Embed Size (px)

Citation preview

Members’ AGMUniversity of Aberdeen Superannuation & Life Assurance Scheme

David Gordon 14 June 2011

© 2011 Towers Watson. All rights reserved.

2towerswatson.com© 2011 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Agenda

Trustees and their responsibilities

Highlights from the accounts

Scheme benefit changes

Actuarial update

3towerswatson.com© 2011 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

3

Trustees

Dr Alistair Mair – Convenor

Ms Irene Bews – Director of Finance

Mr Steve Cannon – Secretary to the University

Prof Chris Gane – Vice Principal

Mrs Diane Massie – Member Nominated

Mr Brian Paterson – Member Nominated

The Trustees met on five occasions over the year

Member nominated trustees serve for three year terms – next election due 2013

The Trustees are also assisted on investment matters by:

Prof Alex Kemp

Prof Angela Black

Towers Watson

4towerswatson.com© 2011 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

4

Roles and responsibilities

Trustees The Scheme is set up under a Trust Assets are held separately from University assets Trustees run the Trust in the line with the Scheme rules Trustees look after the benefits of the members Under the rules of the Scheme the Trustees determine the University’s contribution

rate in consultation with the University

University Funds the Scheme Responsible for deciding what future benefits are provided

The Pensions Regulator Protects members’ benefits

Pension Protection Fund Provides a benefit for members whose employer is insolvent and there are insufficient

assets to pay benefits

5towerswatson.com© 2011 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

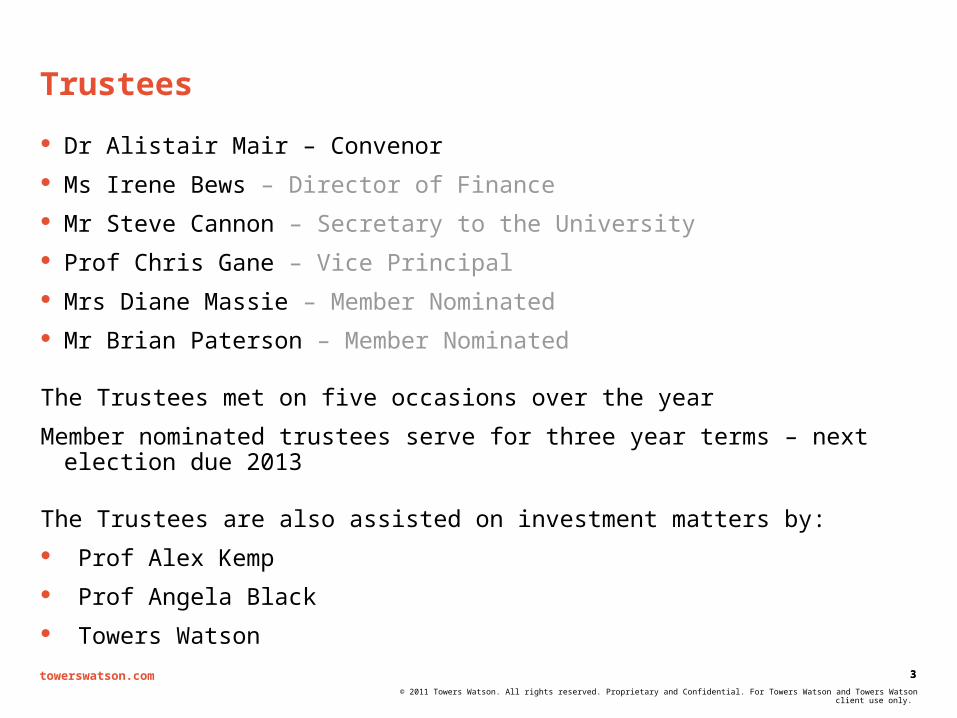

Scheme membership

Scheme membership continues to grow

742 739574 559

905 900

0

100

200

300

400

500

600

700

800

900

1000

Actives Deferred Pensioners Pensioners /Dependants

31-Jul-10 31-Jul-09

6towerswatson.com© 2011 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Cash flows over the year to 31 July 2010

Members contributions: £1.0m 7.05% of pay Includes Pensions Plus

University contributions: £2.6m 17.1% of pay plus life assurance premiums

Cash flows Pensions / other benefits: £4.2m Expenses: £0.2m

Investment return: 22.1% Fund value

31 July 2010: £81.2m 3 May 2011: £89.6m

7towerswatson.com© 2011 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Investment changes

The Trustees carried out a review of their investment arrangements in 2010

They concluded that the Scheme should be invested passively This means the Scheme aims to track the stock market

The Scheme previously invested actively This means the manager aims to out-perform the stock market

Investing passively: Reduces risk of underperforming the stock market

Reduces costs, in terms of management charges and governance time for the trustees

The Scheme’s assets were transferred to Legal & General Investment Management (LGIM) in September 2010

The Trustees will save ~£150k a year in investment charges

8towerswatson.com© 2011 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

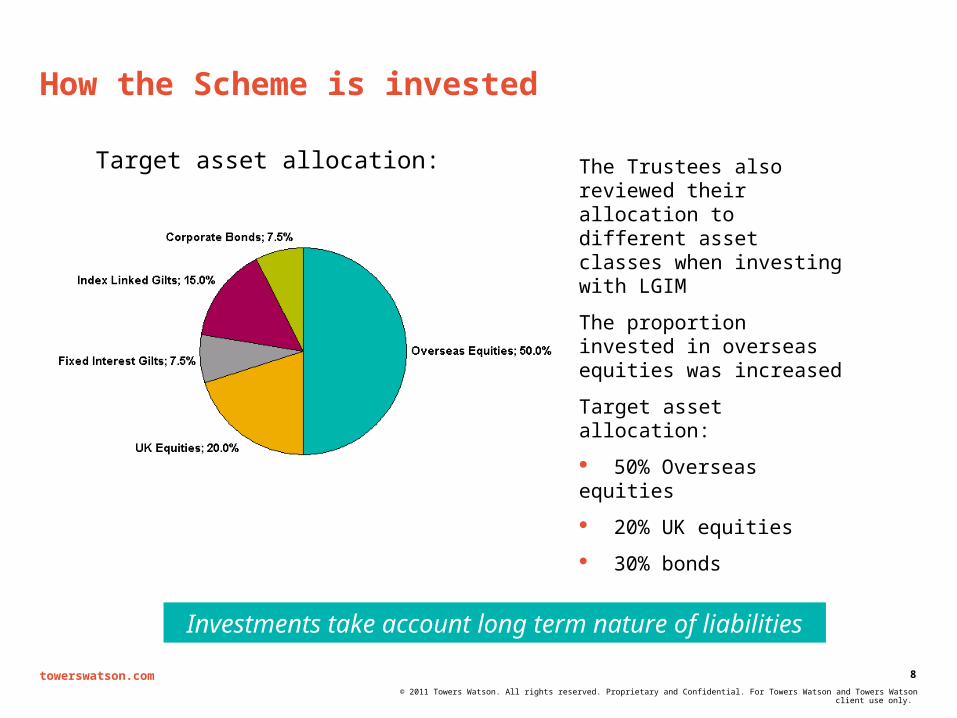

How the Scheme is invested

The Trustees also reviewed their allocation to different asset classes when investing with LGIM

The proportion invested in overseas equities was increased

Target asset allocation:

50% Overseas equities

20% UK equities

30% bonds

Investments take account long term nature of liabilities

Target asset allocation:

9towerswatson.com© 2011 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Benefits explained – RPI or CPI?

The Government has changed the rules on inflationary increases

The Trustees have looked at what the Trust Deed says

Increases to pensions after retirement Mostly based on RPI and subject to minimum of 3%

Element known as “Post 88 GMP” is now based on CPI up to 3%

Some pensioners may get a pension increase a few pounds lower in some years

After leaving but before retirement increases are based on the Government rules

Now mainly based on CPI

Benefits accrued up to 31 July 2011

10towerswatson.com© 2011 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Scheme benefit changes

11towerswatson.com© 2011 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Confirmed benefit changes

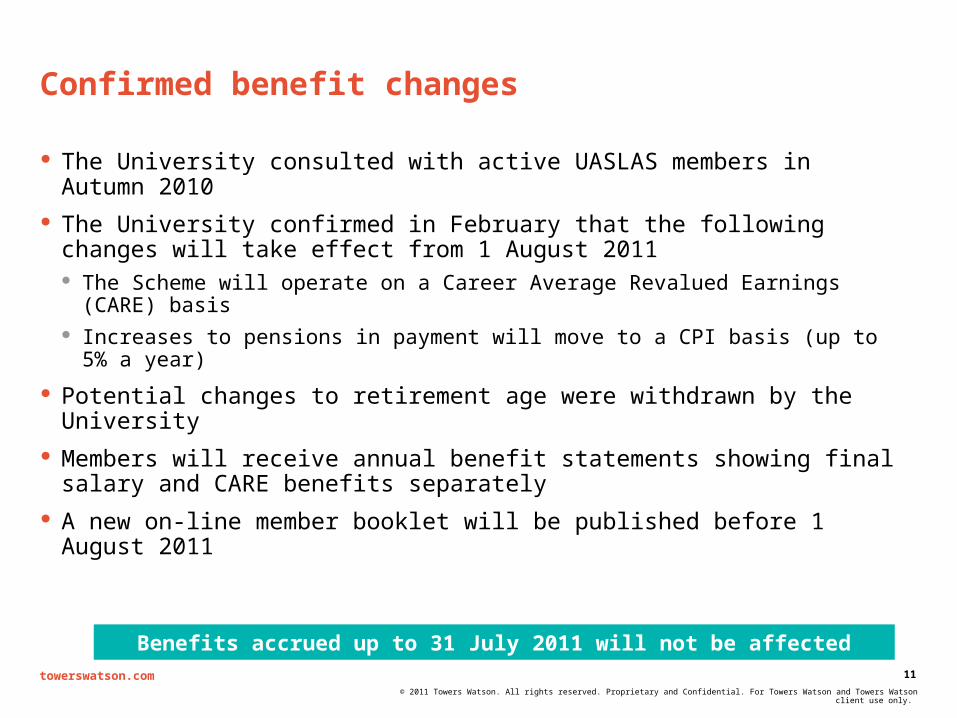

The University consulted with active UASLAS members in Autumn 2010

The University confirmed in February that the following changes will take effect from 1 August 2011 The Scheme will operate on a Career Average Revalued Earnings (CARE)

basis Increases to pensions in payment will move to a CPI basis (up to 5% a year)

Potential changes to retirement age were withdrawn by the University Members will receive annual benefit statements showing final salary

and CARE benefits separately A new on-line member booklet will be published before 1 August 2011

Benefits accrued up to 31 July 2011 will not be affected

12towerswatson.com© 2011 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

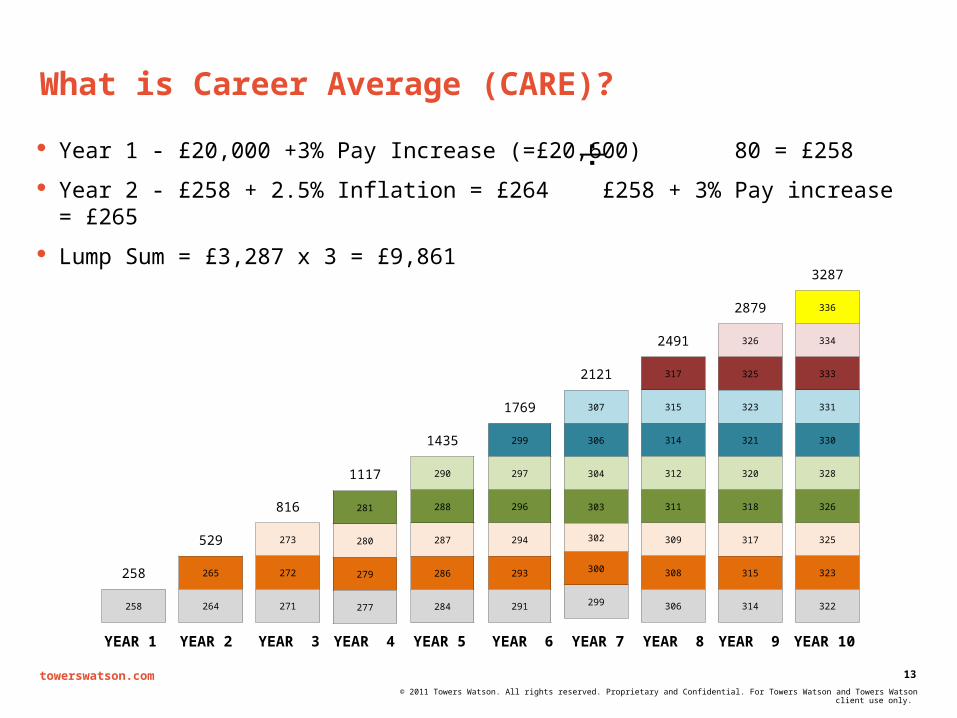

What is Career Average (CARE)?

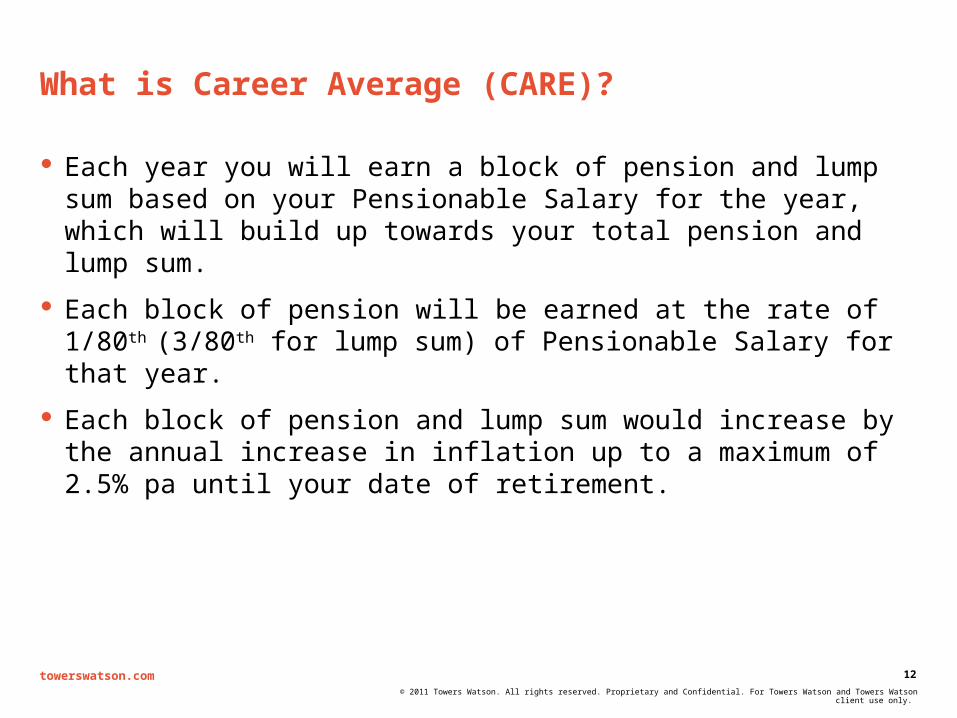

Each year you will earn a block of pension and lump sum based on your Pensionable Salary for the year, which will build up towards your total pension and lump sum.

Each block of pension will be earned at the rate of 1/80th (3/80th for lump sum) of Pensionable Salary for that year.

Each block of pension and lump sum would increase by the annual increase in inflation up to a maximum of 2.5% pa until your date of retirement.

13towerswatson.com© 2011 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

What is Career Average (CARE)?

Year 1 - £20,000 +3% Pay Increase (=£20,600) 80 = £258

Year 2 - £258 + 2.5% Inflation = £264 £258 + 3% Pay increase = £265

Lump Sum = £3,287 x 3 = £9,861

YEAR 1 YEAR 2 YEAR 3 YEAR 4 YEAR 5 YEAR 6 YEAR 7 YEAR 8 YEAR 9 YEAR 10

3287

336

334

333

331

330

328

326

325

323

322

2879

326

325

323

321

320

318

317

315

314

2491

317

315

314

312

311

309

308

306

2121

307

306

304

303

302

300

299

1769

299

297

296

294

293

291

1435

290

288

287

286

284

1117

281

280

279

277

816

273

272

271

529

265

264

258

258

14towerswatson.com© 2011 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

What about benefits built up to 31 July 2011?

These remain on a final salary basis:

1/80th Final Pensionable Salary Pensionable Serviceto 31 July 2011

X X

3/80th Final Pensionable Salary Pensionable Serviceto 31 July 2011

X X

Pension:

Lump Sum:

No change

15towerswatson.com© 2011 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Actuarial update

16towerswatson.com© 2011 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

What is the purpose of an actuarial valuation

Assets

Liabilities

Is there enough money in the Scheme to cover accrued benefits?

How much should be paid into the Scheme in future years?

17towerswatson.com© 2011 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

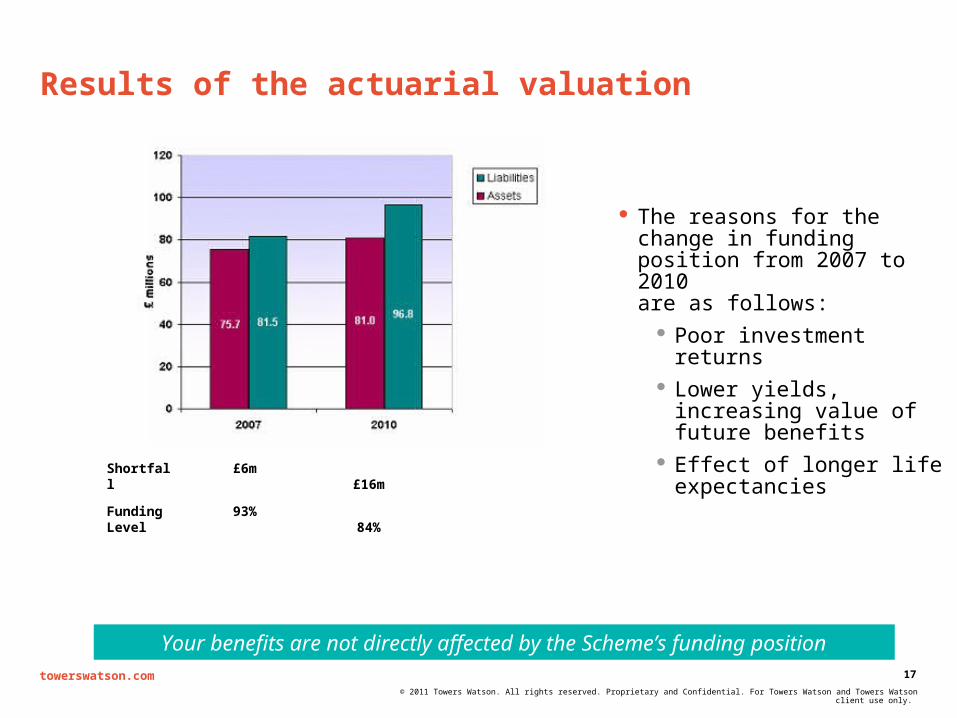

Results of the actuarial valuation

The reasons for the change in funding position from 2007 to 2010 are as follows:

Poor investment returns Lower yields, increasing

value of future benefits Effect of longer life

expectancies

Your benefits are not directly affected by the Scheme’s funding position

Shortfall £6m £16m

Funding Level

93% 84%

18towerswatson.com© 2011 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

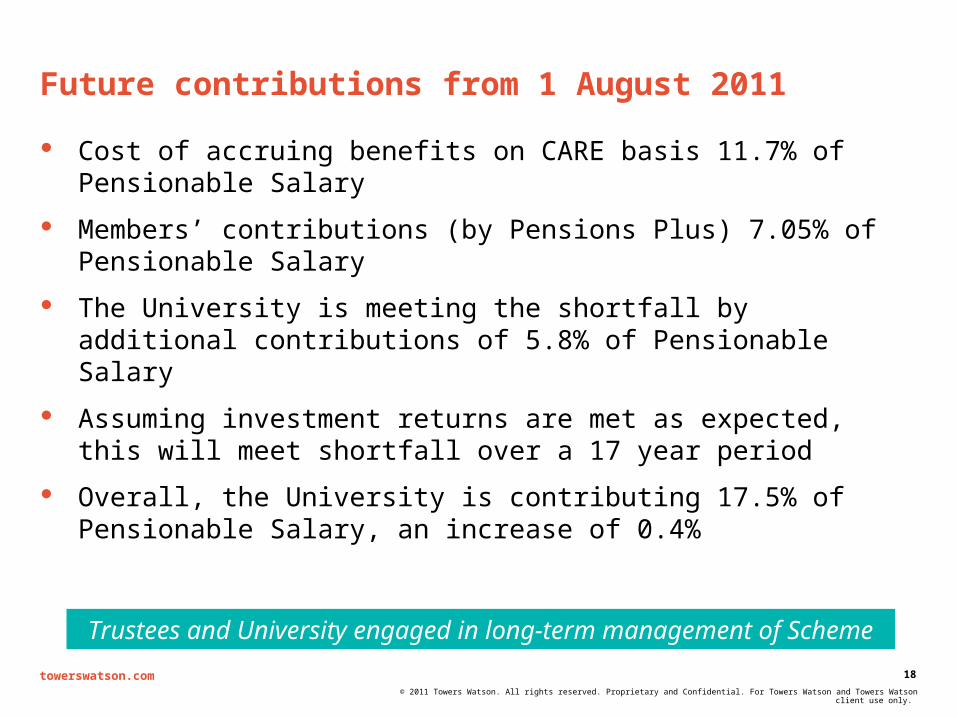

Future contributions from 1 August 2011

Cost of accruing benefits on CARE basis 11.7% of Pensionable Salary

Members’ contributions (by Pensions Plus) 7.05% of Pensionable Salary

The University is meeting the shortfall by additional contributions of 5.8% of Pensionable Salary

Assuming investment returns are met as expected, this will meet shortfall over a 17 year period

Overall, the University is contributing 17.5% of Pensionable Salary, an increase of 0.4%

Trustees and University engaged in long-term management of Scheme

19towerswatson.com© 2011 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Questions

20towerswatson.com© 2011 Towers Watson. All rights reserved. Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

20

Contact Details

David Gordon

Senior Consultant +44 131 221 7815 [email protected]

\\Wwp\data\General Data Edinburgh\D\UniAberdeen\2011\TW agm 2011 ppt.ppt