Embed Size (px)

Citation preview

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores December 2018 1

IBISWorld Industry Report OD4142Medical & Recreational Marijuana Stores in the USDecember 2018 Kelsey Oliver

Legal matter: Despite conflicting regulations, the industry will continue its sky-high growth

2 About this Industry2 Industry Definition

2 Main Activities

2 Similar Industries

2 Additional Resources

3 Industry at a Glance

4 Industry Performance4 Executive Summary

4 Key External Drivers

6 Current Performance

9 Industry Outlook

12 Industry Life Cycle

14 Products and Markets14 Supply Chain

14 Products and Services

15 Demand Determinants

16 Major Markets

17 International Trade

18 Business Locations

20 Competitive Landscape20 Market Share Concentration

20 Key Success Factors

20 Cost Structure Benchmarks

22 Basis of Competition

23 Barriers to Entry

24 Industry Globalization

25 Major Companies

26 Operating Conditions26 Capital Intensity

27 Technology and Systems

27 Revenue Volatility

28 Regulation and Policy

29 Industry Assistance

31 Key Statistics31 Industry Data

31 Annual Change

31 Key Ratios

32 Jargon & Glossary

www.ibisworld.com | 1-800-330-3772 | [email protected]

This report was provided toAutobahn Consultants (2134210691)by IBISWorld on 27 October 2019 in accordance with their license agreement with IBISWorld

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 2

This industry includes stores that retail medical marijuana (by prescription only) and recreational marijuana. However, the legal sale of recreational marijuana is

currently limited to the states of Alaska, California, Colorado, Maine, Massachusetts, Nevada, Oregon, Washington, Michigan and Vermont.

The primary activities of this industry are

Retail edible cannabis products

Retail smokable indica cannabis products

Retail smokable sativa cannabis products

31222 Cigarette & Tobacco Manufacturing in the USThis industry manufactures cigarettes and other tobacco products.

32541a Brand Name Pharmaceutical Manufacturing in the USThis industry manufactures pharmaceutical products used to treat illnesses.

32541d Vitamin & Supplement Manufacturing in the USThis industry manufactures vitamins and other health supplements.

NN001 Biotechnology in the USThis industry manufactures biotechnology products, including medical products.

Industry Definition

Main Activities

Similar Industries

Additional Resources

About this Industry

For additional information on this industry

www.mpp.org Marijuana Policy Project

www.thecannabisindustry.org National Cannabis Industry Association

www.norml.org National Organization for the Reform of Marijuana Laws

The major products and services in this industry are

Pre-rolled joints

Concentrates

Edible cannabis products

Flower products

All other products

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 3

% c

hang

e

4

-4

-2

0

2

2412 14 16 18 20 22Year

Per capita disposable income

% c

hang

e

60

0

12

24

36

48

2410 12 14 16 18 20 22Year

Revenue Employment

Revenue vs. employment growth

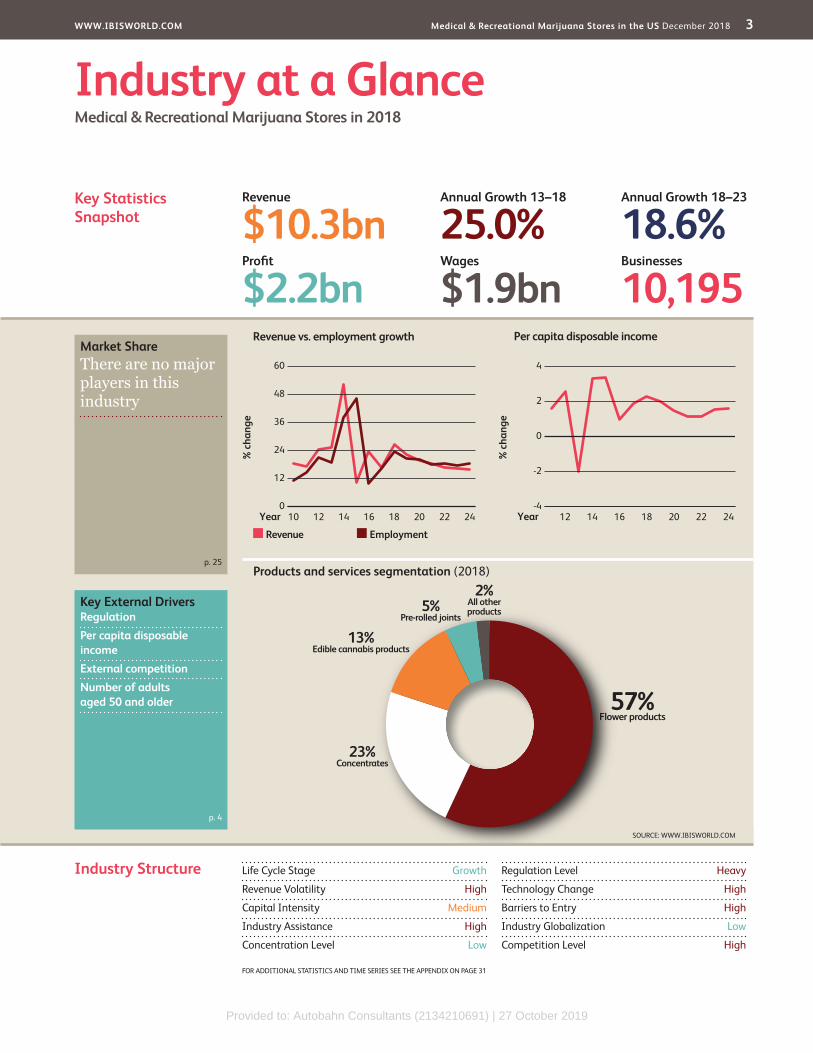

Products and services segmentation (2018)

57%Flower products

23%Concentrates

13%Edible cannabis products

5%Pre-rolled joints

2%All otherproducts

Key Statistics Snapshot

Industry at a GlanceMedical & Recreational Marijuana Stores in 2018

Industry Structure Life Cycle Stage Growth

Revenue Volatility High

Capital Intensity Medium

Industry Assistance High

Concentration Level Low

Regulation Level Heavy

Technology Change High

Barriers to Entry High

Industry Globalization Low

Competition Level High

Revenue

$10.3bnProfit

$2.2bnWages

$1.9bnBusinesses

10,195

Annual Growth 18–23

18.6%Annual Growth 13–18

25.0%

Key External DriversRegulationPer capita disposable incomeExternal competitionNumber of adults aged 50 and older

Market ShareThere are no major players in this industry

p. 25

p. 4

FOR ADDITIONAL STATISTICS AND TIME SERIES SEE THE APPENDIX ON PAGE 31

SOURCE: WWW.IBISWORLD.COM

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 4

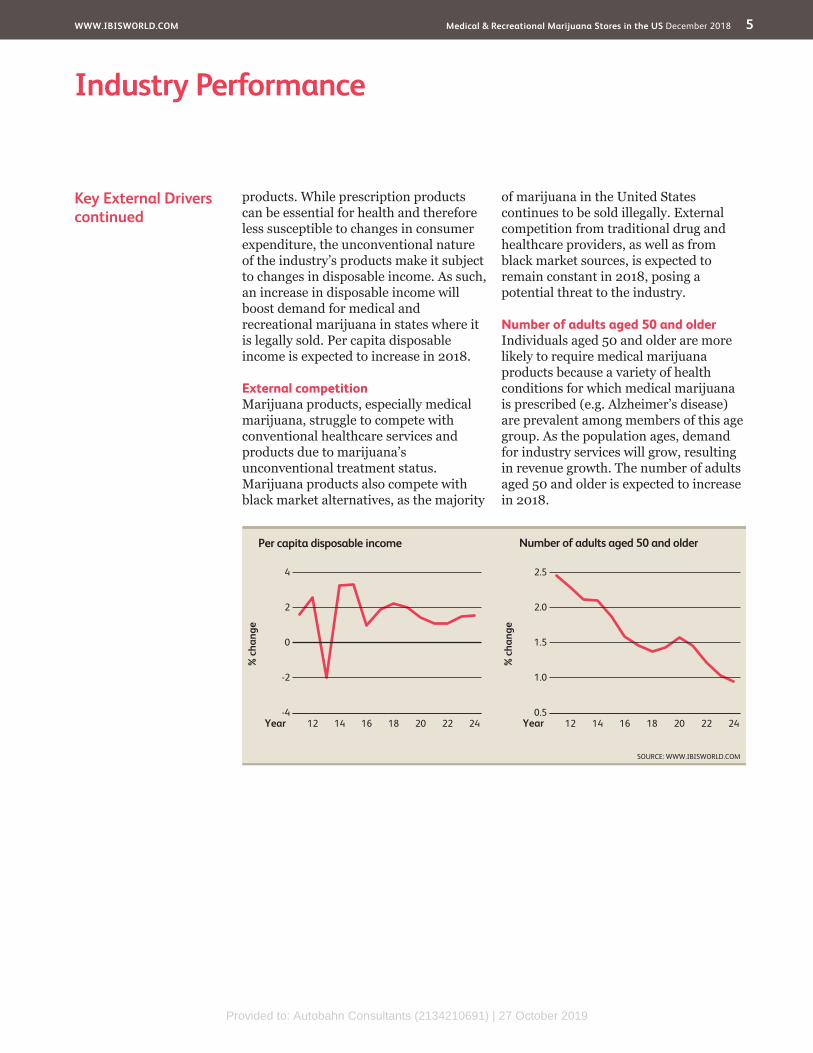

Key External Drivers RegulationMedical and recreational marijuana has been restricted in the past by attempts to impose additional regulations on the industry. In particular, medical marijuana remains a Schedule I controlled substance under federal law, despite legalization by many states. Although the level of federal regulation is expected to remain unchanged in 2018, the industry has

benefited in recent years from favorable regulation at the state level. With legalization expanding across several states following the 2016 and 2018 elections, beneficial regulation is expected to create an opportunity for the industry.

Per capita disposable incomeHousehold income levels determine consumers’ ability to purchase marijuana

Executive Summary The Medical and Recreational Marijuana Stores industry, which includes stores that retail medical marijuana (by prescription only) and recreational marijuana, expanded dramatically over the five years to 2018. The 2016 election cycle, in particular, provided landslide victories for both medical and recreational cannabis retailers. Consequently, the legalization of marijuana for medical and/or recreational purposes and the growing acceptance of medical marijuana provided operators and investors with

unprecedented opportunities. There has been no shortage of demand in recent years, and the cannabis industry has become one of the fastest-growing in the United States.

More recently, the legalization of recreational marijuana sales in several states fueled revenue growth. The licensing of commercial recreational marijuana retailers contributed to industry revenue growth of 23.7% in 2016, as new entrants flooded the recently legalized market. Meanwhile, medical marijuana dispensaries continued to benefit from the steadily

aging population and growing acceptance of the medical applications of marijuana. Chronic illnesses have become more prevalent as the US population continues to age, driving demand for medical marijuana products. Additionally, the development of edible cannabis products helped attract consumers that were unfamiliar with marijuana products or averse to smoking. Edible products and vaporizer pens are projected to be a growth segment for the industry in the coming years, as they are convenient alternatives to traditional cannabis consumption. Overall, the industry is expected to experience an annualized 25.0% increase to $10.3 billion over the five years to 2018, including growth of 26.5% in 2018 alone.

Over the five years to 2023, industry revenue is projected to increase at an annualized rate of 18.6% to $24.1 billion. The industry will remain at risk, however, until the federal government definitively changes its position on the legality of marijuana. Until then, an uptick in the number of medical marijuana patients and a growing recreational cannabis legalization movement will likely reap long-term benefits for the industry. Rising demand is also forecast to widen profit margins, as is the success of for-profit recreational marijuana businesses in states with large consumer markets such as California, Colorado and Washington.

Industry PerformanceExecutive Summary | Key External Drivers | Current Performance Industry Outlook | Life Cycle Stage

The licensing of commercial recreational marijuana retailers contributed to industry revenue growth

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 5

Industry Performance

Key External Driverscontinued

products. While prescription products can be essential for health and therefore less susceptible to changes in consumer expenditure, the unconventional nature of the industry’s products make it subject to changes in disposable income. As such, an increase in disposable income will boost demand for medical and recreational marijuana in states where it is legally sold. Per capita disposable income is expected to increase in 2018.

External competitionMarijuana products, especially medical marijuana, struggle to compete with conventional healthcare services and products due to marijuana’s unconventional treatment status. Marijuana products also compete with black market alternatives, as the majority

of marijuana in the United States continues to be sold illegally. External competition from traditional drug and healthcare providers, as well as from black market sources, is expected to remain constant in 2018, posing a potential threat to the industry.

Number of adults aged 50 and olderIndividuals aged 50 and older are more likely to require medical marijuana products because a variety of health conditions for which medical marijuana is prescribed (e.g. Alzheimer’s disease) are prevalent among members of this age group. As the population ages, demand for industry services will grow, resulting in revenue growth. The number of adults aged 50 and older is expected to increase in 2018.

% c

hang

e

2.5

0.5

1.0

1.5

2.0

2412 14 16 18 20 22Year

Number of adults aged 50 and older

SOURCE: WWW.IBISWORLD.COM

% c

hang

e

4

-4

-2

0

2

2412 14 16 18 20 22Year

Per capita disposable income

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 6

Industry Performance

Current Performance

The Medical and Recreational Marijuana Stores industry has flourished over the five years to 2018, bolstered by increasing consumer acceptance of alternative treatment via marijuana products, as well as sweeping legislative victories across the United States legalizing marijuana in some form. The industry includes stores that retail medical marijuana (by prescription only) and recreational marijuana, although the legal sale of recreational marijuana is currently limited to 10 states. In states that have legalized recreational marijuana, medical marijuana sales have fallen year over year as adult-use recreational purchases outpace medical sales, suggesting that the recreational market is disruptive once legalized.

A growing body of research suggests the expansive medical applications of marijuana. Since 1996, proponents of cannabis have pushed individual states to recognize marijuana as a legitimate treatment or pain reliever for a range of illnesses, including the plant’s non-psychoactive component, CBD, which has proved to be effective in preventing grand mal seizures. New medical research and changing public opinion have advanced these efforts and have contributed to the

prolific growth of medical applications of industry products over the past five years. More recently, the legalization of recreational marijuana spurred the industry’s astronomical growth. Watershed legalization victories in recent years, most notably during the 2016 election cycle, expanded the retail sale of recreational products to 10 US states. Consequently, industry revenue is forecast to grow an annualized 25.0% to $10.3 billion over the five years to 2018, including anticipated growth of 26.5% in 2018.

% c

hang

e

60

0

12

24

36

48

2410 12 14 16 18 20 22Year

Industry revenue

SOURCE: WWW.IBISWORLD.COM

Medical marijuana at the forefront

Medical marijuana has led the industry’s growth for much of the last decade. According to the US Government Accountability Office, under state medical marijuana laws, symptoms and conditions that may be treated by cannabis include Alzheimer’s disease, anorexia, HIV/AIDS, glaucoma, cancer, arthritis, epilepsy, nausea, pain, cachexia, Crohn’s disease, migraines, multiple sclerosis and spasticity. Although for many decades all domestic marijuana transactions were conducted under implicit or explicit prohibition, many states have recently moved to legalize marijuana for medical purposes.

Demographic factors have played a significant role in driving demand for medical marijuana. Currently, the median age of medical marijuana patients is 41.5 years, and BDS Analytics estimates that nearly 1.9 million Americans are regular users of medical marijuana.

Following the 2018 midterm elections, 33 states have legalized medical marijuana. In general, the use of medical marijuana is increasing, particularly among people with chronic illnesses and pain. At the same time, significant concerns persist regarding the legitimacy and efficiency of medical marijuana treatment. Organizations such as the

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 7

Industry Performance

National Cannabis Industry Association have worked toward increasing the legitimacy of medical marijuana use through the establishment of industry standards. These efforts have helped spur demand.

Proponents of medical marijuana have pushed individual states to recognize marijuana as a treatment for a range of diseases. Medical marijuana laws have been adopted by public referendum, as well as by legislation. In late 2009, the US Justice Department instructed federal prosecutors in states with medical marijuana laws not to prioritize

prosecuting individuals and businesses complying with state laws. In 2014, President Obama signed into law historic provisions for medical marijuana, prohibiting the Department of Justice from using federal funding to limit states from implementing their own laws that authorize the use, distribution, possession, or cultivation of medical marijuana. In addition, in August 2016, the federal government loosened the regulations concerning studying the medical applications of cannabinoids. These efforts, in turn, have aided operators and facilitated industry growth.

Medical marijuana at the forefront continued

Recreational marijuana facilitates boom

The legal sale of recreational marijuana provided operators with unprecedented opportunities for expansion, and has even disrupted medical marijuana markets in states such as Colorado. Recreational marijuana users typically smoke to obtain a high which affects the part of the brain that influences pleasure, memory, sensory and time perception, concentration and coordination. At the outset of 2014, legal recreational marijuana use became a reality in Colorado, stimulating demand for industry products as hundreds of retail stores opened throughout the year. While Washington lagged in its implementation

of the voter-approved law legalizing recreational cannabis consumption, recreational marijuana sales began in July 2014. Since then, the number of states that have legalized recreational cannabis has risen to 10. California, Colorado and Washington account for 27.0%, 20.0% and 11.0% of the legal market, respectively, according to BDS Analytics. To meet consumer demand for marijuana, some states issued licenses for the cultivation of recreational marijuana. This development contributed to the industry’s boom in 2014, when revenue rose an astounding 52.0%, according to IBISWorld estimates.

Changing attitudes and rising incomes spur new products

The development of edible cannabis products (edibles) has also spurred greater consumer acceptance of medical and recreational marijuana. Edibles can take the form of food, extracts and oils, ranging from marijuana-infused mints and candies to baked goods and beverages, among many other products. Edibles provide a more-convenient and familiar product to consumers, thereby stimulating consumer demand for marijuana products.

The nature of medical marijuana treatment is rather unconventional. Although expenditure on products essential for health is less susceptible to fluctuations in consumer spending, medical marijuana’s unique nature

Marijuana’s unique nature makes it subject to changes in disposable income

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 8

Industry Performance

Regulation weighs on the industry

Regulation from all levels of government presents the greatest challenge to medical and recreational marijuana dispensaries, especially because state and federal governments often have conflicting regulations. The Controlled Substances Act (CSA), passed as a part of the Comprehensive Drug Abuse Prevention and Control Act of 1970, classifies marijuana as a Schedule I controlled substance. Schedule I substances are deemed by the federal government to have a high potential for abuse; furthermore, prescriptions of them are illegal. Despite the adoption of some state laws during the past two decades permitting the consumption and distribution of marijuana for medical and recreational use, the possession and distribution of marijuana remains illegal under federal law. Consequently, many businesses operate with the risk of being shut down or experiencing a property seizure without notice. In addition, industry operators cannot make standard tax

deductions for business expenses and have difficulty securing standard banking and financial services.

The continued success observed in states that have legalized recreational cannabis provides incentive for other states to legalize for-profit marijuana. In 2016, taxes from the retail sale of marijuana totaled more than $500.0 million in Colorado, Washington and Oregon alone, according to BDS Analytics. Therefore, continued success in these states may provide an incentive for other states to legalize for-profit marijuana distribution. The legalization of for-profit recreational marijuana across numerous states has already had a positive effect on industry profit margins, which are projected to rise to 21.4% of revenue in 2018.

makes it subject to changes in disposable income. The same is largely true for recreational marijuana. Since consumers pay for recreational marijuana out of pocket, growth in per capita disposable income boosts demand for industry products. Per capita disposable income is expected to grow an annualized 2.3% over the five years to 2018, thanks to favorable macroeconomic conditions and

declining unemployment. Greater consumer acceptance of the industry’s products and strong demand growth has caused more companies to enter this industry. Over the five years to 2018, the number of industry enterprises is anticipated to increase an annualized 23.4% to 10,195 while employment is also expected to have increased an annualized 25.9% to 116,498 workers.

Changing attitudes and rising incomes spur new products continued

Regulation from all levels of government presents the greatest challenge

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 9

Industry Performance

Recreational marijuana fuels industry expansion

The Medical and Recreational Marijuana Stores industry is subject to heavy regulation from all levels of government, with state and federal governments at times having conflicting policies. The Department of Justice, through the Drug Enforcement Administration, raids and prosecutes marijuana dispensaries and growers in the United States. However, in 2014, President Obama signed into law historic provisions for medical marijuana, prohibiting the Department of Justice from using federal funding to limit states from implementing their own laws that authorize the use, distribution, possession or cultivation of medical marijuana. Although the industry largely flourished under the Obama administration, its future remains hazy under the current administration.

Nevertheless, the liberalization of regulation regarding the sale of recreational marijuana is expected to fuel the industry’s growth. In 2014 and 2015, operators in Colorado and Washington generated estimated revenue of $350.0

million and $1.0 billion, respectively, from the legal sale of recreational marijuana. In addition to strong growth in recreational marijuana sales in Colorado and Washington, the industry is expected to benefit from the commencement of recreational marijuana sales in a rising number of states. Similar to the previous five years, rising demand will cause more companies to enter the industry. Over the five years to 2023, the number of enterprises is projected to grow at an annualized rate of 17.9% to 23,265, while industry employment is forecast to increase at an annualized rate of 18.8% to 275,169 workers.

The overwhelming successes of states such as Colorado, Washington and

Industry Outlook

The outlook for the Medical and Recreational Marijuana Stores industry is largely positive, with the industry expected to achieve new highs over the five years to 2023. Although the industry will continue to benefit from increasingly favorable attitudes toward medical marijuana treatments, building on the trends of the past five years, the industry will be steered by the growth of legal recreational marijuana sales, which have already disrupted medical sales in legalized states. Sales are expected to continue to explode in the states that legalized recreational marijuana. This includes the industry’s largest market, California, which leads the country in cannabis expenditure. As a result, IBISWorld forecasts that revenue will skyrocket at an annualized

rate of 18.6% to $24.1 billion over the five years to 2023.

In particular, an increase in per capita disposable income is projected to drive demand for industry products. Although medicinal products are essential for health and therefore less susceptible to fluctuations in consumer expenditure, the unconventional nature of the industry’s products still make them subject to changes in disposable income. Nevertheless, because consumers pay for industry products out-of-pocket, growth in disposable income will help boost demand. Additionally, medical and recreational marijuana stores will likely further expand their offerings of edible marijuana products, which will likely be a major growth segment for industry operators moving forward.

The industry will be steered by the growth of legal recreational marijuana sales

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 10

Industry Performance

Recreational marijuana fuels industry expansioncontinued

Medical cannabis demand grows with aging population

A growing number of doctors and patients will turn to the unconventional treatment offered by medical marijuana for conditions such as arthritis, migraines and Alzheimer’s disease. In particular, the rising number of US adults aged 50 and older is expected to bolster demand for medical marijuana products. Over the five years to 2023, IBISWorld anticipates that this demographic will grow at an annualized rate of 1.3% to 123.9 million. By comparison, the total US population is forecast to grow at an annualized rate of 0.7% during the same period. This trend will lead to a growing number of people with health conditions that can be treated with marijuana (e.g. cancer and glaucoma), which increase in incidence with age. Additionally, given that the median age of medical marijuana patients is currently 41.5, demand will likely increase as patients in their 40s enter their 50s.

Moreover, the number of physician visits in the United States is expected to

rise in line with the senior population. Chronic health ailments such as obesity and diabetes will likely support healthcare use, as these patients will increasingly require checkups. The rising prevalence of these chronic diseases is also expected to boost demand for medical marijuana. Although doctors cannot legally prescribe marijuana to patients because it remains a Schedule I substance, they can authorize a patient to visit a company or a cooperative that provides medical marijuana. Therefore, while medical marijuana treatment is not covered by insurance, as the number of physician visits increases, demand for medical marijuana is anticipated to grow accordingly.

Oregon will potentially spur more states to legalize recreational marijuana. From 2014 to 2016, combined retail sales tax in legal cannabis markets in Colorado, Oregon and Washington alone totaled over $771.0 million for recreation, according to BDS Analytics. As a result, many more states are expected to follow suit, legalizing recreational cannabis to generate tax revenue. Thanks to the legislative victories of the 2016 and 2018 midterm elections, as well as Vermont’s 2017 special election, medical marijuana is now legal in 33 states, while 10 states

have also legalized recreational marijuana (Alaska, California, Colorado, Maine, Massachusetts, Michigan, Nevada, Oregon, Vermont and Washington). In the 2018 election cycle, four states had marijuana measures on the ballot. These regulatory changes are expected to increase demand for recreational products, benefiting industry operators. With sales of recreational marijuana expected to comprise a larger share of industry revenue over the five years to 2023, industry-wide profitability is projected to remain high.

The rising prevalence of chronic illness will bolster demand for medical marijuana

Conventional healthcare threatens the industry

Growing acceptance of medical and recreational marijuana will produce numerous business opportunities over the coming years. Development of

value-added, high-quality marijuana products will also drive industry growth. At the same time, medical marijuana dispensaries endure significant risks and

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 11

Industry Performance

hurdles. Over the next five years, conventional healthcare providers will continue challenging alternative care presented by medical marijuana products. Despite growing acceptance of marijuana-based treatment, traditional healthcare providers will continue to

pose a threat to the industry due to the substantial skepticism regarding the legitimacy and effectiveness of marijuana-based medications. Consequently, medical marijuana growers will likely continue to suffer from inadequate capital investments.

Conventional healthcare threatens the industry continued

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 12

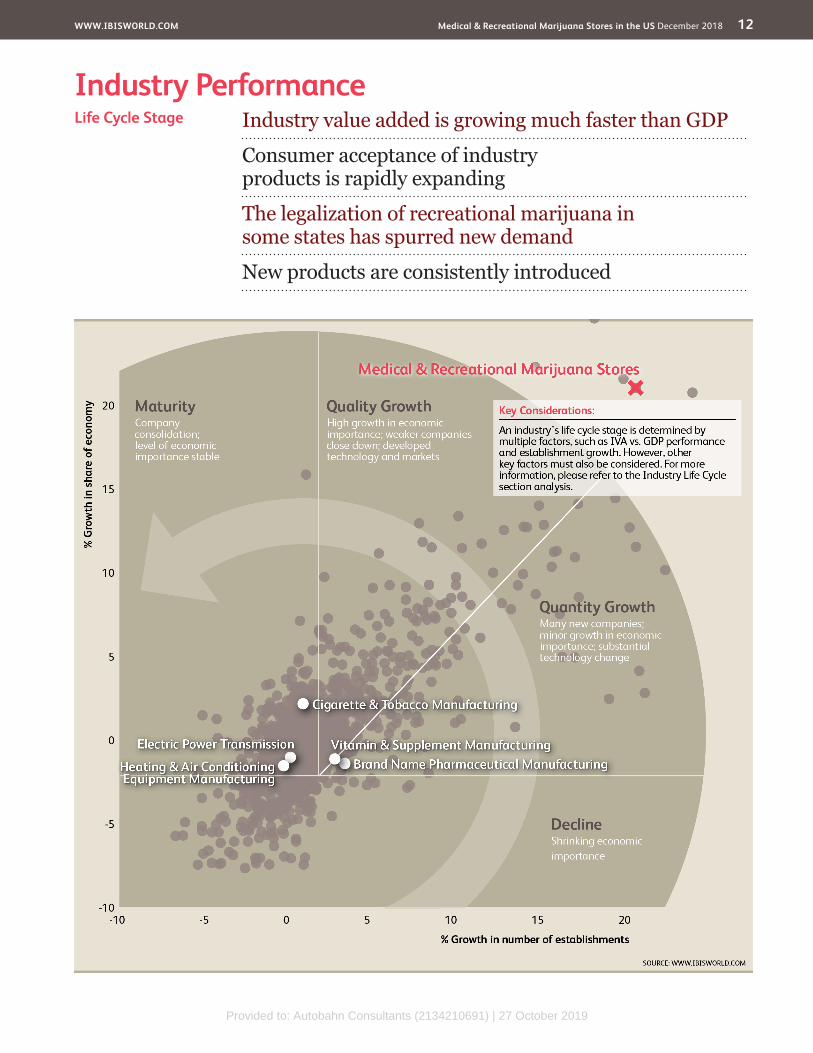

Industry PerformanceIndustry value added is growing much faster than GDP

Consumer acceptance of industry products is rapidly expanding

The legalization of recreational marijuana in some states has spurred new demand

New products are consistently introduced

Life Cycle Stage

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 13

Industry Performance

Industry Life Cycle The Medical and Recreational Marijuana Stores industry is in the growth stage of its life cycle. Over the 10 years to 2023, its industry value-added, which measures the industry’s contribution to the economy, is expected to grow at an annualized rate of 23.9%. This rate is markedly faster than the 2.2% projected growth for US GDP, indicating the industry will make up a larger share of the economy in the years ahead. The industry is growing due to widening acceptance of its safety and legitimacy, which is causing more people to use its products. Although an increasing percentage of Americans have been using medical marijuana products to alleviate pain and to treat other health conditions over the past five years, a large share of the population still does not use them. This factor suggests that there is

significant room for industry growth in the years ahead.

Organizations such as the National Cannabis Industry Association have worked toward increasing the legitimacy of medical marijuana use by creating industry standards, helping spur demand. The aging US population will also promote demand for products offered by this industry. Moreover, the industry’s growth has been spurred by the growing legalization of recreational marijuana sales. Beginning in 2014, recreational marijuana stores began opening in Colorado and Washington, making them the fastest-growing markets in the United States. Currently, 33 states permit medical marijuana in some form. Moreover, the legalization of recreational marijuana in nine states is expected to provide growth opportunities.

This industry is Growing

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 14

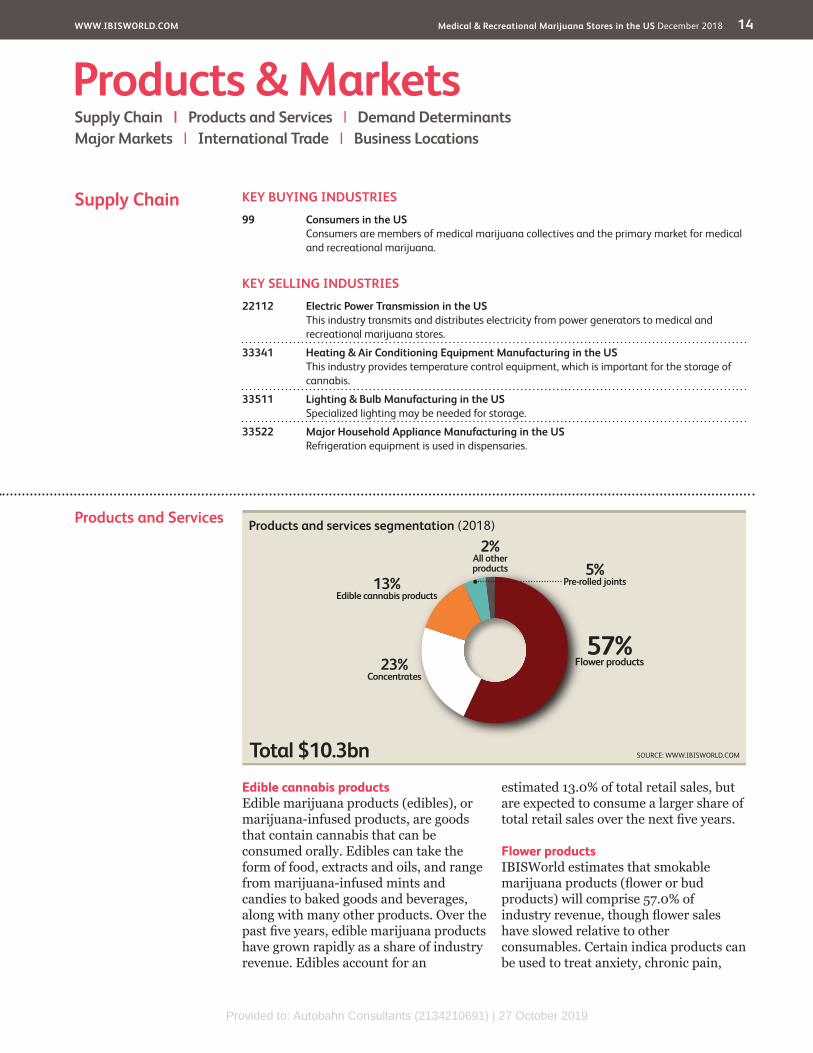

Products and Services

Edible cannabis productsEdible marijuana products (edibles), or marijuana-infused products, are goods that contain cannabis that can be consumed orally. Edibles can take the form of food, extracts and oils, and range from marijuana-infused mints and candies to baked goods and beverages, along with many other products. Over the past five years, edible marijuana products have grown rapidly as a share of industry revenue. Edibles account for an

estimated 13.0% of total retail sales, but are expected to consume a larger share of total retail sales over the next five years.

Flower productsIBISWorld estimates that smokable marijuana products (flower or bud products) will comprise 57.0% of industry revenue, though flower sales have slowed relative to other consumables. Certain indica products can be used to treat anxiety, chronic pain,

Products & MarketsSupply Chain | Products and Services | Demand Determinants Major Markets | International Trade | Business Locations

KEY BUYING INDUSTRIES

99 Consumers in the US Consumers are members of medical marijuana collectives and the primary market for medical and recreational marijuana.

KEY SELLING INDUSTRIES

22112 Electric Power Transmission in the US This industry transmits and distributes electricity from power generators to medical and recreational marijuana stores.

33341 Heating & Air Conditioning Equipment Manufacturing in the US This industry provides temperature control equipment, which is important for the storage of cannabis.

33511 Lighting & Bulb Manufacturing in the US Specialized lighting may be needed for storage.

33522 Major Household Appliance Manufacturing in the US Refrigeration equipment is used in dispensaries.

Supply Chain

Products and services segmentation (2018)

Total $10.3bn

57%Flower products23%

Concentrates

13%Edible cannabis products

5%Pre-rolled joints

2%All otherproducts

SOURCE: WWW.IBISWORLD.COM

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 15

Products & Markets

Demand Determinants

Government regulationDemand for industry products is primarily determined by government regulation. The federal government regulates cannabis as a Schedule I controlled substance and considers all marijuana cultivation, sale and consumption illegal. In states that lack laws legalizing the medical or recreational use of cannabis, marijuana use is explicitly prohibited.

However, a total of 33 states have some level of legalization of medical marijuana. Following legislative victories between 2016 and 2018, a total of 10 states have legalized recreational and medical marijuana (Alaska, California, Colorado, Maine, Massachusetts, Michigan, Nevada, Oregon, Vermont and Washington). These regulatory changes are expected to increase demand for recreational products, benefiting industry operators.

Nonetheless, federal policy continues to limit consumer demand in states where medical marijuana is legal because of pervasive fears of violating federal law.

President Obama’s December 2014 signing of an omnibus spending bill included a directive preventing the Department of Justice from using federal funding to impede states from implementing their own laws authorizing the use, distribution, possession, or cultivation of medical marijuana. The next five years are likely to contain the legalization of medical and recreational marijuana in a score of other states.

Income and demographicsHousehold income is a primary determinant of consumers’ ability to acquire cannabis products. The legalization of medical marijuana, as well as recreational marijuana in some states, has created a market for high-quality cannabis, which can be expensive. Furthermore, because medical marijuana is typically not covered under health insurance plans, demand is largely dependent on patients’ income levels.

Population demographics, particularly age, also dictate demand trends for

Products and Servicescontinued

insomnia and muscle spasms. In general, indica provides more physical relaxation than the sativa strain, and many consumers use indica as a sleep aid. Common indica strains include White Berry, Blueberry and Northern Lights. Sativa cannabis products are used as a stimulant to improve appetite, relieve depression, migraines pain and nausea. Sativa is also more popular for patients during the day or at parties because it can increase alertness. Popular strains include Haze and Trainwreck.

ConcentratesCannabis concentrates includes any product created by an extraction process. Concentrates include: kief, a dry sift or pollen of the cannabis flower; hash, a concentrate made from

compressing cannabis plant resin; butane hash oil (BHO), or a potent concentrate consumed for dabbing and other vaporization methods; CO2 oil, used in portable vaporizer pens; Rick Simpson Oil (RSO) or Phoenix Tears, which is orally administered or applied directly to the skin; and tinctures, a liquid form of concentrate. Concentrates represent a rapidly growing product segment, and is estimated to account for 23.0% of revenue.

Pre-rolled cigarettesIn 2018, pre-rolled marijuana cigarettes (“joints”) accounted for 5.0% of revenue. Pre-rolled joints are especially popular with new marijuana smokers and are expected to increase as a share of revenue over the coming years.

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 16

Products & Markets

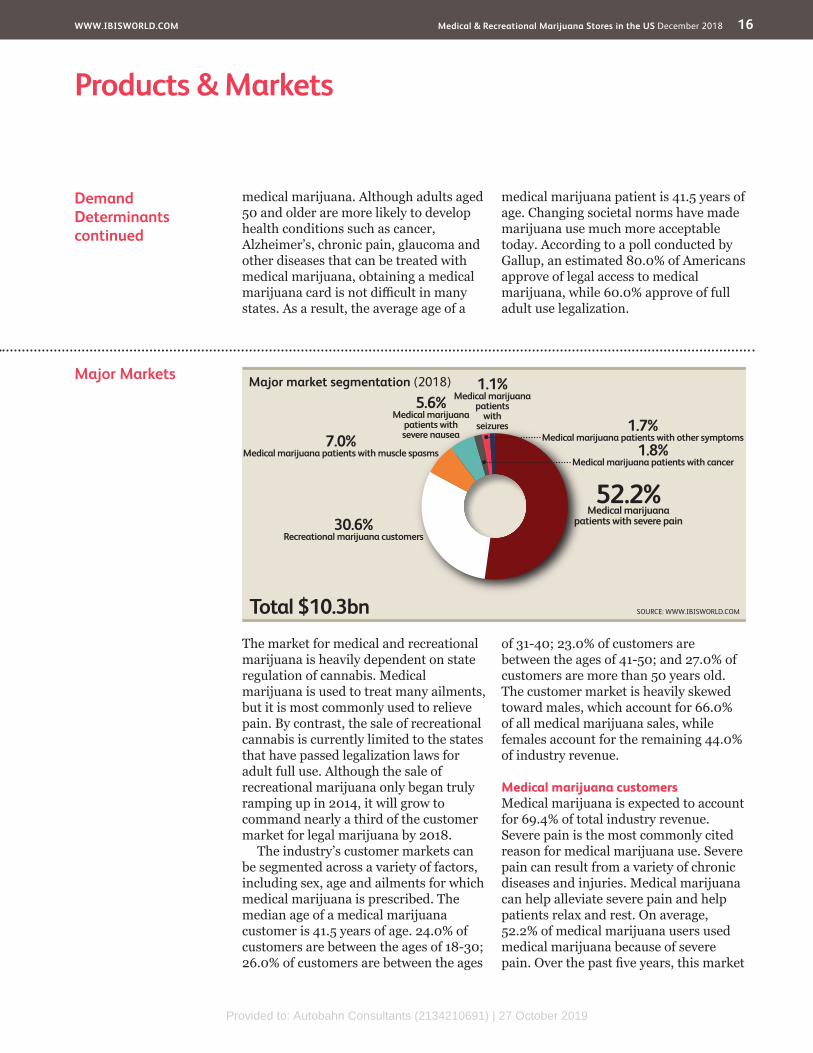

Major Markets

The market for medical and recreational marijuana is heavily dependent on state regulation of cannabis. Medical marijuana is used to treat many ailments, but it is most commonly used to relieve pain. By contrast, the sale of recreational cannabis is currently limited to the states that have passed legalization laws for adult full use. Although the sale of recreational marijuana only began truly ramping up in 2014, it will grow to command nearly a third of the customer market for legal marijuana by 2018.

The industry’s customer markets can be segmented across a variety of factors, including sex, age and ailments for which medical marijuana is prescribed. The median age of a medical marijuana customer is 41.5 years of age. 24.0% of customers are between the ages of 18-30; 26.0% of customers are between the ages

of 31-40; 23.0% of customers are between the ages of 41-50; and 27.0% of customers are more than 50 years old. The customer market is heavily skewed toward males, which account for 66.0% of all medical marijuana sales, while females account for the remaining 44.0% of industry revenue.

Medical marijuana customersMedical marijuana is expected to account for 69.4% of total industry revenue. Severe pain is the most commonly cited reason for medical marijuana use. Severe pain can result from a variety of chronic diseases and injuries. Medical marijuana can help alleviate severe pain and help patients relax and rest. On average, 52.2% of medical marijuana users used medical marijuana because of severe pain. Over the past five years, this market

Demand Determinantscontinued

medical marijuana. Although adults aged 50 and older are more likely to develop health conditions such as cancer, Alzheimer’s, chronic pain, glaucoma and other diseases that can be treated with medical marijuana, obtaining a medical marijuana card is not difficult in many states. As a result, the average age of a

medical marijuana patient is 41.5 years of age. Changing societal norms have made marijuana use much more acceptable today. According to a poll conducted by Gallup, an estimated 80.0% of Americans approve of legal access to medical marijuana, while 60.0% approve of full adult use legalization.

Major market segmentation (2018)

Total $10.3bn

52.2%Medical marijuana

patients with severe pain

1.7%Medical marijuana patients with other symptoms

30.6%Recreational marijuana customers

1.1%Medical marijuana

patientswith

seizures

7.0%Medical marijuana patients with muscle spasms

5.6%Medical marijuana

patients withsevere nausea

1.8%Medical marijuana patients with cancer

SOURCE: WWW.IBISWORLD.COM

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 17

Products & Markets

International Trade Medical and Recreational Marijuana Stores industry does not participate in international trade. Medical marijuana, as well as recreational marijuana in the case of Colorado and Washington, cannot be imported or exported because it is a controlled substance at the federal level.

Cannabis is only legal and regulated by participating states and cannot be transported across state lines at a wholesale level. Some states, however, such as Arizona, permit patients from other states to bring medical marijuana across state lines.

Major Marketscontinued

has remained relatively stable, as many health problems can cause severe pain.

Muscle spasms can be caused by multiple sclerosis, Lou Gehrig’s disease, cerebral palsy, quadriplegia, cranial and spinal nerve injuries and Tourette’s syndrome, among others. Since medical marijuana is purported to help patients relax and sleep better, it is estimated that 7.0% of industry customers used medical marijuana because of muscle spasms. The wide variety of diseases that cause muscle spasms has kept demand stable from this market over the past five years.

A variety of diseases can cause nausea and migraines, including digestive disorders. Medical marijuana can provide relief and muscle relaxation, which helps alleviate nausea. IBISWorld estimates that 5.6% of industry customers used medical marijuana because of severe nausea. This market has not significantly changed over the past five years. All other conditions account for a combined 1.7% of revenue.

Medical marijuana is used to help provide pain relief in a variety of more specific diseases and conditions, such as patients suffering from cancer and seizures. Cancer treatment can be painful, and medical marijuana can help patients relax and rest to accelerate the recovery process. Over the past five years,

demand from other patients has remained stable, as the incidence of these diseases has not significantly changed.

Recreational marijuana customersRecreational marijuana accounts for 30.6% of total industry revenue in terms of marijuana sales. Recreational marijuana users typically smoke in hand-rolled joints or in pipes or water pipes (“bongs”). They also smoke marijuana in “blunts”, which are cigars that have been emptied of tobacco and refilled with a mixture of marijuana and tobacco. Recreational marijuana users typically smoke to obtain a high, which affects the part of the brain that influences pleasure, memory, thinking, concentration, sensory and time perception and coordinated movement. Currently, legal recreational marijuana use is limited to the states of Alaska, California, Colorado, Maine, Massachusetts, Oregon, Vermont and Washington. However, recreational users’ share of the market is set to expand rapidly over the next five years as additional states permit the purchase of cannabis for recreational use and pass legislation authorizing its sale. Moreover, the expansion of recreational marijuana to the industry’s largest market, California, will likely increase this segment of revenue.

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 18

Products & Markets

Business Locations 2018

MO0.0

West

West

West

Rocky Mountains Plains

Southwest

Southeast

New England

VT0.1

MA2.8

RI0.0

NJ0.1

DE0.0

NH0.0

CT0.1

MD0.1

DC0.1

1

5

3

7

2

6

4

8 9

Additional States (as marked on map)

AZ0.0

CA42.1

NV1.1

OR0.8

WA12.5

MT0.3

NE0.0

MN0.1

IA0.0

OH0.0 VA

0.0

FL0.3

KS0.0

CO35.3

UT0.0

ID0.0

TX0.0

OK0.0

NC0.0

AK1.2

WY0.0

TN0.0

KY0.0

GA0.0

IL0.7

ME0.1

ND0.0

WI0.0 MI

1.3 PA0.0

WV0.0

SD0.0

NM0.1

AR0.0

MS0.0

AL0.1

SC0.0

LA0.0

HI0.1

IN0.0

NY0.2 5

67

8

321

4

9

SOURCE: WWW.IBISWORLD.COM

Mid- Atlantic

Establishments (%)

Less than 3% 3% to less than 10% 10% to less than 20% 20% or more

Great Lakes

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 19

Products & Markets

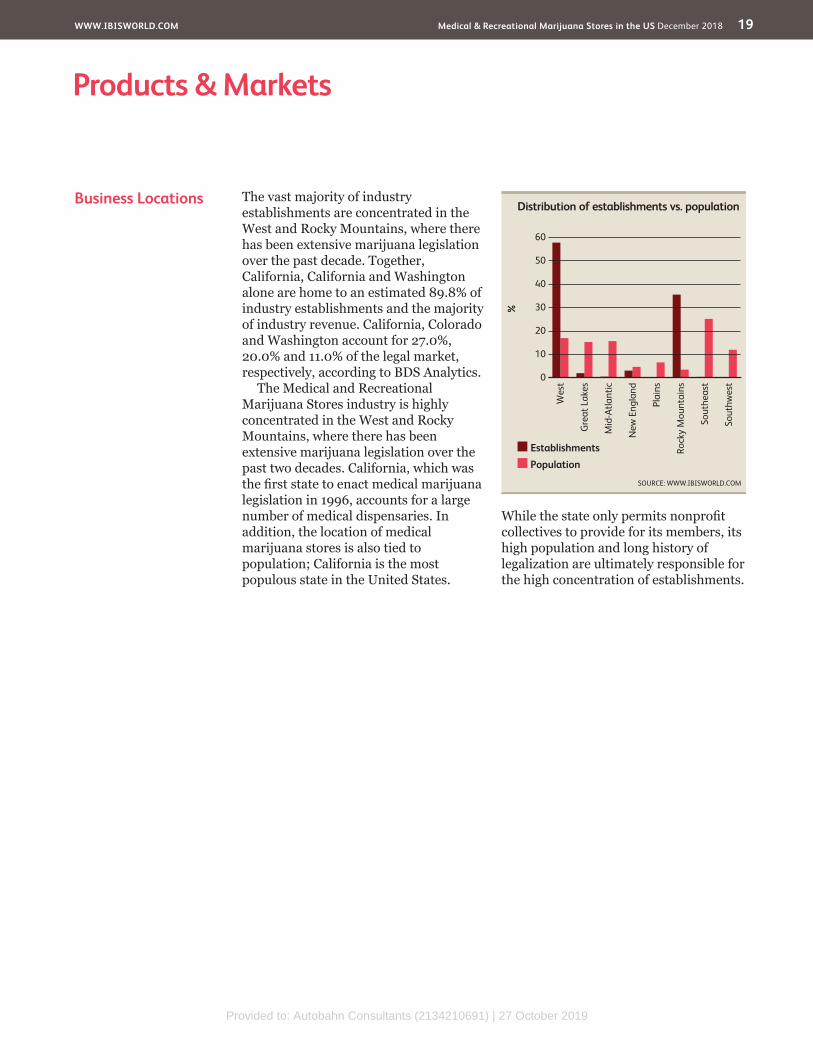

Business Locations The vast majority of industry establishments are concentrated in the West and Rocky Mountains, where there has been extensive marijuana legislation over the past decade. Together, California, California and Washington alone are home to an estimated 89.8% of industry establishments and the majority of industry revenue. California, Colorado and Washington account for 27.0%, 20.0% and 11.0% of the legal market, respectively, according to BDS Analytics.

The Medical and Recreational Marijuana Stores industry is highly concentrated in the West and Rocky Mountains, where there has been extensive marijuana legislation over the past two decades. California, which was the first state to enact medical marijuana legislation in 1996, accounts for a large number of medical dispensaries. In addition, the location of medical marijuana stores is also tied to population; California is the most populous state in the United States.

While the state only permits nonprofit collectives to provide for its members, its high population and long history of legalization are ultimately responsible for the high concentration of establishments.

%

60

0

10

20

30

40

50

Sout

hwes

t

Wes

t

Gre

at L

akes

Mid

-Atla

ntic

New

Eng

land

Plai

ns

Rock

y M

ount

ains

Sout

heas

t

EstablishmentsPopulation

Distribution of establishments vs. population

SOURCE: WWW.IBISWORLD.COM

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 20

Cost Structure Benchmarks

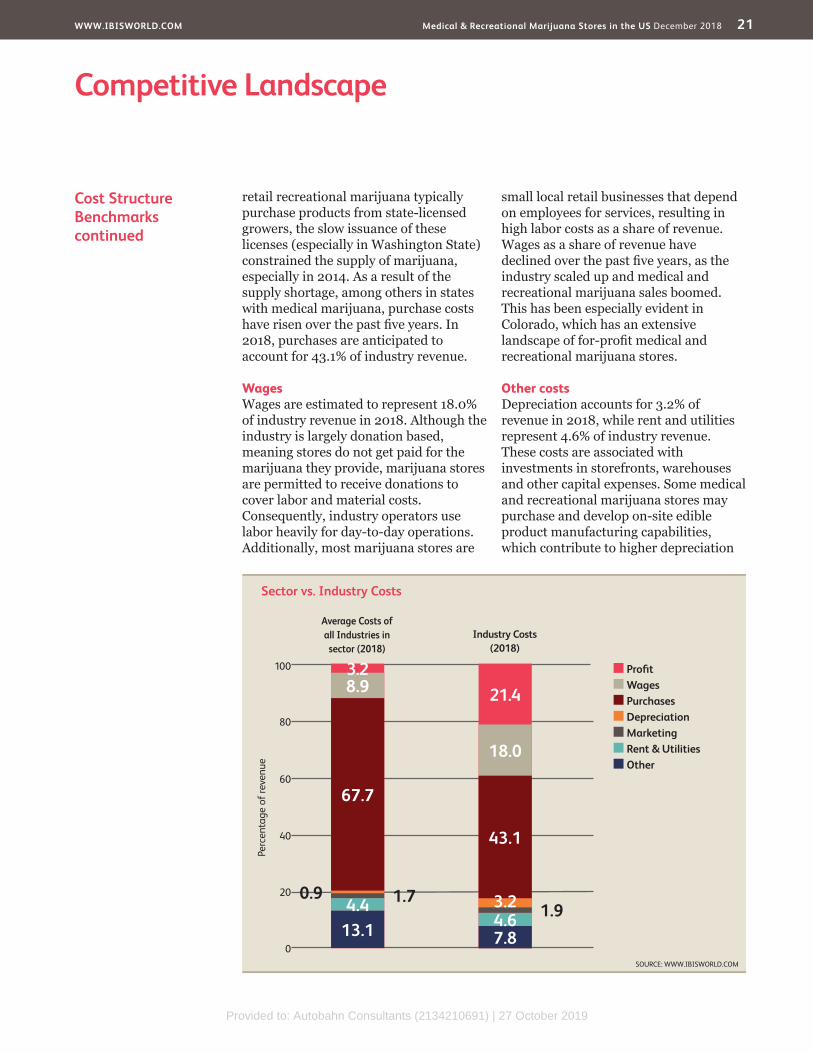

ProfitProfit, measured as earnings before interest and taxes, varies greatly across the industry because of the myriad laws governing medical and recreational marijuana from state to state. More recently, industry-wide margins have grown on account of the legalization of recreational marijuana across various US states, as well as the expanding medical marijuana market in 31 states. Industry profit margins are expected to total 21.4% in 2018.

PurchasesSimilar to the retail sector, purchases make up a significant expense for medical and recreational marijuana stores. Purchases are primarily composed of

storage equipment, medical marijuana accessories and other products that do not contain marijuana. In particular, medical marijuana stores need to purchase specialty lighting, airtight containers and cases, air conditioning and other equipment needed to store marijuana. Additionally, stores retail pipes, vaporizers, lighters and other products used to consume medical marijuana. Lastly, industry operators may purchase and retail edible products that include medical and/or recreational marijuana.

Over the past five years, purchase costs have risen with the legalization of recreational marijuana across various states, which have expanded into the second- and third-largest industry markets, respectively. Since stores that

Key Success Factors Ability to attract community supportMedical and recreational marijuana stores that lack community support may attract federal raids due to complaints from neighbors.

Understanding government policies and their implicationsMarijuana legislation is complicated at all levels of the government. Successful operators must be able to navigate the regulatory landscape at both the state and federal level.

Fast adjustments to changing regulationsRegulations are constantly changing. Growers must comply with the latest legislation or endure fines and arrest, and they must be able to adjust to changing regulation quickly and smoothly.

Marketing of differentiated productsDispensaries must properly promote their products given the differentiated nature of edible cannabis products. Promotional efforts are essential to attracting new customers.

Market Share Concentration

The Medical and Recreational Marijuana Stores industry has a low level of market share concentration. IBISWorld estimates that in 2018, the four largest operators are expected to account for less than 20.0% of industry revenue. By law, in the majority of states where medical marijuana is legal, industry operators must be a part of nonprofit marijuana collectives (also known as dispensaries) to sell marijuana.

IBISWorld anticipates that industry concentration will remain low over the next five years, although this outlook would materially change should the federal government reevaluate its classification of cannabis as a Schedule I substance. Nonetheless, the legalization of marijuana for recreational use in US states is expected to increase operators’ opportunities to expand on a for-profit basis.

Competitive LandscapeMarket Share Concentration | Key Success Factors | Cost Structure Benchmarks Basis of Competition | Barriers to Entry | Industry Globalization

Level Concentration in this industry is Low

IBISWorld identifies 250 Key Success Factors for a business. The most important for this industry are:

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 21

Competitive Landscape

Cost Structure Benchmarkscontinued

retail recreational marijuana typically purchase products from state-licensed growers, the slow issuance of these licenses (especially in Washington State) constrained the supply of marijuana, especially in 2014. As a result of the supply shortage, among others in states with medical marijuana, purchase costs have risen over the past five years. In 2018, purchases are anticipated to account for 43.1% of industry revenue.

WagesWages are estimated to represent 18.0% of industry revenue in 2018. Although the industry is largely donation based, meaning stores do not get paid for the marijuana they provide, marijuana stores are permitted to receive donations to cover labor and material costs. Consequently, industry operators use labor heavily for day-to-day operations. Additionally, most marijuana stores are

small local retail businesses that depend on employees for services, resulting in high labor costs as a share of revenue. Wages as a share of revenue have declined over the past five years, as the industry scaled up and medical and recreational marijuana sales boomed. This has been especially evident in Colorado, which has an extensive landscape of for-profit medical and recreational marijuana stores.

Other costsDepreciation accounts for 3.2% of revenue in 2018, while rent and utilities represent 4.6% of industry revenue. These costs are associated with investments in storefronts, warehouses and other capital expenses. Some medical and recreational marijuana stores may purchase and develop on-site edible product manufacturing capabilities, which contribute to higher depreciation

Sector vs. Industry Costs

n Profi tn Wagesn Purchasesn Depreciationn Marketingn Rent & Utilitiesn Other

Average Costs of all Industries in sector (2018)

Industry Costs (2018)

0

20

40

60

Perc

enta

ge o

f rev

enue

80

100

SOURCE: WWW.IBISWORLD.COM

3.221.4

7.84.6 1.93.2

43.1

18.0

13.14.4 1.70.9

67.7

8.9

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 22

Competitive Landscape

Basis of Competition The legalization of recreational cannabis in eight states, coupled with the high potential for differentiation in the edible cannabis products segment, creates opportunities for larger operators to come into existence. In the absence of legislation at the federal level governing the sale of medical and recreational marijuana, the nature of competition is heavily dependent on the nature of state law. As a result, operators experience substantially different conditions from state to state.

Internal competitionIndustry competition is largely waged on products’ price and quality. Marijuana can have diverse properties and qualities, and only dispensaries that can consistently provide high-quality marijuana will attract demand from consumers. Additionally, dispensaries must be able to provide competitive prices. Customers can purchase marijuana from a wide range of dispensaries, marking it easy to only acquire products from the lowest-priced dispensaries. As a result, it is important that dispensaries use promotional efforts to attract new customers.

Although smokable indica cannabis products and smokable sativa cannabis products lack significant differentiation, there is a great degree of differentiation in the edible cannabis products segment. Edibles can take the form of food, extracts and oils, and range from marijuana-infused mints, candies, baked goods and beverages, among many other products. In fact, a whole field of cannabis-infused culinary cooking has emerged in recent years with the legalization of medical marijuana. It is important that industry operators have access to the newest products and are able to source popular items at competitive prices.

External completionIndustry operators experience competition from pharmaceutical companies that manufacture drugs to treat chronic pain, cancer, HIV and other illnesses that medical marijuana helps relieve. Medical marijuana users typically only turn to marijuana after other treatment has failed, though, resulting in limited external competition from drug manufacturers.

Cost Structure Benchmarkscontinued

costs. Other costs include liability insurance and legal costs. Marketing costs are low because major advertisers

are still hesitant to carry marijuana ads; these costs are estimated to account for 1.9% of total revenue in 2018.

Level & Trend Competition in this industry is High and the trend is Increasing

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 23

Competitive Landscape

Federal regulationProspective medical marijuana store operators, and recreation marijuana store operators must navigate a variety of legal issues before beginning operation. The classification of marijuana as a Schedule I controlled substance and the possibility of federal prosecution poses a significant barrier to entry, as the Drug Enforcement Administration has the requisite power to close dispensaries and seize their cannabis products. Recent favorable policy stances from the federal government on this matter caused a large number of operators to enter the industry during the current period. The omnibus spending bill signed by President Obama in December 2014 included historic provisions for medical marijuana. The bill included a rider to defund Department of Justice operations against medical marijuana, prohibiting federal agencies from using funding to “prevent [medical marijuana states] from implementing their own State laws that authorize the use, distribution, possession, or cultivation of medical marijuana.”

State regulationState regulations have mixed effects. In general, the passage of new legislation has largely benefited industry operators by legalizing medical marijuana. During the current five-year period, barriers to entry have decreased as 33 states have passed legislation legalizing some level of medical marijuana sales, with 10 states have legalized recreational cannabis. While states provide a legal avenue for operators to open dispensaries, regulations are extensive and costly for prospective operators. Although

regulation varies by state, operators must obtain the required licenses and permits.

Capital requirementsAlthough marijuana stores incur limited capital costs because of the low-tech nature of the industry, operators are impeded by their relative inability to obtain financing from traditional sources. To open a dispensary, operators must acquire a location, hire employees, purchase inventory and buy advertising, among other things. However, because the cultivation, distribution and use of cannabis remain illegal at the federal level, traditional financial institutions have been hesitant to provide financing to new entrants. As a result, new operators have been forced to rely on personal savings and loans from family members and friends to enter the industry, limiting entry. However, in 2014, the Obama administration effectively gave the green light to financial institutions to provide access to capital for industry operators in states where medical and recreational cannabis are legal. Consequently, obtaining access to capital is anticipated to become somewhat easier for potential operators over the next five years.

Barriers to Entry checklist

Competition HighConcentration LowLife Cycle Stage GrowthCapital Intensity MediumTechnology Change HighRegulation and Policy HeavyIndustry Assistance High

SOURCE: WWW.IBISWORLD.COM

Barriers to Entry

Level & Trend Barriers to Entry in this industry are High and Decreasing

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 24

Competitive Landscape

Industry Globalization

Legal cannabis, whether intended for medical or recreation use, is not traded internationally, resulting in a very low level of globalization. Outside of the US,

Canada has legalized recreational marijuana. Other countries in the South America have also legalized the sale of recreational marijuana.Level & Trend

Globalization in this industry is Low and the trend is Steady

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 25

Other Companies The Medical and Recreational Marijuana Stores industry does not have any major players. The majority of industry operators are independent, self-employed medical and/or recreational marijuana stores, resulting in very low market share concentration. Since the cultivation, distribution and sale of cannabis remains illegal at the federal level, establishments in states that permit medical marijuana are governed by a patchwork of laws, impeding any

one operator from effectively operating across states.

However, the legalization of marijuana for recreational use in various new locales has the potential to alter the industry landscape moving forward, bringing a flood of private equity and the potential for chain enterprises to become more common. Still, the ability of any company to gain a substantial share of the industry’s market share will ultimately hinge upon the legal status of marijuana at the federal level.

Major CompaniesThere are no Major Players in this industry | Other Companies

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 26

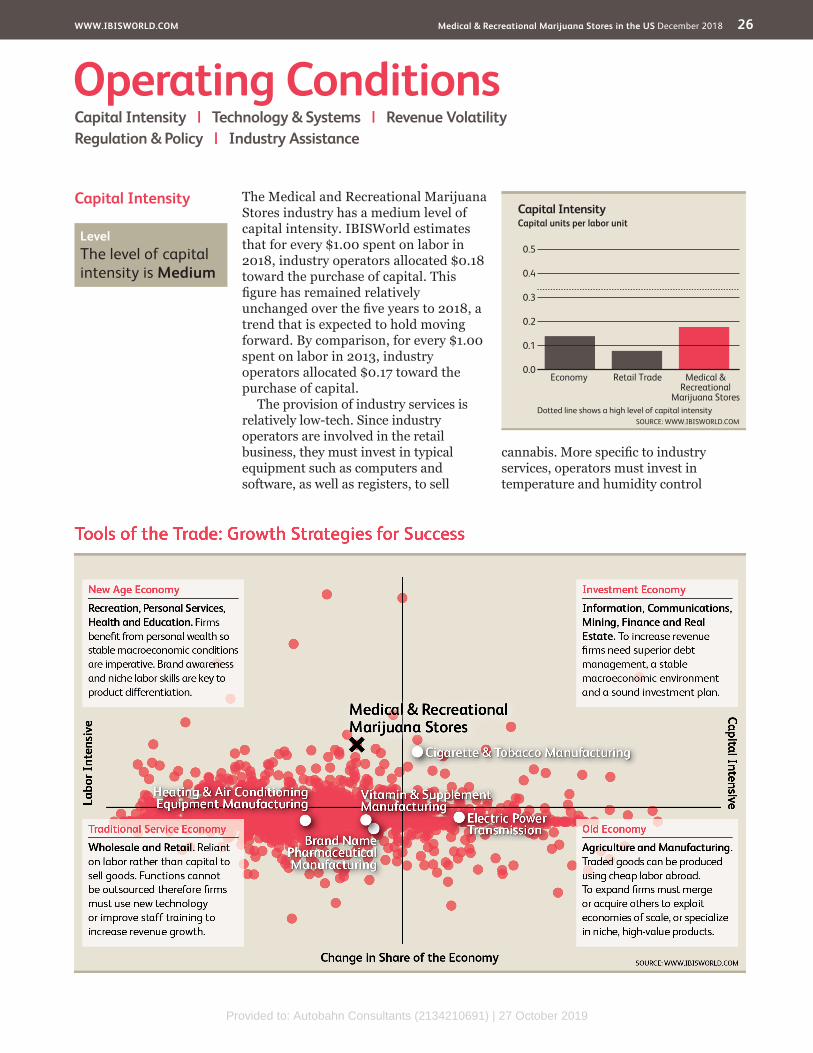

Capital Intensity The Medical and Recreational Marijuana Stores industry has a medium level of capital intensity. IBISWorld estimates that for every $1.00 spent on labor in 2018, industry operators allocated $0.18 toward the purchase of capital. This figure has remained relatively unchanged over the five years to 2018, a trend that is expected to hold moving forward. By comparison, for every $1.00 spent on labor in 2013, industry operators allocated $0.17 toward the purchase of capital.

The provision of industry services is relatively low-tech. Since industry operators are involved in the retail business, they must invest in typical equipment such as computers and software, as well as registers, to sell

cannabis. More specific to industry services, operators must invest in temperature and humidity control

Operating ConditionsCapital Intensity | Technology & Systems | Revenue VolatilityRegulation & Policy | Industry Assistance

Capital Intensity

0.5

0.0

0.1

0.2

0.3

0.4

SOURCE: WWW.IBISWORLD.COMDotted line shows a high level of capital intensity

Capital units per labor unit

Medical & Recreational

Marijuana Stores

Retail TradeEconomy

Level The level of capital intensity is Medium

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 27

Operating Conditions

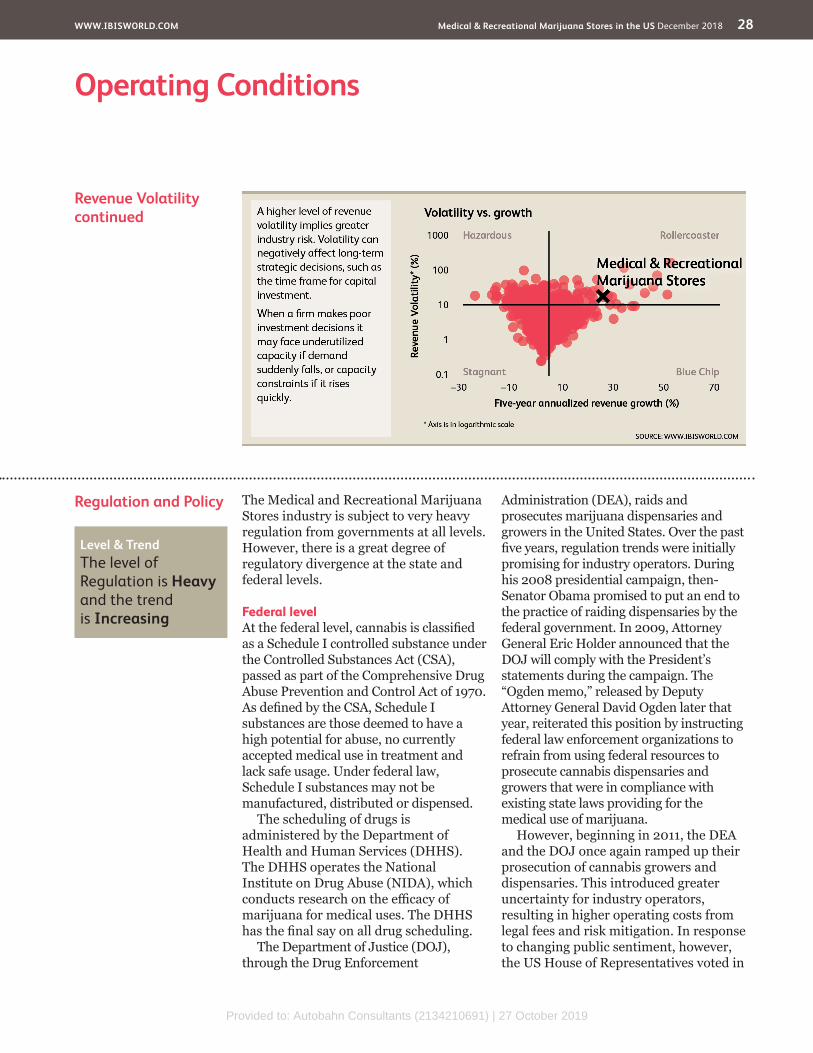

Revenue Volatility The Medical and Recreational Marijuana Stores industry has a high level of revenue volatility. Industry revenue has continually risen and is expected to grow consecutively over the five years to 2018. IBISWorld expects that in 2018 alone, industry revenue will grow 26.5%. Demand for industry products is rapidly expanding due to the growing acceptance of medical marijuana in treating or alleviating symptoms in a variety of medical conditions, including cancer, epilepsy and the Alzheimer’s Disease.

However, changes in the regulatory landscape serve as the most important

driver of revenue fluctuations. The legalization of medical marijuana use in some form across numerous states has caused industry revenue to jump in individual years. In 2014, for example, revenue rose an astronomical 52.0% on account of the legalization of cannabis sales for recreational use in Colorado and Washington, in addition to the wider use of medical marijuana across other states. IBISWorld expects that revenue volatility will increase over the five years to 2023 as other states across the United States legalize the sale of medical and recreational marijuana in some form.

Technology and Systems

While the Medical and Recreational Marijuana Stores industry relies only minimally on capital equipment, cannabis products have changed dramatically in recent decades. Since the legalization of medicinal cannabis, the industry’s fast-growing edible cannabis products segment has experienced a significant amount of innovation.

Cannabis qualityOver the past 30 years, cannabis quality has improved as a result of better cultivation practices. Improvement in quality is measured by the level of tetrahydrocannabinol (THC), which is the principal psychoactive constituent in cannabis plants. Improved cultivation techniques range from the use of more nutrient rich soils to more efficient drying techniques, which have enabled growers to harvest both larger and stronger yields. According to the latest

available data provided by the University of Mississippi’s Potency Monitoring Project, marijuana that was analyzed in 2007 had a THC level of 9.6%, the highest level since analysts began tracking this data in 1976.

Cannabis productsThe legalization of medical marijuana across numerous states, as well as the legalization of recreational marijuana in Colorado and Washington State, has also spurred changes in the kind of cannabis products available for sale, fueling demand for industry goods in turn. Edible cannabis products, the industry’s fastest growing segment, comprises marijuana-infused mints, candies, baked goods and beverages, among numerous other products. With countless new edible marijuana products coming onto the market, the nature of industry products is changing rapidly.

Capital Intensitycontinued

systems to ensure that they are able to maintain the quality of their stock. Perhaps most importantly, industry operators must invest heavily in security equipment, such as video cameras and

alarm systems. Since marijuana dispensaries have been plagued by robberies, it is necessary that industry operators invest in equipment to ensure the safety of their products.

Level The level of technology change is High

Level The level of volatility is High

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 28

Operating Conditions

Regulation and Policy The Medical and Recreational Marijuana Stores industry is subject to very heavy regulation from governments at all levels. However, there is a great degree of regulatory divergence at the state and federal levels.

Federal levelAt the federal level, cannabis is classified as a Schedule I controlled substance under the Controlled Substances Act (CSA), passed as part of the Comprehensive Drug Abuse Prevention and Control Act of 1970. As defined by the CSA, Schedule I substances are those deemed to have a high potential for abuse, no currently accepted medical use in treatment and lack safe usage. Under federal law, Schedule I substances may not be manufactured, distributed or dispensed.

The scheduling of drugs is administered by the Department of Health and Human Services (DHHS). The DHHS operates the National Institute on Drug Abuse (NIDA), which conducts research on the efficacy of marijuana for medical uses. The DHHS has the final say on all drug scheduling.

The Department of Justice (DOJ), through the Drug Enforcement

Administration (DEA), raids and prosecutes marijuana dispensaries and growers in the United States. Over the past five years, regulation trends were initially promising for industry operators. During his 2008 presidential campaign, then-Senator Obama promised to put an end to the practice of raiding dispensaries by the federal government. In 2009, Attorney General Eric Holder announced that the DOJ will comply with the President’s statements during the campaign. The “Ogden memo,” released by Deputy Attorney General David Ogden later that year, reiterated this position by instructing federal law enforcement organizations to refrain from using federal resources to prosecute cannabis dispensaries and growers that were in compliance with existing state laws providing for the medical use of marijuana.

However, beginning in 2011, the DEA and the DOJ once again ramped up their prosecution of cannabis growers and dispensaries. This introduced greater uncertainty for industry operators, resulting in higher operating costs from legal fees and risk mitigation. In response to changing public sentiment, however, the US House of Representatives voted in

Revenue Volatilitycontinued

Level & Trend The level of Regulation is Heavy and the trend is Increasing

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 29

Operating Conditions

Industry Assistance Government regulationAlthough the existence of the Medical and Recreational Marijuana Stores industry is considered illegal at the federal level, the passage of regulation concerning the medical and recreational use of marijuana across over half of US states has facilitated the existence and expansion of the industry. While the industry does not benefit from any government subsidies, the expected continuation of new laws legalizing the medical and recreational use of marijuana will continue to benefit the industry.

Industry associationsThis industry benefits from relatively widespread support from industry associations. The National Cannabis Industry Association is a trade association representing industry operators. The organization lobbies lawmakers in Washington, DC for more favorable marijuana legislation. These include legislation on banking that permits marijuana businesses to work with financial institutions. Currently, banks are hesitant to provide services to marijuana

Regulation and Policycontinued

2014 to restrict the DEA from using funds to target medical marijuana growers and dispensaries. Although this amendment to the DEA appropriations bill would need to be passed by the Senate to become binding, its confirmation would materially alter the outlook for industry operators. The omnibus spending bill signed by President Obama in December 2014 included a rider to defund DOJ operations against medical marijuana, prohibiting federal agencies from using funding to “prevent [medical marijuana states] from implementing their own State laws that authorize the use, distribution, possession, or cultivation of medical marijuana.”

State regulationCurrently, 31 states have some regulation that permitted the use of medical marijuana. Nine states (Alaska, California, Colorado, Maine, Massachusetts, Nevada, Oregon, Vermont and Washington) have permitted the legal sale of cannabis for recreational use. However, because federal law supersedes state law, the cultivation, sale and use of medical or recreational marijuana remain illegal in the United States. California has the

oldest and one of the most extensive regulatory frameworks governing medical marijuana. In 1996, the passage of the Compassionate Use Act (Proposition 215) legalized the use of medical marijuana and prohibited physicians from being punished for recommending medical marijuana to patients. California Senate Bill 420, passed in 2003, further clarified the state’s position on medical marijuana, legalizing organization of nonprofit marijuana collectives where members can cultivate and provide marijuana to each other.

In addition to California, the state of Colorado has some of the most extensive medical marijuana laws. The use of medical marijuana has been legal since the passage of Amendment 20 in 2000. In 2012, the state further loosened marijuana restrictions by passing Amendment 64, which legalized marijuana for recreational use. With the growth of the edible cannabis products segment, the state has moved to enact new regulations. Several high-profile incidents involving edible cannabis products have spurred new rules, signed into law in May 2014, concerning the packaging of edible marijuana products, including improved information regarding serving sizes.

Level & Trend The level of Industry Assistance is High and the trend is Increasing

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 30

Operating Conditions

Industry Assistancecontinued

businesses due to the illegality of marijuana at the federal level.

The National Organization for the Reform of Marijuana Laws (NORML) works to repeal marijuana prohibition at the federal level. The organization

supports the right of adults to use marijuana responsibly, and champions state and federal reforms that are favorable to marijuana users. NORML primarily lobbies Congress and state legislatures to enact marijuana reforms.

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 31

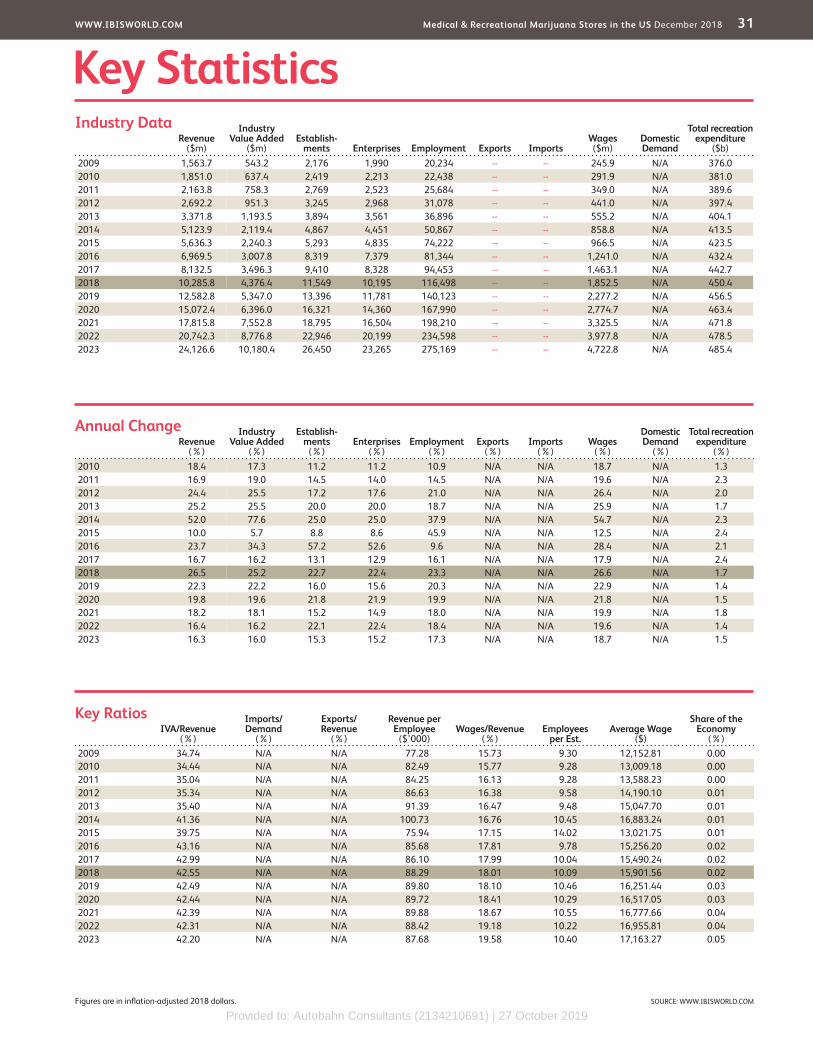

Key StatisticsRevenue

($m)

Industry Value Added

($m)Establish-

ments Enterprises Employment Exports ImportsWages ($m)

Domestic Demand

Total recreation expenditure

($b)2009 1,563.7 543.2 2,176 1,990 20,234 -- -- 245.9 N/A 376.02010 1,851.0 637.4 2,419 2,213 22,438 -- -- 291.9 N/A 381.02011 2,163.8 758.3 2,769 2,523 25,684 -- -- 349.0 N/A 389.62012 2,692.2 951.3 3,245 2,968 31,078 -- -- 441.0 N/A 397.42013 3,371.8 1,193.5 3,894 3,561 36,896 -- -- 555.2 N/A 404.12014 5,123.9 2,119.4 4,867 4,451 50,867 -- -- 858.8 N/A 413.52015 5,636.3 2,240.3 5,293 4,835 74,222 -- -- 966.5 N/A 423.52016 6,969.5 3,007.8 8,319 7,379 81,344 -- -- 1,241.0 N/A 432.42017 8,132.5 3,496.3 9,410 8,328 94,453 -- -- 1,463.1 N/A 442.72018 10,285.8 4,376.4 11,549 10,195 116,498 -- -- 1,852.5 N/A 450.42019 12,582.8 5,347.0 13,396 11,781 140,123 -- -- 2,277.2 N/A 456.52020 15,072.4 6,396.0 16,321 14,360 167,990 -- -- 2,774.7 N/A 463.42021 17,815.8 7,552.8 18,795 16,504 198,210 -- -- 3,325.5 N/A 471.82022 20,742.3 8,776.8 22,946 20,199 234,598 -- -- 3,977.8 N/A 478.52023 24,126.6 10,180.4 26,450 23,265 275,169 -- -- 4,722.8 N/A 485.4

IVA/Revenue (%)

Imports/ Demand

(%)

Exports/ Revenue

(%)

Revenue per Employee

($’000)Wages/Revenue

(%)Employees

per Est.Average Wage

($)

Share of the Economy

(%)2009 34.74 N/A N/A 77.28 15.73 9.30 12,152.81 0.002010 34.44 N/A N/A 82.49 15.77 9.28 13,009.18 0.002011 35.04 N/A N/A 84.25 16.13 9.28 13,588.23 0.002012 35.34 N/A N/A 86.63 16.38 9.58 14,190.10 0.012013 35.40 N/A N/A 91.39 16.47 9.48 15,047.70 0.012014 41.36 N/A N/A 100.73 16.76 10.45 16,883.24 0.012015 39.75 N/A N/A 75.94 17.15 14.02 13,021.75 0.012016 43.16 N/A N/A 85.68 17.81 9.78 15,256.20 0.022017 42.99 N/A N/A 86.10 17.99 10.04 15,490.24 0.022018 42.55 N/A N/A 88.29 18.01 10.09 15,901.56 0.022019 42.49 N/A N/A 89.80 18.10 10.46 16,251.44 0.032020 42.44 N/A N/A 89.72 18.41 10.29 16,517.05 0.032021 42.39 N/A N/A 89.88 18.67 10.55 16,777.66 0.042022 42.31 N/A N/A 88.42 19.18 10.22 16,955.81 0.042023 42.20 N/A N/A 87.68 19.58 10.40 17,163.27 0.05

Figures are in inflation-adjusted 2018 dollars.

Revenue (%)

Industry Value Added

(%)

Establish-ments

(%)Enterprises

(%)Employment

(%)Exports

(%)Imports

(%)Wages

(%)

Domestic Demand

(%)

Total recreation expenditure

(%)2010 18.4 17.3 11.2 11.2 10.9 N/A N/A 18.7 N/A 1.32011 16.9 19.0 14.5 14.0 14.5 N/A N/A 19.6 N/A 2.32012 24.4 25.5 17.2 17.6 21.0 N/A N/A 26.4 N/A 2.02013 25.2 25.5 20.0 20.0 18.7 N/A N/A 25.9 N/A 1.72014 52.0 77.6 25.0 25.0 37.9 N/A N/A 54.7 N/A 2.32015 10.0 5.7 8.8 8.6 45.9 N/A N/A 12.5 N/A 2.42016 23.7 34.3 57.2 52.6 9.6 N/A N/A 28.4 N/A 2.12017 16.7 16.2 13.1 12.9 16.1 N/A N/A 17.9 N/A 2.42018 26.5 25.2 22.7 22.4 23.3 N/A N/A 26.6 N/A 1.72019 22.3 22.2 16.0 15.6 20.3 N/A N/A 22.9 N/A 1.42020 19.8 19.6 21.8 21.9 19.9 N/A N/A 21.8 N/A 1.52021 18.2 18.1 15.2 14.9 18.0 N/A N/A 19.9 N/A 1.82022 16.4 16.2 22.1 22.4 18.4 N/A N/A 19.6 N/A 1.42023 16.3 16.0 15.3 15.2 17.3 N/A N/A 18.7 N/A 1.5

Annual Change

Key Ratios

Industry Data

SOURCE: WWW.IBISWORLD.COM

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

WWW.IBISWORLD.COM Medical & Recreational Marijuana Stores in the US December 2018 32

Jargon & Glossary

BARRIERS TO ENTRY High barriers to entry mean that new companies struggle to enter an industry, while low barriers mean it is easy for new companies to enter an industry.

CAPITAL INTENSITY Compares the amount of money spent on capital (plant, machinery and equipment) with that spent on labor. IBISWorld uses the ratio of depreciation to wages as a proxy for capital intensity. High capital intensity is more than $0.333 of capital to $1 of labor; medium is $0.125 to $0.333 of capital to $1 of labor; low is less than $0.125 of capital for every $1 of labor.

CONSTANT PRICES The dollar figures in the Key Statistics table, including forecasts, are adjusted for inflation using the current year (i.e. year published) as the base year. This removes the impact of changes in the purchasing power of the dollar, leaving only the “real” growth or decline in industry metrics. The inflation adjustments in IBISWorld’s reports are made using the US Bureau of Economic Analysis’ implicit GDP price deflator.

DOMESTIC DEMAND Spending on industry goods and services within the United States, regardless of their country of origin. It is derived by adding imports to industry revenue, and then subtracting exports.

EMPLOYMENT The number of permanent, part-time, temporary and seasonal employees, working proprietors, partners, managers and executives within the industry.

ENTERPRISE A division that is separately managed and keeps management accounts. Each enterprise consists of one or more establishments that are under common ownership or control.

ESTABLISHMENT The smallest type of accounting unit within an enterprise, an establishment is a single physical location where business is conducted or where services or industrial operations are performed. Multiple establishments under common control make up an enterprise.

EXPORTS Total value of industry goods and services sold by US companies to customers abroad.

IMPORTS Total value of industry goods and services brought in from foreign countries to be sold in the United States.

INDUSTRY CONCENTRATION An indicator of the dominance of the top four players in an industry. Concentration is considered high if the top players account for more than 70% of industry revenue. Medium is 40% to 70% of industry revenue. Low is less than 40%.

INDUSTRY REVENUE The total sales of industry goods and services (exclusive of excise and sales tax); subsidies on production; all other operating income from outside the firm (such as commission income, repair and service income, and rent, leasing and hiring income); and capital work done by rental or lease. Receipts from interest royalties, dividends and the sale of fixed tangible assets are excluded.

INDUSTRY VALUE ADDED (IVA) The market value of goods and services produced by the industry minus the cost of goods and services used in production. IVA is also described as the industry’s contribution to GDP, or profit plus wages and depreciation.

INTERNATIONAL TRADE The level of international trade is determined by ratios of exports to revenue and imports to domestic demand. For exports/revenue: low is less than 5%, medium is 5% to 20%, and high is more than 20%. Imports/domestic demand: low is less than 5%, medium is 5% to 35%, and high is more than 35%.

LIFE CYCLE All industries go through periods of growth, maturity and decline. IBISWorld determines an industry’s life cycle by considering its growth rate (measured by IVA) compared with GDP; the growth rate of the number of establishments; the amount of change the industry’s products are undergoing; the rate of technological change; and the level of customer acceptance of industry products and services.

NONEMPLOYING ESTABLISHMENT Businesses with no paid employment or payroll, also known as nonemployers. These are mostly set up by self-employed individuals.

PROFIT IBISWorld uses earnings before interest and tax (EBIT) as an indicator of a company’s profitability. It is calculated as revenue minus expenses, excluding interest and tax.

VOLATILITY The level of volatility is determined by averaging the absolute change in revenue in each of the past five years. Volatility levels: very high is more than ±20%; high volatility is ±10% to ±20%; moderate volatility is ±3% to ±10%; and low volatility is less than ±3%.

WAGES The gross total wages and salaries of all employees in the industry. The cost of benefits is also included in this figure.

Industry Jargon

IBISWorld Glossary

CANNABIS The plant from which medical marijuana is harvested.

DISPENARY Designated medical marijuana retail stores.

EDIBLES Edible cannabis products, often in the form of baked goods or candies.

Provided to: Autobahn Consultants (2134210691) | 27 October 2019

Disclaimer

This product has been supplied by IBISWorld Inc. (‘IBISWorld’) solely for use by its authorized licenses strictly in accordance with their license agreements with IBISWorld. IBISWorld makes no representation to any other person with regard to the completeness or accuracy of the data or information contained herein, and it accepts no responsibility and disclaims all liability (save for liability which cannot be lawfully disclaimed) for loss or damage whatsoever suffered or incurred by any other person resulting from the use

of, or reliance upon, the data or information contained herein. Copyright in this publication is owned by IBISWorld Inc. The publication is sold on the basis that the purchaser agrees not to copy the material contained within it for other than the purchasers own purposes. In the event that the purchaser uses or quotes from the material in this publication – in papers, reports, or opinions prepared for any other person – it is agreed that it will be sourced to: IBISWorld Inc.