Embed Size (px)

Citation preview

Pease International Tradeport • 273 Corporate Drive • Portsmouth, NH 03801 • www.primebuchholz.com • 603.433.1143

May 31, 2012

MONTHLY MARKET REVIEW

Europe’s fragile economic and political condition re-emerged as a

defining issue for investors on several fronts as the optimism

surrounding the European Central Bank’s (ECB’s) long-term refinancing

operation (LTRO) abated. The uncertainty emanating from Europe once

again contributed to a sharp sell-off in risk assets across the globe; the

S&P 500 Index posted its worst monthly loss since September 2011; and

non-U.S. equities, emerging markets equities, commodities, and natural

resources stocks all posted notable declines while long Treasuries posted

strong gains. May served as a strong reminder of the importance of

building a portfolio that contains ample exposure to hedges to help

provide balance for the growth engine of the portfolio.

Within Europe, political resistance to the Franco-German austerity

model has spread from the periphery to core countries like France and

the Netherlands, causing investors to question the direction and

likelihood of success for the policy initiatives being enacted in the region.

Problems intensified among the PIIGS countries, particularly in Greece

and Spain. Inconclusive Greek election results on May 6th and anti-

bailout parties prevented a coalition government from being formed and

postponed possible resolution until elections are held on June 17th.

Pessimism rose regarding Greece’s future in the common currency block,

which would have significant ramifications for the global economy and

financial markets. As the events in Greece unfolded, investors also

became increasingly concerned with Spain, which continued to be

plagued by high unemployment and a troubled banking system where a

debt-fueled property bubble has left many Spanish banks undercapitalized.

The government recently took control of Bankia—the country’s fourth

largest lender—despite announcing the nation will miss deficit reduction

targets. In addition to supporting its banking system and its independent

regions, the country faces higher borrowing costs at a time when it needs

to rollover 45% of its normal government debt issuance during the

remainder of the year. Another factor driving market apprehension in

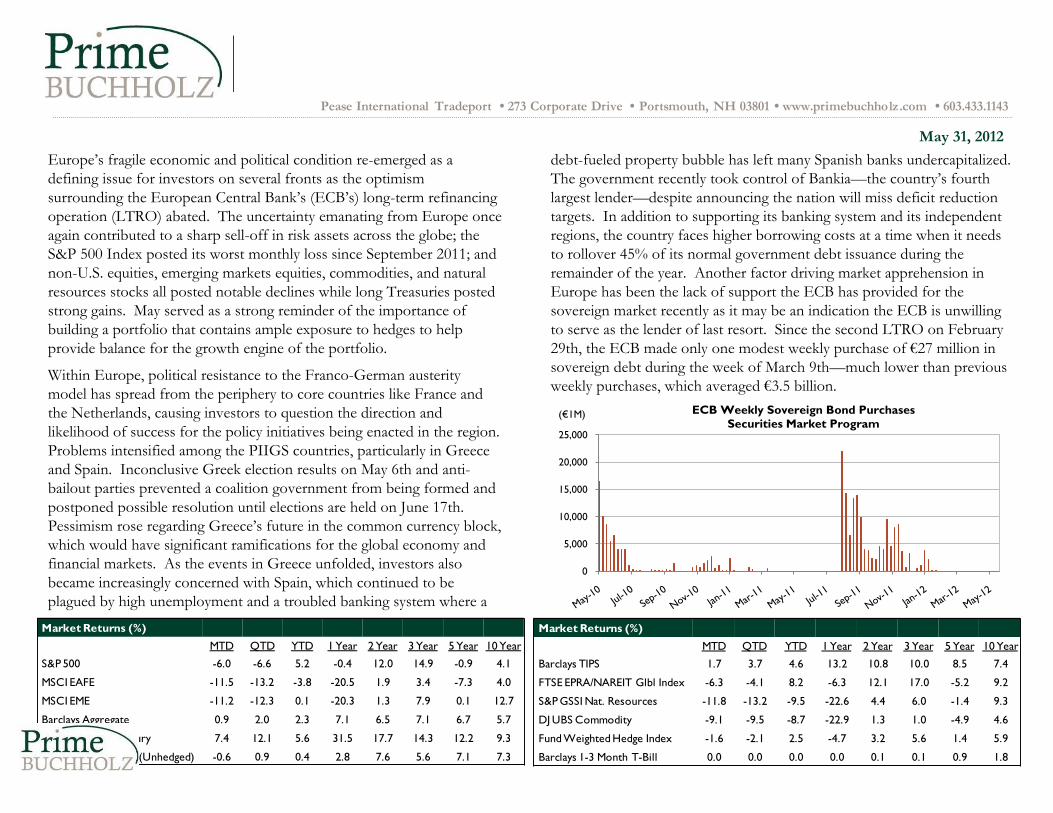

Europe has been the lack of support the ECB has provided for the

sovereign market recently as it may be an indication the ECB is unwilling

to serve as the lender of last resort. Since the second LTRO on February

29th, the ECB made only one modest weekly purchase of €27 million in

sovereign debt during the week of March 9th—much lower than previous

weekly purchases, which averaged €3.5 billion.

0

5,000

10,000

15,000

20,000

25,000

ECB Weekly Sovereign Bond Purchases

Securities Market Program(€1M)

Market Returns (%)

MTD QTD YTD 1 Year 2 Year 3 Year 5 Year 10 Year

S&P 500 -6.0 -6.6 5.2 -0.4 12.0 14.9 -0.9 4.1

MSCI EAFE -11.5 -13.2 -3.8 -20.5 1.9 3.4 -7.3 4.0

MSCI EME -11.2 -12.3 0.1 -20.3 1.3 7.9 0.1 12.7

Barclays Aggregate 0.9 2.0 2.3 7.1 6.5 7.1 6.7 5.7

Barclays Long Treasury 7.4 12.1 5.6 31.5 17.7 14.3 12.2 9.3

Barclays Global TSY (Unhedged) -0.6 0.9 0.4 2.8 7.6 5.6 7.1 7.3

Market Returns (%)

MTD QTD YTD 1 Year 2 Year 3 Year 5 Year 10 Year

Barclays TIPS 1.7 3.7 4.6 13.2 10.8 10.0 8.5 7.4

FTSE EPRA/NAREIT Glbl Index -6.3 -4.1 8.2 -6.3 12.1 17.0 -5.2 9.2

S&P GSSI Nat. Resources -11.8 -13.2 -9.5 -22.6 4.4 6.0 -1.4 9.3

DJ UBS Commodity -9.1 -9.5 -8.7 -22.9 1.3 1.0 -4.9 4.6

Fund Weighted Hedge Index -1.6 -2.1 2.5 -4.7 3.2 5.6 1.4 5.9

Barclays 1-3 Month T-Bill 0.0 0.0 0.0 0.0 0.1 0.1 0.9 1.8

MONTHLY MARKET REVIEW – May 31, 2012

As hope for progress in Europe evaporated, investors sought relative

safety, driving capital to the U.S. dollar (USD) and the Japanese yen.

During the month, the USD rose sharply relative to most other

currencies, serving as a headwind for U.S.-based investors allocated

abroad. Eastern European countries were among the worst-performing

currencies relative to the USD during the month, with the Hungarian

forint, Polish zloty, and the Czech Republic koruna posting noteworthy

losses. This dynamic was partially driven by the potential economic

contagion from contraction in the broader European region. Elsewhere,

signs of slowing growth in China led to heightened fears regarding the

path of global growth and put downward pressure on commodity prices.

In this environment, the currencies of several commodity-driven

economies did poorly within both emerging markets (Russia and South

Africa) and the developed world (Australia and New Zealand). Near

month-end, Bloomberg reported that many emerging markets countries

recently took intervention measures to stem currency losses, including

Brazil, South Korea, India, Russia, and Indonesia. In the case of Brazil,

this action to halt currency depreciation stands in stark contrast to

measures taken in 2010/2011 to stem appreciation of the real. In early

October 2010, the Brazilian government raised the IOF tax (tax on

financial transactions) on foreign bond purchasers from 2% to 4%, and

then subsequently raised it to 6%. As recently as April 2012, the

government had also extended the maturities covered under the IOF tax

and the central bank cut the Selic Rate to 8.5% on May 30th,

representing its lowest rate on record in the Bloomberg database.

Long U.S. Treasuries (+7.4%) continued to serve as the asset of choice

during periods of market stress, despite yields at or near historical lows

along much of the curve. However, it is worth noting the significant

dispersion among the maturity segments within the Treasury market, as

the one- to three-year portion was essentially flat for the month and the

five- to ten-year segment gained only 2.1%. The Federal Reserve’s

Operation Twist is scheduled to be completed at the end of June, with

$45 billion in additional purchases focused on nominal Treasuries

maturing in eight years or more. It remains to be seen how the market

will react when this source of demand ceases, but we note that the next

Federal Reserve meeting is scheduled for June 20th, and several market

participants have dramatically raised the possibility for another round of

quantitative easing. Ten-year U.S. Treasuries ended May at their lowest

level on record according to Bloomberg data, while the 30-year yield was

essentially in line with the record low reached in December 2008. In

contrast to long U.S. Treasuries, gold dropped sharply in May. This

represented the fourth straight monthly decline, which is the first such

streak since 1999. Gold’s status as a hedge against uncertainty has been

in question of late, and the precious metal has recently traded more

closely in line with other commodities. This trend may have been first

seen in September 2011, when gold declined 11.1% amidst European

sovereign worries and an equity market decline. The strengthening USD,

sales by investors to fund short-term capital needs, and/or concerns over

current prices after multi-year increases all likely contributed to the drop

in gold prices. However, without an income stream or fundamental use

for the precious metal, valuation metrics are speculative and we remain

skeptical of gold’s role as a reliable hedge for the total portfolio.

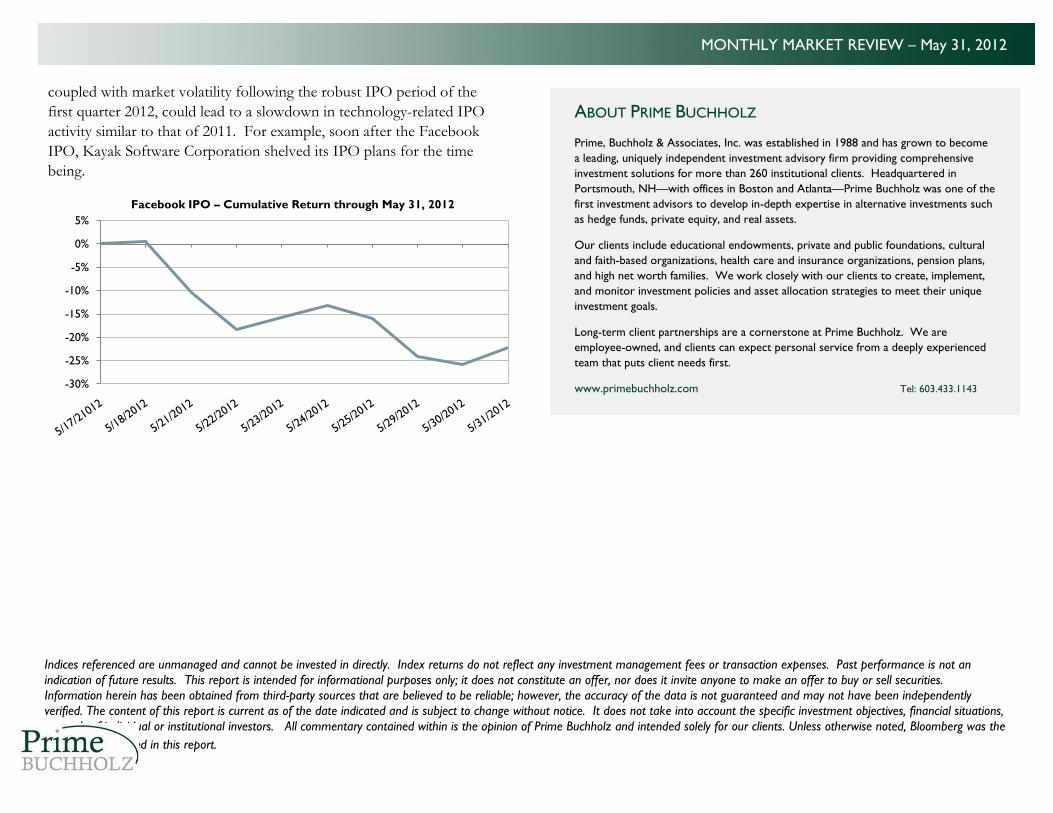

The much-hyped initial public offering (IPO) of Facebook launched on

May 18th, when the company debuted on the NASDAQ with an opening

price of $38 per share. It was the biggest IPO in the history of the

technology sector, but not only did it fail to counter the existing negative

sentiment in the market, the IPO fed into investor pessimism as multiple

problems occurred with the offering. The listing was delayed due to

what NASDAQ termed a technical issue, traders faced uncertainty over

order completions, and soon after the opening, questions arose about

lead underwriter Morgan Stanley’s role in the IPO. These issues and a

declining share price all clouded the early days of the stock and weighed

on the broader equity markets throughout the second half of the month.

By month-end, the share price had fallen to $29.60. The long-term

impact of the IPO on venture capital is difficult to gauge based on a

couple weeks of trading. However, it is possible the negative reaction,

MONTHLY MARKET REVIEW – May 31, 2012

coupled with market volatility following the robust IPO period of the

first quarter 2012, could lead to a slowdown in technology-related IPO

activity similar to that of 2011. For example, soon after the Facebook

IPO, Kayak Software Corporation shelved its IPO plans for the time

being.

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

Facebook IPO – Cumulative Return through May 31, 2012

Indices referenced are unmanaged and cannot be invested in directly. Index returns do not reflect any investment management fees or transaction expenses. Past performance is not an

indication of future results. This report is intended for informational purposes only; it does not constitute an offer, nor does it invite anyone to make an offer to buy or sell securities.

Information herein has been obtained from third-party sources that are believed to be reliable; however, the accuracy of the data is not guaranteed and may not have been independently

verified. The content of this report is current as of the date indicated and is subject to change without notice. It does not take into account the specific investment objectives, financial situations,

or needs of individual or institutional investors. All commentary contained within is the opinion of Prime Buchholz and intended solely for our clients. Unless otherwise noted, Bloomberg was the

source for data used in this report.

ABOUT PRIME BUCHHOLZ

Prime, Buchholz & Associates, Inc. was established in 1988 and has grown to become

a leading, uniquely independent investment advisory firm providing comprehensive

investment solutions for more than 260 institutional clients. Headquartered in

Portsmouth, NH—with offices in Boston and Atlanta—Prime Buchholz was one of the

first investment advisors to develop in-depth expertise in alternative investments such

as hedge funds, private equity, and real assets.

Our clients include educational endowments, private and public foundations, cultural

and faith-based organizations, health care and insurance organizations, pension plans,

and high net worth families. We work closely with our clients to create, implement,

and monitor investment policies and asset allocation strategies to meet their unique

investment goals.

Long-term client partnerships are a cornerstone at Prime Buchholz. We are

employee-owned, and clients can expect personal service from a deeply experienced

team that puts client needs first.

www.primebuchholz.com Tel: 603.433.1143

-3

0

3

6

9

12

15Historical U.S. Inflation

Core CPI Index CPI YOY Index

0

5

10

15

20

25

30

Historical Trailing PE

S&P 500 MSCI EAFE MSCI EM

MACRO ENVIRONMENT

(%)

MONTHLY MARKET REVIEW – May 31, 2012

Key Valuation Metrics Summary Current Period 1 Year Ago LT Average*

Equities – Trailing P/E (x)

S&P 500 13.1 14.9 18.8

MSCI EAFE 11.1 12.8 17.6

MSCI EM 10.2 12.0 12.4

Credit – OAS (bps)

Barclays Aggregate 83 56 57

Barclays High Yield 671 582 529

Barclays IG Corporate 209 185 133

Deflation Hedging – Nominal Yields (%)

10-Year U.S. Treasury 1.6 3.1 6.7

30-Year U.S. Treasury 2.6 4.2 7.1

Inflation Hedging

10-Year U.S. TIPS Yields (%) -0.6 0.8 2.4

S&P Energy Equity Trailing P/E (x) 9.6 14.9 17.2

S&P REITs Dividend Yield (%) 2.9 3.2 4.6

Non-U.S. Bonds

Barclays Global Treasury ex-U.S. Yield (%) 1.7 2.4 4.9

Barclays EM Local Currency Govt. Yields (%) 5.8 6.3 6.4

* Based on longest monthly history available in Bloomberg or Barclays Live

Average Current

S&P 500 18.8 13.1

MSCI EAFE 17.6 11.1

MSCI EM 12.4 10.2

(%)

Average Current

YOY Core CPI 3.9 2.3

YOY CPI 4.0 2.3

As of April 30, 20120

3

5

8

10

13

15

18

Market Yields

S&P Yield 10-Year Treasury Yield

S&P Yield Avg 10-Year Treasury Yield Avg

0.0

0.5

1.0

1.5

2.0

2.5

3.0Market Inflation Forecast

U.S. Breakeven 10-Year Index U.S. Breakeven 10-Year Index Avg.

0

5

10

15

20

25

Historical Central Bank Policy Rates

BOJ BOE ECB Fed

-15

-10

-5

0

5

10

15

20

Quarterly U.S. GDP Growth

-40

-30

-20

-10

0

10

20

30

40

50

60

70

Year-Over-Year U.S. Corporate Profits(%)(%)

(%)

MACRO ENVIRONMENT MONTHLY MARKET REVIEW – May 31, 2012

(%)

As of March 31, 2012As of March 31, 2012Source: Federal Reserve

International USD Returns by Region (%)

MTD QTD YTD 1 Year 2 Year 3 Year 5 Year 10 Year

MSCI ACWI -9.0 -10.0 0.7 -12.3 6.0 8.8 -3.7 4.6

Developed Markets

MSCI EAFE -11.5 -13.2 -3.8 -20.5 1.9 3.4 -7.3 4.0

MSCI Europe ex-U.K. -12.7 -16.4 -6.0 -29.2 -0.8 0.1 -9.8 3.6

MSCI U.K. -11.5 -10.3 -3.5 -13.5 8.1 8.6 -5.6 4.6

MSCI Japan -8.9 -11.8 -1.9 -10.5 -1.2 0.7 -7.5 1.4

MSCI Asia ex-Japan -11.8 -10.5 -0.4 -16.7 7.0 11.8 -0.3 10.8

Emerging Markets

MSCI EM -11.2 -12.3 0.1 -20.3 1.3 7.9 0.1 12.7

MSCI EMEA -14.5 -15.6 -2.1 -24.5 0.2 7.0 -2.7 12.3

MSCI Russia -19.4 -21.6 -7.1 -31.6 -2.7 2.3 -7.8 9.9

MSCI EM Asia -9.5 -9.6 2.4 -18.5 3.0 8.6 0.7 10.9

MSCI China -10.6 -7.4 1.8 -20.8 -3.2 2.2 1.1 15.0

MSCI India -11.6 -15.8 1.1 -29.4 -11.6 -1.1 -3.8 16.8

MSCI EM LatAm -13.1 -16.4 -4.2 -21.7 -2.2 6.7 1.3 18.3

MSCI Brazil -14.4 -19.8 -8.7 -27.7 -7.4 1.7 1.6 20.3

MSCI ACWI USD Returns by Sector (%)

MSCI ACWI Sectors MTD QTD YTD 1 Year 2 Year 3 Year 5 Year 10 Year

Consumer Discretionary -8.5 -8.6 7.2 -4.7 12.4 17.3 -0.5 5.0

Consumer Staples -4.8 -4.3 2.9 1.7 15.4 16.7 5.9 8.3

Energy -12.4 -13.4 -8.9 -19.7 5.6 4.2 -1.3 9.2

Financials -11.2 -13.4 1.9 -20.4 -2.2 2.7 -12.9 0.3

Health Care -5.0 -4.7 2.9 -1.9 13.4 13.1 1.7 4.8

Industrials -8.5 -10.1 1.1 -14.6 6.6 11.5 -3.6 5.8

Information Technology -8.7 -10.6 7.5 -0.2 9.8 14.5 1.5 4.8

Materials -12.8 -14.3 -5.2 -27.0 0.2 5.8 -3.0 9.4

Telecom -5.2 -4.5 -2.0 -8.9 11.0 9.9 -1.0 7.0

Utilities -5.2 -6.1 -3.3 -9.7 2.9 3.0 -4.4 7.3

Equity Market Returns (%)

MTD QTD YTD 1 Year 2 Year 3 Year 5 Year 10 Year

S&P 500 -6.0 -6.6 5.2 -0.4 12.0 14.9 -0.9 4.1

Russell 3000 -6.2 -6.8 5.2 -1.9 11.6 15.4 -0.7 4.6

Russell 2000 -6.6 -8.1 3.4 -8.9 8.7 16.5 -0.7 5.9

Russell 1000 -6.1 -6.7 5.3 -1.2 11.9 15.3 -0.7 4.5

MSCI ACWI (USD) -9.0 -10.0 0.7 -12.3 6.0 8.8 -3.7 4.6

MSCI ACWI (Local) -6.8 -8.1 2.1 -8.1 4.4 8.3 -4.1 3.0

MSCI ACWI ex-U.S. (USD) -11.4 -12.8 -3.0 -20.5 1.6 -4.6 -5.5 5.7

MSCI ACWI ex-U.S. (Local) -7.2 -9.2 -0.2 -13.4 -0.8 3.9 -6.2 2.6

MSCI EAFE (USD) -11.5 -13.2 -3.8 -20.5 1.9 3.4 -7.3 4.0

MSCI EAFE (Local) -7.5 -10.1 -0.9 -14.2 -2.2 2.6 -8.5 0.8

MSCI EM (USD) -11.2 -12.3 0.1 -20.3 1.3 7.9 0.1 12.7

MSCI EM (Local) -6.7 -7.2 2.7 -10.3 3.1 8.1 1.7 11.7

London – FTSE 100* -6.7 -6.9 -2.4 -7.2 5.4 10.7 -0.1 4.6 GBP

Japan – Nikkei 225* -10.3 -15.3 1.9 -10.1 -4.6 -1.8 -12.2 -1.9 JPY

Hong Kong – Hang Seng* -10.7 -8.3 2.6 -18.6 0.1 4.0 1.1 8.7 HKD

China – Shanghai Composite* -0.7 5.1 8.2 -11.8 -2.7 -1.7 -9.1 6.3 CNY

*Returns in local currency

GLOBAL EQUITY DETAILS MONTHLY MARKET REVIEW – May 31, 2012

0

10

20

30

40

50

60

70Equity Volatility

VIX Index V2X (Europe) Index VIX Index Avg V2X (Europe) Index Avg

0

1,000

2,000

3,000

4,000

5,000

6,000

0%

5%

10%

15%

20%

25%

30%

35%

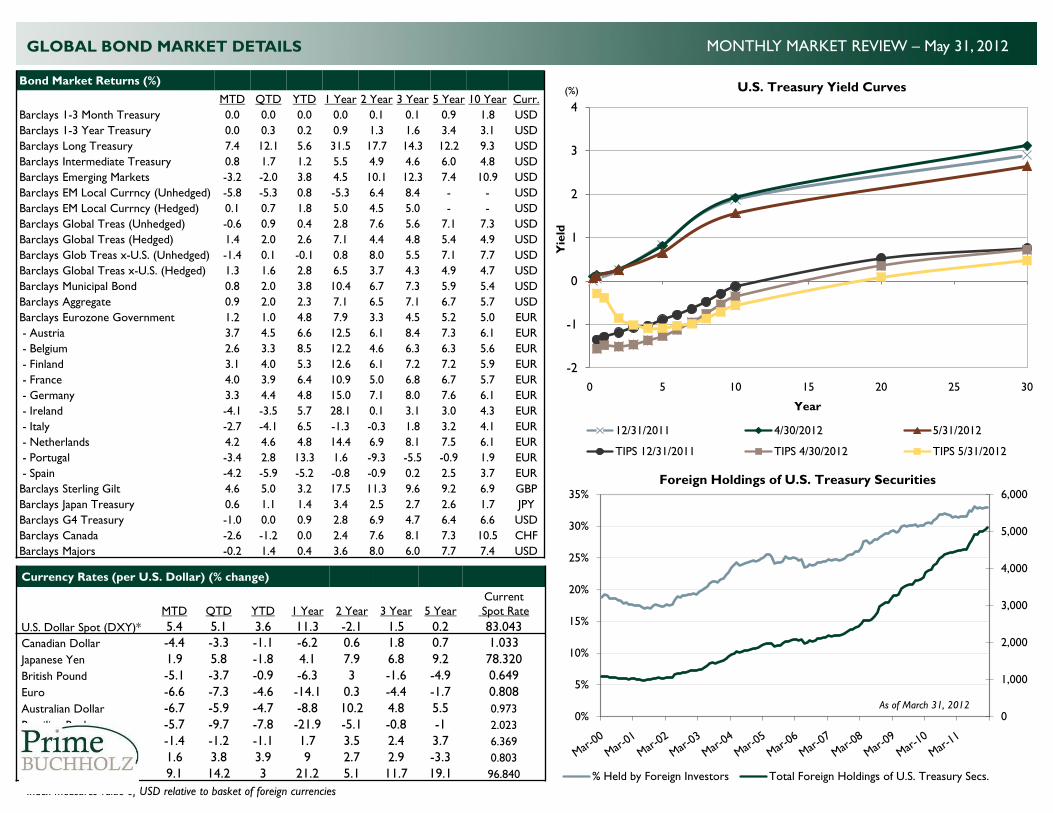

Foreign Holdings of U.S. Treasury Securities

% Held by Foreign Investors Total Foreign Holdings of U.S. Treasury Secs.

As of March 31, 2012

Currency Rates (per U.S. Dollar) (% change)

MTD QTD YTD 1 Year 2 Year 3 Year 5 Year

Current

Spot Rate

U.S. Dollar Spot (DXY)* 5.4 5.1 3.6 11.3 -2.1 1.5 0.2 83.043

Canadian Dollar -4.4 -3.3 -1.1 -6.2 0.6 1.8 0.7 1.033

Japanese Yen 1.9 5.8 -1.8 4.1 7.9 6.8 9.2 78.320

British Pound -5.1 -3.7 -0.9 -6.3 3 -1.6 -4.9 0.649

Euro -6.6 -7.3 -4.6 -14.1 0.3 -4.4 -1.7 0.808

Australian Dollar -6.7 -5.9 -4.7 -8.8 10.2 4.8 5.5 0.973

Brazilian Real -5.7 -9.7 -7.8 -21.9 -5.1 -0.8 -1 2.023

Chinese Yuan/Renminbi -1.4 -1.2 -1.1 1.7 3.5 2.4 3.7 6.369

GBP/Euro 1.6 3.8 3.9 9 2.7 2.9 -3.3 0.803

Yen/Euro 9.1 14.2 3 21.2 5.1 11.7 19.1 96.840

*Index measures value of USD relative to basket of foreign currencies

Bond Market Returns (%)

MTD QTD YTD 1 Year 2 Year 3 Year 5 Year 10 Year Curr.

Barclays 1-3 Month Treasury 0.0 0.0 0.0 0.0 0.1 0.1 0.9 1.8 USD

Barclays 1-3 Year Treasury 0.0 0.3 0.2 0.9 1.3 1.6 3.4 3.1 USD

Barclays Long Treasury 7.4 12.1 5.6 31.5 17.7 14.3 12.2 9.3 USD

Barclays Intermediate Treasury 0.8 1.7 1.2 5.5 4.9 4.6 6.0 4.8 USD

Barclays Emerging Markets -3.2 -2.0 3.8 4.5 10.1 12.3 7.4 10.9 USD

Barclays EM Local Currncy (Unhedged) -5.8 -5.3 0.8 -5.3 6.4 8.4 - - USD

Barclays EM Local Currncy (Hedged) 0.1 0.7 1.8 5.0 4.5 5.0 - - USD

Barclays Global Treas (Unhedged) -0.6 0.9 0.4 2.8 7.6 5.6 7.1 7.3 USD

Barclays Global Treas (Hedged) 1.4 2.0 2.6 7.1 4.4 4.8 5.4 4.9 USD

Barclays Glob Treas x-U.S. (Unhedged) -1.4 0.1 -0.1 0.8 8.0 5.5 7.1 7.7 USD

Barclays Global Treas x-U.S. (Hedged) 1.3 1.6 2.8 6.5 3.7 4.3 4.9 4.7 USD

Barclays Municipal Bond 0.8 2.0 3.8 10.4 6.7 7.3 5.9 5.4 USD

Barclays Aggregate 0.9 2.0 2.3 7.1 6.5 7.1 6.7 5.7 USD

Barclays Eurozone Government 1.2 1.0 4.8 7.9 3.3 4.5 5.2 5.0 EUR

- Austria 3.7 4.5 6.6 12.5 6.1 8.4 7.3 6.1 EUR

- Belgium 2.6 3.3 8.5 12.2 4.6 6.3 6.3 5.6 EUR

- Finland 3.1 4.0 5.3 12.6 6.1 7.2 7.2 5.9 EUR

- France 4.0 3.9 6.4 10.9 5.0 6.8 6.7 5.7 EUR

- Germany 3.3 4.4 4.8 15.0 7.1 8.0 7.6 6.1 EUR

- Ireland -4.1 -3.5 5.7 28.1 0.1 3.1 3.0 4.3 EUR

- Italy -2.7 -4.1 6.5 -1.3 -0.3 1.8 3.2 4.1 EUR

- Netherlands 4.2 4.6 4.8 14.4 6.9 8.1 7.5 6.1 EUR

- Portugal -3.4 2.8 13.3 1.6 -9.3 -5.5 -0.9 1.9 EUR

- Spain -4.2 -5.9 -5.2 -0.8 -0.9 0.2 2.5 3.7 EUR

Barclays Sterling Gilt 4.6 5.0 3.2 17.5 11.3 9.6 9.2 6.9 GBP

Barclays Japan Treasury 0.6 1.1 1.4 3.4 2.5 2.7 2.6 1.7 JPY

Barclays G4 Treasury -1.0 0.0 0.9 2.8 6.9 4.7 6.4 6.6 USD

Barclays Canada -2.6 -1.2 0.0 2.4 7.6 8.1 7.3 10.5 CHF

Barclays Majors -0.2 1.4 0.4 3.6 8.0 6.0 7.7 7.4 USD

MONTHLY MARKET REVIEW – May 31, 2012GLOBAL BOND MARKET DETAILS

-2

-1

0

1

2

3

4

0 5 10 15 20 25 30

Yie

ld

Year

U.S. Treasury Yield Curves

12/31/2011 4/30/2012 5/31/2012

TIPS 12/31/2011 TIPS 4/30/2012 TIPS 5/31/2012

(%)

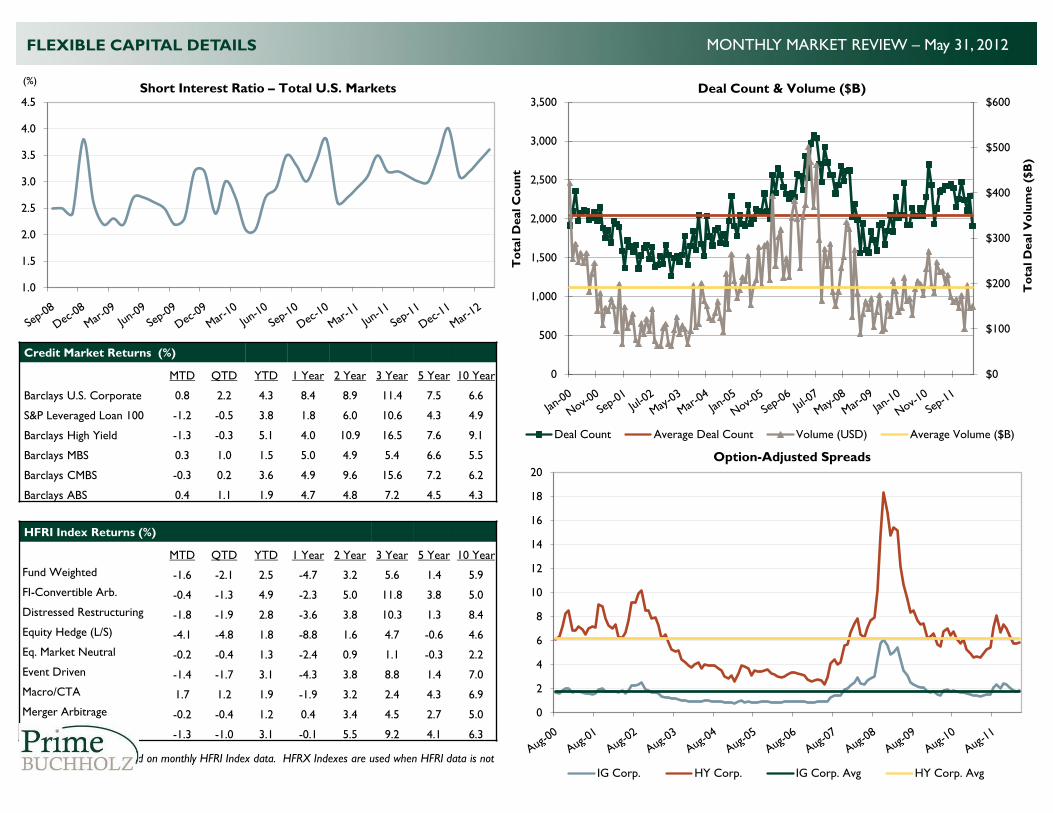

Credit Market Returns (%)

MTD QTD YTD 1 Year 2 Year 3 Year 5 Year 10 Year

Barclays U.S. Corporate 0.8 2.2 4.3 8.4 8.9 11.4 7.5 6.6

S&P Leveraged Loan 100 -1.2 -0.5 3.8 1.8 6.0 10.6 4.3 4.9

Barclays High Yield -1.3 -0.3 5.1 4.0 10.9 16.5 7.6 9.1

Barclays MBS 0.3 1.0 1.5 5.0 4.9 5.4 6.6 5.5

Barclays CMBS -0.3 0.2 3.6 4.9 9.6 15.6 7.2 6.2

Barclays ABS 0.4 1.1 1.9 4.7 4.8 7.2 4.5 4.3

HFRI Index Returns (%)

MTD QTD YTD 1 Year 2 Year 3 Year 5 Year 10 Year

Fund Weighted -1.6 -2.1 2.5 -4.7 3.2 5.6 1.4 5.9

FI-Convertible Arb. -0.4 -1.3 4.9 -2.3 5.0 11.8 3.8 5.0

Distressed Restructuring -1.8 -1.9 2.8 -3.6 3.8 10.3 1.3 8.4

Equity Hedge (L/S) -4.1 -4.8 1.8 -8.8 1.6 4.7 -0.6 4.6

Eq. Market Neutral -0.2 -0.4 1.3 -2.4 0.9 1.1 -0.3 2.2

Event Driven -1.4 -1.7 3.1 -4.3 3.8 8.8 1.4 7.0

Macro/CTA 1.7 1.2 1.9 -1.9 3.2 2.4 4.3 6.9

Merger Arbitrage -0.2 -0.4 1.2 0.4 3.4 4.5 2.7 5.0

Relative Value Arb. -1.3 -1.0 3.1 -0.1 5.5 9.2 4.1 6.3

NOTE: Returns are based on monthly HFRI Index data. HFRX Indexes are used when HFRI data is not

available.

MONTHLY MARKET REVIEW – May 31, 2012FLEXIBLE CAPITAL DETAILS

0

2

4

6

8

10

12

14

16

18

20

Option-Adjusted Spreads

IG Corp. HY Corp. IG Corp. Avg HY Corp. Avg

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5Short Interest Ratio – Total U.S. Markets

(%)

$0

$100

$200

$300

$400

$500

$600

0

500

1,000

1,500

2,000

2,500

3,000

3,500

To

tal D

eal V

olu

me (

$B

)

To

tal D

eal C

ou

nt

Deal Count & Volume ($B)

Deal Count Average Deal Count Volume (USD) Average Volume ($B)

0

2

4

6

8

10

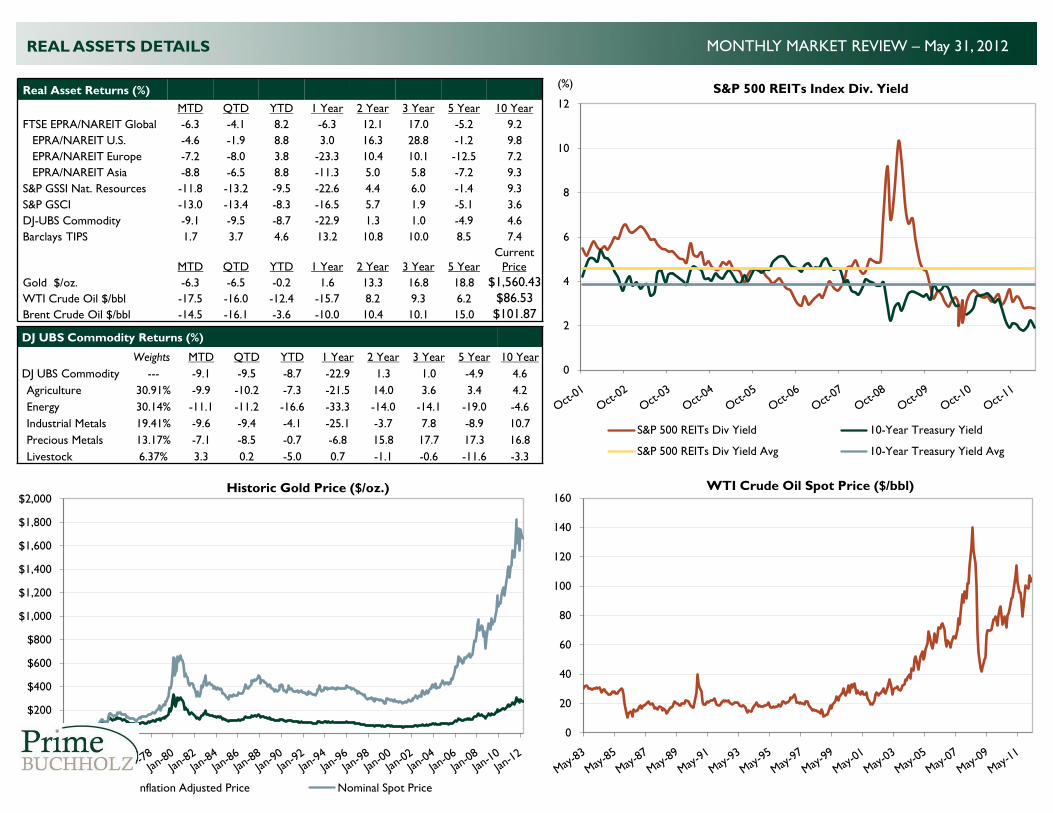

12

S&P 500 REITs Index Div. Yield

S&P 500 REITs Div Yield 10-Year Treasury Yield

S&P 500 REITs Div Yield Avg 10-Year Treasury Yield Avg

Real Asset Returns (%)

MTD QTD YTD 1 Year 2 Year 3 Year 5 Year 10 Year

FTSE EPRA/NAREIT Global -6.3 -4.1 8.2 -6.3 12.1 17.0 -5.2 9.2

EPRA/NAREIT U.S. -4.6 -1.9 8.8 3.0 16.3 28.8 -1.2 9.8

EPRA/NAREIT Europe -7.2 -8.0 3.8 -23.3 10.4 10.1 -12.5 7.2

EPRA/NAREIT Asia -8.8 -6.5 8.8 -11.3 5.0 5.8 -7.2 9.3

S&P GSSI Nat. Resources -11.8 -13.2 -9.5 -22.6 4.4 6.0 -1.4 9.3

S&P GSCI -13.0 -13.4 -8.3 -16.5 5.7 1.9 -5.1 3.6

DJ-UBS Commodity -9.1 -9.5 -8.7 -22.9 1.3 1.0 -4.9 4.6

Barclays TIPS 1.7 3.7 4.6 13.2 10.8 10.0 8.5 7.4

MTD QTD YTD 1 Year 2 Year 3 Year 5 Year

Current

Price

Gold $/oz. -6.3 -6.5 -0.2 1.6 13.3 16.8 18.8 $1,560.43

WTI Crude Oil $/bbl -17.5 -16.0 -12.4 -15.7 8.2 9.3 6.2 $86.53

Brent Crude Oil $/bbl -14.5 -16.1 -3.6 -10.0 10.4 10.1 15.0 $101.87

MONTHLY MARKET REVIEW – May 31, 2012

DJ UBS Commodity Returns (%)

Weights MTD QTD YTD 1 Year 2 Year 3 Year 5 Year 10 Year

DJ UBS Commodity --- -9.1 -9.5 -8.7 -22.9 1.3 1.0 -4.9 4.6

Agriculture 30.91% -9.9 -10.2 -7.3 -21.5 14.0 3.6 3.4 4.2

Energy 30.14% -11.1 -11.2 -16.6 -33.3 -14.0 -14.1 -19.0 -4.6

Industrial Metals 19.41% -9.6 -9.4 -4.1 -25.1 -3.7 7.8 -8.9 10.7

Precious Metals 13.17% -7.1 -8.5 -0.7 -6.8 15.8 17.7 17.3 16.8

Livestock 6.37% 3.3 0.2 -5.0 0.7 -1.1 -0.6 -11.6 -3.3

REAL ASSETS DETAILS

(%)

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000Historic Gold Price ($/oz.)

Inflation Adjusted Price Nominal Spot Price

0

20

40

60

80

100

120

140

160WTI Crude Oil Spot Price ($/bbl)

4

MONTHLY MARKET REVIEW – May 31, 2012

Mergers and Acquisitions (M&A) is a general term used to refer to the

consolidation of companies. A merger is a combination of two companies to form a

new company, while an acquisition is the purchase of one company by another in which

no new company is formed. ―Deal count‖ and ―volume‖ each quantify the mergers and

acquisitions activity occurring within a given time period. Deal count represents the

actual number of deals that were completed each month, while ―volume‖ represents the

total dollar value of the deals that were completed during the month. The premium is

the difference between the actual cost for acquiring a target firm versus the estimate

made of its value before the acquisition.

Short Interest Ratio is an indicator that is derived by dividing the short interest by

the average daily volume for a stock. This indicator is used by both fundamental and

technical traders to identify the prevailing sentiment the market has for a specific stock.

U.S. Corporate Profits is a statistic reported quarterly by the Bureau of Economic

Analysis (BEA) that summarizes the net income of corporations in the National Income

and Product Accounts (NIPA). Corporate profits are an economic indicator

that calculates net income using several different measures: profits from current

production; book profits, and after-tax profits.

Barclays Aggregate Index comprises government securities, mortgage-backed

securities, asset-backed securities, and corporate securities to simulate the universe of

bonds in the market. The maturities of the bonds in the Index are over one year.

Barclays Global Treasury ex-U.S. Index includes government bonds issued by

investment-grade countries outside the United States, in local currencies, that have a

remaining maturity of one year or more and are rated investment grade.

Barclays U.S. TIPS Index is a rules-based, market value-weighted Index that tracks

inflation protected securities issued by the U.S. Treasury.

Chicago Board Options Exchange Volatility Index (VIX) measures traders'

expectations of volatility in the stock market by tracking bid/ask quotes on the Standard

& Poor's 500 Stock Index.

DJ-UBS Commodity Index is composed of futures contracts on physical

commodities. It is composed of commodities traded on U.S. exchanges, with the

exception of aluminum, nickel, and zinc, which trade on the London Metal Exchange

(LME).

FTSE EPRA/NAREIT Developed Index is designed to represent general trends in

eligible real estate equities worldwide. Relevant real estate activities are defined as the

ownership, disposure, and development of income-producing real estate. The Index

series includes a range of regional and country indices.

HFRX Equity Market Neutral Index is designed to reflect the performance of

Equity Market Neutral strategies which employ sophisticated quantitative techniques of

analyzing price data to ascertain information about future price movement and

relationships between securities and select securities for purchase and sale. These can

include both Factor-based and Statistical Arbitrage/Trading strategies. Equity Market

Neutral Strategies typically maintain net equity market exposure no greater than 10%

long or short.

HFRX Global Hedge Index is designed to be representative of the overall

composition of the hedge fund universe. It is comprised of eight strategies: convertible

arbitrage, distressed securities, equity, equity market neutral, event-driven, macro,

merger arbitrage, and relative value arbitrage.

HFRX Relative Value Arbitrage Index is designed to represent investment

managers who maintain positions in which the investment thesis is predicated on

realization of a valuation discrepancy in the relationship between multiple securities.

MSCI ACWI (All Country World Index) Index is a free float-adjusted market

capitalization weighted index that is designed to measure the equity market

performance of developed and emerging markets. The Index consists of a mix of

developed and emerging market country indices.

MSCI China Index is a free float-adjusted market capitalization weighted index that is

designed to measure the equity market performance of Chinese companies listed on the

Hong Kong exchange, which are frequently referred to as H shares.

MSCI EAFE Net Index is a free float-adjusted market capitalization index that is

designed to measure the equity market performance of developed markets, excluding

the U.S. & Canada.

MSCI EM (Emerging Markets) Index is a free float-adjusted market capitalization

index that is designed to measure equity market performance of emerging markets.

Russell 3000 Index measures the performance of the largest 3,000 U.S. companies,

representing approximately 98% of the investable U.S. equity market.

Russell 3000 Growth Index measures the performance of the broad growth segment

of the U.S. equity universe. It includes those Russell 3000 companies with higher price-

to-book ratios and higher forecasted growth values.

Russell 3000 Value Index measures the performance of the broad value segment of

U.S. equity value universe. It includes those Russell 3000 companies with lower price-

to-book ratios and lower forecasted growth values.

Russell Midcap Index measures the performance of the mid cap segment of the U.S.

equity universe. The Index is a subset of the Russell 1000 Index. It includes

approximately 800 of the smallest securities based on a combination of their market cap

and current Index membership.

S&P 500 Index is a gauge of the U.S. equities market and includes 500 leading

companies in leading industries of the U.S. economy.

U.S. Dollar Index indicates the general international value of the U.S. dollar (USD) by

averaging the exchange rates between the USD and six major world currencies.

INDEX DESCRIPTIONS

MK12014_060712 © 2012 Prime, Buchholz & Associates, Inc.

MarketValue

% ofPortfolio 1 Mo. 3 Mo.

FiscalYTD

CalendarYTD 1 YR 3 YRS 5 YRS 10 YRS

ReturnSince

InceptionDate

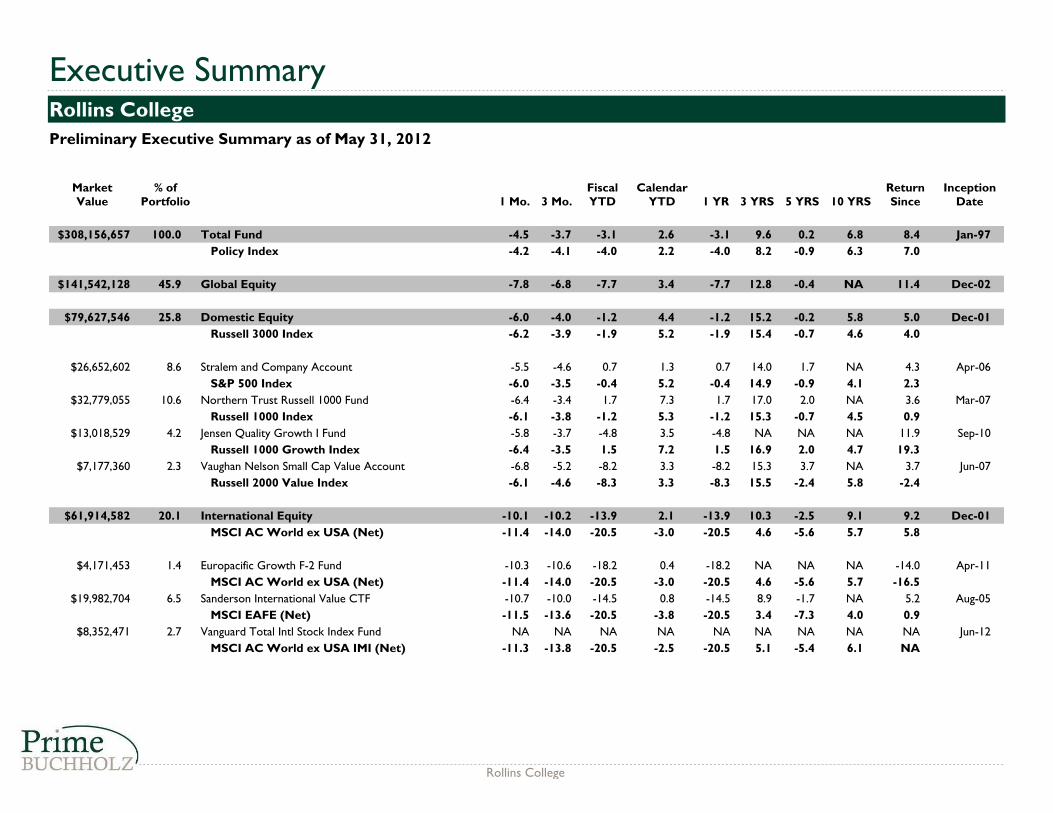

$308,156,657 100.0 Total Fund -4.5 -3.7 -3.1 2.6 -3.1 9.6 0.2 6.8 8.4 Jan-97

Policy Index -4.2 -4.1 -4.0 2.2 -4.0 8.2 -0.9 6.3 7.0

$141,542,128 45.9 Global Equity -7.8 -6.8 -7.7 3.4 -7.7 12.8 -0.4 NA 11.4 Dec-02

$79,627,546 25.8 Domestic Equity -6.0 -4.0 -1.2 4.4 -1.2 15.2 -0.2 5.8 5.0 Dec-01

Russell 3000 Index -6.2 -3.9 -1.9 5.2 -1.9 15.4 -0.7 4.6 4.0

$26,652,602 8.6 Stralem and Company Account -5.5 -4.6 0.7 1.3 0.7 14.0 1.7 NA 4.3 Apr-06

S&P 500 Index -6.0 -3.5 -0.4 5.2 -0.4 14.9 -0.9 4.1 2.3

$32,779,055 10.6 Northern Trust Russell 1000 Fund -6.4 -3.4 1.7 7.3 1.7 17.0 2.0 NA 3.6 Mar-07

Russell 1000 Index -6.1 -3.8 -1.2 5.3 -1.2 15.3 -0.7 4.5 0.9

$13,018,529 4.2 Jensen Quality Growth I Fund -5.8 -3.7 -4.8 3.5 -4.8 NA NA NA 11.9 Sep-10

Russell 1000 Growth Index -6.4 -3.5 1.5 7.2 1.5 16.9 2.0 4.7 19.3

$7,177,360 2.3 Vaughan Nelson Small Cap Value Account -6.8 -5.2 -8.2 3.3 -8.2 15.3 3.7 NA 3.7 Jun-07

Russell 2000 Value Index -6.1 -4.6 -8.3 3.3 -8.3 15.5 -2.4 5.8 -2.4

$61,914,582 20.1 International Equity -10.1 -10.2 -13.9 2.1 -13.9 10.3 -2.5 9.1 9.2 Dec-01

MSCI AC World ex USA (Net) -11.4 -14.0 -20.5 -3.0 -20.5 4.6 -5.6 5.7 5.8

$4,171,453 1.4 Europacific Growth F-2 Fund -10.3 -10.6 -18.2 0.4 -18.2 NA NA NA -14.0 Apr-11

MSCI AC World ex USA (Net) -11.4 -14.0 -20.5 -3.0 -20.5 4.6 -5.6 5.7 -16.5

$19,982,704 6.5 Sanderson International Value CTF -10.7 -10.0 -14.5 0.8 -14.5 8.9 -1.7 NA 5.2 Aug-05

MSCI EAFE (Net) -11.5 -13.6 -20.5 -3.8 -20.5 3.4 -7.3 4.0 0.9

$8,352,471 2.7 Vanguard Total Intl Stock Index Fund NA NA NA NA NA NA NA NA NA Jun-12

MSCI AC World ex USA IMI (Net) -11.3 -13.8 -20.5 -2.5 -20.5 5.1 -5.4 6.1 NA

Executive SummaryRollins College

Preliminary Executive Summary as of May 31, 2012

Rollins College

Executive SummaryRollins College

Preliminary Executive Summary as of May 31, 2012

MarketValue

% ofPortfolio 1 Mo. 3 Mo.

FiscalYTD

CalendarYTD 1 YR 3 YRS 5 YRS 10 YRS

ReturnSince

InceptionDate

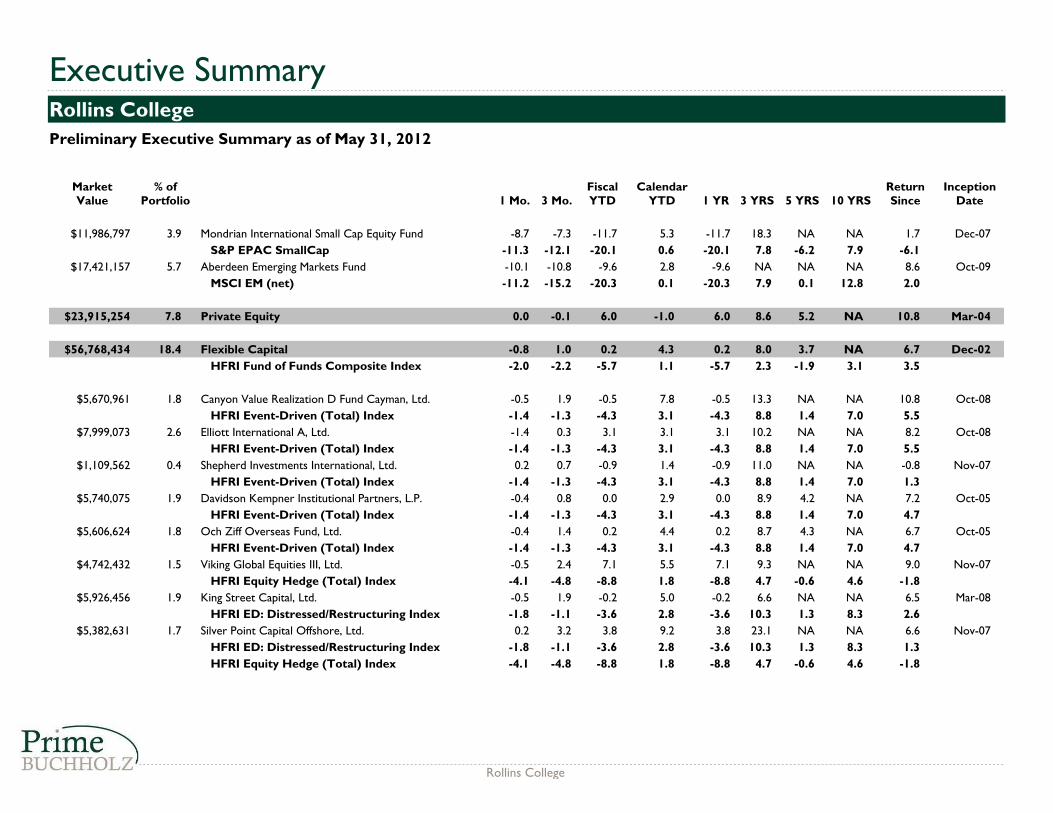

$11,986,797 3.9 Mondrian International Small Cap Equity Fund -8.7 -7.3 -11.7 5.3 -11.7 18.3 NA NA 1.7 Dec-07

S&P EPAC SmallCap -11.3 -12.1 -20.1 0.6 -20.1 7.8 -6.2 7.9 -6.1

$17,421,157 5.7 Aberdeen Emerging Markets Fund -10.1 -10.8 -9.6 2.8 -9.6 NA NA NA 8.6 Oct-09

MSCI EM (net) -11.2 -15.2 -20.3 0.1 -20.3 7.9 0.1 12.8 2.0

$23,915,254 7.8 Private Equity 0.0 -0.1 6.0 -1.0 6.0 8.6 5.2 NA 10.8 Mar-04

$56,768,434 18.4 Flexible Capital -0.8 1.0 0.2 4.3 0.2 8.0 3.7 NA 6.7 Dec-02

HFRI Fund of Funds Composite Index -2.0 -2.2 -5.7 1.1 -5.7 2.3 -1.9 3.1 3.5

$5,670,961 1.8 Canyon Value Realization D Fund Cayman, Ltd. -0.5 1.9 -0.5 7.8 -0.5 13.3 NA NA 10.8 Oct-08

HFRI Event-Driven (Total) Index -1.4 -1.3 -4.3 3.1 -4.3 8.8 1.4 7.0 5.5

$7,999,073 2.6 Elliott International A, Ltd. -1.4 0.3 3.1 3.1 3.1 10.2 NA NA 8.2 Oct-08

HFRI Event-Driven (Total) Index -1.4 -1.3 -4.3 3.1 -4.3 8.8 1.4 7.0 5.5

$1,109,562 0.4 Shepherd Investments International, Ltd. 0.2 0.7 -0.9 1.4 -0.9 11.0 NA NA -0.8 Nov-07

HFRI Event-Driven (Total) Index -1.4 -1.3 -4.3 3.1 -4.3 8.8 1.4 7.0 1.3

$5,740,075 1.9 Davidson Kempner Institutional Partners, L.P. -0.4 0.8 0.0 2.9 0.0 8.9 4.2 NA 7.2 Oct-05

HFRI Event-Driven (Total) Index -1.4 -1.3 -4.3 3.1 -4.3 8.8 1.4 7.0 4.7

$5,606,624 1.8 Och Ziff Overseas Fund, Ltd. -0.4 1.4 0.2 4.4 0.2 8.7 4.3 NA 6.7 Oct-05

HFRI Event-Driven (Total) Index -1.4 -1.3 -4.3 3.1 -4.3 8.8 1.4 7.0 4.7

$4,742,432 1.5 Viking Global Equities III, Ltd. -0.5 2.4 7.1 5.5 7.1 9.3 NA NA 9.0 Nov-07

HFRI Equity Hedge (Total) Index -4.1 -4.8 -8.8 1.8 -8.8 4.7 -0.6 4.6 -1.8

$5,926,456 1.9 King Street Capital, Ltd. -0.5 1.9 -0.2 5.0 -0.2 6.6 NA NA 6.5 Mar-08

HFRI ED: Distressed/Restructuring Index -1.8 -1.1 -3.6 2.8 -3.6 10.3 1.3 8.3 2.6

$5,382,631 1.7 Silver Point Capital Offshore, Ltd. 0.2 3.2 3.8 9.2 3.8 23.1 NA NA 6.6 Nov-07

HFRI ED: Distressed/Restructuring Index -1.8 -1.1 -3.6 2.8 -3.6 10.3 1.3 8.3 1.3

HFRI Equity Hedge (Total) Index -4.1 -4.8 -8.8 1.8 -8.8 4.7 -0.6 4.6 -1.8

Rollins College

Executive SummaryRollins College

Preliminary Executive Summary as of May 31, 2012

MarketValue

% ofPortfolio 1 Mo. 3 Mo.

FiscalYTD

CalendarYTD 1 YR 3 YRS 5 YRS 10 YRS

ReturnSince

InceptionDate

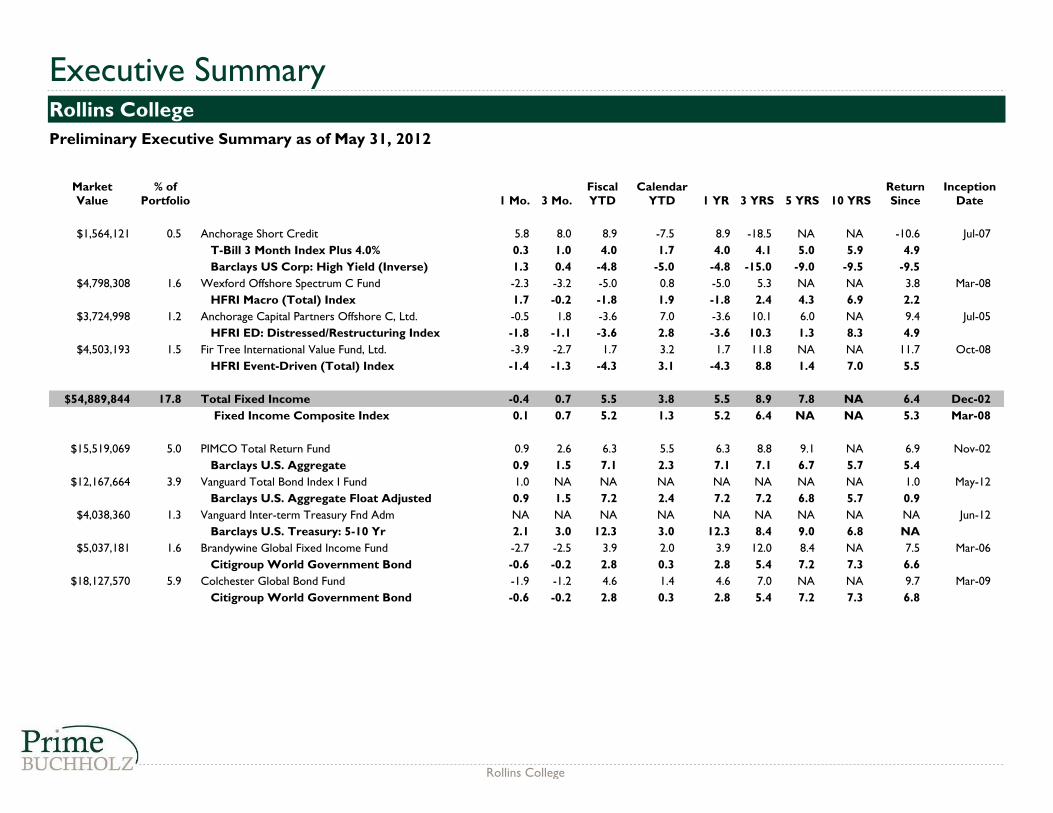

$1,564,121 0.5 Anchorage Short Credit 5.8 8.0 8.9 -7.5 8.9 -18.5 NA NA -10.6 Jul-07

T-Bill 3 Month Index Plus 4.0% 0.3 1.0 4.0 1.7 4.0 4.1 5.0 5.9 4.9

Barclays US Corp: High Yield (Inverse) 1.3 0.4 -4.8 -5.0 -4.8 -15.0 -9.0 -9.5 -9.5

$4,798,308 1.6 Wexford Offshore Spectrum C Fund -2.3 -3.2 -5.0 0.8 -5.0 5.3 NA NA 3.8 Mar-08

HFRI Macro (Total) Index 1.7 -0.2 -1.8 1.9 -1.8 2.4 4.3 6.9 2.2

$3,724,998 1.2 Anchorage Capital Partners Offshore C, Ltd. -0.5 1.8 -3.6 7.0 -3.6 10.1 6.0 NA 9.4 Jul-05

HFRI ED: Distressed/Restructuring Index -1.8 -1.1 -3.6 2.8 -3.6 10.3 1.3 8.3 4.9

$4,503,193 1.5 Fir Tree International Value Fund, Ltd. -3.9 -2.7 1.7 3.2 1.7 11.8 NA NA 11.7 Oct-08

HFRI Event-Driven (Total) Index -1.4 -1.3 -4.3 3.1 -4.3 8.8 1.4 7.0 5.5

$54,889,844 17.8 Total Fixed Income -0.4 0.7 5.5 3.8 5.5 8.9 7.8 NA 6.4 Dec-02

Fixed Income Composite Index 0.1 0.7 5.2 1.3 5.2 6.4 NA NA 5.3 Mar-08

$15,519,069 5.0 PIMCO Total Return Fund 0.9 2.6 6.3 5.5 6.3 8.8 9.1 NA 6.9 Nov-02

Barclays U.S. Aggregate 0.9 1.5 7.1 2.3 7.1 7.1 6.7 5.7 5.4

$12,167,664 3.9 Vanguard Total Bond Index I Fund 1.0 NA NA NA NA NA NA NA 1.0 May-12

Barclays U.S. Aggregate Float Adjusted 0.9 1.5 7.2 2.4 7.2 7.2 6.8 5.7 0.9

$4,038,360 1.3 Vanguard Inter-term Treasury Fnd Adm NA NA NA NA NA NA NA NA NA Jun-12

Barclays U.S. Treasury: 5-10 Yr 2.1 3.0 12.3 3.0 12.3 8.4 9.0 6.8 NA

$5,037,181 1.6 Brandywine Global Fixed Income Fund -2.7 -2.5 3.9 2.0 3.9 12.0 8.4 NA 7.5 Mar-06

Citigroup World Government Bond -0.6 -0.2 2.8 0.3 2.8 5.4 7.2 7.3 6.6

$18,127,570 5.9 Colchester Global Bond Fund -1.9 -1.2 4.6 1.4 4.6 7.0 NA NA 9.7 Mar-09

Citigroup World Government Bond -0.6 -0.2 2.8 0.3 2.8 5.4 7.2 7.3 6.8

Rollins College

Executive SummaryRollins College

Preliminary Executive Summary as of May 31, 2012

MarketValue

% ofPortfolio 1 Mo. 3 Mo.

FiscalYTD

CalendarYTD 1 YR 3 YRS 5 YRS 10 YRS

ReturnSince

InceptionDate

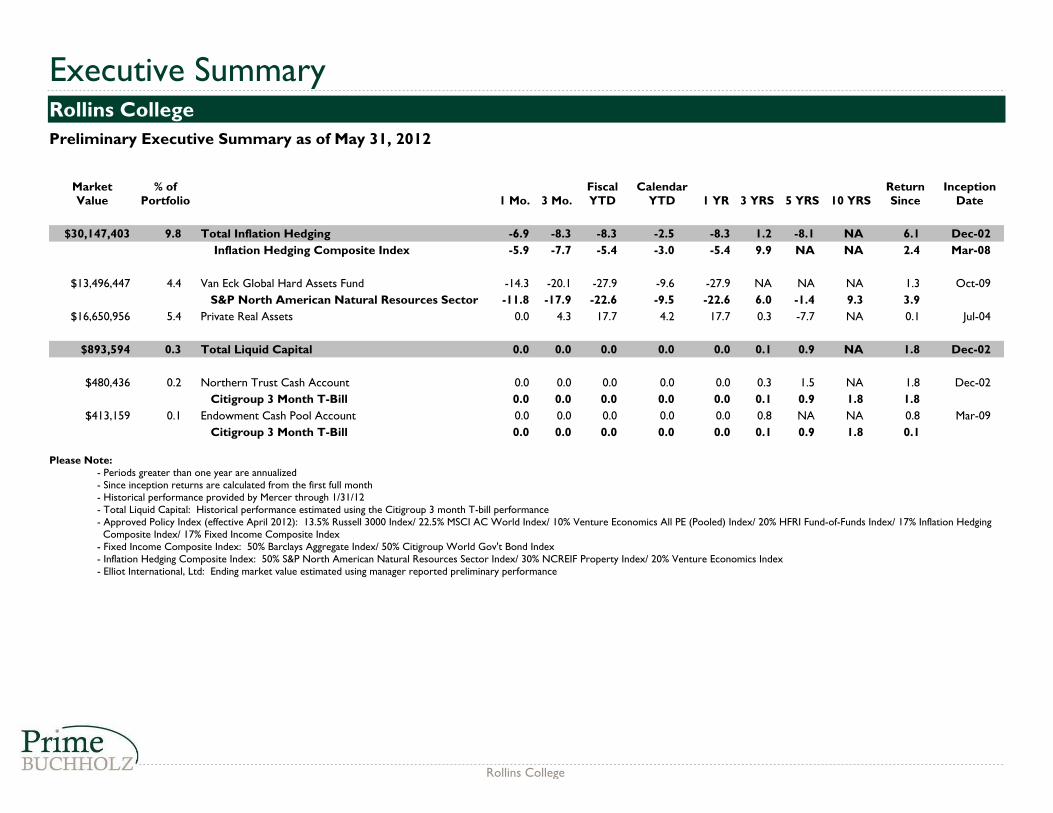

$30,147,403 9.8 Total Inflation Hedging -6.9 -8.3 -8.3 -2.5 -8.3 1.2 -8.1 NA 6.1 Dec-02

Inflation Hedging Composite Index -5.9 -7.7 -5.4 -3.0 -5.4 9.9 NA NA 2.4 Mar-08

$13,496,447 4.4 Van Eck Global Hard Assets Fund -14.3 -20.1 -27.9 -9.6 -27.9 NA NA NA 1.3 Oct-09

S&P North American Natural Resources Sector -11.8 -17.9 -22.6 -9.5 -22.6 6.0 -1.4 9.3 3.9

$16,650,956 5.4 Private Real Assets 0.0 4.3 17.7 4.2 17.7 0.3 -7.7 NA 0.1 Jul-04

$893,594 0.3 Total Liquid Capital 0.0 0.0 0.0 0.0 0.0 0.1 0.9 NA 1.8 Dec-02

$480,436 0.2 Northern Trust Cash Account 0.0 0.0 0.0 0.0 0.0 0.3 1.5 NA 1.8 Dec-02

Citigroup 3 Month T-Bill 0.0 0.0 0.0 0.0 0.0 0.1 0.9 1.8 1.8

$413,159 0.1 Endowment Cash Pool Account 0.0 0.0 0.0 0.0 0.0 0.8 NA NA 0.8 Mar-09

Citigroup 3 Month T-Bill 0.0 0.0 0.0 0.0 0.0 0.1 0.9 1.8 0.1

Please Note:- Periods greater than one year are annualized- Since inception returns are calculated from the first full month- Historical performance provided by Mercer through 1/31/12- Total Liquid Capital: Historical performance estimated using the Citigroup 3 month T-bill performance- Approved Policy Index (effective April 2012): 13.5% Russell 3000 Index/ 22.5% MSCI AC World Index/ 10% Venture Economics All PE (Pooled) Index/ 20% HFRI Fund-of-Funds Index/ 17% Inflation Hedging Composite Index/ 17% Fixed Income Composite Index- Fixed Income Composite Index: 50% Barclays Aggregate Index/ 50% Citigroup World Gov't Bond Index- Inflation Hedging Composite Index: 50% S&P North American Natural Resources Sector Index/ 30% NCREIF Property Index/ 20% Venture Economics Index- Elliot International, Ltd: Ending market value estimated using manager reported preliminary performance

Rollins College

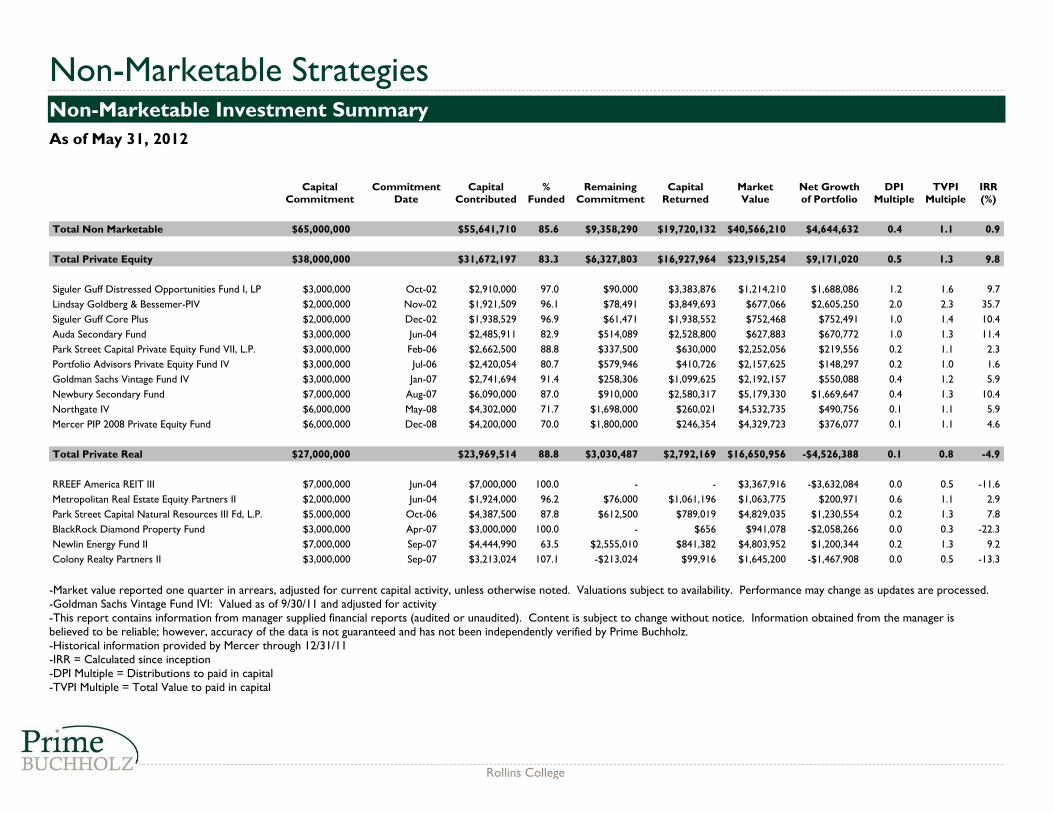

CapitalCommitment

CommitmentDate

CapitalContributed

%Funded

RemainingCommitment

CapitalReturned

MarketValue

Net Growthof Portfolio

DPIMultiple

TVPIMultiple

IRR(%)

Total Non Marketable $65,000,000 $55,641,710 85.6 $9,358,290 $19,720,132 $40,566,210 $4,644,632 0.4 1.1 0.9

Total Private Equity $38,000,000 $31,672,197 83.3 $6,327,803 $16,927,964 $23,915,254 $9,171,020 0.5 1.3 9.8

Siguler Guff Distressed Opportunities Fund I, LP $3,000,000 Oct-02 $2,910,000 97.0 $90,000 $3,383,876 $1,214,210 $1,688,086 1.2 1.6 9.7

Lindsay Goldberg & Bessemer-PIV $2,000,000 Nov-02 $1,921,509 96.1 $78,491 $3,849,693 $677,066 $2,605,250 2.0 2.3 35.7

Siguler Guff Core Plus $2,000,000 Dec-02 $1,938,529 96.9 $61,471 $1,938,552 $752,468 $752,491 1.0 1.4 10.4

Auda Secondary Fund $3,000,000 Jun-04 $2,485,911 82.9 $514,089 $2,528,800 $627,883 $670,772 1.0 1.3 11.4

Park Street Capital Private Equity Fund VII, L.P. $3,000,000 Feb-06 $2,662,500 88.8 $337,500 $630,000 $2,252,056 $219,556 0.2 1.1 2.3

Portfolio Advisors Private Equity Fund IV $3,000,000 Jul-06 $2,420,054 80.7 $579,946 $410,726 $2,157,625 $148,297 0.2 1.0 1.6

Goldman Sachs Vintage Fund IV $3,000,000 Jan-07 $2,741,694 91.4 $258,306 $1,099,625 $2,192,157 $550,088 0.4 1.2 5.9

Newbury Secondary Fund $7,000,000 Aug-07 $6,090,000 87.0 $910,000 $2,580,317 $5,179,330 $1,669,647 0.4 1.3 10.4

Northgate IV $6,000,000 May-08 $4,302,000 71.7 $1,698,000 $260,021 $4,532,735 $490,756 0.1 1.1 5.9

Mercer PIP 2008 Private Equity Fund $6,000,000 Dec-08 $4,200,000 70.0 $1,800,000 $246,354 $4,329,723 $376,077 0.1 1.1 4.6

Total Private Real $27,000,000 $23,969,514 88.8 $3,030,487 $2,792,169 $16,650,956 -$4,526,388 0.1 0.8 -4.9

RREEF America REIT III $7,000,000 Jun-04 $7,000,000 100.0 - - $3,367,916 -$3,632,084 0.0 0.5 -11.6

Metropolitan Real Estate Equity Partners II $2,000,000 Jun-04 $1,924,000 96.2 $76,000 $1,061,196 $1,063,775 $200,971 0.6 1.1 2.9

Park Street Capital Natural Resources III Fd, L.P. $5,000,000 Oct-06 $4,387,500 87.8 $612,500 $789,019 $4,829,035 $1,230,554 0.2 1.3 7.8

BlackRock Diamond Property Fund $3,000,000 Apr-07 $3,000,000 100.0 - $656 $941,078 -$2,058,266 0.0 0.3 -22.3

Newlin Energy Fund II $7,000,000 Sep-07 $4,444,990 63.5 $2,555,010 $841,382 $4,803,952 $1,200,344 0.2 1.3 9.2

Colony Realty Partners II $3,000,000 Sep-07 $3,213,024 107.1 -$213,024 $99,916 $1,645,200 -$1,467,908 0.0 0.5 -13.3

-Market value reported one quarter in arrears, adjusted for current capital activity, unless otherwise noted. Valuations subject to availability. Performance may change as updates are processed.-Goldman Sachs Vintage Fund IVI: Valued as of 9/30/11 and adjusted for activity-This report contains information from manager supplied financial reports (audited or unaudited). Content is subject to change without notice. Information obtained from the manager isbelieved to be reliable; however, accuracy of the data is not guaranteed and has not been independently verified by Prime Buchholz.-Historical information provided by Mercer through 12/31/11-IRR = Calculated since inception-DPI Multiple = Distributions to paid in capital-TVPI Multiple = Total Value to paid in capital

Non-Marketable StrategiesNon-Marketable Investment Summary

As of May 31, 2012

Rollins College

MarketValue

% ofPortfolio 1 Mo. 3 Mo.

FiscalYTD

CalendarYTD 1 YR 3 YRS 5 YRS 10 YRS

ReturnSince

InceptionDate

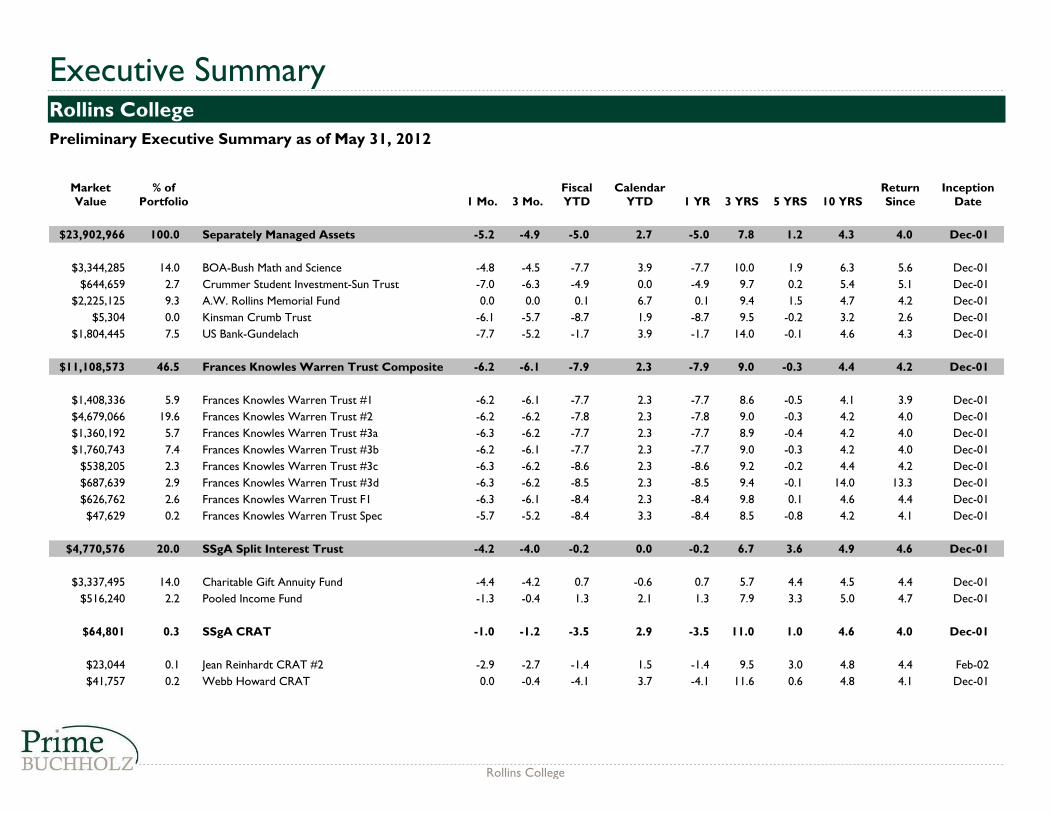

$23,902,966 100.0 Separately Managed Assets -5.2 -4.9 -5.0 2.7 -5.0 7.8 1.2 4.3 4.0 Dec-01

$3,344,285 14.0 BOA-Bush Math and Science -4.8 -4.5 -7.7 3.9 -7.7 10.0 1.9 6.3 5.6 Dec-01

$644,659 2.7 Crummer Student Investment-Sun Trust -7.0 -6.3 -4.9 0.0 -4.9 9.7 0.2 5.4 5.1 Dec-01

$2,225,125 9.3 A.W. Rollins Memorial Fund 0.0 0.0 0.1 6.7 0.1 9.4 1.5 4.7 4.2 Dec-01

$5,304 0.0 Kinsman Crumb Trust -6.1 -5.7 -8.7 1.9 -8.7 9.5 -0.2 3.2 2.6 Dec-01

$1,804,445 7.5 US Bank-Gundelach -7.7 -5.2 -1.7 3.9 -1.7 14.0 -0.1 4.6 4.3 Dec-01

$11,108,573 46.5 Frances Knowles Warren Trust Composite -6.2 -6.1 -7.9 2.3 -7.9 9.0 -0.3 4.4 4.2 Dec-01

$1,408,336 5.9 Frances Knowles Warren Trust #1 -6.2 -6.1 -7.7 2.3 -7.7 8.6 -0.5 4.1 3.9 Dec-01

$4,679,066 19.6 Frances Knowles Warren Trust #2 -6.2 -6.2 -7.8 2.3 -7.8 9.0 -0.3 4.2 4.0 Dec-01

$1,360,192 5.7 Frances Knowles Warren Trust #3a -6.3 -6.2 -7.7 2.3 -7.7 8.9 -0.4 4.2 4.0 Dec-01

$1,760,743 7.4 Frances Knowles Warren Trust #3b -6.2 -6.1 -7.7 2.3 -7.7 9.0 -0.3 4.2 4.0 Dec-01

$538,205 2.3 Frances Knowles Warren Trust #3c -6.3 -6.2 -8.6 2.3 -8.6 9.2 -0.2 4.4 4.2 Dec-01

$687,639 2.9 Frances Knowles Warren Trust #3d -6.3 -6.2 -8.5 2.3 -8.5 9.4 -0.1 14.0 13.3 Dec-01

$626,762 2.6 Frances Knowles Warren Trust F1 -6.3 -6.1 -8.4 2.3 -8.4 9.8 0.1 4.6 4.4 Dec-01

$47,629 0.2 Frances Knowles Warren Trust Spec -5.7 -5.2 -8.4 3.3 -8.4 8.5 -0.8 4.2 4.1 Dec-01

$4,770,576 20.0 SSgA Split Interest Trust -4.2 -4.0 -0.2 0.0 -0.2 6.7 3.6 4.9 4.6 Dec-01

$3,337,495 14.0 Charitable Gift Annuity Fund -4.4 -4.2 0.7 -0.6 0.7 5.7 4.4 4.5 4.4 Dec-01

$516,240 2.2 Pooled Income Fund -1.3 -0.4 1.3 2.1 1.3 7.9 3.3 5.0 4.7 Dec-01

$64,801 0.3 SSgA CRAT -1.0 -1.2 -3.5 2.9 -3.5 11.0 1.0 4.6 4.0 Dec-01

$23,044 0.1 Jean Reinhardt CRAT #2 -2.9 -2.7 -1.4 1.5 -1.4 9.5 3.0 4.8 4.4 Feb-02

$41,757 0.2 Webb Howard CRAT 0.0 -0.4 -4.1 3.7 -4.1 11.6 0.6 4.8 4.1 Dec-01

Executive SummaryRollins College

Preliminary Executive Summary as of May 31, 2012

Rollins College

Executive SummaryRollins College

Preliminary Executive Summary as of May 31, 2012

MarketValue

% ofPortfolio 1 Mo. 3 Mo.

FiscalYTD

CalendarYTD 1 YR 3 YRS 5 YRS 10 YRS

ReturnSince

InceptionDate

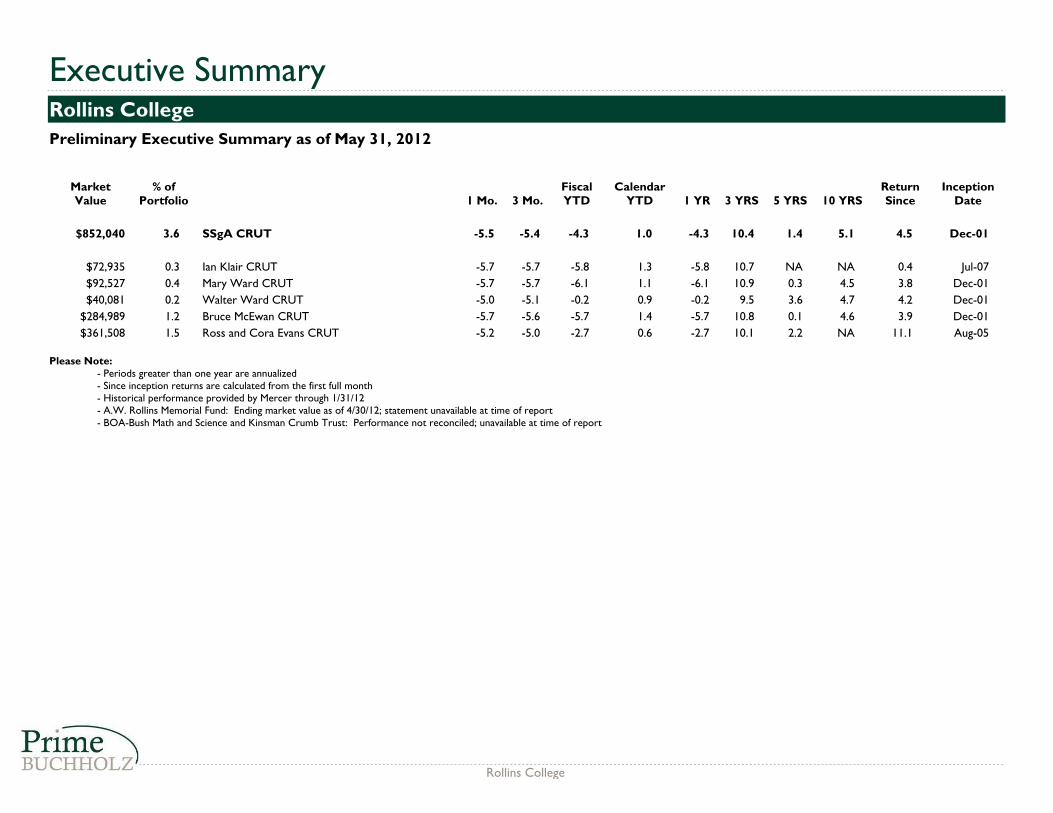

$852,040 3.6 SSgA CRUT -5.5 -5.4 -4.3 1.0 -4.3 10.4 1.4 5.1 4.5 Dec-01

$72,935 0.3 Ian Klair CRUT -5.7 -5.7 -5.8 1.3 -5.8 10.7 NA NA 0.4 Jul-07

$92,527 0.4 Mary Ward CRUT -5.7 -5.7 -6.1 1.1 -6.1 10.9 0.3 4.5 3.8 Dec-01

$40,081 0.2 Walter Ward CRUT -5.0 -5.1 -0.2 0.9 -0.2 9.5 3.6 4.7 4.2 Dec-01

$284,989 1.2 Bruce McEwan CRUT -5.7 -5.6 -5.7 1.4 -5.7 10.8 0.1 4.6 3.9 Dec-01

$361,508 1.5 Ross and Cora Evans CRUT -5.2 -5.0 -2.7 0.6 -2.7 10.1 2.2 NA 11.1 Aug-05

Please Note:- Periods greater than one year are annualized- Since inception returns are calculated from the first full month- Historical performance provided by Mercer through 1/31/12- A.W. Rollins Memorial Fund: Ending market value as of 4/30/12; statement unavailable at time of report- BOA-Bush Math and Science and Kinsman Crumb Trust: Performance not reconciled; unavailable at time of report

Rollins College

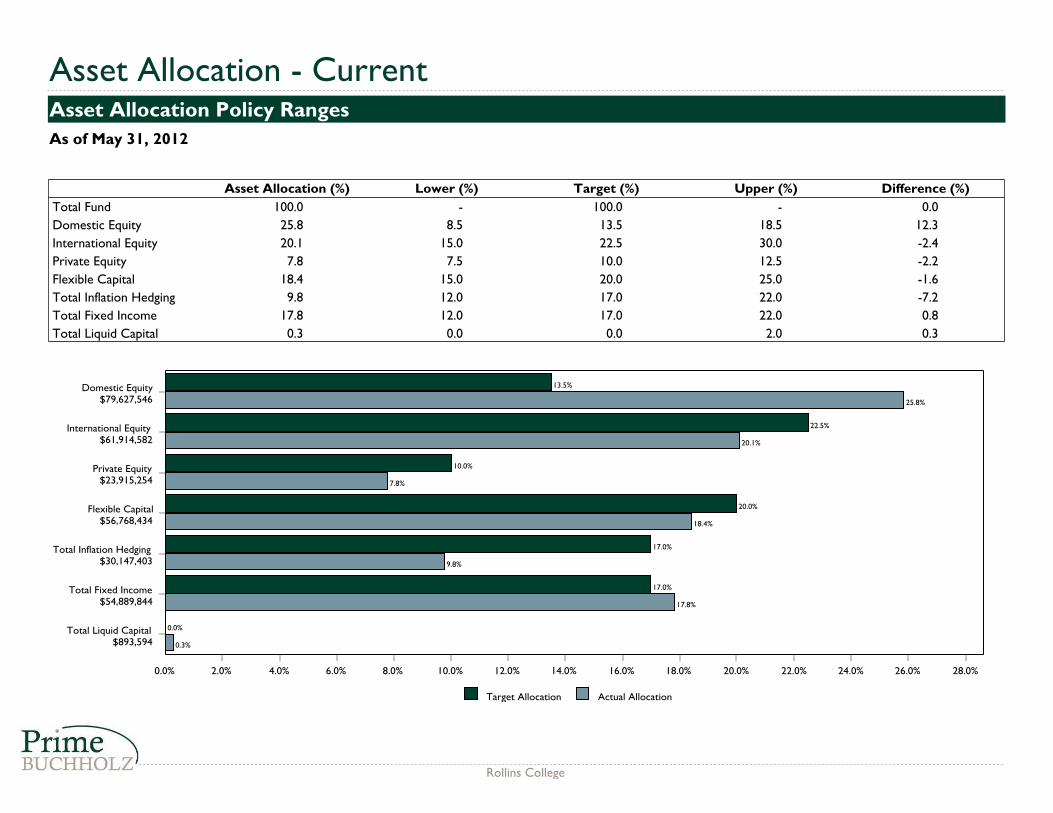

Asset Allocation (%) Lower (%) Target (%) Upper (%) Difference (%)

Total Fund 100.0 - 100.0 - 0.0

Domestic Equity 25.8 8.5 13.5 18.5 12.3

International Equity 20.1 15.0 22.5 30.0 -2.4

Private Equity 7.8 7.5 10.0 12.5 -2.2

Flexible Capital 18.4 15.0 20.0 25.0 -1.6

Total Inflation Hedging 9.8 12.0 17.0 22.0 -7.2

Total Fixed Income 17.8 12.0 17.0 22.0 0.8

Total Liquid Capital 0.3 0.0 0.0 2.0 0.3

Target Allocation Actual Allocation

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0% 18.0% 20.0% 22.0% 24.0% 26.0% 28.0%

Total Liquid Capital$893,594

Total Fixed Income$54,889,844

Total Inflation Hedging$30,147,403

Flexible Capital$56,768,434

Private Equity$23,915,254

International Equity$61,914,582

Domestic Equity$79,627,546

0.0%

17.0%

17.0%

20.0%

10.0%

22.5%

13.5%

0.3%

17.8%

9.8%

18.4%

7.8%

20.1%

25.8%

Asset Allocation - CurrentAsset Allocation Policy Ranges

As of May 31, 2012

Rollins College