Embed Size (px)

Citation preview

MCX IPF PRESENTATION

COTTON PRICE RISK MANAGEMENT

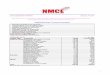

PRESENT COMMODITY EXCHANGE ECOSYSTEM

COMMODITY DERIVATIVES EXCHANGE

VAULTS

ComRIS

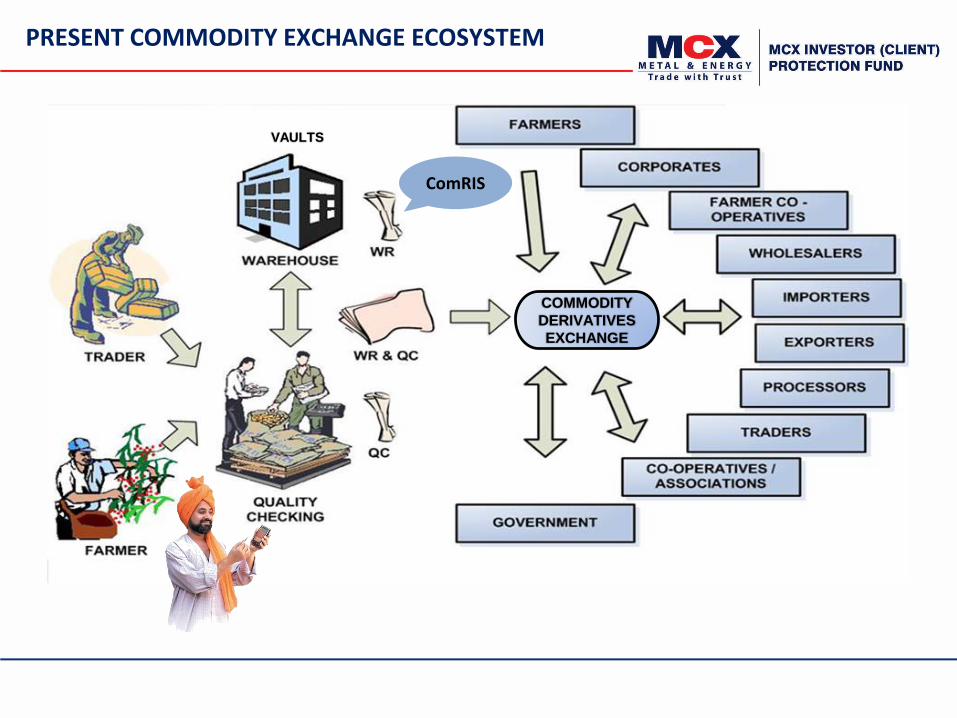

ACTIVE COMMODITIES ON NATIONAL EXCHANGES & COMMODITIES TRADED AT MCX

, Chana

PermittedCommodities

PreciousMetals Metals

Energy &

Others

Agri * Total

SEBI Notified 4 11 12 64 91

Listed at

MCX 2 5 2 6 15

NCDEX, NMCE & ICEX

1 - - 15 14

* Agri includes Cereals, Pulses, Oilseeds, Oil cakes, Spices, Fibres, Sweeteners, Plantation, Dry fruits & other non-farmer linked agri commodities

COMMODITIES TRADED AT MCX

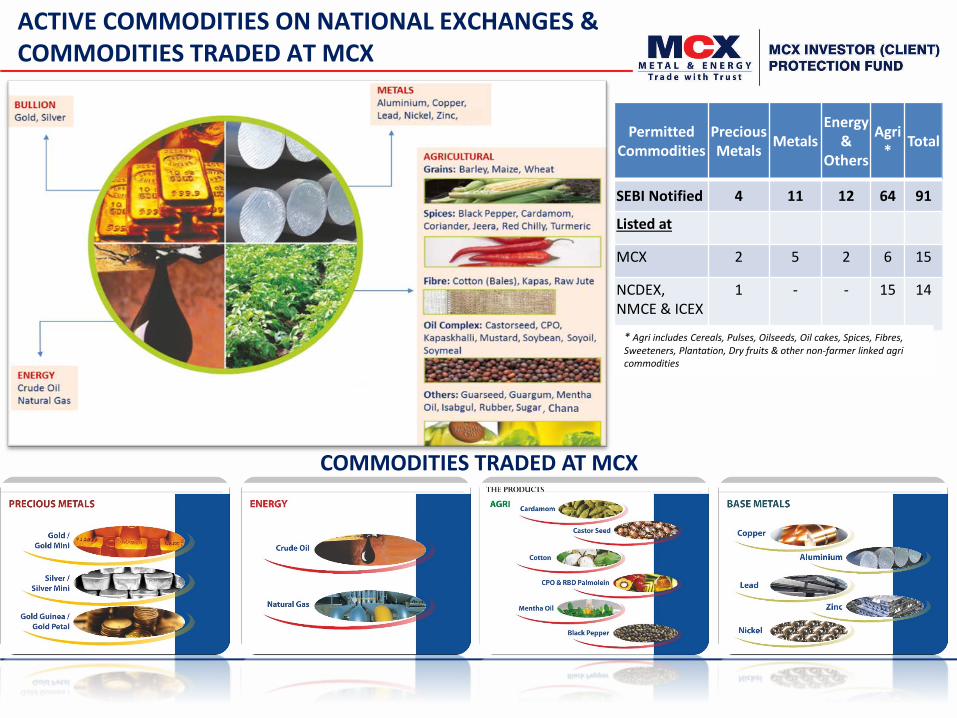

MCX IN INDIAN MARKET

CommoditySegment

MCX Market Share in Indian Commodity Derivatives

Proportion of MCX’s turnover

Precious Metals & Stones 99.92% 27%

Energy 100% 32%

Base Metals 100% 39%

Agri-Commodities 15.58% 2%

MCX: MARKET SHARE IN KEY SEGMENTS FOR FY17-18 (9M)

EXTENSIVE REACH (as on 31.12.2017)

669 Members51,575 Authorized Persons

1,211 cities / towns across IndiaMarket share of 89.73 %

F&O AVERAGE DAILY TURNOVER(ADT) in Rs Crore

20,229

21,023

140

19,500 20,000 20,500 21,000 21,500

Q3 FY 2018

Q3 FY 2017

Futures

Options*

* Option trading in gold contracts commenced on 17th October, 2017

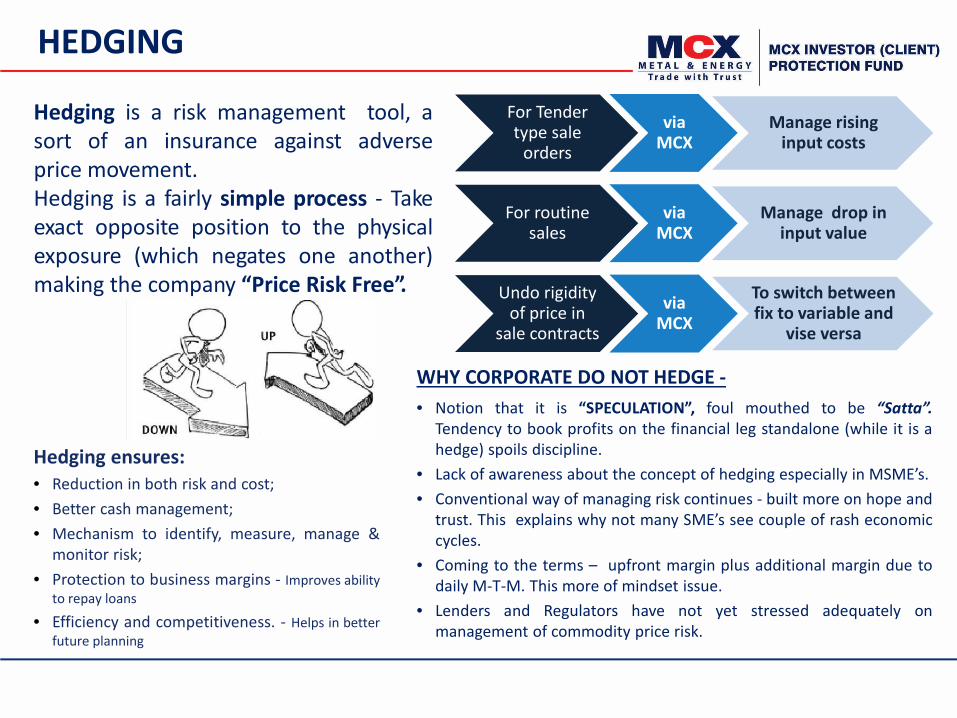

Hedging is a risk management tool, asort of an insurance against adverseprice movement.Hedging is a fairly simple process - Takeexact opposite position to the physicalexposure (which negates one another)making the company “Price Risk Free”.

HEDGING

For Tender type sale

orders

via MCX

Manage rising input costs

For routine sales

via MCX

Manage drop in input value

Undo rigidity of price in

sale contracts

via MCX

To switch between fix to variable and

vise versa

WHY CORPORATE DO NOT HEDGE -• Notion that it is “SPECULATION”, foul mouthed to be “Satta”.

Tendency to book profits on the financial leg standalone (while it is ahedge) spoils discipline.

• Lack of awareness about the concept of hedging especially in MSME’s.• Conventional way of managing risk continues - built more on hope and

trust. This explains why not many SME’s see couple of rash economiccycles.

• Coming to the terms – upfront margin plus additional margin due todaily M-T-M. This more of mindset issue.

• Lenders and Regulators have not yet stressed adequately onmanagement of commodity price risk.

Hedging ensures:• Reduction in both risk and cost;• Better cash management;• Mechanism to identify, measure, manage &

monitor risk;• Protection to business margins - Improves ability

to repay loans

• Efficiency and competitiveness. - Helps in betterfuture planning

IMPACT OF COMMODITY FUTURES - SYNOPSIS OF EVALUATION STUDIES

Impact Assessment Study of Cardamom Futures Trading - IIM Kozhikode (2014): Planter may be better offby selling his output in a futures exchange since, the chances of getting a better price for their high qualityoutput is better.

Study by Deloitte India (2013): Commodity futures market directly generates employment for around 1.5million personnel in India – 0.93% of India’s service sector labor force

The Nielsen Company (2013): Assessing the Impact of Dabba Trading on Commodity markets in India – TheDabba Market (trades outside the regulated markets) is more than 3 times of the trading through regulated Exchanges

IIM Calcutta and NISTADS, New Delhi (2012): Mentha Oil futures facilitated rise of India as major exporterof processed mentha crystals – transitioning from raw material exports.

Tata Institute of Social Sciences (2012): Futures platform has ensured stable and fair prices for the SMEs.Fairer prices reduce the cost of production and import bill, boost growth of the SMEs and provide accuratedemand-supply signals that reduce risks in SMEs.

UNCTAD (2009): Number of intermediaries in Mentha value chain has reduced after introduction offutures market, reducing the price spread in the marketing channel from 11-12% to 7.5-10.5%. In case ofCardamom, it has helped to stabilize prices in the spot market.

IIM Lucknow (2007): Potato and Mentha Oil markets showed substantial improvements in increased pricerealization to farmers during the period after the introduction of futures.

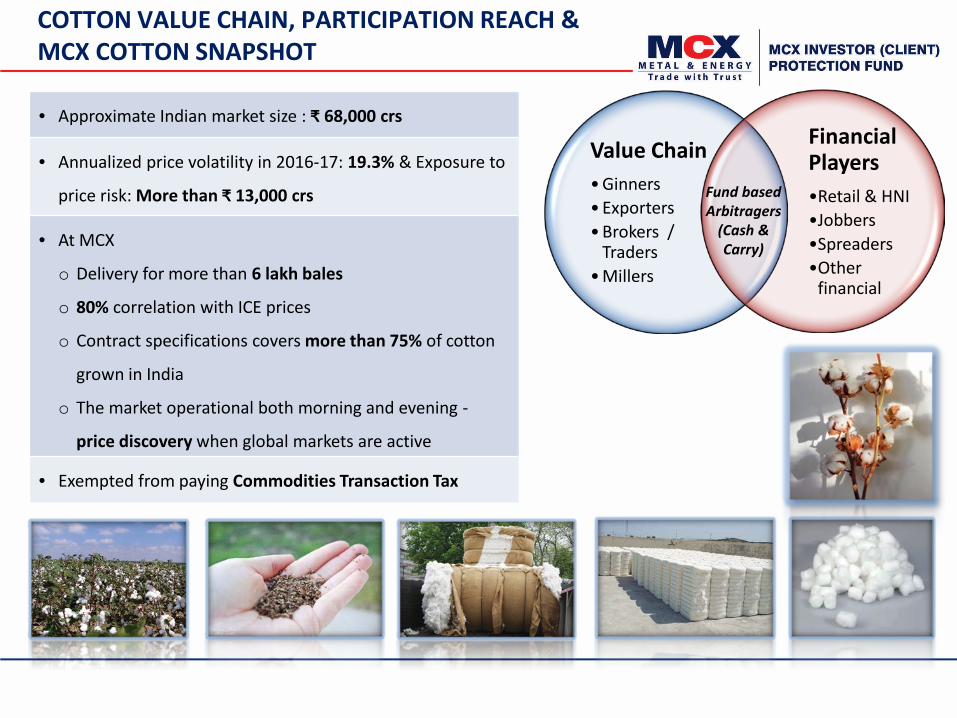

COTTON VALUE CHAIN, PARTICIPATION REACH & MCX COTTON SNAPSHOT

• Approximate Indian market size : ₹ 68,000 crs

• Annualized price volatility in 2016-17: 19.3% & Exposure to

price risk: More than ₹ 13,000 crs

• At MCX

o Delivery for more than 6 lakh bales

o 80% correlation with ICE prices

o Contract specifications covers more than 75% of cotton

grown in India

o The market operational both morning and evening -

price discovery when global markets are active

• Exempted from paying Commodities Transaction Tax

Value Chain• Ginners• Exporters• Brokers /

Traders• Millers

Financial Players•Retail & HNI•Jobbers•Spreaders•Other

financial

Fund based Arbitragers

(Cash & Carry)

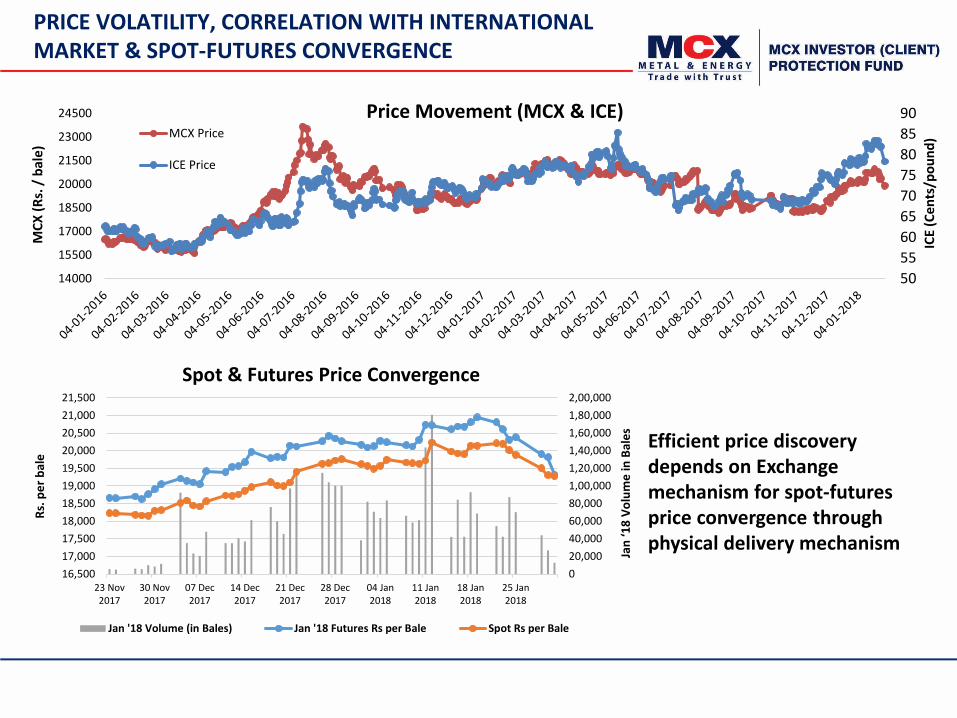

PRICE VOLATILITY, CORRELATION WITH INTERNATIONAL MARKET & SPOT-FUTURES CONVERGENCE

505560657075808590

14000

15500

17000

18500

20000

21500

23000

24500

ICE

(Cen

ts/p

ound

)

MCX

(Rs.

/ b

ale)

Price Movement (MCX & ICE)MCX Price

ICE Price

Efficient price discovery depends on Exchange mechanism for spot-futures price convergence through physical delivery mechanism

020,00040,00060,00080,0001,00,0001,20,0001,40,0001,60,0001,80,0002,00,000

16,50017,00017,50018,00018,50019,00019,50020,00020,50021,00021,500

23 Nov2017

30 Nov2017

07 Dec2017

14 Dec2017

21 Dec2017

28 Dec2017

04 Jan2018

11 Jan2018

18 Jan2018

25 Jan2018

Jan

‘18

Volu

me

in B

ales

Rs. p

er b

ale

Spot & Futures Price Convergence

Jan '18 Volume (in Bales) Jan '18 Futures Rs per Bale Spot Rs per Bale

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

500000

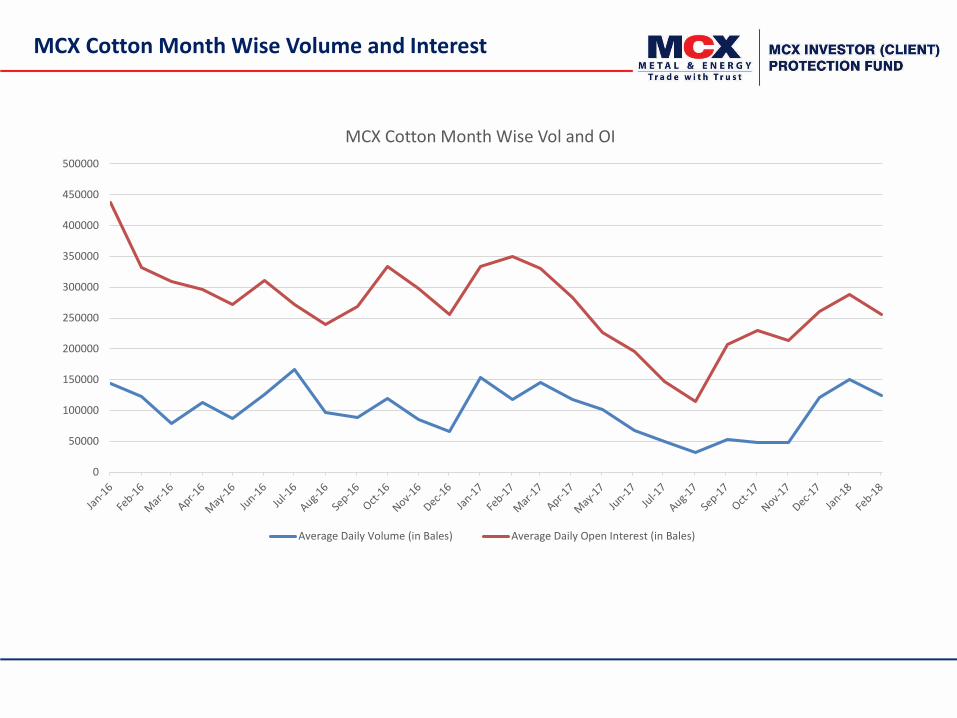

MCX Cotton Month Wise Vol and OI

Average Daily Volume (in Bales) Average Daily Open Interest (in Bales)

MCX Cotton Month Wise Volume and Interest

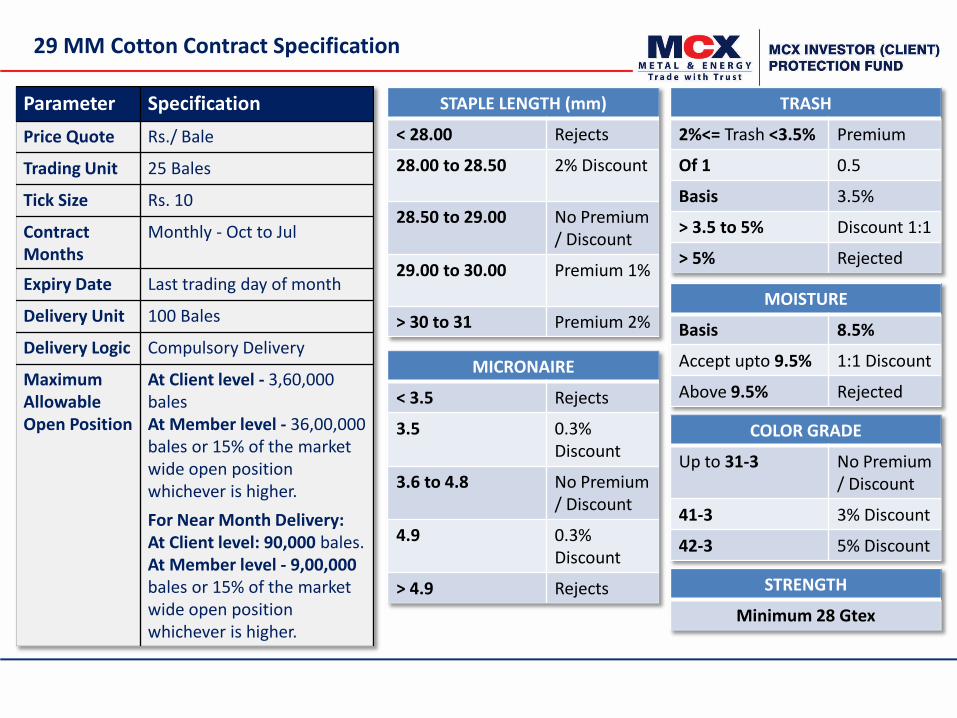

29 MM Cotton Contract Specification

Parameter SpecificationPrice Quote Rs./ Bale

Trading Unit 25 Bales

Tick Size Rs. 10

Contract Months

Monthly - Oct to Jul

Expiry Date Last trading day of month

Delivery Unit 100 Bales

Delivery Logic Compulsory Delivery

Maximum Allowable Open Position

At Client level - 3,60,000 balesAt Member level - 36,00,000 bales or 15% of the market wide open position whichever is higher.For Near Month Delivery:At Client level: 90,000 bales.At Member level - 9,00,000 bales or 15% of the market wide open position whichever is higher.

STAPLE LENGTH (mm)

< 28.00 Rejects

28.00 to 28.50 2% Discount

28.50 to 29.00 No Premium / Discount

29.00 to 30.00 Premium 1%

> 30 to 31 Premium 2%

MICRONAIRE

< 3.5 Rejects

3.5 0.3% Discount

3.6 to 4.8 No Premium / Discount

4.9 0.3% Discount

> 4.9 Rejects

TRASH

2%<= Trash <3.5% Premium

Of 1 0.5

Basis 3.5%

> 3.5 to 5% Discount 1:1

> 5% Rejected

MOISTURE

Basis 8.5%

Accept upto 9.5% 1:1 Discount

Above 9.5% Rejected

COLOR GRADE

Up to 31-3 No Premium / Discount

41-3 3% Discount

42-3 5% Discount

STRENGTH

Minimum 28 Gtex

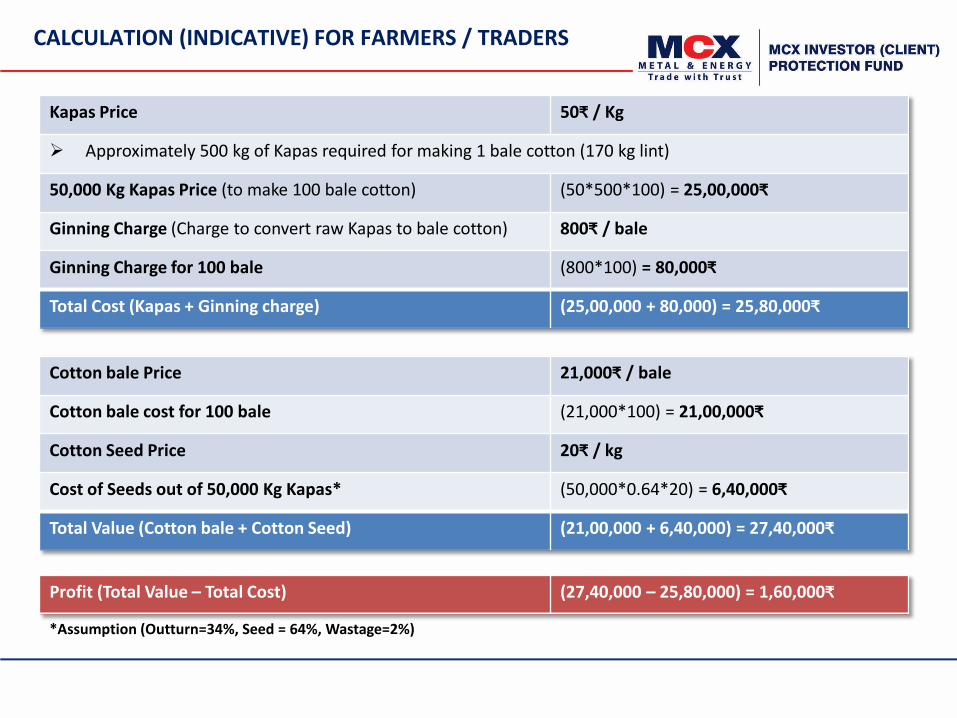

CALCULATION (INDICATIVE) FOR FARMERS / TRADERS

Kapas Price 50₹ / Kg

Approximately 500 kg of Kapas required for making 1 bale cotton (170 kg lint)

50,000 Kg Kapas Price (to make 100 bale cotton) (50*500*100) = 25,00,000₹

Ginning Charge (Charge to convert raw Kapas to bale cotton) 800₹ / bale

Ginning Charge for 100 bale (800*100) = 80,000₹

Total Cost (Kapas + Ginning charge) (25,00,000 + 80,000) = 25,80,000₹

Cotton bale Price 21,000₹ / bale

Cotton bale cost for 100 bale (21,000*100) = 21,00,000₹

Cotton Seed Price 20₹ / kg

Cost of Seeds out of 50,000 Kg Kapas* (50,000*0.64*20) = 6,40,000₹

Total Value (Cotton bale + Cotton Seed) (21,00,000 + 6,40,000) = 27,40,000₹

Profit (Total Value – Total Cost) (27,40,000 – 25,80,000) = 1,60,000₹

*Assumption (Outturn=34%, Seed = 64%, Wastage=2%)

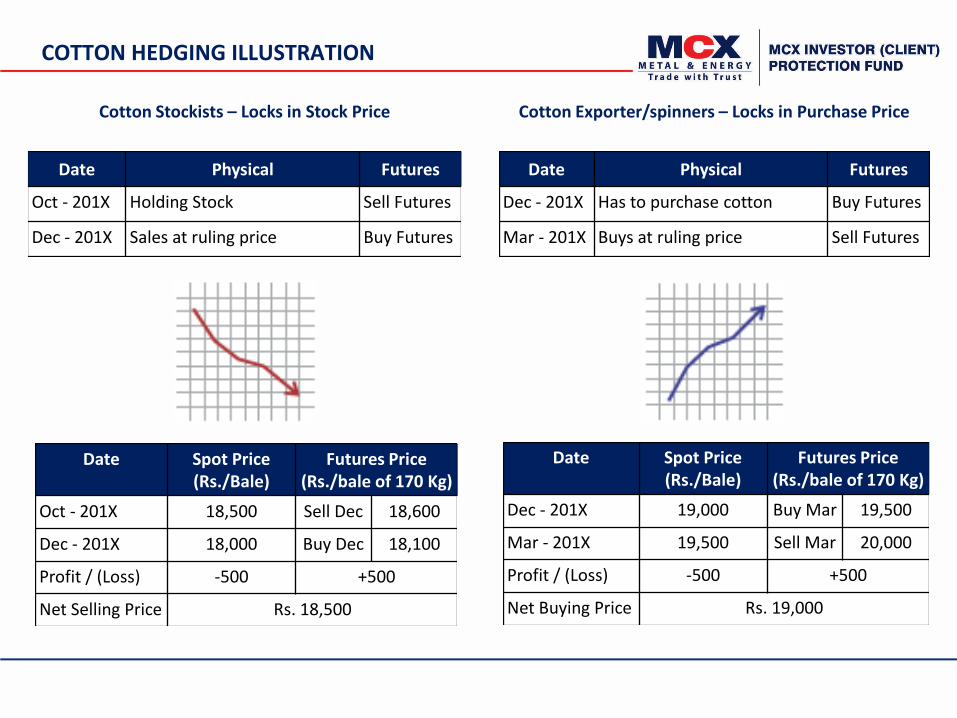

COTTON HEDGING ILLUSTRATION

Cotton Stockists – Locks in Stock Price Cotton Exporter/spinners – Locks in Purchase Price

Date Physical Futures

Oct - 201X Holding Stock Sell Futures

Dec - 201X Sales at ruling price Buy Futures

Date Physical Futures

Dec - 201X Has to purchase cotton Buy Futures

Mar - 201X Buys at ruling price Sell Futures

Date Spot Price (Rs./Bale)

Futures Price (Rs./bale of 170 Kg)

Oct - 201X 18,500 Sell Dec 18,600

Dec - 201X 18,000 Buy Dec 18,100

Profit / (Loss) -500 +500

Net Selling Price Rs. 18,500

Date Spot Price (Rs./Bale)

Futures Price (Rs./bale of 170 Kg)

Dec - 201X 19,000 Buy Mar 19,500

Mar - 201X 19,500 Sell Mar 20,000

Profit / (Loss) -500 +500

Net Buying Price Rs. 19,000

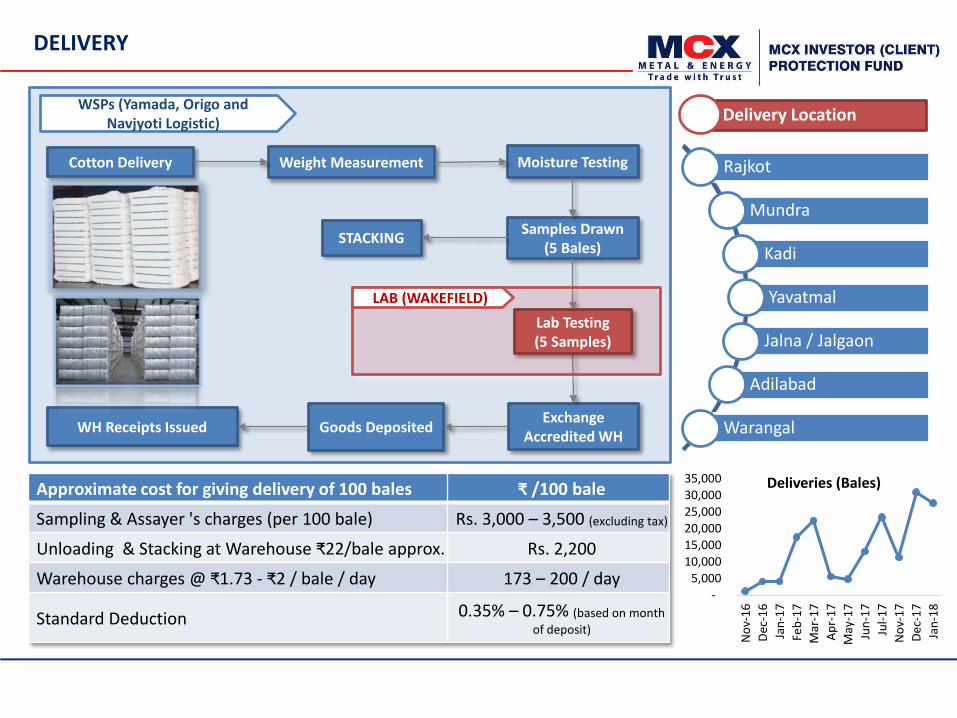

DELIVERY

WSPs (Yamada, Origo and Navjyoti Logistic)

Cotton Delivery Weight Measurement Moisture Testing

Samples Drawn(5 Bales)STACKING

Goods DepositedWH Receipts Issued Exchange Accredited WH

Lab Testing(5 Samples)

LAB (WAKEFIELD)

Approximate cost for giving delivery of 100 bales ₹ /100 bale

Sampling & Assayer 's charges (per 100 bale) Rs. 3,000 – 3,500 (excluding tax)

Unloading & Stacking at Warehouse ₹22/bale approx. Rs. 2,200

Warehouse charges @ ₹1.73 - ₹2 / bale / day 173 – 200 / day

Standard Deduction 0.35% – 0.75% (based on monthof deposit)

Rajkot

Mundra

Kadi

Yavatmal

Jalna / Jalgaon

Adilabad

Warangal

Delivery Location

- 5,000

10,000 15,000 20,000 25,000 30,000 35,000

Nov

-16

Dec-

16Ja

n-17

Feb-

17M

ar-1

7Ap

r-17

May

-17

Jun-

17Ju

l-17

Nov

-17

Dec-

17Ja

n-18

Deliveries (Bales)

Month-Wise Delivery & Stocks

Month-wise Delivery of cotton at MCX PlatformExpiry date Qty (Bales)October 31, 2016 0.00November 30, 2016 1,200December 30, 2016 4,100January 31, 2017 4,100February 28, 2017 17,400March 31, 2017 22,400April 28, 2017 5,600May 31, 2017 4,800June 30, 2017 13,100July 2017 23,500Total (October 2016 to July 2017) 96,200October 31, 2017 0.00November 30, 2017 11,300December 29, 2017 30,900January 31, 2018 27,700February 28, 2018 29,100

Stocks as on March 12, 2018Stock eligible for Exchange Delivery 1,20,200Stock in process for delivery 6,300Capacity of warehouse 1,35,900

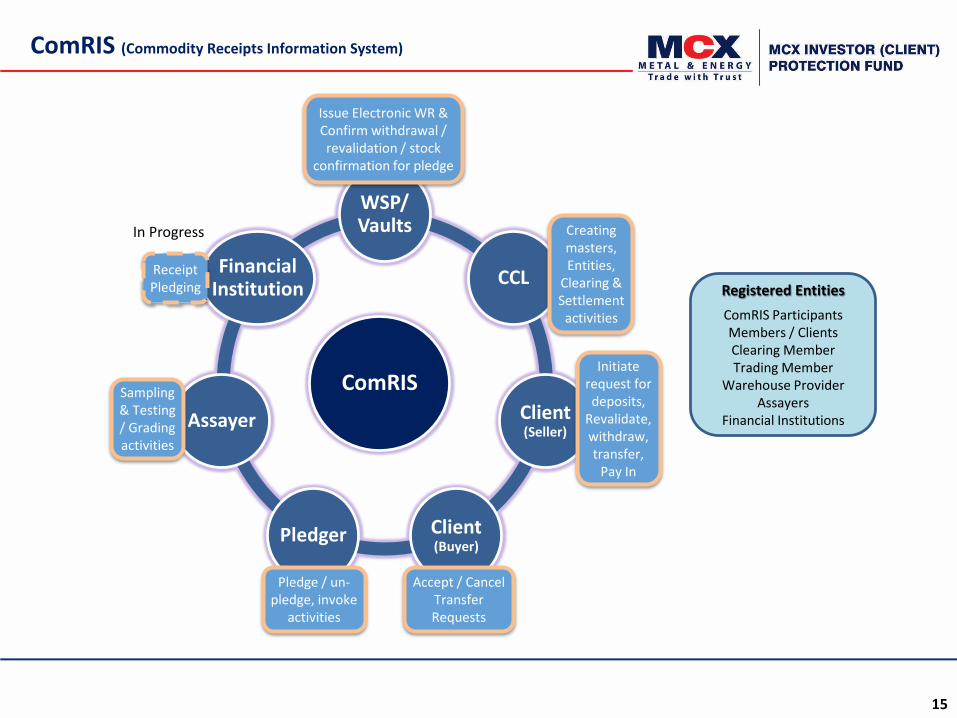

15

ComRIS (Commodity Receipts Information System)

Registered EntitiesComRIS ParticipantsMembers / ClientsClearing MemberTrading Member

Warehouse ProviderAssayers

Financial Institutions

ComRIS

WSP/ Vaults

CCL

Client (Seller)

Client (Buyer)

Pledger

Assayer

Financial Institution

Issue Electronic WR & Confirm withdrawal / revalidation / stock

confirmation for pledge

Creating masters, Entities,

Clearing & Settlement

activities

Pledge / un-pledge, invoke

activities

Accept / Cancel Transfer Requests

Initiate request for deposits,

Revalidate, withdraw, transfer,

Pay In

Sampling & Testing / Grading activities

Receipt Pledging

In Progress

HOW CAN YOU PARTICIPATE ON MCX

• Choose the Member Broker

• Fulfill KYC at Broker level

• Arrange for minimum initial margin

requirement

o Update yourself on Mark-to-Margin requirements

• Know MCX regulations and byelaws

• Select the commodity/ product to trade

• Read the Dos and Don’ts

• Know and distinguish among:

o Brokerage and Transaction Charges

o Margins, Taxation and Stamp Duty

o Default Penalties and Arbitration

THANK YOU

Multi Commodity Exchange of India Ltd.Exchange Square, Suren Road, Chakala, Andheri East, Mumbai-400093

Ph. – 022 67318888

The Contents do not constitute professional advice or provision of any kind of services and should notbe relied upon as such. MCX does not make any recommendation and assumes no responsibilitytowards any investments / trading in commodities or commodity futures done based on theinformation given in the website and any such investment / trade are subject to investment /commercial risks for which MCX shall not be responsible. If financial, investment or any otherprofessional advice is required, please seek advice of competent professionals.