Embed Size (px)

Citation preview

MAY 20, 2016

Economy News Sebi tightened rules on issue of participatory notes (P-notes) to bring in

more transparency and curb misuse of the investment route used byforeign investors not registered in India. Sebi also made it mandatory forthe top 500 listed companies to have a policy for declaring dividends toinvestors. (BS)

India has decided to revoke an order that requires sugar mills to exportexcess supplies, two government officials said, after two consecutivedroughts look set to turn the country into a net importer next season. Thegovernment has scrapped the order in view of tightening supplies in thelocal market. (ET)

The telecom regulator has floated a consultation paper that explores waysto provide mobile Internet to consumers for free without violating a banon discriminatory pricing of data services, saying it wants to connect theunconnected and raising the prospect of another battle over netneutrality. (ET)

Corporate News Maruti Suzuki to recall 20,427 units of S-Cross. The 'service campaign is

being conducted to inspect a suspected fault and replace a brake part inthe S-Cross units. The recall applies to both the variants of S-Cross 1.3 litreand 1.6 litre diesel engines. Maruti refrained from calling the exercise arecall. (Mint)

A section of employees of five associate banks of SBI including listedState Bank of Mysore and State bank of Bikaner & Jaipur hasthreatened to go on strike tomorrow against their proposed merger withparent. Earlier this week, SBI proposed merger of five associate banks andnewly created Bharatiya Mahila Bank with itself. (ET)

Monsanto Co parent of Monsanto India is reviewing an unsolicitedtakeover proposal from Bayer AG, a bold attempt by the Germancompany to snatch the last independent global seeds producer andbecome the world's biggest maker of seeds and farm chemicals. (BS)

ITC will be setting up eight new integrated food processing units by 2019,with investments in excess of Rs 40 bn. The planned investments are a partof its long-term plan to invest Rs 250 bn, a majority of which will beallocated towards its food business. (BS)

Moody's Investors Service has revised its outlook on Adani Ports andSpecial Economic Zone to "negative" from the earlier "stable". Thechange reflects the company's lower volume growth, mainly because oflower coal volumes, and an increase in capex and financial leverage,compared to its previous expectations. (BS)

UK-based oil firm BP announced on its wholly owned subsidiary, Castrol,had sold 11.5 per cent stake from the 71 per cent it held in Castrol India,to domestic and international investors. At a closing price on the BSE, a11.5 per cent stake in the company was valued around Rs 21 bn. (BS)

Lupin has lined up plans for the over-the-counter OTC segment, with apilot project set to roll across two geographies. As per the management,the OTC portfolio will involve in-house products, without divulging detailson the products or segments they would be in. (BS)

After entering the ghee (clarified butter) segment last year, ITC isplanning to foray into the dairy whitener space as it looks to expand itspresence in the dairy segment. (BS)

Equity% Chg

19 May 16 1 Day 1 Mth 3 Mths

Indian IndicesSENSEX Index 25,400 (1.2) (1.7) 7.1NIFTY Index 7,783 (1.1) (1.7) 7.9BANKEX Index 18,829 (1.2) 1.3 15.7SPBSITIP Index 11,262 (0.3) (2.8) 5.3BSETCG INDEX 13,157 (2.4) (2.4) 10.4BSEOIL INDEX 9,116 (1.2) (2.6) 8.0CNXMcap Index 13,039 (1.2) (2.2) 10.3SPBSSIP Index 11,056 (1.0) (0.7) 11.9

World IndicesDow Jones 17,435 (0.5) (3.7) 6.4Nasdaq 4,713 (0.6) (4.8) 4.6FTSE 6,053 (1.8) (5.6) 1.7NIKKEI 16,647 0.0 (1.4) 4.4HANGSENG 19,694 (0.7) (6.2) 3.3

Value traded (Rs cr)19 May 16 % Chg - Day

Cash BSE 4,980 105.1Cash NSE 16,694 6.7Derivatives 329,386 12.7

Net inflows (Rs cr)18 May 16 % Chg MTD YTD

FII (5) (103) 1,471 13,261Mutual Fund 40 (86) 2,350 4,946

FII open interest (Rs cr)18 May 16 % Chg

FII Index Futures 15,491 (1.5)FII Index Options 73,157 0.6FII Stock Futures 50,234 (0.5)FII Stock Options 4,357 0.6

Advances / Declines (BSE)19 May 16 A B T Total % total

Advances 61 364 19 444 29Declines 237 775 36 1,048 68Unchanged - 33 6 39 3

Commodity % Chg

19 May 16 1 Day 1 Mth 3 Mths

Crude (US$/BBL) 48.8 1.2 14.4 64.5Gold (US$/OZ) 1,254.7 (0.3) 0.9 2.4Silver (US$/OZ) 16.5 (2.5) (2.6) 7.6

Debt / forex market19 May 16 1 Day 1 Mth 3 Mths

10 yr G-Sec yield % 7.5 7.5 7.4 7.7Re/US$ 67.4 67.0 66.6 68.5

Sensex

Source: ET = Economic Times, BS = Business Standard, FE = Financial Express,BL = Business Line, ToI: Times of India, BSE = Bombay Stock Exchange

22700

24200

25700

27200

28700

May-15 Aug-15 Nov-15 Feb-16 May-16

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 2

MORNING INSIGHT May 20, 2016

Kotak Securities Limited has two independent equity research groups: Institutional Equities and Private Client Group. This report hasbeen prepared by the Private Client Group. The views and opinions expressed in this document may or may not match or may be contrarywith the views, estimates, rating, target price of the Institutional Equities Research Group of Kotak Securities Limited.

IRB INFRASTRUCTURE DEVELOPERS LTD

PRICE: RS.219 RECOMMENDATION: BUYTARGET PRICE: RS.297 FY18E P/E: 14.6X

Revenues of the company for Q4FY16 were ahead of our estimates dueto better than expected EPC revenues on execution ramp up across newprojects as well as improvement in traffic volumes .

Margins declined in EPC divisions on yearly basis and consolidated op-erating margins stood at 49.3% vs 58.8% during Q4FY16 due to higherproportion of EPC revenues in the overall mix.

Net profit grew by 9.3% YoY for Q4FY16, beating our estimates due tobetter than expected revenue growth.

Toll revenues have been witnessing improvement and we expect com-pany to benefit from improving macroeconomic scenario thereby lead-ing to further improvement in toll revenues going forward. It has ahealthy order book which should sustain EPC revenue growth goingforward. We tweak our FY17 estimates and introduce FY18 estimates.We arrive at a revised price target of Rs 297 on FY18 estimates (asagainst Rs 295 earlier on FY17 estimates). We continue to remain posi-tive on the stock and maintain BUY rating on IRB Infrastructure. Fur-ther developments on setting up of investment trust would be keenlywatched out for.

Consolidated financial highlights

Q4FY16 Q4FY15Rs mn EPC BOT Total EPC BOT Total

Revenues 9780 5932 15712 5156 5032 10188

YoY % 89.7% 17.9% 54.2%

EBITDA 2653 5087 7741 1782 4207 5989

EBITDA % 27.1% 85.8% 49.3% 34.6% 83.6% 58.8%

Depreciation 181 2043 2224 195 1525 1720

EBIT 2472 3044 5517 1588 2682 4270

Interest 827 2439 3265 967 1540 2507

EBT 1646 606 2251 621 1142 1762

YoY % 165.2% -47.0% 27.7%

Tax 596 131 727 199 199 398

Tax% 36.2% 21.6% 32.3% 32.1% 17.4% 22.6%

PAT 1050 475 1524 421 943 1364

Minority interest 0 13 13 -18 -18

Net profit 1050 462 1511 421 961 1382

YoY % 149.1% -51.9% 9.3%

Net profit w/o MAT credit 1050 0 1050 421 756 1177

Shares(mn) 351.5 351.5 351.5 351.5 351.5 351.5

EPS 3.0 1.3 4.3 1.2 2.7 3.9

Source: Company

Revenue growth ahead of our estimatesRevenue growth for the quarter stood at 54.2% YoY and was better than ourestimates. EPC revenues reported a growth of 89.7% YoY for Q4FY16 while tollrevenues have reported an increase of 17.9% YoY mainly led by improvement intraffic volumes as there was no tariff increase.

Summary table - Consolidated

(Rs mn) FY16E FY17E FY18E

Sales 52,541 61,999 66,251Growth (%) 32.7 18.0 6.9EBITDA 27,846 31,816 34,236EBITDA margin (%) 53.0 51.3 51.7PBT 8,680 8,857 7,993Net profit 6,360 6,417 5,258EPS (Rs) 18.1 18.3 15.0Growth (%) 17.1 0.9 (18.1)CEPS(Rs) 42.4 47.4 46.9BV (Rs/share) 139.8 155.7 168.2DPS (Rs) 2.0 2.0 2.0ROE (%) 13.7 12.4 9.2ROCE (%) 10.5 10.7 10.6Net debt 125,596 145,054 165,757P/E (x) 12.1 12.0 14.6P/BV (x) 1.6 1.4 1.3EV/Sales (x) 3.9 3.6 3.7EV/EBITDA (x) 7.3 7.0 7.1

Source: Company, Kotak Securities - Pri-vate Client Research

RESULT UPDATE

Teena [email protected]+91 22 6218 6432

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 3

MORNING INSIGHT May 20, 2016

EPC revenues are largely led by execution of Solapur-Yedeshi, Yedeshi-Aurangabad, Goa-Kundapur and Rajasthan Kaithal project while growth in tollrevenues is led by improvement in traffic volumes in comparison with last quar-ter.

Toll revenues improved due to higher collections across all projects: Forthe full year, Mumbai-Pune project witnessed 11% YoY improvement in rev-enues during the quarter led by 11% growth in traffic volumes. Surat-Dahisarwitnessed a 10.4% increase in revenues during the quarter largely led by 10%improvement in traffic volumes. Tumkur-Chitradurg witnessed 10% YoY growthin traffic while its tariff has witnessed a decline during the quarter. Ahmedabad-Vadodara witnessed 6% growth in traffic. Bharuch-Surat revenues were up by4% YoY and MVR witnessed a 10.5% YoY growth after witnessing decline in tollrevenues during Q3FY16 due to Chennai floods. Jaipur-Deoli and TalegaonAmravati toll collections also improved by nearly 10% YoY led by improvementin traffic volumes.

Order book status: Company's order book stands at Rs 97.5 bn with Rs 58 bn inongoing BOT projects, Rs 18.1 bn in BOT projects in O&M phase and Rs 21.33 bnin BOT projects where LOA is received but construction yet to commence. IRBwas awarded a project worth Rs 100.5 bn for construction, operation and main-tenance of Zozila tunnel in J&K on DBFOT basis during Q3FY16 but was cancelledduring Q4FY16.

Status of under construction projects: For Ahmedabad-Vadodara project,company has completed the work and has received provisional completion cer-tificate from NHAI. Consequently, SPV has started toll collection on NH-8 from6th Dec,15. During Q4FY16, company booked revenues of Rs 850 mn from GoaKundapur project and execution is likely to ramp uo only after monsoons. ForSolapur-Yedeshi project, construction is picking up pace and it booked Rs 1.85bn in EPC revenues during Q3FY16. Yedeshi-Aurangabad project, it booked Rs2.8 bn in EPC revenues while for Kaithal-Rajasthan border project, EPC revenueswere around Rs 2.77 bn. Utility shifting added to Rs 1.25 bn to EPC revenues.Work on Mumbai Pune extension project is delayed and is now expected to com-mence after company gets clarity from government; financial closure has al-ready been achieved for this project. For Agra-Etawah Bypass project, work isexpected to commence from Q1FY17 end. For these under-construction projects,company expects an equity commitment of Rs 18 bn to be invested over next 3years. It expects to put in Rs 7 bn/ 8 bn/3 bn during FY17/18/19 respectively.

We tweak our FY17 estimates for the company and expect revenues to grow ata CAGR of 12.3% between FY16-18. (earlier est of Rs 59.3 bn for FY17)

Margins declined due to change in revenue mix

Operating margins in the construction division stood at 27.1% while marginsalso remained strong in the BOT division at 85.8% for Q4FY16. Overall marginsdeclined on consolidated basis as during the quarter company recognized someutility shifting income of nearly Rs 1.25 bn which is not margin accretive. Con-solidated margins stood at 49.3% for Q4FY16 as against 58.8% in Q4FY15 dueto change in revenue mix. We tweak our estimates and expect margins of51.3% (52.4% est earlier) and 51.7% for FY17/18 respectively.

Net profit growth led by healthy execution and improvement intoll revenues

Net profit grew by 9.3% YoY for Q4FY16 due to healthy growth in revenues andstood ahead of our estimates. Depreciation and interest charges have witnessedan increase due to commissioning of under construction projects such asAhmedabad-Vadodara in comparison with last year. Net debt on consolidatedbasis stands at nearly Rs 135 bn while standalone borrowings stand at around Rs20 bn.

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 4

MORNING INSIGHT May 20, 2016

Company has an equity requirement of nearly Rs 18 bn to be put in the currentportfolio of projects during next three years. Company has also taken a boardapproval for setting up an Infrastructure Investment trust wherein it intends totransfer 6-7 operational projects to unlock value and raise funds for futuregrowth and equity commitments. This process is delayed by few months as com-pany is waiting for clarity regarding accounting standards and is expected tocomplete during FY17. This would help in unlocking value from its operationalprojects.

We tweak our estimates and expect net profits of Rs 6.4 bn/Rs 5.3 bn for FY17/18 respectively. (Rs 5.9 bn est earlier for FY17)

Valuation and recommendation

At current price of Rs 219, stock is trading at 12x and 14.6x P/E and 7.0x and7.1x EV/EBITDA on FY16 and FY17 respectively. Toll revenues have been witness-ing improvement and we expect company to benefit from improving macroeco-nomic scenario thereby leading to further improvement in toll revenues goingforward. It has a healthy order book which should sustain EPC revenue growthgoing forward. We continue to remain positive on the stock and maintain BUYrating on IRB Infrastructure with a revised price target of Rs 297 on FY18 esti-mates (Rs 295 earlier on FY17 estimates). Further developments on setting up ofinvestment trust would be keenly watched out for.

Sum of the parts valuation (FY18)

EPS (FY18E) Multiple (x) EV(Rs mn) Value per share (Rs)

Core construction division 12.1 9 110

BOT projects(based on FY18) Cost of equity(%)

Bharuch Surat 13.5% 3900 11

Thane Ghodbunder 13.5% 2192 6

Surat Dahisar 13.5% 11 0

Mumbai Pune 12.4% 12567 36

Pune-Sholapur 13.5% 588 2

Thane bhiwandi 13.5% 792 2

Pune Nashik 13.5% 1492 4

Kolhapur IRDP 13.5% 2580 7

Talegaon Amravati 13.5% 4891 14

Jaipur-Deoli 13.5% 6648 19

Amritsar-Pathankot 13.5% 6606 19

Tumkur Chitradurg 13.5% 5516 16

Ahmedabad-Vadodara 13.5% 8964 26

MVR 13.5% 1735 5

Goa Kundapur 13.5% 6179 18

Solapur-Yedeshi 13.5% 3966 11

Yedeshi-Aurangabad 13.5% 5881 17

Rajasthan - Kaithal 13.5% 4833 14

Mumbai Pune ext 12.4% 4740 13

Real estate investment valuations 1250 acres 1 1300 4

Net debt at standalone 20000 57

Total 297

Source: Kotak Securities - Private Client Research

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 5

MORNING INSIGHT May 20, 2016

Kotak Securities Limited has two independent equity research groups: Institutional Equities and Private Client Group. This report hasbeen prepared by the Private Client Group. The views and opinions expressed in this document may or may not match or may be contrarywith the views, estimates, rating, target price of the Institutional Equities Research Group of Kotak Securities Limited.

RESULT UPDATE

Sanjeev [email protected]+91 22 6218 6424

VOLTAS LTD

PRICE: RS.323 RECOMMENDATION: ACCUMLATETARGET PRICE: RS.347 FY18E P/E: 21.4X

Voltas delivered impressive quarterly numbers which exceeded ourrevenue (led by MEP segment) and profits estimates. Operatingperformance was strong across all segments.

Improving order backlog and the company's strategy of taking selectiveorders gives us comfort that margins in the MEP segment should continueto strengthen in the medium term.

The ongoing summer season has also panned out well for the industry.Outlook remains positive for Q1FY17 profits. Even in the medium term,we continue to remain positive on the company given market leadership,long term growth potential for room ACs and strong balance sheet (cashper share of ~ Rs 26)

At 21.4x FY18 earnings, the stock is available at a discount to sector peers.We arrive at a target price of Rs 347 (281 earlier) based on exit multiple of23x FY18 earnings (25x FY17 earnings earlier). Since the stock hasoutperformed in the past quarter, the upside has been constrained, hencewe move rating to Accumulate compared to BUY earlier.

Near-term challenges include - impact of decline in crude price on MiddleEast market, weak demand for spinning machinery, sluggish activity inmining sector and intense competition in the room AC segment.

Quarterly performance

(Rs mn) Q4FY16 Q4 FY15 YoY (%)

Net Revenue 18757 14841 26.4Operating other income 130 59 121.8

Expenditure 17035 13470 26.5

Raw Material costs 10600 8007 32.4

Purchase of stock in trade 2917 2314 26.1

Staff costs 1830 1518 20.5

Other expenditure 1688 1631 3.5

Operating profit 1853 1430 29.5Depreciation 80 81 -1.1

Other income 478 303 57.9

EBIT 2251 1652 36.2Interest 59 58 1.9

PBT 2191 1594 37.5Tax 664 413 60.8

minority interest -48 -12 -100.0

Share in profit/(loss) of associates cos 5 -100.0

Adjusted PAT 1485 1168 30.8extraordinary items 279 12 2171.0

Reported PAT 1807 1180 49.5EPS 4.6 3.5EBITDA excl other op income (%) 9.2 9.2

EBITDA incl other op income (%) 9.9 9.6

Raw material to sales (%) 56.5 53.9

Purchase of traded goods to sales (%) 15.6 15.6

Other expenditure to sales (%) 9.0 11.0

Staff costs (%) 9.8 10.2

Tax rate (%) 25.0 25.9

Source: Company

Summary table

(Rs mn) FY16 FY17E FY18E

Sales 58,574 60,240 65,949Growth (%) 13.0 2.8 9.5EBITDA 4,369 5,247 6,137EBITDA margin (%) 7.5 8.7 9.3PBT 5,521 6,195 7,171Net profit 3426 4340 4990EPS (Rs) 10.4 13.1 15.1Growth (%) 1.3 26.7 15.0CEPS (Rs) 11.2 13.9 15.9BV (Rs/share) 71.5 82.0 94.6Dividend/share (Rs) 2.5 2.8 2.8ROE (%) 15.2 16.9 16.9ROCE (%) 14.4 14.9 15.2Net cash (debt) -629 5410 8674NW Capital (Days) 30.7 29.7 30.3EV/Sales (x) 1.7 1.5 1.5EV/EBITDA (x) 22.3 17.4 16.0P/E (x) 31.2 24.6 21.4P/Cash Earnings 28.8 23.2 20.3P/BV (x) 4.5 3.9 3.4

Source: Company, Kotak Securities - Pri-vate Client Research

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 6

MORNING INSIGHT May 20, 2016

Estimates

(Rs mn) Reported Estimated Remarks

Revenue 18757 16559 Higher revenue driven by MEP segment

EBITDA (%) 9.9 7.5 Strong margin gains led by MEP segment

Adjusted PAT 1528 1047 Leading to significant beat in profits

Source: Kotak Securities - Private Client Research

Segment Revenues

Rs mn Q4FY16 Q4FY15 YoY (%)

Electromechanical projects (MEP) 8186 5997 37

Engg products and services 927 811 14

Unitary cooling Products 8591 7807 10

Others 1056 229 360

Source: Company

Segment Margins

(%) Q4FY16 Q4FY15

Electromechanical projects (MEP) 3.4% 0.7%

Engg products and services 32.6% 35.4%

Unitary cooling Products 16.2% 17.8%

Others 8.7% 3.1%

Source: Company

Electromechanical Projects (MEP) Segment - Robust revenuegrowth

Electromechanical Projects and Services accounted for 44% of the quarterly rev-enue. Revenue growth was strong at 37% yoy in Q4FY16 aided by InternationalProjects, esp. Qatar where execution of a couple of newer private sectorprojects have been stepped up.

Segment margins also got a leg up as some of these projects crossed the thresh-old levels for recognition of margins.

Although the segment has turned in a good performance, the ground situation inMiddle East remains challenging chAaracterised by slow pace of project execu-tion, delay in certification / settlement of commercial entitlements, delay in pay-ments, legal disputes and arbitrations.

Domestic business landscape also remained lackluster as corporates and themanufacturing sector continued to defer making fresh investments. However,the government spending has been a savior for the company as it booked ordersfrom rural electrification (through Rohini Electricals). In terms of revenue, thedomestic MEP business ended the fiscal on a flat note.

Engineering Products and Services Business - Textile machinery andmining equipment continue to see slowdown.

This segment includes commission income on sale of textile machinery for LMWand sale and services of mining equipment. The demand from the Textiles andMining equipment businesses continued to remain weak due to muted globaldemand and softening of commodity prices. Yet, the segment reported robustrevenue growth of 14% on a yoy basis.

The textile machinery agency business of Voltas is primarily focused on the Spin-ning machinery which is used to generate yarn, which in turn is exported to tex-tile production countries like China for post spinning activities. However, therehas been a drop in demand for yarn from China which has hurt the prospects forspinning machinery. Even weaving machinery demand remained subdued for thefiscal.

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 7

MORNING INSIGHT May 20, 2016

The demand for mining and construction machinery remained weak due to fac-tors like tepid Chinese demand and lackluster global growth. In this scenario, thecompany's operations in Mozambique continued to do well and offset the im-pact of slowdown on revenues. On the positive side, the company is witnessingearly signs of pickup in construction equipment demand led by governmentspending in the road segment.

Unitary Cooling Products (UCP - largely room AC) Business - Sequen-tial rebound in segment margins surprised us

Coming on the back of a weak first half, the segment's revenue growth indi-cated a recovery in demand as it grew 10% y-o-y. The company's room AC vol-umes got a boost as the demand remained firm even post the festival season.An unusually warmer weather especially in the Southern peninsula also helpedthe company notch good volumes.

Voltas maintained its No.1 market position (21% for FY16 - though there is amarginal moderation in market share from Dec 2015 levels of 21.8%) in theUnitary Cooling Products (room ACs) business. Nevertheless, the company con-tinues to maintain a clear lead of ~ 500 bps over the nearest competitor.

On the margins front, the company reported segment margins of 16.2% inQ4FY16 which surprised us positively as we had built in lower margins to reflectprice pressures in the marketplace.

Order intake was good during the quarter.

During the quarter, the company booked orders of Rs 9.6 bn contributed mainlyby the Middle East region.

At the end of FY16, Voltas has a carry forward order book position of Rs 39 bn(overseas Rs 18.9 bn and domestic Rs 20.2 bn), which is at the same level as inthe previous fiscal-end.

As indicated earlier, the Middle East market continues to present potential risksand in cognizance of this it continues to pursue orders on a selective basis. Themanagement has highlighted that it is negotiating for couple of new orders inthe region.

Outlook

Ground level activity in Middle East as well as India is yet to improve in anymeaningful terms. Having said that, there appears to be a silver lining in that thecompetitive landscape in the Middle East may have improved as the companynoted that due to exit of some players there has been a dearth of credible MEPcontractors like Voltas in the Middle East market. The decline in competitive in-tensity bodes well for Voltas as it can look forward to bag projects at reasonablemargins and acceptable contractual terms.

The company has closed FY16 with an EBIT margin of 1.4% in the MEP segment.Going ahead, management believes that EBIT margins of 4-5% are achievable.However, this is subject to timely completion of projects.

On the UCP division, the management indicated that the ongoing summer sea-son has shaped well. Unless there are weather changes (for example - earlyrains), it is looking forward to strong volume growth in the first quarter.

The management also signaled that provided the forex remains stable and ad-vertising expenses remains at budgeted levels, the profitability in the UCP seg-ment would be governed by volume growth, which has remained strong inQ1FY17. Given this, we expect margins to remain strong in Q1FY17.

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 8

MORNING INSIGHT May 20, 2016

Earnings Revision

Our earnings revision is mainly on account of 1) strong demand trend in UCP di-vision 2) Improved order intake in MEP segment.

Earnings revision - FY17

(Rs mn) Earlier Revised

Revenue 57,651 60,240

EBITDA (%) 7.7 8.7

EPS 11.2 13.1

% change 17.2%

Source: Kotak Securities - Private Client Research

Valuation and Target Price

Voltas is valued at 24.6x and 21.4x FY17 and FY18 earnings respectively.

Valuations are at a premium to historical trend but are at a discount to sectorpeers (Symphony, Whirlpool, IFB, Havells etc).

We arrive at a target price of Rs 347 (281 earlier) based on unchanged exit mul-tiple of 23x FY18 earnings.

Peer Valuation (x)

FY17 PE

Voltas 25

Blue Star 27.8

Havells 37.5

Symphony 46

Whirlpool 30

Source: Kotak Securities - Private Client Research and Industry estimates

RecommendationWe continue to be positive on the long term potential of room AC in India givensignificant under-penetration relative to other consumer durable products. Voltashas a strong brand and wide distribution network which should certainly enablethe company to ride the industry growth, we believe. However, since the stockhas outperformed in the past quarter, the upside has been constrained, hencewe move rating to ACCUMULATE compared to BUY earlier.

We recommendACCUMULATE on Voltas

with a price target ofRs.347

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 9

MORNING INSIGHT May 20, 2016

Kotak Securities Limited has two independent equity research groups: Institutional Equities and Private Client Group. This report hasbeen prepared by the Private Client Group. The views and opinions expressed in this document may or may not match or may be contrarywith the views, estimates, rating, target price of the Institutional Equities Research Group of Kotak Securities Limited.

GUJARAT STATE PETRONET LTD (GSPL)PRICE: RS.136 RECOMMENDATION: ACCUMULATETARGET PRICE: RS.150 FY18E P/E: 12.3X

Pipeline tariff revision and higher gas volumes key triggers

GSPL's Q4FY16 result is lower than our estimates and market consensus.GSPL reported operating profit of Rs.997 mn, lower 19% qoq mainly onaccount of lower transmission tariffs, lower sequential gas volumes,higher sequential other expenses and lower other income.

Going forward, we expect the Company to benefit on account of both 1).Higher gas transmission volumes and 2). Expected upward revision intariffs. Higher gas transmission volumes will be supported by 1) lowerLNG prices, and 2) RLNG demand from the power sector. Additionally,rising city gas distribution growth opportunities, potential shift to naturalgas due to environmental/pollution norms (industrial / CNG) and volumesfrom Mundra LNG terminal (FY18 onwards) provides support to long termvolumes. We expect GSPL to report an EPS of Rs.10.2 and cash EPS ofRs.13.6 for FY17E and an EPS of Rs.11 and cash EPS of Rs.14.6 for FY18E.Due to limited upside, we now recommend Accumulate (earlier BUY) onGSPL with an unchanged target price of Rs.150/Share, given reasonablevaluations at 12.3x PE based on FY2018E earnings.

Quarterly Table

(Rs mn) Q4FY16 Q4FY15 YoY (%) QoQ (%)

Gross Revenue 2341 2393 (2) (6)

Less: Discount, etc 28.2 30.7 (8) 86

Discount (%) 1.20 1.28 (0.1) 0.6

Net Sales/Income from ops 2,313 2,363 (2) (7)

Total Expenditure 271 389 (30) (30)

EBIDTA 2,042 1,973 3 (2)

Depreciation 473 601 (21) 0

EBIT 1,569 1,373 14 (3)

Other income 137 140 (2) (52)

Interest-net 168 262 (36) (9)

PBT 1,538 1,251 23 (10)

Tax 541 580 (7) 12

PAT 997 671 49 (19)

Basic EPS (Rs) 1.77 1.19 49 (19)

Cash EPS (Rs.) 2.61 2.26 16 (14)

Source: Company

Performance Analysis

GSPL (Rs.mn) Q4FY16 Q4FY15 YoY (%) QoQ (%)

Gas Transported: Volume

Gas Transported (MMSCMD) 24.69 23.82 3.6 (1.5)

Gas Transported in each Quarter 2,222 2,144 3.6 (3.7)

Implied Tariff

Rs per 1000 SCM 1,041 1,085 (4) (1)

Source: Company

Summary table

(Rs mn) FY16E FY17E FY18E

Sales 9,919 12,041 12,616Growth (%) -6.8 21.4 4.8EBIDTA 8,654 10,567 11,061EBIDTA margin (%) 87.2 87.8 87.7PBT 6,523 8,587 9,290Net profit 4,279 5,753 6,224EPS (Rs) 8.2 10.2 11.0Growth (%) -4.5 23.8 8.2CEPS (Rs) 11.5 13.6 14.6BV (Rs/Share) 70.9 81.4 90.6DPS (Rs) 1.5 1.5 1.5ROE (%) 12% 13% 13%ROCE (%) 11% 12% 12%Net Cash (debt) (2,602) 3,203 6,968NWC (Days) 93 87 87EV/Sales (x) 8.0 6.1 5.5EV/EBIDTA (x) 9.1 6.9 6.3P/E (x) 16.5 13.3 12.3P/BV (x) 1.9 1.7 1.5P/CEPS (X) 11.8 10.0 9.3

Source: Company, Kotak Securities - Pri-vate Client Research

RESULT UPDATE

Sumit [email protected]+91 22 6218 6438

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 10

MORNING INSIGHT May 20, 2016

Result Analysis:

Revenue: GSPL's net revenue for Q4FY16 decreased 7% qoq to Rs.2.3 bn (-2% yoy). Sequential decline in revenues is on account of both 1). Decline involumes and 2). Decline in tariffs.

Transmission tariffs: GSPL's average implied tariff was at Rs. 1.04 per SCMin Q4FY16, recording marginal decline of 1.2% qoq and 4.1% yoy basis.

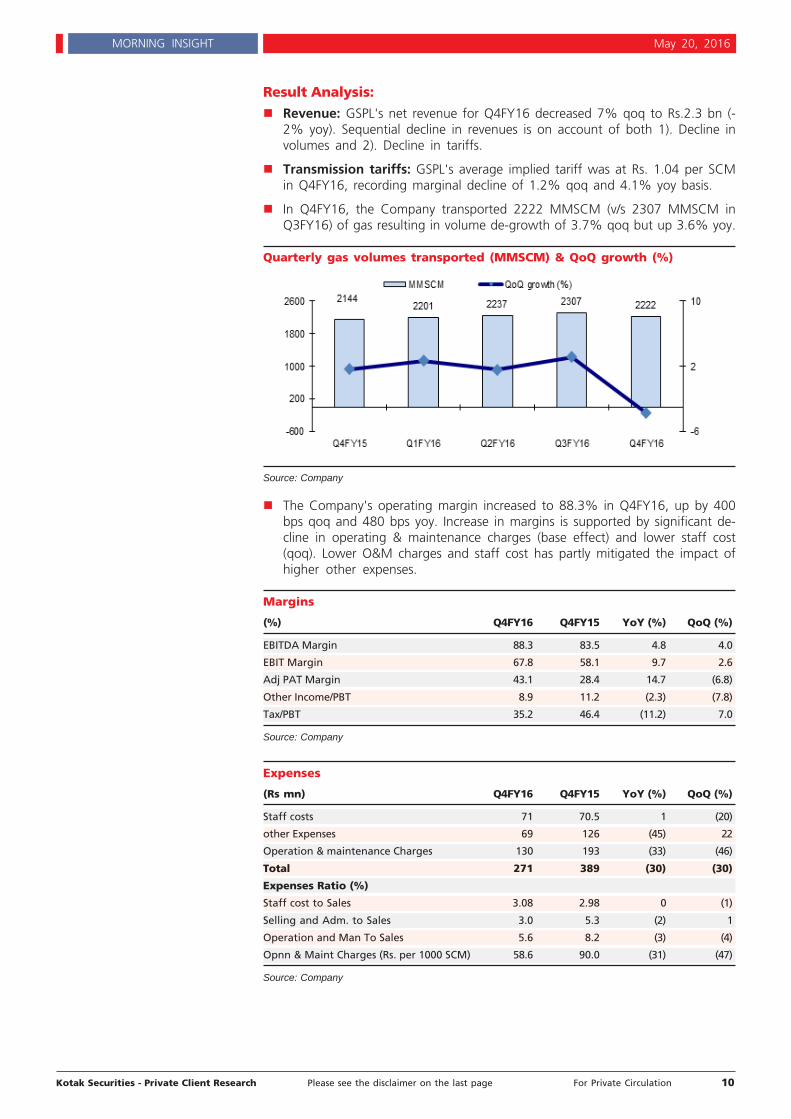

In Q4FY16, the Company transported 2222 MMSCM (v/s 2307 MMSCM inQ3FY16) of gas resulting in volume de-growth of 3.7% qoq but up 3.6% yoy.

Quarterly gas volumes transported (MMSCM) & QoQ growth (%)

Source: Company

The Company's operating margin increased to 88.3% in Q4FY16, up by 400bps qoq and 480 bps yoy. Increase in margins is supported by significant de-cline in operating & maintenance charges (base effect) and lower staff cost(qoq). Lower O&M charges and staff cost has partly mitigated the impact ofhigher other expenses.

Margins

(%) Q4FY16 Q4FY15 YoY (%) QoQ (%)

EBITDA Margin 88.3 83.5 4.8 4.0

EBIT Margin 67.8 58.1 9.7 2.6

Adj PAT Margin 43.1 28.4 14.7 (6.8)

Other Income/PBT 8.9 11.2 (2.3) (7.8)

Tax/PBT 35.2 46.4 (11.2) 7.0

Source: Company

Expenses

(Rs mn) Q4FY16 Q4FY15 YoY (%) QoQ (%)

Staff costs 71 70.5 1 (20)

other Expenses 69 126 (45) 22

Operation & maintenance Charges 130 193 (33) (46)

Total 271 389 (30) (30)

Expenses Ratio (%)

Staff cost to Sales 3.08 2.98 0 (1)

Selling and Adm. to Sales 3.0 5.3 (2) 1

Operation and Man To Sales 5.6 8.2 (3) (4)

Opnn & Maint Charges (Rs. per 1000 SCM) 58.6 90.0 (31) (47)

Source: Company

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 11

MORNING INSIGHT May 20, 2016

Operational profits registered de-growth of 2% qoq but up 3% yoy to Rs.2.04 bn. Lower operating profit is on account of lower volumes/tariffs, higherdiscounts and higher other expenses.

Depreciation cost decreased by 21% yoy but flat sequentially to Rs. 473 mn(Rs.601 mn in Q4FY15). Total capital employed increased 5.2% yoy toRs.55.03 Bn (-0.7% qoq) as on 31st March 2016.

Other income has decreased meaningfully 52% qoq to Rs. 137 mn (-2% yoy)due to lower dividend/interest income. Cash as on 31st March 2016 standshigher at Rs.5.45 bn as against Rs.4.35 bn as on 31st March'15.

The Company has partly paid of the costlier loan resulting in lower interestcash outflow. Interest cost reduced meaningfully 9% qoq (despite lowerbase) to Rs.168 mn (-36% yoy). Long term debt stands lower at Rs.7.89 bn ason 31st March 2016 as against Rs.8.88 bn as on 31st March 2015.

GSPL's PBT decreased 10% qoq to Rs.1.54 bn (+23% yoy) on account of rea-sons mentioned above.

In Q4FY16, GSPL paid tax at the rate of 35.2% as against 28.1% in Q3FY16.The income tax rate looks on higher side.

PAT for Q4FY16 was at Rs.997 mn lower 19% qoq but up 49% yoy basis re-sulting in quarterly EPS of Rs.1.77 and CEPS Rs.2.61.

Key triggers for stocks:

1). Clarity about tariff

2). Commissioning of the gas transmission pipeline

3). Ramp-up in gas supply and

4). Rupee appreciation

Key developments

In the short to medium term, we expect earnings will be supported by incremen-tal power sector gas demand/higher tariffs and in the long term, we expectcommissioning of the 5 mtpa Mundra terminal (as well as Dahej and Hazia ter-minal) would provide meaningful upside to gas transmission volumes, improvingpipeline utilization rates. In short, the Company's long term growth prospectslooks strong.

Natural Gas demand is expected to improve

Growing business: Higher gas transmission volumes will be supported by 1) lowerLNG prices-leading to pick up in demand from refineries, steel, fertilizer andother industries, 2) RLNG demand from the power sector (Gujarat based) adding2-3 mmscmd to volumes and 3) demand of ~1 mmscmd from new industrialunits in Dahej and Sanand. Additionally, rising city gas distribution growth oppor-tunities, potential shift to natural gas due to environmental/pollution norms (in-dustrial / CNG) and volumes from Mundra LNG terminal (FY18 onwards) addssupport to long term volumes.

Potential upward revision in tariffs

Added shine: APTEL quashed PNGRB's previous order on GSPL's pipeline tariffs.On 25th Nov'14, APTEL has asked PNGRB to a). Include the latest available datafor tariff computations, (b) Revisit key parameters which have adversely im-pacted the tariffs, and (c) Ensure a reasonable return of 12% post-tax RoCE forgas transmission pipelines over the life of the asset, as required by the regula-tions for tariff calculations. Hence, we expect a potential upward revision inpipeline tariffs by PNGRB.

We await PNGRB's final decision on gas pipeline tariffs and expect upward tariffrevision.

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 12

MORNING INSIGHT May 20, 2016

APTEL quashed PNGRB's previous order on GSPL's pipeline tariffs

Rs/mmbtu High-pressure gas grid network

Pipeline tariff computation by PNGRB (11th Sep'12)

Levelized tariffs proposed by GSPL 39.55

Total moderations/reductions by PNGRB (15.56)

Levelized tariff computed by PNGRB (Gross calorific value basis) -20 Nov'08 till 11 Mar'26 23.99

Change in date of applicability (From date of authorization of pipeline instead of date of

notification of the tariff regulation) 2.59

Revised levelized tariff computed by PNGRB (27th July'2012 till 11th Mar'26) 26.58

Source: PNGRB and Company

Valuation & RecommendationWe expect the Company to benefit on account of both 1). Higher gas transmis-sion volumes and 2). Expected upward revision in tariffs. Higher gas transmissionvolumes will be supported by 1) lower LNG prices, and 2) RLNG demand from thepower sector. Additionally, rising city gas distribution growth opportunities, po-tential shift to natural gas due to environmental/pollution norms (industrial /CNG) and volumes from Mundra LNG terminal (FY18 onwards) provides supportto long term volumes. We expect GSPL to report an EPS of Rs.10.2 and cash EPSof Rs.13.6 for FY17E and similarly an EPS of Rs.11 and cash EPS of Rs.14.6 forFY18E. Due to limited upside, we now recommend ACCUMULATE (earlier BUY)on GSPL with an unchanged target price of Rs.150/Share, given reasonable valu-ations at 12.3x PE based on FY2018E earnings.

Key risk remains Project execution risk

Lower than expected gas off-take by consumers

Delay in expected tariff hike by PNGRB

Going forward the major growth in GSPL is expected to come from inter-state pipelines across Gujarat, Rajasthan, Maharashtra and Andhra Pradesh.Thus its returns are expected to be capped in the near term.

We recommendACCUMULATE on GujaratState Petronet Ltd with a

price target of Rs.150

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 13

MORNING INSIGHT May 20, 2016

Kotak Securities Limited has two independent equity research groups: Institutional Equities and Private Client Group. This report hasbeen prepared by the Private Client Group. The views and opinions expressed in this document may or may not match or may be contrarywith the views, estimates, rating, target price of the Institutional Equities Research Group of Kotak Securities Limited.

RESULT UPDATE

Amit [email protected]

+91 22 6218 6439

GUJARAT PIPAVAV PORT LTD (GPPL)PRICE: RS.156 RECOMMENDATION: BUYTARGET PRICE: RS.175 FY18E P/E: 30.4X

Efforts taken by the management to add clients and improve services toits existing clients, improve infrastructure, have surplus capacity andsuperior hinterland connectivity has helped GPPL report stable volumesfor the quarter at 177,000 TEUs (+flat QoQ), revenues at Rs 1.61 bn (-2.7%QoQ) with highest ever EBIDTA margin primarily due to depreciation ofrupee in Q4. (INR averaged 67 in Q4 vs. 66 in Q3). We see the containernumbers as positive for GPPL despite weak global container trade andconsolidation in the container shipping industry. Another positive washealthy liquid cargo and car volumes, though both these segments form asmall portion of the overall cargo portfolio of GPPL. GPPL has alsoannounced its maiden equity dividend of Rs 1.9/share for FY16. MaintainBUY with a reduced TP of Rs 175 (from Rs 180) on reduced volumeassumption till 2028 (end of concession period).

Quarterly consolidated numbers

(Rs mn) Q5FY15 Q1FY16 Q2FY16 Q3FY16 Q4FY16

Sales 1,880 1,846 1,492 1,654 1,610

YoY % 20.4 9.7 -12.3 -10.4 -14.4

QoQ % 1.9 -1.8 -19.2 10.9 -2.7

Operating expense 377 405 326 294 295

Employee cost 123 130 138 128 75

Administration 254 326 263 230 248

Operating Expenditure 754 861 727 652 618

EBIDTA 1,126 985 765 1,002 992

EBIDTA (%) 59.9 53.4 51.3 60.6 61.6

Depreciation 162 240 227 249 247

Interest payment 1 1 1 1 1

Other income 51 59 72 64 65

Tax 0 0 681 282 310

PAT 1,014 803 (72) 534 499

Exceptional -354 0.0 604 0 0

PAT after exceptions 660 803 532 534 499

Equity 4,835 4,835 4,835 4,835 4,835

EPS (Rs) 2.1 1.7 -0.1 1.1 1.0

Source: Company

Important financial highlights for the quarter

Other expenses in the quarter includes Rs 60 mn onetime expense towardsdismantling and movement of cranes and installation of new cranes, (whichis now complete). Adjusted for this EBIDTA would have been Rs 1052 mn(OPM of 65.3%)

Employee cost was lower in the quarter at Rs 75 mn (down -39% YoY) on ac-count of lower incentive payment by the company.

Company has paid its maiden dividend of Rs 1.9 for FY16.

Summary table

(Rs mn) FY16 FY17E FY18E

Sales 6,602 7,213 7,736Growth (%) (23.9) 9.3 7.3EBITDA 3,744 4,076 4345EBITDA margin (%) 56.7 56.5 56.2PBT 3,037 3,385 3,610Net profit 1,764 2,370 2,527EPS (Rs) 3.6 4.9 5.2Growth (%) (54.3) 34.3 6.6CEPS (Rs) 5.6 6.9 7.4BV (Rs/share) 38.4 41.8 44.6Dividend / share (Rs) 1.9 1.5 2.5ROE (%) 9.5 11.7 11.7ROCE (%) 13.4 13.7 13.8Net cash (debt) 3,593 3,736 4,028NW Capital (Days) (20.2) (19.5) (18.5)EV/EBITDA (x) 19.6 17.9 16.8P/E (x) 43.6 32.4 30.4P/Cash Earnings 28.2 22.9 21.6P/BV (x) 4.1 3.8 3.6

Source: Company, Kotak Securities - Pri-vate Client Research

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 14

MORNING INSIGHT May 20, 2016

Expansion plans on trackGPPL is investing Rs 4.5bn to expand its container storage yard, add equipment,and strengthen handling capacity of the berths. The expansion is completed byand has increased the container handling capacity to 1.4mn TEU p.a (from 0.85mn TEUs). No investment would be made in expanding capacities of handlingother commodities. GPPL would take a call on further capacity addition oncecapacity utilization reaches the 70% mark. The company has healthy opera-tional cash flows of ~Rs 4 bn p.a and a healthy balance sheet (net cash com-pany). Thus, we do not expect funding of capex to be a challenge.

Making current facilities more efficientGPPL has also taken measures to improve efficiency and turnaround time ofships at its current terminals which should yield results for the company in timesof crisis.

The company has made the draft deeper and installed more efficient craneswhich can lead to the shifting of some shipping vessels other ports in Gujaratand Maharashtra.

Stable Q4FY16 gives comfortGPPL reported weak container volume at 693,000 (-13% YoY),This weaknesswas primarily due to: 1) Loss of business from two shipping lines in FY16, (2) lossof business in July due to heavy rains in Gujarat and most importantly 3) loss ofmarket share. However, the container volumes were stable in H2FY16 at355,000 due to special efforts taken by GPPL. Though the volumes are still awayfrom the quarterly run rate of 190,000/200,000 TEUs per quarter for GPPL, weestimate the container volumes to improve for GPPL in FY17. It is important tonote that GPPL (except for Q2FY16) had been continually adding new clients forits container business. Strategic location on the west coast and ability to provideseamless railway connectivity to hinterland helps GPPL attract container volumesfrom the capacity constrained congested JNPT port in Mumbai.

Quarterly Volumes for GPPL

Segment Q5FY15 Q1FY16 Q2FY16 Q3FY16 Q4FY16

Container ( No of TEUs) 201,000 193,000 146,000 178,000 177,000

Bulk (mn tonnes) 0.92 1.02 0.63 0.44 0.38

Liquid (mn tonnes) 0.13 0.11 0.16 0.19 0.25

Rail volumes (mn tonnes) 2.5 2.5 1.8 1.82 1.77

ICD volumes (TEUs) 143,000 133,000 105,000 124,000 119,000

No of rakes 692 644 550 664 702

Cars handled 6500 4500 8700

No of calls for cars 5 7 10

Source: Company

We estimate volumes to grow at a slow pace in near term

We expect container volumes for the port to grow at a moderate rate due toweak global container trade, weak exports from India and increasing competi-tion. However we are optimistic about the volumes in the longer run and havereduce the long term volume assumptions only marginally.

Volume Estimates for GPPL

Segment CY12 CY13 15mFY15 FY16 FY17E FY18E

Containers (mn TEUs) 0.57 0.64 0.98 0.69 0.77 0.83

Bulk (mn tonnes) 3.9 4.0 4.7 2.5 2.9 3.0

Liquid (mn tonnes) 0.0 0.0 0.3 0.7 1.0 1.2

Source; Company, Kotak Securities - Private Client Research

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 15

MORNING INSIGHT May 20, 2016

Bulk volumes to remain sedateBulk volumes (Coal, Fertilizer & Wheat) in Q4FY16 was sedate at 0.38mn tonnes(2.47 mn tonnes in FY16) for GPPL. Overall, bulk volumes continue to remainweak and we are not very optimistic (even management of GPPL) on bulk cargoin near term for GPPL.

High Margin liquid cargo to improve bottom line for GPPL margin-allyIn September 2014, GPPL commissioned a jetty to handle liquid cargos with ca-pacity of 2 mtpa. It has tied up with three companies - Aegis Logistics, Gulf Pet-rochemicals, and IMC for importing LPG, propane, and butane into India.

GPPL earns revenue in the form of lease rentals from land and charges for theusage of sea side facilities from these contracts. Margins from these contractsare around 80% as they are based on lease-rental model. We estimate the rev-enue contribution from the liquid cargo to be low till FY18E, but could increaseas and when expansion happens post CY17E. In FY16, GPPL handled a total of ~7 lakh tonnes (3 lakh tonnes in FY15) of liquid cargo. We estimate the companyto handle 10 lakh tonnes in FY17E and 12 lakh tonnes of liquid cargo in FY18E.

Creation of tank farms - Potential for Liquid cargo at GPPL

Company Tank Capacity (lakh litres) Status

Aegis Logistics 200,000 Operational

Gulf Petrochem 150.000 Operational

Indian Molasses Company 150,000 Operational

Source: Company, Kotak

Rail subsidiary PRCL continues to contribute to profitability

GPPL holds 38% in Pipavav Rail Corporation Ltd (PRCL) and has made an equityinvestment of Rs 1.6 bn. PRCL maintains and operate 271 kilometer long broadgauge railway line connecting Port of Pipavav to Surendranagar junction ofWestern Railway, in the state of Gujarat.

The rail operation has been reporting profits for the last 5 years. Financials ofPRCL of FY16 are not yet available. PRCL has paid a total dividend Rs 39 mn toGPPL from FY15 profits (Rs 9.8 mn in FY14)

Financial performance of PRCL for the last seven years

(Rs mn) FY09 FY10 FY11 FY12 FY13 FY14 FY15

Sales 684 766 896 1,530 1,790 2,240 2,317

Profit -238 -180 35 553 464 807 437

Source: Company

RoRo terminal has started to add to the revenues

The RoRo terminal at GPPL has started operations in August 2015 with a total of10 calls totaling 8700 cars for Q4FY16 and.GPPL is earning rental income fromthis RoRo terminal managed by NYK Auto Logistics (India) Pvt Ltd (NYK) whichhas an annual designed capacity to handle 250,000 vehicles.

Concerns:

Focused only on container business

Weak global trade

Competition from other ports in Maharashtra and Gujarat

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 16

MORNING INSIGHT May 20, 2016

Valuation and RecommendationLower volumes for GPPL in FY16 and lose market share to rivals is a major causeof concern for the company. Plus the business environment remains weak. Liquidand RoRo though looking promising, but would remain small for GPPL with con-tainer business as the mainstay. But the steps taken by the company to improveefficiency, superior rail connectivity, parentage of Maersk and sufficient capac-ity should yield results for the company.

Our valuation approach assumes that GPPL is a going concern and its concessionagreement would be extended for 20 years more (beyond 2028). We also as-sume that GPPL would reinvest its cash flows to step up container handling ca-pacity through subsequent expansions (it has around 600 acres of unutilized landat its port) and it continues to raise tariffs opportunistically, considering conges-tion at other ports. We build in modest volume growth of 7% p.a till end of FY28(end of concession period). Our estimate of the net present value of equity cashflow of the existing businesses - sum-of-parts value comes at ~ Rs 160 per share(16.8 x EV/EBIDTA FY18E). Pipavav Rail Corporation contributes ~ Rs 15per shareto the value of GPPL valuing the company at Rs 175 per share. Maintain BUY.

We maintain BUY on GujaratPipavav Port Ltd with a price

target of Rs.175

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 17

MORNING INSIGHT May 20, 2016

Kotak Securities Limited has two independent equity research groups: Institutional Equities and Private Client Group. This report hasbeen prepared by the Private Client Group. The views and opinions expressed in this document may or may not match or may be contrarywith the views, estimates, rating, target price of the Institutional Equities Research Group of Kotak Securities Limited.

LUPIN LTD

PRICE: RS.1665 RECOMMENDATION: REDUCETARGET PRICE: RS.1680 FY18E P/E: 20.7X

Revenues were at Rs 40.9bn, up 34% YoY, Domestic revenues have grownat 19% whereas US revenues posted 54% growth. EBIDTA margin is at32.7%, highest ever in last 3 years, was driven by better gross margins (at74%). PAT at Rs 8.07bn came in line with our expectation as (tax rate washigher than our exp, management has guided for a lower tax outgo thisquarter).Though Lupin's 4QFY16 was a robust quarter and the coming twoquarters would also be strong led by exclusivity launch of gGlumetza andbetter pricing in gFortamet, the outlook for the base business looks bleak.Management has lowered its guidance of US$ 5.0bn revenues (in 2018) toUS$ 3.5bn. We tweak our FY17E EPS lower by ~17% to Rs 68.3 (earlier Rs82.7) to factor lower revenues as well as increase in depreciation expenses(led by Gavis amortization). We turn cautious on Lupin and rate thecompany as a Reduce (from our positive stance earlier). We roll ourvaluations to next fiscal and are valuing the company at 21x (earlier 25x)FY18E EPS of Rs 80.0 and arrive at our target price of Rs 1680 (fromRs.2050 earlier).

RESULT UPDATE

Meeta Shetty, [email protected]

+91 22 6218 4425

Quarterly Financials - Snapshot

(Rsmn) 4QFY15 1QFY16 2QFY16 3QFY16 4QFY16 YoY (%) QoQ (%)

Net Revenues 30,540 30,743 31,783 33,577 40,913 34.0 21.9Material Expenses 9,564 9,834 11,294 11,230 10,737 12.3 (4.4)

Employee Expenses 4,822 4,860 5,242 5,284 5,691 18.0 7.7

Other Operating Expenses 5,039 5,841 6,082 6,357 6,597 30.9 3.8

R&D expenses 3,096 3,131 3,878 3,916 5,113 65.1 30.6

Operating Profits 8,020 7,077 5,288 6,790 12,776 59.3 88.2

Other Operating Income 241 759 1,430 1,982 898 272.6 (54.7)

EBITDA 8,261 7,836 6,717 8,772 13,674 65.5 55.9Interest Cost 25 24 102 92 229 830.1 149.2

Depreciation 1,072 1,007 1,068 1,114 1,446 34.9 29.8

Other Income 172 316 415 653 254 47.8 (61.1)

PBT 6,970 7,891 5,963 8,219 12,254 75.8 49.1Tax 1,362 2,644 1,851 2,909 4,132 203.3 42.0

PAT 5,607 5,247 4,111 5,310 8,122 44.9 53.0Minority interest (137) 3 (27) (13) (51) (62.6) 310.4

Reported PAT 5,470 5,250 4,084 5,298 8,071 47.5 52.4E/o (adj for tax) 295 (512) - (162) - (100.0) (100.0)

APAT 5,765 4,738 4,084 5,136 8,071 40.0 57.1AEPS 12.9 10.6 9.1 11.5 18.0 39.7 57.1

Source: Company

Margin Analysis (%)

4QFY15 1QFY16 2QFY16 3QFY16 4QFY16 YoY (bps) QoQ (bps)

Raw mat cost (%) 31.3 32.0 35.5 33.4 26.2 (507.2) (720.3)

Employee cost (%) 15.8 15.8 16.5 15.7 13.9 (187.8) (182.7)

Other expenses (%) 16.5 19.0 19.1 18.9 16.1 (37.6) (280.8)

R&D Expenses (%) 10.1 10.2 12.2 11.7 12.5 236.0 83.3

Operating Margin (%) 26.3 23.0 16.6 20.2 31.2 496.7 1,100.4

EBITDA Margin (%) 26.8 24.9 20.2 24.7 32.7 586.7 803.6

APAT Margin (%) 18.7 15.0 12.3 14.4 19.3 57.3 485.9

Tax Rate (%) 19.5 33.5 31.1 35.4 33.7 1,416.9 (167.6)

Source: Company

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 18

MORNING INSIGHT May 20, 2016

Revenue breakup

(Rs mn) 4QFY15 1QFY16 2QFY16 3QFY16 4QFY16 YoY (%) QoQ (%)

Formulations 27,465 27,486 28,564 30,817 38,075 38.6 23.6

- Domestic Formulations 6,637 8,851 8,738 8,712 7,615 14.7 (12.6)

- US formulations 13,779 11,906 11,550 14,049 21,871 58.7 55.7

- Japan formulations 2,943 3,231 3,234 3,739 3,442 17.0 (7.9)

- Europe formulations 891 856 1,158 1,010 1,254 40.7 24.2

- Other EM formulations 3,215 2,642 3,884 3,307 3,893 21.1 17.7

API 3,075 3,257 3,219 2,760 2,838 (7.7) 2.8

Net Revenues 30,540 30,743 31,783 33,577 40,913 34.0 21.8

Source: Company

Key highlights

Revenues at Rs 40.9 bn were up a robust 34% YoY. Lupin posted higher everrevenues this quarter led by the exclusive launch of gGlumetza.

Domestic formulations revenues posted 15% growth at Rs 7.6bn, previousquarter (3QFY16) growth was at mere 7%.

US revenues were higher than expectations at US$ 325mn, up a strong 54%YoY. The growth was mainly driven by gGlumetza launch, gFortamet pricingand Gavis consolidation. We expect the coming quarter to remain equallystrong.

The Company launched 9 products in the US market during the quarter tak-ing the number of total of launches to 21 products during FY16. Lupin mar-keted 124 products in market till end of FY16.

Lupin filed 17 ANDAs and received 6 approvals from the US FDA during thequarter. The Company filed 36 ANDA's and received 39 approvals duringFY2016. Cumulative ANDA filings with the US FDA stood at 343, March 31st,2016 with the company having received 180 approvals to date. The Companynow has 45 First-to-Files (FTF) filings including 35 exclusive FTF opportunities.

Europe formulations saw ~41% growth YoY whereas the Japan posted 17%growth. Japan posted positive growth for a second consecutive quarter fur-ther reviving hope for strong growth going ahead.

On the margins front, Gross margins improved 720bps QoQ and 500bps YoY,pointing towards better pricing on gGlumetza as well as gFortamet.

EBIDTA margins came in at 32.7%, a sharp recovery, post 2QFY16'sunderperformance (20.2% EBIDTA margins and 24.7% in 3QFY16).

Tax rate for the quarter was at 33.7%, sharply higher both YoY albeit on alow base. We were expecting a lower tax rate as Lupin had already paid~33% tax for 9MFY16 vs. its guidance of 30-31% tax rate for FY16.

Reported PAT came in at Rs 8.07bn, up 40% YoY and 57% QoQ led by bettersales coupled with higher margins.

Capital Expenditure was Rs. 3713 mn during the quarter.

Summary table

(Rs mn) FY16 FY17E FY18E

Sales 137,016 167,127 194,359Growth (%) 6.3 25.9 16.3EBITDA 37,535 50,507 57,630EBITDA margin (%) 26.4 29.2 28.7PBT 34,331 42,898 49,553Net profit 22,795 30,887 36,174EPS(Rs) 50.4 68.3 80.0Growth (%) (6.7) 35.5 17.1CEPS(Rs) 60.9 87.7 101.7BVPS(Rs) 243.8 302.6 372.6DPS (Rs) 8.0 8.0 8.5ROE (%) 22.9 25.0 23.7ROCE (%) 18.5 23.2 23.4Net debt 63,314 32,534 9,305NW Capital (Days) 147.1 102.6 93.0P/E (x) 32.8 24.2 20.7P/BV (x) 6.8 5.5 4.4EV/Sales (x) 5.9 4.7 3.9EV/EBITDA (x) 21.6 15.4 13.0

Source: Company, Kotak Securities - Pri-vate Client Research

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 19

MORNING INSIGHT May 20, 2016

Key concall highlights

Guidance

Lupin had guided for revenues of US$5.0bn by FY18 but post the recent com-pliance issues and pricing pressure in both US and India, the company hasrevised its guidance lower to US$3.5bn. This guidance does not include anyacquisition in future.

The growth drivers will be - growth in US base business, increasing contribu-tion from emerging markets and strong growth from specialty portfolio (bothorganic and inorganic).

US

Pricing pressure has increased since last year, earlier Lupin use to see 5-6%of price erosion but saw it at close to 20% in FY15 and high single digits inFY16. Lupin expects the price erosion to stabilize at earlier levels of 5-6%over the coming year.

Lupin currently has 5.6% prescription share in the US generic market.

For FY17, the growth in US revenues will be driven by gGlumetza andgFortamet as well as Gavis.

Going ahead, growth drivers for US will be specialty generics, partnershipsand new acquisitions. Under the specialty generics - oral contraceptives,ophthal, controlled substances, derma and injectables are the focus areas.

To enhance its branded business, Lupin has launched two new products.These products are from Gavis's portfolio and belong to pediatric andwomen's HC segment.

Lupin expects these two products will aid strong growth in the US brandedsegment and will lead to US$100mn revenues from the segment. (The rev-enues from branded segment stood at US$ 40mn in FY16).

Lupin and Gavis put together, the company has 343 ANDA filing of which 180are approved. Apart from these, the company has 256 molecules under de-velopment.

Lupin received a total 39 USFDA approvals in FY16 of which 14 were fromGavis and rest from Lupin filings. For FY17, Lupin expects ~30 ANDA approv-als of which 15 will be from Gavis and rest from Lupin's filings.

Total outstanding DMF filings stood at 179 as of FY16 of which 19 were filedin FY16.

In spite of a huge amortization cost for Gavis, Lupin still expects Gavis acqui-sition to be EPS accretive.

On the inhalation front, Lupin expects to file for MDI in FY17E and DPI inFY18E.

Domestic

Due to NLEM and FDC, the Indian market has become challenging. Lupin'sNLEM portfolio, in the domestic revenues, stands at 24%.

Company plans to enter alliances and enhance the relationships with existingpartners for keeping the momentum strong in the domestic market. Com-pany expects to post 15% growth in the segment in FY17.

Lupin added 1000 MRs and five new divisions in FY16.

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 20

MORNING INSIGHT May 20, 2016

Japan

Japanese government has been firm on increasing the contribution from ge-nerics within Japan, which will be the volume driver for generic companieslike Lupin; however, the pricing pressure remains an issue. The Yakka cutsthat use to happen at every two years will be every year from 2016. Lupinplans to introduce new products at a faster pace to overcome the pricingpressure.

R&D expenses

Company expects to increase its R&D expenditure to up to 12-15% of rev-enues in FY17E from ~11% in FY16. Of the total spend; generic filings will bethe key reason for the sharp increase in R&D expense followed by NCE filingsand Biosimilars filings.

Of the total R&D expenses, Biosimilars and NCE account for 1/6th each.

Compliance issues

From the outstanding compliance issues, Goa is of a concern due to the re-peat observations. However, the company has already sent across its repliesand a follow up over the last few months and is awaiting feedback fromFDA.

Though the company remains confident of no adverse event in any of itsplants, but as a risk mitigating strategy, Lupin has started site transfers offew key products to different sites to avoid delay in approvals.

Majority of the pending 100 ANDAs for Lupin are from Pitampur and Goa (30)

Others

Acquisitions for Lupin will remain the focus area, however, company is notkeen on any geographical expansion, but will consolidate its position in theexisting markets.

Lupin's acquisition over the past few years have grown up to a significantshare in overall revenues and as of FY16 stood at 20% of sales.

The tax rate has been higher for FY16 but expect it to come down to 28-30%in FY17 led by Gavis (amortization).

Gavis and Temler (both acquired in FY16) amortization stood at Rs 270mn inFY16. Going ahead, in FY17, Lupin expects its depreciation figure to grow 2xled by amortization of the newly acquired companies, mainly Gavis.

Capex for FY17E to be higher than its usual run rate of Rs 10 bn.

Outlook and Valuation

Though Lupin's 4QFY16 was a robust quarter and the coming two quarterswould also be strong led by exclusivity launch of gGlumetza and better pricing ingFortamet, the outlook for the base business looks bleak. Moreover, the over-hang of pending compliance issues adds to the uncertainty on revenues as wellas profitability. Due to the uncertainties, management has lowered its guidanceof US$ 5.0bn revenues (in 2018) to US$ 3.5bn. We were always of the view thatthe target of US$ 5.0bn revenue was far stretched.

We had an 'Under Review' rating on Lupin since Mar-16 due to no visibility onUSFDA compliance issues on its plants. Though the ambiguity on that part re-mains, we derive visibility on revenues/margins from the management interac-tion on opportunities and challenges.

We tweak our FY17E revenues (10%) lower from Rs 185bn to Rs 167bn as wefactor lower off take in US base business due to delay in US approval (led bycompliance issues) and a weak domestic formulation segment growth.

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 21

MORNING INSIGHT May 20, 2016

We also factor a steep increase in depreciation/amortization cost as Lupin willbe aggressively amortizing the (Gavis) intangibles. The depreciation expense isexpected to increase 2x from Rs 4.6bn in FY16 to Rs 8.6bn in FY17E. Our revisedEPS for FY17E now stands at Rs 68.3 from Rs 82.7 (down ~17%)

We foresee challenges for Lupin post 2HFY17 (as the exclusivity benefit will sub-side by then) in both US as well as domestic markets. Plus the cost associatedwith getting back in compliance and escalating R&D expense will restrict bottomline. Hence, we turn cautious on Lupin and rate the company as a REDUCE. Weroll our valuations to next fiscal and are valuing the company at 21x (earlier 25x)FY18E EPS of Rs 80.0 and arrive at our target price of Rs 1680 (Rs.2050 earlier).

We recommend REDUCE onLupin Ltd with a price target

of Rs.1680

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 22

MORNING INSIGHT May 20, 2016

Gainers & Losers Nifty Gainers & LosersPrice (Rs) chg (%) Index points Volume (mn)

Gainers

BPCL 943 1.1 NA 1.0

Lupin Ltd 1,655 1.1 NA 3.5

Power Grid 144 0.9 NA 3.4

Losers

Adani Ports 172 (6.4) NA 13.48

SBI 173 (4.0) NA 25.5

Bank of Baroda 137 (3.7) NA 10.0

Source: Bloomberg

Bulk deals

Forthcoming events Company/MarketDate Event

20 - May Allcargo, DB Corp, IDBI, ITC earnings expected

Source: Bloomberg

Trade details of bulk deals

Date Scrip name Name of client Buy/ Quantity Avg.Sell of shares price

(Rs)

19-May ABHIINFRA Kamal Jaswantlal Sheth B 35,000 35.1

19-May ANSHUS Noormohammed Yusuf Dinath B 74,500 8.7

19-May BITL Competent Textiles Pvt Ltd S 130,766 2.9

19-May BVL Nem Sagar Resources (P) Ltd S 42,000 44.0

19-May BVL Arch Finance Limited B 24,000 44.0

19-May BVL Sunil Kumar Katiyar B 18,000 44.0

19-May CASTROLIND Government Of Singapore

A/C Government Of Singapore C B 3,522,648 365.0

19-May CASTROLIND Citigroup Global Markets Mauritius B 6,300,000 365.0

19-May DARSHANORNA Pinalben R. Shah B 50,000 61.0

19-May DELTA Ravi Kumar S 29,290 11.0

19-May GEETANJ Kamleshkumar G Solanki B 40,000 21.3

19-May JAIHINDS Khushal Das B 25,000 11.4

19-May MALWACOTT IFCI Ltd. S 55,000 5.9

19-May MOLDTEK Ritu Goenka B 150,000 49.1

19-May MOLDTEK Akg Finvest Ltd S 305,000 46.7

19-May MOLDTEK Vimal Sagarmal Jain S 203,500 43.7

19-May MOLDTEK Jagartius Universal S 150,251 46.7

19-May NAVIGANT Naysaa Seurities Ltd S 30,000 6.0

19-May OBRSESY Swati Taparia B 37,000 5.2

19-May PFLINFOTC Dhiraj Nirmal Rathod S 39,500 26.1

19-May RELCHEMQ Ashok Kumar Jain S 33,285 76.7

19-May SAFALSEC Punaji Somaji Thakor B 69,099 3.0

19-May SIKOZY Kshiti Rishit Maniar B 704,110 0.7

19-May SIKOZY Kriyasu Finvest Pvt Ltd S 704,110 0.7

19-May SMFIL Suresh Shastry S 634,026 5.0

19-May TFL Vinod Mohan Nair S 659,670 7.1

19-May TFL Arvind Khattar B 659,670 7.1

19-May YOGYA Indo Jatalia Securities Pvt Ltd B 56,000 4.3

19-May YOGYA Subhlaxmi Investment Advisory S 32,000 4.3

Source: BSE

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 23

MORNING INSIGHT May 20, 2016

RATING SCALE

Definitions of ratingsBUY – We expect the stock to deliver more than 12% returns over the next 9 months

ACCUMULATE – We expect the stock to deliver 5% - 12% returns over the next 9 months

REDUCE – We expect the stock to deliver 0% - 5% returns over the next 9 months

SELL – We expect the stock to deliver negative returns over the next 9 months

NR – Not Rated. Kotak Securities is not assigning any rating or price target to the stock. The report has been prepared for information purposesonly.

RS – Rating Suspended. Kotak Securities has suspended the investment rating and price target for this stock, either because there is not a suffi-cient fundamental basis for determining, or there are legal, regulatory or policy constraints around publishing, an investment rating or target.The previous investment rating and price target, if any, are no longer in effect for this stock and should not be relied upon.

NA – Not Available or Not Applicable. The information is not available for display or is not applicable

NM – Not Meaningful. The information is not meaningful and is therefore excluded.

NOTE – Our target prices are with a 9-month perspective. Returns stated in the rating scale are our internal benchmark.

Fundamental Research Team

Dipen ShahInformation [email protected]+91 22 6218 5409

Sanjeev ZarbadeCapital Goods, [email protected]+91 22 6218 6424

Teena VirmaniConstruction, [email protected]+91 22 6218 6432

Saday SinhaBanking, NBFC, [email protected]+91 22 6218 6437

Arun AgarwalAuto & Auto [email protected]+91 22 6218 6443

Ruchir KhareCapital Goods, [email protected]+91 22 6218 6431

Ritwik RaiFMCG, [email protected]+91 22 6218 6426

Sumit PokharnaOil and [email protected]+91 22 6218 6438

Amit AgarwalLogistics, [email protected]+91 22 6218 6439

Meeta Shetty, [email protected]+91 22 6218 6425

Jatin DamaniaMetals & [email protected]+91 22 6218 6440

Pankaj [email protected]+91 22 6218 6434

Nipun GuptaInformation [email protected]+91 22 6218 6433

Jayesh [email protected]+91 22 6218 5373

K. [email protected]+91 22 6218 6427

Technical Research Team

Shrikant [email protected] 22 6218 5408

Amol [email protected]+91 20 6620 3350

Derivatives Research TeamSahaj [email protected]+91 79 6607 2231

Rahul [email protected]+91 22 6218 5498

Malay [email protected]+91 22 6218 6420

Prashanth [email protected]+91 22 6218 5497

Kotak Securities - Private Client Research Please see the disclaimer on the last page For Private Circulation 24

MORNING INSIGHT May 20, 2016

DisclaimerKotak Securities Limited established in 1994, is a subsidiary of Kotak Mahindra Bank Limited. Kotak Securities is one of India's largest brokerage anddistribution house.Kotak Securities Limited is a corporate trading and clearing member of Bombay Stock Exchange Limited (BSE), National Stock Exchange of India Limited (NSE),Metropolitan Stock Exchange of India Limited (MSEI). Our businesses include stock broking, services rendered in connection with distribution of primarymarket issues and financial products like mutual funds and fixed deposits, depository services and Portfolio Management.Kotak Securities Limited is also a depository participant with National Securities Depository Limited (NSDL) and Central Depository Services (India) Limited(CDSL). Kotak Securities Limited is also registered with Insurance Regulatory and Development Authority as Corporate Agent for Kotak Mahindra Old MutualLife Insurance Limited and is also a Mutual Fund Advisor registered with Association of Mutual Funds in India (AMFI). We are registered as a Research Analystunder SEBI (Research Analyst) Regulations, 2014.We hereby declare that our activities were neither suspended nor we have defaulted with any stock exchange authority with whom we are registered in lastfive years. However SEBI, Exchanges and Depositories have conducted the routine inspection and based on their observations have issued advise letters orlevied minor penalty on KSL for certain operational deviations. We have not been debarred from doing business by any Stock Exchange / SEBI or any otherauthorities; nor has our certificate of registration been cancelled by SEBI at any point of time.We offer our research services to clients as well as our prospects.This document is not for public distribution and has been furnished to you solely for your information and must not be reproduced or redistributed to any otherperson. Persons into whose possession this document may come are required to observe these restrictions.This material is for the personal information of the authorized recipient, and we are not soliciting any action based upon it. This report is not to be construedas an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It is for the generalinformation of clients of Kotak Securities Ltd. It does not constitute a personal recommendation or take into account the particular investment objectives,financial situations, or needs of individual clients.We have reviewed the report, and in so far as it includes current or historical information, it is believed to be reliable though its accuracy or completenesscannot be guaranteed. Neither Kotak Securities Limited, nor any person connected with it, accepts any liability arising from the use of this document. Therecipients of this material should rely on their own investigations and take their own professional advice. Price and value of the investments referred to in thismaterial may go up or down. Past performance is not a guide for future performance. Certain transactions -including those involving futures, options andother derivatives as well as non-investment grade securities - involve substantial risk and are not suitable for all investors. Reports based on technical analysiscenters on studying charts of a stock's price movement and trading volume, as opposed to focusing on a company's fundamentals and as such, may not matchwith a report on a company's fundamentals.Opinions expressed are our current opinions as of the date appearing on this material only. While we endeavor to update on a reasonable basis theinformation discussed in this material, there may be regulatory, compliance or other reasons that prevent us from doing so. Prospective investors and othersare cautioned that any forward-looking statements are not predictions and may be subject to change without notice. Our proprietary trading and investmentbusinesses may make investment decisions that are inconsistent with the recommendations expressed herein.Kotak Securities Limited has two independent equity research groups: Institutional Equities and Private Client Group. This report has been prepared by thePrivate Client Group. The views and opinions expressed in this document may or may not match or may be contrary with the views, estimates, rating, targetprice of the Institutional Equities Research Group of Kotak Securities Limited.We and our affiliates/associates, officers, directors, and employees, Research Analyst(including relatives) worldwide may: (a) from time to time, have long orshort positions in, and buy or sell the securities thereof, of company (ies) mentioned herein or (b) be engaged in any other transaction involving such securitiesand earn brokerage or other compensation or act as a market maker in the financial instruments of the subject company/company (ies) discussed herein oract as advisor or lender / borrower to such company (ies) or have other potential/material conflict of interest with respect to any recommendation and relatedinformation and opinions at the time of publication of Research Report or at the time of public appearance. Kotak Securities Limited (KSL) may haveproprietary long/short position in the above mentioned scrip(s) and therefore may be considered as interested. The views provided herein are general innature and does not consider risk appetite or investment objective of particular investor; readers are requested to take independent professional advicebefore investing. This should not be construed as invitation or solicitation to do business with KSL. Kotak Securities Limited is also a Portfolio Manager.Portfolio Management Team (PMS) takes its investment decisions independent of the PCG research and accordingly PMS may have positions contrary to thePCG research recommendation. Kotak Securities Limited does not provide any promise or assurance of favourable view for a particular industry or sector orbusiness group in any manner. The investor is requested to take into consideration all the risk factors including their financial condition, suitability to riskreturn profile and take professional advice before investing.The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company orcompanies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations orviews expressed in this report.No part of this material may be duplicated in any form and/or redistributed without Kotak Securities' prior written consent.Details of Associates are available on our website ie www.kotak.comResearch Analyst has served as an officer, director or employee of subject company(ies): NoWe or our associates may have received compensation from the subject company(ies) in the past 12 months. We or our associates may have managed or co-managed public offering of securities for the subject company(ies) in the past 12 months. We or our associates may have received compensation forinvestment banking or merchant banking or brokerage services from the subject company(ies) in the past 12 months. We or our associates may have receivedany compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company(ies) in thepast 12 months. We or our associates have not received any compensation or other benefits from the subject company(ies) or third party in connection withthe research report. Our associates may have financial interest in the subject company(ies).Research Analyst or his/her relative's financial interest in the subject company(ies): NoKotak Securities Limited has financial interest in the subject company(ies): Lupin, IRB Infra - YesOur associates may have actual/beneficial ownership of 1% or more securities of the subject company(ies) at the end of the month immediately precedingthe date of publication of Research Report.Research Analyst or his/her relatives has actual/beneficial ownership of 1% or more securities of the subject company(ies) at the end of the monthimmediately preceding the date of publication of Research Report: NoKotak Securities Limited has actual/beneficial ownership of 1% or more securities of the subject company(ies) at the end of the month immediately precedingthe date of publication of Research Report: NoSubject company(ies) may have been client during twelve months preceding the date of distribution of the research report."A graph of daily closing prices of securities is available at www.nseindia.com and http://economictimes.indiatimes.com/markets/stocks/stock-quotes. (Choosea company from the list on the browser and select the "three years" icon in the price chart)."Kotak Securities Limited. Registered Office: 27 BKC, C 27, G Block, Bandra Kurla Complex, Bandra (E), Mumbai 400051. CIN: U99999MH1994PLC134051,Telephone No.: +22 43360000, Fax No.: +22 67132430. Website: www.kotak.com. Correspondence Address: Infinity IT Park, Bldg. No 21, Opp. Film City Road,A K Vaidya Marg, Malad (East), Mumbai 400097. Telephone No: 42856825. SEBI Registration No: NSE INB/INF/INE 230808130, BSE INB 010808153/INF011133230, MSEI INE 260808130/INB 260808135/INF 260808135, AMFI ARN 0164, PMS INP000000258 and Research Analyst INH000000586. NSDL/CDSL: IN-DP-NSDL-23-97. Our research should not be considered as an advertisement or advice, professional or otherwise. The investor is requested to take intoconsideration all the risk factors including their financial condition, suitability to risk return profile and the like and take professional advice before investing.Investments in securities are subject to market risk; please read the SEBI prescribed Combined Risk Disclosure Document prior to investing. Derivatives are asophisticated investment device. The investor is requested to take into consideration all the risk factors before actually trading in derivative contracts.Compliance Officer Details: Mr. Manoj Agarwal. Call: 022 - 4285 6825, or Email: [email protected] case you require any clarification or have any concern, kindly write to us at below email ids: Level 1: For Trading related queries, contact our customer service at '[email protected]' and for demat account related queries contact us at

[email protected] or call us on: Online Customers - 30305757 (by using your city STD code as a prefix) or Toll free numbers 18002099191 / 1800222299,Offline Customers - 18002099292

Level 2: If you do not receive a satisfactory response at Level 1 within 3 working days, you may write to us at [email protected] or call us on 022-42858445 and if you feel you are still unheard, write to our customer service HOD at [email protected] or call us on 022-42858208.

Level 3: If you still have not received a satisfactory response at Level 2 within 3 working days, you may contact our Compliance Officer (Name: ManojAgarwal ) at [email protected] or call on 91- (022) 4285 6825.

Level 4: If you have not received a satisfactory response at Level 3 within 7 working days, you may also approach CEO (Mr. Kamlesh Rao) [email protected] or call on 91- (022) 6652 9160.