Embed Size (px)

Citation preview

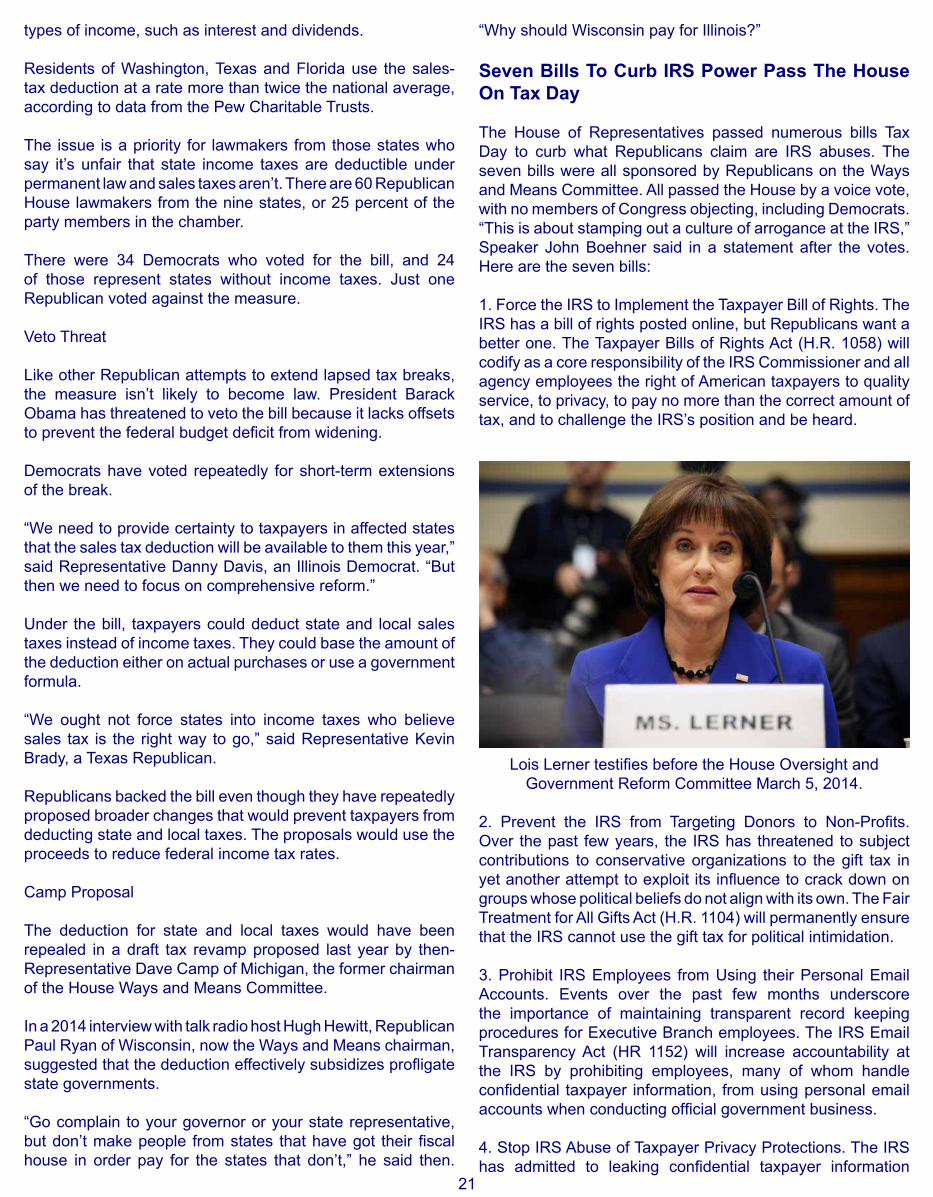

1

Monthly Newsletter for ncpeFellowship Members Vol. 6 No. 5 May 2015

1

Remarks from Beanna

Part I. - What a Filing Season!

It was like no other. When I thought back to the multiple changes of the 1986 tax act, I am convinced that the filing season for 2014 was like 1986 on steroids.

I am always glad to see the season end, wishing I had known as much about taxes and my software in January as I did on April 15th but this year the angst and complexity of the season was overwhelming. It was of little consolation that many of you were suffering as well.

When I am asked, “How did tax season go?” I respond that it went and I am grateful. What didn’t kill me did make me stronger.

Multiple times when encountering difficult situations I remarked to my husband of 47 tax seasons (that’s how we mark our years of marriage) I’m not smart enough to be in this business. But as he tells me, “Beanna, you can’t know everything and taxes are getting more difficult.” And, he is right!

So it begins again, the process of getting ready to encounter a new filing season - the Education we reach out to ncpe to present, the Resources of the ncpeFellowship AND, the Experience that encountering tax issues will bring. The process is proven, the results are our contribution to effective tax administration.

So in all things - Work and play - Stay well and Finish well.

Beanna

Part II - The Fellowship begins its 6th year!

Almost too good to be true, the ncpeFellowship began May 1, 2010 and now we begin our 6th year of bonding our tax professionals in the serious business of tax by education, resources and information.

5th5th

May 1st, 2015

Fellowship Members

Serving

2

As we begin our 6th year we honor those ncpeFellowship Members who had the courage and faith to trust us in creating a new organization that would benefit their practices. The following list of current members were first to join the Fellowship in May, 2010:

Jean Bennett-Dicus - First to join!Deryck FerrierMartha BellRuth BoothCaleb BarnhartDavid EllwangerHarry HiltyDon HoodBonnie KnottRichard ReedmanJane BradleyWesley BrooksShirley CallahanJack ConklinSusan CopelandCarol DouglassBob DudleyWanda GoodsonCharles Hensel, Sr.Laurie LutzDoug RiversAbe WarsenbrotRon MermerTom PintagroAndy AndersonWil DufourSusan CarltonJohn StancilMelody Lavoie-CostaDorothy LeamonDeanne JaredAbigail LauterbornLynn JacobsJim PrimmMichael GreenleafJuan MenaRichard DepewDebra DuncanEdward GonzalesCharles MooreCos Borzumate

The Fellowship appreciates your confidence and loyalty.

Additionally, I want to thank my cadre of roving reporters out there, always with an eye to tax news of interest to the Fellowship:

Marty SteinJoan LeValleyCos BorzumatePat HurleyLynn SchmidtLinda and Richard Odemar

Bonnie Harwick

To our monthly contributors to the Taxing Times:

Wayne Hebert - Wayne’s WorldJerry Riles - Ragin’ Cagin’Marti Myers - Armed Forces TaxDon Williamson - The Estate and Trust Guy

We thank all our fine Sponsors of the Fellowship for providing excellent goods and services to our Members.

And, most importantly, we thank you, our Members, for continuing in your membership. Individually you are fabulous, but together we are AWESOME.

To all in the ncpeFellowship, who encourage, appreciate and respond when needed. We have made significant strides this year in getting the attention of the IRS, notably the Form 3115 simplification on February 14 - Love Small Business Day and on “address change notices” going out to taxpayers when the tax professional should have been notified.

While we encourage the IRS to aggressively take bad preparers off the street, we support the growing recognition that tax professionals are a contributing factor to effective tax administration and the tax profession.

So as we look to the future, let those who join us take up our commitment to be the very best in our chosen profession of tax.

[email protected] or 877-403-1470

Newly Released:

2015 LLCThe Incredible

Limited Liability Company2-CE Hours Webinar

2015 Identity Theft1-CE Hour Webinar

2014 TIPATax Increase Prevention Act

1-CE Hour Webinar

3

Remarks from Beanna (1)

Tax News (5)

What A Nightmare (5)93% of Tax Returns by Preparers Had Errors, Study Finds (6)Complaints Rising Against Tax Preparers (6)Prepared in Error (7)Bottom Line: 94-year-old Tax Preparer Still in Top Form (8)Report Finds Taxes Done By Non-CPA Preparers Riddled with Inaccuracies (9)Tax Complexity Is Expensive for Small Businesses (10)Justice Department Asks Federal Court to Permanently Shut Down Liberty Tax Service Franchise Owner (10)H&R Block to Announce Fiscal 2015 Results on June 8 (11)The Danger Of Overstuffing Your IRA (11)Credit and ID Monitoring Won’t Protect you From Tax Cheats (14)Tax Cheaters Buy Used Non-Winning Lottery Tickets to Offset Winnings (14)Attacking Taxes: Preparers Say Identity Theft, Health Care Top Questions (15)The Affordable Health Care Act (15)Warren Buffett’s Nifty Tax Loophole (16)Summary of Estate and Gift Tax Law Changes for 2015 (16)

Washington Developments (17)ABA Weighs In On Proposals to Require Use of Accrual Method By Personal Service Corporations (17)

Practice Management (19)

Apply the Four-year Rule When Throwing Away Old {payroll Records (19)

Legislative Update From Capitol Hill (20)

Proposed Estate Tax Repeal Pending in U.S. Senate (20)Texas, Florida Win as House Passes State Sales Tax Break (20)Seven Bills To Curb IRS Power Pass The House On Tax Day (21)Tax and Accounting Groups Spending Heavily on Lobbying (22)Favor a Flat Tax? Sen. Richard Shelby Just Introduced a Bill to Make It A Reality (23)House Passes Bill to Repeal Estate Tax (24)

Don the Estate and Trust Guy (25)Extension for Estate and Trust Income Tax Return Likely to Require Many Other Extensions (25)

Armed Forces Tax (25)

You receive Form 1098-T from your Military veteran taxpayer, their spouse or child…WHAT NEXT?? (25)

People in the Tax News (25)

Obamas Paid $93,362 in Income Taxes on Earnings of $477,383 (25)Taxing Stephen King, Taylor Swift And Phil Mickelson (26)Michigan Resident Sentenced to Prison for Criminal Contempt Involving Federal Tax Obligation (27)Study: Sen. Pat Roberts Tops List for Donations From Tax Preparers (27)Lois Lerner Will Not Face Contempt Prosecution Over IRS Scandal (28)San Jose Priest Faces Bank Fraud, Tax Evasion Charges (28)Real-estate Heir Blows $3.5M Meant for Charity on Cars, Hotels, Suit (29)

IRS News (29)

TIGTA Reports on IRS Self-Service by Taxpayers (29)Commissioner Sheds Light on Specific Consequences of IRS Underfunding (30)

Seminars:Listing of 2015 NCPE Seminars

With Course Curriculum, Dates, Locationsare on websites

http://ncpeSeminars.comhttp://ncpeFellowship.com

For npceFellowship Members OnlyNew Features on Websitehttp://ncpeFellowship.com

Tax Subject LibrarySearchable By Topic

andSearch for all

ncpeFellowship Newsletters Taxing Times,Tax Court Cases,

other Articles and Postings

Table Of Contents (page)

4

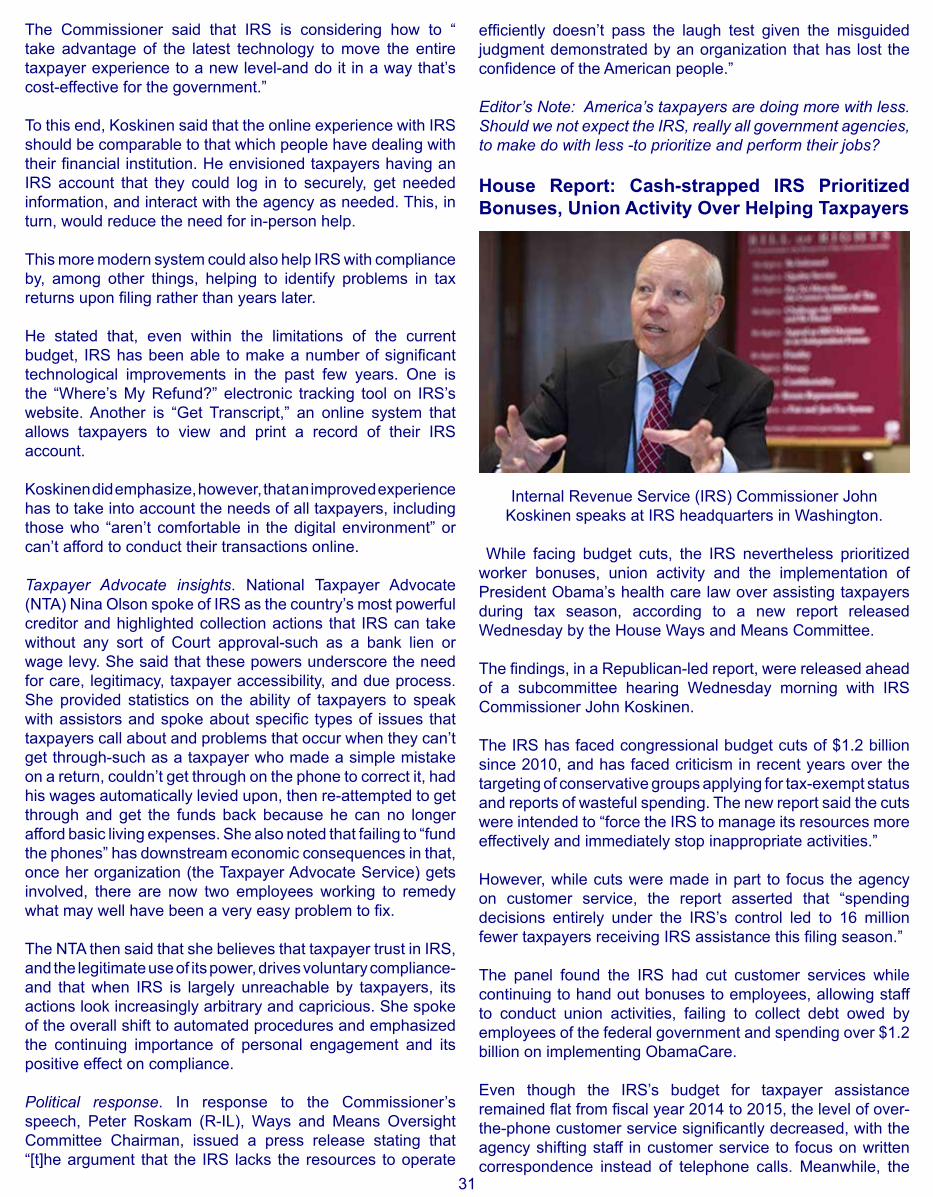

House Report: Cash-strapped IRS Prioritized Bonuses, Union Activity Over Helping Taxpayers (31)Would You Let the I.R.S. Prepare Your Taxes? (32)How the IRS Repeatedly Rewrites Obamacare Tax Credit Provisions (33)OPR is Delegated Authority to Regulate the Representation Activities of Unlicensed Return Preparers (35)Tax Man May Have Awarded $2.7 Billion in Improper Business Credits on Returns (35)IRS Had Tough Tax Season Leaving Workers Depressed (35)IRS Runs Out of Forms as Furious Taxpayers Wait In Line for Hours (40)9 Assets Seized and Put Up for Auction by the IRS (40)IRS Won’t Penalize People for Failing to Say They Have Health Insurance on Tax Form (42)TIGTA Addresses IRS Action on Excess IRA Contributions (42)TIGTA: How IRS Should Better Control Third-party Payroll Service Providers (43)

Tax Pros in Trouble (44)

Alton Woman Sentenced to Prison for False Tax Returns (44)Justice Department Sues San Francisco Enrolled Agent to Bar Promotion of Abusive Tax Avoidance Schemes (44)Broward Tax Preparers Get Prison Time For Tax Fraud (45)Fort Worth Judge Spars with Tax Fraudster Over her Hysterectomy, Prison Date (45)Four El Pasoan Women Indicted in Connection with $90,000 Tax Return Fraud Scheme (46)Federal Complaint Filed Against Mother-daughter Tax Return Preparers (47)New York City Tax Return Preparer Indicted for Aiding or Assisting in Preparation of False Tax Returns (47)

Ragin Cagin (48)

How To Tell Inconsiderate Clients You’ll Be Extending Their Returns (48)

Taxpayer Advocacy (49)

Who is Authorized to Sign a Power of Attorney for a Partnership or LLC? (49)No Deduction for Restitution Amount Paid to Avoid Criminal Prosecution (50)

Foreign Taxes (51)

IRS Issues Housing Cost allowances for Those Working Abroad in High-cost Areas in 2015 (51)

State News of Note (51)

States With the Worst Taxes on Average Earners (51)

Wayne’s World (53)

Supreme Court To Hear Challenge To ACA Subsidies (53)

Letters to the Editor (54)

Tax Jokes and Quotes (54)

Sponsor of the Month (55)

ncpe and ncpeFellowship (55)

Searchable Books of

2014 Summer Series NCPE Seminars2014 Fall Series NCPE Seminars

Available For Purchase

2014 Taxation Of Ministers1-CE Hour

2014 IRS Audits1-CE Hour

2014 ACA(Affordable Healthcare Act)

What We KnowWhat We Think We Know

What We Don’t KnowWhy We Have No Clue

The ACA of Today!3-CE Hours

2014 TIPATax Increase Prevention Act

1-CE Hour

5

Tax News

What A Nightmare

While Tax Day has come and gone, our broken tax code is here to stay. As millions of Americans sat down and filed their taxes this week, they were reminded of how confusing, complex, and unfair the U.S. tax code is for hardworking families and small businesses. You don’t have to be a tax accountant to take a look at the numbers below and know that our tax code is a nightmare - making the U.S. uncompetitive, hurting job growth and wages.

• #1 – The United States has the highest corporate tax rate in the industrialized world, forcing jobs overseas and leaving America and its workers at a disadvantage as our outdated international tax code threatens competitiveness in the global marketplace.

• 70,000 pages – The U.S. tax code is now more than 70,000 pages long – or 50 times the size of Tolstoy’s War and Peace. It is no wonder our tax code is a mess, riddled with loopholes and special exemptions for the few.

• 30 years - The last time we reformed our tax code was in 1986 – almost 30 years ago – before the days of the internet while Maverick, Goose & Iceman were on the highway to the danger zone.

• 6 billion hours – Hardworking taxpayers spend six billion hours trying to sort through the tax code. Time that could be better spent building a business, spending time with your family, or watching Taylor Swift gifs.

• 44.6 percent – Small businesses face tax rates as high as 44.6 percent, placing a huge economic burden on their businesses, stifling their ability to grow, expand, and hire new workers.

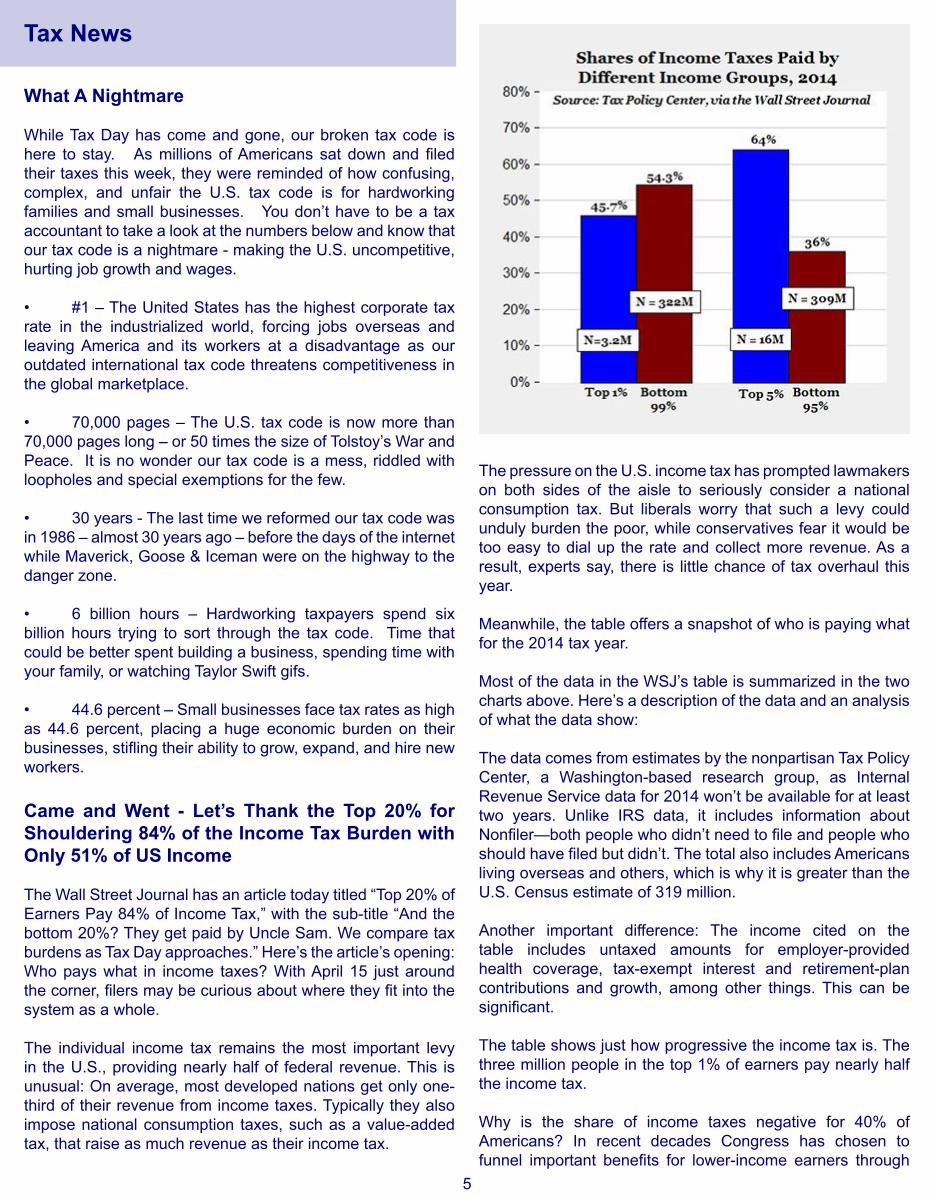

Came and Went - Let’s Thank the Top 20% for Shouldering 84% of the Income Tax Burden with Only 51% of US Income

The Wall Street Journal has an article today titled “Top 20% of Earners Pay 84% of Income Tax,” with the sub-title “And the bottom 20%? They get paid by Uncle Sam. We compare tax burdens as Tax Day approaches.” Here’s the article’s opening:Who pays what in income taxes? With April 15 just around the corner, filers may be curious about where they fit into the system as a whole.

The individual income tax remains the most important levy in the U.S., providing nearly half of federal revenue. This is unusual: On average, most developed nations get only one-third of their revenue from income taxes. Typically they also impose national consumption taxes, such as a value-added tax, that raise as much revenue as their income tax.

The pressure on the U.S. income tax has prompted lawmakers on both sides of the aisle to seriously consider a national consumption tax. But liberals worry that such a levy could unduly burden the poor, while conservatives fear it would be too easy to dial up the rate and collect more revenue. As a result, experts say, there is little chance of tax overhaul this year.

Meanwhile, the table offers a snapshot of who is paying what for the 2014 tax year.

Most of the data in the WSJ’s table is summarized in the two charts above. Here’s a description of the data and an analysis of what the data show:

The data comes from estimates by the nonpartisan Tax Policy Center, a Washington-based research group, as Internal Revenue Service data for 2014 won’t be available for at least two years. Unlike IRS data, it includes information about Nonfiler—both people who didn’t need to file and people who should have filed but didn’t. The total also includes Americans living overseas and others, which is why it is greater than the U.S. Census estimate of 319 million.

Another important difference: The income cited on the table includes untaxed amounts for employer-provided health coverage, tax-exempt interest and retirement-plan contributions and growth, among other things. This can be significant.

The table shows just how progressive the income tax is. The three million people in the top 1% of earners pay nearly half the income tax.

Why is the share of income taxes negative for 40% of Americans? In recent decades Congress has chosen to funnel important benefits for lower-income earners through

6

income tax returns. The other groups that participated in the study were the Florida Alliance for Consumer Protection and Reinvestment Partners in North Carolina.

“To see this level of errors is extremely disturbing,” Chi Chi Wu, staff attorney at the National Consumer Law Center, said in a statement. “A tax return may be the most important financial document for an American consumer during the year, and consumers who use paid preparers are placing their financial well-being in the preparers’ hands.”

This isn’t the first time tax preparers flunked such an examination. The Government Accountability Office last year did a limited test and found that only two of 19 tax preparers the agency tested came up with accurate refund amounts.

Minimal Standards for Preparers

This isn’t the first time that tax preparers flunked such an examination. The Government Accountability Office last year did a limited test and found that only two of 19 tax prepares the agency tested came up with accurate refund amounts.

It’s a major issue, the NCLC said, is that just about anyone can put out a shingle and say they are a tax preparer. There are virtually no standards.

Only Maryland, Oregon, California and New York have rules that establish a minimum level of education, training or competence, the NCLC said. Amelia O’Rourke-Owens, a community and economic development fellow at Reinvestment Partners, noted this irony: “All 50 states regulate hairdressers, but only four regulate tax preparers.”

The test tax returns involved returns prepared for either a single parent or for a graduate student, the NCLC said. Most preparers botched the single parent scenario by not properly accounting for the amount of time spent with the other parent as well as omitting side income that should have been reported.

Of 14 tax preparers given the graduate student scenario, 10 failed to use the right form to record income. And of the four who used the right form, three played fast and loose with deductions.

The groups advocate regulating tax preparers and establishing minimum standards.

Complaints Rising Against Tax Preparers

A KVUE Defenders investigation in Austin, TX has uncovered a rise in complaints submitted to the IRS against tax preparers.The Defenders uncovered tax preparer mistakes can cause an avalanche of IRS fees.

Cynthia Rubin-Whitewolf knows this first hand. In 2013, she went to an Austin H&R Block to prepare her taxes.

A few weeks later, the company called to say it completed her return. She paid $574 for the services, picked up her

the income tax rather than other channels. Some of these benefits, such as the Earned Income Tax Credit and the American Opportunity Credit for education, make cash payments to people who don’t owe income tax.

As the WSJ points out, the US federal income tax system is very progressive – higher income groups pay increasingly higher tax rates, and therefore disproportionately higher and higher shares of the total income taxes collected. A couple key points below based on the two charts above:

1. The top 20% of Americans earn about half of all income (51.3%) and pay almost all income taxes (84%). That top fifth is the only quintile whose tax share exceeds its income share – all bottom four quintiles have a lower tax burden as a share of the total taxes paid than their income as a share of the total. For example, the second highest quintile (with incomes of $79,500 to $134,300) earns 20% of US total income as a group, but shoulders only 13.4% of the total US income tax burden.

2. Both of the bottom two quintiles pay negative income taxes, and are therefore net tax recipients. The 130 million Americans who represent the bottom 40% “get paid by Uncle Sam” as the WSJ says, or more accurately they “get paid by the top 60%” since Uncle Sam has no money of his own, and can only extract taxes from one group and redistribute to another group. That is, Uncle Sam is not reaching into his own pockets to pay the bottom 40%, he’s reaching into your pockets if you make more than $47,000, the threshold income level to be in the top 60%.

3. As the WSJ points out, the top 1% of Americans (about 3.2 million people) earn about 17% of total US income, but pay almost as much in taxes (about 46% of the total) as the 322 million people in the bottom 49% (they pay 54% of taxes while earning 83% of US total income).

Similarly, the top 5% (about 16 million Americans) earn about 29% of total income but pay almost two-thirds (64%).

93% of Tax Returns by Preparers Had Errors, Study Finds

The implications are serious, the group said, given that more than 70 million taxpayers pay tax preparers to do their

7

paperwork and went home.

“He doesn’t say we owe any money. He says they’re done, everything is fine,” said Rubin-Whitewolf.

But, everything wasn’t fine. About six months later, the IRS contacted Rubin-Whitewolf’s to tell her she owed about $3,000 in taxes and late fees totaling an additional $274.94.

A KVUE Defenders investigation has uncovered a rise in complaints submitted to the IRS against tax preparers.

When KVUE called H&R Block, a customer service representative explained, “If you have to pay into the IRS, you will be notified. H&R Block will let you know.”

Rubin-Whitewolf argues that didn’t happen with her, so she filed a complaint with the IRS.

“Extremely frustrating because we had enough money to pay our taxes,” said Rubin-Whitewolf.

According to IRS records reviewed by the Defenders, similar complaints against all types of tax preparers nationwide have grown 39 percent, from 8,035 in 2012 to 11,187 in 2014.

While a tax preparer can lose their license for bad returns, Houston-based IRS spokeswoman Lea Crusberg said consumers are ultimately on the hook for any mistakes.

“Whether you prepare it or someone else prepares it, you are legally responsible for what’s on the tax return, which is why you need to look it over and make sure it’s accurate,” said Crusberg.

Rubin-Whitewolf requested H&R Block refund the late fees for nearly a year. One day after the KVUE Defenders contacted the company on her behalf, she got a call.

Not only did the company pay her IRS late fees, it also refunded the cost to prepare her taxes.“I don’t think the lesson was H&R Block is bad. I think it was just a big mistake happened, and we were very lucky because we were persistent and [KVUE News] helped us,” Rubin-Whitewolf said.

Rubin-Whitewolf admits she should have double-checked H&R Block’s work. Despite her problem, she plans to return to H&R Block this year.

How to prevent tax preparer complaints:

1. Check the BBB for complaints 2. Don’t wait until the last minute to file taxes3. Always double-check returns before submitting it4. If you cannot resolve a complaint, taxpayers can contact the IRS and fill out a complaint form.

Editor’s Note: Oftentimes taxpayers will want to know what to do when someone has prepared a return incorrectly, failed to file electronically when authorized, etc. It never hurts to call the local news - if IRS won’t shut them down, we will.

Prepared in Error

Mystery Shoppers in Florida and North Carolina Uncover Serious Tax Preparer Problems

Advocacy groups in Florida and North Carolina conducted 29 “mystery shopper” tests of paid tax preparers. As with previous studies of paid preparers, test results shows the dire need for regulation of paid tax preparers, and the costs to both taxpayers and the U.S. Treasury due to the lack of minimum standards.

Overview of Testing

8

• Preparers who were unfamiliar with the tax preparation software or common tax forms, or behaved unprofessionally.

Bottom Line: 94-year-old Tax Preparer Still in Top Form

Every year when tax time rolls around clients ask accountant Dawn Mulhern the same question: “Can I call you next year?”

Every year, she gives the same answer: “If I’m perfectly capable and able to do a good job, I’ll do it.”

Her caveat makes sense, considering that Mulhern is a 94-year-old who started filing tax returns for individuals and businesses in 1948. She’s been at it ever since, and recently renewed her Internal Revenue Service registration as a tax preparer.

While afghans, wheelchairs and soft food may come to mind when picturing a nonagenarian, Mulhern is none of that. She’s more Betty White. She’s polished, professional and as sharp as someone one-quarter her age.

“I keep trying to retire, but I have trouble doing it,” she said. “People ask me all the time why I’m still working. I think it’s good for me.”

Mulhern has about 40 clients, down from the 800 she used to juggle in the 1950s and 1960s, when taxes had to be done with paper, a pencil and surefooted knowledge. Most are longtime customers who have become friends.

“I see them once a year and I hear about their families and what’s going on in their lives,” Mulhern said.

Maggie Quinn, a retired saleswoman and part-time sculptor, has used Mulhern as her tax preparer for more than 30 years. “She amazes me every year. She keeps up on all the tax laws, and she’s very good,” Quinn said. “She taught me well - how to keep records properly and what I can do to not get stuck paying more taxes than I have to.”

Mulhern became an accountant by chance, not choice. She earned a business degree from the University of Wisconsin in

Testers used one of two scenarios – the Single Parent and the Graduate Student.Single Parent scenario

The tester in this scenario was not entitled to claim the minor child because the child lived with the other parent for more than 50% of the time.

• 8 of the 15 preparers had the tester claim the child on the tester’s tax return, improperly inflating the tester’s refund and claiming an Earned Income Tax Credit (EITC) of $2,523.

• 7 of these 8 preparers also appear to have knowingly provided incorrect information on an EITC-related form.Preparers also gave the Single Parent testers questionable advice, such as telling the tester she should work out an arrangement with the father to take turns claiming the child in alternate years.

The Single Parent scenario also involved $800 in side income not reported on a W-2.

• 12 of the 15 preparers did not report the $800 in side income.

Graduate Student scenario

The Graduate Student scenario involved a paid internship at a local nonprofit. All of the preparers properly reported the tester’s income. However, preparers did make errors with this scenario.

• 10 of the 14 preparers did not properly use a Schedule C to report the income. This resulted in omitting nearly $1,300 in self-employment income.

• Of the 4 preparers who did use a Schedule C, 3 preparers took questionable deductions, including 1 preparer who made up $9,562 in fictitious businesses expenses.

Overall Observations

In total, there were documented inaccuracies in the vast majority of the tests.

• 27 out of 29 returns prepared for the mystery shopper tests contained an error. Thus, over 90% of the returns were inaccurate.

Other problematic issues observed include:

• Preparers who forged the signatures of other people or otherwise failed to properly note on the tax form that they were the paid preparer who had completed the form.

• The testers were unable to obtain estimates of tax preparation fees in some cases. In one case, the preparer appeared to vary the amount of the fee on the refund amount, which is contrary to IRS rules.

9

Madison, where she was one of 20 women in the 200-student business school.In 1942, fresh out of college, she landed a job with IBM and learned how to key early computers - multiple machines that punch card operators wired individually by job to run payroll or accounts receivable reports.

“We were in training for six months in New York, and it was a fascinating experience,” Mulhern recalled. “The founder, Thomas Watson, was the president of the company. We lived in tents at the IBM homestead in Endicott. They were built on wooded frames, and we had daily maid service.”

Mulhern soon wed law student Bill Mulhern, which cost her the IBM job.

“The company had a policy: Women in my position couldn’t be married,” she said.

Mulhern started helping her husband at his practice near Green Bay, Wis. In the 1940s, there were no tax companies like H&R Block; many people brought their personal and business tax materials to lawyers.

“It’s just the way it was, and with my accounting background, guess who took over most of the tax practice,” Mulhern said.The work was interesting, though, and the husband-and-wife team pioneered a trail that led to changes in the tax laws, she said.

“Bill had a philosophy of finding the best answer for your client, if it was within the law. Just because the IRS interprets the law one way, we might interpret it another,” she said. “We had a number of audits that were very successful.”

Mulhern’s persistence, experience and determination have benefited her clients - and even some who aren’t her regulars. Recently, a friend who wasn’t a client complained that she had to pay $1,800 in taxes last year. Mulhern reviewed her friend’s forms.

“She got the whole $1,800 back. You just have to know what you’re doing,” Mulhern said. “It’s sad to see the number of mistakes in other people’s taxes, and it happens all the time.”Part of Mulhern’s job is calming her clients’ fears.

“Most people go berserk if they get a notice from the IRS,” she said. “I try to talk some sense into them. It’s just an agency. They’re working for us.”

But she thinks the nation’s tax system is broken and isn’t sure if it will ever be fixed.

“Years ago, you could make a call to the IRS and get an answer. Today, you get six answers,” she said. “I think the IRS is very badly run. It’s so huge, and they’ve put too many things into the tax laws.”

Her foremost advice to anyone about taxes is to be honest, and then “be thorough and know what you’re doing.”

Mulhern still drives, and she considers herself lucky to be as fit and active as she is. Her husband died in 1961, and Mulhern kept busy with projects outside her business. She helped form the Suicide Prevention Partnership of the Pikes Peak Region in the 1990s, did free tax returns for AARP members for 18 years and is a wicked bridge player.

So Mulhern has stayed with her tax-preparation work, and that’s a good thing, says her daughter, Susan, a certified public accountant in Denver.

“It’s certainly kept her young and vital,” Susan Mulhern said. “She always told me I could do anything I wanted, and she’s been a good example of that.”

Report Finds Taxes Done By Non-CPA Preparers Riddled with Inaccuracies

Think twice before hiring a tax preparer to file your taxes this year. According to an undercover report by the National Consumer Law Center (NCLC), many unregulated tax preparers are incompetent when it comes to sorting through the complicated IRS paperwork required to file income taxes. What’s worse – tax preparers often knowingly file inaccurate information.

Anticipating such problems, in 2011 the IRS began requiring tax preparers who were not Certified Public Accountants to register and complete tests proving they were capable of filing taxes accurately. As you might expect, tax preparers appealed the case in federal court in 2014, and surprisingly, won the right to continue helping customers prepare their taxes.

The NCLC recently employed secret shoppers to pose as tax filers in 29 test cases in Florida and North Carolina. They found that all but two of the tests resulted in inaccuracies on the tax returns.

Secret shoppers acting as single parents with partial custody of minors were told eight out of fifteen times that they should claim their child as a dependent to earn a $2,523 earned income tax credit, even though this is inaccurate and illegal. It appears that seven of the eight tax preparers were aware that they were illegally misreporting information, and did it anyway. In another test, 12 of 15 tax preparers omitted an $800 side

10

income, even though they were aware of it.In another test, 10 of 14 tax preparers failed to file income from a paid internship on the Schedule C form, resulting in an omission of $1,300.

From the 29 test cases, there were several examples of signature forgery, or of one preparer assisting the customer to fill out the forms, while a different preparer signed them.

“To see this level of errors is extremely disturbing,” according to Chi Chi Wu, a staff attorney at NCLC.

While many of the inaccuracies seemed to help the customer save money or earn a higher tax return, it is important to note that such practices are illegal, and that, should you be audited, it is you, not the tax preparer, who will have to answer to the law.

Tax Complexity Is Expensive for Small Businesses

Taxes are time consuming and expensive for small businesses in the United States.

Nearly a quarter of small business owners in the United States spend over 120 hours each year dealing with their federal taxes, according to the most recent survey by the National Small Business Association. That’s three work weeks spent dealing with federal taxes. Additionally, over half of small business owners spend more than one work week (40 hours) on federal taxes each year, according to the most recent survey by the National Small Business Association.

According to the survey, these taxes come with a heavy cost as well, with over a quarter of businesses spending more than $10,000 each year on simply the administration of federal taxes. This does not include the actual tax burden, which 42 percent of respondents said creates the largest burden on their business.

Small business owners ranked payroll taxes and presenting the largest financial burden, followed by state and local tax compliance, income taxes, property taxes, and capital gains taxes. Nearly 70 percent of small business owners said that federal taxes have a moderate to significant impact on the day to day operations of their businesses.

The survey found that 70 percent of small business owners support tax reform that reduces corporate and individual tax rates and business and individual deductions.

Pass-through businesses make up the vast majority of businesses in the U.S. today (chart below). This makes it crucial that tax reform fix both the individual and the corporate tax system.

Justice Department Asks Federal Court to Permanently Shut Down Liberty Tax Service Franchise Owner

The United States filed a complaint asking a federal court in Detroit to bar a Liberty Tax Service franchise owner and his companies based in Illinois and Michigan from preparing federal tax returns for others, the Justice Department announced.

The civil complaint against Syed N. Ahmed and his businesses, Nasah Inc., Millinium [sic] Financial Solutions Inc., Mars Inc.-Hamtramck, and Mahad Inc., was filed in the U.S. District Court for the Eastern District of Michigan. The complaint alleges that Ahmed operates at least 10 Liberty Tax Service franchise locations.

According to the suit, the defendants improperly obtain inflated tax refunds and refundable credits for customers by preparing tax returns that include, among other things, false or inflated Schedule C (Profit or Loss From Business) income and expenses, bogus dependents, false filing statuses, improper education credits and false itemized deductions.

For example, the complaint alleges that one of defendants’ tax return preparers fabricated a driving business without the customer’s knowledge and reported thousands of dollars of expenses for that business that the customer did not incur. The false expenses enabled the customer to receive an earned income tax credit that she was not otherwise entitled to receive, according to the suit.

The lawsuit states that the defendants prepared more than 17,000 federal income tax returns between 2010 and 2013. Based on audit adjustments the Internal Revenue Service (IRS) has made to tax returns prepared and filed by the defendants between 2010 and 2013, the defendants’ conduct has cost the U.S. Treasury approximately $2.8 million, according to the suit.

Return preparer fraud is one of the IRS’s Dirty Dozen Tax Scams for 2015. The IRS has some tips on its website for choosing a tax preparer, and has launched a free directory of federal tax preparers. In the past decade, the Tax Division has obtained injunctions against hundreds of unscrupulous tax preparers and tax scheme promoters. Information about these cases is available on the Justice Department’s website. An alphabetical listing of persons enjoined from preparing returns and promoting tax schemes can be found on here. If you believe that one of the enjoined persons or businesses may be violating an injunction, please contact the Tax Division with details.

Total H&R Block U.S. assisted returns prepared fell 4.6% through April 16. The company believes this decline is due to the second-year impact of discontinuing the company’s free federal 1040EZ promotion and the ongoing impact of industry-wide fraud, particularly related to behavioral shifts in tax filers who claim the EITC. Tax returns prepared through the company’s tax software products, including online, desktop and mobile applications, increased 8.2%.

“Though our assisted return volume declined, we expect to report revenue growth for the second consecutive year and

11

are on track to achieve our EBITDA margin guidance,” said Cobb. “By focusing on our Tax Plus strategy, we improved client mix in both assisted and digital and continued to provide our clients with the exceptional expertise and client service that they expect from H&R Block.”

The Affordable Care Act (ACA) intersected with tax preparation for the first time in tax season 2015, requiring millions of taxpayers to file additional forms and in many cases resulting in modified refunds and tax penalties.

“This was the first tax season in what we’ve said will be a multi-year journey to fully realize the impacts of the ACA and I believe we are well positioned as the industry’s ACA experts,” said Bill Cobb, H&R Block’s president and chief executive officer. “We invested in our tax professionals to enable them to provide valuable ACA guidance to our clients and I’m proud of how they delivered.”

Additionally, fraud continued to negatively impact the tax industry as tax identity theft and improper EITC payments continue to cost taxpayers billions of dollars.

“The level of fraud we see in this industry is shocking, and we continue to lead the battle against it. While I’m pleased that others in the industry and our government leaders have joined us in this fight, there is still much more that needs to be done,” Cobb said. “We need mandatory standards for paid tax preparers. Without them, consumers will continue to be victimized by people who aren’t sufficiently trained, or worse, knowingly commit fraud. We also need uniform standards for tax returns claiming refundable credits such as the EITC, regardless of the channel through which they are filed. Congress has already provided clear legislative direction on this matter. Now the Treasury Department needs to put this fraud prevention change into effect for the 2016 tax filing season.”

H&R Block to Announce Fiscal 2015 Results on June 8

In conjunction with the announcement of fiscal 2015 results, the company will host a conference call at 4:30 p.m. Eastern time on June 8, 2015 for analysts, institutional investors, and shareholders to discuss fiscal 2015 results, future outlook and a general business update. To access the call, please dial the number below approximately 10 minutes prior to the scheduled starting time:

The Danger Of Overstuffing Your IRA

If you put too much in an Individual Retirement Account, you can expect to hear from the Internal Revenue Service. That’s the bottom line of a new report by the Treasury Inspector General for Tax Administration, “Actions Can Be Taken To Further Improve The Strategy For Addressing Excess Contributions To Individual Retirement Arrangements.”

IRAs are one of the best tax shelters around. With a traditional

IRA, your retirement dollars grow tax-deferred; with a Roth IRA, they grow tax-free. So there are strict rules that limit the amount individuals can contribute to IRAs in a given tax year. Noncompliance means lost revenue for the government.

For 2015, the most you can contribute to all of your traditional and Roth IRAs is the lesser of: $5,500 or $6,500 if you’re age 50 or older by the end of the year; or your taxable compensation for the year. If you put in too much, you get nailed with a 6% penalty that accrues every year until the excess contribution is withdrawn. You can fix an excess contribution by taking the money out up until six months after the April 15th when your return is due for that tax year.

Don’t mess with IRA contribution limits or you’ll have to break your piggy bank to pay a 6% penalty.

In one extreme case pending in district court in Illinois, a couple sold their house in 2007 and put the proceeds–$200,000 each–into their IRAs. After being contacted by the IRS, Michael and Cristina Wu took out the excess contributions (and earnings) in early 2010. They’re stuck with penalties for 2007 and 2008, but they’re arguing that they don’t owe the 2009 penalty because they took out the excess contributions before the 2009 tax year deadline.

How big is this problem? TIGTA found that for fiscal year 2011, 57,484 taxpayers without eligible compensation potentially made $125 million in improper contributions, meaning they owed $7.5 million in excise tax. More than a quarter (29%) of the potential excess contributions were $3,000 or more. The IRS downplays this, saying that it works out to a penalty of only $131 per taxpayer. But consider that the problem repeats itself year after year. And it’s not just that the people getting away with this aren’t paying the penalties. They have thousands of dollars more growing tax-deferred or tax-free for decades. That’s the real loss to the Treasury.

The IRS is already taking steps to address the problem of excess contributions. It developed educational materials for individuals and tax preparers. More significantly, it ran a pilot program issuing “soft notices” to taxpayers who appear to have exceeded contribution limits. Now it says it will cast a wider net to catch taxpayers who have potentially put too much in their IRAs: “As the scale of the notice program is increased, the IRS will use the findings from the analysis of the pilot project results to expand the scope of notice recipients.”

The IRS picked out taxpayers who were too old to be making contributions and those who are too young to be making substantial income (it appears parents are improperly funding IRAs in their children’s names—2,585 of the cases were for kids under 10.) Here’s a chart that shows who the IRS has been targeted with notices in the pilot:

National Center for Professional Education Fellowship

12

TIGTA said that 1 out of 10 of these notices appear to have been sent in error—as the taxpayers corrected the excess contribution in time. So if you get a notice, don’t freak out. If you’re in the wrong, you should file an amended tax return, although technically, you don’t have to: “Although the notice requests that the individual file an amended tax return if appropriate, it is not required. Instead, the notices are designed to serve as an educational tool, encourage self correction, and improve voluntary compliance.”

In most cases, taxpayers are “clueless” and not intentionally trying to game the system, says Joe Cicchinelli, and IRA technical expert at Slott & Co. in Rockville Centre, N.Y.In order to contribute to an IRA, you must have earned income (there’s an exception that says a working spouse can contribute to a non-working spouse’s IRA if they file a joint income tax return). The year you turn 70 ½ you become ineligible to contribute to a traditional IRA (there are no age restrictions to contribute to a Roth IRA, assuming you have earned income).

A common mistake is doing a rollover IRA from one bank or brokerage to another, without first taking out the required minimum distribution amount for the calendar year (you have to start taking distributions the year after you turn 70.5), says Cicchinelli. Any distribution out of an IRA counts as a minimum required distribution and that can’t get rolled over, so you’ve made an excess contribution. If you rolled over $100,000 but should have first taken a $10,000 minimum distribution, then you’ve made a $10,000 excess contribution. “The argument that you don’t need to take out the minimum distribution until Dec. 31 doesn’t cut it,” he adds.

It’s not just taxpayers making mistakes. When analyzing tax year 2011 Forms 5498 for excess contributions, TIGTA determined that approximately 834,000 (7 percent) of 11.9 million Forms 5498 filed by IRA custodians appeared to be inaccurate. The IRS responded that it will launch an education initiative for IRA custodians too.

ETFs and K-1s Tax Reporting

ETFs have become so popular in part because of the tax efficiencies that they offer relative to traditional mutual funds. Due to the nuances of the creation / redemption mechanism, ETFs are generally able to give investors more control over their tax situation–instead of pinning them with capital gains obligations due to the activities of other investors.

Unfortunately, however, the tax treatment of exchange-traded products cannot be summed up simply as being more efficient than mutual funds. There are various complexities across the different product structures that impact the effective tax liabilities that will be incurred on gains. And there are also some nuances that impact how taxes on various ETP positions must be reported that are of major importance to some financial advisors.

As a general rule, gains and losses for a typical ETP are reported on Form 1099, but there are a number of ETPs that are structured as partnerships and as such, will issue a K-1. Exchange traded funds that utilize futures contracts, whether that be commodity, currency, or volatility, or any other product that is structured as a partnership will send out K-1s. As taxes are such an important part of investing, we outline the complete list of ETFs that issue a K-1 for anyone looking to avoid a more complex tax filing, or simply to educate those on who may be unaware of how their investment is treated from a tax perspective,.

What Is a K-1?

13

There is a fair amount of confusion over what exactly a K-1 is and what receiving one of these statements means. A K-1 is a tax document used to report share of profits and losses from interests in limited partnerships. These documents become relevant because many exchange-traded products are technically structured as partnerships, meaning that investors are actually limited partners. Partnerships are typically not required to pay taxes directly, instead passing through those obligations to individual partners. They do that by sending a K-1 to partners each year detailing their interest in the operations of the partnership.

Many investors wish to avoid K-1s primarily because of the inconvenience caused. Schedule K-1 tends to be one of the last documents provided to taxpayers, potentially delaying the timing of their filings. For advisors with hundreds of clients, the administrative burden associated with K-1s can be less-than-optimal. But it should also be noted that receipt of a K-1 generally means a taxable event–even if the related position has not been liquidated. In other words, securities that issue a K-1 may require investors to report and pay taxes on gains annually, even if the security has not been sold.

For some, K-1s are not a significant issue–simply a minor inconvenience. Others try to avoid these schedules at all costs, preferring to use exchange-traded products that can be reported on a Form 1099. Below, we break down the complete list of ETFs that issue a K-1 by their respective asset classes.

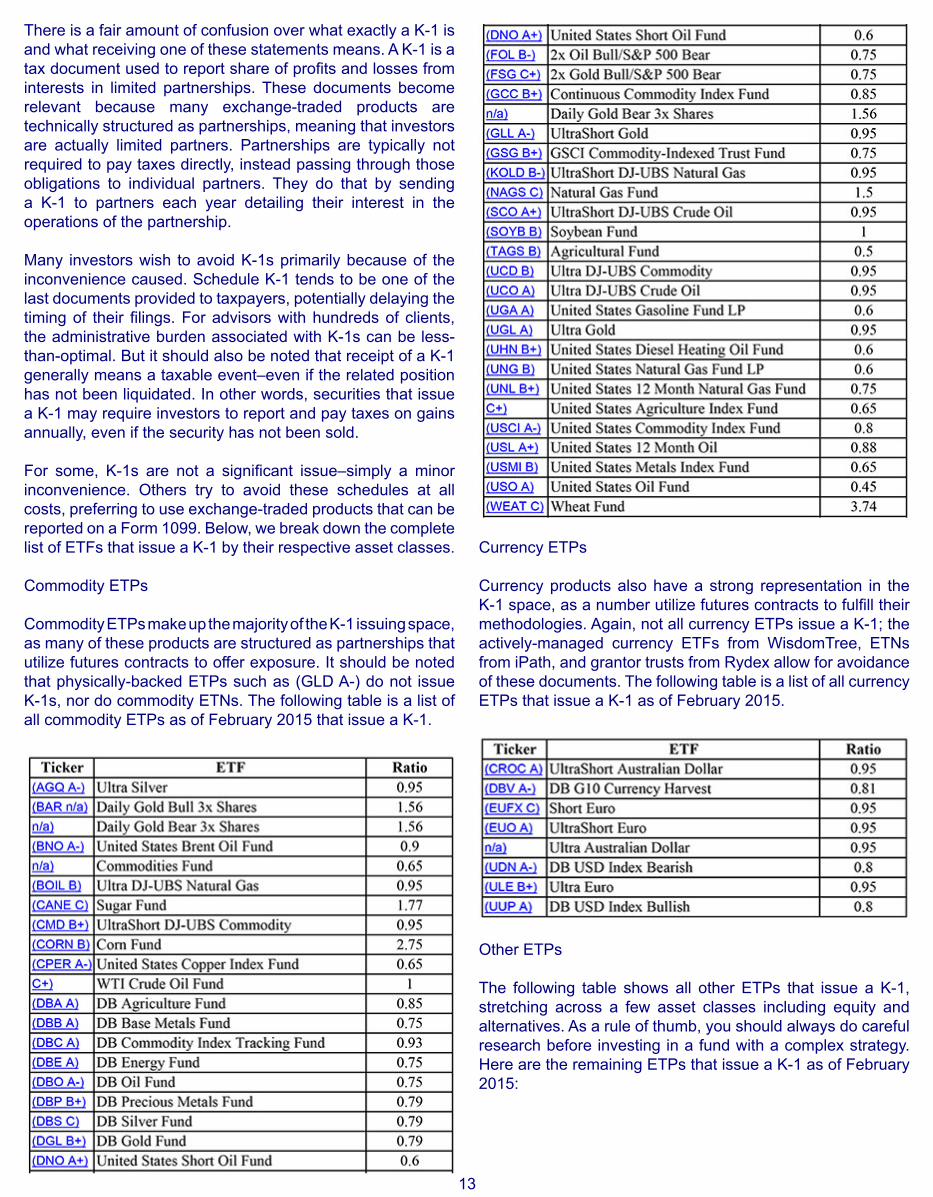

Commodity ETPs

Commodity ETPs make up the majority of the K-1 issuing space, as many of these products are structured as partnerships that utilize futures contracts to offer exposure. It should be noted that physically-backed ETPs such as (GLD A-) do not issue K-1s, nor do commodity ETNs. The following table is a list of all commodity ETPs as of February 2015 that issue a K-1.

Currency ETPs

Currency products also have a strong representation in the K-1 space, as a number utilize futures contracts to fulfill their methodologies. Again, not all currency ETPs issue a K-1; the actively-managed currency ETFs from WisdomTree, ETNs from iPath, and grantor trusts from Rydex allow for avoidance of these documents. The following table is a list of all currency ETPs that issue a K-1 as of February 2015.

Other ETPs

The following table shows all other ETPs that issue a K-1, stretching across a few asset classes including equity and alternatives. As a rule of thumb, you should always do careful research before investing in a fund with a complex strategy. Here are the remaining ETPs that issue a K-1 as of February 2015:

14

Credit and ID Monitoring Won’t Protect you From Tax Cheats

Georgia is proof that when it comes to tax fraud, no one is safe.

“Criminals in general tend to trap over all industries,” said Mark Green, an IRS spokesman

For example, 1,200 jail and prison inmates nationwide had their social security numbers compromised when Bradford Thomas of Cobb County filed $5 million in fraudulent tax returns.

15,000 people in Clayton and surrounding counties were compromised when fake applications for stimulus payments were nothing more than a scam. The Clayton County duo of Kevin Sonnier and Bernardo Davis filed more than $15 million in fraudulent tax returns.

“The bottom line is that they’re after your social security number,” said Green.

Protecting your tax identity isn’t as easy. Victims have learned the hard way that credit monitoring only protects against fraudulent bank accounts and lines of credit, not income tax fraud.

“That’s supposed to be to protect me, but it didn’t,” complained Stevie Williams, who had her tax return compromised.

“I had a fraud alert on my social and that still did not help. They were still able to file taxes in my name,” said Princess Poyntz, a detective with the DeKalb County Police Department.

Whether you hand over your SSN to a tax cheat yourself or they get it like a metro Atlanta trio did, stealing names, date of births, and social security numbers from medical records, you have to be cautious. 1,900 people thought their information was safe with their tax preparer until Shannon Bradley broke into and filed $1 million in fraudulent returns. Georgia’s high rate of fraud is why the IRS is using the identity protection pin program here first.

“That number not only will it add an extra layer or protection, but will give you comfort knowing scam artists cannot use your social security number to file a bogus return,” said Green.

It’s these safeguards like the identity protection PIN and other

filters that have meant longer lines at the IRS office. This year more taxpayers received a 5071c letter requesting they verify their identity either in person, on the phone, or online.

Tax cheats could even target a past refund - more than 36,000 Georgians still haven’t filed a tax return for 2011. The deadline to file is no later than April 15th, 2015.

Experian recommends the following information to keep in mind when you submit your taxes this year:

Tax filers should keep the following actions in mind when submitting taxes this year:

Do:

• Research any paid preparer or tax-preparation software. While plenty of free help can be found online, scammers also are out there setting up fake websites and software downloads solely designed to bilk people out of their personal information during tax time.

• File online using a computer that is protected with up-to-date antivirus and antimalware software, a firewall and password.

• Keep important tax documents in a locked, secure location.

• Ask potential tax preparers to explain how they protect their customers’ information.

• Enroll in identity protection and take action if alerts indicate potentially fraudulent activity.

Don’t:

• Respond to any email, text message or phone call from someone who says they’re with the IRS. The IRS says it never contacts taxpayers through those methods.

• Let letters linger in your mailbox. During January, important tax documents will arrive via the mail. Thieves know this and have been known to pluck data-rich forms from victims’ mailboxes during tax season.

• File taxes over public Wi-Fi networks. Stick with a secure network connection for all online activity.

Tax Cheaters Buy Used Non-Winning Lottery Tickets to Offset Winnings

Crooked lottery winners who want to evade paying taxes on their winnings can buy or rent truckloads of used lottery tickets and show them to IRS auditors as “proof” that their gambling losses exceeding their winnings.

15

Above: eBay sale for “30 bags of $1000 LOSING 2014 NY scratch off lottery tickets. buy what u need”

Attacking Taxes: Preparers Say Identity Theft, Health Care Top Questions

Tania Turner, with Accounting Services of York LLC, works on a client’s taxes in the Springettsbury Township firm. Tax preparers say identity theft, refund delays and confusion about the Affordable Health Care act are among the top issues they’ve have noticed this year.

Tips for filing

• Don’t procrastinate: the IRS advises not to wait until the last minute to file. Waiting may lead to overlooking possible savings and could make your tax return more prone to errors.•File on time: If you owe taxes but you can’t afford to pay, you should still file before April 15 and try to pay as much as you can. This will minimize penalties and interest charges.

•Ask for help: H&R Block suggests seeking professional help with filing your taxes. Doing them yourself may save you money immediately, but you may miss out on possible

deductions and credits because of the changing tax code.

•File an extension: If your tax return is not done by April 15, you can get a six month extension to file, but you should pay any tax due by the deadline.In addition to the usual onslaught of last-minute tax filers who will swarm their offices in the coming days, many tax preparers say identity theft, refund delays and confusion about the Affordable Health Care act are among the top issues they’ve have noticed this year.

Here’s a look at the big issues confronting taxpayers:

Identity Theft

If you filed your taxes early and are still waiting to cash in on your tax return, months after filing, you’re not alone. Tax preparers have noticed some of their customers are having to prove their identities to the IRS before getting their much-anticipated tax return.

“We have people that are waiting nine or 10 weeks to get their money,” said Tammy Curran, a tax preparer with Liberty Tax Service.

Curran said the IRS is cracking down on identity theft and is selecting one of every seven tax filings to “grub by hand.”

The IRS has said it is increasing its efforts to prevent identity theft and has stopped 19 million suspicious returns from 2011 to 2014, resulting in over $63 billion in protected refunds.

Curran said she has noticed Hispanics, in particular, are victims of refund fraud.

“When people come over from Mexico, their ID and social [security cards] are photocopied and sold,” she said.

She said her clients have to go to the IRS office and confirm their identities, but as a result of recent IRS layoffs, this process is taking longer than usual.

“People are having to wait three days to talk to anybody down there,” she said.

The Affordable Health Care Act

While the Affordable Health Care has been around since 2010, the 2014 fiscal year is the first year uninsured taxpayers will have to pay penalties.

David Riggs, president of York Accounting Services, said the penalty for not having health insurance for 2014 is not always $95, contrary to what some people believe.

“We’ve seen some shocked faces,” he said. “They don’t hear about the 1 per cent.”

If you weren’t insured last year, you’ll have to pay either 1 per cent of your yearly household income if it’s higher than

16

$10.150, or $95 per person in the household ($47.50 per child under 18), whichever is higher, according to HealthCare.gov. The maximum penalty per family paying this fee is $285.

For example, Riggs said, if your income is over $50,000, that’s a $500 fine.

The penalties will continue to increase in the following years. Next year, the penalties will be 2 per cent of the household’s income or $325 per person for the year. A family of four with a $60,000 income would pay almost $1,000 for not having coverage in 2015.

Tax preparer Michael Hanscom said some people had no idea the government wants them to have health insurance.

“I had people ask me, ‘Why are you asking me if I have health insurance,’” he said, adding that some people may qualify for a hardship exemption, which exempts people with unusual life circumstances from paying the fee.

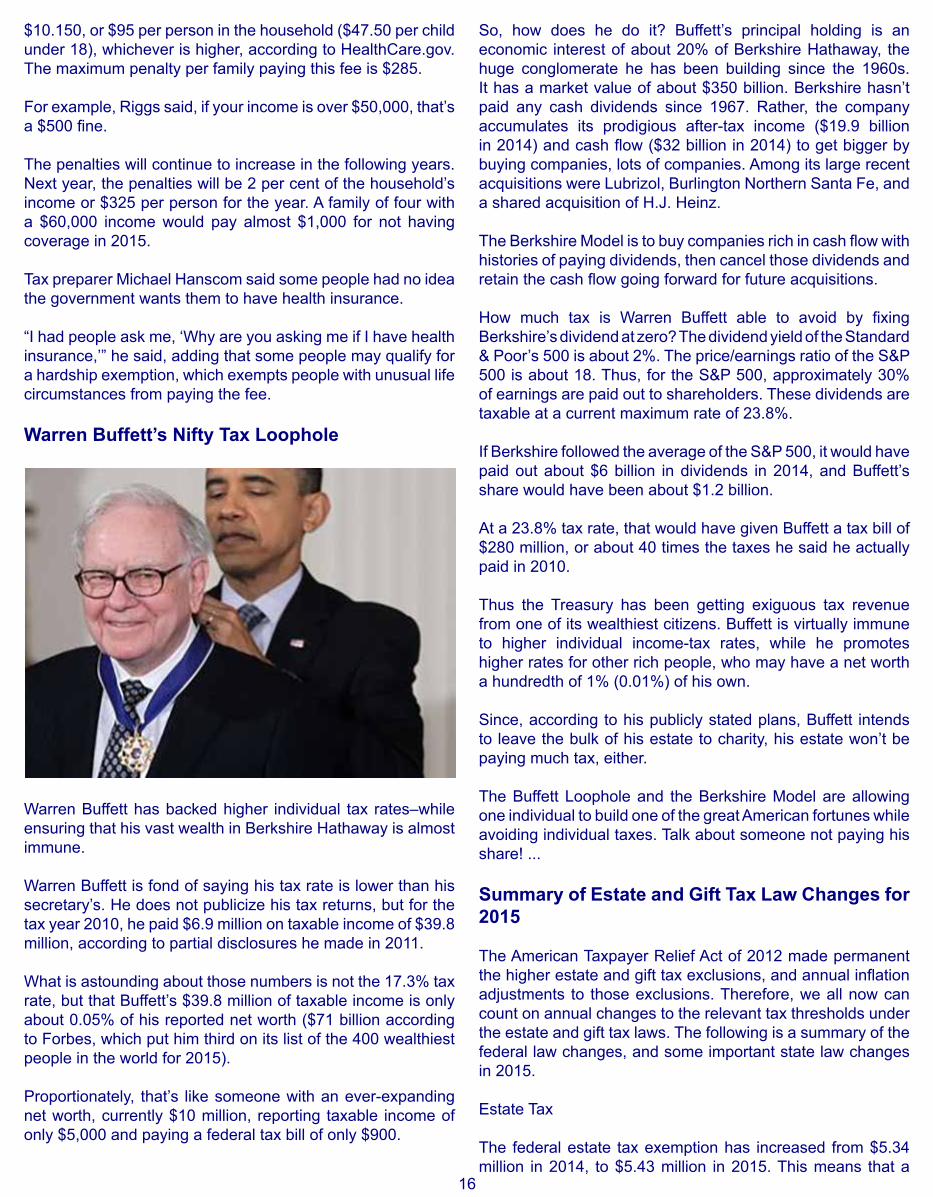

Warren Buffett’s Nifty Tax Loophole

Warren Buffett has backed higher individual tax rates–while ensuring that his vast wealth in Berkshire Hathaway is almost immune.

Warren Buffett is fond of saying his tax rate is lower than his secretary’s. He does not publicize his tax returns, but for the tax year 2010, he paid $6.9 million on taxable income of $39.8 million, according to partial disclosures he made in 2011.

What is astounding about those numbers is not the 17.3% tax rate, but that Buffett’s $39.8 million of taxable income is only about 0.05% of his reported net worth ($71 billion according to Forbes, which put him third on its list of the 400 wealthiest people in the world for 2015).

Proportionately, that’s like someone with an ever-expanding net worth, currently $10 million, reporting taxable income of only $5,000 and paying a federal tax bill of only $900.

So, how does he do it? Buffett’s principal holding is an economic interest of about 20% of Berkshire Hathaway, the huge conglomerate he has been building since the 1960s. It has a market value of about $350 billion. Berkshire hasn’t paid any cash dividends since 1967. Rather, the company accumulates its prodigious after-tax income ($19.9 billion in 2014) and cash flow ($32 billion in 2014) to get bigger by buying companies, lots of companies. Among its large recent acquisitions were Lubrizol, Burlington Northern Santa Fe, and a shared acquisition of H.J. Heinz.

The Berkshire Model is to buy companies rich in cash flow with histories of paying dividends, then cancel those dividends and retain the cash flow going forward for future acquisitions.

How much tax is Warren Buffett able to avoid by fixing Berkshire’s dividend at zero? The dividend yield of the Standard & Poor’s 500 is about 2%. The price/earnings ratio of the S&P 500 is about 18. Thus, for the S&P 500, approximately 30% of earnings are paid out to shareholders. These dividends are taxable at a current maximum rate of 23.8%.

If Berkshire followed the average of the S&P 500, it would have paid out about $6 billion in dividends in 2014, and Buffett’s share would have been about $1.2 billion.

At a 23.8% tax rate, that would have given Buffett a tax bill of $280 million, or about 40 times the taxes he said he actually paid in 2010.

Thus the Treasury has been getting exiguous tax revenue from one of its wealthiest citizens. Buffett is virtually immune to higher individual income-tax rates, while he promotes higher rates for other rich people, who may have a net worth a hundredth of 1% (0.01%) of his own.

Since, according to his publicly stated plans, Buffett intends to leave the bulk of his estate to charity, his estate won’t be paying much tax, either.

The Buffett Loophole and the Berkshire Model are allowing one individual to build one of the great American fortunes while avoiding individual taxes. Talk about someone not paying his share! ...

Summary of Estate and Gift Tax Law Changes for 2015

The American Taxpayer Relief Act of 2012 made permanent the higher estate and gift tax exclusions, and annual inflation adjustments to those exclusions. Therefore, we all now can count on annual changes to the relevant tax thresholds under the estate and gift tax laws. The following is a summary of the federal law changes, and some important state law changes in 2015.

Estate Tax

The federal estate tax exemption has increased from $5.34 million in 2014, to $5.43 million in 2015. This means that a

17

married couple may shield up to $10.86 million from federal estate tax during their lifetimes and at death. The maximum estate tax rate continues to be 40%.

In addition, there have been changes in state estate tax laws for 2015. New York passed legislation in 2014 that will increase the exemption each year until it equals the federal exemption in 2019. On April 1, 2015, the exemption will increase to $3.125 million. However, estates that exceed 105% of the exemption amount will not receive the benefit of the exemption. As a result, estates greater than $3,281,250 will not receive the benefit of the exemption in 2015. The maximum estate tax rate (for estates exceeding $10 million) remains at 16%. Further, New York previously did not have a gift tax, but under the new law, gifts made within three years of death will be included in the decedent’s taxable estate. Gifts are only included if the decedent made them between April 1, 2014 and January 1, 2019 while he or she was a resident of New York. The new law, however, does eliminate New York’s generation-skipping transfer tax, which was previously assessed at the rate of 16%.

In Hawaii, the exemption has increased to $5.43 million (the same as the federal estate tax exemption). In Illinois, the exemption continues to be $4 million. California, Georgia, and Florida continue to have no state estate tax in 2015.

Gift Tax

The federal gift tax exemption has also increased from $5.34 million to $5.43 million. Thus, a married couple may make lifetime gifts having a value of $10.86 million without incurring any federal gift tax. The maximum gift tax rate is still 40%.

The federal gift tax annual exclusion amount for 2015 continues to be $14,000. This means that a married couple may make gifts in 2015 having a value of up to $28,000 per recipient without incurring any federal gift tax. The federal gift tax annual exclusion also is indexed to inflation but in $1,000 minimum increments. This usually means there are several years between adjustments.

The federal estate and gift taxes continue to be unified and have the same exemption amounts and tax rates. This means that at death, the estate tax exclusion is effectively reduced by any exclusion previously used to make lifetime gifts.

Generation-Skipping Transfer (GST) Tax

The federal GST tax is a tax assessed on transfers during lifetime or at death to or for the benefit of grandchildren or more remote descendants. This tax is in addition to any gift or estate tax that may apply.

The GST exemption has also increased from $5.34 million to $5.43 million, which means that a married couple may shield up to $10.86 million from GST tax during their lifetimes and at death. The maximum GST tax rate continues to be 40%.

Tax on Net Investment Income

A 3.8% net investment income tax continues to be imposed on the unearned income of individuals, estates, and trusts that have income above $250,000 (for married couples filing jointly), $200,000 (for single taxpayers), and, for 2015, $12,300 (for estates and trusts). Unearned income includes income from interest, dividends, non-qualified annuities, royalties, rents, capital gains, and other passive income.

Conclusion

Federal and state estate and gift tax laws currently seem to be relatively stable as compared to 2010 and years prior. However, as Congress and many states look for tax law changes to raise revenue, care should be taken to understand the current status of these laws and to monitor for potential changes.

Washington Developments

ABA Weighs In On Proposals to Require Use of Accrual Method By Personal Service Corporations

In a letter sent to key lawmakers, the American Bar Association (ABA) has set out its objections to a tax reform proposal that would impose the accrual accounting method on law firms and other personal service businesses. The ABA stated that forcing these taxpayers to use the accrual method would, among other things, create unnecessary complexity, increase compliance costs, increase taxes on affected taxpayers, and adversely affect clients.

Under the cash method of accounting, gross income includes cash or property actually or constructively received during the tax year. Deductions are usually taken in the year cash or property is actually paid or transferred. It doesn’t matter when the income was earned or when the expense was incurred.

Under the accrual method, income is reported in the tax year in which the right to income becomes fixed and the amount of the income can be determined with reasonable accuracy. Deductions are claimed in the period in which all events have occurred that determine the fact of the liability and the amount of the liability can be determined with reasonable accuracy. ( Code Sec. 446(c) )

The accrual method is mandatory for purchases and sales (unless IRS consents to a change) where inventories must be used. ( Reg. § 1.446-1(c)(2)(i) ) Inventories must generally be used where the production, purchase, or sale of merchandise is an income-producing factor. ( Reg. § 1.446-1(a)(4)(i) )

However, there are exceptions that apply for small businesses, as follows: taxpayers (other than tax shelters) with 3-year average annual gross receipts of $1 million or less do not have to account for inventories or use an accrual method of accounting; and qualifying small businesses with 3-year

18

average annual receipts of more than $1 million but not more than $10 million that are not prohibited from using the cash method and otherwise would have to keep inventories and use accrual accounting may, instead, use the cash method for an eligible trade or business. Qualifying small businesses that may use the cash method for all of their trades or businesses are (1) businesses whose principal business activity for the immediately preceding tax year is other than mining, manufacturing, wholesale trade, retail trade, or information industries; (2) service providers, including those providing property incident to those services; and (3) fabricators or modifiers of certain tangible personal property.

The cash method generally may not be used by C corporations, partnerships that have a C corporation as a partner, or tax shelters. ( Code Sec. 448(a) ) This rule doesn’t apply to farming businesses, qualified personal service corporations (defined in Code Sec. 448(d)(2) , including many law and accounting firms), or entities with annual gross receipts of $5 million or less. ( Code Sec. 448(b) )

In November of 2013, Senate Finance Committee Chairman Max Baucus (D-MT) released a discussion draft containing a number of tax proposals, including the reformation of certain tax accounting rules.

According to a summary of the proposals, businesses “must navigate a maze of tax accounting rules to determine their taxable income,” and “[s]imilarly situated businesses are often subject to substantially different tax accounting rules.”

The goals of the tax accounting proposals in the discussion draft are to simplify tax accounting rules so as to lessen compliance and enforcement costs, and improve tax neutrality by “eliminating the use of certain accounting methods that allow taxpayers in some industries to significantly defer or otherwise distort income measurement.”

To that end, the proposals in the discussion would:

. . . allow all businesses (other than tax shelters) with 3-year average annual gross receipts of $10 million or less to (i) elect to adopt either the cash method or accrual method of accounting, regardless of whether inventory is a material income producing factor in the business; and (ii) immediately deduct the cost of inventory, even if it is a material income producing factor in the business if the cash method of accounting is adopted;

. . . require business that do not satisfy the above gross receipts threshold, including those engaged in farming and personal service businesses, to adopt the accrual method of accounting.

ABA’s position. In a letter sent to Congressional leaders and Mark Mazar, Assistant Secretary of the Treasury for Tax Policy, William C. Hubbard, ABA President, stated that the ABA “unequivocally oppose[s]” proposals to require personal service businesses (namely, law firms) with annual gross receipts over $10 million to switch from the cash method to the

“more complex and costly” accrual method. (The ABA letter focuses its criticism on the proposals in the discussion draft, above, but makes clear that it opposed all similar proposals.) The letter emphasizes that the ABA is generally in favor of tax reform and applauds efforts to simplify the Code, but strongly disagrees with this proposal and urges its removal from any new tax reform legislation.

The letter states that the mandatory accrual accounting proposal would significantly complicate tax compliance for many small business taxpayers. Sole proprietors and personal service corporations tend to favor the cash method because of its simplicity and because it correlates with how they operate their business. In particular, for law firms, imposing the accrual method would force them to calculate and pay taxes on multiple types of accrued income, including work in progress and other unbilled work, accounts receivable (i.e., where the work has been done and billed but not yet paid for), and accounts paid (where the work has been done, billed, and paid for). This, in turn, would require much more detailed work and billing records and, likely, additional accounting and support staff-raising compliance costs and also increasing the risk of noncompliance.

Enacting the proposal would also lead to economic distortions that would adversely affect the businesses that currently use the cash method and those that retain them-such as law firms and their clients. Namely, it would require the businesses to pay taxes on income that they have not and may never receive (“phantom income”). It would also force some firms to borrow funds in order to pay accelerated tax obligations. This would be especially burdensome for the legal profession because many lawyers aren’t paid by clients until long after the work is completed, according to the letter.

The ABA further reasons that mandatory accrual accounting would adversely affect clients since the firm would have to collect its fees much sooner than it currently does. Accident victims, start-up companies, and other clients who require an alternative or flexible fee basis would be especially affected, and many firms would have to reduce the amount of pro bono legal services that they currently provide.

The proposal would also constitute a “major, unjustified tax increase on small businesses.” According to the Joint Committee on Taxation, a comparable proposal would generate $23.6 billion in new taxes over 10 years-by forcing small businesses to pay taxes on phantom income up to a year or more before it is actually (if ever) received. It would also discourage professional service providers from joining with other providers to create or expand a firm and thus discourage the growth of small businesses.

Use Resources and Toolsfor Tax Professionals

On Our WebsitencpeFellowship.com

19

Practice Management

Apply the Four-year Rule When Throwing Away Old {payroll Records

The Spring, 2015 issue of the SSA/IRS Reporter, a joint publication of the Social Security Administration and IRS, offers some valuable pointers for employers to follow in cleaning up their old payroll files. In most (but not all) cases, that means following a four-year retention rule. The Reporter cautions that failure to meet record retention requirements can result in sizable penalties and large settlement awards for employers unable to provide the required information when requested by IRS or in an employment-related lawsuit.

Records relating to income, Social Security, and Medicare taxes. The record retention rule for these taxes is set forth in Reg. § 31.6001-1(e) . As applied to employers that withhold and pay federal income, Social Security, and Medicare taxes, the SSA/IRS Report says records relating to such taxes must be kept for at least four years after the due date of the employee’s personal income tax return (generally, April 15) for the year in which the payment was made.

According to the SSA/IRS Reporter, these records include:

• the Employer Identification Number (EIN);

• the employee’s name, address, occupation, and social security number;

• the total amount and date of each payment of compensation and amounts withheld for taxes or otherwise, including reported tips and the fair market value of non-cash payments;

• the amount of compensation subject to withholding for federal income, social security, and Medicare taxes, and the corresponding amount withheld for each tax (and the date withheld if withholding occurred on a different day than the payment date);

• the pay period covered by each payment of compensation;

• where applicable, the reason(s) why total compensation and taxable amount for each tax rate are different;

• the employee’s Form W-4, Employee’s Withholding Allowance Certificate;

• each employee’s beginning and ending dates of employment;

• any statements provided by the employee reporting tips received;

• fringe benefits provided to employees and any required

substantiation;• adjustments or settlements of taxes; and

• amounts and dates of tax deposits.

Employers should also follow the four-year retention rule for records relating to wage continuation payments made to employees by an employer or third party under an accident or health plan. Such records should include the beginning and ending dates of the period of absence, and the amount and weekly rate of each payment (including payments made by third parties). Employers also should keep copies of the employee’s Form W-4S, Request for Federal Income Tax Withholding From Sick Pay, and, where applicable, copies of Form 8922, Third-Party Sick Pay Recap.

A different rule applies for records substantiating any information returns and employer statements to employees regarding tip allocations. Under Code Sec. 31.6053-1(l), these records must be kept for at least three years after the due date of the return or statement to which they relate.

Claims for refund of withheld tax. The SSA/IRS Reporter says employers that file a claim for refund, credit, or abatement of withheld income and employment taxes must retain records related to the claim for at least four years after the filing date of the claim.

Fringe benefit records. Code Sec. 6039D(b) provides an explicit recordkeeping requirement for employers with enumerated fringe benefit plans, such as health insurance, cafeteria, educational assistance, adoption assistance, or dependent care assistance plan. They are required to keep whatever records are needed to determine whether the plan meets the requirements for excluding the benefit amounts from income.

Unemployment tax records. The Federal Unemployment Tax Act (FUTA) requires employers to retain records relating to compensation earned and unemployment contributions made. Under the “records in general rule” in Reg. § 31.6001-1(e) , such records must be retained for four years after the due date of the Form 940, Employer’s Annual Federal Unemployment (FUTA) Tax Return, or the date the required FUTA tax was paid, whichever is later.

Records should be retained substantiating:

. . . the total amount of employee compensation paid during the calendar year;

. . . the amount of compensation subject to FUTA tax;

. . . state unemployment contributions made, with separate totals for amounts paid by the employer and amounts withheld from employees’ wages (currently, Alaska, New Jersey, and Pennsylvania require employee contributions);

. . . all information shown on Form 940 (with Schedule

20

A and/or R as applicable); and . . . if applicable, the reason why total compensation and the taxable amounts are different.

The SSA/IRS Reporter reminds employers that record retention requirements are also set by the federal Department of Labor (DOL) and state wage-hour and unemployment insurance agencies.

Legislative Update From Capitol Hill

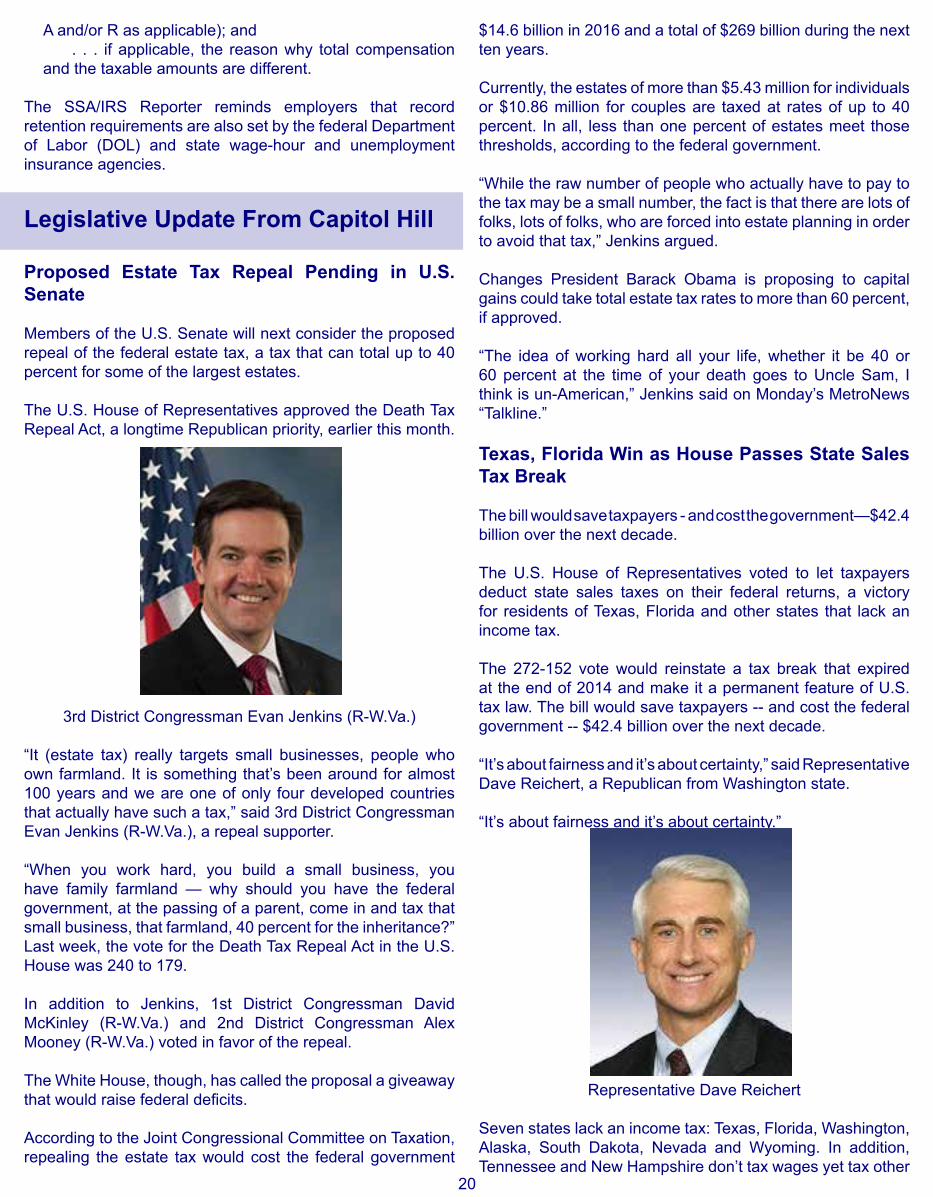

Proposed Estate Tax Repeal Pending in U.S. Senate

Members of the U.S. Senate will next consider the proposed repeal of the federal estate tax, a tax that can total up to 40 percent for some of the largest estates.

The U.S. House of Representatives approved the Death Tax Repeal Act, a longtime Republican priority, earlier this month.

3rd District Congressman Evan Jenkins (R-W.Va.)

“It (estate tax) really targets small businesses, people who own farmland. It is something that’s been around for almost 100 years and we are one of only four developed countries that actually have such a tax,” said 3rd District Congressman Evan Jenkins (R-W.Va.), a repeal supporter.

“When you work hard, you build a small business, you have family farmland — why should you have the federal government, at the passing of a parent, come in and tax that small business, that farmland, 40 percent for the inheritance?”Last week, the vote for the Death Tax Repeal Act in the U.S. House was 240 to 179.

In addition to Jenkins, 1st District Congressman David McKinley (R-W.Va.) and 2nd District Congressman Alex Mooney (R-W.Va.) voted in favor of the repeal.

The White House, though, has called the proposal a giveaway that would raise federal deficits.

According to the Joint Congressional Committee on Taxation, repealing the estate tax would cost the federal government

$14.6 billion in 2016 and a total of $269 billion during the next ten years.

Currently, the estates of more than $5.43 million for individuals or $10.86 million for couples are taxed at rates of up to 40 percent. In all, less than one percent of estates meet those thresholds, according to the federal government.

“While the raw number of people who actually have to pay to the tax may be a small number, the fact is that there are lots of folks, lots of folks, who are forced into estate planning in order to avoid that tax,” Jenkins argued.

Changes President Barack Obama is proposing to capital gains could take total estate tax rates to more than 60 percent, if approved.

“The idea of working hard all your life, whether it be 40 or 60 percent at the time of your death goes to Uncle Sam, I think is un-American,” Jenkins said on Monday’s MetroNews “Talkline.”

Texas, Florida Win as House Passes State Sales Tax Break

The bill would save taxpayers - and cost the government—$42.4 billion over the next decade. The U.S. House of Representatives voted to let taxpayers deduct state sales taxes on their federal returns, a victory for residents of Texas, Florida and other states that lack an income tax.

The 272-152 vote would reinstate a tax break that expired at the end of 2014 and make it a permanent feature of U.S. tax law. The bill would save taxpayers -- and cost the federal government -- $42.4 billion over the next decade.

“It’s about fairness and it’s about certainty,” said Representative Dave Reichert, a Republican from Washington state.

“It’s about fairness and it’s about certainty.”

Representative Dave Reichert

Seven states lack an income tax: Texas, Florida, Washington, Alaska, South Dakota, Nevada and Wyoming. In addition, Tennessee and New Hampshire don’t tax wages yet tax other

21

types of income, such as interest and dividends.

Residents of Washington, Texas and Florida use the sales-tax deduction at a rate more than twice the national average, according to data from the Pew Charitable Trusts.