Embed Size (px)

Citation preview

Country Profile 2004

MexicoThis Country Profile is a reference work, analysing thecountry’s history, politics, infrastructure and economy. It isrevised and updated annually. The Economist IntelligenceUnit’s Country Reports analyse current trends and provide atwo-year forecast.

The full publishing schedule for Country Profiles is nowavailable on our website at http://www.eiu.com/schedule

The Economist Intelligence Unit15 Regent St, London SW1Y 4LRUnited Kingdom

The Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The Economist Intelligence Unit delivers its information in four ways: through its digital portfolio, where itslatest analysis is updated daily; through printed subscription products ranging from newsletters to annualreference works; through research reports; and by organising seminars and presentations. The firm is amember of The Economist Group.

LondonThe Economist Intelligence Unit15 Regent StLondonSW1Y 4LRUnited KingdomTel: (44.20) 7830 1007Fax: (44.20) 7830 1023E-mail: [email protected]

New YorkThe Economist Intelligence UnitThe Economist Building111 West 57th StreetNew YorkNY 10019, USTel: (1.212) 554 0600Fax: (1.212) 586 0248E-mail: [email protected]

Hong KongThe Economist Intelligence Unit60/F, Central Plaza18 Harbour RoadWanchaiHong KongTel: (852) 2585 3888Fax: (852) 2802 7638E-mail: [email protected]

Website: www.eiu.com

Electronic deliveryThis publication can be viewed by subscribing online at www.store.eiu.com

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, on-line databasesand as direct feeds to corporate intranets. For further information, please contact your nearest EconomistIntelligence Unit office

Copyright© 2004 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication norany part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means,electronic, mechanical, photocopying, recording or otherwise, without the prior permissionof The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author's and the publisher's ability. However, theEconomist Intelligence Unit does not accept responsibility for any loss arising from reliance on it.

ISSN 0269-5596

Symbols for tables“n/a” means not available; “–” means not applicable

Printed and distributed by Patersons Dartford, Questor Trade Park, 151 Avery Way, Dartford, Kent DA1 1JS, UK.

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

Mexico 1

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

Contents

3 Regional overview3 Membership of organisations

4 Basic data

5 Politics5 Political background6 Recent political developments9 Constitution, institutions and administration10 Political forces14 International relations and defence

15 Resources and infrastructure15 Population16 Education18 Health19 Natural resources and the environment20 Transport, communications and the Internet23 Energy provision

25 The economy25 Economic structure27 Economic policy29 Economic performance30 Regional trends

32 Economic sectors32 Agriculture33 Manufacturing36 Mining and semi-processing37 Construction37 Financial services41 Other services

42 The external sector42 Trade in goods44 Invisibles and the current account46 Capital flows and foreign debt47 Foreign reserves and the exchange rate

49 Appendices49 Sources of information52 Reference tables52 Population52 Labour force52 Unemployment rates in urban areas52 Crude oil and gas production53 Non-financial public-sector finances53 Federal government budget revenue and expenditure53 Money supply54 Interest rates

2 Mexico

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

54 Gross domestic product54 Gross domestic product by sector55 Gross domestic product by expenditure55 Prices and earnings55 Production of principal crops56 Livestock production56 Manufacturing production56 Minerals production57 Stockmarket indicators57 Merchandise sales57 Tourism57 Main exports and imports58 Main trading partners58 Balance of payments59 Total foreign investment59 External debt, World Bank series59 Gross external debt, national estimates60 Amortisation schedule of global external debt60 Foreign reserves60 Exchange rates

Mexico 3

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

Regional overview

Membership of organisations

The North American Free-Trade Agreement (NAFTA), which came into force onJanuary 1st 1994, will liberalise trade over a 15-year period, although someacceleration of the process was negotiated subsequently. Acknowledgingimbalances in development, the timetable for Mexico to dismantle its tradebarriers is more gradual than that for the US and Canada, and special rulesapply to trade in textiles, vehicles and parts, and agricultural products. Inaddition, the state has retained exclusive rights to ownership, production andinvestment in oil, gas, refining, petro-chemicals, nuclear energy and electricity.The treaty also covers trade in services, including overland transport, ports,telecommunications, financial services and government procurement.

A free-trade agreement between Mexico and the EU was signed on March 23rd2000, and came into force on July 1st. Complete elimination of tariffs will taketen years, with the tariff reduction timetable also addressing the imbalancebetween both parties. Agricultural products deemed sensitive by both partiesare excluded, including several crops, meat, sugar and milk products. Rules oforigin are in the 40-60% range, with those for cars starting at 45%, beforeincreasing to a permanent level of 60% by 2005.

Mexico joined the Asia-Pacific Economic Co-operation (APEC) forum inNovember 1993. APEC works to reduce tariffs and other trade barriers acrossthe Asia-Pacific region. Unlike other multilateral trade bodies, APEC operates onthe basis of non-binding commitments. Decisions made within APEC arereached by consensus and commitments are undertaken voluntarily. APEC has21 member economies: Australia; Brunei Darussalam; Canada; Chile; China;Hong Kong, China; Indonesia; Japan; South Korea; Malaysia; Mexico; NewZealand; Papua New Guinea; Peru; the Philippines; Russia; Singapore; ChineseTaipei; Thailand; the US; Vietnam.

NAFTA

The Mexico-EU free-tradeagreement

APEC

4 Mexico

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

Basic data

1,964,375 sq km

103.6m (according to estimates from the Consejo Nacional de Población(Conapo, the National Population Council)

Population (m), 2000

Mexico City (capital) 17.8Guadalajara 3.7Monterrey 3.2

Tropical in the south, temperate in the highlands, dry in the north

Hottest month, May, 12-26°C (average daily minimum and maximum); coldestmonth, January, 6-19°C; driest month, February, 5 mm average rainfall; wettestmonth, July, 170 mm average rainfall

Spanish is the official language. Over 60 indigenous languages are also spoken,mainly Náhuatl (1.2m speakers), Maya (714,000), Mixtec (387,000) and Zapotec(403,000)

Metric system

Peso (Ps). Average exchange rate in 2002: Ps9.68:US$1; exchange rate onFebruary 23rd 2003: Ps10.9:US$1

Six hours behind GMT in Mexico City

January 1st, February 5th, March 21st, Maundy Thursday, Good Friday, May 1stand 5th, September 16th, October 12th, All Souls’ Day (partial), November 20th,December 12th (partial) and 25th

Main towns

Climate

Weather in Mexico City(altitude 2,309 metres)

Languages

Measures

Currency

Time

Public holidays

Land area

Population

Mexico 5

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

Politics

The election of Vicente Fox Quesada of the Partido Acción Nacional (PAN) aspresident in July 2000 signified the start of a new era in Mexican politics, endingseven decades of political domination by the Partido RevolucionarioInstitucional (PRI). Mr Fox pursues similar market-based policies to those ofprevious administrations. Governability has been weakened, as for the first timein the country’s modern history the ruling party does not have a majority ineither house of Congress. The PAN saw a decline in its representation in theChamber of Deputies (the lower house) following the July 2003 legislativeelections. It will remain in a minority position in the lower house and theSenate until the elections in 2006. Under Mr Fox, consensus-building betweenthe executive and Congress has been poor, and this has severely delayed thepassage of legislation.

Political background

Independence from Spain was achieved in 1821 but Mexico suffered civil warsand predatory incursions. Texas seceded from Mexico in 1835-36. In 1845 a warbroke out with the US, which cost Mexico the additional territorial losses of thestates of California, Arizona and New Mexico. In 1864 France imposed aHapsburg archduke, Maximilian, as emperor. However, after the withdrawal ofFrench troops in 1867, the archduke was quickly overthrown and executed.Under the dictatorship of General Porfirio Díaz (1876-1911), order was imposedand the economy developed. When he engineered his own re-election for theseventh time in 1910, however, opposition forces led by Francisco Maderorebelled. They were joined by peasants who were led by Emiliano Zapata.General Díaz was forced into exile in 1911 and Mr Madero became president, buthe was ousted and killed in 1913. New rebellions followed and although therebels were crushed, their ideals, including land reform, were incorporated into anew constitution in 1917.

General Plutarco Elías Calles (president from 1924 to 1928) had a major impacton political developments, particularly through the creation of the PartidoNacional Revolucionario (PNR). He also sought to suspend the practice ofCatholicism as the Church was deemed to challenge the power of the modernstate that the authorities were trying to establish. This sparked a rebellion byCatholic Mexico, known as the Cristero War (1926-29). The conflict was broughtto an end not by victory by either side but through negotiation. An agreementwas reached by church and state to co-exist and to keep their respective realmsseparate. Another important presidency was that of Lázaro Cárdenas (1934-40),who redistributed land and expropriated foreign oil companies. In 1938Mr Cárdenas re-named the party as the Partido de la Revolución Mexicana(PRM) and instituted a corporatist structure made up of labour, peasant and"middle class" movements. In 1945 the PRM was renamed the PartidoRevolucionario Institucional. For many years sustained economic growthensured that it enjoyed a high degree of popular support, and additionally theregime frequently co-opted potential opponents and engaged in electoral fraud

Instability and dictatorshipfollow independence

The PRI is created

6 Mexico

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

to ensure an absolute monopoly of power. Political stability came under strainin the late 1960s when intellectuals and students sought more politicalopenness, but were repressed by the state. A deterioration in economic policy inthe 1970s precipitated an external debt crisis in 1982 and the then president,Miguel de la Madrid (1982-88), was forced to embark on politically costlystructural reform. His choice of technocrat, Carlos Salinas de Gortari, as the PRI’scandidate in 1987 prompted a split in the PRI, led by a former minister and PRIpresident, Porfirio Muñoz Ledo, and a former governor of Michoacán,Cuauhtémoc Cárdenas, son of Lázaro Cárdenas, who had aimed to democratisethe presidential candidate selection process. They went on to form the FrenteDemocrático Nacional (FDN) alliance to contest the 1988 election withMr Cárdenas as their candidate. The alliance attracted the support of most of theleft. The official results in July 1988, alleged to be fraudulent, gave Mr Salinas avictory with only 50.4% of the vote—the lowest in the PRI's history.

During his presidency (1988-94) Mr Salinas began economic and politicalliberalisation, allowing opposition parties to win gubernatorial races. An up-rising in Chiapas in January 1994 by the Ejército Zapatista de LiberaciónNacional (EZLN) highlighted the fact that despite economic progress, socialtensions were mounting. Consequently, as well as negotiating with the EZLN,the government enacted electoral reform, granting autonomy to the InstitutoFederal Electoral (the Federal Electoral Institute, the electoral authority) and intro-ducing measures to reduce electoral fraud. Elections held in August 1994 wererecognised as transparent. Ernesto Zedillo of the PRI won the presidency with50.2% of the vote. In Congress the PRI held on to its majority, but lost seats to thePAN and the Partido de la Revolución Democrática (PRD, which was formed outof the FDN in 1989).

Mr Zedillo (1994-2000) continued the process of political reform, introducingchanges to the constitution to modernise the electoral rules. The PRI paid aheavy electoral toll throughout the Zedillo administration for the government’sunpopularity following the peso crisis in 1994-1995. For the first time in almost70 years, the PRI lost its majority in the Chamber of Deputies in the 1997 mid-term election, as well as a number of governorships and the mayorship of theFederal District. By the beginning of 2000 the opposition held the governorshipsof ten states. Confidence in clean elections had increased substantially andcandidates and regional issues had become more important. The presidentialelection of July 2000 brought sweeping political change when Mr Fox, thecandidate of the coalition formed by the PAN and the Partido Verde Ecologistade México (PVEM, the green party), defeated the PRI’s candidate, FranciscoLabastida, ending the party’s 71-year reign. Although Mr Fox’s share of the votewas the lowest ever obtained by a winning presidential candidate (42.4%), thisdid not affect his legitimacy as the PRI was defeated by a substantial margin.The PRI won 36.1% of the vote.

Recent political developments

On December 1st 2003 Mr Fox reached the midpoint in his six-year presidentialterm. An opinion poll published by a national daily newspaper, Reforma, on

Reforms accelerate in responseto unrest in 1994

A multiparty democracyemerges

Mr Fox reaches his term mid-point with little achieved

Mexico 7

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

the same day established that Mr Fox remained quite popular. Of thosequestioned, 58% approved of the way he was carrying out his job, whereas 34%disapproved. A much lower fraction approved of the government’s economicmanagement (37%). In fact, the Fox administration is widely perceived asineffectual and this has come about for a number of reasons, but has not beenhelped by the fact that the first non-PRI government in modern history has hadto cope with a difficult external economic environment for much of its time inoffice. Since coming to power in 2000, Mr Fox has had difficulty in gainingsupport for his reform policies. This is partly because of his own limited politicalexperience, negotiating capacity and clout, and his poor management ofrelations with the PAN hierarchy, and partly because of the PAN's minorityposition in Congress, and divisions within the PAN's prime negotiating partner,the PRI.

Following the PAN’s poor showing in the July 2003 congressional election,Mr Fox made a number of important changes to his cabinet in September ofthat year. The changes suggest that Mr Fox is keen to improve relations with thePAN by appointing career politicians from its ranks to replace technocrats.Mr Fox had previously tended to distance himself from the PAN, apparentlytaking its support for granted. A relative newcomer to politics, he was initiallyviewed with suspicion by some party grandees, who resented the fewpositions the party had in the cabinet. In addition, by bringing moreexperienced politicians into the cabinet, the government’s negotiating powershould strengthen. Mr Fox appointed Felipe Calderón Hinojosa as minister ofenergy to replace Ernesto Martens. Previously Mr Calderón had led the PANlegislators in the Chamber of Deputies (2000-03), served as PAN secretarygeneral (1993-95) and president (1996-99). If successful with energy reform,Mr Calderón would become a strong potential PAN presidential candidate forthe 2006 contest. Mr Fox appointed a long-standing personal ally and PANstalwart, Alberto Cárdenas Jiménez, as minister of the environment to replaceVíctor Lichtinger. Mr Cárdenas had previously served—and been quitepopular—as governor of the Pacific state of Jalisco (1995-2001).

Following the election for the Chamber of Deputies in July 2003, the PAN'sminority position was confirmed. This means that governability will continueto be impaired, and the passage of legislation slow, for the remainder ofMr Fox's term. The PAN lost 55 seats whereas the opposition parties, the PRIand the PRD, increased their representation in the lower house. However, noparty won a working majority (as was also the case in the 1997-2000 and 2000-03 legislatures). In the six governorship contests that also took place, the PANhad expected to make some gains. However, the number of states governed bythe PAN (two) and the PRI (four) did not change. The PRI won an importantstrategic victory in the governorship race in the northern state of Nuevo León,an important industrial centre and a traditional PAN stronghold. The PAN wonthe governorship of the central state of San Luis Potosí, ousting the PRI.

Cabinet reshuffle brings inmore career politicians

Minority position in Congressis confirmed

8 Mexico

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

Composition of the Chamber of Deputies, 2000-062000-03

Legislaturea2003-06

LegislatureRMb PRc Total RM PR Total

Partido Acción Nacional (PAN) 136 70 206 80 71 151Partido Revolucionario Institucional (PRI) 132 79 211 161 63 224

Partido de la Revolución Democrática (PRD) 24 26 50 56 41 97Partido Verde Ecologista de México (PVEM) 6 11 17 3 14 17

Partido del Trabajo (PT) 2 6 8 0 6 6Convergencia 0 3 3 0 5 5

Partido de la Sociedad Nacionalista (PSN) 0 3 3 0 0 0Partido Alianza Social (PAS) 0 2 2 0 0 0México Posible (MP) 0 0 0 0 0 0

Fuerza Ciudadana (FC) 0 0 0 0 0 0Partido Liberal Mexicano (PLM) 0 0 0 0 0 0

Total 300 200 500 300 200 500

a Initial share of seats but this changed owing to defections during the three years. b RM is relative majority (first-past-the-post). c PR isproportional representation.

Sources: Chamber of Deputies; Insituto Federal Electoral.

Under Mr Fox, the legislature has begun to fulfil its constitutional role as acounterweight to executive power. Although this is positive for democratisation,it has impaired governability owing to the government's minority position. As aresult, the government has had great difficulty in gaining congressional supportfor its reform programme. Fiscal reform to increase revenue and reduce thereliance on oil revenue, liberalisation of the electricity sector to boost supply andreduce prices, changes to labour legislation to reduce formal sector labour costs,and further liberalisation of telecommunications have all been subject to seriousCongressional delays. Following the inauguration of the 2003-06 Congress, thepolitical parties appeared willing to co-operate to make progress in passingreform. This became impossible when infighting within the PRI broke outtoward the end of 2003 between traditional statists and modernisers, and on apersonal level between the president of the PRI, Roberto Madrazo, and thesecretary general and (at the time) the leader of the PRI in the Chamber ofDeputies, Elba Esther Gordillo. Although the disputes appear to have beensettled for the time being, internal political considerations will continue toinfluence Mr Madrazo's actions and thereby the extent of the PRI's support forthe government. As a further round of gubernatorial races approaches in mid-2004 and the preparations for the presidential election begin in 2005, themomentum to pass reform will slow even further.

The 2003 legislative election also revealed a large degree of apathy amongvoters, with the level of abstention reaching almost 60%, the highest everrecorded. Although Congress now asserts more power (for most of the PRI eraCongress was a rubber stamp for executive decisions), its members remainlargely unaccountable to the electorate. As they cannot be re-elected tosuccessive terms, legislators depend upon their parties to help to find them jobswhen their terms in Congress come to an end. Hence members tend to followthe party whip rather than pursue their constituents’ interests.

Congress is stronger butunaccountable

Mexico 9

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

Important recent events

1998-99

The opposition continues to advance after significant progress in 1997, but the PRIproves resilient. Of the 17 governorships contested in 1998-99, only five go to theopposition. Francisco Labastida wins the first-ever PRI presidential primary, held atthe end of 1999.

July-December 2000

National elections are held. Vicente Fox Quesada, the PAN’s presidential candidate,wins the presidency and takes office on December 1st, appointing a mostly non-partisan pro-business cabinet.

2001-02

A sharp economic slowdown, inexperience in government and clashes withCongress contribute to a failure by the Fox administration to achieve its maininitiatives and a fall in its popularity.

July 2003

Congressional elections are held. The PAN lost 55 seats, whereas the PRI and the PRDincreased their representation, but no party won a working majority (as was also thecase in the 1997-2000 and 2000-03 legislatures). Abstention was around 60%—thehighest ever recorded.

Constitution, institutions and administration

The constitution was enacted in 1917. It subordinated the rights of privateproperty to public interest and made specific provision for land reform, as wellas stressing the rights of labour and curtailing the power and influence of theclergy. The constitution also established the framework for a federal systemcovering 31 states and the Distrito Federal (the Federal District, which includesMexico City) and provided for the separation of executive, legislative andjudicial powers. In practice, government has been centralised and, until themid-1990s, the executive dominated the other branches of government.Reforms implemented in 1994-95 gave the Suprema Corte de Justicia de laNación (SCJN, the Supreme Court) greater autonomy and Congress has alsogained strength. Mr Fox has called several times for a thorough revision of theconstitution, but far-reaching reform is unlikely in the near term.

Congress comprises the Senate (the upper house) and the Chamber of Deputies(the lower house). Senators serve for six years and deputies for three. Indivi-duals cannot be re-elected for either position. In the Chamber of Deputies, 300seats are allocated using the first-past-the-post system and 200 by proportionalrepresentation. In 1993, the number of senators was doubled from 64 to 128 sothat each state and the Federal District has three senators directly elected byrelative majority and one senator elected by the first minority principle (thecandidate that comes second in each state race). Of the directly elected seats inthe Senate, 64 are elected via the first-past-the-post system and 32 are electedusing proportional representation. Reforms approved by Congress in 1996 madeit easier for a single party to gain a working majority in Congress, but imposs-

A resilient constitution

Composition of Congress

10 Mexico

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

ible for any one party to achieve the two-thirds majority necessary to changethe constitution. Despite these reforms, the 2000 election result was unprece-dented in that no single party enjoys a working majority in either house.

The most important political post in the cabinet is that of minister of theinterior, head of the ministry charged with preserving the country’s politicalstability. The Ministry of Finance and Public Credit is responsible for economicpolicymaking at the highest level, although the Ministry of the Economy(formerly the Ministry for Trade and Industry) also plays a major role. TheMinistry of Foreign Relations has acquired greater importance under the Foxadministration, because of the priority that the government has placed onstrengthening bilateral relations with the US and on achieving a much moreactive role for Mexico internationally.

Political forces

Three parties dominate Mexican politics: the PAN, the PRI and the PRD. Aftermore than 60 years in opposition, the PAN won the presidency in the July 2000election. The PAN was founded in 1939 and has built up a support base mainlyin northern and central states and among the urban middle classes, although ithas widened slightly beyond these groups since the early 1990s. Althoughinclined to free-market policies, the party has also shown some populisttendencies. The leadership of Luis Felipe Bravo Mena, who was electedpresident of the party in March 1999, and re-elected for another three-year termon March 9th 2002, has been undermined by the authority of the party chiefs inCongress and by the powerful personality of Mr Fox. PAN members are dividedin their support for Mr Fox as a significant number consider that he hijacked theparty to further his personal ambition. Mr Fox largely shares the party’s policyorientation, notably in his strong support for free-market policies, but he is notseen as a loyal party servant and occasionally breaks from PAN positions. As aresult of his uncertain loyalty to the party line, the PAN cannot count on Mr Foxto put its interests first. Conversely, the president cannot count on the fullsupport of his own party for his legislative initiatives.

For the first time since it was established in 1929, the PRI is in opposition at thefederal level, a reality that has proved difficult for most of its members to accept.Detached from presidential power, the PRI is struggling to reinvent itself. Havinglacked any coherent ideology for decades, the party became a means of winningand exercising power, and largely followed the direction set by the president. Inaddition, since the early 1980s a clear separation developed between the party’straditionalists, mostly positioned in the legislature and local government, andits technocrats, a minority who dominated the federal executive.

Following the loss of the presidency, a battle for control of the party ensued,with the traditionalists emerging as the dominant force. In an election open toall citizens on February 24th 2002, Roberto Madrazo, a former presidential pre-candidate and governor of Tabasco, and Elba Esther Gordillo, the de facto leaderof the powerful Sindicato Nacional de Trabajadores de la Educación (SNTE, theNational Union of Teachers), were elected as party president and secretary-

Ranking of ministries

The PAN adapts to governmentunder Mr Fox

The PRI struggles to adapt toits loss of power

Mexico 11

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

general, respectively. Popular among its grassroots, and with a long career as aPRI member, Mr Madrazo has a populist touch, but he is also considered to be apragmatist. Several governors and legislators, however, have already evolved asimportant figures with authority, and Mr Madrazo frequently finds it difficult tomaintain party unity. This became impossible in late 2003 when clashesbetween traditional statists and modernisers broke out over government plansto extend value-added tax (VAT) to food and medicine and Mr Madrazo'ssimmering antipathy to Ms Gordillo came to the fore. She had been in favourof supporting the government's VAT plan. In the end she was removed as leaderof the PRI in the Chamber of Deputies. She was replaced by Emilio Chuayfettand the PRI voted against the government's reform.

Ideologically, the PRI is evolving into a centre-left party with a social-democraticagenda. It is likely to hold together, aiming to regain the presidency in 2006.Currently it has 17 of the 31 state governorships and the biggest parliamentarygroups both in the Chamber of Deputies and the Senate.

The PRD was formed in 1989 by supporters of Mr Cárdenas’s 1988 presidentialbid. After his defeat in the 1994 election, the party suffered a temporary decline.Between 1996 and 1999, under the leadership of Andrés Manuel López Obrador,the party’s electoral fortunes improved, partly owing to the significant protestvote against the government during the economic crisis. The party diversifiedits base by embracing disaffected PRI members, winning over states that hadbeen considered impregnable. However, in the 2000 presidential election,Mr Cárdenas managed only a distant third place as many of his supportersdefected to vote for Mr Fox. Mr Cárdenas still enjoys a significant following. Inthe 2003 congressional elections, the PRD increased its share of the vote from13% to 18% but its performance was below the expectations created by itspresident, Rosario Robles. Under pressure from opponents within the partywho leaked information about the party’s debt levels to the press, she resignedand Leonel Godoy, a close ally of Mr Cárdenas, was appointed as interimleader for a year.

A three-party system has evolved since 1997, with five other small parties beingrepresented in Congress. The most important among them is the PVEM, whichbenefited greatly from having supported Mr Fox as a presidential candidate (interms of seats in Congress gained from the coalition it formed with PAN).However, it openly broke ranks with the government in September 2001, mainlybecause it did not get any cabinet positions, and opted to fight some legislativeseats with the PRI in 2003. A total of 11 political parties competed in the 2003congressional election but five of them failed to obtain the minimum share of2% of the vote and lost their deposit. These were: the Partido Alianza Social(PAS), the Partido de la Sociedad Nacionalista (PSN), México Posible (MP),Fuerza Ciudadana (FC) and the Partido Liberal Mexicano (PLM). The PVEM,with 17 deputies, reaffirmed its standing as the fourth-biggest party. The twoother survivors were the Partido del Trabajo (PT), which has six seats in theChamber of Deputies, and Convergencia (a PRI splinter founded in 1999), withfive seats.

The PRD loses its popularity

12 Mexico

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

Mexico has an important rebel group, the Ejército Zapatista de LiberaciónNacional (EZLN), which is based in the state of Chiapas. Other relatively smallguerrilla movements have at times emerged, but have either fizzled out or beendeactivated by government forces. No formal peace negotiations have takenplace since 1996 as both the government and the EZLN have been unwilling togive ground on certain questions. The EZLN, cornered militarily, has a smallpolitical base but a formidable propaganda machine. In September 1997 apolitical front, the Frente Zapatista de Liberación Nacional (FZLN), wasestablished to mobilise national support for the Zapatistas, but it will notparticipate in elections. As soon as he entered office, Mr Fox tried to re-startpeace negotiations. He removed the army from several areas, freed EZLNprisoners and sent a constitutional initiative to Congress to increase theautonomy of indigenous groups. Congress ultimately passed a much watered-down version of the initiative that proved unacceptable to the EZLN, which thenrefused to enter into peace talks.

Neither the church nor the military are major participants in politics. Sincegaining constitutional recognition (and the right to vote) in 1992, Roman CatholicChurch leaders have attempted to influence policy, particularly on education,but have been rebuffed by politicians, even by those from PAN (which hastraditionally strong church ties). The military has also become more prominent.The institutional loyalty of the armed forces was tested in the 2000 politicaltransition, but proved to be strong when Mr Fox appointed a minister of defenceof his choosing over several more senior generals.

Main political figures

Vicente Fox Quesada (61)

President. A relative newcomer to politics after a successful career in business.Mr Fox joined the Partido Acción Nacional (PAN) in the late 1980s and becamecongressman for Guanajuato in 1988. Having failed to win the election in 1991, hebecame governor of his state in 1995. From 1995 he campaigned vigorously for thepresidency, becoming a national figure. Although not popular among the leaders ofhis own party, he was able to circumvent their hostility by building a strong politicalsupport group. Despite a flawed campaign, his offer of change was a powerfulmessage, luring many voters away from the Partido Revolucionario Institucional(PRI) and the Partido de la Revolución Democrática (PRD). His pragmatic and pro-business approach to government was reflected in the appointment of severalcabinet ministers with strong business backgrounds. However, Congress has radicallyslowed down and altered his ambitious legislative agenda. After three years ingovernment, his administration is considered ineffectual, but his personal approvalratings remain high. He is perceived as well-intentioned and, most importantly, notcorrupt.

Santiago Creel Miranda (49)

Minister of the interior. Mr Creel, a lawyer, received the PAN’s nomination tobecome a member of the Instituto Federal Electoral (IFE, Federal Electoral Institute) in1994, just as that organisation had been granted full autonomy. He became a deputyfor the PAN in 1997, although he was not officially a party member until 1999,building his political reputation as one of the main leaders of the opposition bloc

Forces outside parliament

Mexico 13

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

that held a majority in the Chamber of Deputies. In 2000 he was the PAN’scandidate for the governorship of Mexico City and came a close second to the PRD.In his role as interior minister, Mr Creel has dealt skilfully with opposition parties,carefully following the presidential line of seeking a consensus whenever possible.

Roberto Madrazo Pintado (53)

PRI national leader. Mr Madrazo, a lawyer, became a nationally known figure in1999, when he stood for the PRI presidential nomination against the eventualwinner, Francisco Labastida. He is popular among the PRI’s grassroots as he has hada long career in the party, having risen from being a leader of its youth movement tothe post of secretary of organisation. Mr Madrazo was governor of Tabasco in1995-2000 and has twice been elected to the Chamber of Deputies—in 1976-79 and in1991-94—and to the Senate in 1988-91. He was elected as PRI leader in February 2002.He faces the challenge of unifying the party and drawing up a cohesive strategy.

Andrés Manuel López Obrador (51)

Mayor of Mexico City. A long-time ally of PRD founder Cuauhtémoc Cárdenas,Mr López Obrador defected from the PRI in 1988. An energetic social activist, he wasfederal deputy (1988-91) and twice (in 1988 and 1994) failed to win the governorshipof his native Tabasco. Supported by Mr Cárdenas, he became president of the PRDfrom 1996 to 1999. Under his vigorous leadership, the party experienced stronggrowth. In 2000 he won the governorship of Mexico City. His straightforwardmanner and populist policies (diverting expenditure from investment to financehandouts to certain groups) have made him very popular and he is tipped as astrong candidate for the 2006 presidential elections.

Diego Fernández de Cevallos (63)

Senator. A long-standing member of the PAN and a powerful lawyer, he gainednational prominence as federal deputy in the 1991-94 legislature, when as leader ofthe PAN faction in the Chamber of Deputies he worked closely with the PRIgovernment. A presidential candidate in the 1994 election, he came a strong second,and positioned his party as a credible electoral alternative. A long-time rival ofVicente Fox Quesada, he has frequently and publicly clashed with the president.Senator for the 2000-06 period, his influence on many PAN members, and abilitiesto work with the PRI, are sorely needed by the government to push forward itslegislative agenda.

Francisco Barrio Terrazas (53)

Comptroller and administrative development (Secodam) minister. One of the fewtraditional PAN members in the cabinet. With a BA in Accounting and an MBA, aswith many PAN members he moved in the early 1980s from business activities topolitics. He joined the party in 1983, and in the same year became mayor of hisnative Chihuahua City. In an election heavily tarnished by fraud in 1986, he wasdefeated as candidate for governor, a position he won six years later (1992-98) Hisinterest in fighting corruption motivated his appointment to Secodam and has madehim a national figure, particularly because of his investigations into the PRI.

14 Mexico

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

International relations and defence

The Fox administration espouses an activist foreign policy, a reversal of thenon-interventionist stance adopted by PRI governments since the 1930s, andone that largely supports US initiatives. But after an auspicious start, relationswere overtaken by the terrorist attacks on the US in 2001 and more recently,differences over the war in Iraq. Since late 2003, however, relations have begunto improve again. This is in part because of the US presidential elections inNovember 2004, and the need of the US president, George W Bush, to court theHispanic vote and in part because of Mexico's importance to the US as astrategic ally in Latin America. This has increased in recent months in the faceof the growing strength of a left-of-centre bloc led by Brazil, which seeks to takea more strident stance against US policy in specific areas of trade, such as accessto agricultural markets, investment and services than has been evidentpreviously. Mexico seems to have won one of the most important measuresthat Mr Fox had sought from Mr Bush, namely improvements in the status andtreatment of illegal Mexican workers in the US. In January 2004 Mr Bushunveiled a plan to change fundamentally the status of illegal immigrants in theUS, although it may well not gain US Congressional approval this year.

Mexico has strengthened ties with other countries and economic blocs. It wasadmitted as a full member of the Asia-Pacific Economic Co-operation (APEC)forum in 1993 and to the OECD in 1994, having joined what is now known asthe World Trade Organisation (WTO) in 1986. Mexico has also pursued greaterregional integration by entering into free-trade agreements (FTAs) with CostaRica, Bolivia, Venezuela and Colombia (1995), Nicaragua (1998), Chile (1992 and1998), Israel and the EU (2000), the European Free-Trade Association (EFTA;2001), and Uruguay (2003). Mexico is also a member of the Triángulo del Norte(Northern Triangle) trade bloc along with Guatemala, Honduras and El Salvador.Negotiations to reach an FTA with Japan started formally in November 2002and despite a number of stumbling blocks, look set to be completed in 2004 (seeEconomic policy).

Armed forces, 2002

Active force

Active forces total 192,770.

Reserve force

The reserved force totals 300,000.

Army

There are 144,000 soldiers, of which 60,000 are conscripts, and 12 military regionswith garrisons in 44 zones. Each garrison comprises 81 infantry brigades, 19motorised cavalry brigades, three artillery regiments and one air-mobile unit. Thestrategic reserve includes four armoured brigades and one presidential guard brigade.

Navy

The navy comprises 37,000 seamen, including 8,700 marines and 1,100 naval airpersonnel. There are 17 naval regions, of which six are in the Gulf of Mexico and 11in the Pacific Ocean. The navy possesses three destroyers and eight frigates.

Strong relations with the US

Mexico 15

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

Air force

The air force comprises 11,770 airmen, including one squadron with ten fighter planesand 47 armed helicopters.

Although the armed forces are ill-equipped to defend Mexico from externalaggression, their role in domestic affairs has increased in the past few years. Inaddition to waging a perennial war against drug-traffickers, they have beencalled on to contain guerrilla groups, notably the EZLN, and even to take onpolicing duties. However, scandals related to corruption and human rightsabuses have tarnished the army’s image. Defence spending is low, andamounted to just 0.5% of GDP in 2002.

Security risk in Mexico

Armed conflict/terrorism

The Ejército Zapatista de Liberación Nacional (EZLN) in Chiapas is located far frommajor urban areas and its activities are thus unlikely to affect business. The EZLN iswell contained by the Mexican military, and has shown no intention of carrying outurban terrorist acts. The movement has a strident but small political base, but isunlikely to threaten political stability.

Unrest/demonstrations

Demonstrations are frequent in major urban areas, especially Mexico City, althoughthey are rarely violent. The US embassy is often a focal point of anger during labourdemonstrations, but US businesses are not generally targeted.

Violent crime

Since the mid-1990s all forms of crime have risen sharply, particularly in Mexico City.Theft of merchandise and assaults on staff are among the top security concerns ofbusinesses operating in Mexico. The judiciary and municipal police are oftencorrupt, making arrest and prosecution of criminals more difficult. Businesses,especially those dealing with the public, should expect to spend heavily on security.Large firms allocate about 10% of their total expenses to security.

Organised crime

Drugs cartels are entrenched in Mexican states near the US border. The assassinationof public officials in these states is often drug-related. Southern states such asGuerrero and Michoacán are used for growing illegal crops like marijuana.

Kidnapping

Although conventional kidnapping gangs do not generally target foreigners, the risingincidence of “express kidnappings” means that executives are at growing risk ofbecoming the targets of violent crime.

Resources and infrastructure

Population

Mexico is in an advanced stage of demographic transition—the transformationof countries from having high birth and death rates to low birth and death

Priorities of the armed forces

16 Mexico

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

rates. According to the Consejo Nacional de Población (Conapo, the NationalPopulation Council), the rate of population growth has slowed from more than3% per year in the early 1970s to an estimated 1.3% in 2003. According to officialdata, the average age of the population is 27, the number of people under sixyears old has fallen since 1990, and life expectancy is 75 years. The number ofpeople aged 6-14 years has also been declining since 1999. Despite thesechanges, a third of the population is aged 14 years or under, which results inpressures on the education system and the labour market.

The deceleration in the rate of population growth reflects a declining fertilityrate (children/woman) and net emigration (around 400,000 emigrate a year).The fertility rate fell from 5.6/woman in 1976, to 3.9/woman in 1986, to2.7/woman in 1996 and finally to an estimated 2.34/woman in 2001. The fall inthe fertility rate has come about owing to a range of factors, including improvedaccess to education for women, increased use of contraceptives and betterhealthcare, which has lowered infant mortality, thereby encouraging people tohave fewer children.

According to the 2000 census, 65% of the population lives in urban areas, witharound 18m in the Metropolitan Area of Mexico City. According to thegovernment's Programa Nacional de Población (2001-06), the demographic andeconomic concentration in large metropolitan areas did not change markedly inthe 1980s and 1990s. Around 24% of the population still lives in small ruralcommunities with fewer than 2,500 inhabitants, many of which are isolatedand widely dispersed. Around 12.7m Mexicans are indigenous and tend tosuffer high poverty rates—68% of high or extremely high levels of margin-alisation are indigenous. There are over 60 recognised ethnic and languagegroups, and around 1% of the total population does not speak any Spanish. Themost numerous indigenous groups are the Náhuatl, the Maya, the Zapotec andthe Mixtec.

Emigration, primarily to the US, continues in large numbers. According togovernment estimates, over 0.4m people migrated every year in 2000-02. In2002 the number of Mexican-born people living in the US was estimated byConapo at 9.5m, around 30% of US immigrants and around 3.5% of the USpopulation. If those of Mexican origin but born in the US are counted, in 2002there were 25.5m Mexicans living in that country. The average age of an illegalimmigrant is estimated at 34 years old, with 61% having at most secondaryeducation. In 2002 76,531 Mexicans became US citizens through naturalisation.According to US statistics, in 2002 the total number of Mexican-born peopleofficially admitted into the US stood at 219,380, and a total of 0.99m weredetected as deportable aliens (although this figure may be considerablyinflated, as many people return to the US soon after being expelled).

Education

In 2000 9.6% of the population aged 15 years and above was illiterate. Theaverage number of years of schooling per child stood at 7.6 years, comparedwith 6.5 years in 1990. Although primary education for children aged betweenfive and 11 years is both free and compulsory, in 2000 only 70.3% of the

The workforce is poorlyeducated

Mexico 17

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

population age 15 years or over had completed the primary level. Only 25% ofthe adult population has reached an upper-secondary level of education (theOECD average being 64%), and of those aged 15-19 years, approximately half arenot in education (the OECD average is 20%).

Given the rapid growth of the population reaching working age (about 1m peryear), a major effort is needed to facilitate the transition from school to work. InAugust 1997 the Programa de Educación, Salud y Alimentación (Progresa, aprogramme promoting better education, health and nutrition) was introducedto provide additional subsidies to some of the country’s poorest families.Secondary schooling for children aged 11-14 years has been made compulsoryand technical training facilities have been expanded. For the 2002/03 academicyear, there were more than 5,533 centres training students for jobs in industry.

In February 2001, the president, Vincente Fox Quesada, announced two neweducation programmes, the Programa Nacional de Becas para Estudios de TipoSuperior (Pronabes, which provides scholarships to poor students in highereducation) and the Programa de Escuelas de Calidad, which will provideadditional financing for public schools to improve their quality. In March 2002the government announced the replacement of Progresa with a programmecalled Oportunidades. In addition to the three areas covered by Progresa,Oportunidades will include temporary employment programmes, financing forsmall-scale projects and the regularisation of housing in urban and rural areas.It is estimated that Oportunidades will benefit over 5m families in 2004.

According to government estimates, spending on education in 2002 amountedto 6.8% of GDP (with 1.3% of GDP coming from private sources), a level thatcompares favourably with the 5.5% OECD average (1999 figure). However,spending is heavily skewed towards higher education, with university studentsreceiving a subsidy that is 4.4 times higher than their counterparts at primaryschool, and double the OECD average. In the 2002/03 academic year therewere only 2,250 students in higher education per 100,000 of the population(about one-third the US figure). It is not yet clear what the government plans todo to rebalance this situation. Total education spending is due to increasesharply. At the end of 2002 Congress changed the General Education Law,establishing that by 2006 the government should spend an equivalent of 8% ofGDP on education. Mr Fox welcomed the change (although it is unclear howthat huge increase will be financed).

Students('000)

2001/02 2002/03 2003/04Pre-school 3,432.3 3,495.7 3,725.2

Primary school 14,843.4 14,858.9 14,878.4Secondary school 5,480.2 5,672.7 5,813.2High school 3,120.5 3,275.6 3,479.2

University 2,147.1 2,259.8 2,354.6Other (technical training) 1,121.9 1,230.0 1,236.9

Total 30,145.4 30,792.7 31,487.5

Source: Presidencia de la República, Tercer Informe de Gobierno.

Educational spending is biasedtowards the tertiary level

18 Mexico

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

Health

Between 1970 and 2003 life expectancy at birth increased from 61 years to anestimated 74.9 years, while infant mortality fell from 69 per 1,000 live births to16 per 1,000 live births. Universal vaccination programmes have helped to reducecases of whooping cough and tuberculosis, and poliomyelitis has been almosteradicated. Efforts continue to be made to curb outbreaks of cholera and thespread of AIDS. The government has tried to combat malnutrition by institutingseveral programmes of food support, including the provision of subsidised milkto 2.93m families, free school breakfasts for about 4.7m children and 1 kg/day offree tortillas to 140,000 families, according to 2003 estimates. Neverthelessmalnutrition remains a serious problem, particularly in remote rural areas.

The Instituto Mexicano del Seguro Social (IMSS, the social security institute) andthe Instituto de Seguridad y Servicios Sociales de los Trabajadores del Estado(ISSSTE, the social security institute for public-sector workers) are the two mainproviders of healthcare. According to official figures, in 2003 an estimated 47.0mpeople were covered by the IMSS, with 15.9m affiliates paying contributions. TheISSSTE, with 2.4m affiliated state workers, offered services to a further 10.3mpeople. The two organisations are funded by employer and employeecontributions, returns on investments and, in the case of the ISSSTE, increasingtransfers from the federal government (otherwise it would become insolvent).

In addition to the IMSS and the ISSSTE, some healthcare services are providedby the Ministry of National Defence, the Ministry for the Navy, PetróleosMexicanos (Pemex, the state oil company) and by state organisations such asthe Instituto Nacional Indigenista (INI, the Institute for Indigenous People) andDesarrollo Integral de la Familia (DIF, an agency promoting familydevelopment), as well as by private institutions. Those people who are notcontributors to the national social security system nor members of privateschemes can obtain free healthcare from either the Ministry of Health or theIMSS-Solidaridad anti-poverty programme.

Many Mexicans use private healthcare services (particularly for minorailments), as service quality in public facilities varies considerably. In 2003 thegovernment estimated that there were 3,124 private medical establishments inthe country (of which 73 had at least 50 beds).

Hospital units, 2003Type No.Open to allMinistry of Health 454Instituto Mexicano del Seguro Social-Solidaridad (IMSS-Solidaridad)a 69Open to beneficiaries onlyInstituto Mexicano del Seguro Social (IMSS) 264Instituto de Seguridad y Servicios Sociales de los Trabajadores del Estado (ISSSTE) 106Petróleos Mexicanos (Pemex) 23Ministry of National Defence 42Ministry for the Navy 32

a Hospitals funded under the IMSS-Solidaridad anti-poverty programme.

Source: Presidencia de la República, Tercer Informe de Gobierno.

Mexico 19

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

Natural resources and the environment

Covering an area of 1.96m sq km, Mexico is the 14th largest country in theworld. It is bounded by the US to the north along a 3,118-km frontier and to thesouth by Guatemala (943 km) and Belize (249 km). The country’s western limitis the Pacific coast (7,360 km) and its eastern limit the Gulf of Mexico and theCaribbean coast (2,780 km).

The country’s topography is complex, ranging from coastal plains to volcanoesstanding over 5,000 metres above sea level. More than one-half of the landarea is over 1,000 metres above sea level.

Climatic conditions vary considerably owing to the topography, but much ofthe country is dry and there are few large rivers. Water resources are unevenlydistributed. Both the Gulf coast to the east and the Baja California peninsula tothe west are vulnerable to tropical storms and hurricanes. The high season forstorms is July-September on the west coast and August-October in the Gulf. Thewest coast of southern Mexico, where the Cocos Plate dips beneath the NorthAmerican Plate, is an active seismic zone, and earthquakes are not uncommonin the central states and the capital, Mexico City. The area has seen 35earthquakes of magnitude greater than 7.0 on the Richter scale since thebeginning of the 20th century.

Climate(% of total area)

Hot & humid 4.8Hot & dry 23Temperate 23.1

Dry 28.3Very dry 20.8

Source: Instituto Nacional de Estadística, Geografía e Informática.

Owing to the topography and climate, only about 21% of the country is suitablefor arable farming and a further 57% for pasture. Forests and woodland coveraround 17% of the land. There is great potential for fishing to be developed.

As a signatory to the North American Free-Trade Agreement (NAFTA), Mexico isunder pressure to raise its environmental standards. Air pollution is a seriousproblem in Mexico City (in 1992 its air was considered the most polluted in theworld by the UN), Guadalajara and Monterrey. Northern border areas, whereindustries have operated without adequate environmental controls, also suffera high degree of pollution and other environmental problems. In the 1980s theauthorities saw the need to tackle environmental degradation, but the GeneralLaw of Ecological Balance and Environmental Protection was not enacted until1988. In 1992, the Procuraduría Federal para la Protección del Ambiente (Profepa,the Federal Bureau for the Protection of the Environment) was established.

During the administration of Ernesto Zedillo (1994-2000), the Ministry forFisheries became the Ministry of Environment, Natural Resources and Fisheries.Amendments to the law in 1996 delegated important enforcement functions to

Topography

Climate

Land use

Environmental standards

20 Mexico

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

both state and local governments and introduced the “polluter pays” principle.Mr Fox has transferred the fisheries brief to the Ministry of Agriculture. Ownersof old cars in Mexico City are required to leave them at home on one day eachweek and on two days a week during environmental emergencies. Moves arebeing made to substitute natural gas for diesel in power stations and industry,and environmental policing is being stepped up generally, althoughenforcement remains lax.

Transport, communications and the Internet

Private companies were offered concessions to build and to operate toll roadsunder the administration of Carlos Salinas de Gortari (1988-94). A lower thanexpected volume of traffic and economic crisis from December 1994 caused thegovernment to revoke 23 of the concessions, while also offering financialassistance to the companies involved. New concessions started to be offeredunder the Fox administration in 2003.

Integral port administrators were created in 1993. The administration of eachseaport was awarded by concession to an administrator, who operates portterminals and facilities, providing related port services. The privatisation of portadministration began in 1995 and continued under the Zedillo administration.Foreign investors may hold up to 49% equity in a port administrator and up to100% equity in ventures providing some port services. Concessions last for upto 50 years.

The Salinas government managed to cut the losses of the FerrocarrilesNacionales (Ferronales, the state-owned railway company); and the Zedilloadministration split the company into regional companies and in 1997-98transferred the management of most of these companies to the private sectorunder 50-year concessions. Small loss-making segments were excluded from thesale, along with the railway running through the Tehuantepec isthmus, owingto its political sensitivity. Three regional railway companies, Noreste, Pacífico-Norte and Sureste, as well as four short lines, are now privately managed.

The process of privatising the country’s 35 airports, which deal with 97% oftotal passengers, started in 1998. The airports were divided into three groups forauction according to their geographical location, with the addition of a specialgroup for Mexico City. A minority but controlling share, usually of 15%, wasoffered to strategic investors, who must include a foreign investor withexperience in airport management, while the rest of the shares are supposed tobe offered to the public on the stock exchange. The 1995 Airports Act permitsup to 49% of investment in enterprises to be from external sources, althoughauthorisation for a higher percentage may be obtained from the ComisiónNacional de Inversiones Extranjeras (CNIE, National Commission for ForeignInvestment).

In October 2001 the government decided to site a new airport for Mexico Cityin Texcoco, about 14 miles east of the city centre, to ease bottlenecks at theexisting Benito Juárez airport. Environmental groups and landowners affected

Roads

Port facilities

Railways

Airports and air transportation

Mexico 21

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

by the project, particularly the latter, sought judicial injunctions and stagedstrong protests to reverse the decision. This led the government to cancel theproject in August 2002. The cancellation of the project has not helped Mr Fox’simage. The new airport had been one of the most important public worksprojects of his presidency. Instead, the government opted in 2003 to extend theexisting Benito Juárez airport.

As an alternative, and without publicising the strategy much, the governmentaims to expand the airports in nearby urban areas in order to ease the pressureon Benito Juárez airport (it cannot be expanded because of the huge costsinvolved). Airports in nearby Toluca, Morelos, Querétaro and Puebla are amongthe alternatives being studied. The expansion of Puebla airport started in earlyNovember 2002, and the new extension of the Querétaro airport was openedin July 2003.

Transport and communications, 2003Roads (km)a 348,529Paved roads (km) 113,590

Registered vehicles (m)b 19633Railway track (km) 26,655

Rail passengers ('000)a 232Rail freight ('000 tonnes)a 81,567International airports (no.) 57

Domestic airports (no.) 28Air passengers (m) 33854

Air freight ('000 tonnes)a 407Ports (no.) 97Port facilities (sq km) 187

Maritime passengers (m)c 7944Shipping ('000 tonnes) 257,286

Telephone lines ('000)d 15,959Cellular telephones ('000)d 28,379

Internet users ('000)e 12,250

a Estimate from the Tercer Informe de Gobierno. b Figure from October 2003. c January-Octoberfigure. d September 2003 figure. e End-2003 estimate.

Sources: Instituto Nacional de Estadística, Geografía e Informática; Secretaría de Comunicaciones y Transportes; Aeropuertos y

Servicios Auxiliares; Caminos y Puentes Federales de Ingreso; Comisión Federal de Telecomunicaciones; Presidencia de la

República, Tercer Informe de Gobierno.

In 1998-2000 three airport groups were privatised. Aeropuertos del Sureste,manager of nine airports in six states, of which Cancún is the jewel in thecrown, was the first group to be auctioned. Control was won by a consortiumwith Mexican, Danish, French and Spanish capital in December 1998. Aconsortium of Mexican and Spanish investors won the bidding to manageAeropuertos del Pacífico, a group of 12 airports, including Guadalajara andTijuana, in August 1999. Control of Aeropuertos del Centro-Norte, a group of 13airports, including those serving Acapulco and Monterrey, was won by aconsortium of Mexican and French investors in May 2000. The privatisation ofMexico City airport has been delayed indefinitely until the expansion workshave been completed. The placement of 85% of shares in privatised airportgroups on the stock exchange has been delayed several times. Shares in the

22 Mexico

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

Sureste group were placed on the Mexico City and New York stock exchangesin September 2000. Share placements for the other airport groups have beenpostponed until market conditions improve.

Adverse market conditions are also the reason why the government hasrepeatedly postponed the privatisation of the airlines that compose the Cintraconsortium (with the two national airlines Aeroméxico and Mexicana at itscore). Cintra is under the management of the Instituto Bancario de Protección alAhorro (IPAB, the Institute for the Protection of Bank Savings), and, inaccordance with the legislation that created IPAB, all the assets under itsadministration are supposed to have been sold off by January 2004. However,the airlines have yet to be sold and it is not clear when this will take place.When the privatisation process is implemented, Aeroméxico and Mexicana willhave to be sold separately to ensure some competition on domestic routes(which currently does not exist), according to a ruling from the ComisiónFederal de Competencia (CFC).

The national telephone company, Teléfonos de México (Telmex), was privatisedin 1990. Since then the number of telephone lines has increased substantially.Between 1990 and 2003 density rose from 6.4 lines per 100 people to 15.5 linesper 100 people (September 2003 figure). With privatisation came concessionsfor cellular telephone operations, and in August 1996 the long-distance marketwas opened to competition.

A total of 24 concessions were granted and 19 companies had won concessionsto compete against Telmex in the local telephone service market by the end of2000. However, Telmex continues to wield considerable market power and hasbeen accused frequently of abusing its position. The Comisión Federal deTelecomunicaciones (Cofetel, the telecoms industry regulator) has tried manytimes to rein in the company, without success as Telmex has won judicialinjunctions against its rulings. The Office of the United States TradeRepresentative (USTR) has pressed more successfully, through requests to theWorld Trade Organisation (WTO) to set up arbitration panels and rule on theopenness of the Mexican telecoms market. These requests (the most recenthaving taken place in February 2002) have pushed Telmex to settle with itscompetitors disputed issues such as interconnection fees. Since March 2001 allpolitical parties have been working on a new telecoms law. The issue is stillofficially on the government's agenda, but a consensus has not been reached,and it is not clear when a proposal will be officially presented to Congress, orwhether it will have enough support to be enacted.

Telmex’s monopoly power and the subsequent high cost of fixed-line servicesare a major reason for the explosion in mobile phone services. The mostpowerful company, and by far the most dominant in the market, is Telcel (partof América Móvil, a Telmex spin-off). However, in that field (contrary to whathas been happening with fixed lines), Telmex faces increasingly powerfulcompetition. Telefónica Móviles México (an affiliate of Spain’s Telefónicagroup) has emerged as the second-largest operator in the country after a buyingspree that included Motorola (in 2000) and Pegaso (2002). As of the fourthquarter of 2003, Móviles México had about 3.5m subscribers (against Telcel’s

Telecommunications

Mexico 23

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

22m). Among the small operators, some consolidation has taken place.MovilAccess, a company owned by Grupo Salinas (that also controls mobiletelephone company Unefon and TV Azteca, the second-biggest televisionbroadcasting company in the country), bought Iusacell, another mobilecompany, at the end of July 2003 from Verizon Communications (US) andVodafone (UK). MovilAccess paid US$10m and officially assumed Iusacell'sestimated US$815m in debt. Verizon and Vodafone are estimated to haveinvested around US$2bn into the company. As a result Grupo Salinas controlsaround 13% of the mobile phone market. Competition is expected to increasebetween Telcel and Telefónica.

The number of households owning a computer has risen markedly, althoughregional differences are large. By the end of 2002 there were an estimated10.03m Internet users in Mexico, with 5.59m accessing the web from homecomputers. At the end of January 2003 the government formally started thefirst phase of the e-Mexico project, which aims to provide high-speedconnection to the Internet through satellite to 3,200 communities.

Mexico has a large number of daily newspapers with national, state and localmunicipal circulation. All national daily newspapers are privately owned.Several newspapers survived for decades despite meagre circulation numbersthanks to advertising, government subsidies, and cash hand-outs, but since theFox administration ceased to prop up the newspapers, some have gone out ofbusiness. The daily Novedades (founded in 1936) and Mexico’s only English-language newspaper, The News (established in 1949), ceased publication at theend of 2002. Two other dailies, Excelsior (founded in 1917 and until the 1970sthe most important newspaper in the country) and Unomásuno (established in1977), are close to bankruptcy. Reforma (founded in 1993) is the best-sellingnewspaper but is closely followed in its importance by El Universal (founded in1916). There are also a great many weekly and monthly magazines. Amongother media there are a total of 40 AM and FM radio stations and ninetelevision stations that offer a wide range of programming in the capital. Manyof these media are also available nationwide.

Energy provision

Mexico was the world’s fourth-largest producer and eighth-largest exporter ofoil in 2002. It was also the second largest supplier of crude oil to the US afterSaudi Arabia. In 2003 production reached an historic high of an average of3.37m barrels/day (b/d), constituting an increase of 6.1% year on year. Theambitious goal set for 2006 is to produce 4m b/d. The country produces threetypes of oil: heavy Maya, at 22.3° American Petroleum Institute (API); Isthmus(34.6° API); and Olmeca (39.1° API). Official hydrocarbons reserves at the start of2002 stood at 52.9bn barrels (enough to keep production at current levels for 35years), of which 43.21bn were crude oil and condensates, and 9.74bn gasequivalent. Reserves have declined steadily in the past 19 years, reflecting acontraction in exploration.

Media

Oil production

24 Mexico

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

Under the constitution, Petróleos Mexicanos (Pemex, the state-owned oilcompany) has a monopoly on all upstream oil and gas activities. Although ithas a refining joint-venture with Royal Dutch/Shell in Texas, Mexico does notallow production joint-ventures. Outside companies have been brought in toundertake drilling operations, although to date they have been doing so underlimited service and performance contracts. The constitution allows Pemex toenter into contracts involving works and delivery of services. However, it alsostates that any remuneration should be made in cash, and under nocircumstances will a percentage of the goods or participation in the results ofthe exploitation be granted.

There has been a steady reduction in Pemex’s monopoly over petrochemicalsproduction. Modifications to the constitution in November 1996 restricted thestate’s exclusive production rights to only eight basic petrochemicals. Otherthan in those products, the private sector may now participate in theproduction of petrochemicals and may own 100% of the equity of a producingcompany, but only 49% of the equity in plants owned by Pemex. Thisrestriction has deterred investors and an attempt to part-privatise somecomplexes foundered in 1999. Apparently the Fox administration has opted toleave the status quo unchanged, and concentrate its political efforts onliberalising the electricity sector.

Despite stiff political opposition, in August 2003 Pemex began to seek privateinvolvement in the exploration and production of non-associated natural gas(gas which exists without the presence of oil) through multiple service contracts(MSCs). The auctions of the MSCs were delayed several times owing to theneed to redraft the texts of the contracts to avoid any constitutional challengeby the opposition, but they finally went ahead in October and November 2003.The first contracts were to produce gas in the Burgos Basin, which lies acrossthe US border from Texas's most productive gas fields. A total of US$8bn ininvestment is expected, which is estimated to double the production of gas inthe area to 2.0bn cu ft/day by 2006.

Pemex aims to reduce the share of its revenue that goes to the government sothat it can invest more in its own infrastructure and in oil exploration. This isunlikely to occur in the medium term as the fiscal reform approved at the endof 2001 did not raise sufficient revenue from other sources to reducesignificantly the state’s reliance on Pemex. The company's directors haveclaimed that, unless Pemex's tax burden is reduced substantially, Mexico willeventually become a net importer of oil, as has occured with natural gas. In themeantime, the company is financing much of its investment through debt soldin the domestic and international capital markets.

Oil and gas productiona

2003 % change on 2002Crude oil incl liquid gas ('000 b/d) 3,788 5.7Gas (m cu ft/day) 4,498 1.7

a January-November.

Source: Petróleos Mexicanos; International Energy Agency.

Gradual participation of theprivate sector

Oil production capacitythreatened by tax burden

Mexico 25

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

The Fox administration is also keen to open the electricity sector to privateinvestment in order to expand supply but this plan has also encounteredconsiderable political opposition. In April 2002 the Senate rejected a far-reaching liberalisation proposal that had initially been made by the Zedilloadministration in early 1999. Also in April 2002 the Suprema Corte de Justiciade la Nación (SCJN, the Supreme Court) overruled changes that Mr Fox hadmade by decree, in May 2001, to legislation governing the sector on thegrounds that he required the assent of Congress. Mr Fox’s changes hadincreased the amount of electrical power that the Comisión Federal deElectricidad (CFE, the electricity commission) could buy from privatecompanies that generate excess electricity. The SCJN ruling has a quitesignificant coda: it calls into question the constitutionality of the Ley delServicio Público de Energía Eléctrica (the public electricity law) enacted in 1992,under which private investment in generation is allowed, through schemessuch as co-generation and production for self-consumption. Investment hascontinued, but the legal uncertainty remains.

Partly to dispel that uncertainty and to increase private investment in the sector,Mr Fox submitted a constitutional reform proposal to the Senate in August 2002that would allow private electricity to be sold to big consumers. Crucially, itwould establish that the government has to guarantee non-discriminatoryaccess to the electricity transmission and distribution infrastructure. This wouldmean that the private sector could supply electricity unhindered, and wouldestablish the concept of the autoconsumidor (self-consumer). Autoconsumidoresare those that use at least 2,500 mw of energy a year, making up about 60% ofthe market, and would be able to purchase energy from the Comisión Federalde Electricidad (CFE, Federal Electricity Commission) and the state-owned Luz yFuerza del Centro (LyFC, that provides electricity to Mexico City and surroun-ding areas) or private companies. A new minister of energy, Felipe CalderónHinojosa, was appointed in September 2003. Mr Calderón started to negotiatea simplified version of the August 2002 initiative with the opposition. A voteon the issue should take place in 2004.

While it awaits legislative approval of its reform plans, the government hassought to make the sector more efficient by cutting subsidies and increasinginvestment through Proyectos de Inversión Diferida en el Registro del Gasto(Pidiregas, investment projects financed initially by the private sector butultimately paid for with the revenues generated by the projects themselves).

The economy

Economic structure

The Mexican economy has undergone a profound transformation since the1980s as a result of economic liberalisation and joining the North AmericanFree-Trade Agreement (NAFTA, a free-trade bloc with the US and Canada).Having relied heavily on oil for foreign-exchange earnings in the late 1970s,manufacturing quickly became the main source of export earnings. In 2003 thesector accounted for around 20% of GDP and around 85% of export earnings,

A service-sector economy

Electricity liberalisation

26 Mexico

Country Profile 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

according to preliminary estimates. Almost half of total exports was producedin maquiladoras (in-bond assembly for re-export plants). Services, however, arethe most important contributor to national output. During the first threequarters of 2003 the sector accounted for 66.6% of GDP.

Main economic indicators, 2003Real GDP growth (%; based on constant 1993 prices) 1.3

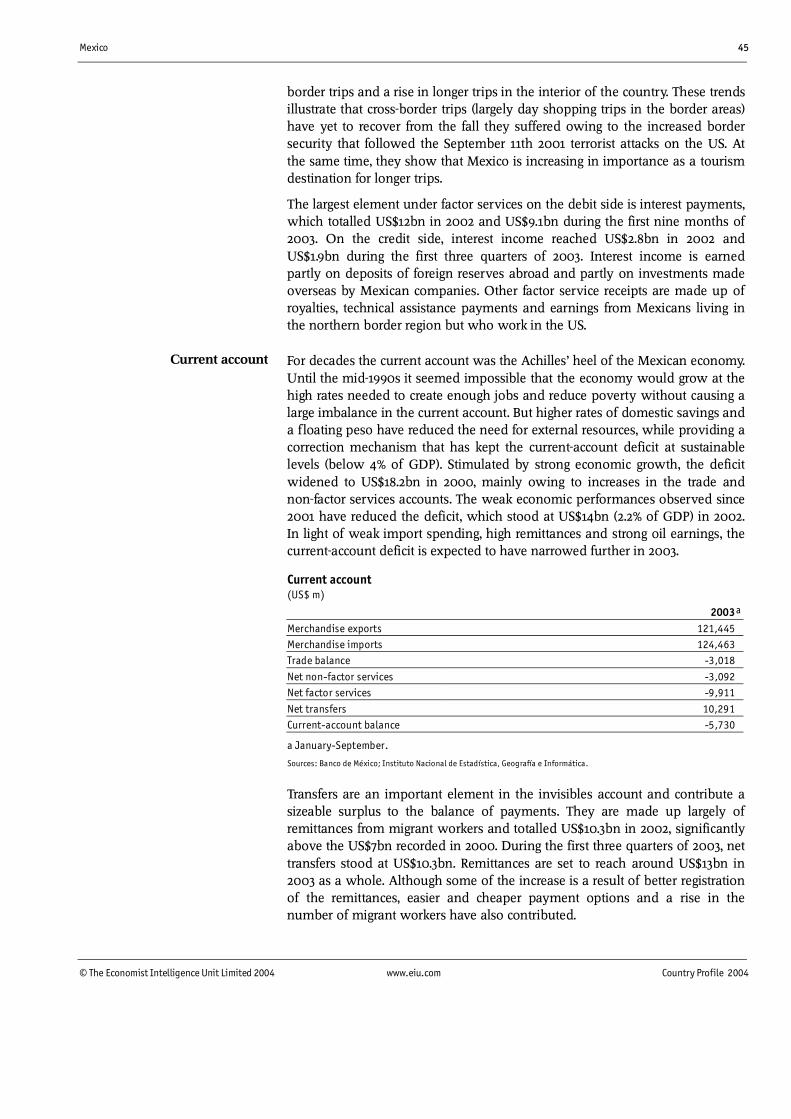

Consumer price inflation (%; year-end) 4.0Current-account balance (US$ bn) -10.5a

External debt (US$ bn) 141.5b

Exchange rate (av; Ps:US$) 10.8Population (m) 103.6

a October 2002 to September 2003. b June 2003.

Sources: Instituto Nacional de Estadística, Geografía e Informática; Banco de México; Secretaría de Hacienda y Crédito Público;

Consejo Nacional de Población.

Agriculture has declined in importance economically (it accounted for just 4%of GDP in 2003) but remains an important source of employment (around one-fifth of the workforce is involved in agricultural activities). Mining is estimatedat just 1.4% of GDP in 2003 but this heavily understates the importance of oilproduction to the economy and, particularly, to the Treasury. Oil exportsrepresented 11.3% of total export earnings in 2003. The average price of oilduring the year stood at US$24.78/barrel, a significant increase compared withUS$21.58/b recorded in 2002.

The results of the first systematic attempt to measure informal economicactivities were published by the Instituto Nacional de Estadística, Geografía eInformática (INEGI, the National Institute of Statistics, Geography andInformatics) in August 2000. According to the results, the informal sector—excluding illegal activities—had a value of Ps445.5bn (US$47bn), equivalent to12.7% of GDP, and provided 17% of the profits generated by the economy. Ofnon-agricultural jobs, 28.5% are in the informal sector. Commerce andrestaurants employ the greatest number of workers informally, estimated ataround 30.8% of the total, followed by personal services (11.5%), manufacturing(6.1%), transportation (4.6%) and construction (3.3%).

The 1994-95 economic crisis hit domestic consumption and investment hard,but thanks to a weak exchange rate and privileged market access in the US andCanada (both of which were growing strongly) exports became the engine ofgrowth. Producers aggressively re-directed their production abroad. Until thesecond quarter of 2001 the growth in external trade was impressive, and largelyattributable to the dynamism of the maquiladora industry. Combined exportsand imports soared, from US$117bn in 1993 to US$341bn in 2000. From April2001 until June 2002, however, a sharp US economic slowdown reversed thetrend. Exports began to recover in July 2002, but strong competition in the USmarket from other countries such as China and weak productivity growth inMexico partly explains an uneven recovery. Estimates from INEGI indicate thatnon-oil exports increased by a meagre 0.4% in 2002 and 0.3% in 2003, with therespective figures for manufacturing being 0.5% and 0.4%.

Mexican exports lose out in USmarket

Mexico 27

© The Economist Intelligence Unit Limited 2004 www.eiu.com Country Profile 2004

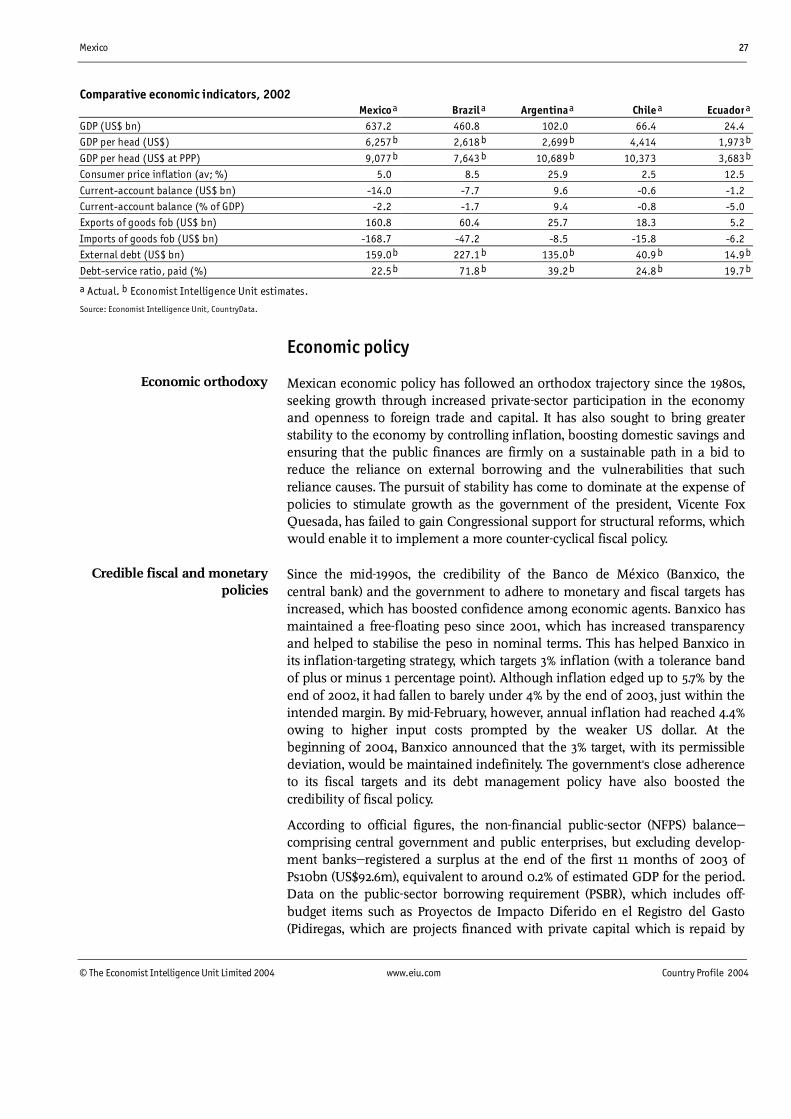

Comparative economic indicators, 2002Mexico a Brazil a Argentinaa Chile a Ecuadora

GDP (US$ bn) 637.2 460.8 102.0 66.4 24.4GDP per head (US$) 6,257b 2,618 b 2,699b 4,414 1,973b

GDP per head (US$ at PPP) 9,077b 7,643 b 10,689b 10,373 3,683b

Consumer price inflation (av; %) 5.0 8.5 25.9 2.5 12.5

Current-account balance (US$ bn) -14.0 -7.7 9.6 -0.6 -1.2Current-account balance (% of GDP) -2.2 -1.7 9.4 -0.8 -5.0Exports of goods fob (US$ bn) 160.8 60.4 25.7 18.3 5.2

Imports of goods fob (US$ bn) -168.7 -47.2 -8.5 -15.8 -6.2External debt (US$ bn) 159.0b 227.1 b 135.0b 40.9 b 14.9b

Debt-service ratio, paid (%) 22.5b 71.8 b 39.2b 24.8 b 19.7b

a Actual. b Economist Intelligence Unit estimates.

Source: Economist Intelligence Unit, CountryData.