Embed Size (px)

Citation preview

NACUSO NEWS

RANCHO CUCAMONGA, Calif.¬–Board Members of the NationalAssociation of Credit UnionService Organizations(NACUSO) and representativesfrom its 14 Platinum Partnersmet here on March 28 to hearcommittee and advisory boardprogress reports, discuss upcom-ing conferences andconfer on strategyimplementation plans. NACUSOChairwoman Ava Milosevichwelcomed everyone and set thetone for the gathering when shesaid, “Thanks for coming, and Ihope we put our heads togetheron ways to further improveNACUSO’s approach to creatingthe means for credit union suc-cess through CUSOcollaboration.”

Milosevich, who has 38 years ofexperience in the CU

industry added, “I began myassociation with CUSOs in 1984(she is the CEO of The SELCOGroup, Frontier Investment Co.and SELCO Mortgage Company)and I’ve never been involvedwith a greater organization thanNACUSO. The work we’re doingnow is so important to thefuture of credit unions.I know each of you feel thesame way or you wouldn’t behere. We have dedicated our-selves to fulfilling our primarystrategic objective, which is tobe the catalyst for innovationand the reinvention of thecredit union industry. That is anambitious goal, but as I lookacross this room and see thetalent gathered here, I feelconfident we will achieve it.”

(SSeeee TToonnyy ppgg.. 22)

NACUSO Platinum Partners Meet to DiscussStrategy, Industry Trends

Credit Union Direct Lending (CUDL) Hosts MeetingNA

CU

SO

Seated left to right is Bob Frizzle, Kevin Mummau, Don Clark, Guy Messick, Lisa Renner, Tony Boutelleand Ava Milosevich. Standing is Tom Davis, Judy Sandberg, Dave Serlo, Craig Lester, Kent Moon,Mike Hales, Jon Bartek, Dave Dickens, Pete Snyder and Jerry Neemann.

1

InnovationThroughCollaboration

Nati

onal

Ass

oci

ati

on o

f C

redit

Unio

n S

erv

ice O

rganiz

ati

ons

Platinum Partner Meeting1-3

A Sense of Urgency4-6

Election Update & President/CEO Search

7

New Advisory Boards7-8

The Ways and Means9-11

Flare Project Update11-12

Expanded Lending Opps.12-13

Collaboration Updates13-14

2006 NACUSO Newsletter© - May 2006

Newsletter copy and photos by:Carol Anne Burger.

Design: Beyond Marketing, LLC

2

Tony Boutelle in what he callsthe Route 66 Room of CUDLheadquarters. Auto-themedphotos and collectibles surerev-up the décor.

(continued from from page 1)

Tony Boutelle, president of CUDirect Corporation (which ownsCUDL and hosted the meeting),offered the full hospitality ofCUDL headquarters (which sharesspace with the California CreditUnion League) and later gaveattendees a personally guidedtour of the facility.

NACUSO Interim COO JudySandberg led the meeting off bynoting, “I have to do so withoutmy tandem partner, Vic Pantea,”(NACUSO’s Interim CEO) becausehe had been taken to a local hos-pital following a board dinner theprevious evening. “Vic is fine; hewas just exhausted and dehydrat-ed from pushing too hard thesepast few weeks,” Sandberg said.Pantea had knee replacement sur-gery one month ago and resumeda tough work schedule too soon,she added.

Sandberg related that Pantea senthis best, appreciated everyone’sconcern and regretted not being

there, but wanted them to carryon the important work beforethem. “We want to know how wecan support our PlatinumPartners, how we can better servemembers and champion the causeof cooperation and collaborationamong credit unions and CUSOs,”said Sandberg.

Meeting Participants

Craig Lester, Central StatesMortgage

Mike Hales, CounterIntelligenceAssociates/NACUSO

Tony Boutelle, CU DirectCorporation/NACUSO

Lisa Renner, CU HoldingCompany, LLC/NACUSO

Bob Frizzle, CU*Answers

Sue Racine & Gary Young,CUNA Mutual Group (via tele-conference)

Kevin Mummau, CUSOFinancial Services, L.P.

Tom Davis, Davis &Company/NACUSO

Judy Sandberg, GatewayServices Group/NACUSO

Kent Moon, MemberBusiness Lending, LLC

Guy Messick, Messick &Weber PC/NACUSO

Don Clark, Mountain AmericaFinancial Services

Dave Serlo, PSCU FinancialServices/NACUSO

Pete Snyder, SnyderConsulting Solutions/NACUSO

Ava Milosevich, The SELCOGroup/NACUSO

Dave Dickens, U.S.Central/NACUSO

Jon Bartek, U.S. Central

Jerry Neemann, CUDL

Shawna Luna, NACUSO

Carol Anne Burger, CarolWrites, Inc./NACUSO

Judy Sandberg is Vice President of Strategic Directionfor Gateway Services Group, LLC and Interim ChiefOperating Officer of NACUSO.

2006 NACUSO Newsletter© - May 2006

(SSeeee NNAACCUUSSOO ppgg.. 33)

I’ve never been

involved with

a greater

organization

than NACUSO.

The work we’re

doing now is so

important to the

future of credit

unions.

– Ava

Milosevich,

NACUSO

Chairwoman.

SEPT OCT NOVCalendarof Events

For the latestinformation,always checknacuso.org.Here is a listof NACUSOevents for thenext fewmonths.

Sept 15th - 18thCEO Collaborative

Conference

Sept 15thBOD Meeting

OCT 15th -16thBOD Meeting

NOV 1st - 3rdBusiness Services

Collaborative

Nov 1stBOD Meeting

3

“NACUSO reinvented itself last year,and we’ve made great strides in com-municating that vision,” Sandberg said.“But we set the bar very high, and aslong as there are credit unions outthere that do not understand the com-petitive benefits and the power thatcomes through the CU/CUSO model, itmeans we still have work to do.”

Sandberg reported that NACUSO’sfinancial position is strong. “We areprofitable through the first months ofthe year; we are financially stable, havehad our first outside CPA audit, andthrough Bob (Frizzle’s) stewardship,have instituted accounting and report-ing standards and formulated growthplans to take us well into the future”

Sandberg said, “NACUSO’s incomestream comes from member dues, con-ference revenue and support fromPlatinum Partners. We’ve haddouble-digit growth in membership andrenewals because our value propositionhas a strong appeal.We are the only organization

dedicated to pursuing collaboration asa business strategy. This shared visionof bringing existing credit unions andCUSOs together, forming new CUSOsfor collective benefit and opening anew avenue of participation for thisindustry has taken hold of the imagina-tion of the CU world at large. We’rehere now to build on that progress.”

Sandberg noted that NACUSO’s premierconference is fast approaching (the2006 Annual Conference at the WynnLas Vegas on May 15-18) and tworegional meeting dates have also beenset. NACUSO’s CEO Collaborative willtake place at the CUNA Mutual Groupheadquarters in Madison, Wisconsin onSeptember 14-16, and the BusinessServices Conference will take place inChicago on November 1-3.

- end

Just Announced.Business Services CollaborativeNovember 1st - 3rdRenaissance Chicago Downtown Hotel

2006 NACUSO Newsletter© - May 2006

NACUSO Vice Chairman Tom Davisprovided the impetus for a passionatediscussion of what comes next –notjust for NACUSO– but for the future ofcredit unions and the businesses thatserve and support them. Davis deliv-ered the “that was then, this is now,this is what will be” data of the creditunion lifecycle that should spur actionon the collaborative model. Phase I isthe history, from creation to around1945 (the Philosophical Foundation);Phase II, from 1945 to around 1970(the Years of National Expansion);Phase III, from around 1970 to 1985(the years of Institution Building),with multiple SEGs and expandedproduct offerings, and Phase IV, from1985 to the present (the MaturingIndustry and the years of technologi-cal advancement and competition).

Throughout the history of the creditunion movement, most credit unionshave shown strong growth in mem-bership and operational success, butthe total number of CUs has been insteep decline. From a high of morethan 30,000 nationwide to 8,900today, the rate of loss is one CU perday,” Davis said. Return on assets(ROA) has been below 1% for the lasteight quarters. Member growth isstagnant at 1.5%, and the total CUshare of the national financial servic-es sector can’t break 6%. There werefewer than 100 new CU charters inthe last 10 years. Davis said these aresorry figures to be sure, especiallywhen compared to community banks,which are posting record profits. Sowhat’s the problem?

Davis said it was a lack of criticalthinking, as well as a strict relianceon peer analysis and inadequate CUorganizational structure. “Strategieshave changed, but the CU organiza-tional structure is the same now as itwas 50 years ago,” he said. Davis hascompiled comprehensive focus groupand survey data over several years,and learned that members want value,convenience and service. ”But at thecore of what people want is to feelgood,” he said.

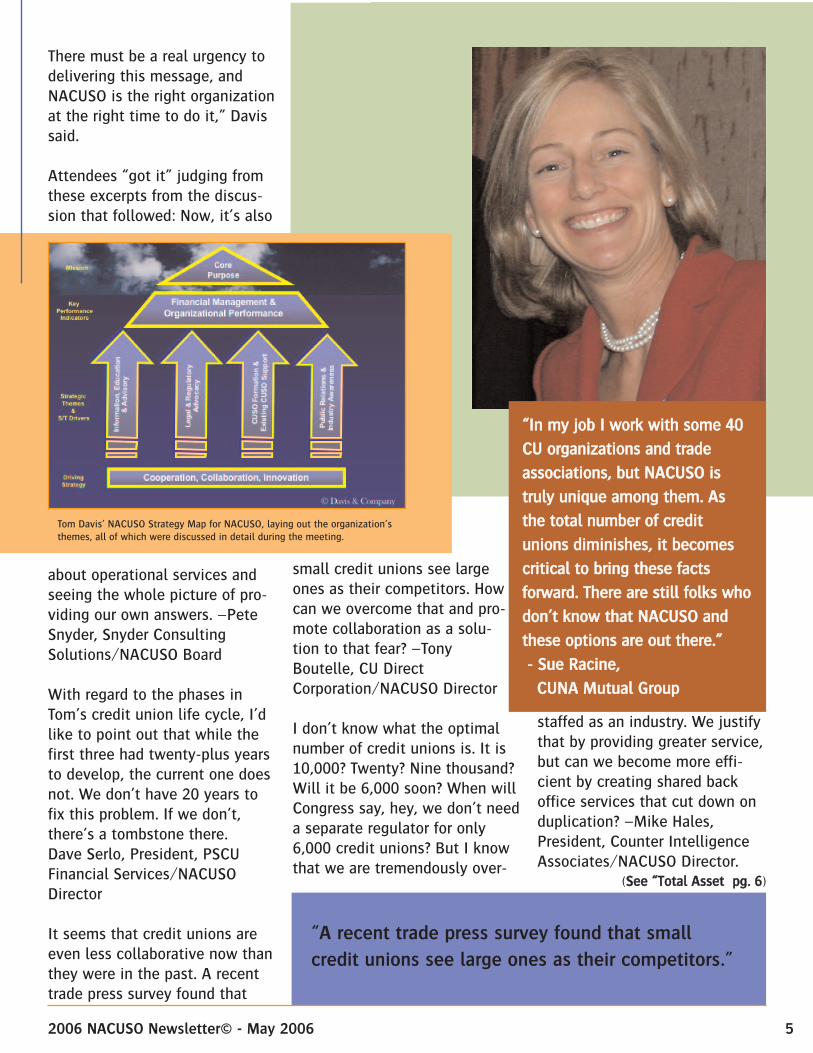

The answer lies in finding new growthmodels, revamped capital moderniza-tion and an increased emphasis oncritical thinking. “When critical think-ing deteriorates, so does innovation,”he stressed. A new level of activism iscalled for, with boards functioning asassets of the credit union, and man-agement setting the example forsuperior execution and implementa-tion of new business plans. “We needcollaboration and cooperation now.The old NACUSO purpose was as theplace to go relative to the distributionof financial services and products, andthat was successful.

Tom Davis spoke of the importance of criticalthinking to making good business decisions, andhow it is diminishing in today’s speed culture.

A Senseof Urgency.

42006 NACUSO Newsletter© - May 2006

“The

ans

wer

lie

s in

fin

ding

new

gro

wth

mod

els,

reva

mpe

d ca

pita

l m

oder

niza

tion

and

an

incr

ease

dem

phas

is o

n cr

itic

al t

hink

ing.

“

(SSeeee ““TThheerree”” ppgg.. 55)

There must be a real urgency todelivering this message, andNACUSO is the right organizationat the right time to do it,” Davissaid.

Attendees “got it” judging fromthese excerpts from the discus-sion that followed: Now, it’s also

about operational services andseeing the whole picture of pro-viding our own answers. –PeteSnyder, Snyder ConsultingSolutions/NACUSO Board

With regard to the phases inTom’s credit union life cycle, I’dlike to point out that while thefirst three had twenty-plus yearsto develop, the current one doesnot. We don’t have 20 years tofix this problem. If we don’t,there’s a tombstone there. Dave Serlo, President, PSCUFinancial Services/NACUSODirector

It seems that credit unions areeven less collaborative now thanthey were in the past. A recenttrade press survey found that

small credit unions see largeones as their competitors. Howcan we overcome that and pro-mote collaboration as a solu-tion to that fear? –TonyBoutelle, CU DirectCorporation/NACUSO Director

I don’t know what the optimalnumber of credit unions is. It is10,000? Twenty? Nine thousand?Will it be 6,000 soon? When willCongress say, hey, we don’t needa separate regulator for only6,000 credit unions? But I knowthat we are tremendously over-

staffed as an industry. We justifythat by providing greater service,but can we become more effi-cient by creating shared backoffice services that cut down onduplication? –Mike Hales,President, Counter IntelligenceAssociates/NACUSO Director.

52006 NACUSO Newsletter© - May 2006

““IInn mmyy jjoobb II wwoorrkk wwiitthh ssoommee 4400

CCUU oorrggaanniizzaattiioonnss aanndd ttrraaddee

aassssoocciiaattiioonnss,, bbuutt NNAACCUUSSOO iiss

ttrruullyy uunniiqquuee aammoonngg tthheemm.. AAss

tthhee ttoottaall nnuummbbeerr ooff ccrreeddiitt

uunniioonnss ddiimmiinniisshheess,, iitt bbeeccoommeess

ccrriittiiccaall ttoo bbrriinngg tthheessee ffaaccttss

ffoorrwwaarrdd.. TThheerree aarree ssttiillll ffoollkkss wwhhoo

ddoonn’’tt kknnooww tthhaatt NNAACCUUSSOO aanndd

tthheessee ooppttiioonnss aarree oouutt tthheerree..””

-- SSuuee RRaacciinnee,,

CCUUNNAA MMuuttuuaall GGrroouupp

“A recent trade press survey found that small

credit unions see large ones as their competitors.”

Tom Davis’ NACUSO Strategy Map for NACUSO, laying out the organization’sthemes, all of which were discussed in detail during the meeting.

(SSeeee ““TToottaall AAsssseett ppgg.. 66)

The total asset size of all lastyear’s merged credit unions wasnear $350 million. What about anational wholesale CUSO? A fed-eration? –Tom Davis, Davis andCompany/NACUSO ViceChairman.Credit union consolidation isn’tthe problem. There is no overallcredit union brand in this coun-try. There are 8,900 differentbrands. Our survival isn’t aboutassuring the survival of the $5million to $25 million creditunion, it’s about the survival ofthe credit union idea, whateverthe size. –Dave Dickens, InterimPresident/CEO of U.S.Central/NACUSO DirectorMountain America is a $1.7 bil-lion credit union, and we’ve haddouble-digit growth in the lastseveral years. Forty-six percentof our growth last year was inMBLs. And we have benefitedfrom collaboration; it’s beengood for us and it can be just asgood for medium sized CUs.–Dan Clark, President, MountainAmerica FinancialServices/NACUSO DirectorLook, 77% of all SBA lending isdone by only 15 banks in thiscountry. It’s economy of scalethat allows us to compete wellagainst banks, so it can be done.I see the problem as resistanceto change. Credit union peoplewill say they want to change, butthey keep doing things the way

they always have. It’ll take anevolution in thinking. Banksdon’t look at transactions; theywant to capture the whole wal-let. –Kent Moon, MemberBusiness Lending, LLCTaxes still worry people, butthey’re nothing compared to thecost of expenses of providingservices; if we can cut those,taxes wouldn’t be the biggestfear. –Pete Snyder.Can credit unions be convincedto outsource all the things theyare afraid of doing but want toand don’t, due to high costs, toCUSOs? –Dave Dickens, InterimPresident/CEO of U.S.Central/NACUSOThose CUSOs would have to beas good or better at deliveringwhatever those services are.–Tony Boutelle, President, CUDirect Corporation/NACUSOThere are some boards out therethat are just plain tired. Theylook around and say, “Look,those guys are merging. Maybewe’ll have to merge too.” –AvaMilosevich, President, SELCOCredit Union/NACUSOChairwoman.Those are the very people weneed to reach! I’d like to have ateam go in there are say, “Votethese guys out before they sellyou out!” It’s such a give up atti-tude. –Bob Frizzle, CU*AnswersClearly, we need some means todevelop measurable statistics of

the value of collaboration.Can we create collaborativecase studies from examplesthat show it works? LikeCUDL, CU*Answers andMountain America and oth-ers? –Judy Sandberg, VP ofStrategic Direction,

Gateway Services Group, LLC,NACUSO Interim COOWe could pick 20 CUs that haveCUSOs and 20 that don’t andcompare the key ratios. –PeteSnyder, Snyder ConsultingServices/NACUSO DirectorThe freewheeling talk benefitedeveryone it seemed, becausethey openly discussed the ele-phant in the room. But talk mustlead to action, and action tomeaningful, workable solutionsfor the greatest number of creditunions.It was a serious, yet upbeat tonethat led Lisa Renner,President/CEO of CU HoldingCo., LLC to say, “I’m new on thisboard, but I am passionate abouthow CUSOs are going to turn thecredit union world around.”Among the strong points of con-sensus were:• NACUSO still needs to promoteawareness of itself and the bene-fits that CUSOs and the PlatinumPartners bring to the CU industrythrough continued PR, press cov-erage and relevant case studies;

• NACUSO will continue itsFlare Project efforts andpromote the great networkingopportunities they create;• NACUSO must continue itslegislative and regulatoryefforts. - end

62006 NACUSO Newsletter© - May 2006

“Credit union consolidationisn’t the problem.”

72006 NACUSO Newsletter© - May 2006

Pete Snyder, Dave Serlo and Mike Hales, membersof the Nominating Committee, reported they hadreceived 11 applications for four open directorspots, eight of which were highly qualified. Theboard has 12 directors. There is one opening ineach category of director classification: CUSOsand Platinum Partners, CUSOs but not PlatinumPartners, Credit Unions and Independent.

Nominations are now closed and voting began onApril 17 and concludes on May 8. NACUSOGeneral Counsel Guy Messick will be Teller ofElections and will announce the results at theannual conference on May 17. - end

Dave Serlo told attendees that at the end ofSeptember the NACUSO Board had engaged theservices of Hilton & Associates in the search for anew president for NACUSO. “We feel this is one ofthe most important tasks we face; finding a newCEO for NACUSO,” Serlo said. “We have met withDave Hilton and given him our criteria for

consideration. Hilton placed ads and began takingapplications, and so far some 150 have beenevaluated. That number will be culled to a shortlist for the Committee’s consideration. “It’surgent that we fill this spot, but we’re looking forthe right candidate, a great candidate. If we haveto wait to find that person, we will. We have toget this right.” - end

In late January NACUSO announced the appoint-ment of four advisory boards to provide input andadvice to the NACUSO board of directors on awide-ranging number of services. The advisoryboards are (1) the Financial Services AdvisoryBoard (investments, insurance and trust services);(2) the Business Services Advisory Board (busi-ness lending, depository and ancillary services);(3) the Consumer Lending Services Advisory

Board (indirect lending, mortgage lending, stu-dent lending, and collections); and (4) theOperational Services Advisory Board (data pro-cessing, disaster recovery, shared branching andmanagement services).

ElectionUpdate

New AdvisoryBoards Added

President/CEOSearch

Dave Serlo updated attendees on the NACUSO CEO search.

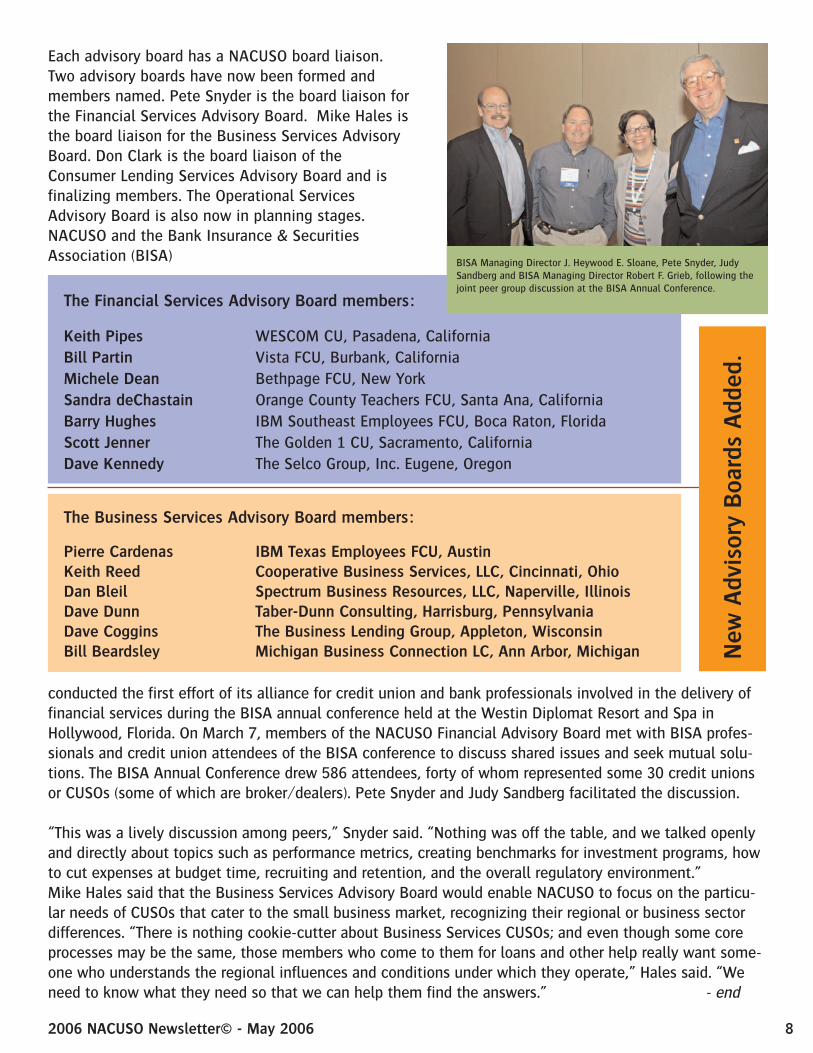

NACUSO Advisory Board Liaisons Pete Snyder (Financial Services), Mike Hales (Business Services) and Don Clark (Consumer LendingServices) provided reports on their respective board’s formation,membership and planned activities.

The Financial Services Advisory Board members:

Keith Pipes WESCOM CU, Pasadena, CaliforniaBill Partin Vista FCU, Burbank, CaliforniaMichele Dean Bethpage FCU, New YorkSandra deChastain Orange County Teachers FCU, Santa Ana, CaliforniaBarry Hughes IBM Southeast Employees FCU, Boca Raton, FloridaScott Jenner The Golden 1 CU, Sacramento, CaliforniaDave Kennedy The Selco Group, Inc. Eugene, Oregon

82006 NACUSO Newsletter© - May 2006

Each advisory board has a NACUSO board liaison.Two advisory boards have now been formed andmembers named. Pete Snyder is the board liaison forthe Financial Services Advisory Board. Mike Hales isthe board liaison for the Business Services AdvisoryBoard. Don Clark is the board liaison of theConsumer Lending Services Advisory Board and isfinalizing members. The Operational ServicesAdvisory Board is also now in planning stages.NACUSO and the Bank Insurance & SecuritiesAssociation (BISA)

The Business Services Advisory Board members:

Pierre Cardenas IBM Texas Employees FCU, AustinKeith Reed Cooperative Business Services, LLC, Cincinnati, OhioDan Bleil Spectrum Business Resources, LLC, Naperville, IllinoisDave Dunn Taber-Dunn Consulting, Harrisburg, PennsylvaniaDave Coggins The Business Lending Group, Appleton, WisconsinBill Beardsley Michigan Business Connection LC, Ann Arbor, Michigan

BISA Managing Director J. Heywood E. Sloane, Pete Snyder, JudySandberg and BISA Managing Director Robert F. Grieb, following thejoint peer group discussion at the BISA Annual Conference.

conducted the first effort of its alliance for credit union and bank professionals involved in the delivery offinancial services during the BISA annual conference held at the Westin Diplomat Resort and Spa inHollywood, Florida. On March 7, members of the NACUSO Financial Advisory Board met with BISA profes-sionals and credit union attendees of the BISA conference to discuss shared issues and seek mutual solu-tions. The BISA Annual Conference drew 586 attendees, forty of whom represented some 30 credit unionsor CUSOs (some of which are broker/dealers). Pete Snyder and Judy Sandberg facilitated the discussion.

“This was a lively discussion among peers,” Snyder said. “Nothing was off the table, and we talked openlyand directly about topics such as performance metrics, creating benchmarks for investment programs, howto cut expenses at budget time, recruiting and retention, and the overall regulatory environment.”Mike Hales said that the Business Services Advisory Board would enable NACUSO to focus on the particu-lar needs of CUSOs that cater to the small business market, recognizing their regional or business sectordifferences. “There is nothing cookie-cutter about Business Services CUSOs; and even though some coreprocesses may be the same, those members who come to them for loans and other help really want some-one who understands the regional influences and conditions under which they operate,” Hales said. “Weneed to know what they need so that we can help them find the answers.” - end

New

Adv

isor

y B

oard

s A

dded

.

2006 NACUSO Newsletter© - May 2006

The Waysand Means

NACUSO General Counsel Guy Messick reportedto attendees his thoughts after a recent confer-ence call with staffers of the Ways and MeansCommittee of the U.S. House of Representativesand subsequent discussions with NCUA officialson CUSO structures and potential tax considera-tions.

The Ways and Means Committee is conductinghearings on non-profit organizations and whetherthe organization non-profit tax treatment shouldcontinue for the various non-profits. Creditunions are included on their examination list.Through the examination of credit unions, theCommittee has become aware of CUSOs. TheCommittee was particularly interested in the abilityof limited liability company CUSOs to serve non-members with services not permitted to be providedby credit unions and to do so on a non-profit taxbasis.

Messick reported that he told the Committeestaffers that CUSOs are growing in the operationalservices area and that this form of CUSO is gearedto cost savings and not income generation. Thestaffers also inquired about the financial servicesCUSOs and income generation. “I spent some timetalking about the need for non-interest income tosustain financial institutions and the need for creditunions to meet the expectation of their members toprovide a wide array of financial services,” Messicksaid.

“They asked me to confirm that it was my under-standing that federal credit unions do not payincome tax or Unrelated Business Income Tax(UBIT) in Limited Liability Companies (LLC) CUSOs,”he said. “I confirmed that this was my understand-ing. As to state chartered credit unions, they toldme that NASCUS told them that 20% of state char-tered credit unions pay UBIT. I told them that I wasnot aware of this statistic. I told them it was my

understanding that the credit uniontrade associations were in talks withthe IRS regarding clearer UBIT rules.”

“When asked about a CUSO servingnon-members and the tax advan-tages a CUSO has, I told them thatthenon-member business by a vastmajority of CUSOs is negligible,”Messick said. “ One, because there isso much untapped potential withinthe credit union membership; two,there is no competitive advantagethat CUSOs have over other providersto serve non-members, and three,credit union people are not experi-enced in the for profit CUSObusinesses and the marketingmethods to tap a market beyondtheir membership.”

Altogether, Messick said the tonewas very cordial and they offered tofollow up with them if they hadadditional questions. “We weren’tsurprised as to their concerns.”

Guy Messick laid out various tax related options available for CUSOs.

9(SSeeee ““NNCCUUAA”” ppgg.. 1100))

102006 NACUSO Newsletter© - May 2006

NCUA May Consider Changes

Owing to political pressure brought about by banks and Congress’ need to raise funds to narrow the deficit,it’s not a big leap to think that the NCUA may consider changes to the CUSO regulation. “As always,NACUSO’s first concern is for credit unions and we fully support the NCUA in its efforts to maintain the taxexemption for credit unions,” Messick said. “While no business desires to pay taxes, the tax issue neverdrove the value of CUSOs to credit unions. CUSOs managed taxation when they were primarily corporationsand they could do it again. We in CUSOs don’t want to be a poster child that promotes credit union taxa-tion.”

Messick reported that it is likely that CUSOs will continue to be able to be limitedliability companies but the tax election of these CUSOs may have to change.Actions that are available to NCUA to consider if action on CUSO taxation isrequired include:

• Only permit CUSOs to be limited liability companies with a disregardedentity tax status if they are performing a service that a credit unioncan perform

• Require that a limited liability CUSO elect to be taxed as corporationsand not disregarded entities when the CUSO provides services thatcannot be performed by credit unions.

These possible actions merit further discussion for the advantages and disadvan-tages. The use of the limited liability company entity for CUSOs has value wellbeyond the tax advantages. In CUSOs that are owned by multiple credit unions,there are often different classes of rights, as some credit unions will be the majorplayers and some will have a lesser role. In CUSOs that are co-owned by entitiesother than credit unions, the role of the credit union and non-credit union ownersare often distinct. The ownership, profit sharing and management powers can becustomized in LLCs so there is great flexibility in the arrangement to meet theneeds of the parties.

In the disregarded entity tax status, the CUSO does not pay taxes but the tax obli-gation is passed to the credit union owners that are exempt from paying income tax. We note that in thecase of state chartered credit unions; unrelated business income tax may be paid. NACUSO favors the useof a limited liability company with a disregarded entity tax election for services being performed for mem-bers or other credit unions that the credit union could itself perform. If a CUSO is providing operationalservices to credit unions and aggregating the effort for economies of scale, then taxing the CUSO for suchoperational support functions does not seem appropriate. Likewise, if a CUSO were providing mortgages orbusiness loans to members, the same analysis would occur. If the service the CUSO provides cannot be per-formed by a credit union, we understand and support the inability of the CUSO to be an LLC with a disre-garded tax election.

Messick pointed out the more difficult question will be whether the LLC with a disregarded tax electioncould serve non-members. “If this issue cannot be avoided, then we would have to discuss whether thecredit union would pay UBIT on that business or whether a corporate tax election would have to be madefor the CUSO. We hear from CUSOs that even if they are not seeking non-member business, there aretimes when a non-member will approach a CUSO for a service, and the CUSO would like to be able to servethe non-member.

“... it is likely

that CUSOs

will continue

to be able to

be limited

liability

companies

but the tax

election of

these CUSOs

may have to

change.”

(SSeeee ““TThhaatt iiss”” ppgg.. 1111))

112006 NACUSO Newsletter© - May 2006

That is why the UBIT payment for non-member businesswould be a great option if needed.” Whether or not feder-al credit unions could voluntarily pay UBIT would have tobe considered.

Limited liability companies can file an election with theIRS electing to pay taxes as a corporation. This quick andeasy resolution saves the LLC as a valuable entity andremoves the tax issue from the political scene. NACUSOwould urge the NCUA to require this corporate tax elec-tion only if the CUSO is providing a service that cannotbe provided by a credit union. The tax election may bechanged in the ensuing tax year by a simple filing. SomeCUSOs that are providing multiple services may have toreorganize and split their services into more than oneCUSO. Consequently, NACUSO would ask that the NCUAconsider a grandfather provision or a majority of servicestest. It is not known how many CUSOs this would affect.

Finally, the inquiry by the Ways and Means Committeehas brought to light the lack of information about CUSOs.It is likely that NCUA will consider requiring CUSOs toprovide more information on an annual basis. NACUSO isworking with NCUA on the types of information thatwould be gathered from CUSOs. - end

Sending up a flare is a universally recognized method ofgetting attention, so NACUSO’s Flare initiative wasdesigned to do several things, explained Judy Sandberg.“We wanted to showcase our ‘action orientation,’ set anexample of how to get a good idea moving and finally,show that we were willing to put our own time and energyinto a good project,” Sandberg said.

The Flare Project identified two key challenges: helpingto stem the rapid decline in credit unions and ways tosuccessfully penetrate expanded field of membership inSEGs or a community charter.

In June 2005 NACUSO brought a group of representativesfrom Michigan CUs together to discuss ways that collabo-ration might help them better compete, save money andgrow.

Meetings were initiated,and the idea of forminga CUSO to do group pur-chasing was discussed.The CUSO would providebulk purchasing powerand allow access to ven-dors and products that individual creditunions could not get separately.

In December 2006 the group decided toform a CUSO and developed a businessplan. In March, six credit unions gotapproval for the initial capital investment.That new CUSO’s name is CU PartnerSolutions, LLC. (See sidebar story.)

“We’re delighted to see the formation ofthis CUSO because it shows that whengiven the vision and opportunity, creditunions recognize the power inherent incollaborating with one another throughCUSOs,” Sandberg said. “They savemoney. To small and mid-size CUs, thatmeans an awful lot. It can be the differ-ence between merger and survival if,rather than spending more for neededproducts and services each year, theyinstead save more each year. That’smoney they can apply to expanded servic-es to members or to better loan rates orsavings rates,” she said.

Sandberg noted that NACUSO’s costs (inhard dollars) were limited to travel andhotel expenses for her and Guy Messick toattend planning sessions, and amountedto nearly $2,000. The intellectual capitalthey provided on a pro-bono basis wasworth considerably more than that. Butshe said it was worth it to put promiseinto action. “The whole point of the FlareProject is to show how it can be done, tohelp lead the way. We hope that thiscatches fire because this kind of collec-tive can make a real difference.”

Flare ProjectUpdate

Send your CUSO Stories to Shawna Lunaat NACUSO • [email protected]

122006 NACUSO Newsletter© - May 2006

A second Flare Project is now in the planning stages. It involves NACUSO Platinum Partner PSCU helpingNevada Federal Credit Union to better penetrate a newly granted membership expansion or market segment.

“People are always asking, ‘What’s in it for you?’” Sandberg said. “I understand that it’s human nature, andin business, as in life, it pays to be skeptical. Fine. What we get out of it is twofold, we spread the goodword and help the continuation of credit unions, and that’s our market. If our market disappears, what hap-pens to us? So, we really are all in this together. And another bonus for us is that two of those credit unionsin Michigan joined NACUSO! - end

Tom Miller, presidentof Affinity GroupCredit Union, Pontiac,Michigan, and afounding partner of CUPartner Solutions, saidthat “credit unionsneed to reach out and

look for opportunities to generate income and reduce expens-es.” He said those were the driving forces behind the group ofcredit unions that came together to form the CUSO. The otherCUSO partners are Crestwood Community CU, Garden City,Clawson Community CU, Clawson, ROME CU, Royal Oak,Southeast Oakland Community CU,Oak Park and Kensington Valley CU, Highland.

“We wanted to collaborate so that our aggregate size wouldhave a positive impact on expenses, but buying power is onlyone part of the equation,” Miller said. “Yes, we asked how wemight work together to save money. But the other part of theequation is to have growth opportunities that generatesincome.”

Working with NACUSO General Counsel Guy Messick andInterim COO Judy Sandberg over several months resulted inthe six CUs forming a CUSO that will let all partners meetboth objectives.

“NACUSO helped us put this together,” Miller said. “The assis-tance and leadership we got from Judy and Guy was invalu-able. Their help on the business plan and the operating agree-ment was just great. I don’t think we could have got it goingwithout them.”

The creation of the CUSO partnershipalso empowers what Miller called the“unwritten rule” that credit union peo-ple share all information openly. “Yes,it does seem that the C for cooperationhas too often been replaced by compe-tition. This makes for reluctance to giveup strategies that prove successful.”

“In the CUSO, it is an open exchangeabout how we achieve saving moneyand finding new loan opportunities,”Miller said. ”Around that table, we arepartners; it’s not the same feeling youget at a chapter meeting.”

The CUSO is seeking various bids onproviding health insurance now thatthey have a larger group, which lowerscosts, and is also looking into employ-ee retirement plans.

Another area in planning stages iscalled “Member Direct,” which isdescribed by Miller as a co-brandedWeb site for the CUSO business part-ners in conjunction with area business-es. “We can work with local businesspartners to approve needed loansovernight and participate out thoseloans among our CUSO partners,” Millersaid.

New CUSO Will ExpandLending Opportunities,Buying Power

Tom Miller

(SSeeee ““CCuu PPaarrttnneerrss”” ppgg.. 1133))

132006 NACUSO Newsletter© - May 2006

CU Partner Solutions isn’t Miller’s first foray into CUSOs. He is a founder and current vice chairman ofMortgage Center, LLC in Southfield (http://www.mortgagecuso.com). “We just rolled out a 25% rebateon real estate commissions for participating in the Home Benefits Plus program through the MortgageCenter. It’ll be a drop-dead success, and we have our own title company, too.”

Miller also pioneered one of the first shared ATM networks for credit unions. His company, ACTSystems, Inc., provided both online and stand-in authorizations for credit unions and community banksin Michigan.

“Now, I’m a relatively little guy. I mean, we’re a $37 million credit union in Pontiac Michigan with 13.7%capital and .62 return on capital (ROA),” Miller said. “But being in the CUSO has done wonders for us asan equal partner. The revenue generated each month has helped the spread when other earnings havebeen lower. It clearly shows how a smaller credit union can play with the big boys and succeed.”

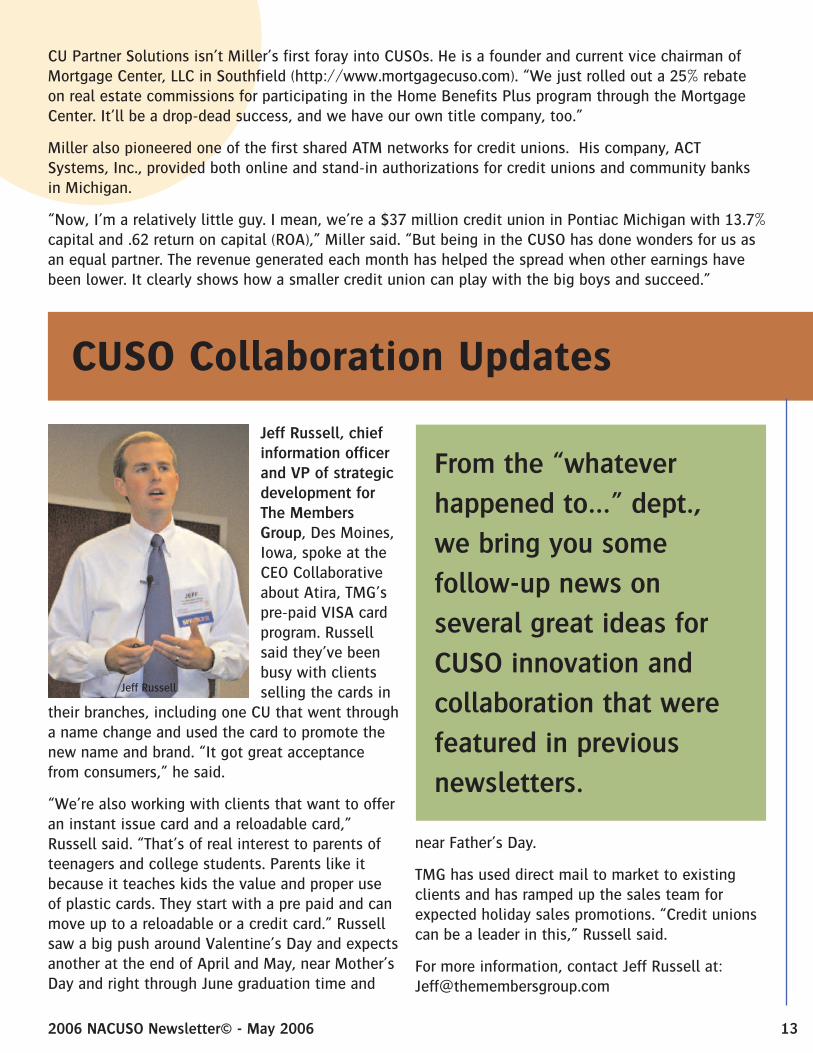

Jeff Russell, chiefinformation officerand VP of strategicdevelopment forThe MembersGroup, Des Moines,Iowa, spoke at theCEO Collaborativeabout Atira, TMG’spre-paid VISA cardprogram. Russellsaid they’ve beenbusy with clientsselling the cards in

their branches, including one CU that went througha name change and used the card to promote thenew name and brand. “It got great acceptancefrom consumers,” he said.

“We’re also working with clients that want to offeran instant issue card and a reloadable card,”Russell said. “That’s of real interest to parents ofteenagers and college students. Parents like itbecause it teaches kids the value and proper useof plastic cards. They start with a pre paid and canmove up to a reloadable or a credit card.” Russellsaw a big push around Valentine’s Day and expectsanother at the end of April and May, near Mother’sDay and right through June graduation time and

near Father’s Day.

TMG has used direct mail to market to existingclients and has ramped up the sales team forexpected holiday sales promotions. “Credit unionscan be a leader in this,” Russell said.

For more information, contact Jeff Russell at:[email protected]

CUSO Collaboration Updates

From the “whatever

happened to…” dept.,

we bring you some

follow-up news on

several great ideas for

CUSO innovation and

collaboration that were

featured in previous

newsletters.

Jeff Russell

142006 NACUSO Newsletter© - May 2006

Allegacy Services, LLC

Ray Crouse, managing director of Allegacy Services, LLC, (a CUSO ofAllegacy FCU, Winston-Salem, N.C.) who spoke to attendees at theCEO Collaborative in Kansas City and the Business ServicesCollaborative in Chicago about franchising a payroll processing serv-ice for credit unions, CU organizations and related member business-es on a nationwide basis, provided a progress report.

“It’s going very well,” Crouse said. “We purchased and installed thesoftware, loaded all Allegacy employees into the system and starteddoing payroll in late February. In April, we start doing the payroll forthe North Carolina League. We’ve also been cultivating SEGs andbusiness services clients.

“We’re very confident with what we have in place at Allegacy,”Crouse said. “Now, the work involves replication of that approach andmaking sure all tasks are coordinated.” Crouse added that he’dreceived inquiries from other interested CU investors, and he indicat-ed that he’s open to that. But as far as CU-owned payroll processingcompanies goes, “We’re the only one in CU-land.” For more informa-tion, contact Ray Crouse at: [email protected]

Ongoing Operations LLC

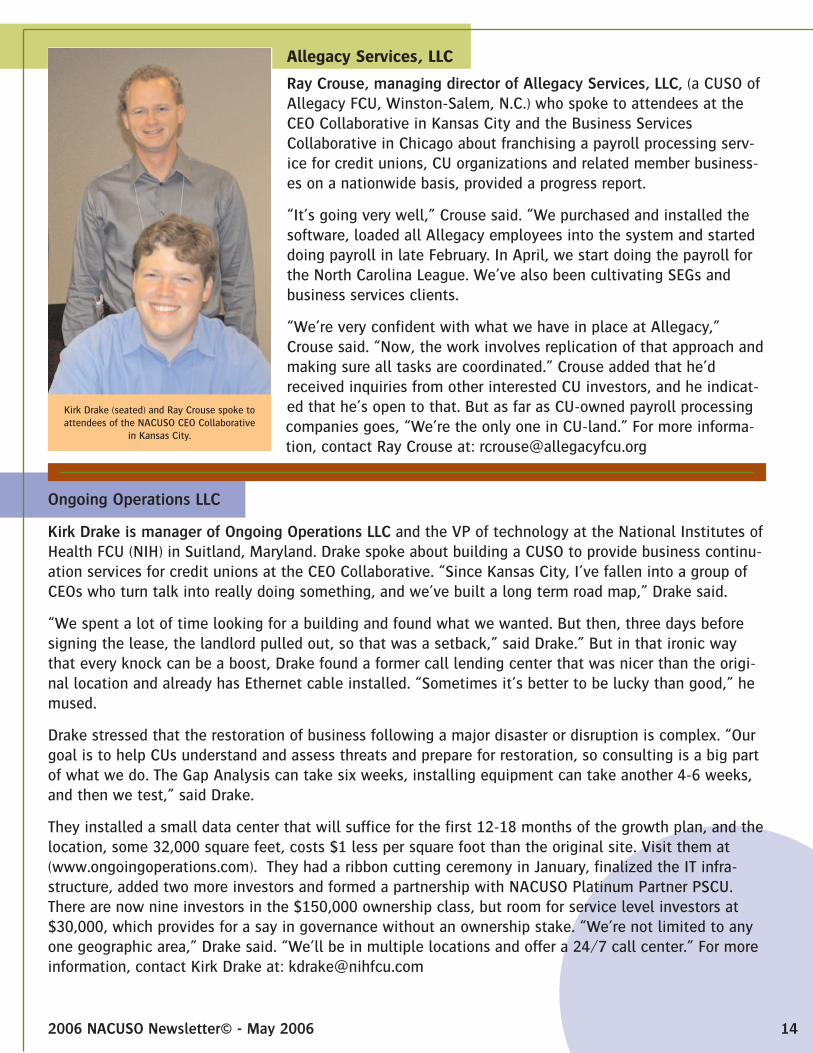

Kirk Drake is manager of Ongoing Operations LLC and the VP of technology at the National Institutes ofHealth FCU (NIH) in Suitland, Maryland. Drake spoke about building a CUSO to provide business continu-ation services for credit unions at the CEO Collaborative. “Since Kansas City, I’ve fallen into a group ofCEOs who turn talk into really doing something, and we’ve built a long term road map,” Drake said.

“We spent a lot of time looking for a building and found what we wanted. But then, three days beforesigning the lease, the landlord pulled out, so that was a setback,” said Drake.” But in that ironic waythat every knock can be a boost, Drake found a former call lending center that was nicer than the origi-nal location and already has Ethernet cable installed. “Sometimes it’s better to be lucky than good,” hemused.

Drake stressed that the restoration of business following a major disaster or disruption is complex. “Ourgoal is to help CUs understand and assess threats and prepare for restoration, so consulting is a big partof what we do. The Gap Analysis can take six weeks, installing equipment can take another 4-6 weeks,and then we test,” said Drake.

They installed a small data center that will suffice for the first 12-18 months of the growth plan, and thelocation, some 32,000 square feet, costs $1 less per square foot than the original site. Visit them at(www.ongoingoperations.com). They had a ribbon cutting ceremony in January, finalized the IT infra-structure, added two more investors and formed a partnership with NACUSO Platinum Partner PSCU.There are now nine investors in the $150,000 ownership class, but room for service level investors at$30,000, which provides for a say in governance without an ownership stake. “We’re not limited to anyone geographic area,” Drake said. “We’ll be in multiple locations and offer a 24/7 call center.” For moreinformation, contact Kirk Drake at: [email protected]

Kirk Drake (seated) and Ray Crouse spoke toattendees of the NACUSO CEO Collaborative

in Kansas City.