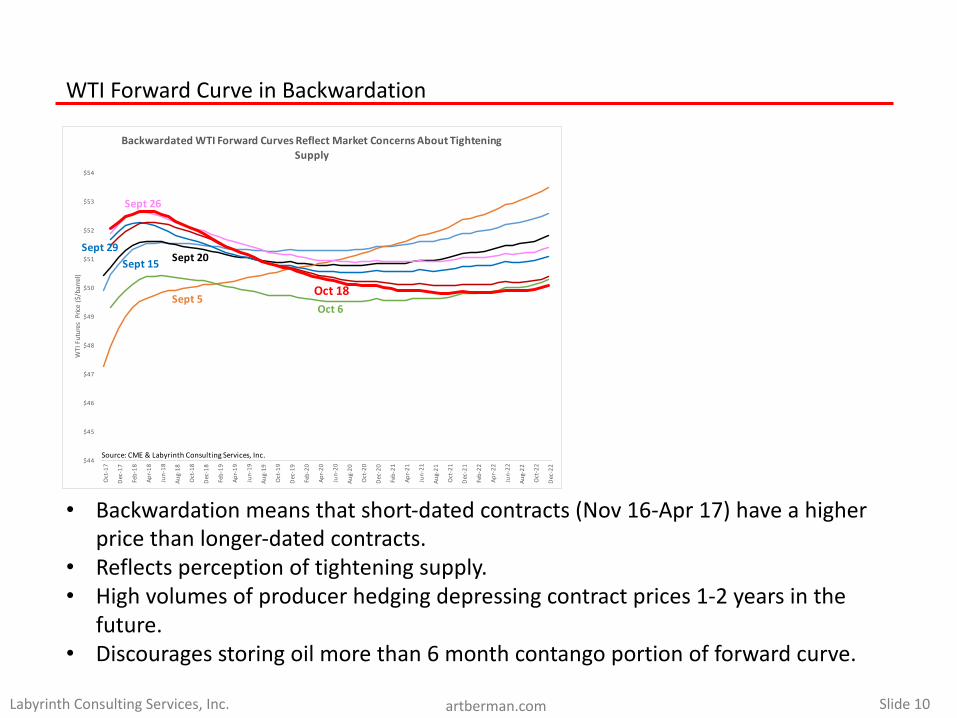

BackwardatedWTIForwardCurvesReflectMarketConcernsAboutTighteningSupply

Source:CME& LabyrinthConsultingServices,Inc.

Sept15 Sept20

Sept5

Sept26

Sept29

Oct6Oct18

WTIForwardCurveinBackwardation

• Backwardationmeansthatshort-datedcontracts(Nov16-Apr17)haveahigherpricethanlonger-datedcontracts.

• Reflectsperceptionoftighteningsupply.• Highvolumesofproducerhedgingdepressingcontractprices1-2yearsinthe

future.• Discouragesstoringoilmorethan6monthcontango portionofforwardcurve.

Slide11LabyrinthConsultingServices,Inc. artberman.com

0.00

-0.27

-1.56

-1.72

-2.25 -2.21

-1.72

-1.41

-1.07

-1.28

-1.08

50

50.5

51

51.5

52

52.5

53

53.5

54

54.5

-2.60

-2.40

-2.20

-2.00

-1.80

-1.60

-1.40

-1.20

-1.00

-0.80

-0.60

-0.40

-0.20

0.00

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

May-17

Jun-17

Jul-17

Aug-17

Sep-17

LiquidsProduction(m

mb/d)

LiquidsProductionComparedWithNovem

ber2016(m

mb/d)

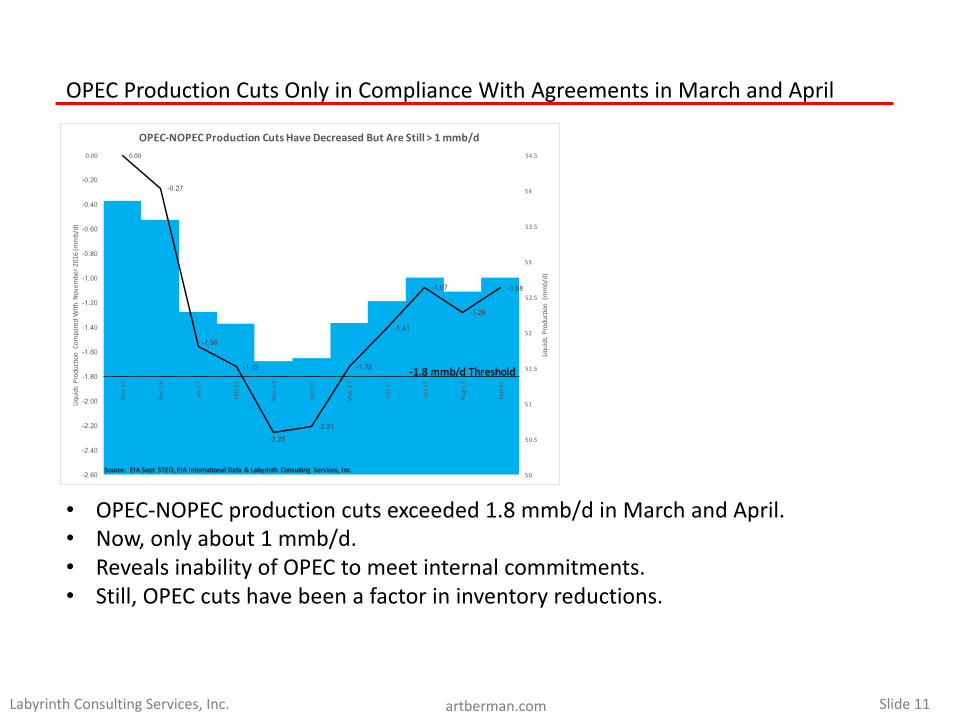

OPEC-NOPECProductionCutsHaveDecreasedButAreStill>1mmb/d

Source:EIASeptSTEO,EIAInternationalData&Labyrinth Consulting Services,Inc.

-1.8mmb/dThreshold

OPECProductionCutsOnlyinComplianceWithAgreementsinMarchandApril

• OPEC-NOPECproductioncutsexceeded1.8mmb/dinMarchandApril.• Now,onlyabout1mmb/d.• RevealsinabilityofOPECtomeetinternalcommitments.• Still,OPECcutshavebeenafactorininventoryreductions.

Slide12LabyrinthConsultingServices,Inc. artberman.com

0.50

0.40

0.40 0.50

0.30

1.30

0.80

0.80 0.85

1.59 1.

722.00

1.20

2.08

1.26

0.46

1.45

0.04 0.440.61

0.50

0.09

-0.90 -1.10 -1.80

-0.90 -1.60

-2.00 -0.70

-0.30 -0.60 -0.70 -0.70

-1.10 -2.10 -2.10

-0.60 -0.70

-1.60 -0.60

-0.50 -1.00

-0.24 -0.11

-0.54 -1.02

-0.02

-0.48 -0.22 -0.25

$0

$20

$40

$60

$80

$100

$120

$140

$160

-2.5

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

1Q06

2Q06

3Q06

4Q06

1Q07

2Q07

3Q07

4Q07

1Q08

2Q

083Q

08

4Q08

1Q

09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

4Q16

Q11

7Q21

7Q31

7Q41

7Q11

8Q21

8Q31

8Q41

8

BrentPrice

(Decem

ber2016DollarsPerBarrel)

MarketBalance(S

upplyMinusDem

andmmb;d)

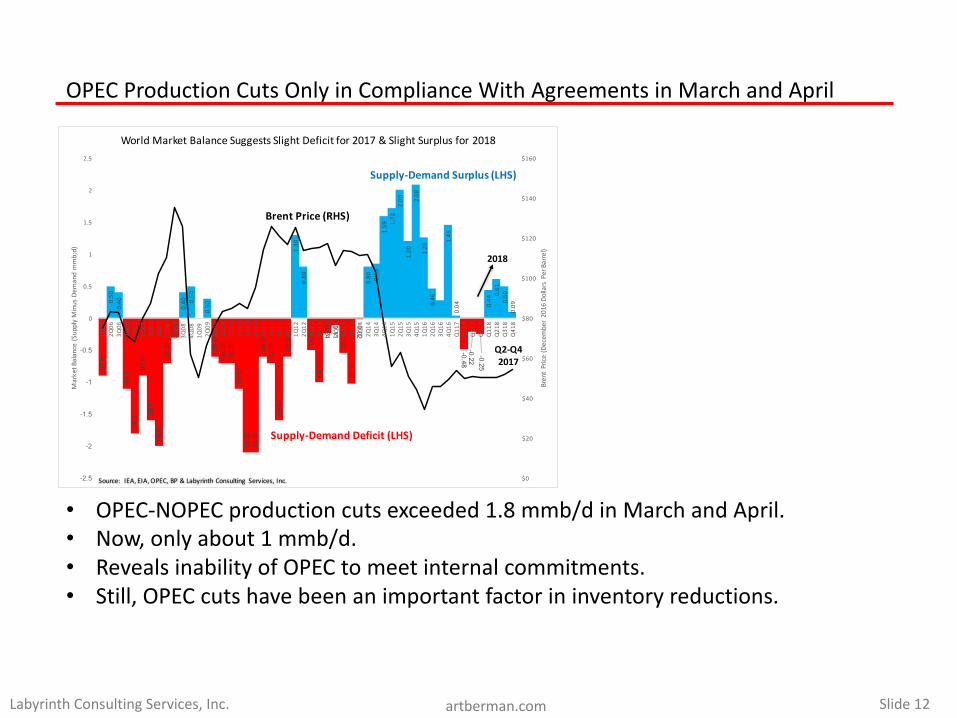

WorldMarketBalanceSuggestsSlightDeficitfor2017&SlightSurplusfor2018

BrentPrice(RHS)

Supply-Demand Surplus(LHS)

Supply-DemandDeficit(LHS)

Source:IEA,EIA,OPEC,BP&LabyrinthConsulting Services,Inc.

Q2-Q42017

2018

OPECProductionCutsOnlyinComplianceWithAgreementsinMarchandApril

• OPEC-NOPECproductioncutsexceeded1.8mmb/dinMarchandApril.• Now,onlyabout1mmb/d.• RevealsinabilityofOPECtomeetinternalcommitments.• Still,OPECcutshavebeenanimportantfactorininventoryreductions.

Slide13LabyrinthConsultingServices,Inc. artberman.com

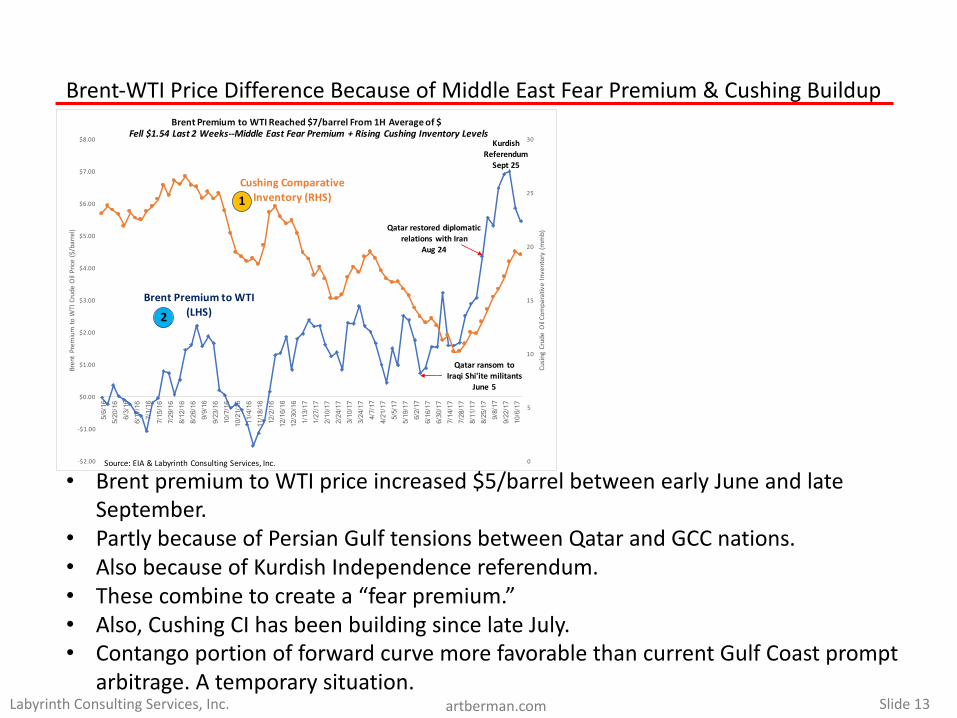

Brent-WTIPriceDifferenceBecauseofMiddleEastFearPremium&CushingBuildup

• BrentpremiumtoWTIpriceincreased$5/barrelbetweenearlyJuneandlateSeptember.

• PartlybecauseofPersianGulftensionsbetweenQatarandGCCnations.• AlsobecauseofKurdishIndependencereferendum.• Thesecombinetocreatea“fearpremium.”• Also,CushingCIhasbeenbuildingsincelateJuly.• Contango portionofforwardcurvemorefavorablethancurrentGulfCoastprompt

arbitrage.Atemporarysituation.

0

5

10

15

20

25

30

-$2.00

-$1.00

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

5/6/16

5/2

0/16

6/3/16

6/1

7/16

7/1/16

7/1

5/16

7/29/1

6 8/1

2/16

8/26/1

6 9/9

/16

9/23/1

6 10

/7/16

10

/21/16

11

/4/16

11

/18/16

12

/2/16

12

/16/16

12

/30/16

1/1

3/17

1/27/1

7 2/1

0/17

2/24/1

7 3/1

0/17

3/24/1

7 4/7

/17

4/21/1

7 5/5

/17

5/19/1

7 6/2

/17

6/16/1

7 6/3

0/17

7/14/1

7 7/2

8/17

8/11/1

7 8/2

5/17

9/8/17

9/2

2/17

10/6/

17

CusingCrudeO

ilComparativeInventory(m

mb)

BrentPrem

iumtoWTICrudeOilPrice($/barrel)

BrentPremiumtoWTIReached$7/barrelFrom1HAverageof$

Qatar restoreddiplomatic

relationswithIran

Aug24

Qatar ransomto

IraqiShi'itemilitants

June5

Kurdish

Referendum

Sept25

Source:EIA&LabyrinthConsultingServices,Inc.

BrentPremiumtoWTI

(LHS)

Fell$1.54Last2Weeks--MiddleEastFearPremium+Rising CushingInventoryLevels

Cushing Comparative

Inventory(RHS)1

2