Embed Size (px)

Citation preview

© 2017 Eversheds SutherlandAll Rights Reserved. This communication is for general informational purposes only and is not intended to constitute legal advice or a recommended course of action in any given situation. This communication is not intended to be, and should not be, relied upon by the recipient in making decisions of a legal nature with respect to the issues discussed herein. The recipient is encouraged to consult independent counsel before making any decisions or taking any action concerning the matters in this communication. This communication does not create an attorney-client relationship between Eversheds Sutherland (US) LLP and the recipient. Eversheds Sutherland (US) LLP is part of a global legal practice, operating through various separate and distinct legal entities, under Eversheds Sutherland. For a full description of the structure and a list of offices, please visit www.eversheds-sutherland.com.

Overview and Main Impacts forUS Financial Institutions

November 1, 2017

Andrew HendersonPartner, London

Holly SmithPartner, Washington DC

Michaela WalkerPartner, London

Meltem KodamanCounsel, Washington DC

Ray RamirezAssociate, Washington DC

Mastering the MiFID 2 Maze

Eversheds Sutherland

Speakers

Andrew HendersonLondon, UK+44 20 7919 [email protected]

Holly SmithWashington DC+1 202 383 [email protected]

Michaela WalkerLondon, UK+44 207 919 [email protected]

Meltem KodamanWashington DC+1 202 383 [email protected]

Ray RamirezWashington DC+1 202 383 [email protected]

Eversheds Sutherland

1 Overview

2 Considerations for US advisers

3 Investment research

4 Implications for US end users of derivatives

Agenda

Eversheds Sutherland

Overview

Eversheds Sutherland Mastering the MiFID 2 Maze

Overview of MiFID 2

─ MiFID 2 repeals and replaces the current Markets in Financial Instruments Directive (MiFID 1) with an EU Directive – requires Member State laws (discretion to impose further requirements) and an EU Regulation – direct application (no Member State discretion)

─ Additional Level 2 and Level 3 measures, providing further detailed rules and guidance

─ Wide application across financial services industry – covers investment banks, broker-dealers, investment managers, investment advisers, exchanges, markets, data providers

─ It only applies to AIFMD and UCITS firms with respect to “MiFID portfolio management” activities and not all MiFID 2 obligations apply, e.g., transaction reporting

─ Individual Member States may apply MiFID 2 requirements to non-MiFID 2 firms via “gold-plating”, e.g., UK applying requirements to AIF and UCITS managers

─ Now coming into force on January 3, 2018 (one-year extension from original deadline of January 3, 2017)

5

Eversheds Sutherland Mastering the MiFID 2 Maze

Overview of Requirements

─ Enhanced reporting: for trading venues

─ Derivatives: trading obligation, position reporting, position limits

─ Transaction reporting and recordkeeping

─ Investor protection: enhanced information for clients, tightening of rules on “inducements,” i.e., soft dollars, change to execution-only regime and duties to determine appropriateness, enhanced reporting for best execution

─ Organizational requirements: product governance and target markets, telephone recording, further rules on protection of client assets

─ Enhanced corporate governance requirements

─ Increased scope: removal of own account exemptions for derivatives

─ Increased powers for regulators: registration and product intervention

6

Eversheds Sutherland

Considerations for US Advisers

Eversheds Sutherland Mastering the MiFID 2 Maze

Territorial Scope and Third Countries

─ MiFID 2 does not change territorial scope of MiFID 1: activities through a branch in the EU

─ Different to AIFMD: no EU activity of “marketing”

─ MiFID 2 power to impose a branch requirement on a third-country firm: optional, not required

─ MiFIR third-country passport for per se professional clients and eligible counterparties: • “Overrides” Member State branch requirement• Equivalence determination

─ Relevant to US branches in London in the event of a hard Brexit

8

Eversheds Sutherland Mastering the MiFID 2 Maze

Territorial Scope and Delegation

─ Level 2 Regulation delegation – Art 31: does not result in delegation of senior management responsibility, i.e., “letter-box”; and does not alter relationship and obligations of EU investment firm and its clients

─ Service providers in third countries (portfolio management) – Art 32: cooperation agreement (compare AIFMD)

─ Commission Q&A on outsourcing under MiFID 1: no breach of obligations when outsourcing BUT no extra-territoriality (compare ESMA AIFMD Remuneration Guidelines)

─ FCA letter to AIMA: “Equivalent Level of Protection”

─ EU Managers may demand compliance

9

Eversheds Sutherland

Investment Research

Eversheds Sutherland Mastering the MiFID 2 Maze

Investment Research Rules

─ Particular area of concern for delegation

─ No longer permissible to pay using bundled or soft-dollar arrangements

─ Payment either by: • Client through a Research Payment Account (RPA); or• The investment firm out of its own resources

─ For RPA – duty to agree on research budget, to assess quality of research

─ Possible to pay for research using a commission-sharing arrangement

11

Eversheds Sutherland Mastering the MiFID 2 Maze

Commission FAQ – Issued October 26, 2017

─ General analysis on delegation of duties the same

─ Research may be bundled subject to• Identification• A reasonable assessment of the need for research• Appropriate controls, which include maintaining a clear audit trail

of payments made to research providers• Internal allocation/budgeting process

12

Eversheds Sutherland Mastering the MiFID 2 Maze

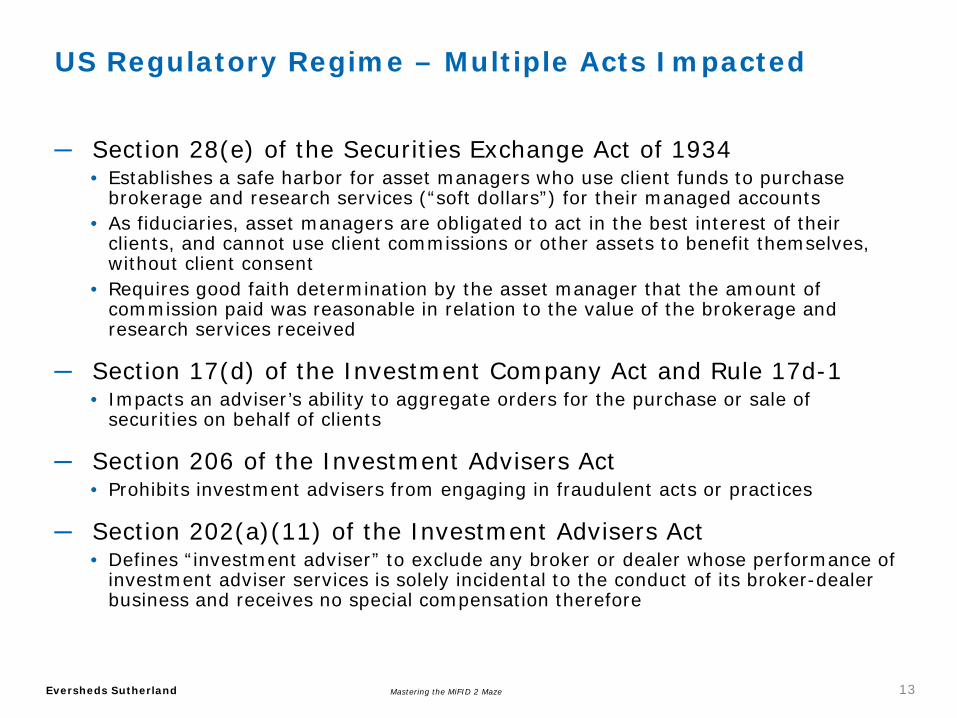

US Regulatory Regime – Multiple Acts Impacted

─ Section 28(e) of the Securities Exchange Act of 1934• Establishes a safe harbor for asset managers who use client funds to purchase

brokerage and research services (“soft dollars”) for their managed accounts• As fiduciaries, asset managers are obligated to act in the best interest of their

clients, and cannot use client commissions or other assets to benefit themselves, without client consent

• Requires good faith determination by the asset manager that the amount of commission paid was reasonable in relation to the value of the brokerage and research services received

─ Section 17(d) of the Investment Company Act and Rule 17d-1• Impacts an adviser’s ability to aggregate orders for the purchase or sale of

securities on behalf of clients

─ Section 206 of the Investment Advisers Act• Prohibits investment advisers from engaging in fraudulent acts or practices

─ Section 202(a)(11) of the Investment Advisers Act • Defines “investment adviser” to exclude any broker or dealer whose performance of

investment adviser services is solely incidental to the conduct of its broker-dealer business and receives no special compensation therefore

13

Eversheds Sutherland Mastering the MiFID 2 Maze

SEC No Action Letters – Issued October 26, 2017

─ SEC issued three no action letters to trade associations related to the research requirements of MiFID 2 to be consistent with the US Securities laws

─ Section 28(e) Safe Harbor No Action Letter• Provides no action position with respect to enforcement against US

money managers using client assets to make payments through an RPA• Conditioned upon:

• The money manager makes payments to the executing broker-dealer out of client assets for research alongside payments to that executing broker-dealer for execution

• The research payments are for research services that are eligible for the safe harbor under Section 28(e)

• The executing broker-dealer effects the securities transaction for purposes of Section 28(e)

• The executing broker-dealer is legally obligated by contract with the money manager to pay for research through the use of an RPA in connection with a Client Commission Arrangement (CCA)

• Letter available at: https://www.sec.gov/divisions/marketreg/mr-noaction/2017/sifma-amg-102617-28e.pdf

14

Eversheds Sutherland Mastering the MiFID 2 Maze

SEC No Action Letters – Issued October 26, 2017

─ Section 17(d) – Aggregation of Client Orders• Provides no action position with respect to enforcement against investment advisers

that aggregate orders for the sale or purchase of securities on behalf of clients• Conditioned upon:

• Each client in an aggregated order pays the average price for the security and the same cost of execution;

• The payment for research in connection with the aggregated order will be consistent with each applicable jurisdiction’s regulatory requirements and disclosures to the client; and

• Subsequent allocation of such trade will conform to the adviser’s allocation statement and/or the adviser’s allocation procedures

• Letter available at: https://www.sec.gov/divisions/investment/noaction/2017/ici-102617-17d1.htm

─ Section 202(a)(11) of the Advisers Act – Broker-Dealer Exclusion• Provides no action position for temporary period of 30 months from MiFID 2’s

implementation date with respect to enforcement against broker-dealers that provide research services that constitute investment advice

• Letter available at: https://www.sec.gov/divisions/investment/noaction/2017/sifma-102617-202a.htm

15

Eversheds Sutherland

Implications for US End Users of Derivatives

Eversheds Sutherland Mastering the MiFID 2 Maze

Three Primary Effects

─ Transparency

─ Position Limits

─ Trading Obligation

17

Eversheds Sutherland Mastering the MiFID 2 Maze

Transparency

─ MiFID 2 greatly expands the scope of reporting requirements

─ Primarily impacts trading venues and goes beyond derivatives

─ With respect to derivatives:• For the most part, the reporting requirements will be borne by

the EU-domiciled entity, e.g., the trading venue or EU-based counterparty

• Generally, requirement will be to obtain an entity identifier (which many entities already have) and, in some instances, waive confidentiality rights

18

Eversheds Sutherland Mastering the MiFID 2 Maze

Position Limits

─ What are position limits?• Hard caps on the size of a speculative position that an entity can take

─ To what transactions do they apply?• Derivatives listed on EU trading venues with an underlying physical commodity and

look-a-like OTC contracts

─ When do they apply?• Spot month• Other months

─ Are there exemptions from position limits available?• Hedge exemptions are available for non-financial entities

─ How is trading by affiliated entities treated?• Aggregation is required outside of a limited exemption for collective investment

vehicles

─ How do the EU position limits impact US market participants?

─ How do the EU position limits compare to US position limits?

19

Eversheds Sutherland Mastering the MiFID 2 Maze

Trading Obligation

─ Certain derivatives transactions will be required to be traded through an “organized trading facility” (OTF), “multi-lateral trading facility” (MTF) or “regulated market” (RM)

─ Akin to the trade execution requirement in the United States

─ Will only apply to swaps that are subject to mandatory clearing under the European Market Infrastructure Regulation that has been designated as subject to the trading obligation by ESMA

─ ESMA published its initial list of swaps that will be subject to the trading obligation last month; it is nearly identical to the list of transactions that are subject to the US trade execution requirement, i.e., interest rate swaps and index-based credit default swaps

20

Eversheds Sutherland Mastering the MiFID 2 Maze

Trading Obligation

─ The trading obligation applies to:• Financial counterparties (FCs)• Non-financial counterparties that exceed specified clearing

thresholds on a group basis (i.e., NFC+)• Third-country entities that would be an FC or NFC+ when trading

with an FC or NFC+

─ Exemptions are available for certain pension scheme arrangements and for intragroup transactions

21

Eversheds Sutherland Mastering the MiFID 2 Maze

Trading Obligation

─ There’s relief on the horizon!

─ On October 13, 2017, CFTC Chairman Chris Giancarlo and the European Commission’s Vice President for Financial Stability, Financial Services and Capital Markets Union, Valdis Dombrovskis, announced a “common approach on certain derivatives trading venues”• I.e., an agreement in principle to recognize each other’s trading obligations as

equivalent• See

http://www.cftc.gov/idc/groups/public/@newsroom/documents/file/dmo_cacdtv101317.pdf

─ The CFTC and European Commission must publish comparability determinations• Expected later this month

─ It’s anticipated that compliance in the US will be deemed compliance in the EU and vice versa

─ Even with equivalence, issues will likely remain• Reporting• Package transactions

22

Eversheds Sutherland Mastering the MiFID 2 Maze

A Few Additional Points – FX Forwards

─ Generally, will be classified as financial instruments when MiFID 2 takes effect

─ Will be subject to variation margin requirements as of the MiFID 2 effective date

─ Certain FX forwards will be exempt from regulation, e.g., those that are connected to a payment transaction• In certain instances, this represents a narrowing of existing

exemptions, e.g., the UK’s commercial use exemption

23

Eversheds Sutherland Mastering the MiFID 2 Maze

A Few Additional Points – Platform Trading

─ MiFID 2 places certain obligations on market participants that have or provide direct electronic access, engage in algorithmic trading, or engage in high-frequency trading.

─ What is “direct electronic access”?• What are the implications of having “direct electronic access”?

─ What is “algorithmic trading”?• What are the implications of engaging in “algorithmic trading”?

─ What is “high frequency trading”?• What are the implications of engaging in “high frequency

trading”?• What steps should US financial institutions take on these issues?

24

Eversheds Sutherland Mastering the MiFID 2 Maze

Questions?

25

eversheds-sutherland.com© 2017 Eversheds SutherlandAll rights reserved.

This communication cannot be used for the purpose of avoiding any penalties that may be imposed under federal, state or local tax law.

Andrew HendersonLondon, UK+44 20 7919 [email protected]

Holly SmithWashington DC+1 202 383 [email protected]

Michaela WalkerLondon, UK+44 207 919 [email protected]

Meltem KodamanWashington DC+1 202 383 [email protected]

Ray RamirezWashington DC+1 202 383 [email protected]

![The Markets in Financial Instruments Directive [ MiFID ] Thursday 1st November 2007 ALAN BURR, FSI](https://img.pdfslide.us/doc/110x75/56649e385503460f94b28c07/the-markets-in-financial-instruments-directive-mifid-thursday-1st-november.jpg)