Embed Size (px)

Citation preview

Modern Retail in Italy | Main features and latest trends Workshop Scanner Data - Rome, 1 October 2015

Hélène HotellierResponsabile Ufficio studi e Affari europeiFederdistribuzione per [email protected]

ADM represents the Modern Retail sector in dealing with the agro-food / Fast Moving Consumer Goods industry. ADM aims at the improvement of the supply chain, boosting and promoting efficiency in relations between operators.

Members of ADM are the three main representative trade associations of the large Modern Retail sector - Federdistribuzione, ANCC-Coop, ANCD-Conad - and about 800 retail companies operating in Italy.

ADM is a forum where the main retail industry associations can discuss to identify possible common paths on institutional issues.

Fe

de

rdis

trib

uzi

on

e p

er A

DM

2

Fe

de

rdis

trib

uzi

on

e p

er A

DM

1. Focus on Italy | Macroeconomic context and forecasts

2. Focus on Italy| Household consumption model: structural trends & impact of the crisis

3. Modern Retail in Italy | Main features, comparison with European countries and latest trends

4. Modern Retail in Italy | New challenges

3

Fe

de

rdis

trib

uzi

on

e p

er A

DM

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.05.4

3.9

1.7 1.8 1.7

2.5 2.7 2.5 2.72.2

1.9 2.11.8

3.3

0.8

1.5

2.8 3.0

1.2

0.2

2.9

1.1

2.0 1.8 1.6

2.9

1.9

0.50.0

1.7

0.9

2.21.7

-1.2

-5.5

1.7

0.6

-2.4-1.9

-0.4

2.2

0.8

3.22.9

2.3

3.3

1.1

0.2

1.00.7 0.6

1.5 1.4

-0.8

-1.6

1.5

-0.3

-4.0

-2.6

0.3

Consumer prices GDP Consumption

1. Focus on Italy | GDP, Households consumption, Consumer prices

Source: Istat 4

Fe

de

rdis

trib

uzi

on

e p

er A

DM

1. Focus on Italy | Macroeconomics forecasts

2014 2015 2016GDP (real terms)

-0,4 +0,9 +1,6

Household consumption(real terms)

+0,3 +0,8 +1,5

Unemployment rate(%)

12,7 12,3 11,9

Consumer prices(% Var.)

+0,2 +0,3 +1,0

Deficit(Deficit/GDP)

-3,0 -2,6 -2,2

Public debt(Public debt/GDP)

132,1 132,8 131,4

Source: DEF Italian Government (18 september 2015)5

Fe

de

rdis

trib

uzi

on

e p

er A

DM

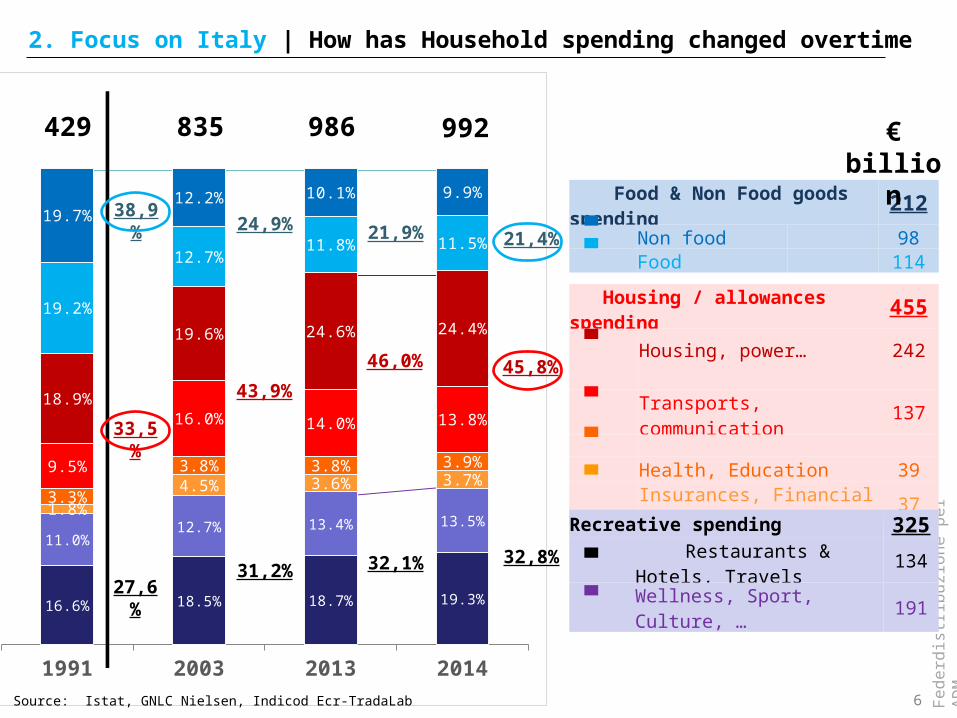

1991 2003 2013 2014

16.6% 18.5% 18.7% 19.3%

11.0%12.7% 13.4% 13.5%

1.8%

4.5% 3.6% 3.7%3.3%

3.8% 3.8% 3.9%9.5%

16.0% 14.0% 13.8%18.9%

19.6% 24.6% 24.4%19.2%

12.7%11.8% 11.5%

19.7%12.2% 10.1% 9.9%

Source: Istat, GNLC Nielsen, Indicod Ecr-TradaLab

Food & Non Food goods spending 212 Non food 98 Food 114

Housing / allowances spending 455

Housing, power… 242

Transports, communication 137 Health, Education 39

Insurances, Financial services 37

Recreative spending 325 Restaurants & Hotels, Travels 134

Wellness, Sport, Culture, … 191

€ billion429 835 992986

38,9%24,9% 21,9% 21,4%

33,5%

43,9%

46,0% 45,8%

27,6%31,2% 32,1% 32,8%

2. Focus on Italy | How has Household spending changed overtime

6

Fe

de

rdis

trib

uzi

on

e p

er A

DM

- 8,0% = € 79,9 bn

- 6,4% = € 63,4 bn

Household consumption

2. Focus on Italy | Household Consumption hit by a 2-phase crisis

Source: TradeLab on Istat data 7

Fe

de

rdis

trib

uzi

on

e p

er A

DM

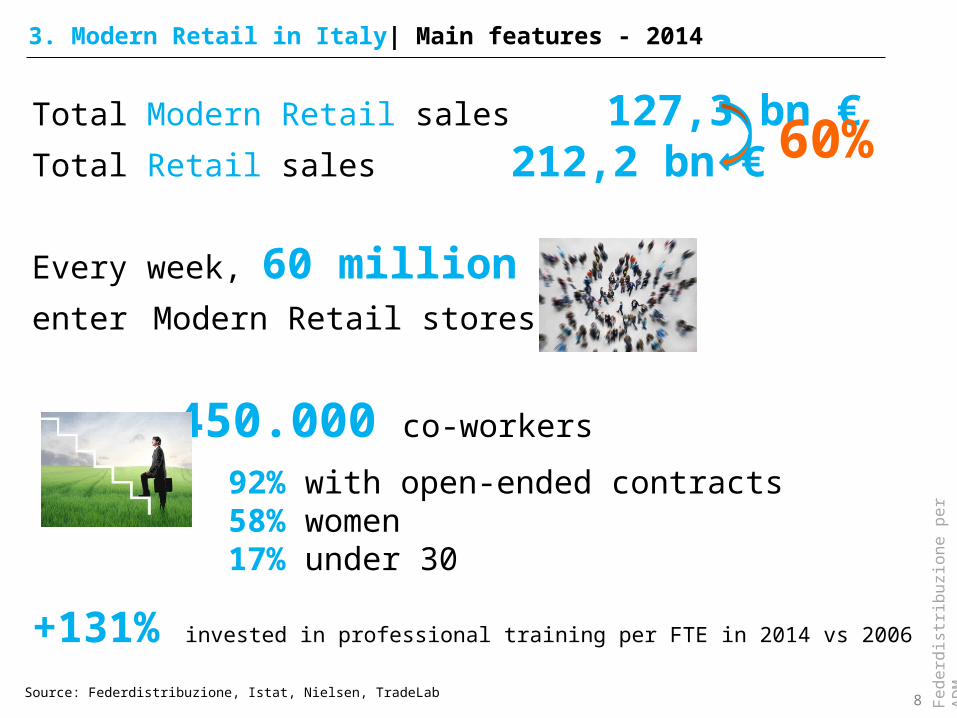

Total Modern Retail sales 127,3 bn € Total Retail sales 212,2 bn €

Every week, 60 million people enter Modern Retail stores

450.000 co-workers

+131% invested in professional training per FTE in 2014 vs 2006

Source: Federdistribuzione, Istat, Nielsen, TradeLab

92% with open-ended contracts58% women17% under 30

3. Modern Retail in Italy| Main features - 2014

60%

8

Fe

de

rdis

trib

uzi

on

e p

er A

DM

• Incl. Cash & CarrySource: AC Nielsen, Istat, Indicod Ecr - TradeLab

2000 2011 2012 2013 2014

11.9 12.5 12.6 12.7 12.8

42.129.8 28.7 27.9 27.2

46.157.7 58.7 59.4 60

Modern Retail

Traditional small shops

Market stalls, e-commerce, …

198,5 215,4220,4 € billion212,2226,3

58.159* stores

696.886 stores

188.274 stores

3. Modern Retail in Italy | Retail formats % market shares - Total retail sales

9

Fe

de

rdis

trib

uzi

on

e p

er A

DM

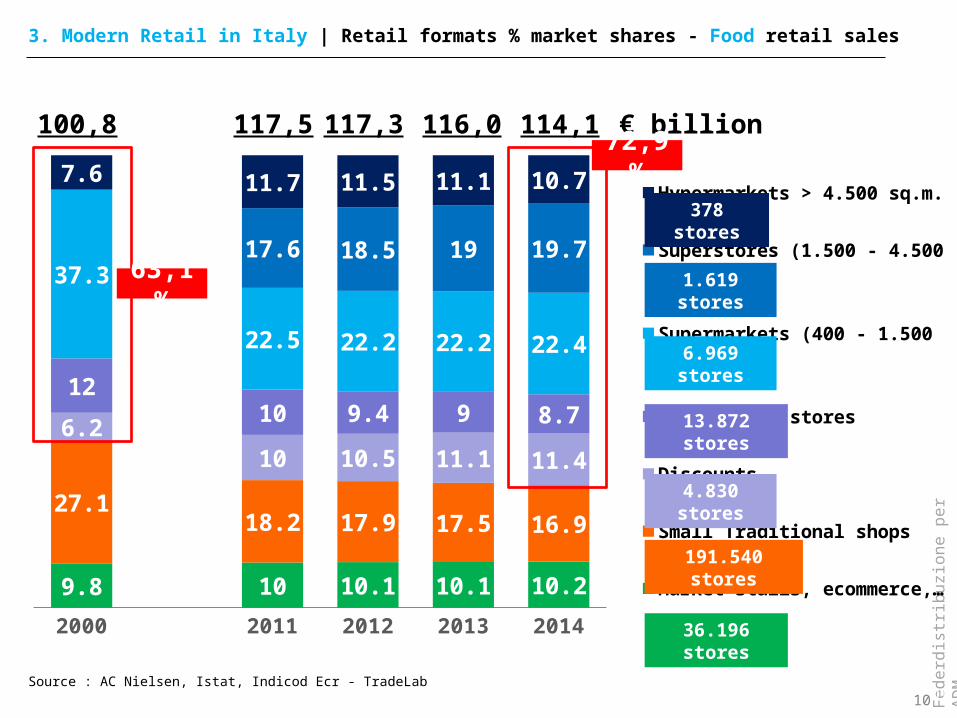

2000 2011 2012 2013 2014

9.8 10 10.1 10.1 10.2

27.118.2 17.9 17.5 16.9

6.210 10.5 11.1 11.4

1210 9.4 9 8.7

37.3

22.5 22.2 22.2 22.4

7.6 11.7 11.5 11.1 10.7

17.6 18.5 19 19.7

Hypermarkets > 4.500 sq.m.

Superstores (1.500 - 4.500 sq.m.)

Supermarkets (400 - 1.500 sq.m.)

Convenience stores

Discounts

Small Traditional shops

Market stalls, ecommerce,…

10

100,8 117,3 € billion116,0117,5

Source : AC Nielsen, Istat, Indicod Ecr - TradeLab

114,1

378 stores

6.969 stores

13.872 stores

4.830 stores

191.540 stores

36.196 stores

1.619 stores

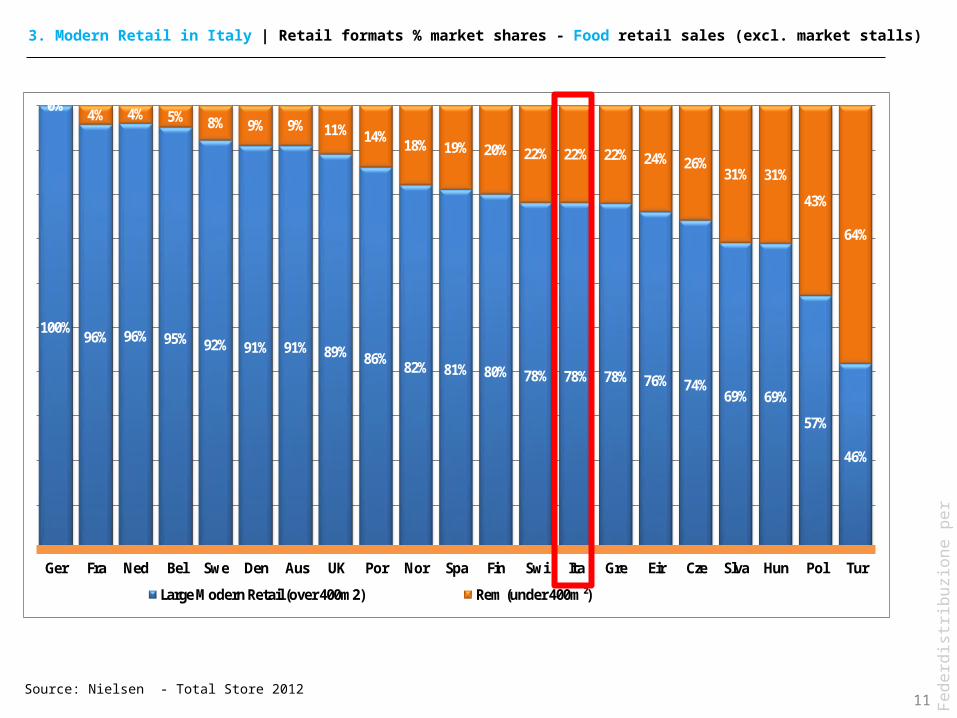

3. Modern Retail in Italy | Retail formats % market shares - Food retail sales

63,1%

72,9%

10

Fe

de

rdis

trib

uzi

on

e p

er A

DM

100%96% 96% 95% 92% 91% 91% 89% 86% 82% 81% 80% 78% 78% 78% 76% 74%

69% 69%

57%

46%

0%4% 4% 5% 8% 9% 9% 11% 14% 18% 19% 20% 22% 22% 22% 24% 26%

31% 31%

43%

64%

Ger Fra Ned Bel Swe Den Aus UK Por Nor Spa Fin Swi Ita Gre Eir Cze Slva Hun Pol Tur

Large Modern Retail (over 400m2) Rem (under 400m²)

Source: Nielsen - Total Store 2012

3. Modern Retail in Italy | Retail formats % market shares - Food retail sales (excl. market stalls)

11

Fe

de

rdis

trib

uzi

on

e p

er A

DM

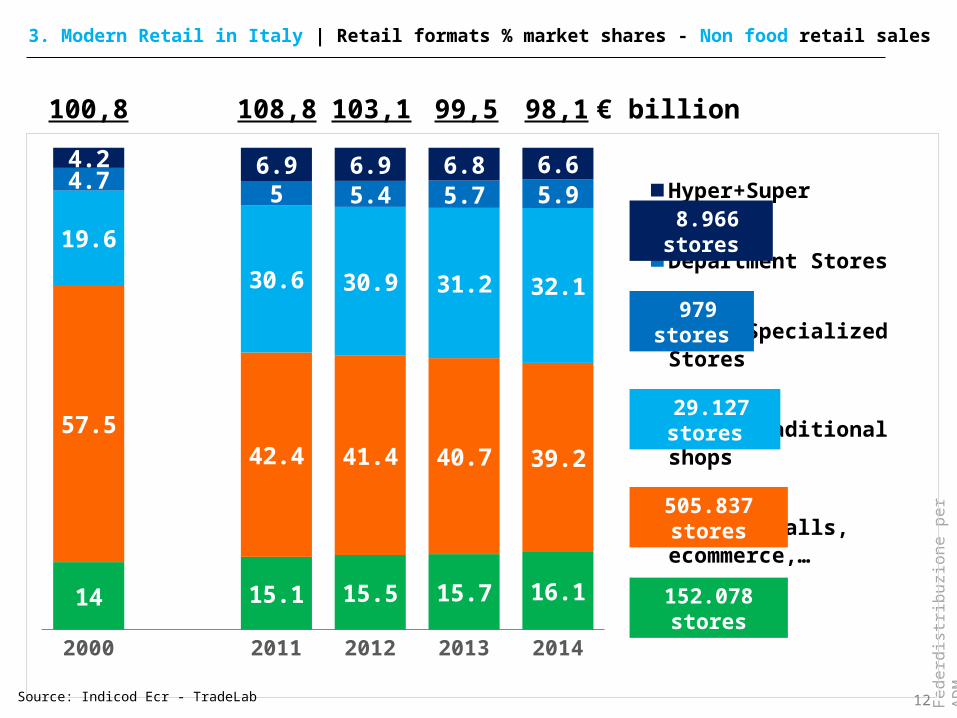

2000 2011 2012 2013 2014

14 15.1 15.5 15.7 16.1

57.542.4 41.4 40.7 39.2

19.6

30.6 30.9 31.2 32.1

4.7 5 5.4 5.7 5.94.2 6.9 6.9 6.8 6.6

Hyper+Super

Department Stores

Large Specialized Stores

Small Traditional shops

Market stalls, ecommerce,…

12

100,8 103,1 € billion99,5108,8 98,1

Source: Indicod Ecr - TradeLab

505.837 stores

152.078 stores

8.966 stores

979 stores

29.127 stores

3. Modern Retail in Italy | Retail formats % market shares - Non food retail sales

12

Fe

de

rdis

trib

uzi

on

e p

er A

DM

13• Incl. Cash & CarrySource: Osservatorio del commercio (MISE) - Nielsen

2010 2014 % Var.2014 vs. 2010 Var.

Retail stores 776.365 755.045 -2,75 -21.320

Modern Retail 59.508* 58.159* -2,27 -1.349

Small traditional shops 716.857 696.886 -2,79 -19.971

Market stalls 170.845 188.274 10,20 17.429

Total stores 947.210 943.319 -0,41 -3.891

3. Modern Retail in Italy | Number of stores by retail formats (1)

13

Fe

de

rdis

trib

uzi

on

e p

er A

DM

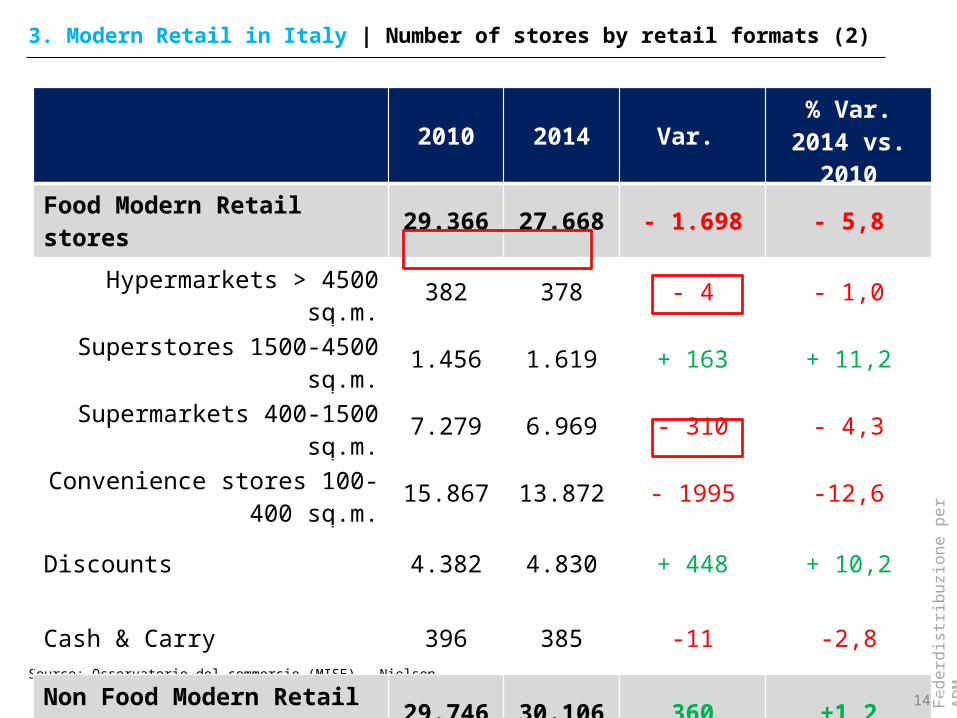

14Source: Osservatorio del commercio (MISE) - Nielsen

2010 2014 Var. % Var.2014 vs. 2010

Food Modern Retail stores 29.366 27.668 - 1.698 - 5,8

Hypermarkets > 4500 sq.m. 382 378 - 4 - 1,0

Superstores 1500-4500 sq.m. 1.456 1.619 + 163 + 11,2

Supermarkets 400-1500 sq.m. 7.279 6.969 - 310 - 4,3

Convenience stores 100-400 sq.m. 15.867 13.872 - 1995 -12,6

Discounts 4.382 4.830 + 448 + 10,2

Cash & Carry 396 385 -11 -2,8

Non Food Modern Retail stores 29.746 30.106 360 +1,2

3. Modern Retail in Italy | Number of stores by retail formats (2)

14

Fe

de

rdis

trib

uzi

on

e p

er A

DM

3. Modern Retail in Italy | Total sales surface - Grocery market

% Var. new sq.m.sq.m. (‘000)

Source: Nielsen GNLC - January ed.15

Fe

de

rdis

trib

uzi

on

e p

er A

DM

Source: AC Nielsen - January 2015

Finiper

Gruppo Pam

Sigma

Eurospin

Gruppo Carrefour

Gruppo Auchan

Esselunga

Selex

Conad

Coop Italia

2.8

3.1

3.4

4.9

6.2

7.2

8.7

9.4

11.7

15

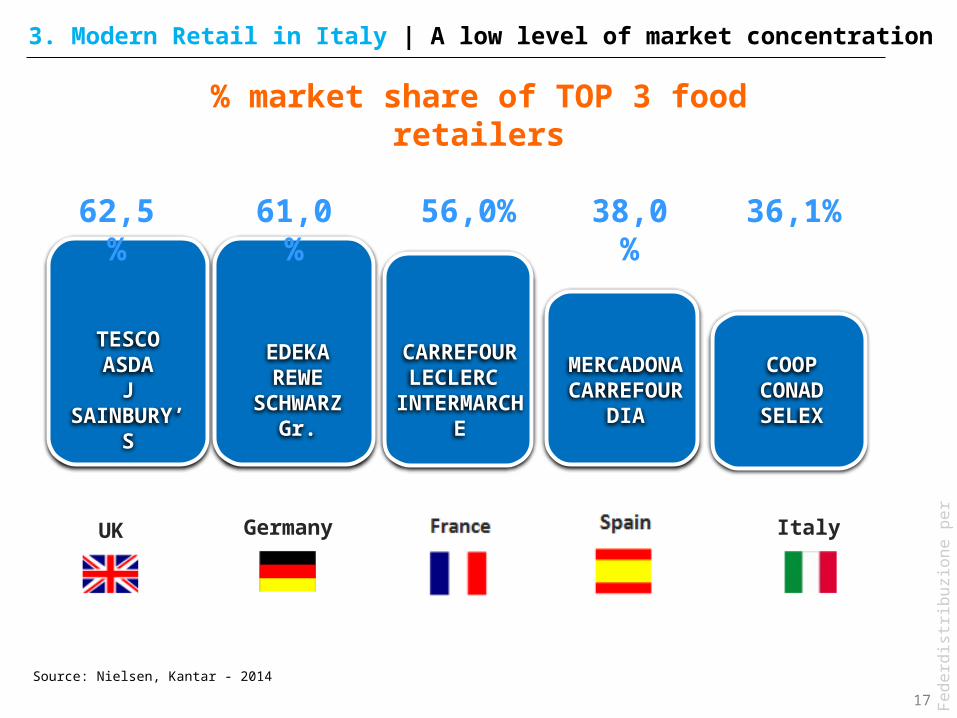

3. Modern Retail in Italy| Top 10 food retailers: % market shares

16

Fe

de

rdis

trib

uzi

on

e p

er A

DMTESCO

ASDA

SAINBURY’S

EDEKA

REWE

ALDI

CARREFOUR

LECLERC

CASINO

COOP

CONAD

SELEX

Source: Nielsen, Kantar - 2014

TESCOASDA

J SAINBURY’S

EDEKAREWE

SCHWARZ Gr.

MERCADONA CARREFOUR

DIA

CARREFOUR LECLERC

INTERMARCHE

COOPCONADSELEX

62,5% 61,0% 38,0%56,0% 36,1%

UK Germany Spain France Italy

3. Modern Retail in Italy | A low level of market concentration

% market share of TOP 3 food retailers

17

Fe

de

rdis

trib

uzi

on

e p

er A

DM

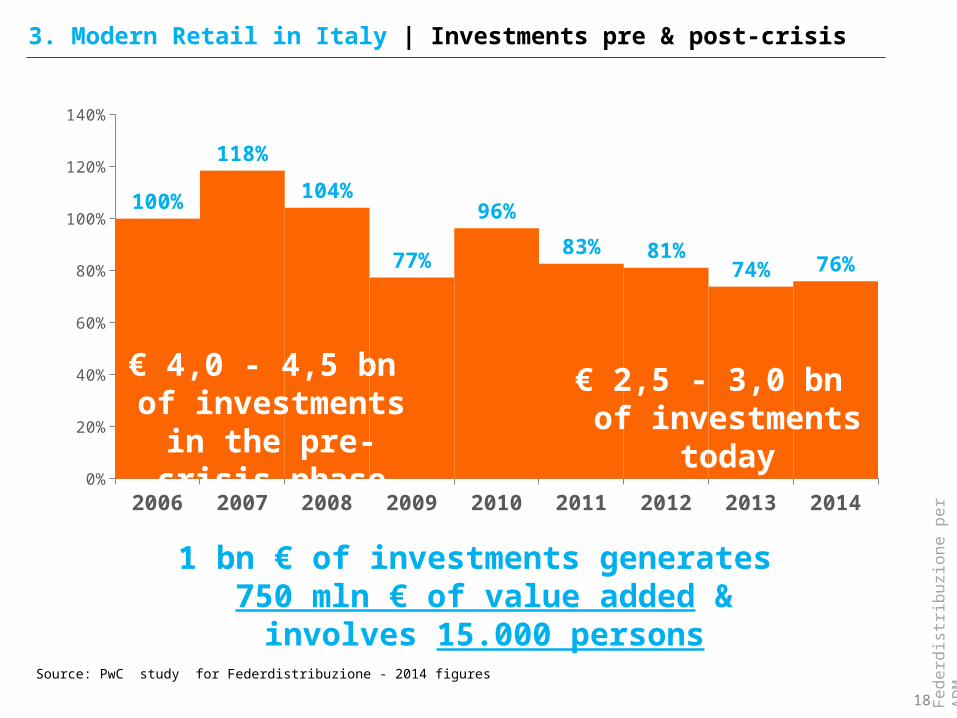

1 bn € of investments generates 750 mln € of value added &

involves 15.000 persons

2006 2007 2008 2009 2010 2011 2012 2013 20140%

20%

40%

60%

80%

100%

120%

140%

100%

118%

104%

77%

96%

83% 81%74% 76%

€ 4,0 - 4,5 bn of investments in the

pre-crisis phase

€ 2,5 - 3,0 bn of investments today

3. Modern Retail in Italy | Investments pre & post-crisis

Source: PwC study for Federdistribuzione - 2014 figures

18

Fe

de

rdis

trib

uzi

on

e p

er A

DM

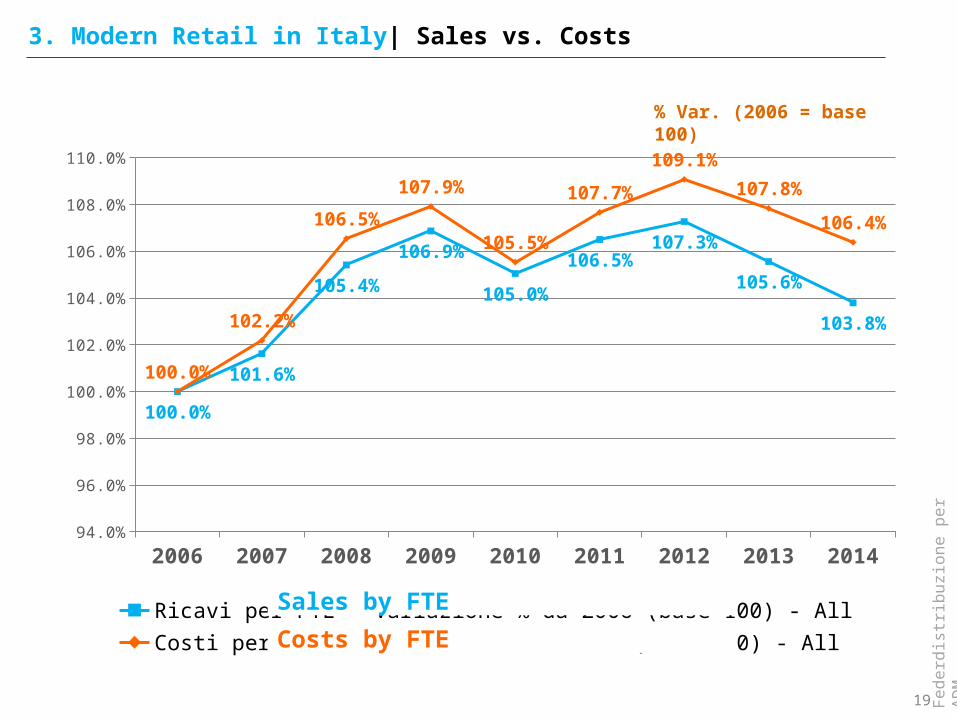

% Var. (2006 = base 100)

2006 2007 2008 2009 2010 2011 2012 2013 201494.0%

96.0%

98.0%

100.0%

102.0%

104.0%

106.0%

108.0%

110.0%

100.0%

101.6%

105.4%

106.9%

105.0%

106.5%107.3%

105.6%

103.8%

100.0%

102.2%

106.5%

107.9%

105.5%

107.7%

109.1%

107.8%

106.4%

Ricavi per FTE - Variazione % da 2006 (base 100) - AllCosti per FTE - Variazione % da 2006 (base 100) - All

3. Modern Retail in Italy| Sales vs. Costs

Sales by FTE

Costs by FTE

19

Fe

de

rdis

trib

uzi

on

e p

er A

DM

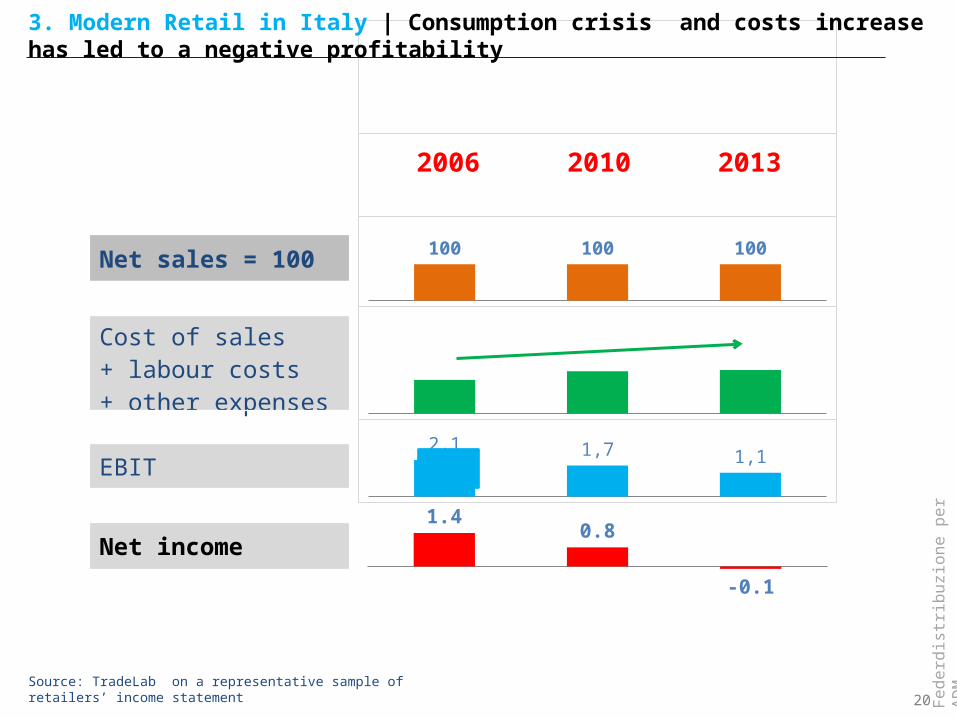

2,1 1,7 1,1

100 100 100

Source: TradeLab on a representative sample of retailers’ income statement

Net sales = 100

Cost of sales+ labour costs+ other expenses

EBIT

Net income

20102006 2013

1.40.8

-0.1

3. Modern Retail in Italy | Consumption crisis and costs increase has led to a negative profitability

20

Fe

de

rdis

trib

uzi

on

e p

er A

DM

RETAILERS Market shares (%)

Retailers with National capital 80,3%

Retailers with Foreign capital 19,7%Auchan (FR) 7,2 %

Carrefour (FR) 6,2 %

Lidl (DE) 2,6 %

Despar (Aspiag - AT) 2,2 %

Penny Market (DE) 1,5 %

Metro (Cash & Carry - DE) not taken into account (wholesale format)

3. Modern Retail in Italy| National vs. Foreign-capital retailers

Source: Nielsen 21

Fe

de

rdis

trib

uzi

on

e p

er A

DM

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 20140

5

10

15

20

25

30

35

17.118.4

19.620.9 21.6 22.5 23.2 23.1 22.4 22.7

24.325.6 26.4 27.4

28.7 29.3

8.47.4 7.9

8.9 9.2 9.6 10.3 10.4 10 10 10.9 11.7 12.2 12.4 12.9 13.4

Share of Price promotion on total sales (%) % ref. with price promotion

Source: Nielsen Trade*Mis - Hyper+Super+LS

3. Modern Retail in Italy| Priority to price convenience to sustain purchasing power

22

Fe

de

rdis

trib

uzi

on

e p

er A

DM

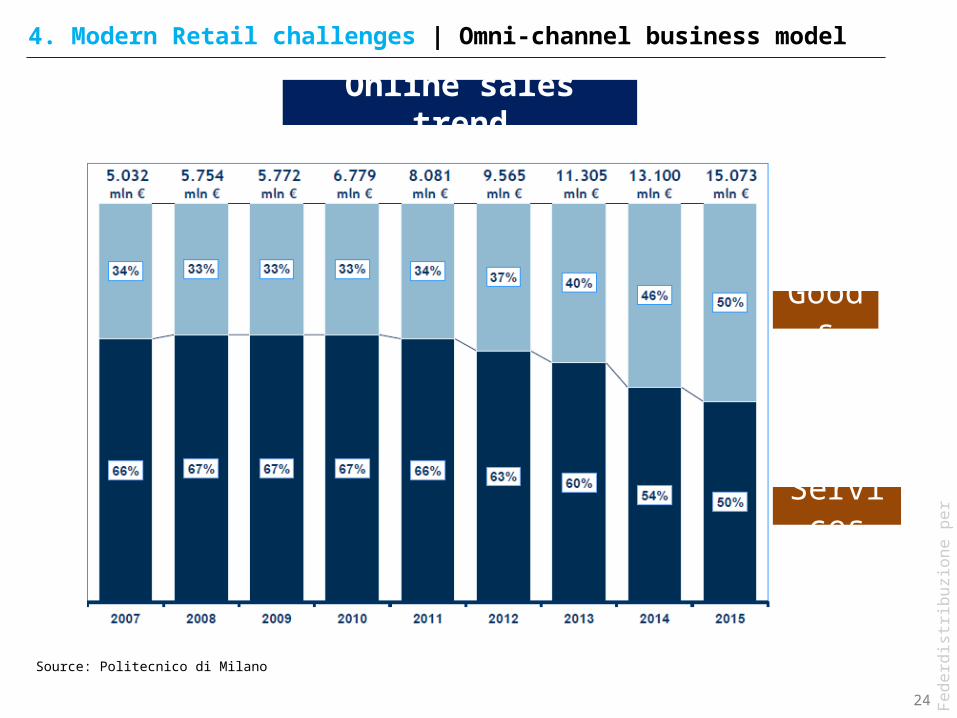

4. Modern Retail challenges | Omni-channel business model

Online sales trend

Source: Politecnico di Milano

23

Fe

de

rdis

trib

uzi

on

e p

er A

DM

Goods

Services

4. Modern Retail challenges | Omni-channel business model

Source: Politecnico di Milano

Online sales trend

24