Embed Size (px)

Citation preview

Nickel pig iron – A long term solution?

Robert Cartman - Hatch

History of the NPI industry

Present situation

Next few years...

3RD EURONICKEL CONFERENCE, HELSINKI, 2012

Contents

© Hatch Associates Limited, 2012 2

Conclusions

40,000

50,000

60,000

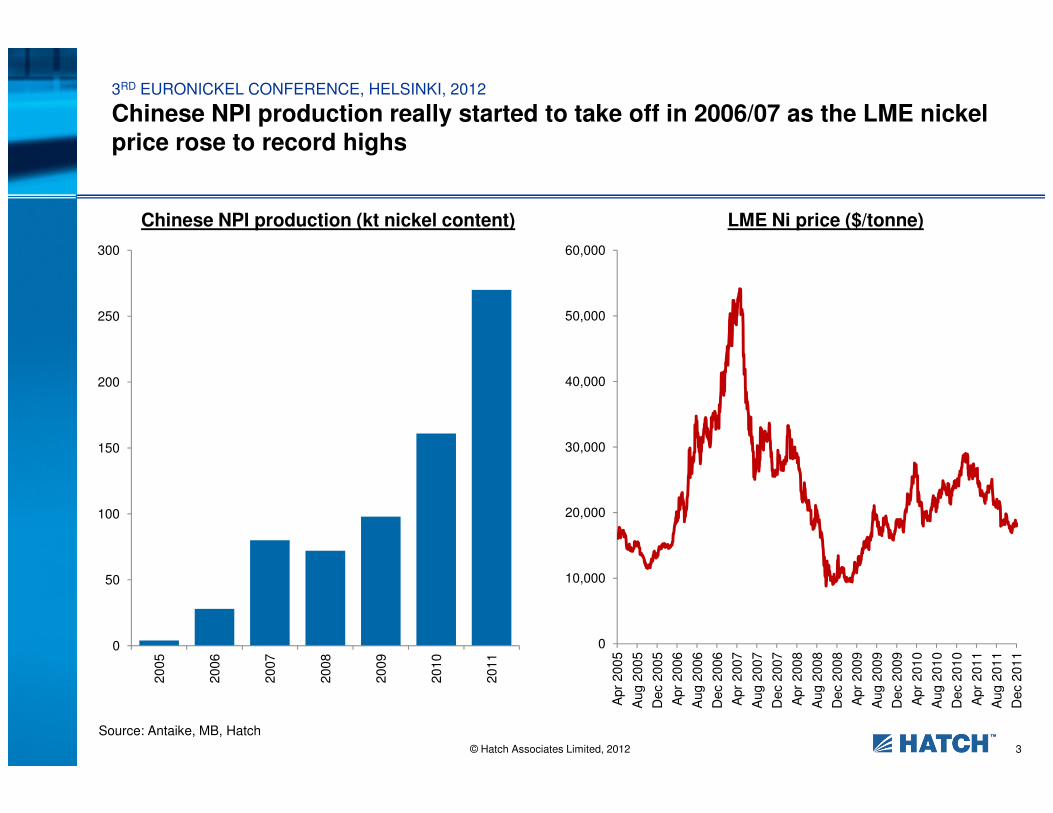

Chinese NPI production (kt nickel content)

3RD EURONICKEL CONFERENCE, HELSINKI, 2012

Chinese NPI production really started to take off in 2006/07 as the LME nickel price rose to record highs

LME Ni price ($/tonne)

200

250

300

© Hatch Associates Limited, 2012

0

10,000

20,000

30,000

Apr

2005

Aug 2

005

Dec 2

005

Apr

2006

Aug 2

006

Dec 2

006

Apr

2007

Aug 2

007

Dec 2

007

Apr

2008

Aug 2

008

Dec 2

008

Apr

2009

Aug 2

009

Dec 2

009

Apr

2010

Aug 2

010

Dec 2

010

Apr

2011

Aug 2

011

Dec 2

011

Source: Antaike, MB, Hatch

3

0

50

100

150

2005

2006

2007

2008

2009

2010

2011

Chinese primary nickel consumption by source, kt

3RD EURONICKEL CONFERENCE, HELSINKI, 2012

Nickel pig iron now accounts for more than 30% of China’s primary nickel consumption, up from just 2% in 2005

400

500

600

© Hatch Associates Limited, 2012

Source: Antaike, China Customs, Hatch

4

0

100

200

300

2005 2006 2007 2008 2009 2010

Nickel Cathode Nickel Salt NPI Net Imports

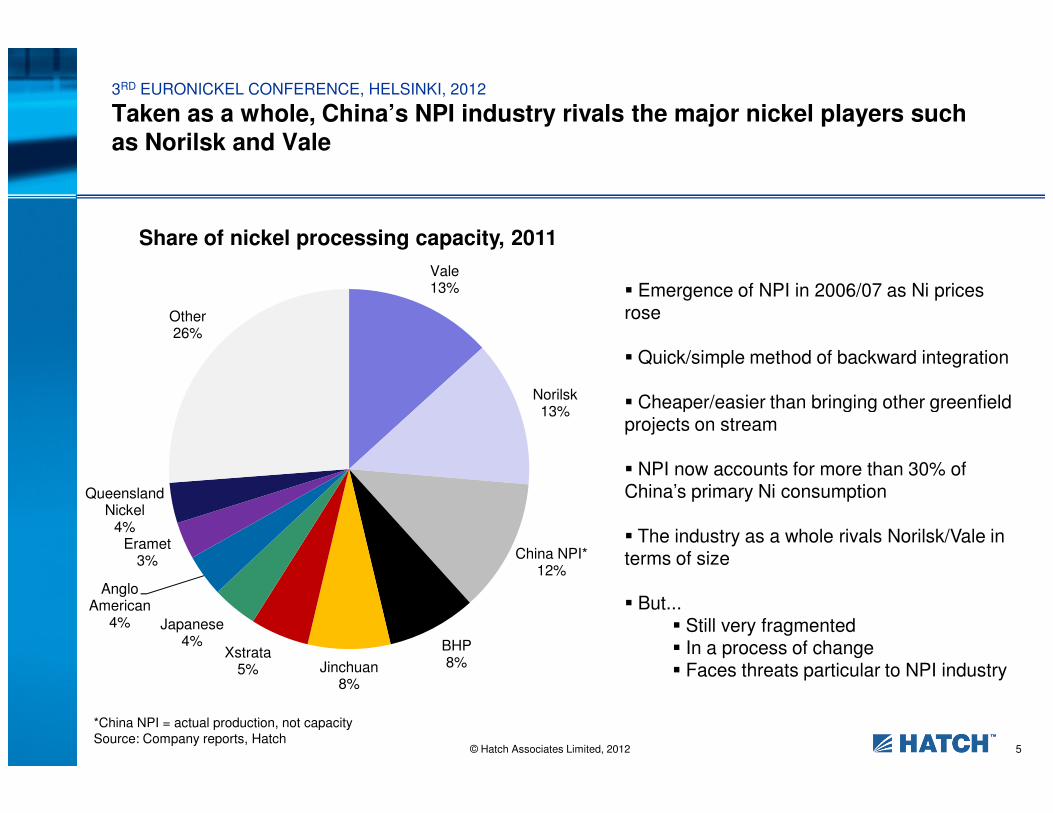

Vale13%

Norilsk13%

Other26%

Share of nickel processing capacity, 2011

3RD EURONICKEL CONFERENCE, HELSINKI, 2012

Taken as a whole, China’s NPI industry rivals the major nickel players such as Norilsk and Vale

� Emergence of NPI in 2006/07 as Ni prices rose

� Quick/simple method of backward integration

� Cheaper/easier than bringing other greenfield

© Hatch Associates Limited, 2012

13%

China NPI*12%

BHP8%Jinchuan

8%

Xstrata5%

Japanese4%

Anglo American

4%

Eramet3%

Queensland Nickel

4%

*China NPI = actual production, not capacity

Source: Company reports, Hatch

� Cheaper/easier than bringing other greenfieldprojects on stream

� NPI now accounts for more than 30% of China’s primary Ni consumption

� The industry as a whole rivals Norilsk/Vale in terms of size

� But...� Still very fragmented� In a process of change� Faces threats particular to NPI industry

5

History of China’s NPI industry

Present situation

Next few years...

3RD EURONICKEL CONFERENCE, HELSINKI, 2012

Contents

© Hatch Associates Limited, 2012 6

Conclusions

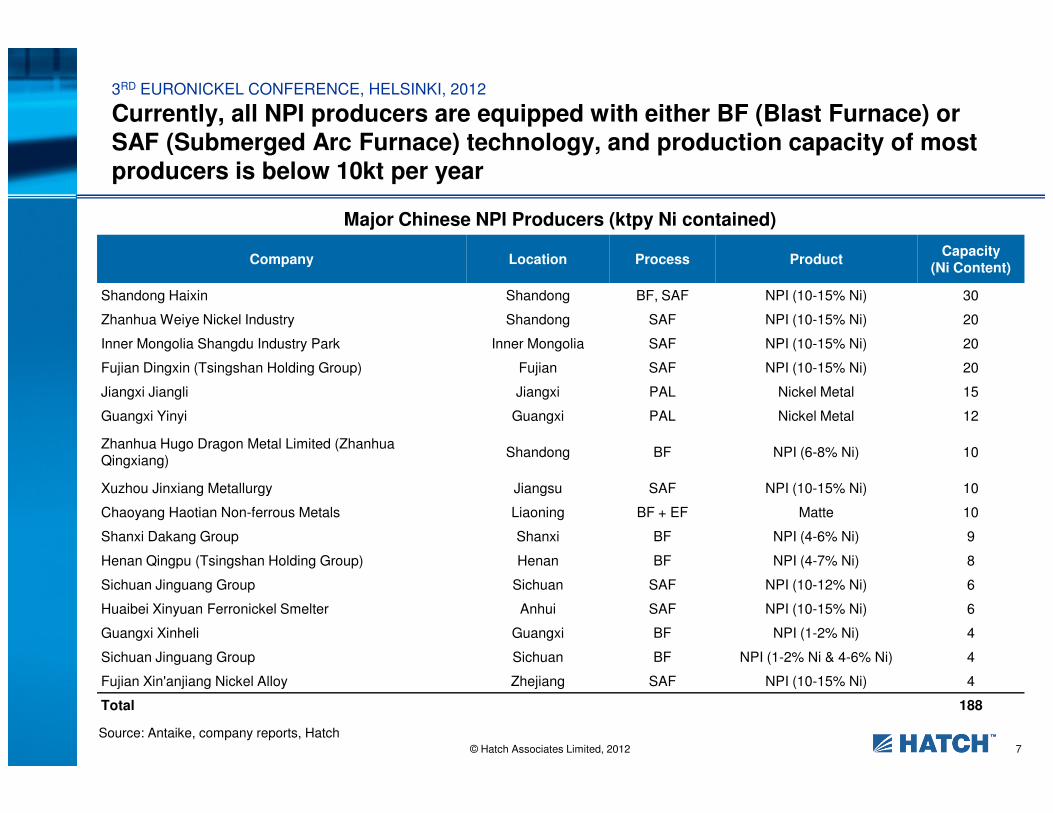

Major Chinese NPI Producers (ktpy Ni contained)

Company Location Process ProductCapacity

(Ni Content)

Shandong Haixin Shandong BF, SAF NPI (10-15% Ni) 30

Zhanhua Weiye Nickel Industry Shandong SAF NPI (10-15% Ni) 20

Inner Mongolia Shangdu Industry Park Inner Mongolia SAF NPI (10-15% Ni) 20

Fujian Dingxin (Tsingshan Holding Group) Fujian SAF NPI (10-15% Ni) 20

Jiangxi Jiangli Jiangxi PAL Nickel Metal 15

3RD EURONICKEL CONFERENCE, HELSINKI, 2012

Currently, all NPI producers are equipped with either BF (Blast Furnace) or SAF (Submerged Arc Furnace) technology, and production capacity of most producers is below 10kt per year

© Hatch Associates Limited, 2012

Source: Antaike, company reports, Hatch

Guangxi Yinyi Guangxi PAL Nickel Metal 12

Zhanhua Hugo Dragon Metal Limited (ZhanhuaQingxiang)

Shandong BF NPI (6-8% Ni) 10

Xuzhou Jinxiang Metallurgy Jiangsu SAF NPI (10-15% Ni) 10

Chaoyang Haotian Non-ferrous Metals Liaoning BF + EF Matte 10

Shanxi Dakang Group Shanxi BF NPI (4-6% Ni) 9

Henan Qingpu (Tsingshan Holding Group) Henan BF NPI (4-7% Ni) 8

Sichuan Jinguang Group Sichuan SAF NPI (10-12% Ni) 6

Huaibei Xinyuan Ferronickel Smelter Anhui SAF NPI (10-15% Ni) 6

Guangxi Xinheli Guangxi BF NPI (1-2% Ni) 4

Sichuan Jinguang Group Sichuan BF NPI (1-2% Ni & 4-6% Ni) 4

Fujian Xin'anjiang Nickel Alloy Zhejiang SAF NPI (10-15% Ni) 4

Total 188

7

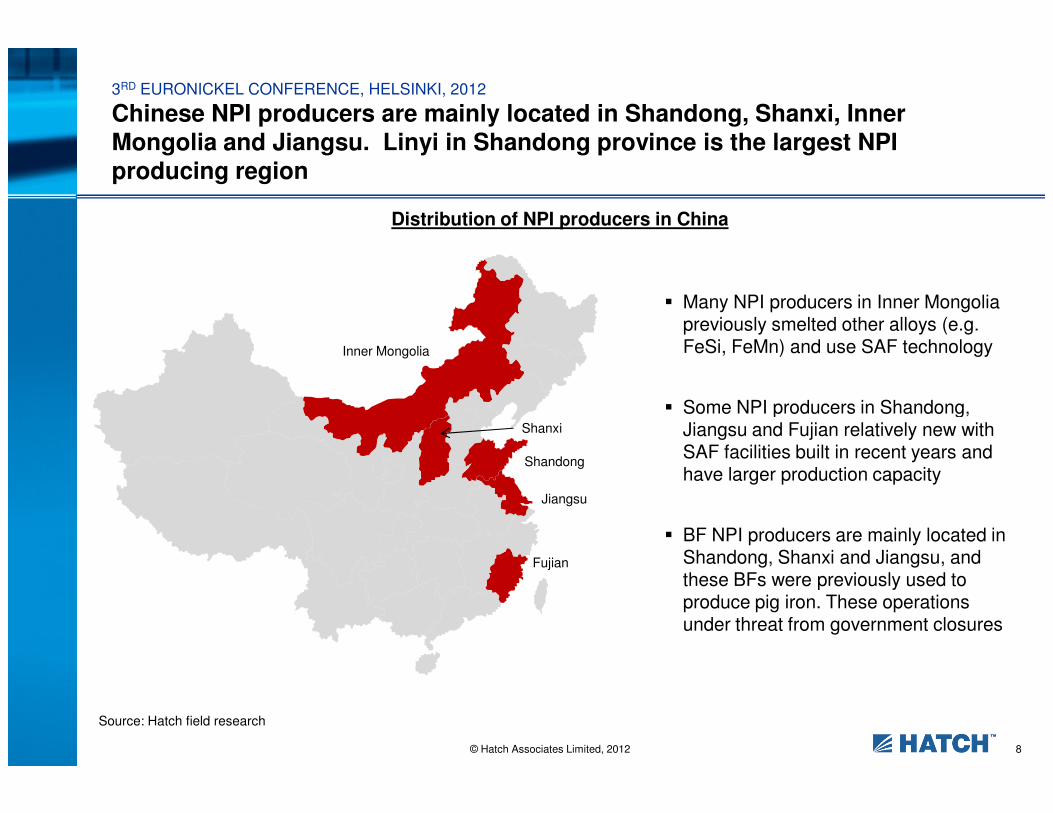

Distribution of NPI producers in China

� Many NPI producers in Inner Mongolia previously smelted other alloys (e.g. FeSi, FeMn) and use SAF technology

� Some NPI producers in Shandong,

Inner Mongolia

3RD EURONICKEL CONFERENCE, HELSINKI, 2012

Chinese NPI producers are mainly located in Shandong, Shanxi, Inner Mongolia and Jiangsu. Linyi in Shandong province is the largest NPI producing region

© Hatch Associates Limited, 2012

Source: Hatch field research

� Some NPI producers in Shandong, Jiangsu and Fujian relatively new with SAF facilities built in recent years and have larger production capacity

� BF NPI producers are mainly located in Shandong, Shanxi and Jiangsu, and these BFs were previously used to produce pig iron. These operations under threat from government closures

Shanxi

Shandong

Jiangsu

Fujian

8

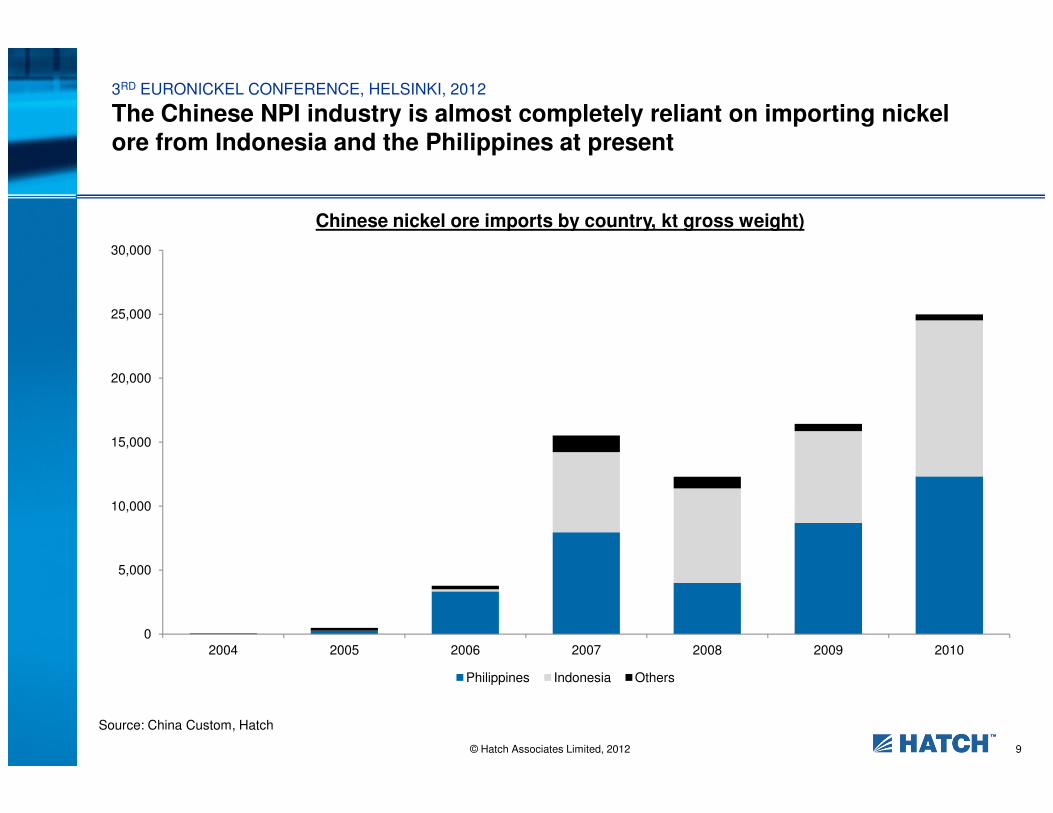

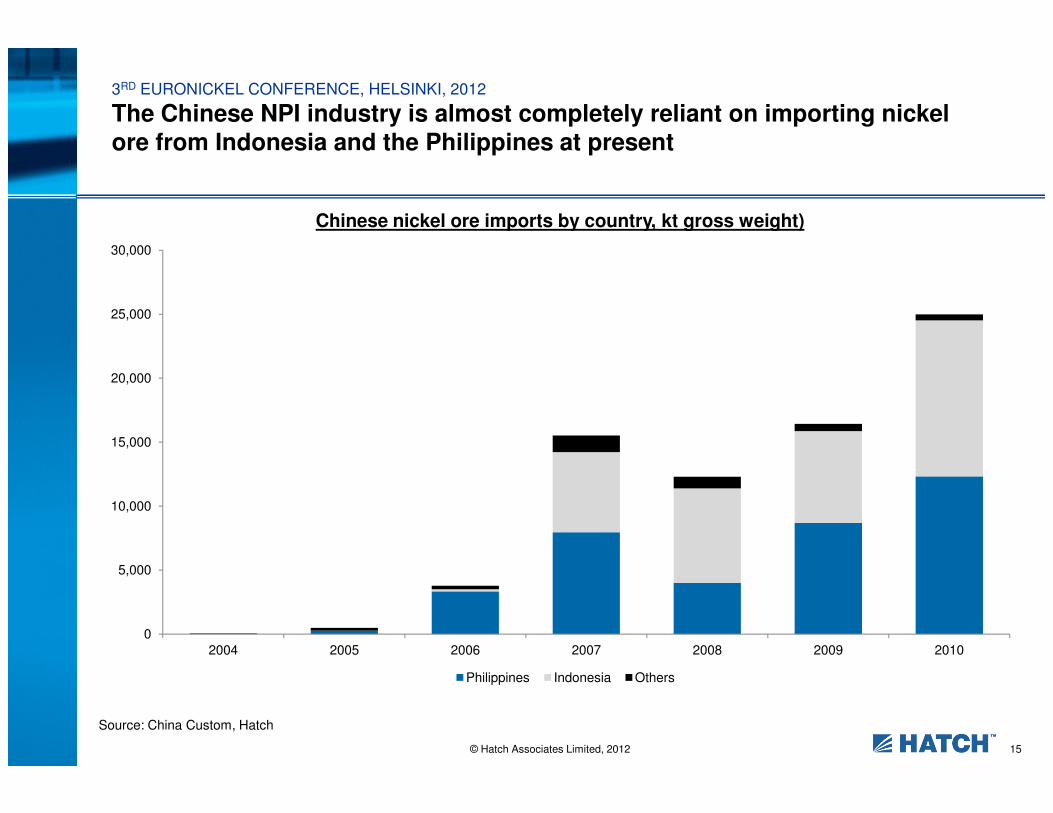

Chinese nickel ore imports by country, kt gross weight)

3RD EURONICKEL CONFERENCE, HELSINKI, 2012

The Chinese NPI industry is almost completely reliant on importing nickel ore from Indonesia and the Philippines at present

20,000

25,000

30,000

© Hatch Associates Limited, 2012

Source: China Custom, Hatch

9

0

5,000

10,000

15,000

2004 2005 2006 2007 2008 2009 2010

Philippines Indonesia Others

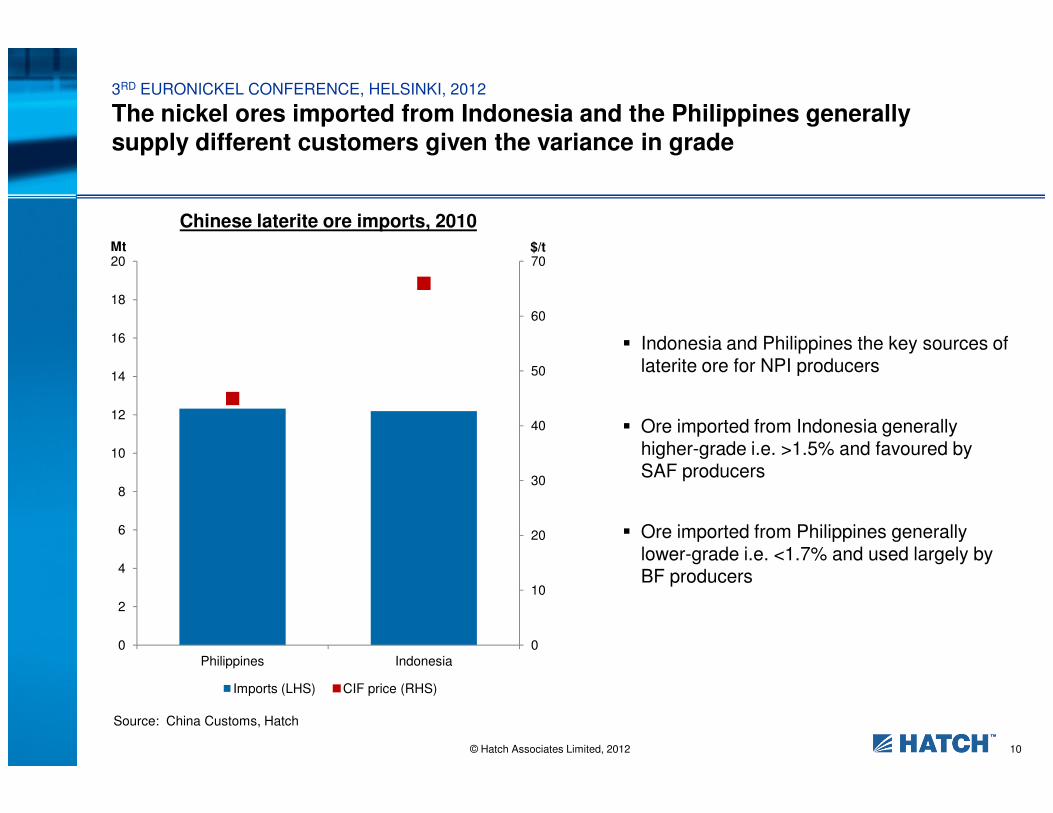

� Indonesia and Philippines the key sources of laterite ore for NPI producers

Chinese laterite ore imports, 2010

3RD EURONICKEL CONFERENCE, HELSINKI, 2012

The nickel ores imported from Indonesia and the Philippines generally supply different customers given the variance in grade

50

60

70

14

16

18

20Mt $/t

© Hatch Associates Limited, 2012

Source: China Customs, Hatch

� Ore imported from Indonesia generally higher-grade i.e. >1.5% and favoured by SAF producers

� Ore imported from Philippines generally lower-grade i.e. <1.7% and used largely by BF producers

10

0

10

20

30

40

0

2

4

6

8

10

12

Philippines Indonesia

Imports (LHS) CIF price (RHS)

Chinese NPI production by process route

3RD EURONICKEL CONFERENCE, HELSINKI, 2012

Producing NPI via electric furnaces has become more popular as the government has targeted small blast furnaces for closure

14%

33%

2008 2010 2011

© Hatch Associates Limited, 2012

Source: CBIChina, Hatch

11

45%

41%65%

35%

67%

33%

SAF BF Other

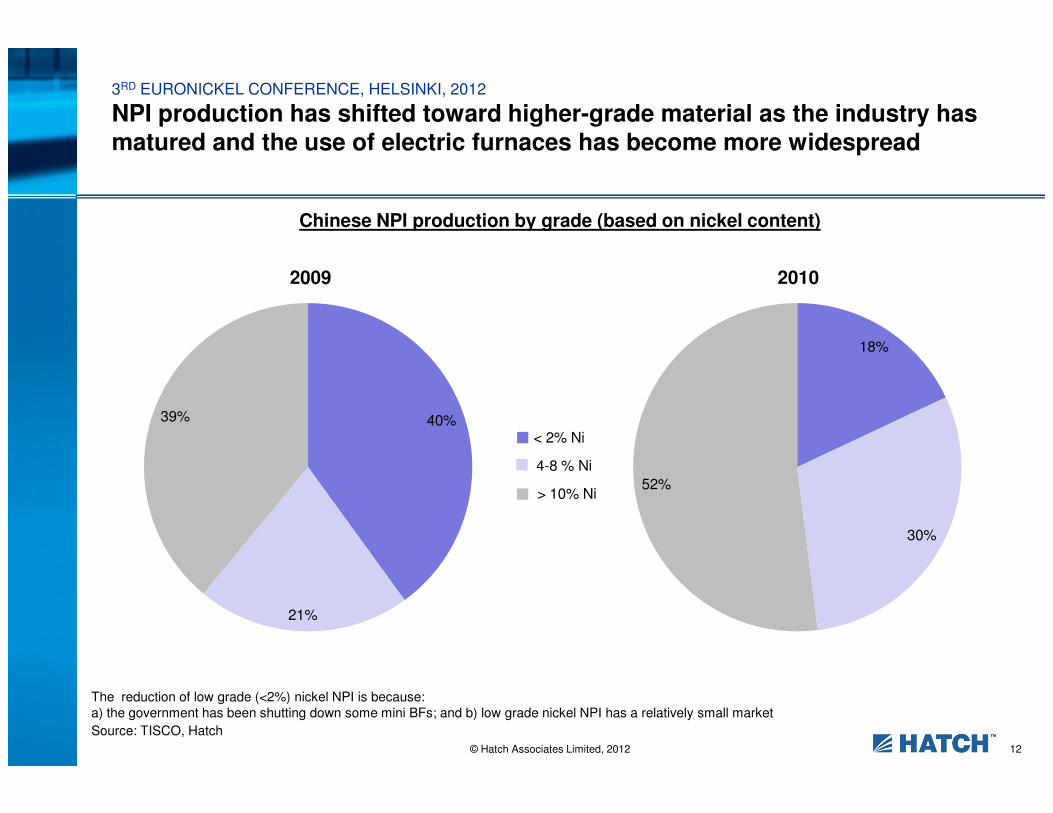

Chinese NPI production by grade (based on nickel content)

3RD EURONICKEL CONFERENCE, HELSINKI, 2012

NPI production has shifted toward higher-grade material as the industry has matured and the use of electric furnaces has become more widespread

2009

18%

2010

© Hatch Associates Limited, 2012

Source: TISCO, Hatch

The reduction of low grade (<2%) nickel NPI is because:

a) the government has been shutting down some mini BFs; and b) low grade nickel NPI has a relatively small market

12

40%

21%

39%

30%

52%

< 2% Ni

4-8 % Ni

> 10% Ni

Planned NPI projects in China (ktpy nickel contained)

Company Location Process StateCapacity

(Ni Content)

Sinosteel Hebei PFK* Phase I, commissioned in 2011 15

Sinosteel Hebei PFK* Phase II, planning 45

JNMC Guangxi RKEF Planning 100

Jien Nickel Inner Mongolia RKEF Phase I, commission in 2013 20

Jien Nickel Inner Mongolia RKEF Phase II, planning 80

3RD EURONICKEL CONFERENCE, HELSINKI, 2012

More than 600kt of new NPI production capacity has been announced and this will have a big impact on the nickel ore markets

© Hatch Associates Limited, 2012

*Pobuzhsky ferronickel plant process: old ferronickel process developed in the Ukraine

Source: Antaike, company reports, Hatch

Jien Nickel Inner Mongolia RKEF Phase II, planning 80

Macrolink Group Guangxi RKEF Planning 50

Sichuan Jinguang Group Guangxi RKEF Commission in 2013 50

Guangdong Guangxin Holding Group Guangdong RKEF Commission in 2012 50

Anhui Tenglong Alloy Anhui RKEF Commission in 2013 20

Hanking Group Liaoning RKEF Phase I, commission in 2013 30

Hanking Group Liaoning RKEF Phase II, planning 30

Delong Nickel Industry Jiangsu RKEF Commission in 2012 20

Taiwan E-United Group Fujian RKEF Planning 30

Fujian Fufeng Fujian RKEF Planning 50

Ruitian Steel Fujian RKEF Planning 30

Total 620

13

History of China’s NPI industry

Present situation

Next few years...

3RD EURONICKEL CONFERENCE, HELSINKI, 2012

Contents

© Hatch Associates Limited, 2012 14

Conclusions

Chinese nickel ore imports by country, kt gross weight)

3RD EURONICKEL CONFERENCE, HELSINKI, 2012

The Chinese NPI industry is almost completely reliant on importing nickel ore from Indonesia and the Philippines at present

20,000

25,000

30,000

© Hatch Associates Limited, 2012

Source: China Custom, Hatch

15

0

5,000

10,000

15,000

2004 2005 2006 2007 2008 2009 2010

Philippines Indonesia Others

Nickel reserves and resources, Mt nickel content

3RD EURONICKEL CONFERENCE, HELSINKI, 2012

Should Indonesia ban the export of nickel ores, the Chinese NPI industry may become even more reliant on the Philippines for ore supply

20

25

30

35

© Hatch Associates Limited, 2012

Source: Metalytics, USGS, Hatch

16

0

5

10

15

Laterite reserves Laterite resources Sulphide reserves Sulphide resources

3RD EURONICKEL CONFERENCE, HELSINKI, 2012

Thoughts and conclusions…

� NPI has grown to become a major source of primary nickel

� Will remain but is constantly evolving and maturing as an industry� Likely to eventually consolidate into larger producers, producing material similar to a FeNi

� Another 400-500kt of primary nickel will be needed over the next ≈ 15yrs to satisfy China’s likely

© Hatch Associates Limited, 2012 17

� Another 400-500kt of primary nickel will be needed over the next ≈ 15yrs to satisfy China’s likely increase in demand

� unless there is a sharp increase in the scrap ratio

� NPI industry faces threats, most notably at the moment the Indonesian ban on nickel ore exports� will have to find alternative supplies, perhaps from further mining expansion in Philippines

� smelters to backward-integrate, purchase mining rights in countries with laterite resources?

3RD EURONICKEL CONFERENCE, HELSINKI, 2012

Contacts for further information

Hatch Beddows Strategy Consulting

+44 20 7906 5100 (switchboard)�

9 Floor, Portland House, Bressenden Place, London SW1E 5BH�

© Hatch Associates Limited, 2012 18

Hatch Beddows is a member of the HATCH GROUP of companies

�

+44 20 7963 0972Fax

+44 20 7906 5119�

ConsultantRobert Cartman