Embed Size (px)

Citation preview

Saratoga, NYSaratoga, NYSeptember 25, 2008

Natural Gas UpdatePresentation to:

Northeast PowerCoordinating Council (NPCC)

General Meeting

Thomas Kiley President and CEOThomas Kiley, President and CEONortheast Gas Association

T iTopics

Winter OutlookGas Supply Task Force & Electric CoordinationInfrastructure DevelopmentsOn the Supply Horizon– Rockies gas– Marcellus Shale

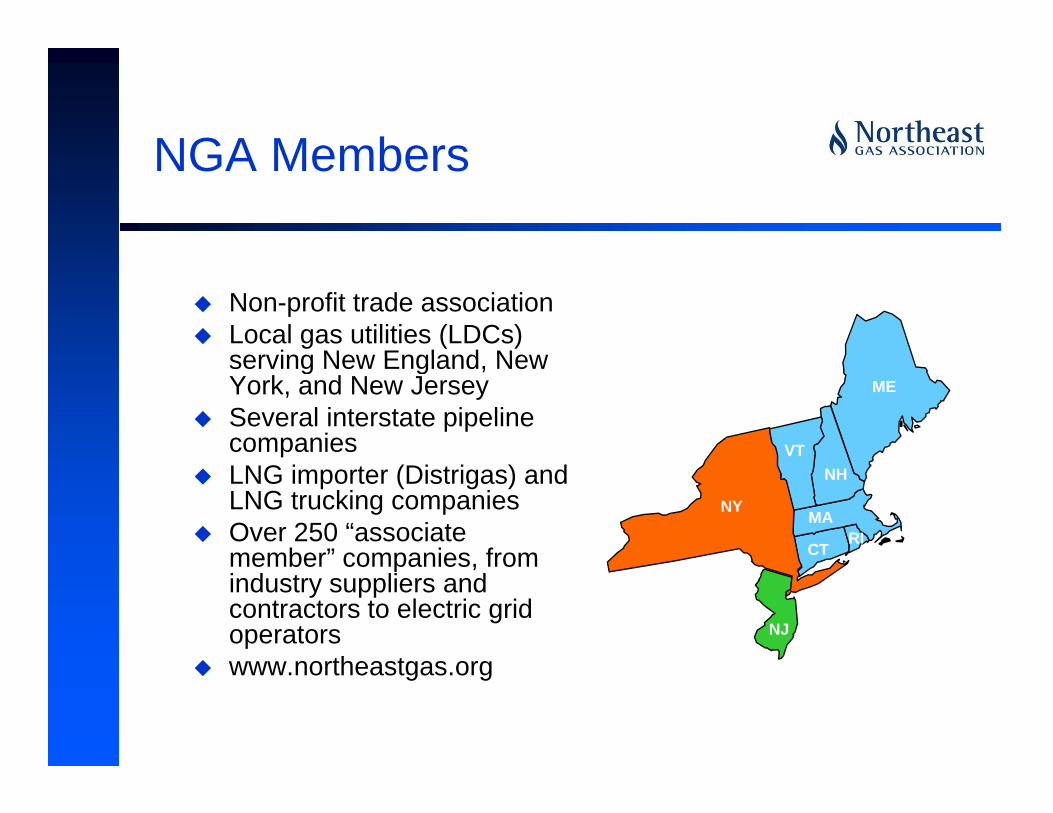

NGA MembersNGA Members

Non-profit trade associationLocal gas utilities (LDCs) serving New England Newserving New England, New York, and New JerseySeveral interstate pipeline companies VT

ME

LNG importer (Distrigas) and LNG trucking companiesOver 250 “associate member” companies from

RIMA

CT

NY

NH

member companies, from industry suppliers and contractors to electric grid operatorswww northeastgas org

NJ

www.northeastgas.org

Wi t O tl kWinter OutlookStorage levels in positive position, on track for Nov. 1 refillStorage levels in positive position, on track for Nov. 1 refill

U.S. gas production up strongly this year (~8%), Canadian imports steady, offsetting much lower total LNG imports compared to last year

New England LNG imports by Distrigas remain steady and consistent

New pipeline serving NY State in-service by year’s end: Millennium

Hurricane season not over yet, but - to date – apparently no major energy system damage from recent Gulf storms

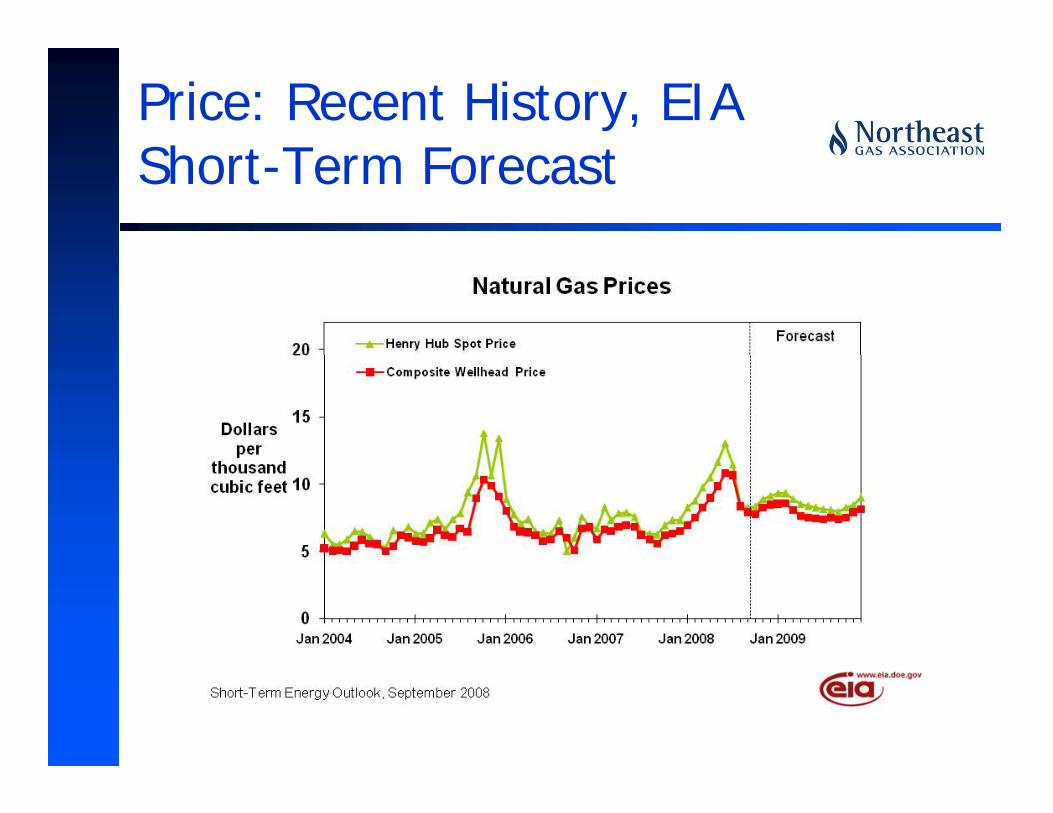

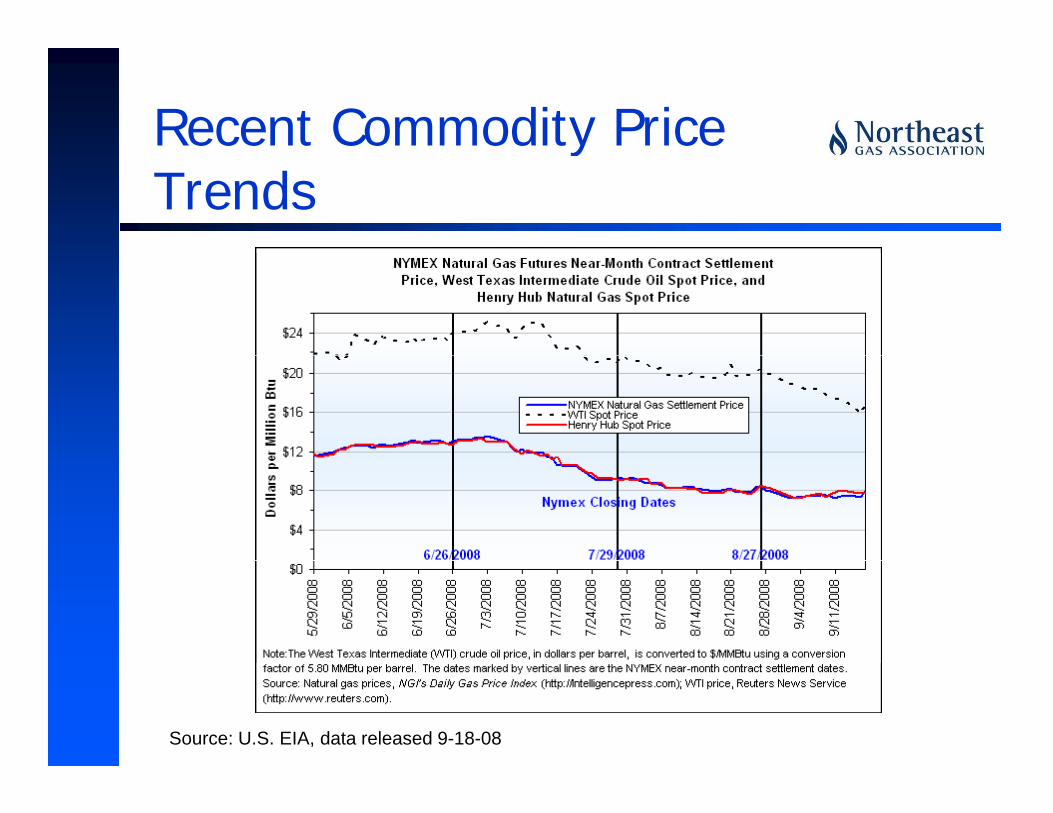

Commodity price has been extremely volatile all year, but down over 30% since July

LDCs reporting strong numbers of conversions in home heating marketLDCs reporting strong numbers of conversions in home heating market

Looking ahead, weather, as always, is the biggest variable in supply/price dynamic

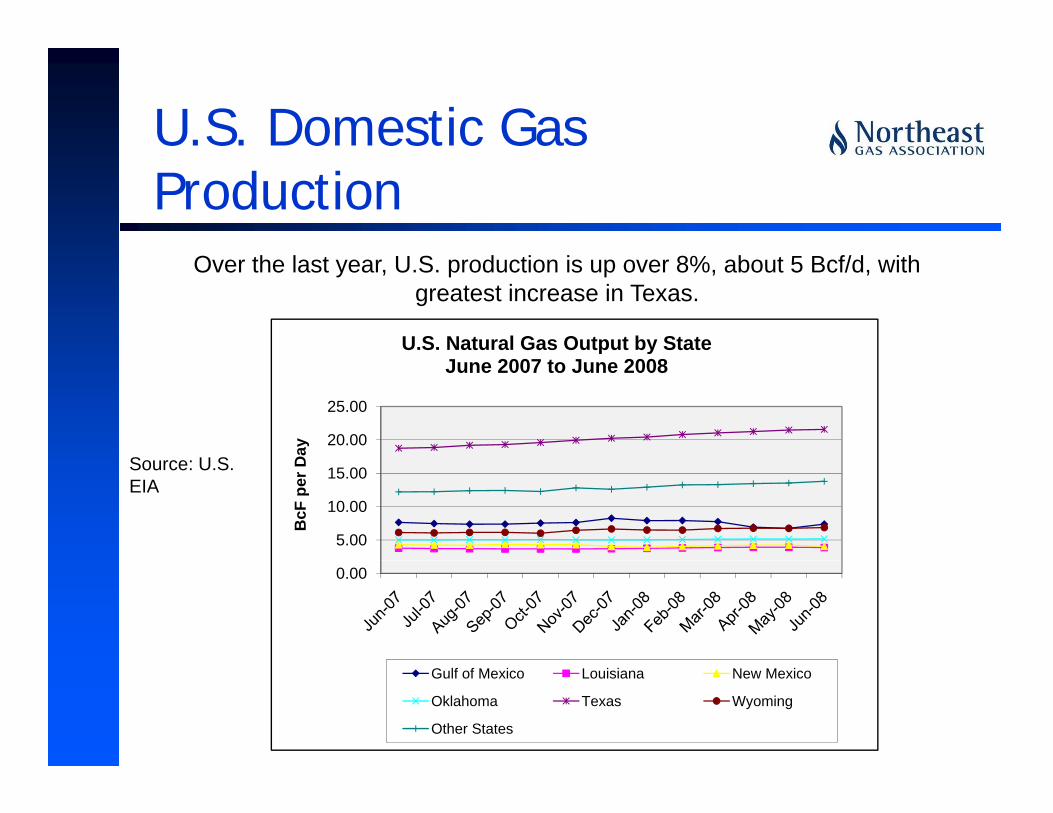

U.S. Domestic Gas Production

Over the last year, U.S. production is up over 8%, about 5 Bcf/d, withgreatest increase in Texas.

U.S. Natural Gas Output by State

S U S20.00

25.00

Day

June 2007 to June 2008

Source: U.S. EIA

5.00

10.00

15.00

BcF

per

D

0.00

Gulf of Mexico Louisiana New Mexico

Oklahoma Texas Wyoming

Other States

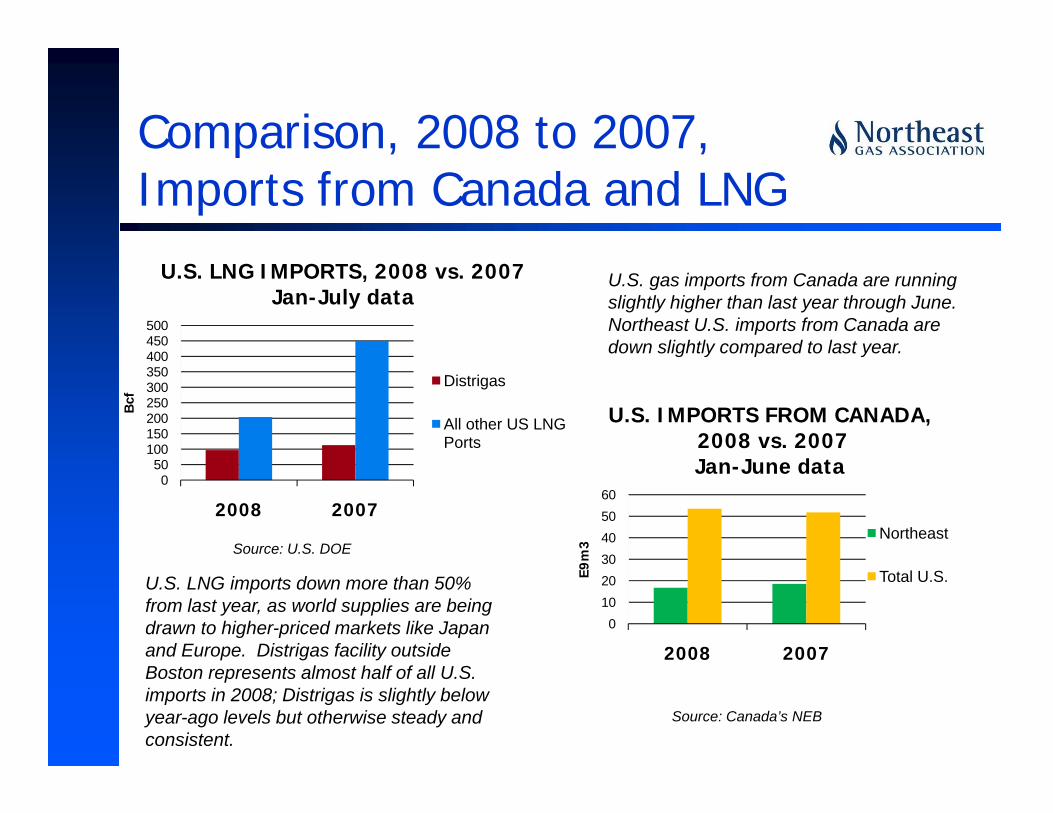

Comparison, 2008 to 2007, p , ,Imports from Canada and LNG

400450500

U.S. LNG IMPORTS, 2008 vs. 2007Jan-July data

U.S. gas imports from Canada are running slightly higher than last year through June. Northeast U.S. imports from Canada are down slightly compared to last year.

100150200250300350400

Bcf

Distrigas

All other US LNG Ports

U.S. IMPORTS FROM CANADA,2008 vs. 2007

d

g y p y

Source: U.S. DOE

050

2008 2007

30

40

50

60

m3

Jan-June data

Northeast

0

10

20

30

2008 2007

E9m

Total U.S.U.S. LNG imports down more than 50%from last year, as world supplies are being drawn to higher-priced markets like Japan and Europe. Distrigas facility outside

Source: Canada’s NEB

Boston represents almost half of all U.S. imports in 2008; Distrigas is slightly below year-ago levels but otherwise steady and consistent.

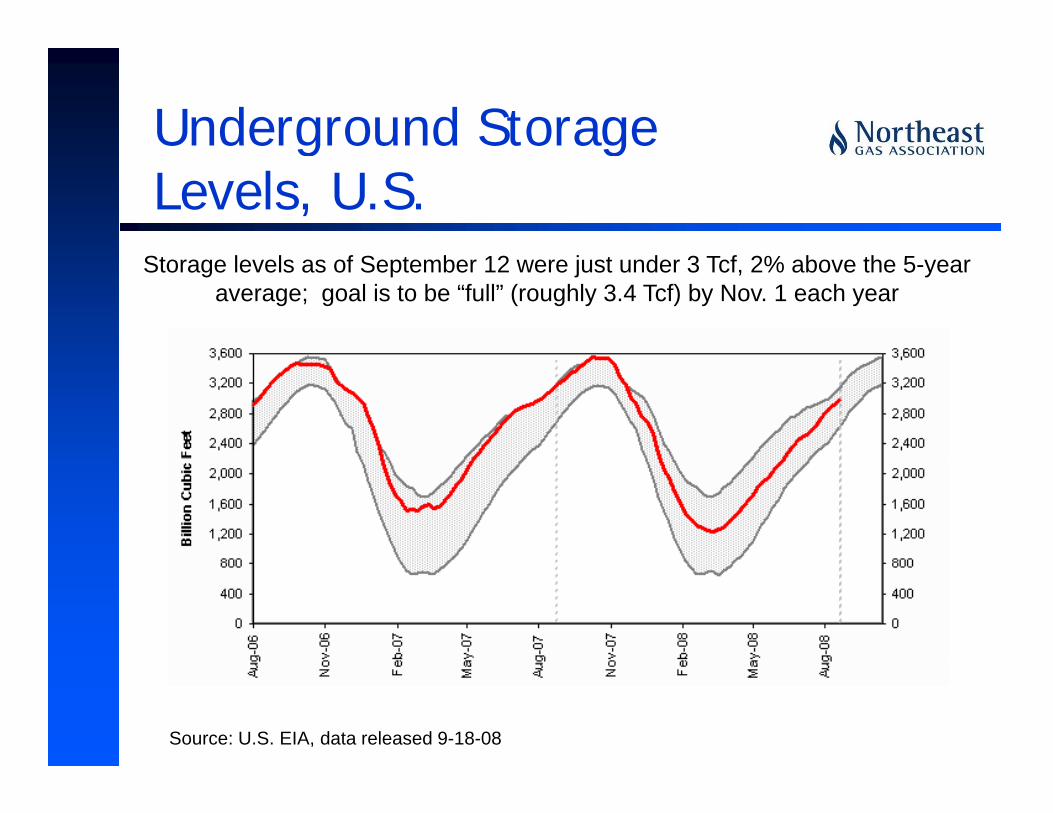

Underground Storage g gLevels, U.S.

Storage levels as of September 12 were just under 3 Tcf, 2% above the 5-year average; goal is to be “full” (roughly 3.4 Tcf) by Nov. 1 each year

Source: U.S. EIA, data released 9-18-08

Price: Recent History, EIA Sh t T F tShort-Term Forecast

Recent Commodity Price yTrends

Source: U.S. EIA, data released 9-18-08

NGA Gas Supply Task Force

Members: all LDCs in region, interstate pipelines (including TransCanada), LNG transporters(including TransCanada), LNG transporters

Purpose: to help deal with meeting winter supply needs and deliverability within the Northeast regionneeds and deliverability within the Northeast region

Tasks: Monitor regional deliverability of its g ymembers’ gas supplies during periods of peak demand or supply curtailment; Advise region’s energy, regulatory and policy officials; also Updategy, g y p y ; pISOs in region of meetings, outcomes

NGA I t f ith ISONGA Interface with ISOs

Electric & Gas Operations Committee NGA and ISO NE/NY ISOElectric & Gas Operations Committee, NGA and ISO-NE/NY ISO– Meets periodically, provides updates on system issues (only publicly

available information discussed – transparency requirements)– Most recent call held 9-17-08, with ISO-NE, NY ISO, PJM, NGA,

and several pipelines and gas LDCs participatingand several pipelines and gas LDCs participating

NY ISO and ISO-NE will participate at NGA winter supply outlook briefing for state government officials in region, 11-6-08g g g

NGA helped develop operations communications protocol between NY ISO and interstate pipelines in early 2008

NGA on behalf of its NE Gas Supply Task Force will notify ISO-NE, NY ISO, PJM when Task Force meets, summary of any actions or status

Key issue remains level of non-firm transportation arrangements among gas-fired power generators

Infrastructure Enhancements:

Anticipated In-ServiceAnticipated In Service Between Last Winter and

Winter 2008 09Winter 2008-09

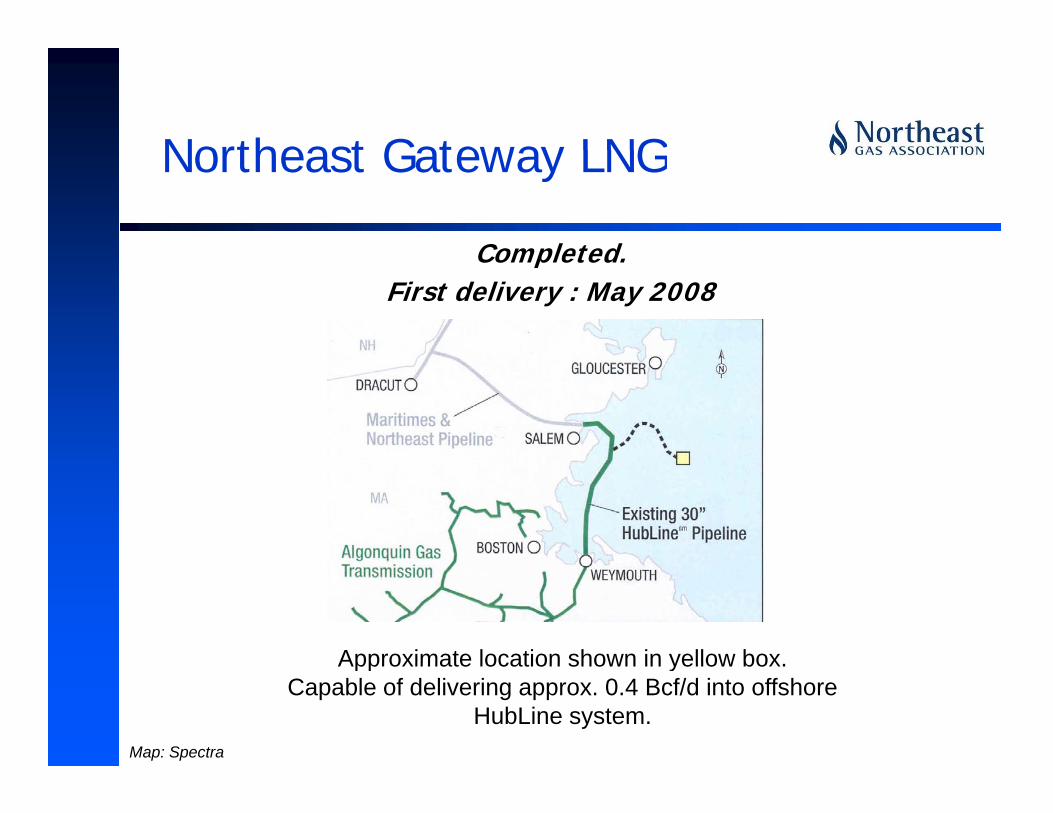

Northeast Gateway LNGNortheast Gateway LNG

CompletedCompleted.First delivery : May 2008

Approximate location shown in yellow boxApproximate location shown in yellow box.Capable of delivering approx. 0.4 Bcf/d into offshore

HubLine system.Map: Spectra

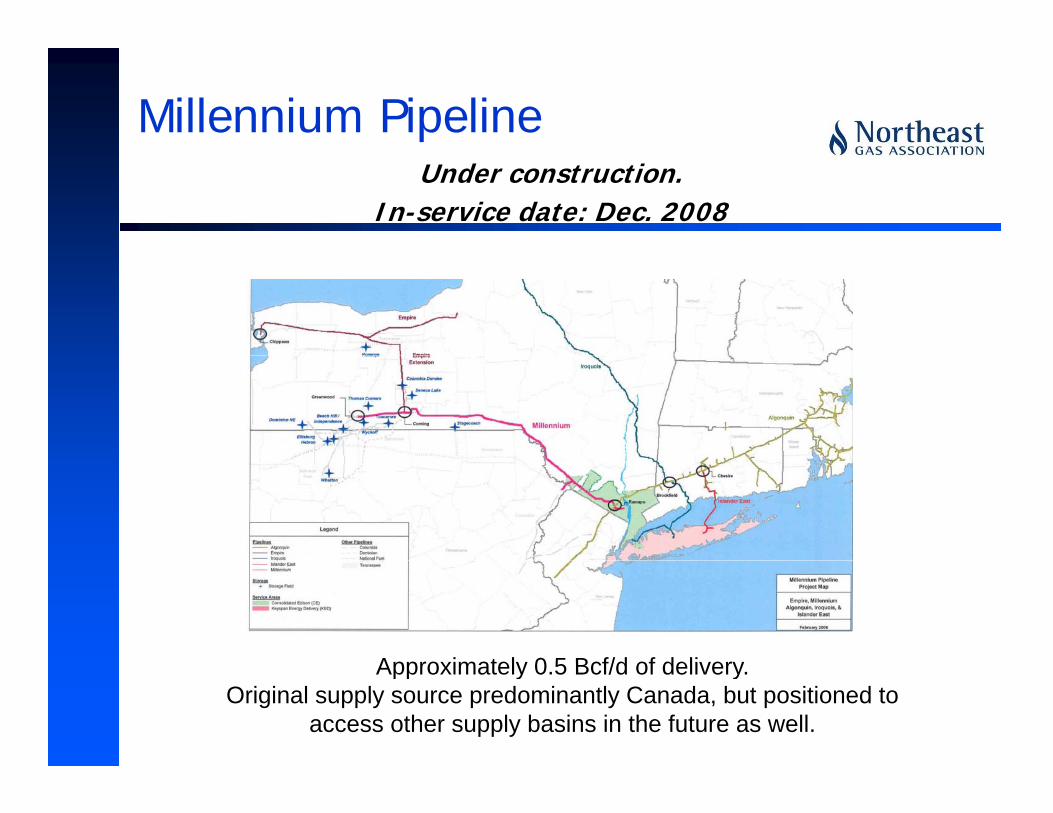

Millennium PipelineUnder construction.

In-service date: Dec. 2008

Approximately 0 5 Bcf/d of deliveryApproximately 0.5 Bcf/d of delivery.Original supply source predominantly Canada, but positioned to

access other supply basins in the future as well.

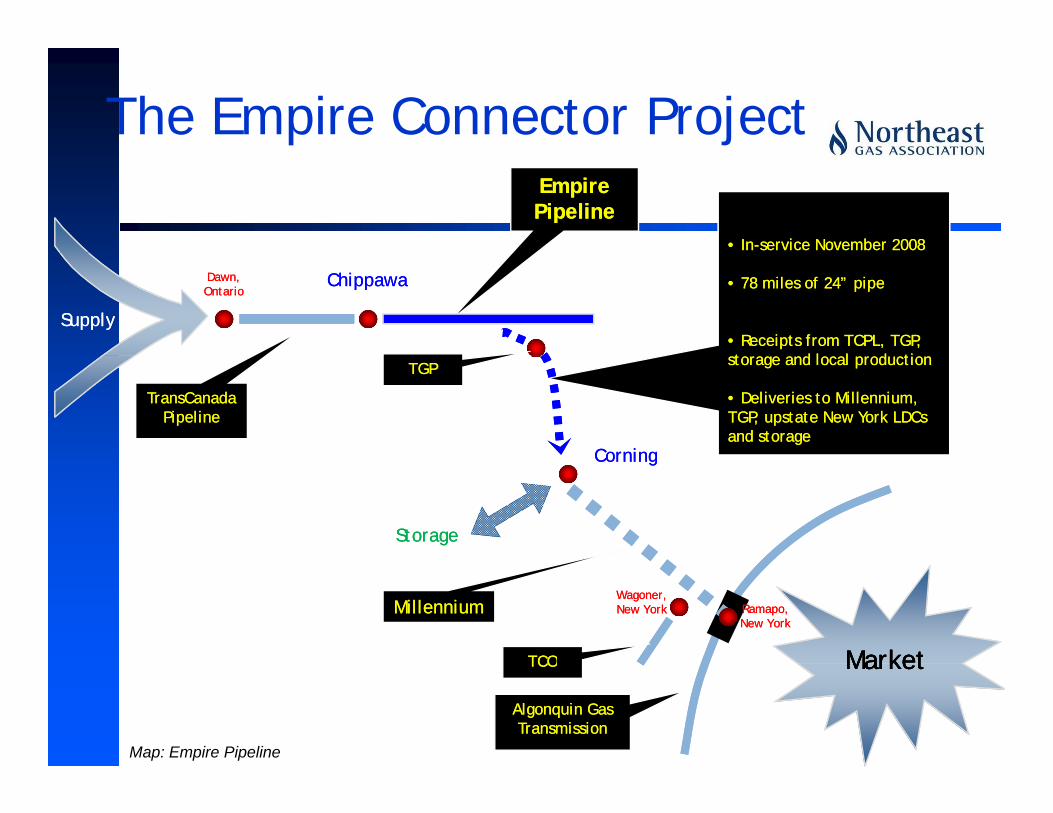

The Empire Connector ProjectEmpireEmpirePipelinePipeline

•• InIn--service November 2008service November 2008

SupplySupply

Dawn,Dawn,OntarioOntario

ChippawaChippawa •• 78 miles of 24” pipe78 miles of 24” pipe

•• Receipts from TCPL, TGP, Receipts from TCPL, TGP, t d l l d tit d l l d ti

CorningCorning

TransCanadaTransCanadaPipelinePipeline

storage and local productionstorage and local production

•• Deliveries to Millennium, Deliveries to Millennium, TGP, upstate New York LDCs TGP, upstate New York LDCs and storageand storage

TGPTGP

CorningCorning

StorageStorage

MarketMarketMarketMarket

Wagoner,Wagoner,New YorkNew York Ramapo,Ramapo,

New YorkNew York

TCOTCO

MillenniumMillennium

MarketMarketMarketMarket

Algonquin GasAlgonquin GasTransmissionTransmission

TCOTCO

Map: Empire Pipeline

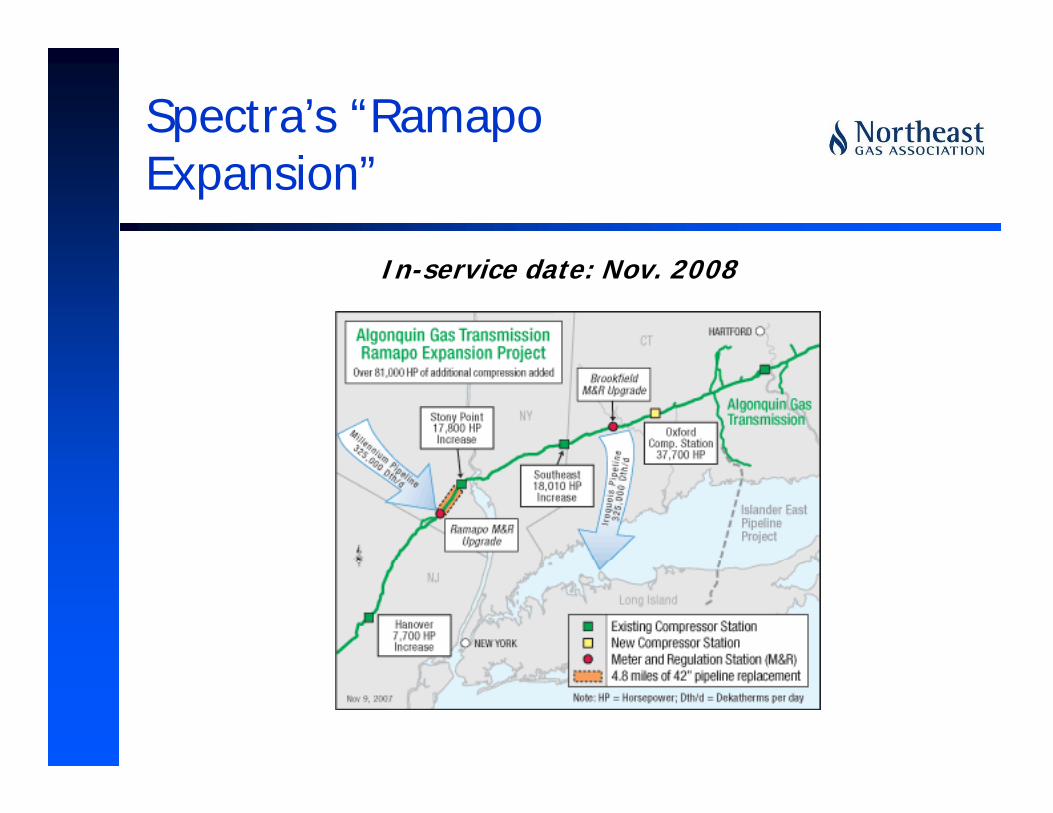

Spectra’s “Ramapo Expansion”

In-service date: Nov. 2008

Iroquois’s “MarketAccessExpansion”

MarketAccessExpansion

Shipper Consolidated Edison Company of NewShipper Consolidated Edison Company of New York

MDQ 100,000 Dt/d (11/1/08)

Receipt Point

Brookfield (100 MDt/d)

D li H t P i t (100 MDt/d)Delivery Point

Hunts Point (100 MDt/d)

Facilities Brookfield, CT – New compressor station – 7700 HP Solar T60

transfer unit – Coolers

Dover Compressor Station

Dover, NY – Coolers

Brookfield Compressor Station

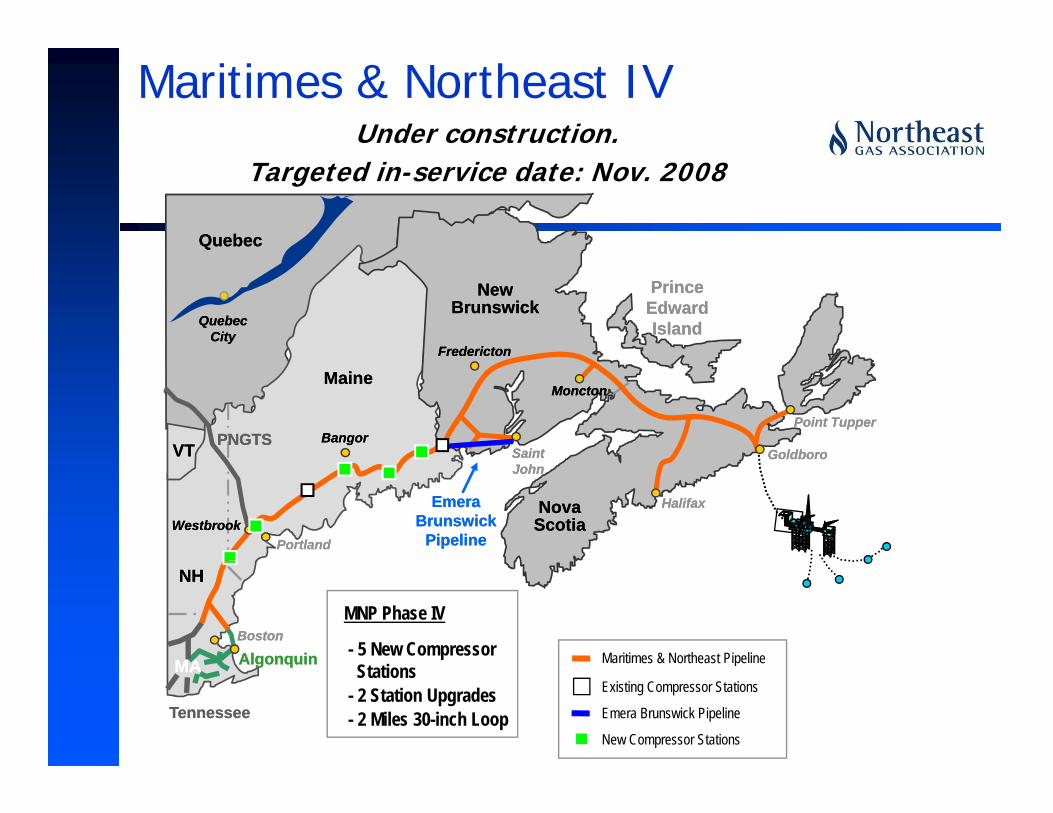

Maritimes & Northeast IVUnder construction.

QuebecQuebec

Targeted in-service date: Nov. 2008

Quebec Quebec CityCity

New New BrunswickBrunswick

Prince Prince Edward Edward IslandIsland

FrederictonFredericton

MonctonMonctonMaineMaine

VTVT

FrederictonFredericton

GoldboroGoldboroBangorBangor

Saint Saint

Point TupperPoint TupperPNGTSPNGTS

PortlandPortland

Nova Nova ScotiaScotia

HalifaxHalifax

GoldboroGoldboroJohnJohn

WestbrookWestbrookEmera Emera

Brunswick Brunswick PipelinePipeline

Maritimes & Northeast Pipeline

NHNH

BostonBoston

AlgonquinAlgonquinMAMA

MNP Phase IV

- 5 New Compressor

TennesseeTennessee

a t es & o t east pe e

Existing Compressor Stations

Emera Brunswick Pipeline

New Compressor Stations

AlgonquinAlgonquinMAMA Stations- 2 Station Upgrades- 2 Miles 30-inch Loop

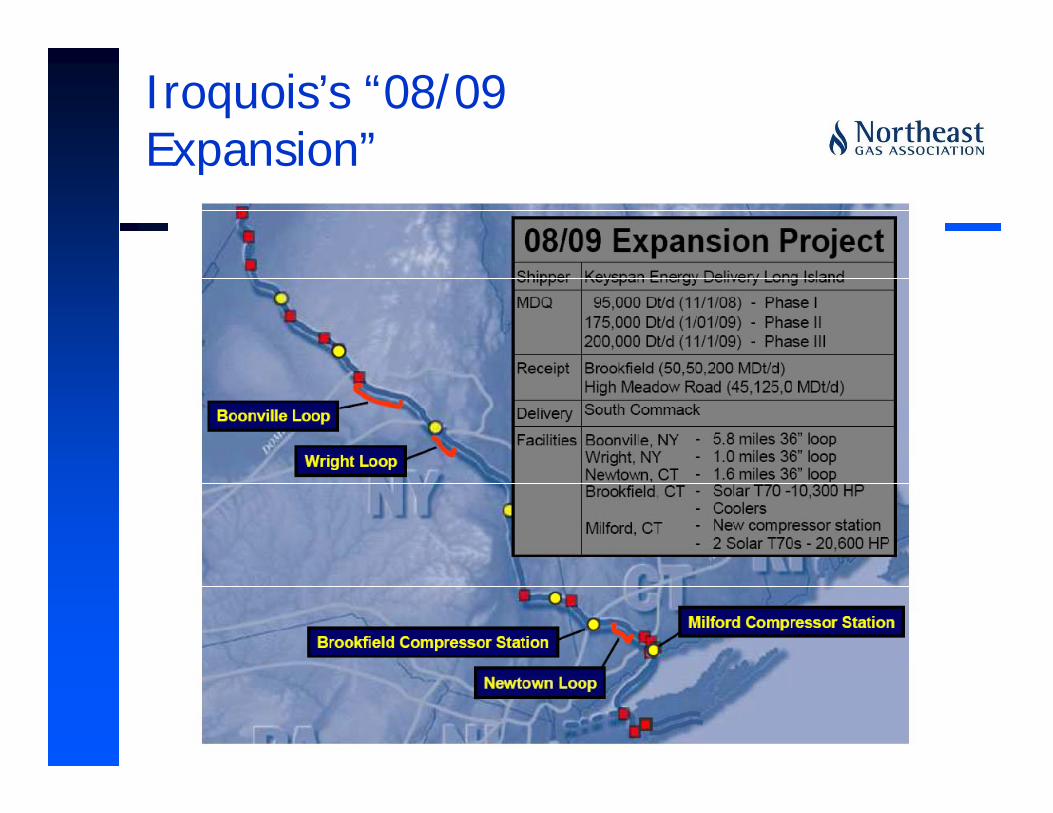

Iroquois’s “08/09 Expansion”Expansion

Infrastructure Enhancements:

Operational in 2009Ope at o a 009

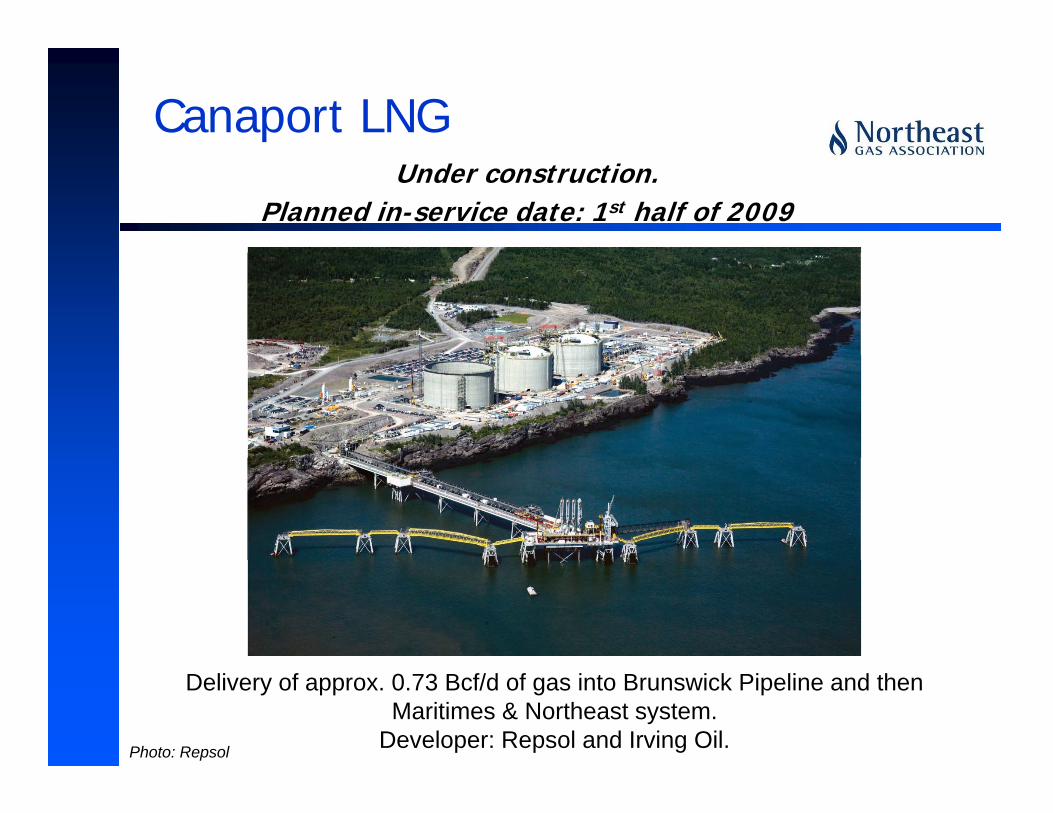

Canaport LNGUnder construction.

Planned in-service date: 1st half of 2009

Delivery of approx. 0.73 Bcf/d of gas into Brunswick Pipeline and then Maritimes & Northeast system.

Developer: Repsol and Irving Oil.Photo: Repsol

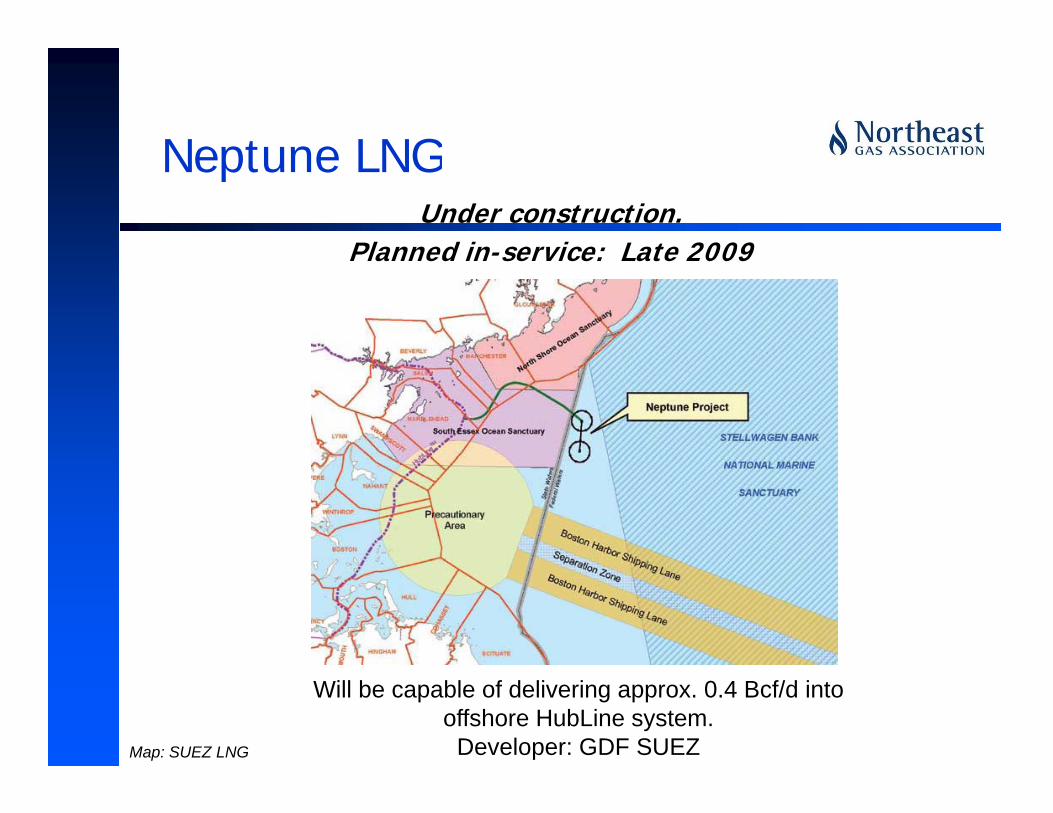

Neptune LNGNeptune LNGUnder construction.

Planned in-service: Late 2009Planned in-service: Late 2009

Will be capable of delivering approx. 0.4 Bcf/d into offshore HubLine system.

Developer: GDF SUEZ Map: SUEZ LNG

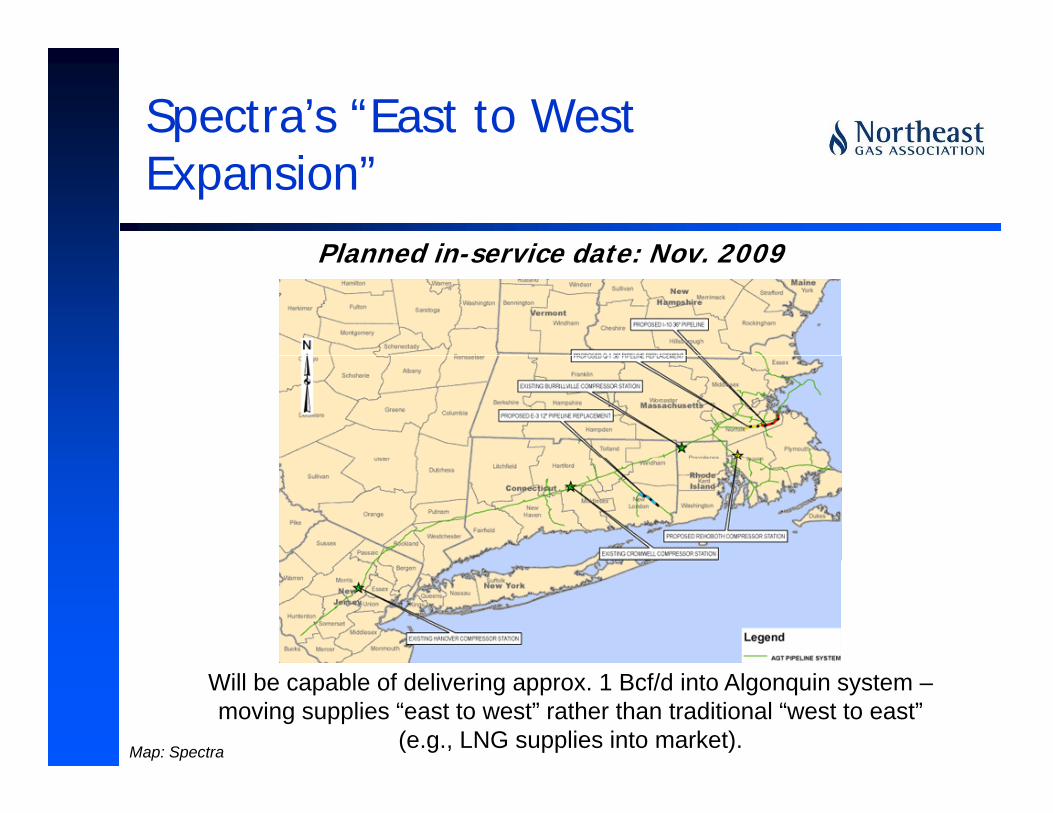

Spectra’s “East to West Expansion”

Planned in-service date: Nov 2009Planned in-service date: Nov. 2009

Will be capable of delivering approx. 1 Bcf/d into Algonquin system –moving supplies “east to west” rather than traditional “west to east”

(e.g., LNG supplies into market).Map: Spectra

On the Supply Horizon:Rockies Gas &Marcellus Shale

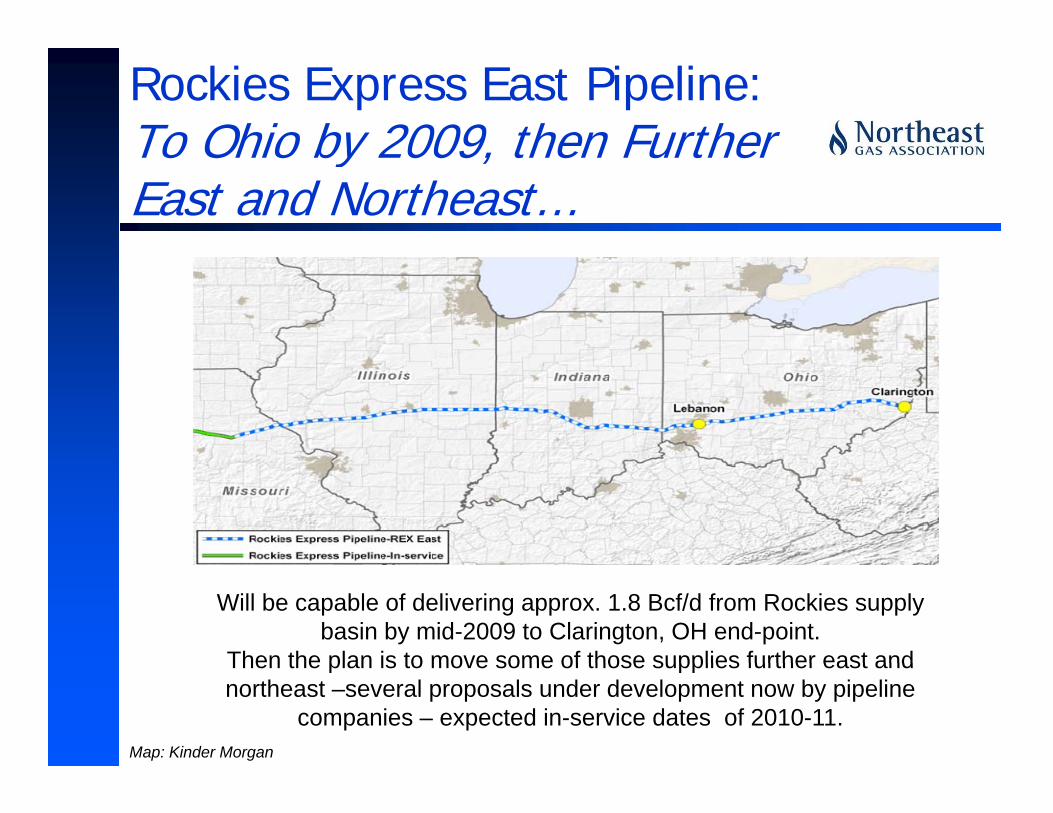

Rockies Express East Pipeline: To Ohio by 2009 then FurtherTo Ohio by 2009, then Further East and Northeast…

Will be capable of delivering approx. 1.8 Bcf/d from Rockies supply basin by mid-2009 to Clarington, OH end-point.

Then the plan is to move some of those supplies further east andThen the plan is to move some of those supplies further east and northeast –several proposals under development now by pipeline

companies – expected in-service dates of 2010-11.Map: Kinder Morgan

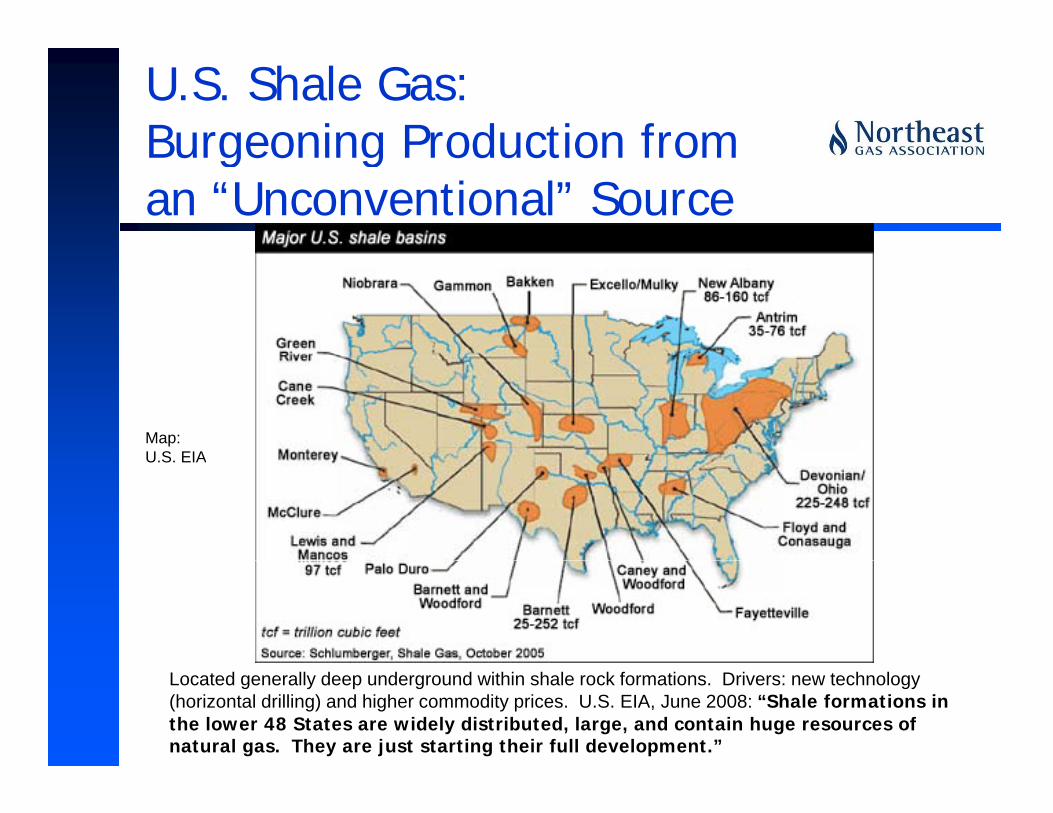

U.S. Shale Gas:Burgeoning Production fromBurgeoning Production from an “Unconventional” Source

Map:U S EIAU.S. EIA

Located generally deep underground within shale rock formations. Drivers: new technology (horizontal drilling) and higher commodity prices. U.S. EIA, June 2008: “Shale formations in the lower 48 States are widely distributed, large, and contain huge resources of natural gas. They are just starting their full development.”

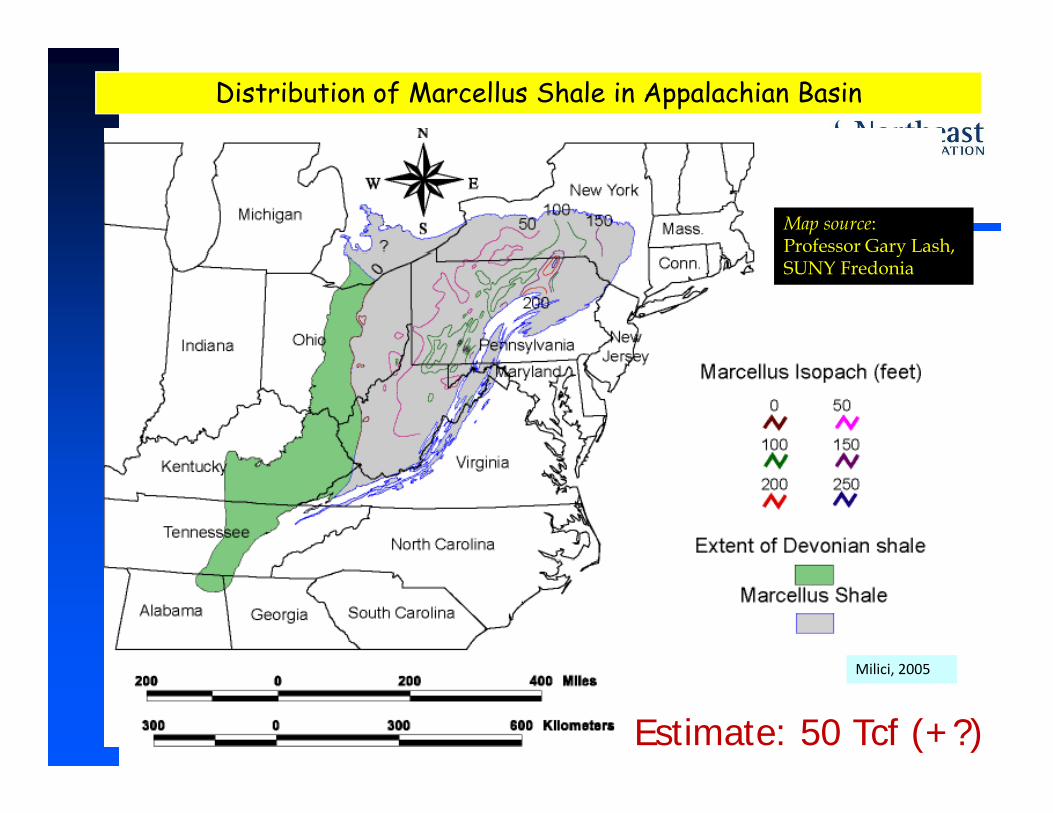

Distribution of Marcellus Shale in Appalachian Basin

Map source: Professor Gary Lash, y ,SUNY Fredonia

Milici, 2005

Estimate: 50 Tcf (+?)

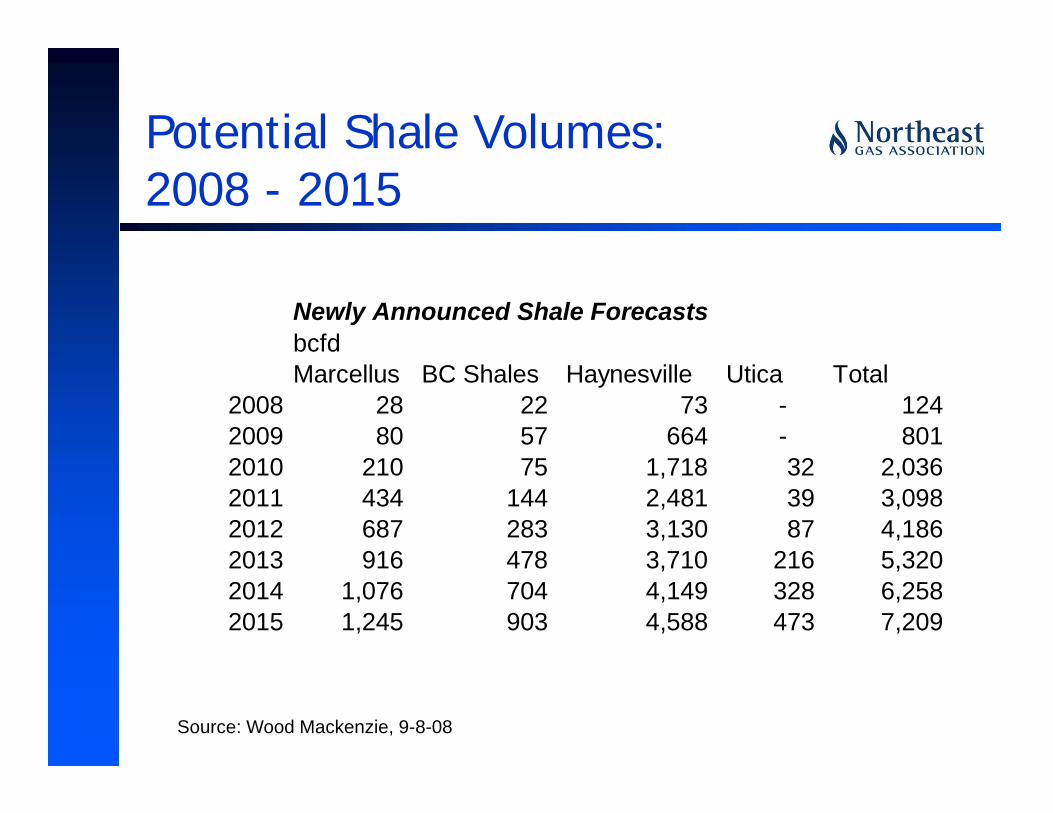

Potential Shale Volumes:2008 - 2015

Newly Announced Shale ForecastsbcfdMarcellus BC Shales Haynesville Utica Total

2008 28 22 73 - 124 2009 80 57 664 - 801 2010 210 75 1 718 32 2 0362010 210 75 1,718 32 2,036 2011 434 144 2,481 39 3,098 2012 687 283 3,130 87 4,186 2013 916 478 3 710 216 5 3202013 916 478 3,710 216 5,320 2014 1,076 704 4,149 328 6,258 2015 1,245 903 4,588 473 7,209

Source: Wood Mackenzie, 9-8-08

75 Second Avenue, Suite 510Needham, MA 02494-2824

Tel. 781-455-6800

1515 Broadway, 43rd floorNew York, NY

Tel. 212-354-4790

www.northeastgas.org