Embed Size (px)

Citation preview

PRECISE. PROVEN. PERFORMANCE. www.moorestephens.co.uk

MiFID II part two Wednesday 29 March 2017

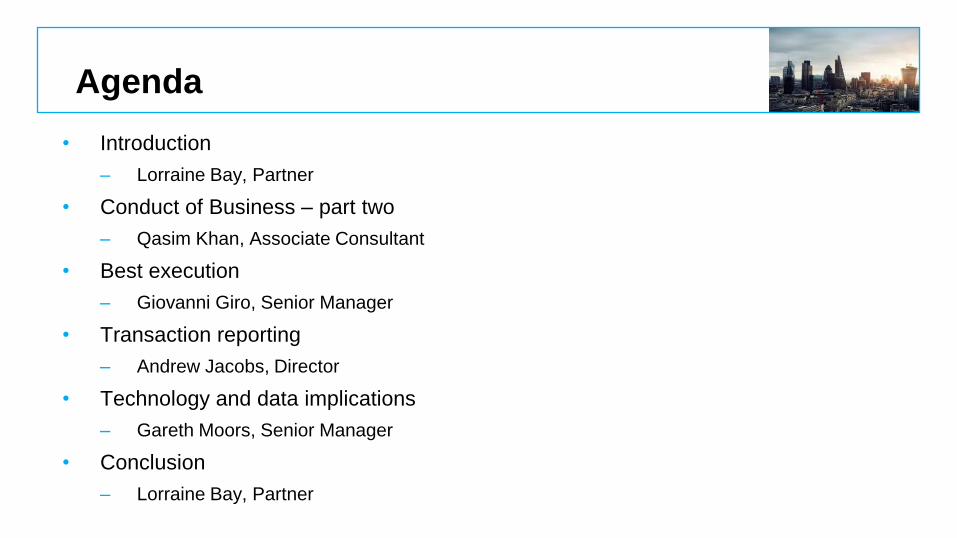

Agenda

• Introduction

– Lorraine Bay, Partner

• Conduct of Business – part two

– Qasim Khan, Associate Consultant

• Best execution

– Giovanni Giro, Senior Manager

• Transaction reporting

– Andrew Jacobs, Director

• Technology and data implications

– Gareth Moors, Senior Manager

• Conclusion

– Lorraine Bay, Partner

Our previous seminar

MiFID II

Market structure

Conduct of Business

Authorisations

PRECISE. PROVEN. PERFORMANCE.

Colour palette for PowerPoint presentations

Primary Cyan

R0 G174 B239

Primary Black

R35 G31 B32

Secondary Red

R191 G49 B26

Secondary colour palette

Primary colour palette

Secondary Maroon

R163 G0 B70 Secondary Purple

R113 G20 B113 Secondary Deep Purple

R96 G82 B112 Secondary Light Purple

R147 G151 B203

Secondary Pastel Green

R122 G204 B200 Secondary Bottle Green

R0 G146 B143 Secondary Pastel Blue

R80 G200 B232 Secondary Blue

R79 G138 B190 Secondary Light Green

R169 G195 B152 Secondary Bright Green

R122 G193 B67 Secondary Deep Green

R109 G141 B36 Secondary Olive

R164 G148 B0 Secondary Bright Yellow

R235 G215 B35 Secondary Deep Yellow

R229 G181 B59 Secondary Ecru

R200 G177 B139

Secondary Light Blue

R195 G208 B228 Conduct of Business – part two Qasim Khan, Associate Consultant

www.moorestephens.co.uk

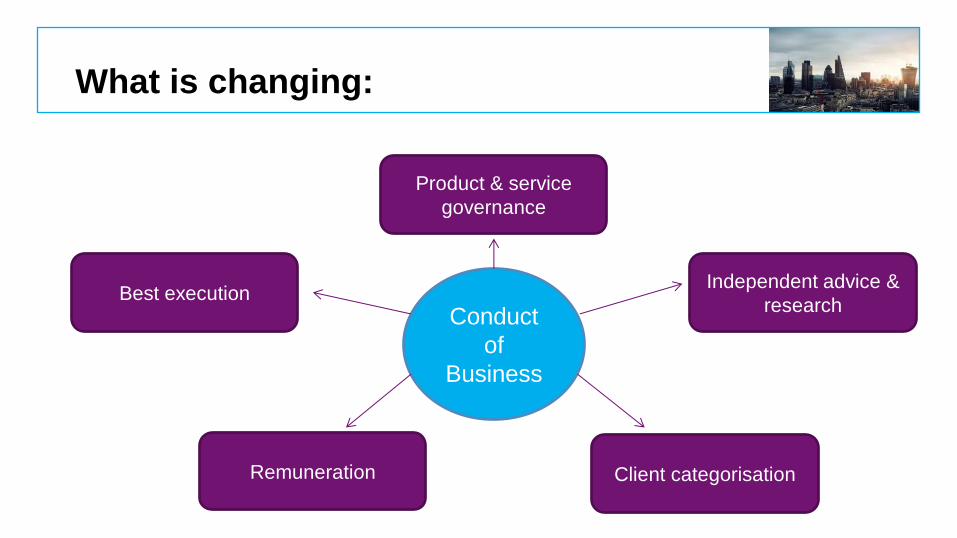

What is changing:

Client categorisation

Product & service

governance

Independent advice &

research Best execution

Remuneration

Conduct

of

Business

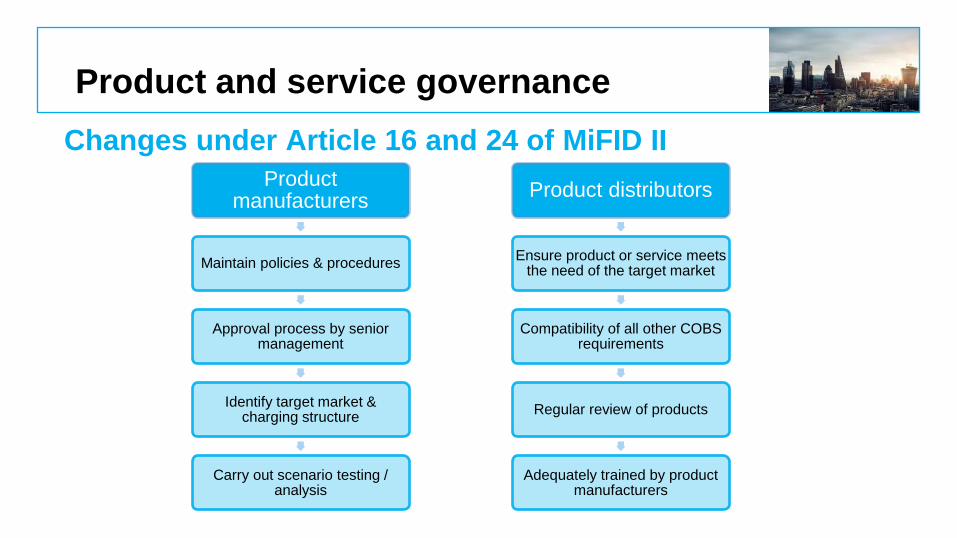

Product and service governance

Changes under Article 16 and 24 of MiFID II

Product manufacturers

Maintain policies & procedures

Approval process by senior management

Identify target market & charging structure

Carry out scenario testing / analysis

Product distributors

Ensure product or service meets the need of the target market

Compatibility of all other COBS requirements

Regular review of products

Adequately trained by product manufacturers

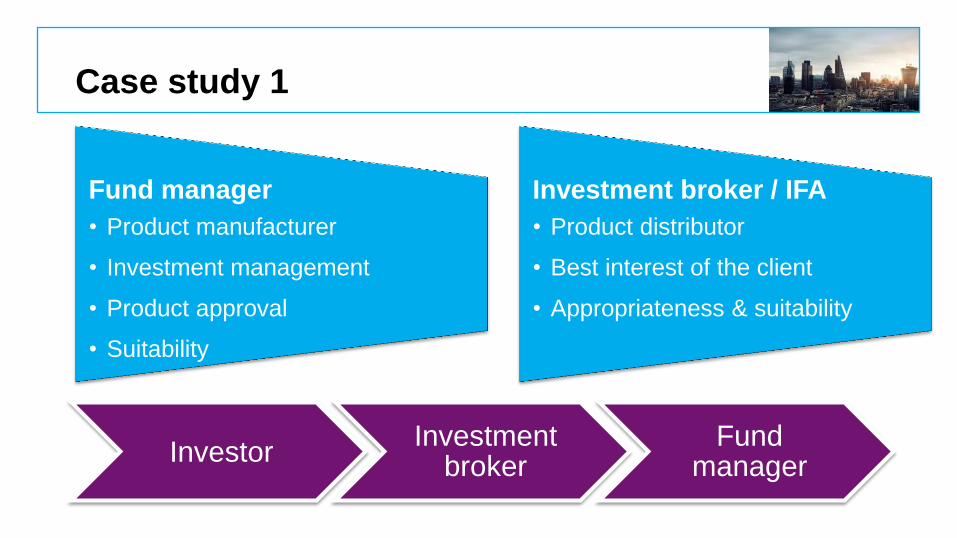

Case study 1

Fund manager

• Product manufacturer

• Investment management

• Product approval

• Suitability

Investment broker / IFA

• Product distributor

• Best interest of the client

• Appropriateness & suitability

Investor Investment

broker Fund

manager

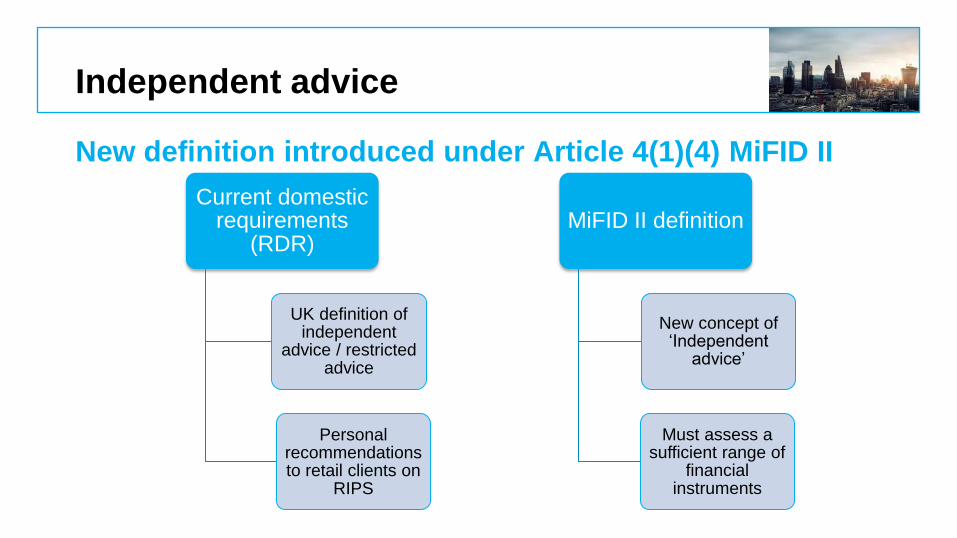

Independent advice

New definition introduced under Article 4(1)(4) MiFID II

Current domestic requirements

(RDR)

UK definition of independent

advice / restricted advice

Personal recommendations to retail clients on

RIPS

MiFID II definition

New concept of ‘Independent

advice’

Must assess a sufficient range of

financial instruments

Investment research & rebates

Changes under Article 36 and 37 MiFID II delegated

regulation

Unbundled and paid

separately

Pay for research directly

Ban on rebates

Update policies, systems

and controls

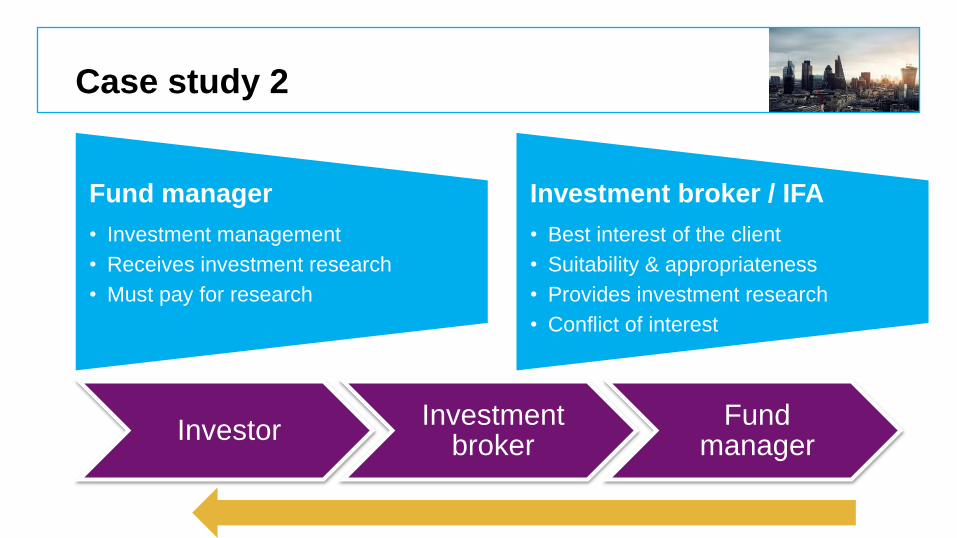

Case study 2

Fund manager

• Investment management

• Receives investment research

• Must pay for research

Investment broker / IFA

• Best interest of the client

• Suitability & appropriateness

• Provides investment research

• Conflict of interest

Investor Investment

broker Fund

manager

Client categorisation

Changes to be introduced under MiFID II

• To be treated as retail

• Re-calibrated quantitative test for opt-up

National Government & Local Public Authorities

• Client agreements

• Communication to professional clients

Professional clients

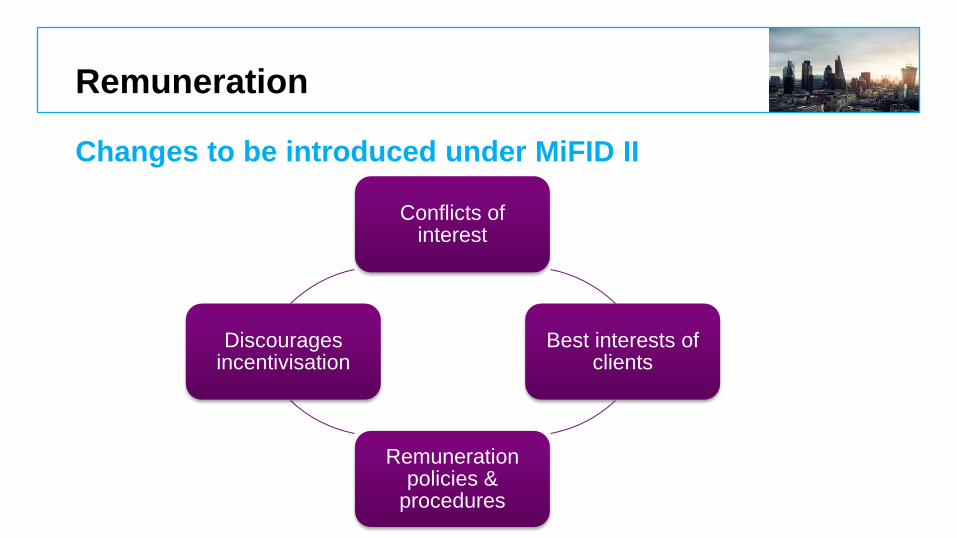

Remuneration

Changes to be introduced under MiFID II

Conflicts of

interest

Best interests of clients

Remuneration policies &

procedures

Discourages incentivisation

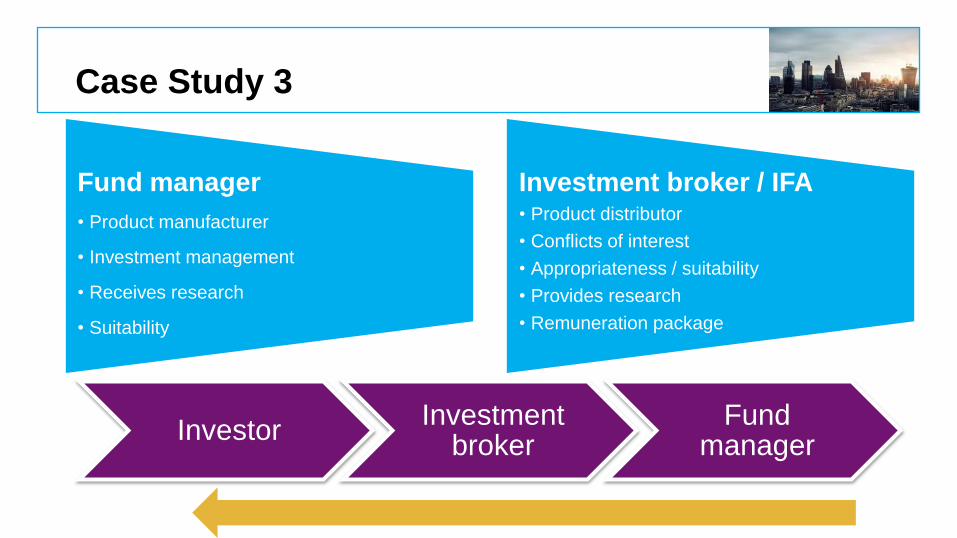

Case Study 3

Fund manager

• Product manufacturer

• Investment management

• Receives research

• Suitability

Investment broker / IFA • Product distributor

• Conflicts of interest

• Appropriateness / suitability

• Provides research

• Remuneration package

Investor Investment

broker Fund

manager

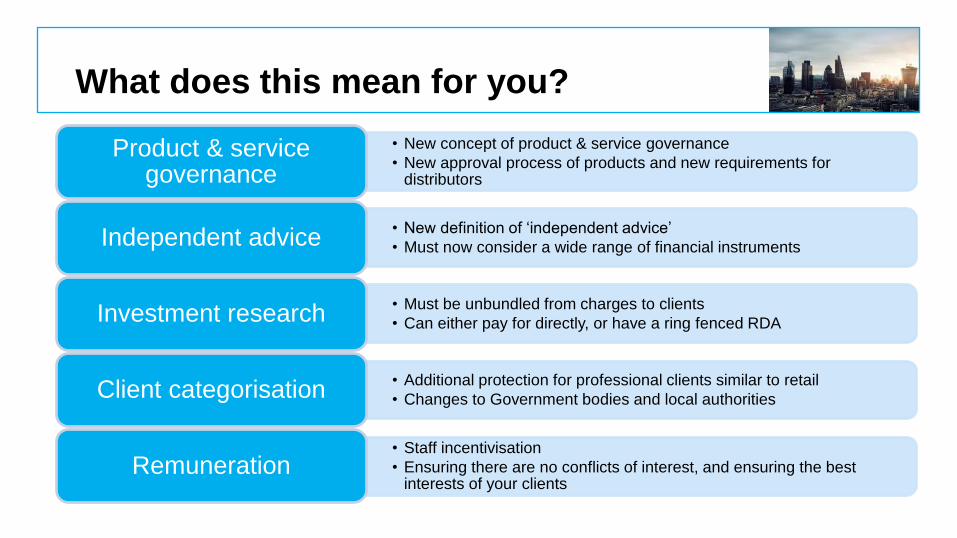

What does this mean for you?

• New concept of product & service governance

• New approval process of products and new requirements for distributors

Product & service governance

• New definition of ‘independent advice’

• Must now consider a wide range of financial instruments Independent advice

• Must be unbundled from charges to clients

• Can either pay for directly, or have a ring fenced RDA Investment research

• Additional protection for professional clients similar to retail

• Changes to Government bodies and local authorities Client categorisation

• Staff incentivisation

• Ensuring there are no conflicts of interest, and ensuring the best interests of your clients

Remuneration

PRECISE. PROVEN. PERFORMANCE.

Colour palette for PowerPoint presentations

Primary Cyan

R0 G174 B239

Primary Black

R35 G31 B32

Secondary Red

R191 G49 B26

Secondary colour palette

Primary colour palette

Secondary Maroon

R163 G0 B70 Secondary Purple

R113 G20 B113 Secondary Deep Purple

R96 G82 B112 Secondary Light Purple

R147 G151 B203

Secondary Pastel Green

R122 G204 B200 Secondary Bottle Green

R0 G146 B143 Secondary Pastel Blue

R80 G200 B232 Secondary Blue

R79 G138 B190 Secondary Light Green

R169 G195 B152 Secondary Bright Green

R122 G193 B67 Secondary Deep Green

R109 G141 B36 Secondary Olive

R164 G148 B0 Secondary Bright Yellow

R235 G215 B35 Secondary Deep Yellow

R229 G181 B59 Secondary Ecru

R200 G177 B139

Secondary Light Blue

R195 G208 B228 Best execution Giovanni Giro, Senior Manager

www.moorestephens.co.uk

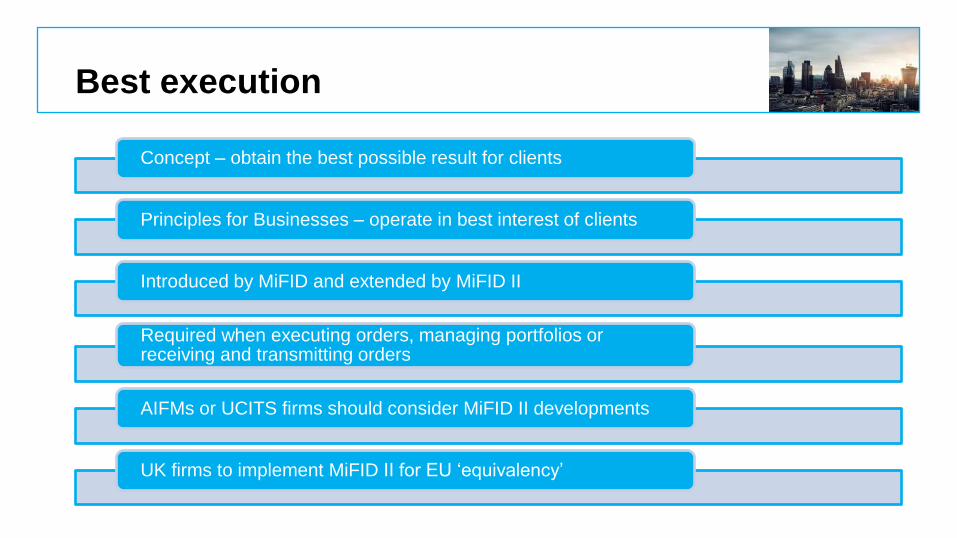

Best execution

Concept – obtain the best possible result for clients

Principles for Businesses – operate in best interest of clients

Introduced by MiFID and extended by MiFID II

Required when executing orders, managing portfolios or receiving and transmitting orders

AIFMs or UCITS firms should consider MiFID II developments

UK firms to implement MiFID II for EU ‘equivalency’

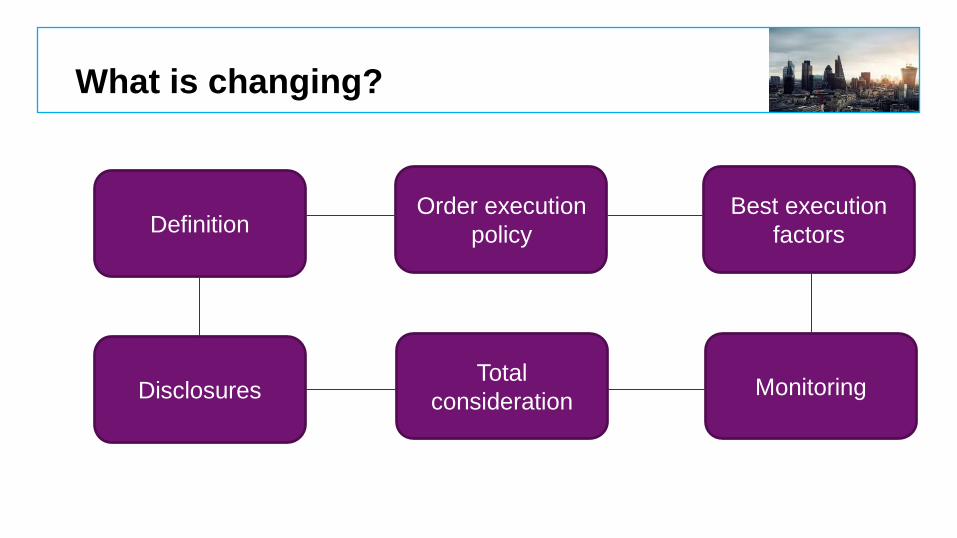

What is changing?

Definition Order execution

policy

Best execution

factors

Disclosures Total

consideration Monitoring

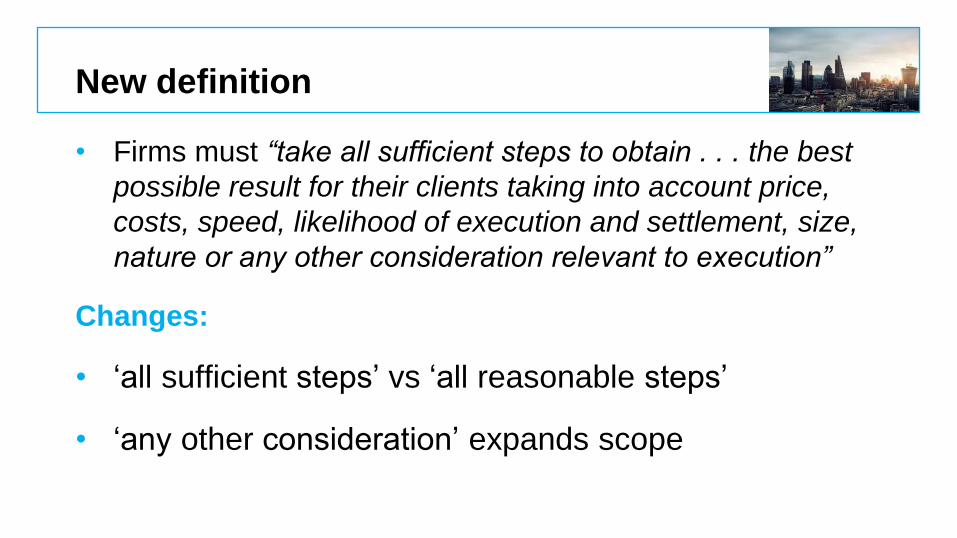

New definition

• Firms must “take all sufficient steps to obtain . . . the best

possible result for their clients taking into account price,

costs, speed, likelihood of execution and settlement, size,

nature or any other consideration relevant to execution”

Changes:

• ‘all sufficient steps’ vs ‘all reasonable steps’

• ‘any other consideration’ expands scope

Execution factors

Type of service offered and type of order

Class of financial instrument

Execution venue

No factor can be considered in isolation

Best possible overall results on a consistent basis

Total consideration

• Price of financial instrument + costs relating to execution

• All expenses directly relating to the execution of the order

– External costs: commissions, fees, taxes, exchange fees, venue fees, third

party fees, clearing and settlement costs

– Internal costs: firm’s own spread / commission

• Consider all fees and costs when choosing a venue

• Cannot discriminate unfairly between venues

• ‘Fair price’ of OTC products

• Compare market prices of similar products

Related requirements

No payments for order flow between brokers and market makers

Avoid preference of one venue over another

Rules on inducements and conflicts of interest

Exemption from best execution upon ‘genuine’ client instruction

Record keeping

Monitoring best execution

• Monitor effectiveness of order execution arrangements

• Review order execution policy

• Identify & correct any deficiencies

• Consider implicit costs when monitoring execution performance

• Review the quality of execution of venues used

• Check that execution venues provide best possible result

• Publish analysis of venues’ performance

• Detailed monitoring processes

Disclosures

• Top 5 execution venues:

– for each class of financial instruments in terms of trading volumes &

quality of execution obtained

• Information on venues’ fees must be fair, clear & not misleading

• Pre-trade analytics & post-trade reporting

• Trading venues & SIs to publish data on quality of execution

• Larger volume of data

Order execution policy

Execution policy must be disclosed & obtain client consent

Policy must be clear, detailed & understandable

Customised to type of investment & service

Include factors for selection of venues

Explain how the firm will take ‘all sufficient steps’

Execution strategies, procedures & results of monitoring

Notify clients of any material changes

What does this mean for you?

Greater challenge around best execution

Consider impact of key changes

Calculate value of total consideration

‘Fairness’ of order execution as standard practice

Update IT systems for data collection and disclosures

Adopt effective monitoring procedures

Redraft order execution policy

….all in good time before the implementation date

1

5

2 3

4 6

7

PRECISE. PROVEN. PERFORMANCE.

Colour palette for PowerPoint presentations

Primary Cyan

R0 G174 B239

Primary Black

R35 G31 B32

Secondary Red

R191 G49 B26

Secondary colour palette

Primary colour palette

Secondary Maroon

R163 G0 B70 Secondary Purple

R113 G20 B113 Secondary Deep Purple

R96 G82 B112 Secondary Light Purple

R147 G151 B203

Secondary Pastel Green

R122 G204 B200 Secondary Bottle Green

R0 G146 B143 Secondary Pastel Blue

R80 G200 B232 Secondary Blue

R79 G138 B190 Secondary Light Green

R169 G195 B152 Secondary Bright Green

R122 G193 B67 Secondary Deep Green

R109 G141 B36 Secondary Olive

R164 G148 B0 Secondary Bright Yellow

R235 G215 B35 Secondary Deep Yellow

R229 G181 B59 Secondary Ecru

R200 G177 B139

Secondary Light Blue

R195 G208 B228 Transaction reporting Andrew Jacobs, Director

www.moorestephens.co.uk

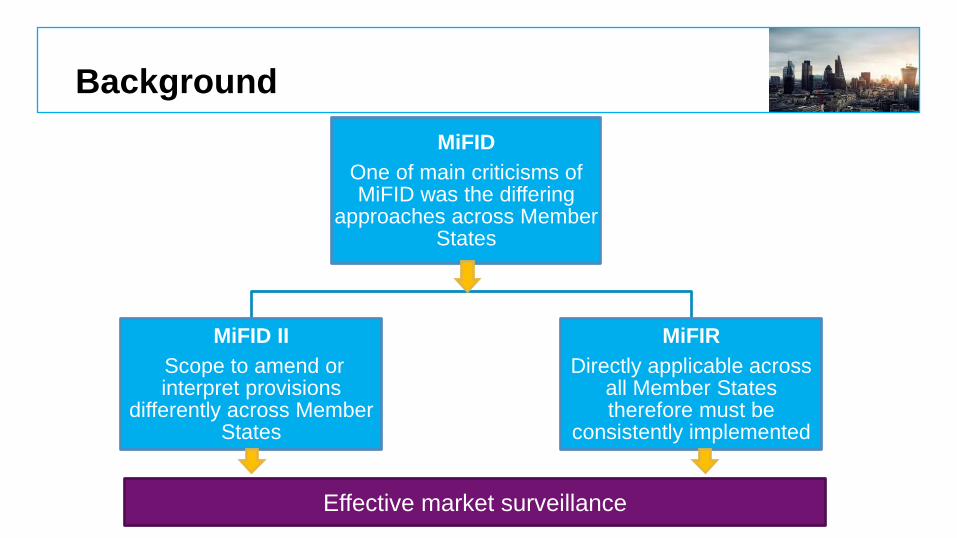

Background

MiFID

One of main criticisms of MiFID was the differing

approaches across Member States

MiFID II

Scope to amend or interpret provisions

differently across Member States

MiFIR

Directly applicable across all Member States therefore must be

consistently implemented

Ensure effective market surveillance

Effective market surveillance

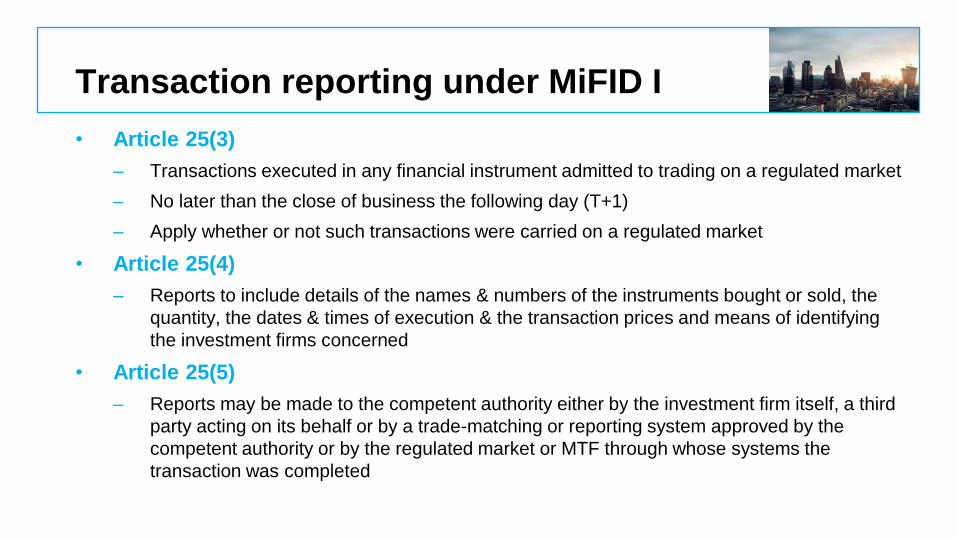

Transaction reporting under MiFID I

• Article 25(3)

– Transactions executed in any financial instrument admitted to trading on a regulated market

– No later than the close of business the following day (T+1)

– Apply whether or not such transactions were carried on a regulated market

• Article 25(4)

– Reports to include details of the names & numbers of the instruments bought or sold, the

quantity, the dates & times of execution & the transaction prices and means of identifying

the investment firms concerned

• Article 25(5)

– Reports may be made to the competent authority either by the investment firm itself, a third

party acting on its behalf or by a trade-matching or reporting system approved by the

competent authority or by the regulated market or MTF through whose systems the

transaction was completed

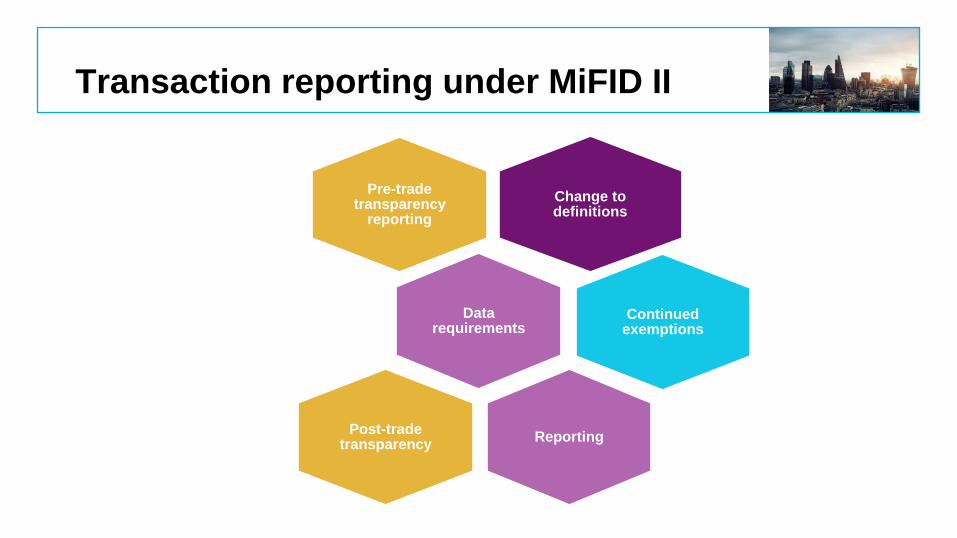

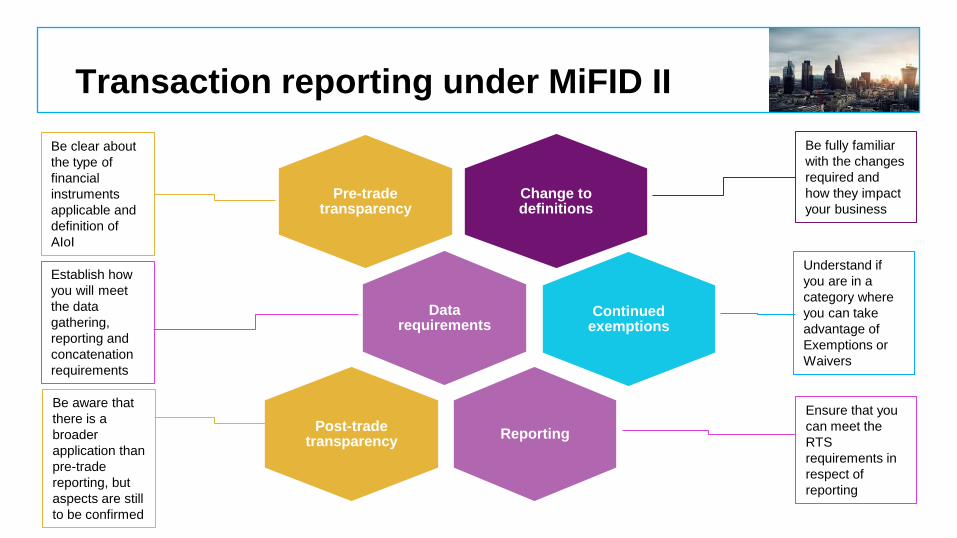

Transaction reporting under MiFID II

Change to definitions

Pre-trade transparency

reporting

Data requirements

Continued exemptions

Reporting Post-trade

transparency

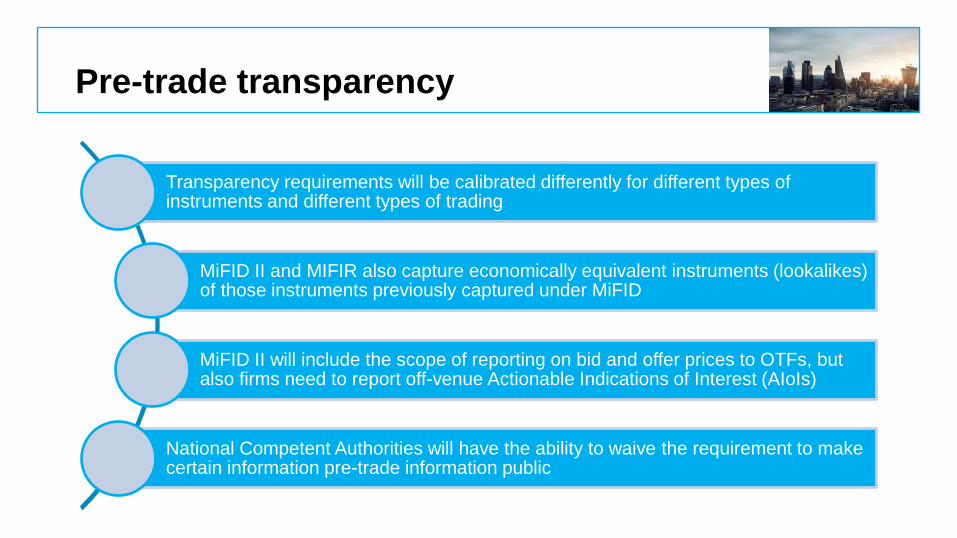

Pre-trade transparency

Transparency requirements will be calibrated differently for different types of instruments and different types of trading

MiFID II and MIFIR also capture economically equivalent instruments (lookalikes) of those instruments previously captured under MiFID

MiFID II will include the scope of reporting on bid and offer prices to OTFs, but also firms need to report off-venue Actionable Indications of Interest (AIoIs)

National Competent Authorities will have the ability to waive the requirement to make certain information pre-trade information public

Post-trade transparency

Post-trade transparency around price and volume also extended to venues, covering the same range of financial instruments as subject to pre-trade requirements

Technical standards not fully concluded at this stage

Exact length of delay permissible in respect of publication of information yet to be confirmed

Publication is required to be as close to real time as possible, but this aspect is also still to be confirmed by the European Commission

Definition changes

Article 26 MiFIR

• Transactions executed in any financial instrument

• As quickly as possible but no later than the close of business the

following day (T+1)

Meaning of a Transaction

• Article 2 RTS 22

• The conclusion of an acquisition or disposal of a financial instrument

shall constitute a transaction

Financial instruments in scope

1. Financial instruments admitted to or traded on a trading venue or for which a request for admission to trading has been made

2. Financial instruments where the underlying is a financial instrument traded on a trading venue

3. Financial instruments where the underlying is an index or a basket composed of financial instruments traded on a trading venue

Execution of a transaction

Article 3 RTS 22

• An investment firm shall be deemed to have executed a transaction where

it provides any of the following services or performs any of the following

activities which results in a transaction:

– reception & transmission of orders in relation to one or more financial instruments

– execution of orders on behalf of clients

– dealing on own account

– making an investment decision in accordance with a discretionary mandate given

by a client

– transfer of financial instruments to or from accounts

Data fields

More complex sphere of data

requiring advanced linkage

Simple data set

• Increase from 24 data fields to 65 under MiFID II

• Only 13 of the existing fields remain unchanged

• Identifiers introduced: distinctions between natural

persons, computer algorithms & legal entities

Data fields

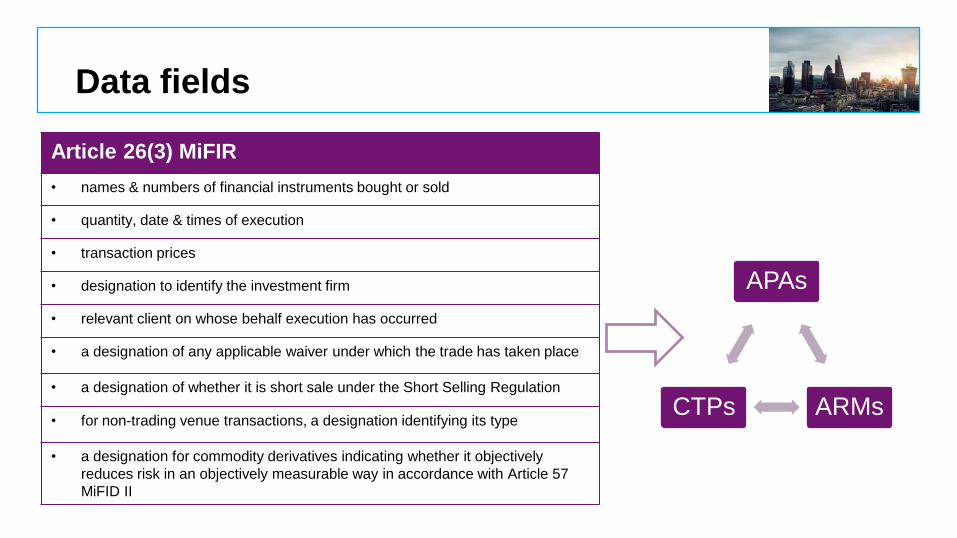

Article 26(3) MiFIR

• names & numbers of financial instruments bought or sold

• quantity, date & times of execution

• transaction prices

• designation to identify the investment firm

• relevant client on whose behalf execution has occurred

• a designation of any applicable waiver under which the trade has taken place

• a designation of whether it is short sale under the Short Selling Regulation

• for non-trading venue transactions, a designation identifying its type

• a designation for commodity derivatives indicating whether it objectively

reduces risk in an objectively measurable way in accordance with Article 57

MiFID II

APAs

ARMs CTPs

Who is responsible for reporting?

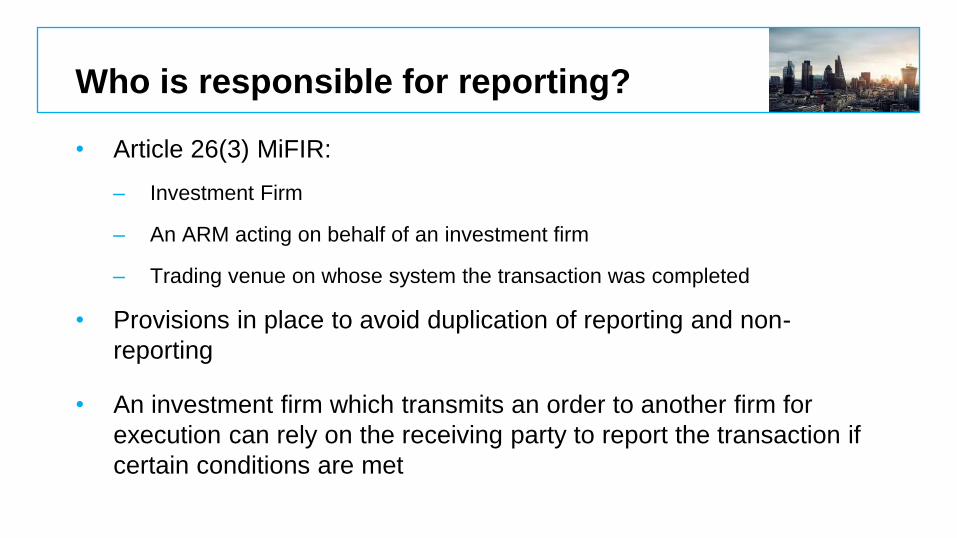

• Article 26(3) MiFIR:

– Investment Firm

– An ARM acting on behalf of an investment firm

– Trading venue on whose system the transaction was completed

• Provisions in place to avoid duplication of reporting and non-

reporting

• An investment firm which transmits an order to another firm for

execution can rely on the receiving party to report the transaction if

certain conditions are met

Exclusions & waivers

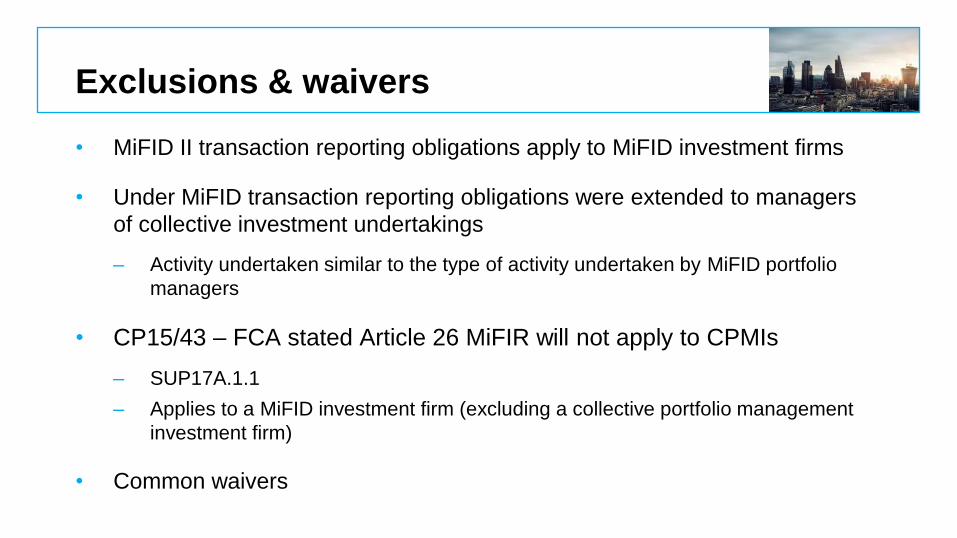

• MiFID II transaction reporting obligations apply to MiFID investment firms

• Under MiFID transaction reporting obligations were extended to managers

of collective investment undertakings

– Activity undertaken similar to the type of activity undertaken by MiFID portfolio

managers

• CP15/43 – FCA stated Article 26 MiFIR will not apply to CPMIs

– SUP17A.1.1

– Applies to a MiFID investment firm (excluding a collective portfolio management

investment firm)

• Common waivers

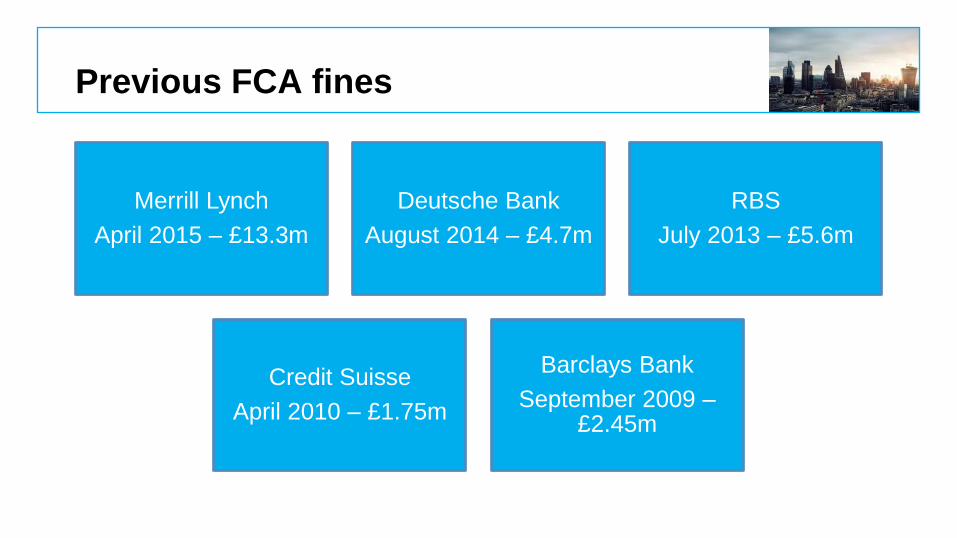

Previous FCA fines

Merrill Lynch

April 2015 – £13.3m

Deutsche Bank

August 2014 – £4.7m

RBS

July 2013 – £5.6m

Credit Suisse

April 2010 – £1.75m

Barclays Bank

September 2009 – £2.45m

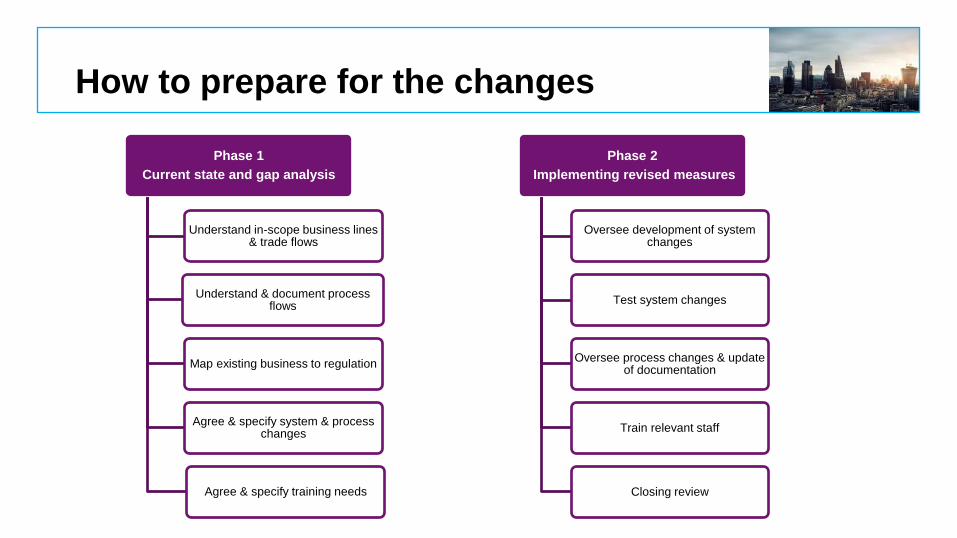

How to prepare for the changes

Phase 1

Current state and gap analysis

Understand in-scope business lines & trade flows

Understand & document process flows

Map existing business to regulation

Agree & specify system & process changes

Agree & specify training needs

Phase 2

Implementing revised measures

Oversee development of system changes

Test system changes

Oversee process changes & update of documentation

Train relevant staff

Closing review

PRECISE. PROVEN. PERFORMANCE.

Colour palette for PowerPoint presentations

Primary Cyan

R0 G174 B239

Primary Black

R35 G31 B32

Secondary Red

R191 G49 B26

Secondary colour palette

Primary colour palette

Secondary Maroon

R163 G0 B70 Secondary Purple

R113 G20 B113 Secondary Deep Purple

R96 G82 B112 Secondary Light Purple

R147 G151 B203

Secondary Pastel Green

R122 G204 B200 Secondary Bottle Green

R0 G146 B143 Secondary Pastel Blue

R80 G200 B232 Secondary Blue

R79 G138 B190 Secondary Light Green

R169 G195 B152 Secondary Bright Green

R122 G193 B67 Secondary Deep Green

R109 G141 B36 Secondary Olive

R164 G148 B0 Secondary Bright Yellow

R235 G215 B35 Secondary Deep Yellow

R229 G181 B59 Secondary Ecru

R200 G177 B139

Secondary Light Blue

R195 G208 B228 Technology and data implications Gareth Moors, Senior Manager

www.moorestephens.co.uk

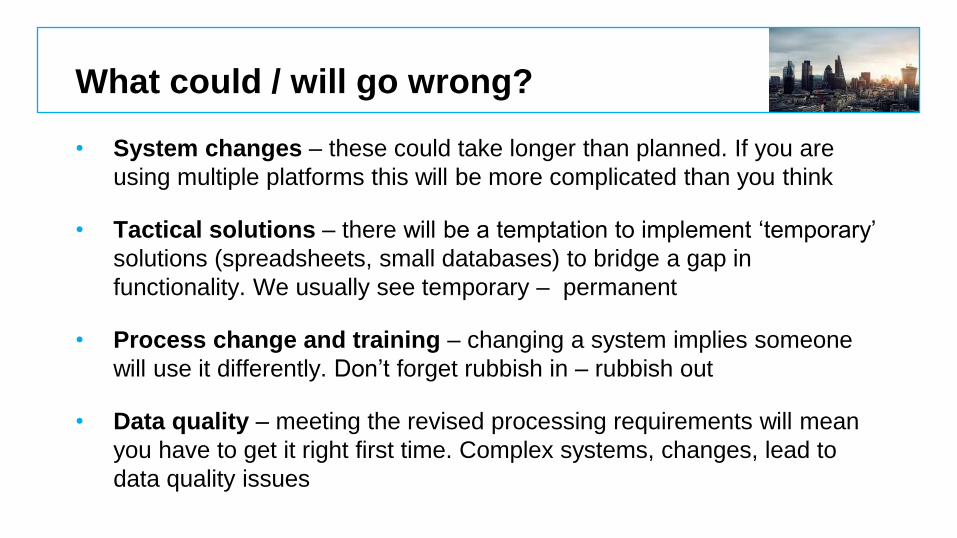

What could / will go wrong?

• System changes – these could take longer than planned. If you are

using multiple platforms this will be more complicated than you think

• Tactical solutions – there will be a temptation to implement ‘temporary’

solutions (spreadsheets, small databases) to bridge a gap in

functionality. We usually see temporary – permanent

• Process change and training – changing a system implies someone

will use it differently. Don’t forget rubbish in – rubbish out

• Data quality – meeting the revised processing requirements will mean

you have to get it right first time. Complex systems, changes, lead to

data quality issues

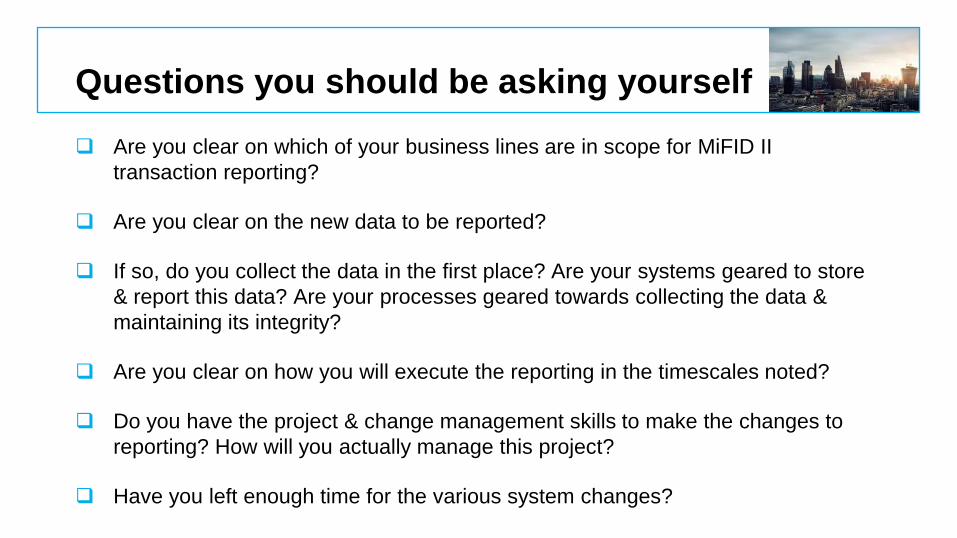

Questions you should be asking yourself

Are you clear on which of your business lines are in scope for MiFID II

transaction reporting?

Are you clear on the new data to be reported?

If so, do you collect the data in the first place? Are your systems geared to store

& report this data? Are your processes geared towards collecting the data &

maintaining its integrity?

Are you clear on how you will execute the reporting in the timescales noted?

Do you have the project & change management skills to make the changes to

reporting? How will you actually manage this project?

Have you left enough time for the various system changes?

Change to definitions

Pre-trade transparency

Data requirements

Continued exemptions

Reporting Post-trade

transparency

Transaction reporting under MiFID II

Be fully familiar

with the changes

required and

how they impact

your business

Establish how

you will meet

the data

gathering,

reporting and

concatenation

requirements

Ensure that you

can meet the

RTS

requirements in

respect of

reporting

Be clear about

the type of

financial

instruments

applicable and

definition of

AIoI

Be aware that

there is a

broader

application than

pre-trade

reporting, but

aspects are still

to be confirmed

Understand if

you are in a

category where

you can take

advantage of

Exemptions or

Waivers

PRECISE. PROVEN. PERFORMANCE.

Colour palette for PowerPoint presentations

Primary Cyan

R0 G174 B239

Primary Black

R35 G31 B32

Secondary Red

R191 G49 B26

Secondary colour palette

Primary colour palette

Secondary Maroon

R163 G0 B70 Secondary Purple

R113 G20 B113 Secondary Deep Purple

R96 G82 B112 Secondary Light Purple

R147 G151 B203

Secondary Pastel Green

R122 G204 B200 Secondary Bottle Green

R0 G146 B143 Secondary Pastel Blue

R80 G200 B232 Secondary Blue

R79 G138 B190 Secondary Light Green

R169 G195 B152 Secondary Bright Green

R122 G193 B67 Secondary Deep Green

R109 G141 B36 Secondary Olive

R164 G148 B0 Secondary Bright Yellow

R235 G215 B35 Secondary Deep Yellow

R229 G181 B59 Secondary Ecru

R200 G177 B139

Secondary Light Blue

R195 G208 B228 Conclusion Lorraine Bay, Partner

www.moorestephens.co.uk

Questions or comments?

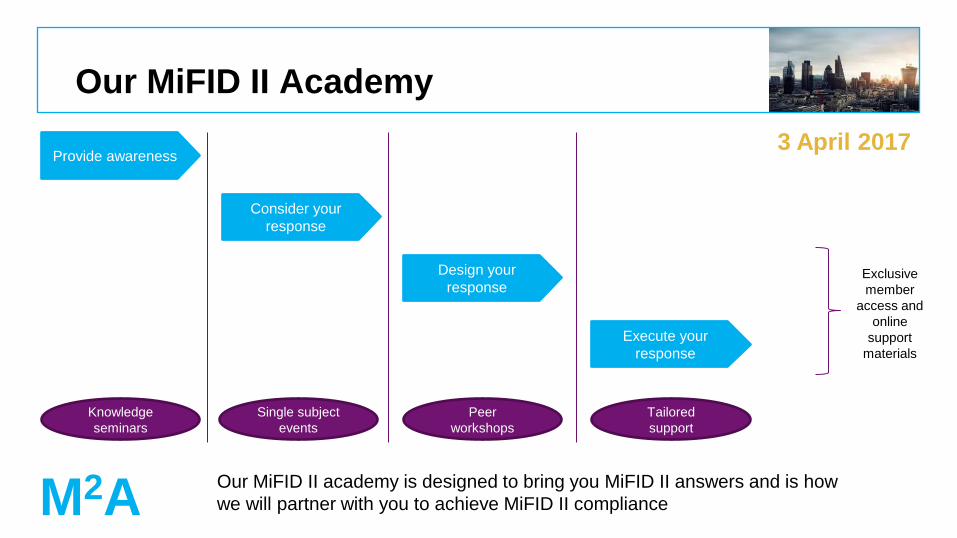

Our MiFID II Academy

Provide awareness

Consider your

response

Design your

response

Execute your

response

M2A

Exclusive

member

access and

online

support

materials

Knowledge

seminars

Single subject

events

Peer

workshops

Tailored

support

Our MiFID II academy is designed to bring you MiFID II answers and is how

we will partner with you to achieve MiFID II compliance

3 April 2017

Helping to keep up-to-date

• Financial Insight – our quarterly newsletter

• E-alerts – subscribe via [email protected]

• Regular seminars

• Follow us on Twitter: @MSFinSec

• Visit our website:

www.moorestephens.co.uk/sectors/financial-services

PRECISE. PROVEN. PERFORMANCE. www.moorestephens.co.uk

MiFID II part two Wednesday 29 March 2017