Embed Size (px)

Citation preview

1

Network and Corporate Governance

Joseph P.H. Fan

Institute of Economics & Finance

The Chinese University of Hong Kong

Keynote speech at the 5th International Conference on Corporate Governance, Tianjin, China, September

2009

Joseph Fan Network Governance 2

Outline

� Why network?

� Enforcement of network

� Effects of network on governance and value

� Limitation of network

2

Joseph Fan Network Governance 3

2010/2/3 CEF 3

Figure 1: Organization Framework of Fusun Group

20% Iron

&S

teel 25%(2)

Commerce

Medicine

24.53%Estate

10% 10%22%

5%

11.95%(2)

10% 58%

95%

13.53%90.3%

20%90%1.94%10% 49%(2)

15.04%(2)

26.04%(1)

70.95%11.36%

8.81%%43.33%

(2)

30%3.77%

30%67.12%36.03%

(1)

48%(2)

20%21%

Shanghai Guangxin Technology

Development Co. Ltd.

Shanghai Fusun High

Technology (Group) Co. Ltd.

NISC

(600282)

FORTE

(HK2337)YYTM

(600655)

53.92%Nanjing Iron

&Steel United

Co.,Ltd.

Shanghai Fusun

Pharmaceutical

Development Co.

Ltd.

Shanghai Fusun I.T.

Development Co.

Ltd. (Subsidiary)LRGF

(600285)

Tianjin

Pharmaceutical

Holdings, Ltd.

TJPC

(600488)

中国医药控股有限公司.ACCORD

PHARM

(000028)

Shanghai

Friendship-

Fusun (holding)

Co. Ltd.

SFGIC

(600827) Tangshan

Jianlong Steel

Co. Ltd.

Lianhua

Supermarket

(HK0980)

Fusun

Pharm

(600196)

Zhaojin

Mining

Co. Ltd.

JianMin

Pharm

(600976)

Shanghai Fusun High Technology Co. Ltd.

Shanghai Fusun

Business

Investment Co. Ltd.

Liang XinjunGUO Guangchang

Wang Qunbin Fan Wei

Business Group – Network by Ownership

Joseph Fan Network Governance 4

Loan Network in Hunan, China国光瓷业600286

张家界430 嘉瑞新材

156亚华种业918

安塑股份156

洞庭水殖600257酒鬼酒

799湖南投资

548湖南海利化工

600731

电广传媒917岳阳恒立

622

现代投资900金荔

600762

金健米业600127

华银电力600744

中国纺织600610

华源股份600094

3

Joseph Fan Network Governance 5

Loan Network in Zhejiang, China

浙江海越600387

海亮股份2203浙江海亮盾安环境

2011

3家非上市公司4家非上市公司 浙江海纳

925

华盛达600687

3家非上市公司航天通信控股

600677

2家非上市公司尖锋集团600668

15家非上市公司浙江巨化 巨化股份

600160氟化学江山化工

2061

浙江江山水泥内蒙古边兴远兴能源683

中宝科控民丰纸业600235

4家非上市公司3家非上市公司戴梦得

600208

4家非上市公司 加西

Joseph Fan Network Governance 6

Lamsam

Wanglee

Chatikavanij (4)

Srivikorn

Krairiksh (3, 4)

Bodiratnangkura

Tangkaravakoon

Bulsook

Hetrakul

Osathanugrah

Thienprasidda (4)

Sukosol

Piya-oui

Sarasin

Lim-atibul (4)

Chearavanont

Virameteekul

PoolvoralaksYip In Tsoi/

Lailert

Charoen-Rajjapak

Bhirombhakdi

Royal families (2)

Chirathivat

Techakraisri (4)Promphan (4)

Tejapaibul

Uahchukiat

Bisalputra (4)

Karnchanachari

Navaphan

PhongsathornPhenjati

Kitikachorn (3)

Tantranont

Na Songkla (3)

Mahagitsiri

Karnasuta

Chutrakul (4)

Sosothikul

Sethteewan (4)

Thavisin (4)

Sethpakdi (4)Uahwatanasakul

Sethpornpong (4)

Leeissaranukul/Phannachet

Rattanin (4)

Chaichanian (4)

Chakkaphak (4)

Wattanavekin

Angubolkul

Mahaphan (4)

Vuthinantha (4)

Maleenont

Attakravisunthorn (3)

Jirakiti (3)

Benjarongkul

Nitibhon (3)Phaoenchoke

Nandhapiwat

Leenutaphong

Noonbhakdi (3)Sibunruang (4)

Osathanont (4)

Teepsuwan (4)

Cholvijarn (4)

Harnpanich (4)

Asavabhokin

Sarasas (4)

Thepkanjana (3)

Jarusatien (3)

Panyarachoon (3)

Tapparangsi (3)

Thailand

Network by Marriages

4

Joseph Fan Network Governance 7

Network versus Market Based

Governance

� Market based model

� Anonymous trading counter parties

� Explicit contract enforced by the court

� Dispute resolution resorting to contract or third-party assistance

� Network based model

� Trading among parties within a web of relationships

� Long-term, recursive

� Implicit contract enforced by loss due to non-salvaged investments (Klein, Crawford, Alchian, 1978)

� Dispute resolution depends on whether to maintain the relationships (Williamson, 1979)

Joseph Fan Network Governance 8

Why Network?

� By passing weak institutions and enforcement that fail to protect contracts

� Relationship help self-enforcement

� Reputation and relationship are costly to build and break

� Emerging markets, including those in China, are typically relationship based

5

Joseph Fan Network Governance 9

Enforcement of Networks

� Informal forces that do not depends on laws and third parties

� Key is investment in non-recoverable assets specialized to the relationship

� Reputation from repeated transactions

� Kinship (a relationship between any entities that share a genealogical origin, through either biological, cultural, or historical descent)

� Marriage

� Society membership

� Specialized payment (gift, kickback, and bribery)

Joseph Fan Network Governance 10

Evidence of Network and Value

Impacts

� Business groups

� Marriages

� Family firm succession

� Loan network

� Corruption network

6

Why Do Shareholders

Value Marriages?

Bunkanwanicha

Fan

Wiwattanakantang

Joseph Fan Network Governance 12

Marriage as a method of building relationship network (Bunkanwanicha, Fan, Wiwattanakantang, 2008)

7

Joseph Fan Network Governance 13

Marriage Sample from Thailand

Year Number Percentage

1991 12 5.9%1992 14 6.9%1993 8 3.9%1994 15 7.4%1995 12 5.9%1996 15 7.4%1997 7 3.5%1998 13 6.4%1999 12 5.9%2000 11 5.4%2001 18 8.9%2002 13 6.4%2003 11 5.4%2004 9 4.4%2005 23 11.3%2006 10 4.9%

Total 203 100.0%

Note: The sample includes 91 families (2 marriages/family on average)

Joseph Fan Network Governance 14

Marriages & Networks

Number Percentage

A. Family backgroundTop business (i) 42 20.7%Business, Professional (ii) 52 25.6%Royal, Noble (iii) 17 8.4%Politician, Military, Civil servant (iv) 50 24.6%Foreigner (v) 11 5.4%Others (vi) 31 15.3%

B. By type of networkBusiness network (i)+(ii) 94 46.3%Political network (iii)+(iv) 67 33.0%Others (v)+(vi) 42 20.7%

C. By type of marriageBusiness & Political networks 161 79.3%Others 42 20.7%

8

Joseph Fan Network Governance 15

Stock Price Effects of Marriages

A. Total sample (N=140)Mean (clustering) 0.85%*** 1.22%***Median (sign-test) 0.54%*** 0.81%***Positive CAR(%) 67% 69%

B. By type of marriage

- Network marriage (N=110) Mean (clustering) 1.08%*** 1.54%***

Median (sign-test) 0.71%*** 0.91%***Positive CAR(%) 72% 71%

- Other marriage (N=30)

Mean (clustering) -0.02% 0.03%

Median (sign-test) 0.00% 0.21%Positive CAR(%) 50% 63%

CAR(-1,+1)

Event: Announcement Date

CAR(-2,+2)

Joseph Fan Network Governance 16

Figure 1C: Long-term Cumulative Abnormal Returns before the Marriage News Date

(-60,+60)

9

Joseph Fan Network Governance 17

Cross country pattern of corporate leverage

(Fan, Titman, Twite, 2009)

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

Ko

rea,

Rep

.

Th

aila

nd

Ind

on

esia

Ind

ia

Bra

zil

Ph

ilip

pin

es

Ch

ina

Au

stri

a

Pak

ista

n

Ita

ly

Po

rtu

gal

Jap

an

Fin

lan

d

De

nm

ark

Sw

itze

rla

nd

Bel

giu

m

Fra

nce

Ho

ng

Ko

ng

, C

hin

a

Can

ad

a

Me

xic

o

Irel

and

Pe

ru

Ta

iwa

n

Ne

w Z

eala

nd

Sp

ain

Ch

ile

Sin

gap

ore

Ma

lay

sia

Ne

the

rla

nd

s

Ger

man

y

Sw

ed

en

No

rway

Un

ite

d S

tate

s

Au

stra

lia

Un

ited

Kin

gd

om

Isra

el

Tu

rke

y

So

uth

Afr

ica

Gre

ece

Joseph Fan Network Governance 18

Cross country pattern of corporate debt

maturity (Fan, Titman, Twite, 2009)

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

Ca

na

da

Sw

ed

en

Ne

w Z

ea

lan

d

Un

ite

d S

tate

s

Au

stra

lia

No

rwa

y

Fin

lan

d

Ire

lan

d

Sw

itz

erl

an

d

Me

xic

o

De

nm

ark

Ind

ia

Ne

the

rla

nd

s

So

uth

Afr

ica

Ch

ile

Po

rtu

ga

l

Bra

zil

Fra

nc

e

Be

lgiu

m

Un

ite

d K

ing

do

m

Ge

rma

ny

Ph

ilip

pin

es

Isra

el

Jap

an

Sp

ain

Au

stri

a

Ko

rea

, R

ep

.

Ho

ng

Ko

ng

, C

hin

a

Ita

ly

Pa

kis

tan

Pe

ru

Ta

iwa

n

Tu

rke

y

Ind

on

esi

a

Ma

lay

sia

Th

ail

an

d

Sin

ga

po

re

Ch

ina

Gre

ec

e

10

Joseph Fan Network Governance 19

Corruption Networks and Access to

Financial Capital

� Emerging markets are featured by high leverage and lack of long-term financing instruments. Why?

� In weak institution countries debt (bank loans) provide better private enforcement than equity

� Bureaucrats/politicians channel funds to their favored firms through banks they control

� Only well connected firms have access to long-term loans

Public Governance and Corporate Finance: Evidence

from Corruption Cases

Joseph P.H. Fan*

Oliver M. Rui*

Mengxin Zhao**

*Chinese University of Hong Kong

**University of Alberta

Journal of Comparative Economics (2008)

11

Joseph Fan Network Governance 21

A Corrupt Bureaucrat and His Publicly Listed

Allies

Joseph Fan Network Governance 22

The Scandal List

12

Joseph Fan Network Governance 23

Corruption and Access to Long-term

Loans (Fan, Rui, Zhao, JCE 2008)

Joseph Fan Network Governance 24

Effects of Network on Corporate

Governance

� Insider based governance� Concentrated ownership and control

� Managers and boards dominated by insiders and connected personnel

� Accounting opacity due to difficulty of measuring network cost and value

� Managerial incentive aligned by controlling ownership rather than explicit compensation

� Is this bad?� No, network and insider based governance are

optimal responses to weak institutions

13

Succession: The Roles of Specialized Assets and

Transfer Costs

Joseph P.H. Fan (CUHK)Ming Jian (NTU, Singapore)

Li Jin (HBS)

Yin-Hua Yeh (Fu-Jen Catholic University, Taiwan)

Joseph Fan Network Governance 26

Relationship/network based business dictate family successions (Fan, Jian, Li, Yeh, 2009)

100%217100%108100%47100%62Total

2%50%011%50%0Unknown

12%254%417%821%13Sold-out

22%4722%2436%1710%6Outsiders

28%6121%2328%1340%25Relative

36%7953%579%429%18Heir

65%14074%8036%1769%43Family

member

TotalTaiwanSingaporeHong Kong

14

Joseph Fan Network Governance 27

Poor Corporate Transparency Opacity Premium in Asia (Source: PricewaterhouseCoopers)

0

2

4

6

8

10

12

14

Economy

China

Taiwan

Hong Kong

Indonesia

Japan

Korea (South)

Singapore

Thailand

Joseph Fan Network Governance 28

Why are emerging market firms opaque?

� Complex organizational and ownership structures

� Covering up: rent seeking, corruption, or difficulties of putting investors’ interests before family interest (Fan and Wong, JAE 2002)

� Measurement difficulty: Network/relationship-based business post difficulty of measuring benefits and costs

15

Joseph Fan Network Governance 29

Joseph Fan, TJ Wong, and Tianyu Zhang

Forthcoming, Contemporary Accounting Review

Founder Succession and

Accounting Properties

29

Joseph Fan Network Governance 30

Table 2: Level of discretionary accruals

16

Joseph Fan Network Governance 31

Table 3 Timely loss Recognition

Joseph Fan Network Governance 32

Table 4: Change in Accruals

17

Joseph Fan Network Governance 33

Table 5 Panel A: Change in TLR

Joseph Fan Network Governance 34

Relationship Networks and Earnings

Informativeness:

Evidence from Corruption Cases

Joseph P.H. FAN/CUHK

Zengquan LI /SUFE

Yong George Yang /CUHK

34

18

Joseph Fan Network Governance 35

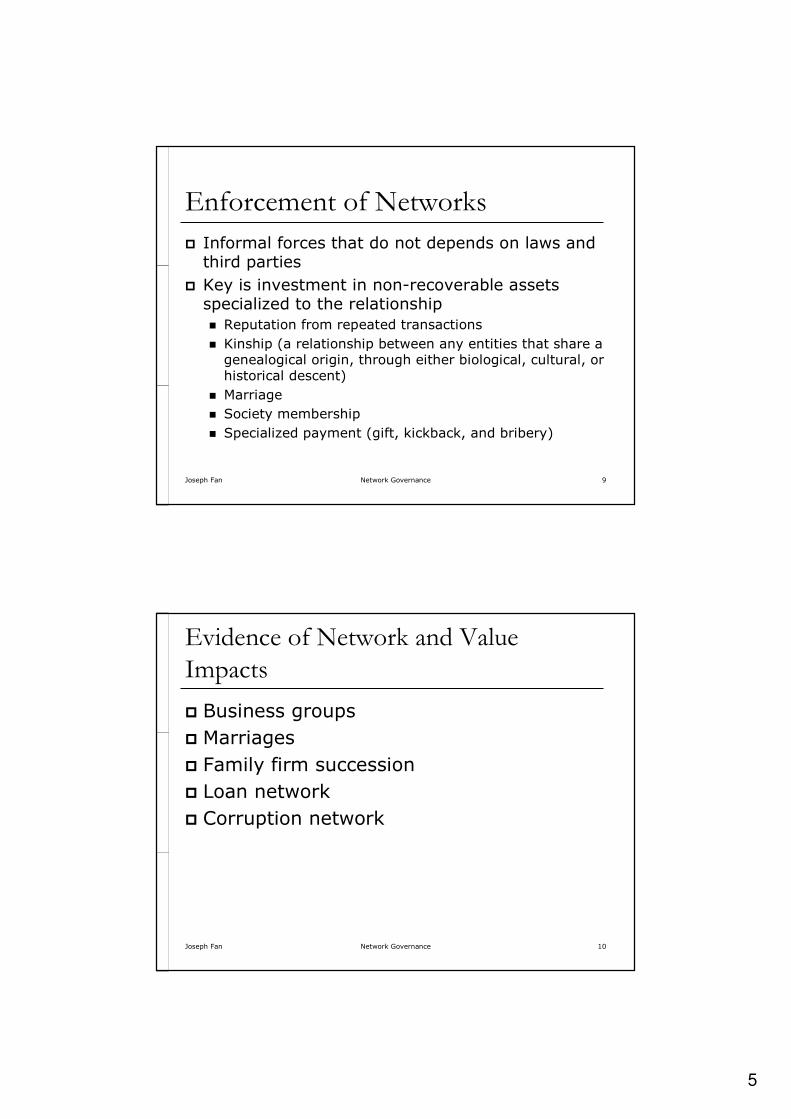

Earnings informativeness of politically connected

firms before and after corruption exposure (Fan, Yang, Zhang, 2009)

-1-0.500.511.5Connected Bribers Related

ERC for Politically Connected Firms Before exposureAfter exposure

Joseph Fan Network Governance 36

Politically Connected Chairmen/CEOs

in China’s Publicly Listed Companies

Bureaucrat chairman or CEO

0%

10%

20%

30%

40%

50%

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

All

SOE

Private

19

Joseph Fan Network Governance 37

Politically Connected Directors and Managers in

China’s Publicly Listed Companies

B ureaucrat d irectors and managers

0%

10%

20%

30%

40%

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

All

SO E

Priva te

Joseph Fan Network Governance 38

Limitation of Network Based

Governance

� Insiders dominate, conflict of interest costly to manage

� Specialized, difficulty of transfer

� Small scale, internal transactions not sufficient for large, sophisticated projects

� Low professionalism, not suitable for projects requiring high skills

� Localized, not suitable for the increasingly global business environment

20

Joseph Fan Network Governance 39

Post-IPO stock return performance (CAR) distinguished by whether CEOs have been bureaucrats (Fan, Wong, Zhang, JFE 2007)

-45.00%

-40.00%

-35.00%

-30.00%

-25.00%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35

Months after IPO

Retu

rn

mean of firms whose CEOs

are potically connected

mean of firms whose CEOs

are not potically connected

Figure 3: Cumulative market-adjusted compound stock returns

Joseph Fan Network Governance 40

Ownership Discount (Claessens, Djankov, Fan, Lang, JF

2002)

Company Valuation and the Difference

between Control and Ownership

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

0% 1-5% 6-10% 11-15% 16-20% 21-25% 26-30% 31-35% 36-40%

Control Minus Ownership

Mean

Mark

et-

to-b

oo

k V

alu

e

21

Joseph Fan Network Governance 41

Challenges of transferring

network/relationship in family firms

� Sustainability of the relationship based business model is questionable� Relationship is difficult to partition and transfer

across individuals and firms

� Moving from the relationship based to market based model is a common challenge to most emerging market firms� Specialized assets difficult to standardized

� Managerial entrenchment

� Political entrenchment - politicians and bureaucrats do not want to lose their influences on the corporate sector

Joseph Fan Network Governance 42

Li Ka-shing (77) was sent to hospital on Sep. 6th ,

2005.

42

Cumulated Daily Stock

Return

22

Joseph Fan Network Governance 43

Succession and firm value (Fan, Jian, Li, Yeh, 2009)

Monthly cumulative abnormal stock return (CAR) around succession

-0.9

-0.8

-0.7

-0.6

-0.5

-0.4

-0.3

-0.2

-0.1

0

0.1

-60 -48 -36 -24 -12 0 12 24 36

Joseph Fan Network Governance 44

Succession and firm value (Fan, Jian, Li, Yeh, 2009)

Monthly cumulative abnormal stock return (CAR) around succession, by economy

-1.4

-1.2

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

-60 -48 -36 -24 -12 0 12 24 36

Hongkong

Singarpore

Taiwan

23

Joseph Fan Network Governance 45

Conclusions

� Emerging market corporate governance is relationship based

� Network governance is optimal response to weak institutions

� Government imposing Western arm’s length based model will not work

� Firms evolve to arm’s length governance when their business model change due to change of leadership, market, or institutional environment

� We know very little about these. More research is needed

![PRIMORDIAL BLACK HOLE - University of Miami · REFERENCES P.H. Frampton, The Primordial Black Hole Mass Range arXiv:1511.xxxxx [hep-ph] P.H. Frampton, Searching for Dark Matter Constituents](https://img.pdfslide.us/doc/110x75/5af2eb827f8b9a154c8c2556/primordial-black-hole-university-of-miami-ph-frampton-the-primordial-black.jpg)