Embed Size (px)

Citation preview

Imperial College London

Department of Computing

Numerical Methods for Pricing Exotic Options

by

Hardik Dave - 00517958

Supervised by Dr. Daniel Kuhn

Second Marker: Professor Berc Rustem

Submitted in partial fulfilment of the requirements for the MSc Degree in AdvancedComputing of Imperial College London

September 2008

Abstract

Since the introduction of Fischer Black and Myron Scholes’ famous option pricing model [3] in1973, several authors have proposed alternative models and methodologies for pricing optionsaccurately. In this project, we evaluate and extend two such recently proposed methodologies.

In the semi-parametric approach for pricing options, originally proposed by Lo in [22] andsubsequently extended by Bertsimas and Popescu in [1] and [2] and Gotoh and Konno in [9], theoption price is identified with associated semidefinite programming (SDP) problems, the solutionof which provides tight upper and lower bounds, given the first n moments of the distribution ofthe underlying security price. While Gotoh and Konno used their own cutting plane algorithmfor solving the associated SDP problems in [9], we derive and solve such problems with our ownsoftware in this project.

Subsequently, in [21], Lasserre, Prieto-Rumeau and Zervos introduced a new methodology fornumerical pricing of exotic derivatives such as Asian and down-and-out Barrier options. In theirmethodology, the underlying asset price dynamics are modeled by geometric Brownian motionor other mean-reverting processes. For pricing derivatives, they solve a finite dimensional SDPproblem (utilizing their own software GloptiPoly), derived from another infinite dimensionallinear programming problem with moments of appropriate measures.

In this project we investigate and build upon the theory of both of the above approaches.We also extend the theory developed by Lasserre, Prieto-Rumeau and Zervos to model the SDPproblems for pricing European, up-and-out and double Barrier options. Direct implementationof software for solving the associated SDP problems for pricing the European, Asian and (down-and-out, up-and-out and double) Barrier options is given along with detailed analysis of theresults. Secondly, reimplementation of numerical methodology given by Gotoh and Konno is alsogiven, solving the associated SDP problem directly, without using their Cutting Plane algorithm.The efficiency of the above two methods is analysed and compared with other standard optionpricing techniques such as Monte Carlo methods.

i

ii

Acknowledgements

First of all, I would like to acknowledge Dr. Daniel Kuhn who provided me with constantguidance and encouragement through out the project. I am deeply indebted to Dr. Kuhn forembarking with me on this project journey. I could not have wished for better supervisor andcollaborator. Your contributions, insightful comments and awe inspiring conversations have beenof great value to me.

I would also like to acknowledge Professor Berc Rustem for his constructive comments andagreeing to be the second marker for this project.

I also acknowledge my family and friends for their moral and intellectual support during thisproject. Lastly, I would like to thank Nikita for being the indefatigable and untiring source ofstrength for me, when I needed it most.

Contents

List of Figures vi

List of Tables vii

1 Introduction 11.1 Two Recent Methodologies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11.2 Contributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

2 Options and Valuation Techniques 42.1 Class of Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

2.1.1 European Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42.1.2 Asian Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52.1.3 Barrier Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

2.2 Models for Underlying Asset Price . . . . . . . . . . . . . . . . . . . . . . . . . . 72.2.1 Geometric Brownian Motion . . . . . . . . . . . . . . . . . . . . . . . . . 72.2.2 Ornstein-Uhlenbeck Process . . . . . . . . . . . . . . . . . . . . . . . . . . 82.2.3 Cox Ingersoll Ross process . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

2.3 Monte Carlo Methods . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102.3.1 European Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102.3.2 Asian Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112.3.3 Barrier Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 122.3.4 Advantages and Disadvantages of Monte Carlo Methods . . . . . . . . . . 15

2.4 Black Scholes PDE and Analytical Solution . . . . . . . . . . . . . . . . . . . . . 152.4.1 Analytical Solution for European Options . . . . . . . . . . . . . . . . . . 162.4.2 Analytical Solution for Barrier Options . . . . . . . . . . . . . . . . . . . 162.4.3 Assumptions and Shortcomings of Black Scholes Formula . . . . . . . . . 18

3 Semi-Parametric Approach for Bounding Option Price 203.1 Review of Basic Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 203.2 SDP Formulation of the Bounding Problems . . . . . . . . . . . . . . . . . . . . . 253.3 Computing the Moments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

4 Method of Moments and SDP Relaxations 314.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 314.2 Deriving Infinite-Dimensional LP Problem . . . . . . . . . . . . . . . . . . . . . . 32

4.2.1 Basic Adjoint Equation . . . . . . . . . . . . . . . . . . . . . . . . . . . . 324.2.2 Martingale Moment Conditions . . . . . . . . . . . . . . . . . . . . . . . . 344.2.3 Using Available Moments . . . . . . . . . . . . . . . . . . . . . . . . . . . 354.2.4 Using Martingale Moments Conditions . . . . . . . . . . . . . . . . . . . . 35

4.3 Polynomial Optimisation and Problem of Moments . . . . . . . . . . . . . . . . . 364.3.1 Notation and Definition . . . . . . . . . . . . . . . . . . . . . . . . . . . . 364.3.2 Necessary Moment conditions . . . . . . . . . . . . . . . . . . . . . . . . . 37

iv

4.3.3 SDP Relaxations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 384.3.4 Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

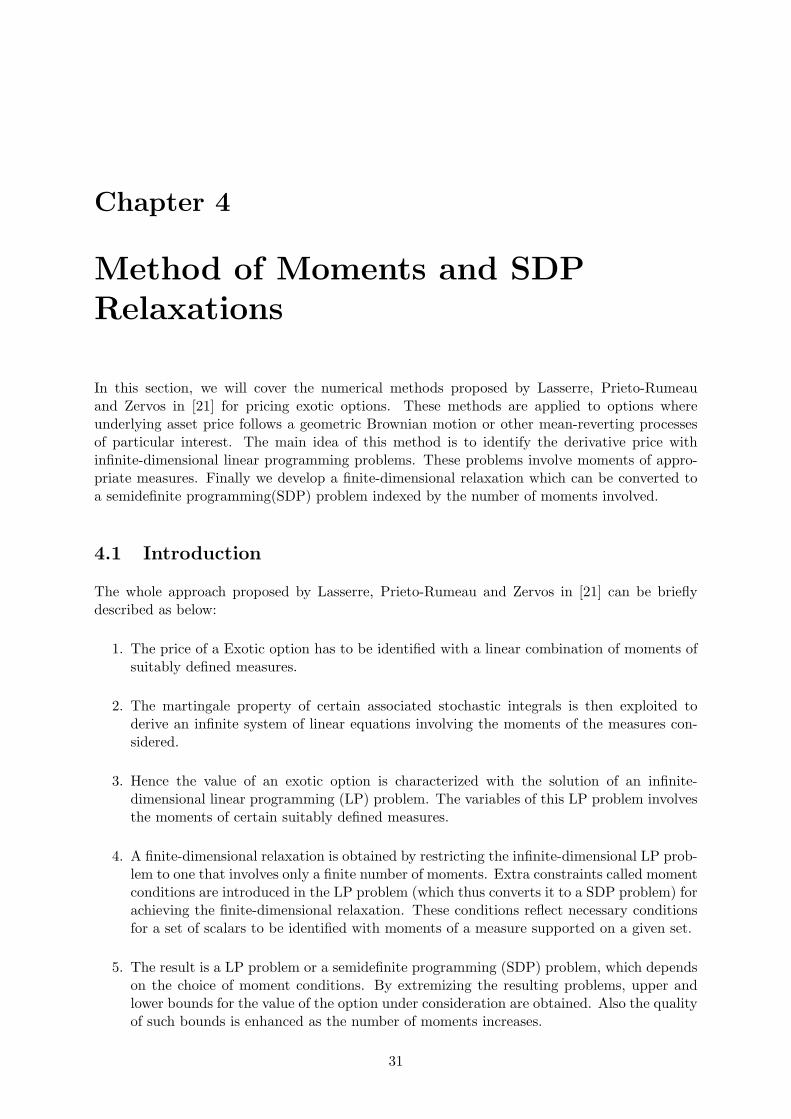

4.4 Finite Dimensional Relaxations . . . . . . . . . . . . . . . . . . . . . . . . . . . . 394.5 SDP Relaxations for European Options . . . . . . . . . . . . . . . . . . . . . . . 40

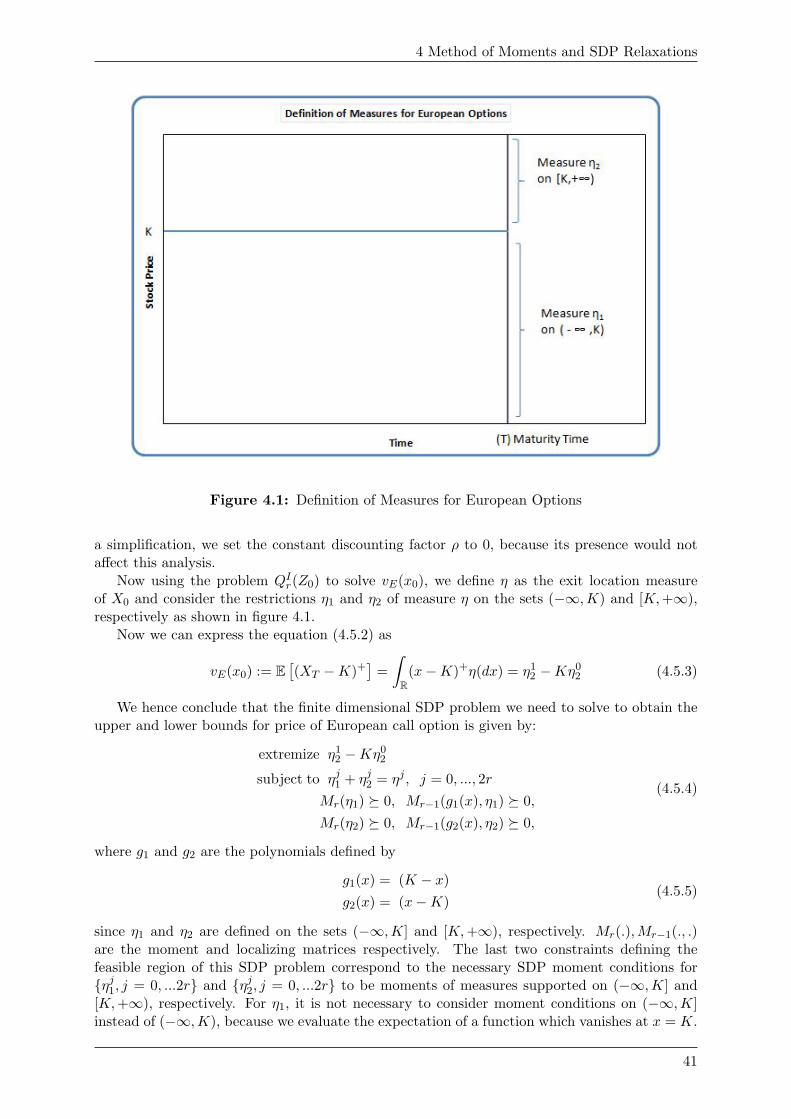

4.5.1 Moments Computation . . . . . . . . . . . . . . . . . . . . . . . . . . . . 424.6 SDP Relaxations for Asian Options . . . . . . . . . . . . . . . . . . . . . . . . . . 43

4.6.1 Moments Computation . . . . . . . . . . . . . . . . . . . . . . . . . . . . 454.7 SDP Relaxations for Barrier Options . . . . . . . . . . . . . . . . . . . . . . . . . 47

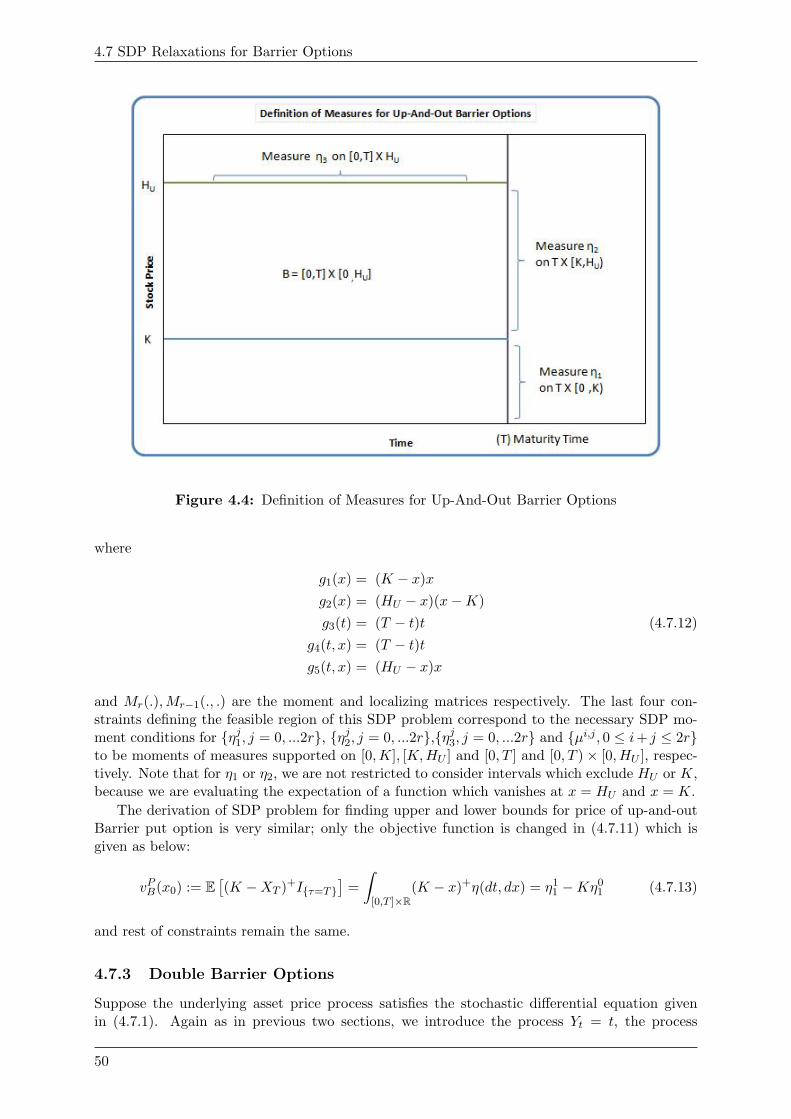

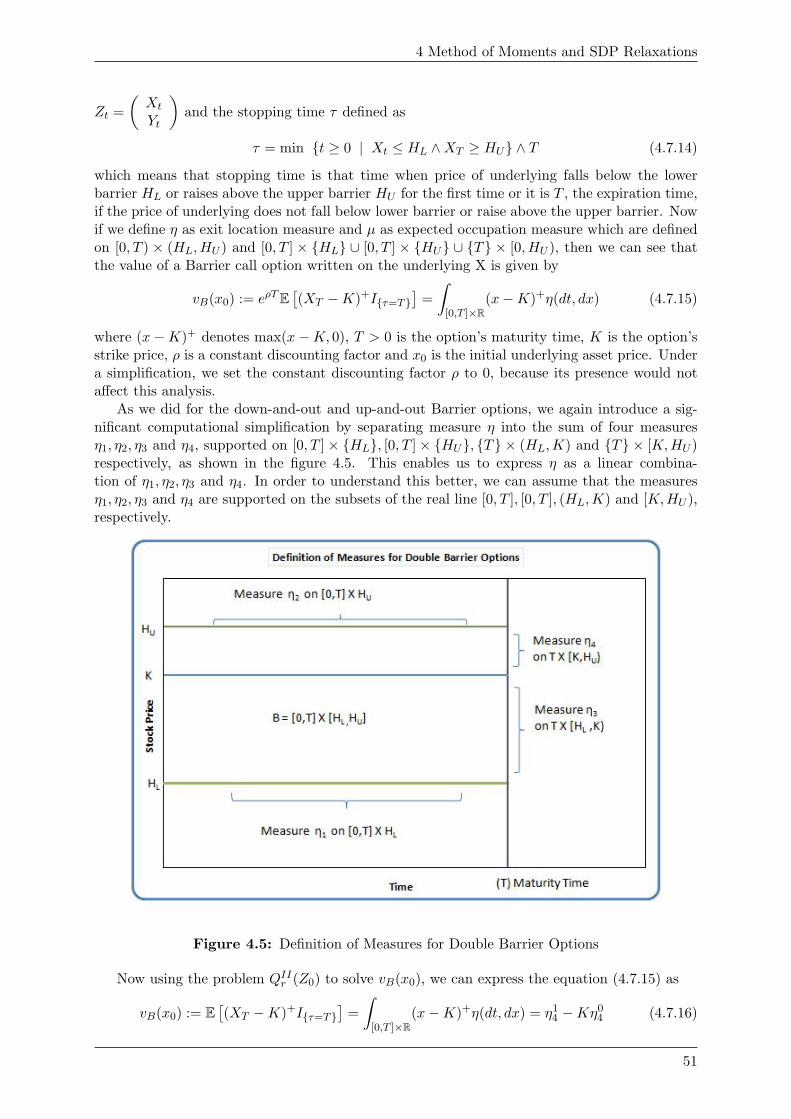

4.7.1 Down-and-out Barrier Options . . . . . . . . . . . . . . . . . . . . . . . . 474.7.2 Up-and-out Barrier Options . . . . . . . . . . . . . . . . . . . . . . . . . . 494.7.3 Double Barrier Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . 504.7.4 Evaluating Basic Adjoint Equation . . . . . . . . . . . . . . . . . . . . . . 52

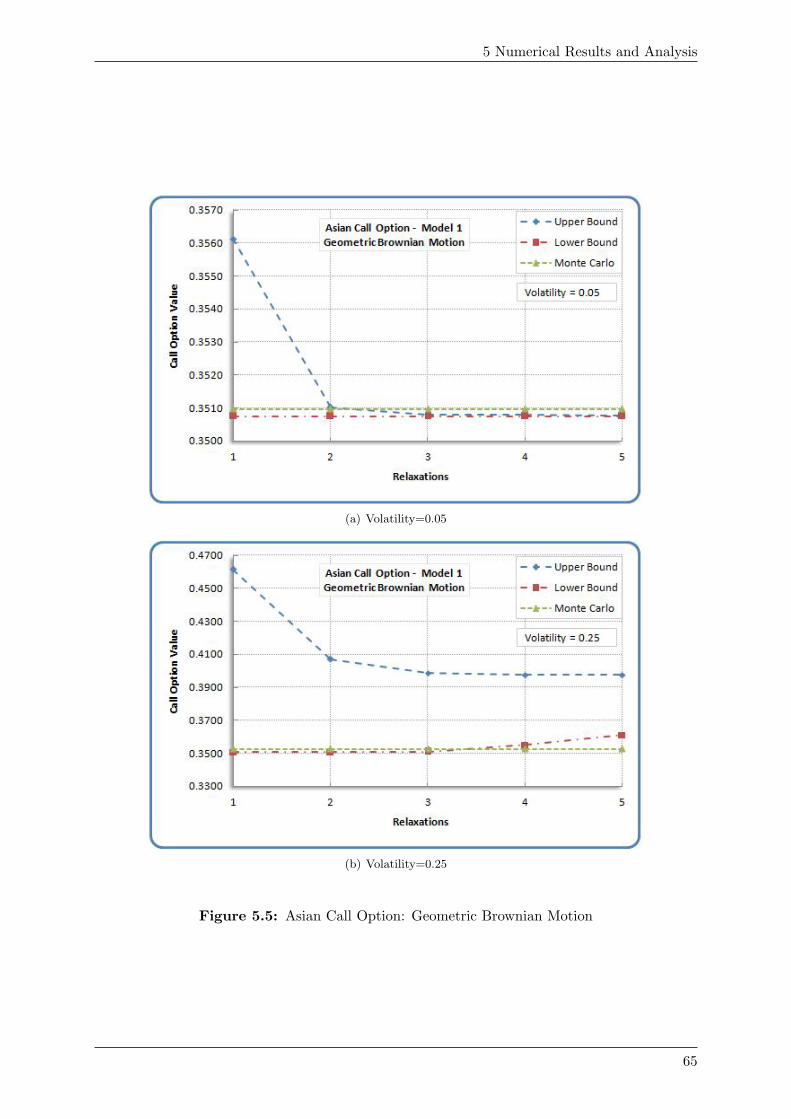

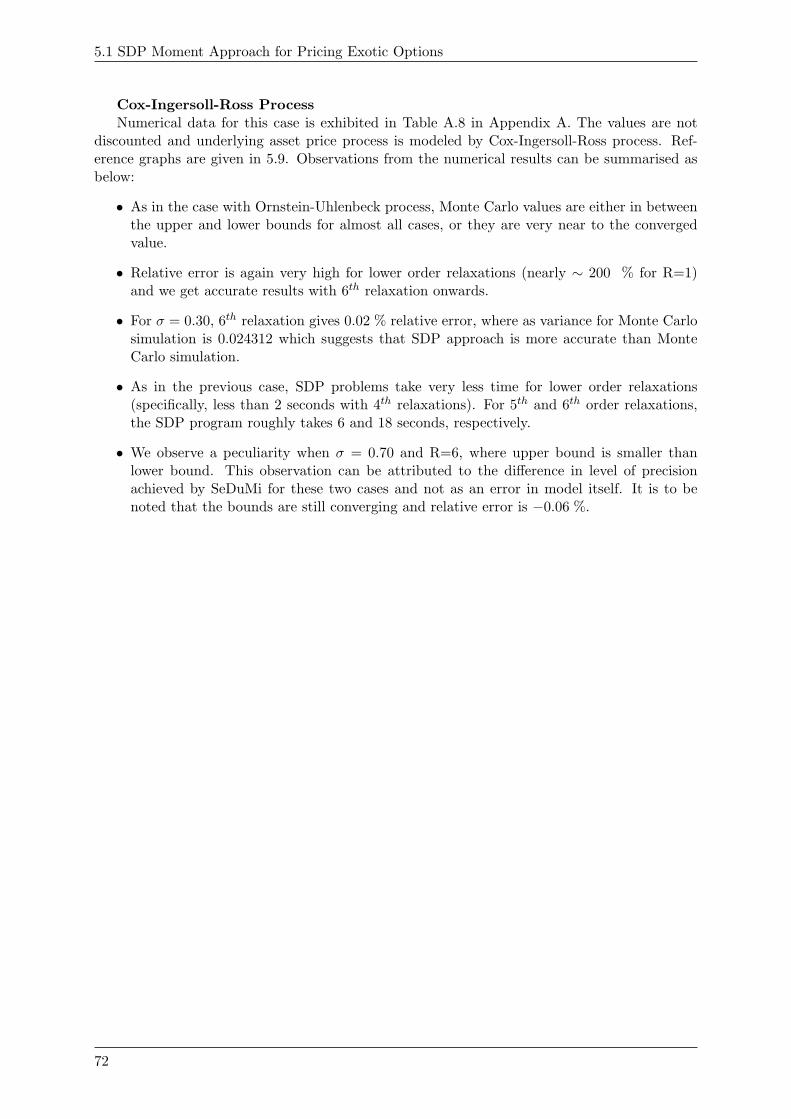

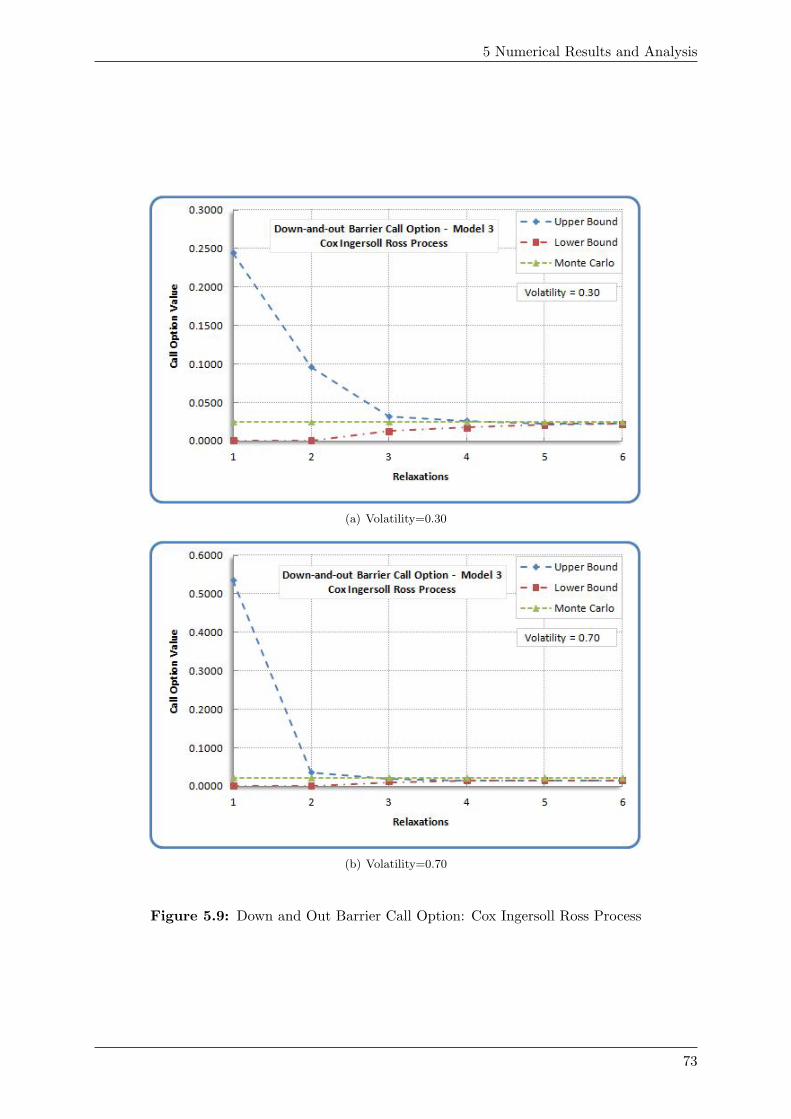

5 Numerical Results and Analysis 555.1 SDP Moment Approach for Pricing Exotic Options . . . . . . . . . . . . . . . . . 55

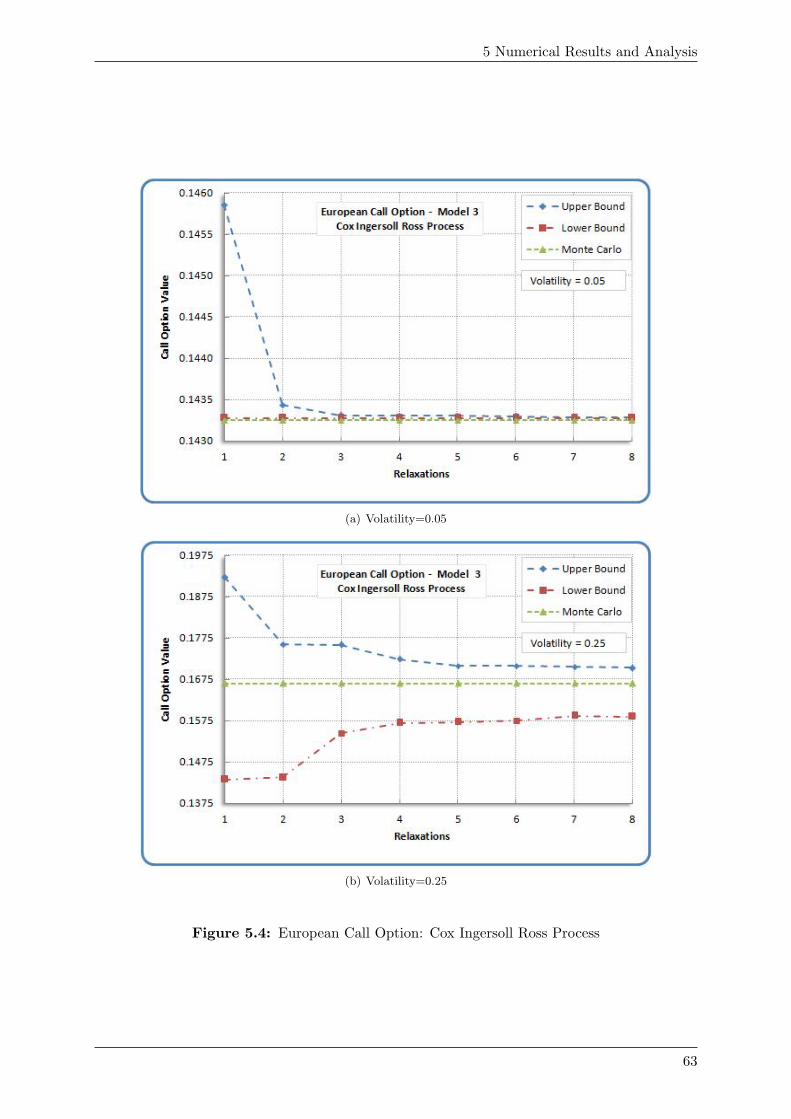

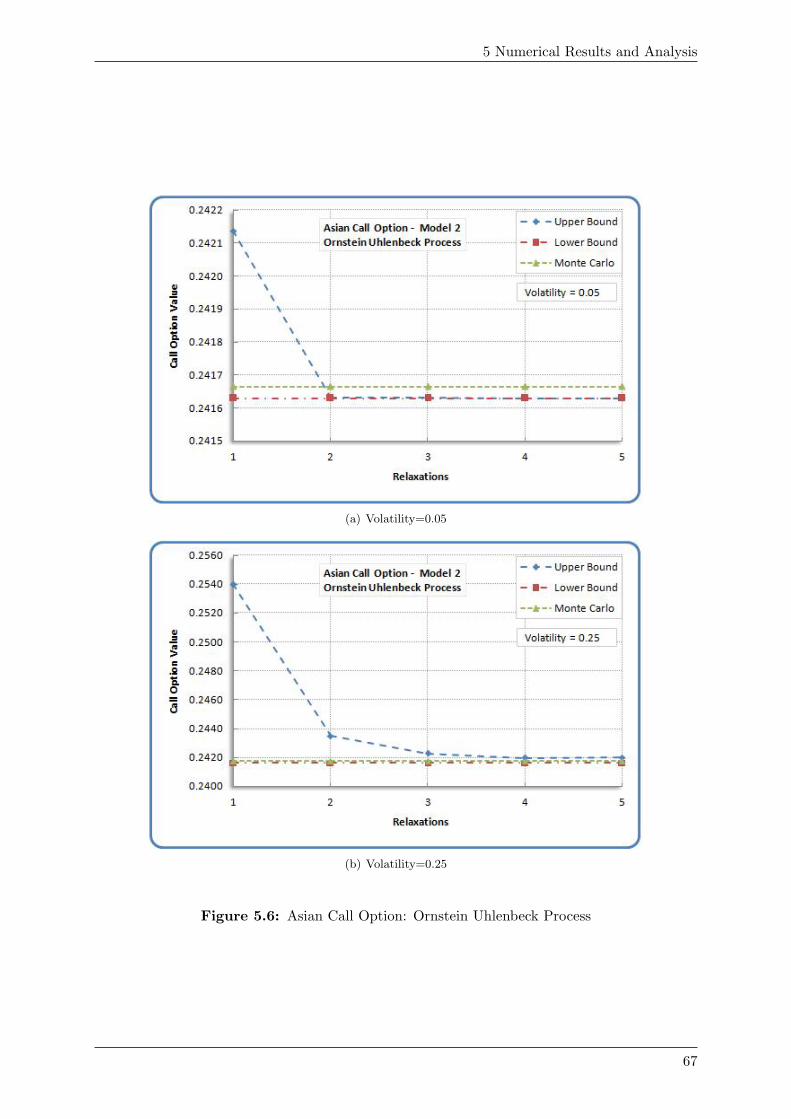

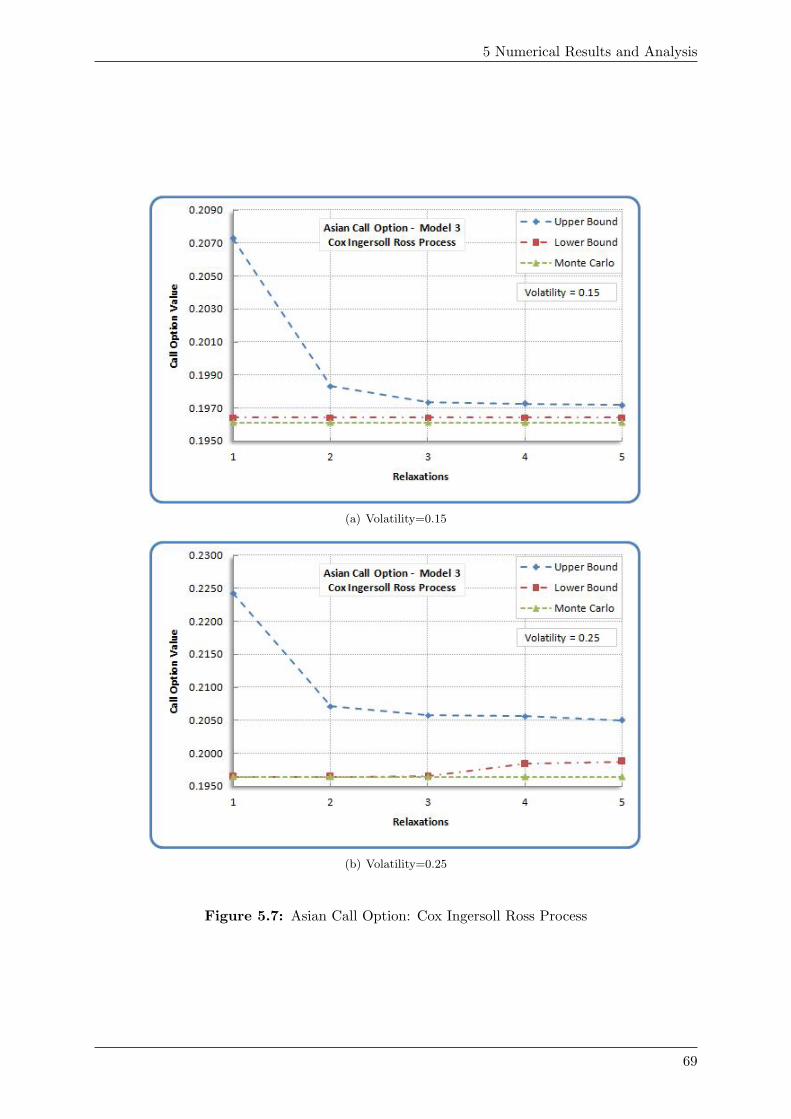

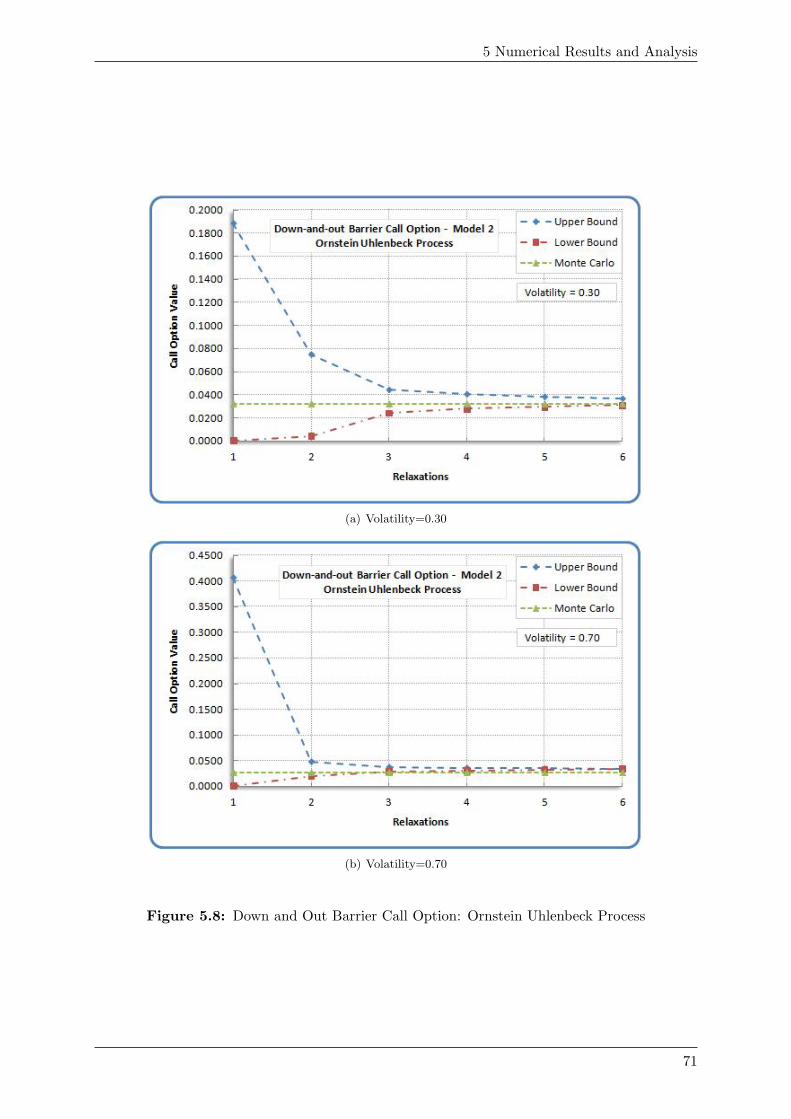

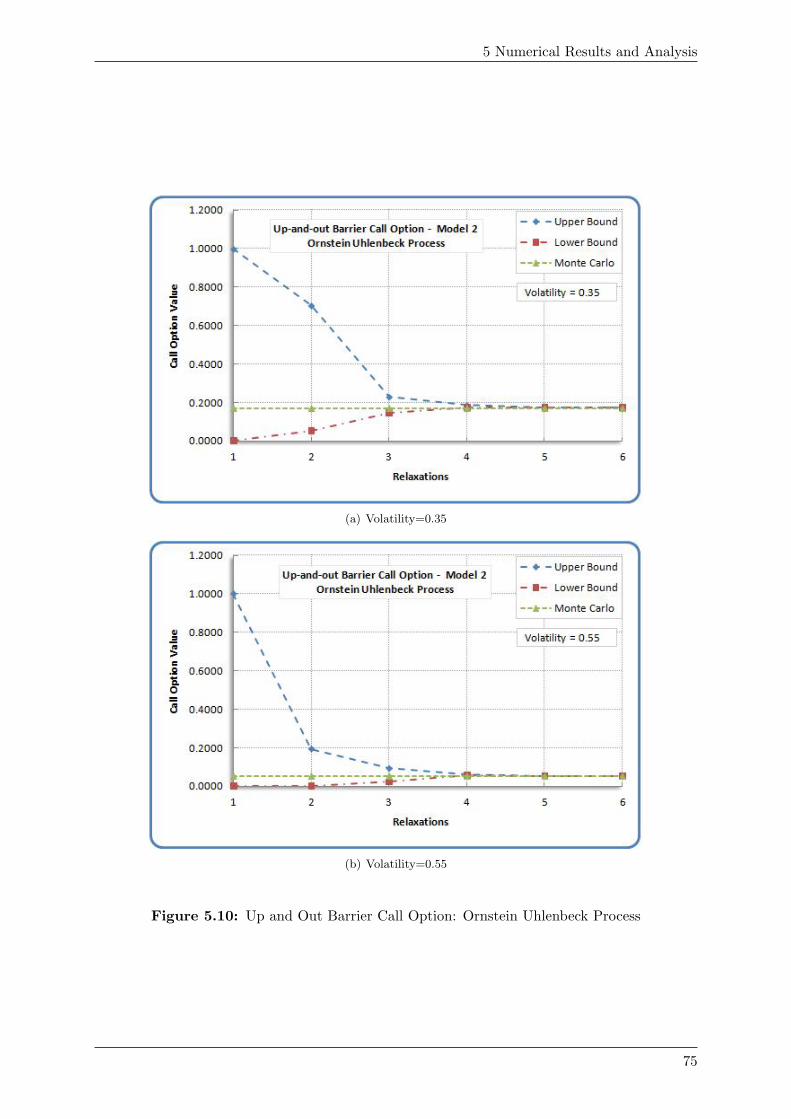

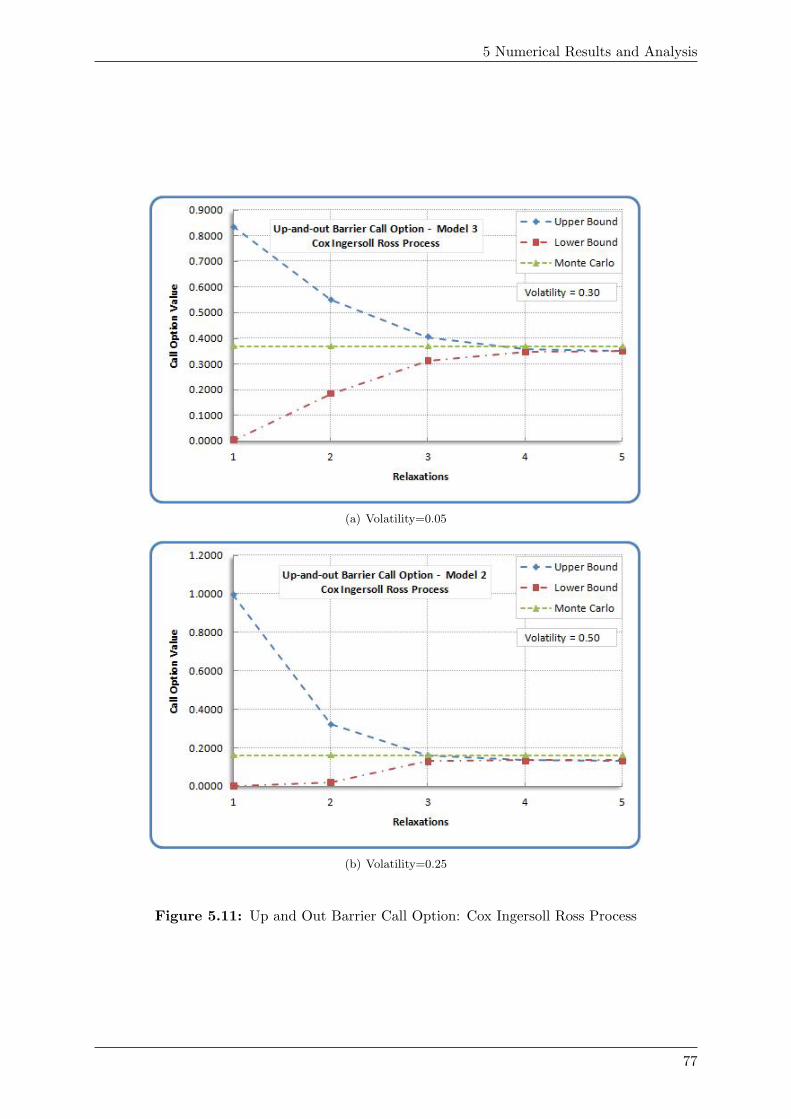

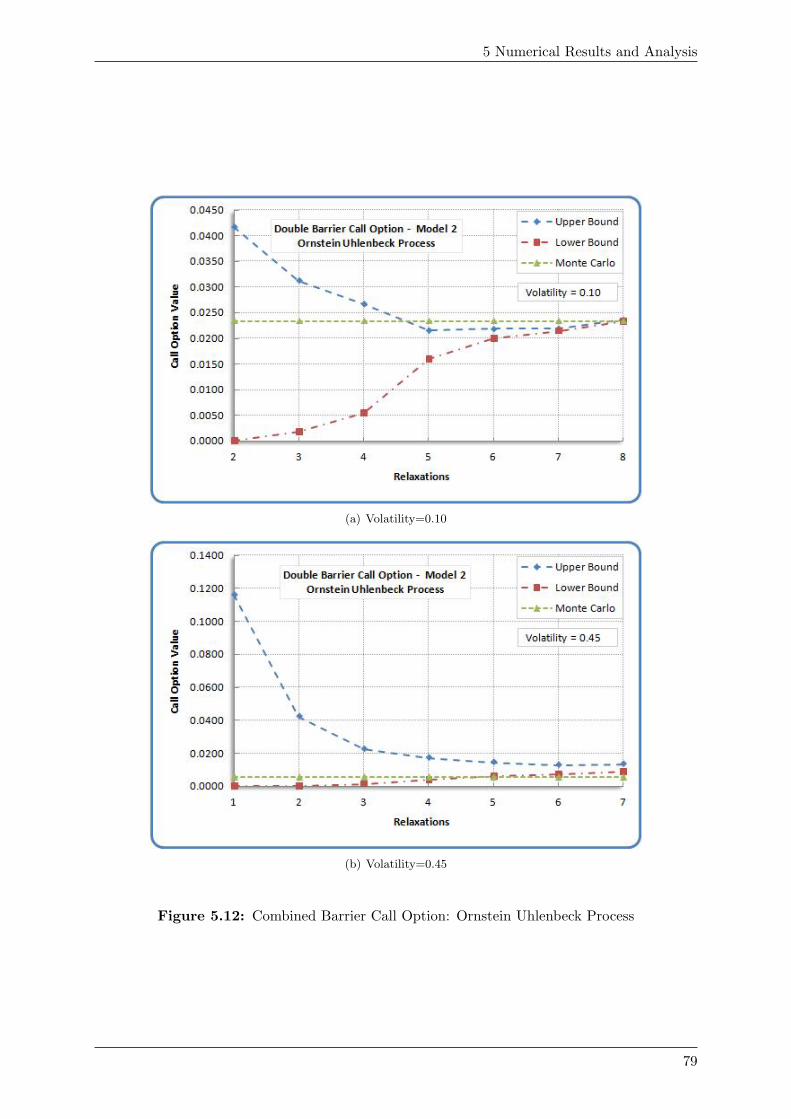

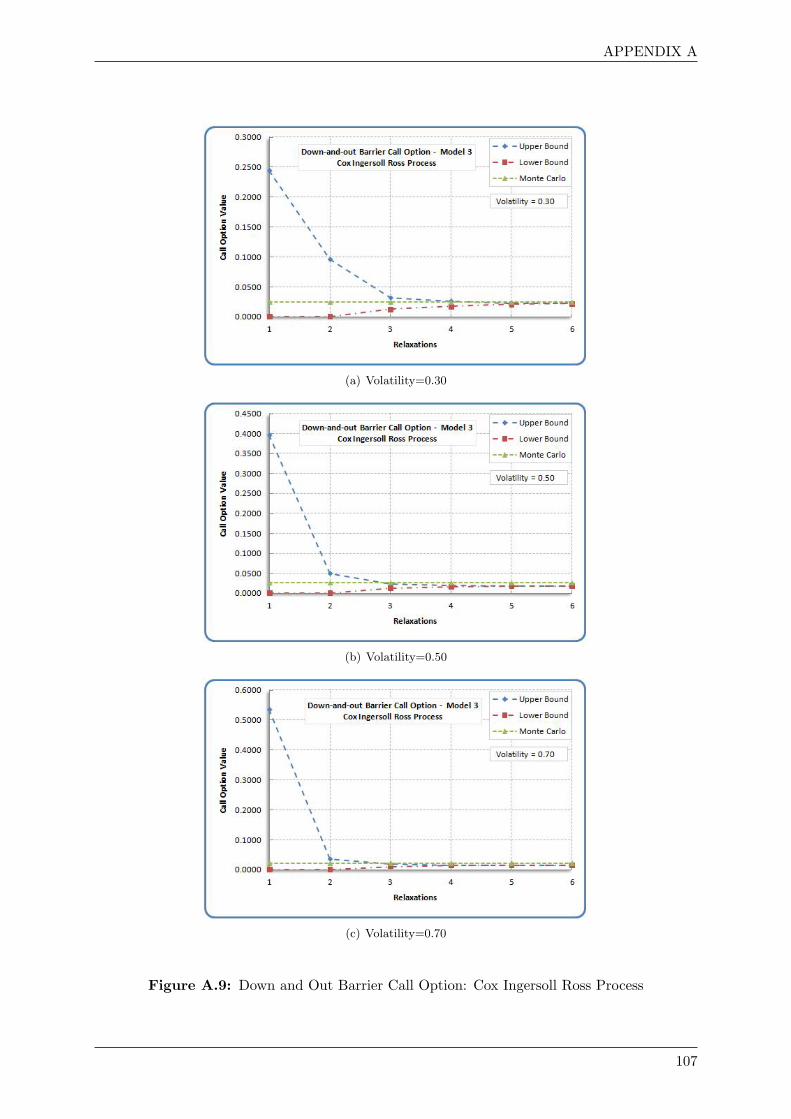

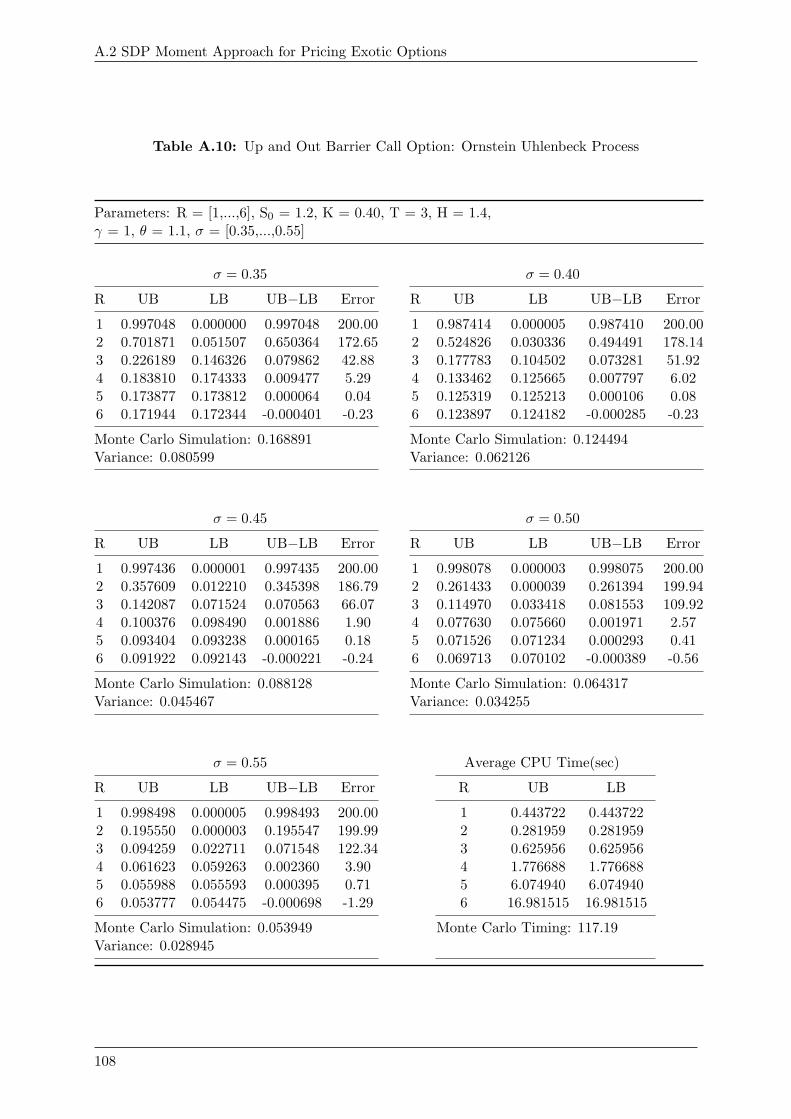

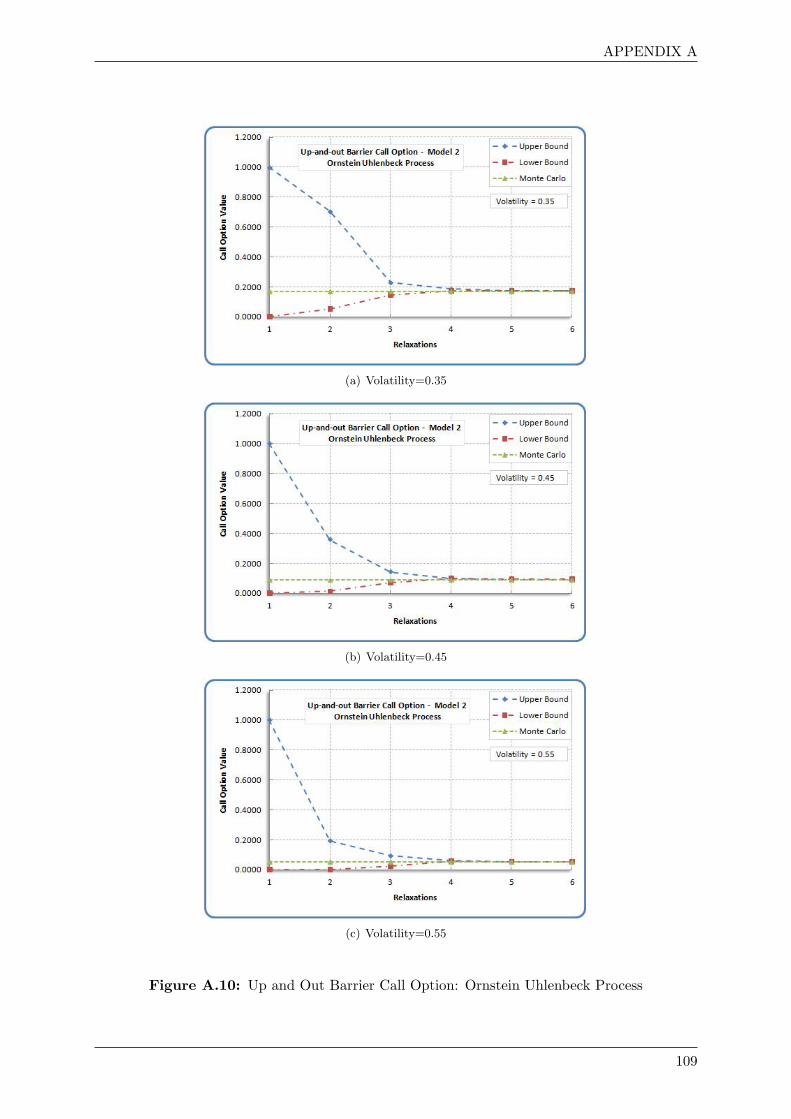

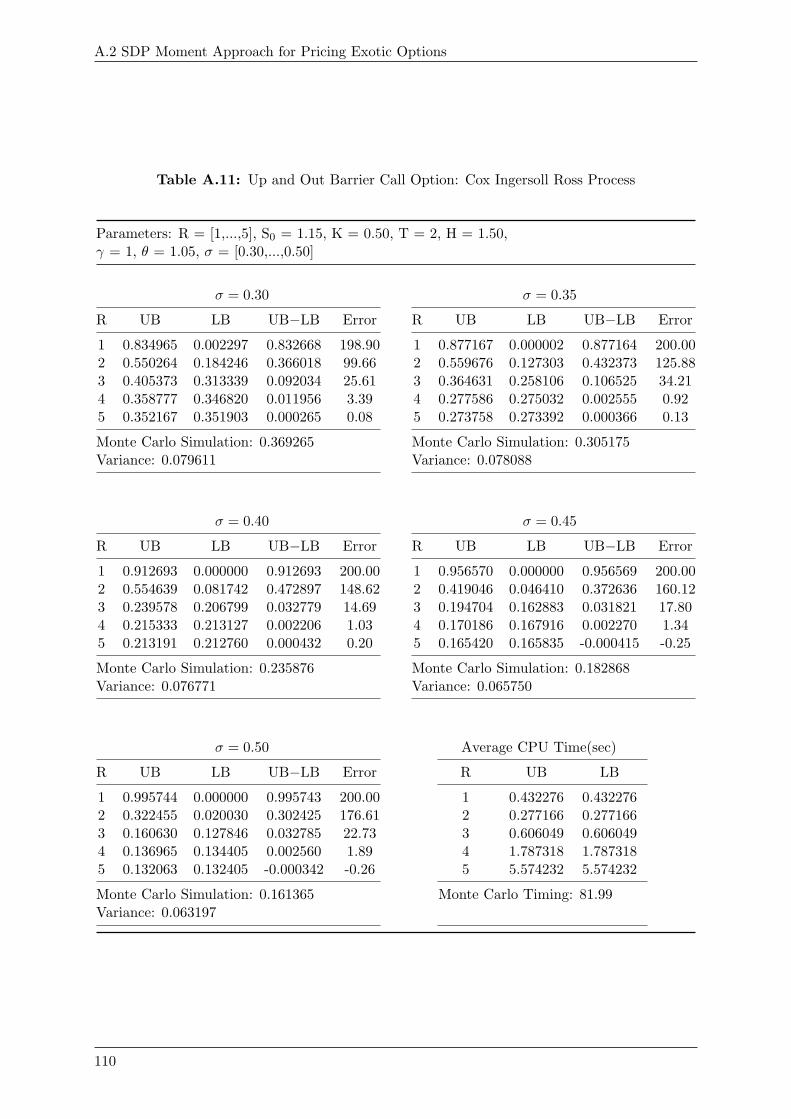

5.1.1 European Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 565.1.2 Asian Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 645.1.3 Down-and-out Barrier Options . . . . . . . . . . . . . . . . . . . . . . . . 705.1.4 Up-and-out Barrier Options . . . . . . . . . . . . . . . . . . . . . . . . . . 745.1.5 Double Barrier Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78

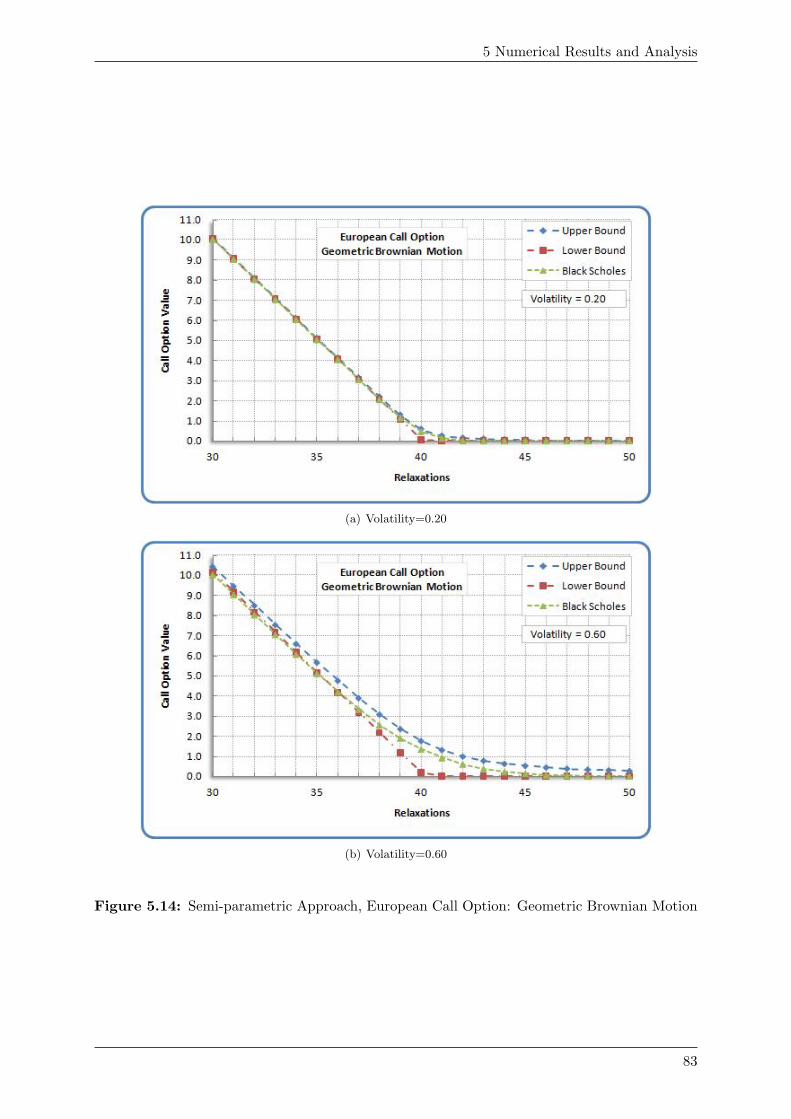

5.2 Semi-parametric Approach for Pricing European Options . . . . . . . . . . . . . 82

6 Conclusion 866.1 Numerical Remarks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 866.2 Future Direction of Research . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87

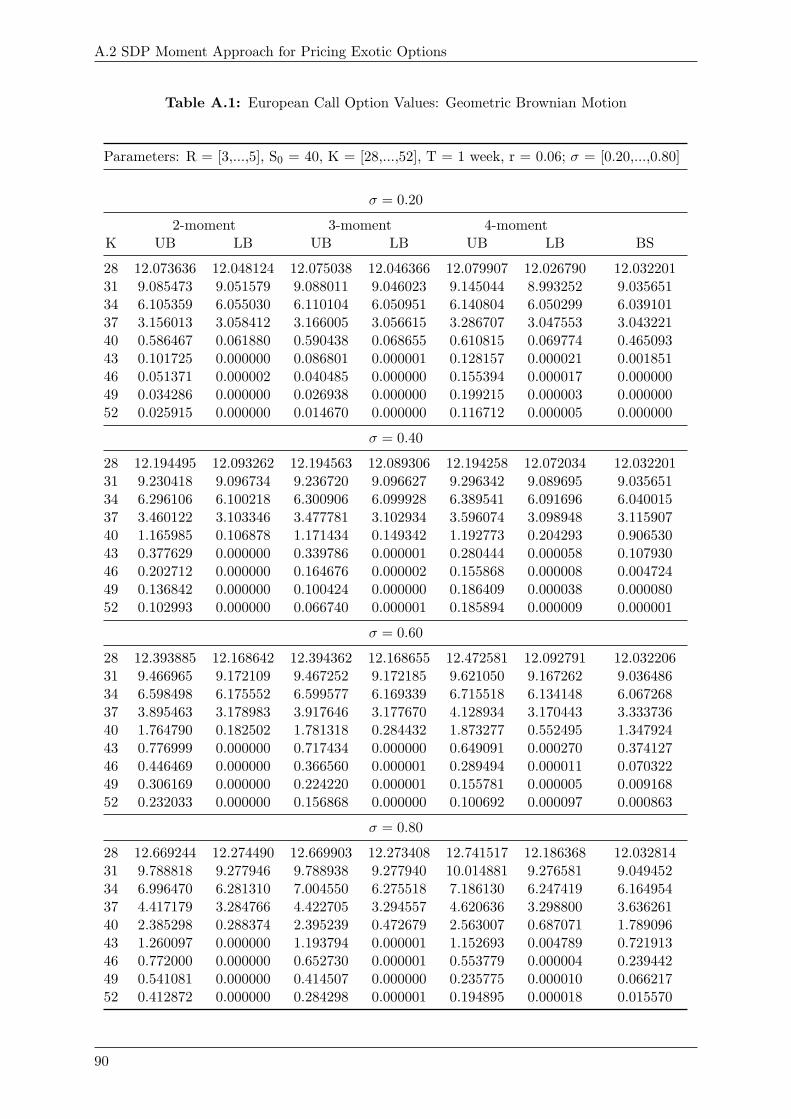

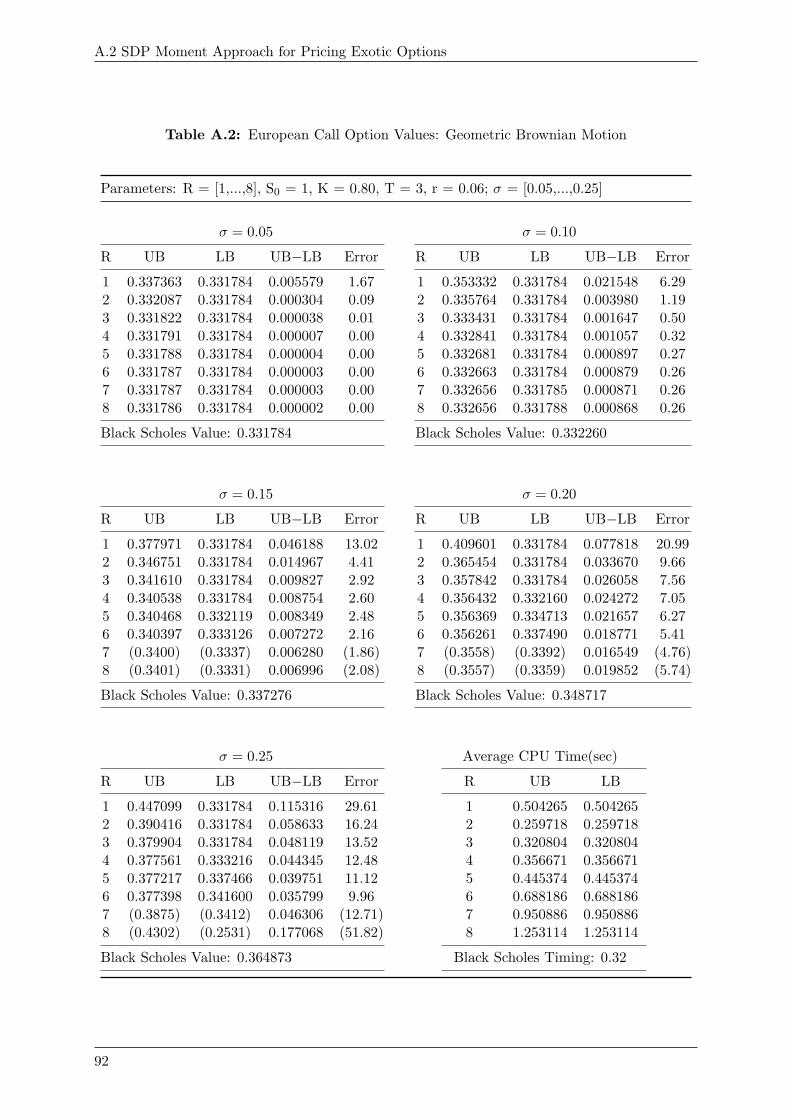

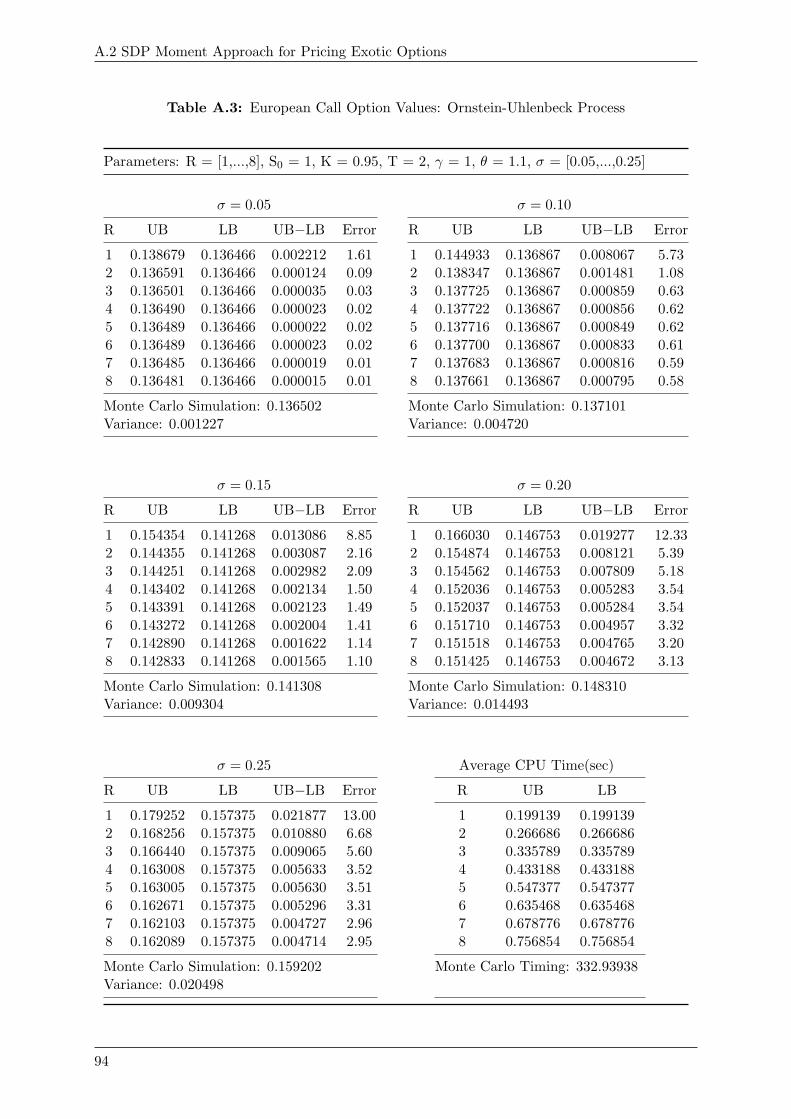

A Tables and Figures for Numerical Results 89A.1 Semi-parametric Approach for Pricing European Options . . . . . . . . . . . . . 89A.2 SDP Moment Approach for Pricing Exotic Options . . . . . . . . . . . . . . . . . 89

Bibliography 116

v

List of Figures

2.1 Value of European Option at Expiration . . . . . . . . . . . . . . . . . . . . . . . 52.2 Value of Barrier Call Option . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

4.1 Definition of Measures for European Options . . . . . . . . . . . . . . . . . . . . 414.2 Definition of Measures for Asian Options . . . . . . . . . . . . . . . . . . . . . . . 444.3 Definition of Measures for Down-And-Out Barrier Options . . . . . . . . . . . . . 484.4 Definition of Measures for Up-And-Out Barrier Options . . . . . . . . . . . . . . 504.5 Definition of Measures for Double Barrier Options . . . . . . . . . . . . . . . . . 51

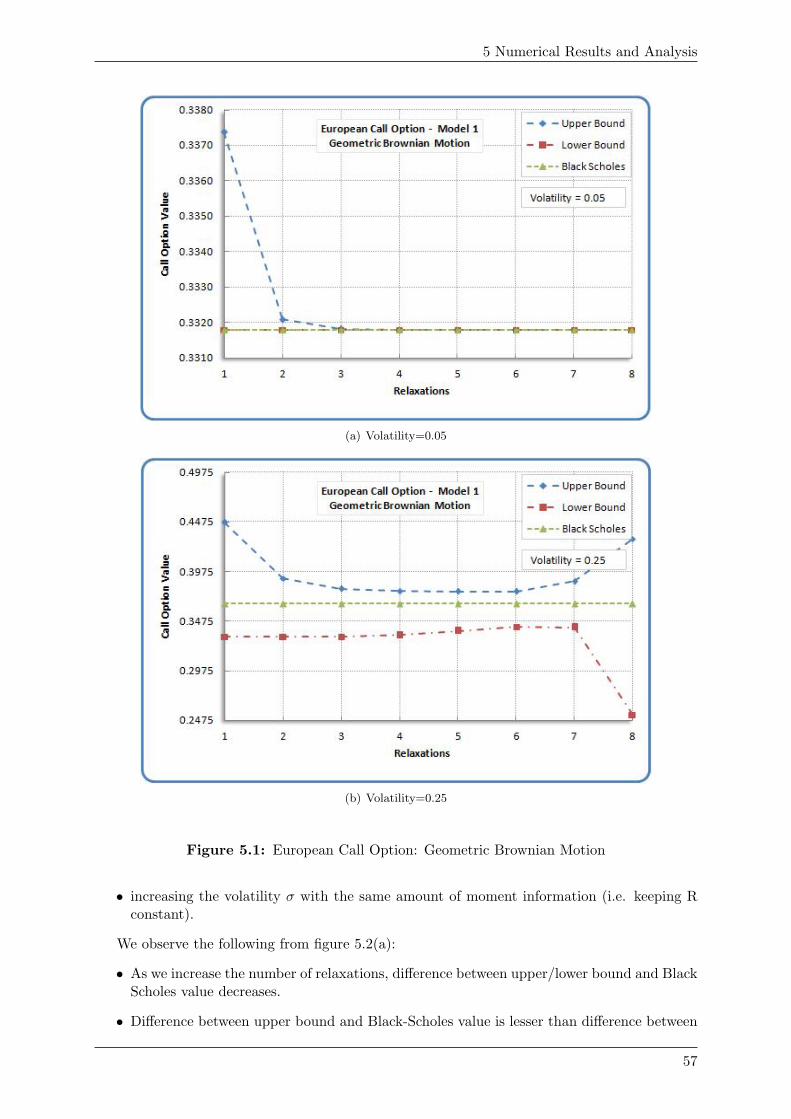

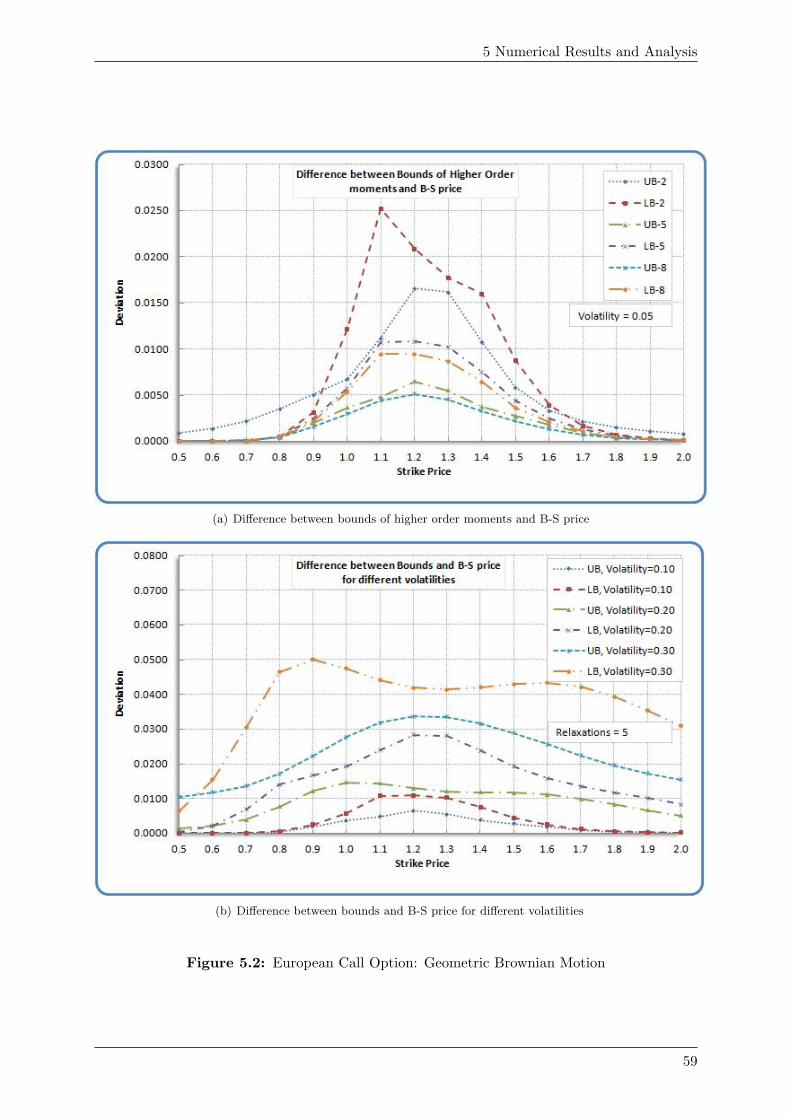

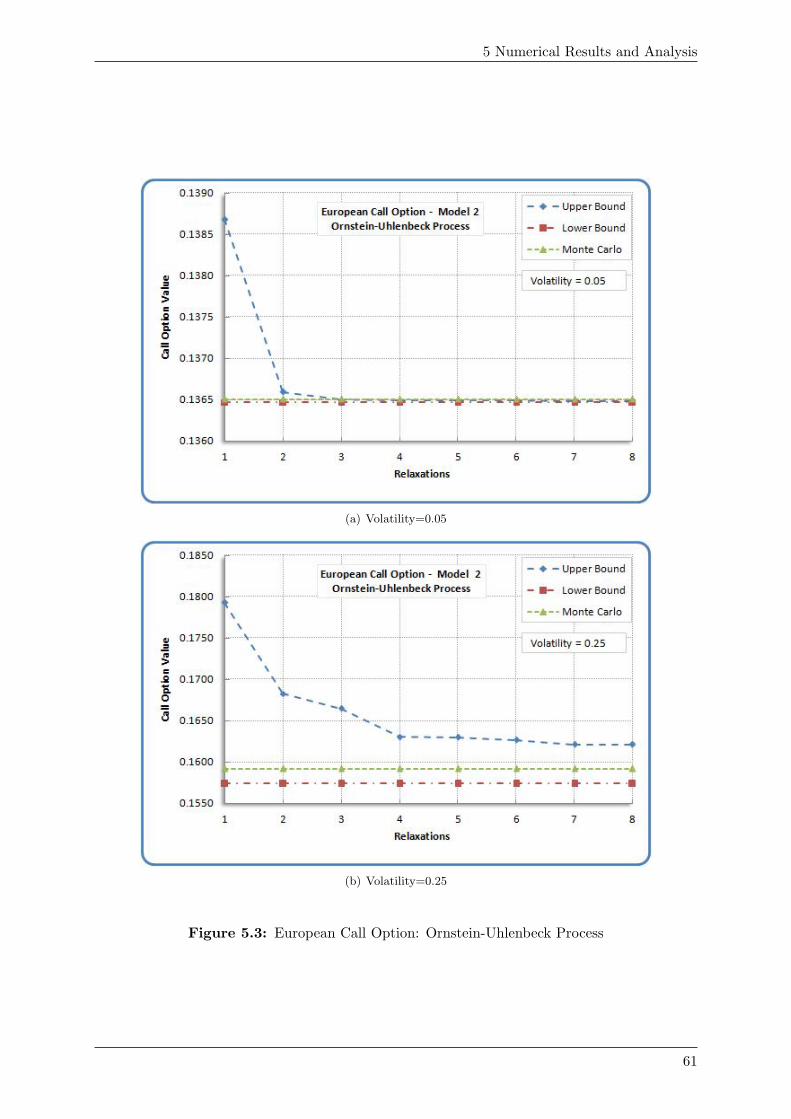

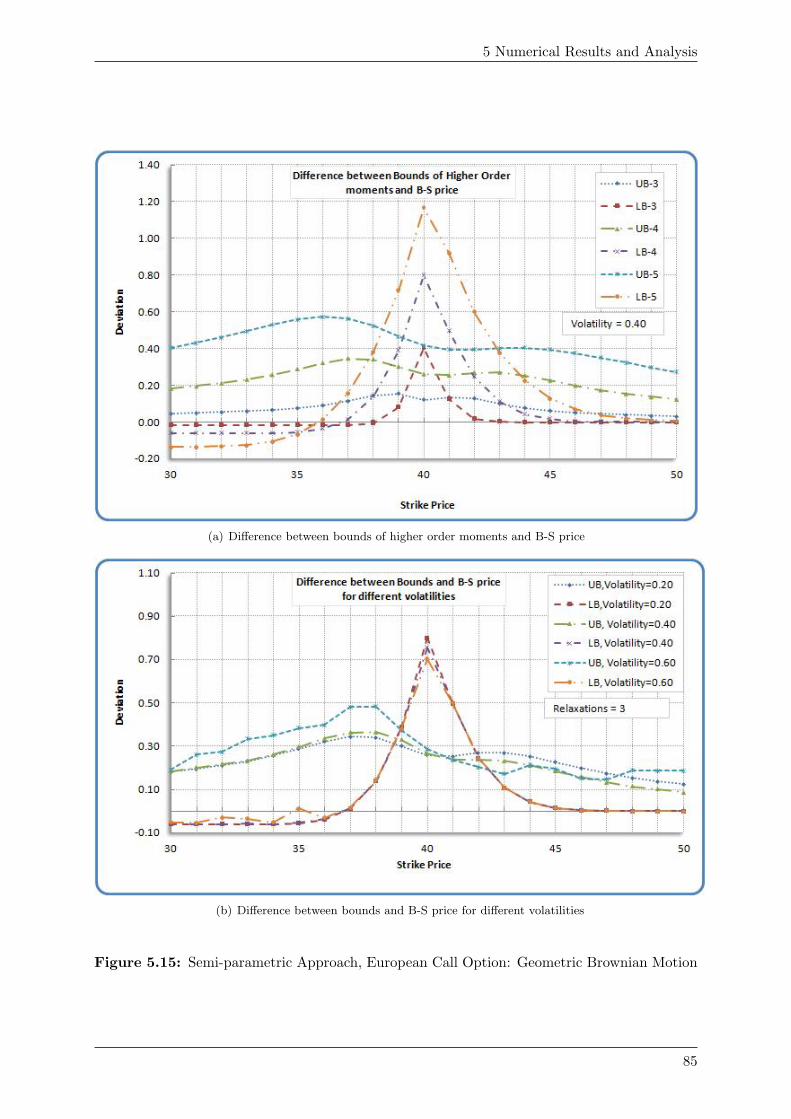

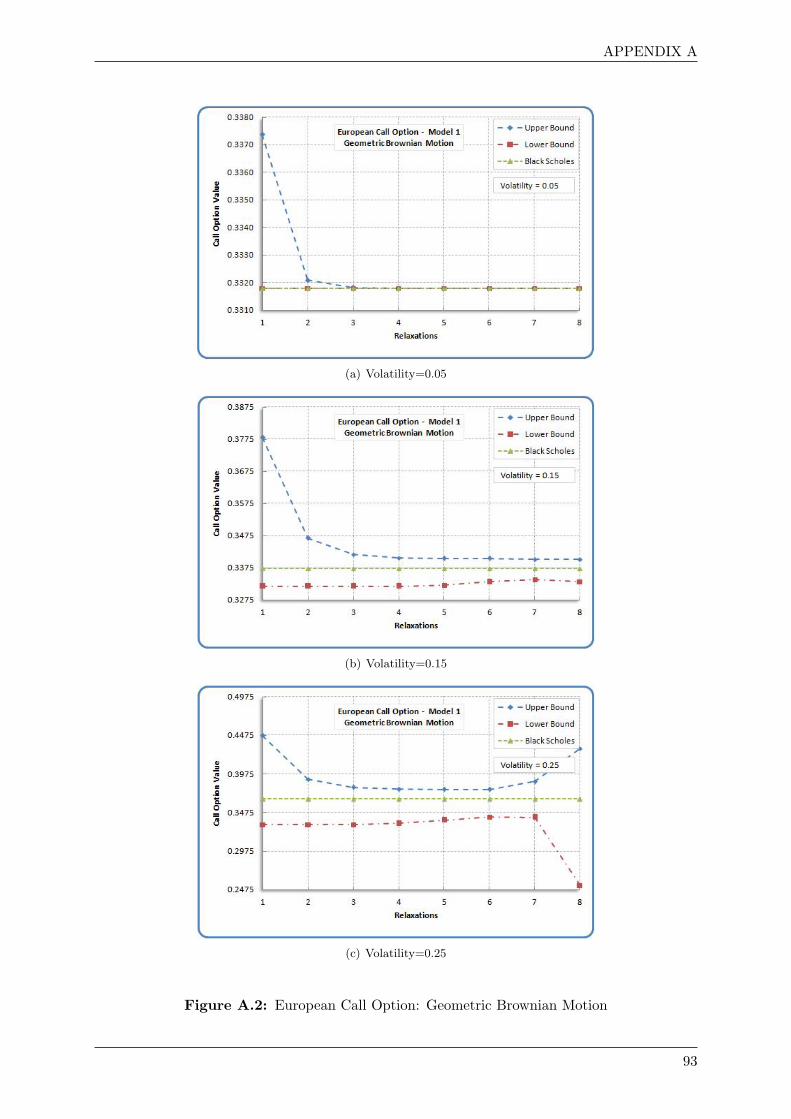

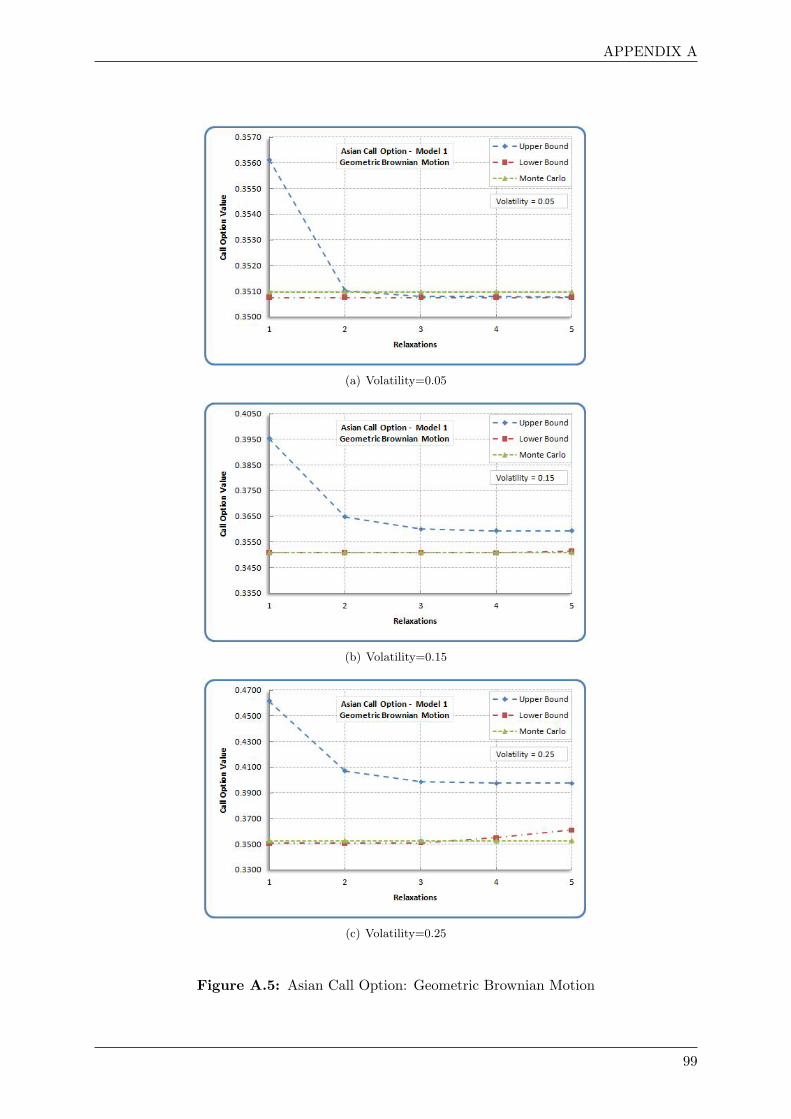

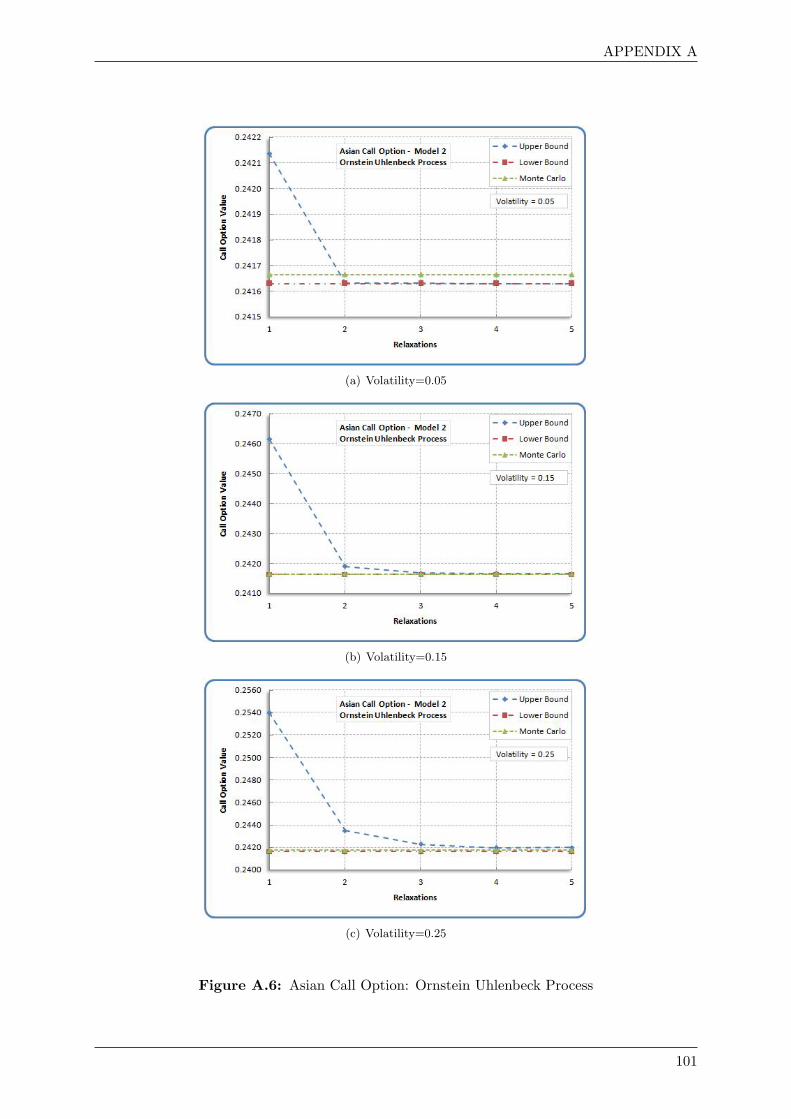

5.1 European Call Option: Geometric Brownian Motion . . . . . . . . . . . . . . . . 575.2 European Call Option: Geometric Brownian Motion . . . . . . . . . . . . . . . . 595.3 European Call Option: Ornstein-Uhlenbeck Process . . . . . . . . . . . . . . . . 615.4 European Call Option: Cox Ingersoll Ross Process . . . . . . . . . . . . . . . . . 635.5 Asian Call Option: Geometric Brownian Motion . . . . . . . . . . . . . . . . . . 655.6 Asian Call Option: Ornstein Uhlenbeck Process . . . . . . . . . . . . . . . . . . . 675.7 Asian Call Option: Cox Ingersoll Ross Process . . . . . . . . . . . . . . . . . . . 695.8 Down and Out Barrier Call Option: Ornstein Uhlenbeck Process . . . . . . . . . 715.9 Down and Out Barrier Call Option: Cox Ingersoll Ross Process . . . . . . . . . . 735.10 Up and Out Barrier Call Option: Ornstein Uhlenbeck Process . . . . . . . . . . . 755.11 Up and Out Barrier Call Option: Cox Ingersoll Ross Process . . . . . . . . . . . 775.12 Combined Barrier Call Option: Ornstein Uhlenbeck Process . . . . . . . . . . . . 795.13 Combined Barrier Call Option: Cox Ingersoll Ross Process . . . . . . . . . . . . 815.14 Semi-parametric Approach, European Call Option: Geometric Brownian Motion 835.15 Semi-parametric Approach, European Call Option: Geometric Brownian Motion 85

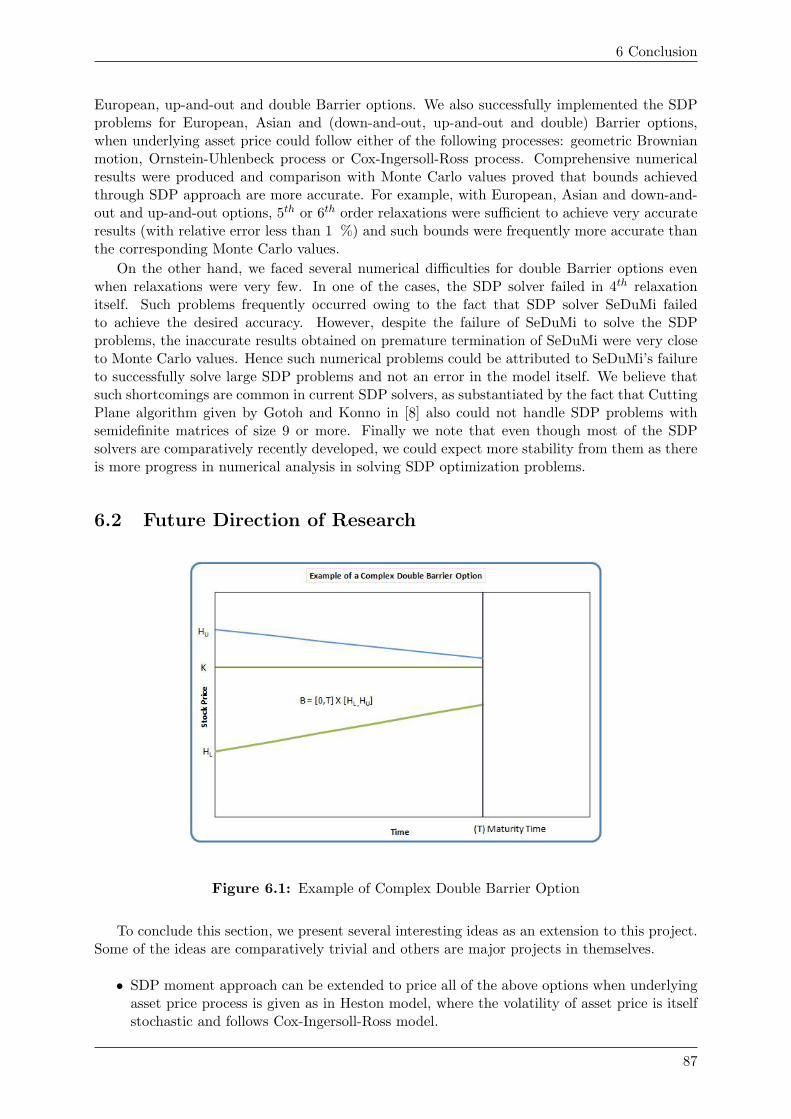

6.1 Example of Complex Double Barrier Option . . . . . . . . . . . . . . . . . . . . . 87

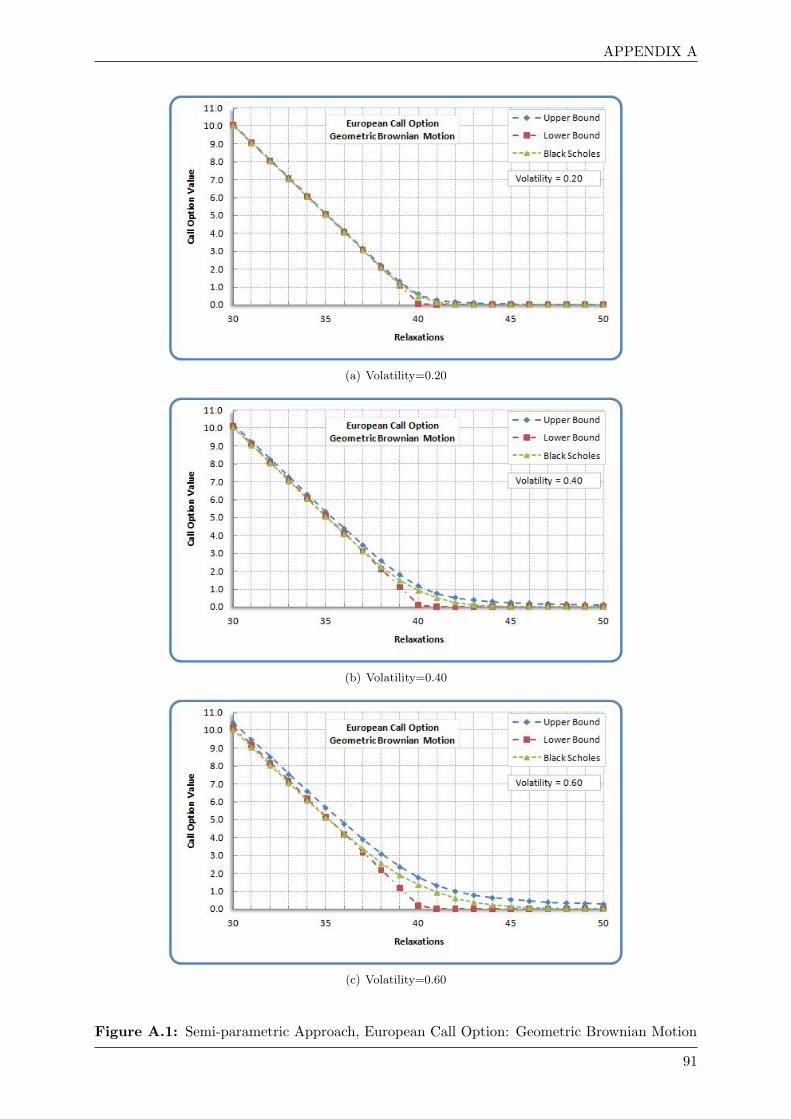

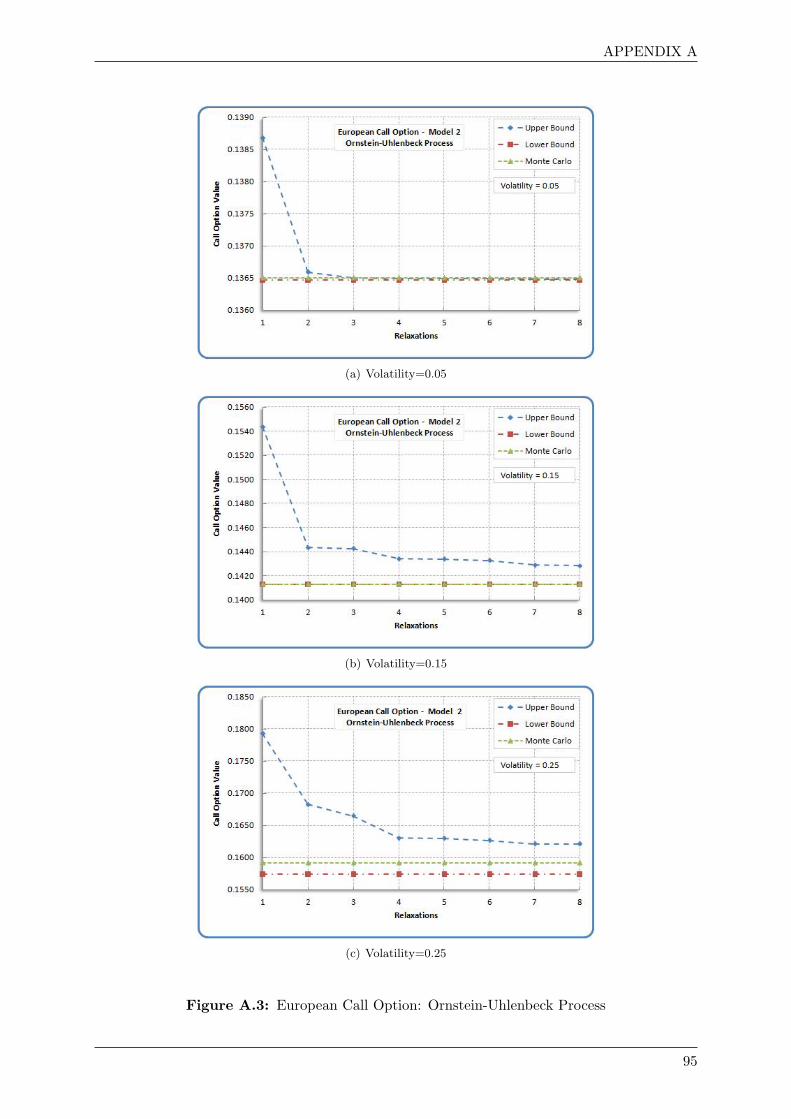

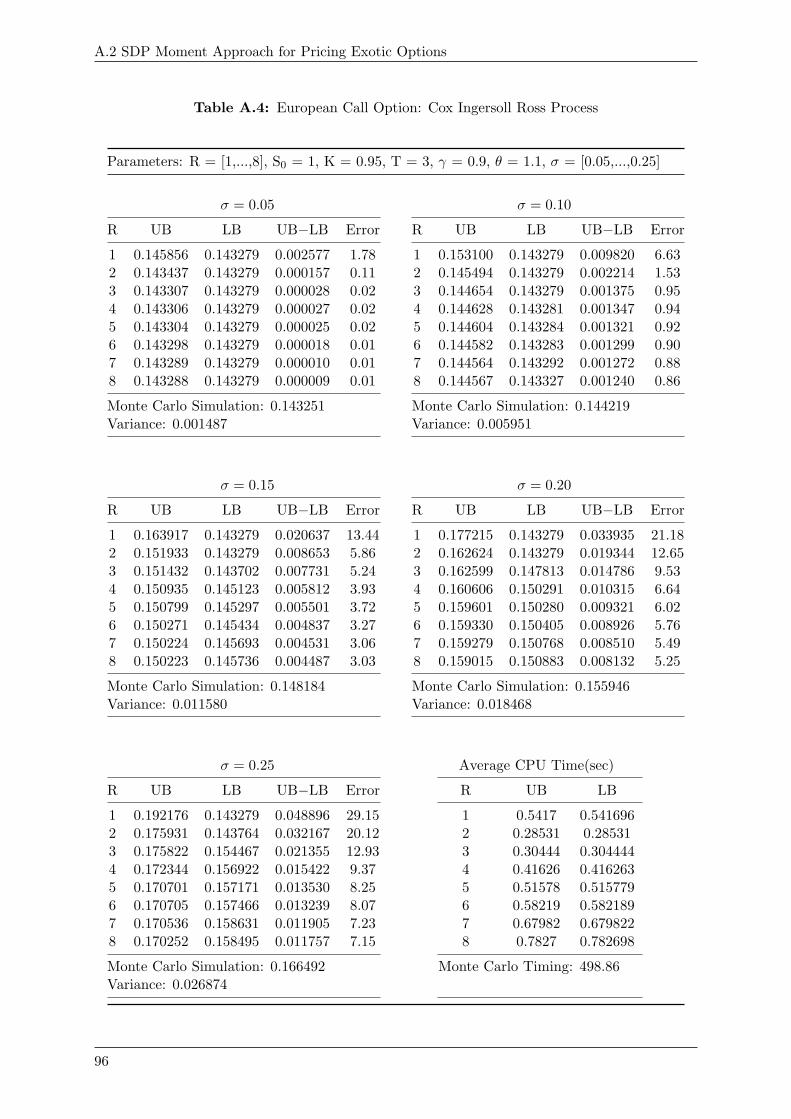

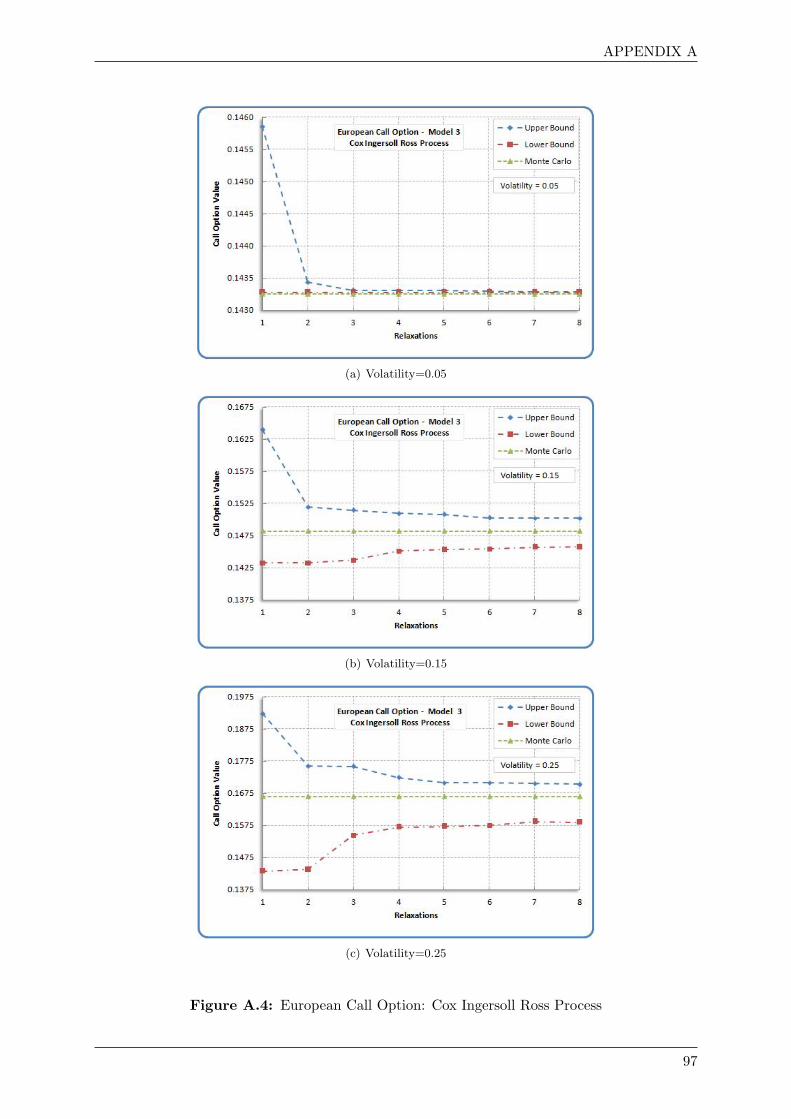

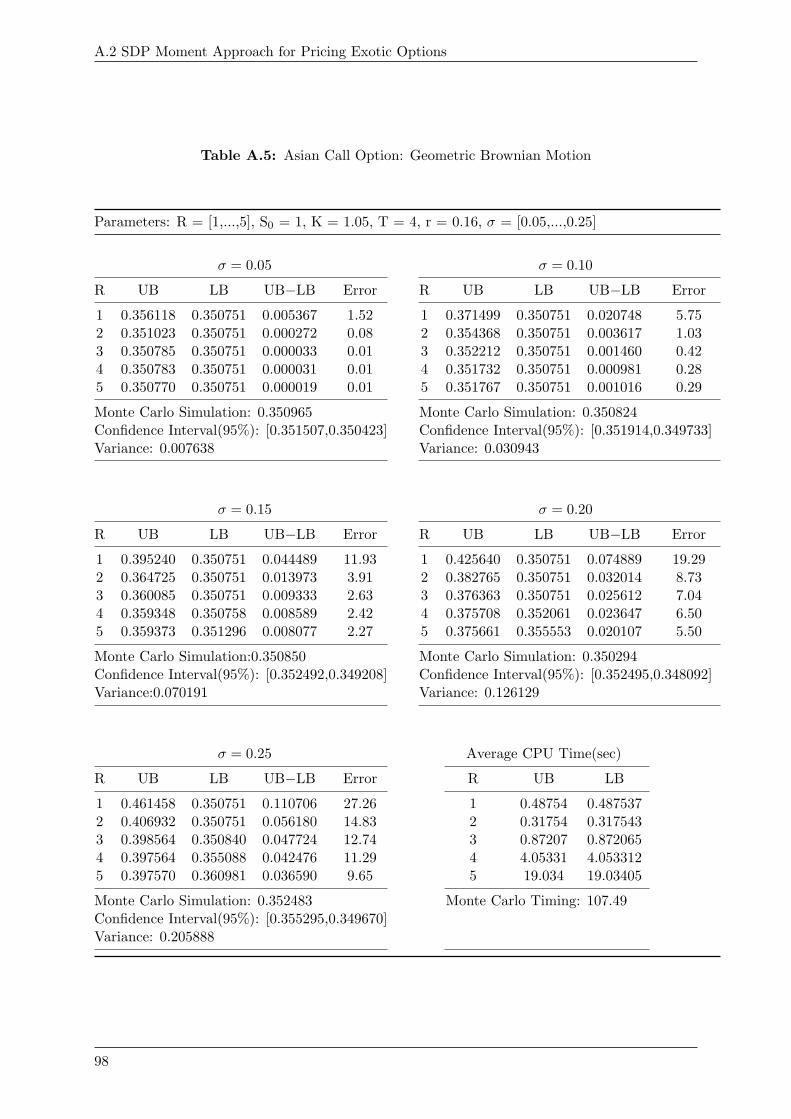

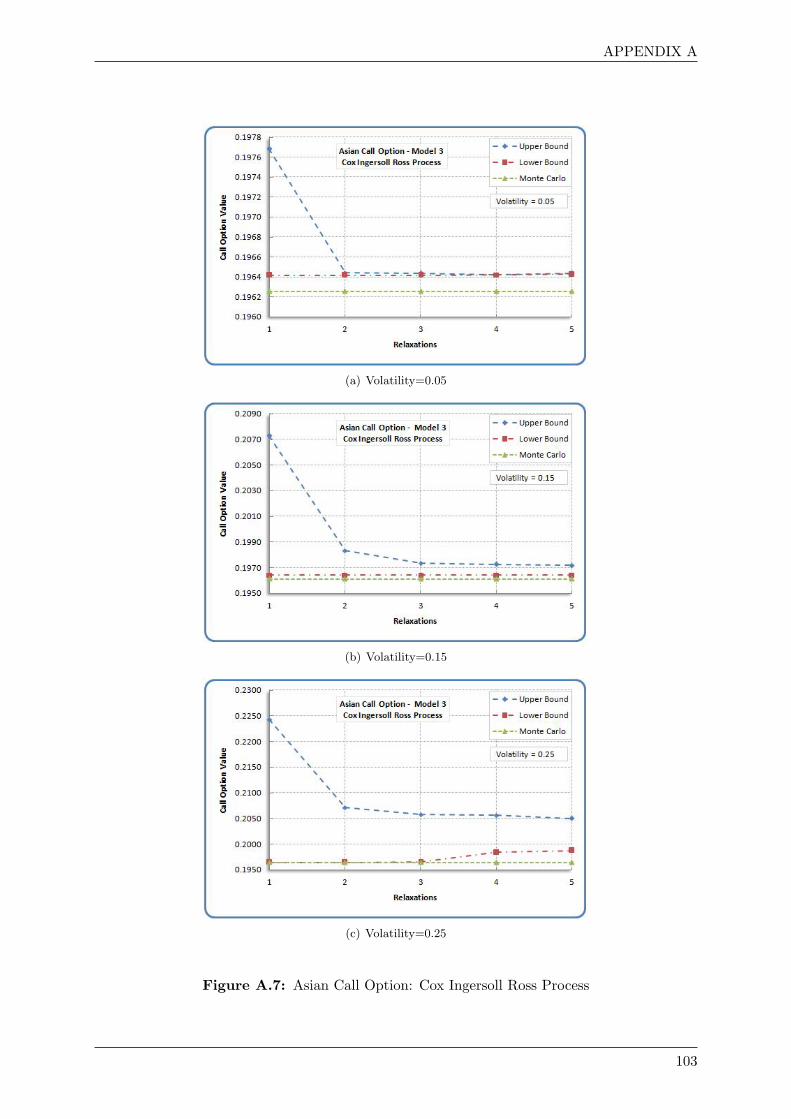

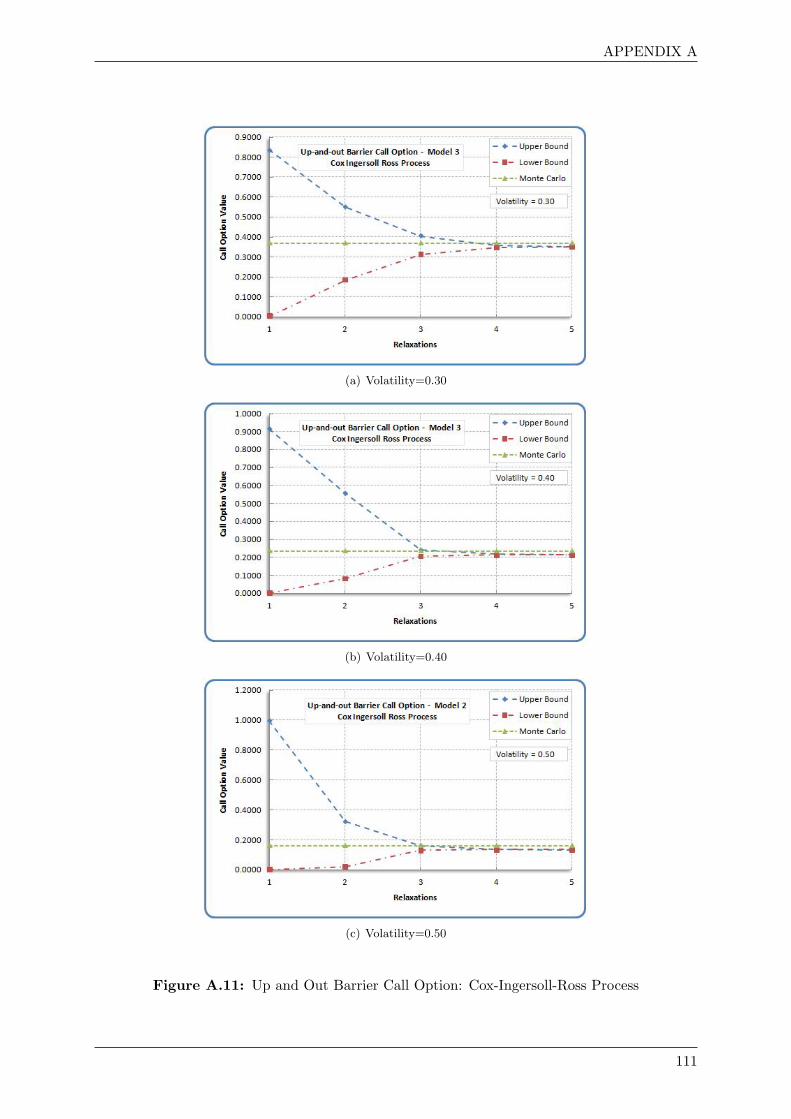

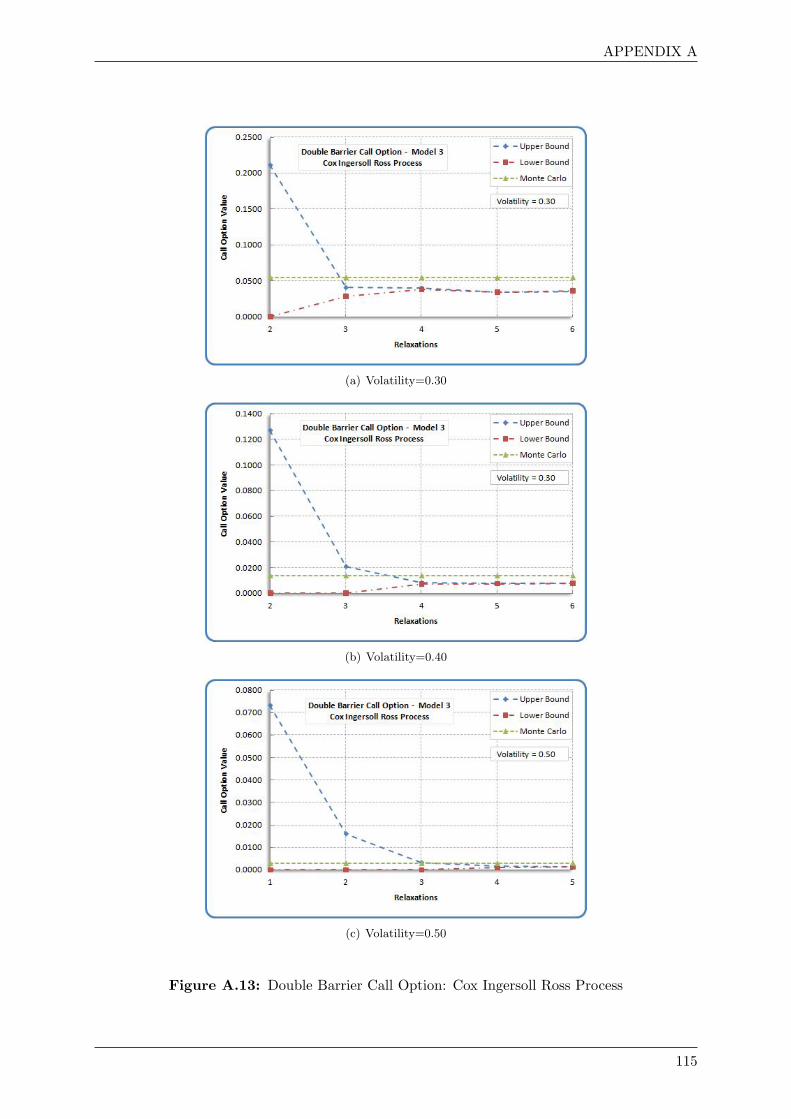

A.1 Semi-parametric Approach, European Call Option: Geometric Brownian Motion 91A.2 European Call Option: Geometric Brownian Motion . . . . . . . . . . . . . . . . 93A.3 European Call Option: Ornstein-Uhlenbeck Process . . . . . . . . . . . . . . . . 95A.4 European Call Option: Cox Ingersoll Ross Process . . . . . . . . . . . . . . . . . 97A.5 Asian Call Option: Geometric Brownian Motion . . . . . . . . . . . . . . . . . . 99A.6 Asian Call Option: Ornstein Uhlenbeck Process . . . . . . . . . . . . . . . . . . . 101A.7 Asian Call Option: Cox Ingersoll Ross Process . . . . . . . . . . . . . . . . . . . 103A.8 Down and Out Barrier Call Option: Ornstein Uhlenbeck Process . . . . . . . . . 105A.9 Down and Out Barrier Call Option: Cox Ingersoll Ross Process . . . . . . . . . . 107A.10 Up and Out Barrier Call Option: Ornstein Uhlenbeck Process . . . . . . . . . . . 109A.11 Up and Out Barrier Call Option: Cox-Ingersoll-Ross Process . . . . . . . . . . . 111A.12 Double Barrier Call Option: Ornstein Uhlenbeck Process . . . . . . . . . . . . . 113A.13 Double Barrier Call Option: Cox Ingersoll Ross Process . . . . . . . . . . . . . . 115

vi

List of Tables

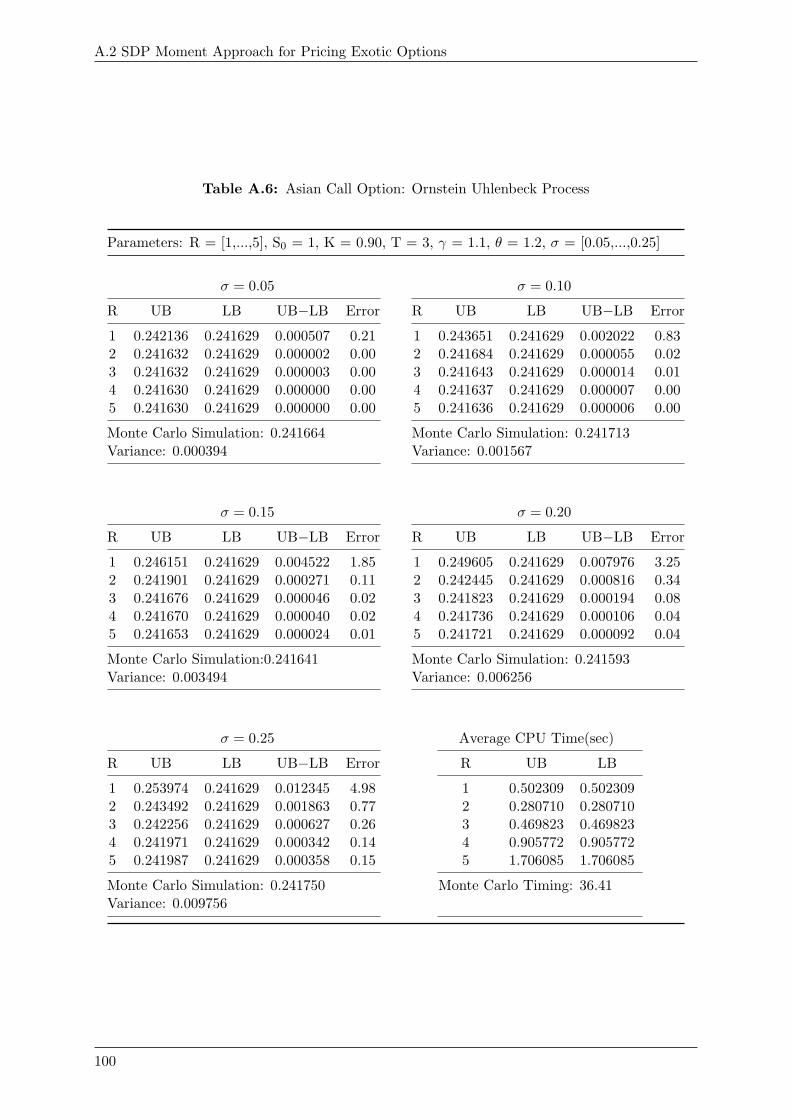

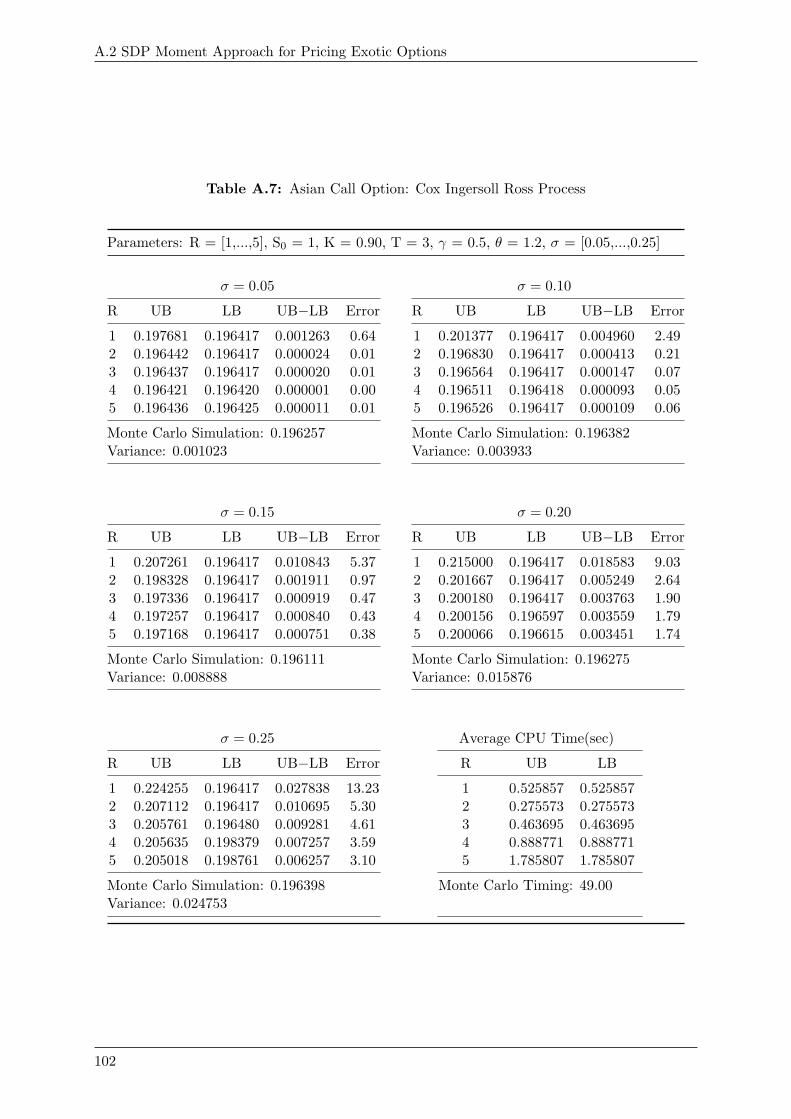

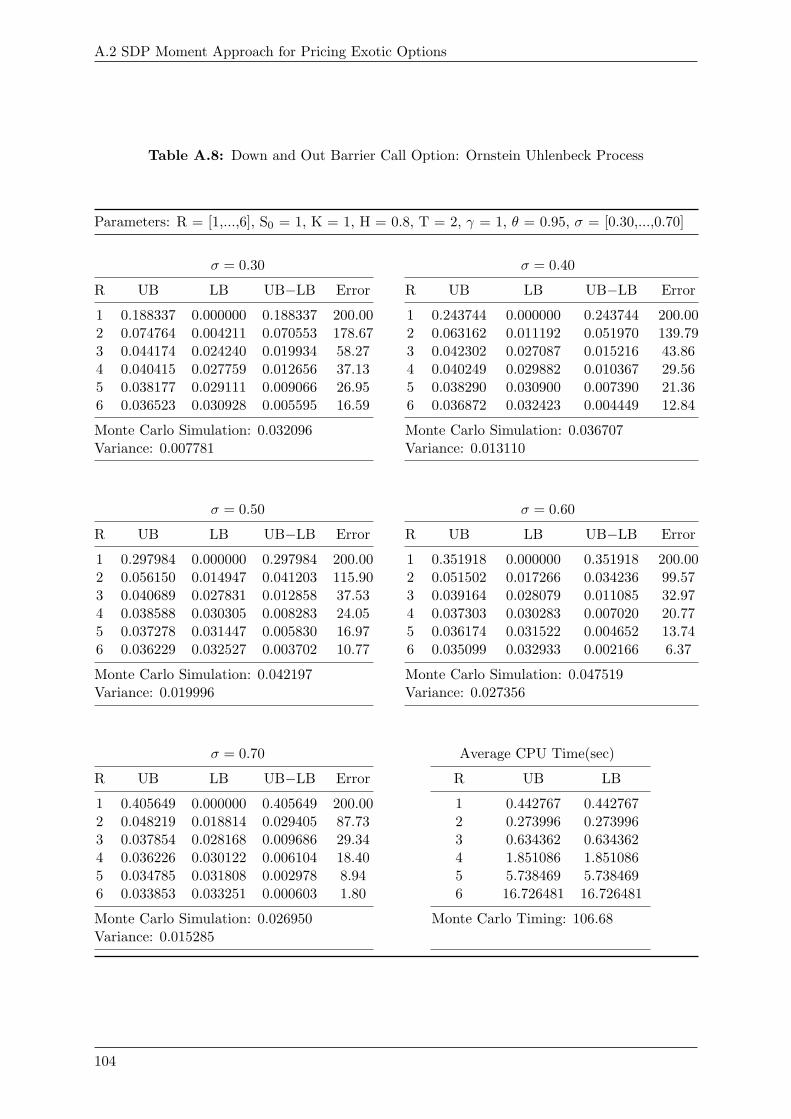

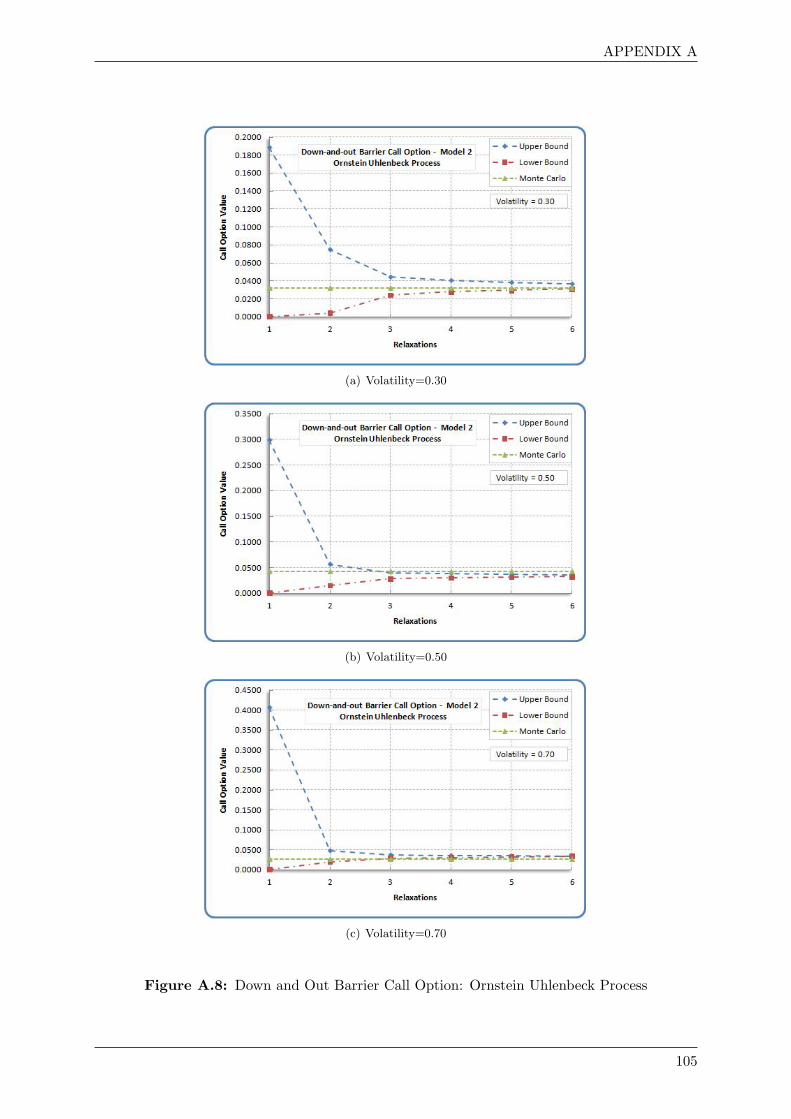

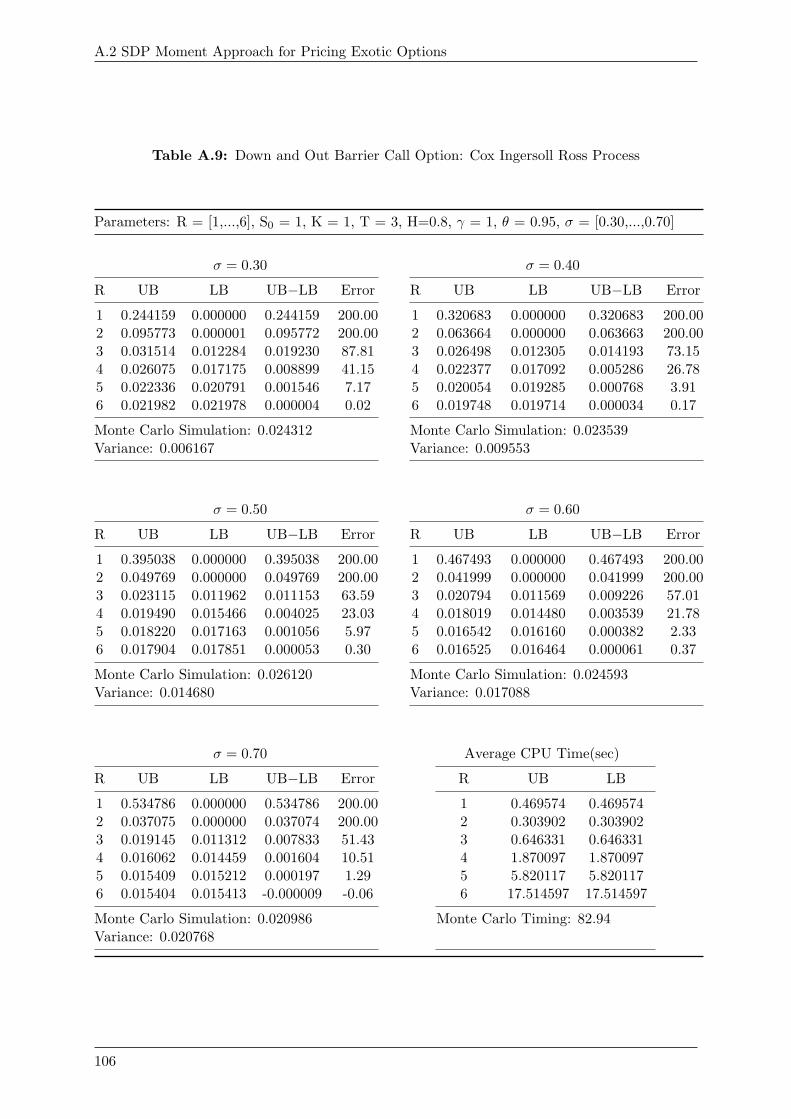

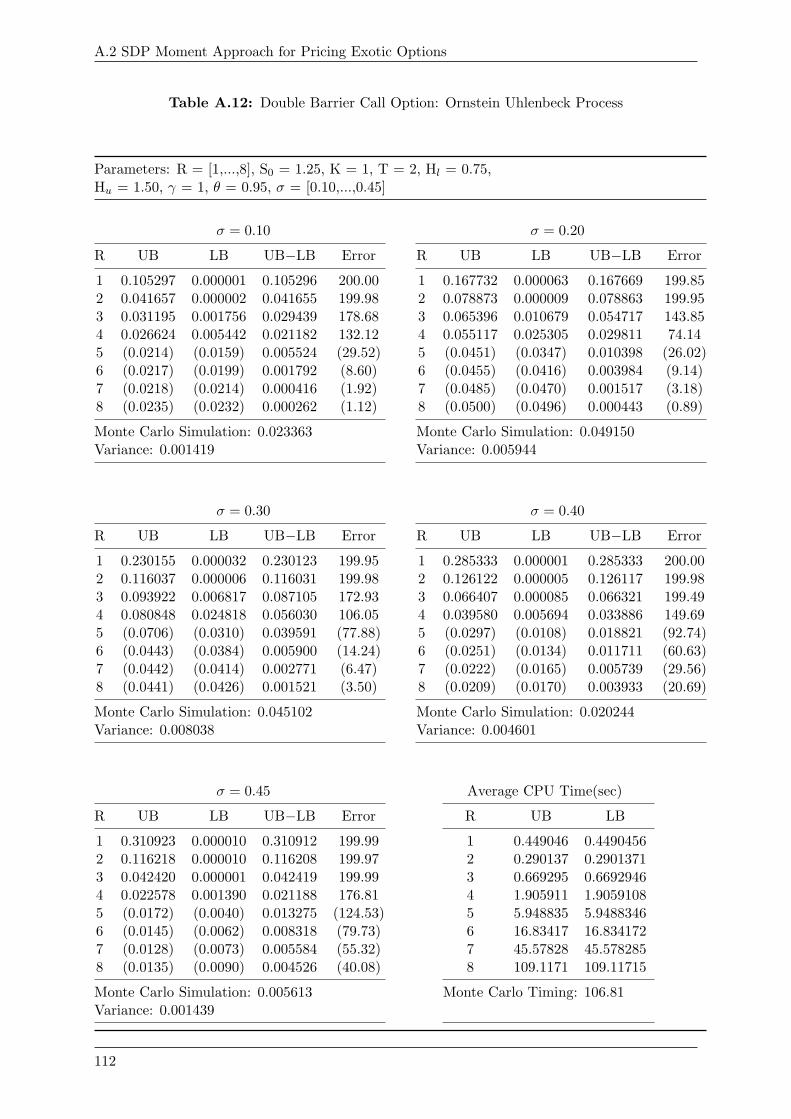

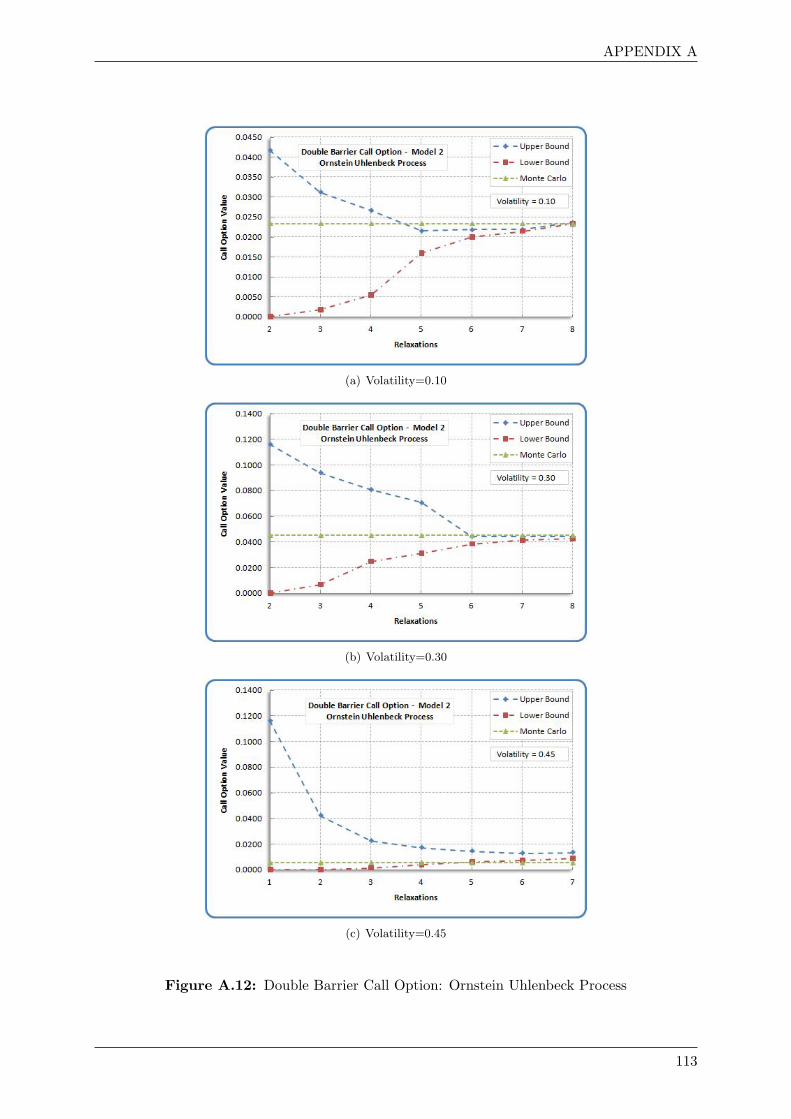

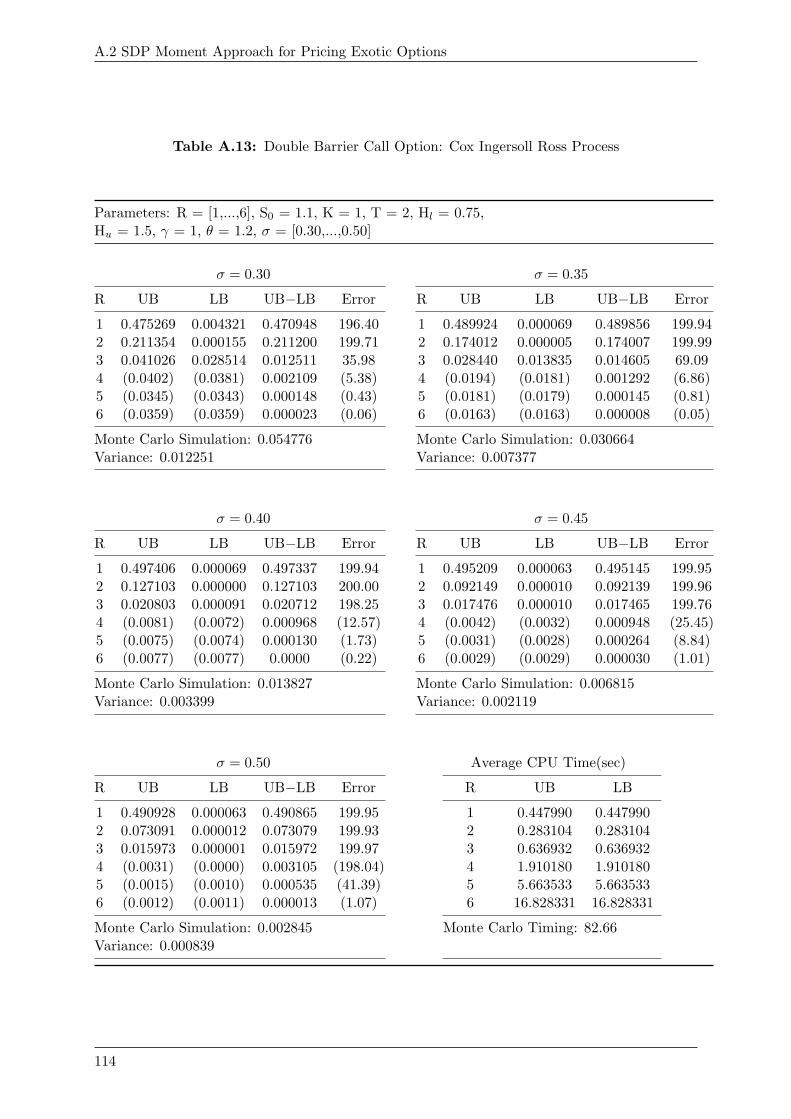

A.1 European Call Option Values: Geometric Brownian Motion . . . . . . . . . . . . 90A.2 European Call Option Values: Geometric Brownian Motion . . . . . . . . . . . . 92A.3 European Call Option Values: Ornstein-Uhlenbeck Process . . . . . . . . . . . . 94A.4 European Call Option: Cox Ingersoll Ross Process . . . . . . . . . . . . . . . . . 96A.5 Asian Call Option: Geometric Brownian Motion . . . . . . . . . . . . . . . . . . 98A.6 Asian Call Option: Ornstein Uhlenbeck Process . . . . . . . . . . . . . . . . . . . 100A.7 Asian Call Option: Cox Ingersoll Ross Process . . . . . . . . . . . . . . . . . . . 102A.8 Down and Out Barrier Call Option: Ornstein Uhlenbeck Process . . . . . . . . . 104A.9 Down and Out Barrier Call Option: Cox Ingersoll Ross Process . . . . . . . . . . 106A.10 Up and Out Barrier Call Option: Ornstein Uhlenbeck Process . . . . . . . . . . . 108A.11 Up and Out Barrier Call Option: Cox Ingersoll Ross Process . . . . . . . . . . . 110A.12 Double Barrier Call Option: Ornstein Uhlenbeck Process . . . . . . . . . . . . . 112A.13 Double Barrier Call Option: Cox Ingersoll Ross Process . . . . . . . . . . . . . . 114

vii

viii

Chapter 1

Introduction

An option is defined as a financial instrument that gives its holder the right, but not the obliga-tion, to buy (call option) or sell (put option) a predefined underlying security at a set exerciseprice at a specified maturity date. Options are a form of derivative security, as they derivetheir values from their underlying asset. An example of a very common option is a single assetoption which consists of one underlying asset, for example stock option which includes a definednumber of shares in a listed public company.

There are several types of options, differentiated on the basis of maturity date, the methodof pay off calculation, etc. For example, European options can only exercised at the maturitydate, as compared to American option which may be exercised on any trading day on orbefore expiration. Other type of options include Bermudan option which may be exercised onlyon specified dates on or before expiration and Barrier option which depends on underlyingsecurity’s price reaching some barrier before the exercise can occur. Although above type ofoptions are most common, they are not exhaustive. There are several numerical variations onthe basic design of above options for control of risk as perceived by investors and which easesexecution and book keeping.

Based on the concept of risk neutral pricing and using stochastic calculus, variety of numericalmodels and methodologies have been used to determine the theoretical value of an option. Intheir pioneering Noble Prize winning work, Fischer Black and Myron Scholes devised the firstquantitative model (called Black-Scholes option pricing model in [3]) for pricing of a varietyof simple option contracts. The basis if their technique was Black-Scholes partial differentialequation (PDE) which must be satisfied by the price of any derivative dependent on a nondividend paying stock. By creating a risk neutral portfolio that replicates the returns of holdingan option, a closed-form solution for an European option’s theoretical price was obtained.

However, it was discovered that the Black-Scholes model made several assumptions whichlead to non eligible pricing biases. Two important tenets on which Black-Scholes model was builtwere that there were no-arbitrage opportunities, and that the underlying asset (stock) followeda geometric Brownian motion. However, it is well known and proved that stock prices do notfollow geometric Brownian motion(for example, see [14]). Therefore, there has been researchinto pricing models that do not have the underlying log-normal distribution assumption.

1.1 Two Recent Methodologies

Recently, there have been approaches using semidefinite programming to derive bounds basedon the moments of the underlying asset price. An excellent introduction to semidefinite pro-gramming is given by Vandenbergh in [28] and for a detailed reference, reader is encouraged torefer [28]. It has been shown that bounds on the option prices can be derived from only theno-arbitrage assumption(see [22]).

In [22], Lo derived a distribution-free upper bound on single call and put options given the

1

1.1 Two Recent Methodologies

mean and variance of the underlying asset price. These bounds were termed as semi-parametricbecause they depended only on the mean and variance of the terminal asset price and not itsentire distribution. In [4], Boyle and Lin extended Lo’s result to the multi-asset case where theyutilized the correlations between the assets for determining the upper bound of a call option.It is to be noted that in both Lo’s and Boyle and Lin’s approach, the assumption that price ofunderlying asset following a lognormal distribution is not required and hence the upper boundsachieved are distribution-free. Using mean and covariance matrix of the underlying asset prices,Boyle and Lin show that the upper bound can be achieved by solving the associated SDP (solvedby an interior point algorithm).

Extending Boyle and Lin’s work, Bertsimas and Popescu, in [2] and [1], developed a distribution-free tight upper bound on a standard single asset option, given the first n moments of the un-derlying asset price. They also showed that this upper bound can be found by solving it as anSDP problem.

Subsequently, the work of Bertsimas and Popescu was extended by Gotoh and Konno in[9], by finding a tight lower bound for a single asset option by solving another SDP problem.They solved the SDP problem with a cutting plane algorithm which they presented in [8], anapproach similar to what was developed in [11]. The central idea of their algorithm was toview a semidefinite programming problem as a linear program with an infinite number of linearconstraints. They achieved impressive numerical results in real time and derived upper andlower bounds which were extremely close to the actual option price, especially as the number ofmoments became large, i.e. n ≥ 4.

In [10], Han, Li and Sun generalized the above two approaches, to find tight upper bound ofthe price of a multi-asset European call option by solving a sequence of semidefinite programmingproblems. In particular their work generalized Boyle and Lin’s work as they have first n momentsrather than only two moments. Their work also generalized Bertsimas and Popescu’s and Gotohand Konno’s work as they derive the bounds for multi-assets and not single assets. Their resultsshowed that as the dimension of the semidefinite relaxations increases, the bound becomes moreaccurate and converges to the tight bound.

In a related approach, we also choose to extend and reimplement the work done by Lasserre,Prieto-Rumeau and Zervos in [21]. In their original paper, the authors focus on fixed-strike,arithmetic average Asian and down-and-out Barrier options. The underlying asset price dynam-ics in their model is not restricted to geometric Brownian motion, as their model is applicableto number of other diffusions with a special property. Their technique is based on methodologyof moments introduced by Dawson in [7] for solving measure-valued martingale problems whichrepresented geostochastic systems.

In brief, the technique is described as follows. The price of an exotic option has to be iden-tified with a linear combination of moments of appropriately defined probability measures. Inthe next step, an infinite system of linear equations is derived using the martingale property ofassociated stochastic integrals. These infinite linear equations involve the moments of associ-ated measures as its variables. In order to solve this infinite dimensional linear problem, finitedimensional semidefinite relaxations are obtained by involving only finite number or moments.This is done by introducing extra constraints called moment conditions (in form of Moment andLocalizing matrices) which reflect necessary conditions for a set of scalars to be identified withmoments of a measure supported on a given set. The approach of using SDP relaxations andproblem of moments was introduced by Lasserre in [18] for global optimization of polynomials.The authors have given their own reference implementation, a MATLAB software GloptiPolyin [21], which in turn used SeDuMi as the underlying SDP solver developed in [16].

2

1 Introduction

1.2 Contributions

The major contributions and achievements of this project are summarised below.

• We develop and elaborate the theory for the two recently proposed methodologies, specif-ically for semi-parametric approach by Gotoh and Konno in chapter 3 and for method ofmoments and SDP relaxations by Lasserre, Prieto-Rumeau and Zervos in chapter 4.

• The theory of semi-parametric approach is handled with more detailed explanations inchapter 3 than given originally by Gotoh and Konno in [9].

• The theory given by Lasserre, Prieto-Rumeau and Zervos is extended to develop the SDPproblems for pricing European, up-and-out and double Barrier options in chapter 4.

• The theory in chapter 4 also includes explanation for problem of moments and SDP re-laxations for global optimization of polynomials.

• While developing the theory in chapter 4, we also correct several minor errors which werepresent in the original paper [21] by Lasserre, Prieto-Rumeau and Zervos.

• The numerical methodology given by Gotoh and Konno was reimplemented and associatedSDP problems were solved using our own programs directly, without using their CuttingPlane algorithm. The detailed numerical results are analysed in section 5.2 and appendixA.

• The SDP problems obtained in chapter 4 were solved using our own reference implemen-tation for pricing following 5 type of options: European, Asian and (down-and-out, up-and-out and double) Barrier options. The comprehensive numerical results are analysedin section 5.1 and appendix A.

• In chapter 2, we introduce the type of options and the underlying asset price processesconsidered in this project. We also have a look at some of the standard option pricingtechniques such as Monte Carlo methods, and present several analytical formulae basedon Black-Scholes PDE for calculating option prices.

• Finally, we analyse and compare the above two methods for efficiency and accuracy withother standard option pricing techniques such as Monte Carlo methods in detail, in chapter5 and present our conclusions in chapter 6.The comprehensive data obtained from numer-ical experiments done with the two approaches developed in chapters 3 and 4, is listed inAppendix A in tabular and graphical format.

3

Chapter 2

Options and Valuation Techniques

In this section, we present the options on which our analysis focuses in this project. We alsointroduce the standard analytical and numerical techniques used for pricing those options. Weuse these techniques for comparison with the two approaches (semi-parametric approach andmethod of moments with SDP relaxations) which we introduce and implement in later chapters.Specifically, we introduce the type of options in section 2.1 briefly. Then we explain the typeof underlying asset price diffusions in section 2.2 along with analytical solution of geometricBrownian motion and Ornstein Uhlenbeck process. We then introduce the Monte Carlo methodsfor pricing European, Asian and Barrier Options in section 2.3. Finally, the Black-Scholesframework and analytical formulas for pricing call and put versions of European and (down-and-out and up-and-out) Barrier options are explained in section 2.4.

2.1 Class of Options

An option is a contract, or a provision of a contract, that gives one party (the option holder) theright, but not the obligation, to perform a specified transaction with another party (the optionissuer or option writer) according to specified terms. Option contracts are a form of derivativeinstrument and could be linked to a variety of underlying assets, such as bonds, currencies,physical commodities, swaps, or baskets of assets.

Options take many forms. The two most common are:

1. Call options, which provide the holder the right to purchase an underlying asset at aspecified price;

2. Put options, which provide the holder the right to sell an underlying asset at a specifiedprice.

In the next few sections, we introduce the three category of options which we interact within this project: European, Asian and Barrier options.

2.1.1 European Options

The strike price of a call (put) option is the contractual price at which the underlying asset willbe purchased (sold) in the event that the option is exercised. The last date on which an optioncan be exercised is called the expiration date and it can be categorised in two types as below,on the basis of exercise time:

1. With American exercise, the option can be exercised at any time up to the expiration date.

2. With European exercise, the option can be exercised only on the expiration date.

4

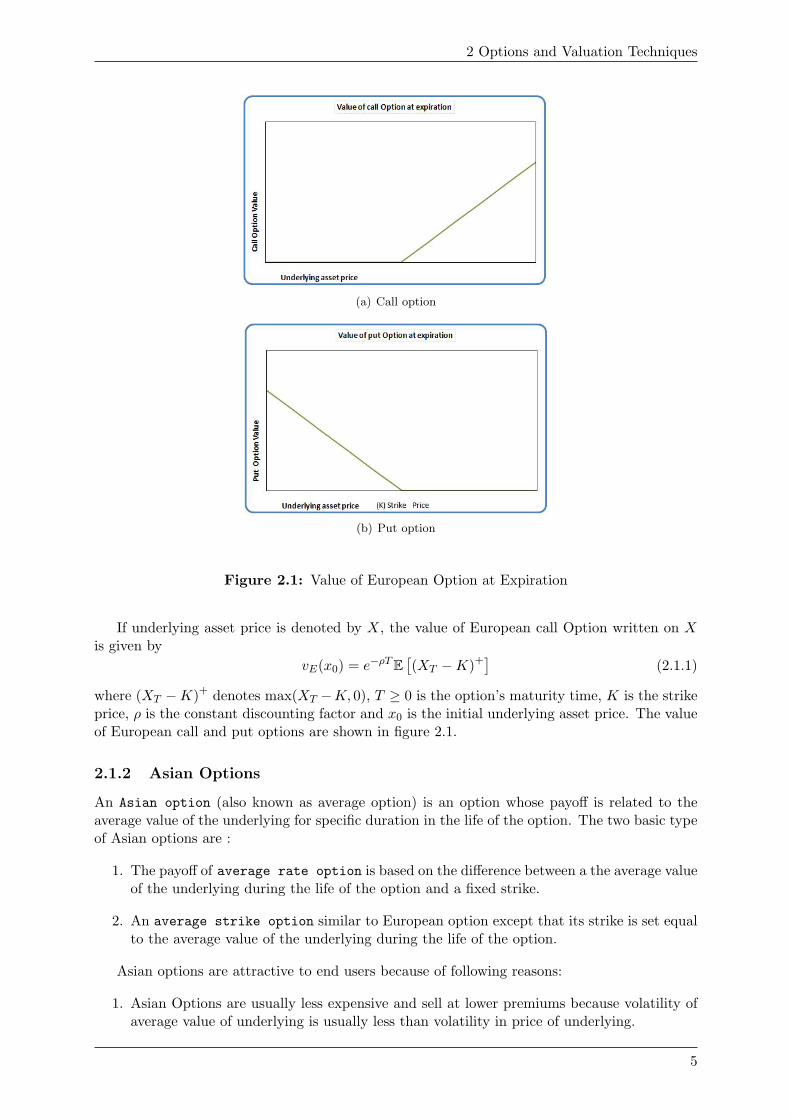

2 Options and Valuation Techniques

(a) Call option

(b) Put option

Figure 2.1: Value of European Option at Expiration

If underlying asset price is denoted by X, the value of European call Option written on Xis given by

vE(x0) = e−ρTE[(XT −K)+

](2.1.1)

where (XT −K)+ denotes max(XT −K, 0), T ≥ 0 is the option’s maturity time, K is the strikeprice, ρ is the constant discounting factor and x0 is the initial underlying asset price. The valueof European call and put options are shown in figure 2.1.

2.1.2 Asian Options

An Asian option (also known as average option) is an option whose payoff is related to theaverage value of the underlying for specific duration in the life of the option. The two basic typeof Asian options are :

1. The payoff of average rate option is based on the difference between a the average valueof the underlying during the life of the option and a fixed strike.

2. An average strike option similar to European option except that its strike is set equalto the average value of the underlying during the life of the option.

Asian options are attractive to end users because of following reasons:

1. Asian Options are usually less expensive and sell at lower premiums because volatility ofaverage value of underlying is usually less than volatility in price of underlying.

5

2.1 Class of Options

2. Asian options offer protection, as manipulation in price of underlying asset is not possibleover prolonged period of time.

3. End users of commodities which tend to be exposed to average prices over time find Asianoptions useful.

If underlying asset price is denoted by X, the value of fixed strike arithmetic-average Asiancall option written on X is given by

vA(x0) = e−ρTE

[(1T

∫ T

0XTdt−K

)+]

(2.1.2)

where (X − Y )+ denotes max(X − Y, 0), T ≥ 0 is the option’s maturity time, K is the strikeprice, ρ is the constant discounting factor and x0 is the initial underlying asset price.

2.1.3 Barrier Options

A barrier option is a path dependent option that has one of the following two features:

1. A knock-out feature causes the option to immediately terminate if the underlying asset’sprice reaches a specified (upper or lower) barrier level, or

2. A knock-in feature causes the option to become effective only if the underlying asset’sprice first reaches a specified (upper or lower) barrier level.

Hence for a simple Barrier option, we can derive eight different flavours, i.e. put and call foreach of the following:

1. Up and in

2. Down and in

3. Up and out

4. Down and out

Due to the contingent nature of the option, they tend to be priced lower than for a correspondingvanilla option.

If underlying asset price is denoted by X, the value of Barrier call option written on X isgiven by

vA(x0) = e−ρTE[(XT −K)+ Iτ=T

](2.1.3)

where (XT −K)+ denotes max(XT −K, 0), T ≥ 0 is the option’s maturity time, K is the strikeprice, ρ is the constant discounting factor, x0 is the initial underlying asset price and τ is the(Ft)-stopping time defined by

τd = inf t ≥ 0|Xt ≤ Hl ∧ Tτu = inf t ≥ 0|Xt ≥ Hu ∧ Tτc = inf t ≥ 0|Xt ≤ Hl ∧Xt ≥ Hu ∧ T

(2.1.4)

for down-and-out, up-and-out and double Barrier options, respectively, and Hl, Hu are lowerand upper knock-out barriers. As an example, the value of down-and-out Barrier call option isshown in figure 2.2.

6

2 Options and Valuation Techniques

(a) Down-and-Out Call option

Figure 2.2: Value of Barrier Call Option

2.2 Models for Underlying Asset Price

Given the filtered probability space, (Ω,F ,Ft,P), where Ω is given sample space , σ-algebra Fof subsets of Ω, a measure P on (Ω,F), such that P (Ω) = 1 and a filtration Ft on F . For thisproject we will consider that the underlying asset prices of derivatives, which we mentioned inprevious section, would satisfy the stochastic differential equation:

dXt = b (Xt) dt+ σ (Xt) dWt, X0 = x0 ∈ I (2.2.1)

where Wt is the Wiener process, I is either (0,+∞) or R and b, σ : I → I are given functions andwhich enable equation (2.2.1) to have a strong1 solution contained in I, for all t ≥ 0, probabilityalmost surely.

Specifically, for this project, we assume that underlying asset price X is given by three mod-els: geometric Brownian motion, Ornstein-Uhlenbeck process and Cox-Ingersoll-Ross processwhich are termed as Model 1, Model 2 and Model 3, respectively in this project. We describeeach of above diffusions in detail in following sections and give analytical formula for solutionof geometric Brownian motion and Ornstein Uhlenbeck process.

Before proceeding to next section, we note that any diffusions, other than the ones mentionedabove, could be considered aptly for analysis of numerical methodology proposed by Lasserre,Prieto-Rumeau and Zervos in [21] provided that they satisfy this important assumption: theinfinitesimal generator of this diffusion should map polynomials into polynomials of same orsmaller degree.

2.2.1 Geometric Brownian Motion

A continuous-time stochastic process in which the logarithm of the randomly varying quantityfollows a Brownian motion, or a Wiener process is called geometric Brownian motion(GBM).In other words, a stochastic process Xt is said to follow a GBM, if it satisfies the followingstochastic differential equation:

dXt = µXtdt+ σXtdz (2.2.2)

where dz = ε(t)√dt is a Wiener process, ε(t) is a standardized normal random variable, µ is

called as the percentage drift and σ is called the percentage volatility.

1Compared to weak solution which consists of a probability space and a process that satisfies the SDE, astrong solution is a process that satisfies the equation and is defined on a given probability space.

7

2.2 Models for Underlying Asset Price

We will now derive an analytical formula for XT , the price of underlying asset at time T ,when we are given X0 and other parameters of GBM. Now Ito’s Lemma states that for a randomprocess x defined by the Ito process

dx(t) = a(x, t)dt+ b(x, t)dz (2.2.3)

where z is a standard Wiener process, process y(t) defined by y(t) = F (x, t) satisfies the Itoequation

dy(t) =(a∂F

∂x+∂F

∂t+ b2

12∂2F

∂x2

)dt+ b

∂F

∂xdz (2.2.4)

where z is the same Wiener process in (2.2.2).

If we apply Ito’s Lemma to the process F (X(t)) = lnXt, then we identify

a = µX, b = σX,∂F

∂X=

1X, and

∂2F

∂X2= − 1

X2

Substituting these values in (2.2.4), we get

d lnX =(a

X− 1

2b2

X2

)dt+

b

Xdz

=(µ− 1

2σ2

)dt+ σdz

(2.2.5)

Ito-integrating both sides, we get

ln (Xt)− ln (X0) =(µ− 1

2σ2

)(t− 0) + σdz

⇔ Xt = X0e(µ− 1

2σ2)4t+σdz

(2.2.6)

or finally, using the fact that dz = ε(t)√4t for a Wiener process.

Xt = X0e(µ− 1

2σ2)4t+σε(t)

√4t, ε(t) ∼ N(0, 1) (2.2.7)

2.2.2 Ornstein-Uhlenbeck Process

The diffusion Xt governed by following stochastic differential equation,

dXt = γ(θ −Xt)dt+ σdz (2.2.8)

where dz = ε(t)√dt is a Wiener process and ε(t) is a standardized normal random variable, is

known as Ornstein-Uhlenbeck process. The parameters of this diffusion are γ ≥ 0 which isthe rate of mean reversion, θ which is the long term mean of the process and σ is the volatilityor average magnitude, per square-root time, of the random fluctuations that are modelled asBrownian motions. The Vasicek one-factor equilibrium model of interest rates described in [24]is an example which involves Ornstein-Uhlenbeck process.

Ornstein Uhlenbeck process has an important property called mean reversion property. Wecan see thatXt has an overall drift towards the mean value θ, if we ignore the random fluctuationsin the process due to dz. The rate of reversion of diffusion Xt to mean θ is at an exponentialrate γ, and magnitude directly proportional to the distance between the current value of Xt andθ.

8

2 Options and Valuation Techniques

We can also observe that for any fixed T , the random variable XT , conditional upon X0, isnormally distributed with

mean = θ + (X0 − θ)e−γT

variance =σ2

2γ(1− e−2γT )

(2.2.9)

We will now derive an analytical formula for XT , the price of underlying asset at time T , aswe did for geometric Brownian motion, when we are given X0 and other parameters of OrnsteinUhlenbeck process. Introducing the change of variable Yt = Xt−θ, then Yt satisfies the equation

dYt = dXt = −γYtdt+ σdz (2.2.10)

In (2.2.8), Yt shows a drift towards the value zero, at exponential rate γ, hence we introducethe change of variable

Yt = e−γtZt ⇔ Zt = eγtYt (2.2.11)

which eliminates the drift. Now applying the product rule for Ito Integrals we obtain

dZt = γeγtYtdt+ eγtdYt

= γeγtYtdt+ eγt(−γYtdt+ σdz)= 0dt+ σeγtdz

(2.2.12)

Ito-Integrating both sides from 0 to t we get

Zt = Z0 + σ

∫ t

0eγzdz (2.2.13)

Next step would be to reverse the change of variables to obtain

Yt = e−γtZt

= e−γ(t−0)Y0 + σe−γt∫ t

0eγzdz

= e−γtY0 + σ

∫ t

0e−γ(t−z)dz

(2.2.14)

thus we obtain original variable Xt as

Xt = θ + Yt

= θ + e−γt(X0 − θ) + σ

∫ t

0e−γ(t−z)dz

(2.2.15)

which can further be simplified to

Xt ∼ θ + e−γt(X0 − θ) + σ

√1− e−2γt

2γε(t), ε(t) ∼ N(0, 1) (2.2.16)

2.2.3 Cox Ingersoll Ross process

In the Vasicek model which involves Ornstein-Uhlenbeck process (2.2.8), the short term interestrate Xt, can become negative. To overcome this drawback, an alternative one-factor equilibriummodel was proposed by Cox, Ingersoll and Ross in [15] for short term or instantaneous interestrate in which rates would always remain positive.

9

2.3 Monte Carlo Methods

Specifically, a diffusion (short-term or instantaneous interest rate in Cox-Ingersoll-Ross in-terest rate model) which satisfies the following stochastic differential equation

dXt = γ(θ −Xt)dt+ σ√Xtdz (2.2.17)

where dz = ε(t)√dt is a Wiener process and ε(t) is a standardized normal random variable,

is known as Cox-Ingersoll-Ross process. The parameters of this diffusion are same as theones in Ornstein-Uhlenbeck process except the fact that the standard deviation factor, σ

√Xt

does not allow the interest rate Xt to become negative. Hence we observe that, when the valueof Xt is low, the standard deviation becomes close to zero, in turn cancelling the effect of therandom shock on the interest rate. We also note that γθ ≥ 1

2σ2 is necessary and sufficient for

non explosiveness of solution of (2.2.17), or in other words, for instantaneous rate to assume thevalue zero at infinite time with probability 1.

2.3 Monte Carlo Methods

Considering valuation of an option as computing its expected value, we can use repeated randomsampling in order to compute this expected value. Monte Carlo methods are a class of algorithmswhich could be used for such repeated random sampling and thus calculating the expected valueof the derivative price. We describe Monte Carlo algorithms for pricing European options insection 2.3.1, Asian Options in section 2.3.2 and (down-and-out and up-and-out) Barrier optionsin section 2.3.3. Also note that, although the Monte Carlo methods in this section are given forgeometric Brownian motion only, they can be adapted very easily for Ornstein-Uhlenbeck andCox-Ingersoll-Ross diffusions.

2.3.1 European Options

In this section we will give Monte Carlo algorithm for valuation of European put and call options.Pseudo random number generators can be used to compute the estimates of expected values.Consider an European style option with payoff which is some function F of asset price Xt. Nowwe get the model of asset price to be described by geometric Brownian motion (2.2.2), and usingthe risk neutrality approach, option value can be found by calculating e−rTF (XT ), or in otherwords, we intend to calculate

e−rTF (X0e(µ− 1

2σ2)dt+σε(t)

√dt) (2.3.1)

where ε(t) ∼ N(0, 1).The resulting Monte Carlo algorithm can be described as below

10

2 Options and Valuation Techniques

Algorithm 1: Monte Carlo method for valuation of European options

Data: Initial stock price X0,strike price K, risk-free rate r, expiration time T , volatilityσ, sample size M , path size N

Result: Call and put value of European optionbegin

// Step 0: InitializationsSet callValue = 0Set putValue = 0// Step 1: Compute samplesfor i = 1 to M do

Compute an N(0,1) sample εiSet Xi = X0e

(µ− 12σ2)dt+σ

√dtεi

Set Vi = e−rTF (Xi)// Step 2, Calculate option value

Set V = 1M

∑Mi=1 Vi

if V ≥ K thenSet callValue = V −K

elseSet putValue = K − V

// Step 3, Calculate approximately 95 % confidence intervals

Set B = 1M−1

∑Mi=1(Vi − V )2

Set Confidence Interval =[V − 1.96B√

M, V + 1.96B√

M

]end

2.3.2 Asian Options

In the previous algorithm, we were interested in option price XT at time T , where as for Asianoptions, we need to calculate the average of all the values taken by the option price betweentime 0 and T . This is evident from the Monte Carlo algorithm which we have described belowfor pricing an Asian option (of type average strike).

11

2.3 Monte Carlo Methods

Algorithm 2: Monte Carlo method for valuation of Asian option

Data: Initial stock price X0,strike price K, risk-free rate r, expiration time T , volatilityσ, sample size M , path size N

Result: Call and put values of Asian optionbegin

// Step 0: InitializationsSet callValue = 0Set putValue = 0Set 4T = T

N−1Set XInc = X0 * Array(M)Set XPathArray = X0 * Array(M)// Step 1: Compute samplesfor i = 1 to N − 1 do

for j = 1 to M doCompute an N(0,1) sample εjSet XIncj = XIncje(µ−

12σ2)dt+σ

√4Tεj

Set XPathArrayj = XPathArrayj + XIncj

for i = 1 to M do

Set Xmeani =

XPathArrayiN

Set Vi = e−rTmax(K −Xmeani , 0)

// Step 2, Calculate option value

Set V = 1M

∑Mi=1 Vi

if V ≥ K thenSet callValue = V −K

elseSet putValue = K − V

// Step 3, Calculate approximately 95 % confidence intervals

Set B2 = 1M−1

∑Mi=1(Vi − V )2

Set ConfidenceInterval =[V − 1.96B√

M, V + 1.96B√

M

]end

2.3.3 Barrier Options

In the Monte Carlo algorithm 3 given below, we describe the method for pricing put and callvalues for down-and-out Barrier options. Please note that the below mentioned algorithm is anmodified and more efficient version of algorithm taken from [6].

The above algorithm can easily adapted to price any kind of put and call Barrier options,from the eight categories mentioned in section 2.1.3. As an example, the Monte Carlo algorithm4 for double Barrier options is also given below:

12

2 Options and Valuation Techniques

Algorithm 3: Monte Carlo method for valuation of down-and-out Barrier option

Data: Initial stock price X0,strike price K, lower barrier HL, risk-free rate r, expirationtime T , volatility σ

Result: Put and call values of down-and-out Barrier optionbegin

// Step 0: InitializationsSet callValue = 0Set putValue = 0Set 4T = T

N−1Set XInc = X0 * Array(M)Set XPathArray = X0 * Array(M)Set BarrierBrokenFlag = 0 * Array(M)// Step 1: Compute samplesfor i = 1 to N − 1 do

for j = 1 to M doif BarrierBrokenFlagj 6= 1 then

Compute an N(0,1) sample εjSet XIncj = XIncje(µ−

12σ2)dt+σ

√4Tεj

if XIncj ≤ HL thenSet BarrierBrokenFlagj = 1Set XPathArrayj = 0

elseSet XPathArrayj = XPathArrayj + XIncj

for i = 1 to M do

Set Xmeani =

XPathArrayiN

Set Vi = e−rTmax(K −Xmeani , 0)

// Step 2, Calculate option value

Set V = 1M

∑Mi=1 Vi

if V ≥ K thenSet callValue = V −K

elseSet putValue = K − V

// Step 3, Calculate approximately 95 % confidence intervals

Set B2 = 1M−1

∑Mi=1(Vi − V )2

Set ConfidenceInterval =[V − 1.96B√

M, V + 1.96B√

M

]end

13

2.3 Monte Carlo Methods

Algorithm 4: Monte Carlo method for valuation of double Barrier options

Data: Initial stock price X0,strike price K, upper barrier HU , lower barrier HL, risk-freerate r, expiration time T , volatility σ

Result: Put and call values of double Barrier Optionbegin

// Step 0: InitializationsSet callValue = 0Set putValue = 0Set 4T = T

N−1Set XInc = X0 * Array(M)Set XPathArray = X0 * Array(M)Set BarrierBrokenFlag = 0 * Array(M)// Step 1: Compute samplesfor i = 1 to N − 1 do

for j = 1 to M doif BarrierBrokenFlagj 6= 1 then

Compute an N(0,1) sample εjSet XIncj = XIncje(µ−

12σ2)dt+σ

√4Tεj

if XIncj ≤ HL OR XIncj ≥ HU thenSet BarrierBrokenFlagj = 1Set XPathArrayj = 0

elseSet XPathArrayj = XPathArrayj + XIncj

for i = 1 to M do

Set Xmeani =

XPathArrayiN

Set Vi = e−rTmax(K −Xmeani , 0)

// Step 2, Calculate option value

Set V = 1M

∑Mi=1 Vi

if V ≥ K thenSet callValue = V −K

elseSet putValue = K − V

// Step 3, Calculate approximately 95 % confidence intervals

Set B2 = 1M−1

∑Mi=1(Vi − V )2

Set ConfidenceInterval =[V − 1.96B√

M, V + 1.96B√

M

]end

14

2 Options and Valuation Techniques

2.3.4 Advantages and Disadvantages of Monte Carlo Methods

Even though Monte Carlo algorithms are simple and elegant to implement, they have certainmerits and demerits of their own, as a class of algorithms which are enlisted below:

Advantages

• The major advantage of Monte Carlo methods is that they are very simple to implementand adapt. Usually an expression of solution or its analytical properties are not requiredfor performing Monte Carlo simulations.

• Owing to their genericity and simplicity in implementation, Monte Carlo methods offerunrestricted choice of functions for implementation.

• As Monte Carlo simulations intrinsically involve certain type of repetitive tasks, they canbe easily parallelized.

Disadvantages

• The most important drawback of Monte Carlo algorithms is that they are slow whenthe dimension of integration is low. We can prove that for Monte Carlo integration theprobabilistic error bound is inversely proportional to the square root of the number ofsamples, hence in order to achieve one more decimal digit of precision, we would require100 times more the number of samples.

• The probabilistic error bound is also dependent on variance. Hence it is not a goodrepresentation of the error when the underlying probability distributions are skewed.

• The error in values computed through Monte Carlo algorithms also depend on the un-derlying probability distributions. As we can consider that Monte Carlo methods tryto estimate the expectation of certain values by sampling, this estimated value may beerroneous, if the underlying probability distribution is heavily skewed or has heavier-than-normal tails. This disadvantage can be taken care of by using appropriate non-randomnumerical methods.

• As Monte-Carlo methods typically follow a Black-box approach, it is difficult to performsensitivity analysis for the input parameters, which would be otherwise possible withcertain types of analytical approximation techniques.

Effects of several of above disadvantages can be decreased there by increasing the accuracyof results in Monte Carlo simulations. For example, there are several techniques for reducingvariance in the sampled values, such as use of antithetic and control variates, importance sam-pling, etc. However, as these topics are not in the scope of this project, we will not elaborate onthem. Interested reader is encouraged to refer [25] for comprehensive treatment of Monte Carlomethods.

2.4 Black Scholes PDE and Analytical Solution

A mathematical model of market for equity was given by Black-Scholes, where the underlying isa stochastic process and the price of derivative on the underlying satisfies a partial differentialequation called Black-Scholes PDE. We briefly summarize the Black Scholes model, PDE andsolution formula obtained by solving the Black-Scholes PDE for European put and call optionsbelow. Suppose that underlying Xt is governed by geometric Brownian motion (2.2.2):

dXt = µXtdt+ σXtdz (2.4.1)

15

2.4 Black Scholes PDE and Analytical Solution

where dz = ε(t)√dt is a Wiener process and ε(t) is a standardized normal random variable.

Now let V be some sort of option on X, or in other words, consider V as a function of Xand t. Hence, V (X, t) is the value of the option at time t if the price of the underlying stock attime t is X. We also assume that V (X, t) is differentiable twice with respect to X and once withrespect to t. Then V (X, t) must satisfy the Black-Scholes partial differential equation:

∂V

∂t+ rX

∂V

∂X+ σ2X2 1

2∂2V

∂X2= rV (2.4.2)

where r is the interest rate.

2.4.1 Analytical Solution for European Options

By solving (2.4.2) for price of European call and put options(for solution techniques and moredetails please refer [14],[6] and [26]), we get

Ct = XtΦ(d1)−Ke−rTΦ(d2)

Pt = Ke−rTΦ(d2)−XtΦ(d1)(2.4.3)

where

d1 =ln

(Xt

K

)+ T

(r + σ2

2

)σ√T

d2 =ln

(Xt

K

)+ T

(r − σ2

2

)σ√T

= d1 − σ√T

Φ(dn) =1√2π

∫ dn

−∞e−

x2

2 dx

(2.4.4)

or in other words, Φ(.) is the standard normal cumulative distribution function.

2.4.2 Analytical Solution for Barrier Options

We present here the analytical formulae used in this project for comparison with bounds obtainedby following the numerical approach given by Lasserre, Prieto-Rumeau and Zervos in [21]. Bysolving (2.4.2) for price of different types of Barrier call and put options (for solution techniquesplease refer [27]), we get the following solutions:

Down-and-out and down-and-in call options:

When H ≤ K, we get

Cdit = X0

(H

X0

)2e1

Φ(e2)−Ke−rT(H

X0

)2e1−2

Φ(e2 − σ√T ) (2.4.5)

16

2 Options and Valuation Techniques

where

e1 =r + σ2

2

σ2

e2 =ln

[H2

X0K

]σ√T

+ e1σ√T

f1 =ln

(X0

H

)σ√T

+ e1σ√T

f2 =ln

(H

X0

)σ√T

+ e1σ√T

(2.4.6)

We also quote the known fact, that the sum of any type of out and in calls is equal to value ofregular call given in (2.4.3). Hence the value of down-and-out Barrier call option is given by

Cdot = Ct − Cdit (2.4.7)

On the other hand if H ≥ K, we have

Cdot = −X0Φ(f1)−Ke−rTΦ(f1 − σ√T )

−X0 (H/X0)2e1 Φ(f2)

+Ke−rT(H

X0

)2e1−2

Φ(f2 − σ√T )

(2.4.8)

andCdit = Ct − Cdot (2.4.9)

Up-and-out and up-and-in call options:When H ≥ K

Cuit = X0Φ(f1)−Ke−rTΦ(f1 − σ√T )

−X0

(H

X0

)2e1

[Φ(−e2)− Φ(−f2)]

+Ke−rT(H

X0

)2e1−2

[Φ(−e2 + σ√T )− Φ(f2 + σ

√T )]

(2.4.10)

andCuot = Ct − Cuit (2.4.11)

where as when H ≤ K,Cuot = 0 (2.4.12)

andCuit = Ct (2.4.13)

Up-and-out and up-and-in put options:When H ≤ K

P dit = −X0

(H

X0

)2e1

Φ(−e2) +Ke−rT(H

X0

)2e1−2

Φ(−e2 + σ√T ) (2.4.14)

17

2.4 Black Scholes PDE and Analytical Solution

andP uot = Pt − P uit (2.4.15)

where as when H ≤ K,

P uot = −X0Φ(f1) +Ke−rTΦ(−f1 + σ√T )

+X0

(H

X0

)2e1

Φ(−f2)

−Ke−rT(H

X0

)2e1−2

Φ(−f2 + σ√T )

(2.4.16)

andP uit = Pt − P uit (2.4.17)

Down-and-out and Down-and-in put options:When H ≥ K

P dit = −X0Φ(−f1) +Ke−rTΦ(−f1 + σ√T )

+X0

(H

X0

)2e1

[Φ(e2)− Φ(f2)]

−Ke−rT(H

X0

)2e1−2

[Φ(e2 − σ√T )− Φ(f1 − σ

√T )]

(2.4.18)

andP dot = Pt − P dit (2.4.19)

where as when H ≤ K,P dot = 0 (2.4.20)

andP dit = Pt (2.4.21)

2.4.3 Assumptions and Shortcomings of Black Scholes Formula

There are several assumptions under which above formulation and results were obtained, whichare mentioned as below (for more details, please refer [17], [14], [5] and [6]):

• The price of the underlying asset follows a Wiener process, and the price changes arelog-normally distributed.

• The stock does not pay a dividend and there are no transaction costs or taxes.

• It is possible to short sell the underlying stock and trading in the stock is continuous.Sudden and large changes in stock prices do not occur.

• It is possible to borrow and lend cash at a risk-free interest rate which remains constantover time. Also, there are no arbitrage opportunities.

• The volatility of stock price also remains constant over time.

Some of the assumptions above can be changed, and corresponding Black-Scholes formula can bederived (for example, for extension of Black-Scholes model to price options on dividend payingstocks, please refer to chapter 13 in [14]). On the other hand, certain assumptions cannot becorrected and often lead to an error in the computed option value. For example, it is a wellknown fact that probability distribution of underlying asset is not lognormal which leads to an

18

2 Options and Valuation Techniques

incorrect bias in pricing done by Black-Scholes method. The most prevalent assumption, forexample, when underlying asset is equity, is that equity price has a heavier left tail and lessheavier right tail in comparison with lognormal model.

Many alternative models have been proposed for overcoming the above disadvantages. Inthe next two sections, we give two such methodologies for pricing simple and exotic options.

19

Chapter 3

Semi-Parametric Approach forBounding Option Price

In their original article [1], Bertsimas and Popescu addressed the problem of deriving optimalinequalities for E[φ(X)] for a random variable X when given collection of general momentsE[fi(X)] = qi. Utilizing semidefinite and convex optimization methods in order to derive optimalbounds on the probability that variable X belongs in a given set, given first few moments for therandom variable X, they substantiate their theory by finding optimal upper bounds for optionprices with general payoff. The advantage of their approach is that probability distribution ofunderlying asset price is not required, only the moments are sufficient for deriving the optimalbounds. Later on, Gotoh and Konno [9] extended the above approach to obtain tight lowerbound for the option price with general payoff, given its first few moments.

In this section, we investigate and elaborate the semi-parametric approach for pricing optionsoriginally proposed by Lo in [22] and extended by Bertsimas and Popescu in [2] and [1] andmodified by Gotoh and Konno in [9] for obtaining tighter upper and lower bounds on Europeantype call option price, when we are given the first n moments of the underlying security price.The main idea in this approach is to view a semidefinite programming problem as a linearprogram with an infinite number of linear constraints.

3.1 Review of Basic Results

Introducing the notation: T and K are exercise time and exercise price of European type calloption, respectively. St and r are stock price at time t, and risk-free rate, respectively. Alsoπ is the risk-neutral probability of ST and Eπ[.] denotes the expected value of random variableunder the probability measure π. Then the call option price Ct is given by

Ct = e−r(T−t)Eπ [max(0, ST −K)] (3.1.1)

If we are given the first n moments qi, i = 1, ..., n of π, then the upper and lower bounds of thecall option price can be obtained by solving the following linear programming problems withinfinite number of variables π(ST ):

maximizeπ(ST )

e−rτ∫ ∞

0max(0, ST −K)× π(ST )dST

s.t. e−jrτ∫ ∞

0SjTπ(ST )dST = qj ,

j = 0, 1, ..., n, π(ST ) ≥ 0.

(3.1.2)

20

3 Semi-Parametric Approach for Bounding Option Price

minimizeπ(ST )

e−rτ∫ ∞

0max(0, ST −K)× π(ST )dST

s.t. e−jrτ∫ ∞

0SjTπ(ST )dST = qj ,

j = 0, 1, ..., n, π(ST ) ≥ 0.

(3.1.3)

where q0 = 1 and τ = T − t. Also to be noted is the fact that above problems are feasible. Wenow intend to derive the dual problems of (3.1.2) and (3.1.3). Denoting x = e−rτST and dualvariables as yi, i = 0, 1, ..., n, we can derive their dual problems:

minimizeπ(ST )

n∑i=0

qiyi

s.t.n∑i=0

xiyi ≥ max(0, x− e−rτK),

∀x ∈ R1+.

(3.1.4)

maximizeπ(ST )

n∑i=0

qiyi

s.t.n∑i=0

xiyi ≤ max(0, x− e−rτK),

∀x ∈ R1+.

(3.1.5)

We will now reiterate the propositions given by Bertsimas and Popescu which will assist us toconvert (3.1.4) and (3.1.5) into semidefinite programming problems.

Proposition 1. The polynomial g(x) =∑2k

r=0 yrxr satisfies g(x) ≥ 0 for all x ∈ R1 if and only

if there exists a positive semidefinite matrix X = [xij ] , i, j = 0, ..., k, such that

yr =∑

i,j:i+j=r

xij , r = 0, ..., 2k, X 0. (3.1.6)

Proof. We will first prove the if part, i.e. we assume that (3.1.6) holds, and we need to provethat g(x) =

∑2nr=0 yrx

r satisfies g(x) ≥ 0 for all x ∈ R1. Let x′k = (1, x, x2, ..., xk). Then

g(x) =2k∑r=0

∑i+j=r

xijxr

=k∑i=0

k∑j=0

xijxixj

= x′kXxk

≥ 0

and last step is obtained because we are given that X is positive semidefinite, i.e. X 0. Nowwe will prove the only-if part. We assume that the polynomial g(x) ≥ 0, ∀x ∈ R1 and degreeof g(x) is 2k. Then, we observe the fact that real roots of g(x) should have even multiplicity.This is because if they have odd multiplicity then g(x) would alter sign in an neighborhood of aroot. Denoting λi, i = 1, ..., r as the real roots of g(x) and 2mi as its corresponding multiplicity,its complex roots can then be arranged in conjugate pairs, aj + ibj , aj − ibj , j = 1, ..., h. Hence

g(x) = y2k

r∏i=1

(x− λi)2mih∏j=1

((x− aj)2 + b2j ).

21

3.1 Review of Basic Results

We note the fact that the leading coefficient y2k needs to be positive. Thus, by expanding theterms in the products, we can see that g(x) can be written as a sum of squares of polynomials,of the form

g(x) =k∑i=0

k∑j=0

xijxj

2

= x′kXxk

which proves that X is positive semidefinite, i.e. X 0, as we assumed that g(x) ≥ 0.

Proposition 2. The polynomial g(x) =∑k

r=0 yrxr satisfies g(x) ≥ 0 for all x ∈ R1 if and only

if there exists a positive semidefinite matrix X = [xij ] . i, j = 0, ..., k, such that∑i,j: i+j=2l−1

xij = 0, l = 1, ..., k,

∑i,j: i+j=2l

xij = yl, l = 0, ..., k,

X 0

(3.1.7)

Proof. We observe that g(x) ≥ 0 for all x ≥ 0 if and only if g(t2) ≥ 0, ∀t, which is a directresult of applying Proposition 1. Now in order to prove that g(t2) ≥ 0, ∀t, we evaluate g(t2) asbelow:

g(t2) = y0t0 + y1t

2 + y2t4 + ...+ ykt

2k,

= y0 + 0.t+ y1t2 + 0.t3 + y2t

4 + ...+ 0.t2k−1 + ykt2k,

from which we observe that all terms can be amalgamated into following two terms:

0.t+ 0.t3 + ...+ 0.t2k−1,

and

y0 + y2t4 + ...+ ykt

2k,

hence we obtain

g(t2) =k∑r=0

∑i,j: i+j=2r−1

xijt2r−1 +

k∑r=0

∑i,j: i+j=2r

xijt2r

Now finally we see that g(t2) ≥ 0, ∀ t if and only ifk∑r=0

∑i,j: i+j=2r−1

xijt2r−1+

k∑r=0

∑i,j: i+j=2r

xijt2r ≥ 0

⇔k∑r=0

∑i,j: i+j=2r−1

xijt2r−1 ≥ 0 and

k∑r=0

∑i,j: i+j=2r

xijt2r ≥ 0

⇔k∑r=0

∑i,j: i+j=2r−1

xijt2r−1 = 0 and

k∑r=0

∑i,j: i+j=2r

xijt2r ≥ 0

which proves the proposition, noting the fact that t2 ≥ 0, ∀t ∈ R1.

22

3 Semi-Parametric Approach for Bounding Option Price

Proposition 3. The polynomial g(x) =∑2k

r=0 yrxr satisfies g(x) ≥ 0 for all x ∈ [0, a] if and

only if there exists a positive semidefinite matrix X = [xij ] , i, j = 0, ..., k, such that

0 =∑

i,j: i+j=2l−1

xij , l = 1, ..., k,

l∑r=0

yr

(k − rl − r

)ar =

∑i,j: i+j=2l

xij , l = 0, ..., k,

X 0

(3.1.8)

Proof. We observe that g(x) ≥ 0 for all x ∈ [0, a] if and only if

(1 + t2)kg(

at2

1 + t2

)≥ 0, ∀ t

Now in order to prove the above fact, we evaluate the following expression:

(1 + t2)kg(

at2

1 + t2

)=

k∑r=0

yrart2r(a+ t2)k−r

= (1 + t2)k[y0 + y2

a2t4

(1 + t2)2+ ...+ yk

akt2k

(1 + t2)k

]=

k∑r=0

yrark−r∑l=0

(k − rl

)t2(l+r)

=k∑j=0

t2j

(j∑r=0

yr

(k − rj − r

)ar

)

Using the equality conditions on semidefinite matrix X given in Proposition 3, we get the finalexpression as

(1 + t2)kg(

at2

1 + t2

)≥ 0, ∀ t

if and only if

k∑j=0

t2j

(j∑r=0

yr

(k − rj − r

)ar

)≥ 0

⇔k∑r=0

∑i,j: i+j=2r

xijt2r ≥ 0

which we have proved to be true in Proposition 2.

Proposition 4. The polynomial g(x) =∑2k

r=0 yrxr satisfies g(x) ≥ 0 for all x ∈ [a,∞) if and

only if there exists a positive semidefinite matrix X = [xij ] , i, j = 0, ..., k, such that

0 =∑

i,j: i+j=2l−1

xij , l = 1, ..., k,

k∑r=l

yr

(rl

)ar−l =

∑i,j: i+j=2l

xij , l = 1, ..., k,

X 0

(3.1.9)

23

3.1 Review of Basic Results

Proof. We observe that g(x) ≥ 0, ∀x ∈ [0, a] if and only if

g(a+ t2) ≥ 0, ∀ t

Now in order to prove that g(a+ t2) ≥ 0 ∀ t, we evaluate g(a+ t2) as below:

g(a+ t2) =k∑r=0

yr(a+ t2)r

=k∑r=0

yr

r∑l=0

(rl

)ar−lt2l

=k∑l=0

t2l

(k∑r=l

yr

(rl

)ar−l

)Using the equality conditions on semidefinite matrix X given in Proposition 4, we get the finalexpression as

g(a+ t2) ≥ 0, ∀ t

if and only if

k∑l=0

t2l

(k∑r=l

yr

(rl

)ar−l

)≥ 0

⇔k∑r=0

∑i,j: i+j=2r

xijt2r ≥ 0

which we have proved to be true in Proposition 2.

Proposition 5. The polynomial g(x) =∑2k

r=0 yrxr satisfies g(x) ≥ 0 for all x ∈ (−∞, a] if and

only if there exists a positive semidefinite matrix X = [xij ] , i, j = 0, ..., k, such that

0 =∑

i,j: i+j=2l−1

xij , l = 1, ..., k,

(−1)lk∑r=l

yr

(rl

)ar−l =

∑i,j: i+j=2l

xij , l = 1, ..., k,

X 0

(3.1.10)

Proof. The proof is similar to that given for Proposition 4, but we just replace t2 by −t2 ing(a+ t2). We observe that g(x) ≥ 0, ∀ x ∈ [0, a] if and only if

g(a− t2) ≥ 0 ∀ t

Now in order to prove that g(a− t2) ≥ 0 ∀ t, we evaluate g(a− t2) as below:

g(a− t2) =k∑r=0

yr(a− t2)r

=k∑r=0

yr

r∑l=0

(rl

)ar−l(−t2)l

=k∑l=0

t2l

((−1)l

k∑r=l

yr

(rl

)ar−l

)we obtain (3.1.10) by applying (3.1.6) in a similar fashion to Proposition 4.

24

3 Semi-Parametric Approach for Bounding Option Price

Proposition 6. The polynomial g(x) =∑2k

r=0 yrxr satisfies g(x) ≥ 0 for all x ∈ [a, b] if and

only if there exists a positive semidefinite matrix X = [xij ] , i, j = 0, ..., k, such that

0 =∑

i,j: i+j=2l−1

xij , l = 1, ..., k,

l∑m=0

k+m−l∑r=m

yr

(rm

)(k − rl −m

)ar−mbm =

∑i,j: i+j=2l

xij , l = 1, ..., k,

X 0

(3.1.11)

Proof. We observe that g(x) ≥ 0, ∀x ∈ [a, b] if and only if

(1 + t2)kg(a+ (b− a)

t2

1 + t2

)≥ 0, ∀ t

Since

(1 + t2)kg(a+ (b− a)

t2

1 + t2

)=

k∑r=0

yr(a+ bt2)r(1 + t2)k−r

=k∑r=0

yr

r∑m=0

(rm

)ar−mbmt2m

k−r∑j=0

(k − rj

)t2j

=k∑l=0

t2l

(l∑

m=0

k+m−l∑r=m

yr

(rm

)(k − rl −m

)ar−mbm

)we obtain (3.1.11) by applying (3.1.6).

3.2 SDP Formulation of the Bounding Problems

Now that we have seen the basic results we are equipped to convert problems (3.1.4) and (3.1.5)which have infinite constraints, into equivalent SDP problems.

Theroem 1. An optimal solution of problem (3.1.4) can be obtained by solving the followingSDP problem

minimizeπ(ST )

n∑i=0

qiyi

s.t.∑

i,j:i+j=2l−1

xij = 0, l = 1, ..., n

yl −∑

i,j:i+j=2l

xij = 0, l = 0, ..., n

∑i,j:i+j=2l−1

zij = 0, l = 1, ..., n

y0 − z00 = −K,

y1 −∑

i,j:i+j=2

zij = 1

y1 −∑

i,j:i+j=2l

zij = 0, l = 2, ..., n

X,Z 0

(3.2.1)

where X 0, Z 0 denote that X and Y are positive semidefinite and K = e−rτK.

25

3.2 SDP Formulation of the Bounding Problems

Proof. We wish to convert the infinite constraints of problem (3.1.4) in finite constraints, thusobtaining a SDP problem. Representing the feasible region of (3.1.4) as

n∑i=0

qiyi ≥ 0, ∀ x ≥ 0 (3.2.2)

and

(y0 + K) + (y1 − 1)x+n∑i=2

qiyi ≥ 0, ∀ x ≥ 0 (3.2.3)

Using Proposition 2, we conclude that (3.2.2) is true if and only if there exists a positive semidef-inite matrix X = [xij ] . i, j = 0, ..., n, such that

∑i,j: i+j=2l−1

xij = 0, l = 1, ..., n,

∑i,j: i+j=2l

xij = yl, l = 0, ..., n,

X 0

(3.2.4)

Using Proposition 2 again for (3.2.3) we conclude that (3.2.3) is true if and only if there existsa positive semidefinite matrix Z = [zij ] . i, j = 0, ..., n, such that

∑i,j: i+j=2l−1

zij = 0, l = 1, ..., n,

∑i,j: i+j=2l

zij − K = yl, l = 0,

∑i,j: i+j=2l

zij + 1 = yl, l = 1,

∑i,j: i+j=2l

zij = yl, l = 2, ..., n,

X 0

(3.2.5)

Hence we obtain the constraints for our SDP problem by simplifying (3.2.4) and (3.2.5).

Now we will present another way of simplifying the constraints in (3.1.4), for obtaining aSDP problem.

Theroem 2. An optimal solution of problem (3.1.4) can be obtained by solving the following

26

3 Semi-Parametric Approach for Bounding Option Price

SDP problem

minimizeπ(ST )

n∑i=0

qiyi

s.t.∑

i,j:i+j=2l−1

xij = 0, l = 1, ..., n

l∑h=0

(n− hl − h

)Kh =

∑i,j:i+j=2l

xij , l = 0, ..., n

∑i,j:i+j=2l−1

zij = 0, l = 1, ..., n

n∑h=0

Khyh = z00,

n∑h=1

hKh−1yh − 1 =∑

i,j:i+j=2

zij ,

n∑h=l

(hl

)Kh−lyh =

∑i,j:i+j=2l

zij , l = 2, ..., n

X,Z 0

(3.2.6)

Proof. If we partition x ∈ [0,+∞) in two parts, i.e. x ∈ [0, K) and x ∈ [K,+∞). Using thisfact we note that the feasible region of (3.1.4) can be represented as

n∑i=0

qiyi ≥ 0, ∀ x ∈ [0, K) (3.2.7)

and

(y0 + K) + (y1 − 1)x+n∑i=2

qiyi ≥ 0, ∀ x ∈ [K,+∞) (3.2.8)

Using Proposition 3, we conclude that (3.2.7) is true if and only if there exists a positive semidef-inite matrix X = [xij ] , i, j = 0, ..., n, such that

0 =∑

i,j: i+j=2l−1

xij , l = 1, ..., n,

l∑r=0

yr

(n− rl − r

)Kr =

∑i,j: i+j=2l

xij , l = 0, ..., n,

X 0

(3.2.9)

Using Proposition 4, we conclude that (3.2.8) is true if and only if there exists a positive semidef-

27

3.2 SDP Formulation of the Bounding Problems

inite matrix Z = [zij ] , i, j = 0, ..., n, such that∑i,j: i+j=2l−1

zij = 0, l = 1, ..., n,

n∑h=l

yh

(hl

)Kh−l =

∑i,j: i+j=2l

zij , l = 0,

n∑h=l

yh

(hl

)Kh−l − 1 =

∑i,j: i+j=2l

zij , l = 1,

n∑h=l

yh

(hl

)Kh−l =

∑i,j: i+j=2l

zij , l = 2, ...n

Z 0

(3.2.10)

Hence we obtain the constraints for our SDP problem by simplifying (3.2.9) and (3.2.10).

We now turn our attention to convert problem (3.1.5) which has infinite constraints, intoequivalent SDP problem.

Theroem 3. An optimal solution of problem (3.1.5) can be obtained by solving the followingSDP problem

maximizeπ(ST )

n∑i=0

qiyi

s.t.∑

i,j:i+j=2l−1

xij = 0, l = 1, ..., n

l∑h=0

yh

(n− hl − h

)Kh =

∑i,j:i+j=2l

xij , l = 0, ..., n

∑i,j:i+j=2l−1

zij = 0, l = 1, ..., n

n∑h=0

Khyh + z00 = 0,

n∑h=1

hKh−1yh − 1 =∑

i,j:i+j=2

zij ,

n∑h=l

(hl

)Kh−lyh =

∑i,j:i+j=2l

zij , l = 2, ..., n

X,Z 0

(3.2.11)

Proof. We will follow a procedure similar to one used in Theorem 2 for proving this Theorem.If we partition x ∈ [0,+∞) in two parts, i.e. x ∈ [0, K) and x ∈ [K,+∞). Using this fact wenote that the feasible region of (3.1.5) can be represented as

−n∑i=0

qiyi ≥ 0, ∀ x ∈ [0, K) (3.2.12)

and

−(y0 + K)− (y1 − 1)x−n∑i=2

qiyi ≥ 0, ∀ x ∈ [K,+∞) (3.2.13)

28

3 Semi-Parametric Approach for Bounding Option Price

Using Proposition 3, we conclude that (3.2.12) is true if and only if there exists a positivesemidefinite matrix X = [xij ] , i, j = 0, ..., n, such that

0 =∑

i,j: i+j=2l−1

xij , l = 1, ..., n,

l∑r=0

yr

(n− rl − r

)Kr = −

∑i,j: i+j=2l

xij , l = 0, ..., n,

X 0

(3.2.14)

Using Proposition 4, we conclude that (3.2.13) is true if and only if there exists a positivesemidefinite matrix Z = [zij ] , i, j = 0, ..., n, such that∑

i,j: i+j=2l−1

zij = 0, l = 1, ..., n,

n∑h=l

yh

(hl

)Kh−l = −

∑i,j: i+j=2l

zij , l = 0,

n∑h=l

yh

(hl

)Kh−l − 1 = −

∑i,j: i+j=2l

zij , l = 1,

n∑h=l

yh

(hl

)Kh−l = −

∑i,j: i+j=2l

zij , l = 2, ...n

Z 0

(3.2.15)

Hence we obtain the constraints for our SDP problem by simplifying (3.2.14) and (3.2.15).

3.3 Computing the Moments

In order to implement the SDP problems given in 3.2.1, 3.2.6 and 3.2.11, we need to computethe moments qi, i = 0, ..., n of the underlying asset price. For reference implementation, wewill assume that the underlying asset price follows geometric Brownian motion(GBM) and thuscompare the derived option values with Black Scholes results. We now present an explicit formulato calculate the nth moment of underlying asset price Xt as below. Assuming that Xt follows astandard geometric Brownian motion, it satisfies

dXt = µXtdt+ σXtdz (3.3.1)

where dz = ε(t)√dt is a Wiener process, ε(t) is a standardized normal random variable. We

know the analytical solution for Geometric Brownian motion is given by:

Eπ [(XT )] = X0eντ+σdz

where dz ∼ N(0,√dt) and ν = µ− 1

2σ2. Now, we intend to calculate Eπ [(XT )n] as below:

Eπ [(XT )n] = Eπ[(X0e

ντ+σ√τε)n]

where φε (z) =e−

12zn

√2π

=∫ +∞

−∞Xn

0 enντ+nσ

√τz e− 1

2zn

√2π

dz

= Xn0 e

nντ

∫ +∞

−∞

enσ√τz− 1

2z

√2π

dz

29

3.3 Computing the Moments

Knowing the fact that

nσ√τz − 1

2z2 = −1

2(z − nσ

√τ)2 +

n2σ2τ

2

we get

Eπ [(XT )n] = Xn0 e

nντ

∫ +∞

−∞

en2σ2τ

2 e−12(z−nσ√τ)2

√2π

dz

= Xn0 e

nντ+n2σ2τ2

∫ +∞

−∞

e−12(z−nσ√τ)2

√2π

dz

= Xn0 e

nµτ+n2σ2τ2

because ∫ +∞

−∞

e−12(z−nσ√τ)2

√2π

dz = 1

Finally we conclude that the nth moment of XT , Eπ [(XT )n], is given by,

Eπ [(XT )n] = Xn0 e

nντ+n2σ2τ2 (3.3.2)

30

Chapter 4

Method of Moments and SDPRelaxations

In this section, we will cover the numerical methods proposed by Lasserre, Prieto-Rumeauand Zervos in [21] for pricing exotic options. These methods are applied to options whereunderlying asset price follows a geometric Brownian motion or other mean-reverting processesof particular interest. The main idea of this method is to identify the derivative price withinfinite-dimensional linear programming problems. These problems involve moments of appro-priate measures. Finally we develop a finite-dimensional relaxation which can be converted toa semidefinite programming(SDP) problem indexed by the number of moments involved.

4.1 Introduction

The whole approach proposed by Lasserre, Prieto-Rumeau and Zervos in [21] can be brieflydescribed as below:

1. The price of a Exotic option has to be identified with a linear combination of moments ofsuitably defined measures.

2. The martingale property of certain associated stochastic integrals is then exploited toderive an infinite system of linear equations involving the moments of the measures con-sidered.

3. Hence the value of an exotic option is characterized with the solution of an infinite-dimensional linear programming (LP) problem. The variables of this LP problem involvesthe moments of certain suitably defined measures.

4. A finite-dimensional relaxation is obtained by restricting the infinite-dimensional LP prob-lem to one that involves only a finite number of moments. Extra constraints called momentconditions are introduced in the LP problem (which thus converts it to a SDP problem) forachieving the finite-dimensional relaxation. These conditions reflect necessary conditionsfor a set of scalars to be identified with moments of a measure supported on a given set.

5. The result is a LP problem or a semidefinite programming (SDP) problem, which dependson the choice of moment conditions. By extremizing the resulting problems, upper andlower bounds for the value of the option under consideration are obtained. Also the qualityof such bounds is enhanced as the number of moments increases.

31

4.2 Deriving Infinite-Dimensional LP Problem

4.2 Deriving Infinite-Dimensional LP Problem

Suppose we are given a diffusion Zt

dZt = β (Zt) dt+ e (Zt) dBt, Z0 = z0 ∈ Rn (4.2.1)

We intend to approximate a function of diffusion Zt given above. In this section methodology ofmoments will be developed as a first step in achieving this goal. We will first derive an infinite-dimensional optimization problem, solution of which will give us the approximate value of thisfunctional. As this infinite-dimensional problem is unsolvable, the next step is to derive finitedimensional relaxations of these problems. The variables in these optimization problems aremoments defined on appropriate measures. When we derive the finite dimensional relaxation,we replace these unknown moments by scalars, and add necessary conditions (called momentconditions) for these scalars to be identical with the moments of measures with appropriatesupports.

4.2.1 Basic Adjoint Equation

In order to derive the Basic Adjoint Equation, necessary for developing the moments ap-proach, we will first introduce following notations and terminology.

Diffusion being considered: Given the filtered probability space, (Ω,F ,Ft,P), where Ωis given sample space , σ-algebra F of subsets of Ω, a measure P on (Ω,F), such that P (Ω) = 1and a filtration Ft on F . Define Zt as an n-dimensional diffusion defined on (Ω,F ,Ft,P)

dZt = β (Zt) dt+ e (Zt) dBt, Z0 = z0 ∈ Rn (4.2.2)

where β : Rn → Rn and e : Rn → Rn × Rm are deterministic functions such that SDE (4.2.2)has unique strong1 solution.

Infinitesimal Generator: The infinitesimal generator of diffusion Zt is given by

Af (z) =∑i

βi (z)∂f

∂zi+

12

∑i,j

(σ (z)σ (z)T

) ∂2f

∂zi∂zj(z) (4.2.3)

or in terms of the gradient and scalar and Frobenius inner products,

Af (z) = b (z) .Ozf (z) +12

(σ (z)σ (z)T

).Ozzf (z) (4.2.4)

where f ∈ D (A), and D (A) contains set of all twice-continuously differentiable functions f :Rn → R with compact support. We now impose two assumptions for further development ofthis approach.

Assumption 1: The entries of the vector β(z) and the matrix (eeT )(z) are polynomials inz, hence A maps polynomials into polynomials.

Assumption 2: Sum of all moments for diffusion Zt is finite, i.e.

supt∈[0,t]

n∑i=0

E[|Zjt |k

]≤ ∞, ∀ T ≥ 0, ∀ k ∈ N (4.2.5)

Now we consider the following two measures on diffusion ZtExpected Occupation Measure: The expected occupation measure µ(.) = µ(.; z0) of

diffusion Z up to time τ that is defined by

µ(B) := E[∫ τ

0IZs∈Bds

], B ∈ B (Rn) , (4.2.6)

1Compared to weak solution which consists of a probability space and a process that satisfies the SDE, astrong solution is a process that satisfies the equation and is defined on a given probability space.

32

4 Method of Moments and SDP Relaxations

where B (Rn) is the Borel σ-algebra on Rn.Exit Location Measure: The exit location measure ν(.) = ν(.; z0) that is defined by

ν(B) := P (Zτ ∈ B) , B ∈ B (Rn) , (4.2.7)

which is nothing but probability distribution of Zτ .

We are now ready to derive the Basic Adjoint Equation given the definitions and assumptionsabove. Specifically, given the Assumptions 1 and 2 above the following process

Mft := f(Zt)− f(z0)−

∫ t

0Af(ZS)ds

=∫ t

0[eTOzf ]T (ZS)dBS , t ≥ 0,

(4.2.8)

where f : Rn → R, f ∈ D (A) as defined above, is a square integrable martingale.

Now, Doob’s optional sampling theorem2 states: For X = Xtt≥0, which is an (Ft,P)martingale, and S, T are stopping times bounded by constant c, with S ≤ T , almost surely, thenEP[XT |FS ] = XS , P almost surely.

Applying Doob’s optional sampling theorem to (4.2.8) at times 0 and T we get,

E[Mft

]= E

[Mf

0

]E[f(Zt)− f(z0)−

∫ t

0Af(ZS)ds

]= E

[f(Z0)− f(z0)−

∫ 0

0Af(ZS)ds

]E [f(Zt)]− f(z0)− E

[∫ t

0Af(ZS)ds

]= f(Z0)− f(z0)− E

[∫ 0

0Af(ZS)ds

] (4.2.9)

and by simple calculations we know that,

f(Z0)− f(z0)− E[∫ 0

0Af(ZS)ds

]= 0 (4.2.10)

hence we get the following result

E [f(Zt)]− f(z0)− E[∫ t

0Af(ZS)ds

]= 0 (4.2.11)

Using the definitions of expected occupation measure µ(.), and exit location measure ν(.) asgiven above, we can rewrite (4.2.11) as below∫

Rnf (z) ν(dz)− f(z0)−

∫RnAf(z)µ(dz) = 0 (4.2.12)

which is called the basic adjoint equation. We can consider this equation as defining therelationship between the measures µ and ν associated with the generator A (for more detailsplease refer to article [12] by Helmes, Rohl and Stockbridge).

2We can roughly interpret Doob’s optional sampling theorem implying that in a Casino in a fair world, wherereturns are martingales and gambler is restricted to quit at stopping times, then there is almost zero probabilityto improve the expected return by judicious choice of stopping time.

33

4.2 Deriving Infinite-Dimensional LP Problem

4.2.2 Martingale Moment Conditions

Given a multiindex α ∈ N, if f is the monomial

f(z) = zα =n∏j=1

zαjj (4.2.13)

it can be seen from then Assumption 1 (4.2.5) that there exists a finite collection cβ(α) of realnumbers such that

Af(z) =∑β

cβ(α)zβ, ∀z ∈ Rn (4.2.14)

Defining µα = µα(z0) and να = να(z0) as the moments of µ and ν respectively, which we assumeare finite, i.e.

µα =∫

Rnzαµ(dz) ≤ ∞ (4.2.15)

and

να =∫

Rnzαν(dz) ≤ ∞ (4.2.16)

then basic adjoint equation (4.2.12) gives us the following infinite system of linear equationswhich link the moments µ and ν,

να −∑β

cβ(α)µβ = zα0 , ∀α ∈ N (4.2.17)

Consider the functional J(z0) of the diffusion Zt that is defined by

J(z0) := E [p (Zτ )] =k∑j=1

∫Kj

j (z) ν (dz) , (4.2.18)

where Kj , j = 0, ..., k is a given Borel measurable partition of Rn, and p(z) and pj(z) aredefined as

p(z) :=k∑j=1

pj(z)IKj (z), z ∈ Rn, (4.2.19)

andpj(z) :=

∑α

pjαzα, z ∈ Kj , ∀ j = 1, ..., k, (4.2.20)

Considering νj as partitions of ν, each defined on Kj , for j = 1, ...k, i.e.

νj(.) := νj(.; z0) := νj(.; z0)|Kj (4.2.21)

then from (4.2.19) and (4.2.20) we can see that

J(z0) =k∑j=1

∑α

pjαναj (4.2.22)

which is a linear combination of the moments ναj = ναj (z0) of the measures νj .

34

4 Method of Moments and SDP Relaxations

4.2.3 Using Available Moments

If the moments ναj of the measure να are easily computable (which is the case in European andAsian options as elucidated in subsequent sections), we can bound the functional J(z0) definedin (4.2.18) by obtaining the upper and lower bounds of infinite dimensional LP problem QI(z0)defined by

extremizek∑j=1

∑α

pjαναj ,

subject tok∑j=1

ναj = να, α ∈ Nn

νj ∈M(Kj), j = 1, ..., k,

(4.2.23)

noting that space of all Borel measures with finite moments of all orders that are supported ona given Borel measurable set K ⊆ Rn is denoted by M(Kj). We also note that the constraintsdefining the feasible region of QI(z0) are necessary moment conditions and hence

inf QI(z0) ≤ J(z0) ≤ sup QI(z0) (4.2.24)

When ν is moment-determinate3 then (4.2.24) is satisfied with equality because measure ν(.) isunique.

4.2.4 Using Martingale Moments Conditions

More generally when we cannot compute moments ν easily, we consider the infinite dimensionalLP problem QII(z0) defined by

extremizek∑j=1

∑α