Embed Size (px)

Citation preview

MiFID II seminar

Hannah Meakin (Partner)Floortje Nagelkerke (Senior Associate)

17 April 2014

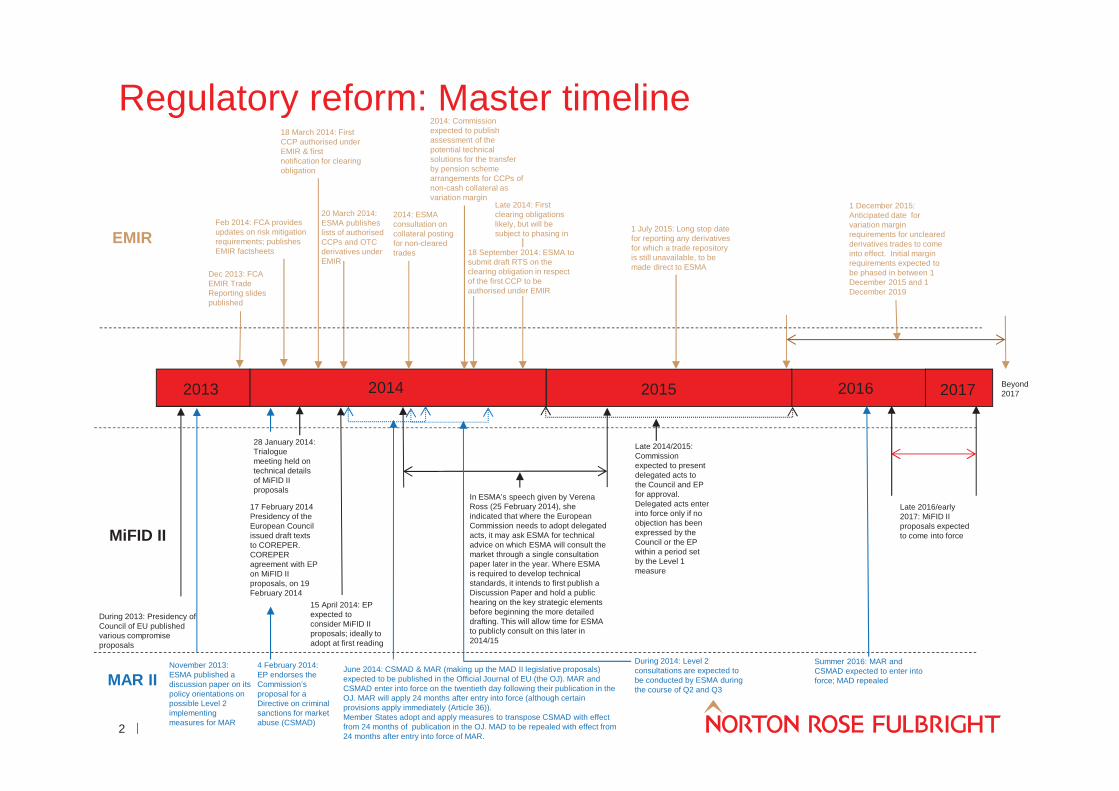

Regulatory reform: Master timeline

During 2013: Presidency ofCouncil of EU publishedvarious compromiseproposals

EMIR

MiFID II

2013 2014 2015 2016

15 April 2014: EPexpected toconsider MiFID IIproposals; ideally toadopt at first reading

2017

Late 2016/early2017: MiFID IIproposals expectedto come into force

In ESMA’s speech given by VerenaRoss (25 February 2014), sheindicated that where the EuropeanCommission needs to adopt delegatedacts, it may ask ESMA for technicaladvice on which ESMA will consult themarket through a single consultationpaper later in the year. Where ESMAis required to develop technicalstandards, it intends to first publish aDiscussion Paper and hold a publichearing on the key strategic elementsbefore beginning the more detaileddrafting. This will allow time for ESMAto publicly consult on this later in2014/15

28 January 2014:Trialoguemeeting held ontechnical detailsof MiFID IIproposals

17 February 2014Presidency of theEuropean Councilissued draft textsto COREPER.COREPERagreement with EPon MiFID IIproposals, on 19February 2014

18 March 2014: FirstCCP authorised underEMIR & firstnotification for clearingobligation

1 December 2015:Anticipated date forvariation marginrequirements for unclearedderivatives trades to comeinto effect. Initial marginrequirements expected tobe phased in between 1December 2015 and 1December 2019

2014: ESMAconsultation oncollateral postingfor non-clearedtrades

2014: Commissionexpected to publishassessment of thepotential technicalsolutions for the transferby pension schemearrangements for CCPs ofnon-cash collateral asvariation margin

1 July 2015: Long stop datefor reporting any derivativesfor which a trade repositoryis still unavailable, to bemade direct to ESMA

20 March 2014:ESMA publisheslists of authorisedCCPs and OTCderivatives underEMIR

Feb 2014: FCA providesupdates on risk mitigationrequirements; publishesEMIR factsheets

Dec 2013: FCAEMIR TradeReporting slidespublished

MAR II

18 September 2014: ESMA tosubmit draft RTS on theclearing obligation in respectof the first CCP to beauthorised under EMIR

4 February 2014:EP endorses theCommission’sproposal for aDirective on criminalsanctions for marketabuse (CSMAD)

During 2014: Level 2consultations are expected tobe conducted by ESMA duringthe course of Q2 and Q3

November 2013:ESMA published adiscussion paper on itspolicy orientations onpossible Level 2implementingmeasures for MAR

Beyond2017

June 2014: CSMAD & MAR (making up the MAD II legislative proposals)expected to be published in the Official Journal of EU (the OJ). MAR andCSMAD enter into force on the twentieth day following their publication in theOJ. MAR will apply 24 months after entry into force (although certainprovisions apply immediately (Article 36)).Member States adopt and apply measures to transpose CSMAD with effectfrom 24 months of publication in the OJ. MAD to be repealed with effect from24 months after entry into force of MAR.

Summer 2016: MAR andCSMAD expected to enter intoforce; MAD repealed

Late 2014/2015:Commissionexpected to presentdelegated acts tothe Council and EPfor approval.Delegated acts enterinto force only if noobjection has beenexpressed by theCouncil or the EPwithin a period setby the Level 1measure

Late 2014: Firstclearing obligationslikely, but will besubject to phasing in

2

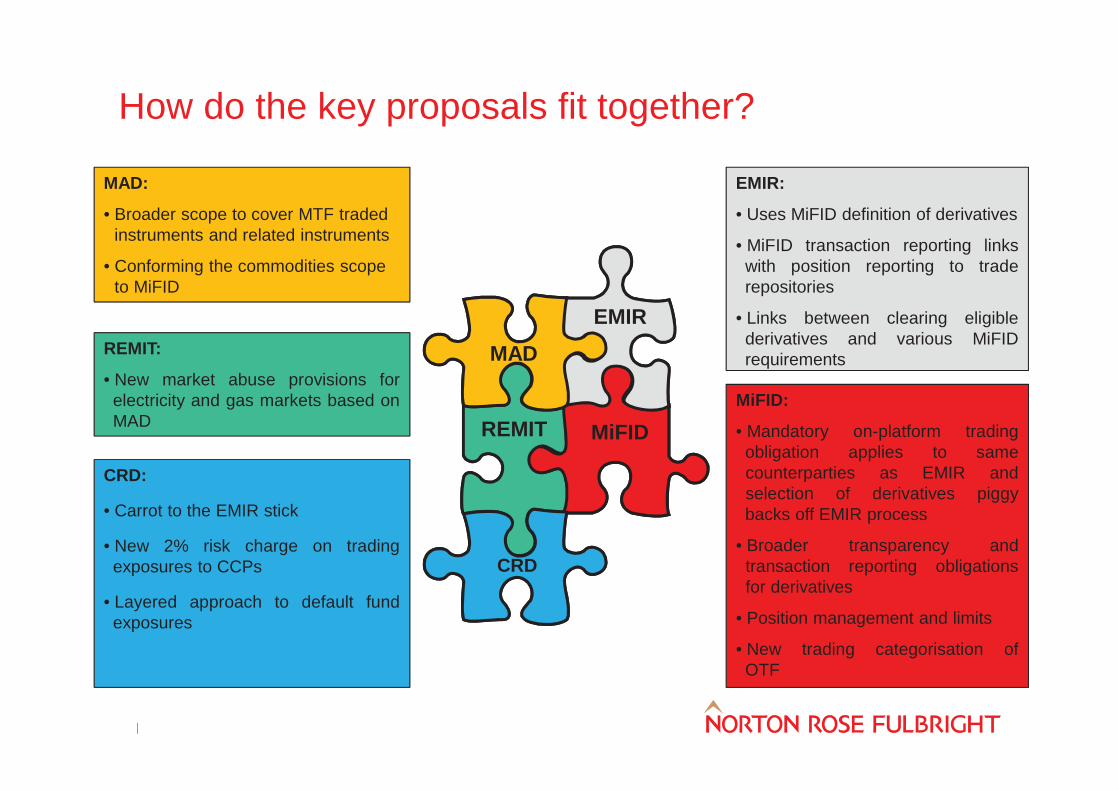

How do the key proposals fit together?

MAD:

• Broader scope to cover MTF tradedinstruments and related instruments

• Conforming the commodities scopeto MiFID

REMIT:

• New market abuse provisions forelectricity and gas markets based onMAD

EMIR:

• Uses MiFID definition of derivatives

• MiFID transaction reporting linkswith position reporting to traderepositories

• Links between clearing eligiblederivatives and various MiFIDrequirements

MiFID:

• Mandatory on-platform tradingobligation applies to samecounterparties as EMIR andselection of derivatives piggybacks off EMIR process

• Broader transparency andtransaction reporting obligationsfor derivatives

• Position management and limits

• New trading categorisation ofOTF

CRD:

• Carrot to the EMIR stick

• New 2% risk charge on tradingexposures to CCPs

• Layered approach to default fundexposures

REMIT

EMIRMAD

MiFID

CRDCRD

REMIT

EMIRMAD

MiFID

CRD

MiFID II: Macro themes in your MiFID II project

Macro theme 1: Strategicimplications – group

reorganisation necessarydue to changes in

exemptions and thirdcountry requirements?

Macro theme 2: Conduct ofbusiness – many small

amendments which add upto significant changes

including amendments toterms of business

Macro theme 3: Dealingeffectively with the newmarkets requirements –

OFTs, algorithmic trading,position limits, increased

transparency etc

Macro theme 4: Creatinga project team – we move

onto detailed Level 2measures shortly and thekey question is how you

keep track of the mass ofpaper

4

5

The big four themes of post-crisis EU regulation• Theme 1: a much “thicker” EU legal framework

• Links to the issue of a single EU conduct of business (COB) sourcebook and thecommon standards debate

• Use of Regulations and regulatory technical standards• A tale of two stories as shown in a series of Level 2 powers in the conduct of

business arena and in fundamental change in markets regulation: micro versusmacro change but cumulative micro costs may be large

• This theme is evident when considering the impact of the new regulation ontrading venues, market and information infrastructure

• Theme 2: post-crisis reaction• The banking crisis and regaining trust are at the core of regulatory thinking• Reflects change in political consensus away from free market thinking and

towards some protections even for ECPs and professional clients• Product regulation, position limits and the requirement for mandatory trading are

good examples of this

6

The big four themes of post-crisis EU regulation• Theme 3: keeping up with technology

• One of the reasons for MiFID II is that the markets have moved on and the EUinstitutions do not want this to happen again

• Globally and across all markets, economic pressures and competition arepushing businesses to find the most effective ways to invest and hedge risks

• The desire to keep up with technology is reflected in the way high frequency andalgorithmic trading will be treated

• Trading venues have adapted to the speed and automation of today’s markets bydeploying sophisticated risk mitigation and surveillance technology, and arecontinuing to innovate in these areas to further enhance the safety, stability andintegrity of the markets

• Theme 4: the EU versus world problem• Belief that Europe is strongest if it negotiates together but great tensions between

institutions• Concerns on free rider issues with firms based in the rest of the world and need

for level playing field• These motivations explain the treatment by the EU of third country firms seeking

access to the EU

The markets dimension of MiFID II

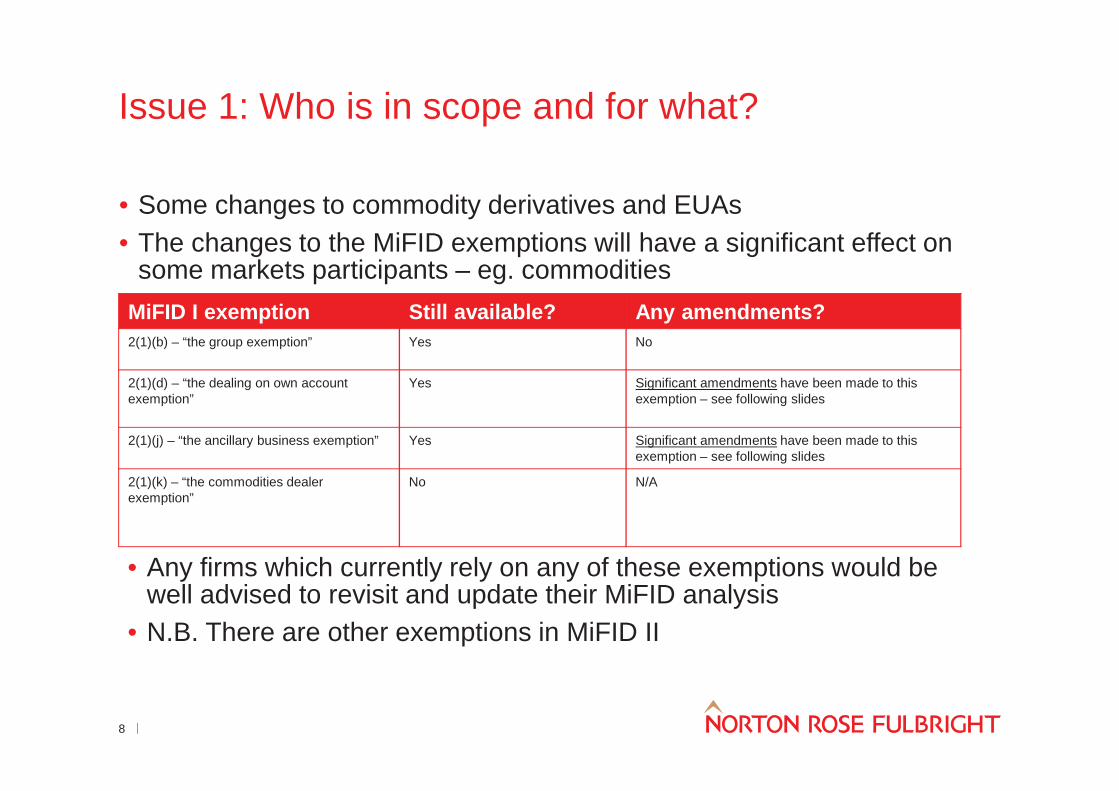

Issue 1: Who is in scope and for what?

• Some changes to commodity derivatives and EUAs• The changes to the MiFID exemptions will have a significant effect on

some markets participants – eg. commoditiesMiFID I exemption Still available? Any amendments?2(1)(b) – “the group exemption” Yes No

2(1)(d) – “the dealing on own accountexemption”

Yes Significant amendments have been made to thisexemption – see following slides

2(1)(j) – “the ancillary business exemption” Yes Significant amendments have been made to thisexemption – see following slides

2(1)(k) – “the commodities dealerexemption”

No N/A

8

• Any firms which currently rely on any of these exemptions would bewell advised to revisit and update their MiFID analysis

• N.B. There are other exemptions in MiFID II

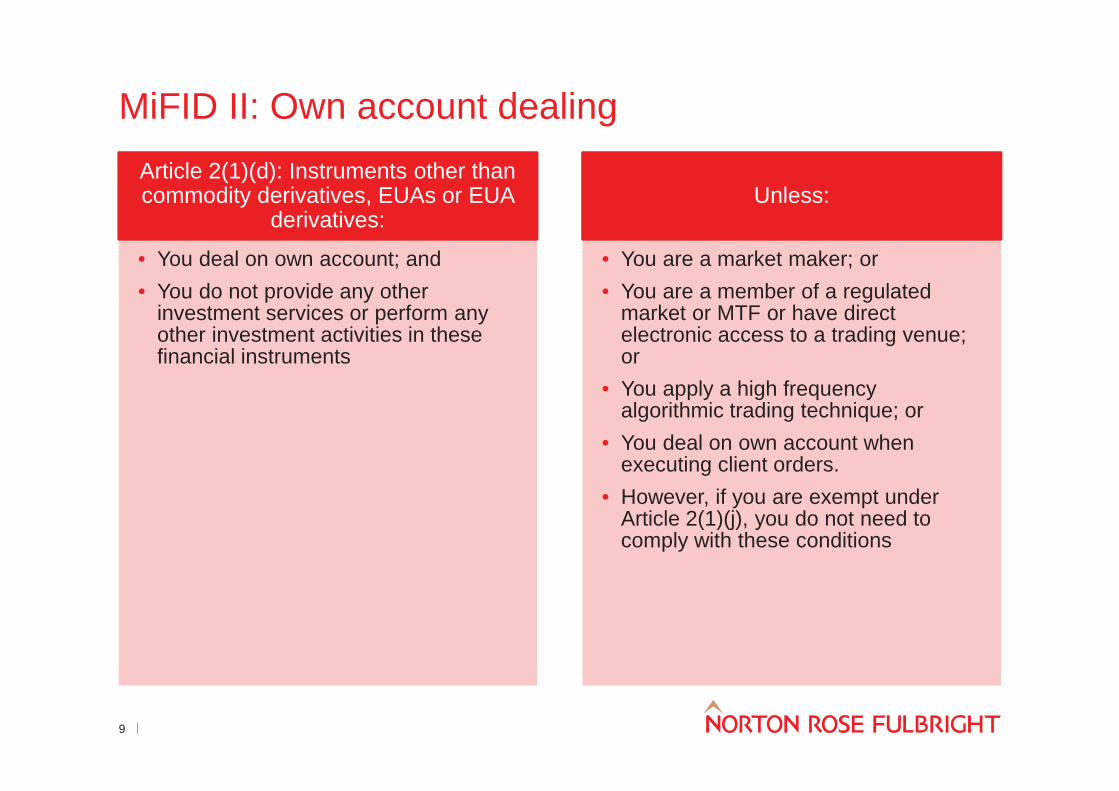

MiFID II: Own account dealing

9

• You deal on own account; and• You do not provide any other

investment services or perform anyother investment activities in thesefinancial instruments

• You are a market maker; or• You are a member of a regulated

market or MTF or have directelectronic access to a trading venue;or

• You apply a high frequencyalgorithmic trading technique; or

• You deal on own account whenexecuting client orders.

• However, if you are exempt underArticle 2(1)(j), you do not need tocomply with these conditions

Article 2(1)(d): Instruments other thancommodity derivatives, EUAs or EUA

derivatives:Unless:

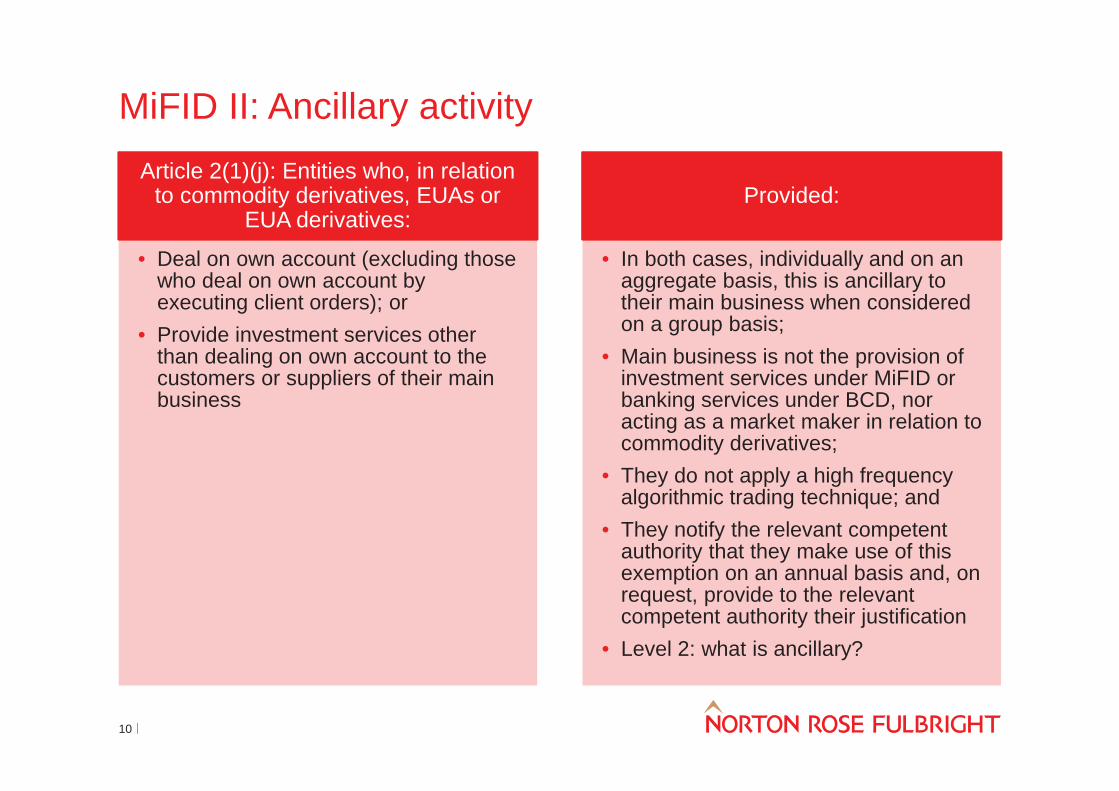

MiFID II: Ancillary activity

10

• Deal on own account (excluding thosewho deal on own account byexecuting client orders); or

• Provide investment services otherthan dealing on own account to thecustomers or suppliers of their mainbusiness

• In both cases, individually and on anaggregate basis, this is ancillary totheir main business when consideredon a group basis;

• Main business is not the provision ofinvestment services under MiFID orbanking services under BCD, noracting as a market maker in relation tocommodity derivatives;

• They do not apply a high frequencyalgorithmic trading technique; and

• They notify the relevant competentauthority that they make use of thisexemption on an annual basis and, onrequest, provide to the relevantcompetent authority their justification

• Level 2: what is ancillary?

Article 2(1)(j): Entities who, in relationto commodity derivatives, EUAs or

EUA derivatives:Provided:

Even if you are out, are you really out?

Can we reallydescribethem as

exemptionsany longer?

Persons relying on new2(1)(e) or (j) will be subjectto the MiFID provisions in

relation to algorithmictrading to the extent thatthey are members of orparticipants in a RM or

MTF

The position managementand position limit powers ofboth the NCAs and ESMA

apply to anyone with acommodity derivative

position – regardless ofwhether they are exemptunder any part of Article 2

Product interventionpowers apply to anyone

regardless of whether theyare exempt under any part

of Article 2

The trading obligation inrespect of OTC derivatives

applies to EMIR NFC+sregardless of the fact that

they are exempt underArticle 2

11

12

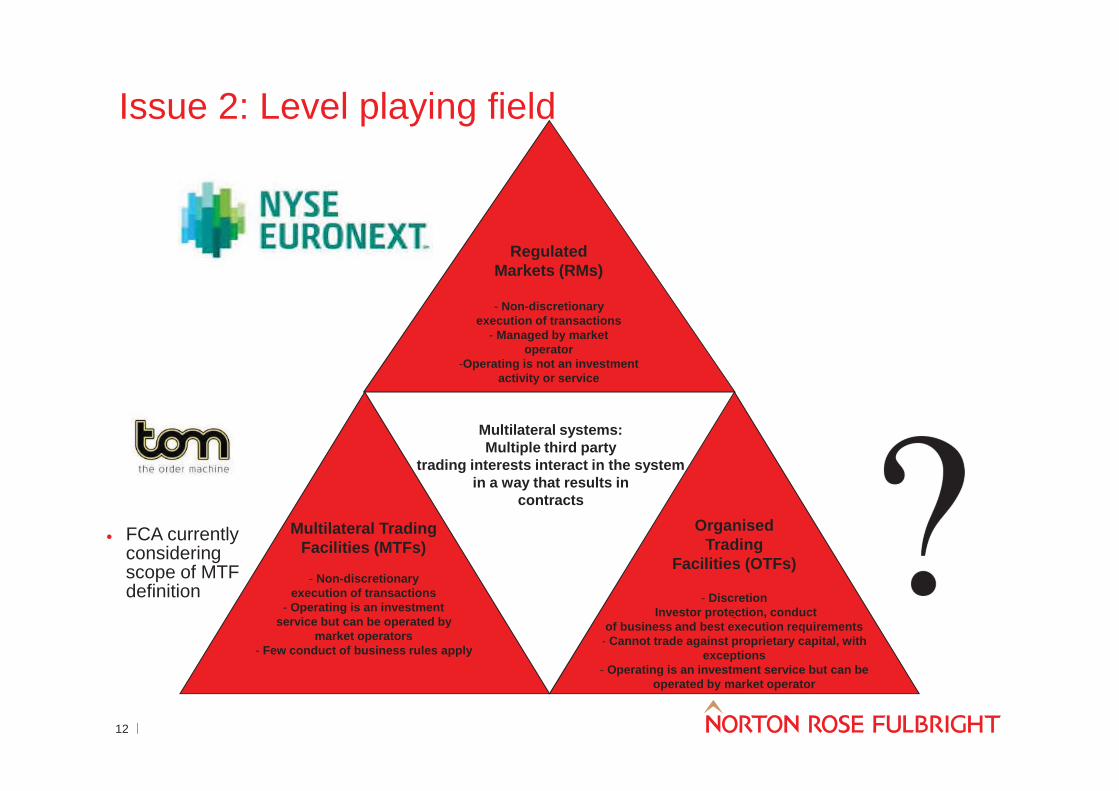

Issue 2: Level playing field

Multilateral systems:Multiple third party

trading interests interact in the systemin a way that results in

contracts

-

FCA currentlyconsideringscope of MTFdefinition

OrganisedTrading

Facilities (OTFs)

- DiscretionInvestor protection, conduct

of business and best execution requirements- Cannot trade against proprietary capital, with

exceptions- Operating is an investment service but can be

operated by market operator

RegulatedMarkets (RMs)

- Non-discretionaryexecution of transactions

- Managed by marketoperator

-Operating is not an investmentactivity or service

Multilateral TradingFacilities (MTFs)

- Non-discretionaryexecution of transactions

- Operating is an investmentservice but can be operated by

market operators- Few conduct of business rules apply

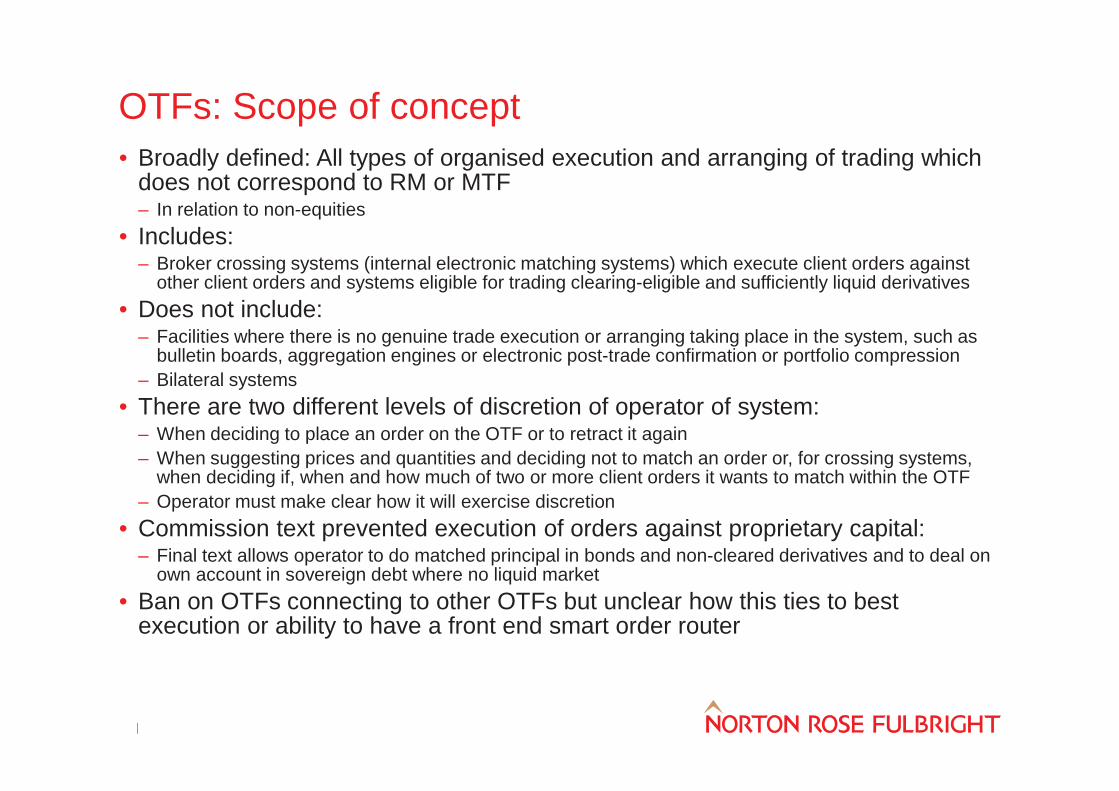

OTFs: Scope of concept• Broadly defined: All types of organised execution and arranging of trading which

does not correspond to RM or MTF– In relation to non-equities

• Includes:– Broker crossing systems (internal electronic matching systems) which execute client orders against

other client orders and systems eligible for trading clearing-eligible and sufficiently liquid derivatives• Does not include:

– Facilities where there is no genuine trade execution or arranging taking place in the system, such asbulletin boards, aggregation engines or electronic post-trade confirmation or portfolio compression

– Bilateral systems• There are two different levels of discretion of operator of system:

– When deciding to place an order on the OTF or to retract it again– When suggesting prices and quantities and deciding not to match an order or, for crossing systems,

when deciding if, when and how much of two or more client orders it wants to match within the OTF– Operator must make clear how it will exercise discretion

• Commission text prevented execution of orders against proprietary capital:– Final text allows operator to do matched principal in bonds and non-cleared derivatives and to deal on

own account in sovereign debt where no liquid market• Ban on OTFs connecting to other OTFs but unclear how this ties to best

execution or ability to have a front end smart order router

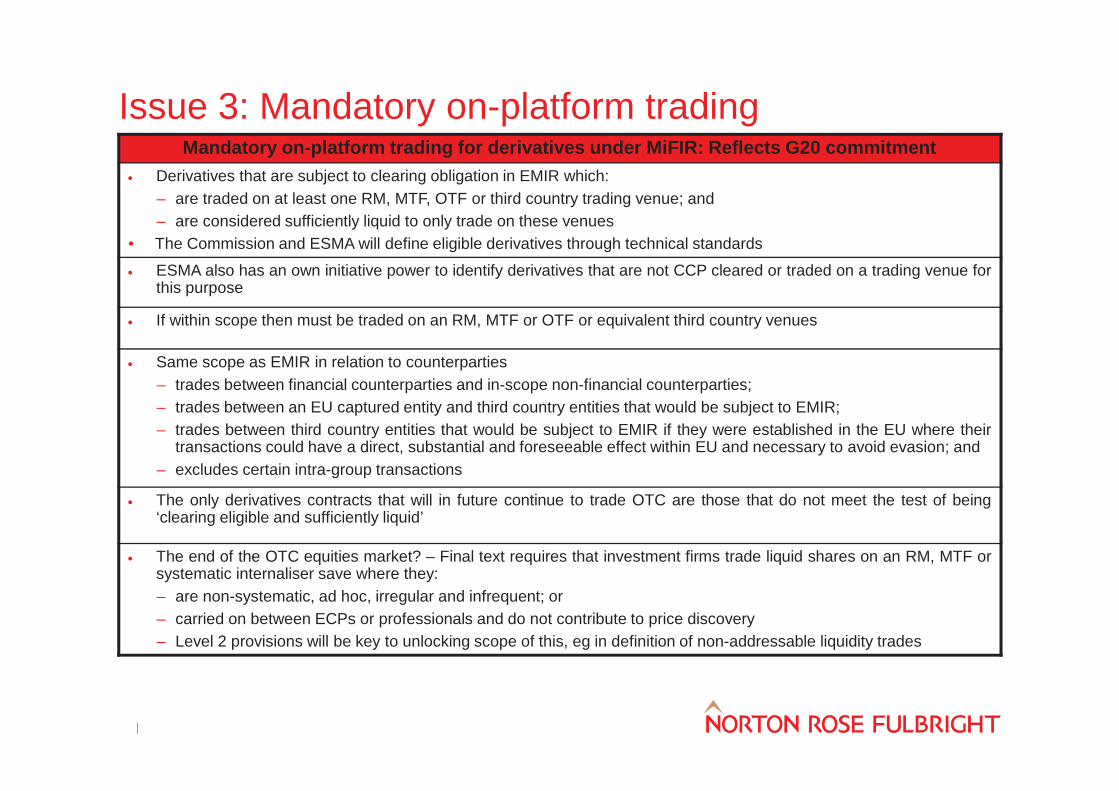

Issue 3: Mandatory on-platform tradingMandatory on-platform trading for derivatives under MiFIR: Reflects G20 commitment

Derivatives that are subject to clearing obligation in EMIR which:– are traded on at least one RM, MTF, OTF or third country trading venue; and– are considered sufficiently liquid to only trade on these venues

• The Commission and ESMA will define eligible derivatives through technical standards

ESMA also has an own initiative power to identify derivatives that are not CCP cleared or traded on a trading venue forthis purpose

If within scope then must be traded on an RM, MTF or OTF or equivalent third country venues

Same scope as EMIR in relation to counterparties– trades between financial counterparties and in-scope non-financial counterparties;– trades between an EU captured entity and third country entities that would be subject to EMIR;– trades between third country entities that would be subject to EMIR if they were established in the EU where their

transactions could have a direct, substantial and foreseeable effect within EU and necessary to avoid evasion; and– excludes certain intra-group transactions

The only derivatives contracts that will in future continue to trade OTC are those that do not meet the test of being‘clearing eligible and sufficiently liquid’

The end of the OTC equities market? – Final text requires that investment firms trade liquid shares on an RM, MTF orsystematic internaliser save where they:– are non-systematic, ad hoc, irregular and infrequent; or– carried on between ECPs or professionals and do not contribute to price discovery– Level 2 provisions will be key to unlocking scope of this, eg in definition of non-addressable liquidity trades

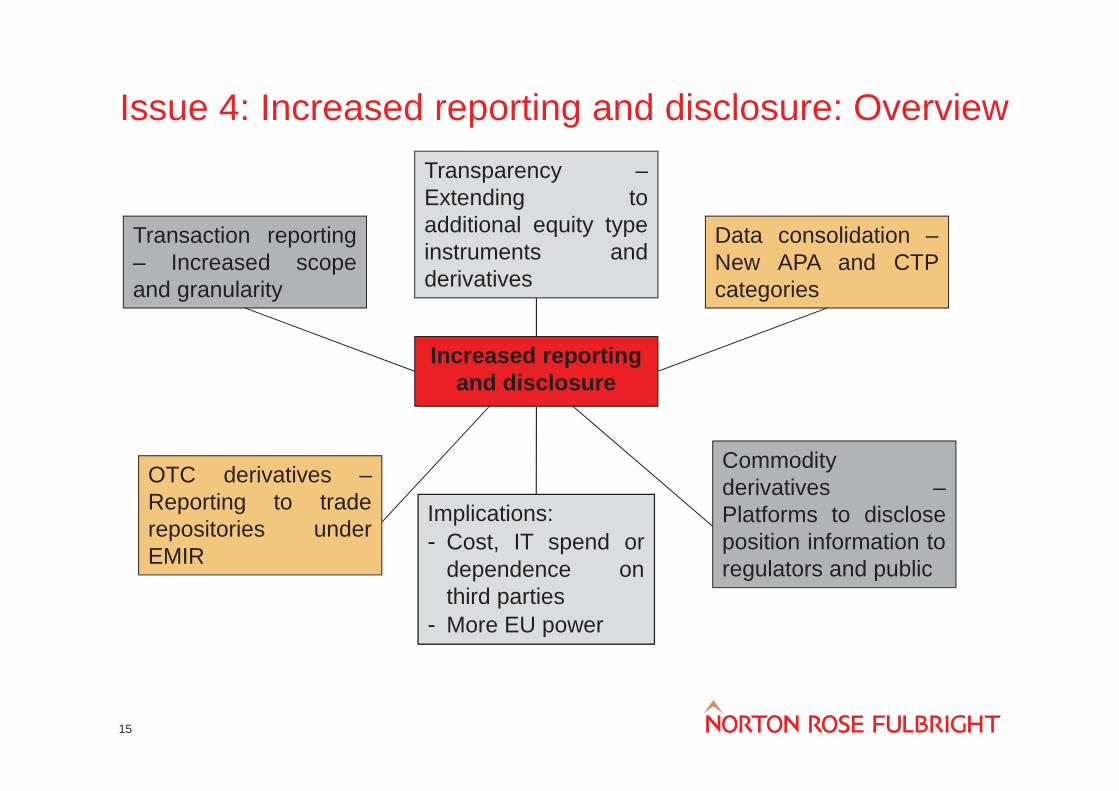

Issue 4: Increased reporting and disclosure: Overview

OTC derivatives –Reporting to traderepositories underEMIR

Increased reportingand disclosure

Transparency –Extending toadditional equity typeinstruments andderivatives

Transaction reporting– Increased scopeand granularity

Data consolidation –New APA and CTPcategories

Implications:- Cost, IT spend or

dependence onthird parties

- More EU power

Commodityderivatives –Platforms to discloseposition information toregulators and public

15

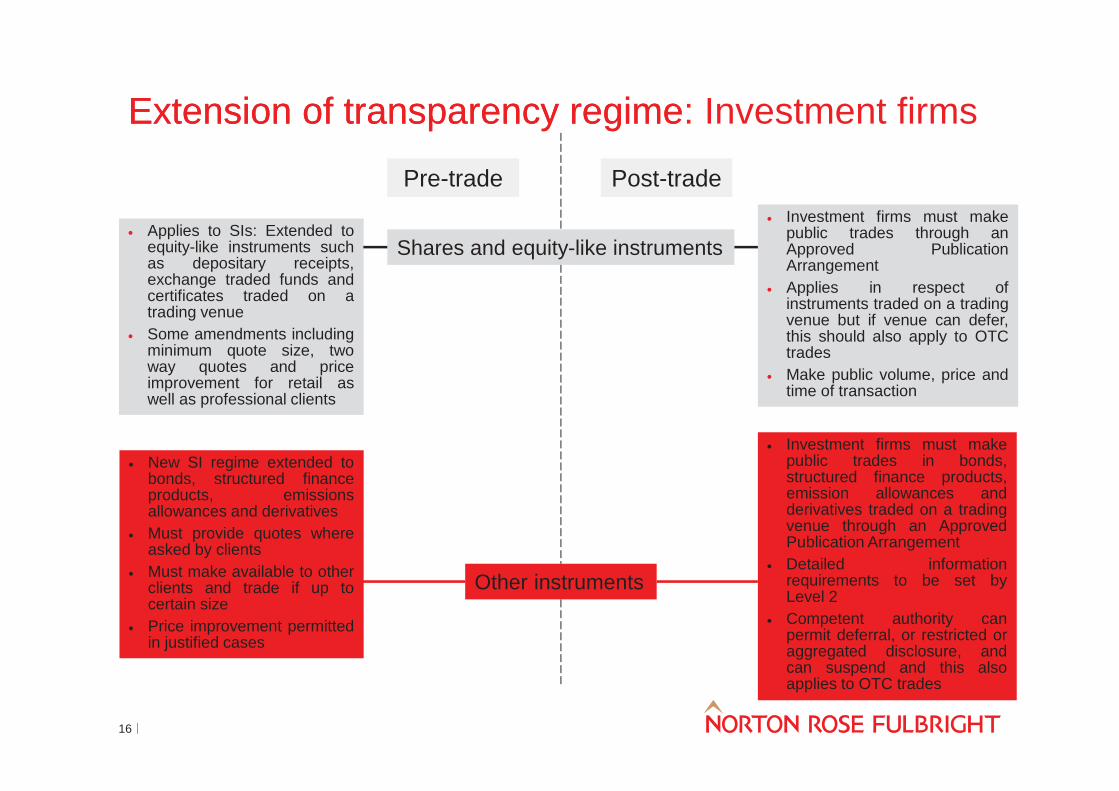

Extension of transparency regime Investment firmsExtension of transparency regime:

Shares and equity-like instruments

Pre-trade Post-trade

Other instruments

Applies to SIs: Extended toequity-like instruments suchas depositary receipts,exchange traded funds andcertificates traded on atrading venueSome amendments includingminimum quote size, twoway quotes and priceimprovement for retail aswell as professional clients

Investment firms must makepublic trades through anApproved PublicationArrangementApplies in respect ofinstruments traded on a tradingvenue but if venue can defer,this should also apply to OTCtradesMake public volume, price andtime of transaction

New SI regime extended tobonds, structured financeproducts, emissionsallowances and derivativesMust provide quotes whereasked by clientsMust make available to otherclients and trade if up tocertain sizePrice improvement permittedin justified cases

Investment firms must makepublic trades in bonds,structured finance products,emission allowances andderivatives traded on a tradingvenue through an ApprovedPublication ArrangementDetailed informationrequirements to be set byLevel 2Competent authority canpermit deferral, or restricted oraggregated disclosure, andcan suspend and this alsoapplies to OTC trades

16

17

Systematic Internalisers (SIs)• An investment firm which on an organised, frequent, systematic and

substantial basis deals on own account by executing client ordersoutside a RM, MT or OTF

• Pre-set limits which must be crossed• Or firm can choose to opt in

• Equities• Minimum quote sizes at least 10% of standard market size• Price improvement now permitted provided in range close to market conditions and old

retail size limit has gone• Additional flexibility for professional client orders

• Non-equities• Flexibility on providing access in accordance with commercial policy provided that this

is objective and non-discriminatory – can consider eg. counterparty risk• Can impose limits on number of transactions undertaken pursuant to a quote

• SIs do not have to make public any quotes for large size orders or blocktrades

• SIs must make post-trade derivatives data public via an APA: however,competent authorities may permit SIs to defer publication

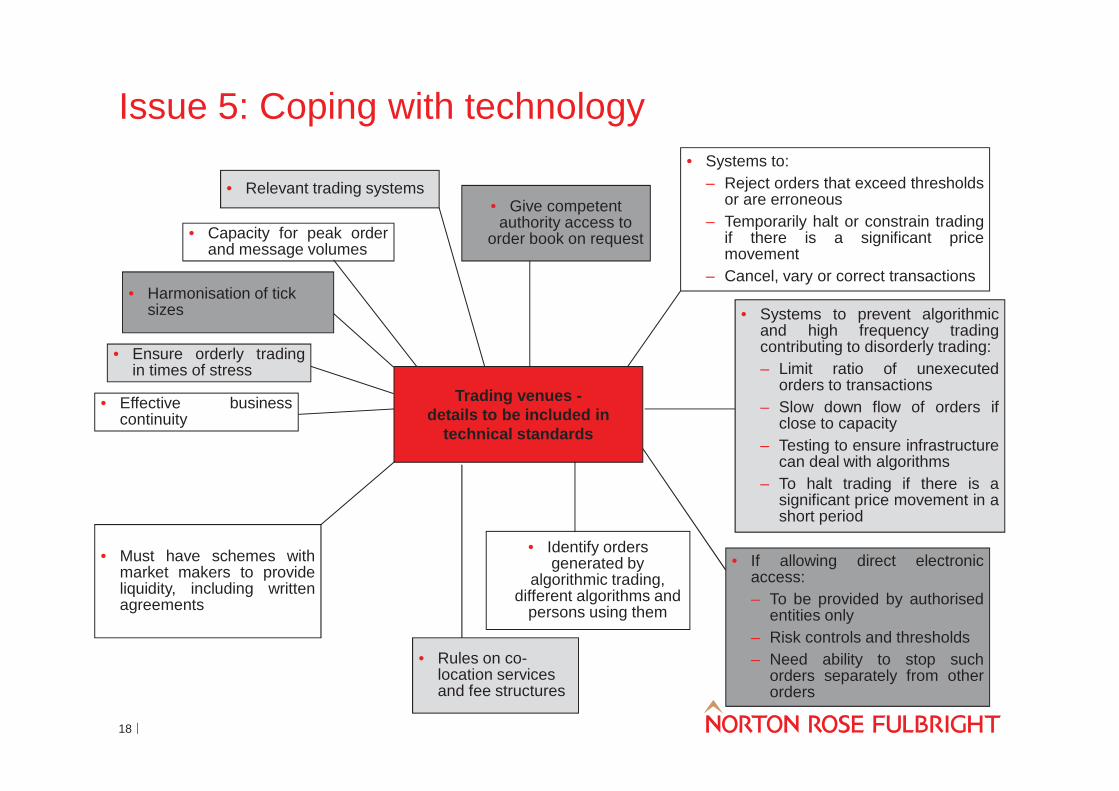

Issue 5: Coping with technology• Systems to:

– Reject orders that exceed thresholdsor are erroneous

– Temporarily halt or constrain tradingif there is a significant pricemovement

– Cancel, vary or correct transactions

Trading venues -details to be included in

technical standards

• Systems to prevent algorithmicand high frequency tradingcontributing to disorderly trading:– Limit ratio of unexecuted

orders to transactions– Slow down flow of orders if

close to capacity– Testing to ensure infrastructure

can deal with algorithms– To halt trading if there is a

significant price movement in ashort period

• If allowing direct electronicaccess:– To be provided by authorised

entities only– Risk controls and thresholds– Need ability to stop such

orders separately from otherorders

• Must have schemes withmarket makers to provideliquidity, including writtenagreements

• Rules on co-location servicesand fee structures

• Identify ordersgenerated by

algorithmic trading,different algorithms and

persons using them

• Give competentauthority access to

order book on request

• Relevant trading systems

• Capacity for peak orderand message volumes

• Ensure orderly tradingin times of stress

• Effective businesscontinuity

• Harmonisation of ticksizes

18

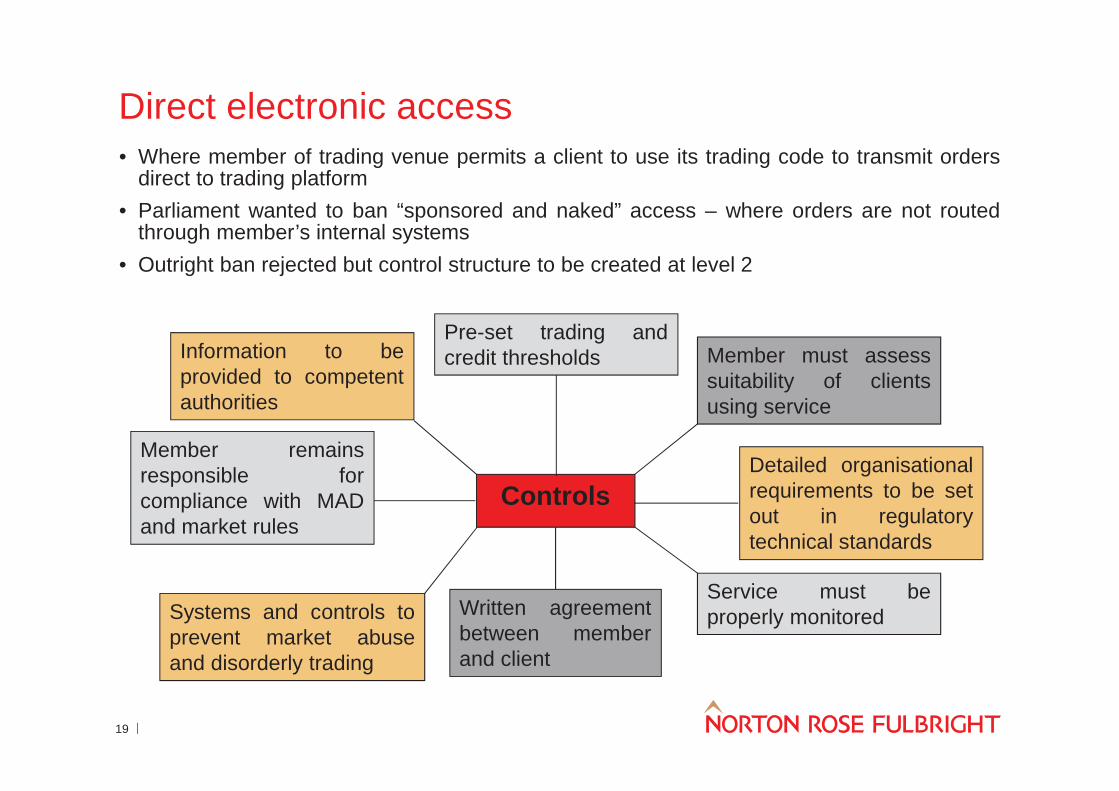

19

Direct electronic access• Where member of trading venue permits a client to use its trading code to transmit orders

direct to trading platform• Parliament wanted to ban “sponsored and naked” access – where orders are not routed

through member’s internal systems• Outright ban rejected but control structure to be created at level 2

Information to beprovided to competentauthorities

Detailed organisationalrequirements to be setout in regulatorytechnical standards

Member must assesssuitability of clientsusing service

Member remainsresponsible forcompliance with MADand market rules

Pre-set trading andcredit thresholds

Written agreementbetween memberand client

Service must beproperly monitoredSystems and controls to

prevent market abuseand disorderly trading

Controls

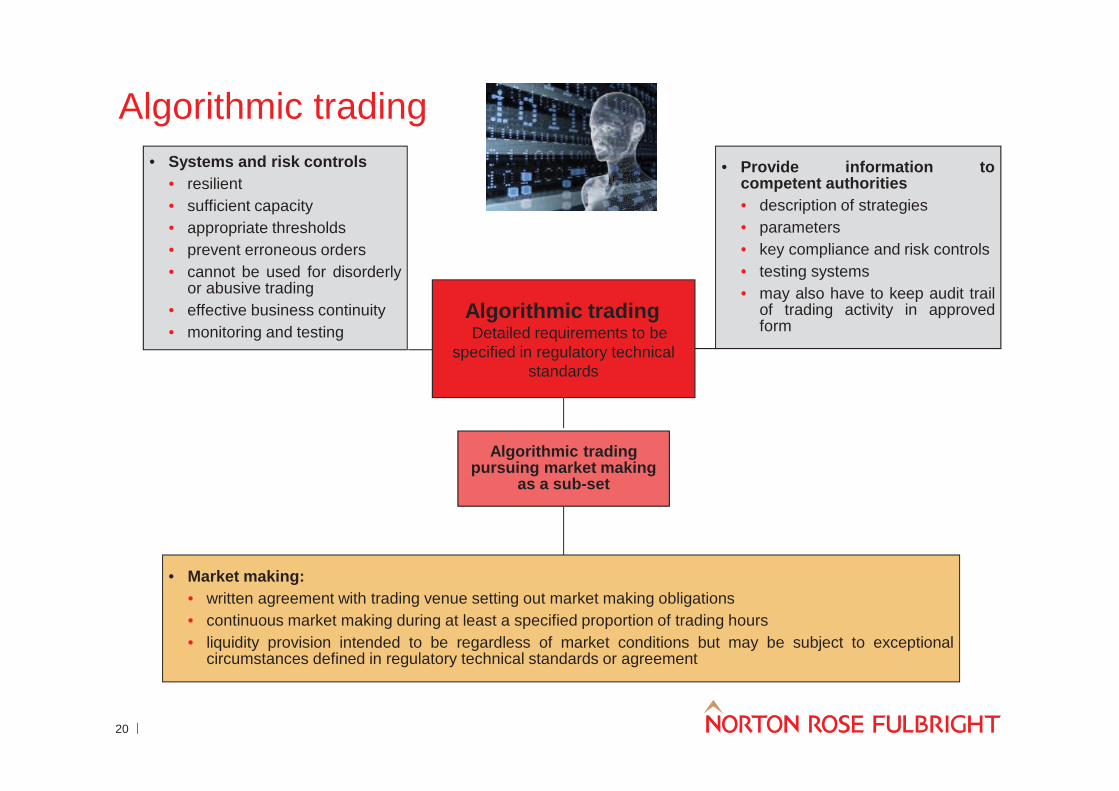

20

Algorithmic trading• Provide information to

competent authorities• description of strategies• parameters• key compliance and risk controls• testing systems• may also have to keep audit trail

of trading activity in approvedform

Algorithmic trading• Detailed requirements to be

specified in regulatory technicalstandards

• Systems and risk controls• resilient• sufficient capacity• appropriate thresholds• prevent erroneous orders• cannot be used for disorderly

or abusive trading• effective business continuity• monitoring and testing

Algorithmic tradingpursuing market making

as a sub-set

• Market making:• written agreement with trading venue setting out market making obligations• continuous market making during at least a specified proportion of trading hours• liquidity provision intended to be regardless of market conditions but may be subject to exceptional

circumstances defined in regulatory technical standards or agreement

The conduct of business dimension of MiFID II

Putting together the COB puzzle• At first glance:

– The headline changes to the MiFID regime centre on market infrastructure– But it is clear that many of the proposed conduct of business amendments are

likely to have a significant impact on the way firms carry on business– Many small changes that snow ball into significant regulatory reform

• Post crisis reaction:– Theme 1: Commission strengthening the right to information for both retail and

professional clients and small changes reg. ECPs– Theme 2: Suspicion of wholesale business and protection of consumers - fees

and commission restrictions and product banning examples– Theme 3: The devil in the detail - many of the provisions will be layered by

Level 2 measures and ESMA guidelines - best execution, suitability andappropriateness examples

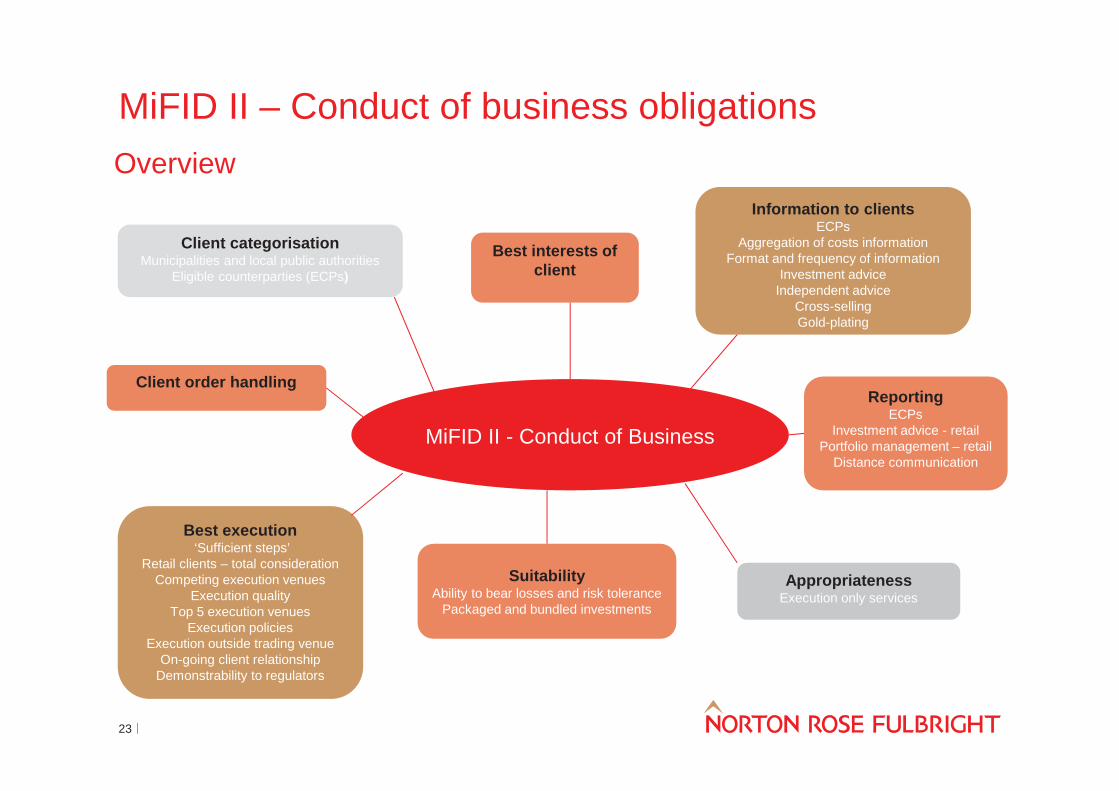

MiFID II – Conduct of business obligationsOverview

MiFID II - Conduct of Business

Client categorisationMunicipalities and local public authorities

Eligible counterparties (ECPs)

Best interests ofclient

Information to clientsECPs

Aggregation of costs informationFormat and frequency of information

Investment adviceIndependent advice

Cross-sellingGold-plating

Best execution‘Sufficient steps’

Retail clients – total considerationCompeting execution venues

Execution qualityTop 5 execution venues

Execution policiesExecution outside trading venue

On-going client relationshipDemonstrability to regulators

Client order handling

SuitabilityAbility to bear losses and risk tolerance

Packaged and bundled investments

AppropriatenessExecution only services

ReportingECPs

Investment advice - retailPortfolio management – retail

Distance communication

23

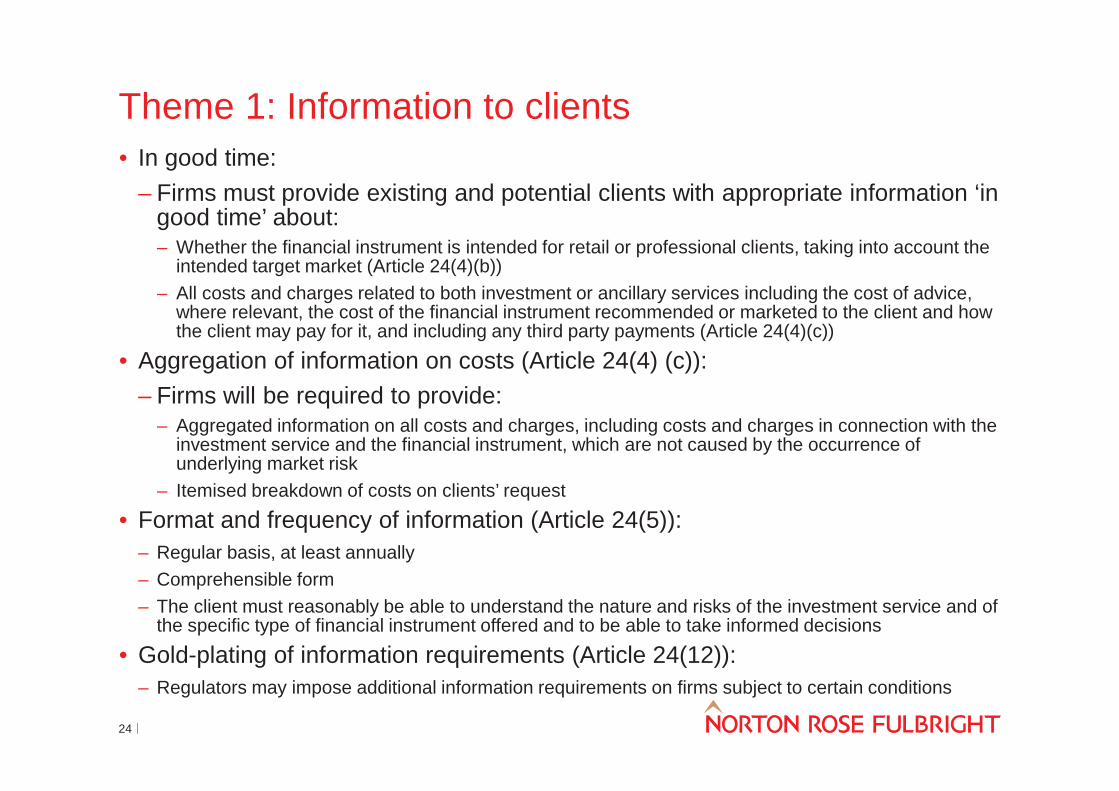

Theme 1: Information to clients• In good time:

– Firms must provide existing and potential clients with appropriate information ‘ingood time’ about:– Whether the financial instrument is intended for retail or professional clients, taking into account the

intended target market (Article 24(4)(b))– All costs and charges related to both investment or ancillary services including the cost of advice,

where relevant, the cost of the financial instrument recommended or marketed to the client and howthe client may pay for it, and including any third party payments (Article 24(4)(c))

• Aggregation of information on costs (Article 24(4) (c)):– Firms will be required to provide:

– Aggregated information on all costs and charges, including costs and charges in connection with theinvestment service and the financial instrument, which are not caused by the occurrence ofunderlying market risk

– Itemised breakdown of costs on clients’ request

• Format and frequency of information (Article 24(5)):– Regular basis, at least annually– Comprehensible form– The client must reasonably be able to understand the nature and risks of the investment service and of

the specific type of financial instrument offered and to be able to take informed decisions

• Gold-plating of information requirements (Article 24(12)):– Regulators may impose additional information requirements on firms subject to certain conditions

24

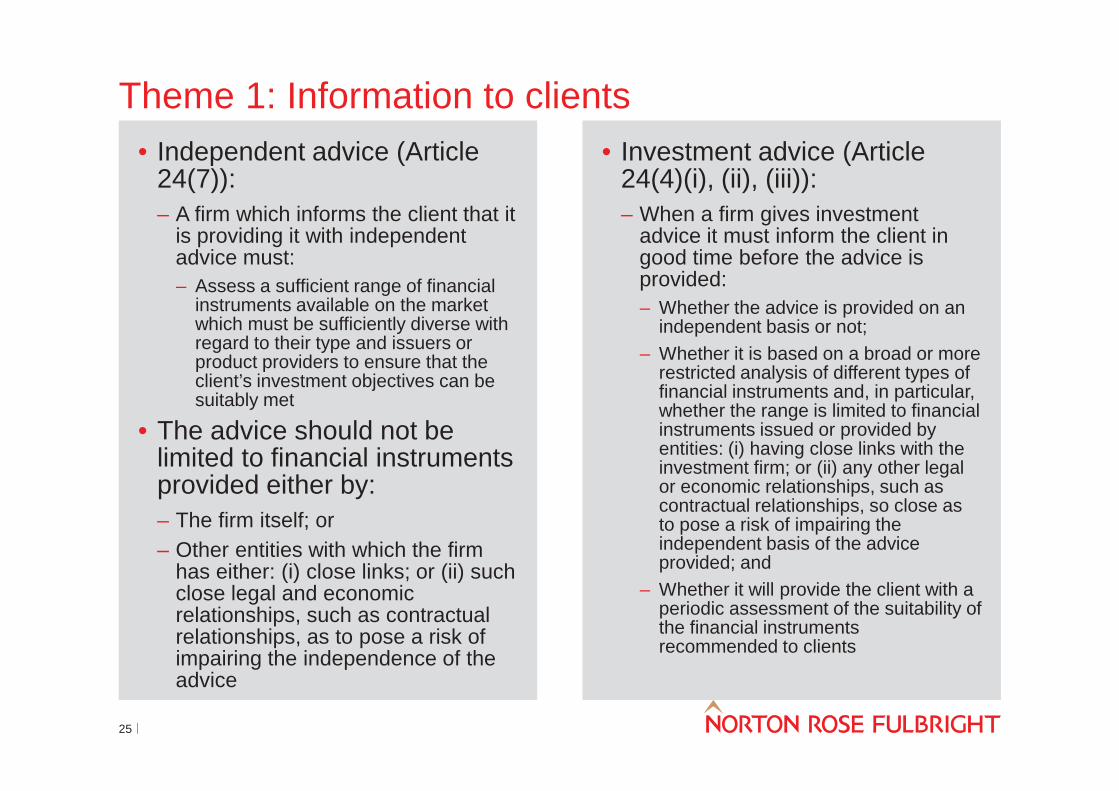

Theme 1: Information to clients• Independent advice (Article

24(7)):– A firm which informs the client that it

is providing it with independentadvice must:– Assess a sufficient range of financial

instruments available on the marketwhich must be sufficiently diverse withregard to their type and issuers orproduct providers to ensure that theclient’s investment objectives can besuitably met

• The advice should not belimited to financial instrumentsprovided either by:– The firm itself; or– Other entities with which the firm

has either: (i) close links; or (ii) suchclose legal and economicrelationships, such as contractualrelationships, as to pose a risk ofimpairing the independence of theadvice

• Investment advice (Article24(4)(i), (ii), (iii)):– When a firm gives investment

advice it must inform the client ingood time before the advice isprovided:– Whether the advice is provided on an

independent basis or not;– Whether it is based on a broad or more

restricted analysis of different types offinancial instruments and, in particular,whether the range is limited to financialinstruments issued or provided byentities: (i) having close links with theinvestment firm; or (ii) any other legalor economic relationships, such ascontractual relationships, so close asto pose a risk of impairing theindependent basis of the adviceprovided; and

– Whether it will provide the client with aperiodic assessment of the suitability ofthe financial instrumentsrecommended to clients

25

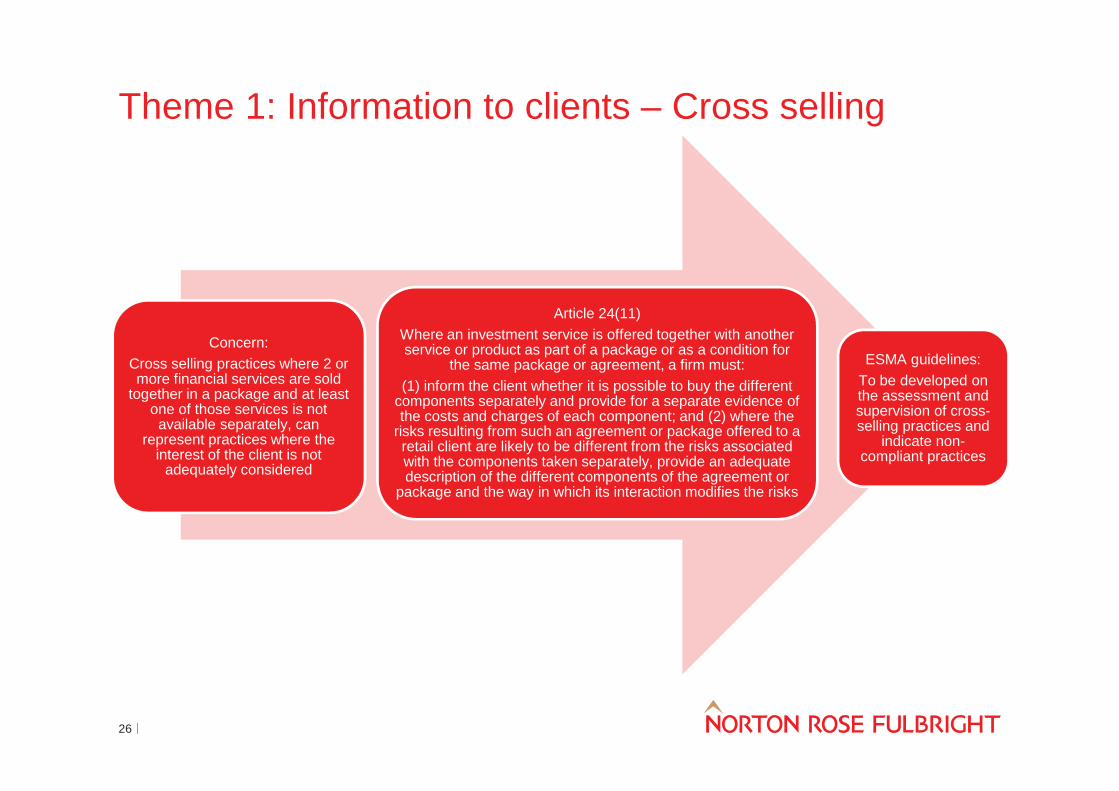

Theme 1: Information to clients – Cross selling

Concern:Cross selling practices where 2 ormore financial services are sold

together in a package and at leastone of those services is notavailable separately, can

represent practices where theinterest of the client is not

adequately considered

Article 24(11)Where an investment service is offered together with anotherservice or product as part of a package or as a condition for

the same package or agreement, a firm must:(1) inform the client whether it is possible to buy the different

components separately and provide for a separate evidence ofthe costs and charges of each component; and (2) where the

risks resulting from such an agreement or package offered to aretail client are likely to be different from the risks associatedwith the components taken separately, provide an adequatedescription of the different components of the agreement or

package and the way in which its interaction modifies the risks

ESMA guidelines:To be developed onthe assessment andsupervision of cross-selling practices and

indicate non-compliant practices

26

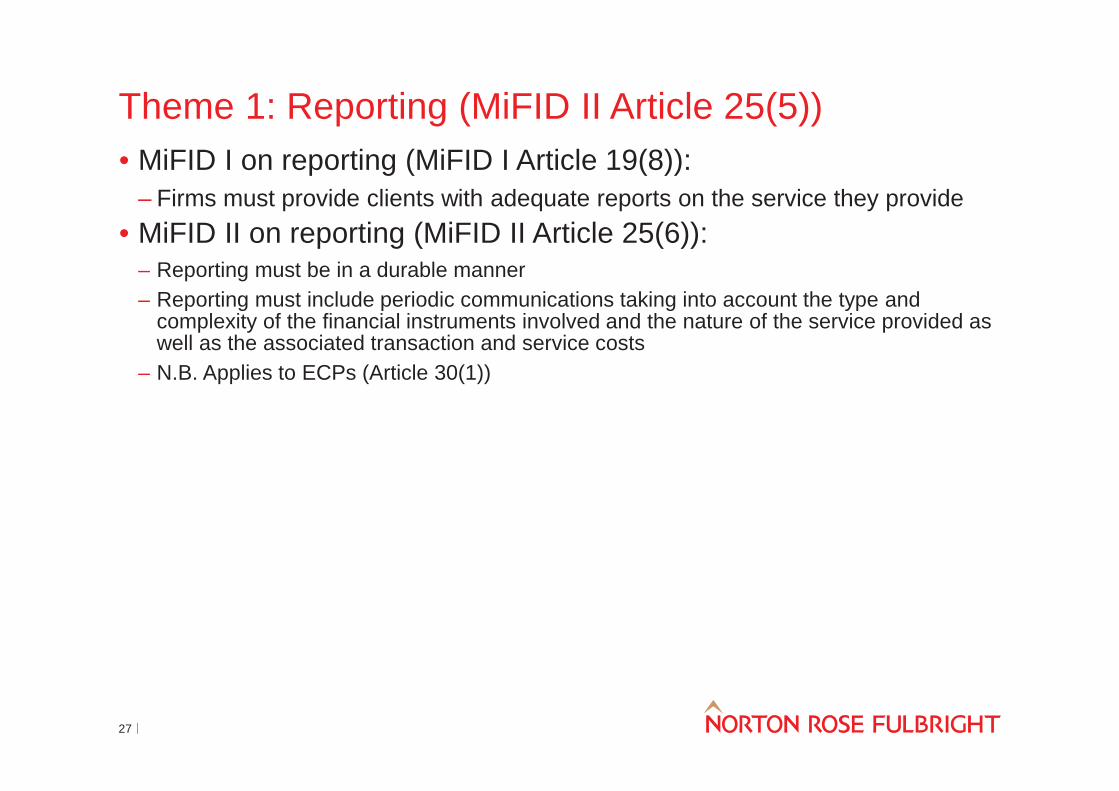

Theme 1: Reporting (MiFID II Article 25(5))• MiFID I on reporting (MiFID I Article 19(8)):

– Firms must provide clients with adequate reports on the service they provide• MiFID II on reporting (MiFID II Article 25(6)):

– Reporting must be in a durable manner– Reporting must include periodic communications taking into account the type and

complexity of the financial instruments involved and the nature of the service provided aswell as the associated transaction and service costs

– N.B. Applies to ECPs (Article 30(1))

27

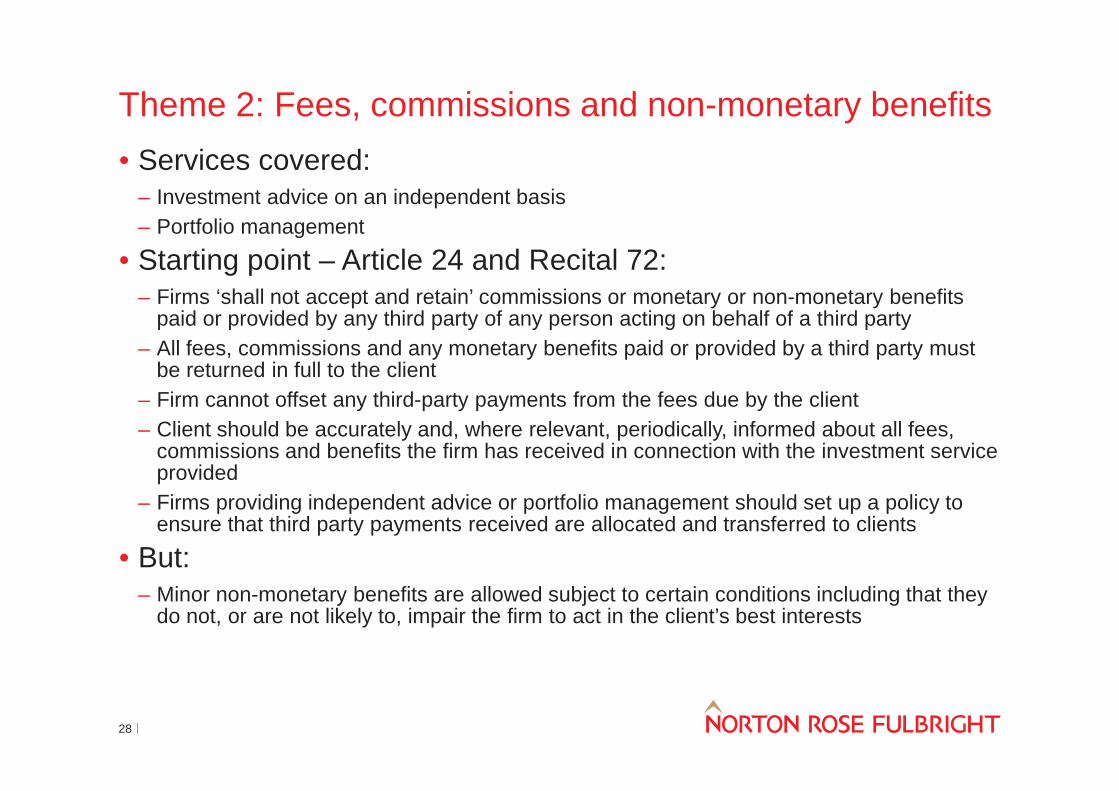

Theme 2: Fees, commissions and non-monetary benefits• Services covered:

– Investment advice on an independent basis– Portfolio management

• Starting point – Article 24 and Recital 72:– Firms ‘shall not accept and retain’ commissions or monetary or non-monetary benefits

paid or provided by any third party of any person acting on behalf of a third party– All fees, commissions and any monetary benefits paid or provided by a third party must

be returned in full to the client– Firm cannot offset any third-party payments from the fees due by the client– Client should be accurately and, where relevant, periodically, informed about all fees,

commissions and benefits the firm has received in connection with the investment serviceprovided

– Firms providing independent advice or portfolio management should set up a policy toensure that third party payments received are allocated and transferred to clients

• But:– Minor non-monetary benefits are allowed subject to certain conditions including that they

do not, or are not likely to, impair the firm to act in the client’s best interests

28

Theme 2: Fees, commissions and non-monetary benefits• The requirement:

– When providing investment advice on an independent basis and portfoliomanagement, fees, commissions or non-monetary benefits paid or provided bya person on behalf of the client are allowed BUT only as far as the person isaware that such payments have been made on his behalf and that the amountand frequency of any payment is agreed between the client and the investmentfirm and not determined by a third party

• Cases which would satisfy the caveat:– Where a client pays a firm’s invoice directly or it is paid by an independent third

party who has no connection with the investment firm regarding the investmentservice provided to the client and is acting only on the instructions of the client

– Where the client negotiates a fee for a service provided by an investment firmand pays that fee

• To further protect consumers:– Investment firm that provides investment services to clients shall ensure that it

does not remunerate or assess the performance of its staff in a way thatconflicts with its duty to act in the best interests of its clients (Article 24 (10))

29

Theme 2: Product banning - General• Recitals indicate that product banning can be better achieved at

the EU level• The distribution, sale or marketing of any financial instrument or

structured deposit may be prohibited or restricted• Any ban must address one of the following:

– A significant investor protection concern– A threat to the orderly functioning and integrity of financial or commodity

markets– A threat to the stability of the whole or part of the EU financial system

• Commission will give further detail regarding the criteria andfactors to be taken into account, including the:– Degree of complexity of a financial instrument and the relation to the type of

client to whom it is marketed and sold– Size or the notional value of an issuance of financial instruments– Degree of innovation of a financial instrument, an activity or a practice– Leverage a product or practice provides

30

Theme 2: Product banning - Competent Authorities• Competent authorities should where relevant coordinate with

ESMA or the EBA• ESMA/EBA may temporarily ban products• The banning authority will notify the public and, where relevant,

the competent authorities regarding any measures taken• ESMA or, where relevant, the EBA will issue an opinion on the

steps taken by competent authorities to ban/restrict products• ESMA/EBA will review measures taken to prohibit a product at

least once every three months• Competent authorities will revoke a prohibition once the rationale

for it no longer applies

31

Theme 3: Best execution

• New obligations of best execution (Article 27):– Firms must now take ‘sufficient steps’ to obtain best execution for their clients (Article

27(1))• Execution quality data – trading venues, execution venues and

systematic internalisers (Article 27(3)):– On at least an annual basis and without charge, data relating to the quality of execution of

transactions on a venue, including details about price, costs, speed and likelihood ofexecution for individual financial instruments, must be made available to the public bytrading venues and systematic internalisers, in the case of financial instruments subject tothe trading obligations in Article 23 and 28 of MiFIR, and by execution venues, in the caseof all other financial instruments (Article 27(3))– ESMA regulatory technical standards:

– To determine the specific content, format and periodicity of data to be published on executionquality (Article 2710)(a))

– Following the execution of an order, a firm must inform its client where that order wasexecuted (Article 27(3))

– A firm must summarise and make public on an annual basis, for each class of financialinstruments, the top five execution venues in terms of trading volumes where theyexecuted client orders in the preceding year and information on the quality of executionobtained (Article 27(6))

32

Theme 3: Best execution

– In complying with its existing obligation to monitor the effectiveness of its order executionarrangements and to, where appropriate, correct any deficiencies, a firm will also be required totake into account the information published by trading venues, systematic internalisers andexecution venues, under Article 27(3), on the execution quality of transactions and thesummary of its top five execution venues for each class of financial instruments under Article27(6) (Article 27(7))

• New obligations of best execution (Article 27):– Information on a firm’s order execution policy must now explain clearly, in sufficient detail and in

a way that can be easily understood by clients, how orders will be executed by the firm for theclient (Article 27(5)

– A firm must now inform clients where there is a possibility that their order will be executedoutside a trading venue and it must obtain prior consent from its client before doing so (Article27(5). Under MiFID, firms only have the obligation to do this where there is a possibility thattheir clients’ orders will be executed outside a regulated market or a multilateral trading facility(MTF)

– A firm’s obligation to inform clients of material changes to its order execution arrangements hasbeen limited to an obligation to inform clients with whom the firm has an ‘on-going relationship’(Article 27(7))– ESMA regulatory technical standards:

– To determine the content and format of this information– Upon request, firms will not only be required to demonstrate to the regulator that they have

executed their orders in accordance with their execution policy but also their generalcompliance with the best execution obligation in Article 27 (Article 27(8))

33

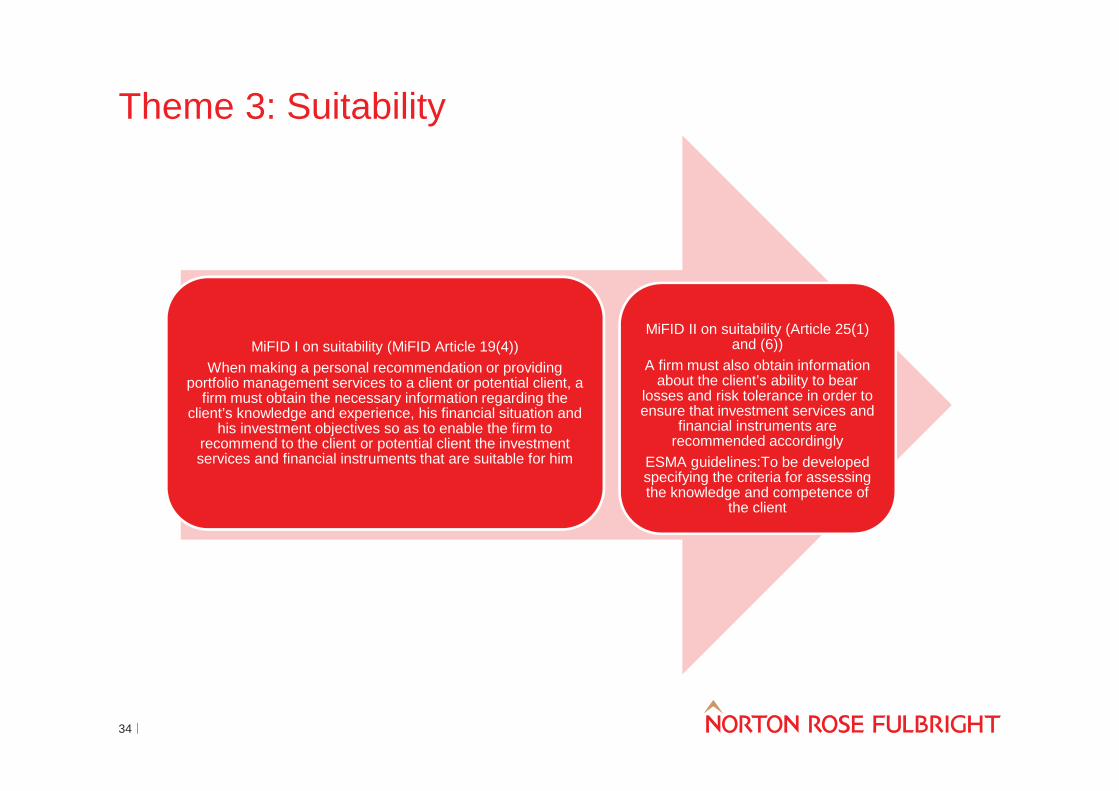

Theme 3: Suitability

MiFID I on suitability (MiFID Article 19(4))When making a personal recommendation or providing

portfolio management services to a client or potential client, afirm must obtain the necessary information regarding the

client’s knowledge and experience, his financial situation andhis investment objectives so as to enable the firm to

recommend to the client or potential client the investmentservices and financial instruments that are suitable for him

MiFID II on suitability (Article 25(1)and (6))

A firm must also obtain informationabout the client’s ability to bear

losses and risk tolerance in order toensure that investment services and

financial instruments arerecommended accordingly

ESMA guidelines:To be developedspecifying the criteria for assessingthe knowledge and competence of

the client

34

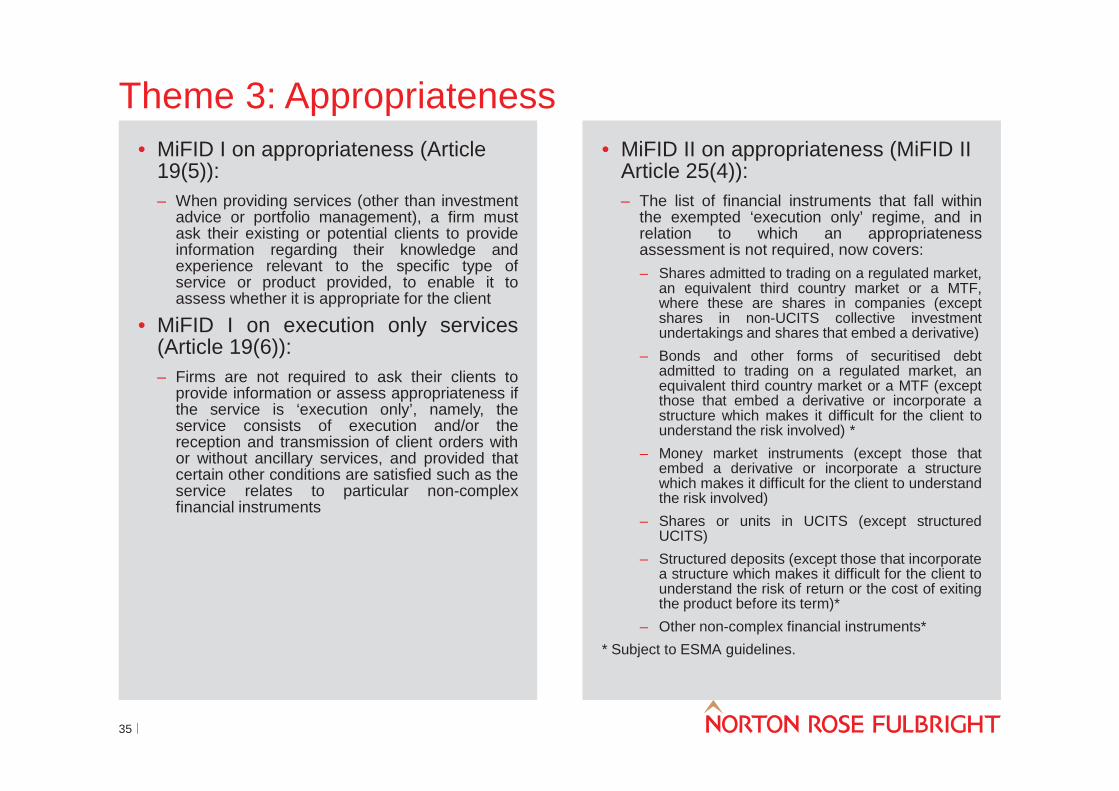

Theme 3: Appropriateness• MiFID I on appropriateness (Article

19(5)):– When providing services (other than investment

advice or portfolio management), a firm mustask their existing or potential clients to provideinformation regarding their knowledge andexperience relevant to the specific type ofservice or product provided, to enable it toassess whether it is appropriate for the client

• MiFID I on execution only services(Article 19(6)):– Firms are not required to ask their clients to

provide information or assess appropriateness ifthe service is ‘execution only’, namely, theservice consists of execution and/or thereception and transmission of client orders withor without ancillary services, and provided thatcertain other conditions are satisfied such as theservice relates to particular non-complexfinancial instruments

• MiFID II on appropriateness (MiFID IIArticle 25(4)):– The list of financial instruments that fall within

the exempted ‘execution only’ regime, and inrelation to which an appropriatenessassessment is not required, now covers:– Shares admitted to trading on a regulated market,

an equivalent third country market or a MTF,where these are shares in companies (exceptshares in non-UCITS collective investmentundertakings and shares that embed a derivative)

– Bonds and other forms of securitised debtadmitted to trading on a regulated market, anequivalent third country market or a MTF (exceptthose that embed a derivative or incorporate astructure which makes it difficult for the client tounderstand the risk involved) *

– Money market instruments (except those thatembed a derivative or incorporate a structurewhich makes it difficult for the client to understandthe risk involved)

– Shares or units in UCITS (except structuredUCITS)

– Structured deposits (except those that incorporatea structure which makes it difficult for the client tounderstand the risk of return or the cost of exitingthe product before its term)*

– Other non-complex financial instruments** Subject to ESMA guidelines.

35

Contacts

36

Gijs van LeeuwenPartner, AmsterdamTel +31 20 462 [email protected]

Floortje NagelkerkeSenior associate, AmsterdamTel +31 20 462 [email protected]

Hannah MeakinPartner, LondonTel +44 20 7444 [email protected]

DisclaimerNorton Rose Fulbright LLP, Norton Rose Fulbright Australia, Norton Rose Fulbright Canada LLP, Norton Rose Fulbright South Africa (incorporated as Deneys Reitz Inc) and Fulbright & Jaworski LLP,each of which is a separate legal entity, are members (‘the Norton Rose Fulbright members’) of Norton Rose Fulbright Verein, a Swiss Verein. Norton Rose Fulbright Verein helps coordinate theactivities of the Norton Rose Fulbright members but does not itself provide legal services to clients.References to ‘Norton Rose Fulbright’, ‘the law firm’, and ‘legal practice’ are to one or more of the Norton Rose Fulbright members or to one of their respective affiliates (together ‘Norton RoseFulbright entity/entities’). No individual who is a member, partner, shareholder, director, employee or consultant of, in or to any Norton Rose Fulbright entity (whether or not such individual isdescribed as a ‘partner’) accepts or assumes responsibility, or has any liability, to any person in respect of this communication. Any reference to a partner or director is to a member, employee orconsultant with equivalent standing and qualifications of the relevant Norton Rose Fulbright entity.The purpose of this communication is to provide information as to developments in the law. It does not contain a full analysis of the law nor does it constitute an opinion of any Norton RoseFulbright entity on the points of law discussed. You must take specific legal advice on any particular matter which concerns you. If you require any advice or further information, please speak to yourusual contact at Norton Rose Fulbright.

38

![The Markets in Financial Instruments Directive [ MiFID ] Thursday 1st November 2007 ALAN BURR, FSI](https://img.pdfslide.us/doc/110x75/56649e385503460f94b28c07/the-markets-in-financial-instruments-directive-mifid-thursday-1st-november.jpg)