Embed Size (px)

DESCRIPTION

Marketing Strategies

Citation preview

EFFECTS OF MARKETING STRATEGIES ON PERFORMANCE OF

COMMERCIAL BANKS IN KENYA: A CASE STUDY OF CO-OPERATIVE

BANK NAROK BRANCH.

BY

MOSES TOPOTI

A RESEARCH PROJECT TO BE SUBMITTED IN PARTIAL FULFILMENT OF

THE REQUIREMENT FOR THE AWARD OF DIPLOMA IN MANAGEMENT

(BUSINESS MANAGEMENT OPTION) OF THE KENYA INSTITUTE OF

MANAGEMENT

NOVEMBER 2013

ii

DECLARATION

iii

DEDICATION

This work is dedicated to my loving family members, my dear wife Margaret and my

loving boy Mark and to my dear mum Ann. To you all thank you very much for the

support.

iv

ACKNOWLEDGEMENTS

I begin in the name of God, Most Beneficent and Most Merciful. Praise to God for

providing me with great health, strength and emotional support in completing this

dissertation. It is with great appreciation that I acknowledge the contributions and support

in completing this dissertation.

It is with great appreciation that I acknowledge the contributions and support of my

supervisor Dick Safari whose time, effort and guidance were highly beneficial especially

during the study.

My heartfelt appreciation to my family members who were forced to understand their

son‟s need to be away most of the times, their endless support, encouragement and

understanding throughout my good times as well as my tough times are so meaningful.

Finally I acknowledge the respondent of the study for cooperation during the study, may

God Almighty bless them abundantly.

v

ABSTRACT

The purpose of this study was to determine the effects of marketing strategies on

performance of commercial banks in Kenya, a case study of co-operative bank-narok

branch. The specific objectives were; to find out the availability of marketing strategies in

co-operative bank-Narok branch, to determine whether marketing strategies improves the

co-operative bank‟s competition in the market, to determine whether marketing strategies

increases revenue collections of co-operative bank-Narok branch and to find out whether

marketing strategies improves the corporate image of co-operative bank-Narok branch. A

descriptive research design was used in the study. The target population of the study was

67 employees of co-operative bank-Narok branch. The study used stratified random

sampling to select a sample size of 40 employees of co-operative bank-Narok branch.

Data was collected using questionnaires which were distributed to the respondents who

came from co-operative bank-Narok branch. Data was tabulated and analyzed using

descriptive statistics and it was presented using tables, bar graphs and pie charts. The

findings indicated that marketing strategies affects the performance of the organization.

The study therefore recommends that banks should embark, from time to time on

marketing research. This is because effective marketing strategies are a product of

marketing research. Thus, good and adequate marketing mix is a product of effective

marketing research too. Marketing research will bring about innovation, better services

for customer and better method of production and processing. The study shall provide

Scholars in the field of strategic management and marketing as they will use this

information to understand the state of the sector better. They will also use the information

as a reference point to research on the strategy formulation and innovations in other

industries.

vi

TABLE OF CONTENTS

DECLARATION……………………….…………..………………….….......…………..ii

DEDICATION…………………………………….….……………..…………...……….iii

ACKNOWLEDGEMENT…………………………………..…………………………... iv

ABSTRACT …………………………………………………....…………………………v

TABLE OF CONTENTS ………………………………………...………………….…...vi

LIST OF TABLES……………………………………………………………….……..viii

LIST OF FIGURES……………………………………………………………...……….ix

ABBREVIATIONS AND ACRONYMS……………………………......…………….….x

DEFINITION OF OPERATIONAL TERMS……………………………………...….....xi

CHAPTER ONE…………………………………………………………………………1

1.0 INTRODUCTION OF THE STUDY…………………………………………………1

1.1 Background of the Study……………………………………………………………...1

1.2 Statement of the Problem……………………………………………………………...6

1.3 Purpose of the Study…………………………………………………………………..7

1.4 Objectives of the Study………………………………………………………………..7

1.5 Research Questions……………………………………………………………………7

1.6 Significance of the Study……………………………………………………………...8

1.7 Limitations of the Study……………………………………………………………….8

1.8 Scope of the Study…………………………………………………………………….9

CHAPTER TWO……………………………………………………………………….10

2.0 LITERATURE REVIEW………………………………...………………………….10

2.1 Introduction…………………………………………………………………………..10

2.2 Review of Related Literature………………………………………………………...10

2.2.1 Availability of Marketing Strategies in Commercial Banks……………………….13

2.2.2 Marketing Strategies and the Bank‟s Competition in the Market ………………...18

2.2.3 Marketing Strategies and the Corporate Image of Commercial Banks……………22

2.3 Review of Analytical Literature……………………………………………………...24

2.4 Summary of the Review……………………………………………………………...28

2.5 Conceptual Framework of the Study…………………………………………….......28

vii

CHAPTER THREE…………………………………………………………………….30

3.0 RESEARCH DESIGN AND METHODOLOGY……………………..…………….30

3.1 Introduction…………………………………………………………………………..30

3.2 Research Design……………………………………………………………………...30

3.3 Target Population of the Study………………………………………………………30

3.4 Sample Size and Sampling Procedure……………………………………………….30

3.5 Data Collection Instruments and Procedure…………………………………………31

3.6 Data Analysis………………………………………………………………………...32

CHAPTER FOUR………………………………………………………………………33

4.0 DATA ANALYSIS, PRESENTATION AND INTERPRETATION…………….…33

4.1 Introduction…………………………………………………………………………..33

4.2 Presentation and Findings……………………………………………………………33

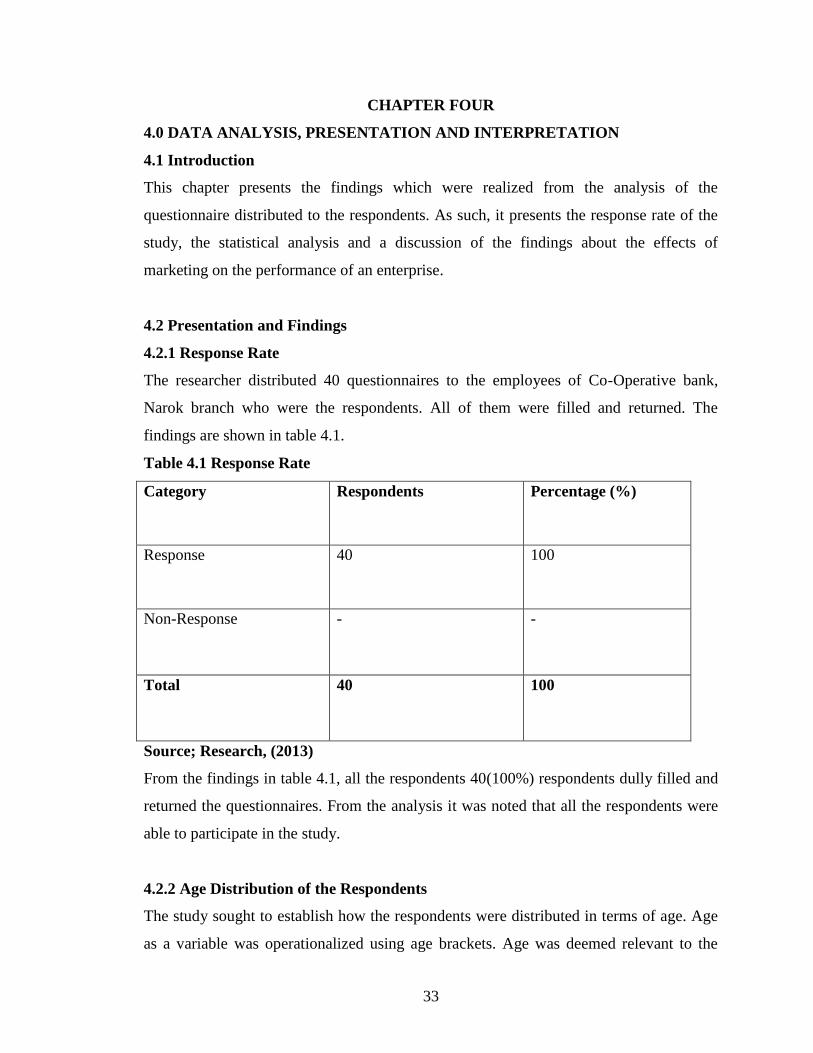

4.2.1 Response Rate……………………………………………………………………...33

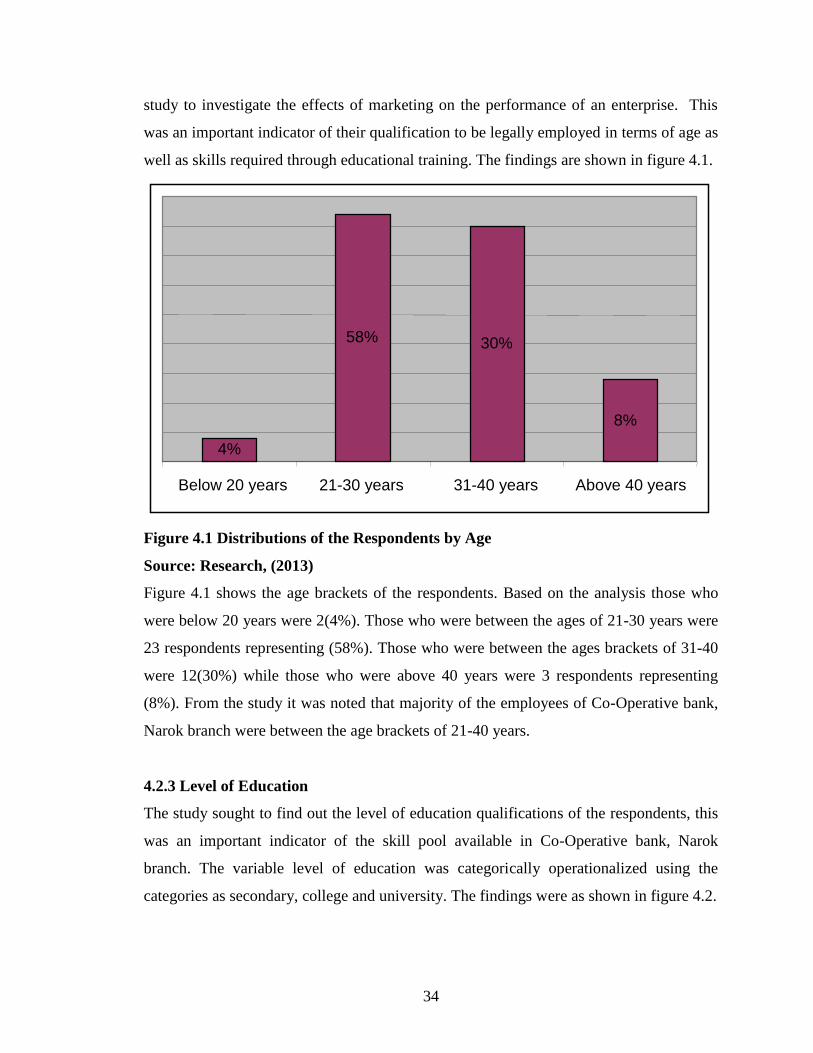

4.2.2 Age Distribution of the Respondents………………………………………………33

4.2.3 Level of Education…………………………………………………………………34

4.2.4 Work Experience of the Respondents……………………………………………...35

4.2.5 Current Department………………………………………………………………..36

4.3 Availability of Marketing Strategies in Co-Operative Bank-Narok…........................37

4.4 Marketing Strategies and the Bank‟s Competition in the Market…….……………...40

4.5 Marketing Strategies and the Corporate Image of the Bank…………………….…...42

4.6 Summary of the Chapter…………….……………………………………………….44

CHAPTER FIVE……………………………………………………………………….45

5.0 SUMMARY, CONCLUSION AND RECOMMENDATIONS………………..……45

5.1 Introduction…………………………………………………………………………..45

5.2 Summary of the Findings…………………………………………………………….45

5.3 Conclusion of the Study……………………………………………………………...46

5.4 Recommendations of the Study……………………………………………………...48

5.5 Areas for Further Research…………………………………………………………..48

REFERENCES…………………………………………………………………………..50

APPENDIX I: LETTER OF INTRODUCTION……………..…………………………53

II: QUESTIONNAIRE……………………………………………………...54

viii

LIST OF TABLES

Table 4.1 Response Rate…………………………………………………………………33

Table 4.2 Marketing……………………………………………………………………...38

Table 4.3 Rating of Marketing…………………………………………………………...38

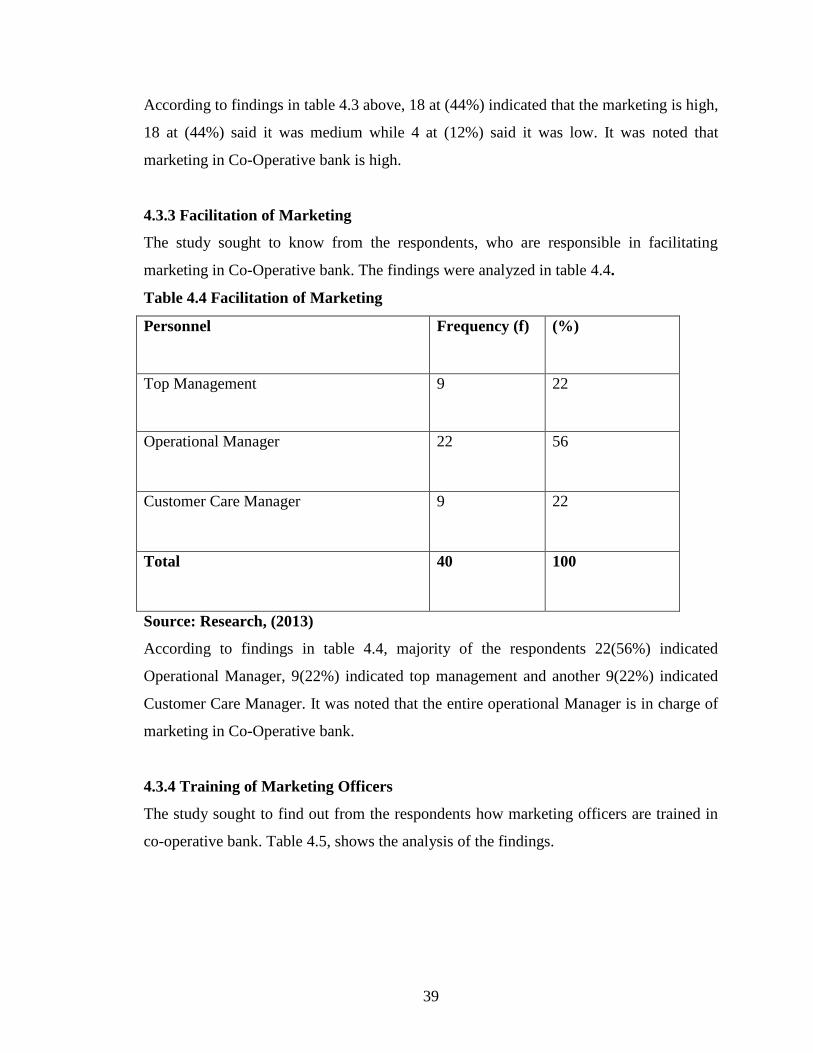

Table 4.4 Facilitation of Marketing……………………………………………………...39

Table 4.5 Training of Marketing Officers……………………………………………….40

Table 4.6 Marketing Strategies…………………………………………………………..40

Table 4.7 Competition of the Bank………………………………………………………41

Table 4.8 Rating of Competition…………...……………………………………………42

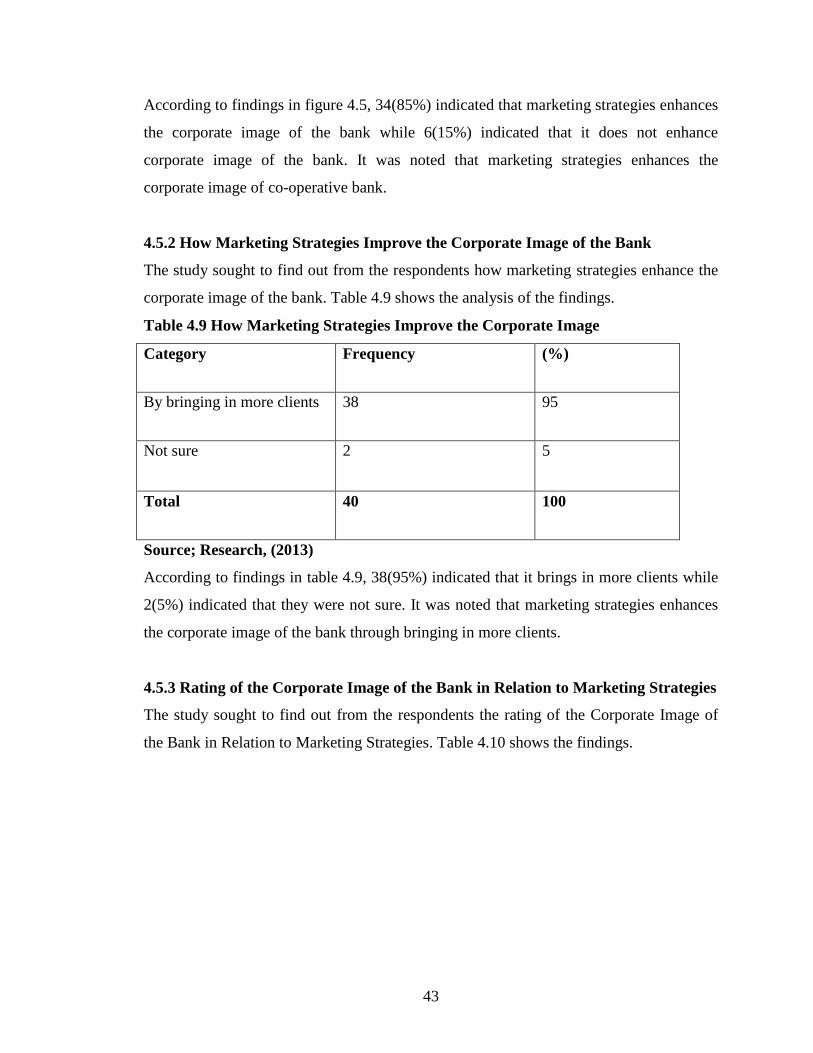

Table 4.9 How Marketing Strategies Improve the Corporate Image ……………….…...43

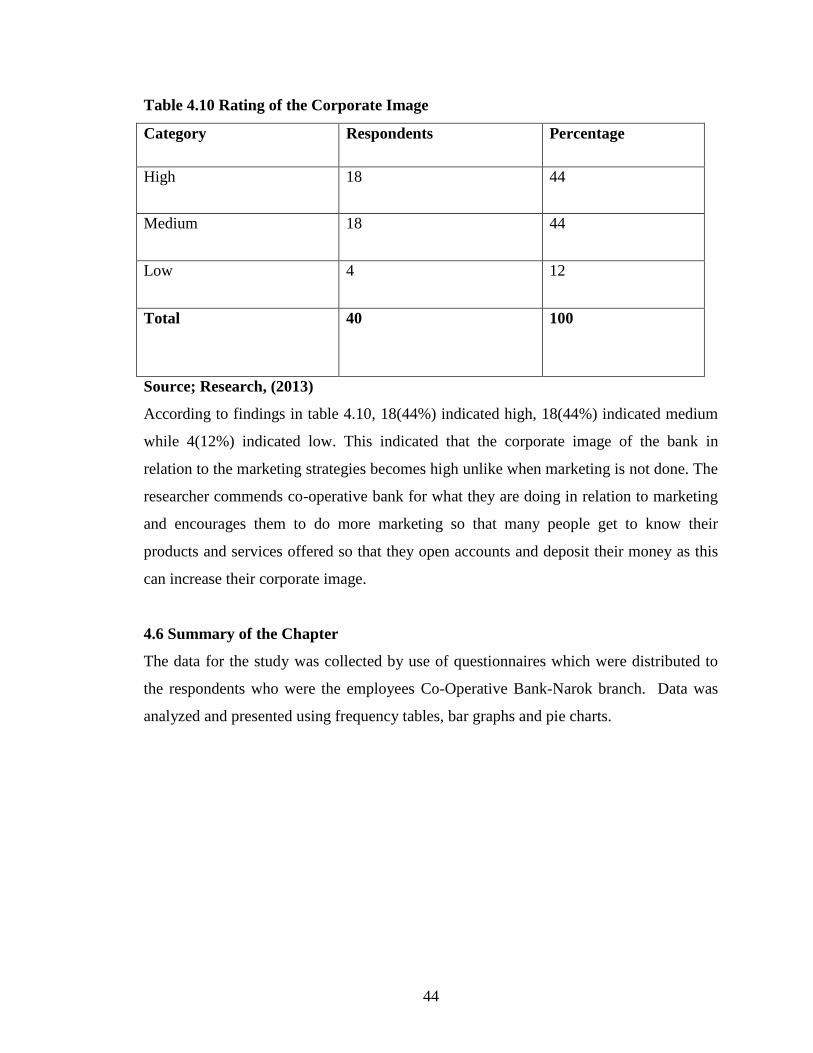

Table 4.10 Rating of Corporate Image…………………………………………………..44

ix

LIST OF FIGURES

Figure 2.1 Conceptual Framework………………………………………….…………...28

Figure 4.1 Distributions of the Respondents by Age…………………………………….34

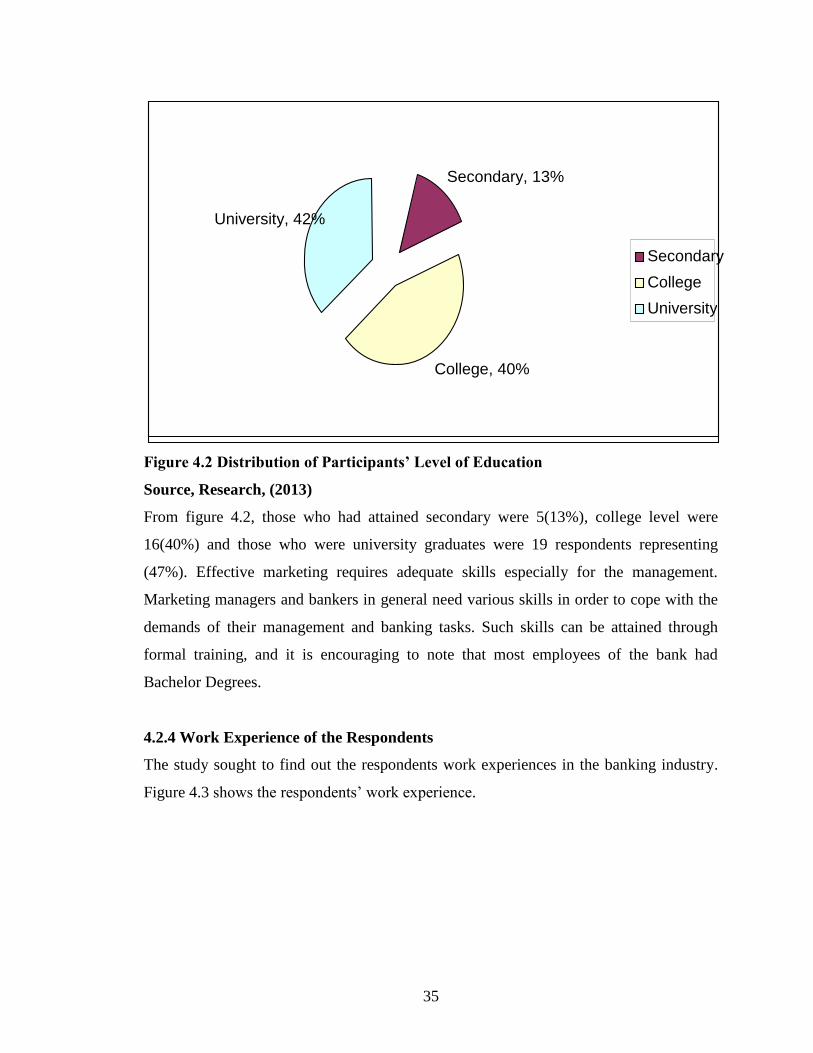

Figure 4.2 Distribution of Participants‟ Level of Education……………………………..35

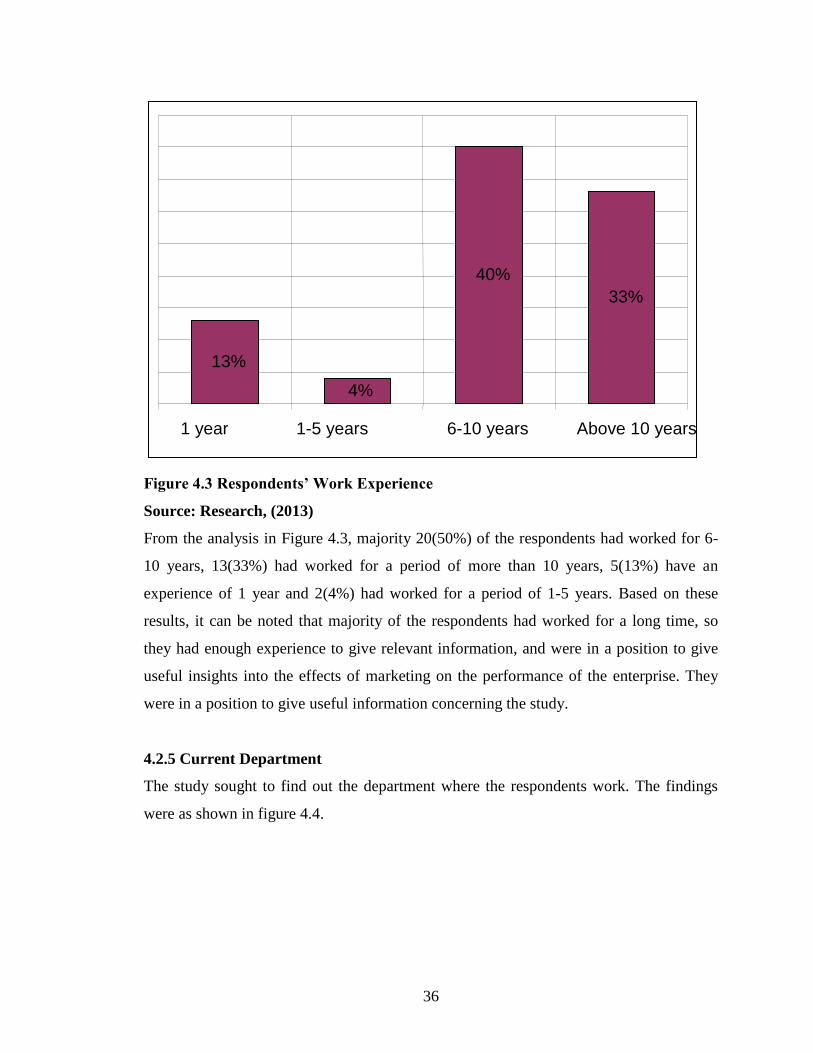

Figure 4.3 Respondents‟ Work Experience……………………………………………...36

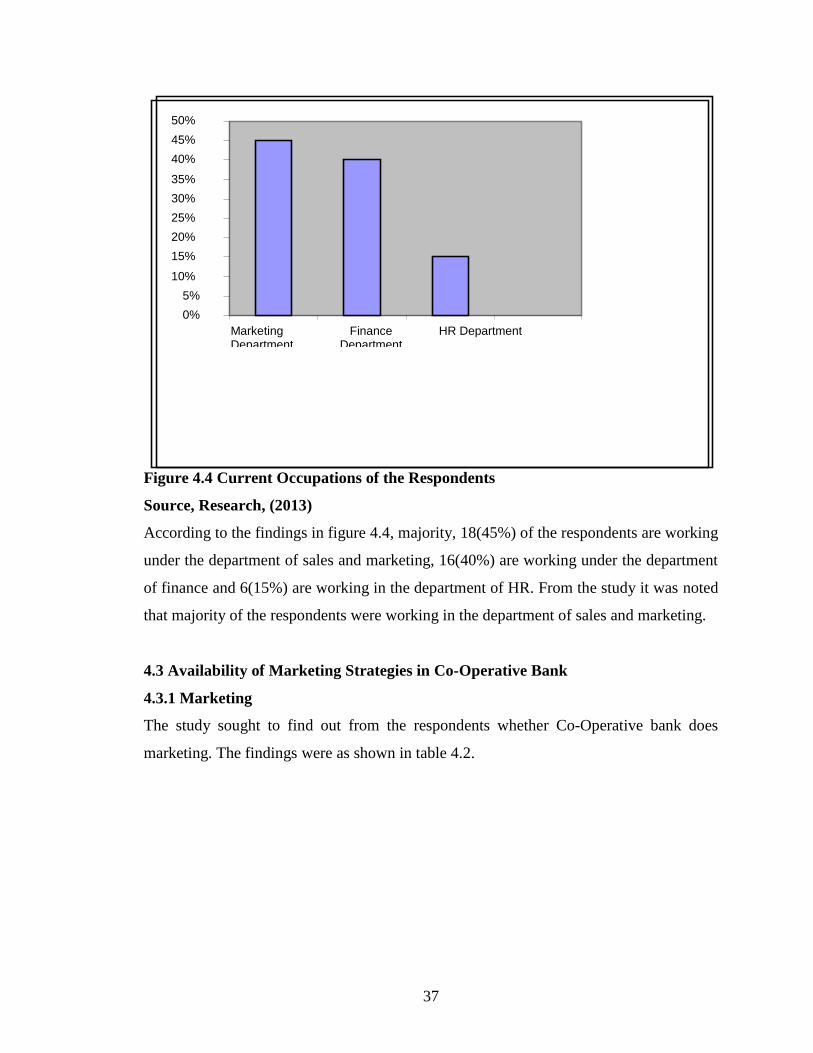

Figure 4.4 Current Occupations of the Respondents…………………………………….37

Figure 4.5 Marketing Strategies and Corporate Image…………………………..………42

x

LIST OF ABBRIVIETIONS AND ACRONYMS

F- Frequency

KCB- Kenya Commercial Bank

SME- Small and Medium Enterprises

SWOT- Strength, Weakness, Opportunities and Threats

xi

DEFINATION OF OPPERATIONAL TERMS

Availability-Availability refers to a state of being at hand when needed. Marketing

strategies availability can boost the organization‟s performance as it makes the business

and its products and services known to the clients.

Competition-It is the rivalry between people or organizations. Marketing strategies can

bring about competitions and in return it can make the organization offer quality services

to the clients.

Corporate Image-Corporate image refers to the business unit. Marketing strategies can

improve the corporate image of the business in that efficiency is increased.

Revenue- Refers to the income of an organization. Marketing strategies improves the

revenue of an organization as it makes the organization known to the public.

1

CHAPTER ONE

2.0 INTRODUCTION TO THE STUDY

This chapter deals with the background of the study, the statement of the problem,

objectives of the study, research questions, significance of the study, scope of the study,

limitation of the study and the conceptual frame work.

1.1 Background of the Study

A market-focused organization first determines the potential customer‟s desire, and then

builds the products or services. Marketing theory and practice are justified in the belief

that customers use a product or service because they have a need, or because it provides a

perceived benefit (Kotler and Keller, 2006). Two major factors of marketing are the

recruitment of new customers (acquisition) and the retention and expansion of

relationships with existing customers (base management). For marketing plan to be

successful, the mix of the four “Ps” must reflect the wants and desires of the consumers

in the target market.

Trying to convince a market segment to buy something they do not want is extremely

expensive and seldom unsuccessful. Marketers depend on insights from marketing

research, both formal and informal, to determine what consumers want and what they are

willing to pay for. Marketers hope that this process will give them a sustainable

competitive advantage. The study of Akinyele (2011) for the oil and gas sector in Nigeria

suggest that strategic marketing is a driver of organizational positioning in a dynamic

environment, and that it helps to enhance the development of new product for existing

markets.

Banks offer a wide range of financial services, to personal and business customers; some

of these services which are bank account, guarantorship, and investment adviser are

needed by an appreciable number of customers, but many other financial services such as

import/export services, money transfers, credit cards that will be brought to the attention

of bank‟s potential customers, whom then must be persuaded to use them (Abolaji, 2009).

2

Many services offered by banks are also offered by „rival‟ organizations. Building

societies have developed customer accounts which are similar in many ways to a bank

account.

Thrift and cooperative societies provide lending services to their numerous members and

indirectly to the society at large. Solicitors act as executors and trustees and accountants

give advice and so on. Banks not only compete with each other but also have to contend

with challenges from other types of organization in the market. To do this successfully,

bankers need an understanding of the process of marketing which will aid in improving

banks performance. Marketing is an area of activity infamous for re-inventing itself and

its vocabulary according to the times and the culture. Marketing is all about acquiring

new customers and retaining existing customers (Abolaji, 2009).

The concept of marketing has received a great deal of attention from Scholars in the field

of marketing. The concept has been investigated from many perspectives and examined

in many ways indicating its conceptual and practical importance. Marketing concept is

based on the paradigm of a true balance between "giving and getting" as a key benefit to

encourage an active role and is conducive in delivering two- way value, where loyalty is

based on trust and partnership, will prove to be one of the most significant policies to be

pursued in development and sustenance of competitive advantage (Abolaji, 2009).

According to Abolaji, (2009), the real purpose of business is to create and sustain

mutually beneficial relationships, especially with selected customers. With the main

proposition which assume that successful relationships is the two-way flow of value.

Positive relationship has been established between marketing and organization

performance. Marketing usually results in strong economic, technical and social ties

among the stakeholder‟s parties thereby reducing their transactions costs and increasing

exchange efficiencies included in marketing which are not only buyers or sellers

exchanges but also business partnerships, strategic alliances and cooperative marketing

networks.

3

The relationship typically involves seller- customer exchange, but it could involve any

stakeholder‟s relationship (Morgan and Hunt, 1994). Abolaji, (2009) opines that

marketing emphasizes that relationships are partnerships with emphasis on social

bonding, co-operation and joint problem solving, sharing resources and activities and

basing relationship on common goals. He, however, challenged that the benefit should be

relational and dyadic too. Most of the studies have been emphasizing the effect of

marketing on organization performance neglecting customer benefits. Moreover,

relationship marketing emphasizes that long-term relationships are mutually beneficial.

In any genuine relationship, both parties involved should be beneficiaries of the outcome

of such relationship. Ismail (2009) observed that if genuine partnerships, as marketing

suggests exist, relational quality and relational benefits must be of great value. Drawing

inspiration from similar study conducted by Ismail (2009) in Jordianian Insurance

companies. This study seeks to examine the strategies used by Commercial banks in

Kenya to deal with Service breakdown. A company‟s strategy consists of the business

approaches and initiatives it undertakes to attract customers and fulfill their expectations,

to withstand competitive pressures and to strengthen its market position.

These strategies provide opportunities for the organization to respond to the various

challenges within its operating environment. Firms also develop strategies to enable them

seize strategic initiatives and maintain a competitive edge in the market (Porter, 1985).

The competitive aim is to do a significantly better job to its customers. The success of

every organization is determined by its responsiveness to the customer needs. The

competitive aim is to do a significantly better job of providing what customers are

looking for, thereby enabling the company to earn a competitive advantage and outsmart

rivals in the market place.

The core of a company‟s marketing strategy consists of its internal initiatives to deliver

satisfaction to customers but also includes offensive and defensive moves to counter the

maneuvering of rivals, actions to shift resources around to improve the firm‟s long term

competitive capabilities and market position, and tactical efforts to respond to prevailing

4

market conditions. Assuming that there are a number of providers, customers will choose

which offering to accept on their perception of value-for-money. Finance has been

identified as the most important factor determining the survival and growth of small and

medium sized enterprises in Kenya.

Access to finance allows Small and Medium Enterprises (SME‟s) to undertake

productive investments to expand their businesses and to acquire the latest technologies,

thus ensuring their competitiveness and that of the nation as a whole. Poorly functioning

financial systems can seriously undermine the microeconomic fundamentals of a country,

resulting in lower growth in income and employment (Griliches, 1998). Landes (1998)

argues that despite their dominant numbers and importance in job creation, SME‟s

traditionally have faced difficulties in obtaining formal credit or equity. These difficulties

are what the commercial banks call service breakdown.

For example, maturities of commercial bank loans extended to SME‟s are often limited to

a period far too short to pay off any sizeable investment; secondly SME‟s are regarded by

creditors and investors as high-risk borrowers due to insufficient assets and low

capitalization, vulnerability to market fluctuations and high mortality rates; thirdly

information asymmetry arising from SME‟s‟ lack of accounting records, inadequate

financial statements or business plans makes it difficult for creditors and investors to

assess the creditworthiness of potential SME proposals; and lastly is the high

administrative/transaction costs of lending or investing small amounts do not make SME

financing a profitable business (Griliches, 1998).

To compete effectively in the SME financing sector, and faced with this service

breakdown, commercial banks need to provide financial services that meet the

specialized needs of SME‟s while coping with the high risks and costs associated with

servicing them (Landes, 1998). To achieve this, an increasing number of banks have

adopted separate strategies to service SME customers. The current trend is to shift from a

product-based focus to a more customer oriented focus of providing packages of financial

services tailored to their needs.

5

This has the potential of considerably improving the banks‟ relations with the SME

sector, as well as increasing the profitability of providing financial services to it (Landes,

1998). In Kenya, the rise of SME‟s has been hindered by financial challenges and

political instability (Carrier, 1999). Kenya has created conditions for private-sector

growth but is still held back by an inadequate financial system. Kenya‟s private sector

consists of mostly informal micro enterprises, operating alongside large firms. Most

companies are small because the private sector is new and because of legal and financial

obstacles to capital accumulation.

Between these large and small firms, SME‟s are very scarce and constitute a “missing

middle. Financing is necessary to help SME‟s set up and expand their operations, develop

new products, and invest in new staff or production facilities (Gomez-Mejia, 1998).

Many small businesses start out as an idea from one or two people, who invest their own

money and probably turn to family and friends for financial help in return for a share in

the business. But if they are successful, there comes a time for all developing SME‟s

when they need new investment to expand or innovate further. That is where they often

run into problems, because they find it much harder than larger businesses to obtain

financing from banks, capital markets or other suppliers of credit.

This “financing gap” is all the more important in a fast-changing knowledge-based

economy because of the speed of innovation (Groke and Kreidle 1997). Innovative

SME‟s with high growth potential, many of them in high-technology sectors, have played

a pivotal role in raising productivity and maintaining competitiveness in recent years. But

innovative products and services, however great their potential, need investment to

flourish (Carrier, 1999). If SME‟s cannot find the financing they need, brilliant ideas may

fall by the wayside and this represents a loss in potential growth for the economy.

The “bagless” vacuum cleaner and the “wind-up” radio or flashlight which need no

batteries are now common household items, but nearly failed to see the light of day

because their inventors could not find financial backing to transform their ideas into

production. Already, differences are emerging between countries in terms of how easy it

6

is for innovative SME‟s to grow and develop. This sector has been very dynamic in the

United States and a few other countries, but has lagged in many continental European

countries and Japan, to the detriment of job creation and competitiveness (Gomez-Mejia,

1998).

Improving access to finance of small and medium enterprises is crucial in fostering

entrepreneurship, competition, innovation and growth in Kenya. Access to sufficient and

adequate capital to grow and further develop their activities is a difficulty faced by many

Kenyan SME‟s. This situation is compounded by the difficulties in accessing finance as

SME financing is considered by many financial providers as a high risk activity that

generates high transaction costs and/or low returns on investment. Moreover SME‟s need

is to meet the challenge of adapting to the changing financial environment and the

increasing complexity and extent of financial acquisition (Gomez-Mejia, 1998).

1.2 Statement of the Problem

The practice of marketing has proved to be very important for all business performance in

all sectors of the economy. It has thus been the subject of much discussion over the past

decade since there has been a move from traditional marketing to customer orientation

where the customer is the king. In the today‟s volatile environment, organizations will

not survive in this changing environment unless they focused their attention to creating

and maintaining a formidable relationship with their customers. Existing literature

proposes that there is a positive relationship between marketing strategies and

organizational performance.

Numerous studies have shown positive links between loyalty and firm profitability. For

example, the work of Reichheld (1996) and Gronroos (2000) among others have been

significant in establishing the importance of marketing strategies and business

performance. Over the past years the interest in retaining customers has increased

considerably with marketing attention shifting gradually but definitely from mutually

independent transactions to loyalty-based repeat purchases (Berry, 1995 and Winer,

2001). Despite the existence of a large and growing body of literature on marketing

7

strategies in general, there is still some inadequacy surrounding the practice and how it

influences performance particularly in the banking sector. Although these studies

employed diverse methodologies and measures, they shared a common interest in

exploring the financial performance consequences of the basic tools, techniques, and

activities of formal strategic marketing for example, systematic intelligence- gathering,

market research, SWOT analysis, portfolio analysis, mathematical and computer model

of formal planning meetings and written long- range plans. The studies did not generally

examine the relationship between performance and the extent of formal planning;

variously referred to as comprehensiveness, rationality, formality, or simply, strategic

marketing. It is with this in mind that this study sets out to establish the effects of

marketing strategies on the performance of commercial banks in Kenya.

1.3 Purpose of the Study

The purpose of this study was to determine the effects of marketing strategies on the

performance of commercial banks in Kenya, a caser study of co-operative bank-Narok

branch.

1.4 Objectives of the Study

i. To find out the availability of marketing strategies in co-operative bank-Narok branch.

ii. To determine whether marketing strategies improves the co-operative bank‟s

competition in the market.

iii. To find out whether marketing strategies improves the corporate image of co-

operative bank-Narok branch.

1.5 Research Questions

i. Are there marketing strategies in co-operative bank, Narok branch?

ii. Does marketing strategies improve the co-operative bank‟s competition in the market?

iii. Does marketing strategies improve the corporate image of co-operative bank-Narok

branch?

8

1.6 Significance of the Study

This study is of significance in that Executives in the banking industry will be able to use

the findings of this study in drafting strategies on how to operate in the Kenyan market. It

will help them understand better the problems facing SME‟s as they relate with financial

institutions in their pursuit for survival. As a result, it is expected that the executives will

be able to formulate policies that are more benign to the sector. The investors in the SME

sector will use the information from this study to make decisions regarding investing in

the area. The findings of the research will expose some of the challenges they are likely

to encounter in their attempt to get banking services in Kenya.

As a result, the investors will be more endowed with knowledge and prepared to fit in the

prevailing banking environment. Scholars in the field of strategic management and

marketing will use the information to understand the state of the sector better. They will

also use the information as a reference point to research on the strategy formulation and

innovations in other industries. Finally, the Government will find the information useful

in diagnosing the problems affecting the SME sector and come up with regulative

solutions that would protect and help the SME‟s thrive.

1.7 Limitations of the Study

The limitation of this study included non respondent from the target population for the

fear of exposing the bank. Many of the marketing officers and managers have worked in

the for less than two years so they did not have much information on the main

contribution of marketing strategies to the bank. There is a high turnover of marketing

officers and managers from one bank to other banks or to senior positions in the same

bank. Some managers and officers feared giving some information due to victimization

by the employer. The researcher however overcame this limitation by targeted the

marketing officers who have worked in the bank for at least 2 years either doing the same

job or doing a different job in the same bank. Also the research questions were structured

in a way that they will not expose the bank to competition or pose a danger of giving

confidential information.

9

1.8 Scope of the Study

The study was carried out in Narok town, Narok County, Kenya. It addressed the effects

of marketing strategies on the banking sector, co-operative bank, Narok branch. The

target population of the study was 67 employees of co-operative bank, Narok branch.

Data was collected using questionnaires.

10

CHAPTER TWO

2.0 LITERATURE REVIEW

2.1 Introduction

In this chapter, the researcher presents a review of literature, the theoretical framework

and the conceptual framework of the study.

2.2 Review of Related Literature

Marketing is defined as the process of determining the needs and wants of consumers and

being able to deliver products that satisfy those needs and wants. Marketing includes all

of the activities necessary to move a product from the producer to the consumer.

Marketing starts with market research, a learning process in which marketers get to know

everything they can about the needs and wants of consumers, and it ends when somebody

buys something. Many companies feel that services provided to customers after the

purchase also are an important part of marketing (Lovelock et al, 1996).

With the rapid changes surrounding organizations, the traditional marketing mix of the 4

Ps has been criticized for being too myopic in this current market situation. The

traditional marketing mix has also been disparaged for being too product-focused and for

taking an overly inward-looking strategy with regards to the organization‟s resources and

capabilities in production matters. The service environment has evolved due to the

following factors: changing patterns of government regulation, technological innovations,

the service quality movement, pressures to improve productivity, relaxation of previous

professional association restrictions on marketing, internationalization and globalization

etc (Lovelock et al, 1996).

This has caused a lot of dynamism in the service sector: competition has increased and

consumers are exposed to more information. To survive, service companies have to

differentiate themselves mainly by being as close to the customer as possible; this has led

to an over emphasis in the area of service marketing to enable marketers in developing

service strategies to respond to the market. Service marketing concepts and strategies

have developed in response to the tremendous growth of service industries resulting in

11

their increased importance to world economies (Zeithaml and Bitner, 1996). This is in

relation to employment, gross domestic product and business opportunities.

As technological advancement has equalized most production processes, one of the few

remaining strategies that can set one company apart from others is customer service.

Chandler (1992) stated that strategy determines the basic long-term goals of an

enterprise, and the adoption of courses of action (strategy as plan of action) and the

allocation of resources necessary for carrying out these goals (strategy as re-source

allocation). While Porter (1996) viewed strategy as the process of creating a unique and

valuable position with means of a set of activities in a way that creates synergistic pursuit

of the objectives of a firm.

According to Mintzberg (1990), the term strategy is used to mean a plan, a ploy, a

pattern, a position or a perspective the 5 Ps. Mintzberg defines strategy in terms of a

process. Since strategy has almost inevitably been conceived in terms of what the leaders

of an organization plan to do in the future, strategy formation has, not surprisingly,

tended to be treated as an analytic process for establishing long-range goals and action

plans for an organization, that is, as one of formulation followed by implementation.

Strategy can be viewed as building defenses against the competitive forces, or as finding

positions in the industry which forces are weakest (Pearce & Robinson, 1997).

Strategy is all about competitions and trying to gain competitive advantage. Batemand

(1990) suggested that strategy is a pattern of actions and resource allocations designed to

achieve the goals of the organization. The strategy that an organization implements is an

attempt to match the skills and resources of the organization to the opportunities found in

the External Environment. Jauch (1998) argued that decisions and actions taken will lead

to the development of an effective strategy which will help to achieve organizational

objectives Porter (1990). Banking sector reforms and consolidation all over the world are

predicted upon the need for repositioning of the existing state of affairs in the sector in

order to attain an effective and efficient status.

12

This is more so in the developing nations like Kenya where the banking sector has not

been able to effectively provide the needed funds and services for the development of the

real sector as expected. Hence, banking reforms become inevitable in the light of the

global dynamic exigencies and emerging landscape. Consequently, the banking sector, as

an important sector in the financial landscape needs to be reformed in order to enhance its

competitiveness and capacity to play a fundamental role of financing investments. The

early strategic marketing performance studies date from the time of rapid expansion of

formal strategic marketing in the 1960s (Henry 1999).

Although same studies employed diverse methodologies and measures, they shared a

common interest in exploring the financial performance consequences of the basic tools,

techniques, and activities of formal strategic marketing for example, systematic

intelligence- gathering, market research, SWOT analysis, portfolio analysis,

mathematical and computer model of formal planning meetings and written long- range

plans. The studies did not generally examine the relationship between performance and

the extent of formal planning; variously referred to as comprehensiveness, rationality,

formality, or simply, strategic marketing (Henry 1999).

However, strategic marketing is a continuous and systematic process where people make

decisions about intended future outcomes, how these outcomes are to be achieved and

how success is to be measured and evaluated. Strategic marketing will help organizations

capitalize on their strengths, overcome their weaknesses, take advantage of opportunities

and defend themselves against threats. According to Allison and Kaye, (2005), strategic

marketing is making choices. It is a process designed to support leaders in being

intentional about their goals and methods. Differently expressed, strategic marketing is a

marketing management tool and like any tool, it is used for one purpose only namely to

help an organization to do its job better. Hence, strategic marketing is a systematic

process by which an organization agrees on and builds commitment among key

stakeholders to priorities that are essential to it and are responsive to the environment.

13

According to Bryson, (2004) strategic marketing is a disciplined effort to produce

fundamental decisions and actions that shape and guide what an organization is, what it

does, and why it does it, with a focus on the future. (Woodward 2004) argues that

strategic marketing is a process by which one can envision the future and develop the

necessary procedures and operations to influence and achieve the future. Organizations

can develop a planning process based on six simple questions. Realistic answers to these

can help to guide the owners and managers of any business or organization toward a

successful future.

2.2.1 Availability of Marketing Strategies in Commercial Banks

Strategic marketing, according to Berry (1997), is the process of determining; what your

organization intends to accomplish and how you will direct the organization and its

resources towards attaining the goals set over the coming months and years. In other

words, strategic marketing is a tool for finding the best future for your organization and

the best path to reach the desired destination. (Mintzberg 1994) is of the opinion that

strategic marketing can be defined as the process of using systematic criteria and rigorous

investigation to formulate, implement, and control strategy, and formally document

organizational expectations.

Strategic marketing as the systematic process of determining the firm‟s goals and

objectives for at least three years into the future and developing the strategies that will

guide the acquisition and use of resources to achieve the set objectives. Steiner, (1997),

sees strategic marketing as the process of determining the mission, major objectives,

strategies and policies that govern the acquisition and allocation of resources to achieve

organizational aims. Strategic marketing has come to be “inextricably interwoven into the

entire fabric of management” it is not seen as separate and distinct from the process of

management (Kudler 1996).

Bradford and Duncan (2000), argues that strategic marketing is an organization‟s process

of defining its strategy and making decisions on allocating its resources to pursue this

strategy, including its capital and people. The outcome is normally a strategic plan which

14

is used as a guide to define functional and divisional plans, technology, and marketing

among others. Hunsaker, (2001) observes that strategic plans apply to the entire

organization. They establish the organization‟s overall objectives and seek to position the

organization in terms of its environment. Strategic marketing is done by top level

managers to determine the long- term focus and directions of the entire organization.

All short- term and specific plans for lower- level managers are linked and coordinated so

that they may contribute to the organization‟s strategic plan. (Paley 2004) sees strategic

marketing as representing the managerial process for developing and maintaining a

strategic fit between the organizations and changing market opportunities. It relies on the

development of the following sections; a strategic direction or mission statement,

objectives and goals, growth strategies, a business portfolio. Gup and Whitehead, (2000),

on other part, see strategic marketing as the formulation of a unified, comprehensive and

integrated plan aimed at relating the strategic advantages of the firm to the challenges of

the environment.

It is concerned with appraising the environment in relation to the company, identifying

the strategies to obtain sanction for one of the alternatives to be interpreted and

communicated in an operationally useful manner. Anderson, (2004), states that strategic

marketing is the logical and systematic process by which top management reaches a

consensus on the major strategic direction of the company. He enumerate major

characteristics of strategic marketing as a process of deciding in advance what will be

done, when and by who, and how it will be done, the future impact of current decisions,

an integral part of the management process, and a structure of plans integrating major

objectives, strategies, policies and functions of the organization.

Marketing management horizons vary from two to fifteen years depending on the nature

of the industry and individual business characteristics. Anderson, (2004) presents eight

major steps that are commonly recognized in the strategic marketing process as;

determination of the long-range direction of the business, defining the company‟s major

areas of business, key market segments and key resources, evaluation of the company‟s

15

position relative to that of its competitors in the industry, assessment of the company‟s

capabilities, strengths and weaknesses, identification of objectives and goals having

regard to available opportunities and existing threats (Anderson, 2004).

Determination of the long-range direction of the business, Defining the company‟s major

areas of business, key market segments and key resources Evaluation of the company‟s

position relative to that of its competitors in the industry, Assessment of the company‟s

capabilities, strengths and weaknesses, identification of objectives and goals having

regard to available opportunities and existing threats, formulation of strategies to achieve

the desired objectives and goals, development of a monitoring system to ensure the

implementation of the plan. Finally, he states that for strategic marketing to succeed an

appropriate climate must exist, top management must be committed and involved, and

there must be a disciplined but flexible planning approach (Anderson, 2004).

Paley, (2004) further observes that line personnel must participate, performance standards

for monitoring and evaluation must be established and planning must be integrated with

decision making. Advocating the adoption of strategic marketing in solving

organization‟s problems, remarks that the organization which does not plan for its future

does not deserve any future. Citing the work of (Ansoff 1998), Paley, (2004) contrasts

strategic marketing with long- range planning and concludes that both concepts are not

synonymous. He argues that long- range planning is based upon the extrapolation of past

situations, a questionable premise on the ground that present conditions are not the same

as those of the past.

Ulrich & Barney, (2004), further criticize the traditional extrapolation techniques of long

range planning and suggest the use of scenario analysis which encourages broad and

creative thinking about the future. The authors cite the work of Wing, (1997) which

contest that traditional forecasting techniques are based on the assumption that

tomorrow‟s world will be much like todays. Commenting on New Age Strategic

marketing Ginsberg, (1997) explains that the present complex environment is

characterized by side effects, time delays, non-linearity and multiple feedback processes.

16

Ansoff, (2004), reports that newly invented strategic marketing displaced long range

planning because of the growing discontinuity of the environment. He gives the

following reasons for this replacement: that the firm‟s environment has its own

turbulence level and that there are specific systems appropriate for given turbulence

levels. He states further that each firm therefore needs to diagnose its own future

turbulence level and the appropriate systems chosen to explain that under an environment

of slow change, without urgent needs to anticipate, familiar pattern can be extrapolated.

The type of environment was reported to have characterized the pre-1950 year of long

range or corporate planning after which the 1980s changes became progressively

discontinuous from the past and less predictable. The author explains the difference

between long range planning and strategic marketing as essentially one of more of

perception of the future. With long range planning, the future is expected to be

predictable through extrapolation of historical events which also assumes that the future

would be better than the past. Strategic marketing on the other hand does not necessarily

expect an improved future or extrapolatable past (Ansoff, 2004).

Hinterhuber, (1992), argued that a manager is not necessarily a strategist and that a

manager‟s vision is also not an entrepreneurial vision. He explains that while the manager

would rather have an orientation point of guiding a company in a specific direction, an

entrepreneur having strategic competence should state his vision clearly, aggressively and

in an optimistic manner. A strategist and not just a manager therefore, should have an

entrepreneurial vision, corporate philosophy, competitive advantages, and should involve

line managers in strategic marketing. Line managers are the ones to implement strategies

who should therefore be involved early in the strategic marketing process.

Realizing however that strategic marketing process does not specify how plans should be

translated into action, the issue of strategic marketing implementation led to the evolution

of strategic marketing management. The Nigerian experience indicates that banking

sector reforms are propelled by the need to deepen the financial sector and reposition it

for growth; to become integrated into the global financial architecture; and evolve a

17

banking sector that is consistent with regional integration requirements and international

best practices. Bank consolidation is viewed as the reduction in the number of banks and

other deposit-taking institutions with a simultaneous increase in size and concentration of

the consolidated entities in the sector (Gianni 2003).

It is mostly motivated by technological innovations, deregulation of financial services,

enhancing intermediation and increased emphasis on shareholder value, privatization and

international competition (Gianni 2003). The nexus between consolidation and financial

sector stability and growth is explained by two polar views. Proponents of consolidation

opine that increased size could potentially increase bank returns, through revenue and

cost efficiency gains. It may also, reduce industry risks through the elimination of weak

banks and create better diversification opportunities (Berger, 2000).

On the other hand, the opponents argue that consolidation could increase banks‟

propensity toward risk taking through increases in leverage and off balance sheet

operations. In addition, scale economies are not unlimited as larger entities are usually

more complex and costly to manage. Banking reforms involve several elements that are

unique to each country based on historical, economic and institutional imperatives. For

example, in the reforms in the banking sector proceeded against the backdrop of banking

crisis due to highly undercapitalization of state owned banks; weakness in the regulatory

and supervisory framework; weak management practices; and the tolerance of

deficiencies in the corporate governance behavior of banks (Gyargy Szapáry, 2001).

In the Yugoslav economy, banking industry restructuring was motivated by the need to

establish a healthy banking sector that will carry out its financial intermediation role at a

minimal cost; effectively provide services consistent with world standards and which will

involve foreign financial institutions; and banks privatization as the ultimate goal. The

central focus was to shore up the capital base of banks consolidated through mergers and

takeovers of local banks and selection of strategic investors for additional capitalization.

Specifically, foreign banks permeated the industry exclusively by providing additional

capitalization through investment in the existing infrastructure, particularly new banking

18

products and operating technologies and buying shares of the existing banks (Gyargy

Szapáry, 2001).

The banking sector reforms and consolidation in Japan involved the reform of the

regulatory and supervisory framework, the safety net arrangements, as well as

mechanisms to speed up attempts at resolution of banks‟ non-performing loans. From the

above, it is obvious that the fundamental objective of banks consolidation is the

repositioning of the banking industry to attain an effective and efficient status that will

promote economic development. Consequently, consolidation has increased the level of

competition in the industry and this in turn has increased the marketing activities in the

Nigerian banking industry as well as other nations of the world (Gyargy Szapáry, 2001).

2.2.2 Marketing Strategies and the Bank’s Competition in the Market

Commercial banks face many challenges in today‟s dynamic marketplace. In a global

economy that has become increasingly competitive, there is need for efficient

development of products that can quickly satisfy a more demanding customer base and

build long-term customer trust. It must enhance risk management and address a broad

range of service breakdowns and regulatory changes that require reporting with greater

standardization and transparency. It must optimize both internal and external innovation,

while seeking operational excellence at all levels (Parasuraman, (1985).

Meeting these challenges requires new business and marketing strategies that boost

revenues, improve operational efficiency, cut costs, and enhance the overall management

of business. Today, banks are looking beyond traditional practices to new tactics and

tools that analysts and thought leaders have identified as the best for the industry. Service

breakdown manifests itself by way of delayed approval of loans. SME customers are deal

seekers and they always look for a financial institution that can serve them within the

minimum time possible (Parasuraman, 1985).

In Kenyan commercial banks, however, the approval of business loans takes weeks or

even months depending on the availability of the required documentation. This delay is

19

costly especially when a firm has a limited time frame to demonstrate that it can raise the

required capital to carry out a particular task. Also, intrusive documentation is of concern.

At the point of application for banking services, some banks are known to be too

demanding on documentation. Customers feel that the documentation required (such as

tax compliance certificate) before the approval of the much needed loans is an intrusion

into their financial privacy (Gyargy Szapáry, 2001).

Discouraged by this exercise some customers have opted for other informal financial

institutions that do not require too much detail. Flexibility is also another matter of

service to SME‟s. Customers have become demanding and the loyalties are diffused if

they think a bank is not serving them well. To them there are multiple choices; the wallet

share is reduced per bank with demand on flexibility and customization. Given the

relatively low switching costs; customer retention calls for customized service and hassle

free, flawless service delivery will influence their choice (Gyargy Szapáry, 2001).

Having a good relationship with customers in a service industry is the most important

thing. Customers want to have a sense of belonging that will keep them from seeking

alternatives. Premier banking which in most cases is associated with the wealthy business

class is founded on the basis of relationship management. Banks however need to take a

step further and relate more with its SME customers to avoid giving a reason to go for

alternative service providers. Banks should improve their relationship management with

businesses and their advisors. Restoring trust between banks and their clients will require

a commitment to transparency and consistency on the part of lending institutions (Gyargy

Szapáry, 2001).

It is clear that some banks have re-appraised their risk and reward preferences for SME‟s.

Banks need to address the consequential „fear of approach‟ held by businesses by clearly

explaining how the changed economic environment has affected banks‟ business lending

policies. In particular, they should make a sustained effort to better communicate with

businesses at early stages in the lending application process to improve understanding of

the following: How long credit applications are likely to take; what restrictions on

20

decision-making are imposed on relationship managers and branch managers by head

office and whether specific decisions will be transferred to higher levels and how many

credit committees will examine the application; the full extent of non-price lending

conditions; the enforcement regime for covenant breaches (Kotler, 1999).

Marketing the quality of service is central to the success and growth of business.

Developing the service quality model defined service as the gap between service and

perceived performance. A service firm may win by delivering consistently higher quality

service than competitors and exceeding customer‟s expectations (Kotler, 1999). After

receiving the service, customers compare the perceived service and expected service

Researches have found that consumers consider five dimensions in their assessment of

service quality as reliability, responsiveness, assurance, empathy and tangibles (Kotler,

1999).

Reliability is the ability to perform the promised service dependably and accurately while

responsiveness is the willingness to help customers and provide prompt service.

Assurance, on the other hand, is the employees knowledge and courtesy and their ability

to inspire trust and confidence. Empathy is caring, individualized attention given the

customers and tangibles are appearance of physical facilities, equipment, personnel and

written materials. The five dimensions represent how consumers organize information

about service quality in their minds and were found relevant for banking among other

industries. There are numerous strategies a service marketer can use to overcome

challenges (Kotler, 1999).

Some of the strategies include; Consumer research provides the basis for the development

of new service concepts to meet targeted consumer needs (Lovelock et al, 1996). Finding

out what customers expect is essential to providing service quality, and marketing

research the key to understanding customer expectations and perceptions of service

(Kotler 1999). Firms also develop strategies to enable them seize strategic initiatives and

maintain a competitive edge in the market. Service breakdown manifests itself by way of

delayed loans. A service organization cannot serve an entire market for a particular

21

service as customer needs and wants are diverse. It must identify segments of a market

that it can serve most effectively. A market segments consists of a large identifiable

group within a market with similar wants, purchasing power, among other attributes

(Kotler, 1999).

Once a company has identified a specific market segment to serve, the next phase is to

position the service in the market place. How the service is designed (service blueprinting

and physical evidence) will impact the image of the service in the consumers mind

(Ziethmal et al, 1996). A service offering‟s position is the way it is perceived by

consumers, particularly in relation to competing offerings. To develop effective

positioning strategies, managers need insights into how the various attributes of a service

are valued by the current and prospective customers within that segment.

An organization‟s service offering is successfully positioned if it has established and

maintains a distinctive place for itself in the consumer‟s mind relative to competing

organization‟s offerings. If a service is successfully positioned, the mention of the service

will conjure up in the customer‟s mind an image that is distinct from images of similar

service offerings (Ziethaml et al, 1996). Relationship marketing is philosophy of doing

business that focuses on keeping and improving current customers rather than on

acquiring new ones. Service companies must see customers as their long term partners

and need to make a commitment in maintaining the relationship through quality, service

and innovation (Lovelock et al, 1996).

Once managers of service business accurately understand what customers expect, the

second critical challenge is to set service quality standards and goals for the

organizations. Excellent service businesses realize the crucial role that the setting and

review of service standards can play in driving quality performance. They understand the

benefits brought about by the business, its customers and the individuals involved in

service delivery, the pay-off in terms of customer loyalty as well as reduce the cost of

correcting errors and handling complaints. The setting of quality service standards is the

beginning of a cycle of continuous improvements (Lovelock et al, 1996).

22

With people as part of the service, no service business can afford to divorce its customer

contact employees from the firm‟s marketing strategy (Lovelock et al, 1996). The

primary responsibility for an organization‟s success often rests with relatively junior staff

in such customer contact positions as a bank clerk, security guard etc. These individuals,

who are often young and inexperienced, need both technical and interpersonal skill to

succeed. Not only must they do their job quickly and accurately, but to do so while

relating well to customers (Lovelock et al, 1996).

Because contact employees represent the organization and can directly influence

customer satisfaction, they perform the role of marketers (Ziethaml et al, 1996).

Therefore careful recruitment, training and ongoing mentoring of employees can

contribute to improvements in both productivity and service quality. Developing a

communication strategy for intangible services is quite different from advertising and

promoting psychical goods. The company should recognize that service is a performance

rather than an object; advertising should not only encourage customers to buy the service,

but should also target employees as a second audience, motivating them to deliver high-

quality service.

2.2.3 Marketing Strategies and the Corporate Image of Commercial Banks

Various models been developed empirically to analyze the impact of marketing strategies

on corporate performance. Some of these empirical studies include; this model recognizes

the importance of a firm‟s internal organizational resources as determinants of the firm‟s

strategy and performance (Grant 1991). Grant, (1991) defines the term internal

organizational resources as all assets, capabilities, organizational processes, firm

attributes, information, knowledge, that are controlled by a firm and that enable it to

envision and implement strategies to improve its efficiency and effectiveness.

Although the RBV recognizes that a firm‟s physical resources are important determinants

of performance, it places primary emphasis on the intangible skills and organizational

resources of the firm (Collis, 1991). Some intangibles resources of the firm are the

market-assets such as customer satisfaction and brand equity. The Dynamic Capabilities

23

emphasizes on how combinations of resources and competences (Teece et al., 1997) can

be developed, deployed and protected. The factors that determine the essence of a firm‟s

dynamic capabilities are the organizational processes where capabilities are embedded,

the positions the firms have gained (e.g. assets endowment) and the evolutionary paths

adopted and inherited.

Based on this perspective, the marketing factors that determine the competitive advantage

are marketing efficiency resulting from the marketing organizational process and the

endowments of market assets that has generated such as customer satisfaction and brand

equity, i.e. marketing positions. In the context of global competition, Dynamic

capabilities theory suggest that historical evolution of a firm (accumulation of different

physical assets and acquisition of different intangible organizational assets through tacit

learning) constrains its strategic choice and so will affect market outcomes (Collis, 1991).

According to (Douglas and Craig, 1999), the development of a Marketing Strategy is

carried out during the stage of global rationalization. It means that the firm has had to

take the step of initial foreign market entry and expansion of national markets during its

process of internationalization. Consequently, in the two previous stages, the firm learned

and accumulated not only different physical assets but also different intangible

organizational assets; likewise, it faced and took risks in different and complex market

contexts. This process of learning affected its performance. The need for measuring

marketing impact is intensified as firms feel increasing pressure to justify their marketing

expenditures (Gruca and Rego 2005).

Accordingly, marketing practitioners and scholars are under increased pressure to be

more accountable for showing how marketing activities link to shareholder value. It is

important to know that marketing actions, such as packaging, brand name, density of the

distribution channel, advertising, permanent exhibitions, sponsoring, press bulletins,

among others (Van, 1992) can help build long-term assets or positions as brand equity

and customer satisfaction, (Srivastava, 1998). These assets can be leveraged to deliver

short-term profitability and shareholder value.

24

The other way by which research in Marketing has faced Marketing performance is

related to efficiency. Efficiency is the comparison among firms of the ratio of outcomes

over the inputs required to achieve them. On the other hand, Sheth, (2002) define

marketing efficiency as the ratio of marketing output over input. Getting loyal customers

at low marketing costs, on the other hand, (Rust, 2004) use the term marketing

productivity to refer to how marketing activities are linked to short-term and long-term

profits.

2.3 Review of Analytical Literature

Marketing as a distinct discipline was borne out of economics around the beginning of

this century and has been developing over the year. The primary focus was on

transactions and exchanges. However, marketing as a field of study and practice is still in

the process of reconceptualization in its orientation. Axioms of transactional marketing

are the belief that competition and self-interest are the drivers of value creation and

maintaining an „arm‟s length relationship‟ is vital for marketing efficiency. Development

of relationship marketing is a significant shift in the axioms of marketing: competition

and conflict to mutual cooperation, and choice independence to mutual interdependence

(Sheth and Parvatiyar, 2000).

There has been a shift from transactions to relationships in marketing orientation. (Kotler,

1990). The emphasis on relationships as opposed to transaction based exchanges has

redefined the domain of marketing. Every marketing transaction involves a relationship

between the buyer and seller in a transaction-based situation, the relationship may be

quite short in duration and narrow in scope, on the other hand, the customer-seller bonds

developed in a relationship marketing situation last longer and cover a much broader

scope than those developed in transaction marketing. Customer contacts are more

frequent, a company emphasis on customer service contributes to consumer satisfaction

in relationship marketing, (Armstrong and Kotler, 2007).

Brodie, (1997) suggested that marketing strategies be applied at four levels. At the first

level, marketing strategies is a technology-based tool of database marketing. At a second

25

level, relationship marketing focuses on relationships between businesses and its

customers with an emphasis of customer retention. At a third level, relationship

marketing is a form of „customer partnering‟ with buyers cooperatively involved in the

design of the product or service offering. At a fourth and broadest level, relationship

marketing was seen as incorporating everything from databases to personalized services,

loyalty programs, brand loyalty, internal marketing, personal/social relationships and

strategic alliances.

Marketing strategies orientation involves a company integrates customer service and

quality with marketing, the result is a relationship marketing orientation. Relationship

marketing creates a new level of interaction between buyers and sellers. Rather than

focusing exclusively on attracting new customers, marketers have discovered that it pays

to retain current customers as the cost of retention is lower compared to the cost of

acquiring a new customers. It has been established that strong economic, technical and

social ties among the stakeholders‟ parties reduce transactions costs and increase

exchange efficiencies. These are the benefit of relationship marketing.

Jobber, (2006), views marketing strategy as the process of creating, developing and

enhancing relationship with customers and other stakeholders. Relationship marketing

refers to the development, growth, maintenance of long- term, cost- effective exchange

relationship with individual customers, suppliers, employees, and other partner for

mutual benefit (Boone and Kurtz, 2007). Developing excellent service quality creates the

opportunity to build an ongoing relationship with customers. The idea of relationship can

apply to many industries. It is particularly important in service industry of which banking

is central because of direct contact between the banks and customers.

Marketing strategies are always concerned about the direct marketing otherwise, known

as interactive marketing, activities and managing these dimensions with the aim of

establishing, developing and maintaining co-operative customer relationships for mutual

benefit (Boone and Kurtz, 2007). Direct marketing refers to buyers-seller

communications in which the consumer controls the amount and type of information

26

received from a marketer. Interactive techniques have been used for more than a decade;

point-of-sales brochures and coupon dispensers are a simple form of interactive

advertising.

Today, however, the term also includes two-way electronic communication using a

variety of media such as the internet, CD-ROMS, and virtual reality kiosks (Boone and

Kurtz, 2007). Relationship quality is all about customer satisfaction, trust and

commitment. It can be regarded as a variable composed of several key components

reflecting the overall nature of relationships between companies and costumers. There

has not been a common consensus regarding the conceptualization of relationship quality

but there has been considerable speculation as to the central components of this all

important variable in measuring relational quality.

Components of relationship quality proposed in past research include cooperative norms

(Siguaw 1999), opportunism, customer orientation, seller expertise and conflict,

willingness to invest, and expectation to continue. From the previous studies, there is

general consensus that customer satisfaction with the service provider‟s performance,

trust in the service provider, and commitment to the relationship with the service firm are

key components of relationship quality. Strategic marketing should enhance customers'

perceived benefits such as perceived relationship improvement and perceived economic

benefits of engaging in relationships (O'Malley and Tynan, 2000).

The Relational Benefits approach assumes that both parties in a relationship must benefit

for it to continue in the long run. For the customer, these benefits can be focused on

either the core service or on the relationship itself (Gremler 2000). Benefits customers are

likely to receive as a result of having cultivated a long-term relationship with a service

provider are referred to as relational benefits. These relational benefits are benefits that

exist above and beyond the core service provided. According to earlier researchers,

relational benefits include confidence benefits, social benefits and special treatment

benefits (Bitner, 1998).

27

According to Bitner, (1998), confidence benefits refer to perceptions of reduced anxiety

and comfort in knowing what to expect in the service encounter, social benefits pertain to

the emotional part of the relationship and are characterized by personal recognition of

customers by employees, the customer‟s own familiarity with employees, and the

creation of friendships between customers and employees; and special treatment benefits

take the form of relational consumers receiving price breaks, faster service, or

individualized additional services.

This has to do with organization employee‟s job satisfaction (Chi 2005), work motivation

and organizational commitment. Few studies have explicitly examined customer-related

outcome of internal marketing, such as service quality. Earlier research on internal

marketing concurs on three important themes. First, it is crucial that employees are “well-

attuned to the mission, goals, strategies, and systems of the company”. Second, internal

marketing builds on the formation of a corporate identity or collective mind (Ahmed and

Rafiq 2002). Third, internal marketing must go beyond short-term marketing training

programs and evolve into a management philosophy that requires multilevel management

to continuously encourage and enhance employees‟ understanding of their roles and

organizations.

All marketing activities are ultimately evaluated on the basis of the company‟s overall

performance. However, as a firm‟s profitability is influenced by a number of variables

largely independent of relationship marketing activities that may include leadership style,

capital base and technological know-how, it seems appropriate to conceptualize

relationship marketing outcomes on a more concrete level when investigating possible

antecedents (Ismail, 2009). Performance indicator such as target goals, sales goals,

customer retention (customer loyalty and positive customer word-of-mouth

communication), better reputation in quality product and new product development and

employee satisfaction measured by employee turnover rate are found appropriate in this

context.

28

2.4 Summary of the Review

Marketing is the process of determining the needs and wants of consumers and being able

to deliver products that satisfy those needs and wants. Marketing includes all of the

activities necessary to move a product from the producer to the consumer. The

framework suggested that marketing strategies in banking industry directly affect its

performance in terms of client numbers. Therefore arising from the gaps identified in the

literature review, the study therefore sought to bridge the gap by investigating the effects

of marketing strategies on the performance of co-operative bank Narok branch.

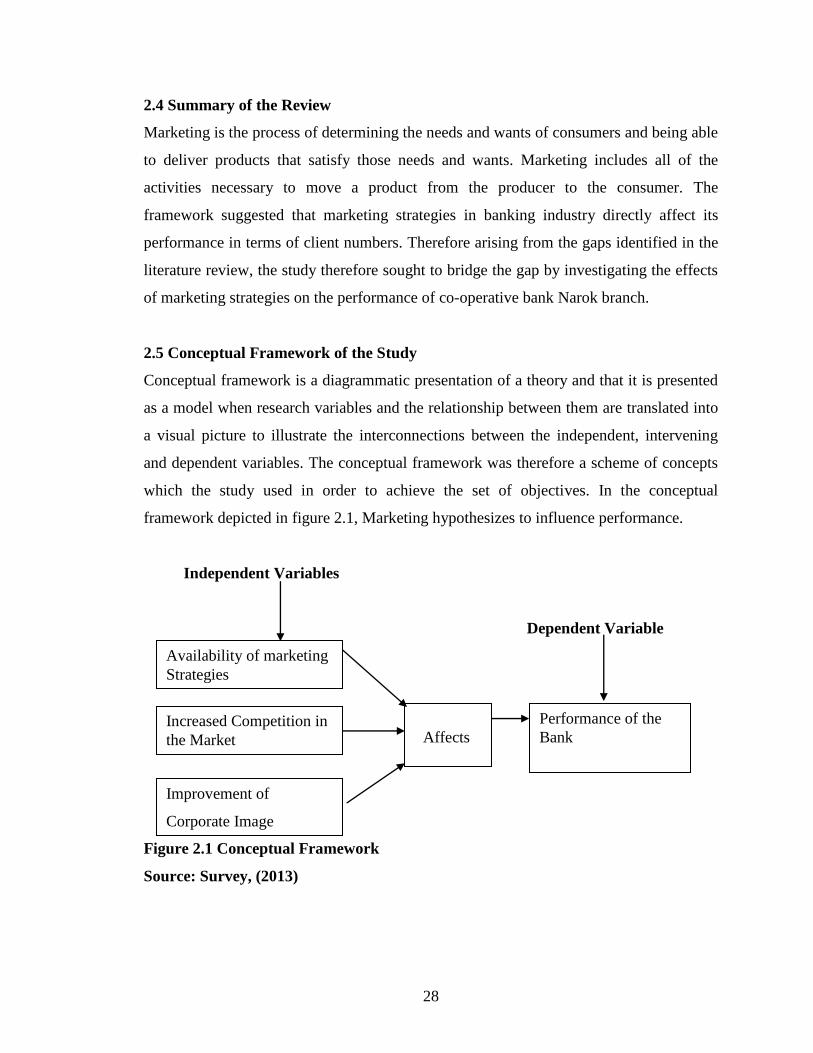

2.5 Conceptual Framework of the Study

Conceptual framework is a diagrammatic presentation of a theory and that it is presented

as a model when research variables and the relationship between them are translated into

a visual picture to illustrate the interconnections between the independent, intervening

and dependent variables. The conceptual framework was therefore a scheme of concepts

which the study used in order to achieve the set of objectives. In the conceptual

framework depicted in figure 2.1, Marketing hypothesizes to influence performance.

Independent Variables

Dependent Variable

Figure 2.1 Conceptual Framework

Source: Survey, (2013)

Availability of marketing

Strategies

Increased Competition in

the Market

Affects

Performance of the

Bank

Improvement of

Corporate Image

29

2.5.1 Availability of Marketing Strategies

Marketing the quality of service is central to the success and growth of business.

Developing the service quality model defined service as the gap between service and

perceived performance. The company should recognize that service is a performance

rather than an object; advertising should not only encourage customers to buy the service,

but should also target employees as a second audience, motivating them to deliver high-

quality service.

2.5.2 Increase in Competition

There is a connection between banks competition brought about by banks reforms and

marketing activities. An overall significance of the marketing variables adopted, although

not much effect is seen when a marketing variable is compared with bank performance in

isolation of other variables. This helps to conclude that the marketing strategies

techniques must be adequately combined in order to bring about improved performance.

2.5.3 Increase in Revenue Collections

Banks are encouraged to be more customers-focused and embrace marketing strategies

rather than transaction marketing. This will enable them to gain customers loyalty and

maintain a long term relationship with customers. The management of the banking

institutions should be transparent and follow the laid down rules so as to create and

sustain public confidence. Marketing the quality of service is central to the success and

growth of business.

2.5.4 Improvement of Corporate Image

Strategic marketing should enhance customers' perceived benefits such as perceived

relationship improvement and perceived economic benefits of engaging in relationships.

Developing the service quality model defined service as the gap between service and

perceived performance. Various models been developed empirically to analyze the

impact of marketing strategies on corporate performance.

30

CHAPTER THREE

3.0 RESEARCH DESIGN AND METHODOLOGY

3.1 Introduction

This chapter describes the research design used for the study. It includes the research

design, target population, sample size, sampling procedure and instrumentation, data

collection and data analysis.

3.2 Research Design

Research design is the outline that is used to generate answers to a research problem. This

study employed a descriptive survey research design. Descriptive survey research designs

are used in preliminary and exploratory studies to allow researchers to gather

information, summarize, present and interpret for the purpose of clarification (Orodho,

2002). Mugenda and Mugenda (2003) on the other hand give the purpose of descriptive

research as determining and reporting the way things are. Descriptive survey research is

intended to produce statistical information about aspects of education that interest policy

makers and educators. The study fitted within the provisions of descriptive survey

research design because the researcher collected data and reported the way things are

without manipulating any variable.

3.3 Target Population of the Study

Target population is defined as all the members of a real or hypothetical set of people,

events or objects to which a researcher wishes to generalize the results of the research

study (Orodho, 2002). The population under study comprised of all the 67 employees of

Co-operative bank-Narok branch.

3.4 Sample Size and Sampling Procedure

Sampling means selecting a given number of subjects from a defined population as

representative of that population. Any statements made about the sample should also be

true of the population (Orodho, 2002). It is however agreed that the larger the sample the

smaller the sampling error (Gay, 1992). From the 67 members of the target population,

the researcher used stratified random sampling technique to select 40 respondents.

31

3.5 Data Collection Instruments and Procedure

The main tool for data collection was a questionnaire. The questionnaire was used for

data collection because it offers considerable advantages in the administration. It also

presents an even stimulus potentially to large numbers of people simultaneously and

provides the investigation with an easy accumulation of data (Gay, 1992). Questionnaires

give respondents freedom to express their views or opinion and also to make suggestions.

It is also anonymous. Anonymity helps to produce more candid answers than is possible

in an interview. Before the actual data was collected, the researcher conducted a pilot

study in the same bank among 4 employees who were not included in the final study

population. These employees were randomly selected for the pilot study.

The purpose of the pilot study was to enable the researcher to ascertain the reliability and

validity of the instruments, and to familiarize himself with the administration of the

questionnaires therefore improve the instruments and procedures. Mugenda and Mugenda

(2003) define reliability as a measure of the degree to which a research instrument yields

consistent results or data after repeated trial. The pilot study enabled the researcher to

assess the clarity of the questionnaire items so that those items found to be inadequate

were modified to improve the quality of the research instrument thus increasing its

reliability.

Validity is defined as the accuracy and meaningfulness of inferences, which are based on

the research results (Mugenda & Mugenda, 1999). In other words, validity is the degree

to which results obtained from the analysis of the data actually represents the phenomena

under study. Validity is the degree to which a test measures what it purports to measure.