Embed Size (px)

Citation preview

This second edition of Mergers & Acquisitions aims to provide an updated fi rst port of call for clients and lawyers to start to appreciate the issues in each jurisdiction. Each chapter is set out in such a way that readers can make quick comparisons between the litigation terrain in each country.

Foreword Martin Lipton, Wachtell, Lipton, Rosen & Katz

Australia Jonathan Wenig with Jeremy Lanzer & Jason van Grieken, Arnold Bloch Leibler

Austria Christian Herbst, Schoenherr

Belgium Peter Callens,Mathias Hendrickx & Gaia Pattyn,Loyens & Loeff

Brazil Antonio Corrêa Meyer, Arthur Bardawil Penteado, Clarissa Figueiredo de Souza Freitas & Raissa Fini, Machado, Meyer, Sendacz e Opice Advogados

British Virgin IslandsJohn Gosling, Walkers

Canada William M Ainley & Robin R Upshall, Davies Ward Phillips & Vineberg LLP

Cayman Islands Rolf Lindsay, Walkers

China Marissa Dong, Rui Liu & Zhang Xian, JunHe

Czech Republic Pavla Kopečková Přikrylová & Eva Špuláková, PETERKA & PARTNERS advokátní kancelář s.r.o.

Denmark Tomas Haagen & Caroline Boysen,Gorrissen Federspiel

Finland Juha Koponen,Janni Hiltunen & Johannes Piha, Borenius Attorneys Ltd

France Pierre Casanova, Benjamin Burman & Nicolas Mennesson,Darrois Villey Maillot Brochier

Germany Rolf Koerfer, Dr Günter Seulen & Dr Christoph Niemeyer, Oppenhoff & Partner

Greece Nikos Papachristopoulos & Sofi a Kontou,M & P Bernitsas Law Offi ces

Hungary Adam Illés &Blanka Pintér,PETERKA & PARTNERS

India Zia Mody, AZB & Partners

Italy Francesco Gianni, Raimondo Premonte & Massimiliano Macaione, Gianni, Origoni, Grippo, Cappelli & Partners

Japan Michi Yamagami,Yuichiro Nukada & Keita Tokura,Anderson Mori & Tomotsune

Jersey Adam Chester &Nigel Weston, Walkers

Luxembourg Thierry Lohest & Frédéric Franckx, Loyens & Loeff

The Netherlands Paul Cronheim & Michael Schouten, De Brauw Blackstone Westbroek NV

Poland Arkadiusz Rumiński & Krzysztof Banaszek,Noerr Menzer sp.k.

Republic of IrelandJustin McKenna & Matthew Cole,Mason Hayes & Curran

Romania Ioana Sebestin &Ioana Savan,PETERKA & PARTNERS

Russia Arkady Krasnikhin, Michael Copeland & Vyacheslav Yugai, Egorov Puginsky Afanasiev & Partners

Singapore Ng Wai King, Andrew Ang & Dawn Law, WongPartnership LLP

South Africa Prof Michael Katz, Doron Joffe, Matthew Morrison & Sanjay Kassen, ENSafrica

Spain Juan Carlos Machuca & Joaquín García-Cazorla,Uría Menéndez Abogados, SLP

Switzerland Mariel Hoch &Rolf Watter, Bär & Karrer AG

United Kingdom Charles Martin, Simon Perry, Harry Coghill &Tom Rose, Macfarlanes

United States of America Andrew J Nussbaum & Bert Y Ma, Wachtell, Lipton, Rosen & Katz

This second edition of Mergers & Acquisitions aims to provide an updated fi rst port of call for clients and lawyers to start to appreciate the issues in each jurisdiction. Each chapter is set out in such a way that readers can make quick comparisons between the litigation terrain in each country.

Foreword Martin Lipton, Wachtell, Lipton, Rosen & Katz

Australia Jonathan Wenig with Jeremy Lanzer & Jason van Grieken, Arnold Bloch Leibler

Austria Christian Herbst, Schoenherr

Belgium Peter Callens,Mathias Hendrickx & Gaia Pattyn,Loyens & Loeff

Brazil Antonio Corrêa Meyer,Arthur Bardawil Penteado, Clarissa Figueiredo de Souza Freitas & Raissa Fini, Machado, Meyer, Sendacz e Opice Advogados

British Virgin IslandsJohn Gosling, Walkers

Canada William M Ainley &Robin R Upshall, Davies Ward Phillips & Vineberg LLP

Cayman Islands Rolf Lindsay, Walkers

China Marissa Dong, Rui Liu & Zhang Xian, JunHe

Czech Republic Pavla Kopečková Přikrylová & Eva Špuláková, PETERKA & PARTNERS advokátní kancelář s.r.o.

Denmark Tomas Haagen & kCaroline Boysen,Gorrissen Federspiel

Finland Juha Koponen,Janni Hiltunen & Johannes Piha, Borenius Attorneys Ltd

France Pierre Casanova, Benjamin Burman & Nicolas Mennesson,Darrois Villey Maillot Brochier

Germany Rolf Koerfer, Dr Günter ySeulen & Dr Christoph Niemeyer, Oppenhoff & Partner

Greece Nikos Papachristopoulos & Sofi a Kontou,M & P Bernitsas Law Offi ces

Hungary Adam Illés &yBlanka Pintér,PETERKA & PARTNERS

India Zia Mody, AZB & Partners

Italy Francesco Gianni, yRaimondo Premonte &Massimiliano Macaione, Gianni, Origoni, Grippo, Cappelli & Partners

Japan Michi Yamagami,Yuichiro Nukada & Keita Tokura,Anderson Mori & Tomotsune

Jersey Adam Chester &yNigel Weston, Walkers

Luxembourg Thierry Lohest & Frédéric Franckx, Loyens & Loeff

The Netherlands Paul Cronheim & Michael Schouten, De Brauw Blackstone Westbroek NV

Poland Arkadiusz Rumiński & Krzysztof Banaszek,Noerr Menzer sp.k.

Republic of IrelandJustin McKenna & Matthew Cole,Mason Hayes & Curran

Romania Ioana Sebestin &Ioana Savan,PETERKA & PARTNERS

Russia Arkady Krasnikhin,Michael Copeland & VyacheslavYugai, Egorov Puginsky Afanasiev & Partners

Singapore Ng Wai King,Andrew Ang & Dawn Law, WongPartnership LLP

South Africa Prof Michael Katz,Doron Joffe, Matthew Morrison & Sanjay Kassen, ENSafrica

Spain Juan Carlos Machuca &Joaquín García-Cazorla,Uría Menéndez Abogados, SLP

Switzerland Mariel Hoch &Rolf Watter, Bär & Karrer AG

United Kingdom Charles Martin,Simon Perry, Harry Coghill &Tom Rose, Macfarlanes

United States of America Andrew J Nussbaum & Bert Y Ma, Wachtell, Lipton, Rosen & Katz

ME

RG

ER

S &

AC

QU

ISIT

ION

SIN

TE

RN

AT

ION

AL

SE

RIE

SS

EC

ON

D E

DIT

ION

M

ER

GE

RS

& A

CQ

UIS

ITIO

NS

INT

ER

NA

TIO

NA

L S

ER

IES

MERGERS &

ACQUISITIONSINTERNATIONAL SERIES

General Editors: Andrew J. Nussbaum, Wachtell, Lipton, Rosen & Katz &Charles Martin & Simon Perry, Macfarlanes LLP

SECOND EDITION

INTERNATIONAL SERIES

General Editors: Andrew J. Nussbaum, Wachtell, Lipton, Rosen & Katz &Charles Martin & Simon Perry, Macfarlanes LLP

SECOND EDITIONSECOND EDITION

MERGERS &

ACQUISITIONSINTERNATIONAL SERIES

General Editors:

Andrew J. Nussbaum

Wachtell, Lipton, Rosen & Katz

&

Charles Martin & Simon Perry

Macfarlanes LLP

General Editors

Andrew J. Nussbaum, Charles Martin & Simon Perry

Commissioning Editor

Emily Kyriacou

Commercial Director

Katie Burrington

Publishing Editor

Dawn McGovern

Editor

Chris Myers

Editorial Publishing Co-ordinator

Nicola Pender

Published in April 2016 by Thomson Reuters (Professional) UK Limited, trading as Sweet & Maxwell

Friars House, 160 Blackfriars Road, London, SE1 8EZ

(Registered in England & Wales, Company No 1679046.

Registered Offi ce and address for service:

2nd fl oor, 1 Mark Square, Leonard Street, London EC2A 4EG)

A CIP catalogue record for this book is available from the British Library.

ISBN: 9780414055407

Thomson Reuters and the Thomson Reuters logo are trade marks of Thomson Reuters.

Sweet & Maxwell and the Sweet & Maxwell logo are trade marks of Thomson Reuters.

Crown copyright material is reproduced with the permission of the Controller of HMSO and the Queen’s Printer for Scotland.

While all reasonable care has been taken to ensure the accuracy of the publication, the publishers cannot accept

responsibility for any errors or omissions.

This publication is protected by international copyright law.

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, or stored in any

retrieval system of any nature without prior written permission, except for permitted fair dealing under the Copyright, Designs

and Patents Act 1988, or in accordance with the terms of a licence issued by the Copyright Licensing Agency in respect of

photocopying and/or reprographic reproduction.

Application for permission for other use of copyright material including permission to reproduce extracts in other published works

shall be made to the publishers. Full acknowledgement of author, publisher and source must be given.

© 2016 Thomson Reuters (Professional) UK Limited

iii

CONTENTS

INTERNATIONAL SERIES

FOREWORD Martin Lipton | Wachtell, Lipton, Rosen & Katz ......................................................................................v

AUSTRALIA Jonathan Wenig with Jeremy Lanzer & Jason van Grieken | Arnold Bloch Leibler................................ 1

AUSTRIA Christian Herbst | Schoenherr ......................................................................................................................21

BELGIUM Peter Callens, Mathias Hendrickx & Gaia Pattyn | Loyens & Loeff ........................................................... 39

BRAZIL Antonio Corrêa Meyer, Arthur Bardawil Penteado, Clarissa Figueiredo de Souza Freitas & Raissa Fini |

Machado, Meyer, Sendacz e Opice Advogados ............................................................................................................... 53

BRITISH VIRGIN ISLANDS John Gosling | Walkers ............................................................................................. 71

CANADA William M Ainley & Robin R Upshall | Davies Ward Phillips & Vineberg LLP ........................................... 83

CAYMAN ISLANDS Rolf Lindsay | Walkers .............................................................................................................103

CHINA Marissa Dong, Rui Liu & Zhang Xian | JunHe ................................................................................................. 127

CZECH REPUBLIC Pavla Kopečková Přikrylová & Eva Špuláková | PETERKA & PARTNERS advokátní

kancelář s.r.o. ...................................................................................................................................................................145

DENMARK Tomas Haagen & Caroline Boysen | Gorrissen Federspiel .................................................................... 161

FINLAND Juha Koponen, Janni Hiltunen & Johannes Piha | Borenius Attorneys Ltd ............................................. 177

FRANCE Pierre Casanova, Benjamin Burman & Nicolas Mennesson | Darrois Villey Maillot Brochier ..................195

GERMANY Rolf Koerfer, Dr Günter Seulen & Dr Christoph Niemeyer | Oppenhoff & Partner ...............................219

GREECE Nikos Papachristopoulos & Sofi a Kontou | M & P Bernitsas Law Offi ces .................................................235

HUNGARY Adam Illés & Blanka Pintér | PETERKA & PARTNERS ..........................................................................249

INDIA Zia Mody | AZB & Partners ................................................................................................................................261

ITALY Francesco Gianni, Raimondo Premonte & Massimiliano Macaione | Gianni, Origoni, Grippo, Cappelli &

Partners ............................................................................................................................................................................281

JAPAN Michi Yamagami, Yuichiro Nukada & Keita Tokura | Anderson Mori & Tomotsune ......................................301

JERSEY Adam Chester & Nigel Weston | Walkers ..................................................................................................... 323

LUXEMBOURG Thierry Lohest & Frédéric Franckx | Loyens & Loeff ..................................................................... 337

THE NETHERLANDS Paul Cronheim & Michael Schouten | De Brauw Blackstone Westbroek NV ...................351

POLAND Arkadiusz Rumiński & Krzysztof Banaszek | Noerr Menzer sp.k. .............................................................365

REPUBLIC OF IRELAND Justin McKenna & Matthew Cole | Mason Hayes & Curran .......................................383

ROMANIA Ioana Sebestin & Ioana Savan | PETERKA & PARTNERS .....................................................................403

RUSSIA Arkady Krasnikhin, Michael Copeland & Vyacheslav Yugai | Egorov Puginsky Afanasiev & Partners ......421

iv

CONTENTS

INTERNATIONAL SERIES

SINGAPORE Ng Wai King, Andrew Ang & Dawn Law | WongPartnership LLP ..................................................... 437

SOUTH AFRICA Prof Michael Katz, Doron Joffe, Matthew Morrison & Sanjay Kassen | ENSafrica .................... 457

SPAIN Juan Carlos Machuca & Joaquín García-Cazorla | Uría Menéndez Abogados, SLP .....................................471

SWITZERLAND Mariel Hoch & Rolf Watter | Bär & Karrer AG ..............................................................................489

UNITED KINGDOM Charles Martin, Simon Perry, Harry Coghill & Tom Rose | Macfarlanes ............................ 509

UNITED STATES OF AMERICA Andrew J Nussbaum & Bert Y Ma | Wachtell, Lipton, Rosen & Katz ........... 537

CONTACT DETAILS ................................................................................................................................................. 557

vINTERNATIONAL SERIES v

FOREWORDMartin Lipton | Wachtell, Lipton, Rosen & Katz

No doubt this publication, which highlights the central M&A features in jurisdictions around the world, will be

well worn by dealmakers if 2016 resembles the 2015 global M&A environment. 2015 was a record year for M&A

transactions, both in the United States and globally, surpassing $5 trillion. Somewhat less well known is the cross-

border nature of a very high percentage of this activity.

While the US accounted for roughly 50% of recent deal volume, cross-border deals played a leading role as well.

Indeed, the very largest transactions in recent years have involved acquirors in different jurisdictions – witness the

blockbuster ($160 billion) Pfi zer–Allergan transaction, or Anheuser-Busch Inbev’s $130 billion bid for SABMiller plc.

One cannot fully appreciate the M&A landscape without global perspective; this is more true today than even a few

years ago, when the fi rst edition of this book appeared.

Indeed, it is not just in deal mass that the cross-border infl uence emerges. Hostile deals likewise know no borders –

consider, for example, Dutch Mylan NV’s hostile bid for Irish Perrigo Company plc, which, albeit unsuccessful, also

led to Israeli Teva Pharmaceutical’s unsolicited $40 billion bid for Perrigo (also later withdrawn when Teva agreed

to acquire a US-based generics business). There can be no doubt that dealmakers in one jurisdiction have become

both willing to pursue transformative deals outside their home country and comfortable in diving deeply into the

local rules, engaging with local investors and developing innovative deal techniques to gain traction. Of course,

legal and fi nancial advisors play a key role in developing this cross-border fl uency.

An interesting aspect of the current M&A boom is its persistence in spite of economic headwinds in many key

jurisdictions. While economic growth provides an important stimulus to strategic M&A activity, it is worth considering

whether the correlation on the downside is as strong. Even during a downturn, industry-specifi c factors, stockholder

activism and the need for cost savings may motivate acquirors even in a negative economic environment. A case in

point is the continued heavy pace of acquisitions by Chinese companies, which does not seem to have slowed despite

the downturn in the Chinese economy, Renminbi devaluation and volatile local equity markets. In the case of China,

deal-making refl ects long-term strategic decisions by companies largely immune to short-term pressures. The role

of activists in the US M&A market continues to grow. Some of our most well known companies have been infl uenced

by relatively small investments from vocal activists – DuPont, Dow and Yahoo!, to name but a few. Activists continue

to push aggressively for transactions, primarily for the expected short-term profi ts, whether through a spin-off,

divisional sale or whole-company transaction. Some of these US-based funds have begun to take their show on the

road, occasionally appearing in Europe, for example, and this should be expected to continue. When one considers

the large holdings of a relatively small number of institutional investors in many European companies, one can

easily see activists coalescing with these investors to exert substantial pressure on management for short-term deal-

making, particularly in jurisdictions where management and the board have a limited ability to implement takeover

defences once they are under attack. Companies would be well advised to assess their vulnerability to this line of

attack.

Another certainty is the ability of activists to invent new lines of attack. Consider the partnership between Pershing

Square and Valeant in the failed hostile bid for Allergan. Other activists have been willing on occasion to directly

make overbids when dissatisfi ed with deal terms, or to solicit competitive bids from third parties. In hostile situations,

vi

FOREWORD

INTERNATIONAL SERIES

activists who have invested in the bidder have even been known to make “investor presentations” publicly to the

target’s shareholders, encouraging them to pressure management to come to the table.

While traditional private equity transactions in recent years have been largely overwhelmed by corporate deal-

making, private capital continues to fi nd creative transactions and to be global in reach. Savvy private capital

investors have found new solutions to close deals, such as the innovative cash and tracking-stock structure used by

Dell and Silver Lake to acquire EMC Corporation. 3G Capital and Berkshire Hathaway have become models for the

relationship between corporate management and stable private equity capital.

In the United States, fi nancing private equity deals has become more challenging due to the Federal Reserve’s

leveraged lending guidelines, but large alternative non-bank fi nancing sources almost immediately emerged to fi ll

this gap, albeit sometimes on more onerous terms. The last few years have seen periods of tremendous uncertainty

in the high-yield market. While interest rates have generally been at historical lows, it has become apparent that not

all private equity deals are treated equally by lenders. On the other hand, the convergence of lending practices and

terms in the US and European debt markets has given issuers, both private equity and corporate, a further route to

successful fi nancing. The corporate debt environment has closely tracked the corporate M&A tempo, with several

record-breaking M&A fi nancings by corporate issuers being heavily oversubscribed.

While dealmakers have been busy, so too have regulators and other constituencies. One important lesson that

emerges is the absolute necessity to carefully and fully develop the regulatory, political and local benefi ts for a

deal prior to announcement. Competition authorities worldwide have become more sophisticated in analysing

the competitive impact of a transaction, and also entirely willing to scuttle large cross-border deals (such as the

Tokyo Electron–Applied Materials transaction), but experience demonstrates that even deals that are diffi cult from

a competitive standpoint can get done (such as the Holcim–Lafarge merger). The views of works councils, trade

unions and local politicians require especially careful consideration in the context of a cross-border deal, where the

perception of “exiting a country” may lead to legal and practical hurdles to a smooth closing.

In the United States, inversion transactions are not just the subject of regulatory scrutiny, but have also become

a feature of the presidential election debate. Political candidates have been heard to criticise as unpatriotic large

cross-border inversion deals that result in billions in savings to the parties due to lower global tax rates. Lacking

congressional consensus, the Treasury Department has developed ever more nuanced regulations to impede

these deals. And at least one large transaction, the $55 billion AbbVie–Shire plc merger, was abandoned when the

Treasury Department altered the rules in the interlocutory period.

Reviewing the recent years in M&A, it is diffi cult to predict yet another boom year ahead. Geopolitical confl icts span

the globe, oil prices continue to decline, markets have become even more volatile and important economies show

macro-fi nancial vulnerabilities. These factors will hamper confi dence, a key ingredient in any M&A deal, but just as

surely opportunities will also emerge. We look forward to further engagement with our international friends and

colleagues in this shared endeavour.

323INTERNATIONAL SERIES 323

JERSEYAdam Chester & Nigel Weston | Walkers

1. MARKET OVERVIEW

1.1 Please give a brief overview of the public M&A market in your jurisdiction

Jersey is a leading international fi nancial centre, with numerous Jersey companies listed on major stock exchanges

throughout the world, including the London Stock Exchange (LSE), the LSE’s AIM market (AIM)), Euronext, the New

York Stock Exchange, NASDAQ, the Toronto Stock Exchange and the Hong Kong Stock Exchange. The underlying

businesses owned by these listed Jersey companies span all continents and the full range of business sectors. The

market capitalisations of such companies range from a few million to billions of US dollars, with an aggregate

market capitalisation, as of 30 June 2015, of GBP 215 billion.

In addition, listed companies worldwide may have subsidiary entities in Jersey, and M&A transactions in any

jurisdiction may have an impact on relevant Jersey group companies.

There have recently been several high-profi le listed Jersey companies which have been the subject of a takeover

offer or scheme of arrangement and, as the market for public M&A is anticipated to improve generally, we expect to

see continued activity in this area.

1.2 What are the main laws and regulations governing the conduct of public M&A activity

in your jurisdiction?

The Companies (Jersey) Law 1991 (Companies Law) is the primary corporate law statute relevant to the regulation

of mergers and acquisitions of Jersey-incorporated companies. Part 18 (Takeovers) of the Companies Law includes

provisions concerning takeover offers and, in particular, squeeze-out rights.

Other statutes which may be relevant are:

• Financial Services (Jersey) Law 1998 – this law contains certain offences relevant to the conduct of public

M&A activity, including offences relating to insider dealing, market manipulation and providing misleading

information. Additionally, this is the primary statute under which fi nancial service businesses are regulated

in Jersey by the Jersey Financial Services Commission. Any relevant regulatory obligations (for example, prior

consent or notifi cation provisions) in respect of a regulated business are likely to derive from this legislation.

• Competition (Jersey) Law 2005 – this law promotes competition in the supply of goods and services in

Jersey. It provides that certain mergers and acquisitions must not be executed without approval of the Jersey

Competition Regulatory Authority, which may refuse to grant its approval if it is satisfi ed that the merger or

acquisition would substantially lessen competition in Jersey or any part of Jersey.

• Control of Housing and Work (Jersey) Law 2012 – this law controls the carrying on of business and

employment in Jersey. Pursuant to this law, it may be necessary to notify and/or obtain consent from the States

of Jersey in relation to a change of control of a Jersey entity that trades or conducts business in Jersey (but this

does not apply to any undertaking listed on a recognised stock exchange).

324

JERSEY

INTERNATIONAL SERIES

In addition, the City Code on Takeovers and Mergers (the Code) applies in Jersey as a result of the implementation

of the Companies (Takeovers and Mergers Panel) (Jersey) Law 2009, which placed the authority of the UK Panel on

Takeovers and Mergers (the Panel) in Jersey on a statutory footing.

The Code applies in relation to any offer (also referred to below as a bid (and therefore any offeror is referred to

as a bidder below)) for a Jersey company which has its securities admitted to trading on a regulated market or a

multilateral trading facility in the UK (for example, the London Stock Exchange’s main or AIM markets), or on any

stock exchange in the Channel Islands or the Isle of Man. The Code may also apply in relation to a bid for a public

(and sometimes private) Jersey company which is considered by the Panel to have its place of central management

and control in the UK, the Channel Islands or the Isle of Man.

If the Code applies, the relevant takeover or merger will be regulated by the Panel, whose main functions are to issue

and administer the Code, and to supervise and regulate takeovers and other matters to which the Code applies.

1.3 Other than in relation to competition, are there other applicable regulations such as

exchange and investment controls?

In certain circumstances, it will be necessary to obtain the prior approval of the Jersey Financial Services Commission

(for example, where the target company carries on any regulated business, such as fi nancial service business within

the meaning of the Financial Services (Jersey) Law 1998 or deposit-taking business within the meaning of the

Banking Business (Jersey) Law 1991). Other matters are referred to briefl y in Section 1.2.

There are no foreign exchange controls or foreign exchange regulations under the currently applicable laws of

Jersey.

1.4 Do the main laws and regulations governing the conduct of public M&A facilitate or

hinder such activity in your jurisdiction?

The laws and regulations of Jersey, which provide protections for consumers and shareholders in the context of

M&A, are similar in many ways to those afforded in respect of UK companies (for example, the application of the

Code and competition law). To the extent that there are local requirements for M&A (for example, where the target

is a locally regulated business or trade, or does business in Jersey), our experience is that the Jersey authorities apply

local regulations in a pragmatic way to facilitate M&A activity provided that they are satisfi ed that consumers and

the local economy are adequately protected.

2. PREPARATION AND PRE-ANNOUNCEMENT

2.1 What are the main structural means of obtaining control of a public company? If there

is more than one, what are the key advantages and disadvantages of each route? Is one

route more commonly used than others?

The main structural means of obtaining control of a Jersey company are:

• Takeover offer under Part 18 of the Companies Law: for example, Company A makes an offer to the shareholders

of Company B to acquire the shares of Company B. If the offer is accepted, Company B becomes a subsidiary of

325

JERSEY

INTERNATIONAL SERIES

Company A. Assuming that Company B is a Jersey company, the required shareholder approval percentage of

Company B to enable Company A to implement the “squeeze-out” provisions under Jersey law is 90%.

• Statutory merger under Part 18B of the Companies Law: Jersey law enables Jersey-incorporated companies to

merge with a range of corporate bodies, whether incorporated in or outside of Jersey. In the case of a merger

effected pursuant to Jersey law, the required shareholder approval percentage of any Jersey company which is

a party to the merger is a two-thirds majority (unless a higher threshold is specifi ed in the Jersey company’s

constitutional documents).

• Scheme of arrangement under Part 18A of the Companies Law: where an arrangement or compromise is

proposed between a Jersey company and its members, the Jersey court may order a meeting of the members

to be called in such manner as the court directs. If a majority constituting three-quarters of the members at the

meeting agrees to the arrangement or compromise, it will be binding on the members and the Jersey company,

if sanctioned by the court. The court of Jersey is very familiar with and experienced at approving schemes of

arrangement over Jersey companies.

In terms of advantages and disadvantages, the main advantage of a statutory merger is that it requires shareholder

approval by way of special resolution (of any Jersey company which is a party to the merger) in order to achieve full

control of the target. In contrast, attaining full control in a takeover requires acceptances from at least 90% of the

shares subject to the offer (to entitle the bidder to “squeeze out” the remaining shareholders) and attaining 100%

control in a scheme of arrangement requires approval from a majority in number representing at least 75% in value

of those target shareholders who vote on the scheme (together with the court’s approval). Schemes of arrangement

are more commonly used than takeovers despite the added cost of obtaining the court’s sanction because of the

ability to bind all shareholders with a lower acceptance threshold. Statutory mergers, despite the potentially lower

shareholder approval threshold, are not used frequently because of a requirement to notify creditors of a merger

and their ability to object.

2.2 Outline any secrecy and disclosure obligations placed on bidders and target companies

ahead of any formal announcement of a bid

If the Code applies, then, prior to the announcement of a bid or a possible bid, all persons privy to confi dential

information, and particularly price-sensitive information, concerning the bid or possible bid must treat that

information as secret and may only pass it to another person if it is necessary to do so and if that person is made

aware of the need for secrecy. All such persons must conduct themselves so as to minimise the chances of any leak

of information (Rule 2.1 of the Code).

If the Code does not apply, Jersey law does not otherwise specify any secrecy or disclosure obligations. However, it

may be prudent to maintain secrecy for commercial and/or other reasons. In addition, the laws and/or regulations of

other jurisdictions (for example, the rules of the stock exchange on which the target company is admitted to trading)

might impose secrecy or disclosure obligations on the bidder and/or target company.

326

JERSEY

INTERNATIONAL SERIES

2.3 Are there any constraints on the ability of a bidder to carry out due diligence on the

target?

This will usually depend on whether the bid is a recommended bid or a hostile bid. In the case of a hostile bid, the

bidder’s due diligence will usually be limited to publicly available information regarding the target company. The

following information regarding a Jersey public company will generally be publicly available:

• Its latest annual audited accounts.

• Its constitutional documents.

• Any special (but not ordinary) resolutions passed by its shareholders.

• Its annual returns, which in the case of a public company will confi rm the names of the directors of record and

the shareholders with over 1% of the shareholding of the company (as well as the number of shareholders

holding less than 1%) as at 1 January in the relevant year (in any event, the register of shareholders and register

of directors of a public company must be available for public inspection).

• Whether it is a regulated entity in Jersey.

• Whether it has been declared bankrupt (en désastre) in Jersey.

• Whether certain types of litigation have been commenced against it in the courts of Jersey.

However, if the Code applies, and the target company has provided information to a competing bidder or a potential

bidder, Rule 20.2 of the Code provides that any information given to such competing bidder or potential bidder,

whether publicly identifi ed or not, must, on request, be given equally and promptly to another bidder or bona fi de

potential bidder even if that other bid is less welcome. This requirement will usually only apply when there has been

a public announcement of the existence of the bidder or potential bidder to which information has been given or,

if there has been no public announcement, when the bidder or bona fi de potential bidder requesting information

under this rule has been informed authoritatively of the existence of another potential bidder.

In the case of a recommended bid, access to information regarding the target company will normally be a condition

of the bidder agreeing to proceed with the bid. However, a target company will often seek to limit the extent of the

information made available to the bidder (for example, if the bidder is a competitor and/or the target company does

not want to risk having to provide such information to a hostile bidder due to the operation of Rule 20.2).

2.4 Is it possible for a target company to grant a bidder exclusivity and/or a break fee? Are

there any other steps which can be taken to provide greater certainty to a bidder that

its bid will be successful?

Under Rule 21.2 of the Code, neither a target company nor a person acting in concert with it may, except with the

consent of the Panel, enter into any “offer-related arrangement” with a bidder (or any person acting in concert with a

bidder) during an offer period or when a bid is reasonably in contemplation. “Offer-related arrangement” is broadly

defi ned, and would include an exclusivity or break fee arrangement.

327

JERSEY

INTERNATIONAL SERIES

If the Code does not apply, then the granting of exclusivity and/or a break fee will need to be carefully considered

in the context of the statutory and fi duciary duties of the directors of the target company. Jersey law provides that a

director, in exercising the director’s powers and discharging the director’s duties, must act honestly and in good faith

with a view to the best interests of the company, and must exercise the care, diligence and skill that a reasonably

prudent person would exercise in comparable circumstances.

2.5 Are there any restrictions on a bidder obtaining commitments from a target company’s

shareholders ahead of the announcement of a bid?

If the Code applies, then due consideration will need to be given to Rule 2.2(e), which requires an announcement

to be made when negotiations or discussions are about to be extended to more than a very restricted number of

people (outside of those who need to know in the parties concerned and their immediate advisers). In addition, Rule

4.3 of the Code provides that any person proposing to contact a private individual or small corporate shareholder

with a view to seeking an irrevocable commitment must consult the Panel in advance.

If the Code does not apply, Jersey law does not otherwise specify any restrictions on obtaining commitments from a

target company’s shareholders ahead of the announcement of a bid. However, the target company’s constitutional

documents may contain applicable provisions, and the laws and/or regulations of other jurisdictions (for example,

the rules of a stock exchange on which the target company’s shares are traded) might also be relevant.

2.6 Are the directors of the target company under any particular obligations or duties in

the period leading up to a bid?

If the Code applies, then the directors of the target company will be under the obligations and duties specifi ed therein.

These include the secrecy obligations described above and the obligations regarding when an announcement is

required as specifi ed in Rule 2.2 of the Code (see Section 3).

If the Code does not apply, then Jersey law does not specify any particular obligations or duties in these

circumstances.

3. ANNOUNCEMENT OF A BID

3.1 At what stage does a bid have to be announced?

If the Code applies, there are a number of situations in which an announcement is required by Rule 2.2 of the Code.

These include:

• When a fi rm intention to make a bid is notifi ed to the board of the target company by or on behalf of a bidder,

irrespective of the attitude of the board to the bid.

• Where the bidder (or parties acting in concert with the bidder) acquires an interest that results in it holding: (i)

30% or more of the voting rights in the target company; or (ii) an interest in shares carrying between 30% and

50% of the voting rights in the target company.

328

JERSEY

INTERNATIONAL SERIES

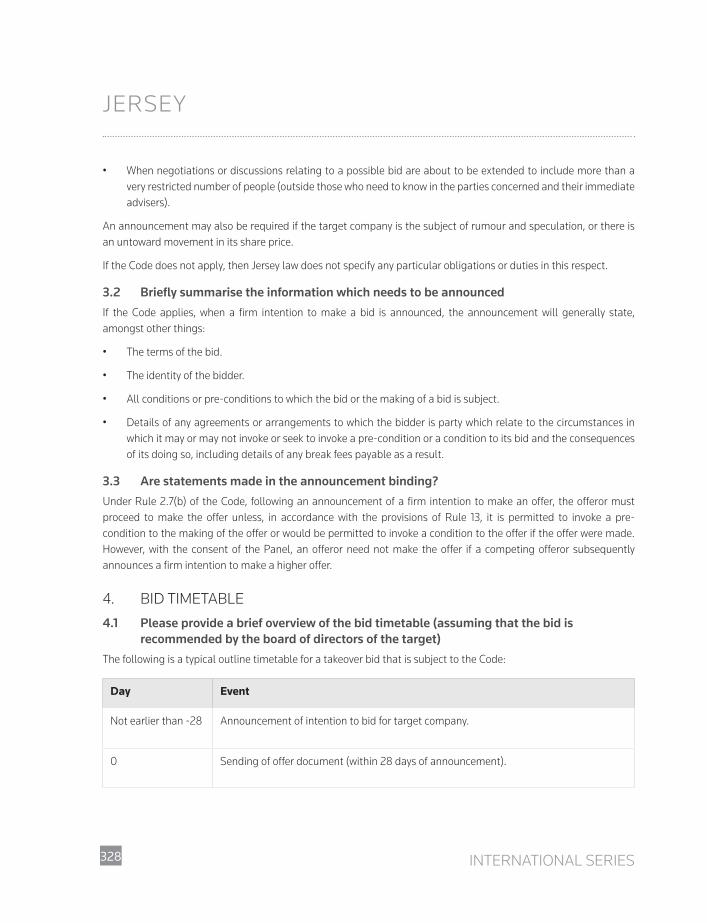

• When negotiations or discussions relating to a possible bid are about to be extended to include more than a

very restricted number of people (outside those who need to know in the parties concerned and their immediate

advisers).

An announcement may also be required if the target company is the subject of rumour and speculation, or there is

an untoward movement in its share price.

If the Code does not apply, then Jersey law does not specify any particular obligations or duties in this respect.

3.2 Briefl y summarise the information which needs to be announced

If the Code applies, when a fi rm intention to make a bid is announced, the announcement will generally state,

amongst other things:

• The terms of the bid.

• The identity of the bidder.

• All conditions or pre-conditions to which the bid or the making of a bid is subject.

• Details of any agreements or arrangements to which the bidder is party which relate to the circumstances in

which it may or may not invoke or seek to invoke a pre-condition or a condition to its bid and the consequences

of its doing so, including details of any break fees payable as a result.

3.3 Are statements made in the announcement binding?

Under Rule 2.7(b) of the Code, following an announcement of a fi rm intention to make an offer, the offeror must

proceed to make the offer unless, in accordance with the provisions of Rule 13, it is permitted to invoke a pre-

condition to the making of the offer or would be permitted to invoke a condition to the offer if the offer were made.

However, with the consent of the Panel, an offeror need not make the offer if a competing offeror subsequently

announces a fi rm intention to make a higher offer.

4. BID TIMETABLE

4.1 Please provide a brief overview of the bid timetable (assuming that the bid is

recommended by the board of directors of the target)

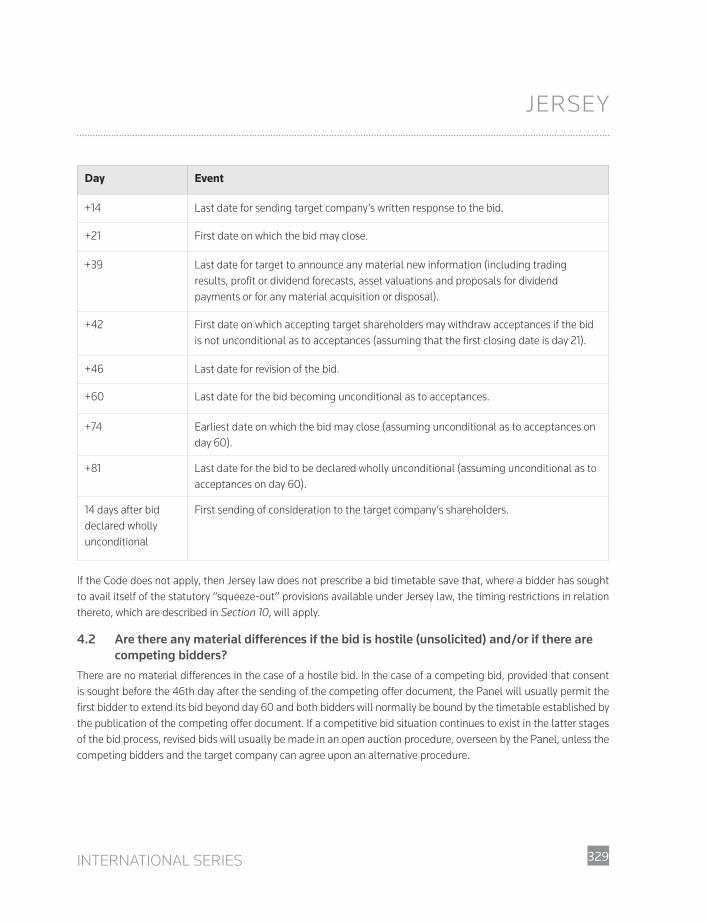

The following is a typical outline timetable for a takeover bid that is subject to the Code:

Day Event

Not earlier than -28 Announcement of intention to bid for target company.

0 Sending of offer document (within 28 days of announcement).

329

JERSEY

INTERNATIONAL SERIES

Day Event

+14 Last date for sending target company’s written response to the bid.

+21 First date on which the bid may close.

+39 Last date for target to announce any material new information (including trading

results, profi t or dividend forecasts, asset valuations and proposals for dividend

payments or for any material acquisition or disposal).

+42 First date on which accepting target shareholders may withdraw acceptances if the bid

is not unconditional as to acceptances (assuming that the fi rst closing date is day 21).

+46 Last date for revision of the bid.

+60 Last date for the bid becoming unconditional as to acceptances.

+74 Earliest date on which the bid may close (assuming unconditional as to acceptances on

day 60).

+81 Last date for the bid to be declared wholly unconditional (assuming unconditional as to

acceptances on day 60).

14 days after bid

declared wholly

unconditional

First sending of consideration to the target company’s shareholders.

If the Code does not apply, then Jersey law does not prescribe a bid timetable save that, where a bidder has sought

to avail itself of the statutory “squeeze-out” provisions available under Jersey law, the timing restrictions in relation

thereto, which are described in Section 10, will apply.

4.2 Are there any material differences if the bid is hostile (unsolicited) and/or if there are

competing bidders?

There are no material differences in the case of a hostile bid. In the case of a competing bid, provided that consent

is sought before the 46th day after the sending of the competing offer document, the Panel will usually permit the

fi rst bidder to extend its bid beyond day 60 and both bidders will normally be bound by the timetable established by

the publication of the competing offer document. If a competitive bid situation continues to exist in the latter stages

of the bid process, revised bids will usually be made in an open auction procedure, overseen by the Panel, unless the

competing bidders and the target company can agree upon an alternative procedure.

330

JERSEY

INTERNATIONAL SERIES

4.3 What are the key documents which the shareholders of a target company would

typically receive on a bid?

In the case of a recommended bid, the target company’s shareholders will typically receive an offer document, a

circular (where their approval of the bid is required), an acceptance form, and a prospectus or equivalent document

(if required). In the case of a hostile bid, the target will also typically receive defence documents, which will often

include trading updates, profi t or dividend forecasts and, where applicable, a revised offer document.

5. FUNDING AND CONSIDERATION

5.1 At what stage does a bidder need to have funding in place? Are there any legal or

regulatory requirements which the bidder must satisfy to show that its funding is

suffi cient?

If the Code applies, the bidder must announce a bid only after ensuring that it can fulfi l in full any cash consideration,

if such is offered, and after taking all reasonable measures to secure the implementation of any other type of

consideration (General Principle 5). When the bid is for cash or includes an element of cash, the offer document

must include confi rmation by an appropriate third party (for example, the bidder’s fi nancial adviser) that suffi cient

resources are available to the bidder to satisfy full acceptance of the bid (Rule 24.8).

If the Code does not apply, then Jersey law does not specify any particular obligations or duties in this respect.

However, if a bidder has sought to avail itself of the statutory “squeeze-out” provisions described in Section 10, then

the bidder must make payment to the company for the shares at the end of six weeks from the date of the “squeeze-

out” notice.

5.2 What are the main sources of funding usually obtained by bidders (for example, capital

markets/banks/alternative lenders)?

The main sources of funding for recent bids have tended to be debt fi nancing, in many cases together with the

bidder’s existing cash resources, and often combined with an equity issue.

5.3 Are there any limits on the ability to use assets of the target company to secure a

bidder’s funding?

It is fairly typical for a lender to require as collateral the new assets of the bidder (that is, the target), the value of

which would correlate to the lending.

5.4 Can the consideration offered by a bidder take any form? Are there any special

requirements the bidder must satisfy if the consideration is not in cash? Is a foreign

bidder able to offer its shares as consideration for the bid

If the Code applies, the type of consideration will depend on whether the bid is voluntary or mandatory. In the case of

a voluntary bid, there is generally no restriction on the method of its fi nancing, though consideration will typically be

in the form of cash, loan notes and/or shares. By contrast, mandatory bids must be made in cash (or at least contain

a cash alternative). Broadly, a mandatory bid must be made where the bidder (or parties acting in concert with the

331

JERSEY

INTERNATIONAL SERIES

bidder) acquires an interest that results in it holding: (i) 30% or more of the voting rights in the target company; or

(ii) an interest in shares carrying between 30% and 50% of the voting rights in the target company.

If the Code does not apply, then Jersey law does not specify any particular obligations or duties in this respect.

5.5 Can the bidder offer different consideration to different shareholders?

The fi rst General Principle of the Code is that all holders of the securities of an offeree company of the same class

must be afforded equivalent treatment.

The Code states that an offer made under Rule 9 must, in respect of each class of share capital involved, be in cash

or be accompanied by a cash alternative at not less than the highest price paid by the offeror or any person acting

in concert with the offeror for any interest in shares of that class during the 12 months prior to the announcement

of that offer. The Panel should be consulted where there is more than one class of share capital involved. The

Companies Law provides that a “takeover offer”, being one over which “squeeze-out” rights can be invoked, must be

an offer on terms which are the same in relation to all the shares to which the offer relates. However, the Companies

Law allows an offer to still constitute a takeover offer if shareholders in a jurisdiction where it is impossible or diffi cult

to accept the offer are excluded from the offer and it also allows variations to be made to an offer if the laws of a

particular jurisdiction are unduly onerous or preclude the offer being made to a particular shareholder provided that

an alternative that is offered is of substantially equivalent value. This enables a bidder to avoid breaching certain

securities laws in some shareholders’ jurisdictions (for example, by offering those shareholders a cash alternative

rather than shares).

6. CONDITIONS

6.1 Can a bid be made subject to the satisfaction of any pre-conditions? If so is there any

restriction on the content of any such pre-conditions?

If the Code applies, then a voluntary bid can be made subject to the satisfaction of pre-conditions. In such a case, the

Panel must be consulted in advance about any proposal to include in an announcement any pre-condition to which

the bid will be subject. As a general rule, the Panel will not consent to the inclusion of a pre-condition if such pre-

condition depends solely on subjective judgements by the directors of the bidder or of the target company. Except

with the consent of the Panel, a bid must not be announced subject to a pre-condition unless the pre-condition

relates to a decision that there will be no reference to the competition authority or initiation of proceedings by the

European Commission, or it involves another material offi cial authorisation or regulatory clearance relating to the

bid. In the case of a mandatory bid, save with the consent of the Panel, no conditions are permitted (other than that

the bidder obtain acceptances which give it over 50% of the voting rights of the target company).

If the Code does not apply, then Jersey law does not specify any particular obligations or duties in relation to

conditions or pre-conditions.

332

JERSEY

INTERNATIONAL SERIES

6.2 Are there any conditions usually attached to a bid? Other than as a result of law and

regulation specifi c to particular sectors and/or bidders are there any mandatory

conditions?

If the Code applies, it is typically a condition of a voluntary bid that the bidder’s shareholders pass any resolutions

necessary to approve the bid and that any applicable merger and/or other regulatory clearance is obtained. Where

the bidder itself is a listed company and the consideration for the bid includes new shares in the bidder, it will usually

also be a condition of the bid that the relevant listing authority or stock exchange approves the listing of such new

shares.

If the Code applies, it must be a condition of any bid for voting equity share capital or for other transferable securities

carrying voting rights which, if accepted in full, would result in the bidder holding shares carrying more than 50% of

the voting rights of the target company that the bid will not become or be declared unconditional as to acceptances

unless the bidder has acquired or agreed to acquire (either pursuant to the bid or otherwise) shares carrying more

than 50% of the voting rights. However, it is often a condition of bids for Jersey companies that the bidder acquire

at least 90% of the company’s shares, so that the bidder can avail itself of the statutory “squeeze-out” provisions

described in Section 10.

If the Code does not apply, then Jersey law does not specify any particular obligations or duties in this respect.

However, the rules of the stock exchange on which the target company is admitted to trading might impose

obligations or duties on the target company.

6.3 If a condition is not satisfi ed, can the bidder choose not to proceed with the bid?

If the Code applies, except with the consent of the Panel, all conditions must be fulfi lled or the bid must lapse

within 21 days of the fi rst closing date or of the date the bid becomes or is declared unconditional as to acceptances,

whichever is the later (Rule 31.7).

If the Code does not apply, then there is no restriction on this from a Jersey law perspective.

7. STAKEBUILDING

7.1 Is a bidder free to buy shares in the target in the period leading up to a bid and

subsequently? If so, what are the disclosure requirements?

Restrictions

If the Code applies, there are a number of restrictions on dealings in shares of the target company (Rules 4.1, 4.2 and

4.4). For example, no dealings in shares of the target company by any person who is not the bidder but who is privy

to confi dential price-sensitive information concerning a bid or contemplated bid may take place between the time

when there is reason to suppose that an approach or a bid is contemplated and the announcement of the approach

or bid or of the termination of the discussions.

Pursuant to Rule 5 of the Code, save in the case of the exceptions in Rule 5.2 (one of which is where a mandatory

offer is made under Rule 9), a bidder (and parties acting in concert with the bidder) must not acquire an interest that

333

JERSEY

INTERNATIONAL SERIES

results in it holding: (i) 30% or more of the voting rights in the target company; or (ii) an interest in shares carrying

between 30% and 50% of the voting rights in the target company.

In addition, except with the consent of the Panel, a bidder (or parties acting in concert with a bidder) may not make

any arrangements with shareholders and may not deal or enter into arrangements to deal in shares of the target

company, or enter into arrangements which involve acceptance of a bid, either during a bid or when one is reasonably

in contemplation, if there are favourable conditions attached which are not being extended to all shareholders (Rule

16.1).

If the Code does not apply, then Jersey law does not specify any particular obligations or duties in this respect.

However, it should be noted that both market manipulation and insider dealing are offences under Jersey law.

Disclosure

If the Code applies, then Rule 8 of the Code requires the bidder to make certain disclosures of its dealings and

positions in the target company’s shares after the announcement that fi rst identifi es it as a bidder.

If the Code does not apply, the target company’s constitutional documents may still impose disclosure obligations in

relation to dealings and positions in the company’s shares, and failure to comply with any such disclosure obligations

may result in the imposition of penalties (for example, loss of voting rights).

7.2 Are there any material consequences for the bidder or target if stakebuilding does take

place?

The most obvious issue with stakebuilding is the requirement to make a mandatory bid in cash for the target where

the bidder (or parties acting in concert with the bidder) acquires an interest that results in it holding: (i) 30% or more

of the voting rights in the target company; or (ii) an interest in shares carrying between 30% and 50% of the voting

rights in the target company (Rule 9). Furthermore, any stakebuilding ahead of a takeover offer might make it more

diffi cult to acquire or contract to acquire 90% of the shares in the target company (and therefore, consequently,

being able to invoke “squeeze-out” rights).

7.3 Are there any circumstances in which a bidder could become bound to make a

mandatory bid?

Yes – see the commentary above in respect of Rule 9 of the Code.

8. RECOMMENDED BIDS

8.1 Where a bid is recommended, does the target board require a “fi duciary out” (the

ability to withdraw its recommendation)? If so, what is the scope of this right and what

are the consequences for the bid?

There are no requirements under Jersey law in this respect. However, from a commercial perspective, and in order to

allow a target company board to take account of its statutory and fi duciary obligations, a commitment of such board

to recommend a bid will generally be given subject to a “fi duciary out”.

334

JERSEY

INTERNATIONAL SERIES

9. HOSTILE BIDS

9.1 How can a target company defend against a hostile bid?

If the Code applies, then General Principle 3 and Rule 21 of the Code restrict the ability of a target company board

to frustrate a bid. General Principle 3 states that a target company board must not deny the holders of shares the

opportunity to decide on the merits of a bid. Rule 21 provides that, during the course of a bid, or even before the date

of the bid if the board of the target company has reason to believe that a bona fi de bid might be imminent, the board

must not, without the approval of the shareholders in general meeting:

• Take any action which may result in any bid or bona fi de possible bid being frustrated or shareholders being

denied the opportunity to decide on its merits.

• Issue any shares, or transfer or sell, or agree to transfer or sell, any shares out of treasury; issue or grant

options in respect of any unissued shares; create or issue, or permit the creation or issue of, any securities

carrying rights of conversion into or subscription for shares; sell, dispose of or acquire, or agree to sell,

dispose of or acquire, assets of a material amount; or enter into contracts otherwise than in the ordinary

course of business.

Rule 21 prohibits certain defence tactics which would be permitted in other jurisdictions – for example,

“poison pills”, whereby actions are taken to prevent the target company from being able to be acquired or to

discourage a bid by making it more expensive to acquire the target company or by reducing the value of the target

company.

Typically, including in cases where the Code does not apply, a target company board will seek to fend off a hostile

bid by attempting to persuade shareholders that the bid undervalues the company or is unattractive for some

other reason (for example, the bid will place a signifi cant fi nancial strain on the business, or consent of a relevant

regulatory authority is unlikely to be granted).

10. CONTROL REQUIREMENTS, TREATMENT OF DISSENTING SHAREHOLDERS AND COMPULSORY ACQUISITION OF SHARES

10.1 What are the minimum acceptance thresholds required to obtain control of a target

company?

Generally, 50% of the target company’s shares is the minimum acceptance threshold.

10.2 What protections (if any) do non-accepting shareholders have against a bid becoming

successful and/or its terms?

Under the Companies Law, on delivery of a “squeeze-out” notice, a non-accepting shareholder has a right to apply

to the Jersey court that the offeror not be entitled to acquire the shares or specify terms of acquisition that are

different to the offer. In a scheme of arrangement, a dissenting shareholder has an opportunity to attend the court

hearing to consider the application to sanction the scheme and may try to challenge the application.

335

JERSEY

INTERNATIONAL SERIES

10.3 Briefl y describe any compulsory acquisition or “squeeze-out” provisions a bidder may

be able to take advantage of to acquire the shares of non-accepting shareholders

Where a person has acquired or contracted to acquire 90% of a company’s shares (to which a bid relates) by virtue

of a bid to acquire all of the shares in the company (other than those already held by the bidder), they can serve

a notice on the remaining shareholders confi rming that they wish to buy the shares held by those shareholders.

No notice can be served unless the person has acquired or contracted to acquire 90% of the shares within four

months of the original bid. The notice must be given within two months of acquiring or contracting to acquire

90% of the shares. The bidder must send a copy of the notice to the company. The bidder is bound to acquire the

shares on the terms of the bid. At the end of six weeks from the date of the notice, the bidder must send a copy

of the notice to the company and pay the company for the shares. The copy of the notice must be accompanied

by a share transfer form executed on behalf of the shareholder by a person appointed by the bidder. On receipt,

the company must register the bidder as the shareholder. There are also rights of minority shareholders to serve

a notice requiring their shares be bought by a bidder who has acquired or contracted to acquire 90%. Generally,

there is no requirement for an application to the court. However, the court has jurisdiction to hear relevant

applications.

11. DE-LISTING

11.1 What are the requirements for de-listing a target company’s shares following a

successful bid?

This will depend on the rules of the relevant listing authority or stock exchange, but will typically require shareholder

approval.

12. TRANSFER TAXES

12.1 Are there any transfer taxes payable on a bid for a target company incorporated in your

jurisdiction under the various routes described above?

No stamp duty or other transfer taxes will be payable in Jersey in relation to a public takeover transaction in respect

of a Jersey company.

13. EMPLOYEE ISSUES

13.1 Are there any employee notifi cation or consultation requirements on a bid?

If the Code applies, then the offer document must state, among other things, the bidder’s intentions regarding the

continued employment of the employees of the target company and its subsidiaries, including any material change

in the conditions of employment. It must also state the bidder’s strategic plans for the target company, and their

likely repercussions on employment and the locations of the target company’s places of business (Rule 24.2).

The Code also requires certain documents (for example, the offer announcement and offer document) to be made

available to the appropriate employee representatives or, where there are no such representatives, to the employees

themselves.

336

JERSEY

INTERNATIONAL SERIES

If the Code does not apply, then Jersey law does not otherwise oblige a target company to notify or consult with its

employees in relation to a bid.

14. FOREIGN BIDS

14.1 Describe your jurisdiction’s level of cross-border M&A activity (including whether

particular countries or regions are more active counterparties than others)

Almost all public M&A activity in Jersey is cross-border. M&A sentiment has generally been recovering since the

economic downturn and we anticipate stronger performance in this sector. Counterparties tend to be global

businesses, but many derive from the US, UK, Russia and China.

14.2 Are there any laws or regulations or local practice that may raise particular challenges

or impediments for foreign bidders?

There should not be any particular impediments just because a bidder of a target company’s shares is foreign,

although foreign bidders should be aware that there is likely to be a requirement for regulatory consent to be

obtained if the target company is a regulated entity under the Financial Services (Jersey) Law 1998.

14.3 Are there any particular legal, regulatory or other requirements applied to foreign

bidders that are not generally applied to local bidders?

There are not likely to be any except possibly in relation to the Control of Housing and Work (Jersey) Law 2012 insofar

as the bid results in a change of control over a target company that trades or conducts business in Jersey and which

is not listed on a recognised stock exchange.

15. CURRENT TOPICAL ISSUES AND TRENDS

15.1 Please summarise any current issues or trends relating to public M&A activity in your

jurisdiction

In common with other global fi nancial centres, there has been an increase in M&A activity involving Jersey vehicles

and the cross-border element has grown in prominence. Much of the focus on the M&A side globally has been on

small- to mid-cap companies as they expand and look to become more international in both their investor base and

strategic outlook.

As mentioned above, the Companies Law permits the merger between a Jersey-incorporated company and

companies incorporated outside of Jersey. Previously, if a foreign company and a Jersey company had wanted to

merge, then one company would have had to relocate to where the other was incorporated.

With the current interest in Jersey-incorporated companies from growing markets such as India, Hong Kong and

China, investors have a wide range of options to meet their investment objectives and, in particular, are fi nding it

easier to put capital to work in Europe and repatriate the profi ts.